PaddingThe Padding library is a comprehensive and flexible toolkit designed to extend time series data within TradingView, making it an indispensable resource for advanced signal processing tasks such as FFT, filtering, convolution, and wavelet analysis. At its core, the library addresses the common challenge of edge effects by "padding" your data—that is, by appending additional data points beyond the natural boundaries of your original dataset. This extension not only mitigates the distortions that can occur at the endpoints but also helps to maintain the integrity of various transformations and calculations performed on the series. The library accomplishes this while preserving the ordering of your data, ensuring that the most recent point always resides at index 0.

Central to the functionality of this library are two key enumerations: Direction and PaddingType. The Direction enum determines where the padding will be applied. You can choose to extend the data in the forward direction (ahead of the current values), in the backward direction (behind the current values), or in both directions simultaneously. The PaddingType enum defines the specific method used for extending the data. The library supports several methods—including symmetric, reflect, periodic, antisymmetric, antireflect, smooth, constant, and zero padding—each of which has been implemented to suit different analytical scenarios. For instance, symmetric padding mirrors the original data across its boundaries, while reflect padding continues the trend by reflecting around endpoint values. Periodic padding repeats the data, and antisymmetric padding mirrors the data with alternating signs to counterbalance it. The antireflect and smooth methods take into account the derivatives of your data, thereby extending the series in a way that preserves or smoothly continues these derivative values. Constant and zero padding simply extend the series using fixed endpoint values or zeros. Together, these enums allow you to fine-tune how your data is extended, ensuring that the padding method aligns with the specific requirements of your analysis.

The library is designed to work with both single variable inputs and array inputs. When using array-based methods—particularly with the antireflect and smooth padding types—please note that the implementation intentionally discards the last data point as a result of the delta computation process. This behavior is an important consideration when integrating the library into your TradingView studies, as it affects the overall data length of the padded series. Despite this, the library’s structure and documentation make it straightforward to incorporate into your existing scripts. You simply provide your data source, define the length of your data window, and select the desired padding type and direction, along with any optional parameters to control the extent of the padding (using both_period, forward_period, or backward_period).

In practical application, the Padding library enables you to extend historical data beyond its original range in a controlled and predictable manner. This is particularly useful when preparing datasets for further signal processing, as it helps to reduce artifacts that can otherwise compromise the results of your analytical routines. Whether you are an experienced Pine Script developer or a trader exploring advanced data analysis techniques, this library offers a robust solution that enhances the reliability and accuracy of your studies by ensuring your algorithms operate on a more complete and well-prepared dataset.

Library "Padding"

A comprehensive library for padding time series data with various methods. Supports both single variable and array inputs, with flexible padding directions and periods. Designed for signal processing applications including FFT, filtering, convolution, and wavelets. All methods maintain data ordering with most recent point at index 0.

symmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies symmetric padding by mirroring the input data across boundaries

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

method symmetric(source, direction, both_period, forward_period, backward_period)

Applies symmetric padding to an array by mirroring the data across boundaries

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with symmetric padding applied

reflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies reflect padding by continuing trends through reflection around endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

method reflect(source, direction, both_period, forward_period, backward_period)

Applies reflect padding to an array by continuing trends through reflection around endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with reflect padding applied

periodic(source, series_length, direction, both_period, forward_period, backward_period)

Applies periodic padding by repeating the input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

method periodic(source, direction, both_period, forward_period, backward_period)

Applies periodic padding to an array by repeating the data

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with periodic padding applied

antisymmetric(source, series_length, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding by mirroring data and alternating signs

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

method antisymmetric(source, direction, both_period, forward_period, backward_period)

Applies antisymmetric padding to an array by mirroring data and alternating signs

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antisymmetric padding applied

antireflect(source, series_length, direction, both_period, forward_period, backward_period)

Applies antireflect padding by reflecting around endpoints while preserving derivatives

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied

method antireflect(source, direction, both_period, forward_period, backward_period)

Applies antireflect padding to an array by reflecting around endpoints while preserving derivatives

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with antireflect padding applied. Note: Last data point is lost when using array input

smooth(source, series_length, direction, both_period, forward_period, backward_period)

Applies smooth padding by extending with constant derivatives from endpoints

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied

method smooth(source, direction, both_period, forward_period, backward_period)

Applies smooth padding to an array by extending with constant derivatives from endpoints

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with smooth padding applied. Note: Last data point is lost when using array input

constant(source, series_length, direction, both_period, forward_period, backward_period)

Applies constant padding by extending endpoint values

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

method constant(source, direction, both_period, forward_period, backward_period)

Applies constant padding to an array by extending endpoint values

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with constant padding applied

zero(source, series_length, direction, both_period, forward_period, backward_period)

Applies zero padding by extending with zeros

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

method zero(source, direction, both_period, forward_period, backward_period)

Applies zero padding to an array by extending with zeros

Namespace types: array

Parameters:

source (array) : Array of values to pad

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with zero padding applied

pad_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to input data

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied

method pad_data(source, padding_type, direction, both_period, forward_period, backward_period)

Generic padding function that applies specified padding type to array input

Namespace types: array

Parameters:

source (array) : Array of values to pad

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to array length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to array length if not specified

Returns: Array ordered with most recent point at index 0, containing original data with specified padding applied. Note: Last data point is lost when using antireflect or smooth padding types

make_padded_data(source, series_length, padding_type, direction, both_period, forward_period, backward_period)

Creates a window-based padded data series that updates with each new value. WARNING: Function must be called on every bar for consistency. Do not use in scopes where it may not execute on every bar.

