Buffett Indicator with Historical Bubbles (Clean)The Buffett Indicator is a trusted macroeconomic gauge that compares the total US stock market capitalization to the nation’s GDP. Popularized by Warren Buffett, this metric highlights periods of overvaluation and undervaluation in the market.

This tool offers a clean and accurate visualization of the Buffett Indicator, enhanced with historical bubble annotations for key market events:

Dot-com Bubble (2000)

Global Financial Crisis Peak (2007)

COVID-19 Pre-crash Peak (2020)

Post-COVID Bull Market Peak (2021)

Features:

Dynamic Buffett Ratio (%) calculation using Wilshire 5000 Index as the market cap proxy.

Customizable GDP input for accuracy (update quarterly).

Visual thresholds for fair value, undervaluation, and overvaluation zones.

Historical event markers for educational and analytical context.

Optimized to display clearly across all timeframes: Daily, Weekly, Monthly.

How to Use:

Manually update the GDP input as new data is released.

Use this indicator for macro-level market sentiment analysis and valuation tracking.

Combine with other tools and risk management strategies for comprehensive market insights.

Disclaimer:

This indicator is for educational purposes only. It does not constitute financial advice. Always perform your own research and analysis.

Version: 1.0

we ask Allah reconcile and repay

#BuffettIndicator #MarketValuation #MacroAnalysis #BubbleDetector #LongTermInvestor #USMarket #Wilshire5000 #TradingViewScript

Su Pine

Market Clock with Inline HoursThis script displays a powerful, configurable market session clock that shows the open/closed status and trading hours for major global financial markets — including specialized logic for NY Futures (Globex).

🔑 Key Features:

✅ Real-Time Session Status:

Shows whether each selected market is currently OPEN or CLOSED, based on the user’s selected time zone.

✅ NY Futures Weekend Logic:

Built-in logic ensures NY Futures are marked CLOSED:

Friday after 5:00 PM ET

All of Saturday

Sunday until 6:00 PM ET

This reflects the true CME Globex trading schedule.

✅ 12-Hour Format + Timezone Labels:

Session hours are displayed in 12-hour AM/PM format alongside their associated timezone (EST, GMT, JST, etc.) for clarity.

✅ Fully Configurable Markets:

You can choose to display:

NY Market (RTH)

NY Futures (Globex)

London

Tokyo

Frankfurt

And you can easily toggle them on/off in the settings.

✅ Text Size & Position Customization:

Easily control the text size (tiny → huge) and screen position (top/bottom, left/center/right).

✅ Auto Timezone Offset Support:

Select from a list of common time zones (EST, UTC, JST, etc.), or enter your own custom UTC offset for global flexibility.

✅ Compact & Clean Design:

The layout groups each market’s:

Real-time OPEN/CLOSED status

Trading hours

All into a single column, making the layout clean and dashboard-ready.

🧠 Who is this for?

Day traders

Futures traders

Forex traders

Anyone who tracks multiple time zones or global markets

📌 Notes:

Clock updates based on chart timeframe (e.g., every 1m on a 1-minute chart)

Pine Script doesn't support real-time per-second updates, but works well for market status tracking

💬 Feedback Welcome!

This script was designed to be lightweight and user-friendly. Suggestions and improvements are always welcome — feel free to leave a comment or reach out directly.

Prior LevelThe "Prior Level" indicator displays the previous day's key price levels (Open, High, Low, Close) directly on your chart. These reference levels are essential for intraday trading strategies, support/resistance analysis, and breakout identification.

Key features:

- Shows previous session's Open, High, Low and Close values

- Customizable line colors for better visual distinction

- Adjustable line length for cleaner chart appearance

- Optional data table showing exact values

- Simple and lightweight design for easy chart reading

This indicator helps traders identify important price zones from the previous trading session, allowing for more informed trading decisions based on how current price action interacts with these established levels.

