Vector2Library "Vector2"

Representation of two dimensional vectors or points.

This structure is used to represent positions in two dimensional space or vectors,

for example in spacial coordinates in 2D space.

~~~

references:

docs.unity3d.com

gist.github.com

github.com

gist.github.com

gist.github.com

gist.github.com

~~~

new(x, y)

Create a new Vector2 object.

Parameters:

x : float . The x value of the vector, default=0.

y : float . The y value of the vector, default=0.

Returns: Vector2. Vector2 object.

-> usage:

`unitx = Vector2.new(1.0) , plot(unitx.x)`

from(value)

Assigns value to a new vector `x,y` elements.

Parameters:

value : float, x and y value of the vector.

Returns: Vector2. Vector2 object.

-> usage:

`one = Vector2.from(1.0), plot(one.x)`

from(value, element_sep, open_par, close_par)

Assigns value to a new vector `x,y` elements.

Parameters:

value : string . The `x` and `y` value of the vector in a `x,y` or `(x,y)` format, spaces and parentesis will be removed automatically.

element_sep : string . Element separator character, default=`,`.

open_par : string . Open parentesis character, default=`(`.

close_par : string . Close parentesis character, default=`)`.

Returns: Vector2. Vector2 object.

-> usage:

`one = Vector2.from("1.0,2"), plot(one.x)`

copy(this)

Creates a deep copy of a vector.

Parameters:

this : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = Vector2.new(1.0) , b = a.copy() , plot(b.x)`

down()

Vector in the form `(0, -1)`.

Returns: Vector2. Vector2 object.

left()

Vector in the form `(-1, 0)`.

Returns: Vector2. Vector2 object.

right()

Vector in the form `(1, 0)`.

Returns: Vector2. Vector2 object.

up()

Vector in the form `(0, 1)`.

Returns: Vector2. Vector2 object.

one()

Vector in the form `(1, 1)`.

Returns: Vector2. Vector2 object.

zero()

Vector in the form `(0, 0)`.

Returns: Vector2. Vector2 object.

minus_one()

Vector in the form `(-1, -1)`.

Returns: Vector2. Vector2 object.

unit_x()

Vector in the form `(1, 0)`.

Returns: Vector2. Vector2 object.

unit_y()

Vector in the form `(0, 1)`.

Returns: Vector2. Vector2 object.

nan()

Vector in the form `(float(na), float(na))`.

Returns: Vector2. Vector2 object.

xy(this)

Return the values of `x` and `y` as a tuple.

Parameters:

this : Vector2 . Vector2 object.

Returns: .

-> usage:

`a = Vector2.new(1.0, 1.0) , = a.xy() , plot(ax)`

length_squared(this)

Length of vector `a` in the form. `a.x^2 + a.y^2`, for comparing vectors this is computationaly lighter.

Parameters:

this : Vector2 . Vector2 object.

Returns: float. Squared length of vector.

-> usage:

`a = Vector2.new(1.0, 1.0) , plot(a.length_squared())`

length(this)

Magnitude of vector `a` in the form. `sqrt(a.x^2 + a.y^2)`

Parameters:

this : Vector2 . Vector2 object.

Returns: float. Length of vector.

-> usage:

`a = Vector2.new(1.0, 1.0) , plot(a.length())`

normalize(a)

Vector normalized with a magnitude of 1, in the form. `a / length(a)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = normalize(Vector2.new(3.0, 2.0)) , plot(a.y)`

isNA(this)

Checks if any of the components is `na`.

Parameters:

this : Vector2 . Vector2 object.

Returns: bool.

usage:

p = Vector2.new(1.0, na) , plot(isNA(p)?1:0)

add(a, b)

Adds vector `b` to `a`, in the form `(a.x + b.x, a.y + b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = add(a, b) , plot(c.x)`

add(a, b)

Adds vector `b` to `a`, in the form `(a.x + b, a.y + b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = add(a, b) , plot(c.x)`

add(a, b)

Adds vector `b` to `a`, in the form `(a + b.x, a + b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = add(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a.x - b.x, a.y - b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = subtract(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a.x - b, a.y - b)`.

Parameters:

a : Vector2 . vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = subtract(a, b) , plot(c.x)`

subtract(a, b)

Subtract vector `b` from `a`, in the form `(a - b.x, a - b.y)`.

Parameters:

a : float . value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = subtract(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a.x * b.x, a.y * b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = one() , c = multiply(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a.x * b, a.y * b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = one() , b = 1.0 , c = multiply(a, b) , plot(c.x)`

multiply(a, b)

Multiply vector `a` with `b`, in the form `(a * b.x, a * b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 1.0 , b = one() , c = multiply(a, b) , plot(c.x)`

divide(a, b)

Divide vector `a` with `b`, in the form `(a.x / b.x, a.y / b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = from(2.0) , c = divide(a, b) , plot(c.x)`

divide(a, b)

Divide vector `a` with value `b`, in the form `(a.x / b, a.y / b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = 2.0 , c = divide(a, b) , plot(c.x)`

divide(a, b)

Divide value `a` with vector `b`, in the form `(a / b.x, a / b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 3.0 , b = from(2.0) , c = divide(a, b) , plot(c.x)`

negate(a)

Negative of vector `a`, in the form `(-a.x, -a.y)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = a.negate , plot(b.x)`

pow(a, b)

Raise vector `a` with exponent vector `b`, in the form `(a.x ^ b.x, a.y ^ b.y)`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = from(2.0) , c = pow(a, b) , plot(c.x)`

pow(a, b)

Raise vector `a` with value `b`, in the form `(a.x ^ b, a.y ^ b)`.

Parameters:

a : Vector2 . Vector2 object.

b : float . Value.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = 2.0 , c = pow(a, b) , plot(c.x)`

pow(a, b)

Raise value `a` with vector `b`, in the form `(a ^ b.x, a ^ b.y)`.

