Liquidity Index with Advanced Statistical NormalizationLiquidity Index with Advanced Statistical Normalization

An open-source TradingView indicator for analyzing global liquidity cycles using robust statistical methods

Overview

This Pine Script indicator combines multiple macroeconomic data sources to construct a composite liquidity index that tracks global financial conditions. It employs advanced statistical techniques typically found in quantitative finance research, adapted for real-time charting.

Key Features

📊 Multi-Source Data Integration

- Federal Reserve Components: Fed Funds Rate, Reverse Repo (RRP), Treasury General Account (TGA)

- PBOC Components: China M2 Money Stock adjusted by CNY/USD exchange rate

- Volatility Index: MOVE Index (bond market volatility)

🔬 Advanced Statistical Methods

1. Theil-Sen Estimator: Robust trend detection resistant to outliers

2. Triple Normalization:

- Z-score normalization

- MAD (Median Absolute Deviation) normalization

- Quantile normalization via inverse normal CDF

3. Multi-Timeframe Analysis: Short (8-bar) and long (34-bar) windows with blended composite

📈 Signal Processing

- Log-transformation for non-linear relationships

- Smoothing via customizable SMA

- Composite signal averaging across normalization methods

Why This Approach?

Traditional liquidity indicators often suffer from:

- Sensitivity to outliers in economic data

- Assumption of normal distributions

- Single-timeframe bias

This script addresses these issues by:

- Using median-based robust statistics (Theil-Sen, MAD)

- Applying multiple normalization techniques

- Blending short and long-term perspectives

Customization Options

short_length // Short window (default: 8)

long_length // Long window (default: 34)

show_short // Display short composite

show_long // Display long composite

show_blended // Display blended signal

smoothing_length // SMA smoothing period (default: 10)

How to Use

1. Liquidity Expansion (positive values): Risk-on environment, favorable for asset prices

2. Liquidity Contraction (negative values): Risk-off environment, potential market stress

3. Divergences: Compare indicator direction vs. price action for early warnings

Potential Improvements

Community members are encouraged to enhance:

- Additional data sources (ECB balance sheet, BOJ operations, etc.)

- Alternative normalization methods (robust scaling, rank transformation)

- Machine learning integration (LSTM forecasting, regime detection)

- Alert conditions for liquidity inflection points

- Volatility-adjusted weighting schemes

Technical Notes

- Uses request.security() for multi-symbol data fetching

- All calculations handle missing data via nz() functions

- Median-based statistics computed via array operations

- Custom inverse CDF approximation (no external libraries required)

Contributing

This is a foundation for liquidity analysis. Potential extensions:

- LLM Integration: Use language models to parse Fed/PBOC meeting minutes and adjust weights dynamically

- Sentiment Layer: Incorporate crypto funding rates or options skew

- Adaptive Parameters: Auto-tune window lengths based on market regime

- Cross-Asset Validation: Backtest signals against BTC, equities, bonds

---

License: Open source - modify and redistribute freelyDisclaimer: For educational purposes only. Not financial advice.

Cerca negli script per "如何用wind搜索股票的发行价和份数"

Adaptive Vol Gauge [ParadoxAlgo]This is an overlay tool that measures and shows market ups and downs (volatility) based on daily high and low prices. It adjusts automatically to recent price changes and highlights calm or wild market periods. It colors the chart background and bars in shades of blue to cyan, with optional small labels for changes in market mood. Use it for info only—combine with your own analysis and risk controls. It's not a buy/sell signal or promise of results.Key FeaturesSmart Volatility Measure: Tracks price swings with a flexible time window that reacts to market speed.

Market Mood Detection: Spots high-energy (wild) or low-energy (calm) phases to help see shifts.

Visual Style: Uses smooth color fades on the background and bars—cyan for calm, deep blue for wild—to blend nicely on your chart.

Custom Options: Change settings like time periods, sensitivity, colors, and labels.

Chart Fit: Sits right on your main price chart without extra lines, keeping things clean.

How It WorksThe tool figures out volatility like this:Adjustment Factor:Looks at recent price ranges compared to longer ones.

Tweaks the time window (between 10-50 bars) based on how fast prices are moving.

Volatility Calc:Adds up logs of high/low ranges over the adjusted window.

Takes the square root for the final value.

Can scale it to yearly terms for easy comparison across chart timeframes.

Mood Check:Compares current volatility to its recent average and spread.

Flags "high" if above your set level, "low" if below.

Neutral in between.

This setup makes it quicker in busy markets and steadier in quiet ones.Settings You Can ChangeAdjust in the tool's menu:Base Time Window (default: 20): Starting point for calculations. Bigger numbers smooth things out but might miss quick changes.

Adjustment Strength (default: 0.5): How much it reacts to price speed. Low = steady; high = quick changes.

Yearly Scaling (default: on): Makes values comparable across short or long charts. Turn off for raw numbers.

Mood Sensitivity (default: 1.0): How strict for calling high/low moods. Low = more shifts; high = only big ones.

Show Labels (default: on): Adds tiny "High Vol" or "Low Vol" tags when moods change. They point up or down from bars.

Background Fade (default: 80): How see-through the color fill is (0 = invisible, 100 = solid).

Bar Fade (default: 50): How much color blends into your candles or bars (0 = none, 100 = full).

How to Read and Use ItColor Shifts:Background and bars fade based on mood strength:Cyan shades mean calm markets (good for steady, back-and-forth trades).

Deep blue shades mean wild markets (watch for big moves or turns).

Smooth changes show volatility building or easing.

Labels:"High Vol" (deep blue, from below bar): Start of wild phase.

"Low Vol" (cyan, from above bar): Start of calm phase.

Only shows at changes to avoid clutter. Use for timing strategy tweaks.