Parameters:

source (float) : Input value to pad from

series_length (int) : Length of the data window

padding_type (series PaddingType) : Type of padding to apply (see PaddingType enum)

direction (series Direction) : Direction to apply padding

both_period (int) : Optional - periods to pad in both directions. Overrides forward_period and backward_period if specified

forward_period (int) : Optional - periods to pad forward. Defaults to series_length if not specified

backward_period (int) : Optional - periods to pad backward. Defaults to series_length if not specified

Returns: Array ordered with most recent point at index 0, containing windowed data with specified padding applied

FFT

Fourier For Loop [BackQuant]Fourier For Loop

PLEASE Read the following, as understanding an indicator's functionality is essential before integrating it into a trading strategy. Knowing the core logic behind each tool allows for a sound and strategic approach to trading.

Introducing BackQuant's Fourier For Loop (FFL) — a cutting-edge trading indicator that combines Fourier transforms with a for-loop scoring mechanism. This innovative approach leverages mathematical precision to extract trends and reversals in the market, helping traders make informed decisions. Let's break down the components, rationale, and potential use-cases of this indicator.

Understanding Fourier Transform in Trading

The Fourier Transform decomposes price movements into their frequency components, allowing for a detailed analysis of cyclical behavior in the market. By transforming the price data from the time domain into the frequency domain, this indicator identifies underlying patterns that traditional methods may overlook.

In this script, Fourier transforms are applied to the specified calculation source (defaulted to HLC3). The transformation yields magnitude values that can be used to score market movements over a defined range. This scoring process helps uncover long and short signals based on relative strength and trend direction.

Why Use Fourier Transforms?

Fourier Transforms excel in identifying recurring cycles and smoothing noisy data, making them ideal for fast-paced markets where price movements may be erratic. They also provide a unique perspective on market volatility, offering traders additional insights beyond standard indicators.

Calculation Logic: For-Loop Scoring Mechanism

The For Loop Scoring mechanism compares the magnitude of each transformed point in the series, summing the results to generate a score. This score forms the backbone of the signal generation system.

Long Signals: Generated when the score surpasses the defined long threshold (default set at 40). This indicates a strong bullish trend, signaling potential upward momentum.

Short Signals: Triggered when the score crosses under the short threshold (default set at -10). This suggests a bearish trend or potential downside risk.'

Thresholds & Customization

The indicator offers customizable settings to fit various trading styles:

Calculation Periods: Control how many periods the Fourier transform covers.

Long/Short Thresholds: Adjust the sensitivity of the signals to match different timeframes or risk preferences.

Visualization Options: Traders can visualize the thresholds, change the color of bars based on trend direction, and even color the background for enhanced clarity.

Trading Applications

This Fourier For Loop indicator is designed to be versatile across various market conditions and timeframes. Some of its key use-cases include:

Cycle Detection: Fourier transforms help identify recurring patterns or cycles, giving traders a head-start on market direction.

Trend Following: The for-loop scoring system helps confirm the strength of trends, allowing traders to enter positions with greater confidence.

Risk Management: With clearly defined long and short signals, traders can manage their positions effectively, minimizing exposure to false signals.

Final Note

Incorporating this indicator into your trading strategy adds a layer of mathematical precision to traditional technical analysis. Be sure to adjust the calculation start/end points and thresholds to match your specific trading style, and remember that no indicator guarantees success. Always backtest thoroughly and integrate the Fourier For Loop into a balanced trading system.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future .

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

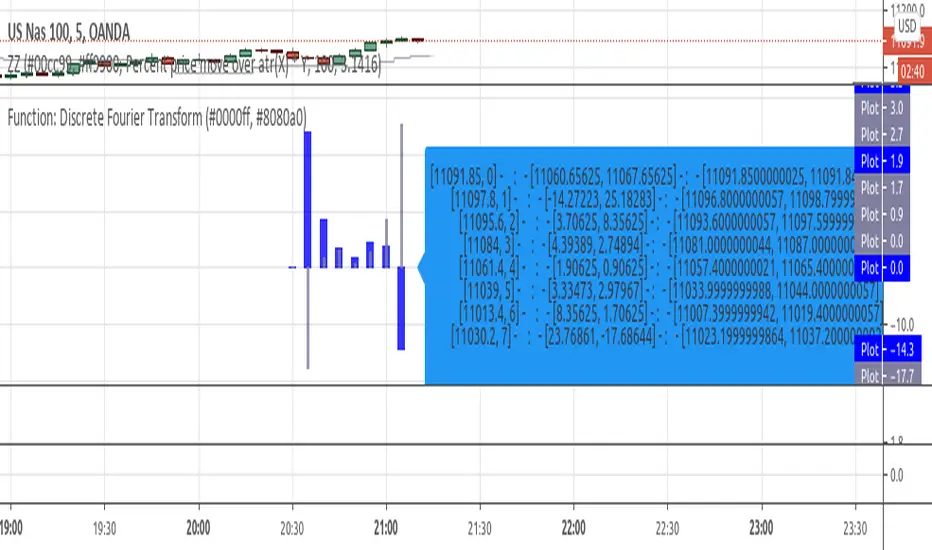

SpectrumLibrary "Spectrum"

This library includes spectrum analysis tools such as the Fast Fourier Transform (FFT).

method toComplex(data, polar)

Creates an array of complex type objects from a float type array.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

polar (bool) : Initialization coordinates; the default is false (cartesian).

