Stockbee LabelUnlock the full potential of your TradingView charts with this powerful indicator designed specifically for Stockbee methods. Instantly gain key market insights at a glance with a sleek, easy-to-read label displayed on your chart. This dynamic label provides critical data including Volume, Total Float, Market Capitalization, Trend Intensity, Average Daily Range (ADR), Half-Day Stop Loss level, and Modified Double Trouble (MDT) .

Elevate your trading strategy with real-time, essential metrics all in one place—streamlining your decision-making and boosting your confidence in the market.

Disclaimer: This indicator is inspired by and built upon the original concepts of Stockbee and EG.

Analisi fondamentale

Future Value ProjectionFuture Value Projection with Actual CAGR

This indicator calculates the future value (FV) of the current ticker’s price using its historical Compound Annual Growth Rate (CAGR). It measures how much the price has grown over a chosen lookback period, derives the average annual growth rate, and then projects the current price forward into the future.

Formulae:

CAGR:

CAGR = ( PV_now / PV_past )^(1 / t) - 1

Future Value:

FV = PV_now × ( 1 + CAGR / n )^( n × T )

Where:

PV_now = Current price

PV_past = Price t years ago

t = Lookback period (years)

CAGR = Compound Annual Growth Rate

n = Compounding periods per year (1=annual, 12=monthly, 252=daily, etc.)

T = Projection horizon (years forward)

How it works:

Select a lookback period (e.g., 3 years).

The script finds the price from that time and computes the CAGR.

It then projects the current price forward by T years using the CAGR.

The chart shows:

Current price (blue)

Projected FV target (green)

A table with CAGR and projection details

Use case:

Helps investors and traders visualize long-term growth projections if the ticker continues growing at its historical pace.

VWAP Confluência 3x VWAP Confluence 3x — Daily · Weekly · Anchored

Purpose

A pragmatic VWAP suite for execution and risk management. It plots three institutional reference lines: Daily VWAP, Weekly VWAP, and an Anchored VWAP (AVWAP) starting from a user-defined event (news, earnings, session open, swing high/low).

Why it matters

VWAP is the market’s “fair price” weighted by where volume actually traded. Confluence across timeframes and events turns noisy charts into actionable bias and clean levels.

What it does

Daily VWAP — resets each trading day; intraday “fair value.”

Weekly VWAP — resets each week; swing context and larger player defense.

Anchored VWAP — starts at a precise timestamp you set (e.g., news release).

Price source toggle — Typical Price

(

𝐻

+

𝐿

+

𝐶

)

/

3

(H+L+C)/3 or Close.

Visibility switches — enable/disable each line independently.

Anchor marker — labels the first bar of the AVWAP.

Inputs

Show Daily VWAP (on/off)

Show Weekly VWAP (on/off)

Show Anchored VWAP (on/off)

Price Source: Typical (H+L+C)/3 or Close

Anchor Time: timestamp of your event (uses the chart/exchange timezone)

How to anchor to a news event

Find the exact release time as shown in your chart’s timezone.

Open the indicator settings → set Anchor Time to that minute.

The AVWAP begins at that bar and accumulates forward.

Playbook (examples, not signals)

Strong long bias: price above Daily and Weekly VWAP; AVWAP reclaimed after news.

Strong short bias: price below Daily and Weekly; AVWAP reject after news.

Mean-revert zones: price stretches far from the active VWAPs and snaps back; size around VWAP with tight risk.

Targets: opposite VWAP, prior day/week highs/lows, or liquidity pools near AVWAP.

Best used with

Session highs/lows, liquidity sweeps, volume profile, and time-of-day filters.

Notes & limitations

Works best on markets with reliable volume (equities, futures, liquid crypto). FX spot uses synthetic volume—interpret accordingly.

Anchor Time respects the chart’s timezone. Convert news times before setting.

This is an indicator, not a backtestable strategy. No trade advice.

Disclaimer

For educational purposes only. Trading involves risk. Do your own research and manage risk responsibly.

Future 8 AM MarkerThis simple script marks the 8:00 AM New York open on the chart each day. It’s especially useful in Replay Mode to track price reactions and practice setups around this key time.

Big Mo’s Glaskugel — Macro Drawdown Risk (v1.1.2)What it does / what you see

An at-a-glance drawdown-risk oscillator that blends several macro US signals.

• A smooth, color-blended line (green→orange→red) shows the scaled risk score (0–100).

• Subtle shading marks “re-steepen warning windows” (starts when the yield curve re-steepens after an inversion; ends on normalization/cool-down).

• A compact status table summarizes: overall risk level, Yield Curve (10y–3m), Credit Stress (Baa–10y), Economy (LEI), and Valuation (CAPE).

Data used & why

Yield Curve (10y–3m) — FRED:T10Y3M. Inversions and subsequent re-steepens often precede recessions/equity drawdowns.

Credit Stress — FRED:BAA10Y vs its 1-year average (deviation in bps). Widening credit spreads flag tightening financial conditions.

Economy (LEI) — ECONOMICS:USLEI. 6-month annualized growth below a cutoff highlights macro deterioration.

Valuation (CAPE) — SHILLER_PE_RATIO_MONTH. Elevated valuations can amplify downside risk.

VIX spikes — optional boost that recognizes sudden risk repricings.

Important disclaimer

This is not a reliable or predictive indicator in all regimes. No guarantees or warranties of any kind are provided. It is not financial advice. Signals can be early, late, or wrong.