Trading Ideas:Mood-Based Plays: In wild phases (deep blue), try chase-momentum or breakout trades since swings are bigger. In calm phases (cyan), stick to bounce-back or range trades.

Risk Tips: Cut trade sizes in wild times to handle bigger losses. Use calm times for longer holds with close stops.

Chart Time Tips: Turn on yearly scaling for matching short and long views. Test settings on past data—loosen for quick trades (more alerts), tighten for longer ones (fewer, stronger).

Mix with Others: Add trend lines or averages—buy in calm up-moves, sell in wild down-moves. Check with volume or key levels too.

Special Cases: In big news events, it reacts faster. On slow assets, it might overstate swings—ease the adjustment strength.

Limits and TipsIt looks back at past data, so it trails real-time action and can't predict ahead.

Results differ by stock or timeframe—test on history first.

Colors and tags are just visuals; set your own alerts if needed.

Follows TradingView rules: No win promises, for learning only. Open for sharing; share thoughts in forums.

With this, you can spot market energy and tweak your trades smarter. Start on practice charts.

Volume Percentile Supertrend [BackQuant]Volume Percentile Supertrend

A volatility and participation aware Supertrend that automatically widens or tightens its bands based on where current volume sits inside its recent distribution. The goal is simple: fewer whipsaws when activity surges, faster reaction when the tape is quiet.

What it does

Calculates a standard Supertrend framework from an ATR on a volume weighted price source.

Measures current volume against its recent percentile and converts that context into a dynamic ATR multiplier.

Widens bands when volume is unusually high to reduce chop. Tightens bands when volume is unusually low to catch turns earlier.

Paints candles, draws the active Supertrend line and optional bands, and prints clear Long and Short signal markers.

Why volume percentile

Fixed ATR multipliers assume all bars are equal. They are not. When participation spikes, price swings expand and a static band gets sliced.

Percentiles place the current bar inside a recent distribution. If volume is in the top slice, the Supertrend allows more room. If volume is in the bottom slice, it expects smaller noise and tightens.

This keeps the same playbook usable across busy sessions and sleepy ones without constant manual retuning.

How it works

Volume distribution - A rolling window computes the Pth percentile of volume. Above that is flagged as high volume. A lower reference percentile marks quiet bars.

Dynamic multiplier - Start from a Base Multiplier. If bar is high volume, scale it up by a function of volume-to-average and a Sensitivity knob. If bar is low volume, scale it down. Smooth the result with an EMA to avoid jitter.

VWMA source - The price input for bands is a short volume weighted moving average of close. Heavy prints matter more.

ATR envelope - Compute ATR on your length. UpperBasic = VWMA + Multiplier x ATR. LowerBasic = VWMA - Multiplier x ATR.

Trailing logic - The final lines trail price so they only move in a direction that preserves Supertrend behavior. This prevents sudden flips from transient pokes.

Direction and signals - Direction flips when price crosses through the relevant trailing line. SupertrendLong and SupertrendShort mark those flips. The plotted Supertrend is the active trailing side.

Inputs and what they change

Volume Lookback - Window for percentile and average. Larger window = stabler percentile, smaller = snappier.

Volume Percentile Level - Threshold that defines high volume. Example 70 means top 30 percent of recent bars are treated as high activity.

Volume Sensitivity - Gain from volume ratio to the dynamic multiplier. Higher = bands expand more when volume spikes.

VWMA Source Length - Smoothing of the volume weighted price source for the bands.

ATR Length - Standard ATR window. Larger = slower, smaller = quicker.

Base Multiplier - Core band width before volume adjustment. Think of this as your neutral volatility setting.

Multiplier Smoothing - EMA on the dynamic multiplier. Reduces back and forth changes when volume oscillates around the threshold.

Show Supertrend on chart - Toggles the active line.

Show Upper Lower Bands - Draws both sides even when inactive. Good for context.

Paint candles according to Trend - Colors bars by trend direction.

Show Long and Short Signals - Prints 𝕃 and 𝕊 markers at flips.

Colors - Choose your long and short palette.

Reading the plot

Supertrend line - Thick line that hugs price from above in downtrends and from below in uptrends. Its distance breathes with volume.

Bands - Optional upper and lower rails. Useful to see the inactive side and judge how wide the envelope is right now.

Signals - 𝕃 prints when the trend flips long. 𝕊 prints when the trend flips short.

Candle colors - Quick bias read at a glance when painting is enabled.

Typical workflows

Trend following - Use 𝕃 flips to initiate longs and ride while bars remain colored long and price respects the lower trailing line. Mirror for shorts with 𝕊 and the upper trailing line. During high volume phases the line will give more room, which helps stay in the move.

Pullback adds - In an established trend, shallow tags toward the active line after a high volume expansion can be add points. The dynamic envelope adjusts to the session so your add distance is not fixed to a stale volatility regime.

Mean reversion filter - In quiet tape the multiplier contracts and flips come earlier. If you prefer fading, watch for quick toggles around the bands when volume percentile remains low. In high volume, avoid fading into the widened line unless you have other strong reasons.

Notes on behavior

High volume bar: the percentile gate opens, volRatio > 1 powers up the multiplier through the Sensitivity lever, bands widen, fewer false flips.

Low volume bar: multiplier contracts, bands tighten, flips can happen earlier which is useful when you want to catch regime changes in quiet conditions.

Smoothing matters: both the price source (VWMA) and the multiplier are smoothed to keep structure readable while still adapting.

Quick checklist

If you see frequent chop and today feels busy: check that volume is above your percentile. Wider bands are expected. Consider letting the trend prove itself against the expanded line before acting.

If everything feels slow and you want earlier entries: percentile likely marks low volume, so bands tighten and 𝕃 or 𝕊 can appear sooner.

