Adaptive Z-Score Oscillator [QuantAlgo]🟢 Overview

The Adaptive Z-Score Oscillator transforms price action into statistical significance measurements by calculating how many standard deviations the current price deviates from its moving average baseline, then dynamically adjusting threshold levels based on historical distribution patterns. Unlike traditional oscillators that rely on fixed overbought/oversold levels, this indicator employs percentile-based adaptive thresholds that automatically calibrate to changing market volatility regimes and statistical characteristics. By offering both adaptive and fixed threshold modes alongside multiple moving average types and customizable smoothing, the indicator provides traders and investors with a robust framework for identifying extreme price deviations, mean reversion opportunities, and underlying trend conditions through the visualization of price behavior within a statistical distribution context.

🟢 How It Works

The indicator begins by establishing a dynamic baseline using a user-selected moving average type applied to closing prices over the specified length period, then calculates the standard deviation to measure price dispersion:

basis = ma(close, length, maType)

stdev = ta.stdev(close, length)

The core Z-Score calculation quantifies how many standard deviations the current price sits above or below the moving average basis, creating a normalized oscillator that facilitates cross-asset and cross-timeframe comparisons:

zScore = stdev != 0 ? (close - basis) / stdev : 0

smoothedZ = ma(zScore, smooth, maType)

The adaptive threshold mechanism employs percentile calculations over a historical lookback period to determine statistically significant extreme zones. Rather than using fixed levels like ±2.0, the indicator identifies where a specified percentage of historical Z-Score readings have fallen, automatically adjusting to market regime changes:

upperThreshold = adaptive ? ta.percentile_linear_interpolation(smoothedZ, percentilePeriod, upperPercentile) : fixedUpper

lowerThreshold = adaptive ? ta.percentile_linear_interpolation(smoothedZ, percentilePeriod, lowerPercentile) : fixedLower

The visualization architecture creates a four-tier coloring system that distinguishes between extreme conditions (beyond the adaptive thresholds) and moderate conditions (between the midpoint and threshold levels), providing visual gradation of statistical significance through opacity variations and immediate recognition of distribution extremes.

🟢 How to Use This Indicator

▶ Overbought and Oversold Identification:

The indicator identifies potential overbought conditions when the smoothed Z-Score crosses above the upper threshold, indicating that price has deviated to a statistically extreme level above its mean. Conversely, oversold conditions emerge when the Z-Score crosses below the lower threshold, signaling statistically significant downward deviation. In adaptive mode (default), these thresholds automatically adjust to the asset's historical behavior, i.e., during high volatility periods, the thresholds expand to accommodate wider price swings, while during low volatility regimes, they contract to capture smaller deviations as significant. This dynamic calibration reduce false signals that plague fixed-level oscillators when market character shifts between volatile and ranging conditions.

▶ Mean Reversion Trading Applications:

The Z-Score framework excels at identifying mean reversion opportunities by highlighting when price has stretched too far from its statistical equilibrium. When the oscillator reaches extreme bearish levels (below the lower threshold with deep red coloring), it suggests price has become statistically oversold and may snap back toward the mean, presenting potential long entry opportunities for mean reversion traders. Symmetrically, extreme bullish readings (above the upper threshold with bright green coloring) indicate potential short opportunities or long exit points as price becomes statistically overbought. The moderate zones (lighter colors between midpoint and threshold) serve as early warning areas where traders can prepare for potential reversals, while exits from extreme zones (crossing back inside the thresholds) often provide confirmation that mean reversion is underway.

▶ Trend and Distribution Analysis:

Beyond discrete overbought/oversold signals, the histogram's color pattern and shape reveal the underlying trend structure and distribution characteristics. Sustained periods where the Z-Score oscillates primarily in positive territory (green bars) indicate a bullish trend where price consistently trades above its moving average baseline, even if not reaching extreme levels. Conversely, predominant negative readings (red bars) suggest bearish trend conditions. The distribution shape itself provides insight into market behavior, e.g., a narrow, centered distribution clustering near zero indicates tight ranging conditions with price respecting the mean, while a wide distribution with frequent extreme readings reveals volatile trending or choppy conditions. Asymmetric distributions skewed heavily toward one side demonstrate persistent directional bias, whereas balanced distributions suggest equilibrium between bulls and bears.

▶ Built-in Alerts:

Seven alert conditions enable automated monitoring of statistical extremes and trend transitions. Enter Overbought and Enter Oversold alerts trigger when the Z-Score crosses into extreme zones, providing early warnings of potential reversal setups. Exit Overbought and Exit Oversold alerts signal when price begins reverting from extremes, offering confirmation that mean reversion has initiated. Zero Cross Up and Zero Cross Down alerts identify transitions through the neutral line, indicating shifts between above-mean and below-mean price action that can signal trend changes. The Extreme Zone Entry alert fires on any extreme threshold penetration regardless of direction, allowing unified monitoring of both overbought and oversold opportunities.

