Fuzzy SMA with DCTI Confirmation[FibonacciFlux]FibonacciFlux: Advanced Fuzzy Logic System with Donchian Trend Confirmation

Institutional-grade trend analysis combining adaptive Fuzzy Logic with Donchian Channel Trend Intensity for superior signal quality

Conceptual Framework & Research Foundation

FibonacciFlux represents a significant advancement in quantitative technical analysis, merging two powerful analytical methodologies: normalized fuzzy logic systems and Donchian Channel Trend Intensity (DCTI). This sophisticated indicator addresses a fundamental challenge in market analysis – the inherent imprecision of trend identification in dynamic, multi-dimensional market environments.

While traditional indicators often produce simplistic binary signals, markets exist in states of continuous, graduated transition. FibonacciFlux embraces this complexity through its implementation of fuzzy set theory, enhanced by DCTI's structural trend confirmation capabilities. The result is an indicator that provides nuanced, probabilistic trend assessment with institutional-grade signal quality.

Core Technological Components

1. Advanced Fuzzy Logic System with Percentile Normalization

At the foundation of FibonacciFlux lies a comprehensive fuzzy logic system that transforms conventional technical metrics into degrees of membership in linguistic variables:

// Fuzzy triangular membership function with robust error handling

fuzzy_triangle(val, left, center, right) =>

if na(val)

0.0

float denominator1 = math.max(1e-10, center - left)

float denominator2 = math.max(1e-10, right - center)

math.max(0.0, math.min(left == center ? val <= center ? 1.0 : 0.0 : (val - left) / denominator1,

center == right ? val >= center ? 1.0 : 0.0 : (right - val) / denominator2))

The system employs percentile-based normalization for SMA deviation – a critical innovation that enables self-calibration across different assets and market regimes:

// Percentile-based normalization for adaptive calibration

raw_diff = price_src - sma_val

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

normalized_diff_raw = raw_diff / diff_abs_percentile

normalized_diff = useClamping ? math.max(-clampValue, math.min(clampValue, normalized_diff_raw)) : normalized_diff_raw

This normalization approach represents a significant advancement over fixed-threshold systems, allowing the indicator to automatically adapt to varying volatility environments and maintain consistent signal quality across diverse market conditions.

2. Donchian Channel Trend Intensity (DCTI) Integration

FibonacciFlux significantly enhances fuzzy logic analysis through the integration of Donchian Channel Trend Intensity (DCTI) – a sophisticated measure of trend strength based on the relationship between short-term and long-term price extremes:

// DCTI calculation for structural trend confirmation

f_dcti(src, majorPer, minorPer, sigPer) =>

H = ta.highest(high, majorPer) // Major period high

L = ta.lowest(low, majorPer) // Major period low

h = ta.highest(high, minorPer) // Minor period high

l = ta.lowest(low, minorPer) // Minor period low

float pdiv = not na(L) ? l - L : 0 // Positive divergence (low vs major low)

float ndiv = not na(H) ? H - h : 0 // Negative divergence (major high vs high)

float divisor = pdiv + ndiv

dctiValue = divisor == 0 ? 0 : 100 * ((pdiv - ndiv) / divisor) // Normalized to -100 to +100 range

sigValue = ta.ema(dctiValue, sigPer)

DCTI provides a complementary structural perspective on market trends by quantifying the relationship between short-term and long-term price extremes. This creates a multi-dimensional analysis framework that combines adaptive deviation measurement (fuzzy SMA) with channel-based trend intensity confirmation (DCTI).

Multi-Dimensional Fuzzy Input Variables

FibonacciFlux processes four distinct technical dimensions through its fuzzy system:

Normalized SMA Deviation: Measures price displacement relative to historical volatility context

Rate of Change (ROC): Captures price momentum over configurable timeframes

Relative Strength Index (RSI): Evaluates cyclical overbought/oversold conditions

Donchian Channel Trend Intensity (DCTI): Provides structural trend confirmation through channel analysis

Each dimension is processed through comprehensive fuzzy sets that transform crisp numerical values into linguistic variables:

// Normalized SMA Deviation - Self-calibrating to volatility regimes

ndiff_LP := fuzzy_triangle(normalized_diff, norm_scale * 0.3, norm_scale * 0.7, norm_scale * 1.1)

ndiff_SP := fuzzy_triangle(normalized_diff, norm_scale * 0.05, norm_scale * 0.25, norm_scale * 0.5)

ndiff_NZ := fuzzy_triangle(normalized_diff, -norm_scale * 0.1, 0.0, norm_scale * 0.1)

ndiff_SN := fuzzy_triangle(normalized_diff, -norm_scale * 0.5, -norm_scale * 0.25, -norm_scale * 0.05)

ndiff_LN := fuzzy_triangle(normalized_diff, -norm_scale * 1.1, -norm_scale * 0.7, -norm_scale * 0.3)

// DCTI - Structural trend measurement

dcti_SP := fuzzy_triangle(dcti_val, 60.0, 85.0, 101.0) // Strong Positive Trend (> ~85)

dcti_WP := fuzzy_triangle(dcti_val, 20.0, 45.0, 70.0) // Weak Positive Trend (~30-60)

dcti_Z := fuzzy_triangle(dcti_val, -30.0, 0.0, 30.0) // Near Zero / Trendless (~+/- 20)

dcti_WN := fuzzy_triangle(dcti_val, -70.0, -45.0, -20.0) // Weak Negative Trend (~-30 - -60)

dcti_SN := fuzzy_triangle(dcti_val, -101.0, -85.0, -60.0) // Strong Negative Trend (< ~-85)

Advanced Fuzzy Rule System with DCTI Confirmation

The core intelligence of FibonacciFlux lies in its sophisticated fuzzy rule system – a structured knowledge representation that encodes expert understanding of market dynamics:

// Base Trend Rules with DCTI Confirmation

cond1 = math.min(ndiff_LP, roc_HP, rsi_M)

strength_SB := math.max(strength_SB, cond1 * (dcti_SP > 0.5 ? 1.2 : dcti_Z > 0.1 ? 0.5 : 1.0))

// DCTI Override Rules - Structural trend confirmation with momentum alignment

cond14 = math.min(ndiff_NZ, roc_HP, dcti_SP)

strength_SB := math.max(strength_SB, cond14 * 0.5)

The rule system implements 15 distinct fuzzy rules that evaluate various market conditions including:

Established Trends: Strong deviations with confirming momentum and DCTI alignment

Emerging Trends: Early deviation patterns with initial momentum and DCTI confirmation

Weakening Trends: Divergent signals between deviation, momentum, and DCTI

Reversal Conditions: Counter-trend signals with DCTI confirmation

Neutral Consolidations: Minimal deviation with low momentum and neutral DCTI

A key innovation is the weighted influence of DCTI on rule activation. When strong DCTI readings align with other indicators, rule strength is amplified (up to 1.2x). Conversely, when DCTI contradicts other indicators, rule impact is reduced (as low as 0.5x). This creates a dynamic, self-adjusting system that prioritizes high-conviction signals.

Defuzzification & Signal Generation

The final step transforms fuzzy outputs into a precise trend score through center-of-gravity defuzzification:

// Defuzzification with precise floating-point handling

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10

fuzzyTrendScore := (strength_SB * STRONG_BULL + strength_WB * WEAK_BULL +

strength_N * NEUTRAL + strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1.0 (Strong Bear) to +1.0 (Strong Bull), with critical threshold zones at ±0.3 (Weak trend) and ±0.7 (Strong trend). The histogram visualization employs intuitive color-coding for immediate trend assessment.

