Cross-Market Regime Scanner [BOSWaves]Cross-Market Regime Scanner - Multi-Asset ADX Positioning with Correlation Network Visualization

Overview

Cross-Market Regime Scanner is a multi-asset regime monitoring system that maps directional strength and trend intensity across correlated instruments through ADX-based coordinate positioning, where asset locations dynamically reflect their current trending versus ranging state and bullish versus bearish bias.

Instead of relying on isolated single-asset trend analysis or static correlation matrices, regime classification, spatial positioning, and intermarket relationship strength are determined through ADX directional movement calculation, percentile-normalized coordinate mapping, and rolling correlation network construction.

This creates dynamic regime boundaries that reflect actual cross-market momentum patterns rather than arbitrary single-instrument levels - visualizing trending assets in right quadrants when ADX strength exceeds thresholds, positioning ranging assets in left quadrants during consolidation, and incorporating correlation web topology to reveal which instruments move together or diverge during regime transitions.

Assets are therefore evaluated relative to ADX-derived regime coordinates and correlation network position rather than conventional isolated technical indicators.

Conceptual Framework

Cross-Market Regime Scanner is founded on the principle that meaningful market insights emerge from simultaneous multi-asset regime awareness rather than sequential single-instrument analysis.

Traditional trend analysis examines assets individually using separate chart windows, which often obscures the broader cross-market regime structure and correlation patterns that drive coordinated moves. This framework replaces isolated-instrument logic with unified spatial positioning informed by actual ADX directional measurements and correlation relationships.

Three core principles guide the design:

Asset positioning should be determined by ADX-based regime coordinates that reflect trending versus ranging state and directional bias simultaneously.

Spatial mapping must normalize ADX values to place assets within consistent quadrant boundaries regardless of instrument volatility characteristics.

Correlation network visualization reveals which assets exhibit coordinated behavior versus divergent regime patterns during market transitions.

This shifts regime analysis from isolated single-chart monitoring into unified multi-asset spatial awareness with correlation context.

Theoretical Foundation

The indicator combines ADX directional movement calculation, coordinate normalization methodology, quadrant-based regime classification, and rolling correlation network construction.

A Wilder's smoothing implementation calculates ADX, +DI, and -DI for each monitored asset using True Range and directional movement components. The ADX value relative to a configurable threshold determines X-axis positioning (ranging versus trending), while the difference between +DI and -DI determines Y-axis positioning (bearish versus bullish). Coordinate normalization caps values within fixed boundaries for consistent quadrant placement. Pairwise correlation calculations over rolling windows populate a network graph where line thickness and opacity reflect correlation strength.

Five internal systems operate in tandem:

Multi-Asset ADX Engine : Computes smoothed ADX, +DI, and -DI values for up to 8 configurable instruments using Wilder's directional movement methodology.

Coordinate Transformation System : Converts ADX strength and directional movement into normalized X/Y coordinates with threshold-relative scaling and boundary capping.

Quadrant Classification Logic : Maps coordinate positions to four distinct regime states—Trending Bullish, Trending Bearish, Ranging Bullish, Ranging Bearish—with color-coded zones.

Historical Trail Rendering : Maintains rolling position history for each asset, drawing gradient-faded trails that visualize recent regime trajectory and velocity.

Correlation Network Calculator : Computes pairwise return correlations across all enabled assets, rendering weighted connection lines in circular web topology with strength-based styling.

This design allows simultaneous cross-market regime awareness rather than reacting sequentially to individual instrument signals.

How It Works

Cross-Market Regime Scanner evaluates markets through a sequence of multi-asset spatial processes:

Data Request Processing : Security function retrieves high, low, and close values for up to 8 configurable symbols with lookahead offset to ensure confirmed bar data.

ADX Calculation Per Asset : True Range computed from high-low-close relationships, directional movement derived from up-moves versus down-moves, smoothed via Wilder's method over configurable period.

Directional Index Derivation : +DI and -DI calculated as smoothed directional movement divided by smoothed True Range, scaled to percentage values.

Coordinate Transformation : X-axis position equals (ADX - threshold) * 2, capped between -50 and +50; Y-axis position equals (+DI - -DI), capped between -50 and +50.