CFD Lot Calculator [MT5 Optimized]CFD Position Size Calculator for MT5 (ES/NQ)

A clean, professional Pine Script tool that calculates optimal position sizes in lots for ES/NQ CFDs based on:

Account balance

Risk percentage per trade

Stop loss in pips

Contract size (default = 1 for MT5)

Features:

✅ Bottom-right compact table

✅ Displays risk amount, stop loss, and lot size

✅ Works with any CFD broker (adjust pip/contract values if needed)

✅ Detailed tooltips explain all inputs

Perfect for traders who want precise position sizing without chart clutter.

RiskCalc FX & GoldRiskCalc FX & Gold is a multi-market position sizing tool designed to help you manage risk quickly and accurately. With this script, simply enter your account capital, the percentage of risk you wish to take, and your stop in ticks. Depending on the selected market—Forex or XAUUSD—the script automatically adjusts its calculations:

Forex: Assumes 1 lot equals 100,000 units.

XAUUSD: Assumes 1 lot equals 100 ounces.

The script calculates your risk in dollars and, using a fixed value of 1 USD per tick per lot, determines the ideal position size in both lots and total contracts. Results are displayed in a clear, centralized table at the top of the chart for real-time decision-making.

Perfect for traders operating across multiple markets who need an automated and consistent approach to risk management.

Market Sessions [APIDEVs]Description

The 🐸 Market Sessions 👑 indicator is an advanced and highly customizable tool designed for traders who want to visualize and manage market sessions directly on their TradingView charts. With support for up to four configurable sessions (by default: Sydney, Tokyo, London, and New York), this indicator allows you to adjust times, time zones, day filters, and display styles to suit your trading strategy.

In addition to displaying active sessions on the chart using dotted lines or colored backgrounds, it includes an interactive table that provides a quick overview of each session's status, active hours, and the current date adjusted to your time zone. Ideal for intraday traders, forex traders, or anyone needing precise control over market periods.

Main Features

Customizable Sessions: Define up to four sessions with unique names, times (HHMM-HHMM format), and colors.

Time Zone Adjustment: Select your time zone (UTC-12 to UTC+12) to align the sessions with your local time.

Day Filter: Enable or disable sessions by day of the week (Monday to Sunday).

Flexible Visualization: Choose between dotted lines ("Line"), colored background ("Background"), or no visual representation ("None").

Information Table: Displays session status (🟢 active / 🔴 inactive), active hours, and the current date in a compact and configurable format (adjustable size and position).

Daily Dividers: Optionally, add vertical lines and labels to mark the change of day (useful on timeframes ≤ 4 hours).

How to Use

Add the indicator to your chart.

Configure the sessions in the settings menu:

Enable/disable sessions and define their names, times, and colors.

Select your time zone to synchronize the times.

Choose the days of the week you want the sessions to be visible.

Customize the display:

Decide if you prefer lines, background, or no representation on the chart.

Adjust the size and position of the table according to your needs.

Analyze the sessions in real-time using the table and the chart.