That said, it leans on well-studied warning factors (yield-curve dynamics, credit spreads, LEI weakness, valuation extremes) that have flagged major market downturns in the past.

Key customization / tweaks

Weights for each component (Yield, Credit, LEI, VIX, CAPE).

Thresholds: yield inversion months, re-steepen lookback, credit-stress bps, LEI cutoff, CAPE level, VIX spike levels.

Re-steepen boost: enable/disable, base points, half-life decay.

Shading behavior: cool-down bars to “unwarn,” max warning duration, only shade when risk ≠ green.

Scaling & smoothing: dynamic rolling max, EMA length, yellow/red thresholds.

Status table: position, and a snapshot mode to view values at a chosen historical time.

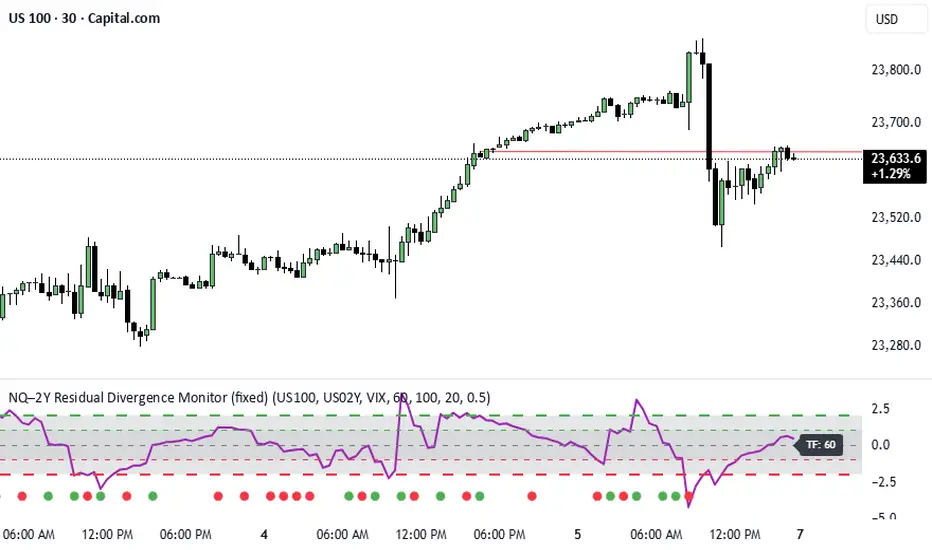

NQ–2Y CorrelationThis indicator tracks the relationship between the Nasdaq futures (NQ) and the US 2-Year Treasury yield (US02Y). The two typically move in opposite directions. This tool highlights when that relationship breaks down, and when moves become stretched to extremes. This can be useful for traders to find inflection points in price representing either overbought or oversold extremes.

Key Features

Residual Z-Score: Shows how far NQ’s returns deviate from what would be expected given moves in the 2Y. Useful for spotting stretched conditions (+/- 2σ bands).

Correlation Tracking: Fast and slow correlations between NQ and inverted 2Y returns. Helps identify regime shifts in the relationship.

Same-Direction Signals: Green dots mark when NQ and 2Y both move strongly in the same direction (rare alignment). Red dots mark strong opposing moves.

Alerts: Triggers available for residual stretches, correlation flips, and significant same-direction or opposite moves.

Usage

Monitor Z-Score to identify when the equity–rates linkage is stretched beyond typical bounds. I typically use this on the H1 or H4 timeframe.

Watch for correlation regime shifts to spot changing market dynamics. Typically price falling into support or moving into resistance as there is a false correlation or a flip.

Same-direction dots help flag unusual synchronized moves between risk assets and yields - these are especially useful for identifying false moves.

Beta Zones [MMT]Beta Zones

Overview

The Beta Zones indicator is a multi-timeframe analysis tool designed to identify and visualize price ranges (zones) across different timeframes on a TradingView chart. It draws boxes to represent high and low price levels for each enabled timeframe, helping traders spot key support and resistance zones, track price movements, and assess market signals relative to these zones. The indicator is highly customizable, allowing users to toggle timeframes, adjust colors, and control historical visibility.

Features

Multi-Timeframe Support : Tracks up to five user-defined timeframes (default: 15m, 1H, 4H, 1D, 1W) to display price zones.

Dynamic Price Boxes : Draws boxes on the chart to represent the high and low prices for each timeframe, updating dynamically as new bars form.

Signal Indicators : Provides directional signals (▲, ▼, →) based on the previous close relative to the current box's top and bottom.

Customizable Display : Includes options to show or hide historical boxes, adjust box colors, and configure a summary table.

Summary Table : Displays a table with timeframe status, price range, and signal information for quick reference.

Settings

Timeframes

Enable/Disable : Toggle each timeframe (e.g., 15m, 1H, 4H, 1D, 1W) to display or hide its respective zones.

Timeframe Selection : Choose custom timeframes for each of the five slots.

Color Customization : Set unique fill and border colors for each timeframe's boxes (default colors: green, blue, orange, purple, red).

Display

Max Historical Boxes : Limit the number of historical boxes per timeframe (default: 1, max: 50).

Show History : Toggle visibility of historical boxes (default: false, showing only the latest box).

Min Box Height : Ensures boxes have a minimum height in ticks (default: 1.0, currently hardcoded).

Table

Show Table : Enable or disable the summary table (default: true).

Background Color : Customize the table's background color.

Header Color : Set the color for the table's header row.

Text Color : Adjust the text color for table content.

Table Columns

Timeframe : Displays the selected timeframe (e.g., 15m, 1H).