Strategic Applications for Institutional Trading

FibonacciFlux provides substantial advantages for sophisticated trading operations:

Multi-Timeframe Signal Confirmation: Institutional-grade signal validation across multiple technical dimensions

Trend Strength Quantification: Precise measurement of trend conviction with noise filtration

Early Trend Identification: Detection of emerging trends before traditional indicators through fuzzy pattern recognition

Adaptive Market Regime Analysis: Self-calibrating analysis across varying volatility environments

Algorithmic Strategy Integration: Well-defined numerical output suitable for systematic trading frameworks

Risk Management Enhancement: Superior signal fidelity for risk exposure optimization

Customization Parameters

FibonacciFlux offers extensive customization to align with specific trading mandates and market conditions:

Fuzzy SMA Settings: Configure baseline trend identification parameters including SMA, ROC, and RSI lengths

Normalization Settings: Fine-tune the self-calibration mechanism with adjustable lookback period, percentile rank, and optional clamping

DCTI Parameters: Optimize trend structure confirmation with adjustable major/minor periods and signal smoothing

Visualization Controls: Customize display transparency for optimal chart integration

These parameters enable precise calibration for different asset classes, timeframes, and market regimes while maintaining the core analytical framework.

Implementation Notes

For optimal implementation, consider the following guidance:

Higher timeframes (4H+) benefit from increased normalization lookback (800+) for stability

Volatile assets may require adjusted clamping values (2.5-4.0) for optimal signal sensitivity

DCTI parameters should be aligned with chart timeframe (higher timeframes require increased major/minor periods)

The indicator performs exceptionally well as a trend filter for systematic trading strategies

Acknowledgments

FibonacciFlux builds upon the pioneering work of Donovan Wall in Donchian Channel Trend Intensity analysis. The normalization approach draws inspiration from percentile-based statistical techniques in quantitative finance. This indicator is shared for educational and analytical purposes under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Past performance does not guarantee future results. All trading involves risk. This indicator should be used as one component of a comprehensive analysis framework.

Shout out @DonovanWall

Cerca negli script per "中海油+10年股价涨幅"

IWMA - DolphinTradeBot1️⃣ WHAT IS IT ?

▪️ The Inverted Weighted Moving Average (IWMA) is the reversed version of WMA, where older prices receive higher weights, while recent prices receive lower weights. As a result, IWMA focuses more on past price movements while reducing sensitivity to new prices.

2️⃣ HOW IS IT WORK ?

🔍 To understand the IWMA(Inverted Weighted Moving Average) indicator, let's first look at how WMA (Weighted Moving Average) is calculated.

LET’S SAY WE SELECTED A LENGTH OF 5, AND OUR CURRENT CLOSING VALUES ARE .

▪️ WMA Calculation Method

When calculating WMA, the most recent price gets the highest weight, while the oldest price gets the lowest weight.

The Calculation is ;

( 10 ×1)+( 12 ×2)+( 21 ×3)+( 24 ×4)+( 38 ×5) = 10+24+63+96+190 = 383

1+2+3+4+5 = 15

WMA = 383/15 ≈ 25.53

WMA = ta.wma(close,5) = 25.53

▪️ IWMA Calculation Method

The Inverted Weighted Moving Average (IWMA) is the reversed version of WMA, where older prices receive higher weights, while recent prices receive lower weights. As a result, IWMA focuses more on past price movements while reducing sensitivity to new prices.

The Calculation is ;

( 10 ×5)+( 12 ×4)+( 21 ×3)+( 24 ×2)+( 38 ×1) = 50+48+63+48+38 = 247

1+2+3+4+5 = 15

IWMA = 247/15 ≈ 16.46

IWMA = iwma(close,5) = 16.46

3️⃣ SETTINGS

in the indicator's settings, you can change the length and source used for calculation.

With the default settings, when you first add the indicator, only the iwma will be visible. However, to observe how much it differs from the normal wma calculation, you can enable the "show wma" option to see both indicators with the same settings or you can enable the Show Signals to see IWMA and WMA crossover signals .

4️⃣ 💡 SOME IDEAS

You can use the indicator for support and resistance level analysis or trend analysis and reversal detection with short and long moving averages like regular moving averages.

Another option is to consider whether the iwma is above or below the normal wma or to evaluate the crossovers between wma and iwma.

db.Volume Spike IndicatorAn indicator that finds the average volume of the previous 10 candles and compares it with the volume of the last closed candle. If the volume of the last candle is 5 times the average of the last 10 candles, it marks this candle with a yellow symbol above or below the candle, depending on the direction of the candle.

=====

Индикатор, который находит среднее значение объём предыдущих 10 свечей и сравнивает его с объёмом последней закрытой свечи. Если объём последней свечи в 5 раз больше среднего за последние 10, то помечает эту свечу жёлтым символом над или под свечой в зависимости от направления свечи.

BTCUSD with adjustable sl,tpThis strategy is designed for swing traders who want to enter long positions on pullbacks after a short-term trend shift, while also allowing immediate short entries when conditions favor downside movement. It combines SMA crossovers, a fixed-percentage retracement entry, and adjustable risk management parameters for optimal trade execution.

Key Features:

✅ Trend Confirmation with SMA Crossover

The 10-period SMA crossing above the 25-period SMA signals a bullish trend shift.

The 10-period SMA crossing below the 25-period SMA signals a bearish trend shift.

Short trades are only taken if the price is below the 150 EMA, ensuring alignment with the broader trend.

📉 Long Pullback Entry Using Fixed Percentage Retracement

Instead of entering immediately on the SMA crossover, the strategy waits for a retracement before going long.

The pullback entry is defined as a percentage retracement from the recent high, allowing for an optimized entry price.

The retracement percentage is fully adjustable in the settings (default: 1%).

A dynamic support level is plotted on the chart to visualize the pullback entry zone.

📊 Short Entry Rules

If the SMA(10) crosses below the SMA(25) and price is below the 150 EMA, a short trade is immediately entered.

Risk Management & Exit Strategy:

🚀 Take Profit (TP) – Fully customizable profit target in points. (Default: 1000 points)

🛑 Stop Loss (SL) – Adjustable stop loss level in points. (Default: 250 points)

🔄 Break-Even (BE) – When price moves in favor by a set number of points, the stop loss is moved to break-even.

📌 Extra Exit Condition for Longs:

If the SMA(10) crosses below SMA(25) while the price is still below the EMA150, the strategy force-exits the long position to avoid reversals.

How to Use This Strategy:

Enable the strategy on your TradingView chart (recommended for stocks, forex, or indices).

Customize the settings – Adjust TP, SL, BE, and pullback percentage for your risk tolerance.

Observe the plotted retracement levels – When the price touches and bounces off the level, a long trade is triggered.

Let the strategy manage the trade – Break-even protection and take-profit logic will automatically execute.

Ideal Market Conditions:

✅ Trending Markets – The strategy works best when price follows strong trends.

✅ Stocks, Indices, or Forex – Can be applied across multiple asset classes.

✅ Medium-Term Holding Period – Suitable for swing trades lasting days to weeks.

Equity Curve with Trend Indicator (Long & Short) - SimulationOverview:

Market Regime Detector via Virtual Equity Curve is a unique indicator that simulates the performance of a trend-following trading system—incorporating both long and short trades—to help you identify prevailing market regimes. By generating a “virtual equity” curve based on simple trend signals and applying trend analysis directly on that curve, this indicator visually differentiates trending regimes from mean-reverting (or sideways) periods. The result is an intuitive display where green areas indicate a trending (bullish) regime (i.e., where trend-following strategies are likely to perform well) and red areas indicate a mean-reverting (bearish) regime.

Features:

Simulated Trade Performance:

Uses a built-in trend-following logic (a simple 10/50 SMA crossover example) to simulate both long and short trades. This simulation creates a virtual equity curve that reflects the cumulative performance of the system over time.

Equity Trend Analysis:

Applies an Exponential Moving Average (EMA) to the simulated equity curve to filter short-term noise. The EMA acts as a trend filter, enabling the indicator to determine if the equity curve is in an upward (trending) or downward (mean-reverting) phase.

Dynamic Visual Regime Detection:

Fills the area between the equity curve and its EMA with green when the equity is above the EMA (indicating a healthy trending regime) and red when below (indicating a mean-reverting or underperforming regime).

Customizable Parameters:

Easily adjust the initial capital, the length of the equity EMA, and other settings to tailor the simulation and visual output to your trading style and market preferences.