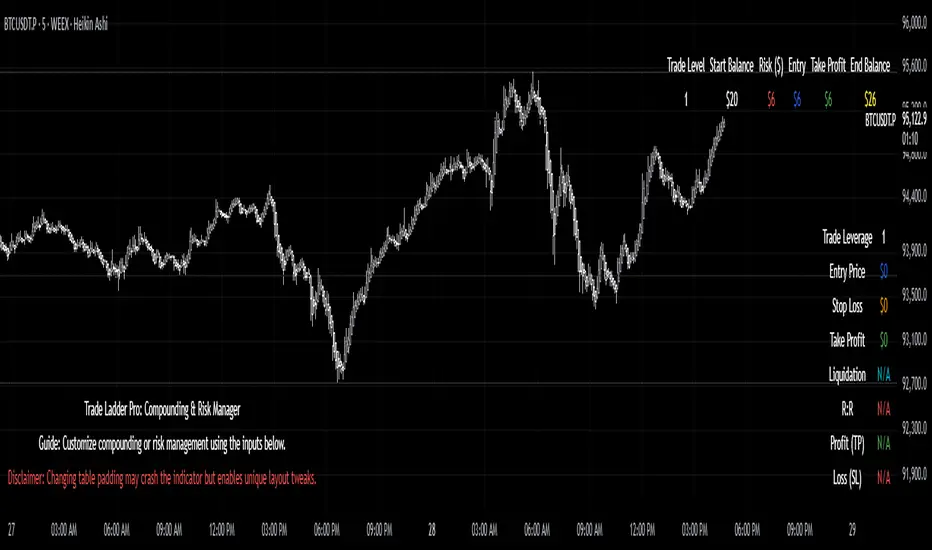

Trade Ladder Pro: Compounding & Risk ManagerTrade Ladder Pro: Compounding & Risk Manager

Inspired by the popular $20 to $52,000 trading challenge, this tool is designed to help you scale your trading account using systematic compounding and enhanced risk management techniques. Whether you’re aiming for disciplined growth or fine-tuning your risk/reward, Trade Ladder Pro offers a flexible approach to visualizing your trade levels.

How to Use:

Inputs:

Compounding Mode:

Set your starting balance, final balance goal, number of trades, and current trade level. You can move to the next trade after a successful trade in settings. The entries are not signals. They are there to help manage risk.

The script calculates the necessary compounding factor to grow your balance across the defined trades.

Risk Management Mode:

In addition to the above, specify a risk percentage and risk/reward ratio.

Input an entry price (or leave it at 0 to use the current price) to automatically compute the stop loss and take profit levels.

Display Options:

Choose the table’s position on the chart (e.g., Top Right, Top Left, Bottom Right, Bottom Left).

Pick between a vertical or horizontal layout for a display that suits your workflow.

Results:

The table will display the trade level, starting balance, risk amount, entry price, take profit, and (if in Risk Management mode) stop loss along with the projected ending balance.

Community & Feedback:

Your feedback is invaluable! Please share any tips or report any errors you encounter so we can continue to improve this tool. Happy trading!

ATR SL and TP with Candle Freeze & DataWindowThis indicator uses the Average True Range (ATR) to automatically calculate your stop loss (SL) and take profit (TP) levels based on the current market volatility and your chosen multipliers. Here's how it works:

ATR Calculation:

The indicator computes the ATR, which measures the average market volatility over a set period. This value helps gauge how much the price typically moves.

SL and TP Determination:

Depending on whether you're in a long or short trade, the SL and TP are calculated relative to the current price:

For a long trade, the stop loss is set below the current price (by subtracting a multiple of the ATR) and the take profit is set above it (by adding a multiple of the ATR).

For a short trade, the calculations are reversed.

Candle Freeze Feature:

Once a new candle starts, the calculated SL and TP values are "frozen" for that candle. This means they remain constant during the candle's formation, preventing them from updating continuously as the price fluctuates. This can make it easier to plan your trades without the levels shifting mid-candle.

Data Window & Labels:

The SL and TP values are plotted on the chart as lines and displayed in labels for quick reference. Additionally, they appear in TradingView's Data Window, so you can easily copy the price numbers if needed.

Overall, the indicator is designed to help you manage your trades by setting dynamic, volatility-adjusted SL and TP levels that only update at the start of each new candle, aligning with your chosen timeframe. Let me know if you have any more questions or need further adjustments!

Pro Volume By TradeINskiOverview

The Pro Volume By TradeINski indicator is a comprehensive trading tool designed to enhance volume analysis, position sizing, and trend identification. It integrates multiple trading metrics into a single dashboard, helping traders make informed decisions based on volume dynamics, momentum bursts, trend intensity, and risk management.

Key Features

1. Position Size Calculator

Helps traders determine optimal position sizes based on risk parameters:

Capital & Risk Amount: Set account size and risk per trade.

Lot Size Adjustments: Automatically calculates nearest lot size for futures trading.