Color : Shows the color associated with the timeframe's boxes.

Status : Indicates if the timeframe is "Active" (valid and lower than the chart's timeframe), "Invalid" (enabled but not lower), or "Disabled".

Range : Shows the price range (high - low) of the current box.

Signal : Displays ▲ (price above box), ▼ (price below box), or → (price within box) based on the previous close.

How to Use

Add to Chart : Apply the indicator to your TradingView chart.

Configure Timeframes : Enable desired timeframes and adjust their settings (e.g., 15m, 1H) to match your trading strategy.

Analyze Zones : Use the boxes to identify key price levels for support, resistance, or breakout opportunities.

Monitor Signals : Check the table's "Signal" column to gauge price direction relative to each timeframe's zone.

Customize Appearance : Adjust colors and historical box visibility to suit your preferences.

Ideal For

Swing Traders : Identify key price zones across multiple timeframes for entry/exit points.

Day Traders : Monitor short-term price movements relative to higher timeframe zones.

Technical Analysts : Combine with other indicators to confirm support/resistance levels.

Liquidity Sweep Breakout - LSBLiquidity Sweep Breakout - LSB

A professional session-based breakout system designed for OANDA:USDJPY and other JPY pairs.

Not guesswork, but precision - built on detailed observation of institutional moves to capture clear trade direction daily.

Master the Market’s Daily Bank Flow.

---

Strategy Detail:

I discovered this strategy after carefully studying how Japanese banks influence the forex market during their daily settlement period. Banks are some of the biggest players in the financial world, and when they adjust or settle their accounts in the morning, it often creates a push in the market. From years of observation, I noticed a consistent pattern, once banks finish their settlements, the market usually continues moving in the same direction that was formed right after those actions. This daily banking flow often sets the tone for the entire trading session, especially for JPY pairs like USDJPY.

To capture this move, I built the indicator so that it follows the bank-driven trend with clear rules for entries, stop-loss (SL), and take-profit (TP). The system is designed with professional risk management in mind. By default, it assumes a $10,000 account size, risks only 1% of that balance per trade, and targets a 1:1.5 reward-to-risk ratio. This means for every $100 risked, the potential profit is $150. Such controlled risk makes the system safer and more sustainable for long-term traders. At the same time, users are not limited to this setup, they can adjust the account balance in the settings, and the indicator will automatically recalculate the lot size and risk levels based on their own capital. This ensures the strategy works for small accounts and larger accounts alike.

🌍 Why It Works

Fundamentally driven: Based on **daily Japanese banking settlement flows**.

Session-specific precision: Targets the exact window when USDJPY liquidity reshapes.

Risk-managed: Always calculates lot size based on account and risk preferences.

Automatable: With webhook + MT5 EA, it can be fully hands-free.

---

✅ Recommended

Pair: USDJPY (best observed behavior).

Timeframe: 3-Minute chart.

Platform: TradingView Premium (for webhooks).

Execution: MT5 via EA.

---

🔎 Strategy Concept

The Tokyo Magic Breakout (TMB) is built on years of session observation and the unique daily rhythm of the Japanese banking system.

Every morning between 5:50 AM – 6:10 AM PKT (09:50 – 10:10 JST), Japanese banks perform daily reconciliation and settlement. This often sets the tone for the USDJPY direction of the day.

This strategy isolates that critical moment of liquidity adjustment and waits for a clean breakout confirmation. Instead of chasing noise, it executes only when price action is aligned with the Tokyo market’s hidden flows.

---

🕒 Timing Logic

Session Start: 5:00 AM PKT (Tokyo market open range).

Magic Candle: The 5:54 AM PKT candle is marked as the reference “breakout selector.”

Checkpoints: First confirmation at 6:30 AM PKT, then every 15 minutes until 8:30 AM PKT.

* If price stays inside the magic range → wait.

* If a breakout happens but the candle wick touches the range → wait for the next checkpoint.

* If by 8:30 AM PKT no clean breakout occurs → the day is marked as No Trade Day (NTD).

👉 Recommended timeframe: 3-Minute chart (3M) for precise signals.

---

📈 Trade Execution

Entry: Clean break above/below the magic candle’s range.

Stop-Loss: Opposite side of the Tokyo session high/low.

Take-Profit: Calculated by Reward\:Risk ratio (default 1.5:1).

Lot Size: Auto-calculated based on your risk model:

* Fixed Dollar

* % of Equity

* Conservative (minimum of both).

Visuals include:

✅ Entry/SL/TP lines

✅ Shaded risk (red) and reward (green) zones

✅ Trade labels (Buy/Sell with lot size & levels)

✅ TP/SL hit markers

---

🔔 Alerts & Automation (AutoTMB)

This strategy is fully automation-ready with EA + MT5:

1. Enable alerts in TMB settings.

2. Insert your PineConnector License Key.

3. Configure your risk management preferences.

4. Create a TradingView alert → in the message box simply type:

Pine Script®

{{alert_message}}

and set the EA webhook.

Now, every breakout trade (with exact entry, SL, TP, and lot size) is sent instantly.

👉 On your MT5:

* Install the EA.

* Use the same license key.

* Run it on a VPS or local MT5 terminal.

You now have a hands-free trading system: AutoTMB.

Economic Profit (Fixed & Labeled) — Rated + PeersFRAC (Fundamental-Rated-Asset-Calculate)

FRAC is a fundamentals-driven tool designed to measure whether a company is creating or destroying shareholder value. Unlike surface ratios, FRAC uses Economic Profit (ROIC – WACC) as its engine, showing whether a business truly outperforms its cost of capital.