Quadrant Assignment : Positive X indicates trending (ADX > threshold), negative X indicates ranging; positive Y indicates bullish (+DI > -DI), negative Y indicates bearish.

Trail History Management : Configurable-length position history maintains recent coordinates for each asset, rendering gradient-faded lines connecting sequential positions.

Velocity Vector Calculation : 7-bar coordinate change converted to directional arrow overlays showing regime momentum and trajectory.

Return Correlation Processing : Bar-over-bar returns calculated for each asset, pairwise correlations computed over rolling window.

Network Graph Construction : Assets positioned in circular topology, correlation lines drawn between pairs exceeding threshold with thickness/opacity scaled by correlation strength, positive correlations solid green, negative correlations dashed red.

Risk Regime Scoring : Composite score aggregates bullish risk-on assets (equities, crypto, commodities) minus bullish risk-off assets (gold, dollar, VIX), generating overall market risk sentiment with colored candle overlay.

Together, these elements form a continuously updating spatial regime framework anchored in multi-asset momentum reality and correlation structure.

Interpretation

Cross-Market Regime Scanner should be interpreted as unified spatial regime boundaries with correlation context:

Top-Right Quadrant (TREND ▲) : Assets positioned here exhibit ADX above threshold with +DI exceeding -DI - confirmed bullish trending conditions with directional conviction.

Bottom-Right Quadrant (TREND ▼) : Assets positioned here exhibit ADX above threshold with -DI exceeding +DI - confirmed bearish trending conditions with directional conviction.

Top-Left Quadrant (RANGE ▲) : Assets positioned here exhibit ADX below threshold with +DI exceeding -DI - ranging consolidation with bullish bias but insufficient trend strength.

Bottom-Left Quadrant (RANGE ▼) : Assets positioned here exhibit ADX below threshold with -DI exceeding +DI - ranging consolidation with bearish bias but insufficient trend strength.

Position Trails : Gradient-faded lines connecting recent coordinate history reveal regime trajectory - curved paths indicate regime rotation, straight paths indicate sustained directional conviction.

Velocity Arrows : Directional vectors overlaid on current positions show 7-bar regime momentum - arrow length indicates speed of regime change, angle indicates trajectory direction.

Correlation Web : Circular network graph positioned left of main quadrant map displays pairwise asset relationships - solid green lines indicate positive correlation (moving together), dashed red lines indicate negative correlation (diverging moves), line thickness reflects correlation strength magnitude.

Asset Dots : Multi-layer glow effects with color-coded markers identify each asset on both quadrant map and correlation web-symbol labels positioned adjacent to current location.

Regime Summary Bar : Vertical boxes on right edge display condensed regime state for each enabled asset - box background color reflects quadrant classification, border color matches asset identifier.

Risk Regime Candles : Overlay candles on price chart colored by composite risk score - green indicates risk-on dominance (bullish equities/crypto exceeding bullish safe-havens), red indicates risk-off dominance (bullish gold/dollar/VIX exceeding bullish risk assets), gray indicates neutral balance.

Quadrant positioning, trail trajectory, correlation network topology, and velocity vectors outweigh isolated single-asset readings.

Signal Logic & Visual Cues

Cross-Market Regime Scanner presents spatial positioning insights rather than discrete entry signals:

Regime Clustering : Multiple assets congregating in same quadrant suggests broad market regime consensus - all assets in TREND ▲ indicates coordinated bullish momentum across instruments.

Regime Divergence : Assets splitting across opposing quadrants reveals intermarket disagreement - equities in TREND ▲ while safe-havens in TREND ▼ suggests healthy risk-on environment.

Quadrant Transitions : Assets crossing quadrant boundaries mark regime shifts - movement from left (ranging) to right (trending) indicates breakout from consolidation into directional phase.

Trail Curvature Patterns : Sharp curves in position trails signal rapid regime rotation, straight trails indicate sustained directional conviction, loops indicate regime uncertainty with back-and-forth oscillation.

Velocity Acceleration : Long arrows indicate rapid regime change momentum, short arrows indicate stable regime persistence, arrow direction reveals whether asset moving toward trending or ranging state.