Stop Loss-Based Quantity: Computes position size based on distance from stop-loss levels (LOD or mid-price).

Standard Stop Losses: Predefined stop-loss levels (1%, 1.25%, 1.5%, 1.75%) for quick risk assessment.

Reverse Pyramiding: Enhances position sizing with adjustable risk multipliers (25%, 50%).

Closing Range & Range Expansion: Measures price strength and volatility expansion.

2. Volume Analysis & Bar Coloring

Default Bar Colors: Green for bullish bars, red for bearish bars.

Dry Volume Detection: Highlights low-volume bars (below 20-period SMA) in gray.

3. Momentum Burst (MB)

Identifies high-momentum moves:

Bullish Momentum: Volume surge + price rise ≥ user-defined threshold (default: 4%).

Bearish Momentum: Volume surge + price drop ≥ user-defined threshold (default: -4%).

4. Trend Intensity (TI)

Measures trend strength using moving averages:

Fast MA (7) vs. Slow MA (65): Highlights strong bullish/bearish trends when deviation exceeds sensitivity threshold (default: 5%).

5. Anticipation (ANTS)

Detects consolidation before potential breakouts:

Price Change Range: Filters minor price fluctuations (default: -0.4% to +0.4%).

Trend Confirmation: Requires TI_65 sensitivity (default: 5%) for validation.

6. Episodic Pivot (EP)

Flags unusually high-volume bars (default: 9M+ volume) as potential trend reversal or continuation signals.

7. Data Metrics Table

Displays key trading metrics:

Trend Intensity (TI): 21-period SMA comparison.

Industry & Sector: Stock classification.

Market Cap & Free Float: Fundamental liquidity metrics.

Volume × Price (VP): Monetary value of traded volume.

Relative Volume (RV): Today’s volume vs. previous day.

Persistent Intensity (PI): Count of consecutive up closes (default: 21-period).

Use Cases for Traders

✅ Day Traders: Identify momentum bursts and high-volume breakouts.

✅ Swing Traders: Use trend intensity and episodic pivots to confirm trends.

✅ Position Traders: Optimize risk with dynamic position sizing.

✅ Risk Managers: Set stop-loss levels and reverse pyramiding for controlled exposure.

Settings & Customization Overview

The Pro Volume By TradeINski indicator is a comprehensive trading tool designed to enhance volume analysis, position sizing, and trend identification. It integrates multiple trading metrics into a single dashboard, helping traders make informed decisions based on volume dynamics, momentum bursts, trend intensity, and risk management.

Key Features

1. Position Size Calculator

Helps traders determine optimal position sizes based on risk parameters:

Capital & Risk Amount: Set account size and risk per trade.

Lot Size Adjustments: Automatically calculates nearest lot size for futures trading.

Stop Loss-Based Quantity: Computes position size based on distance from stop-loss levels (LOD or mid-price).

Standard Stop Losses: Predefined stop-loss levels (1%, 1.25%, 1.5%, 1.75%) for quick risk assessment.

Reverse Pyramiding: Enhances position sizing with adjustable risk multipliers (25%, 50%).

Closing Range & Range Expansion: Measures price strength and volatility expansion.

2. Volume Analysis & Bar Coloring

Default Bar Colors: Green for bullish bars, red for bearish bars.

Dry Volume Detection: Highlights low-volume bars (below 20-period SMA) in gray.

3. Momentum Burst (MB)

Identifies high-momentum moves:

Bullish Momentum: Volume surge + price rise ≥ user-defined threshold (default: 4%).

Bearish Momentum: Volume surge + price drop ≥ user-defined threshold (default: -4%).

4. Trend Intensity (TI)

Measures trend strength using moving averages:

Fast MA (7) vs. Slow MA (65): Highlights strong bullish/bearish trends when deviation exceeds sensitivity threshold (default: 5%).

5. Anticipation (ANTS)

Detects consolidation before potential breakouts:

Price Change Range: Filters minor price fluctuations (default: -0.4% to +0.4%).

