What Fed the Feeder Cattle Fiasco?

- The feeder cattle market has had an incredible 2023, including a rally of $58 and subsequent selloff of nearly $60.

- Much of the activity has been driven by the flow of noncommercial money, often in the face of what was happening on the commercial side.

- The selloff was enhanced by traders supposedly ignoring key market filters normally used to manage risk.

As you likely know, the feeder cattle market has been a wild ride this past year. If we look at the weekly chart for the January 2024 futures contract we see it started life in Janaury 2023 with a contract low of $210.50. From there it was almost a straight climb higher, culminating with a peak of $268.50 the week of September 11. What happened after that, though will be talked about in the annals of livestock trading for years to come. While not quite to the level of the old pork belly market, it wasn’t far behind.

Jan24 feeders (GFF24) fell from its mid-September peak to a low of $209.15 the week of December 4. In other words, while it took roughly 8 months to gain $58, it took less than 3 months to erase it all, with an extra $1.35 thrown in for good measure. To start putting together the pieces as to what happened, let’s start with Newton’s First Law of Motion applied to markets: A trending market will stay in that trend until acted upon by an outside force, with that outside force usually noncommercial (fund) activity. This is also why Newsom’s Market Rule #1 says: Don’t get crossways with the trend. If you do, you are getting crossways with large noncommercial money, a situation that usually doesn’t end well.

