Refining the Thesis: Is Valero's Recovery Priced In?

1: Valero Energy in the First Quarter of 2025: Performance, Challenges, and the Trump Administration's Impact, if any.

Company Overview

Valero Energy Corporation ![]() VLO is a prominent independent oil refiner based in the United States. As we begin 2025, Valero finds itself at a crucial juncture, which we will explore in this article regarding the first quarter results for 2025, released on April 24, 2025. Founded in 1980 and headquartered in Houston, Texas, Valero is a Fortune 500 company with over 10,000 employees.

VLO is a prominent independent oil refiner based in the United States. As we begin 2025, Valero finds itself at a crucial juncture, which we will explore in this article regarding the first quarter results for 2025, released on April 24, 2025. Founded in 1980 and headquartered in Houston, Texas, Valero is a Fortune 500 company with over 10,000 employees.

Operational Footprint and Revenue Breakdown

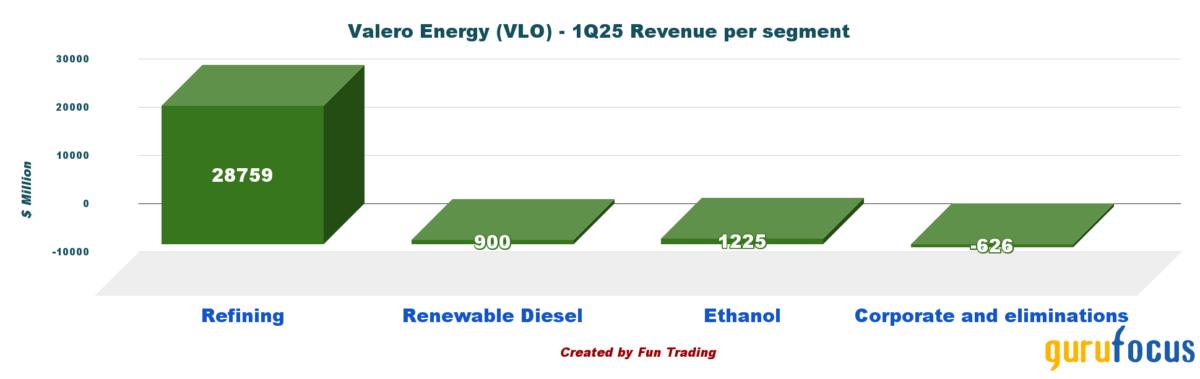

The company operates 15 petroleum refineries across the United States, Canada, and the United Kingdom, processing approximately 2.8 million barrels of oil per day. The US represents approximately 72% of the revenue.The quarterly revenue for the first quarter of 2025 is generated from three primary segments, as shown in the chart below:

Refining Dominates Revenue Generation

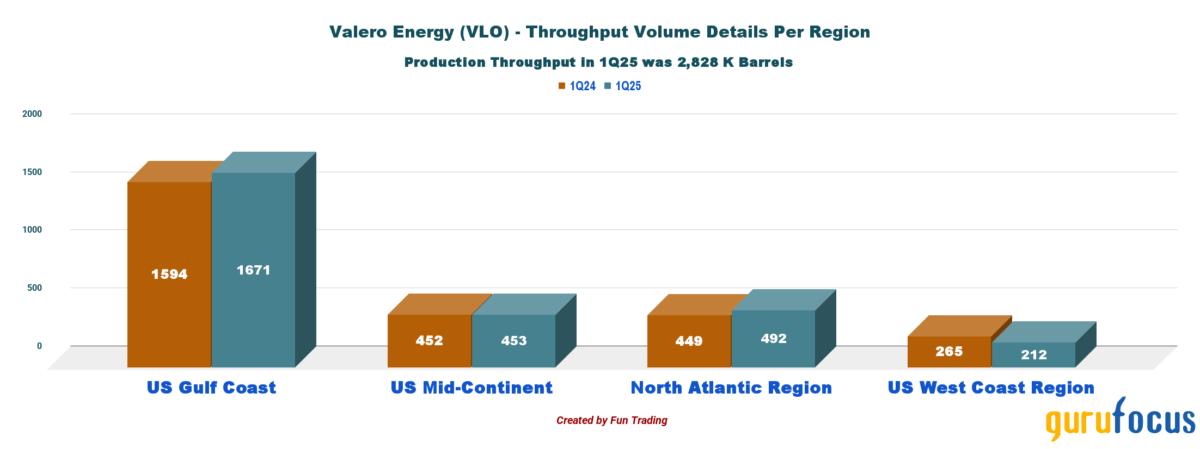

In the first quarter of 2025, 95% of the revenue was generated by the refining segment. Valero, the world's largest independent petroleum refiner, offers a diverse range of products, including gasoline, diesel, jet fuel, asphalt, petrochemicals, and lubricants. The refining business is divided into four regions: the U.S. Gulf Coast (7), the U.S. Mid-Continent (3), the North Atlantic (2), and the U.S. West Coast (2, including Benicia). The total throughput volume in 1Q25 was 2,828 thousand barrels per calendar day (Bpcd).

