Morning Break OutThis indicator visualizes a classic morning breakout setup for the DAX and other European markets. The first hour often sets the tone for the trading day — this tool helps you identify that visually and react accordingly.

🔍 How It Works:

Box Range Calculation:

The high and low between 09:00 and 10:00 define the top and bottom of the box.

Color Logic:

Green: Price breaks above the box after 10:00 → bullish breakout

Red: Price breaks below the box after 10:00 → bearish breakout

Gray: No breakout → neutral phase

📈 Use Cases:

Identify breakout setups visually

Ideal for intraday traders and momentum strategies

Combine with volume or trend filters

⚙️ Notes:

Recommended for timeframes 1-minute and above

Uses the chart’s local timezone (e.g. CET/CEST for XETRA/DAX)

Works on all instruments with data before 09:00 — perfect for DAX, EuroStoxx, futures, FX, CFDs, etc.

Cerca negli script per "大位科技同行业可替代股票的技术面分析数据(如5日均线、10日均线、支撑位、压力位)"

ES Gap Trading Levels# ES Gap Trading Levels

## Overview

A professional gap trading indicator designed specifically for ES Futures traders. This indicator automatically captures the closing price at 3:59 PM ET (NYSE close) and immediately displays key gap levels for the evening trading session starting at 6:00 PM ET.

## Key Features

### ✅ **Automatic Gap Level Detection**

- Captures ES Futures closing price at 3:59-4:00 PM ET

- Instantly displays gap levels for immediate session planning

- Resets daily for fresh gap analysis

### ✅ **Six Critical Gap Levels**

- **±10 Points** (White lines) - Short-term gap targets

- **±20 Points** (Light Blue lines) - Medium gap targets

- **±30 Points** (Red lines) - Extended gap targets

### ✅ **Professional Display**

- Clean horizontal lines with customizable colors

- Clear labels showing point values (+30, +20, +10, -10, -20, -30)

- Gap levels table showing exact price targets

- Optional closing price reference line

### ✅ **Customizable Settings**

- Adjustable line colors, width, and extension

- Toggle labels and reference table on/off

- Manual closing price override for testing

- Debug mode for troubleshooting

### ✅ **Smart Management**

- Automatic cleanup of previous day's levels

- Lines appear immediately after market close

- Optimized for ES1!, MES1!, and other ES futures contracts

## How It Works

1. **Market Close Capture**: At 3:59 PM ET, the indicator captures the ES closing price

2. **Instant Display**: Gap levels immediately appear on your chart

3. **Evening Session Ready**: Lines are positioned for 6:00 PM ET session start

4. **Daily Reset**: Old levels are automatically cleared each new trading day

## Perfect For:

- Gap trading strategies

- Overnight futures trading

- ES futures scalping

- Session transition analysis

- Risk management levels

## Usage Tips:

- Best used on 1-15 minute ES futures charts

- Ensure chart timezone shows ET times

- Use manual mode for backtesting specific dates

- Combine with volume and momentum indicators

## Settings Guide:

- **Display Settings**: Control lines, labels, and table visibility

- **Colors**: Customize each gap level color scheme

- **Manual Settings**: Override closing price for testing

- **Debug**: View time detection and diagnostic information

*Designed by traders, for traders. Clean, professional, and reliable gap level detection for serious ES futures trading.*

SG CBC Table - Full 10min & 2minBased on SG CBC Table has 10 min and 2 min CBC status and GC. Also customizable table colors of the background can be changed or made transparent. Indicator Updates every 10 minutes on a 10 minute chart and every 2 minutes on a 2 minute chart

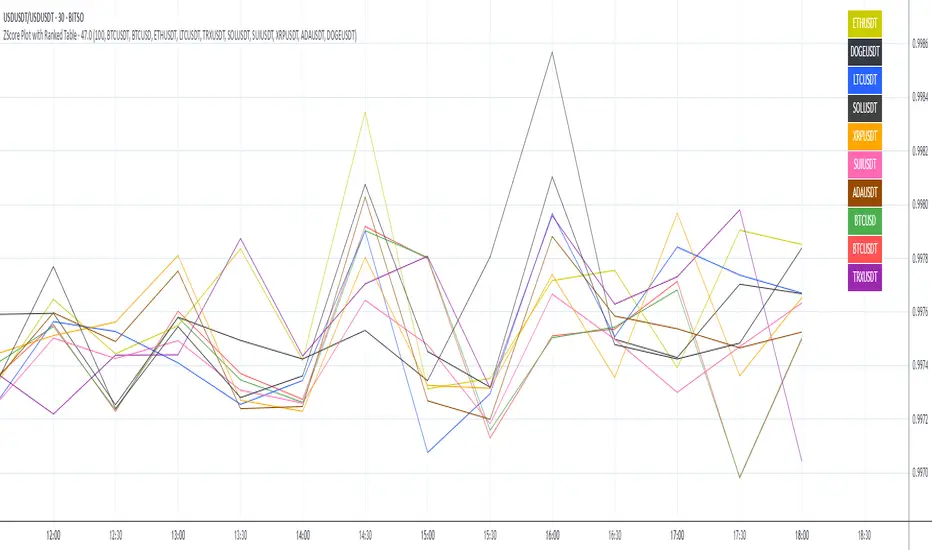

ZScore Plot with Ranked TableVersion 0.1

ZScore Plot with Ranked Table — Overview

This indicator visualizes the rolling ZScores of up to 10 crypto assets, giving traders a normalized view of log return deviations over time. It's designed for volatility analysis, anomaly detection, and clustering of asset behavior.

🎯 Purpose

• Show how each asset's performance deviates from its historical mean

• Identify potential overbought/oversold conditions across assets

• Provide a ranked leaderboard to compare asset behavior instantly

⚙️ Inputs

• Lookback: Number of bars to calculate mean and standard deviation

• Asset 1–10: Choose up to 10 symbols (e.g. BTCUSDT, ETHUSDT)

📈 Outputs

• ZScore Lines: Each asset plotted on a normalized scale (mean = 0, SD = 1)

• End-of-Line Labels: Asset names displayed at latest bar

• Leaderboard Table: Ranked list (top-right) showing:

◦ Asset name (color-matched)

◦ Final ZScore (rounded to 3 decimals)

🧠 Use Cases

• Quantitative traders seeking cross-asset momentum snapshots

• Signal engineers tracking volatility clusters

• Risk managers monitoring outliers and systemic shifts

Aggregated VolumeHow to Read the “Aggregated Volume” Signal

This indicator combines normalized volume, short-term volume bursts, pivot levels, VWAP, and a 200-period EMA to give you a multi-dimensional view of trading activity. Here’s how to interpret each component and synthesize them into actionable insights.

1. Custom Volume Signal (vSignal)

• Calculation

• vSignal = Sum of over bars, divided by the current price.

• A rising vSignal means more volume is being traded per unit of price, signaling growing interest relative to price level.

• Plot styling

• Bars are lime when (bullish volume days)

• Bars are orange when (bearish volume days)

How to read it

• Trend confirmation: Increasing lime bars alongside rising price suggests buyers in control.

• Warning sign: Rising orange bars on a down move indicate accelerating selling pressure.

• Divergence:

• Price making new highs while vSignal stalls or drops → potential top.

• Price making new lows while vSignal holds → potential bottom.

2. Short-Term Volume Bursts

Three semi-transparent histograms show how much the last 2, 5, and 10-bar raw volumes exceed (or fall below) the current vSignal:

• Blue = vol(2) – vSignal

• Green = vol(5) – vSignal

• Red = vol(10) – vSignal

If a colored bar sits above zero, that lookback’s volume is surging relative to the longer-term average (vSignal).

How to read it

• Clustered bursts:

• Blue + Green + Red above zero → strong, broad-based volume surge.

• Great for confirming breakouts and shakeouts.

• Isolated burst:

• Only Blue (> 0) on a small range bar → might be a false breakout or intrabar squeeze.

• Only Red (> 0) on a wide range → institutional involvement; act with caution.

3. Pivot Volume Levels (v & t)

• Every 21 bars, the script finds the highest and lowest vSignal values and plots them as shaded price levels:

• Magenta area = recent vSignal high (resistance)

• Cyan area = recent vSignal low (support)

How to read it

• Rejection/Break:

• Price approaches magenta zone and stalls → sellers defending that volume high.

• Break above magenta with high vSignal → likely sustained rally.

• Support flip:

• Cyan zone hold → buyers stepping in at heavy-volume lows.

• Break below cyan with rising vSignal → bearish conviction.