How It Works:

Trade Simulation:

The indicator generates trading signals using a simple SMA crossover:

When the 10-period SMA is above the 50-period SMA, it simulates a long entry.

When the 10-period SMA is below the 50-period SMA, it simulates a short entry. The virtual equity is updated bar-by-bar based on these simulated positions.

Equity Trend Filtering:

An EMA is calculated on the simulated equity curve to smooth out fluctuations. The relative position of the equity curve versus its EMA is then used as a proxy for the market regime:

Bullish Regime: Equity is above its EMA → fill area in green.

Bearish Regime: Equity is below its EMA → fill area in red.

Visualization:

The indicator plots:

A gray line representing the simulated equity curve.

An orange line for the EMA of the equity curve.

A dynamic fill between the two lines, colored green or red based on the prevailing regime.

Inputs & Customization:

Initial Capital: Set your starting virtual account balance (default: 10,000 USD).

Equity EMA Length: Specify the lookback period for the EMA applied to the equity curve (default: 30).

Trend Signal Logic:

The current implementation uses a simple SMA crossover for demonstration purposes. Users can modify or replace this logic with their own trend-following indicator to tailor the simulation further.

Smart Scalper Indicator🎯 How the Smart Scalper Indicator Works

1. EMA (Exponential Moving Average)

EMA 10 (Blue Line):

Shows the short-term trend.

If the price is above this line, the trend is bullish; if below, bearish.

EMA 20 (Orange Line):

Displays the longer-term trend.

If EMA 10 is above EMA 20, it indicates a bullish trend (Buy signal).

2. SuperTrend

Green Line:

Represents support levels.

If the price is above the green line, the market is considered bullish.

Red Line:

Represents resistance levels.

If the price is below the red line, the market is considered bearish.

3. VWAP (Volume Weighted Average Price)

Purple Line:

Indicates the average price considering volume.

If the price is above the VWAP, the market is strong (Buy signal).

If the price is below the VWAP, the market is weak (Sell signal).

4. ATR (Average True Range)

Used to measure market volatility.

An increasing ATR indicates higher market activity, enhancing the reliability of signals.

ATR is not visually displayed but is factored into the signal conditions.

⚡ Entry Signals

Green Up Arrow (Buy):

EMA 10 is above EMA 20.

The price is above the SuperTrend green line.

The price is above the VWAP.

Volatility (ATR) is increasing.

Red Down Arrow (Sell):

EMA 10 is below EMA 20.

The price is below the SuperTrend red line.

The price is below the VWAP.

Volatility (ATR) is increasing.

🔔 Alerts

"Buy Alert" — Notifies when a Buy condition is met.

"Sell Alert" — Notifies when a Sell condition is met.

✅ How to Use the Indicator:

Add the indicator to your TradingView chart.

Enable alerts to stay updated on signal triggers.

Check the signal:

A green arrow suggests a potential Buy.

A red arrow suggests a potential Sell.

Set Stop-Loss:

Below the SuperTrend line or based on ATR levels.

Take Profit:

Target 1-2% for short-term trades.

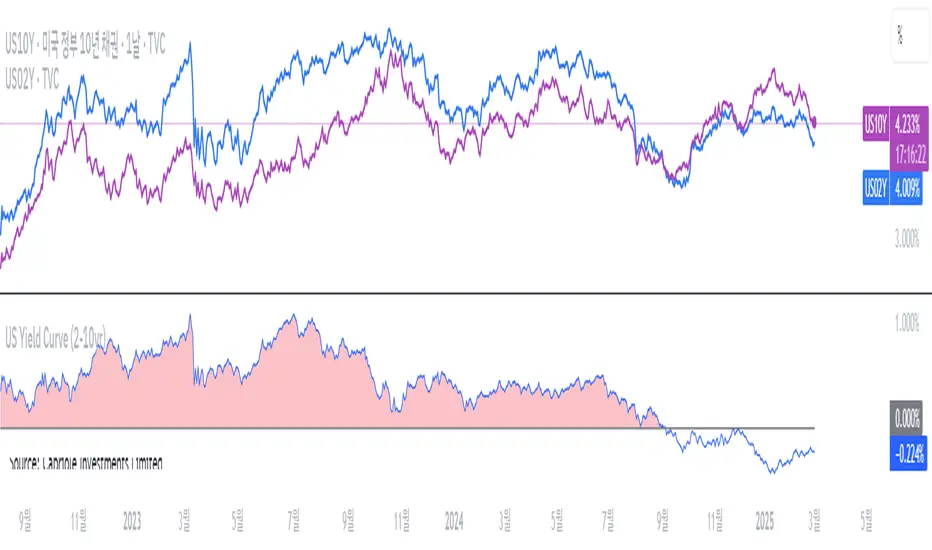

US Yield Curve (2-10yr)US Yield Curve (2-10yr) by oonoon

2-10Y US Yield Curve and Investment Strategies

The 2-10 year US Treasury yield spread measures the difference between the 10-year and 2-year Treasury yields. It is a key indicator of economic conditions.

Inversion (Spread < 0%): When the 2-year yield exceeds the 10-year yield, it signals a potential recession. Investors may shift to long-term bonds (TLT, ZROZ), gold (GLD), or defensive stocks.

Steepening (Spread widening): A rising 10-year yield relative to the 2-year suggests economic expansion. Investors can benefit by shorting bonds (TBT) or investing in financial stocks (XLF). The Amundi US Curve Steepening 2-10Y ETF can be used to profit from this trend.

Monitoring the curve: Traders can track US10Y-US02Y on TradingView for real-time insights and adjust portfolios accordingly.

Vertical Lines at Specific Times### **Script Description**

This **Pine Script v6** indicator for **TradingView** plots **vertical dotted lines** at user-specified times, marking key time ranges during the day. It is designed to help traders visually track market movements within specific timeframes.

#### **Features:**

✔ **Custom Timeframes:**

- Two separate time ranges can be defined:

- **Morning Session:** (Default: 9 AM - 10 AM, New York Time)

- **Evening Session:** (Default: 9 PM - 10 PM, New York Time)

✔ **Adjustable Line Properties:**

- **Line Width:** Users can change the thickness of the vertical lines.

- **Line Colors:** Users can select different colors for morning and evening session lines.

✔ **New York Local Time Support:**

- Ensures that the vertical lines appear correctly based on **Eastern Time (ET)**.

✔ **Full-Height Vertical Lines:**

- Lines extend across the **entire chart**, from the highest high to the lowest low, for clear visibility.

- Uses **dotted line style** to avoid cluttering the chart.

#### **How It Works:**

1. The script retrieves the **current date** (year, month, day) in **New York time**.

2. Converts the **user-defined input times** into **timestamps** for accurate placement.

3. When the current time matches a specified session time, a **dotted vertical line** is drawn.

4. The script **repeats this process daily**, ensuring automatic updates.

#### **Customization Options (Inputs):**

- **Morning Start & End Time** (Default: 9 AM - 10 AM)

- **Evening Start & End Time** (Default: 9 PM - 10 PM)

- **Line Width** (Default: 2)

- **Morning Line Color** (Default: Blue)

- **Evening Line Color** (Default: Green)

#### **Use Case Scenarios:**

📈 Marking market **open & close** hours.

📊 Highlighting **key trading sessions** for day traders.

🔎 Identifying time-based **price action patterns**.

Enhanced Volume Profile█ OVERVIEW

The Enhanced Volume Profile (EVP) is an indicator designed to plot a volume profile on the chart based on either the visible chart range or a fixed lookback period. The script helps analyze the distribution of volume at different price levels over time, providing insights into areas of high trading activity and potential support/resistance zones.