As shown in the chart below, the US Gulf Coast is the most prolific, with a 4.8% year-over-year increase.

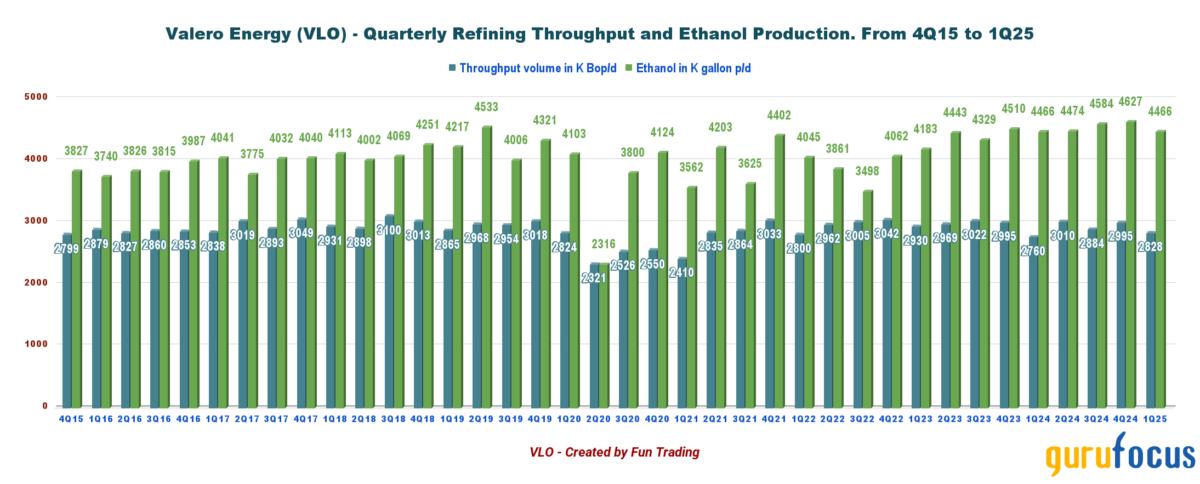

Renewable Fuels and Ethanol Production

Valero is also the world's second-largest producer of corn ethanol, producing 4,466 K gallons per day in 1Q25. Finally, through its joint venture with Darling Ingredients, Diamond Green Diesel can produce approximately 1.2 billion gallons of low-carbon renewable diesel and renewable naphtha annually.