4. Midline Cross (Volume Equilibrium)

• A 10-bar SMA of

• Drawn as a faint white cross on price

How to read it

• Above midline → overall volume bias is skewed bullish.

• Below midline → bearish volume bias.

Crossovers of vSignal through this midline can signal shifts in underlying conviction.

5. VWAP & 200-Period EMA Overlays

• VWAP (transparent red if above price, green if below)

• EMA(200) plotted as aqua circles

How to read them

• VWAP tells you the intraday “value area.”

• Price above VWAP + rising vSignal = intraday buyers in charge.

• Price below VWAP + rising vSignal = aggressive sellers.

• EMA(200) gives you the longer-term trend.

• Above EMA200 = bullish regime

• Below EMA200 = bearish regime

6. Putting It All Together: Example Scenarios

1. Bullish Entry

• Price > EMA200 & VWAP is green

• vSignal rising in lime

• All three short-term bursts above zero

• Price near or breaking the magenta pivot with volume confirmation

2. Bearish Entry

• Price < EMA200 & VWAP is red

• vSignal rising in orange

• Two-bar burst (blue) spikes on a down bar

• Price failing at magenta pivot or breaking cyan support

3. Divergence Play

• Price makes new high, but vSignal peaks lower than last high → look for a reversal.

• Price drops to new low, but vSignal stays above its last low → prepare for a bounce.

By combining these layers—normalized volume, burst indicators, pivot levels, VWAP, and EMA—you get a clear map of where volume is clustering, which lets you anticipate support/resistance, gauge real interest, and spot potential reversals or breakouts with greater confidence.

Multi SMA AnalyzerMulti SMA Analyzer with Custom SMA Table & Advanced Session Logic

A feature-rich SMA analysis suite for traders, offering up to 7 configurable SMAs, in-depth trend detection, real-time table, and true session-aware calculations.

Ideal for those who want to combine intraday, swing, and higher-timeframe trend analysis with maximum chart flexibility.

Key Features

📊 Multi-SMA Overlay

- 7 SMAs (default: 5, 20, 50, 100, 200, 21, 34)—individually configurable (period, source, color, line style)

- Show/hide each SMA, custom line style (solid, stepline, circles), and color logic

- Dynamic color: full opacity above SMA, reduced when below

⏰ Session-Aware SMAs

- Each SMA can be calculated using only user-defined session hours/days/timezone

- “Ignore extended hours” option for accurate intraday trend

📋 Smart Data Table

- Live SMA values, % distance from price, and directional arrows (↑/↓/→)

- Bull/Bear/Sideways trend classification

- Custom table position, size, colors, transparency

- Table can run on chart or custom (higher) timeframe for multi-TF analysis

🎯 Golden/Death Cross Detection

- Flexible crossover engine: select any two from (5, 10, 20, 50, 100, 200) for fast/slow SMA cross signals

- Plots icons (★ Golden, 💀 Death), optional crossover labels with custom size/colors

🏷️ SMA Labels

- Optional on-chart SMA period labels

- Custom placement (above/below/on line), size, color, offset

🚨 Signal & Trend Engine

- Bull/Bear/Sideways logic: price vs. multiple SMAs (not just one pair)

- Volume spike detection (2x 20-period SMA)

- Bullish engulfing candlestick detection

- All signals can use chart or custom table timeframe

🎨 Visual Customization

- Dynamic background color (Bull: green, Bear: red, Neutral: gray)

- Every visual aspect is customizable: label/table colors, transparency, size, position

🔔 Built-in Alerts

- Crossovers (SMA20/50, Golden/Death)

- Bull trend, volume spikes, engulfing pattern—all alert-ready

How It Works

- Session Filtering:

- SMAs can be set to count only bars from your chosen market session, for true intraday/trading-hour signals

Dynamic Table & Signals:

- Table and all signal logic run on your selected chart or custom timeframe

Flexible Crossover:

- Choose any pair (5, 10, 20, 50, 100, 200) for cross detection—SMA 10 is available for crossover even if not shown as an SMA line

Everything is modular:

- Toggle features, set visuals, and alerts to your workflow

🚨 How to Use Alerts

- All key signals (crossovers, trend shifts, volume spikes, engulfing patterns) are available as alert conditions.

To enable:

- Click the “Alerts” (clock) icon at the top of TradingView.

- Select your desired signal (e.g., “Golden Cross”) from the condition dropdown.

- Set your alert preferences and create the alert.

- Now, you’ll get notified automatically whenever a signal occurs!

Perfect For

- Multi-timeframe and swing traders seeking higher timeframe SMA confirmation

- Intraday traders who want to ignore pre/post-market data

- Anyone wanting a modern, powerful, fully customizable multi-SMA overlay

// P.S: Experiment with Golden Cross where Fast SMA is 5 and Slow SMA is 20.

// Set custom timeframe for 4 hr while monitoring your chart on 15 min time frame.

// Enable Background Color and Use Table Timeframe for Background.

// Uncheck Pine labels in Style tab.

Clean, open-source, and loaded with pro features—enjoy!

Like, share, and let me know if you'd like any new features added.

NQ Position Size CalculatorNQ Position Size Line Calculator is designed specifically for Nasdaq 100 futures (NQ) and micro futures (MNQ) traders who want to maintain disciplined risk management. This visual tool eliminates the guesswork from position sizing by displaying distance lines and contract calculations directly on your chart.

The indicator creates horizontal lines at 10-tick intervals from your stop loss level, showing you exactly how many contracts to trade at each distance to maintain your predetermined risk amount. Whether you're trading regular NQ contracts or micro MNQ contracts, this calculator ensures you never risk more than intended while providing instant visual feedback for optimal position sizing decisions.

How to Use the Indicator

Step 1: Configure Your Settings

Stop Loss Price: Enter your exact stop loss level (e.g., 20000.00)

Risk Amount ($): Set your maximum dollar risk per trade (e.g., $500)

Contract Type: Choose between:

NQ (Regular): $5 per tick - for larger accounts

MNQ (Micro): $0.50 per tick - for smaller accounts or conservative sizing

Display Options:

Max Lines: Number of distance lines to show (default: 30)

Show Labels: Toggle tick distance and contract count labels

Line Color: Customize the color of distance lines

Label Size: Choose tiny, small, or normal label sizes

Step 2: Read the Visual Display

Once configured, the indicator displays:

Stop Loss Line:

Thick yellow line marking your exact stop loss level

Yellow label showing the stop loss price

Distance Lines:

Dashed red lines at 10-tick intervals above and below your stop loss

Lines appear on both sides for long and short position planning

Labels (if enabled):

Green labels (right side): For long positions above your stop loss

Red labels (left side): For short positions below your stop loss

Format: "20T 5x" means 20 ticks distance, 5 contracts maximum

Step 3: Use the Information Tables

The indicator provides two helpful tables:

Position Size Table (top-right):

Shows common tick distances (10, 20, 40, 80, 160 ticks)

Displays risk per contract at each distance

Contract count for your specified risk amount

Total risk with rounded contract numbers

Settings Table (bottom-right):

Confirms your current risk amount

Shows selected contract type

Displays current settings for quick reference

Step 4: Apply to Your Trading

For Long Positions:

Look at the green labels on the right side of your chart

Find your desired entry level

Read the label to see: distance in ticks and maximum contracts

Example: "30T 8x" = 30 ticks from stop, buy 8 contracts maximum

For Short Positions:

Look at the red labels on the left side of your chart

Find your desired entry level

Read the label for tick distance and contract count

Example: "40T 6x" = 40 ticks from stop, sell 6 contracts maximum

Step 5: Trading Execution

Before Entering a Trade:

Identify your stop loss level and input it into the indicator

Choose your entry point by looking at the distance lines

Note the contract count from the corresponding label

Verify the risk amount matches your trading plan

Execute your trade with the calculated position size

Risk Management Features:

Contract rounding: All position sizes are rounded down (never up) to ensure you don't exceed your risk limit

Zero position filtering: Lines only show where position size is at least 1 contract

Dual-sided display: Plan both long and short opportunities simultaneously

Adiyogi Trend🟢🔴 “Adiyogi” Trend — Market Alignment Visualizer

“Adiyogi” Trend is a powerful, non-intrusive trend detection system built for traders who seek clarity, discipline, and alignment with true market flow. Inspired by the meditative stillness of Adiyogi and the need for mindful, high-probability decisions, this tool offers a clean and intuitive visual guide to trending environments — without cluttering the chart or pushing forced trades.

This is not a buy/sell signal generator. Instead, it is designed as a background confirmation engine that helps you stay on the right side of the market by identifying moments of true directional strength.