If you want more or fewer flips overall: adjust Base Multiplier first. If you want more reaction specifically tied to volume surges: raise Volume Sensitivity. If the envelope breathes too fast: raise Multiplier Smoothing.

What the signals mean

SupertrendLong - Direction changed from non-long to long. 𝕃 marker prints. The active line switches to support below price.

SupertrendShort - Direction changed from non-short to short. 𝕊 marker prints. The active line switches to resistance above price.

Trend color - Bars painted long or short help validate context for entries and management.

Summary

Volume Percentile Supertrend adapts the classic Supertrend to the day you are trading. Volume percentile sets the mood, sensitivity translates it into dynamic band width, and smoothing keeps it clean. The result is a single plot that aims to stay conservative when the tape is loud and act decisively when it is quiet, without you having to constantly retune settings.

Pro Momentum Table + Trade Alerts📊 Indicator Name: Pro Momentum Table – ADX + DI + ATR + Astro Timing

🧠 Concept:

This indicator is designed for professional scalpers and intraday traders who want to capture only strong momentum waves — not noise. It combines trend strength, volatility, directional movement, momentum oscillation, vega divergence, and astrological timing into a single compact table on your chart.

⚙️ Components Explained:

Metric Description

ADX (Average Directional Index) Measures the strength of the trend. Values above 20 indicate that a meaningful move is starting.

+DI / -DI (Directional Indicators) Show whether buyers (+DI) or sellers (-DI) are dominating. Increasing +DI with ADX rising = bullish momentum. Increasing -DI with ADX rising = bearish momentum.

ATR (Average True Range) Shows volatility and expected range. Used for setting realistic stop-loss and multi-level targets (1×, 1.5×, 2×, 2.5× ATR).

Price Displays the current price level for quick reference.

CMO (Chande Momentum Oscillator) Measures short-term momentum direction and strength. Helps identify overbought/oversold conditions in trend continuation.

Vega Divergence Shows a synthetic reading of volatility pressure — "Bullish" when volatility expansion supports upward moves, "Bearish" for downward pressure, and "Neutral" otherwise.

Astro Remark Suggests ideal time windows based on planetary cycles for scalping entries. “Bullish Window” often aligns with high-probability long trades; “Bearish Window” favors shorts.

Trade Signal The core momentum condition: “Bullish Momentum” if ADX > 20 and +DI rising, “Bearish Momentum” if ADX > 20 and -DI rising, else “No Clear Momentum.”

📈 How to Use:

Wait for ADX > 20 – This confirms that the market is entering a strong momentum phase.

Check DI direction:

✅ +DI rising: Buyers gaining strength → look for long setups.

✅ -DI rising: Sellers gaining strength → look for short setups.

Use ATR to plan exits:

🎯 TP1 = Entry ± 1 × ATR

🎯 TP2 = Entry ± 1.5 × ATR

🎯 TP3 = Entry ± 2 × ATR

🎯 TP4 = Entry ± 2.5 × ATR

CMO & Vega Divergence: Confirm momentum direction and volatility expansion before committing.

Astro Remark: Align your scalping activity with the planetary support window for higher probability trades.

🪙 Pro Tips for Scalpers:

Only trade when ADX > 20 and DI is consistently rising. Ignore signals in choppy or sideways phases.

Avoid trades if Vega is neutral and CMO is flat – these usually indicate fake breakouts.

If targets aren’t hit within expected ATR-based time, treat the move as false and exit early.

Combine with 9 EMA and 20 EMA (hidden) for wave structure confirmation without cluttering the chart.

💡 Summary:

This indicator acts as a real-time trade decision dashboard. It removes clutter from the chart and delivers everything a professional scalper needs — strength, direction, volatility, momentum, timing, and actionable trade bias — all in one elegant table.

Volume-Weighted Money Flow [sgbpulse]Overview

The VWMF indicator is an advanced technical analysis tool that combines and summarizes five leading momentum and volume indicators (OBV, PVT, A/D, CMF, MFI) into one clear oscillator. The indicator helps to provide a clear picture of market sentiment by measuring the pressure from buyers and sellers. Unlike single indicators, VWMF provides a comprehensive view of market money flow by weighting existing indicators and presenting them in a uniform and understandable format.

Indicator Components

VWMF combines the following indicators, each normalized to a range of 0 to 100 before being weighted:

On-Balance Volume (OBV): A cumulative indicator that measures positive and negative volume flow.

Price-Volume Trend (PVT): Similar to OBV, but incorporates relative price change for a more precise measure.

Accumulation/Distribution Line (A/D): Used to identify whether an asset is being bought (accumulated) or sold (distributed).

Chaikin Money Flow (CMF): Measures the money flow over a period based on the close price's position relative to the candle's range.

Money Flow Index (MFI): A momentum oscillator that combines price and volume to measure buying and selling pressure.

Understanding the Normalized Oscillators

The indicator combines the five different momentum indicators by normalizing each one to a uniform range of 0 to 100 .

Why is Normalization Important?

Indicators like OBV, PVT, and the A/D Line are cumulative indicators whose values can become very large. To assess their trend, we use a Moving Average as a dynamic reference line . The Moving Average allows us to understand whether the indicator is currently trending up or down relative to its average behavior over time.

How Does Normalization Work?

Our normalization fully preserves the original trend of each indicator.

For Cumulative Indicators (OBV, PVT, A/D): We calculate the difference between the current indicator value and its Moving Average. This difference is then passed to the normalization process.

- If the indicator is above its Moving Average, the difference will be positive, and the normalized value will be above 50.

- If the indicator is below its Moving Average, the difference will be negative, and the normalized value will be below 50.