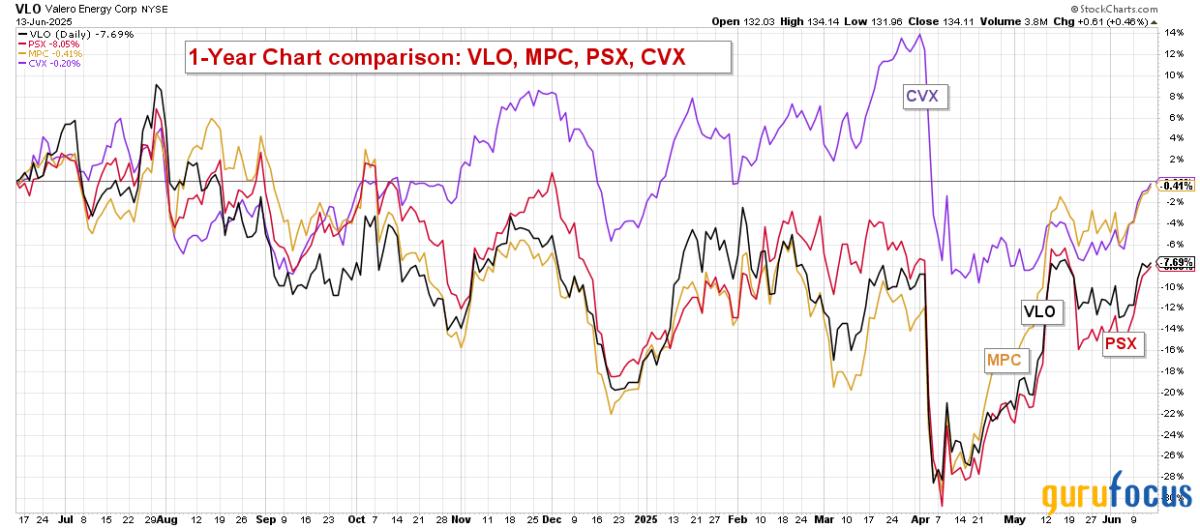

Chevron, Marathon Petroleum, Valero Energy, and Phillips 66 rank among the largest and most prominent refiners in the United States. Each company holds a key position in the downstream oil and gas industry, specializing in the transformation of crude oil into fuels and other valuable petroleum products. Here is their performance on a one year basis.

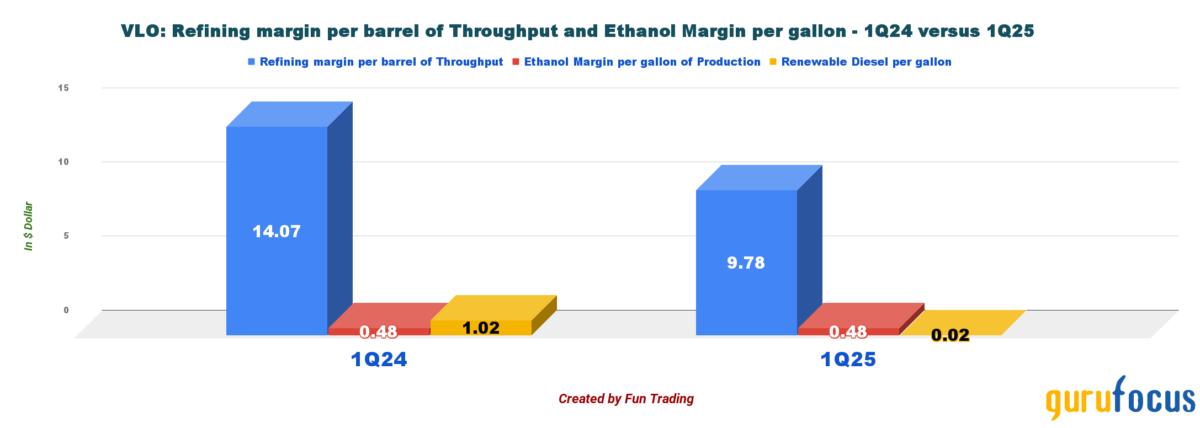

Challenges in Refining Margins

Valero's primary challenge lies in the structural weakening of its core refining operations, as illustrated in the chart below. Refining margins, representing the profit from converting crude oil into usable fuels, have tightened significantly.

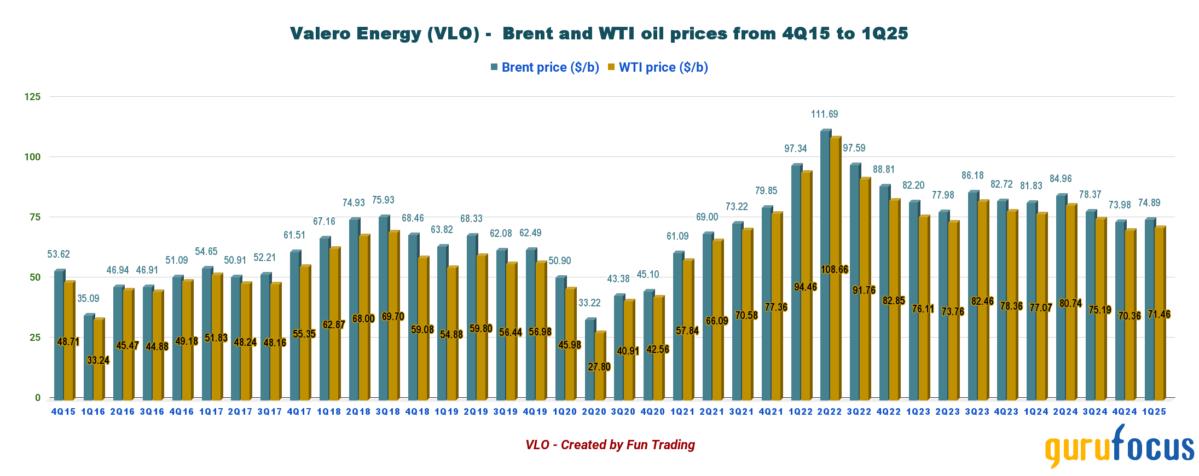

The difference between crude oil prices and the prices of refined products, such as gasoline and diesel, determines the profit margins for refiners. In the first quarter of 2025, this price gap significantly decreased due to reduced global demand, particularly in the US, China, and Europe.