Correlation Breakdown Events : Previously strong correlation lines (thick, opaque) suddenly thinning or disappearing indicates relationship decoupling - often precedes major regime transitions.

Correlation Inversion Signals : Assets shifting from positive correlation (solid green) to negative correlation (dashed red) marks structural market regime change - historically correlated assets beginning to diverge.

Risk Score Extremes : Composite score reaching maximum positive (all risk-on bullish, all risk-off bearish) or maximum negative (all risk-on bearish, all risk-off bullish) marks regime conviction extremes.

The primary value lies in simultaneous multi-asset regime awareness and correlation pattern recognition rather than isolated timing signals.

Strategy Integration

Cross-Market Regime Scanner fits within macro-aware and intermarket analysis approaches:

Regime-Filtered Entries : Use quadrant positioning as directional filter for primary trading instrument - favor long setups when asset in TREND ▲ quadrant, short setups in TREND ▼ quadrant.

Correlation Confluence Trading : Enter positions when target asset and correlated instruments occupy same quadrant - multiple assets in TREND ▲ provides conviction for long exposure.

Divergence-Based Reversal Anticipation : Monitor for regime divergence between correlated assets - if historically aligned instruments split to opposite quadrants, anticipate mean-reversion or regime rotation.

Breakout Confirmation via Cross-Asset Validation : Confirm primary instrument breakouts by verifying correlated assets simultaneously transitioning from ranging to trending quadrants.

Risk-On/Risk-Off Positioning : Use composite risk score and safe-haven positioning to determine overall market environment - scale risk exposure based on risk regime dominance.

Velocity-Based Timing : Enter during periods of high regime velocity (long arrows) when momentum carries assets decisively into new quadrants, avoid entries during low velocity regime uncertainty.

Multi-Timeframe Regime Alignment : Apply higher-timeframe regime scanner to establish macro context, use lower-timeframe price action for entry timing within aligned regime structure.

Correlation Web Pattern Recognition : Identify regime transitions early by monitoring correlation network topology changes - previously disconnected assets forming strong correlations suggests regime coalescence.

Technical Implementation Details

Core Engine : Wilder's smoothing-based ADX calculation with separate True Range and directional movement tracking per asset

Coordinate Model : Threshold-relative X-axis scaling (trending versus ranging) with directional movement differential Y-axis (bullish versus bearish)

Normalization System : Boundary capping at ±50 for consistent spatial positioning regardless of instrument volatility

Trail Rendering : Rolling array-based position history with gradient alpha decay and width tapering

Correlation Engine : Return-based pairwise correlation calculation over rolling window with configurable lookback

Network Visualization : Circular topology with trigonometric positioning, weighted line rendering based on correlation magnitude

Risk Scoring : Composite calculation aggregating directional states across classified risk-on and risk-off asset categories

Performance Profile : Optimized for 8 simultaneous security requests with efficient array management and conditional rendering

Optimal Application Parameters

Timeframe Guidance:

1 - 5 min : Micro-regime monitoring for intraday correlation shifts and short-term regime rotations

15 - 60 min : Intraday regime structure with meaningful ADX development and correlation stability

4H - Daily : Swing and position-level macro regime identification with sustained trend classification

Weekly - Monthly : Long-term regime cycle tracking with structural correlation pattern evolution

Suggested Baseline Configuration:

ADX Period : 14

ADX Smoothing : 14

Trend Threshold : 25.0

Trail Length : 15

Correlation Period : 50

Min |Correlation| to Show Line : 0.3

Web Radius : 30

Show Quadrant Colors : Enabled

Show Regime Summary Bar : Enabled

Show Velocity Arrows : Enabled

Show Correlation Web : Enabled

These suggested parameters should be used as a baseline; their effectiveness depends on the selected assets' volatility profiles, correlation characteristics, and preferred spatial sensitivity, so fine-tuning is expected for optimal performance.

Parameter Calibration Notes

Use the following adjustments to refine behavior without altering the core logic:

Assets clustering too tightly : Decrease Trend Threshold (e.g., 20) to spread ranging/trending separation, or increase ADX Period for smoother ADX calculation reducing noise.