█ KEY FEATURES

1. Visible Chart Range vs. Fixed Lookback Depth

Visible Chart Range

- Default analysis mode

- Calculates profile based on visible portion of the chart

- Dynamically updates with chart view changes

Fixed Lookback Depth

- Optional alternative to visible range

- Uses specified number of bars (10-3000)

- Provides consistent analysis depth

- Independent of chart view

2. Custom Resolution

Auto-Resolution Mode

Automatically selects timeframes based on chart's current timeframe:

≤ 1 minute: Uses 1-minute resolution

≤ 5 minutes: Uses 1-minute resolution

≤ 15 minutes: Uses 5-minute resolution

≤ 1 hour: Uses 5-minute resolution

≤ 4 hours: Uses 15-minute resolution

≤ 12 hours: Uses 15-minute resolution

≤ 1 day: Uses 1-hour resolution

≤ 3 days: Uses 2-hours resolution

≤ 1 week: Uses 4-hours resolution

Custom Resolution Override

Optional override of auto-resolution system

Provides control over data granularity

Must be lower than or equal to chart's timeframe

Falls back to auto-resolution if validation fails

3. Volume Profile Resolution

Adjustable number of points (10-400)

Controls profile granularity

Higher resolution provides more detail

Balance between precision and performance

4. Point of Control (PoC)

Identifies price level with highest traded volume

Optional display with customizable appearance

Adjustable line thickness (1-30)

Configurable color

5. Value Area (VA)

Shows price range of majority trading volume

Adjustable coverage (5-95%), default is 68%

Customizable boundary lines

Configurable lines color and thickness (1-20)

█ INPUT PARAMETERS

Lookback Settings

Use Visible Chart Range

- Default: true

- Calculates profile based on visible bars

- Ideal for focused analysis

Fixed Lookback Bars

- Range: 10-3000

- Default: 200

- Used when visible range is disabled

Resolution Settings

Enable Custom Resolution

- Default: false

- Overrides auto-resolution

Custom Resolution

- Default: 1-minute

- Changes automatically when "Enable Custom Resolution" is disabled

Volume Profile Appearance

Profile Resolution

- Range: 10-400

- Default: 200

- Controls detail level

Profile Width Scale

- Range: 1-50

- Default: 15

- Adjusts profile width

Right Offset

- Range: 0-500

- Default: 20

- Controls spacing from price bars

Profile Fill Color

- Default: #5D606B (70% transparency)

Point of Control Settings

Show Point of Control

- Default: true

- Toggles PoC visibility

PoC Line Thickness

- Range: 1-30

- Default: 1

PoC Line Color

- Default: Red

Value Area Settings

Show Value Area

- Default: true

- Toggles VA lines

Value Area Coverage

- Range: 5-95%

- Default: 68%

Value Area Line Color

- Default: Blue

Value Area Line Thickness

- Range: 1-20

- Default: 1

█ TECHNICAL IMPLEMENTATION DETAILS

Exceeding Bars Management

The script dynamically adjusts the number of bars used in the volume profile calculation based on the selected timeframe and the maximum allowed bars (max_bars_back).

If the total number of bars exceeds the predefined threshold (6000 bars), the script reduces the lookback period (lookback_bars) by trimming some of the historical data, ensuring the chart does not become overloaded with data.

The adjustment is made based on the ratio of bars per candle (bars_per_candle), ensuring that the volume profile remains computationally efficient while maintaining its relevance.

█ EXAMPLE USE CASES

1. Visible Range Mode

For analyzing a recent trend and focusing on only the visible part of the chart, enabling the "Use Visible Chart Range" option calculates the profile based on the current view, without considering historical data outside the visible area.

2. Fixed Lookback Depth

For analyzing a specific period in the past (e.g., the last 200 bars), disabling the visible range and setting a fixed lookback depth of 200 bars ensures the profile always considers the last 200 bars, regardless of the visible range.

3. Custom Resolution

If there’s a need for greater control over the timeframe used for volume profile calculations (e.g., using a 5-minute resolution on a 15-minute chart), enabling custom resolution and setting the desired timeframe provides this control.

HAPPY TRADING ✌️

The Final Countdown//Credit to ©SamRecio for the original indicator that this is based on, which is called, "HTF Bar Close Countdown".

Here are the key differences between the two indicators (That a user would care about):

1.) 10 timeframe slots (double the original number).

2.) Many more timeframe options ('1', '3', '5', '10', '15', '30', '45', '1H', '2H', '4H', '6H', '8H', '12H', 'D', 'W').

3.) Ability to structure timeframes however you want (Higher up top descending, vice versa, or just randomly.).

4.) Support for hour-based timeframes (1H, 2H, etc.).

5.) Displays minutes as numbers, hours with a number followed by H (ex. 1H), and anything above with a letter (D for day, W for week).

6.) Dynamic colors based on remaining time percentage (green->yellow->red) with two user-defined thresholds.

7.) Alerts for when timeframes are close to closing (yellow->red).

8.) More granular timeframe selection options.

9.) Background colors for an additional visual alert.

------Colors background the selected color for each timeframe (Default is all timeframes are blue with 80% transparency).

------This does not repaint, so the color will persist once the red condition is over.

------As soon as you leave the timeframe though, it will be erased and the new timeframe will begin tracking red conditions.

------It always starts from the current bar, so it is not applicable to historical bars unless you leave it running for an extended period of time.

------Do note that since this is not actual paint or colored pencils, the colors do not blend.

------The most recent timeframe to enter a red condition will be the background that you see unless you leave the timeframe and return.

--------------------------------------------------------------------------------------------------------------------

Now for the description and instructions....

IT'S THE FINAL COUNTDOWN!

This indicator helps shorter-timeframe traders track multiple timeframe closings simultaneously, providing visual, audio and notification alerts when bars are nearing their close. It's particularly useful for traders who want to prepare for potential price action around bar closings across different timeframes. If you're a HODL till you're broke kind of trader, you don't need this.

-------------------------------

Multi-Timeframe Tracking

-------------------------------

- Monitors up to 10 different timeframes simultaneously

- Supports various timeframes from 1 minute to weekly (1m, 3m, 5m, 10m, 15m, 30m, 45m, 1H, 2H, 4H, 6H, 8H, 12H, Daily, Weekly)

- Timeframes can be arranged in any order (ascending, descending, or custom)

-----------------

Visual Display

-----------------

- Shows a countdown timer for each selected timeframe

- Dynamic color changes based on time remaining:

Green: More than 15% of bar time remaining

Yellow: Between 15% and 5% remaining

Red: Less than 5% remaining

- Customizable background colors appear when timeframes enter their red zone

----------------

Alert System

----------------

- Built-in alerts trigger when any timeframe enters its red zone

- Each timeframe can have its alerts toggled independently

------

-------------

--------------------------

- Setup Instructions -

--------------------------

-------------

------

-------------------------

Timeframe Selection

-------------------------

- Choose up to 10 timeframes to monitor

- Each timeframe has its own toggle switch to turn it on/off

- Default configuration starts from 5m and goes up to 12H

-------------------------

Visual Customization

-------------------------

- Adjust the table size, position

- Customize frame and border colors

- Modify the yellow and red threshold percentages

--------------------------------

Background Color Settings

--------------------------------

- Enable/disable background colors for each timeframe

- Choose custom colors for each timeframe's background

- Default setting is blue (with a fixed 80% transparency)

-------------

Usage Tips

-------------

- Use the countdown table to prepare for multiple timeframe closes as big moves (especially reversals) tend to begin come after higher timeframe changes (sometimes to the second).

- Watch for color changes to anticipate important closing periods to avoid getting trapped in bad trade (please always use stop losses if trading, in general).

- Set up alerts for critical timeframes that require immediate attention (2H, 4H, etc.).

- Use background colors as an additional visual cue for timeframe closes.

- Position the table where it won't interfere with your chart analysis.

BBSS+This Pine Script implements a custom indicator overlaying Bollinger Bands with additional features for trend analysis using Exponential Moving Averages (EMAs). Here's a breakdown of its functionality:

Bollinger Bands:

The script calculates the Bollinger Bands using a 20-period Simple Moving Average (SMA) as the basis and a multiplier of 2 for the standard deviation.

It plots the Upper Band and Lower Band in red.