Additionally, fluctuations in crude oil prices did not lead to corresponding increases in the prices of refined products. This volatility is expected to persist in 2025, with major shocks followed by periods of recovery.

3-2-1 crack spread: A potential bullish scenario for VLO

The 3-2-1 crack spreads measure refinery profit by comparing the prices of refined products to the cost of crude oil. As of June 20, 2025, the 3-2-1 crack spreads were $25.88 per barrel, increasing toward $26 to $28 per barrel.

As one of the largest and most efficient refiners in the U.S., Valero Energy could benefit substantially from the recent recovery in 3-2-1 crack spreads if these levels remain stable, further solidifying the bullish outlook for the stock in 2025. These higher margins indicate that refining economics are strengthening after a period of weakness, leading to higher earnings, increased free cash flow, and potential returns for shareholders.

Policy Impacts Under the Trump Administration

Under the current Trump administration, Valero benefits from deregulation but faces several challenges. These include trade tensions primarily with China and Europe, as well as uncertainty surrounding Renewable Fuel Standard (RFS) policies. Additionally, the recent bombing of nuclear sites in Iran has contributed to this uncertainty.

Furthermore, unpredictable ethanol blending mandates create more volatility, complicating long-term investment planning, which is essential for the industry's survival.

Threats of tariffs on crude imports and potential global retaliation put pressure on refining margins, which have dropped significantly this quarter. Despite some short-term gains, inconsistency in government policy introduces strategic risks to Valero's long-term operations.

2: Performance Overview: First quarter 2025 Results

Headline and Adjusted Earnings. 1Q25 loss explained.

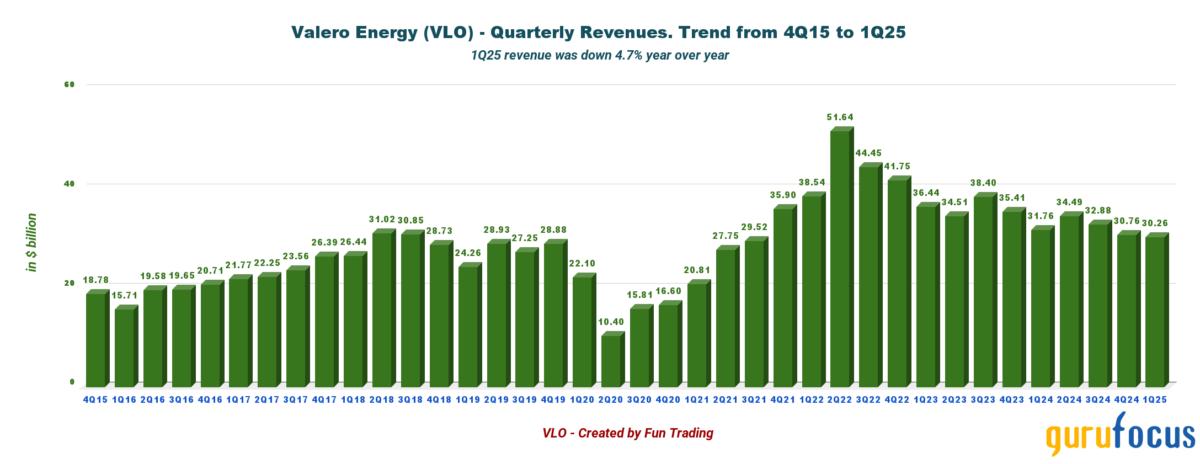

Valero's financial performance in the first quarter of 2025 was mixed, highlighted by a significant headline net loss of $595 million. This loss was primarily attributed to a $1.1 billion impairment charge related to its West Coast refineries (notably at Benicia). However, when excluding this non-cash charge, the company reported an adjusted net income of $282 million, or $0.89 per share, which surpassed Wall Street's expectations.

These results indicate a resilient underlying business and demonstrate that the company is capable of navigating considerable external and internal challenges. Below is shown the quarterly revenue history.

Refining Segment Performance: Renewable Diesel Segment Setback

The refining segment, which has traditionally been Valero's flagship, faced challenges this quarter. It reported an operating loss of $530 million, significantly down from the $1.745 billion operating income recorded during the same period in the previous year. This decline was mainly due to narrower refining margins and extensive maintenance activities that reduced throughput and increased costs.

