V3 Valentini Pro Scalper [Dashboard]Gemini 3.0 pro's take on Fabio Valentini's world #1 strategy scalp 12/19/2025

Model

Forecasting Quadratic Regression [UPDATED V6] Forecasting Quadratic Regression applies a second-degree polynomial regression model to price data, offering a non-linear alternative to traditional linear regression. By fitting a quadratic curve of the form:

y=a+bx+cx2

the indicator captures both directional trend and curvature, allowing traders to detect momentum shifts earlier than with straight-line models.

🔹 Core Features

Fits a quadratic regression curve to user-defined lookback periods

Extends the fitted curve forward to generate forecast projections

Calculates slope curvature to highlight trend acceleration or deceleration

Adapts dynamically as new bars are added

🔹 Trading Applications

Identify potential reversal zones when the curve inflects (2nd derivative sign change)

Forecast near-term mean reversion targets or extended trend continuations

Filter trades by measuring momentum curvature rather than linear slope

Visualize higher-order structure in price beyond standard regression lines

⚠️ Note: This model is statistical and assumes past curvature informs short-term future price paths. It should be combined with confirmation signals (volume, oscillators, support/resistance) to reduce false inflection points.

Bitcoin Expectile Model [LuxAlgo]The Bitcoin Expectile Model is a novel approach to forecasting Bitcoin, inspired by the popular Bitcoin Quantile Model by PlanC. By fitting multiple Expectile regressions to the price, we highlight zones of corrections or accumulations throughout the Bitcoin price evolution.

While we strongly recommend using this model with the Bitcoin All Time History Index INDEX:BTCUSD on the 3 days or weekly timeframe using a logarithmic scale, this model can be applied to any asset using the daily timeframe or superior.

Please note that here on TradingView, this model was solely designed to be used on the Bitcoin 1W chart, however, it can be experimented on other assets or timeframes if of interest.

🔶 USAGE

The Bitcoin Expectile Model can be applied similarly to models used for Bitcoin, highlighting lower areas of possible accumulation (support) and higher areas that allow for the anticipation of potential corrections (resistance).

By default, this model fits 7 individual Expectiles Log-Log Regressions to the price, each with their respective expectile ( tau ) values (here multiplied by 100 for the user's convenience). Higher tau values will return a fit closer to the higher highs made by the price of the asset, while lower ones will return fits closer to the lower prices observed over time.

Each zone is color-coded and has a specific interpretation. The green zone is a buy zone for long-term investing, purple is an anomaly zone for market bottoms that over-extend, while red is considered the distribution zone.

The fits can be extrapolated, helping to chart a course for the possible evolution of Bitcoin prices. Users can select the end of the forecast as a date using the "Forecast End" setting.

While the model is made for Bitcoin using a log scale, other assets showing a tendency to have a trend evolving in a single direction can be used. See the chart above on QQQ weekly using a linear scale as an example.

The Start Date can also allow fitting the model more locally, rather than over a large range of prices. This can be useful to identify potential shorter-term support/resistance areas.

🔶 DETAILS

🔹 On Quantile and Expectile Regressions

Quantile and Expectile regressions are similar; both return extremities that can be used to locate and predict prices where tops/bottoms could be more likely to occur.

The main difference lies in what we are trying to minimize, which, for Quantile regression, is commonly known as Quantile loss (or pinball loss), and for Expectile regression, simply Expectile loss.

You may refer to external material to go more in-depth about these loss functions; however, while they are similar and involve weighting specific prices more than others relative to our parameter tau, Quantile regression involves minimizing a weighted mean absolute error, while Expectile regression minimizes a weighted squared error.

The squared error here allows us to compute Expectile regression more easily compared to Quantile regression, using Iteratively reweighted least squares. For Quantile regression, a more elaborate method is needed.

In terms of comparison, Quantile regression is more robust, and easier to interpret, with quantiles being related to specific probabilities involving the underlying cumulative distribution function of the dataset; on the other expectiles are harder to interpret.

🔹 Trimming & Alterations

It is common to observe certain models ignoring very early Bitcoin price ranges. By default, we start our fit at the date 2010-07-16 to align with existing models.

By default, the model uses the number of time units (days, weeks...etc) elapsed since the beginning of history + 1 (to avoid NaN with log) as independent variable, however the Bitcoin All Time History Index INDEX:BTCUSD do not include the genesis block, as such users can correct for this by enabling the "Correct for Genesis block" setting, which will add the amount of missed bars from the Genesis block to the start oh the chart history.

🔶 SETTINGS

Start Date: Starting interval of the dataset used for the fit.