🧠 Core Logic

The “Adiyogi” Trend indicator highlights the background of your chart in green or red when multiple layers of strength and structure align — including momentum, market positioning, and relative force. Only when these internal components agree does the system activate a directional state.

It’s built on three foundational energies of trend confirmation:

Strength of movement

Structure in price action

Conviction in momentum

By combining these into one visual background, the indicator filters out indecision and helps you stay focused during real trend phases — whether you're day trading, swing trading, or holding longer-term positions.

📌 Core Concepts Behind the Tool

The indicator integrates three essential market filters—each confirming a different dimension of trend strength:

ADX (Average Directional Index) – Measures trend momentum.

You’ve chosen a very responsive setting (ADX Length = 2), which helps catch the earliest possible signs of momentum emergence.

The threshold is ADX ≥ 22, ensuring that weak or sideways markets are filtered out.

SuperTrend (10,1) – Captures short-term trend direction.

This setup follows price closely and reacts quickly to reversals, making it ideal for fast-moving assets or intraday strategies.

SuperTrend acts as the structural confirmation of directional bias.

RSI (Relative Strength Index) – Measures strength based on recent price closes.

You’ve configured RSI > 50 for bullish zones and < 50 for bearish—a neutral midpoint standard often used by professional traders.

This ensures that only trades in sync with momentum and recent strength are highlighted.

🌈 How It Visually Works

Background turns GREEN when:

ADX ≥ 22, indicating strong momentum

Price is above the 20 EMA and above SuperTrend (10,1)

RSI > 50, confirming recent strength

Background turns RED when:

ADX ≥ 22, indicating strong momentum

Price is below the 20 EMA and below SuperTrend (10,1)

RSI < 50, confirming recent weakness

The background remains neutral (transparent) when trend conditions are not clearly aligned—this is the tool's way of keeping you out of indecisive markets.

A label (BULL / BEAR) appears only when the bias flips from the previous one. This helps avoid repeated or redundant alerts, focusing your attention only when something changes.

📊 Practical Uses & Benefits

✅ Stay with the trend: Perfectly filters out choppy or sideways markets by only activating when conditions align across momentum, structure, and strength.

✅ Pre-trade confirmation: Use this tool to confirm trade setups from other indicators or price action patterns.

✅ Avoid noise: Prevent overtrading by focusing only on high-quality trend conditions.

✅ Visual clarity: Unlike arrows or plots that clutter the chart, this tool subtly highlights trend conditions in the background, preserving your price action view.

📍 Important Notes

This is not a buy/sell signal generator. It is a trend-confirmation system.

Use it in conjunction with your existing entry setups—such as breakouts, order blocks, retests, or candlestick patterns.

The tool helps you stay in sync with the dominant direction, especially when combining multiple timeframes.

Can be used on any market (stocks, forex, crypto, indices) and on any timeframe.

Frahm Factor Position Size CalculatorThe Frahm Factor Position Size Calculator is a powerful evolution of the original Frahm Factor script, leveraging its volatility analysis to dynamically adjust trading risk. This Pine Script for TradingView uses the Frahm Factor’s volatility score (1-10) to set risk percentages (1.75% to 5%) for both Margin-Based and Equity-Based position sizing. A compact table on the main chart displays Risk per Trade, Frahm Factor, and Average Candle Size, making it an essential tool for traders aligning risk with market conditions.

Calculates a volatility score (1-10) using true range percentile rank over a customizable look-back window (default 24 hours).

Dynamically sets risk percentage based on volatility:

Low volatility (score ≤ 3): 5% risk for bolder trades.

High volatility (score ≥ 8): 1.75% risk for caution.

Medium volatility (score 4-7): Smoothly interpolated (e.g., 4 → 4.3%, 5 → 3.6%).

Adjustable sensitivity via Frahm Scale Multiplier (default 9) for tailored volatility response.

Position Sizing:

Margin-Based: Risk as a percentage of total margin (e.g., $175 for 1.75% of $10,000 at high volatility).

Equity-Based: Risk as a percentage of (equity - minimum balance) (e.g., $175 for 1.75% of ($15,000 - $5,000)).

Compact 1-3 row table shows:

Risk per Trade with Frahm score (e.g., “$175.00 (Frahm: 8)”).

Frahm Factor (e.g., “Frahm Factor: 8”).

Average Candle Size (e.g., “Avg Candle: 50 t”).

Toggles to show/hide Frahm Factor and Average Candle Size rows, with no empty backgrounds.

Four sizes: XL (18x7, large text), L (13x6, normal), M (9x5, small, default), S (8x4, tiny).

Repositionable (9 positions, default: top-right).

Customizable cell color, text color, and transparency.

Set Frahm Factor:

Frahm Window (hrs): Pick how far back to measure volatility (e.g., 24 hours). Shorter for fast markets, longer for chill ones.

Frahm Scale Multiplier: Set sensitivity (1-10, default 9). Higher makes the score jumpier; lower smooths it out.

Set Margin-Based:

Total Margin: Enter your account balance (e.g., $10,000). Risk auto-adjusts via Frahm Factor.

Set Equity-Based:

Total Equity: Enter your total account balance (e.g., $15,000).

Minimum Balance: Set to the lowest your account can go before liquidation (e.g., $5,000). Risk is based on the difference, auto-adjusted by Frahm Factor.

Customize Display:

Calculation Method: Pick Margin-Based or Equity-Based.

Table Position: Choose where the table sits (e.g., top_right).

Table Size: Select XL, L, M, or S (default M, small text).

Table Cell Color: Set background color (default blue).

Table Text Color: Set text color (default white).

Table Cell Transparency: Adjust transparency (0 = solid, 100 = invisible, default 80).

Show Frahm Factor & Show Avg Candle Size: Check to show these rows, uncheck to hide (default on).

Logarithmic Moving Average (LMA) [QuantAlgo]🟢 Overview

The Logarithmic Moving Average (LMA) uses advanced logarithmic weighting to create a dynamic trend-following indicator that prioritizes recent price action while maintaining statistical significance. Unlike traditional moving averages that use linear or exponential weights, this indicator employs logarithmic decay functions to create a more sophisticated price averaging system that adapts to market volatility and momentum conditions.

The indicator displays a smoothed signal line that oscillates around zero, with positive values indicating bullish momentum and negative values indicating bearish momentum. The signal incorporates trend quality assessment, momentum confirmation, and multiple filtering mechanisms to help traders and investors identify trend continuation and reversal opportunities across different timeframes and asset classes.

🟢 How It Works

The indicator's core innovation lies in its logarithmic weighting system, where weights are calculated using the formula: w = 1.0 / math.pow(math.log(i + steepness), 2) The steepness parameter controls how aggressively recent data is prioritized over historical data, creating a dynamic weight decay that can be fine-tuned for different trading styles. This logarithmic approach provides more nuanced weight distribution compared to exponential moving averages, offering better responsiveness while maintaining stability.

The LMA calculation combines multiple sophisticated components. First, it calculates the logarithmic weighted average of closing prices. Then it measures the slope of this average over a 10-period lookback: lmaSlope = (lma - lma ) / lma * 100 The system also incorporates trend quality assessment using R-squared correlation analysis of log-transformed prices, measuring how well the price data fits a linear trend model over the specified period.

The final signal generation uses the formula: signal = lmaSlope * (0.5 + rSquared * 0.5) which combines the LMA slope with trend quality weighting. When momentum confirmation is enabled, the indicator calculates annualized log-return momentum and applies a multiplier when the momentum direction aligns with the signal direction, strengthening confirmed signals while filtering out weak or counter-trend movements.

🟢 How to Use

1. Signal Interpretation and Threshold Zones

Positive Values (Above Zero): LMA slope indicating bullish momentum with upward price trajectory relative to logarithmic baseline

Negative Values (Below Zero): LMA slope indicating bearish momentum with downward price trajectory relative to logarithmic baseline

Zero Line Crosses: Signal transitions between bullish and bearish regimes, indicating potential trend changes

Long Entry Threshold Zone: Area above positive threshold (default 0.5) indicating confirmed bullish signals suitable for long positions

Short Entry Threshold Zone: Area below negative threshold (default -0.5) indicating confirmed bearish signals suitable for short positions

Extreme Values: Signals exceeding ±1.0 represent strong momentum conditions with higher probability of continuation

2. Momentum Confirmation and Visual Analysis

Signal Color Intensity: Gradient coloring shows signal strength, with brighter colors indicating stronger momentum

Bar Coloring: Optional price bar coloring matches signal direction for quick visual trend identification

Position Labels: Real-time position classification (Bullish/Bearish/Neutral) displayed on the latest bar

Momentum Weight Factor: When short-term log-return momentum aligns with LMA signal direction, the signal receives additional weight confirmation

Trend Quality Component: R-squared values weight the signal strength, with higher correlation indicating more reliable trend conditions

3. Examples: Preconfigured Settings

Default: Universally applicable configuration balanced for medium-term investing and general trading across multiple timeframes and asset classes.