The renewable diesel segment, which was viewed as a promising area for growth, has recently faced challenges.

Valero's joint venture, Diamond Green Diesel, reported an operating loss of $141 million, marking the first loss in the segment's history. A decrease in demand and lower credit pricing for renewable fuels have negatively impacted profitability in this area, which the company had previously identified as a key pillar for future growth.

Operational Disruptions and West Coast Impacts

Valero encountered challenges this quarter due to scheduled maintenance and unplanned downtime at several facilities, particularly in California. An impairment charge associated with these assets raises concerns about the company's long-term viability, which stricter environmental regulations on the West Coast may influence.

In addition to increasing cost pressures, these operational issues have raised doubts about Valero's ability to compete in the market, as operating margins have decreased significantly from last year.

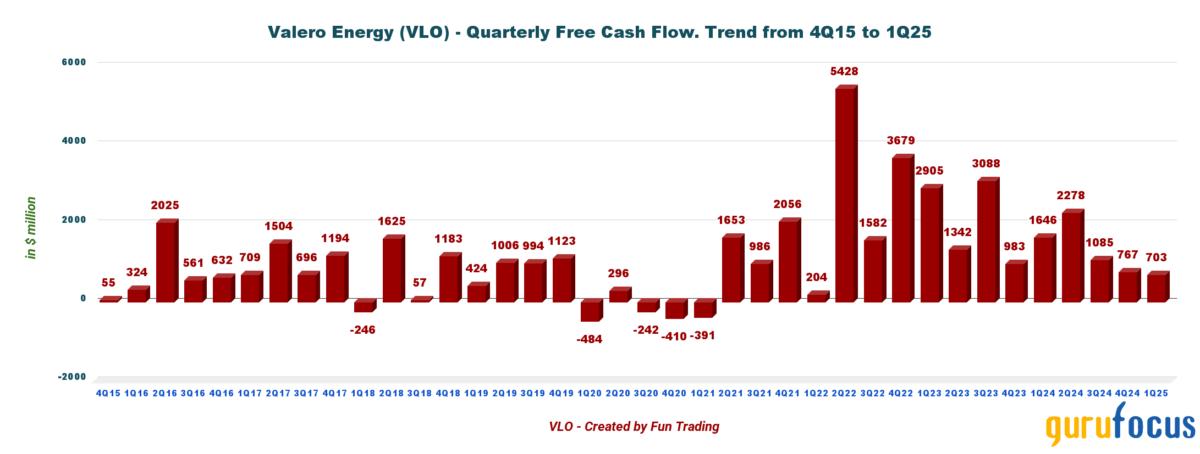

Free Cash Flow Decline

The result was a significant drop in free cash flow this quarter, with a free cash flow of $703 million compared to $1,646 million in 1Q24, representing a substantial year-over-year decline.

A free cash flow analysis is crucial for investors interested in Valero because the refining business is highly capital-intensive. It requires continuous investments in maintenance, upgrades, and compliance with environmental regulations to enhance efficiency and control emissions. By generating free cash flow, Valero can meet these needs internally, reducing the reliance on external debt.

Furthermore, free cash flow can be used to pay dividends and may support the initiation of a share buyback program. It's worth noting that EBITDA for the first quarter of 2025 was a negative $85 million.

Dividend safety check

Despite the drop in free cash flow this quarter, Valero reported that it returned a total of $633 million to its shareholders. Out of this amount, $277 million was allocated for the purchase of approximately 2.1 million shares of common stock.

Additionally, the company increased its quarterly dividend to $1.13 per share, representing a 5.6% increase compared to the previous quarter.