🔹 What FRAC Does

Calculates ROIC (Return on Invested Capital) vs. WACC (Weighted Average Cost of Capital).

Shows whether a company is creating or destroying shareholder value.

Uses tiered color coding for clarity:

🔵 Superior (Aqua Blue) → Top tier; best of the best.

🟣 Elite (Purple) → Strong value creation.

🟢 Positive (Green) → Solid, creating shareholder value.

🟡 Marginal (Yellow) → Barely covering cost of capital.

🔴 Negative (Red) → Value destruction.

🔹 Composite Ranking System (1–4)

FRAC also assigns each company a Composite Rank so you can compare multiple names side by side. The rank works like this:

Rank 1 → Superior (🔵 Aqua Blue)

Best possible rating; wide gap between ROIC and WACC.

Rank 2 → Elite (🟣 Purple)

Strongly positive; above-average capital efficiency.

Rank 3 → Positive (🟢 Green)

Creating value but only moderately; not a top compounder.

Rank 4 → Marginal/Negative (🟡/🔴)

Weak or destructive; either barely covering WACC or losing money on capital.

✅ How to Use the Ranks

When comparing a set of peers (e.g., NVDA, AMD, INTC):

FRAC will display each company’s color rating + composite rank (1–4).

You can instantly see who is strongest vs. weakest in the group.

Best decisions = overweight Rank 1 & 2 companies, avoid Rank 4 names.

🔹 Key Inputs Explained

Risk-Free Asset → Typically the 10-Year US Treasury yield (US10Y).

Corporate Tax Rate → Effective tax rate for the company’s country (e.g., USCTR).

Expected Market Return → Historical average ~8–10%, adjustable.

Beta Lookback Period → Controls how far back Beta is calculated (longer = more stable, shorter = more reactive).

👉 These must be set correctly for FRAC to calculate WACC accurately.

🔹 Example Comparison

NVDA: ROIC 25% – WACC 7% = +18% → 🔵 Superior → Rank 1

AMD: ROIC 17% – WACC 8% = +9% → 🟣 Elite → Rank 2

INTC: ROIC 11% – WACC 9% = +2% → 🟢 Positive → Rank 3

FSLY: ROIC 5% – WACC 10% = –5% → 🔴 Negative → Rank 4

🔹 Why It Matters

Buffett said: “The best businesses are those that can consistently generate returns on capital above their cost of capital.”

FRAC turns that into a visual + numeric rating system (1–4), making comparisons across peers simple and actionable.

🔹 Credit

FRAC was created by Hunter Hammond (Elite x FineFir), inspired by corporate finance models of Economic Profit and Economic Value Added (EVA).

⚠️ Disclaimer: FRAC is a research framework, not financial advice. Always pair with full due diligence.

US Liquidity-Weighted Business Cycle📈 BTC Liquidity-Weighted Business Cycle

This indicator models the Bitcoin macro cycle by comparing its logarithmic price against a log-transformed liquidity proxy (e.g., US M2 Money Supply). It helps visualize cyclical tops and bottoms by measuring the relative expansion of Bitcoin price versus fiat liquidity.

🧠 How It Works:

Transforms both BTC and M2 using natural logarithms.

Computes a liquidity ratio: log(BTC) – log(M2) (i.e., log(BTC/M2)).

Runs MACD on this ratio to extract business cycle momentum.

Plots:

🔴 Histogram bars showing cyclical growth or contraction.

🟢 Top line to track the relative price-to-liquidity trend.

🔴 Cycle peak markers to flag historical market tops.

⚙️ Inputs:

Adjustable MACD lengths

Toggle for liquidity trend line overlay

🔍 Use Cases:

Identifying macro cycle tops and bottoms

Timing long-term Bitcoin accumulation or de-risking

Confirming global liquidity's influence on BTC price movement

Note: This version currently uses US M2 (FRED:M2SL) as the liquidity base. You can easily expand it with other global M2 sources or adjust the weights.

NQ FVG + MSS ChecklistThe NQ FVG + MSS Quick Checklist is a visual trading HUD for Nasdaq 100 (NQ) futures. It helps traders quickly track key setup elements: session & previous day levels, 5M FVG, retests, 1M MSS, and 1M FVG inside MSS.

Each step can be manually ticked, and a Trade Score shows setup strength at a glance. The checklist table sits on top of all chart elements for easy reference without interfering with your analysis.

Features:

Step-by-step NQ trading checklist

Manual inputs with visual ✅/❌

Trade Score for quick setup confirmation

Table overlay always on top of the chart

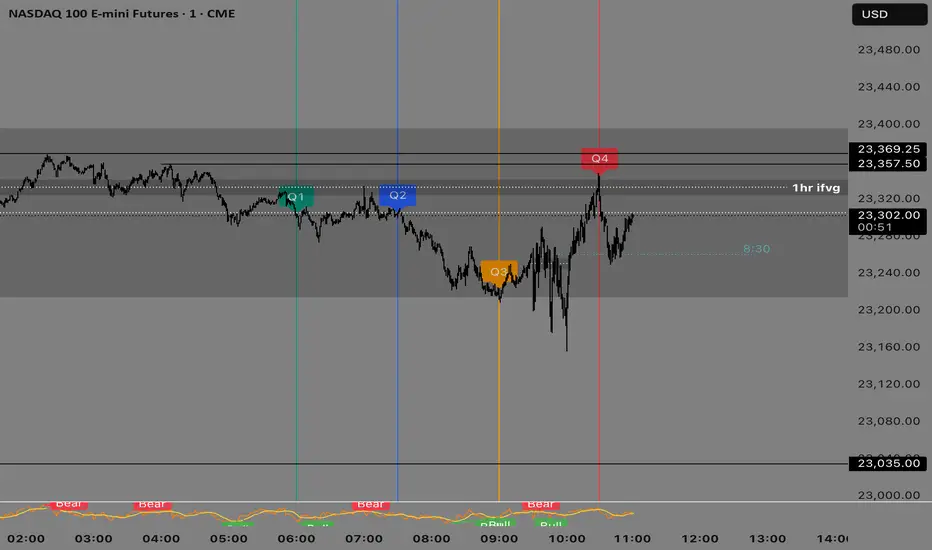

Quarterly Theory —Q1,Q2,Q3,Q4The Quarterly Theory Indicator is a trading tool designed to visualize the natural time-based cycles of the market, based on the principles of Quarterly Theory, popularized by the Inner Circle Trader (ICT). The indicator divides market sessions into four equal “quarters” to help traders identify potential accumulation, manipulation, and distribution phases (AMD model) and improve the timing of entries and exits.

Key Features:

Quarter Divisions (Q1–Q4):

Each market session (e.g., NY AM, London, Asia) is divided into four quarters.

Vertical lines mark the beginning of each quarter, making it easy to track session structure.

Optional labels show Q1, Q2, Q3, and Q4 directly on the chart.

True Open (Q2 Open):

The True Open is the opening price of Q2, considered a key reference point in Quarterly Theory.

A horizontal red line is drawn at the True Open price with a label showing the exact value.

This line helps traders filter bullish and bearish setups:

Buy below the True Open if the market is bullish.

Sell above the True Open if the market is bearish.

Session Awareness:

The indicator can automatically detect market sessions and reset lines and labels for each new session.

Ensures that only the current session’s True Open and quarter lines are displayed, reducing chart clutter.

Timeframe Flexibility:

Works on any chart timeframe (1-minute to daily).

Maintains accurate alignment of quarters and True Open regardless of the timeframe used.

Purpose of Quarterly Theory:

Quarterly Theory is based on the idea that market behavior is fractal and time-driven. By dividing sessions into four quarters, traders can anticipate potential market phases:

Q1: Initial price discovery and setup for the session.

Q2: Accumulation or manipulation phase, where the True Open is established.

Q3: Manipulation or Judas Swing phase designed to trap traders.

Q4: Distribution or trend continuation/reversal.

By visualizing these quarters and the True Open, traders can reduce ambiguity, identify high-probability setups, and improve their timing in line with the ICT AMD (Accumulation, Manipulation, Distribution) framework.

Forward P/E CalculatorI could not find a forward P/E indicator that gave me proper results. So here is mine.

Locked 5m 13 EMA & 15m 20 EMA with Mid EMA & SignalsThis indicator overlays the 5-minute 13 EMA and the 15-minute 20 EMA on any chart timeframe up to 15 minutes, along with a mid EMA (5-minute 36-period) for reference.

Features include:

EMA Cross Detection: Shows bullish and bearish cross arrows when the 5m 13 EMA crosses the 15m 20 EMA.

EMA Fill: Highlights the area between the EMAs in green (bullish) or red (bearish).

Mid EMA Buy/Sell Signals: Generates buy signals when price touches the mid EMA in a bullish stack and sell signals in a bearish stack.

Custom Alerts: Alerts for EMA crosses, EMA stack direction, and mid EMA buy/sell triggers.

Timeframe Safety Warning: Alerts if applied on timeframes higher than 15 minutes.

Ideal For:

Traders who want a locked, non-repainting EMA setup for multi-timeframe analysis and clear entry/exit signals based on mid-range EMA interaction.

Inputs:

Show/Hide arrows for EMA crosses

Show/Hide fill between EMAs

Show/Hide mid EMA line

Show/Hide buy/sell signals

Fill transparency adjustment

SPX → NQ Levels ConverterSPX → NQ Levels Converter is a Pine Script indicator that projects key S&P 500 (SPX) levels onto the NASDAQ 100 (NQ) chart using a configurable conversion ratio.

• Dynamic ratio: calculates the live SPX/NQ ratio in real time.

• Static ratio: allows manual input of a fixed ratio.

• Supports up to 10 custom SPX levels, automatically converted into their equivalent NQ values.

• Each level is displayed with a line and label (SPX → NQ) with independent color settings.

• Advanced visualization controls:

• line extension (right, left, both, or fixed)

• line length & placement

• label side & offset.

• Lines and labels auto-update on every bar to stay accurate over time.

Use case: particularly useful for traders who track SPX option levels or support/resistance zones but execute trades on the NQ.

XMR Divergences vs KrakenSUMMARY

This script finds the percentage difference between Kraken, and multiple other exchanges, for the price of XMRUSD, and then runs a variable length moving average of those differences. Optionally, you can multiply by the reported volume of the exchange in question. Skip to "USAGE" at the bottom for a quick view of the settings. But I recommend reading DETAILED DESCRIPTION as well.

PURPOSE

The purpose of this script is to get a look into the relative funds flows of XMR between Kraken and the other exchanges. So long as an exchange withdraws are open: 1) Negative divergences indicate XMR outflows from the exchange under consideration, 2) Postive divergences indicate XMR inflows from Kraken to the exchange.