Trend Confirmation: Requires TI_65 sensitivity (default: 5%) for validation.

6. Episodic Pivot (EP)

Flags unusually high-volume bars (default: 9M+ volume) as potential trend reversal or continuation signals.

7. Data Metrics Table

Displays key trading metrics:

Trend Intensity (TI): 21-period SMA comparison.

Industry & Sector: Stock classification.

Market Cap & Free Float: Fundamental liquidity metrics.

Volume × Price (VP): Monetary value of traded volume.

Relative Volume (RV): Today’s volume vs. previous day.

Persistent Intensity (PI): Count of consecutive up closes (default: 21-period).

Use Cases for Traders

✅ Day Traders: Identify momentum bursts and high-volume breakouts.

✅ Swing Traders: Use trend intensity and episodic pivots to confirm trends.

✅ Position Traders: Optimize risk with dynamic position sizing.

✅ Risk Managers: Set stop-loss levels and reverse pyramiding for controlled exposure.

Settings & Customization

Trade Direction: Long, Short, or Both (auto-detects based on % change).

Table Positioning: Adjust location (Top/Middle/Bottom, Left/Center/Right).

Color Customization: Modify bar colors, table lines, and background.

Trade Direction: Long, Short, or Both (auto-detects based on % change).

Table Positioning: Adjust location (Top/Middle/Bottom, Left/Center/Right).

Color Customization: Modify bar colors, table lines, and background.

Journal Trade By TradeINskiThis indicator, "Journal Trade By TradeINski" (JT), is designed to assist traders in maintaining a comprehensive trade journal directly on their TradingView charts. It provides a customizable table overlay that displays key trade metrics for analysis and record-keeping purposes.

Key Features and Functionality:

Trade Journaling Table:

Displays user-inputted and calculated trade data in a structured table format.

Facilitates the recording of essential trade details, including entry price, stop-loss, position size, and risk parameters.

Risk Management Calculations:

Calculates and displays risk-related information, such as risk percentage, risk amount, and risk per share, to aid in risk management.

Calculates the dollar and percentage distance from entry to stop loss.

Position Sizing Assistance:

Calculates and displays position size as a percentage of account capital.

Displays the quantity of shares/units.

Calculates the quantity based on a half stop loss.

R-Multiple Visualization:

Calculates and displays R-multiples to assess risk-reward ratios.

Offers customizable color coding for R-multiples to visually represent different risk-reward levels.

Trade Management Tools:

Displays information to assist in part selling, and selling into strength strategies.

Displays part numbers, part quantities, and remainders.

User Customization:

Provides various customization options, including table position, size, and color, to suit individual preferences.

This indicator is intended to be a tool for traders to:

Maintain a detailed record of their trades.

Analyze trade performance.

Improve risk management practices.

Enhance trade planning and execution.

VSA Vol Key VSA Signals

(1) No Demand – Bearish Signal

Low volume, narrow spread.

Price rises, but volume does not increase → Weak market, lack of buyers.

If this appears in an uptrend, it may indicate a potential reversal.

(2) No Supply – Bullish Signal

Low volume, narrow spread.

Price declines, but volume does not increase → Weak selling pressure.

If this appears in an uptrend, it may confirm the continuation of the uptrend.

(3) Stopping Volume – Bullish Reversal Signal

Strong price decline, but unusually high volume.

Candle shows a long lower wick, closing near the top.

Indicates Smart Money absorbing supply, signaling a potential reversal upwards.

(4) Climactic Volume – Possible Trend Reversal

Extremely high volume with a sharp price increase or decrease.

If this occurs after a long trend, it may indicate a trend reversal.

Smart Money may be taking profits after a prolonged price movement.

(5) Effort vs. Result

If volume is high but price movement is weak → Inefficient buying/selling, possible reversal.

If volume is high and price moves strongly in the same direction → Trend is likely to continue.