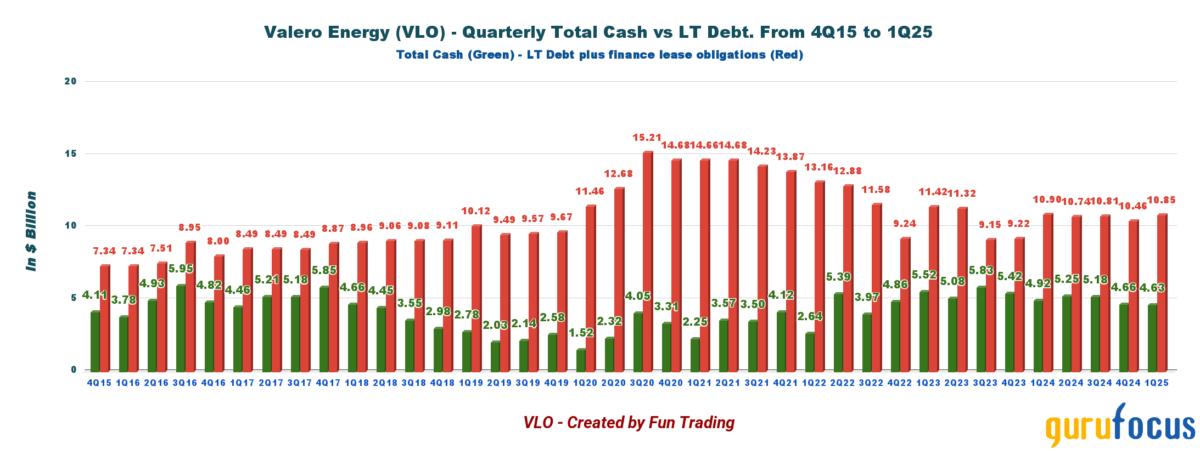

Balance Sheet and Liquidity Position

Valero's debt is well-managed, with a low net leverage of 0.75 times EBITDA. The company has strong liquidity, totaling $5.3 billion, and cash reserves of $4.634 billion, a decrease from $4.917 billion last year.

While there are near-term risks, including earnings volatility and costs associated with the renewable transition, the current financial coverage and capital strength indicate there are no immediate concerns. To maintain this stable economic position, Valero needs to continue executing its strategies and recovering margins. The chart below shows a slight increase in net debt due to the low free cash flow this quarter.

3: Conclusion: Strategic Crossroads for Valero

Valero faces important decisions starting in 2025 and beyond. Three important topics.

Stabilizing the Refining Business

First, it is crucial to stabilize and revitalize its refining operations. This involves optimizing maintenance schedules, investing in efficiency improvements, and considering the divestment of underperforming assets. By prioritizing cost discipline, the company can alleviate the margin pressures observed during the first quarter. The key indicators to watch for improvements will be higher profit margins and a return to profitability for the renewable business.

Reassessing Renewable Investments

Second, Valero must reassess the viability and scale of its renewable energy investments. Although the political climate in Washington may have shifted temporarily, the global trend toward decarbonization remains strong. Valero must balance its short-term advantages under the Trump administration with the long-term necessity of transitioning to cleaner energy sources.

Adapting to Regulatory and Geopolitical Dynamics

Finally, the company needs to adapt its strategic approach quickly, and it has performed well in this regard so far. This includes staying informed about geopolitical developments, evolving regulatory frameworks, and macroeconomic changes that could impact energy markets.

I believe management is aware of the challenges ahead. Valero's plans to idle, restructure, or cease operations at its Benicia refinery in California by the end of April 2026, affecting approximately 400 direct jobs, illustrate this important point.

Valero's challenges at Benicia underscore the growing tension between fossil fuel operations and stringent environmental regulations. It's a clear sign that regulatory pressure is intensifying, making long-term investments in older refineries riskier and pushing the need for cleaner energy strategies.

4: Technical Analysis: A Descending Channel.

Note: The chart has been adjusted to account for the dividend.

Valero Energy is currently trading within an ascending channel pattern, with resistance at $142 and support at $130.5. The relative strength index (RSI) currently stands at 72 and is in a upward trend, suggesting that VLO is now overbought (sell signal) and could reach a strong resistance at $140-$143.

An ascending channel is typically viewed as a bullish continuation pattern, which can persist until either a breakdown or a breakout occurs, usually following the initial trend established at the beginning of the channel (up in this case). For more details, please refer to the chart above.

I recommend adopting a Last-In, First-Out (LIFO) strategy for approximately half of your position. Set your target sell price between $140 and $143. As mentioned in my previous article on OXY, given the current level of market uncertainty, it is advisable to utilize a LIFO strategy for most of your investments.

Conversely, it may be wise to accumulate more shares between $131 and $127, but do so cautiously. A small breakdown could be tested at approximately $122.5 (50 MA).

If negative news regarding tariffs arises or if the bond market starts to show concerning signs due to a lack of confidence in the U.S. ability to manage its growing debt, VLO could drop below $100 very quickly, as it did in early April. Therefore, it is essential to maintain a solid cash position to capitalize on such unpredictable events.

Note: It is essential to frequently update the TA chart to remain relevant, as we operate in an extremely volatile environment.