Correct for genesis block: When enabled, offset the X axis by the number of bars between the Bitcoin genesis block time and the chart starting time.

🔹 Expectiles

Toggle: Enable fit for the specified expectile. Disabling one fit will make the script faster to compute.

Expectile: Expectile (tau) value multiplied by 100 used for the fit. Higher values will produce fits that are located near price tops.

🔹 Forecast

Forecast End: Time at which the forecast stops.

🔹 Model Fit

Iterations Number: Number of iterations performed during the reweighted least squares process, with lower values leading to less accurate fits, while higher values will take more time to compute.

Profitable Loser Model [MMT]Profitable Loser Model

Overview

The Profitable Loser Model is a powerful PineScript v6 indicator designed to enhance your trading by visualizing key price levels, session open zones, Fibonacci retracements, and premium/discount zones. This overlay indicator provides traders with a customizable toolkit to analyze market structure across any timeframe, making it ideal for intraday and swing trading strategies.

Features

Open Zone Visualization

- Plots a box based on the open and close of the first candle in a user-defined timeframe (default: 5-minute).

- Customizable box color, projection offset, and label size (Tiny, Small, Normal, Large).

- Displays a timeframe label (e.g., "5m Open Zone") for quick reference, toggleable on/off.

Session Open Lines

- Optionally draws horizontal lines at key session opens (8:30 AM, 9:30 AM, 1:30 PM, Midnight, New York time).

- Customize line color, style (Solid, Dashed, Dotted), width, and label size for each session.

- Perfect for identifying critical intraday price levels.

Premium and Discount Zones

- Highlights premium (above midpoint) and discount (below midpoint) zones based on session high/low.

- Toggleable with customizable colors and projection offsets.

- Helps traders spot overbought/oversold areas for potential mean-reversion trades.

Fibonacci Retracement Levels

- Plots user-defined Fibonacci levels (default: 0.23, 0.35, 0.5, 0.62, 0.705, 0.79, 0.886, 1, 1.1).

- Customizable line style, width, color, and labels (showing percentage and/or price).

- Dynamically adjusts based on price movement relative to the open zone.

Take Profit (TP) and Stop Loss (SL) Levels

- Highlights TP (default: 0.23) and SL (default: 1.1) Fibonacci levels with distinct colors.

- Fully customizable to align with your risk-reward strategy.

How It Works

- Session Detection : Resets daily (or per user-defined timeframe) to capture the first candle's open, high, low, and close.

- Open Zone : Draws a box between the open and close, extended forward by the projection offset.

- Session Lines : Plots lines at specified session opens with customizable styles and labels.

- Fibonacci Retracement : Adjusts levels dynamically based on session high/low and price action.

- Premium/Discount Zones : Calculated from the session range midpoint, updated in real-time.

Settings

- Open Zone :

- Timeframe (default: 5m), Calculate Timeframe (default: Daily).

- Toggle label, adjust size, box color, and projection offset.

- Session Open Lines :

- Enable/disable lines for 8:30 AM, 9:30 AM, 1:30 PM, Midnight.

- Customize color, style, width, label size, and vertical offset.

- Premium/Discount Zones :

- Toggle visibility, set colors, and adjust projection offset.

- Fibonacci Retracement :

- Toggle visibility, set custom levels, line style, width, color, and label options.

- Adjust projection offset.

- TP/SL :

- Set TP/SL Fibonacci levels and colors.

Use Cases

- Intraday Trading : Use session open lines and open zones to trade key market hours.

- Swing Trading : Leverage Fibonacci levels for potential reversal or continuation zones.

- Risk Management : Set precise TP/SL levels based on Fibonacci retracements.

- Market Structure : Identify overbought/oversold zones with premium/discount areas.

Notes

- Optimized with `dynamic_requests = true` for efficient real-time data handling.

- Visual elements (boxes, lines, labels) are cleaned up at the start of each new session.

- Session lines use New York time (`America/New_York`) for alignment with major markets.

Bitcoin Power Law [LuxAlgo]The Bitcoin Power Law tool is a representation of Bitcoin prices first proposed by Giovanni Santostasi, Ph.D. It plots BTCUSD daily closes on a log10-log10 scale, and fits a linear regression channel to the data.

This channel helps traders visualise when the price is historically in a zone prone to tops or located within a discounted zone subject to future growth.

🔶 USAGE

Giovanni Santostasi, Ph.D. originated the Bitcoin Power-Law Theory; this implementation places it directly on a TradingView chart. The white line shows the daily closing price, while the cyan line is the best-fit regression.

A channel is constructed from the linear fit root mean squared error (RMSE), we can observe how price has repeatedly oscillated between each channel areas through every bull-bear cycle.