Returns: The complex type array of converted data.

method sAdd(data, value, end, start, step)

Performs scalar addition of a given float type array and a simple float value.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

value (float) : The simple float type value to be added.

end (int) : The last index of the input array (exclusive) on which the operation is performed.

start (int) : The first index of the input array (inclusive) on which the operation is performed; the default value is 0.

step (int) : The step by which the function iterates over the input data array between the specified boundaries; the default value is 1.

Returns: The modified input array.

method sMult(data, value, end, start, step)

Performs scalar multiplication of a given float type array and a simple float value.

Namespace types: array

Parameters:

data (array) : The float type array of input data.

value (float) : The simple float type value to be added.

end (int) : The last index of the input array (exclusive) on which the operation is performed.

start (int) : The first index of the input array (inclusive) on which the operation is performed; the default value is 0.

step (int) : The step by which the function iterates over the input data array between the specified boundaries; the default value is 1.

Returns: The modified input array.

method eMult(data, data02, end, start, step)

Performs elementwise multiplication of two given complex type arrays.

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : the first complex type array of input data.

data02 (array type from RezzaHmt/Complex/1) : The second complex type array of input data.

end (int) : The last index of the input arrays (exclusive) on which the operation is performed.

start (int) : The first index of the input arrays (inclusive) on which the operation is performed; the default value is 0.

step (int) : The step by which the function iterates over the input data array between the specified boundaries; the default value is 1.

Returns: The modified first input array.

method eCon(data, end, start, step)

Performs elementwise conjugation on a given complex type array.

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : The complex type array of input data.

end (int) : The last index of the input array (exclusive) on which the operation is performed.

start (int) : The first index of the input array (inclusive) on which the operation is performed; the default value is 0.

step (int) : The step by which the function iterates over the input data array between the specified boundaries; the default value is 1.

Returns: The modified input array.

method zeros(length)

Creates a complex type array of zeros.

Namespace types: series int, simple int, input int, const int

Parameters:

length (int) : The size of array to be created.

method bitReverse(data)

Rearranges a complex type array based on the bit-reverse permutations of its size after zero-padding.

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : The complex type array of input data.

Returns: The modified input array.

method R2FFT(data, inverse)

Calculates Fourier Transform of a time series using Cooley-Tukey Radix-2 Decimation in Time FFT algorithm, wikipedia.org

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : The complex type array of input data.

inverse (int) : Set to -1 for FFT and to 1 for iFFT.

Returns: The modified input array containing the FFT result.

method LBFFT(data, inverse)

Calculates Fourier Transform of a time series using Leo Bluestein's FFT algorithm, wikipedia.org This function is nearly 4 times slower than the R2FFT function in practice.

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : The complex type array of input data.

inverse (int) : Set to -1 for FFT and to 1 for iFFT.

Returns: The modified input array containing the FFT result.

method DFT(data, inverse)

This is the original DFT algorithm. It is not suggested to be used regularly.

Namespace types: array

Parameters:

data (array type from RezzaHmt/Complex/1) : The complex type array of input data.

inverse (int) : Set to -1 for DFT and to 1 for iDFT.

Returns: The complex type array of DFT result.

loxxfftLibrary "loxxfft"

This code is a library for performing Fast Fourier Transform (FFT) operations. FFT is an algorithm that can quickly compute the discrete Fourier transform (DFT) of a sequence. The library includes functions for performing FFTs on both real and complex data. It also includes functions for fast correlation and convolution, which are operations that can be performed efficiently using FFTs. Additionally, the library includes functions for fast sine and cosine transforms.

Reference:

www.alglib.net

fastfouriertransform(a, nn, inversefft)

Returns Fast Fourier Transform

Parameters:

a (float ) : float , An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

nn (int) : int, The number of function values. It must be a power of two, but the algorithm does not validate this.

inversefft (bool) : bool, A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

Returns: float , Modifies the input array a in-place, which means that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution. The transformed data will have real and imaginary parts interleaved, with the real parts at even indices and the imaginary parts at odd indices.

realfastfouriertransform(a, tnn, inversefft)

Returns Real Fast Fourier Transform

Parameters:

a (float ) : float , A float array containing the real-valued function samples.

tnn (int) : int, The number of function values (must be a power of 2, but the algorithm does not validate this condition).

inversefft (bool) : bool, A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

Returns: float , Modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

fastsinetransform(a, tnn, inversefst)

Returns Fast Discrete Sine Conversion

Parameters:

a (float ) : float , An array of real numbers representing the function values.