Handling Extreme Values: To overcome the issue of extreme values in indicators like OBV, PVT, and the A/D Line , the function calculates the highest absolute value over the selected period. This value is used to prevent sharp spikes or drops in a single indicator from compromising the accuracy of the normalization over time. It's a sophisticated method that ensures the oscillators remain relevant and accurate.

For Bounded Indicators (CMF, MFI): These indicators already operate within a known range (for example, CMF is between -1 and 1, and MFI is between 0 and 100), so they are normalized directly without an additional reference line.

Reference Line Settings:

Moving Average Type: Allows the user to choose between a Simple Moving Average (SMA) and an Exponential Moving Average (EMA).

Volume Flow MA Length: Allows the user to set the lookback period for the Moving Average, which affects the indicator's sensitivity.

The 50 line serves as the new "center line." This ensures that, even after normalization, the determination of whether a specific indicator supports a bullish or bearish trend remains clear.

Settings and Visual Tools

The indicator offers several customization options to provide a rich analysis experience:

VWMF Oscillator (Blue Line): Represents the weighted average of all five indicators. Values above 50 indicate bullish momentum, and values below 50 indicate bearish momentum.

Strength Metrics (Bullish/Bearish Strength %): Two metrics that appear on the status line, showing the percentage of indicators supporting the current trend. They range from 0% to 100%, providing a quick view of the strength of the consensus.

Dynamic Background Colors: The background color of the chart automatically changes to bullish (a blue shade by default) or bearish (a default brown-gray shade) based on the trend. The transparency of the color shows the consensus strength—the more opaque the background, the more indicators support the trend.

Advanced Settings:

- Background Color Logic: Allows the user to choose the trigger for the background color: Weighted Value (based on the combined oscillator) or Strength (based on the majority of individual indicators).

- Weights: Provides full control over the weight of each of the five indicators in the final oscillator.

Using the Data Window

TradingView provides a useful Data Window that allows you to see the exact numerical values of each normalized oscillator separately, in addition to the trend strength data.

You can use this window to:

Get more detailed information on each indicator: Viewing the precise numerical data of each of the five indicators can help in making trading decisions.

Calibrate weights: If you want to manually adjust the indicator weights (in the settings menu), you can do so while tracking the impact of each indicator on the weighted oscillator in the Data Window.

The indicator's default setting is an equal weight of 20% for each of the five indicators.

Alert Conditions

The indicator comes with a variety of built-in alerts that can be configured through the TradingView alerts menu:

VWMF Cross Above 50: An alert when the VWMF oscillator crosses above the 50 line, indicating a potential bullish momentum shift.

VWMF Cross Below 50: An alert when the VWMF oscillator crosses below the 50 line, indicating a potential bearish momentum shift.

Bullish Strength: High But Not Absolute Consensus: An alert when the bullish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bullish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bullish strength, indicating a full and absolute consensus.

Bearish Strength: High But Not Absolute Consensus: An alert when the bearish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bearish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bearish strength, indicating a full and absolute consensus.

Summary

The VWMF indicator is a powerful, all-in-one tool for analyzing market momentum, money flow, and sentiment. By combining and normalizing five different indicators into a single oscillator, it offers a holistic and accurate view of the market's underlying trend. Its dynamic visual features and customizable settings, including the ability to adjust indicator weights, provide a flexible experience for both novice and experienced traders. The built-in alerts for momentum shifts and trend consensus make it an effective tool for spotting trading opportunities with confidence. In essence, VWMF distills complex market data into clear, actionable signals.

Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

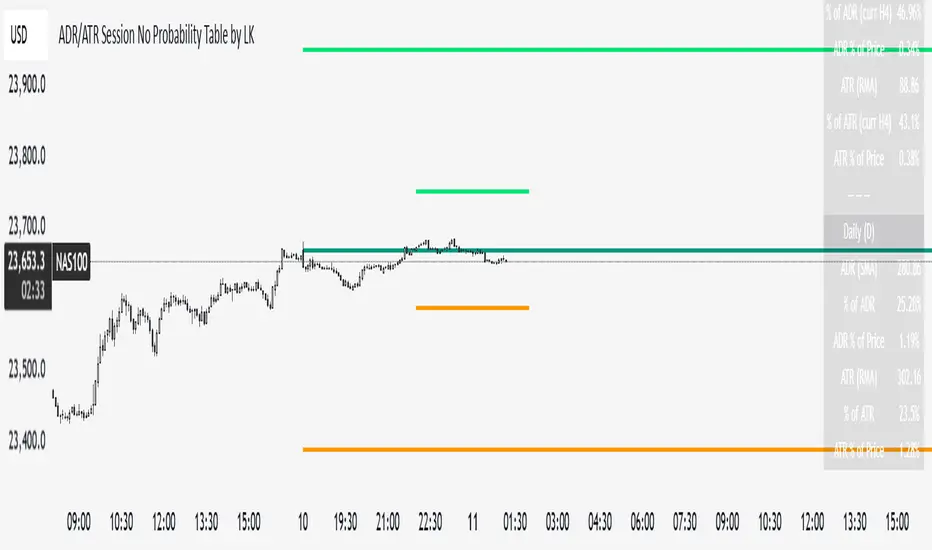

ADR/ATR Session No Probability Table by LKHere you go—clear, English docs you can drop into your script’s description or share with teammates.

ADR/ATR Session by LK — Overview

This indicator summarizes Average Daily Range (ADR) and Average True Range (ATR) for two horizons:

• Session H4 (e.g., 06:00–13:00 on a 4‑hour chart)

• Daily (D)

It shows:

• Current ADR/ATR values (using your chosen smoothing method)

• How much of ADR/ATR today/this bar has already been consumed (% of ADR/ATR)

• ADR/ATR as a percent of price

• Optional probability blocks: likelihood that %ADR will exceed user‑defined thresholds over a lookback window

• Optional on‑chart lines for the current H4 and Daily candles: Open, ADR High, ADR Low

⸻

What the metrics mean

• ADR (H4 / D): Moving average of the bar range (high - low).