Excursions into the upper channel area can be followed by price surges and finishing on a top, whereas price touching the lower channel area coincides with a cycle low.

Users can change the channel areas multipliers, helping capture moves more precisely depending on the intended usage.

This tool only works on the daily BTCUSD chart. Ticker and timeframe must match exactly for the calculations to remain valid.

🔹 Linear Scale

Users can toggle on a linear scale for the time axis, in order to obtain a higher resolution of the price, (this will affect the linear regression channel fit, making it look poorer).

🔶 DETAILS

One of the advantages of the Power Law Theory proposed by Giovanni Santostasi is its ability to explain multiple behaviors of Bitcoin. We describe some key points below.

🔹 Power-Law Overview

A power law has the form y = A·xⁿ , and Bitcoin’s key variables follow this pattern across many orders of magnitude. Empirically, price rises roughly with t⁶, hash-rate with t¹² and the number of active addresses with t³.

When we plot these on log-log axes they appear as straight lines, revealing a scale-invariant system whose behaviour repeats proportionally as it grows.

🔹 Feedback-Loop Dynamics

Growth begins with new users, whose presence pushes the price higher via a Metcalfe-style square-law. A richer price pool funds more mining hardware; the Difficulty Adjustment immediately raises the hash-rate requirement, keeping profit margins razor-thin.

A higher hash rate secures the network, which in turn attracts the next wave of users. Because risk and Difficulty act as braking forces, user adoption advances as a power of three in time rather than an unchecked S-curve. This circular causality repeats without end, producing the familiar boom-and-bust cadence around the long-term power-law channel.

🔹 Scale Invariance & Predictions

Scale invariance means that enlarging the timeline in log-log space leaves the trajectory unchanged.

The same geometric proportions that described the first dollar of value can therefore extend to a projected million-dollar bitcoin, provided no catastrophic break occurs. Institutional ETF inflows supply fresh capital but do not bend the underlying slope; only a persistent deviation from the line would falsify the current model.

🔹 Implications

The theory assigns scarcity no direct role; iterative feedback and the Difficulty Adjustment are sufficient to govern Bitcoin’s expansion. Long-term valuation should focus on position within the power-law channel, while bubbles—sharp departures above trend that later revert—are expected punctuations of an otherwise steady climb.

Beyond about 2040, disruptive technological shifts could alter the parameters, but for the next order of magnitude the present slope remains the simplest, most robust guide.

Bitcoin behaves less like a traditional asset and more like a self-organising digital organism whose value, security, and adoption co-evolve according to immutable power-law rules.

🔶 SETTINGS

🔹 General

Start Calculation: Determine the start date used by the calculation, with any prior prices being ignored. (default - 15 Jul 2010)

Use Linear Scale for X-Axis: Convert the horizontal axis from log(time) to linear calendar time

🔹 Linear Regression

Show Regression Line: Enable/disable the central power-law trend line

Regression Line Color: Choose the colour of the regression line

Mult 1: Toggle line & fill, set multiplier (default +1), pick line colour and area fill colour

Mult 2: Toggle line & fill, set multiplier (default +0.5), pick line colour and area fill colour

Mult 3: Toggle line & fill, set multiplier (default -0.5), pick line colour and area fill colour

Mult 4: Toggle line & fill, set multiplier (default -1), pick line colour and area fill colour

🔹 Style

Price Line Color: Select the colour of the BTC price plot

Auto Color: Automatically choose the best contrast colour for the price line

Price Line Width: Set the thickness of the price line (1 – 5 px)

Show Halvings: Enable/disable dotted vertical lines at each Bitcoin halving

Halvings Color: Choose the colour of the halving lines

Excess Liquidity IndicatorExcess Liquidity Indicator

This script visualizes excess liquidity trends in relation to risk assets. It estimates excess liquidity by combining various macroeconomic factors such as WW M2 money supply, central bank balance sheets, and interest rates, oil, and the dollar index, and it substracts WW GDP. The tool helps traders analyze liquidity-driven market trends in a structured manner.

Note: This script is for research purposes only and does not provide financial advice.

I cannot point names cause I get banned but work is inspired by others...

Market Structure Targets Model [LuxAlgo]The Market Structure Targets Model indicator provides an algorithmic approach to setting targets from market structure shifts (MSS) and market structure breaks (MSB), two popular Smart Money Concept (SMC) concepts. Depending on the target % settings, they can be used as take profit, confirmation levels, or potential reversal points.