tnn (int) : int, Number of function values (must be a power of two, but the code doesn't validate this).

inversefst (bool) : bool, A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

Returns: float , The output is the transformed array 'a', which will contain the result of the transformation.

fastcosinetransform(a, tnn, inversefct)

Returns Fast Discrete Cosine Transform

Parameters:

a (float ) : float , This is a floating-point array representing the sequence of values (time-domain) that you want to transform. The function will perform the Fast Cosine Transform (FCT) or the inverse FCT on this input array, depending on the value of the inversefct parameter. The transformed result will also be stored in this same array, which means the function modifies the input array in-place.

tnn (int) : int, This is an integer value representing the number of data points in the input array a. It is used to determine the size of the input array and control the loops in the algorithm. Note that the size of the input array should be a power of 2 for the Fast Cosine Transform algorithm to work correctly.

inversefct (bool) : bool, This is a boolean value that controls whether the function performs the regular Fast Cosine Transform or the inverse FCT. If inversefct is set to true, the function will perform the inverse FCT, and if set to false, the regular FCT will be performed. The inverse FCT can be used to transform data back into its original form (time-domain) after the regular FCT has been applied.

Returns: float , The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

fastconvolution(signal, signallen, response, negativelen, positivelen)

Convolution using FFT

Parameters:

signal (float ) : float , This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

response (float ) : float , This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

negativelen (int) : int, This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

positivelen (int) : int, This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

Returns: float , The resulting convolved values are stored back in the input signal array.

fastcorrelation(signal, signallen, pattern, patternlen)

Returns Correlation using FFT

Parameters:

signal (float ) : float ,This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array.

pattern (float ) : float , This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

patternlen (int) : int, This is an integer representing the length of the pattern array.

Returns: float , The signal array containing the correlation values at points from 0 to SignalLen-1.

tworealffts(a1, a2, a, b, tn)

Returns Fast Fourier Transform of Two Real Functions

Parameters:

a1 (float ) : float , An array of real numbers, representing the values of the first function.

a2 (float ) : float , An array of real numbers, representing the values of the second function.

a (float ) : float , An output array to store the Fourier transform of the first function.

b (float ) : float , An output array to store the Fourier transform of the second function.

tn (int) : float , An integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

Returns: float , The a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Detailed explaination of each function

Fast Fourier Transform

The fastfouriertransform() function takes three input parameters:

1. a: An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

2. nn: The number of function values. It must be a power of two, but the algorithm does not validate this.

3. inversefft: A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

The function performs the FFT using the Cooley-Tukey algorithm, which is an efficient algorithm for computing the discrete Fourier transform (DFT) and its inverse. The Cooley-Tukey algorithm recursively breaks down the DFT of a sequence into smaller DFTs of subsequences, leading to a significant reduction in computational complexity. The algorithm's time complexity is O(n log n), where n is the number of samples.

The fastfouriertransform() function first initializes variables and determines the direction of the transformation based on the inversefft parameter. If inversefft is True, the isign variable is set to -1; otherwise, it is set to 1.

Next, the function performs the bit-reversal operation. This is a necessary step before calculating the FFT, as it rearranges the input data in a specific order required by the Cooley-Tukey algorithm. The bit-reversal is performed using a loop that iterates through the nn samples, swapping the data elements according to their bit-reversed index.

After the bit-reversal operation, the function iteratively computes the FFT using the Cooley-Tukey algorithm. It performs calculations in a loop that goes through different stages, doubling the size of the sub-FFT at each stage. Within each stage, the Cooley-Tukey algorithm calculates the butterfly operations, which are mathematical operations that combine the results of smaller DFTs into the final DFT. The butterfly operations involve complex number multiplication and addition, updating the input array a with the computed values.

The loop also calculates the twiddle factors, which are complex exponential factors used in the butterfly operations. The twiddle factors are calculated using trigonometric functions, such as sine and cosine, based on the angle theta. The variables wpr, wpi, wr, and wi are used to store intermediate values of the twiddle factors, which are updated in each iteration of the loop.

Finally, if the inversefft parameter is True, the function divides the result by the number of samples nn to obtain the correct inverse FFT result. This normalization step is performed using a loop that iterates through the array a and divides each element by nn.

In summary, the fastfouriertransform() function is an implementation of the Cooley-Tukey FFT algorithm, which is an efficient algorithm for computing the DFT and its inverse. This FFT library can be used for a variety of applications, such as signal processing, image processing, audio processing, and more.

Feal Fast Fourier Transform

The realfastfouriertransform() function performs a fast Fourier transform (FFT) specifically for real-valued functions. The FFT is an efficient algorithm used to compute the discrete Fourier transform (DFT) and its inverse, which are fundamental tools in signal processing, image processing, and other related fields.

This function takes three input parameters:

1. a - A float array containing the real-valued function samples.

2. tnn - The number of function values (must be a power of 2, but the algorithm does not validate this condition).

3. inversefft - A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

The function modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

The algorithm uses a combination of complex-to-complex FFT and additional transformations specific to real-valued data to optimize the computation. It takes into account the symmetry properties of the real-valued input data to reduce the computational complexity.