Scalping: Highly responsive setup with shorter period and higher steepness for ultra-short-term trades on 1-15 minute charts, optimized for quick momentum shifts.

Swing Trading: Extended period with moderate steepness and increased smoothing for multi-day positions, designed to filter noise while capturing larger price swings on 1-4 hour and daily charts.

Trend Following: Maximum smoothing with lower steepness for established trend identification, generating fewer but more reliable signals optimal for daily and weekly timeframes.

Mean Reversion: Shorter period with high steepness for counter-trend strategies, more sensitive to extreme moves and reversal opportunities in ranging market conditions.

Aetherium Institutional Market Resonance EngineAetherium Institutional Market Resonance Engine (AIMRE)

A Three-Pillar Framework for Decoding Institutional Activity

🎓 THEORETICAL FOUNDATION

The Aetherium Institutional Market Resonance Engine (AIMRE) is a multi-faceted analysis system designed to move beyond conventional indicators and decode the market's underlying structure as dictated by institutional capital flow. Its philosophy is built on a singular premise: significant market moves are preceded by a convergence of context , location , and timing . Aetherium quantifies these three dimensions through a revolutionary three-pillar architecture.

This system is not a simple combination of indicators; it is an integrated engine where each pillar's analysis feeds into a central logic core. A signal is only generated when all three pillars achieve a state of resonance, indicating a high-probability alignment between market organization, key liquidity levels, and cyclical momentum.

⚡ THE THREE-PILLAR ARCHITECTURE

1. 🌌 PILLAR I: THE COHERENCE ENGINE (THE 'CONTEXT')

Purpose: To measure the degree of organization within the market. This pillar answers the question: " Is the market acting with a unified purpose, or is it chaotic and random? "

Conceptual Framework: Institutional campaigns (accumulation or distribution) create a non-random, organized market environment. Retail-driven or directionless markets are characterized by "noise" and chaos. The Coherence Engine acts as a filter to ensure we only engage when institutional players are actively steering the market.

Formulaic Concept:

Coherence = f(Dominance, Synchronization)

Dominance Factor: Calculates the absolute difference between smoothed buying pressure (volume-weighted bullish candles) and smoothed selling pressure (volume-weighted bearish candles), normalized by total pressure. A high value signifies a clear winner between buyers and sellers.

Synchronization Factor: Measures the correlation between the streams of buying and selling pressure over the analysis window. A high positive correlation indicates synchronized, directional activity, while a negative correlation suggests choppy, conflicting action.

The final Coherence score (0-100) represents the percentage of market organization. A high score is a prerequisite for any signal, filtering out unpredictable market conditions.

2. 💎 PILLAR II: HARMONIC LIQUIDITY MATRIX (THE 'LOCATION')

Purpose: To identify and map high-impact institutional footprints. This pillar answers the question: " Where have institutions previously committed significant capital? "

Conceptual Framework: Large institutional orders leave indelible marks on the market in the form of anomalous volume spikes at specific price levels. These are not random occurrences but are areas of intense historical interest. The Harmonic Liquidity Matrix finds these footprints and consolidates them into actionable support and resistance zones called "Harmonic Nodes."

Algorithmic Process:

Footprint Identification: The engine scans the historical lookback period for candles where volume > average_volume * Institutional_Volume_Filter. This identifies statistically significant volume events.

Node Creation: A raw node is created at the mean price of the identified candle.

Dynamic Clustering: The engine uses an ATR-based proximity algorithm. If a new footprint is identified within Node_Clustering_Distance (ATR) of an existing Harmonic Node, it is merged. The node's price is volume-weighted, and its magnitude is increased. This prevents chart clutter and consolidates nearby institutional orders into a single, more significant level.

Node Decay: Nodes that are older than the Institutional_Liquidity_Scanback period are automatically removed from the chart, ensuring the analysis remains relevant to recent market dynamics.

3. 🌊 PILLAR III: CYCLICAL RESONANCE MATRIX (THE 'TIMING')

Purpose: To identify the market's dominant rhythm and its current phase. This pillar answers the question: " Is the market's immediate energy flowing up or down? "

Conceptual Framework: Markets move in waves and cycles of varying lengths. Trading in harmony with the current cyclical phase dramatically increases the probability of success. Aetherium employs a simplified wavelet analysis concept to decompose price action into short, medium, and long-term cycles.

Algorithmic Process:

Cycle Decomposition: The engine calculates three oscillators based on the difference between pairs of Exponential Moving Averages (e.g., EMA8-EMA13 for short cycle, EMA21-EMA34 for medium cycle).

Energy Measurement: The 'energy' of each cycle is determined by its recent volatility (standard deviation). The cycle with the highest energy is designated as the "Dominant Cycle."

Phase Analysis: The engine determines if the dominant cycles are in a bullish phase (rising from a trough) or a bearish phase (falling from a peak).

Cycle Sync: The highest conviction timing signals occur when multiple cycles (e.g., short and medium) are synchronized in the same direction, indicating broad-based momentum.

🔧 COMPREHENSIVE INPUT SYSTEM

Pillar I: Market Coherence Engine

Coherence Analysis Window (10-50, Default: 21): The lookback period for the Coherence Engine.

Lower Values (10-15): Highly responsive to rapid shifts in market control. Ideal for scalping but can be sensitive to noise.

Balanced (20-30): Excellent for day trading, capturing the ebb and flow of institutional sessions.

Higher Values (35-50): Smoother, more stable reading. Best for swing trading and identifying long-term institutional campaigns.

Coherence Activation Level (50-90%, Default: 70%): The minimum market organization required to enable signal generation.

Strict (80-90%): Only allows signals in extremely clear, powerful trends. Fewer, but potentially higher quality signals.

Standard (65-75%): A robust filter that effectively removes choppy conditions while capturing most valid institutional moves.

Lenient (50-60%): Allows signals in less-organized markets. Can be useful in ranging markets but may increase false signals.

Pillar II: Harmonic Liquidity Matrix

Institutional Liquidity Scanback (100-400, Default: 200): How far back the engine looks for institutional footprints.

Short (100-150): Focuses on recent institutional activity, providing highly relevant, immediate levels.

Long (300-400): Identifies major, long-term structural levels. These nodes are often extremely powerful but may be less frequent.

Institutional Volume Filter (1.3-3.0, Default: 1.8): The multiplier for detecting a volume spike.

High (2.5-3.0): Only registers climactic, undeniable institutional volume. Fewer, but more significant nodes.

Low (1.3-1.7): More sensitive, identifying smaller but still relevant institutional interest.

Node Clustering Distance (0.2-0.8 ATR, Default: 0.4): The ATR-based distance for merging nearby nodes.

High (0.6-0.8): Creates wider, more consolidated zones of liquidity.

Low (0.2-0.3): Creates more numerous, precise, and distinct levels.

Pillar III: Cyclical Resonance Matrix

Cycle Resonance Analysis (30-100, Default: 50): The lookback for determining cycle energy and dominance.

Short (30-40): Tunes the engine to faster, shorter-term market rhythms. Best for scalping.

Long (70-100): Aligns the timing component with the larger primary trend. Best for swing trading.

Institutional Signal Architecture

Signal Quality Mode (Professional, Elite, Supreme): Controls the strictness of the three-pillar confluence.

Professional: Loosest setting. May generate signals if two of the three pillars are in strong alignment. Increases signal frequency.

Elite: Balanced setting. Requires a clear, unambiguous resonance of all three pillars. The recommended default.

Supreme: Most stringent. Requires perfect alignment of all three pillars, with each pillar exhibiting exceptionally strong readings (e.g., coherence > 85%). The highest conviction signals.

Signal Spacing Control (5-25, Default: 10): The minimum bars between signals to prevent clutter and redundant alerts.

🎨 ADVANCED VISUAL SYSTEM

The visual architecture of Aetherium is designed not merely for aesthetics, but to provide an intuitive, at-a-glance understanding of the complex data being processed.

Harmonic Liquidity Nodes: The core visual element. Displayed as multi-layered, semi-transparent horizontal boxes.

Magnitude Visualization: The height and opacity of a node's "glow" are proportional to its volume magnitude. More significant nodes appear brighter and larger, instantly drawing the eye to key levels.

Color Coding: Standard nodes are blue/purple, while exceptionally high-magnitude nodes are highlighted in an accent color to denote critical importance.

🌌 Quantum Resonance Field: A dynamic background gradient that visualizes the overall market environment.

Color: Shifts from cool blues/purples (low coherence) to energetic greens/cyans (high coherence and organization), providing instant context.

Intensity: The brightness and opacity of the field are influenced by total market energy (a composite of coherence, momentum, and volume), making powerful market states visually apparent.

💎 Crystalline Lattice Matrix: A geometric web of lines projected from a central moving average.

Mathematical Basis: Levels are projected using multiples of the Golden Ratio (Phi ≈ 1.618) and the ATR. This visualizes the natural harmonic and fractal structure of the market. It is not arbitrary but is based on mathematical principles of market geometry.

🧠 Synaptic Flow Network: A dynamic particle system visualizing the engine's "thought process."

Node Density & Activation: The number of particles and their brightness/color are tied directly to the Market Coherence score. In high-coherence states, the network becomes a dense, bright, and organized web. In chaotic states, it becomes sparse and dim.

⚡ Institutional Energy Waves: Flowing sine waves that visualize market volatility and rhythm.

Amplitude & Speed: The height and speed of the waves are directly influenced by the ATR and volume, providing a feel for market energy.

📊 INSTITUTIONAL CONTROL MATRIX (DASHBOARD)

The dashboard is the central command console, providing a real-time, quantitative summary of each pillar's status.

Header: Displays the script title and version.

Coherence Engine Section:

State: Displays a qualitative assessment of market organization: ◉ PHASE LOCK (High Coherence), ◎ ORGANIZING (Moderate Coherence), or ○ CHAOTIC (Low Coherence). Color-coded for immediate recognition.

Power: Shows the precise Coherence percentage and a directional arrow (↗ or ↘) indicating if organization is increasing or decreasing.

Liquidity Matrix Section:

Nodes: Displays the total number of active Harmonic Liquidity Nodes currently being tracked.

Target: Shows the price level of the nearest significant Harmonic Node to the current price, representing the most immediate institutional level of interest.

Cycle Matrix Section:

Cycle: Identifies the currently dominant market cycle (e.g., "MID ") based on cycle energy.

Sync: Indicates the alignment of the cyclical forces: ▲ BULLISH , ▼ BEARISH , or ◆ DIVERGENT . This is the core timing confirmation.

Signal Status Section:

A unified status bar that provides the final verdict of the engine. It will display "QUANTUM SCAN" during neutral periods, or announce the tier and direction of an active signal (e.g., "◉ TIER 1 BUY ◉" ), highlighted with the appropriate color.

🎯 SIGNAL GENERATION LOGIC

Aetherium's signal logic is built on the principle of strict, non-negotiable confluence.

Condition 1: Context (Coherence Filter): The Market Coherence must be above the Coherence Activation Level. No signals can be generated in a chaotic market.

Condition 2: Location (Liquidity Node Interaction): Price must be actively interacting with a significant Harmonic Liquidity Node.

For a Buy Signal: Price must be rejecting the Node from below (testing it as support).

For a Sell Signal: Price must be rejecting the Node from above (testing it as resistance).

Condition 3: Timing (Cycle Alignment): The Cyclical Resonance Matrix must confirm that the dominant cycles are synchronized with the intended trade direction.

Signal Tiering: The Signal Quality Mode input determines how strictly these three conditions must be met. 'Supreme' mode, for example, might require not only that the conditions are met, but that the Market Coherence is exceptionally high and the interaction with the Node is accompanied by a significant volume spike.

Signal Spacing: A final filter ensures that signals are spaced by a minimum number of bars, preventing over-alerting in a single move.

🚀 ADVANCED TRADING STRATEGIES

The Primary Confluence Strategy: The intended use of the system. Wait for a Tier 1 (Elite/Supreme) or Tier 2 (Professional/Elite) signal to appear on the chart. This represents the alignment of all three pillars. Enter after the signal bar closes, with a stop-loss placed logically on the other side of the Harmonic Node that triggered the signal.

The Coherence Context Strategy: Use the Coherence Engine as a standalone market filter. When Coherence is high (>70%), favor trend-following strategies. When Coherence is low (<50%), avoid new directional trades or favor range-bound strategies. A sharp drop in Coherence during a trend can be an early warning of a trend's exhaustion.

Node-to-Node Trading: In a high-coherence environment, use the Harmonic Liquidity Nodes as both entry points and profit targets. For example, after a BUY signal is generated at one Node, the next Node above it becomes a logical first profit target.

⚖️ RESPONSIBLE USAGE AND LIMITATIONS

Decision Support, Not a Crystal Ball: Aetherium is an advanced decision-support tool. It is designed to identify high-probability conditions based on a model of institutional behavior. It does not predict the future.

Risk Management is Paramount: No indicator can replace a sound risk management plan. Always use appropriate position sizing and stop-losses. The signals provided are probabilistic, not certainties.

Past Performance Disclaimer: The market models used in this script are based on historical data. While robust, there is no guarantee that these patterns will persist in the future. Market conditions can and do change.

Not a "Set and Forget" System: The indicator performs best when its user understands the concepts behind the three pillars. Use the dashboard and visual cues to build a comprehensive view of the market before acting on a signal.

Backtesting is Essential: Before applying this tool to live trading, it is crucial to backtest and forward-test it on your preferred instruments and timeframes to understand its unique behavior and characteristics.

🔮 CONCLUSION

The Aetherium Institutional Market Resonance Engine represents a paradigm shift from single-variable analysis to a holistic, multi-pillar framework. By quantifying the abstract concepts of market context, location, and timing into a unified, logical system, it provides traders with an unprecedented lens into the mechanics of institutional market operations.

It is not merely an indicator, but a complete analytical engine designed to foster a deeper understanding of market dynamics. By focusing on the core principles of institutional order flow, Aetherium empowers traders to filter out market noise, identify key structural levels, and time their entries in harmony with the market's underlying rhythm.

"In all chaos there is a cosmos, in all disorder a secret order." - Carl Jung

— Dskyz, Trade with insight. Trade with confluence. Trade with Aetherium.

TPO[Fixed Range, Anchored, Bars Back]TPO Bars Back, Fixed Range and Anchored

Overview

The TPO Profile (Time Price Opportunity Profile) is a powerful market profile indicator that displays the amount of time price spent at different levels during a specified period. Unlike traditional volume profile indicators that show volume distribution, TPO Profile shows time distribution , providing insights into where price has spent the most time and identifying key support and resistance levels.

Key Advantages Over TradingView's Built-in TPO

Simplified Composite Creation : Automatically creates TPO profiles for any time range without manual split/merge operations

Instant Value Area Calculation : Immediately shows Value Area, POC, VAH, and VAL for your selected period

No Manual Assembly Required : TradingView's native TPO requires you to manually split sessions and merge them to create composites - this indicator does it automatically

Flexible Time Ranges : Create composites for any custom time period (multiple days, weeks, specific events) with a few clicks

Real-time Composite Updates : Anchor mode creates live composites that update as new data arrives

Multiple Composite Analysis : Easily compare different time periods without the tedious manual process

Key Features

Core Functionality

Time-Based Analysis : Shows time spent at each price level rather than volume

Configurable Time Blocks : Use any timeframe for TPO counting (30min, 1H, 4H, etc.)

Multiple Price Levels : Adjustable from 5 to 200 levels for granular analysis

Point of Control (POC) : Automatically identifies the price level with highest time activity

Value Area Calculation : Shows the price range containing 70% (configurable) of time activity

Automatic Composite Generation : Creates multi-session composites without manual intervention

Three Operating Modes

1. Bars Back Mode

Analyzes the last N bars from the current bar

Perfect for recent market activity analysis

Range: 10-500 bars

Use Case : Intraday analysis, recent session review

2. Fixed Range Mode

Analyzes a specific time period between start and end times

Ideal for historical analysis of specific events

Creates perfect composites for multi-day periods

Use Case : Earnings periods, news events, specific trading sessions, weekly/monthly composites

3. Anchor Mode (NEW)

Starts from a specific time and extends to the current bar

Dynamically updates as new bars form

Perfect for building live composites from any starting point

Use Case : Live session monitoring, event-based analysis from a specific point, growing composites

Visual Elements

TPO Bars

Horizontal bars showing time distribution at each price level

Longer bars = more time spent at that level

Color-coded to distinguish Value Area from outlying levels

Point of Control (POC)

Red line marking the price level with highest time activity

Most significant support/resistance level

Configurable line style (Solid/Dashed/Dotted) and width

Value Area High/Low (VAH/VAL)

Green and Orange lines marking the boundaries of the Value Area

Shows the price range containing the specified percentage of time activity

Optional display with customizable line styles

Single Print Detection

Identifies price levels touched by only one time block

Display options: Lines or Boxes

Purple color highlighting these significant levels

Often act as strong support/resistance in future trading

Customization Options

Time Block Configuration

Block Time : Choose timeframe for TPO counting (30min, 1H, 4H, etc.)

Allows analysis at different time granularities

Higher timeframes = broader perspective, Lower timeframes = finer detail

Visual Styling

Line Styles : Solid, Dashed, or Dotted for all line elements

Line Widths : 1-5 pixels for POC, VAH, and VAL lines

Colors : Fully customizable colors for all elements

Transparency : Adjustable transparency for better chart readability

Label Management

Show/Hide Labels : Toggle POC, VAH, VAL labels

Font Sizes : Tiny, Small, Normal, Large, Huge

Label Positioning : 8 different position options relative to lines

Offset Controls : Fine-tune label positioning

Line Extension

Level Offset Right : Controls how far lines extend

Smart extension logic:

Value ≤ 0: Infinite extension (extend.right)

Value ≥ 1: Extends exactly N bars ahead

Trading Applications

Support & Resistance

POC often acts as strong support/resistance

Value Area boundaries provide key levels

Single prints frequently become significant levels

Market Structure Analysis

Identify areas of price acceptance (thick TPO bars)

Spot areas of price rejection (thin TPO bars)

Understand where market participants are comfortable trading

Composite Profile Analysis

Create multi-day, weekly, or monthly composites instantly

Compare different composite periods without manual work

Analyze longer-term price acceptance levels

Build composites around specific events or announcements

Session Analysis

Monitor intraday session development in real-time

Compare different sessions (London, New York, Asia)

Track how profiles change throughout the trading day

Build live composites across multiple sessions

Event Analysis

Use Fixed Range mode for earnings, news events

Use Anchor mode to track price development from specific events

Compare pre/post event price acceptance levels

Create event-based composites automatically

Input Parameters

Mode Selection

Mode : Bars Back | Fixed Range | Anchor

Bars Back : Number of bars to analyze (10-500)

Start Time : Beginning time for Fixed Range and Anchor modes

End Time : Ending time for Fixed Range mode only

Analysis Configuration

Block Time : Timeframe for TPO blocks (e.g., "30" for 30-minute blocks)

TPO Levels : Number of price levels (5-200)

Value Area % : Percentage for Value Area calculation (50-95%)

Display Options

Show POC : Display Point of Control line

Show Value Area : Display Value Area box

Show VAH/VAL Lines : Display Value Area boundary lines

Show Single Prints : Display single print detection

Single Print Style : Lines or Boxes

Styling Controls

Colors : TPO, POC, Value Area, VAH, VAL, Single Print colors

Line Styles : POC, VAH, VAL line styles

Line Widths : POC, VAH, VAL line widths

Labels : Show/hide, font size, position, offset controls

Technical Details

Calculation Method

Divides the price range into equal levels based on TPO Levels setting

For each time block, determines which price levels it crosses

Adds +1 count to each crossed level

Identifies POC as the level with highest count

Calculates Value Area by expanding from POC until target percentage is reached

Performance Considerations

Historical data limited to prevent buffer overflow errors

Smart bounds checking for different timeframes

Optimized cleanup routines to prevent drawing object accumulation

Pine Script Version

Built on Pine Script v6

Uses modern Pine Script best practices

Efficient array handling and drawing object management

Best Practices

Timeframe Selection

Block Time = Chart Timeframe : Traditional TPO approach

Block Time > Chart Timeframe : Smoother, broader perspective

Block Time < Chart Timeframe : More granular, detailed analysis

Level Count Guidelines

Low levels (10-20) : Better for swing trading, major levels

High levels (50-100) : Better for scalping, precise entries

Very high levels (100+) : For very detailed analysis

Mode Selection

Bars Back : Daily analysis, recent activity

Fixed Range : Historical events, specific periods, manual composites

Anchor : Live monitoring, event-based analysis, growing composites

Composite Creation Workflow

Select Fixed Range or Anchor mode

Set your desired start time (and end time for Fixed Range)

Adjust TPO Levels for desired granularity

Enable VAH/VAL lines to see Value Area boundaries

The composite profile generates automatically with all key levels

This indicator eliminates the tedious manual process of creating composite TPO profiles in TradingView. Instead of splitting sessions and manually merging them, you get instant composite analysis with automatic Value Area calculation, POC identification, and single print detection. The combination of time-based analysis, multiple operating modes, and extensive customization options makes it a powerful tool for understanding market structure and price acceptance levels across any time period.

Simple Pips GridOverview

This is a clean, simple, and highly practical indicator that draws horizontal grid lines at user-defined pip intervals.

Unlike other complex grid indicators, this script is designed to be lightweight and error-free. It eliminates automatic symbol detection and instead gives you full manual control, ensuring it works perfectly with any symbol you trade—FX, CFDs, Crypto, Stocks, Indices, and more.

Key Features

Universal Compatibility: Works with any trading pair by letting you manually define the pip value.

Fully Customizable: Easily set the pip interval for your grid (e.g., 10 pips, 50 pips, 100 pips).

Lightweight & Fast: Simple code ensures smooth performance without lagging your chart.

Visual Customization: Change the color, width, and style (solid, dashed, dotted) of the grid lines.

How to Use

It's incredibly simple to set up. You only need to configure two main settings:

Step 1: Set the "Pip Value"

This is the most important setting. You need to tell the indicator what "1 pip" means for the symbol you are currently viewing.

Go to the indicator settings and find the "Pip Value" input. Here are some common examples:

Symbol Pip Value (Input this number)

USD/JPY 0.01

EUR/USD 0.0001

GBP/USD 0.0001

XAU/USD (Gold) 0.1

JP225 (Nikkei 225) 10

US500 (S&P 500) 1

BTC/USD 0.1 or 1.0 (depending on your preference)

Step 2: Set the "Pip Interval"

Next, in the "Pip Interval" input, simply type how many pips you want between each line.

For a 10-pip grid, enter 10.

For a 50-pip grid, enter 50.

That's it! The grid will now be perfectly aligned to your specifications.

Additional Settings

Line Color, Width, Style: Customize the appearance of the lines to match your chart theme.

Number of Lines: Adjust how many lines are drawn above and below the current price to optimize performance and visibility.

This script was created with the assistance of Gemini (Google's AI) to be a simple and reliable tool for all traders. Feel free to use and modify it. Happy trading!

Heatmap Trailing Stop with Breakouts (Zeiierman)█ Overview

Heatmap Trailing Stop with Breakouts (Zeiierman) is a trend and breakout detection tool that combines dynamic trailing stop logic, Fibonacci-based levels, and a real-time market heatmap into a single, intuitive system.

This indicator is designed to help traders visualize pressure zones, manage stop placement, and identify breakout opportunities supported by contextual price–derived heat. Whether you're trailing trends, detecting reversals, or entering on explosive breakouts — this tool keeps you anchored in structure and sentiment.

It projects adaptive trailing stop levels and calculates Fibonacci extensions from swing-based extremes. These levels are then colored by a market heatmap engine that tracks price interaction intensity — showing where the market is "hot" and likely to respond.

On top of that, it includes breakout signals powered by HTF momentum conditions, trend direction, and heatmap validation — giving you signals only when the context is strong.

█ How It Works

⚪ Trailing Stop Engine

At its core, the script uses an ATR-based trailing stop with trend detection:

ATR Length – Defines volatility smoothing using EMA MA of true range.

Multiplier – Expands/retracts the trailing offset depending on market aggression.

Real-Time Extremum Tracking – Uses local highs/lows to define Fibonacci anchors.

⚪ Fibonacci Projection + Heatmap

With each trend shift, Fibonacci levels are projected from the new swing to the current trailing stop. These include:

Fib 61.8, 78.6, 88.6, and 100% (trailing stop) lines

Heatmap Coloring – Each level'slevel's color is determined by how frequently price has interacted with that level in the recent range (defined by ATR).

Strength Score (1–10) – The number of touches per level is normalized and averaged to create a heatmap ""score"" displayed as a colored bar on the chart.

⚪ Breakout Signal System

This engine detects high-confidence breakout signals using a higher timeframe candle structure:

Bullish Breakout – Strong bullish candle + momentum + trend confirmation + heatmap score threshold.

Bearish Breakout – Strong bearish candle + momentum + trend confirmation + heatmap score threshold.

Cooldown Logic – Prevents signals from clustering too frequently during volatile periods.

█ How to Use

⚪ Trend Following & Trail Stops

Use the Trailing Stop line to manage positions or time entries in line with trend direction. Trailing stop flips are highlighted with dot markers.

⚪ Fibonacci Heat Zones

The projected Fibonacci levels serve as price magnets or support/resistance zones. Watch how price reacts at Fib 61.8/78.6/88.6 levels — especially when they're glowing with high heatmap scores (more glow = more historical touches = stronger significance).

⚪ Breakout Signals

Enable breakout signals when you want to trade breakouts only under strong context. Use the "Heatmap Strength Threshold" to require a minimum score (1–10).

█ Settings

Stop Distance ATR Length – ATR period for volatility smoothing

Stop Distance Multiplier – Adjusts the trailing stop'sstop's distance from price

Heatmap Range ATR Length – Defines how far back the heatmap scans for touches

Number of Heat Levels – Total levels used in the heatmap (more = finer resolution)

Minimum Touches per Level – Defines what counts as a ""hot"" level

Heatmap Strength Threshold – Minimum average heat score (1–10) required for breakouts

Timeframe – HTF source used to evaluate breakout momentum structure

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Anomalous Holonomy Field Theory🌌 Anomalous Holonomy Field Theory (AHFT) - Revolutionary Quantum Market Analysis

Where Theoretical Physics Meets Trading Reality

A Groundbreaking Synthesis of Differential Geometry, Quantum Field Theory, and Market Dynamics

🔬 THEORETICAL FOUNDATION - THE MATHEMATICS OF MARKET REALITY

The Anomalous Holonomy Field Theory represents an unprecedented fusion of advanced mathematical physics with practical market analysis. This isn't merely another indicator repackaging old concepts - it's a fundamentally new lens through which to view and understand market structure .

1. HOLONOMY GROUPS (Differential Geometry)

In differential geometry, holonomy measures how vectors change when parallel transported around closed loops in curved space. Applied to markets:

Mathematical Formula:

H = P exp(∮_C A_μ dx^μ)

Where:

P = Path ordering operator

A_μ = Market connection (price-volume gauge field)

C = Closed price path

Market Implementation:

The holonomy calculation measures how price "remembers" its journey through market space. When price returns to a previous level, the holonomy captures what has changed in the market's internal geometry. This reveals:

Hidden curvature in the market manifold

Topological obstructions to arbitrage

Geometric phase accumulated during price cycles

2. ANOMALY DETECTION (Quantum Field Theory)

Drawing from the Adler-Bell-Jackiw anomaly in quantum field theory:

Mathematical Formula:

∂_μ j^μ = (e²/16π²)F_μν F̃^μν

Where:

j^μ = Market current (order flow)

F_μν = Field strength tensor (volatility structure)

F̃^μν = Dual field strength

Market Application:

Anomalies represent symmetry breaking in market structure - moments when normal patterns fail and extraordinary opportunities arise. The system detects:

Spontaneous symmetry breaking (trend reversals)

Vacuum fluctuations (volatility clusters)

Non-perturbative effects (market crashes/melt-ups)

3. GAUGE THEORY (Theoretical Physics)

Markets exhibit gauge invariance - the fundamental physics remains unchanged under certain transformations:

Mathematical Formula:

A'_μ = A_μ + ∂_μΛ

This ensures our signals are gauge-invariant observables , immune to arbitrary market "coordinate changes" like gaps or reference point shifts.

4. TOPOLOGICAL DATA ANALYSIS

Using persistent homology and Morse theory:

Mathematical Formula:

β_k = dim(H_k(X))

Where β_k are the Betti numbers describing topological features that persist across scales.

🎯 REVOLUTIONARY SIGNAL CONFIGURATION

Signal Sensitivity (0.5-12.0, default 2.5)

Controls the responsiveness of holonomy field calculations to market conditions. This parameter directly affects the threshold for detecting quantum phase transitions in price action.

Optimization by Timeframe:

Scalping (1-5min): 1.5-3.0 for rapid signal generation

Day Trading (15min-1H): 2.5-5.0 for balanced sensitivity

Swing Trading (4H-1D): 5.0-8.0 for high-quality signals only

Score Amplifier (10-200, default 50)

Scales the raw holonomy field strength to produce meaningful signal values. Higher values amplify weak signals in low-volatility environments.

Signal Confirmation Toggle

When enabled, enforces additional technical filters (EMA and RSI alignment) to reduce false positives. Essential for conservative strategies.

Minimum Bars Between Signals (1-20, default 5)

Prevents overtrading by enforcing quantum decoherence time between signals. Higher values reduce whipsaws in choppy markets.

👑 ELITE EXECUTION SYSTEM

Execution Modes:

Conservative Mode:

Stricter signal criteria

Higher quality thresholds

Ideal for stable market conditions

Adaptive Mode:

Self-adjusting parameters

Balances signal frequency with quality

Recommended for most traders

Aggressive Mode:

Maximum signal sensitivity

Captures rapid market moves

Best for experienced traders in volatile conditions

Dynamic Position Sizing:

When enabled, the system scales position size based on:

Holonomy field strength

Current volatility regime

Recent performance metrics

Advanced Exit Management:

Implements trailing stops based on ATR and signal strength, with mode-specific multipliers for optimal profit capture.

🧠 ADAPTIVE INTELLIGENCE ENGINE

Self-Learning System:

The strategy analyzes recent trade outcomes and adjusts:

Risk multipliers based on win/loss ratios

Signal weights according to performance

Market regime detection for environmental adaptation

Learning Speed (0.05-0.3):

Controls adaptation rate. Higher values = faster learning but potentially unstable. Lower values = stable but slower adaptation.

Performance Window (20-100 trades):

Number of recent trades analyzed for adaptation. Longer windows provide stability, shorter windows increase responsiveness.

🎨 REVOLUTIONARY VISUAL SYSTEM

1. Holonomy Field Visualization

What it shows: Multi-layer quantum field bands representing market resonance zones

How to interpret:

Blue/Purple bands = Primary holonomy field (strongest resonance)

Band width = Field strength and volatility

Price within bands = Normal quantum state

Price breaking bands = Quantum phase transition

Trading application: Trade reversals at band extremes, breakouts on band violations with strong signals.

2. Quantum Portals

What they show: Entry signals with recursive depth patterns indicating momentum strength

How to interpret:

Upward triangles with portals = Long entry signals

Downward triangles with portals = Short entry signals

Portal depth = Signal strength and expected momentum

Color intensity = Probability of success

Trading application: Enter on portal appearance, with size proportional to portal depth.

3. Field Resonance Bands

What they show: Fibonacci-based harmonic price zones where quantum resonance occurs

How to interpret:

Dotted circles = Minor resonance levels

Solid circles = Major resonance levels

Color coding = Resonance strength

Trading application: Use as dynamic support/resistance, expect reactions at resonance zones.

4. Anomaly Detection Grid

What it shows: Fractal-based support/resistance with anomaly strength calculations

How to interpret:

Triple-layer lines = Major fractal levels with high anomaly probability

Labels show: Period (H8-H55), Price, and Anomaly strength (φ)

⚡ symbol = Extreme anomaly detected

● symbol = Strong anomaly

○ symbol = Normal conditions

Trading application: Expect major moves when price approaches high anomaly levels. Use for precise entry/exit timing.

5. Phase Space Flow

What it shows: Background heatmap revealing market topology and energy

How to interpret:

Dark background = Low market energy, range-bound

Purple glow = Building energy, trend developing

Bright intensity = High energy, strong directional move

Trading application: Trade aggressively in bright phases, reduce activity in dark phases.

📊 PROFESSIONAL DASHBOARD METRICS

Holonomy Field Strength (-100 to +100)

What it measures: The Wilson loop integral around price paths

>70: Strong positive curvature (bullish vortex)

<-70: Strong negative curvature (bearish collapse)

Near 0: Flat connection (range-bound)

Anomaly Level (0-100%)

What it measures: Quantum vacuum expectation deviation

>70%: Major anomaly (phase transition imminent)

30-70%: Moderate anomaly (elevated volatility)

<30%: Normal quantum fluctuations

Quantum State (-1, 0, +1)

What it measures: Market wave function collapse

+1: Bullish eigenstate |↑⟩

0: Superposition (uncertain)

-1: Bearish eigenstate |↓⟩

Signal Quality Ratings

LEGENDARY: All quantum fields aligned, maximum probability

EXCEPTIONAL: Strong holonomy with anomaly confirmation

STRONG: Good field strength, moderate anomaly

MODERATE: Decent signals, some uncertainty

WEAK: Minimal edge, high quantum noise

Performance Metrics

Win Rate: Rolling performance with emoji indicators

Daily P&L: Real-time profit tracking

Adaptive Risk: Current risk multiplier status

Market Regime: Bull/Bear classification

🏆 WHY THIS CHANGES EVERYTHING

Traditional technical analysis operates on 100-year-old principles - moving averages, support/resistance, and pattern recognition. These work because many traders use them, creating self-fulfilling prophecies.

AHFT transcends this limitation by analyzing markets through the lens of fundamental physics:

Markets have geometry - The holonomy calculations reveal this hidden structure

Price has memory - The geometric phase captures path-dependent effects

Anomalies are predictable - Quantum field theory identifies symmetry breaking

Everything is connected - Gauge theory unifies disparate market phenomena

This isn't just a new indicator - it's a new way of thinking about markets . Just as Einstein's relativity revolutionized physics beyond Newton's mechanics, AHFT revolutionizes technical analysis beyond traditional methods.

🔧 OPTIMAL SETTINGS FOR MNQ 10-MINUTE

For the Micro E-mini Nasdaq-100 on 10-minute timeframe:

Signal Sensitivity: 2.5-3.5

Score Amplifier: 50-70

Execution Mode: Adaptive

Min Bars Between: 3-5

Theme: Quantum Nebula or Dark Matter

💭 THE JOURNEY - FROM IMPOSSIBLE THEORY TO TRADING REALITY

Creating AHFT was a mathematical odyssey that pushed the boundaries of what's possible in Pine Script. The journey began with a seemingly impossible question: Could the profound mathematical structures of theoretical physics be translated into practical trading tools?

The Theoretical Challenge:

Months were spent diving deep into differential geometry textbooks, studying the works of Chern, Simons, and Witten. The mathematics of holonomy groups and gauge theory had never been applied to financial markets. Translating abstract mathematical concepts like parallel transport and fiber bundles into discrete price calculations required novel approaches and countless failed attempts.

The Computational Nightmare:

Pine Script wasn't designed for quantum field theory calculations. Implementing the Wilson loop integral, managing complex array structures for anomaly detection, and maintaining computational efficiency while calculating geometric phases pushed the language to its limits. There were moments when the entire project seemed impossible - the script would timeout, produce nonsensical results, or simply refuse to compile.

The Breakthrough Moments:

After countless sleepless nights and thousands of lines of code, breakthrough came through elegant simplifications. The realization that market anomalies follow patterns similar to quantum vacuum fluctuations led to the revolutionary anomaly detection system. The discovery that price paths exhibit holonomic memory unlocked the geometric phase calculations.

The Visual Revolution:

Creating visualizations that could represent 4-dimensional quantum fields on a 2D chart required innovative approaches. The multi-layer holonomy field, recursive quantum portals, and phase space flow representations went through dozens of iterations before achieving the perfect balance of beauty and functionality.

The Balancing Act:

Perhaps the greatest challenge was maintaining mathematical rigor while ensuring practical trading utility. Every formula had to be both theoretically sound and computationally efficient. Every visual had to be both aesthetically pleasing and information-rich.

The result is more than a strategy - it's a synthesis of pure mathematics and market reality that reveals the hidden order within apparent chaos.

📚 INTEGRATED DOCUMENTATION

Once applied to your chart, AHFT includes comprehensive tooltips on every input parameter. The source code contains detailed explanations of the mathematical theory, practical applications, and optimization guidelines. This published description provides the overview - the indicator itself is a complete educational resource.

⚠️ RISK DISCLAIMER

While AHFT employs advanced mathematical models derived from theoretical physics, markets remain inherently unpredictable. No mathematical model, regardless of sophistication, can guarantee future results. This strategy uses realistic commission ($0.62 per contract) and slippage (1 tick) in all calculations. Past performance does not guarantee future results. Always use appropriate risk management and never risk more than you can afford to lose.

🌟 CONCLUSION

The Anomalous Holonomy Field Theory represents a quantum leap in technical analysis - literally. By applying the profound insights of differential geometry, quantum field theory, and gauge theory to market analysis, AHFT reveals structure and opportunities invisible to traditional methods.

From the holonomy calculations that capture market memory to the anomaly detection that identifies phase transitions, from the adaptive intelligence that learns and evolves to the stunning visualizations that make the invisible visible, every component works in mathematical harmony.

This is more than a trading strategy. It's a new lens through which to view market reality.

Trade with the precision of physics. Trade with the power of mathematics. Trade with AHFT.

I hope this serves as a good replacement for Quantum Edge Pro - Adaptive AI until I'm able to fix it.

— Dskyz, Trade with insight. Trade with anticipation.

21DMA Structure Counter (EMA/SMA Option)21DMA Structure Counter (EMA/SMA Option)

Overview

The 21DMA Structure Counter is an advanced technical indicator that tracks consecutive periods where price action remains above a 21-period moving average structure. This indicator helps traders identify momentum phases and potential trend exhaustion points using statistical analysis.

Key Features

Moving Average Structure

- Configurable MA Type: Choose between EMA (Exponential Moving Average) or SMA (Simple Moving Average)

- 21-Period Default: Optimized for the widely-watched 21-period moving average

- Triple MA Structure: Tracks high, close, and low moving averages for comprehensive analysis

Statistical Analysis

- Cycle Counting: Automatically counts consecutive periods above the MA structure

- Historical Data: Maintains up to 2,500 historical cycles (approximately 10 years of daily data)

- Z-Score Calculation: Provides statistical context using mean and standard deviation

- Multiple Standard Deviation Levels: Displays +1, +2, and +3 standard deviation thresholds

Visual Indicators

Color-Coded Bars:

- Gray: Below 10-year average

- Yellow: Between average and +1 standard deviation

- Orange: Between +1 and +2 standard deviations

- Red: Between +2 and +3 standard deviations

- Fuchsia: Above +3 standard deviations (extreme readings)

Breadth Integration

- Multiple Breadth Options: NDFI, NDTH, NDTW (NASDAQ breadth indicators), or VIX

- Background Shading: Visual alerts when breadth reaches extreme levels

- High/Low Thresholds: Customizable levels for breadth analysis

- Real-time Display: Current breadth value shown in data table

Smart Reset Logic

- High Below Structure Reset: Automatically resets count when daily high falls below the lowest MA

- Flexible Hold Period: Continues counting during temporary weakness as long as structure isn't violated

- Precise Entry/Exit: Strict criteria for starting cycles, flexible for maintaining them

How to Use

Trend Identification

- Rising Counts: Indicate sustained momentum above key moving average structure

- Extreme Readings: Z-scores above +2 or +3 suggest potential trend exhaustion

- Historical Context: Compare current cycles to 10-year statistical averages

Risk Management

- Breadth Confirmation: Use breadth shading to confirm market-wide strength/weakness

- Statistical Extremes: Exercise caution when readings reach +3 standard deviations

- Reset Signals: Pay attention to structure violations for potential trend changes

Multi-Timeframe Application

- Daily Charts: Primary timeframe for swing trading and position management

- Weekly/Monthly: Longer-term trend analysis

- Intraday: Shorter-term momentum assessment (adjust MA period accordingly)

Settings

Moving Average Options

- Type: EMA or SMA selection

- Period: Default 21 (customizable)

- Reset Days: Days below structure required for reset

Visual Customization

- Standard Deviation Lines: Toggle and customize colors for +1, +2, +3 SD

- Breadth Selection: Choose from NDFI, NDTH, NDTW, or VIX

- Threshold Levels: Set custom high/low breadth thresholds

- Table Styling: Customize text colors, background, and font size

Technical Notes

- Data Retention: Maintains 2,500 historical cycles for robust statistical analysis

- Real-time Updates: Calculations update with each new bar

- Breadth Integration: Uses security() function to pull external breadth data

- Performance Optimized: Efficient array management prevents memory issues

Best Practices

1. Combine with Price Action: Use alongside support/resistance and chart patterns

2. Monitor Breadth Divergences: Watch for breadth weakness during strong readings

3. Respect Statistical Extremes: Exercise caution at +2/+3 standard deviation levels

4. Context Matters: Consider overall market environment and sector rotation

5. Risk Management: Use appropriate position sizing, especially at extreme readings

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis and proper risk management techniques.

Compatible with Pine Script v6 | Optimized for daily timeframes | Best used on major indices and liquid stocks

DCI### 📌 **DCI – Direction Correlation Index**

#### 🔹 **What It Is**