• ATR (H4 / D): Moving average of True Range (max(hi-lo, |hi-close |, |lo-close |)).

• % of ADR (curr H4): (H4 range of the current H4 bar) / ADR(H4) × 100. Updates live even if the current time is outside the session.

• % of ADR (Daily): (today’s intra‑day range) / ADR(D) × 100.

• % of ATR (curr H4 / Daily): TR / ATR × 100 for that horizon.

• ADR % of Price / ATR % of Price: ADR or ATR divided by current price × 100 (a quick “volatility vs. price” gauge).

Session logic (H4): ADR/ATR(H4) only update on bars that fall inside the configured session window; outside the window the values hold steady (no recalculation “bleed”).

Daily range tracking: The indicator tracks today’s high/low in real‑time and resets at the day change.

⸻

Inputs (quick reference)

Core

• Length (ADR/ATR): smoothing length for ADR/ATR (default 21).

• Wait for Higher TF Bar Close: if true, updates ADR/ATR only after the higher‑TF bar closes when using request.security.

Timeframes

• Session Timeframe (H4): default 240.

• Daily Timeframe: default D.

Session time

• Session Timezone: “Chart” (default) or a fixed timezone.

• Session Start Hour, End Hour (minutes are fixed to 0 in this version).

Smoothing methods

• H4 ADR Method / H4 ATR Method: SMA/EMA/RMA/WMA.

• Daily ADR Method / Daily ATR Method: SMA/EMA/RMA/WMA.

Table appearance

• Table BG, Table Text, Table Font Size.

Lines (optional)

• Show current H4 segments, Show current Daily segments

• Line colors for Open / ADR High / ADR Low

• Line width

Probability

• H4 Probability Lookback (bars): number of H4 bars to examine (e.g., 300).

• Daily Probability Lookback (days): number of D bars (e.g., 180).

• ADR thresholds (%): CSV list of thresholds (e.g., 25,50,55,60,65,70,75,80,85,90,95,100,125,150).

The table will show the % of lookback bars where %ADR ≥ threshold.

Tip: If you want probabilities only for session H4 bars (not every H4 bar), ask and I can add a toggle to filter by inSess.

⸻

How to read the table

H4 block

• ADR (method) / ATR (method): the session‑aware averages.

• % of ADR (curr H4): live progress of this H4 bar toward the session ADR.

• ADR % of Price: ADR(H4) relative to price.

• % of ATR (curr H4) and ATR % of Price: same idea for ATR.

H4 Probability (lookback N bars)

• Rows like “≥ 80% ADR” show the fraction (in %) of the last N H4 bars that reached at least 80% of ADR(H4).

Daily block

• Mirrors the H4 block, but for Daily.

Daily Probability (lookback M days)

• Rows like “≥ 100% ADR” show the fraction of the last M daily bars whose daily range reached at least 100% of ADR(D).

⸻

Practical usage

• Use % of ADR (curr H4 / Daily) to judge exhaustion or room left in the day/session.

E.g., if Daily %ADR is already 95%, be cautious with momentum continuation trades.

• The probability tables give a quick historical context:

If “≥ 125% ADR” is ~18%, the market rarely stretches that far; your trade sizing/targets can reflect that.

• ADR/ATR % of Price helps normalize volatility between instruments.

⸻

Troubleshooting

• If probability rows are blank: ensure lookback windows are large enough (and that the chart has enough history).

• If ADR/ATR show … (NA): usually you don’t have enough bars for the chosen length/TF yet.

• If line segments are missing: verify you’re on a chart with visible current H4/D bars and the toggles are enabled.

⸻

Notes & customization ideas

• Add a toggle to count only session bars in H4 probability.

• Add separate thresholds for H4 vs Daily.

• Let users pick minutes for session start/end if needed.

• Add alerts when %ADR crosses specified thresholds.

If you want me to bundle any of the “ideas” above into the code, say the word and I’ll ship a clean patch.

Opening Range Breakout🧭 Overview

The Open Range Breakout (ORB) indicator is designed to capture and display the initial price range of the trading day (typically the first 15 minutes), and help traders identify breakout opportunities beyond this range. This is a popular strategy among intraday and momentum traders.

🔧 Features

📊 ORB High/Low Lines

Plots horizontal lines for the session’s high and low

🟩 Breakout Zones

Background highlights when price breaks above or below the range

🏷️ Breakout Labels

Text labels marking breakout events

🧭 Session Control

Customizable session input (default: 09:15–09:30 IST)

📍 ORB Line Labels

Text labels anchored to the ORB high and low lines (aligned right)

🔔 Alerts

Configurable alerts for breakout events

⚙️ Adjustable Settings

Show/hide background, labels, session window, etc.

⏱️ Session Logic

• The ORB range is calculated during a defined session window (default: 09:15–09:30).

• During this window, the highest high and lowest low are recorded as ORB High and ORB Low.

📈 Breakout Detection

• Breakout Above: Triggered when price crosses above the ORB High.

• Breakout Below: Triggered when price crosses below the ORB Low.

• Each breakout can trigger:

• A background highlight (green/red)

• A text label (“Breakout ↑” / “Breakout ↓”)

• An optional alert

🔔 Alerts

Two built-in alert conditions:

1. Breakout Above ORB High

• Message: "🔼 Price broke above ORB High: {{close}}"

2. Breakout Below ORB Low

• Message: "🔽 Price broke below ORB Low: {{close}}"

You can create alerts in TradingView by selecting these from the Add Alert window.