Assets spreading too widely : Increase Trend Threshold (e.g., 30-35) to demand stronger ADX confirmation before classifying as trending, tightening quadrant boundaries.

Trail too short to show trajectory : Increase Trail Length (20-25) to visualize longer regime history, revealing sustained directional patterns.

Trail too cluttered : Decrease Trail Length (8-12) for cleaner visualization focusing on recent regime state, reducing visual complexity.

Unstable ADX readings : Increase ADX Period and ADX Smoothing (18-21) for heavier smoothing reducing bar-to-bar regime oscillation.

Sluggish regime detection : Decrease ADX Period (10-12) for faster response to directional changes, accepting increased sensitivity to noise.

Too many correlation lines : Increase Min |Correlation| threshold (0.4-0.6) to display only strongest relationships, decluttering network visualization.

Missing significant correlations : Decrease Min |Correlation| threshold (0.2-0.25) to reveal weaker but potentially meaningful relationships.

Correlation too volatile : Increase Correlation Period (75-100) for more stable correlation measurements, reducing network line flickering.

Correlation too stale : Decrease Correlation Period (30-40) to emphasize recent correlation patterns, capturing regime-dependent relationship changes.

Velocity arrows too sensitive : Modify 7-bar lookback in code to longer period (10-14) for smoother velocity representation, or increase magnitude threshold for arrow display.

Adjustments should be incremental and evaluated across multiple session types rather than isolated market conditions.

Performance Characteristics

High Effectiveness:

Macro-aware trading approaches requiring cross-market regime context for directional bias

Intermarket analysis strategies monitoring correlation breakdowns and regime divergences

Portfolio construction decisions requiring simultaneous multi-asset regime classification

Risk management frameworks using safe-haven positioning and risk-on/risk-off scoring

Trend-following systems benefiting from cross-asset regime confirmation before entry

Mean-reversion strategies identifying regime extremes via clustering patterns and correlation stress

Reduced Effectiveness:

Single-asset focused strategies not incorporating cross-market context in decision logic

High-frequency trading approaches where multi-security request latency impacts execution

Markets with consistently weak correlations where network topology provides limited insight

Extremely low volatility environments where ADX remains persistently below threshold for all assets

Instruments with erratic or unreliable ADX characteristics producing unstable coordinate positioning

Integration Guidelines

Confluence : Combine with BOSWaves structure, volume analysis, or primary instrument technical indicators for entry timing within aligned regime

Quadrant Respect : Trust signals occurring when primary trading asset occupies appropriate quadrant for intended trade direction

Correlation Context : Prioritize setups where target asset exhibits strong correlation with instruments in same regime quadrant

Divergence Awareness : Monitor for safe-haven assets moving opposite to risk assets - regime divergence validates directional conviction

Velocity Confirmation : Favor entries during periods of strong regime velocity indicating decisive momentum rather than regime oscillation

Risk Score Alignment : Scale position sizing and exposure based on composite risk score - larger positions during clear risk-on/risk-off environments

Trail Pattern Recognition : Use trail curvature to identify regime stability (straight) versus rotation (curved) versus uncertainty (looped)

Multi-Timeframe Structure : Apply higher-timeframe regime scanner for macro filter, lower-timeframe for tactical positioning within established regime

Disclaimer

Cross-Market Regime Scanner is a professional-grade multi-asset regime visualization and correlation analysis tool. It uses ADX-based coordinate positioning and rolling correlation calculation but does not predict future regime transitions or guarantee relationship persistence. Results depend on selected assets' characteristics, parameter configuration, correlation stability, and disciplined interpretation. Security request timing may introduce minor latency in real-time data retrieval. BOSWaves recommends deploying this indicator within a broader analytical framework that incorporates price structure, volume context, fundamental macro awareness, and comprehensive risk management.

Intermarket

BTC Fundamental Value Hypothesis [OmegaTools]BTC Fundamental Value Hypothesis is a macro-valuation and regime-detection model designed to contextualize Bitcoin’s price through relative market-cap comparisons against major capital reservoirs: Gold, Silver, the Altcoin market, and large-cap equities. Instead of relying on traditional on-chain metrics or purely technical signals, this tool frames BTC as an asset competing for global liquidity and “store-of-value mindshare”, then estimates an implied fair value based on how BTC historically coexists (or diverges) from these benchmark universes.