🔶 USAGE

Our Market Structure Targets Model scripts provide automated and customizable targets from MSS and MSB. Each displayed target can be used in several ways described in the sub-sections below:

🔹 Take Profit

The targets can be used as take profit levels, where the target distance can be set separately for bullish/bearish MSS/MSB respectively.

🔹 Confirmation Levels

Alternatively, targets can be used as an additional confirmation level of a trend reversal when set at a lower percentage, filtering out fake signals that might be given from market structures. In this way, targets can be used as potential entry levels.

🔹 Potential Reversal Points

In some circumstances, targets being reached can be indicative of trend reversals. The percentage of the targets would be typically set higher to allow for trend exhaustion.

The above examples highlight this usage for bearish reversal scenarios, while the image below highlights it for bullish reversal scenarios.

🔹 Support/Resistance Levels

The targets, being horizontal levels, can also serve as potential support/resistances, with breakouts potentially confirming new trends. It is important to remain observant of the market structure. An MSS or MSB in the opposite direction provides essential information to be included in future decisions.

Using multiple timeframes can help detect longer-term trends. Depending on the user's preference, they can choose the appropriate timeframe for their needs.

Note that Target lines will only be drawn when the Target Level exceeds the close value when it is drawn.

🔹 Maximum Target Duration

The Maximum Target Duration setting removes unreached target levels when the amount of bars since the associated market structure of that target exceeds the user set limit. This effectively allows the removal of any target that might no longer be relevant to newer trends.

🔹 Type: Switch/Hold

This setting is another way to control unreached target levels.

Switch: When a new MSS/MSB is found, the previous target level associated with a market structure with the same direction (bullish/bearish) is deleted if it hasn't been reached.

Hold: Target levels are retained and continuously evaluated when a new MSS/MSB is formed.

The target level will be removed in both cases when the Maximum Target Duration condition is applied.

The above example shows the case when the Type setting is set to Switch , while in the example below, it is set to Hold .

🔶 DETAILS

🔹 Market Structure

Market structures are commonly classified as follows:

Market Structure Shift (MSS), also referred to as Change of Character (CHoCH)

Market Structure Break (MSB), also referred to as Break of Structure (BOS)

MSS indicates a shift in the market trend, confirming trend reversals. Conversely, MSB occurs once a trend is already determined, confirming new higher highs/lower lows.

🔹 Targets

A: Highest/lowest between the extremities of the MSS/MSB line

B: Price value of the MSS/MSB line

The distance between A and B is projected on the opposite side of the MSS/MSB line, adjusted with a percentage that can be set by the user. The above example used 100% of the distance between A and B.

The Target Percentage of MSS and MSB can be set separately for bullish or bearish market structures.

🔶 SETTINGS

Swings: Period used for the swing detection, with higher values returning longer-term Swing Levels.

Type: the Switch/Hold setting controls unattained target levels

Maximum Target Duration: removes the target lines when the amount of bars since the drawing of the target exceeds the limit and the target has not been reached

🔹 Market Structure Shift (MSS)

Bullish: Toggle, color setting, % Target

Bearish: Toggle, color setting, % Target

🔹 Market Structure Break (MSB)

Bullish: Toggle, color setting, % Target

Bearish: Toggle, color setting, % Target

Returns Model by TenozenHey there! I've been diving into the book "Paul Wilmott on Quantitative Finance," and I stumbled upon this cool model for calculating and modeling returns. Basically, it helps us figure out how much a price has changed over a set number of periods—I like to use 20 periods as a default. Once we get that rate of change value, we crunch some numbers to find the standard deviation and mean using all the historical data we have. That's the foundation of this model.

Now, let's talk about how to use it. This model shows us how returns and price behavior are connected. When returns hang out in the +1 to +2 standard deviation range, it usually means returns are about to drop, and vice versa. Often, this leads to corresponding price moves. But here's the thing: sometimes prices don't do what we expect. Why? It's because there's another hidden factor at play—I like to call it "power."

This "power" isn't something we can see directly, but it's there. Basically, when returns are within that standard deviation range, the market faces resistance when trying to move in its preferred direction, whether bullish or bearish. The strength of this "power" determines if the market will snap back to the average or go for a wild ride. It can show up as small price wiggles, big price jumps, or lightning-fast moves. By understanding this "power," we can get a better handle on what the market might do next and avoid getting blindsided. In the meantime, I couldn't explain "power" yet, but In the future, when I've learned enough, I'd love to share the model with you guys!

So... I'm planning to explore and share more models from this book as I learn, even if those pesky math formulas can be tough to crack. I hope you find this indicator as helpful as I do, and if you've got any suggestions or feedback, please feel free to share! Ciao!

