Spotify's Path Looks Clear, Its Valuation Doesn't

Spotify Technology SA ![]() SPOT has a powerful bullish thesis. In the last year, the stock has advanced 144%, and that's thanks to ever-improving results and an execution that is proving that the company is well on its way to becoming a compounder.

SPOT has a powerful bullish thesis. In the last year, the stock has advanced 144%, and that's thanks to ever-improving results and an execution that is proving that the company is well on its way to becoming a compounder.

Spotify is still growing its user base, improving its margins, and holds several long-term optionalities that could unlock shareholder value. It is, by all measures, a business that is winning its category.

However, the market is fully aware of this success. The stock's valuation has soared to levels that no longer offer a clear margin of safety. As noted by GuruFocus's own GF Value chart, the stock is now considered "significantly overvalued." While the company's future is bright, the current price seems to have already priced in a decade of flawless execution. This creates a difficult proposition for new investors.

The Path to Higher Margins: More Than Just Music

The core appeal of Spotify's business model is its powerful flywheel. A superior user experience attracts more listeners, which in turn attracts more creators (musicians, podcasters), which then enriches the platform and attracts even more listeners. This has allowed Spotify to amass a staggering 678 million monthly active users.

User growth seems likely, even with some risks related to competition from big players like YouTube Music and Apple Music. Revenue per user is also a crucial point for the future, since a mix geared more towards premium users could have a positive impact on this, in addition to this subscription having a relatively high pricing power. My take is that even if Spotify's price is higher than that of its peers, the majority would not migrate because they like the service and are already very used to it, with playlists created, friends who use the same service, part of this community, and this creates this stickiness in the subscription.

In my view, the key to unlocking shareholder value from this massive base is margin expansion. The most direct path to this is the continued mix shift towards Premium subscribers. While the ad-supported tier is great for user acquisition, Premium subscribers are far more profitable. Every free user that converts to a paid plan directly improves the company's gross margin. With ongoing price increases and new features being added to the premium tiers, this lever for profit growth remains robust.

Another long-term opportunity for expanding margins is to remove the relevance of record labels. Companies like Universal Music Group NV (UMGNF) receive huge royalty payments from Spotify, and this ends up creating a recurring and relevant cost for the platforms and also pointing to a ceiling for the gross margin, i.e., even if the company manages to dilute a lot of the costs, these royalties are not very dilutable.

But things like Spotify for Artists and other tools allow Spotify to connect directly with artists. At some point, it may be that artists need Spotify more than the traditional record labels themselves, but it's too early to say. Other points include the diversification of what subscribers are consuming, as podcasts and audiobooks may have a greater margin.

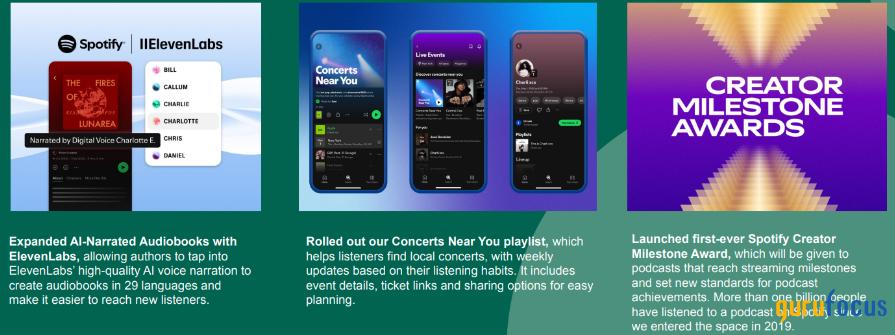

Note in the image below how the company is committed to making the platform and its relationship with artists, fans and creators better and better, with products such as Creator Milestone Award initiatives and Concerts Near You playlist, as well as AI-narrated audiobooks with ElevenLabs.

The Gurus Are A Little Divided

Given this dynamic of a great business at a high price, it's no surprise that the so-called "smart money" is divided on the stock. A look at recent guru activity reveals this split sentiment.