Core concept: relative market-cap anchoring

The indicator builds a reference-based fair price by translating external market capitalizations into implied BTC valuation using a dominance framework. In practice, you choose one or more reference universes (Gold, Silver, Altcoins, Stocks). For each selected universe, the script computes how large BTC “should be” relative to that universe (dominance ratio), and converts that into an implied BTC price. The final fair price is the average of the implied prices from the enabled universes.

Two dominance modes: automatic vs manual

1. Automatic Dominance % (default)

When enabled, the model estimates dominance ratios dynamically using a 252-period simple moving average of BTC market cap divided by each reference market cap. This produces an adaptive baseline that follows structural changes over time and reduces sensitivity to short-term spikes.

2. Manual Dominance %

If you prefer a discretionary macro thesis, you can directly input dominance parameters for each reference universe. This is useful when you want to stress-test scenarios (e.g., “BTC should converge toward X% of Gold’s market cap”) or align the model with a specific long-term adoption narrative.

Reference universes and data construction

- BTC market cap: pulled from CRYPTOCAP:BTC.

- Gold and Silver market caps: derived from the corresponding futures symbols (GC1!, SI1!) multiplied by an assumed total above-ground quantity (constant tonnage converted to troy ounces). This provides a practical and tradable proxy for spot valuation context.

- Altcoin market cap: pulled from CRYPTOCAP:TOTAL2 (total crypto market excluding BTC).

- Stocks market cap proxy (Σ3): a deliberately conservative equity benchmark built from three mega-cap stocks (AAPL, MSFT, AMZN) using total shares outstanding (request.financial) multiplied by price. This avoids index licensing complexity while still tracking a meaningful slice of global equity beta/liquidity.

Valuation output: overvalued vs undervalued (log-based)

The valuation readout is expressed as a percentage derived from the logarithmic distance between BTC price and the model’s fair price. This choice makes valuation comparable across long time horizons and reduces distortion during exponential growth phases. A positive valuation indicates BTC trading below the model’s implied value (undervalued), while a negative valuation indicates trading above it (overvalued).

Oscillator: relative momentum and regime confirmation

In addition to fair value, the indicator includes a momentum differential oscillator built from RSI(50):

- BTC RSI is compared to the average RSI of the selected reference universes.

- The oscillator highlights when BTC strength is leading or lagging the broader macro benchmarks.

- Color is rendered through a gradient to provide immediate regime readability (risk-on vs risk-off behavior, expansion vs contraction phases).

Visualization and UI components

- Fair Price overlay: the computed fair price is plotted directly on the BTC chart for immediate comparison with spot price action.

- Valuation shading: the area between price and fair price is filled to visually emphasize dislocation and potential mean-reversion zones.

- Oscillator panel: a zero-centered oscillator with filled bands helps you identify persistent trend regimes versus transitional conditions.

- Summary table: a right-side table displays the current valuation (over/under) and, when Automatic mode is enabled, the live dominance ratios used in the model (BTC/GOLD, BTC/SILVER, BTC/ALTC, BTC/STOCKS).

How to use it (practical workflows)

- Macro valuation context: use fair price as a structural anchor to assess whether BTC is trading at a premium or discount relative to external liquidity baselines.

- Regime filtering: combine valuation with the oscillator to distinguish “cheap but weak” from “cheap and strengthening” (and the inverse for tops).

- Mean-reversion mapping: large, persistent deviations from fair value often highlight speculative extremes or capitulation zones; this can support systematic entries/exits, position sizing, or hedging decisions.

- Scenario analysis: switch to Manual Dominance % to model adoption outcomes, policy-driven shifts, or multi-year re-rating assumptions.

Important notes and limitations (read before use)

- This is a hypothesis-driven macro model, not a literal intrinsic value calculation. Results depend on dominance assumptions, proxies, and data availability.

- Gold/Silver market caps are approximations based on futures pricing and fixed supply constants; real-world supply dynamics, above-ground estimates, and spot/futures basis can differ.

- The Stocks (Σ3) benchmark is a proxy and intentionally not “the whole market”. It is designed to represent a large-cap liquidity reference, not total equity capitalization.

- Always validate signals with additional context (market structure, volatility regime, risk management rules). This indicator is best used as a macro layer in a broader decision framework.

Designed for clarity, macro discipline, and repeatability

BTC Fundamental Value Hypothesis by OmegaTools is built for traders and investors who want a clean, data-driven way to interpret BTC through the lens of competing asset classes and capital flows. It is particularly effective on higher timeframes (Daily/Weekly) where macro relationships are more stable and valuation signals are less noisy.

© OmegaTools, Eros

Ultimate Major Contextual Dashboard (Multi-Asset)Overview : The Ultimate Major Dashboard is a performance-optimized market overview tool designed to provide a consolidated snapshot of the 7 major Forex pairs and Gold. It aggregates correlation, trend, momentum, and volatility data into a single, clean table, allowing users to view broader market context without switching charts.

Technical Logic & Components : This indicator utilizes a modular function to analyze EURUSD, GBPUSD, USDJPY, USDCHF, AUDUSD, USDCAD, NZDUSD, and XAUUSD across four key dimensions:

Intermarket Correlation (Pearson Coefficient): Uses ta.correlation() to compare each asset against the symbol currently on your main chart.

Logic: Values above 0.7 (Dark Green) suggest a strong positive relationship, while values below -0.7 (Dark Red) suggest inverse behavior. This is calculated over a rolling 50-period window to balance stability with current market sensitivity.

Trend Bias (EMA-200): Evaluates the long-term trend by checking price position relative to the 200-period Exponential Moving Average.

Visuals: An upward arrow (⬆) indicates price is above the EMA; a downward arrow (⬇) indicates it is below.

Momentum (RSI-14): Calculates the Relative Strength Index. The dashboard automatically highlights readings above 70 (OB) or below 30 (OS) to help identify potential momentum extremes.

Volatility (ATR-14): Displays the Average True Range as a reference for the current active range of each market, helping users compare volatility levels across the majors.

How to Interpret the Dashboard

Asset Alignment: Correlation values help identify when pairs are moving in "unison" versus when a specific currency is diverging from the group.

Directional Context: Combining the Trend (EMA) and Momentum (RSI) columns provides a quick view of whether a market is trending strongly or reaching an exhaustion point.

Volatility Benchmarking: The ATR values offer perspective on which pairs are currently the most active, assisting in market comparison based on volatility preference.

Data Handling & Customization

Multi-Symbol Sync: Data is fetched using request.security(). The calculations are synchronized with the chart's current bar state for real-time accuracy.

Dynamic TF: Users can select the analysis timeframe (60, 240, D, W) via the settings menu.

Flexibility: The dashboard position can be toggled between all four corners of the chart to avoid overlapping with price action.

Disclaimer

This tool is provided for analytical and educational purposes only. It does not generate trading signals and should not be considered financial advice.

TFPS_EngineLibrary "TFPS_Engine"

f_calculate_lead_lag(series1, series2, length, max_lag)

Parameters:

series1 (float)

series2 (float)

length (int)

max_lag (int)

f_calculate_pressure_score(spx_ticker, vix_ticker, dxy_ticker, us10y_ticker, benchmark_source, trend_lookback, score_smoothing, use_dynamic_weights, corr_lookback, w_spx, w_vix, w_dxy, w_us10y, zscore_lookback, max_lag)

Parameters:

spx_ticker (string)

vix_ticker (string)

dxy_ticker (string)

us10y_ticker (string)

benchmark_source (float)

trend_lookback (int)

score_smoothing (simple int)

use_dynamic_weights (bool)

corr_lookback (int)

w_spx (float)

w_vix (float)

w_dxy (float)

w_us10y (float)

zscore_lookback (int)

max_lag (int)

LeadLagOutput

Fields:

best_lag (series int)

max_corr (series float)

TFPS_Output

Fields:

historical_score (series float)

smoothed_score (series float)

z_score (series float)

regime_signal (series int)

lead_lag_bars (series int)

lead_lag_corr (series float)

weight_spx (series float)

weight_vix (series float)

weight_dxy (series float)

weight_us10y (series float)

Strength Comparison @joshuuuexample:

if you want to find the stronger/weaker pair between eurusd and gbpusd, what you can do is check the eurgbp charts. if eurgbp is bullish, that means, that longs longs on eurusd are better than on gbpusd.

Unfortunately, there is no such thing to compare for example usoil with ukoil, or us100 with us500.

That's where this indicator comes in handy. You can choose whatever two symbols you want, that are supported by tradingview and you will get a chart, which shows symbol1/symbol2.

Now you can use normal market structure, or the ema option, to find out the stronger symbol.

This can also help predicting the so called SMT Divergences, taught by ICT.

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

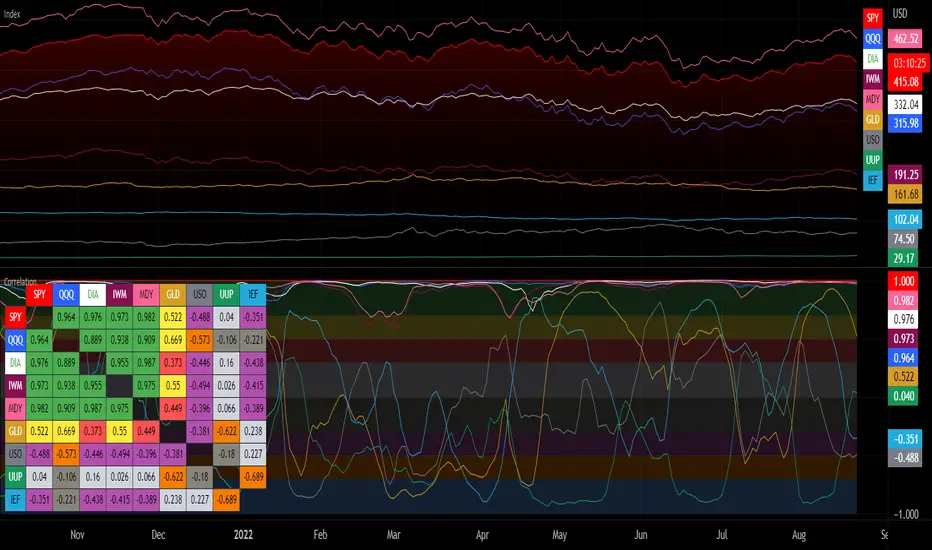

Correlation with Matrix TableCorrelation coefficient is a measure of the strength of the relationship between two values. It can be useful for market analysis, cryptocurrencies, forex and much more.

Since it "describes the degree to which two series tend to deviate from their moving average values" (1), first of all you have to set the length of these moving averages. You can also retrieve the values from another timeframe, and choose whether or not to ignore the gaps.

After selecting the reference ticker, which is not dependent from the chart you are on, you can choose up to eight other tickers to relate to it. The provided matrix table will then give you a deeper insight through all of the correlations between the chosen symbols.

Correlation values are scored on a scale from 1 to -1

A value of 1 means the correlation between the values is perfect.

A value of 0 means that there is no correlation at all.

A value of -1 indicates that the correlation is perfectly opposite.

For a better view at a glance, eight level colors are available and it is possible to modify them at will. You can even change level ranges by setting their threshold values. The background color of the matrix's cells will change accordingly to all of these choices.

The default threshold values, commonly used in statistics, are as follows:

None to weak correlation: 0 - 0.3

Weak to moderate correlation: 0.3 - 0.5

Moderate to high correlation: 0.5 - 0.7

High to perfect correlation: 0.7 - 1

Remember to be careful about spurious correlations, which are strong correlations without a real causal relationship.

(1) www.tradingview.com

USDJPY Assumption v1Based on the "logical trading" post of Charles Cornley (thanks!).

Indicator States:

Very Bullish (Lime) = USD trend rising and JPY trend falling and Gold trend falling and US 10Y Bond trend falling and

Dow Jones trend rising and Nasdaq trend rising and Russell 2000 trend rising and

S&P 500 trend rising and Nikkei 225 trend rising

Bullish (Green) = USD trend rising and JPY trend falling

Bearish (Red) = USD trend falling and JPY trend rising