[TTI] MarketSmith & IBD Style Model Stock Quarters 📜 ––––HISTORY & CREDITS––––

The MarketSmith & IBD Style Model Stock Quarters another Utility indicator is an original creation by TintinTrading inspired by Investor's Business Daily and William O'Neil style of presenting information. While going through the Model Stocks that IBD has been publishing, I realized that I wanted to see the exam same Quarterly presentation on the time axis in order to compare William O'Neil notes better with my own notes from Tradingview. The script is simple and could help you if you study the CANSLIM methodology.

🦄 –––UNIQUENESS–––

The distinctiveness of this indicator lies in its ability to visually delineate stock quarters directly on the price chart. It serves as a handy tool for traders who adopt a quarterly review of stock performance, in line with MarketSmith and IBD's analysis frameworks.

🛠️ ––––WHAT IT DOES––––

Quarter Marking : Draws a black line at the beginning of each financial quarter (January, April, July, and October).

Quarter Labeling : Places a label at the close of the last month in a quarter, indicating the upcoming quarter with its abbreviation and the last two digits of the year.

💡 ––––HOW TO USE IT––––

👉Installation: Add the indicator to your TradingView chart by searching for " MarketSmith & IBD Style Model Stock Quarters" in the indicator library.

👉Add to New Pane and squash the Pane Length: I add the indicator to a new pane under the price and volume charts and squash the height of the pane so that it looks exactly like the MarketSmith visuals.

👉Visual Cues:

Look for the black lines marking the start of a new quarter.

Observe the labels indicating the upcoming quarter and year, positioned at the close of the last month in a quarter.

👉Interpretation: Use these quarterly markers to align your trading strategies with quarterly performance metrics or to conduct seasonal analysis.

👉Settings: The indicator does not require any user-defined settings, making it straightforward to use.

Normal Distribution CurveThis Normal Distribution Curve is designed to overlay a simple normal distribution curve on top of any TradingView indicator. This curve represents a probability distribution for a given dataset and can be used to gain insights into the likelihood of various data levels occurring within a specified range, providing traders and investors with a clear visualization of the distribution of values within a specific dataset. With the only inputs being the variable source and plot colour, I think this is by far the simplest and most intuitive iteration of any statistical analysis based indicator I've seen here!

Traders can quickly assess how data clusters around the mean in a bell curve and easily see the percentile frequency of the data; or perhaps with both and upper and lower peaks identify likely periods of upcoming volatility or mean reversion. Facilitating the identification of outliers was my main purpose when creating this tool, I believed fixed values for upper/lower bounds within most indicators are too static and do not dynamically fit the vastly different movements of all assets and timeframes - and being able to easily understand the spread of information simplifies the process of identifying key regions to take action.

The curve's tails, representing the extreme percentiles, can help identify outliers and potential areas of price reversal or trend acceleration. For example using the RSI which typically has static levels of 70 and 30, which will be breached considerably more on a less liquid or more volatile asset and therefore reduce the actionable effectiveness of the indicator, likewise for an asset with little to no directional volatility failing to ever reach this overbought/oversold areas. It makes considerably more sense to look for the top/bottom 5% or 10% levels of outlying data which are automatically calculated with this indicator, and may be a noticeable distance from the 70 and 30 values, as regions to be observing for your investing.

This normal distribution curve employs percentile linear interpolation to calculate the distribution. This interpolation technique considers the nearest data points and calculates the price values between them. This process ensures a smooth curve that accurately represents the probability distribution, even for percentiles not directly present in the original dataset; and applicable to any asset regardless of timeframe. The lookback period is set to a value of 5000 which should ensure ample data is taken into calculation and consideration without surpassing any TradingView constraints and limitations, for datasets smaller than this the indicator will adjust the length to just include all data. The labels providing the percentile and average levels can also be removed in the style tab if preferred.

Additionally, as an unplanned benefit is its applicability to the underlying price data as well as any derived indicators. Turning it into something comparable to a volume profile indicator but based on the time an assets price was within a specific range as opposed to the volume. This can therefore be used as a tool for identifying potential support and resistance zones, as well as areas that mark market inefficiencies as price rapidly accelerated through. This may then give a cleaner outlook as it eliminates the potential drawbacks of volume based profiles that maybe don't collate all exchange data or are misrepresented due to large unforeseen increases/decreases underlying capital inflows/outflows.

Thanks to @ALifeToMake, @Bjorgum, vgladkov on stackoverflow (and possibly some chatGPT!) for all the assistance in bringing this indicator to life. I really hope every user can find some use from this and help bring a unique and data driven perspective to their decision making. And make sure to please share any original implementaions of this tool too! If you've managed to apply this to the average price change once you've entered your position to better manage your trade management, or maybe overlaying on an implied volatility indicator to identify potential options arbitrage opportunities; let me know! And of course if anyone has any issues, questions, queries or requests please feel free to reach out! Thanks and enjoy.