Parameters:

a : float . Value.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = 3.0 , b = from(2.0) , c = pow(a, b) , plot(c.x)`

sqrt(a)

Square root of the elements in a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(3.0) , b = sqrt(a) , plot(b.x)`

abs(a)

Absolute properties of the vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(-3.0) , b = abs(a) , plot(b.x)`

min(a)

Lowest element of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = min(a) , plot(b)`

max(a)

Highest element of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = max(a) , plot(b)`

vmax(a, b)

Highest elements of two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = vmax(a, b) , plot(c.x)`

vmax(a, b, c)

Highest elements of three vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = new(1.5, 4.5) , d = vmax(a, b, c) , plot(d.x)`

vmin(a, b)

Lowest elements of two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = vmin(a, b) , plot(c.x)`

vmin(a, b, c)

Lowest elements of three vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 2.0) , b = new(2.0, 3.0) , c = new(1.5, 4.5) , d = vmin(a, b, c) , plot(d.x)`

perp(a)

Perpendicular Vector of `a`, in the form `(a.y, -a.x)`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = perp(a) , plot(b.x)`

floor(a)

Compute the floor of vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = floor(a) , plot(b.x)`

ceil(a)

Ceils vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = ceil(a) , plot(b.x)`

ceil(a, digits)

Ceils vector `a`.

Parameters:

a : Vector2 . Vector2 object.

digits : int . Digits to use as ceiling.

Returns: Vector2. Vector2 object.

round(a)

Round of vector elements.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = round(a) , plot(b.x)`

round(a, precision)

Round of vector elements.

Parameters:

a : Vector2 . Vector2 object.

precision : int . Number of digits to round vector "a" elements.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(0.123456, 1.234567) , b = round(a, 2) , plot(b.x)`

fractional(a)

Compute the fractional part of the elements from vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.123456, 1.23456) , b = fractional(a) , plot(b.x)`

dot_product(a, b)

dot_product product of 2 vectors, in the form `a.x * b.x + a.y * b.y.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = dot_product(a, b) , plot(c)`

cross_product(a, b)

cross product of 2 vectors, in the form `a.x * b.y - a.y * b.x`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = cross_product(a, b) , plot(c)`

equals(a, b)

Compares two vectors

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: bool. Representing the equality.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = equals(a, b) ? 1 : 0 , plot(c)`

sin(a)

Compute the sine of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = sin(a) , plot(b.x)`

cos(a)

Compute the cosine of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = cos(a) , plot(b.x)`

tan(a)

Compute the tangent of argument vector `a`.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = tan(a) , plot(b.x)`

atan2(x, y)

Approximation to atan2 calculation, arc tangent of `y/x` in the range (-pi,pi) radians.

Parameters:

x : float . The x value of the vector.

y : float . The y value of the vector.

Returns: float. Value with angle in radians. (negative if quadrante 3 or 4)

-> usage:

`a = new(3.0, 1.5) , b = atan2(a.x, a.y) , plot(b)`

atan2(a)

Approximation to atan2 calculation, arc tangent of `y/x` in the range (-pi,pi) radians.

Parameters:

a : Vector2 . Vector2 object.

Returns: float, value with angle in radians. (negative if quadrante 3 or 4)

-> usage:

`a = new(3.0, 1.5) , b = atan2(a) , plot(b)`

distance(a, b)

Distance between vector `a` and `b`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = distance(a, b) , plot(c)`

rescale(a, length)

Rescale a vector to a new magnitude.

Parameters:

a : Vector2 . Vector2 object.

length : float . Magnitude.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 2.0 , c = rescale(a, b) , plot(c.x)`

rotate(a, radians)

Rotates vector by a angle.

Parameters:

a : Vector2 . Vector2 object.

radians : float . Angle value in radians.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 2.0 , c = rotate(a, b) , plot(c.x)`

rotate_degree(a, degree)

Rotates vector by a angle.

Parameters:

a : Vector2 . Vector2 object.

degree : float . Angle value in degrees.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = 45.0 , c = rotate_degree(a, b) , plot(c.x)`

rotate_around(this, center, angle)

Rotates vector `target` around `origin` by angle value.

Parameters:

this

center : Vector2 . Vector2 object.

angle : float . Angle value in degrees.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = rotate_around(a, b, 45.0) , plot(c.x)`

perpendicular_distance(a, b, c)

Distance from point `a` to line between `b` and `c`.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(1.5, 2.6) , b = from(1.0) , c = from(3.0) , d = perpendicular_distance(a, b, c) , plot(d.x)`

project(a, axis)

Project a vector onto another.

Parameters:

a : Vector2 . Vector2 object.

axis : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = project(a, b) , plot(c.x)`

projectN(a, axis)

Project a vector onto a vector of unit length.

Parameters:

a : Vector2 . Vector2 object.

axis : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = projectN(a, b) , plot(c.x)`

reflect(a, axis)

Reflect a vector on another.

Parameters:

a : Vector2 . Vector2 object.

axis

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = reflect(a, b) , plot(c.x)`

reflectN(a, axis)

Reflect a vector to a arbitrary axis.

Parameters:

a : Vector2 . Vector2 object.

axis

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = reflectN(a, b) , plot(c.x)`

angle(a)

Angle in radians of a vector.

Parameters:

a : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = angle(a) , plot(b)`

angle_unsigned(a, b)

unsigned degree angle between 0 and +180 by given two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_unsigned(a, b) , plot(c)`

angle_signed(a, b)

Signed degree angle between -180 and +180 by given two vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_signed(a, b) , plot(c)`

angle_360(a, b)

Degree angle between 0 and 360 by given two vectors

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = angle_360(a, b) , plot(c)`

clamp(a, min, max)

Restricts a vector between a min and max value.

Parameters:

a : Vector2 . Vector2 object.

min

max

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = from(2.5) , d = clamp(a, b, c) , plot(d.x)`

clamp(a, min, max)

Restricts a vector between a min and max value.

Parameters:

a : Vector2 . Vector2 object.

min : float . Lower boundary value.

max : float . Higher boundary value.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = clamp(a, 2.0, 2.5) , plot(b.x)`

lerp(a, b, rate)

Linearly interpolates between vectors a and b by rate.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

rate : float . Value between (a:-infinity -> b:1.0), negative values will move away from b.

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = lerp(a, b, 0.5) , plot(c.x)`

herp(a, b, rate)

Hermite curve interpolation between vectors a and b by rate.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

rate : Vector2 . Vector2 object. Value between (a:0 > 1:b).

Returns: Vector2. Vector2 object.

-> usage:

`a = new(3.0, 1.5) , b = from(2.0) , c = from(2.5) , d = herp(a, b, c) , plot(d.x)`

transform(position, mat)

Transform a vector by the given matrix.

Parameters:

position : Vector2 . Source vector.

mat : M32 . Transformation matrix

Returns: Vector2. Transformed vector.

transform(position, mat)

Transform a vector by the given matrix.