▶ Color Customization:

Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and aesthetic preferences, ensuring optimal contrast and readability across trading platforms. The bar transparency control (0-90%) allows fine-tuning of visual prominence, with minimal transparency creating bold, attention-grabbing bars for primary analysis, while higher transparency values produce subtle background context when using the oscillator alongside other indicators. The extreme and moderate zone coloring system uses automatic opacity variation to create instant visual hierarchy, with darkest colors highlight the most statistically significant deviations demanding immediate attention, while lighter shades mark developing conditions that warrant monitoring but may not yet justify action. Optional candle coloring extends the Z-Score color scheme directly to the price candles on the main chart, enabling traders to instantly recognize statistical extremes and trend conditions without needing to reference the oscillator panel, creating a unified visual experience where both price action and statistical analysis share the same color language.

Normaldistribution

RSI Profile [Kodexius]RSI Profile is an advanced technical indicator that turns the classic RSI into a distribution profile instead of a single oscillating line. Rather than only showing where the RSI is at the current bar, it displays where the RSI has spent most of its time or most of its volume over a user defined lookback period.

The script builds a histogram of RSI values between 0 and 100, splits that range into configurable bins, and then projects the result to the right side of the chart. This gives you a clear visual representation of the RSI structure, including the Point of Control (POC), the Value Area High (VAH), and the Value Area Low (VAL). The POC marks the RSI level with the highest activity, while VAH and VAL bracket the percentage based value area around it.

By combining standard RSI, a distribution profile, and value area logic, this tool lets you study RSI behavior statistically instead of only bar by bar. You can immediately see whether the current RSI reading is located inside the dominant zone, extended above it, or depressed below it, and whether the recent regime has been biased toward overbought, oversold, or neutral territory. This is particularly useful for swing traders, mean reversion systems, and anyone who wants to integrate RSI context into a more profile oriented workflow.

🔹 Features

1. RSI-Based Distribution Profile

-Builds a histogram of RSI values between 0 and 100.

-The RSI range is divided into a user-defined number of bins (e.g., 30 bins).

-Each bin represents a band of RSI values, such as 0–3.33, 3.33–6.66, ..., 96.66–100.

-For each bar in the lookback period, the script:

-Finds which bin the RSI value belongs to

Adds either:

-1.0 → if using time/frequency

-volume → if using volume-weighted RSI distribution

This creates a clear profile of where RSI has been concentrated over the chosen lookback window.

2. Time / Volume Weighting Mode

Under Profile Settings, you can choose:

-Weight by Volume = false

→ Profile is built using time spent at each RSI level (frequency).

-Weight by Volume = true

→ Profile is built using volume traded at each RSI level.

This flexibility allows you to decide whether you want:

-A pure momentum structure (time spent at each RSI)

-Or a participation-weighted structure (where higher-volume zones are emphasized)

3. Configurable Lookback & Resolution

-Profile Lookback: number of historical bars to analyze.

-Number of Bins: controls the resolution of the histogram:

Fewer bins → smoother, fewer gaps

More bins → more detail, but potentially more visual sparsity

-Profile Width (Bars): defines how wide the histogram extends into the future (visually), converted into time using average bar duration.

This provides a balance between performance, clarity, and visual density.

4. Value Area, POC, VAH, VAL

The script computes:

-POC (Point of Control)

→ The RSI bin with the highest total value (time or volume).

-Value Area (VA)

→ The range of RSI bins that contain a user-specified percentage of total activity (e.g., 70%).

-VAH & VAL

→ Upper and lower RSI boundaries of this Value Area.

These are then drawn as horizontal lines and labeled:

-POC line and label

-VAH line and label

-VAL line and label

This gives you a profile-style view similar to classical volume profile, but entirely on the RSI axis.

5. Color Coding & Visual Design

The histogram bars (boxes) are colored using a smart scheme:

-Below 30 RSI → Oversold zone, uses the Oversold Color (default: green).

-Above 70 RSI → Overbought zone, uses the Overbought Color (default: red).

-Between 30 and 70 RSI → Neutral zone, uses a gradient between:

A soft blue at lower mid levels

A soft orange at higher mid levels

Additional styling:

-POC bin is highlighted in bright yellow.

-Bins inside the Value Area → lower transparency (more solid).

-Bins outside the Value Area → higher transparency (faded).

This makes it easy to visually distinguish:

-Core RSI activity (VA)

-Extremes (oversold/overbought)

-The single dominant zone (POC)

🔹 Calculations

This section summarizes the core logic behind the script and highlights the main building blocks that power the profile.

