PatternTransitionTablesPatternTransitionTables Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 Overview

This library provides precomputed state transition tables to enable ultra-efficient, O(1) computation of Ordinal Patterns. It is designed specifically to support high-performance indicators calculating Permutation Entropy and related complexity measures.

💮 The Problem & Solution

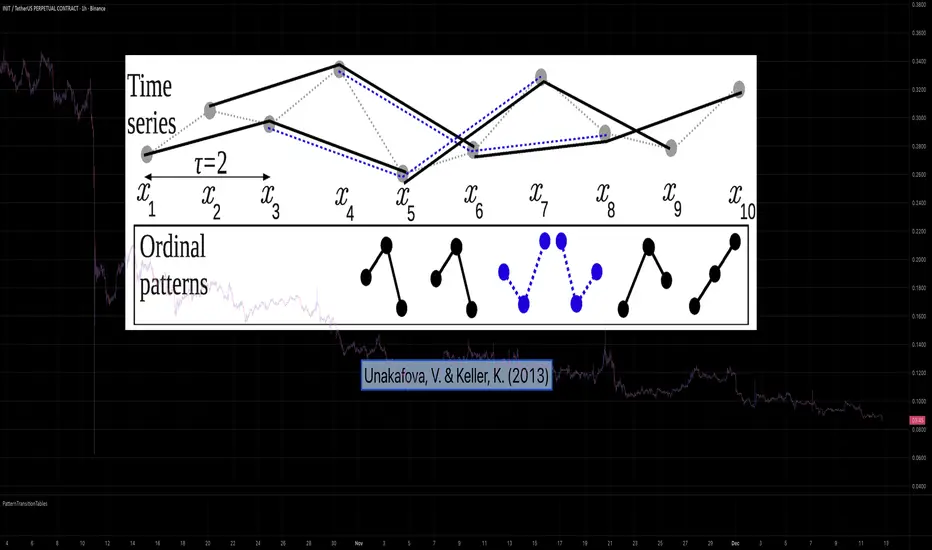

Calculating Permutation Entropy, as introduced by Bandt and Pompe (2002), typically requires computing ordinal patterns within a sliding window at every time step. The standard successive-pattern method (Equations 2+3 in the paper) requires ≤ 4d-1 operations per update.

Unakafova and Keller (2013) demonstrated that successive ordinal patterns "overlap" significantly. By knowing the current pattern index and the relative rank (position l) of just the single new data point, the next pattern index can be determined via a precomputed look-up table. Computing l still requires d comparisons, but the table lookup itself is O(1), eliminating the need for d multiplications and d additions. This reduces total operations from ≤ 4d-1 to ≤ 2d per update (Table 4). This library contains these precomputed tables for orders d = 2 through d = 5.

🌸 --------- 2. THEORETICAL BACKGROUND --------- 🌸

💮 Permutation Entropy

Bandt, C., & Pompe, B. (2002). Permutation entropy: A natural complexity measure for time series.

doi.org

This concept quantifies the complexity of a system by comparing the order of neighbouring values rather than their magnitudes. It is robust against noise and non-linear distortions, making it ideal for financial time series analysis.

💮 Efficient Computation

Unakafova, V. A., & Keller, K. (2013). Efficiently Measuring Complexity on the Basis of Real-World Data.

doi.org

This library implements the transition function φ_d(n, l) described in Equation 5 of the paper. It maps a current pattern index (n) and the position of the new value (l) to the successor pattern, reducing the complexity of updates to constant time O(1).

🌸 --------- 3. LIBRARY FUNCTIONALITY --------- 🌸

💮 Data Structure

The library stores transition matrices as flattened 1D integer arrays. These tables are mathematically rigorous representations of the factorial number system used to enumerate permutations.

💮 Core Function: get_successor()

This is the primary interface for the library for direct pattern updates.

• Input: The current pattern index and the rank position of the incoming price data.