Harmonic Sine Waves model plot Hey,

Here is another tool that I created. I could not find anything similar.

This script is creating a sine wave, based on the given length, amplitude, horizontal vertical offset.

After this it plots also nearest harmonics to the base sine wave and draws it on the chart.

At the last step it sums up the value for base sine wave with its harmonics.

This is a great way to experience how 4 basic sine waves, when summed up, are creating more complex chart.

This shows that the 'chaotic' chart can be built on just a few most important factors.

You do not have to "know every single fact" about the asset to make a proper forecast.

You just need those most important.

It is crucial though, to offset the chart in a correct way, so it is in phase with the asset that we work on.

FunctionBlackScholesLibrary "FunctionBlackScholes"

Some methods for the Black Scholes Options Model, which demonstrates several approaches to the valuation of a European call.

// reference:

// people.math.sc.edu

// people.math.sc.edu

asset_path(s0, mu, sigma, t1, n) Simulates the behavior of an asset price over time.

Parameters:

s0 : float, asset price at time 0.

mu : float, growth rate.

sigma : float, volatility.

t1 : float, time to expiry date.

n : int, time steps to expiry date.

Returns: option values at each equal timed step (0 -> t1)

binomial(s0, e, r, sigma, t1, m) Uses the binomial method for a European call.

Parameters:

s0 : float, asset price at time 0.

e : float, exercise price.

r : float, interest rate.

sigma : float, volatility.

t1 : float, time to expiry date.

m : int, time steps to expiry date.

Returns: option value at time 0.

bsf(s0, t0, e, r, sigma, t1) Evaluates the Black-Scholes formula for a European call.

Parameters:

s0 : float, asset price at time 0.

t0 : float, time at which the price is known.

e : float, exercise price.

r : float, interest rate.

sigma : float, volatility.

t1 : float, time to expiry date.

Returns: option value at time 0.

forward(e, r, sigma, t1, nx, nt, smax) Forward difference method to value a European call option.

Parameters:

e : float, exercise price.

r : float, interest rate.

sigma : float, volatility.

t1 : float, time to expiry date.

nx : int, number of space steps in interval (0, L).

nt : int, number of time steps.

smax : float, maximum value of S to consider.

Returns: option values for the european call, float array of size ((nx-1) * (nt+1)).

mc(s0, e, r, sigma, t1, m) Uses Monte Carlo valuation on a European call.

Parameters:

s0 : float, asset price at time 0.

e : float, exercise price.

r : float, interest rate.

sigma : float, volatility.

t1 : float, time to expiry date.

m : int, time steps to expiry date.

Returns: confidence interval for the estimated range of valuation.

vix_vx_regressionAn example of the linear regression library, showing the regression of VX futures on the VIX. The beta might help you weight VX futures when hedging SPX vega exposure. A VX future has point multiplier of 1000, whereas SPX options have a point multiplier of 100. Suppose the front month VX future has a beta of 0.6 and the front month SPX straddle has a vega of 8.5. Using these approximations, the VX future will underhedge the SPX straddle, since (0.6 * 1000) < (8.5 * 100). The position will have about 2.5 ($250) vega. Use the R^2 (coefficient of determination) to check how well the model fits the relationship between VX and VIX. The further from one this value, the less useful the model.

(Note that the mini, VXM futures also have a 100 point multiplier).