1. Profile Structure and Bin Initialization

A custom Profile type groups together configuration, bins and drawing objects. During initialization, the script splits the 0 to 100 RSI range into evenly spaced bins, each represented by a Bin record:

method initBins(Profile p) =>

p.bins := array.new()

float step = 100.0 / p.binCount

for i = 0 to p.binCount - 1

float low = i * step

float high = (i + 1) * step

p.bins.push(Bin.new(low, high, 0.0, box(na)))

2. Filling the Profile Over the Lookback Window

On the last bar, the script clears previous drawings and walks backward through the selected lookback window. For each historical bar, it reads the RSI and volume series and feeds them into the profile:

if barstate.islast

myProfile.reset()

int start = math.max(0, bar_index - lookback)

int end = bar_index

for i = 0 to (end - start)

float r = rsi

float v = volume

if not na(r)

myProfile.add(r, v)

The add method converts each RSI value into a bin index and accumulates either a frequency count or the bar volume, depending on the chosen mode:

method add(Profile p, float rsiValue, float volumeValue) =>

int idx = int(rsiValue / (100.0 / p.binCount))

if idx >= p.binCount

idx := p.binCount - 1

if idx < 0

idx := 0

Bin targetBin = p.bins.get(idx)

float addedValue = p.useVolume ? volumeValue : 1.0

targetBin.value += addedValue

3. Finding POC and Building the Value Area

Inside the draw method, the script first scans all bins to determine the maximum value and the total sum. The bin with the highest value becomes the POC. The value area is then constructed by expanding from that center bin until the desired percentage of total activity is covered:

for in p.bins

totalVal += b.value

if b.value > maxVal

maxVal := b.value

pocIdx := i

float vaTarget = totalVal * (p.vaPercent / 100.0)

float currentVaVol = maxVal

int upIdx = pocIdx

int downIdx = pocIdx

while currentVaVol < vaTarget

float upVol = (upIdx < p.binCount - 1) ? p.bins.get(upIdx + 1).value : 0.0

float downVol = (downIdx > 0) ? p.bins.get(downIdx - 1).value : 0.0

if upVol == 0 and downVol == 0

break

if upVol >= downVol

upIdx += 1

currentVaVol += upVol

else

downIdx -= 1

currentVaVol += downVol

Rolling Z-Score Trend [QuantAlgo]🟢 Overview

The Rolling Z-Score Trend measures how far the current price deviates from its rolling mean in terms of standard deviations. It transforms price data into standardized scores to identify overbought and oversold conditions while tracking momentum shifts.

The indicator displays a Z-Score line showing price deviation from statistical norms, with background momentum columns showing the rate of change in these deviations. This helps traders and investors identify mean reversion opportunities and momentum shifts across different asset classes and timeframes.

🟢 How It Works

The indicator uses the Z-Score formula: Z = (X - μ) / σ, where X is the current closing price, μ is the rolling mean, and σ is the rolling standard deviation over a user-defined lookback period. This creates a dynamic baseline that adapts to changing market conditions and standardizes price movements for interpretation across different assets and volatility conditions. The raw Z-Score undergoes 3-period EMA smoothing to reduce noise while maintaining responsiveness to market signals.

Beyond the basic Z-Score calculation, the indicator measures the rate of change in Z-Score values between successive bars, displayed as background momentum columns. This momentum component shows acceleration and deceleration of statistical deviations. All calculations are processed through confirmation filters, displaying signals only on confirmed bars to reduce premature signals based on incomplete price action.

🟢 How to Use

1. Z-Score Interpretation and Threshold Zones

Positive Values (Above Zero) : Price trading above statistical mean, suggesting bullish momentum or potential overbought conditions

Negative Values (Below Zero) : Price trading below statistical mean, suggesting bearish momentum or potential oversold conditions

Zero Line Crosses : Signal transitions between statistical regimes and potential trend changes

Upper Threshold Zone : Area above entry threshold (default 1.5) indicating potential overbought conditions

Lower Threshold Zone : Area below negative entry threshold (default -1.5) indicating potential oversold conditions

Extreme Values (±2.0 or higher) : Statistically significant deviations that may indicate reversal opportunities

2. Momentum Background Analysis and Info Table

Green Columns : Accelerating positive momentum in Z-Score values

Red Columns : Accelerating negative momentum in Z-Score values

Column Height : Magnitude of momentum change between bars

Momentum Divergence : When columns contradict primary Z-Score direction, often signals impending reversals

Info Table : Displays real-time numerical values for both Z-Score and momentum, including trend direction indicators and bar-to-bar change calculations for position management

3. Preconfigured Settings

Default : Balanced performance across multiple timeframes and asset classes for general trading and medium-term position management.

Scalping : Responsive setup for ultra-short-term trading on 1-15 minute charts with frequent signals and increased sensitivity to quick price movements.

Swing Trading : Optimized for multi-day positions with noise filtering, focusing on larger price swings. Most effective on 1-4 hour and daily timeframes.