EMA Calculations:

Three EMAs are calculated for the close price with periods of 5, 10, and 40.

The EMAs are plotted in green (5-period), cyan (10-period), and orange (40-period) to distinguish between them.

Trend Detection:

The script determines bullish or bearish EMA alignments:

Bullish Order: EMA 5 > EMA 10 > EMA 40.

Bearish Order: EMA 5 < EMA 10 < EMA 40.

Entry Signals:

Long Entry: Triggered when:

The close price crosses above the Upper Bollinger Band.

The Upper Band is above its 5-period SMA (indicating momentum).

The EMAs are in a bullish order.

Short Entry: Triggered when:

The close price crosses below the Lower Bollinger Band.

The Lower Band is below its 5-period SMA.

The EMAs are in a bearish order.

Trend State Tracking:

A variable tracks whether the market is in a Long or Short trend based on conditions:

A Long trend continues unless conditions for a Short Entry are met or the Upper Band dips below its average.

A Short trend continues unless conditions for a Long Entry are met or the Lower Band rises above its average.

Visual Aids:

Signal Shapes:

Triangle-up shapes indicate Long Entry points below the bar.

Triangle-down shapes indicate Short Entry points above the bar.

Bar Colors:

Green bars indicate a Long trend.

Red bars indicate a Short trend.

This script combines Bollinger Bands with EMA crossovers to generate entry signals and visualize market trends, making it a versatile tool for identifying momentum and trend reversals.

G&S SMT### Description of the Pine Script

This Pine Script is designed to identify **Smart Money Technique (SMT)** setups between **Gold (GC1!)** and **Silver (SI1!) Futures** on a **15-minute timeframe**. It specifically looks for divergences between the price movements of Gold and Silver over the last 4 candles and compares it with the next candle's price movement. The script provides **Bullish** and **Bearish** signals for SMT during a specified time range of **8:45 AM EST to 10:30 AM EST**.

### Key Features of the Script:

1. **Futures Symbols**:

- The script uses **Gold Futures (GC1!)** and **Silver Futures (SI1!)** on a 15-minute timeframe to monitor their price movements.

2. **Time Range Filtering**:

- The signals are only active between **8:45 AM EST and 10:30 AM EST**, ensuring that the script only signals within the most relevant trading hours for your strategy.

3. **SMT Calculation (Last 4 Candles vs Next Candle)**:

- **Gold and Silver Price Change Calculation**: The script compares the price changes of **Gold** and **Silver** over the **last 4 candles** and then compares them with the price movement of the **next candle**:

- **Bullish SMT**: Occurs when Gold shows an increase in the last 4 candles while Silver shows a decrease, and both Gold and Silver show an increase in the next candle.

- **Bearish SMT**: Occurs when Gold shows a decrease in the last 4 candles while Silver shows an increase, and both Gold and Silver show a decrease in the next candle.

4. **Bullish and Bearish Signals**:

- **Bullish SMT Signal**: The script will plot a **green** arrow below the bar when a Bullish SMT setup is identified.

- **Bearish SMT Signal**: A **red** arrow above the bar is plotted when a Bearish SMT setup is identified.

5. **Gold and Silver Difference Plot**:

- The difference between the prices of **Gold** and **Silver** is plotted as a **blue line**, giving a visual representation of the relationship between the two assets. When the difference line moves significantly, it can indicate a potential divergence or convergence in the prices of Gold and Silver.

### Script Logic Breakdown:

1. **Price Change for Last 4 Candles**:

- The script calculates the price change for Gold and Silver from the 4th-to-last candle to the last candle.

- `gold_change_last4` and `silver_change_last4` calculate these price differences.

2. **Price Change for Next Candle**:

- It then calculates the price change from the last candle to the next candle.

- `gold_change_next` and `silver_change_next` calculate these price differences.

3. **Bullish SMT Condition**:

- If Gold increased while Silver decreased in the last 4 candles, and both Gold and Silver show an increase in the next candle, it indicates a **Bullish SMT**.

4. **Bearish SMT Condition**:

- If Gold decreased while Silver increased in the last 4 candles, and both Gold and Silver show a decrease in the next candle, it indicates a **Bearish SMT**.

5. **Time Filter**:

- Signals are only plotted when the current time is between **8:45 AM EST and 10:30 AM EST** to match your preferred trading hours.

### Visualization:

- **Bullish Signals**: Plotted as **green arrows** below the bars when a Bullish SMT setup is identified.

- **Bearish Signals**: Plotted as **red arrows** above the bars when a Bearish SMT setup is identified.

- **Gold - Silver Difference**: A **blue line** is plotted to show the price difference between Gold and Silver, helping visualize any divergence.

### How It Helps:

- **Divergence Identification**: This script highlights potential divergences between Gold and Silver Futures, which can provide insights into market sentiment and smart money movements.

- **Focus on Relevant Time Frame**: By filtering signals between 8:45 AM EST and 10:30 AM EST, you are focusing on a timeframe that can be more beneficial for trading.

- **Visual Clarity**: The arrows and the price difference line provide clear signals and a visual representation of the relationship between Gold and Silver, helping you make informed trading decisions.

This script is an automated approach to detecting **SMT setups** and helping traders recognize when Gold and Silver might be signaling a bullish or bearish move based on their divergence patterns.

Alerts and symbolswhat is "Alerts and symbols"?

It is an indicator that allows you to watch more trading pairs and add alarms to them.

what it does?

It allows you to set a total of 20 different intersection alarms, 2 in each pair, for 10 different trading pairs at the same time.

It draws the candlestick chart of a pair you choose among 10 trading pairs and the alarm lines you created for this trading pair on the chart.

It also allows you to see the prices of 10 different trading pairs at the same time, thanks to the table it creates.

how to use it?

First, select the alarm pairs you want to use, for example, BTCUSDT pair is the default value for "pair 1". You can choose 10 different trading pairs as you wish. Just below each trading pair, there are two different sections titled "line 1" and "line 2" so that you can set an alarm. Type here the price levels at which you want to be alerted in case of a price crossover.

You can use the "candle source" section to examine the candlestick charts of trading pairs. The indicator draws the candle chart of the trading pair selected in the "candle source" section.

Check the "show alert lines on chart" box to see the levels you have set an alarm for.

When everything is ready, first click on the three dots next to the indicator's name and then on the clock icon. then create an alarm and that's it.

Auto-Support v 0.3The "Auto-Support v 0.3" indicator is designed to automatically detect and plot multiple levels of support and resistance on a chart. It aims to help traders identify key price levels where the market tends to reverse or consolidate. Here’s a breakdown of its functionality and goals:

Objective:

The primary objective of the Auto-Support v 0.3 indicator is to provide traders with a clear, visual representation of support and resistance levels. These levels are determined based on a predefined sensitivity parameter, which adjusts how tightly or loosely the indicator reacts to recent price movements. The indicator can be applied to any chart to assist in identifying potential entry and exit points for trades, enhancing technical analysis by displaying these important price zones.

Description:

Support and Resistance Calculation:

The indicator calculates multiple levels of support and resistance using the highest and lowest prices over a defined period. The "sensitivity" parameter, which ranges from 1 to 10, determines how sensitive the calculation is to recent price changes. A higher value increases the number of bars used to calculate these levels, making the levels more stable but less responsive to short-term price movements.

Visual Representation:

The support levels are drawn in green with a customizable transparency setting, while resistance levels are displayed in red with similar transparency controls. This visual representation helps traders identify these levels on the chart and see the strength or weakness of the support/resistance zones depending on the transparency setting.

Multiple Levels:

The indicator plots 10 distinct levels of support and resistance (from 1 to 10), which can offer a more granular view of price action. Traders can use these levels to assess potential breakout or breakdown points.

Customization:

Sensitivity: The sensitivity input allows traders to adjust how aggressively the indicator reacts to recent price data. This ensures flexibility, enabling the indicator to be tailored to different trading styles and market conditions.

Transparency: The transparency input adjusts the visual opacity of the support and resistance lines, making it easier to overlay the indicator without obscuring other chart elements.

