MERV: Market Entropy & Rhythm Visualizer [BullByte]The MERV (Market Entropy & Rhythm Visualizer) indicator analyzes market conditions by measuring entropy (randomness vs. trend), tradeability (volatility/momentum), and cyclical rhythm. It provides traders with an easy-to-read dashboard and oscillator to understand when markets are structured or choppy, and when trading conditions are optimal.

Purpose of the Indicator

MERV’s goal is to help traders identify different market regimes. It quantifies how structured or random recent price action is (entropy), how strong and volatile the movement is (tradeability), and whether a repeating cycle exists. By visualizing these together, MERV highlights trending vs. choppy environments and flags when conditions are favorable for entering trades. For example, a low entropy value means prices are following a clear trend line, whereas high entropy indicates a lot of noise or sideways action. The indicator’s combination of measures is original: it fuses statistical trend-fit (entropy), volatility trends (ATR and slope), and cycle analysis to give a comprehensive view of market behavior.

Why a Trader Should Use It

Traders often need to know when a market trend is reliable vs. when it is just noise. MERV helps in several ways: it shows when the market has a strong direction (low entropy, high tradeability) and when it’s ranging (high entropy). This can prevent entering trend-following strategies during choppy periods, or help catch breakouts early. The “Optimal Regime” marker (a star) highlights moments when entropy is very low and tradeability is very high, typically the best conditions for trend trades. By using MERV, a trader gains an empirical “go/no-go” signal based on price history, rather than guessing from price alone. It’s also adaptable: you can apply it to stocks, forex, crypto, etc., on any timeframe. For example, during a bullish phase of a stock, MERV will turn green (Trending Mode) and often show a star, signaling good follow-through. If the market later grinds sideways, MERV will shift to magenta (Choppy Mode), warning you that trend-following is now risky.

Why These Components Were Chosen

Market Entropy (via R²) : This measures how well recent prices fit a straight line. We compute a linear regression on the last len_entropy bars and calculate R². Entropy = 1 - R², so entropy is low when prices follow a trend (R² near 1) and high when price action is erratic (R² near 0). This single number captures trend strength vs noise.

Tradeability (ATR + Slope) : We combine two familiar measures: the Average True Range (ATR) (normalized by price) and the absolute slope of the regression line (scaled by ATR). Together they reflect how active and directional the market is. A high ATR or strong slope means big moves, making a trend more “tradeable.” We take a simple average of the normalized ATR and slope to get tradeability_raw. Then we convert it to a percentile rank over the lookback window so it’s stable between 0 and 1.

Percentile Ranks : To make entropy and tradeability values easy to interpret, we convert each to a 0–100 rank based on the past len_entropy periods. This turns raw metrics into a consistent scale. (For example, an entropy rank of 90 means current entropy is higher than 90% of recent values.) We then divide by 100 to plot them on a 0–1 scale.

Market Mode (Regime) : Based on those ranks, MERV classifies the market:

Trending (Green) : Low entropy rank (<40%) and high tradeability rank (>60%). This means the market is structurally trending with high activity.

Choppy (Magenta) : High entropy rank (>60%) and low tradeability rank (<40%). This is a mostly random, low-momentum market.

Neutral (Cyan) : All other cases. This covers mixed regimes not strongly trending or choppy.

The mode is shown as a colored bar at the bottom: green for trending, magenta for choppy, cyan for neutral.

Optimal Regime Signal : Separately, we mark an “optimal” condition when entropy_norm < 0.3 and tradeability > 0.7 (both normalized 0–1). When this is true, a ★ star appears on the bottom line. This star is colored white when truly optimal, gold when only tradeability is high (but entropy not quite low enough), and black when neither condition holds. This gives a quick visual cue for very favorable conditions.

What Makes MERV Stand Out

Holistic View : Unlike a single-oscillator, MERV combines trend, volatility, and cycle analysis in one tool. This multi-faceted approach is unique.

Visual Dashboard : The fixed on-chart dashboard (shown at your chosen corner) summarizes all metrics in bar/gauge form. Even a non-technical user can glance at it: more “█” blocks = a higher value, colors match the plots. This is more intuitive than raw numbers.

Adaptive Thresholds : Using percentile ranks means MERV auto-adjusts to each market’s character, rather than requiring fixed thresholds.

Cycle Insight : The rhythm plot adds information rarely found in indicators – it shows if there’s a repeating cycle (and its period in bars) and how strong it is. This can hint at natural bounce or reversal intervals.

Modern Look : The neon color scheme and glow effects make the lines easy to distinguish (blue/pink for entropy, green/orange for tradeability, etc.) and the filled area between them highlights when one dominates the other.

Recommended Timeframes

MERV can be applied to any timeframe, but it will be more reliable on higher timeframes. The default len_entropy = 50 and len_rhythm = 30 mean we use 30–50 bars of history, so on a daily chart that’s ~2–3 months of data; on a 1-hour chart it’s about 2–3 days. In practice:

Swing/Position traders might prefer Daily or 4H charts, where the calculations smooth out small noise. Entropy and cycles are more meaningful on longer trends.

Day trader s could use 15m or 1H charts if they adjust the inputs (e.g. shorter windows). This provides more sensitivity to intraday cycles.

Scalpers might find MERV too “slow” unless input lengths are set very low.

In summary, the indicator works anywhere, but the defaults are tuned for capturing medium-term trends. Users can adjust len_entropy and len_rhythm to match their chart’s volatility. The dashboard position can also be moved (top-left, bottom-right, etc.) so it doesn’t cover important chart areas.

How the Scoring/Logic Works (Step-by-Step)

Compute Entropy : A linear regression line is fit to the last len_entropy closes. We compute R² (goodness of fit). Entropy = 1 – R². So a strong straight-line trend gives low entropy; a flat/noisy set of points gives high entropy.

Compute Tradeability : We get ATR over len_entropy bars, normalize it by price (so it’s a fraction of price). We also calculate the regression slope (difference between the predicted close and last close). We scale |slope| by ATR to get a dimensionless measure. We average these (ATR% and slope%) to get tradeability_raw. This represents how big and directional price moves are.

Convert to Percentiles : Each new entropy and tradeability value is inserted into a rolling array of the last 50 values. We then compute the percentile rank of the current value in that array (0–100%) using a simple loop. This tells us where the current bar stands relative to history. We then divide by 100 to plot on .

Determine Modes and Signal : Based on these normalized metrics: if entropy < 0.4 and tradeability > 0.6 (40% and 60% thresholds), we set mode = Trending (1). If entropy > 0.6 and tradeability < 0.4, mode = Choppy (-1). Otherwise mode = Neutral (0). Separately, if entropy_norm < 0.3 and tradeability > 0.7, we set an optimal flag. These conditions trigger the colored mode bars and the star line.

Rhythm Detection : Every bar, if we have enough data, we take the last len_rhythm closes and compute the mean and standard deviation. Then for lags from 5 up to len_rhythm, we calculate a normalized autocorrelation coefficient. We track the lag that gives the maximum correlation (best match). This “best lag” divided by len_rhythm is plotted (a value between 0 and 1). Its color changes with the correlation strength. We also smooth the best correlation value over 5 bars to plot as “Cycle Strength” (also 0 to 1). This shows if there is a consistent cycle length in recent price action.

Heatmap (Optional) : The background color behind the oscillator panel can change with entropy. If “Neon Rainbow” style is on, low entropy is blue and high entropy is pink (via a custom color function), otherwise a classic green-to-red gradient can be used. This visually reinforces the entropy value.

Volume Regime (Dashboard Only) : We compute vol_norm = volume / sma(volume, len_entropy). If this is above 1.5, it’s considered high volume (neon orange); below 0.7 is low (blue); otherwise normal (green). The dashboard shows this as a bar gauge and percentage. This is for context only.

Oscillator Plot – How to Read It

The main panel (oscillator) has multiple colored lines on a 0–1 vertical scale, with horizontal markers at 0.2 (Low), 0.5 (Mid), and 0.8 (High). Here’s each element:

Entropy Line (Blue→Pink) : This line (and its glow) shows normalized entropy (0 = very low, 1 = very high). It is blue/green when entropy is low (strong trend) and pink/purple when entropy is high (choppy). A value near 0.0 (below 0.2 line) indicates a very well-defined trend. A value near 1.0 (above 0.8 line) means the market is very random. Watch for it dipping near 0: that suggests a strong trend has formed.

Tradeability Line (Green→Yellow) : This represents normalized tradeability. It is colored bright green when tradeability is low, transitioning to yellow as tradeability increases. Higher values (approaching 1) mean big moves and strong slopes. Typically in a market rally or crash, this line will rise. A crossing above ~0.7 often coincides with good trend strength.