Here's a detailed walkthrough of the algorithm:

1. Depending on the inversefft flag, the initial values for ttheta, c1, and c2 are determined. These values are used for the initial data preprocessing and post-processing steps specific to the real-valued FFT.

2. The preprocessing step computes the initial real and imaginary parts of the data using a combination of sine and cosine terms with the input data. This step effectively converts the real-valued input data into complex-valued data suitable for the complex-to-complex FFT.

3. The complex-to-complex FFT is then performed on the preprocessed complex data. This involves bit-reversal reordering, followed by the Cooley-Tukey radix-2 decimation-in-time algorithm. This part of the code is similar to the fastfouriertransform() function you provided earlier.

4. After the complex-to-complex FFT, a post-processing step is performed to obtain the final real-valued output data. This involves updating the real and imaginary parts of the transformed data using sine and cosine terms, as well as the values c1 and c2.

5. Finally, if the inversefft flag is True, the output data is divided by the number of samples (nn) to obtain the inverse DFT.

The function does not return a value explicitly. Instead, the transformed data is stored in the input array a. After the function execution, you can access the transformed data in the a array, which will have the real part at even indices and the imaginary part at odd indices.

Fast Sine Transform

This code defines a function called fastsinetransform that performs a Fast Discrete Sine Transform (FST) on an array of real numbers. The function takes three input parameters:

1. a (float array): An array of real numbers representing the function values.

2. tnn (int): Number of function values (must be a power of two, but the code doesn't validate this).

3. inversefst (bool): A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

The output is the transformed array 'a', which will contain the result of the transformation.

The code starts by initializing several variables, including trigonometric constants for the sine transform. It then sets the first value of the array 'a' to 0 and calculates the initial values of 'y1' and 'y2', which are used to update the input array 'a' in the following loop.

The first loop (with index 'jx') iterates from 2 to (tm + 1), where 'tm' is half of the number of input samples 'tnn'. This loop is responsible for calculating the initial sine transform of the input data.

The second loop (with index 'ii') is a bit-reversal loop. It reorders the elements in the array 'a' based on the bit-reversed indices of the original order.

The third loop (with index 'ii') iterates while 'n' is greater than 'mmax', which starts at 2 and doubles each iteration. This loop performs the actual Fast Discrete Sine Transform. It calculates the sine transform using the Danielson-Lanczos lemma, which is a divide-and-conquer strategy for calculating Discrete Fourier Transforms (DFTs) efficiently.

The fourth loop (with index 'ix') is responsible for the final phase adjustments needed for the sine transform, updating the array 'a' accordingly.

The fifth loop (with index 'jj') updates the array 'a' one more time by dividing each element by 2 and calculating the sum of the even-indexed elements.

Finally, if the 'inversefst' flag is True, the code scales the transformed data by a factor of 2/tnn to get the inverse Fast Sine Transform.

In summary, the code performs a Fast Discrete Sine Transform on an input array of real numbers, either in the direct or inverse direction, and returns the transformed array. The algorithm is based on the Danielson-Lanczos lemma and uses a divide-and-conquer strategy for efficient computation.

Fast Cosine Transform

This code defines a function called fastcosinetransform that takes three parameters: a floating-point array a, an integer tnn, and a boolean inversefct. The function calculates the Fast Cosine Transform (FCT) or the inverse FCT of the input array, depending on the value of the inversefct parameter.

The Fast Cosine Transform is an algorithm that converts a sequence of values (time-domain) into a frequency domain representation. It is closely related to the Fast Fourier Transform (FFT) and can be used in various applications, such as signal processing and image compression.

Here's a detailed explanation of the code:

1. The function starts by initializing a number of variables, including counters, intermediate values, and constants.

2. The initial steps of the algorithm are performed. This includes calculating some trigonometric values and updating the input array a with the help of intermediate variables.

3. The code then enters a loop (from jx = 2 to tnn / 2). Within this loop, the algorithm computes and updates the elements of the input array a.

4. After the loop, the function prepares some variables for the next stage of the algorithm.

5. The next part of the algorithm is a series of nested loops that perform the bit-reversal permutation and apply the FCT to the input array a.

6. The code then calculates some additional trigonometric values, which are used in the next loop.

7. The following loop (from ix = 2 to tnn / 4 + 1) computes and updates the elements of the input array a using the previously calculated trigonometric values.

8. The input array a is further updated with the final calculations.

9. In the last loop (from j = 4 to tnn), the algorithm computes and updates the sum of elements in the input array a.

10. Finally, if the inversefct parameter is set to true, the function scales the input array a to obtain the inverse FCT.

The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

Fast Convolution

This code defines a function called fastconvolution that performs the convolution of a given signal with a response function using the Fast Fourier Transform (FFT) technique. Convolution is a mathematical operation used in signal processing to combine two signals, producing a third signal representing how the shape of one signal is modified by the other.

The fastconvolution function takes the following input parameters:

1. float signal: This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

3. float response: This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

4. int negativelen: This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

5. int positivelen: This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

The function works by:

1. Calculating the length nl of the arrays used for FFT, ensuring it's a power of 2 and large enough to hold the signal and response.

2. Creating two new arrays, a1 and a2, of length nl and initializing them with the input signal and response function, respectively.