📌 Best Use Cases

• Intraday momentum trading

• Breakout and scalping strategies

• First 15-minute range traders (NSE, BSE markets)

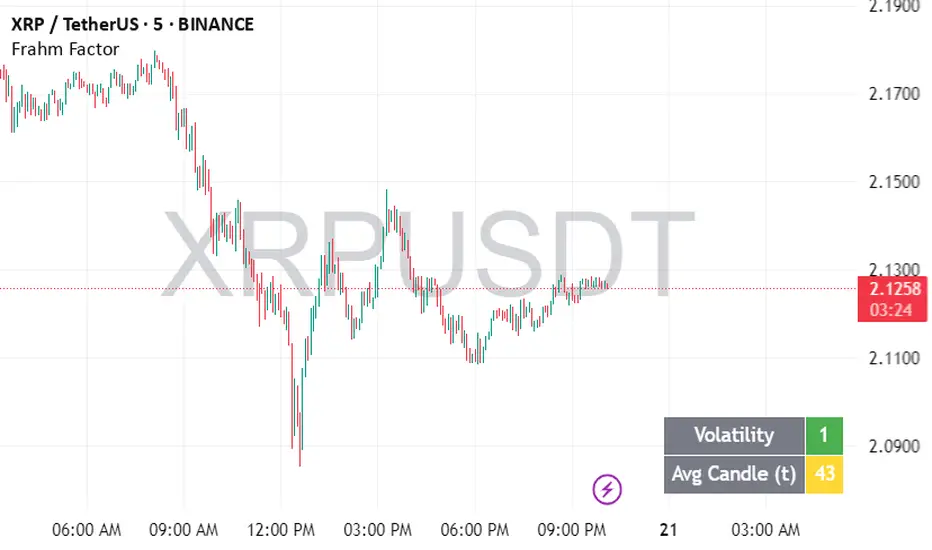

Frahm FactorIntended Usage of the Frahm Factor Indicator

The Frahm Factor is designed to give you a rapid, at-a-glance assessment of how volatile the market is right now—and how large the average candle has been—over the most recent 24-hour window. Here’s how to put it to work:

Gauge Volatility Regimes

Volatility Score (1–10)

A low score (1–3, green) signals calm seas—tight ranges, low risk of big moves.

A mid score (4–6, yellow) warns you that volatility is picking up.

A high score (7–10, red) tells you to prepare for disorderly swings or breakout opportunities.

How to trade off it

In low-volatility periods, you might favor mean-reversion or range-bound strategies.

As the score climbs into the red zone, consider widening stops, scaling back position size, or switching to breakout momentum plays.

Monitor Average Candle Size

Avg Candle (ticks) cell shows you the mean true-range of each bar over that 24h window in ticks.

When candles are small, you know the market is consolidating and liquidity may be thin.

When candles are large, momentum and volume are driving strong directional bias.

The optional dynamic color ramp (green→yellow→red) immediately flags when average bar size is unusually small or large versus its own 24h history.

Customize & Stay Flexible

Timeframes: Works on any intraday chart—from 1-minute scalping to 4-hour swing setups—because it always looks back exactly 24 hours.

Toggles:

Show or hide the Volatility and Avg-Candle cells to keep your screen uncluttered.

Turn on the dynamic color ramp only when you want that extra visual cue.

Alerts: Built-in alerts fire automatically at meaningful thresholds (Volatility ≥ 8 or ≤ 3), so you’ll never miss regime shifts, even if you step away.

Real-World Applications

Risk Management: Automatically adjust your stop-loss distances or position sizing based on the current volatility band.

Strategy Selection: Flip between range-trading and momentum strategies as the volatility regime changes.

Session Analysis: Pinpoint when during the day volatility typically ramps—perfect for doorway sessions like London opening or the US midday news spikes.

Bottom line: the Frahm Factor gives you one compact dashboard to see the pulse of the market—so you can make choices with conviction, dial your risk in real time, and never be caught off guard by sudden volatility shifts.

Logic Behind the Frahm Factor Indicator

24-Hour Rolling Window

On every intraday bar, we append that bar’s True Range (TR) and timestamp to two arrays.

We then prune any entries older than 24 hours, so the arrays always reflect exactly the last day of data.

Volatility Score (1–10)

We count how many of those 24 h TR values are less than or equal to the current bar’s TR.

Dividing by the total array size gives a percentile (0–1), which we scale and round into a 1–10 score.

Average Candle Size (ticks)

We sum all TR values in the same 24 h window, divide by array length to get the mean TR, then convert that price range into ticks.

Optionally, a green→yellow→red ramp highlights when average bar size is unusually small, medium or large versus its own 24 h history.

Color & Alerts

The Volatility cell flips green (1–3), yellow (4–6) or red (7–10) so you see regime shifts at a glance.

Built-in alertcondition calls fire when the score crosses your high (≥ 8) or low (≤ 3) thresholds.

Modularity

Everything—table location, which cells to show, dynamic coloring—is controlled by simple toggles, so you can strip it back or layer on extra visual cues as needed.

That’s the full recipe: a true 24 h look-back, a percentile-ranked volatility gauge, and a mean-bar-size meter, all wrapped into one compact dashboard.

Volume PercentileThis Pine Script indicator highlights bars where the current volume exceeds a configurable percentile threshold (e.g., 80th percentile) based on a rolling window of historical volume data.

🔍 Key Features:

Calculates a user-defined volume percentile (e.g., 75th, 80th, 90th) over a rolling window.

Marks candles where current volume is higher than the selected percentile.

Helps detect volume spikes, breakouts, or unusual activity.