Filled Area (Orange Shade) : The orange-ish fill between the entropy and tradeability lines highlights when one dominates the other. If the area is large, the two metrics diverge; if small, they are similar. This is mostly aesthetic but can catch the eye when the lines cross over or remain close.

Rhythm (Cycle) Line : This is plotted as (best_lag / len_rhythm). It indicates the relative period of the strongest cycle. For example, a value of 0.5 means the strongest cycle was about half the window length. The line’s color (green, orange, or pink) reflects how strong that cycle is (green = strong). If no clear cycle is found, this line may be flat or near zero.

Cycle Strength Line : Plotted on the same scale, this shows the autocorrelation strength (0–1). A high value (e.g. above 0.7, shown in green) means the cycle is very pronounced. Low values (pink) mean any cycle is weak and unreliable.

Mode Bars (Bottom) : Below the main oscillator, thick colored bars appear: a green bar means Trending Mode, magenta means Choppy Mode, and cyan means Neutral. These bars all have a fixed height (–0.1) and make it very easy to see the current regime.

Optimal Regime Line (Bottom) : Just below the mode bars is a thick horizontal line at –0.18. Its color indicates regime quality: White (★) means “Optimal Regime” (very low entropy and high tradeability). Gold (★) means not quite optimal (high tradeability but entropy not low enough). Black means neither condition. This star line quickly tells you when conditions are ideal (white star) or simply good (gold star).

Horizontal Guides : The dotted lines at 0.2 (Low), 0.5 (Mid), and 0.8 (High) serve as reference lines. For example, an entropy or tradeability reading above 0.8 is “High,” and below 0.2 is “Low,” as labeled on the chart. These help you gauge values at a glance.

Dashboard (Fixed Corner Panel)

MERV also includes a compact table (dashboard) that can be positioned in any corner. It summarizes key values each bar. Here is how to read its rows:

Entropy : Shows a bar of blocks (█ and ░). More █ blocks = higher entropy. It also gives a percentage (rounded). A full bar (10 blocks) with a high % means very chaotic market. The text is colored similarly (blue-green for low, pink for high).

Rhythm : Shows the best cycle period in bars (e.g. “15 bars”). If no calculation yet, it shows “n/a.” The text color matches the rhythm line.

Cycle Strength : Gives the cycle correlation as a percentage (smoothed, as shown on chart). Higher % (green) means a strong cycle.

Tradeability : Displays a 10-block gauge for tradeability. More blocks = more tradeable market. It also shows “gauge” text colored green→yellow accordingly.

Market Mode : Simply shows “Trending”, “Choppy”, or “Neutral” (cyan text) to match the mode bar color.

Volume Regime : Similar to tradeability, shows blocks for current volume vs. average. Above-average volume gives orange blocks, below-average gives blue blocks. A % value indicates current volume relative to average. This row helps see if volume is abnormally high or low.

Optimal Status (Large Row) : In bold, either “★ Optimal Regime” (white text) if the star condition is met, “★ High Tradeability” (gold text) if tradeability alone is high, or “— Not Optimal” (gray text) otherwise. This large row catches your eye when conditions are ripe.

In short, the dashboard turns the numeric state into an easy read: filled bars, colors, and text let you see current conditions without reading the plot. For instance, five blue blocks under Entropy and “25%” tells you entropy is low (good), and a row showing “Trending” in green confirms a trend state.

Real-Life Example

Example : Consider a daily chart of a trending stock (e.g. “AAPL, 1D”). During a strong uptrend, recent prices fit a clear upward line, so Entropy would be low (blue line near bottom, perhaps below the 0.2 line). Volatility and slope are high, so Tradeability is high (green-yellow line near top). In the dashboard, Entropy might show only 1–2 blocks (e.g. 10%) and Tradeability nearly full (e.g. 90%). The Market Mode bar turns green (Trending), and you might see a white ★ on the optimal line if conditions are very good. The Volume row might light orange if volume is above average during the rally. In contrast, imagine the same stock later in a tight range: Entropy will rise (pink line up, more blocks in dashboard), Tradeability falls (fewer blocks), and the Mode bar turns magenta (Choppy). No star appears in that case.

Consolidated Use Case : Suppose on XYZ stock the dashboard reads “Entropy: █░░░░░░░░ 20%”, “Tradeability: ██████████ 80%”, Mode = Trending (green), and “★ Optimal Regime.” This tells the trader that the market is in a strong, low-noise trend, and it might be a good time to follow the trend (with appropriate risk controls). If instead it reads “Entropy: ████████░░ 80%”, “Tradeability: ███▒▒▒▒▒▒ 30%”, Mode = Choppy (magenta), the trader knows the market is random and low-momentum—likely best to sit out until conditions improve.

Example: How It Looks in Action

Screenshot 1: Trending Market with High Tradeability (SOLUSD, 30m)

What it means:

The market is in a clear, strong trend with excellent conditions for trading. Both trend-following and active strategies are favored, supported by high tradeability and strong volume.

Screenshot 2: Optimal Regime, Strong Trend (ETHUSD, 1h)

What it means:

This is an ideal environment for trend trading. The market is highly organized, tradeability is excellent, and volume supports the move. This is when the indicator signals the highest probability for success.

Screenshot 3: Choppy Market with High Volume (BTC Perpetual, 5m)

What it means:

The market is highly random and choppy, despite a surge in volume. This is a high-risk, low-reward environment, avoid trend strategies, and be cautious even with mean-reversion or scalping.

Settings and Inputs

The script is fully open-source; here are key inputs the user can adjust:

Entropy Window (len_entropy) : Number of bars used for entropy and tradeability (default 50). Larger = smoother, more lag; smaller = more sensitivity.

Rhythm Window (len_rhythm ): Bars used for cycle detection (default 30). This limits the longest cycle we detect.

Dashboard Position : Choose any corner (Top Right default) so it doesn’t cover chart action.

Show Heatmap : Toggles the entropy background coloring on/off.

Heatmap Style : “Neon Rainbow” (colorful) or “Classic” (green→red).

Show Mode Bar : Turn the bottom mode bar on/off.

Show Dashboard : Turn the fixed table panel on/off.

Each setting has a tooltip explaining its effect. In the description we will mention typical settings (e.g. default window sizes) and that the user can move the dashboard corner as desired.

Oscillator Interpretation (Recap)

Lines : Blue/Pink = Entropy (low=trend, high=chop); Green/Yellow = Tradeability (low=quiet, high=volatile).

Fill : Orange tinted area between them (for visual emphasis).

Bars : Green=Trending, Magenta=Choppy, Cyan=Neutral (at bottom).

Star Line : White star = ideal conditions, Gold = good but not ideal.

Horizontal Guides : 0.2 and 0.8 lines mark low/high thresholds for each metric.

Using the chart, a coder or trader can see exactly what each output represents and make decisions accordingly.

Disclaimer

This indicator is provided as-is for educational and analytical purposes only. It does not guarantee any particular trading outcome. Past market patterns may not repeat in the future. Users should apply their own judgment and risk management; do not rely solely on this tool for trading decisions. Remember, TradingView scripts are tools for market analysis, not personalized financial advice. We encourage users to test and combine MERV with other analysis and to trade responsibly.

-BullByte

M-oscillator

Swing Strategy MTF with Auto SL/TP + Weekly Pivotsested and Working Notes:

Works on any intraday chart (like 1H or 4H)

Uses Daily trend for confirmation by default

Adjust trend EMAs or pivot TF if needed

Wait for a signal label after candle close

Targets and SL are drawn automatically

—

MACD Signal with Williams %R ColoringA simple fused indicator of 2, 1) MACD signal lines made colouring when 2) Williams % R is in overbought or oversold. not my own coding, just took two readily available indicators and coded them together.

strategy15min bar, short-term and scalp strategy, eth, using stdev as trend line, long when price hits the lower line, short when price hits the upper line.

Gold 3min Trading Pro [XAU/USD]# Gold 3min Trading Pro - User Guide

## Overview

This is a professional scalping indicator specifically designed for Gold (XAU/USD) trading on 3-minute timeframes. It combines multiple technical analysis methods to provide high-probability entry signals for short-term trading.

## Key Features

### 1. Multi-Timeframe Trend Analysis

- **Major Trend**: Analyzes 15min, 1H, and 4H timeframes using moving averages

- **Short-term Trend**: Focuses on 3-minute price action and moving average alignment

- **Trend Strength**: Rated from 1-3 based on timeframe agreement

### 2. Core Indicators

- **RSI (9-period)**: Momentum oscillator for overbought/oversold conditions

- **Stochastic (9-period)**: %K and %D lines for entry timing

- **MACD**: Additional trend confirmation

- **Volume Analysis**: Detects volume spikes for signal validation

- **ATR-based Volatility Filter**: Ensures adequate market movement

### 3. Signal Types

- **Primary Signals**: Green triangles (LONG) and Red triangles (SHORT)

- **Enhanced Signals**: Stronger signals with multiple confirmations

- **Confirmation Signals**: Small circles for stochastic crossovers

## How to Use

### 1. Setup

- **Timeframe**: Use on 3-minute charts for Gold (XAU/USD)

- **Settings**: Default settings are optimized for Gold scalping

- **Session Filter**: Enable for London/New York sessions (recommended)

### 2. Entry Conditions

#### LONG Entry:

- Major trend is bullish (green background)

- Short-term trend is up or neutral

- RSI shows bullish momentum

- Stochastic indicates oversold recovery

- Volume spike confirmation

- Strong price action (bullish candle)

#### SHORT Entry:

- Major trend is bearish (red background)

- Short-term trend is down or neutral

- RSI shows bearish momentum

- Stochastic indicates overbought reversal

- Volume spike confirmation

- Strong price action (bearish candle)

### 3. Trade Management

- **Quick Target**: 50% of ATR-based calculation

- **Main Target**: Full ATR-based target

- **Stop Loss**: 60% of ATR below/above entry

- **Time Limit**: Exit if no progress within 20 bars (60 minutes)

### 4. Risk Management

- **Position Size**: Risk 1-2% of account per trade

- **Maximum Trades**: 3-5 trades per session

- **Avoid**: Low volatility periods and major news events

## Visual Elements

### Background Colors

- **Light Green**: Bullish major trend

- **Light Red**: Bearish major trend

- **Yellow**: Volume spike detected

- **Intense Colors**: Very strong trend alignment

### Chart Indicators

- **RSI Line (Blue)**: Main momentum indicator

- **Stochastic %K (Orange)**: Fast stochastic line

- **Stochastic %D (Yellow)**: Slow stochastic line

- **Horizontal Lines**: 70 (overbought), 30 (oversold), 50 (midline)

### Information Table (Top Right)

- Total signal count and performance statistics

- Current market conditions and trend strength

- RSI levels and volatility status

- Trading session information

- Last signal timing

## Alert System

### Standard Alerts

- **Scalp Long Signal**: Basic long entry signal

- **Scalp Short Signal**: Basic short entry signal

- **Premium Signals**: High-quality signals with strong confirmation

- **Trend Reversal**: Major trend change notifications

### Alert Setup

1. Right-click on chart → "Add Alert"

2. Select desired alert condition

3. Configure notification method (popup, email, webhook)

4. Set alert frequency to "Once Per Bar Close"

## Best Practices

### 1. Trading Sessions

- **Optimal**: London-NY overlap (3:00-5:00 PM EST)

- **Good**: London session (2:00-11:00 AM EST)

- **Avoid**: Asian session and major news releases

### 2. Market Conditions

- **Best**: Trending markets with normal to high volatility

- **Moderate**: Ranging markets during active sessions

- **Avoid**: Extremely low volatility or choppy conditions

### 3. Confirmation Rules

- Wait for signal triangle to appear

- Check that major trend aligns with signal direction

- Verify volume spike (yellow background)

- Ensure volatility is adequate (check info table)

### 4. Entry Timing

- Enter immediately after signal confirmation

- Use market orders for scalping speed

- Set stop loss and take profit levels immediately

## Settings Customization

### Essential Settings

- **MA Type**: EMA (recommended) or SMA

- **RSI Length**: 9 (default, can adjust 5-14)

- **Volume Threshold**: 1.8 (higher = fewer but stronger signals)

- **Volatility Filter**: Keep enabled for better signal quality

### Display Options

- **Show Scalping Signals**: Main entry signals

- **Show Performance Stats**: Information table

- **Show Trend Filter**: Background trend colors

- **Use Time Filter**: Session-based filtering

## Performance Optimization

### 1. Backtesting Tips

- Test on different market conditions

- Analyze win rate and average profit/loss

- Adjust settings based on historical performance

### 2. Signal Quality

- Higher trend strength (2-3) = better signals

- Volume confirmation improves success rate

- Enhanced signals have higher probability

### 3. Risk Control

- Never risk more than 2% per trade

- Use proper position sizing

- Stop trading after 3 consecutive losses

## Troubleshooting

### Common Issues

1. **No Signals**: Check volatility filter and session timing

2. **Too Many Signals**: Increase volume threshold or enable filters

3. **Poor Performance**: Verify timeframe (must be 3-minute) and symbol (XAU/USD)

### Support

- Ensure TradingView Pro+ subscription for multi-timeframe data

- Verify Gold symbol matches your broker's format

- Update to latest TradingView version

This indicator is designed for experienced traders familiar with scalping techniques and risk management. Always practice on demo accounts before live trading.

MACD-RSI Divergence OscillatorMACD-RSI Divergence Oscillator: Dual Confirmation with Momentum + Divergence Signals

This powerful oscillator combines MACD and RSI into a single normalized visual tool, enriched with automatic divergence detection and smart signal alerts. It’s designed to give traders advanced insights into momentum shifts and trend reversals.

Key Features:

• MACD + RSI Combo: Both indicators are scaled and merged into one oscillator for clearer interpretation.

• Automatic Divergence Detection:

• Bullish & Bearish divergences on both MACD and RSI

• Highlights strong divergences when both confirm

• Trading Signals:

• Detects MACD crossovers and RSI reversals

• Smart buy/sell signals based on momentum + divergence

• Custom Oscillator View:

• Plots MACD and RSI on the same scale

• Visual zero-line, overbought/oversold levels, and customizable colors

• Optional Dashboard Table:

• Displays live indicator values, signal states, and divergence status

Ideal For:

• Spotting early trend reversals

• Confirming trade entries/exits

• Avoiding false signals using dual indicator logic

Highly customizable and suitable for all timeframes and asset types.

ATR%The time period can be customized, which is suitable for finding short-term high-volatility trading pairs, and may be suitable for finding grid trading.

Smart Price Divergence (MACD Filter) + EMA📌 Purpose

This indicator detects Price Divergences with MACD filtered by a 200 EMA trend condition.

It helps identify high-probability reversal zones aligned with market trend context.

🧠 How It Works

1. MACD Divergence Logic

Bearish Divergence:

Price makes a higher high.

MACD makes a lower high.

Price is above EMA (indicating possible exhaustion in bullish trend).

Bullish Divergence:

Price makes a lower low.

MACD makes a higher low.

Price is below EMA (indicating possible exhaustion in bearish trend).

2. EMA Trend Filter

EMA(200) is used as a directional filter:

Bearish divergences considered above EMA (extended bullish conditions).

Bullish divergences considered below EMA (extended bearish conditions).

3. Visual & Alerts

EMA(200) plotted on chart in orange.

Red triangles for Bearish Divergence.

Green triangles for Bullish Divergence.

Alerts fire for both divergence types.

📈 How to Use

Look for divergence signals as potential reversal alerts.

Combine with support/resistance or price action for confirmation.

EMA ensures signals occur in extended zones, increasing reliability.

Recommended Timeframes: 1h, 4h, D.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

MACD Fast / Slow / Signal Length

EMA Length (default 200)

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before live trading.

Smart RSI Divergence PRO | Auto Lines + Alerts📌 Purpose

This indicator automatically detects Regular and Hidden RSI Divergences between price action and the RSI oscillator.

It plots divergence lines directly on the chart, labels signals, and includes alerts for automated monitoring.

🧠 How It Works

1. RSI Calculation

RSI is calculated using the selected Source (default: Close) and RSI Length (default: 14).

2. Divergence Detection via Fractals

Swing points on both price and RSI are detected using fractal logic (5-bar patterns).

Regular Divergence:

Bearish: Price forms a higher high, RSI forms a lower high.

Bullish: Price forms a lower low, RSI forms a higher low.

Hidden Divergence:

Bearish: Price forms a lower high, RSI forms a higher high.

Bullish: Price forms a higher low, RSI forms a lower low.

3. Auto Drawing Lines

Lines are drawn automatically between divergence points:

Red = Regular Bearish

Green = Regular Bullish

Orange = Hidden Bearish

Blue = Hidden Bullish

Line width and transparency are adjustable.

4. Labels and Alerts

Labels mark divergence points with up/down arrows.

Alerts trigger for each divergence type.

📈 How to Use

Use Regular Divergences to anticipate trend reversals.

Use Hidden Divergences to confirm trend continuation.

Combine with support/resistance, trendlines, or volume for higher probability setups.

Recommended Timeframes: Works on all timeframes; more reliable on 1h, 4h, and Daily.

Markets: Forex, Crypto, Stocks.

⚙️ Inputs

Source (Close, HL2, etc.)

RSI Length

Toggle Regular / Hidden Divergence visibility

Toggle Lines / Labels

Line Width & Line Transparency

⚠️ Disclaimer

This script is for educational purposes only. It does not constitute financial advice.

Always test thoroughly before using in live trading.

Smart Impulse Exhaustion Finder (ATR + ADX Filter)📌 Purpose

This indicator detects potential exhaustion of strong bullish or bearish impulses at fresh swing highs/lows by combining multiple price action and volatility-based filters.

🧠 How It Works

A signal is triggered only when all core conditions are satisfied:

1. Swing High/Low Detection

Current high (or low) must be the highest (or lowest) over the last Extremum Lookback bars (default: 50).

This ensures the move is significant relative to recent price action.

2. Impulse Confirmation

Price must extend by at least 1 × ATR from the previous swing point.

This filters out minor fluctuations.

3. Exhaustion Conditions (at least 2 out of 3 must be met)

RSI Extreme: RSI > Overbought Level (default: 80) for bearish signals, RSI < Oversold Level (default: 20) for bullish signals.

Volume Spike: Volume > SMA(Volume, Volume SMA Length) × Volume Spike Multiplier.

Candle Wick Rejection: Upper wick ≥ Wick Threshold % for bearish setups, Lower wick ≥ Wick Threshold % for bullish setups.

4. Trend Filter

ADX > ADX Threshold ensures the market is trending and filters out sideways conditions.

5. Candle Body Filter

Candle body must be ≥ Body Size ATR Factor × ATR.

This avoids weak signals from small candles or doji formations.

📈 How to Use

Bearish Signal:

Appears at fresh swing highs with exhaustion conditions met. Useful for tightening stops, taking partial profits, or counter-trend shorts.

Bullish Signal:

Appears at fresh swing lows with exhaustion conditions met. Useful for trailing stops, profit-taking, or counter-trend longs.

Recommended Timeframes: Works best on 1h, 4h, and Daily charts.

Markets: Crypto, Forex, Stocks — wherever volatility and trends are present.

⚙️ Inputs

RSI Length / Overbought / Oversold

Volume SMA Length & Volume Spike Multiplier

Wick Threshold %

Extremum Lookback (bars for highs/lows)

ADX Length & Threshold

Body Size ATR Factor

⚠️ Disclaimer

This script is for educational purposes only and does not constitute financial advice.

Always test thoroughly and apply proper risk management before live trading.

💡 Tip: Combine this tool with your own market context and confluence factors for higher probability setups.

JHW Volume Based Buy and Sell MomentumThe JHW Volume-Based Buy and Sell Momentum indicator is a custom momentum oscillator designed to capture market sentiment based on volume dynamics and price rate of change (ROC). It aims to identify bullish or bearish momentum by analyzing how price reacts to increasing or decreasing trading volume.

Core Logic:

The indicator calculates the Rate of Change (ROC) of the closing price.

It then accumulates this ROC separately based on whether the current volume is lower or higher than the previous bar:

If volume decreases, the ROC is added to a "negative volume index" accumulator.

If volume increases, the ROC is added to a "positive volume index" accumulator.

These two accumulators are combined to form a net momentum line.

Smoothing:

A Simple Moving Average (SMA) is applied to both accumulators over a user-defined period (default: 25 bars).

The sum of these smoothed values forms the signal line.

Visualization:

The indicator plots:

The net momentum line (yellow).

The smoothed signal line (blue).

The area between the two lines is filled with color:

Yellow when momentum is above the signal (bullish).

Blue when momentum is below the signal (bearish).

Bar colors are also adjusted to reflect the current momentum state.

Use Case:

This indicator helps traders:

Detect volume-driven momentum shifts.

Identify potential buy or sell zones based on volume behavior.

Confirm trends or spot early reversals.

Trigonometric StochasticTrigonometric Stochastic - Mathematical Smoothing Oscillator

Overview

A revolutionary approach to stochastic oscillation using sine wave mathematical smoothing. This indicator transforms traditional stochastic calculations through trigonometric functions, creating an ultra-smooth oscillator that reduces noise while maintaining sensitivity to price changes.

Mathematical Foundation

Unlike standard stochastic oscillators, this version applies sine wave smoothing:

• Raw Stochastic: (close - lowest_low) / (highest_high - lowest_low) × 100

• Trigonometric Smoothing: 50 + 50 × sin(2π × raw_stochastic / 100)

• Result: Naturally smooth oscillator with mathematical precision

Key Features

Advanced Smoothing Technology

• Sine Wave Filter: Eliminates choppy movements while preserving signal integrity

• Natural Boundaries: Mathematically constrained between 0-100

• Reduced False Signals: Trigonometric smoothing filters market noise effectively

Traditional Stochastic Levels

• Overbought Zone: 80 level (dashed line)

• Oversold Zone: 20 level (dashed line)

• Midline: 50 level (dotted line) - equilibrium point

• Visual Clarity: Clean oscillator panel with clear level markings

Smart Signal Generation

• Anti-Repaint Logic: Uses confirmed previous bar values

• Buy Signals: Generated when crossing above 30 from oversold territory

• Sell Signals: Generated when crossing below 70 from overbought territory

• Crossover Detection: Precise entry/exit timing

Professional Presentation

• Separate Panel: Dedicated oscillator window (overlay=false)

• Price Format: Formatted as price indicator with 2-decimal precision

• Theme Adaptive: Automatically matches your chart color scheme

Parameters

• Cycle Length (5-200): Period for highest/lowest calculations

- Shorter periods = more sensitive, more signals

- Longer periods = smoother, fewer but stronger signals

Trading Applications

Momentum Analysis

• Overbought/Oversold: Clear visual identification of extreme levels

• Momentum Shifts: Early detection of momentum changes

• Trend Strength: Monitor oscillator position relative to midline

Signal Trading

• Long Entries: Buy when crossing above 30 (oversold bounce)

• Short Entries: Sell when crossing below 70 (overbought rejection)

• Confirmation Tool: Use with trend indicators for higher probability trades

Divergence Detection

• Bullish Divergence: Price makes lower lows, oscillator makes higher lows

• Bearish Divergence: Price makes higher highs, oscillator makes lower highs

• Early Warning: Spot potential trend reversals before they occur

Trading Strategies

Scalping (5-15min timeframes)

• Use cycle length 10-14 for quick signals

• Focus on 20/80 level bounces

• Combine with price action confirmation

Swing Trading (1H-4H timeframes)

• Use cycle length 20-30 for reliable signals

• Wait for clear crossovers with momentum

• Monitor divergences for reversal setups

Position Trading (Daily+ timeframes)

• Use cycle length 50+ for major signals

• Focus on extreme readings (below 10, above 90)

• Combine with fundamental analysis

Advantages Over Standard Stochastic

1. Smoother Action: Sine wave smoothing reduces whipsaws

2. Mathematical Precision: Trigonometric functions provide consistent behavior

3. Maintained Sensitivity: Smoothing doesn't compromise signal quality

4. Reduced Noise: Cleaner signals in volatile markets

5. Visual Appeal: More aesthetically pleasing oscillator movement

Best Practices

• Market Context: Consider overall trend direction

• Multiple Timeframe: Confirm signals on higher timeframes

• Risk Management: Always use proper position sizing

• Backtesting: Test parameters on your preferred instruments

• Combination: Works excellently with trend-following indicators

Built-in Alerts

• Buy Alert: Trigonometric stochastic oversold crossover

• Sell Alert: Trigonometric stochastic overbought crossunder

Technical Specifications

• Pine Script Version: v6

• Panel: Separate oscillator window

• Format: Price indicator with 2-decimal precision

• Performance: Optimized for all timeframes

• Compatibility: Works with all instruments

Free and open-source indicator. Modify, improve, and share with the community!

Educational Value: Perfect for traders wanting to understand how mathematical smoothing improves oscillators and trigonometric applications in technical analysis.

COT Comm OsciDescription

The COT Comm Osci is a sentiment oscillator based on net positions from the weekly Commitments of Traders (COT) report.

It transforms net positions of Commercials, Noncommercials, or Nonreportables into a 0–100 index.

A value of 100 = highest net position within the selected timeframe.

A value of 0 = lowest net position.

You can define three historical intervals (e.g. 26/ 52 / 156 weeks).

Tip

To improve your analysis, it's recommended to add a separate COT indicator that visualizes raw Long/Short or net positions directly. This helps interpret the oscillator in context.

This script is based on “Commercial Index–Buschi” by MagicEins and has been extended with new features and error handling.

Features

Select between Commercial, Noncommercial, or Nonreportable trader groups

Proper handling of HG Futures (Copper)

Displays a warning if the root code is invalid (unsupported market symbol)

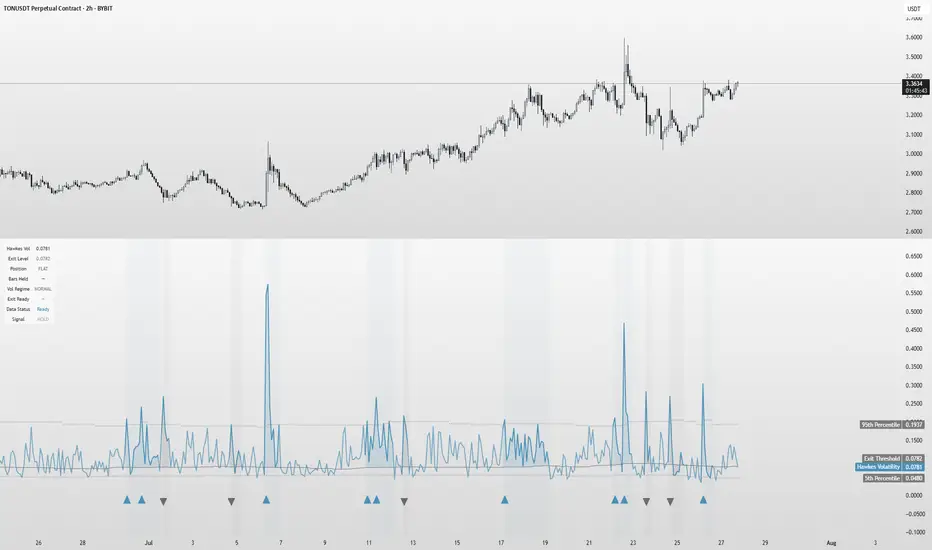

Hawkes Volatility Exit IndicatorOverview

The Hawkes Volatility Exit Indicator is a powerful tool designed to help traders capitalize on volatility breakouts and exit positions when momentum fades. Built on the Hawkes process, it models volatility clustering to identify optimal entry points after quiet periods and exit signals during volatility cooling. Designed to be helpful for swing traders and trend followers across markets like stocks, forex, and crypto.

Key Features Volatility-Based Entries: Detects breakouts when volatility spikes above the 95th percentile (adjustable) after quiet periods (below 5th percentile).

This indicator is probably better on exits than entries.

Smart Exit Signals: Triggers exits when volatility drops below a customizable threshold (default: 30th percentile) after a minimum hold period.

Hawkes Process: Uses a decay-based model (kappa) to capture volatility clustering, making it responsive to market dynamics.

Visual Clarity: Includes a volatility line, exit threshold, percentile bands, and intuitive markers (triangles for entries, X for exits).

Status Table: Displays real-time data on position (LONG/SHORT/FLAT), volatility regime (HIGH/LOW/NORMAL), bars held, and exit readiness.

Customizable Alerts: Set alerts for breakouts and exits to stay on top of trading opportunities.

How It Works Quiet Periods: Identifies low volatility (below 5th percentile) that often precede significant moves.

Breakout Entries: Signals bullish (triangle up) or bearish (triangle down) entries when volatility spikes post-quiet period.

Exit Signals: Suggests exiting when volatility cools below the exit threshold after a minimum hold (default: 3 bars).

Visuals & Table: Tracks volatility, position status, and signals via lines, shaded zones, and a detailed status table.

Settings

Hawkes Kappa (0.1): Adjusts volatility decay (lower = smoother, higher = more sensitive).

Volatility Lookback (168): Sets the period for percentile calculations.

ATR Periods (14): Normalizes volatility using Average True Range.

Breakout Threshold (95%): Volatility percentile for entries.

Exit Threshold (30%): Volatility percentile for exits.

Quiet Threshold (5%): Defines quiet periods.

Minimum Hold Bars (3): Ensures positions are held before exiting.

Alerts: Enable/disable breakout and exit alerts.

How to Use

Entries: Look for triangle markers (up for long, down for short) and confirm with the status table showing "ENTRY" and "LONG"/"SHORT."

Exits: Exit on X cross markers when the status table shows "EXIT" and "Exit Ready: YES."

Monitoring: Use the status table to track position, bars held, and volatility regime (HIGH/LOW/NORMAL).

Combine: Pair with price action, support/resistance, or other indicators for better context.

Tips : Adjust thresholds for your market: lower breakout thresholds for more signals, higher exit thresholds for earlier exits.

Test on your asset to ensure compatibility (best for markets with volatility clustering).

Use alerts to automate signal detection.

Limitations Requires sufficient data (default: 168 bars) for reliable signals. Check "Data Status" in the table.

Focuses on volatility, not price direction—combine with trend tools.

May lag slightly due to the smoothing nature of the Hawkes process.

Why Use It?

The Hawkes Volatility Exit Indicator offers a unique, data-driven approach to timing trades based on volatility dynamics. Its clear visuals, customizable settings, and real-time status table make it a valuable addition to any trader’s toolkit. Try it to catch breakouts and exit with precision!

This indicator is based on neurotrader888's python repo. All credit to him. All mistakes mine.

This conversion published for wider attention to the Hawkes method.

RV Indicator This Pine Script defines a custom Relative Volatility (RV) Indicator, which measures the ratio of directional price movement to volatility over a specified number of bars. Below is a full explanation of what this script does.

Title:

RV Indicator — Relative Volatility Oscillator

Purpose:

This indicator measures how aggressively price is moving compared to recent volatility, and smooths the result with a signal line. It can be used to gauge momentum shifts and trend strength.

How It Works – Step by Step

1. Measuring Price Momentum (v1)

It calculates the difference between the close and open prices of the last 4 candles.

A weighted average is applied:

The current candle and the one 3 bars ago get weight 1.

The two middle candles (1 and 2 bars ago) get weight 2.

This creates a smoothed momentum measure:

If close > open (bullish), v1 is positive.

If close < open (bearish), v1 is negative.

2. Measuring Volatility (v2)

Similarly, it calculates the high-low range for the last 4 candles.

The same weighting (1, 2, 2, 1) is applied.

This gives a smoothed volatility measure.

3. Combining Momentum and Volatility (RV Ratio)

For the past ti bars (default: 10), it sums up:

All v1 values (momentum sum)

All v2 values (volatility sum)

Then it divides them:

𝑅𝑉= sum of price momentum % sum of volatility

This produces the RV value:

RV > 0: Momentum is bullish (price is generally moving up relative to its volatility).

RV < 0: Momentum is bearish (price is moving down relative to its volatility).

4. Smoothed Signal Line (rvsig)

A smoothed version of the RV is created using a weighted average of the latest 4 RV values.

This acts like a signal line, similar to how MACD uses a signal line.

Crossovers between RV and this signal line can be used to detect shifts in momentum.

5. Visual Output

Orange Line (RV): Shows the raw momentum/volatility ratio.

Blue Line (Signal): A smoother line that follows RV more slowly.

Zero Line: Divides bullish vs. bearish momentum.

How to Use It in Trading

1. Look for Crossovers:

If RV crosses above its signal line → Possible buy signal (momentum turning bullish).

If RV crosses below its signal line → Possible sell signal (momentum turning bearish).

2. Check the Zero Line:

If both RV and Signal are above zero, momentum is bullish.

If both are below zero, momentum is bearish.

3. Filter False Signals:

Combine RV with a trend filter (like a 50 or 200 EMA) to avoid trading against the main trend.

Disclaimer: This script is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading decisions are solely your responsibility. Use at your own risk.

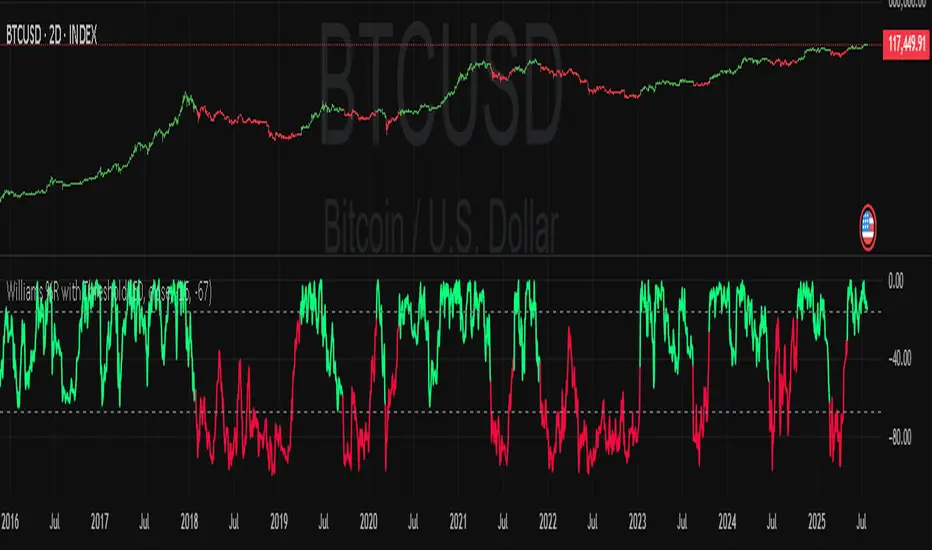

Williams Percent Range with ThresholdEnhance your trading analysis with the "Williams Percent Range with Threshold" indicator, a powerful modification of the classic Williams %R oscillator. This custom version introduces customizable uptrend and downtrend thresholds, combined with dynamic candlestick coloring to visually highlight market trends. Originally designed to identify overbought and oversold conditions, this script takes it a step further by allowing traders to define specific threshold levels for trend detection, making it a versatile tool for momentum and trend-following strategies.

Key Features:

Customizable Thresholds: Set your own uptrend (default: -16) and downtrend (default: -67) thresholds to adapt the indicator to your trading style.

Dynamic Candlestick Coloring: Candles turn green during uptrends, red during downtrends, and gray in neutral conditions, providing an intuitive visual cue directly on the price chart.

Flexible Length: Adjust the lookback period (default: 50) to fine-tune sensitivity.

Overlay Design: Integrates seamlessly with your price chart, enhancing readability without clutter.

How It Works:

The Williams %R calculates the current closing price's position relative to the highest and lowest prices over a specified period, expressed as a percentage between -100 and 0. This version adds trend detection based on user-defined thresholds, with candlestick colors reflecting the trend state. The indicator plots the %R line with color changes (green for uptrend, red for downtrend) and includes dashed lines for the custom thresholds.

Usage Tips:

Use the uptrend threshold (-16 by default) to identify potential buying opportunities when %R exceeds this level.

Apply the downtrend threshold (-67 by default) to spot selling opportunities when %R falls below.

Combine with other indicators (e.g., moving averages or support/resistance levels) for confirmation signals.

Adjust the length and thresholds based on the asset's volatility and your trading timeframe.

RSS-Stochastik [afterworktrading]Hi all,

this is the first script from the series "afterworktrading". The goal is to develop and provide tools for traders with a fulltime job or little time for trading/analyzing charts.

Over time some of the scripts will also be linked to complete trading systems.

Let's start with my favourite one, the "RSS-Stochastik" with alert function.

The RSS-concept (Relative Spread Strength, developed by Ian Copsey) is based on the variance between a "short" and a "long" moving averages (or "slow" and "fast"), here between two EMA.

This variance is calculated and plotted in a RSI-diagram to show "overbought" and "oversold" conditions, helping to identify an ideal entry setup for trend continuation or catching a possible reversal.

Compared to the conventional RSI etc., possible reversal or trend continuation areas are often better represented in terms of quality, as an example see the Amazon-Chart.

The EMA-values, limit value thresholds and background colors can be set in the script. As a special feature, alarms can be set to be notified when a value has reached the extreme range. This reduces the screen time to the minimum.

In my personal trading, this indicator forms the basis for almost all trades, but is not a pure signal indicator on its own.

However, the informative value can be further improved if volume or support/resistance zones etc. are linked to the RSS, see example NASDAQ future with support zone price or 200 EMA.

Example for a possible RSS-Trade-Setup:

- choose an asset with a strong trend

- set alerts for crossing the oversold or overbought condition in direction of the trend

- in case of an alert check possible support/resistance areas on the current chart level (EMA, price zones, volume zones, anchored VWAP etc.)

- trade in the direction of the trend using your preferred entry setup

In my opinion, the system can be used very well, especially in trend phases, in order to obtain optimal entries.

Does it works also on lower timeframes?

Yes, it might work on every timeframe with a strong trend of high quality. Please see attached a 5m-Chart of GPBUSD-pair, notice the signal quality in direction of the trend.

Like every trading system this is not the "holy grail setup" and you will have losing trades. But handling this indicator with care you can have better entries especially in trend direction with less screen time due to the alert function.

Good luck with it! Further indicators will be published in the coming months, some will also be based on the RSS system.

As always: no liability for losing trades, no investment advice etc. Observe the risk limit for every trade!

[Pandora] Laguerre Ultimate Explorations MulticatorIt's time to begin demonstrations differentiating the difference between known and actual feasibility beyond imagination... Welcome to my algorithmic twilight zone .

INTRODUCTION:

Hot off my press, I present this Laguerre multicator employing PSv6.0, originally formulated by John Ehlers for TASC - July 2025 Traders Tips. Basically I transcended Ehlers' notions of transversal filtration with an overhaul of his Laguerre design with my "what if" Pandora notions included. Striving beyond John Ehlers' original intended design. This action packed indicator is a radically revamped version of his original filter using novel techniques. My aim was to explore whether providing even more enhanced responsiveness and lesser lag is possible and how. Presented here is my mind warping results to witness.

EHLERS' LAGUERRE EXPLAINED:

First and foremost, the concept of Ehlers' Laguerre-izing method deserves a comprehensive deep dive. Ehlers' Laguerre filter design, as it functions originally, begins with his Ultimate Smoother (US) followed by a gang of four LERP (jargon for Linear intERPolation) filters. Following a myriad of cascading LERPs is a window-like FIR filter tapped into the LERP delay values to provide extra smoothness via the output.

On a side note, damping factor controlled LERP filters resemble EMAs indeed, but aren't exactly "periodic" filters that would have a period/length parameter and their subsequent calculations. I won't go into fine-grained relationship details, but EMA and LERP are indeed related in approach, being cousins of similar pedigree.

EXAMINING LAGUERRE:

I focused firstly on US initialization obstacles at Pine's bar_index==0 with nz() in abundance. The next primary notion of intrigue I mostly wondered about was, why are there four LERP elements instead of fewer or more. Why not three or why not two LERPs, etc... 1-4-6-4-1, I remember seeing those coefficients before in high pass filters.

Gathering my thoughts from that highpass knowledge base, I devised other tapped configuration modes to inspect their behavior out of curiosity. Eureka! There is actually more to Laguerre than Ehlers' mind provided, now that I had formulated additional modes. Each mode exhibits it's own lag/smoothness characteristics better than the quad LERPed version. I narrowed it down to a total of 5 modes for exploration. Mode 0 is just the raw US by itself.

ANALYZING FILTER BEHAVIORS:

Which option might be possibly superior, and how may I determine that? Fortunately, I have a custom-built analyzer allowing me to thoroughly examine transient responses across multiple periodicities simultaneously, providing remarkable visual insights.

While Ehlers has meagerly touched upon presenting general frequency responses in his books, I have excelled far beyond that. This robust filter analysis capability enables me to observe finer aspects hidden to others, ultimately leading to the deprecation of numerous existing filters. Not only this, but inventing entirely new species of filtration whether lowpass, highpass, or bandpass is already possible with a thorough comprehensive evaluation.

Revealing what's quirky with each filter and having the ability to discover what filters may be lacking in performance, is one of it's implications. I'm just going to explain this: For example US has a little too much overshoot to my liking, along with nonconformant cutoff frequency compliance with the period parameter. Perhaps Ehlers should inspect US coefficients a bit closer... I hope stating this is not received in an ill manner, as it's not my intention here.

What this technically eludes to is that UltimateSmoother can be further improved, analogous to my Laguerre alterations described above. I will also state Laguerre can indeed be reformulated to an even greater extent concerning group delay, from what I have already discussed. Another exciting time though... More investigative research is warranted.

LAGUERRE CONCLUSIONS:

After analyzing Laguerre's frequency compliance, transient responses, amplitudes, lag, symmetry across periodicities, noise rejection, and smoothness... I favor mode 3 for a multitude of reasons over the mode 4 configuration, but mostly superb smoothing with less lag, AND I also appreciated mode 1 & 2 for it's lower lag performance options.

Each mode and lag (phase shift) damping value has it's own unique characteristics at extremes, yet they demonstrate additional finesse in it's new hybrid form without adding too much more complexity. This multicator has a bunch of Laguerre filters in the overlay chart over many periodicities so you can easily witness it's differing periodic symmetries on an input signal while adjusting lag and mode.

LAGUERRE OSCILLATOR:

The oscillator is integrated into the laguerreMulti() function for the intention of posterity only. I performed no evaluation on it, only providing the code in Pine. That wasn't part of my intended exploration adventure, as I'm more TREND oriented for the time being, focusing my efforts there.

Market analysis has two primary aspects in my observations, one cyclic while the other is trending dynamics... There's endless oscillators, but my expectations for trend analysis seems a little lesser explored in my opinion, hence my laborious trend endeavors. Ehlers provided both indicator facets this time around, and I hope you find the filtration aspect more intriguing after absorption of this reading.

FUNCTION MODULES EXPLAINED:

The Ultimate Smoother is an advanced IIR lowpass smoothing filter intended to minimize noise in time series data with minimal group delay, similar to a traditional biquad filter. This calculation helps to create a smoother version of the original signal without the distortions of short-term fluctuations and with minimal lag, adjustable by period.