3. Applying the forward FFT (realfastfouriertransform) to both arrays, a1 and a2.

4. Performing element-wise multiplication of the FFT results in the frequency domain.

5. Applying the inverse FFT (realfastfouriertransform) to the multiplied results in a1.

6. Updating the original signal array with the convolution result, which is stored in the a1 array.

The result of the convolution is stored in the input signal array at the function exit.

Fast Correlation

This code defines a function called fastcorrelation that computes the correlation between a signal and a pattern using the Fast Fourier Transform (FFT) method. The function takes four input arguments and modifies the input signal array to store the correlation values.

Input arguments:

1. float signal: This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array.

3. float pattern: This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

4. int patternlen: This is an integer representing the length of the pattern array.

The function performs the following steps:

1. Calculate the required size nl for the FFT by finding the smallest power of 2 that is greater than or equal to the sum of the lengths of the signal and the pattern.

2. Create two new arrays a1 and a2 with the length nl and initialize them to 0.

3. Copy the signal array into a1 and pad it with zeros up to the length nl.

4. Copy the pattern array into a2 and pad it with zeros up to the length nl.

5. Compute the FFT of both a1 and a2.

6. Perform element-wise multiplication of the frequency-domain representation of a1 and the complex conjugate of the frequency-domain representation of a2.

7. Compute the inverse FFT of the result obtained in step 6.

8. Store the resulting correlation values in the original signal array.

At the end of the function, the signal array contains the correlation values at points from 0 to SignalLen-1.

Fast Fourier Transform of Two Real Functions

This code defines a function called tworealffts that computes the Fast Fourier Transform (FFT) of two real-valued functions (a1 and a2) using a Cooley-Tukey-based radix-2 Decimation in Time (DIT) algorithm. The FFT is a widely used algorithm for computing the discrete Fourier transform (DFT) and its inverse.

Input parameters:

1. float a1: an array of real numbers, representing the values of the first function.

2. float a2: an array of real numbers, representing the values of the second function.

3. float a: an output array to store the Fourier transform of the first function.

4. float b: an output array to store the Fourier transform of the second function.

5. int tn: an integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

The function performs the following steps:

1. Combine the two input arrays, a1 and a2, into a single array a by interleaving their elements.

2. Perform a 1D FFT on the combined array a using the radix-2 DIT algorithm.

3. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

Here is a detailed breakdown of the radix-2 DIT algorithm used in this code:

1. Bit-reverse the order of the elements in the combined array a.

2. Initialize the loop variables mmax, istep, and theta.

3. Enter the main loop that iterates through different stages of the FFT.

a. Compute the sine and cosine values for the current stage using the theta variable.

b. Initialize the loop variables wr and wi for the current stage.

c. Enter the inner loop that iterates through the butterfly operations within each stage.

i. Perform the butterfly operation on the elements of array a.

ii. Update the loop variables wr and wi for the next butterfly operation.

d. Update the loop variables mmax, istep, and theta for the next stage.

4. Separate the FFT results of the two input functions from the combined array a and store them in output arrays a and b.

At the end of the function, the a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Example scripts using functions contained in loxxfft

Real-Fast Fourier Transform of Price w/ Linear Regression

Real-Fast Fourier Transform of Price Oscillator

Normalized, Variety, Fast Fourier Transform Explorer

Variety RSI of Fast Discrete Cosine Transform

STD-Stepped Fast Cosine Transform Moving Average

Spectral Gating (SG)The Spectral Gating (SG) Indicator is a technical analysis tool inspired by music production techniques. It aims to help traders reduce noise in their charts by focusing on the significant frequency components of the data, providing a clearer view of market trends.

By incorporating complex number operations and Fast Fourier Transform (FFT) algorithms, the SG Indicator efficiently processes market data. The indicator transforms input data into the frequency domain and applies a threshold to the power spectrum, filtering out noise and retaining only the frequency components that exceed the threshold.

Key aspects of the Spectral Gating Indicator include:

Adjustable Window Size: Customize the window size (ranging from 2 to 6) to control the amount of data considered during the analysis, giving you the flexibility to adapt the indicator to your trading strategy.

Complex Number Arithmetic: The indicator uses complex number addition, subtraction, and multiplication, as well as radius calculations for accurate data processing.

Iterative FFT and IFFT: The SG Indicator features iterative FFT and Inverse Fast Fourier Transform (IFFT) algorithms for rapid data analysis. The FFT algorithm converts input data into the frequency domain, while the IFFT algorithm restores the filtered data back to the time domain.

Spectral Gating: At the heart of the indicator, the spectral gating function applies a threshold to the power spectrum, suppressing frequency components below the threshold. This process helps to enhance the clarity of the data by reducing noise and focusing on the more significant frequency components.

Visualization: The indicator plots the filtered data on the chart with a simple blue line, providing a clean and easily interpretable representation of the results.

Although the Spectral Gating Indicator may not be a one-size-fits-all solution for all trading scenarios, it serves as a valuable tool for traders looking to reduce noise and concentrate on relevant market trends. By incorporating this indicator into your analysis toolkit, you can potentially make more informed trading decisions.