• Process: Routes the request to the specific transition table for the chosen order (d=2 to d=5).

• Output: The integer index of the next ordinal pattern.

💮 Table Access: get_table()

This function returns the entire flattened transition table for a specified dimension. This enables local caching of the table (e.g. in an indicator's init() method), avoiding the overhead of repeated library calls during the calculation loop.

💮 Supported Orders & Terminology

The parameter d is the order of ordinal patterns (following Bandt & Pompe 2002). Each pattern of order d contains (d+1) data points, yielding (d+1)! unique patterns:

• d=2: 3 points → 6 unique patterns, 3 successor positions

• d=3: 4 points → 24 unique patterns, 4 successor positions

• d=4: 5 points → 120 unique patterns, 5 successor positions

• d=5: 6 points → 720 unique patterns, 6 successor positions

Note: d=6 is not implemented. The resulting code size (approx. 191k tokens) exceeds the Pine Script limit of 100k tokens (as of 2025-12).

Complexity

Approximate Entropy Zones [PhenLabs]Version: PineScript™ v6

Description

This indicator identifies periods of market complexity and randomness by calculating the Approximate Entropy (ApEn) of price action. As the movement of the market becomes complex, it means the current trend is losing steam and a reversal or consolidation is likely near. The indicator plots high-entropy periods as zones on your chart, providing a graphical suggestion to anticipate a potential market direction change. This indicator is designed to help traders identify favorable times to get in or out of a trade by highlighting when the market is in a state of disarray.

Points of Innovation

Advanced Complexity Analysis: Instead of relying on traditional momentum or trend indicators, this tool uses Approximate Entropy to quantify the unpredictability of price movements.

Dynamic Zone Creation: It automatically plots zones on the chart during periods of high entropy, providing a clear and intuitive visual guide.

Customizable Sensitivity: Users can fine-tune the ‘Entropy Threshold’ to adjust how frequently zones appear, allowing for calibration to different assets and timeframes.

Time-Based Zone Expiration: Zones can be set to expire after a specific time, keeping the chart clean and relevant.

Built-in Zone Size Filter: Excludes zones that form on excessively large candles, filtering out noise from extreme volatility events.

On-Chart Calibration Guide: A persistent note on the chart provides simple instructions for adjusting the entropy threshold, making it easy for users to optimize the indicator’s performance.

Core Components

Approximate Entropy (ApEn) Calculation: The core of the indicator, which measures the complexity or randomness of the price data.

Zone Plotting: Creates visual boxes on the chart when the calculated ApEn value exceeds a user-defined threshold.

Dynamic Zone Management: Manages the lifecycle of the zones, from creation to expiration, ensuring the chart remains uncluttered.

Customizable Settings: A comprehensive set of inputs that allow users to control the indicator’s sensitivity, appearance, and time-based behavior.

Key Features

Identifies Potential Reversals: The high-entropy zones can signal that a trend is nearing its end, giving traders an early warning.

Works on Any Timeframe: The indicator can be applied to any chart timeframe, from minutes to days.

Customizable Appearance: Users can change the color and transparency of the zones to match their chart’s theme.

Informative Labels: Each zone can display the calculated entropy value and the direction of the candle on which it formed.

Visualization

Entropy Zones: Shaded boxes that appear on the chart, highlighting candles with high complexity.

Zone Labels: Text within each zone that displays the ApEn value and a directional arrow (e.g., “0.525 ↑”).

Calibration Note: A small table in the top-right corner of the chart with instructions for adjusting the indicator’s sensitivity.