Trend Following : Maximum smoothing that prioritizes established trends over short-term volatility. Generates fewer signals for daily and weekly charts.

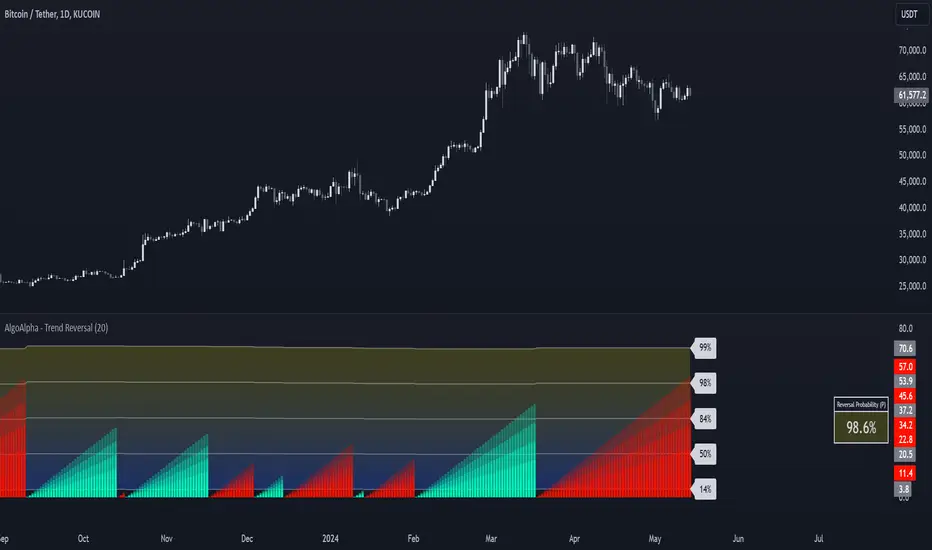

Trend Reversal Probability [Algoalpha]Introducing Trend Reversal Probability by AlgoAlpha – a powerful indicator that estimates the likelihood of trend reversals based on an advanced custom oscillator and duration-based statistics. Designed for traders who want to stay ahead of potential market shifts, this indicator provides actionable insights into trend momentum and reversal probabilities.

Key Features :

🔧 Custom Oscillator Calculation: Combines a dual SMA strategy with a proprietary RSI-like calculation to detect market direction and strength.

📊 Probability Levels & Visualization: Plots average signal durations and their statistical deviations (±1, ±2, ±3 SD) on the chart for clear visual guidance.

🎨 Dynamic Color Customization: Choose your preferred colors for upward and downward trends, ensuring a personalized chart view.

📈 Signal Duration Metrics: Tracks and displays signal durations with columns representing key percentages (80%, 60%, 40%, and 20%).

🔔 Alerts for High Probability Events: Set alerts for significant reversal probabilities (above 84% and 98% or below 14%) to capture key trading moments.

How to Use :

Add the Indicator: Add Trend Reversal Probability to your favorites by clicking the star icon.

Market Analysis: Use the plotted probability levels (average duration and ±SD bands) to identify overextended trends and potential reversals. Use the color of the duration counter to identify the current trend.

Leverage Alerts: Enable alerts to stay informed of high or extreme reversal probabilities without constant chart monitoring.

How It Works :

The indicator begins by calculating a custom oscillator using short and long simple moving averages (SMA) of the midpoint price. A proprietary RSI-like formula then transforms these values to estimate trend direction and momentum. The duration between trend reversals is tracked and averaged, with standard deviations plotted to provide probabilistic guidance on trend longevity. Additionally, the indicator incorporates a cumulative probability function to estimate the likelihood of a trend reversal, displaying the result in a data table for easy reference. When probability levels cross key thresholds, alerts are triggered, helping traders take timely action.

GaussianDistributionLibrary "GaussianDistribution"

This library defines a custom type `distr` representing a Gaussian (or other statistical) distribution.

It provides methods to calculate key statistical moments and scores, including mean, median, mode, standard deviation, variance, skewness, kurtosis, and Z-scores.

This library is useful for analyzing probability distributions in financial data.

Disclaimer:

I am not a mathematician, but I have implemented this library to the best of my understanding and capacity. Please be indulgent as I tried to translate statistical concepts into code as accurately as possible. Feedback, suggestions, and corrections are welcome to improve the reliability and robustness of this library.

mean(source, length)

Calculate the mean (average) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Mean (μ)

stdev(source, length)

Calculate the standard deviation (σ) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Standard deviation (σ)

skewness(source, length, mean, stdev)

Calculate the skewness (γ₁) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Skewness (γ₁)

skewness(source, length)

Overloaded skewness to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Skewness (γ₁)

mode(mean, stdev, skewness)

Estimate mode - Most frequent value in the distribution (approximation based on skewness)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Mode

mode(source, length)

Overloaded mode to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Mode

median(mean, stdev, skewness)