GKD-C RSI of Fast Discrete Cosine Transform [Loxx]Giga Kaleidoscope GKD-C RSI of Fast Discrete Cosine Transform is a Confirmation module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ Giga Kaleidoscope Modularized Trading System

What is Loxx's "Giga Kaleidoscope Modularized Trading System"?

The Giga Kaleidoscope Modularized Trading System is a trading system built on the philosophy of the NNFX (No Nonsense Forex) algorithmic trading.

What is the NNFX algorithmic trading strategy?

The NNFX (No-Nonsense Forex) trading system is a comprehensive approach to Forex trading that is designed to simplify the process and remove the confusion and complexity that often surrounds trading. The system was developed by a Forex trader who goes by the pseudonym "VP" and has gained a significant following in the Forex community.

The NNFX trading system is based on a set of rules and guidelines that help traders make objective and informed decisions. These rules cover all aspects of trading, including market analysis, trade entry, stop loss placement, and trade management.

Here are the main components of the NNFX trading system:

1. Trading Philosophy: The NNFX trading system is based on the idea that successful trading requires a comprehensive understanding of the market, objective analysis, and strict risk management. The system aims to remove subjective elements from trading and focuses on objective rules and guidelines.

2. Technical Analysis: The NNFX trading system relies heavily on technical analysis and uses a range of indicators to identify high-probability trading opportunities. The system uses a combination of trend-following and mean-reverting strategies to identify trades.

3. Market Structure: The NNFX trading system emphasizes the importance of understanding the market structure, including price action, support and resistance levels, and market cycles. The system uses a range of tools to identify the market structure, including trend lines, channels, and moving averages.

4. Trade Entry: The NNFX trading system has strict rules for trade entry. The system uses a combination of technical indicators to identify high-probability trades, and traders must meet specific criteria to enter a trade.

5. Stop Loss Placement: The NNFX trading system places a significant emphasis on risk management and requires traders to place a stop loss order on every trade. The system uses a combination of technical analysis and market structure to determine the appropriate stop loss level.

6. Trade Management: The NNFX trading system has specific rules for managing open trades. The system aims to minimize risk and maximize profit by using a combination of trailing stops, take profit levels, and position sizing.

Overall, the NNFX trading system is designed to be a straightforward and easy-to-follow approach to Forex trading that can be applied by traders of all skill levels.

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the Stochastic Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v1.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data between modules. Data is passed between each module as described below:

GKD-B => GKD-V => GKD-C(1) => GKD-C(2) => GKD-C(Continuation) => GKD-E => GKD-BT

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: Strategy with 1-3 take profits, trailing stop loss, multiple types of PnL volatility, and 2 backtesting styles

Baseline: Hull Moving Average

Volatility/Volume: Hurst Exponent

Confirmation 1: RSI of Fast Discrete Cosine Transform as shown on the chart above

Confirmation 2: Williams Percent Range

Continuation: Fisher Transform

Exit: Rex Oscillator

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD protocol chain.

Giga Kaleidoscope Modularized Trading System Signals (based on the NNFX algorithm)

Standard Entry

1. GKD-C Confirmation 1 Signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

6. GKD-C Confirmation 1 signal was less than 7 candles prior

Continuation Entry

1. Standard Entry, Baseline Entry, or Pullback; entry triggered previously

2. GKD-B Baseline hasn't crossed since entry signal trigger

3. GKD-C Confirmation Continuation Indicator signals

4. GKD-C Confirmation 1 agrees

5. GKD-B Baseline agrees

6. GKD-C Confirmation 2 agrees

1-Candle Rule Standard Entry

1. GKD-C Confirmation 1 signal

2. GKD-B Baseline agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume agrees

1-Candle Rule Baseline Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

4. GKD-C Confirmation 1 signal was less than 7 candles prior

Next Candle:

1. Price retraced (Long: close < close or Short: close > close )

2. GKD-B Baseline agrees

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

PullBack Entry

1. GKD-B Baseline signal

2. GKD-C Confirmation 1 agrees

3. Price is beyond 1.0x Volatility of Baseline

Next Candle:

1. Price is within a range of 0.2x Volatility and 1.0x Volatility of the Goldie Locks Mean

3. GKD-C Confirmation 1 agrees

4. GKD-C Confirmation 2 agrees

5. GKD-V Volatility/Volume Agrees

█ Fast Discrete Cosine Transform

What is the Fast Discrete Cosine Transform?

Algolib is a C++ library for algorithmic trading that provides various algorithms for processing and analyzing financial data. The library includes a Fast Discrete Cosine Transform (FDCT) implementation, which is a fast version of the Discrete Cosine Transform (DCT) algorithm used for signal processing and data compression.

The FDCT implementation in Algolib is based on the FFT (Fast Fourier Transform) algorithm, which is a widely used method for computing the DCT. The implementation is optimized for performance and can handle large datasets efficiently. It uses the standard divide-and-conquer approach to compute the DCT recursively and combines the resulting coefficients to obtain the final DCT of the input signal.

The input to the FDCT algorithm in Algolib is a one-dimensional array of real numbers, which represents a time series or a financial signal. The algorithm then computes the DCT of the input sequence and returns a one-dimensional array of DCT coefficients, which represent the frequency components of the signal.