Key Goals:

Dynamic Support/Resistance Identification: Automatically detect and display relevant support and resistance levels based on price history, removing the need for manual chart analysis.

Customizable Sensitivity: Offer a flexible method to adjust how the indicator identifies key levels, allowing it to fit different market conditions.

Clear Visualization: Provide easy-to-read support and resistance levels with customizable colors and transparencies, enhancing visual clarity and decision-making.

Multiple Levels: Display up to 10 levels of support and resistance, allowing traders to consider both short-term and longer-term price action when making trading decisions.

By using this indicator, traders can more effectively identify key price zones where price may reverse, consolidate, or break out, providing a solid foundation for developing trading strategies.

ICT Macro Sessions by @zeusbottradingICT Macro Sessions Indicator

The ICT Macro Sessions Indicator is a powerful tool designed for traders who follow the ICT (Inner Circle Trader) methodology and want to optimize their trading during specific high-probability time intervals. This indicator highlights all the key macro sessions throughout the trading day in the GMT+8 (Hong Kong) time zone.

What Does the Indicator Do?

This indicator visually marks ICT Macro Sessions on your trading chart using background colors and optional labels. Each session corresponds to specific time intervals when institutional activity is most likely to drive price action. By focusing on these periods, traders can align their strategies with market volatility and liquidity, increasing their chances of success.

Highlighted Sessions

The indicator covers all major ICT Macro Sessions, each with a unique color for easy identification:

London Macro 1 (15:33–16:00 GMT+8):

- Marks the early London session, often characterized by strong directional moves.

London Macro 2 (17:03–17:30 GMT+8):

- Captures the mid-London session, where price frequently reacts to liquidity levels.

New York AM Macro 1 (22:50–23:10 GMT+8):

- Highlights the start of the New York session, a prime time for price reversals or continuations.

New York AM Macro 2 (23:50–00:10 GMT+8):

- Focuses on late-morning New York activity, often aligning with key news releases.

New York Lunch Macro (00:50–01:10 GMT+8):

- Covers the lunch period in New York, where price may consolidate or set up for afternoon moves.

New York PM Macro 1 (02:10–02:40 GMT+8):

- Tracks post-lunch activity in New York, often featuring renewed volatility.

New York PM Macro 2 (04:15–04:45 GMT+8):

- Captures late-session moves as institutional traders finalize their positions.

Features of the Indicator

Fixed Time: The indicator is pre-configured for GMT+8 but it will adapt automatically to your timezone. No need to change anything in the code.

Background Highlighting: Each session is visually marked with a unique background color for quick recognition.

Optional Labels: Traders can enable or disable labels for each session, providing flexibility in how information is displayed.

Session Toggles: You can choose which sessions to display based on your trading preferences and strategy.

Intraday Timeframes: The indicator is optimized for intraday charts with timeframes of 45 minutes or less. You can change it to anything you like.

Why Use This Indicator?

The ICT Macro Sessions Indicator helps traders focus on the most critical times of the trading day when institutional activity is at its peak. These periods often coincide with significant price movements, making them ideal for scalping, day trading, or even swing trading setups. By visually highlighting these sessions, the indicator eliminates guesswork and allows traders to plan their trades with precision.

CPR by NKDCentral Pivot Range (CPR) Trading Strategy:

The Central Pivot Range (CPR) is a widely-used tool in technical analysis, helping traders pinpoint potential support and resistance levels in the market. By using the CPR effectively, traders can better gauge market trends and determine favorable entry and exit points. This guide explores how the CPR works, outlines its calculation, and describes how traders can enhance their strategies using an extended 10-line version of CPR.

What Really Central Pivot Range (CPR) is?

At its core, the CPR consists of three key lines:

Pivot Point (PP) – The central line, calculated as the average of the previous day’s high, low, and closing prices.

Upper Range (R1) – Positioned above the Pivot Point, acting as a potential ceiling where price may face resistance.

Lower Range (S1) – Found below the Pivot Point, serving as a potential floor where price might find support.

Advanced traders often expand on the traditional three-line CPR by adding extra levels above and below the pivot, creating up to a 10-line system. This extended CPR allows for a more nuanced understanding of the market and helps identify more detailed trading opportunities.

Applying CPR for Trading Success

1. How CPR is Calculation

The CPR relies on the previous day's high (H), low (L), and close (C) prices to create its structure:

Pivot Point (PP) = (H + L + C) / 3

First Resistance (R1) = (2 * PP) - L

First Support (S1) = (2 * PP) - H

Additional resistance levels (R2, R3) and support levels (S2, S3) are calculated by adding or subtracting multiples of the previous day’s price range (H - L) from the Pivot Point.

2. Recognizing the Market Trend

To effectively trade using CPR, it’s essential to first determine whether the market is trending up (bullish) or down (bearish). In an upward-trending market, traders focus on buying at support levels, while in a downward market, they look to sell near resistance.

3. Finding Ideal Entry Points

Traders often look to enter trades when price approaches key levels within the CPR range. Support levels (S1, S2) offer buying opportunities, while resistance levels (R1, R2) provide selling opportunities. These points are considered potential reversal zones, where price may bounce or reverse direction.

4. Managing Risk with Stop-Loss Orders

Proper risk management is crucial in any trading strategy. A stop-loss should be set slightly beyond the support level for buy positions and above the resistance level for sell positions, ensuring that losses are contained if the market moves against the trader’s position.

5. Determining Profit Targets

Profit targets are typically set based on the distance between entry points and the next support or resistance level. Many traders apply a risk-reward ratio, aiming for larger potential profits compared to the potential losses. However, if the next resistance and support level is far then middle levels are used for targets (i.e. 50% of R1 and R2)

6. Confirmation Through Other Indicators

While CPR provides strong support and resistance levels, traders often use additional indicators to confirm potential trade setups. Indicators such as moving averages can

help validate the signals provided by the CPR.

7. Monitoring Price Action At CPR Levels

Constantly monitoring price movement near CPR levels is essential. If the price fails to break through a resistance level (R1) or holds firm at support (S1), it can offer cues on when to exit or adjust a trade. However, a strong price break past these levels often signals a continued trend.

8. Trading Breakouts with CPR

When the price breaks above resistance or below support with strong momentum, it may signal a potential breakout. Traders can capitalize on these movements by entering positions in the direction of the breakout, ideally confirmed by volume or other technical indicators.

9. Adapting to Changing Market Conditions

CPR should be used in the context of broader market influences, such as economic reports, news events, or geopolitical shifts. These factors can dramatically affect market direction and how price reacts to CPR levels, making it important to stay informed about external market conditions.

10. Practice and Backtesting for Improvements

Like any trading tool, the CPR requires practice. Traders are encouraged to backtest their strategies on historical price data to get a better sense of how CPR works in different market environments. Continuous analysis and practice help improve decision-making and strategy refinement.

The Advantages of Using a 10-Line CPR System

An extended 10-line CPR system—comprising up to five resistance and five support levels—provides more granular control and insight into market movements. This expanded view helps traders better gauge trends and identify more opportunities for entry and exit. Key benefits include:

R2, S2 Levels: These act as secondary resistance or support zones, giving traders additional opportunities to refine their trade entries and exits.

R3, S3 Levels: Provide an even wider range for identifying reversals or trend continuations in more volatile markets.

Flexibility: The broader range of levels allows traders to adapt to changing market conditions and make more precise decisions based on market momentum.

So in Essential:

The Central Pivot Range is a valuable tool for traders looking to identify critical price levels in the market. By providing a clear framework for identifying potential support and resistance zones, it helps traders make informed decisions about entering and exiting trades. However, it’s important to combine CPR with sound risk management and additional confirmation through other technical indicators for the best results.

Although no trading tool guarantees success, the CPR, when used effectively and combined with practice, can significantly enhance a trader’s ability to navigate market fluctuations.