Usage Guidelines

Entropy Analysis

Source: The price data used for the ApEn calculation. (Default: close)

Lookback Length: The number of bars used in the ApEn calculation. (Default: 20, Range: 10-50)

Embedding Dimension (m): The length of patterns to be compared; a standard value for financial data. (Default: 2)

Tolerance Multiplier (r): Adjusts the tolerance for pattern matching; a larger value makes matching more lenient. (Default: 0.2)

Entropy Threshold: The ApEn value that must be exceeded to plot a zone. Increase this if too many zones appear; decrease it if too few appear. (Default: 0.525)

Time Settings

Analysis Timeframe: How long a zone remains on the chart after it forms. (Default: 1D)

Custom Period (Bars): The zone’s lifespan in bars if “Analysis Timeframe” is set to “Custom”. (Default: 1000)

Zone Settings

Zone Fill Color: The color of the entropy zones. (Default: #21f38a with 80% transparency)

Maximum Zone Size %: Filters out zones on candles that are larger than this percentage of their low price. (Default: 0.5)

Display Options

Show Entropy Label: Toggles the visibility of the text label inside each zone. (Default: true)

Label Text Position: The horizontal alignment of the text label. (Default: Right)

Show Calibration Note: Toggles the visibility of the calibration note in the corner of the chart. (Default: true)

Best Use Cases

Trend Reversal Trading: Identifying when a strong trend is likely to reverse or pause.

Breakout Confirmation: Using the absence of high entropy to confirm the strength of a breakout.

Ranging Market Identification: Periods of high entropy can indicate that a market is transitioning into a sideways or choppy phase.

Limitations

Not a Standalone Signal: This indicator should be used in conjunction with other forms of analysis to confirm trading signals.

Lagging Nature: Like all indicators based on historical data, ApEn is a lagging measure and does not predict future price movements with certainty.

Calibration Required: The effectiveness of the indicator is highly dependent on the “Entropy Threshold” setting, which needs to be adjusted for different assets and timeframes.

What Makes This Unique

Quantifies Complexity: It provides a numerical measure of market complexity, offering a different perspective than traditional indicators.

Clear Visual Cues: The zones make it easy to see when the market is in a state of high unpredictability.

User-Friendly Design: With features like the on-chart calibration note, the indicator is designed to be easy to use and optimize.

How It Works

Calculate Standard Deviation: The indicator first calculates the standard deviation of the source price data over a specified lookback period.

Calculate Phi: It then calculates a value called “phi” for two different pattern lengths (embedding dimensions ‘m’ and ‘m+1’). This involves comparing sequences of data points to see how many are “similar” within a certain tolerance (determined by the standard deviation and the ‘r’ multiplier).

Calculate ApEn: The Approximate Entropy is the difference between the two phi values. A higher ApEn value indicates greater irregularity and unpredictability in the data.

Plot Zones: If the calculated ApEn exceeds the user-defined ‘Entropy Threshold’, a zone is plotted on the chart.

Note: The “Entropy Threshold” is the most important setting to adjust. If you see too many zones, increase the threshold. If you see too few, decrease it.

Smart Market Bias [PhenLabs]📊 Smart Market Bias Indicator (SMBI)

Version: PineScript™ v6

Description

The Smart Market Bias Indicator (SMBI) is an advanced technical analysis tool that combines multiple statistical approaches to determine market direction and strength. It utilizes complexity analysis, information theory (Kullback Leibler divergence), and traditional technical indicators to provide a comprehensive market bias assessment. The indicator features adaptive parameters based on timeframe and trading style, with real-time visualization through a sophisticated dashboard.

🔧 Components

Complexity Analysis: Measures price movement patterns and trend strength

KL Divergence: Statistical comparison of price distributions

Technical Overlays: RSI and Bollinger Bands integration

Filter System: Volume and trend validation

Visual Dashboard: Dynamic color-coded display of all components

Simultaneous current timeframe + higher time frame analysis

🚨Important Explanation Feature🚨

By hovering over each individual cell in this comprehensive dashboard, you will get a thorough and in depth explanation of what each cells is showing you

Visualization

HTF Visualization

📌 Usage Guidelines

Based on your own trading style you should alter the timeframe length that you would like to be analyzing with your dashboard

The longer the term of the position you are planning on entering the higher timeframe you should have your dashboard set to

Bias Interpretation:

Values > 50% indicate bullish bias

Values < 50% indicate bearish bias

Neutral zone: 45-55% suggests consolidation

✅ Best Practices:

Use appropriate timeframe preset for your trading style

Monitor all components for convergence/divergence

Consider filter strength for signal validation

Use color intensity as confidence indicator

⚠️ Limitations

Requires sufficient historical data for accurate calculations

Higher computational complexity on lower timeframes

May lag during extremely volatile conditions

Best performance during regular market hours

What Makes This Unique

Multi-Component Analysis: Combines complexity theory, statistical analysis, and traditional technical indicators

Adaptive Parameters: Automatically optimizes settings based on timeframe

Triple-Layer Filtering: Uses trend, volume, and minimum strength thresholds

Visual Confidence System: Color intensity indicates signal strength

Multi-Timeframe Capabilities: Allowing the trader to analyze not only their current time frame but also the higher timeframe bias

🔧 How It Works

The indicator processes market data through four main components:

Complexity Score (40% weight): Analyzes price returns and pattern complexity

Kullback Leibler Divergence (30% weight): Compares current and historical price distributions

RSI Analysis (20% weight): Momentum and oversold/overbought conditions

Bollinger Band Position (10% weight): Price position relative to volatility

Underlying Method

Maintains rolling windows of price data for multiple calculations

Applies custom normalization using hyperbolic tangent function

Weights component scores based on reliability and importance

Generates final bias percentage with confidence visualization

💡 Note: For optimal results, use in conjunction with price action analysis and consider multiple timeframe confirmation. The indicator performs best when all components show alignment.

Surface Roughness EstimatorIntroduction

Roughness of a signal is often non desired since smooth signals are easier to analyse, its logical to say that anything interacting with rough price is subject to decrease in accuracy/efficiency and can induce non desired effects such as whipsaws. Being able to measure it can give useful information and potentially avoid errors in an analysis.

It is said that roughness appear when a signal have high-frequencies (short wavelengths) components with considerable amplitudes, so its not wrong to say that "estimating roughness" can be derived into "estimating complexity".

Measuring Roughness

There are a lot of way to estimate roughness in a signal, the most well know method being the estimation of fractal dimensions. Here i will use a first order autocorrelation function.

Auto-correlation is defined by the linear relationship between a signal and a delayed version of itself, for exemple if the price goes on the same direction than the price i bars back then the auto-correlation will increase, else decrease. So what this have to do with roughness ? Well when the auto-correlation decrease it means that the dominant frequency is high, and therefore that the signal is rough.

Interpretation Of The Indicator

When the indicator is high it means that price is rough, when its low it indicate that price is smooth. Originally its the inverse way but i found that it was more convenient to do it this way. We can interpret low values of the indicator as a trending market but its not totally true, for example high values dont always indicate that the market is ranging.

Here the comparison with the indicator applied to price (orange) and a moving average (purple)

The average measurement applied to a moving average is way lower than the one using the price, this is because a moving average is smoother than price.

Its also interesting to see that some trend strength estimator like efficiency ratio can treat huge volatility signals as trend as shown below.

Here the efficiency ratio treat this volatile movement as a trending market, our indicator instead indicate that this movement is rough, such indication can avoid situation where price is followed by another huge volatile movement in the opposite direction.

Its important to make the distinction between volatility and trend strength, the trend is defined by low frequencies components of a signal, therefore measuring trend strength can be resumed as measuring the amplitude of such frequencies, but roughness estimation can do a great job as well.

Conclusion

I have showed how to estimate roughness in price and compared how our indicator behaved in comparison with a classic trend strength measurement tool. Filters or any other indicator can be way more efficient if they know how to filter according to a situation, more commonly smoothing more when price is rough and smoothing less when price is smooth. Its good to have a wider view of how market is behaving and not sticking with the binary view of "Trending" and "Ranging" .

I hope you find a use to this script :)

Best Regards