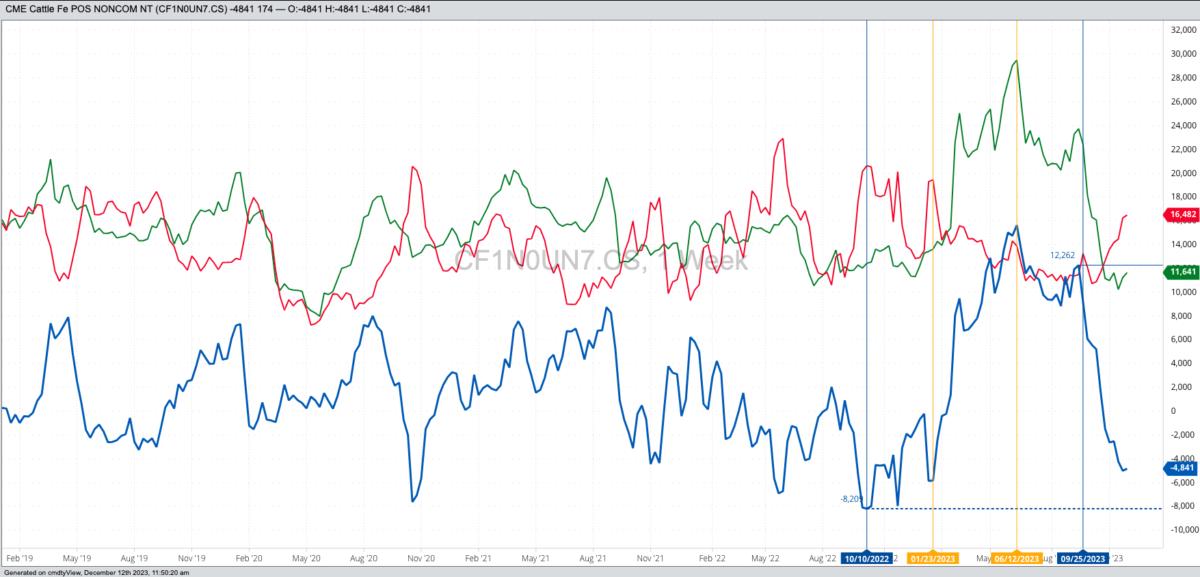

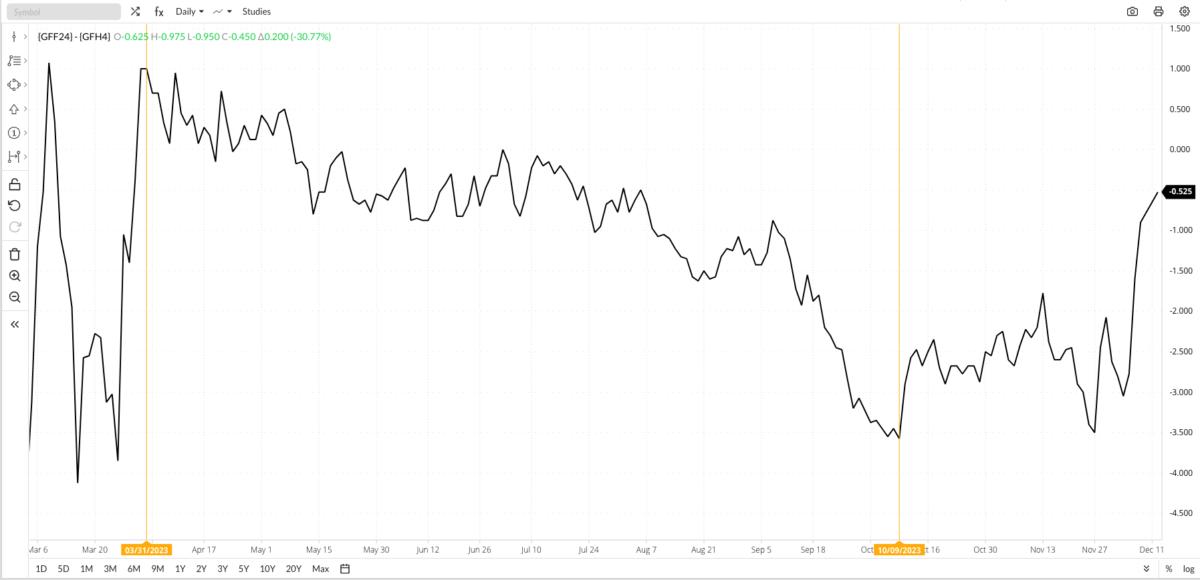

In the case of feeder cattle, a look at the CFTC Commitments of Traders legacy/futures only chart for noncommercial net futures position shows funds held a net-short futures position of 5.800 contracts when Jan24 first came on the board (week of January 23, 2023). From there, noncommercial traders would switch to a net-long of 15,625 contracts through the week of June 12, the largest net-long in feeders since 17,050 contracts the week of November 14, 2017. The 2023 situation was precarious given fundamentals weren’t providing support. The 2024 Jan-March futures spread had peaked at $1.00 (weekly closes only) in late March and was starting to see commercial selling of the nearby issue versus the deferred. By the time we reached mid-September the spread was already on its way to a low weekly close of (-$3.45) the week of October 2.

This tells us a classic Rubber Band Disposition had developed, meaning the market had been stretched between noncommercial buying and commercial selling until it finally snapped. When a rubber band breaks, it tends to snap back to its base, which in the case of markets is its real fundamentals.

As the market was rallying through the summer and early fall, implied volatility was low meaning options were either well priced or possibly undervalued. With futures being pushed to an all-time high by noncommercial buying and commercials unwilling to play along, the best strategy was to buy put options, and roll them up as the market extended its uptrend. I talked about this strategy often in Weekly Analysis on my website, and though it isn’t a sexy strategy it was the best at the time for alleviating some of the growing downside risk.

Some of this was done with folks actually buying put options, while others turned to Livestock Revenue Protection to do basically the same thing. Where things went south quickly was when some of these same positions were “enhanced” by selling put options below the market, because as we heard so many times, “The cattle markets are never coming down”. Funny thing about that.

There the market sat with put spreads in place, noncommercial traders overloaded with long futures while commercial interests had been selling. What happened next was the only thing that could happen: The rubber band broke, meaning noncommercial traders started to sell. So much so that by last Friday’s CoT report the net-futures position was back to being short 4,840 contracts. And while the futures market was being driven lower leaps at a time, implied volatility was ratcheting up as well. This meant more margin required to hold the short options positions that were now likely bleeding money, so how to staunch the flow? By selling more futures, of course.

As my friend in the industry was relating these steps to me, I was reminded of the optionsellers.com fiasco back in 2018. The company’s strategy was to sell options, on natural gas (aka The Widow Maker) no less, completely ignoring such things as historic price range, seasonality, and volatility. Those of you who have followed me over the years will recognize those as the filters I talk about in Market Rule #3: Use filters to manage risk. It also brings to mind, a visual that is hard to erase, something I call the Speedo Situation: Being short options is right for everyone. When selling options; feeder cattle, natural gas, or another market, one has to be aware of the risk/reward (unlimited risk, limited reward) and pay close attention to the previously mentioned filters.

Once again it seems none of this happened, with selling options promoted as a seemingly can’t miss strategy. I learned otherwise the hard way many years ago, oddly enough in the live cattle futures market, and it’s a lesson I’ve never forgotten.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.