Exact Dynamic Yield SpreadYield Spread Overlay

"Yield Spread Overlay" is an indicator that displays the yield spread between two currencies based on their respective 10-year bond yields. It overlays directly onto the Forex chart, allowing real-time visualization of the relationship between the yield spread and the currency pair's price movements.

This indicator saves time by avoiding the manual addition of bond yields. Unlike manual methods, it supports smaller timeframes (1h, 4h, etc.), making it particularly useful.

Several customization options are available to suit individual preferences:

Custom Display: Adjust the line thickness and color.

Scale Position: Choose between displaying the scale on the right or left side of the chart.

This indicator helps traders better understand currency relationships and can serve as an additional tool within a Forex trading strategy.

All feedback, suggestions, and critiques—positive or negative—are welcome to continually improve this tool.

Trailing Lagged AssetThis indicator allows you to overlay a secondary asset on your main chart with a customizable lag and trailing lag which are additional offsets in relation to the main lag variable.

Daily Range %The Daily Range % Indicator calculates and plots a percentage of the daily range (high to low) based on a custom lookback period. It identifies outside bars from past daily data, prioritizing the most recent unbroken range. If no outside bar is found, it defaults to yesterday's range. The selected percentage of this range is then displayed on the chart, updating once per 5-minute bar (or the chosen resolution).

Mark Hours/Minutes (Formula + Minutes)This Pine Script code is a TradingView indicator that analyzes the hour and minutes of each candle in a 1-minute timeframe and plots a red triangle above the candle if one of the following conditions is met:

Sum/Difference Condition: The sum or the absolute difference of the hours and minutes is equal to 29, 35, or 71, with a tolerance of +/- 1.

Minutes Condition: The minutes are equal to 00, 29, or 35.

This indicator is based on the Goldbach theory and the "algo path" concept popularized by Hopiplaka, which posits that algorithmic trading paths often initiate from minute values of 00, 29, and 35. Use this indicator according to your trading strategy.

Correlation X macroeconomicsFind the correlation between financial assets and the main Brazilian macroeconomic variables:

SELIC rate (Red)

PIB (Green)

Inflation (Blue)

Employment and income (Yellow)

Unlike other indicators that measure the correlation between two assets, the indicator "Correlation X macroeconomics" measures, for example, the correlation that the VALE3 asset has with the SELIC rate.

The correlation is obtained by calculating the variation suffered by a given asset on the day a given Brazilian macroeconomic variable is released.

This indicator can be used on any financial asset.

Use time frame chart = 1 day.

To calculate the correlation, data published by IBGE and the Central Bank of Brazil over a period of time are used. This time period is different depending on the selected macroeconomic variable. Namely:

16 PIB disclosures (4 years)

24 SELIC rate disclosures (3 years)

24 disclosures of IPCA and employment and income data (2 years)

You can select one or more macroeconomic variables to check the effect of correlation separately on each of them.

This indicator "Correlation X macroeconomics" will be updated monthly, as detailed below:

At the end of the day on which the PIB is released

At the end of the day on which employment and income data are released

At the end of the day following the day on which the SELIC rate is published

On the last business day of the month if none of the aforementioned disclosures occur

XAUUSD Correlation IndicatorXAUUSD Correlation Indicator

Questo indicatore per TradingView calcola e visualizza la correlazione tra il prezzo di XAUUSD (oro) e una serie di altri asset finanziari, tra cui valute (EURUSD, AUDUSD, NZDUSD, GBPUSD), metalli preziosi (platino, argento), indici azionari (SPX500, DJI, NASDAQ) e il dollaro statunitense (DXY).

L'indicatore offre:

1. Correlazione: Calcola la correlazione tra XAUUSD e gli altri asset su un periodo personalizzabile, dove un numero superiore allo 0 indica una correlazione positiva ed un numero inferiore allo 0 indica una correlazione negativa.