Estimate median - Middle value of the distribution (approximation)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Median

median(source, length)

Overloaded median to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Median

variance(stdev)

Calculate variance (σ²) - Square of the standard deviation

Parameters:

stdev (float) : the standard deviation (σ) of the distribution

@return Variance (σ²)

variance(source, length)

Overloaded variance to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Variance (σ²)

kurtosis(source, length, mean, stdev)

Calculate kurtosis (γ₂) - Degree of "tailedness" in the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Kurtosis (γ₂)

kurtosis(source, length)

Overloaded kurtosis to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Kurtosis (γ₂)

normal_score(source, mean, stdev)

Calculate Z-score (standard score) assuming a normal distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Z-Score

normal_score(source, length)

Overloaded normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

non_normal_score(source, mean, stdev, skewness, kurtosis)

Calculate adjusted Z-score considering skewness and kurtosis

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

kurtosis (float) : the "tailedness" in the distribution

@return Z-Score

non_normal_score(source, length)

Overloaded non_normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

method init(this)

Initialize all statistical fields of the `distr` type

Namespace types: distr

Parameters:

this (distr)

method init(this, source, length)

Overloaded initializer to set source and length

Namespace types: distr

Parameters:

this (distr)

source (float)

length (int)

distr

Custom type to represent a Gaussian distribution

Fields:

source (series float) : Distribution source (typically a price or indicator series)

length (series int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mode (series float) : Most frequent value in the distribution

median (series float) : Middle value separating the greater and lesser halves of the distribution

mean (series float) : μ (1st central moment) - Average of the distribution

stdev (series float) : σ or standard deviation (square root of the variance) - Measure of dispersion

variance (series float) : σ² (2nd central moment) - Squared standard deviation

skewness (series float) : γ₁ (3rd central moment) - Asymmetry of the distribution

kurtosis (series float) : γ₂ (4th central moment) - Degree of "tailedness" relative to a normal distribution

normal_score (series float) : Z-score assuming normal distribution

non_normal_score (series float) : Adjusted Z-score considering skewness and kurtosis

Likelihood of Winning - Probability Density FunctionIn developing the "Likelihood of Winning - Probability Density Function (PDF)" indicator, my aim was to offer traders a statistical tool to quantify the probability of reaching target prices. This indicator, grounded in risk assessment principles, enables users to analyze potential outcomes based on the normal distribution, providing insights into market dynamics.

The tool's flexibility allows for customization of the data series, lookback periods, and target settings for both long and short scenarios. It features a color-coded visualization to easily distinguish between probabilities of hitting specified targets, enhancing decision-making in trading strategies.

I'm excited to share this indicator with the trading community, hoping it will enhance data-driven decision-making and offer a deeper understanding of market risks and opportunities. My goal is to continuously improve this tool based on user feedback and market evolution, contributing to more informed trading practices.

This indicator leverages the "NormalDistributionFunctions" library, enabling easy integration into other indicators or strategies. Users can readily embed advanced statistical analysis into their trading tools, fostering innovation within the Pine Script community.

NormalDistributionFunctionsLibrary "NormalDistributionFunctions"

The NormalDistributionFunctions library encompasses a comprehensive suite of statistical tools for financial market analysis. It provides functions to calculate essential statistical measures such as mean, standard deviation, skewness, and kurtosis, alongside advanced functionalities for computing the probability density function (PDF), cumulative distribution function (CDF), Z-score, and confidence intervals. This library is designed to assist in the assessment of market volatility, distribution characteristics of asset returns, and risk management calculations, making it an invaluable resource for traders and financial analysts.

meanAndStdDev(source, length)

Calculates and returns the mean and standard deviation for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

length (int) : int: The lookback period for the calculation.

Returns: Returns an array where the first element is the mean and the second element is the standard deviation of the data series for the given period.

skewness(source, mean, stdDev, length)

Calculates and returns skewness for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns skewness value

kurtosis(source, mean, stdDev, length)

Calculates and returns kurtosis for a given data series over a specified period.

Parameters:

source (float) : float: The data series to analyze.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

length (int) : int: The lookback period for the calculation.

Returns: Returns kurtosis value

pdf(x, mean, stdDev)

pdf: Calculates the probability density function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the PDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the probability density function value for x.

cdf(x, mean, stdDev)

cdf: Calculates the cumulative distribution function for a given value within a normal distribution.

Parameters:

x (float) : float: The value to evaluate the CDF at.

mean (float) : float: The mean of the distribution.

stdDev (float) : float: The standard deviation of the distribution.

Returns: Returns the cumulative distribution function value for x.

confidenceInterval(mean, stdDev, size, confidenceLevel)

Calculates the confidence interval for a data series mean.