Works directly on the main chart window for easier analysis.

🛠️ Inputs:

Window Length: Number of bars used to calculate the percentile (default = 20).

Percentile: The percentile threshold to trigger a high-volume signal (default = 80).

🖥️ Visualization:

Displays a red triangle marker below bars with volume above the selected percentile.

Double Top/Bottom DetectorDouble Top/Bottom Detector Indicator Description

Overview

The Double Top/Bottom Detector is a technical analysis tool designed to automatically identify and label potential double top and double bottom patterns on price charts. By combining pivot point detection with configurable height tolerance and pullback depth criteria, this indicator helps traders visually spot possible trend reversal zones without manual drawing or guesswork.

Key Features

• Pivot Point Identification

The indicator uses a symmetric window approach to find true highs and lows. A pivot high is confirmed only when a bar’s high exceeds the highs of a specified number of bars both before and after it. Likewise, a pivot low is established when a bar’s low is the lowest in its surrounding window.

• Double Top and Double Bottom Detection

– Height Tolerance: Ensures that the two pivot points forming the pattern are within a user-defined percentage of each other.

– Pullback Depth: Measures the drop (for a double top) or the rise (for a double bottom) between the two pivot points and confirms that it meets a minimum percentage threshold.

• Automatic Drawing and Labeling

When a valid double top is detected, a red line connects the two pivot highs and a “Double Top” label is centered above the line. For a double bottom, a green line connects the two pivot lows and a “Double Bottom” label appears below the midpoint.

• Pivot Visualization for Debugging

Small red and green triangles mark every detected pivot high and pivot low on the chart, making it easy to verify and fine-tune settings.

Parameters

Height Tolerance (%) – The maximum allowable percentage difference between the two pivot heights (default 2.0).

Pullback Minimum (%) – The minimum required percentage pullback (for tops) or rebound (for bottoms) between the two pivots (default 5.0).

Pivot Lookback – The number of bars to look back and forward for validating pivot points (default 5).

Window Length – The number of bars over which to compute pullback extrema, equal to twice the pivot lookback plus one (default derived from pivot lookback).

Usage Instructions

1. Copy the Pine Script code into TradingView’s editor and select version 6.

2. Adjust the parameters based on the asset’s volatility and timeframe. A larger lookback window yields fewer but more reliable pivots; tighter height tolerance produces more precise pattern matches.

3. Observe the chart for red and green triangles marking pivot highs and lows. When two qualifying pivots occur, the indicator draws a connecting line and displays a descriptive label.

4. To extend the number of visible historical lines and labels, increase the max\_lines\_count and max\_labels\_count settings in the indicator declaration.

Customization Ideas

• Add volume or moving average filters to reduce false signals.

• Encapsulate pivot logic into reusable functions for cleaner code.

• Incorporate alert conditions to receive notifications when new double top or bottom patterns form.

This indicator is well suited for medium- to long-term analysis and can be combined with risk management rules to enhance decision making.

Volume-Weighted Pivot BandsThe Volume-Weighted Pivot Bands are meant to be a dynamic, rolling pivot system designed to provide traders with responsive support and resistance levels that adapt to both price volatility and volume participation. Unlike traditional daily pivot levels, this tool recalculates levels bar-by-bar using a rolling window of volume-weighted averages, making it highly relevant for intraday traders, scalpers, swing traders, and algorithmic systems alike.

-- What This Indicator Does --

This tool calculates a rolling VWAP-based pivot level, and surrounds that central pivot with up to five upper bands (R1–R5) and five lower bands (S1–S5). These act as dynamic zones of potential resistance (R) and support (S), adapting in real time to price and volume changes.

Rather than relying on static session or daily data, this indicator provides continually evolving levels, offering more relevant levels during sideways action, trending periods, and breakout conditions.

-- How the Bands Are Calculated --

Pivot (VWAP Pivot):

The core of this system is a rolling Volume-Weighted Average Price, calculated over a user-defined window (default 20 bars). This ensures that each bar’s price impact is weighted by its volume, giving a more accurate view of fair value during the selected lookback.

Volume-Weighted Range (VW Range):

The highest high and lowest low over the same window are used to calculate the volatility range — this acts as a spread factor.

Support & Resistance Bands (S1–S5, R1–R5):

The bands are offset above and below the pivot using multiples of the VW Range:

R1 = Pivot + (VW Range × multiplier)

R2 = R1 + (VW Range × multiplier)

R3 = R2 + (VW Range x multiplier)

...

S1 = Pivot − (VW Range × multiplier)

S2 = S1 − (VW Range × multiplier)

S3 = S2 - (VW Range x multiplier)

...

You can control the multiplier manually (default is 0.25), to widen or tighten band spacing.

Smoothing (Optional):

To prevent erratic movements, you can optionally toggle on/off a simple moving average to the pivot line (default length = 20), providing a smoother trend base for the bands.

-- How to Use It --

This indicator can be used for:

Support and resistance identification:

Price often reacts to R1/S1, and the outer bands (R4/R5 or S4/S5) act as overshoot zones or strong reversal areas.

Trend context:

If price is respecting upper bands (R2–R3), the trend is likely bullish. If price is pressing into S3 or lower, it may indicate sustained selling pressure or a breakdown.

Volatility framing:

The distance between bands adjusts based on price range over the rolling window. In tighter markets, the bands compress — in volatile moves, they expand. This makes the indicator self-adaptive.

Mean reversion trades:

A move into R4/R5 or S4/S5 without continuation can be a sign of exhaustion — potential for reversal toward the pivot.

Alerting:

Built-in alerts are available for crosses of all major bands (R1–R5, S1–S5), enabling trade automation or scalp alerts with ease.