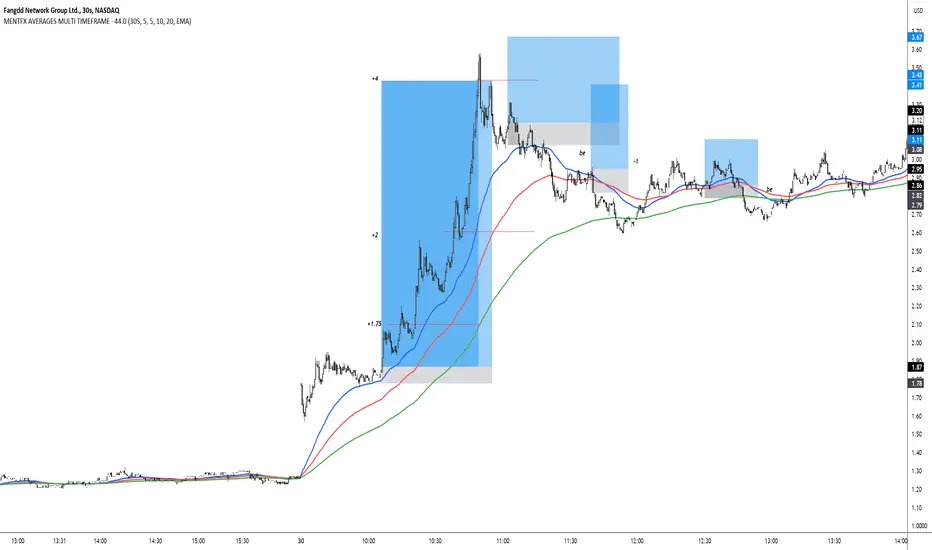

MENTFX AVERAGES MULTI TIMEFRAMEThe MENTFX AVERAGES MULTIME TIMEFRAME indicator is designed to provide traders with the ability to visualize multiple moving averages (MAs) from higher timeframes on their current chart, regardless of the chart's timeframe. It combines the power of exponential moving averages (EMAs) to help traders identify trends, spot potential reversal points, and make more informed trading decisions.

Key Features:

Multi-Timeframe Moving Averages: This indicator plots moving averages from daily timeframes directly on your chart, helping you keep track of higher timeframe trends while trading in any timeframe.

Customizable Moving Averages: You can adjust the length and visibility of up to three EMAs (default settings are 5, 10, and 20-period EMAs) to suit your trading style.

Overlay on Price: The indicator is designed to be overlaid on your price chart, seamlessly integrating with your existing analysis.

Simple but Effective: By offering a clear visual guide to where price is trading relative to important higher timeframe levels, this indicator helps traders avoid trading against major trends.

Why It’s Unique:

Validation Timeframe Flexibility: Unlike traditional moving average indicators that only work within the same chart's timeframe, the MENTFX AVERAGES M indicator allows you to pull moving averages from higher timeframes (default: Daily) and overlay them on any chart you're currently viewing, whether it's intraday (minutes) or even weekly. This cross-timeframe visibility is critical in determining the true market trend, adding context to your trades.

Customizability: Although the default settings focus on daily EMAs (5, 10, and 20 periods), traders can modify the parameters, including the type of moving average (Simple, Weighted, etc.), making it adaptable for any strategy. Whether you want shorter-term or longer-term averages, this indicator covers your needs.

Trend Confirmation Tool: The use of multiple EMAs helps traders confirm trend direction and potential price breakouts or reversals. For example, when the shorter-term 5 EMA crosses above the 20 EMA, it can signal a potential bullish trend, while the opposite could indicate bearish pressure.

How This Indicator Helps:

Identify Key Support and Resistance Levels: Higher timeframe moving averages often act as dynamic support and resistance. This indicator helps you stay aware of those critical levels, even when trading lower timeframes.

Trend Identification: Knowing where the market is relative to the 5, 10, and 20 EMAs from a higher timeframe gives you a clearer picture of whether you're trading with or against the prevailing trend.

Improved Decision Making: By aligning your trades with the direction of higher timeframe trends, you can increase your confidence in trade entries and exits, avoiding low-probability setups.

Multi-Market Use: This indicator works well across various asset classes—stocks, forex, crypto, and commodities—making it versatile for any trader.

How to Use:

Intraday Trading: Use the daily EMAs as a guide to see if intraday price movements align with longer-term trends.

Swing Trading: Plot daily EMAs to track the strength of a larger trend, using pullbacks to the moving averages as potential entry points.

Trend Trading: Monitor crossovers between the moving averages to signal potential changes in trend direction.

Default Settings:

5 EMA (Daily) – Blue Line

10 EMA (Daily) – Black Line

20 EMA (Daily) – Red Line

These lines will plot on your chart with a subtle opacity (33%) to ensure they don’t obstruct price action, while still providing crucial visual guidance on market trends.

This indicator is perfect for traders who want to blend technical analysis with multi-timeframe insights, helping you stay in sync with broader market movements while executing trades on any timeframe.

Bull/Bear Ratio By Month Table [MsF]Japanese below / 日本語説明は英文の後にあります。

-------------------------

This is an indicator that shows monthly bull-bear ratio in a table.

By specifying the start year and end year, the ratio will be calculated and showed based on the number of bullish and bearish lines in the monthly bar. It allows you to analyze the trend of each symbol and month (bullish / bearish). Up to 10 symbols can be specified.

You can take monthly bull-bear ratio for the past 10 or 20 years on the web, but with this indicator, you can narrow it down to the period in which you want to see the symbols you want to see. It is very convenient because you can take statistics at will.

Furthermore, if the specified ratio is exceeded, the font color can be changed to any color, making it very easy to read.

=== Parameter description ===

- From … Year of start of aggregation

- To … Year of end of aggregation

- Row Background Color … Row title background color

- Col Background Color … Column title background color

- Base Text Color … Text color

- Background Color … Background Color

- Border Color … Border Color

- Location … Location

- Text Size … Text Size

- Highlight Threshold … Ratio threshold, and color

- Display in counter? … Check if you want to show the number of times instead of the ratio

-------------------------

月別陰陽確率をテーブル表示するインジケータです。

開始年から終了年を指定することで、月足における陽線数および陰線数を元に確率を計算して表示します。

この機能により各シンボルおよび各月の特徴(買われやすい/売られやすい)を認識することができアノマリー分析が可能です。

シンボルは10個まで指定可能です。

過去10年、20年の月別陰陽確率は、Web上でよく見かけますが、このインジケータでは見たいシンボルを見たい期間に絞って、

自由自在に統計を取ることができるため大変便利です。

なお、指定した確率を上回った場合、文字色を任意の色に変更することができるため、大変見やすくなっています。

=== パラメータの説明 ===

- From … 集計開始年

- To … 集計終了年

- Row Background Color … 行タイトルの背景色

- Col Background Color … 列タイトルの背景色

- Base Text Color … テキストカラー

- Background Color … 背景色

- Border Color … 区切り線の色

- Location … 配置

- Text Size … テキストサイズ

- Highlight Threshold … 色変更する確率の閾値、および色

- Display in counter? … 確率ではなく回数表示する場合はチェックする

JordanSwindenLibraryLibrary "JordanSwindenLibrary"

TODO: add library description here

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

getPipSize(multiplier)

Calculates the pip size of the current market

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float) : The number to truncate

decimalPlaces (simple float) : (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float) : The first value to reference

value2 (float) : The second value to reference

lookback (int) : The lookback period to analyze

Returns: The percent change over the two values and lookback period

random(minRange, maxRange)

Wichmann–Hill Pseudo-Random Number Generator

Parameters:

minRange (float) : The smallest possible number (default: 0)

maxRange (float) : The largest possible number (default: 1)

Returns: A random number between minRange and maxRange

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (! MUST BE CALLED ON EVERY TICK TO BE ACCURATE, don't place in scopes)

Parameters:

length (simple int) : The MA period

maType (string) : The type of MA

Returns: A moving average with the given parameters

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently (based on closing prices)