This appears to be moderately correlated with price movements in Monero (but not always). There is also the theory that positive accumulation is a leading indication of a growing probability of postive price action in the general crypto market, and negative accumulation is a leading indicator of an upcoming peak. In other words, exchanges like to accumulate Monero quietly during calm downtimes, and they like to manage its price from gaining too much attention (pump) during broad market positivity.

BACKGROUND

It's well known among XMR traders that most exchanges are operating on a heavy fractional reserve basis as regards Monero. The past 2 years have seen regular and repeated withdraw freezes, sometimes for weeks/months at a time. Occasionally, liquidity stress tests have been performed, with predictable results - none of these exchanges are able to continue supporting withdraws.

Kraken is the only exchange of meaningful volume that has never frozen withdraws for more than an hour or so. Thus, we theorize that Kraken is operating with all, or most of the XMR they claim to have.

Furthermore, we have seen in the past, large price negative price divergences of these fractional reserve exchanges relative to Kraken. As the social outcry grew stronger for this malfeasance, these exchanges have gone to greater lengths to hide their price divergences.

On minute-by-minute ; hour-by-hour basis, typically, a look with the naked eye would show oscillation around the zero point. But when you average it out, especially on lower timeframes (like the 1 and 5 min candles), you can very clearly see that when withdraws are shut down, these exchanges simultaneously diverge their prices downwards as well.

DETAILED DESCRIPTION

The ideal view of price divergence would compare second-by-second prices, and then run something like a rolling 4-hr or 1-day SMA to average out the overall divergences. However, due to limitations of TradingView, this is impractical/impossible for actual usage/viewing. As a result, a balance must be struck, when selecting the combination of the candle period, and the SMA lookback length.

I find that 5min candles, with a 48-period lookback (that equates to a rolling 4-hour SMA), offers the best view of recent and historical price divergence activity. This of course means that we're only sampling price divergences once every 5 minutes, but it still provides a decent look at what's happening. If this script gets popular, I wouldn't be surprised if these exchanges start timing their candle closes to mask their misdeeds, but that's of course speculative on my part.

The other important factor here, *IS TO MULTIPLY BY VOLUME*. Some of these no-volume exchanges have large price divergences. But if they're not doing any real volume, then it doesn't really have any real market impact. Thus, I recommend keeping the "Make volume adjustment" option on.

If that ends up happening, we'll have to infer that by comparing the difference in close prices, vs the difference in the highest or lowest intra-candle prices (wicks). Typically a divergence should have all 3 showing similar results.

Notes regarding "Sum_of_All": This only makes sense when multiplying by volume. So only check this if you also made the volume adjustment. Generally I believe that *Binance* sets the tone. However, we have seen numerous occasions where Binance diverges down, and the others diverge up. I believe this is a social influence tactic, since most people look at Binance price. Meanwhile, they're trying to accumulate some small amount on the other exchanges to minimize their overall loss. This of course assumes collusion by these exchanges, which is a high likely hood, seeing as how in May 2021, they all diverged together simultaneously (among other evidence).

USAGE

I recommend using your browser zoom, to see data beyond 1 month in the past.

Lookback - The number of candles over which to conduct a moving average. On 5-min candles for example, here's how the math works out:

12 - Equates to a 1 hr MA

24 - 2 hrs

48 - 4 hrs (default)

288 - 1 day

2880 - 10 days

Make Volume Adjustment - Recommend that you usually keep this on.

Line Widths - Set to preference

Show_Close_Price? - You can compute the difference at candle close. Or you can check the other boxes to compare the highest/lowest prices for intra candle prices (wicks).

Show Sum_of_All? - You can sum all of the differences, which only makes sense if you're making the volume adjustement. Default is off. Below, you can also choose which exchanges to include in the sum.

This works best on lower timeframes, like the 1m, 5, and 15m charts. I personally use 5m, with 48 or 96 length lookback. You get a better view of the real time price divergences that way.

AI Fib Strategy (Full Trade Plan)This indicator automatically plots Fibonacci retracements and a Golden Zone box (61.8%–65% retracement) based on the 4H candle body high/low.

Features:

Auto-detects session breaks or daily breaks (configurable).

Draws standard Fib retracement levels (0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, 100%).

Highlights the Golden Zone for high-probability trade entries.

Optional Take Profit extensions (TP1, TP2, TP3).

Fully compatible with Pine Script v6.

Usage:

Best applied on intraday charts (15m, 30m, 1H).

Use the Golden Zone for entry confirmations.

Combine with candlestick patterns, order blocks, or volume for stronger signals.

BTC Power Law Valuation BandsBTC Power Law Rainbow

A long-term valuation framework for Bitcoin based on Power Law growth — designed to help identify macro accumulation and distribution zones, aligned with long-term investor behavior.

🔍 What Is a Power Law?

A Power Law is a mathematical relationship where one quantity varies as a power of another. In this model:

Price ≈ a × (Time)^b

It captures the non-linear, exponentially slowing growth of Bitcoin over time. Rather than using linear or cyclical models, this approach aligns with how complex systems, such as networks or monetary adoption curves, often grow — rapidly at first, and then more slowly, but persistently.

🧠 Why Power Law for BTC?

Bitcoin:

Has finite supply and increasing adoption.

Operates as a monetary network , where Metcalfe’s Law and power laws naturally emerge.

Exhibits exponential growth over logarithmic time when viewed on a log-log chart .

This makes it uniquely well-suited for power law modeling.

🌈 How to Use the Valuation Bands

The central white line represents the modeled fair value according to the power law.