On one hand, some respected value-conscious investors are signaling caution. Notably, four gurus recently sold or reduced their positions, including well-known managers like Joel Greenblatt (Trades, Portfolio) and Steve Mandel (Trades, Portfolio). Their moves suggest a belief that the risk/reward profile is no longer attractive at current levels, likely due to the stretched valuation.

On the other hand, there are still some believers in the long term story, such as Ken Fisher (Trades, Portfolio) and Jefferies Group (Trades, Portfolio).

The Valuation Demands Optimistic Assumptions

This brings us to the core of the cautious case. The current valuation leaves little room for error. To make sense of today's price, one must underwrite a set of very optimistic assumptions about the company's future growth.

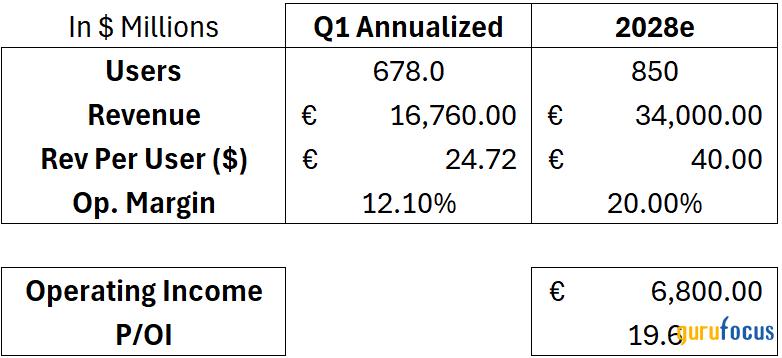

Let's run a forward-looking thought experiment to see what needs to happen by 2028 to justify the current stock price.

User Growth: Let's assume Spotify grows its monthly active user base from 678 million today to 850 million by 2028. This means adding another 172 million users, a monumental feat requiring continued dominance and successful expansion in emerging markets.

ARPU: Let's assume Spotify can increase the average revenue per user from around 24.70 today to 40 by 2028. This represents a 60% increase, which seems feasible, mainly because the mix can unlock a higher ARPU as the company manages to make premium subscribers more relevant in this base, and price increases can also be considered in the long term, in addition to other optionalities of the thesis.

Margin expansion: Let's assume the operating margin expands from 12% today to 20% in this same time frame. This also seems possible due to continued gains in scale, diversification of content, more premium subscribers in the base, and other initiatives related to cost and expense management, but note that this is also a very optimistic assumption, although the margin trend is positive.

These assumptions would result in an operating income of 6.8 billion, or a price-to-OI of 19.6x.

While this multiple seems reasonable, the journey to get there has risks. I don't believe that the above scenario exactly represents a base case. They are assumptions that could come true, but they actually look more like a bull case.

In other words, the current stock price is not just betting on growth, it is betting on an almost perfect execution of an optimistic scenario. If user growth slows, if subscribers push back against price increases or if label records maintain pricing power and Spotify continues to depend on them, the margin expansion could be lower, those targets could be missed and the valuation would look even more stretched.

Considering only 2028 may not seem much, and some might even say that the assumptions are not that optimistic, but considering that the company would reach billions of users in a few years and still face significant competition, seems very optimistic to me. As well as assuming that the margin will grow well above 20%, since even if there is potential for scale, there are still structural factors that limit some of this growth.

As a disclaimer, I already think Spotify deserves a quality premium because it already has a robust free cash flow and a business model that allows for compounder status for financials, but the premium is currently too much, and uncertainties both related to execution and external market factors, such as competition, exist.

The Bottom Line

Spotify is a phenomenal business with a clear vision and multiple levers for long-term shareholder value creation. Its dominant platform, sticky subscribers, new opportunities emerging, and optionalities such as its relationship with creators, it's enough to say that they developed a great business model and strong moats.

However, the stock price has gotten a little far from the fundamentals. The valuation already seems to reflect a future where much of its growth is priced in, at least in the medium term.

For these reasons, I'm taking a more cautious view of Spotify. The potential is there, and it's easy to believe that the company will achieve it, but at the same time, the margin of safety seems too compressed to be optimistic about the stock itself.