2. Variazione percentuale: Mostra la variazione percentuale dei prezzi degli asset rispetto all'apertura.

3. Visualizzazione personalizzabile: Permette di ordinare i dati in base alla correlazione o alla variazione percentuale.

4. Tabella interattiva: I risultati sono visualizzati in una tabella colorata, con opzioni per personalizzare i colori di sfondo, testo e bordi.

Ideale per trader e analisti che vogliono monitorare le relazioni tra l'oro e altri mercati in tempo reale, questo strumento aiuta a identificare opportunità di trading basate su correlazioni e tendenze di mercato.

TRP Stop-Loss and Position SizingScript is based on TRP to see both Long Stop Loss and Short Stop Loss, You can Also adjust the position size based on your capital and percentage risk.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

High and Low with Horizontal TableHigh and Low with Horizontal Table Indicator

Overview

The "High and Low with Horizontal Table" indicator is designed for traders who wish to monitor key levels based on specific candle times, along with dynamic risk-to-reward ratios and ATR-based values. This indicator features real-time calculations, visual cues, and a table for quick reference of the calculated values.

Key Features

Custom Time Inputs:

Users can define two specific time inputs to select the candles for the High and Low prices. These times can target the same or separate candles.

ATR-based Calculation:

The indicator allows users to apply an ATR Multiplier to adjust the calculation of key levels. By default, the ATR multiplier is set to 1.2, but users can adjust it to their preferred value (e.g., 1.5 or 2).

Risk-to-Reward (R:R) Calculation:

The Risk-to-Reward Ratio (R:R) is used to calculate potential Take Profit (TP) levels based on the high and low of the selected candle(s).

The default R:R ratio is 2.0, but it can be customized to suit the trader’s strategy.

Visual Markings:

The High and Low values are plotted with subtle markers on the chart (cross style) for easy identification. The display of these markers is subdued for minimal visual distraction.

Horizontal Table Display:

A horizontal table is generated in the top-right corner of the chart, providing a quick reference for the following values:

High and Low of the selected candle(s)

High + ATR Multiplier and Low - ATR Multiplier

R:R ratio

Buy TP and Sell TP levels

Each value is displayed with a reasonable number of decimal places (4 decimals) for major forex pairs, XAUUSD, and BTCUSD.

Input Parameters

Hour and Minute for High Candle: Select the time for the candle that will determine the High.

Hour and Minute for Low Candle: Select the time for the candle that will determine the Low.

ATR Multiplier: A customizable input for adjusting the ATR-based calculations (default is 1.2).

Risk-to-Reward (R:R): Set the ratio to determine the TP levels (default is 2.0).

How It Works

The user defines two distinct time inputs (one for the High and one for the Low).

At the specified times, the indicator captures the High and Low prices of the candles.

The ATR is calculated and adjusted by the user-defined ATR Multiplier to determine buffers above the High and below the Low.

The Risk-to-Reward ratio is applied to calculate the Take Profit levels.

All of these values are displayed on the chart and updated in real time. The horizontal table ensures quick reference to all the key levels without cluttering the main chart.

Use Cases

Trend Trading: Identify potential support and resistance levels based on specific timeframes and adjust TP targets using ATR.

Scalping: Use the ATR and R:R calculations to target precise entry and exit points.

Market Opens: Track key market opens (such as New York and London) with candle times that reflect your trading strategy.

Conclusion

The High and Low with Horizontal Table indicator is a powerful tool for traders looking to combine precise candle-based level tracking with ATR-based risk management. By displaying key levels and TP targets in a clear, tabular format, traders can quickly assess and act on key price levels throughout their trading sessions.

Position Tracker by GG_ALGOPosition Tracker – Custom Stop Loss & Take Profit Calculator

This script is a position tracking tool designed to help traders automatically calculate Stop Loss (SL) and Take Profit (TP) levels based on a given Entry Price. It works across all markets, including Crypto, Forex, Indices, and Stocks.

How It Works :

1️⃣ Set Your Entry Price – Click on the chart to select your trade entry.