Parameters:

mean (float) : float: The mean of the data series.

stdDev (float) : float: The standard deviation of the data series.

size (int) : int: The sample size.

confidenceLevel (float) : float: The confidence level (e.g., 0.95 for 95% confidence).

Returns: Returns the lower and upper bounds of the confidence interval.

Normal Distribution Asymmetry & Volatility ZonesNormal Distribution Asymmetry & Volatility Zones Indicator provides insights into the skewness of a price distribution and identifies potential volatility zones in the market. The indicator calculates the skewness coefficient, indicating the asymmetry of the price distribution, and combines it with a measure of volatility to define buy and sell zones.

The key features of this indicator include :

Skewness Calculation : It calculates the skewness coefficient, a statistical measure that reveals whether the price distribution is skewed to the left (negative skewness) or right (positive skewness).

Volatility Zones : Based on the skewness and a user-defined volatility threshold, the indicator identifies buy and sell zones where potential price movements may occur. Buy zones are marked when skewness is negative and prices are below a volatility threshold. Sell zones are marked when skewness is positive and prices are above the threshold.

Signal Source Selection : Traders can select the source of price data for analysis, allowing flexibility in their trading strategy.

Customizable Parameters : Users can adjust the length of the distribution, the volatility threshold, and other parameters to tailor the indicator to their specific trading preferences and market conditions.

Visual Signals : Buy and sell zones are visually displayed on the chart, making it easy to identify potential trade opportunities.

Background Color : The indicator changes the background color of the chart to highlight significant zones, providing a clear visual cue for traders.

By combining skewness analysis and volatility thresholds, this indicator offers traders a unique perspective on potential market movements, helping them make informed trading decisions. Please note that trading involves risks, and this indicator should be used in conjunction with other analysis and risk management techniques.

Oscillator: Which follows Normal Distribution?When doing machine learning using oscillators, it would be better if the oscillators were normally distributed.

So I analyzed the distribution of oscillators.

The value of the oscillator was divided into 50 groups each from 0 to 100.

ex) if rsi value is 45.43 -> group_44, 58.23 -> group_58

Ocscillators : RSI, Stoch, MFI, WT, RVI, etc....

Caution: The normal distribution was verified through an empirical formula.

RSI is in Normal Distribution?Does RSI Follow a Normal Distribution?

The value of RSI was converted to a value between 0~2, 2~4, ..., 98~100, and the number of samples was graphed.

The Z values are expressed so that the values corresponding to 30 and 70 of the RSI can be compared with the standard normal distribution.

Additionally, when using the RSI period correction function of the 'RSI Candle Advanced V2' indicator that I made before, it shows no change in standard deviation.

RSI는 정규분포를 따를까요

RSI의 값을 0~2, 2~4, ..., 98~100 사이 값으로 변환하고 그 표본 갯수를 그래프로 표현하였습니다.

Z 값은 RSI의 30, 70에 해당하는 값을 표준정규분포와 비교할 수 있도록 표현하였습니다.

추가적으로 제가 예전에 만들었던 'RSI Candle Advanced V2' 지표의 RSI 기간 보정 함수를 사용할 경우 표준편차의 변화가 없음을 보입니다.

Return Abnormality Score [SpiritualHealer117]The Return Abnormality Score indicator is designed to help traders identify potential reversals in price by detecting abnormal daily returns beyond a certain significance level. The indicator uses a normal cumulative distribution function to calculate the probability of the daily return and flags it when it exceeds the specified significance level.

Traders can use this indicator by monitoring the abnormality score. If the daily return is negative, the probability is multiplied by a negative number. Therefore, if the abnormality score goes above the positive threshold, it suggests that the price is oversold, while if it goes below the negative threshold, it indicates that the price is overbought. It can also be helpful for spotting bear or bull traps due to their irregular behavior.

Depending on the trader's preference, the indicator can be smoothed or unsmoothed.

This indicator should be paired with other technical analysis tools like SSL Hybrid for trend confirmation, and proper risk management strategies.

normsinvLibrary "normsinv"

Description:

Returns the inverse of the standard normal cumulative distribution.

The distribution has a mean of zero and a standard deviation of one; i.e.,

normsinv seeks that value z such that a normal distribtuion of mean of zero

and standard deviation one is equal to the input probability.

Reference:

github.com

normsinv(y0)

Returns the inverse of the standard normal cumulative distribution. The distribution has a mean of zero and a standard deviation of one.

Parameters:

y0 : float, probability corresponding to the normal distribution.

Returns: float, z-score

cndevLibrary "cndev"

This function returns the inverse of cumulative normal distribution function

Reference:

The Full Monte, by Boris Moro, Union Bank of Switzerland . RISK 1995(2)

CNDEV(U)

Returns the inverse of cumulative normal distribution function

Parameters:

U : float,

Returns: float.

ctndLibrary "ctnd"

Description:

Double precision algorithm to compute the cumulative trivariate normal distribution

found in A.Genz, Numerical computation of rectangular bivariate and trivariate normal

and t probabilities”, Statistics and Computing, 14, (3), 2004. The cumulative trivariate

normal is needed to price window barrier options, see G.F. Armstrong, Valuation formulae

or window barrier options”, Applied Mathematical Finance, 8, 2001.