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

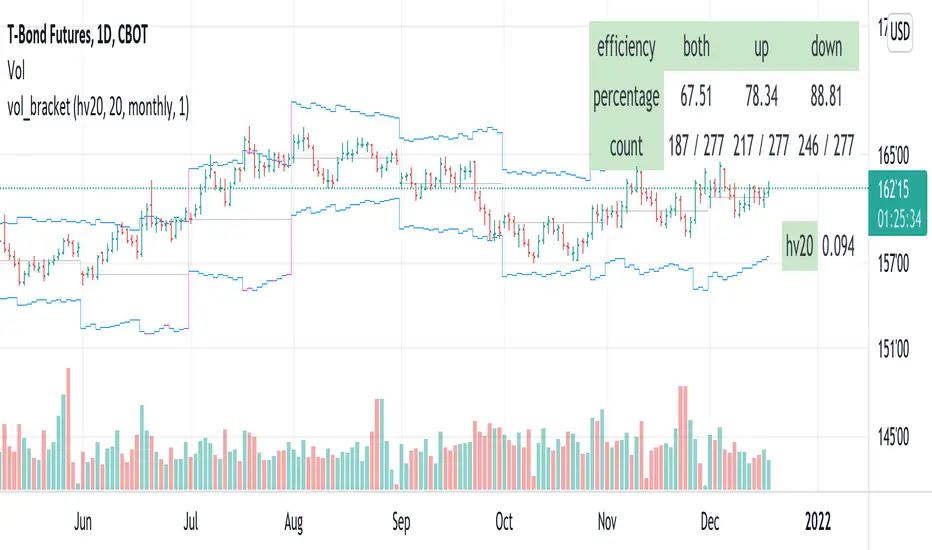

vol_bracketThis simple script shows an "N" standard deviation volatility bracket, anchored at the opening price of the current month, week, or quarter. This anchor is meant to coincide roughly with the expiration of options issued at the same interval. You can choose between a manually-entered IV or the hv30 volatility model.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

Fourier series Model Of The Market█ OVERVIEW

The Fourier Series Model of the Market (FSMM) decomposes price action into harmonic components using bandpass filtering, then reconstructs a composite wave weighted by rolling energy ratios. This approach isolates cyclical market behavior at multiple frequencies, emphasizing dominant cycles for cleaner signal generation. The energy-adaptive weighting is the key differentiator from simple harmonic summation: cycles that dominate current price action contribute more to the output.

Based on Fourier analysis principles applied to financial markets, the indicator extracts harmonics (fundamental, 2nd, 3rd, etc.) using second-order IIR bandpass filters, then weights each harmonic's contribution by its relative energy compared to adjacent harmonics. This energy-adaptive weighting naturally emphasizes the cycles that are most prominent in current market conditions.

█ CONCEPTS

Fourier Decomposition

Fourier analysis represents any periodic signal as a sum of sine waves at different frequencies. In market analysis, price action can be decomposed into a fundamental cycle (the base period) plus harmonics at integer multiples of that frequency (period/2, period/3, etc.). Each harmonic captures oscillations at a specific frequency band, and their sum reconstructs the original cyclical behavior.

Bandpass Filtering

Each harmonic is extracted using a second-order IIR (Infinite Impulse Response) bandpass filter tuned to that harmonic's frequency. The filter isolates price activity within a narrow frequency range while rejecting both higher-frequency noise and lower-frequency trend drift. Before filtering, the source is debiased via 2-bar momentum to remove DC offset, ensuring each bandpass operates around true zero.

Energy-Weighted Reconstruction

Rather than simply summing all harmonics equally, FSMM weights each harmonic by its rolling energy relative to the previous harmonic. The energy score combines the current harmonic value with its rate of change, so it reflects both amplitude and momentum. Higher harmonics that hold comparatively more energy therefore contribute more to the composite wave, while weaker harmonics fade out. This adaptive weighting allows the model to respond to changing market cyclicality.

Quadrature Component (Rate of Change)

The rate of change output represents the 90°-phase-shifted (quadrature) component of the wave. When the wave is at zero and rising, the rate of change is at maximum positive. This provides complementary information about cycle phase and can be used for timing entries relative to cycle position.

█ INTERPRETATION

Wave Output

The composite wave oscillates around zero, representing the sum of all extracted harmonic components weighted by energy:

• Above zero : Net bullish cyclical momentum across harmonics

• Below zero : Net bearish cyclical momentum across harmonics

• Zero crossings : Cycle phase transitions - potential reversal points

• Wave amplitude : Strength of cyclical behavior; larger swings indicate cleaner cycles

Rate of Change

The quadrature component (90° phase-shifted) provides cycle phase information:

• Maximum rate of change : Wave is near zero and accelerating - early cycle phase

• Zero rate of change : Wave is at peak or trough - cycle extremes

• Rate/Wave divergence : When wave makes new highs/lows but rate of change does not confirm (lower momentum), suggests cycle exhaustion or impending phase shift

Combined Analysis

• Wave crossing above zero with positive rate of change: Strong bullish cycle initiation

• Wave crossing below zero with negative rate of change: Strong bearish cycle initiation

• Wave at extreme with rate of change reversing: Potential cycle peak/trough

Threshold Bands

When enabled, threshold bands define statistically significant wave deviations:

• Breach above +threshold : Unusually strong bullish cyclical behavior

• Breach below -threshold : Unusually strong bearish cyclical behavior

• Return inside thresholds : Normalizing behavior, potential mean reversion ahead

Alert Conditions

Four built-in alerts trigger on bar close (no repainting):

• Above +Threshold : Strong bullish cycle behavior

• Below -Threshold : Strong bearish cycle behavior

• Above Zero : Bullish cycle phase shift

• Below Zero : Bearish cycle phase shift

█ SETTINGS & PARAMETER TUNING

Fourier Series Model

• Source : Price series to decompose into harmonic components.