The Modified Laguerre Lowpass Filter (MLLF) enhances the functionality of US by introducing a Laguerre mode parameter along side the lag parameter to refine control over the amount of additional smoothing/lag applied to the signal. By tethering US with this LERPed lag mechanism, MLLF achieves an effective balance between responsiveness and smoothness, allowing for customizable lag adjustments via multiple inputs. This filter ends with selecting from a choice of weighted averages derived from a gang of up to four cascading LERP calculations, resulting with smoother representations of the data.

The Laguerre Oscillator is a momentum-like indicator derived from the output of US and a singular LERPed lowpass filter. It calculates the difference between the US data and Laguerre filter data, normalizing it by the root mean square (RMS). This quasi-normalization technique helps to assess the intensity of the momentum on any timeframe within an expected bound range centered around 0.0. When the Laguerre Oscillator is positive, it suggests that the smoothed data is trending upward, while a negative value indicates a downward trend. Adjustability is controlled with period, lag, Laguerre mode, and RMS period.

MVRV Altcoins📌 Technical Description of Indicator: MVRV Altcoins

This advanced script calculates the Market Value to Realized Value (MVRV) ratio across multiple cryptocurrencies simultaneously. It offers two analytical modes: Normal and Z-Score, optimized for visual comparison and real-time monitoring of up to 13 predefined assets. If a user applies the indicator to a symbol that is not among the 13 programmed assets, the default behavior displays the Bitcoin chart as a fallback reference.

🔍 What Is MVRV and Why Is It Important?

MVRV is an on-chain metric designed to assess whether a cryptocurrency is overvalued or undervalued by comparing its market capitalization to its realized capitalization.

- Market Cap: The total circulating supply multiplied by the current market price.

- Realized Cap: The sum value of all coins based on the price at the time they last moved on-chain, offering a time-weighted valuation.

Normal Calculation:

MVRV_Normal = Market Cap / Realized Cap

This version reflects investor profitability and identifies potential accumulation or distribution zones.

📊 Z-Score Calculation:

MVRV_ZScore = (Market Cap − Realized Cap) / Standard Deviation of Market Cap

This formula evaluates how extreme the current market conditions are compared to historical norms. It normalizes the difference using statistical dispersion, turning it into a volatility-aware metric that better reflects valuation extremes.

🔎 How Market Cap Is Computed

Unlike conventional indicators relying on consolidated feeds, this script uses modular components from CoinMetrics to construct the active capitalization more accurately, especially for altcoins. Here's the breakdown:

Active Capitalization = MARKETCAPFF + MARKETCAPACTSPLY

Realized Capitalization = MARKETCAPREAL

Component Definitions:

- MARKETCAPFF: Market Cap Free Float — total valuation based only on truly circulating coins.

- MARKETCAPACTSPLY: Capitalization from actively circulating supply — filters dormant or locked coins.

- MARKETCAPREAL: Realized Cap — historical valuation weighted by the last on-chain movement of each coin.

This method offers enhanced precision and compatibility across assets that may lack comprehensive data from centralized providers.

⚙️ User-Configurable Parameters

- MVRV Mode: Choose between Normal and Z-Score.

- Percentage Scale View: If enabled, visual output is scaled using predefined divisors (100 / 3.5 or 100 / 6).

- Thresholds for Analysis:

- Normal mode: Define overbought and oversold levels (default 1.0 and 3.5).

- Z-Score mode: Configure statistical boundaries (default 0.0 and 6.0).

- Table Controls:

- Adjustable position on screen (9 options).

- Font size customization: tiny, small, normal, large.

- Color scheme personalization:

- Header: text and background

- Body: text and background

- Central column separator color

📊 Multicrypto Table Architecture

The indicator renders a high-performance visual table displaying data from up to 13 assets simultaneously. Each asset is represented as a vertical column featuring eigth historical data points plus the most recent value.

- Assets are displayed in two blocks separated by a decorative column.

- Each value is rounded to one decimal place for clarity.

- Cells are styled dynamically based on user settings.

🎨 Decorative Column Separator

Since the entire table is built as a unified structure, a color-configurable empty column is inserted mid-table to act as a visual divider. This approach improves readability and aesthetic balance without duplicating code or splitting table logic.

🔁 Default Behavior on Unsupported Assets

If the active chart is not one of the 13 predefined assets, the indicator will automatically display Bitcoin’s data. This ensures the chart remains functional and informative even outside the target asset group.

🎯 Color Interpretation by Condition

The MVRV value for each asset is highlighted using a traffic light system:

- Green: Undervalued (below oversold threshold)

- Red: Overvalued (above overbought threshold)

- Yellow: Neutral zone

This coding simplifies decision-making and visual scanning across assets.

Final Notes

This indicator is modular and fully adaptable, with well-commented sections designed for efficient customization. Its multiactive architecture makes it a valuable tool for crypto analysts tracking diversified portfolios beyond Bitcoin and Ethereum.

It supports visual storytelling across assets, comparative historical evaluation, and identification of strategic zones — whether for accumulation, distribution, or monitoring on-chain sentiment.

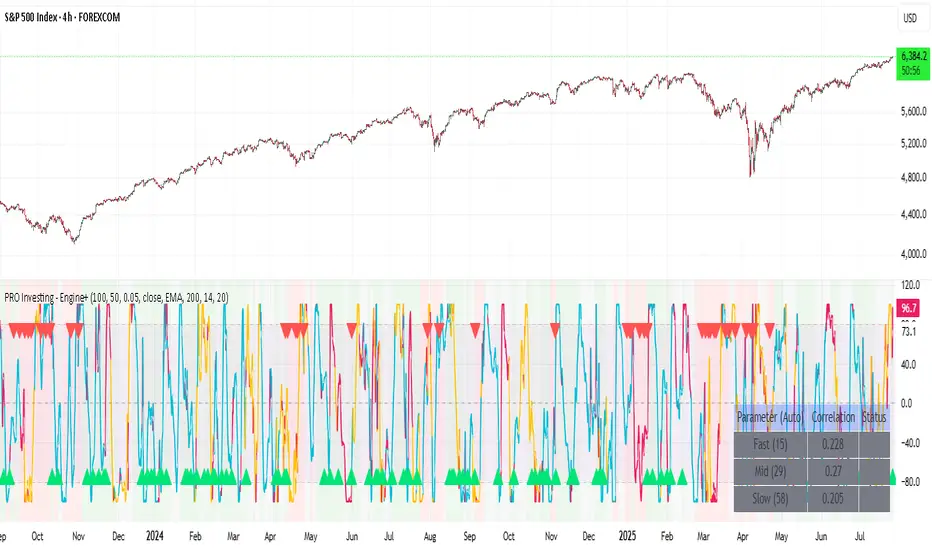

PRO Investing - Apex EnginePRO Investing - Apex Engine

1. Core Concept: Why Does This Indicator Exist?

Traditional momentum oscillators like RSI or Stochastic use a fixed "lookback period" (e.g., 14). This creates a fundamental problem: a 14-period setting that works well in a fast, trending market will generate constant false signals in a slow, choppy market, and vice-versa. The market's character is dynamic, but most tools are static.

The Apex Engine was built to solve this problem. Its primary innovation is a self-optimizing core that continuously adapts to changing market conditions. Instead of relying on one fixed setting, it actively tests three different momentum profiles (Fast, Mid, and Slow) in real-time and selects the one that is most synchronized with the current price action.

This is not just a random combination of indicators; it's a deliberate synthesis designed to create a more robust momentum tool. It combines:

Volatility analysis (ATR) to generate adaptive lookback periods.

Momentum measurement (ROC) to gauge the speed of price changes.

Statistical analysis (Correlation) to validate which momentum measurement is most effective right now.

Classic trend filters (Moving Average, ADX) to ensure signals are only taken in favorable market conditions.

The result is an oscillator that aims to be more responsive in volatile trends and more stable in quiet periods, providing a more intelligent and adaptive signal.

2. How It Works: The Engine's Three-Stage Process

To be transparent, it's important to understand the step-by-step logic the indicator follows on every bar. It's a process of Adapt -> Validate -> Signal.

Stage 1: Adapt (Dynamic Length Calculation)

The engine first measures market volatility using the Average True Range (ATR) relative to its own long-term average. This creates a volatility_factor. In high-volatility environments, this factor causes the base calculation lengths to shorten. In low-volatility, they lengthen. This produces three potential Rate of Change (ROC) lengths: dynamic_fast_len, dynamic_mid_len, and dynamic_slow_len.

Stage 2: Validate (Self-Optimizing Mode Selection)

This is the core of the engine. It calculates the ROC for all three dynamic lengths. To determine which is best, it uses the ta.correlation() function to measure how well each ROC's movement has correlated with the actual bar-to-bar price changes over the "Optimization Lookback" period. The ROC length with the highest correlation score is chosen as the most effective profile for the current moment. This "active" mode is reflected in the oscillator's color and the dashboard.