References:

link.springer.com

www.tandfonline.com

citeseerx.ist.psu.edu

The Complete Guide to Option Pricing Formulas, 2nd ed. (Espen Gaarder Haug)

CTND(LIMIT1, LIMIT2, LIMIT3, SIGMA1, SIGMA2, SIGMA3)

Returns the Cumulative Trivariate Normal Distribution

Parameters:

LIMIT1 : float,

LIMIT2 : float,

LIMIT3 : float,

SIGMA1 : float,

SIGMA2 : float,

SIGMA3 : float,

Returns: float.

norminvLibrary "norminv"

Description:

An inverse normal distribution is a way to work backwards

from a known probability to find an x-value. It is an informal term and

doesn't refer to a particular probability distribution. Returns the

value of the inverse normal distribution function for a specified value,

mean, and standard deviation.

Reference:

github.com

support.microsoft.com

norminv(x, mean, stdev)

Returns the value of the inverse normal distribution function for a specified value, mean, and standard deviation.

Parameters:

x : float, The input to the normal distribution function.

mean : float, The mean (mu) of the normal distribution function

stdev : float, The standard deviation (sigma) of the normal distribution function.

Returns: float.

cndLibrary "cnd"

Cumulative Normal Distribution

CND1(x)

Returns the Cumulative Normal Distribution (CND) using the Hart (1968) method. (preferred method, 14-18 decimal accuracy)

Parameters:

x : float,

Returns: float.

CND2(x)

Returns the Cumulative Normal Distribution (CND) using the Abromowitz and Stegun (1974) Polynomial Approximation.

Parameters:

x : float,

Returns: float.

CND3(x)

Returns the Cumulative Normal Distribution (CND) using Newton-Cotes method, Boole’s rule

Parameters:

x : float,

Returns: float.

One-Sided Gaussian Filter w/ Channels [Loxx]One-Sided Gaussian Filter w/ Channels is a Gaussian Moving Average that is calculated using a Fibonacci weighting function. Keltner channels have been added to show zones of exhaustion. A better name would be "Half Gaussian bell weighted" or "Half normal distribution weighted" indicator, since the weights for calculation of the average (similar to linear weighted average) are taken from a normal distribution curve like function--but only the half of the curve is used for calculation.

Information of the Gaussian distribution can be found here : en.wikipedia.org and once you take a look at the standard normal distribution curve, it will be much clearer what is exactly done in this indicator.

After the Gaussian Filter is applied to the source input, an Ehlers' 2-Pole Super Smoother is applied to reduce noise without significant lag.

Included:

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

Is the Bollinger Bands assumption wrong?Bollinger Bands are the result of the assumption that closing prices will follow a normal distribution.

However, when I actually calculated the probability, the closing price does not follow a normal distribution.

According to the normal distribution, the probability that Z > 2 should be 2.2%, but on the chart, the probability is 6~9%.

Can we get a useful value for Bollinger Bands that we can use in our strategy?

We can measure volatility, but can we judge volatility based on a fixed value?

To the right of each Bollinger band value, the probability that the price is above the band is displayed.

The script is simply annotated with how each probability is calculated.

Probability Distribution HistogramProbability Distribution Histogram

During data exploration it is often useful to plot the distribution of the data one is exploring. This indicator plots the distribution of data between different bins.

Essentially, what we do is we look at the min and max of the entire data set to determine its range. When we have the range of the data, we decide how many bins we want to divide this range into, so that the more bins we get, the smaller the range (a.k.a. width) for each bin becomes. We then place each data point in its corresponding bin, to see how many of the data points end up in each bin. For instance, if we have a data set where the smallest number is 5 and the biggest number is 105, we get a range of 100. If we then decide on 20 bins, each bin will have a width of 5. So the left-most bin would therefore correspond to values between 5 and 10, and the bin to the right would correspond to values between 10 and 15, and so on.

Once we have distributed all the data points into their corresponding bins, we compare the count in each bin to the total number of data points, to get a percentage of the total for each bin. So if we have 100 data points, and the left-most bin has 2 data points in it, that would equal 2%. This is also known as probability mass (or well, an approximation of it at least, since we're dealing with a bin, and not an exact number).

Usage

This is not an indicator that will give you any trading signals. This indicator is made to help you examine data. It can take any input you give it and plot how that data is distributed.

The indicator can transform the data in a few ways to help you get the most out of your data exploration. For instance, it is usually more accurate to use logarithmic data than raw data, so there is an option to transform the data using the natural logarithmic function. There is also an option to transform the data into %-Change form or by using data differencing.