Parameters:

position : Vector2 . Source vector.

mat : M44 . Transformation matrix

Returns: Vector2. Transformed vector.

transform(position, mat)

Transform a vector by the given matrix.

Parameters:

position : Vector2 . Source vector.

mat : matrix . Transformation matrix, requires a 3x2 or a 4x4 matrix.

Returns: Vector2. Transformed vector.

transform(this, rotation)

Transform a vector by the given quaternion rotation value.

Parameters:

this : Vector2 . Source vector.

rotation : Quaternion . Rotation to apply.

Returns: Vector2. Transformed vector.

area_triangle(a, b, c)

Find the area in a triangle of vectors.

Parameters:

a : Vector2 . Vector2 object.

b : Vector2 . Vector2 object.

c : Vector2 . Vector2 object.

Returns: float.

-> usage:

`a = new(1.0, 2.0) , b = from(2.0) , c = from(1.0) , d = area_triangle(a, b, c) , plot(d.x)`

random(max)

2D random value.

Parameters:

max : Vector2 . Vector2 object. Vector upper boundary.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(2.0) , b = random(a) , plot(b.x)`

random(max)

2D random value.

Parameters:

max : float, Vector upper boundary.

Returns: Vector2. Vector2 object.

-> usage:

`a = random(2.0) , plot(a.x)`

random(min, max)

2D random value.

Parameters:

min : Vector2 . Vector2 object. Vector lower boundary.

max : Vector2 . Vector2 object. Vector upper boundary.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(1.0) , b = from(2.0) , c = random(a, b) , plot(c.x)`

random(min, max)

2D random value.

Parameters:

min : Vector2 . Vector2 object. Vector lower boundary.

max : Vector2 . Vector2 object. Vector upper boundary.

Returns: Vector2. Vector2 object.

-> usage:

`a = random(1.0, 2.0) , plot(a.x)`

noise(a)

2D Noise based on Morgan McGuire @morgan3d.

Parameters:

a : Vector2 . Vector2 object.

Returns: Vector2. Vector2 object.

-> usage:

`a = from(2.0) , b = noise(a) , plot(b.x)`

to_string(a)

Converts vector `a` to a string format, in the form `"(x, y)"`.

Parameters:

a : Vector2 . Vector2 object.

Returns: string. In `"(x, y)"` format.

-> usage:

`a = from(2.0) , l = barstate.islast ? label.new(bar_index, 0.0, to_string(a)) : label(na)`

to_string(a, format)

Converts vector `a` to a string format, in the form `"(x, y)"`.

Parameters:

a : Vector2 . Vector2 object.

format : string . Format to apply transformation.

Returns: string. In `"(x, y)"` format.

-> usage:

`a = from(2.123456) , l = barstate.islast ? label.new(bar_index, 0.0, to_string(a, "#.##")) : label(na)`

to_array(a)

Converts vector to a array format.

Parameters:

a : Vector2 . Vector2 object.

Returns: array.

-> usage:

`a = from(2.0) , b = to_array(a) , plot(array.get(b, 0))`

to_barycentric(this, a, b, c)

Captures the barycentric coordinate of a cartesian position in the triangle plane.

Parameters:

this : Vector2 . Source cartesian coordinate position.

a : Vector2 . Triangle corner `a` vertice.

b : Vector2 . Triangle corner `b` vertice.

c : Vector2 . Triangle corner `c` vertice.

Returns: bool.

from_barycentric(this, a, b, c)

Captures the cartesian coordinate of a barycentric position in the triangle plane.

Parameters:

this : Vector2 . Source barycentric coordinate position.

a : Vector2 . Triangle corner `a` vertice.

b : Vector2 . Triangle corner `b` vertice.

c : Vector2 . Triangle corner `c` vertice.

Returns: bool.

to_complex(this)

Translate a Vector2 structure to complex.

Parameters:

this : Vector2 . Source vector.

Returns: Complex.

to_polar(this)

Translate a Vector2 cartesian coordinate into polar coordinates.

Parameters:

this : Vector2 . Source vector.

Returns: Pole. The returned angle is in radians.

Library

Replica of TradingView's Backtesting Engine with ArraysHello everyone,

Here is a perfectly replicated TradingView backtesting engine condensed into a single library function calculated with arrays. It includes TradingView's calculations for Net profit, Total Trades, Percent of Trades Profitable, Profit Factor, Max Drawdown (absolute and percent), and Average Trade (absolute and percent). Here's how TradingView defines each aspect of its backtesting system:

Net Profit: The overall profit or loss achieved.

Total Trades: The total number of closed trades, winning and losing.

Percent Profitable: The percentage of winning trades, the number of winning trades divided by the total number of closed trades.

Profit Factor: The amount of money the strategy made for every unit of money it lost, gross profits divided by gross losses.

Max Drawdown: The greatest loss drawdown, i.e., the greatest possible loss the strategy had compared to its highest profits.

Average Trade: The sum of money gained or lost by the average trade, Net Profit divided by the overall number of closed trades.

Here's how each variable is defined in the library function:

_backtest(bool _enter, bool _exit, float _startQty, float _tradeQty)

bool _enter: When the strategy should enter a trade (entry condition)

bool _exit: When the strategy should exit a trade (exit condition)

float _startQty: The starting capital in the account (for BTCUSD, it is the amount of USD the account starts with)

float _tradeQty: The amount of capital traded (if set to 1000 on BTCUSD, it will trade 1000 USD on each trade)

Currently, this library only works with long strategies, and I've included a commented out section under DEMO STRATEGY where you can replicate my results with TradingView's backtesting engine. There's tons I could do with this beyond what is shown, but this was a project I worked on back in June of 2022 before getting burned out. Feel free to comment with any suggestions or bugs, and I'll try to add or fix them all soon. Here's my list of thing to add to the library currently (may not all be added):

Add commission calculations.

Add support for shorting

Add a graph that resembles TradingView's overview graph.

Clean and optimize code.

Clean up in a way that makes it easy to add other TradingView calculations (such as Sharpe and Sortino ratio).

Separate all variables, so they become accessible outside of calculations (such as gross profit, gross loss, number of winning trades, number of losing trades, etc.).