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA (based on closing prices)

getPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

lookback (int) : The lookback period to look back over

direction (int) : The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float) : (default=2) The maximum top wick size compared to the bottom (and vice versa)

bodySize (float) : (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bullish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bearish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar()

Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar()

Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range

Parameters:

startTime (int) : The UNIX date timestamp to begin searching from

endTime (int) : the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze

Parameters:

monday (bool) : Should the script analyze this day? (true/false)

tuesday (bool) : Should the script analyze this day? (true/false)

wednesday (bool) : Should the script analyze this day? (true/false)

thursday (bool) : Should the script analyze this day? (true/false)

friday (bool) : Should the script analyze this day? (true/false)

saturday (bool) : Should the script analyze this day? (true/false)

sunday (bool) : Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(atrValue, maxSize)

Parameters:

atrValue (float)

maxSize (float)

tradeCount()

Calculate total trade count

Returns: Total closed trade count

isLong()

Check if we're currently in a long trade

Returns: True if our position size is positive

isShort()

Check if we're currently in a short trade

Returns: True if our position size is negative

isFlat()

Check if we're currentlyflat

Returns: True if our position size is zero

wonTrade()

Check if this bar falls after a winning trade

Returns: True if we just won a trade

lostTrade()

Check if this bar falls after a losing trade

Returns: True if we just lost a trade

maxDrawdownRealized()

Gets the max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

Returns: The max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

totalPipReturn()

Gets the total amount of pips won/lost (as a whole number)

Returns: Total amount of pips won/lost (as a whole number)

longWinCount()

Count how many winning long trades we've had

Returns: Long win count

shortWinCount()

Count how many winning short trades we've had

Returns: Short win count

longLossCount()

Count how many losing long trades we've had

Returns: Long loss count

shortLossCount()

Count how many losing short trades we've had

Returns: Short loss count

breakEvenCount(allowanceTicks)

Count how many break-even trades we've had

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even count

longCount()

Count how many long trades we've taken

Returns: Long trade count

shortCount()

Count how many short trades we've taken

Returns: Short trade count

longWinPercent()

Calculate win rate of long trades

Returns: Long win rate (0-100)

shortWinPercent()

Calculate win rate of short trades

Returns: Short win rate (0-100)

breakEvenPercent(allowanceTicks)

Calculate break even rate of all trades

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even win rate (0-100)

averageRR()

Calculate average risk:reward

Returns: Average winning trade divided by average losing trade

unitsToLots(units)

(Forex) Convert the given unit count to lots (multiples of 100,000)

Parameters:

units (float) : The units to convert into lots

Returns: Units converted to nearest lot size (as float)

getFxPositionSize(balance, risk, stopLossPips, fxRate, lots)

(Forex) Calculate fixed-fractional position size based on given parameters

Parameters:

balance (float) : The account balance

risk (float) : The % risk (whole number)

stopLossPips (float) : Pip distance to base risk on

fxRate (float) : The conversion currency rate (more info below in library documentation)

lots (bool) : Whether or not to return the position size in lots rather than units (true by default)

Returns: Units/lots to enter into "qty=" parameter of strategy entry function

EXAMPLE USAGE:

string conversionCurrencyPair = (strategy.account_currency == syminfo.currency ? syminfo.tickerid : strategy.account_currency + syminfo.currency)

float fx_rate = request.security(conversionCurrencyPair, timeframe.period, close )

if (longCondition)

strategy.entry("Long", strategy.long, qty=zen.getFxPositionSize(strategy.equity, 1, stopLossPipsWholeNumber, fx_rate, true))

skipTradeMonteCarlo(chance, debug)

Checks to see if trade should be skipped to emulate rudimentary Monte Carlo simulation

Parameters:

chance (float) : The chance to skip a trade (0-1 or 0-100, function will normalize to 0-1)

debug (bool) : Whether or not to display a label informing of the trade skip

Returns: True if the trade is skipped, false if it's not skipped (idea being to include this function in entry condition validation checks)

fillCell(tableID, column, row, title, value, bgcolor, txtcolor, tooltip)

This updates the given table's cell with the given values

Parameters:

tableID (table) : The table ID to update

column (int) : The column to update

row (int) : The row to update

title (string) : The title of this cell

value (string) : The value of this cell

bgcolor (color) : The background color of this cell

txtcolor (color) : The text color of this cell

tooltip (string)

Returns: Nothing.

Rempi Volume

Greetings, dear traders. I present to your attention the concept of a Rempi Volume indicator + info table.

Rempi Volume displays volume in a color palette, where:

gray color - very weak volume,

blue color - weak volume,

green color - normal volume,

orange color - high volume,

red color - very high volume,

purple color - ultra high volume

The indicator also supports the function of displaying a moving average, the default is 20.

The indicator can color bars on the main price chart, depending on how much volume is currently inside the bar.

The Rempi Volume indicator table has the following information for the trader:

Current Bar -information about the current bar: its volume in real time, as well as the percentage of buyers and sellers.

Previous Bar - information about the previous bar: its volume, as well as the percentage of buyers and sellers. (data is updated at bar close)

10 Bar Volume Comparison - data on the volume of buyers or sellers for the previous 10 bars on the chart.

Volume Change - changing the amount of volume between the current and previous bar, in real time.

Average Volume - average trading volume for the current day.

Market Volatility - market volatility and recommendations.

Current Trend - current trend on the market.

RSI - RSI indicator and recommendations.

/////////////////////////////////////////////////////////////

Приветствую вас уважаемые трейдеры. Вашему вниманию представляю концепт индикатора объемов Rempi Volume + информативная таблица.

Rempi Volume отображает объем в цветовой палитре , где:

серый цвет - очень слабый объем,

голубой цвет - слабый объем,

зеленый цвет - нормальный объем,

оранжевый цвет - высокий объем,

красный цвет - очень высокий объем,

фиолетовый цвет - ультра высокий объем

Также индикатор поддерживает функцию отображения скользящей средней, по умолчанию равна 20.

Индикатор может окрашивать бары на основном графике цены, в зависимости ,какой объем в данный момент внутри бара.

Таблица индикатора Rempi Volume имеет следующую информацию для трейдера:

Current Bar - информация о текущем баре: его объем в режиме реального времени, а также процентное соотношение покупателей и продавцов.

Previous Bar - информация о предыдущем баре: его объем , а также процентное соотношение покупателей и продавцов. ( данные обновляются на закрытии бара )

10 Bar Volume Comparison - данные об объеме покупателей или продавцов за предыдущие 10 баров на графике.

Volume Change - изменение количества объема между текущим и предыдущим баром,в режиме реального времени.

Average Volume - средний объем торгов за текущий день.

Market Volatility - волатильность рынка и рекомендации.

Current Trend - текущее направление рынка.

RSI - показатель RSI и рекомендации.

Swing Trend AnalysisIntroducing the Swing Trend Analyzer: A Powerful Tool for Swing and Positional Trading

The Swing Trend Analyzer is a cutting-edge indicator designed to enhance your swing and positional trading by providing precise entry points based on volatility contraction patterns and other key technical signals. This versatile tool is packed with features that cater to traders of all timeframes, offering flexibility, clarity, and actionable insights.

Key Features:

1. Adaptive Moving Averages:

The Swing Trend Analyzer offers multiple moving averages tailored to the timeframe you are trading on. On the daily chart, you can select up to four different moving average lengths, while all other timeframes provide three moving averages. This flexibility allows you to fine-tune your analysis according to your trading strategy. Disabling a moving average is as simple as setting its value to zero, making it easy to customize the indicator to your needs.

2. Dynamic Moving Average Colors Based on Relative Strength:

This feature allows you to compare the performance of the current ticker against a major index or any symbol of your choice. The moving average will change color based on whether the ticker is outperforming or underperforming the selected index over the chosen period. For example, on a daily chart, if the 21-day moving average turns blue, it indicates that the ticker has outperformed the selected index over the last 21 days. This visual cue helps you quickly identify relative strength, a key factor in successful swing trading.

3. Visual Identification of Price Contractions: