Chande Momentum Oscillator (CMO) Buy Sell Strategy [TradeDots]The "Chande Momentum Oscillator (CMO) Buy Sell Strategy" leverages the CMO indicator to identify short-term buy and sell opportunities.

HOW DOES IT WORK

The standard CMO indicator measures the difference between recent gains and losses, divided by the total price movement over the same period. However, this version of the CMO has some limitations.

The primary disadvantage of the original CMO is its responsiveness to short-term volatility, making the signals less smooth and more erratic, especially in fluctuating markets. This instability can lead to misleading buy or sell signals.

To address this, we integrated the concept from the Moving Average Convergence Divergence (MACD) indicator. By applying a 9-period exponential moving average (EMA) to the CMO line, we obtained a smoothed signal line. This line acts as a filter, identifying confirmed overbought or oversold states, thereby reducing the number of false signals.

Similar to the MACD histogram, we generate columns representing the difference between the CMO and its signal line, reflecting market momentum. We use this momentum indicator as a criterion for entry and exit points. Trades are executed when there's a convergence of CMO and signal lines during an oversold state, and they are closed when the CMO line diverges from the signal line, indicating increased selling pressure.

APPLICATION

Since the 9-period EMA smooths the CMO line, it's less susceptible to extreme price fluctuations. However, this smoothing also makes it more challenging to breach the original +50 and -50 benchmarks.

To increase trading opportunities, we've tightened the boundary ranges. Users can customize the target benchmark lines in the settings to adjust for the volatility of the underlying asset.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

Commission: 0.01%

Initial Capital: $10,000

Equity per Trade: 80%

Signal Cool Down Period: 5

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

CMO

Combo Backtest 123 Reversal & CMOaDisparity Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related CMOaDisparity Index article is copyrighted material from Stocks & Commodities Dec 2009

My strategy modification.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOfilt This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOav This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder?s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMOabsThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & CMO & WMA This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Chande Momentum Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.

WARNING:

- For purpose educate only

- This script to change bars colors

CMO & WMA Backtest ver 2.0 This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

CMOaDisparity Index Backtest The related article is copyrighted materialfrom Stocks & Commodities Dec 2009

My strategy modification.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

CMOfilt BacktestThis indicator plots a CMO which ignores price changes which are less

than a threshold value. CMO was developed by Tushar Chande. A scientist,

an inventor, and a respected trading system developer, Mr. Chande developed

the CMO to capture what he calls "pure momentum". For more definitive

information on the CMO and other indicators we recommend the book The New

Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change, etc.

It is most closely related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to the

CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

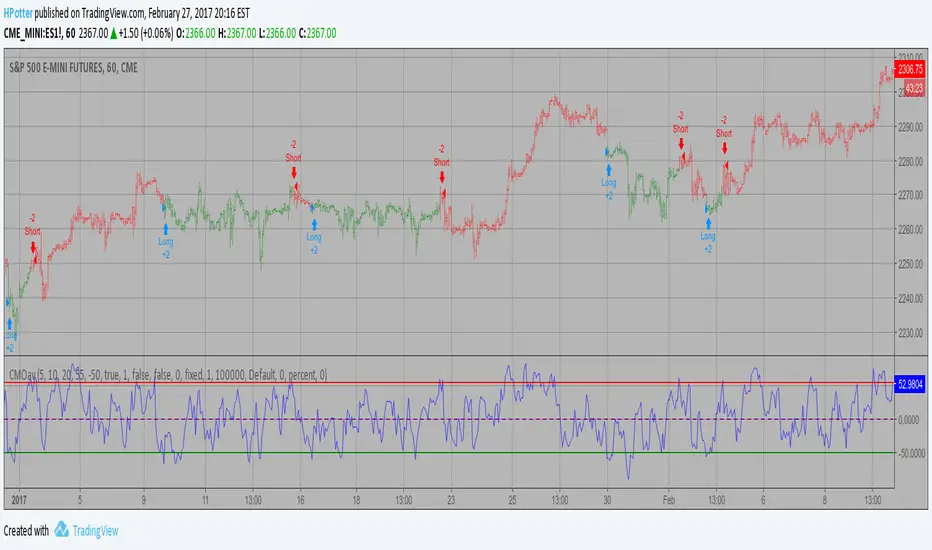

CMOav Backtest This indicator plots average of three different length CMO's. This indicator

was developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what he

calls "pure momentum". For more definitive information on the CMO and other

indicators we recommend the book The New Technical Trader by Tushar Chande

and Stanley Kroll.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMOabsav Backtest This indicator plots the absolute value of CMO averaged over three

different lengths. This indicator plots a classical-looking oscillator,

which is really an averaged value based on three different periods.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMOabs Backtest This indicator plots the absolute value of CMO. CMO was developed by Tushar

Chande. A scientist, an inventor, and a respected trading system developer,

Mr. Chande developed the CMO to capture what he calls "pure momentum". For

more definitive information on the CMO and other indicators we recommend the

book The New Technical Trader by Tushar Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented indicators

such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

related to Welles Wilder`s RSI, yet it differs in several ways:

- It uses data for both up days and down days in the numerator, thereby directly

measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term extreme

movements in price are not hidden. Once calculated, smoothing can be applied to

the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly see

changes in net momentum using the 0 level. The bounded scale also allows you to

conveniently compare values across different securities.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CMO & WMA Backtest This indicator plots Chande Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

CMO (Chande Momentum Oscillator) Strategy Backtest This indicator plots Chande Momentum Oscillator. This indicator was

developed by Tushar Chande. A scientist, an inventor, and a respected

trading system developer, Mr. Chande developed the CMO to capture what

he calls "pure momentum". For more definitive information on the CMO and

other indicators we recommend the book The New Technical Trader by Tushar

Chande and Stanley Kroll.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder`s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to

clearly see changes in net momentum using the 0 level. The bounded scale

also allows you to conveniently compare values across different securities.