Stage 3: Signal (Normalized Velocity Oscillator)

The winning ROC series is then normalized into a consistent oscillator (the Velocity line) that ranges from -100 (extreme oversold) to +100 (extreme overbought). This ensures signals are comparable across any asset or timeframe. Signals are only generated when this Velocity line crosses its signal line and the trend filters (explained below) give a green light.

3. How to Use the Indicator: A Practical Guide

Reading the Visuals:

Velocity Line (Blue/Yellow/Pink): The main oscillator line. Its color indicates which mode is active (Fast, Mid, or Slow).

Signal Line (White): A moving average of the Velocity line. Crossovers generate potential signals.

Buy/Sell Triangles (▲ / ▼): These are your primary entry signals. They are intentionally strict and only appear when momentum, trend, and price action align.

Background Color (Green/Red/Gray): This is your trend context.

Green: Bullish trend confirmed (e.g., price above a rising 200 EMA and ADX > 20). Only Buy signals (▲) can appear.

Red: Bearish trend confirmed. Only Sell signals (▼) can appear.

Gray: No clear trend. The market is likely choppy or consolidating. No signals will appear; it is best to stay out.

Trading Strategy Example:

Wait for a colored background. A green or red background indicates the market is in a tradable trend.

Look for a signal. For a green background, wait for a lime Buy triangle (▲) to appear.

Confirm the trade. Before entering, confirm the signal aligns with your own analysis (e.g., support/resistance levels, chart patterns).

Manage the trade. Set a stop-loss according to your risk management rules. An exit can be considered on a fixed target, a trailing stop, or when an opposing signal appears.

4. Settings and Customization

This script is open-source, and its settings are transparent. You are encouraged to understand them.

Synaptic Engine Group:

Volatility Period: The master control for the adaptive engine. Higher values are slower and more stable.

Optimization Lookback: How many bars to use for the correlation check.

Switch Sensitivity: A buffer to prevent frantic switching between modes.

Advanced Configuration & Filters Group:

Price Source: The data source for momentum calculation (default close).

Trend Filter MA Type & Length: Define your long-term trend.

Filter by MA Slope: A key feature. If ON, allows for "buy the dip" entries below a rising MA. If OFF, it's stricter, requiring price to be above the MA.

ADX Length & Threshold: Filters out non-trending, choppy markets. Signals will not fire if the ADX is below this threshold.

5. Important Disclaimer

This indicator is a decision-support tool for discretionary traders, not an automated trading system or financial advice. Past performance is not indicative of future results. All trading involves substantial risk. You should always use proper risk management, including setting stop-losses, and never risk more than you are prepared to lose. The signals generated by this script should be used as one component of a broader trading plan.

RSI with Williams %R Coloringsimple fusion of RSI to seek divergence and williams % R coloring to see overbought/oversold price.

not my own work, just merely took two standard indicators and infused them.

Cross-Correlation Lead/Lag AnalyzerCross-Correlation Lead/Lag Analyzer (XCorr)

Discover which instrument moves first with advanced cross-correlation analysis.

This indicator analyzes the lead/lag relationship between any two financial instruments using rolling cross-correlation at multiple time offsets. Perfect for pairs trading, market timing, and understanding inter-market relationships.

Key Features:

Universal compatibility - Works with any two symbols (stocks, futures, forex, crypto, commodities)

Multi-timeframe analysis - Automatically adjusts lag periods based on your chart timeframe

Real-time correlation table - Shows current correlation values for all lag scenarios

Visual lead/lag detection - Color-coded plots make it easy to spot which instrument leads

Smart "Best" indicator - Automatically identifies the strongest relationship

How to Use:

Set your symbols in the indicator settings (default: NQ1! vs RTY1!)

Adjust correlation length (default: 20 periods for smooth but responsive analysis)

Watch the colored lines:

• Red/Orange: Symbol 2 leads Symbol 1 by 1-2 periods

• Blue: Instruments move simultaneously

• Green/Purple: Symbol 1 leads Symbol 2 by 1-2 periods

Check the table for exact correlation values and the "Best" relationship

Interpreting Results:

Correlation > 0.7: Strong positive relationship

Correlation 0.3-0.7: Moderate relationship

Correlation < 0.3: Weak/no relationship

Highest line indicates the optimal timing relationship

Popular Use Cases:

Index Futures : NQ vs ES, RTY vs IWM

Sector Rotation : XLF vs XLK, QQQ vs SPY

Commodities : GC vs SI, CL vs NG

Currency Pairs : EURUSD vs GBPUSD

Crypto : BTC vs ETH correlation analysis

Technical Notes:

Cross-correlation measures linear relationships between two time series at different time lags. This implementation uses Pearson correlation with adjustable periods, calculating correlations from -2 to +2 period offsets to detect leading/lagging behavior.

Perfect for quantitative analysts, pairs traders, and anyone studying inter-market relationships.

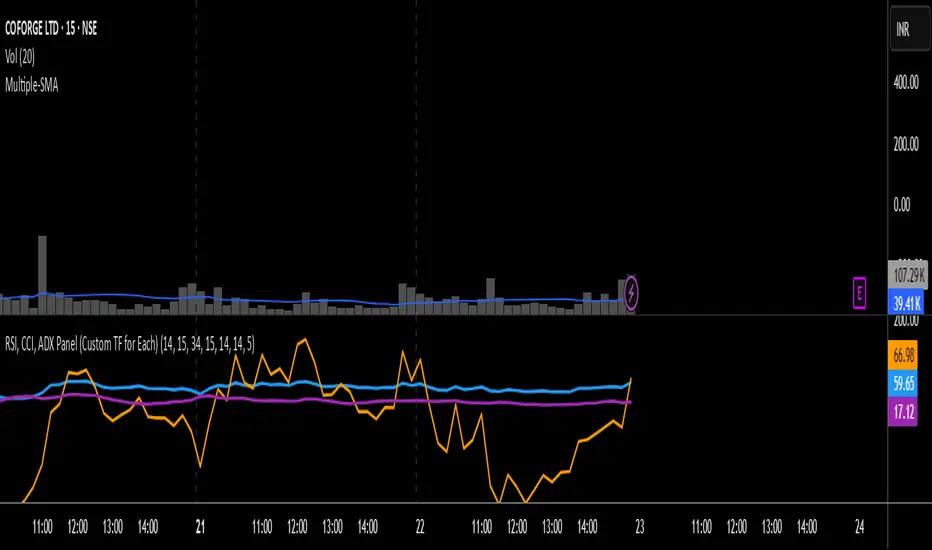

RSI, CCI, ADX Panel (Custom TF for Each)RSI, CCI, and ADX Combined – Multi-Timeframe, Fully Customizable Panel Indicator for TradingView

Overview

This Pine Script indicator integrates the Relative Strength Index (RSI), Commodity Channel Index (CCI), and Average Directional Index (ADX) into a single, clean panel for effortless technical analysis. Each indicator operates independently, with customizable length, smoothing, and time frame for maximum flexibility. Traders can now monitor momentum, trend strength, and overbought/oversold conditions across different time frames—all in one place.

Key Features

Independent Controls: Set length, smoothing (ADX), and time frame individually for each indicator via the settings panel.

Multi-Timeframe Support: Each oscillator (RSI, CCI, ADX) can be calculated on its own time frame, enabling nuanced inter-timeframe analysis.

Customizable Visualization: Adjust line color and thickness for each indicator to match your chart style.

Clean, Non-Overlay Display: All three indicators are plotted in a dedicated panel beneath the price chart, reducing clutter.

Reference Levels: Includes standard reference lines for oversold/overbought (RSI, CCI) and trend threshold (ADX) for quick visual cues.

Usage Ideas

Swing Trading: Compare short- and long-term momentum using different time frames for RSI, CCI, and ADX.

Trend Confirmation: Use ADX to filter RSI and CCI signals—only trade overbought/oversold conditions during strong trends.

Divergence Hunting: Spot divergences between time frames for early reversal signals.

Scalping: Set RSI and CCI to lower time frames for entry, while monitoring higher timeframe ADX for trend context.

How to Install

Paste the script into the Pine Editor on TradingView.

Add to chart. Adjust settings as desired.

Save as a template for quick reuse on any chart—all your custom settings will be preserved.

Customization

Edit lengths and time frames in the indicator’s settings dialog.

Toggle reference lines on/off as needed.

Fine-tune line appearance (color, thickness) for clarity.

Note:

This indicator does not provide automated buy/sell signals. It is a customizable analytical tool for manual or semi-automated trading. Use in combination with other technical or fundamental analysis for best results.

Combine Momentum, Trend, and Volatility—Seamlessly and Visually—With One Indicator.