The implementation of the FDCT algorithm in Algolib uses C++ templates to provide a generic implementation that can work with different data types. It also includes various optimizations, such as loop unrolling, to improve the performance of the algorithm.

The steps involved in the FDCT algorithm in Algolib are:

-Divide the input sequence into even and odd parts.

-Compute the DCT of the even and odd parts recursively.

-Combine the DCT coefficients of the even and odd parts to obtain the final DCT coefficients.

-The implementation of the FDCT algorithm in Algolib uses the FFTW (Fastest Fourier Transform in the West) library to perform the FFT computations, which is a highly optimized library for computing Fourier transforms.

In summary, the Fast Discrete Cosine Transform implementation in Algolib is a fast and efficient implementation of the DCT algorithm, which is used for processing financial signals and time series data. The implementation is optimized for performance and uses the FFT algorithm for fast computation. The implementation is generic and can work with different data types, and includes optimizations such as loop unrolling to improve the performance of the algorithm.

What is the Fast Discrete Cosine Transform in terms of Forex trading?

The Fast Discrete Cosine Transform (FDCT) is an algorithm used for signal processing and data compression that can also be applied in trading forex. The FDCT is used to transform financial data into a set of coefficients that represent the data in terms of cosine functions of different frequencies. These coefficients can be used to analyze the frequency components of financial signals and to develop trading strategies based on these components.

In trading forex, the FDCT can be applied to various financial signals, such as price data, volume data, and technical indicators. By applying the FDCT to these signals, traders can identify the dominant frequency components of the signals and use this information to develop trading strategies.

For example, traders can use the FDCT to identify cycles in the market and use this information to develop trend-following strategies. The FDCT can also be used to identify short-term fluctuations in the market and develop mean-reversion strategies based on these fluctuations.

The FDCT can also be used in combination with other technical analysis tools, such as moving averages, to improve the accuracy of trading signals. For example, traders can apply the FDCT to the moving average of a financial signal to identify the dominant frequency components of the moving average and use this information to develop trading signals.

The FDCT can also be used in conjunction with machine learning algorithms to develop predictive models for financial markets. By applying the FDCT to financial data and using the resulting coefficients as inputs to a machine learning algorithm, traders can develop models that predict future price movements and identify profitable trading opportunities.

In summary, the FDCT can be applied in trading forex to analyze the frequency components of financial signals and develop trading strategies based on these components. The FDCT can be used in conjunction with other technical analysis tools and machine learning algorithms to improve the accuracy of trading signals and develop predictive models for financial markets.

What is the Fast Discrete Cosine Transform in terms of Forex trading?

The Fast Discrete Cosine Transform (FDCT) is an algorithm used for signal processing and data compression that can also be applied in trading forex. The FDCT is used to transform financial data into a set of coefficients that represent the data in terms of cosine functions of different frequencies. These coefficients can be used to analyze the frequency components of financial signals and to develop trading strategies based on these components.

In trading forex, the FDCT can be applied to various financial signals, such as price data, volume data, and technical indicators. By applying the FDCT to these signals, traders can identify the dominant frequency components of the signals and use this information to develop trading strategies.

For example, traders can use the FDCT to identify cycles in the market and use this information to develop trend-following strategies. The FDCT can also be used to identify short-term fluctuations in the market and develop mean-reversion strategies based on these fluctuations.

The FDCT can also be used in combination with other technical analysis tools, such as moving averages, to improve the accuracy of trading signals. For example, traders can apply the FDCT to the moving average of a financial signal to identify the dominant frequency components of the moving average and use this information to develop trading signals.

The FDCT can also be used in conjunction with machine learning algorithms to develop predictive models for financial markets. By applying the FDCT to financial data and using the resulting coefficients as inputs to a machine learning algorithm, traders can develop models that predict future price movements and identify profitable trading opportunities.

In summary, the FDCT can be applied in trading forex to analyze the frequency components of financial signals and develop trading strategies based on these components. The FDCT can be used in conjunction with other technical analysis tools and machine learning algorithms to improve the accuracy of trading signals and develop predictive models for financial markets.

█ Relative Strength Index (RSI)

This indicator contains 7 different types of RSI .

RSX

Regular

Slow

Rapid

Harris

Cuttler

Ehlers Smoothed

What is RSI?

RSI stands for Relative Strength Index . It is a technical indicator used to measure the strength or weakness of a financial instrument's price action.

The RSI is calculated based on the price movement of an asset over a specified period of time, typically 14 days, and is expressed on a scale of 0 to 100. The RSI is considered overbought when it is above 70 and oversold when it is below 30.

Traders and investors use the RSI to identify potential buy and sell signals. When the RSI indicates that an asset is oversold, it may be considered a buying opportunity, while an overbought RSI may signal that it is time to sell or take profits.

It's important to note that the RSI should not be used in isolation and should be used in conjunction with other technical and fundamental analysis tools to make informed trading decisions.

What is RSX?

Jurik RSX is a technical analysis indicator that is a variation of the Relative Strength Index Smoothed ( RSX ) indicator. It was developed by Mark Jurik and is designed to help traders identify trends and momentum in the market.