2️⃣ Choose Trade Direction – Select Long or Short in the settings.

3️⃣ Customizable Stop Loss & Take Profit

– Users can adjust SL and TP levels in the settings.

The default values are:

Stop Loss (SL): 0.5%

Take Profit (TP) 1: 1%

Take Profit (TP) 2: 2%

Take Profit (TP) 3: 3%

Why Use This Indicator?

✅ Fully Customizable – Adjust SL & TP percentages to match your trading strategy.

✅ Works for All Markets – Supports Crypto, Forex, Stocks, and Indices.

✅ Saves Time – No need for manual SL/TP calculations.

✅ User-Friendly – Just set the entry price and direction, and the script does the rest.

This tool helps traders quickly define risk-reward setups and execute trades efficiently.

Chart Box Session Indicator [The Quant Science]This indicator allows highlighting specific time sessions within a chart by creating colored boxes to represent the price range of the selected session. Is an advanced and flexible tool for chart segmenting trading sessions. Thanks to its extensive customization options and advanced visualization features, it allows traders to gain a clear representation of key market areas based on chosen time intervals.

The indicator offers two range calculation modes:

Body to Body: considers the range between the opening and closing price.

Wick to Wick: considers the range between the session's low and high.

Body To Body

Wick to Wick

Key Features

1. Session Configuration

- Users can select the time range of the session of interest.

- Option to choose the day of the week for the calculation.

- Supports UTC timezone selection to correctly align data.

2. Customizable Visualization

- Option to display session price lines.

- Ability to show a central price line.

- Extension of session lines beyond the specified duration.

3. Design Display Configuration

- Three different background configurations to suit light and dark themes.

- Two gradient modes for session coloring:

- Centered: the color is evenly distributed.

- Off-Centered: the gradient is asymmetrical.

How It Works

The indicator determines whether the current time falls within the selected session, creating a colored box that highlights the corresponding price range. Depending on user preferences, the indicator draws horizontal lines at the minimum and maximum price levels and, optionally, a central line.

During the session:

- The lowest and highest session prices are dynamically updated.

- The range is divided into 10 bands to create a gradient effect.

- A colored box is generated to visually highlight the chosen session.

If the Extend Lines option is enabled, price lines continue even after the session ends, keeping the range visible for further analysis.

This indicator is useful for traders who want to analyze price behavior in specific timeframes. It is particularly beneficial for strategies based on market sessions (e.g., London or New York open) or for identifying accumulation and distribution zones.

200 EMA AlertHow It Works:

The 200 EMA calculates the average price over the last 200 periods, giving more weight to recent price movements for a smoother and more responsive trend line.

It helps traders determine whether the market is in a bullish (above 200 EMA) or bearish (below 200 EMA) phase.

Why Traders Use the 200 EMA:

✅ Trend Confirmation – If the price is above the 200 EMA, the trend is bullish; if below, the trend is bearish.

✅ Dynamic Support & Resistance – Price often reacts around the 200 EMA, making it a key level for entries and exits.

✅ Works on All Timeframes – Whether on the 1-minute chart or the daily timeframe, the 200 EMA is effective for scalping, swing trading, and long-term investing.

✅ Easy to Combine with Other Indicators – Traders pair it with RSI, MACD, or price action for stronger confirmation.

How to Use It in Trading:

📌 Trend Trading – Buy when price pulls back to the 200 EMA in an uptrend; sell when price retests it in a downtrend.

📌 Breakout Strategy – A strong candle breaking above/below the 200 EMA signals a possible trend reversal.

📌 Filtering Trades – Many traders only take long trades above and short trades below the 200 EMA to align with the overall market trend.

Conclusion:

The 200 EMA is an essential indicator for traders of all levels, offering clear trend direction, strong support/resistance zones, and trade filtering for better decision-making. Whether you're trading forex, stocks, or crypto, mastering the 200 EMA can give you a significant edge in the markets. 🚀📈