• Period (6-100): Base period for the fundamental harmonic. Higher harmonics divide this period (harmonic 2 = period/2, harmonic 3 = period/3). Match to the dominant market cycle for best results. Default 20.

• Bandwidth (0.05-0.5): Bandpass filter selectivity. Lower values create narrower passbands that isolate harmonics more precisely but may miss slightly off-frequency cycles. Higher values capture broader ranges but reduce harmonic separation. Default 0.1 balances precision and robustness.

• Harmonics (1-20): Number of harmonic components to extract. More harmonics capture finer cyclical detail but increase computation. For most applications, 3-5 harmonics suffice. The fundamental alone (1 harmonic) functions as a simple bandpass filter.

Display Settings

• Wave Outputs : Toggle visibility and color of the composite Fourier wave.

• Rate of Change : Toggle visibility and color of the quadrature component (90° phase-shifted wave).

• Zero Line : Reference line for oscillator neutrality.

Diagnostics - Dynamic Thresholds

Optional significance bands that identify when wave readings indicate strong cyclical behavior:

• Dynamic Threshold : Toggle threshold bands and set colors.

• Threshold Mode : Select calculation method:

- MAD (Median Absolute Deviation) : Robust, outlier-resistant measure using k * MAD where MAD ≈ 0.6745 * stdev.

- Standard Deviation : Volatility-sensitive, calculated as k * stdev of wave over the lookback period.

- Percentile Rank : Fixed probability bands using percentile of |wave| (90% means only 10% of values exceed threshold).

• Period (2-200): Lookback for threshold calculations. Default 50.

• Multiplier (k) : Scaling for MAD/Standard Deviation modes. Default 1.5.

• Percentile (%) (0-100): For Percentile Rank mode only. Default 90%.

Parameter Interactions

• Shorter periods respond faster to cycle changes but may capture noise.

• Lower bandwidth + more harmonics = more precise decomposition but requires accurate period setting.

• Higher bandwidth is more forgiving of period mismatches.

• For strongly trending markets, restrict harmonics to 1-2 so the model tracks the dominant cycle with fewer higher-frequency components.

• For ranging/oscillating markets, more harmonics (4-6) capture complex cycles.

█ LIMITATIONS

Inherent Characteristics

• Period dependency : Effectiveness depends on correctly matching the Period parameter to actual market cycles. Use cycle measurement tools (autocorrelation, FFT, dominant cycle indicators) to identify appropriate periods.

• Stationarity assumption : The indicator assumes cycle frequencies remain relatively stable within the lookback window. Rapidly shifting dominant cycles (regime transitions) may produce inconsistent results until the buffer adapts.

• Filter lag : Despite bandpass design, some lag remains inherent to causal filtering. Higher harmonics have less lag but more noise sensitivity.

• Energy weighting artifacts : During regime changes when harmonic energy ratios shift rapidly, weighting may produce transient anomalies.

Market Conditions to Avoid

• Strong trending markets : Pure trends with no cyclicality produce weak, meandering signals. The indicator assumes cyclical market behavior.

• News events/gaps : Large discontinuities disrupt filter continuity. Requires 1-2 full periods to stabilize.

• Period mismatch : If the Period parameter doesn't match actual market cycles, harmonic extraction produces noise rather than signal.

Parameter Selection Pitfalls

• Too many harmonics : Beyond 5-6 harmonics, additional components often capture noise rather than meaningful cycles.

• Bandwidth too narrow : Very low bandwidth (< 0.05) requires extremely precise period matching; slight mismatches cause signal loss.

• Over-optimization : Perfect historical parameter fits typically fail forward. Use robust defaults across multiple instruments.

█ NOTES

Credits

This indicator applies Fourier analysis principles to financial market data, building on the extensive work of Dr. John F. Ehlers in applying digital signal processing to trading. The bandpass filter implementation and harmonic decomposition approach draw from DSP fundamentals as presented in Ehlers' publications.

For those interested in the underlying mathematics and DSP concepts:

• Ehlers, J.F. (2001). Rocket Science for Traders: Digital Signal Processing Applications . John Wiley & Sons.

• Ehlers, J.F. (2013). Cycle Analytics for Traders . John Wiley & Sons.

• Various TASC articles by John Ehlers on bandpass filters, cycle analysis, and harmonic decomposition.

by ♚@e2e4