Thanks for reading,

OztheWoz

HendrixLIBRARY - utilsLibrary "HendrixLIBRARY"

getVolumeData()

getLTF(customTimeframe, ltf)

Parameters:

customTimeframe

ltf

sumArray(a)

Parameters:

a

arrs2vals(upVolumeArray, downVolumeArray, volArr)

Parameters:

upVolumeArray

downVolumeArray

volArr

getVolumesFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getDeltaFromVolumes(upVolume, downVolume)

Parameters:

upVolume

downVolume

getDeltaFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getUpColor()

getDownColor()

getBlackColor()

getColors()

printTableTR(txt)

Parameters:

txt

printTableBR(txt)

Parameters:

txt

printTableMR(txt)

Parameters:

txt

print(txt, lbl)

Parameters:

txt

lbl

printSyminfo(sym)

Parameters:

sym

ReduceSecurityCallsLibrary "ReduceSecurityCalls"

This library allows you to reduce the number of request.security calls to 1 per symbol per timeframe. Script provides example how to use it with request.security and possible optimisation applied to htf data call.

This data can be used to calculate everything you need and more than that (for example you can calculate 4 emas with one function call on mat_out).

ParseSource(mat_outs, o)

Should be used inside request.security call. Optimise your calls using timeframe.change when htf data parsing! Supports up to 5 expressions (results of expressions must be float or int)

Parameters:

mat_outs : Matrix to be used as outputs, first value is newest

o : Please use parametres in the order they specified (o should be 1st, h should be 2nd etc..)

Returns: outs array, due to weird limitations do not try this :matrix_out = matrix.copy(ParseSource)

SetSessionTimesIndiaLibrary "SetSessionTimesIndia"

This library might be useful to code an indicator or strategy that requires to call Indian trading sessions at NSE and MCX.

SetSessionTimes()

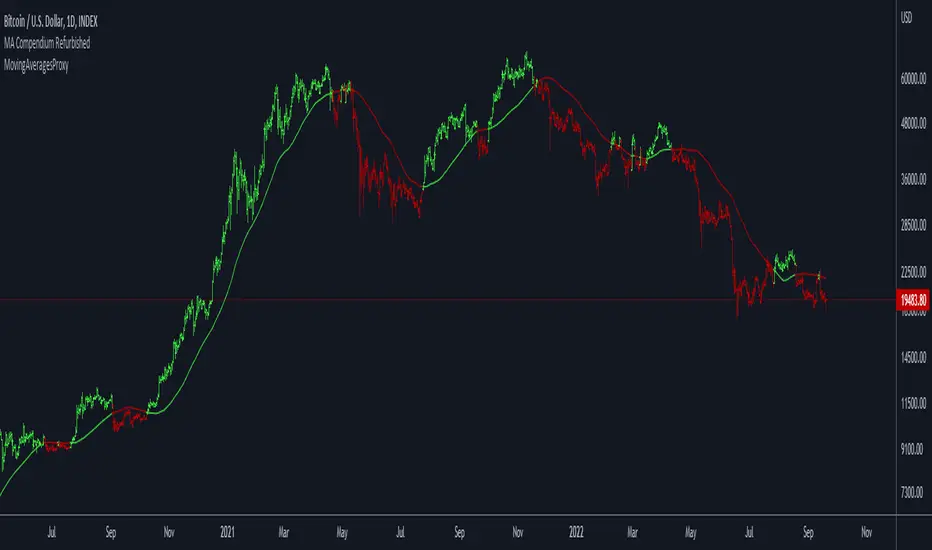

Moving Averages ProxyLibrary "MovingAveragesProxy"

Moving Averages Proxy - Library of all moving averages spread out in different libraries

rvwap(_src, fixedTfInput, minsInput, hoursInput, daysInput, minBarsInput)

Calculates the Rolling VWAP (customized VWAP developed by the team of TradingView)

Parameters:

_src : (float) Source. Default: close

fixedTfInput : (bool) Use a fixed time period. Default: false

minsInput : (int) Minutes. Default: 0

hoursInput : (int) Hours. Default: 0

daysInput : (int) Days. Default: 1

minBarsInput : (int) Bars. Default: 10

Returns: (float) Rolling VWAP

correlationMa(src, len, factor)

Correlation Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

factor : (float) Factor. Default: 1.7

Returns: (float) Correlation Moving Average

regma(src, len, lambda)

Regularized Exponential Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

lambda : (float) Lambda. Default: 0.5

Returns: (float) Regularized Exponential Moving Average

repma(src, len)

Repulsion Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

Returns: (float) Repulsion Moving Average

epma(src, length, offset)

End Point Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

offset : (float) Offset. Default: 4

Returns: (float) End Point Moving Average

lc_lsma(src, length)

1LC-LSMA (1 line code lsma with 3 functions)

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) 1LC-LSMA Moving Average

aarma(src, length)

Adaptive Autonomous Recursive Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Adaptive Autonomous Recursive Moving Average

alsma(src, length)

Adaptive Least Squares

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Adaptive Least Squares

ahma(src, length)

Ahrens Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Ahrens Moving Average

adema(src)

Ahrens Moving Average

Parameters:

src : (float) Source. Default: close

Returns: (float) Moving Average

autol(src, lenDev)

Auto-Line

Parameters:

src : (float) Source. Default: close

lenDev : (int) Length for standard deviation

Returns: (float) Auto-Line

fibowma(src, length)

Fibonacci Weighted Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

fisherlsma(src, length)

Fisher Least Squares Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

leoma(src, length)

Leo Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

linwma(src, period, weight)

Linear Weighted Moving Average

Parameters:

src : (float) Source. Default: close

period : (int) Length

weight : (int) Weight

Returns: (float) Moving Average

mcma(src, length)

McNicholl Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

srwma(src, length)

Square Root Weighted Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

EDSMA(src, len)

Ehlers Dynamic Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: EDSMA smoothing.

dema(x, t)

Double Exponential Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: DEMA smoothing.

tema(src, len)

Triple Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TEMA smoothing.

smma(src, len)

Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: SMMA smoothing.

hullma(src, len)

Hull Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Hull smoothing.

frama(x, t)

Fractal Reactive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: FRAMA smoothing.

kama(x, t)

Kaufman's Adaptive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: KAMA smoothing.

vama(src, len)

Volatility Adjusted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: VAMA smoothing.

donchian(len)

Donchian Calculation.

Parameters:

len : Lookback length to use.

Returns: Average of the highest price and the lowest price for the specified look-back period.

Jurik(src, len)

Jurik Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: JMA smoothing.

xema(src, len)

Optimized Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: XEMA smoothing.

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

getMovingAverage(type, src, len, lsmaOffset, inputAlmaOffset, inputAlmaSigma, FC, SC, a1_t3, fixedTfInput, daysInput, hoursInput, minsInput, minBarsInput, lambda, volumeWeighted, gamma_aarma, smooth, linweight, volatility_lookback, jurik_phase, jurik_power)

Abstract proxy function that invokes the calculation of a moving average according to type

Parameters:

type : (string) Type of moving average

src : (float) Source of series (close, high, low, etc.)

len : (int) Period of loopback to calculate the average

lsmaOffset : (int) Offset for Least Squares MA

inputAlmaOffset : (float) Offset for ALMA

inputAlmaSigma : (float) Sigma for ALMA

FC : (int) Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : (int) Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

a1_t3 : (float) Tillson T3 Volume Factor

fixedTfInput : (bool) Use a fixed time period in Rolling VWAP

daysInput : (int) Days in Rolling VWAP

hoursInput : (int) Hours in Rolling VWAP

minsInput : (int) Minutrs in Rolling VWAP

minBarsInput : (int) Bars in Rolling VWAP

lambda : (float) Regularization Constant in Regularized EMA

volumeWeighted : (bool) Apply volume weighted calculation in selected moving average

gamma_aarma : (float) Gamma for Adaptive Autonomous Recursive Moving Average

smooth : (float) Smooth for Adaptive Least Squares

linweight : (float) Weight for Volume Weighted Moving Average

volatility_lookback : (int) Loopback for Volatility Adjusted Moving Average

jurik_phase : (int) Phase for Jurik Moving Average

jurik_power : (int) Power for Jurik Moving Average

Returns: (float) Moving average

L_BetaLibrary "L_Beta"

TODO: add library description here

length()

beta()

simple_beta()

index_selector()

Color Library: Rainbow Index & Simplest Return ColorLibrary "Color Library!"

To help with large projects that need colors!

If you guys make the library bigger, share it so we can all have tons of colors!

2 Functions

Uppercase and Lowercase, because why not?

import library as color

1.) color.this("Brown") // or color.this("brown") both work

2.) color.rainbow(1) //Returns first index of Rainbow

this(x)

TODO: color.this(Brown)

Parameters:

x : TODO: String Color Name

Returns: TODO: Color

rainbow(x)

TODO: Return Rainbow Index

Parameters:

x : TODO: Number is index of Rainbow :)

Returns: TODO: Color

Binance_Min_Limit_Order_amount_libraryLibrary "Binance_Min_Limit_Order_amount_library"

TODO: This library give us the minimum Limit Order amount for the contract in Binance.

m_qty(n_v, m_fee, t_fee, cost, m_t)

TODO: it give us the Minimum Qty for the trading in Binance

Parameters:

n_v : TODO: min_notional_value. 5 dollar is the minimum notional amount in Binance at the moment.

m_fee : TODO: maker_fee %

t_fee : TODO: taker_fee %

cost : TODO: your investing money

m_t : TODO: if you want Limit_Order, put the "T", if you want Market_Order, put the "M" defval="M"

Returns: TODO: for the coin of binance on your chart,

Reference: www.binance.com

MiteTricksLibrary "MiteTricks"

Matrix Global Registry.

Get, Set, automatic growing, universal get/set,

multi-matrix dictionaries, multi-dictionary matrixes..

add slice matrixes of any type, share one common global key registry

pull up an item from a category, and item name ie a table of info.

same cell needs a color, a size, a string, a value, etc..

all of which can be pulled up with the same group id, and key id.

just swap which matrix you pull the value from.

this has a side benefit of non-repainting and recalculating

when pulling values, changing inputs..

makes for very fast/clean usage..

benefit :

floats = value

strings = names

lines = drawn items

table =table of data items for this key

colors = color for line/table/fill,label..

all of those can be pulled with "get(_VALUES,_groupIDX,_keyIDX)" where only the values matrix needs be swapped, and the same item/coordinates remains for all the possible matrixes that item appears in.

also useful as a dictionary/registry for any given type of item,,

and goes very handy with floats/strings/colors/bools with my matrixautotable

very helpful when prototyping or doing development work as a shortcut.

initRegistry()

Registry inititalizer

Returns: registry of string matrix type

newbool(optional, optional, optional)

create bool type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is bool (na)

Returns: bool matrix of specified size and fill, or blank 2x2 for registry use

newbox(optional, optional, optional)

create box type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is box (na)

Returns: box matrix of specified size and fill, or blank 2x2 for registry use

newcolor(optional, optional, optional)

create color type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is color (na)

Returns: color matrix of specified size and fill, or blank 2x2 for registry use

newfloat(optional, optional, optional)

create float type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is float (na)

Returns: float matrix of specified size and fill, or blank 2x2 for registry use

newint(optional, optional, optional)

create int type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is int (na)

Returns: int matrix of specified size and fill, or blank 2x2 for registry use

newlabel(optional, optional, optional)

create label type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is label (na)

Returns: label matrix of specified size and fill, or blank 2x2 for registry use

newline(optional, optional, optional)

create line type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is line (na)

Returns: line matrix of specified size and fill, or blank 2x2 for registry use

newlinefill(optional, optional, optional)

create linefill type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is linefill(na)

Returns: linefill matrix of specified size and fill, or blank 2x2 for registry use

newstring(optional, optional, optional)

create string type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is string (na)

Returns: string matrix of specified size and fill, or blank 2x2 for registry use

newtable(optional, optional, optional)

create table type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is table (na)

Returns: table matrix of specified size and fill, or blank 2x2 for registry use

newfrom(INIT_FILL)

newfrom Matrix full of item input

Parameters:

INIT_FILL: item to fill (2x2) the matri and set type. a type(na) works

addrow(m, v)

addrow Add new row to matrix

Parameters:

m: matrix of type being added to

v: value of type being added to ( best leave NA on string for registry purposes)

addcolumn(matrix, value)

addcolumn

Parameters:

matrix: of type being added to

value: of type being added to ( best leave NA on string for registry purposes)

get(_VALS, _KEYREG, _GROUP, _KEY)

get Grabs value and returns single item

Parameters:

_VALS: Matrix Values slice

_KEYREG: Registry values matrix (strings)

_GROUP: name of group/category or int group key

_KEY: name of item to fetch from value registry or int key id

Returns: item

get(_VALS, _GROUP, _KEY)

get Grabs value and returns single item

Parameters:

_VALS: Matrix Values slice

_GROUP: name of group/category

_KEY: name of item to fetch from value registry

getgid(_KEYREG, _GROUP)

getgid

Parameters:

_KEYREG: Reg to pull group id from

_GROUP: group index int, or string name to get the other missing type

getkid(_KEYREG, _GROUP, _KEY)

getkid

Parameters:

_KEYREG: Reg to pull Key id from

_GROUP: group index int, or string name

_KEY: index of string key id to get it's ID int

getkey(_KEYREG, _GROUP, _KEY)

getkey

Parameters:

_KEYREG: Reg to pull Key id from

_GROUP: group index int, or string name for getting key string

_KEY: index of string key id to get it's match of other type

set(_VALS, _KEYREG, _GROUP, _KEY, _value)

set items to reg and matrix container

Parameters:

_VALS: Values matrix container

_KEYREG: Key registry

_GROUP: (string) Group/Category name

_KEY: (string) Key for item

_value: item

Returns: void

del(_VALS, _KEYREG, _GROUP, _KEY)

del grroup id

Parameters:

_VALS: Matrix Values slice

_KEYREG: Registry values matrix (strings)

_GROUP: name of group/category

_KEY: name of item to Delete from values and key

detached(_GROUP, _KEY, _VALUE)

detached make detached registry/val matrix

Parameters:

_GROUP: Name of first group

_KEY: Name of first item

_VALUE: Item of any type, sets the output type too.

threengine_global_automation_libraryLibrary "threengine_global_automation_library"

A collection of functions used for trade automation

getBaseCurrency()

Gets the base currency for the chart's ticker. Supported trade pairs are USD, USDT, USDC, BTC, and PERP.

Returns: Base currency as a string

getChartSymbol()

Get the current chart's symbol without the base currency appended to it. Supported trade paris are USD, USDT, USDC, BTC, and PERP.

Returns: Ssymbol and base currency

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current deimal places on the market quote price

checkVar()

Plot a string as a label on the chart to test variable value. Use str.tostring() for any variable that isn't a string.

Returns: Label with stringified variable

getStrategyAlertMessage()

Generates stringified JSON for a limit order that can be passed to the strategy alert_message for a long entry.

Returns: Stringifed JSON for a long entry

taGetAdx()

Calculates the Average Directional Index

Returns: The value of ADX as a float

taGetEma()

Calculates the EMA based on a type, source, and length. Supported types are EMA, SMA, RMA, and WMA.

Returns: The value of the selected EMA

isBetweenTwoTimes()

Checks to see if within a rage based on two times

@retunrs true/false boolean

getAllTradeIDs()

This gets all closed trades and open trades

@retunrs an array of all open and closed trade ID's

getOpenTradeIDs()

This gets all open trades

@retunrs an array of all open trade ID's

orderAlreadyExists()

This checks to see if a provided order id uses the getAllTradeIDs() function to check

@retunrs an array of all open and closed trade ID's

orderCurrentlyExists()

This checks to see if a provided order id uses the getAllTradeIDs() function to check

Returns: an array of all open and closed trade ID's

getContractCount()

calulates the number of contracts you can buy with a set amount of capital and a limit price

Returns: number of contracts you can buy based on amount of capital you want to use and a price

getLadderSteps()

Returns: array of ladder entry prices and amounts based on total amount you want to invest across all ladder rungs and either a range between ladderStart and LadderStop based on specificed number of ladderRungs OR ladderStart, ladderRungs, and LadderSpacingPercent

"Swap" - Bool/Position/Value : Array / Matrix / Var AutoswapLibrary "swap"

Side / Boundary Based All Types Swapper

- three automagical types for Arrays, Matrixes, and Variables

-- no signal : Long/ Short position autoswap

-- true / false : Boolean based side choice

-- Src / Thresh : if source is above or below the threshold

- two operating modes for variables, Holding mode only for arrays/matrixes

-- with two items, will automatically change between the two caveat is it does not delete table/box/line(fill VAR items automatically)

-- with three items, a neutral is available for NA input or neutral

- one function name for all of them. One import name that's easy to type/remember

-- make life easy for your conditional items.

side(source, thresh, _a, _b, _c)

side Change outputs based on position or a crossing level

Parameters:

source : (float) OPTIONAL value input

thresh : (float) OPTIONAL boundary line to cross

_a : (any) if Long/True/Above

_b : (any) if Short/False/Below

_c : (any) OPTIONAL NOT FOR MTX OR ARR... Neutral Item, if var/varip on a/b it will leave behind, ie, a table or box or line will not erase , if it's a varip you're sending in.

Returns: first, second, or third items based on input conditions

Please notify if bugs found.

Thanks.

fontilabLibrary "fontilab"

Provides function's indicators for pivot - trend - resistance.

pivots(src, lenght, isHigh) Detecting pivot points (and returning price + bar index.

Parameters:

src : The chart we analyse.

lenght : Used for the calcul.

isHigh : lookging for high if true, low otherwise.

Returns: The bar index and the price of the pivot.

calcDevThreshold(tresholdMultiplier, closePrice) Calculate deviation threshold for identifying major swings.

Parameters:

tresholdMultiplier : Usefull to equilibrate the calculate.

closePrice : Close price of the chart wanted.

Returns: The deviation threshold.

calcDev(basePrice, price) Custom function for calculating price deviation for validating large moves.

Parameters:

basePrice : The reference price.

price : The price tested.

Returns: The deviation.

pivotFoundWithLines(dev, isHigh, index, price, dev_threshold, isHighLast, pLast, iLast, lineLast) Detecting pivots that meet our deviation criteria.

Parameters:

dev : The deviation wanted.

isHigh : The type of pivot tested (high or low).

index : The Index of the pivot tested.

price : The chart price wanted.

dev_threshold : The deviation treshold.

isHighLast : The type of last pivot.

pLast : The pivot price last.

iLast : Index of the last pivot.

lineLast : The lst line.

Returns: The Line and bool is pivot High.

getDeviationPivots(thresholdMultiplier, depth, lineLast, isHighLast, iLast, pLast, deleteLines, closePrice, highPrice, lowPrice) Get pivot that meet our deviation criteria.

Parameters:

thresholdMultiplier : The treshold multiplier.

depth : The depth to calculate pivot.

lineLast : The last line.

isHighLast : The type of last pivot

iLast : Index of the last pivot.

pLast : The pivot price last.

deleteLines : If the line are draw or not.

closePrice : The chart close price.

highPrice : The chart high price.

lowPrice : The chart low price.

Returns: All pivot the informations.

getElIntArrayFromEnd() Get the last element of an int array.

getElFloatArrayFromEnd() Get the last element of an float array.

getElBoolArrayFromEnd() Get the last element of a bool array.

isTrendContinuation(isTrendUp, arrayBounds, lastPrice, precision) Check if last price is between bounds array.

Parameters:

isTrendUp : Is actual trend up.

arrayBounds : The trend array.

lastPrice : The pivot Price that just be found.

precision : The percent we add to actual bounds to validate a move.

Returns: na if price is between bounds, true if continuation, false if not.

getTrendPivots(trendBarIndexes, trendPrices, trendPricesIsHigh, interBarIndexes, interPrices, interPricesIsHigh, isTrendHesitate, isTrendUp, trendPrecision, pLast, iLast, isHighLast) Function to update array and trend related to pivot trend interpretation.

Parameters:

trendBarIndexes : The array trend bar index.

trendPrices : The array trend price.

trendPricesIsHigh : The array trend is high.

interBarIndexes : The array inter bar index.

interPrices : The array inter price.

interPricesIsHigh : The array inter ishigh.

isTrendHesitate : The actual status of is trend hesitate.

isTrendUp : The actual status of is trend up.

trendPrecision : The var precision to add in "iscontinuation" function.

pLast : The last pivot price.

iLast : The last pivot bar index.

isHighLast : The last pivot "isHigh".

Returns: trend & inter arrays, is trend hesitate, is trend up.

drawBoundLines(startIndex, startPrice, endIndex, endPrice, breakingPivotIndex, breakingPivotPrice, isTrendUp) Draw bounds and breaking line of the trend.

Parameters:

startIndex : Index of the first bound line.

startPrice : Price of first bound line.

endIndex : Index of second bound line.

endPrice : price of second bound line.

breakingPivotIndex : The breaking line index.

breakingPivotPrice : The breaking line price.

isTrendUp : The actual status of the trend.

Returns: The lines bounds and breaking line.

merge_pinbarLibrary "merge_pinbar"

merge_pinbar: merge bars and check whether the bar is a pinbar

merge_pinbar(simple, simple) merge_pinbar: merge bars and check whether the bar is a pinbar

Parameters:

simple : int period: the statistic bar period

simple : int max_bars: the max bars to be merged

Returns: array:

Timed_exit_alert_for_webhookLibrary "Timed_exit_alert_for_webhook"

TODO: add library description here

fun(x) TODO: add function description here

Parameters:

x : TODO: add parameter x description here

Returns: TODO: add what function returns

for exiting FCM like Tradovate and AMP using API and python MT5 and Webhooks

the writer take no responsibility for trades made using this script its written for informational purposes only

adx: Configurable ADX (library) Library "adx"

Calculate ADX (and its constituent parts +DI, -DI, ATR),

using different moving averages and periods.

adx(atrMA, diMA, adxMA, atrLen, diLen, adxLen, h, l, c)

Parameters:

atrMA : Moving Average used for calculating the Average True Range.

Traditionally RMA, but using SMA here and in adxMA gives good results too.

diMA : Moving Average used for calculating the Directional Index.

Traditionally, RMA.

adxMA : Moving Average used for calculating the Average Directional

Index. Traditionally RMA, but using SMA here and in atrMA gives good results

too.

atrLen : Length of the Average True Range.

diLen : Length of the Directional Index.

adxLen : Length (smoothing) of the Average Directional Index.

h : Candle's high.

l : Candle's low.

c : Candle's close.

Returns:

statisticsLibrary "statistics"

General statistics library.

erf(x) The "error function" encountered in integrating the normal

distribution (which is a normalized form of the Gaussian function).

Parameters:

x : The input series.

Returns: The Error Function evaluated for each element of x.

erfc(x)

Parameters:

x : The input series

Returns: The Complementary Error Function evaluated for each alement of x.

sumOfReciprocals(src, len) Calculates the sum of the reciprocals of the series.

For each element 'elem' in the series:

sum += 1/elem

Should the element be 0, the reciprocal value of 0 is used instead

of NA.

Parameters:

src : The input series.

len : The length for the sum.

Returns: The sum of the resciprocals of 'src' for 'len' bars back.

mean(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the mean.

Returns: The mean of 'src' for 'len' bars back.

average(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the average.

Returns: The average of 'src' for 'len' bars back.

geometricMean(src, len) The Geometric Mean of the series.

The geometric mean is most important when using data representing

percentages, ratios, or rates of change. It cannot be used for

negative numbers

Since the pure mathematical implementation generates a very large

intermediate result, we performed the calculation in log space.

Parameters:

src : The input series.

len : The length for the geometricMean.

Returns: The geometric mean of 'src' for 'len' bars back.

harmonicMean(src, len) The Harmonic Mean of the series.

The harmonic mean is most applicable to time changes and, along

with the geometric mean, has been used in economics for price

analysis. It is more difficult to calculate; therefore, it is less

popular than eiter of the other averages.

0 values are ignored in the calculation.

Parameters:

src : The input series.

len : The length for the harmonicMean.

Returns: The harmonic mean of 'src' for 'len' bars back.

median(src, len) The median of the series.

(a wrapper around ta.median)

Parameters:

src : The input series.

len : The length for the median.

Returns: The median of 'src' for 'len' bars back.

variance(src, len, biased) The variance of the series.

Parameters:

src : The input series.

len : The length for the variance.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The variance of 'src' for 'len' bars back.

stdev(src, len, biased) The standard deviation of the series.

Parameters:

src : The input series.

len : The length for the stdev.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The standard deviation of 'src' for 'len' bars back.

skewness(src, len) The skew of the series.

Skewness measures the amount of distortion from a symmetric

distribution, making the curve appear to be short on the left

(lower prices) and extended to the right (higher prices). The

extended side, either left or right is called the tail, and a

longer tail to the right is called positive skewness. Negative

skewness has the tail extending towards the left.

Parameters:

src : The input series.

len : The length for the skewness.

Returns: The skewness of 'src' for 'len' bars back.

kurtosis(src, len) The kurtosis of the series.

Kurtosis describes the peakedness or flatness of a distribution.

This can be used as an unbiased assessment of whether prices are

trending or moving sideways. Trending prices will ocver a wider

range and thus a flatter distribution (kurtosis < 3; negative

kurtosis). If prices are range-bound, there will be a clustering

around the mean and we have positive kurtosis (kurtosis > 3)

Parameters:

src : The input series.

len : The length for the kurtosis.