Another option that the indicator has is the ability to trim data from the data set before plotting the distribution. This can help if you know there are outliers that are made up of corrupted data or data that is not relevant to your research.

I also included the option to plot the normal distribution as well, for comparison. This can be useful when the data is made up of residuals from a prediction model, to see if the residuals seem to be normally distributed or not.

ema exhaustion (exa)The exa is an oscillator that combines fisher transform with distance from moving average and it is based on a theory that exhaustion can be derived from how far price is able to extend from a moving average, on average.

The fisher transform converts price into a gaussian normal distribution, also known as a bell curve {1}. A normal distribution is a type of probability distribution for a real-valued random variable {2}. Applying this method to the price of an asset can help to identify probabilities, but it will never identify certainties.

‘exa’ is an abbreviation for ema exhaustion. It can be used to identify when price is probable to revert to the mean but I prefer using it to confirm entries that are signaled following a reversion to the mean (aka buying the dip in bull markets). When price gets oversold into support, in a bull trend, then that can provide a good opportunity to enter long. However that isn’t necessarily the case when the same metrics indicate oversold conditions in a bear trend. In this situation the exa is best suited for identifying profit taking opportunities on shorts.

The default settings are a 9 lookback period and a 50 ema. By default signals will be derived from how far price is from the 50 ema relative to the probable distribution of the last 9 periods. If the exa is above 2, or below -2, then the price is in the 80th percentile of the prior 9 candles. Being outside of 3, or -3, represents the 90th percentile and 4, or -4, represents the 95th percentile.

Those ranges will never indicate a necessity of reverting to the mean, but they will indicate a higher and higher probability. I prefer to use this oscillator in combination with an indicator(s) that identifies the trend. When the oscillator reaches -2 in a bull trend then it can confirm long entry signals, whereas if it reaches +2 in a bull trend then it can be used to confirm signals to take profit.

Crossovers are especially significant because they indicate a shift in the tide. When the exa reaches 2 without crossing over then it is very much in a position to move to 3 or 4+. When it crosses above 2 then it is an indication that price is extended from the mean and exhausted.

This is certainly not a situation that implies price will revert to the mean, it simply provides confirmation.

The default settings are what I have been finding most effective personally, however that is mostly a function of the trend following tools that I use. The same principles should apply with all settings and I would encourage users to experiment with various lookback periods and emas.

{1} www.investopedia.com

{2} en.wikipedia.org

Simplest volatility bandsVolatility bands based on average candle percentage spread. Tested on BTCUSD charts only.

Based on the 68-95-99.7 rule, it seems that the spread, for daily and 4-H candles, follows a normal distribution: that means, around 85% of candles have a %-spread within sma(low/high, some_len) and sma(high/low, some_len) , and around 95% of candles within the pow2 of that range.

If you take the mean between the boundaries of the first %-spreads band, and calculate the 1.5 standard deviation of past some_len candles (I'm speaking from memory, it has been a while since I did them), the 1.5 standard deviation bands match similarly the %-spread bands, and around 85% of the candles are within these %-spread bands.

If you then take the pow2 of the bands, it will be similar to the 2 * std of the original bands, with around 95% of data within the pow2 bands.

You can take ema or other similar means with similar results, and the same for different lengths, but it seems that sma with a len of 14 is the more stable ones for both daily and 4-H, and taken other average calculations doesn't cause too many differences respect to the sma. I haven't tested too much for lower or higher timeframes.

With those %-spread bands, I multiple and divide those spreads to the open value of a new candle to get the two bands.

So, in short, you know that 85% of candles are within the closer bands, and around 95% of candles, around the bigger one. Once a new candle is born, the bands won't move (the bands are calculated from the previous candle, so the current candle's price movement doesn't move the band).

Going out the bands implies a sudden increase in volality, which usually causes rejection. They happen mostly at breakouts and ends of heavy trends. If a candle closes above the bigger band, you have probably got a breakout (a rejection rarely happens if the candle have already closed), although a breakout can happen without closing above the bands if volatility was already high.

If a trend is already stablished and is healthy, you won't probably see candles going out the bands, not even with a wick. When the trend is parabolic, and goes above the candle, the trend has probably ended, although the trend can be exhausted without going out the bands as well.

Heavy but not yet exhausted trends (specially recently started heavy downtrends), usually reach the bottom of the bigger bands during 4 o 5 contiguous candles (check visually looking at bitcoin history though, I'm speaking from memory).

So, the possibilities are multiple and you cannot use the bands to form a strategy, as usual. It can be comfortable enough psycologically for going to sleep, by moving your stop-loss to a point out of the bands in the opposite direction of your trade, and adjusting your position size accordingly; or just to check momentum looking at how close are the candle limits to the bands.

But, as usual, you are responsible of what you do with your money :)