Colored bands represent deviations from the model in logarithmic space, acting as macro zones:

🔵 Lower Bands: Deep value / Accumulation zones.

🟡 Mid Bands: Fair value.

🔴 Upper Bands: Euphoria / Risk of macro tops.

📐 Smart Money Concepts (SMC) Alignment

Accumulation: Occurs when price consolidates near lower bands — often aligning with institutional positioning.

Markup: As price re-enters or ascends the bands, we often see breakout behavior and trend expansion.

Distribution: When price extends above upper bands, potential for exit liquidity creation and distribution events.

Reversion: Historically, price mean-reverts toward the model — rarely staying outside the bands for long.

This makes the model useful for:

Cycle timing

Long-term DCA strategy zones

Identifying value dislocations

Filtering short-term noise

⚠️ Disclaimer

This tool is for educational and informational purposes only . It is not financial advice. The power law model is a non-predictive, mathematical framework and does not guarantee future price movements .

Always use additional tools, risk management, and your own judgment before making trading or investment decisions.

NAS100 Component Sentiment Scanner# NAS100 Component Sentiment Scanner

## 🎯 Overview

The NAS100 Component Sentiment Scanner analyzes the top-weighted stocks in the NASDAQ-100 index to provide real-time bullish/bearish sentiment signals that can help predict NAS100 price movements. This indicator combines multiple technical analysis methods to give traders a comprehensive view of underlying market sentiment.

## 📊 How It Works

The indicator calculates sentiment scores for major NASDAQ-100 components (AAPL, MSFT, NVDA, GOOGL, AMZN, META, TSLA, AVGO, COST, NFLX) using:

- **RSI Analysis**: Identifies overbought/oversold conditions

- **Moving Average Trends**: Compares fast vs slow MA positioning

- **Volume Confirmation**: Validates moves with volume thresholds

- **Price Momentum**: Analyzes recent price direction

- **Market Cap Weighting**: Uses actual NASDAQ-100 weightings for accuracy

## 🚀 Key Features

### Real-Time Sentiment Analysis

- Weighted composite score based on individual stock analysis

- Color-coded sentiment line (Green = Bullish, Red = Bearish)

- Dynamic background coloring for strong signals

### Interactive Data Table

- Shows individual stock scores and signals

- Bullish/Bearish stock count summary

- Customizable position and size

### Smart Signal System

- **Bullish Signals**: Green triangle up when sentiment crosses threshold

- **Bearish Signals**: Red triangle down when sentiment falls below threshold

- **Alert Conditions**: Automatic notifications for signal changes

## ⚙️ Customization Options

### Technical Analysis Settings

- **RSI Period**: Adjust lookback period (default: 14)

- **RSI Levels**: Set overbought/oversold thresholds

- **Moving Averages**: Configure fast/slow MA periods

- **Volume Threshold**: Set volume confirmation multiplier

### Signal Thresholds

- **Bullish/Bearish Levels**: Customize trigger points

- **Strong Signal Levels**: Set extreme sentiment thresholds

- Fine-tune sensitivity to market conditions

### Display Options

- **Toggle Table**: Show/hide sentiment data table

- **Table Position**: 6 position options (Top/Bottom/Middle + Left/Right)

- **Table Size**: Choose from Tiny, Small, Normal, or Large

- **Background Colors**: Enable/disable signal backgrounds

- **Signal Arrows**: Show/hide buy/sell indicators

### Stock Selection

- **Individual Control**: Enable/disable any of the 10 major stocks

- **Dynamic Weighting**: Automatically adjusts calculations based on selected stocks

- **Flexible Analysis**: Focus on specific sectors or market leaders

## 📈 How to Use

### 1. Basic Setup

1. Add the indicator to your NAS100 chart

2. Default settings work well for most traders

3. Observe the sentiment line and signals

### 2. Signal Interpretation

- **Score > 30**: Bullish bias for NAS100

- **Score > 50**: Strong bullish signal

- **Score -30 to 30**: Neutral/consolidation

- **Score < -30**: Bearish bias for NAS100

- **Score < -50**: Strong bearish signal

### 3. Trading Strategies

**Trend Following:**

- Buy NAS100 when bullish signals appear

- Sell/short when bearish signals trigger

- Use background colors for quick visual confirmation

**Divergence Trading:**

- Watch for sentiment/price divergences

- Strong sentiment with weak NAS100 price = potential breakout

- Weak sentiment with strong NAS100 price = potential reversal

**Consensus Trading:**

- Monitor bullish/bearish stock counts in table

- 8+ stocks aligned = strong directional bias

- Mixed signals = wait for clearer consensus

### 4. Advanced Usage

- Combine with your existing NAS100 trading strategy

- Use multiple timeframes for confirmation

- Adjust thresholds based on market volatility

- Focus on specific stocks by disabling others

## 🔔 Alert Setup

The indicator includes built-in alert conditions:

1. Go to TradingView Alerts

2. Select "NAS100 Component Sentiment Scanner"

3. Choose from available alert types:

- NAS100 Bullish Signal

- NAS100 Bearish Signal

- Strong Bullish Consensus

- Strong Bearish Consensus

## 💡 Pro Tips

### Optimization

- **High Volatility**: Increase signal thresholds (±40, ±60)

- **Low Volatility**: Decrease thresholds (±20, ±40)

- **Day Trading**: Use smaller table, focus on real-time signals

- **Swing Trading**: Enable background colors, larger thresholds

### Best Practices

- Don't use as a standalone system - combine with price action

- Check individual stock table for context

- Monitor during market open for most reliable signals

- Consider earnings seasons for individual stock impacts

### Market Conditions

- **Trending Markets**: Higher accuracy, use with trend following

- **Ranging Markets**: Watch for false signals, increase thresholds

- **News Events**: Individual stock news can skew sentiment temporarily

## 🎨 Visual Guide

- **Green Line Above Zero**: Bullish sentiment building

- **Red Line Below Zero**: Bearish sentiment building

- **Background Color Changes**: Strong signal confirmation

- **Triangle Arrows**: Entry/exit signal points

- **Table Colors**: Quick sentiment overview

## ⚠️ Important Notes

- This indicator analyzes component stocks, not NAS100 directly

- Market cap weightings approximate real NASDAQ-100 weightings

- Sentiment can change rapidly during volatile periods

- Always use proper risk management

- Combine with other technical analysis tools

## 🔧 Troubleshooting

- **No signals**: Check if thresholds are too extreme

- **Too many signals**: Increase threshold sensitivity

- **Table not showing**: Ensure "Show Sentiment Table" is enabled

- **Missing stocks**: Verify individual stock toggles in settings

---

**Suitable for**: Day traders, swing traders, NAS100 specialists, index traders

**Best Timeframes**: 5min, 15min, 1H, 4H

**Market Sessions**: US market hours for highest accuracy

EPS YoY% Labels (MarketSurge / IBD style)This script automatically calculates and displays year-over-year quarterly EPS growth (%) directly on the chart, in the same style used by MarketSurge / IBD.

🔹 Key Features

Detects each quarterly earnings report and shows EPS YoY growth as a label above the bar.

Works with both reported EPS and standardized EPS (selectable in settings).

Positive growth is highlighted in green, while negative growth is highlighted in red.

Optional setting to hide negative results for a cleaner, bullish-focused view.

Adjustable decimal precision (0–2 decimals) for percentage display.

🔹 Why it’s useful

EPS growth is one of the core fundamentals that top traders like Mark Minervini and William O’Neil (IBD) focus on when screening for market leaders.

Now you can see at a glance how a stock’s earnings power is accelerating or decelerating — without flipping between platforms.

Combine with Relative Strength (RS) analysis and price/volume patterns for a complete growth-stock trading workflow.

🔹 Example

If a company reports EPS of $1.20 this quarter vs. $0.80 in the same quarter last year, the label will display:

EPS +50% (green).

Currency Strength v3.0Currency Strength v3.0

Summary

The Currency Strength indicator is a powerful tool designed to gauge the relative strength of major and emerging market currencies. By plotting the True Strength Index (TSI) of various currency indices, it provides a clear visual representation of which currencies are gaining momentum and which are losing it. This indicator automatically detects the currency pair on your chart and highlights the corresponding strength lines, simplifying analysis and helping you quickly identify potential trading opportunities based on currency dynamics.

Key Features

Comprehensive Currency Analysis: Tracks the strength of 19 currencies, including major pairs and several emerging market currencies.

Automatic Pair Detection: Intelligently identifies the base and quote currency of the active chart, automatically highlighting the relevant strength lines.

Dynamic Coloring: The base currency is consistently colored blue, and the quote currency is colored gold, making it easy to distinguish between the two at a glance.

Non-Repainting TSI Calculation: Uses the True Strength Index (TSI) for smooth and reliable momentum readings that do not repaint.

Customizable Settings: Allows for adjustment of the fast and slow periods for the TSI calculation to fit your specific trading style.

Clean Interface: Features a minimalist legend table that only displays the currencies relevant to your current chart, keeping your workspace uncluttered.

How It Works

The indicator pulls data from major currency indices (like DXY for the US Dollar and EXY for the Euro). For currencies that don't have a dedicated index, it uses their USD pair (e.g., USDCNY) and inverts the calculation to derive the currency's strength relative to the dollar. It then applies the True Strength Index (TSI) to this data. The TSI is a momentum oscillator that is less volatile than other oscillators, providing a more reliable measure of strength. The resulting values are plotted on the chart, allowing you to see how different currencies are performing against each other in real-time.

How to Use

Trend Confirmation: When the base currency's line is rising and above the zero line, and the quote currency's line is falling, it can confirm a bullish trend for the pair. The opposite would suggest a bearish trend.

Identifying Divergences: Look for divergences between the currency strength lines and the price action of the pair. For example, if the price is making higher highs but the base currency's strength is making lower highs, it could signal a potential reversal.

Crossovers: A crossover of the base and quote currency lines can signal a shift in momentum. A bullish signal occurs when the base currency line crosses above the quote currency line. A bearish signal occurs when it crosses below.

Overbought/Oversold Levels: The horizontal dashed lines at 0.5 and -0.5 can be used as general guides for overbought and oversold conditions, respectively. Strength moving beyond these levels may indicate an unsustainable move that is due for a correction.

Settings

Fast Period: The short-term period for the TSI calculation. Default is 7.

Slow Period: The long-term period for the TSI calculation. Default is 15.

Index Source: The price source used for the calculations (e.g., Close, Open). Default is Close.

Base Currency Color: The color for the base currency line. Default is Royal Blue.

Quote Currency Color: The color for the quote currency line. Default is Goldenrod.

Disclaimer

This indicator is intended for educational and analytical purposes only. It is not financial advice. Trading involves substantial risk, and past performance is not indicative of future results. Always conduct your own research and risk management before making any trading decisions.