Returns: The kurtosis of 'src' for 'len' bars back.

excessKurtosis(src, len) The normalized kurtosis of the series.

kurtosis > 0 --> positive kurtosis --> trending

kurtosis < 0 --> negative krutosis --> range-bound

Parameters:

src : The input series.

len : The length for the excessKurtosis.

Returns: The excessKurtosis of 'src' for 'len' bars back.

normDist(src, len, value) Calculates the probability mass for the value according to the

src and length. It calculates the probability for value to be

present in the normal distribution calculated for src and length.

Parameters:

src : The input series.

len : The length for the normDist.

value : The series of values to calculate the normal distance for

Returns: The normal distance of 'value' to 'src' for 'len' bars back.

normDistCumulative(src, len, value) Calculates the cumulative probability mass for the value according

to the src and length. It calculates the cumulative probability for

value to be present in the normal distribution calculated for src

and length.

Parameters:

src : The input series.

len : The length for the normDistCumulative.

value : The series of values to calculate the cumulative normal distance

for

Returns: The cumulative normal distance of 'value' to 'src' for 'len' bars

back.

zScore(src, len, value) Returns then z-score of objective to the series src.

It returns the number of stdev's the objective is away from the

mean(src, len)

Parameters:

src : The input series.

len : The length for the zScore.

value : The series of values to calculate the cumulative normal distance

for

Returns: The z-score of objectiv with respect to src and len.

er(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

efficiencyRatio(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

fractalEfficiency(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

mse(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

meanSquaredError(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

rmse(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

rootMeanSquaredError(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

mae(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

meanAbsoluteError(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

CRCHud - HUD Library (Heads Up Display)Library "CRCHud"

Library of functions which will contain functions that allow reusable HUD (Heads up Display) components to used from within other scripts

add_cell_change() - Adds a new cell to designated table which displays the data source value, the line color, data title, and automatically calculated %percent change stats based on lookback value supplied (default - previous bar)

Punchline_LibLibrary "Punchline_Lib"

roundSmart(float) Truncates decimal points of a float value based on the amount of digits before the decimal point

Parameters:

float : _value any number

Returns: float

tostring_smart(float) converts a float to a string, intelligently cutting off decimal points

Parameters:

float : _value any number

Returns: string

The Divergent LibraryLibrary "TheDivergentLibrary"

The Divergent Library is only useful when combined with the Pro version of The Divergent - Advanced divergence indicator . This is because the Basic (free) version of The Divergent does not expose the "Divergence Signal" value.

Usage instructions:

1. Create a new chart

2. Add The Divergent (Pro) indicator to your chart

3. Create a new strategy, import this library, add a "source" input, link it to "The Divergent: Divergence Signal", and use the library to decode the divergence signals from The Divergent (You can find example strategy code published in our profile)

4. Act on the divergences signalled by The Divergent

---

isRegularBullishEnabled(context) Returns a boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

isHiddenBullishEnabled(context) Returns a boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

isRegularBearishEnabled(context) Returns a boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

isHiddenBearishEnabled(context) Returns a boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

getPivotDetectionSource(context) Returns the 'Pivot Detection Source' setting of The Divergent. The returned value can be either "Oscillator" or "Price".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Oscillator" or "Price".

getPivotDetectionMode(context) Returns the 'Pivot Detection Mode' setting of The Divergent. The returned value can be either "Bodies" or "Wicks".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Bodies" or "Wicks".

isLinked(context) Returns a boolean value indicating the link status to The Divergent indicator.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating the link status to The Divergent indicator.

init(firstBarSignal, displayLinkStatus, debug) Initialises The Divergent Library's context with the signal produced by The Divergent on the first bar. The value returned from this function is called the "context of The Divergent Library". Some of the other functions of this library requires you to pass in this context.

Parameters:

firstBarSignal : The signal from The Divergent indicator on the first bar.

displayLinkStatus : A boolean value indicating whether the Link Status window should be displayed in the bottom left corner of the chart. Defaults to true.

debug : A boolean value indicating whether the Link Status window should display debug information. Defaults to false.

Returns: A bool array containing the context of The Divergent Library.

processSignal(signal) Processes a signal from The Divergent and returns a 5-tuple with the decoded signal: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd]. `divergenceType` can be one of the following values: na → No divergence was detected, 1 → Regular Bullish, 2 → Regular Bullish early, 3 → Hidden Bullish, 4 → Hidden Bullish early, 5 → Regular Bearish, 6 → Regular Bearish early, 7 → Hidden Bearish, 8 → Hidden Bearish early.

Parameters:

signal : The signal from The Divergent indicator.

Returns: A 5-tuple with the following values: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd].

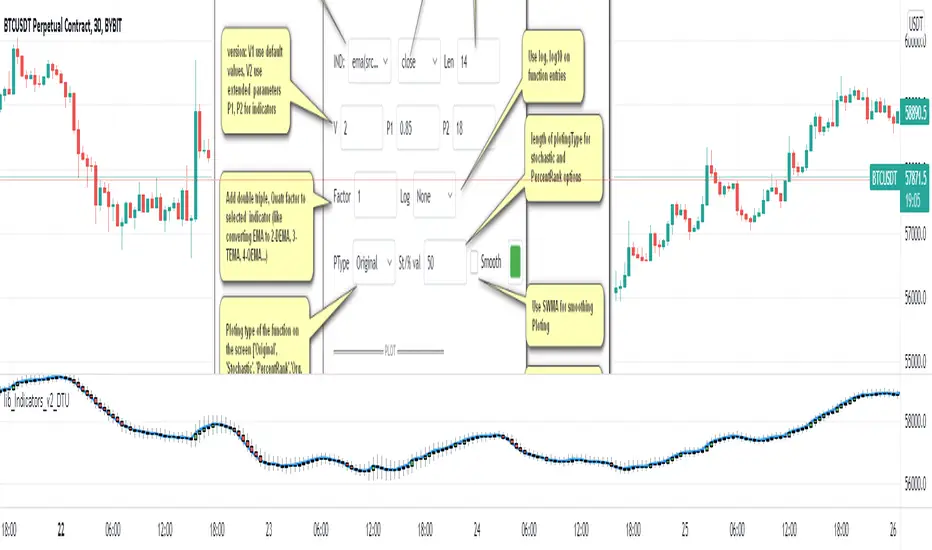

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change