-- Visual Features --

Fuchsia Lines: Mark all Resistance (R1–R5) levels.

Lime Lines: Mark all Support (S1–S5) levels.

Gray Circle Line: Marks the rolling pivot (VWAP-based).

-- Customizable Settings --

Rolling Length: Number of bars used to calculate VWAP and VW Range.

Multiplier: Controls how wide the bands are spaced.

Smooth Pivot: Toggle on/off to smooth the central pivot.

Pivot Smoothing Length: Controls how many bars to average when smoothing is enabled.

Offset: Visually shift all bands forward/backward in time.

-- Why Use This Over Standard Pivots? --

Traditional pivots are based on previous session data and remain fixed. That’s useful for static setups, but may become irrelevant as price action evolves. In contrast:

This system updates every bar, adjusting to current price behavior.

It includes volume — a key feature missing from most static pivots.

It shows multiple bands, giving a full view of compression, breakout potential, or trend exhaustion.

-- Who Is This For? --

This tool is ideal for:

Day traders & scalpers who need relevant intraday levels.

Swing traders looking for evolving areas of confluence.

Algorithmic/systematic traders who rely on quantifiable, volume-aware support/resistance.

Traders on all assets: works on crypto, stocks, futures, forex — any chart that has volume.

[blackcat] L3 Trendmaster XOVERVIEW

The L3 Trendmaster X is an advanced trend-following indicator meticulously crafted to assist traders in identifying and capitalizing on market trends. This sophisticated tool integrates multiple technical factors, including Average True Range (ATR), volume dynamics, and price spreads, to deliver precise buy and sell signals. By plotting dynamic trend bands directly onto the chart, it offers a comprehensive visualization of potential trend directions, enabling traders to make informed decisions swiftly and confidently 📊↗️.

FEATURES

Customizable Input Parameters: Tailor the indicator to match your specific trading needs with adjustable settings:

Trendmaster X Multiplier: Controls the sensitivity of the ATR-based levels.

Trendmaster X Period: Defines the period over which the ATR is calculated.

Window Length: Specifies the length of the moving window for standard deviation calculations.

Volume Averaging Length: Determines how many periods are considered for averaging volume.

Volatility Factor: Adjusts the impact of volatility on the trend bands.

Core Technical Metrics:

Dynamic Range: Measures the range between high and low prices within each bar.

Candle Body Size: Evaluates the difference between open and close prices.

Volume Average: Assesses the cumulative On-Balance Volume relative to the dynamic range.

Price Spread: Computes the standard deviation of the price ranges over a specified window.

Volatility Factor: Incorporates volatility into the calculation of trend bands.

Advanced Trend Bands Calculation:

Upper Level: Represents potential resistance levels derived from the ATR multiplier.

Lower Level: Indicates possible support levels using the same ATR multiplier.

High Band and Low Band: Dynamically adjust to reflect current trend directions, offering a clear view of market sentiment.

Visual Representation:

Plots distinct green and red trend lines representing bullish and bearish trends respectively.

Fills the area between these trend lines and the middle line for enhanced visibility.

Displays clear buy ('B') and sell ('S') labels on the chart for immediate recognition of trading opportunities 🏷️.

Alert System:

Generates real-time alerts when buy or sell conditions are triggered, ensuring timely action.

Allows customization of alert messages and frequencies to align with individual trading strategies 🔔.

HOW TO USE

Adding the Indicator:

Open your TradingView platform and navigate to the "Indicators" section.

Search for " L3 Trendmaster X" and add it to your chart.

Adjusting Settings:

Fine-tune the input parameters according to your preferences and trading style.

For example, increase the Trendmaster X Multiplier for higher sensitivity during volatile markets.

Decrease the Window Length for shorter-term trend analysis.

Monitoring Trends:

Observe the plotted trend bands and labels on the chart.

Look for buy ('B') labels at potential support levels and sell ('S') labels at resistance levels.

Setting Up Alerts:

Configure alerts based on the generated buy and sell signals.

Choose notification methods (e.g., email, SMS) and set alert frequencies to stay updated without constant monitoring 📲.

Combining with Other Tools:

Integrate the Trendmaster X with other technical indicators like Moving Averages or RSI for confirmation.

Utilize fundamental analysis alongside the indicator for a holistic approach to trading.

Backtesting and Optimization:

Conduct thorough backtests on historical data to evaluate performance.

Optimize parameters based on backtest results to enhance accuracy and reliability.

Real-Time Application:

Apply the optimized settings to live charts and monitor real-time signals.

Execute trades based on confirmed signals while considering risk management principles.

LIMITATIONS

Market Conditions: The indicator might produce false signals in highly volatile or sideways-trending markets due to increased noise and lack of clear direction 🌪️.

Complementary Analysis: Traders should use this indicator in conjunction with other analytical tools to validate signals and reduce the likelihood of false positives.

Asset-Specific Performance: Effectiveness can vary across different assets and timeframes; therefore, testing on diverse instruments is recommended.

NOTES

Data Requirements: Ensure adequate historical data availability for accurate calculations and reliable signal generation.

Demo Testing: Thoroughly test the indicator on demo accounts before deploying it in live trading environments to understand its behavior under various market scenarios.

Parameter Customization: Regularly review and adjust parameters based on evolving market conditions and personal trading objectives.

SYMPL Reversal BandsThis is an expansion of the Hybrid moving average. It uses the same hybrid moving code from the hybrid moving average script with an additional layer using the ta.hma function for some slight additional smoothing. Colors of the bands change dynamically based of the long and short hybrid moving averages running in the background. This can be really helpful in identifying periods to short bounces or long dips.

Below is the explanation of the hybrid moving average

Hybrid Moving Average Market Trend System - , designed to visualize market trends using a combination of three moving averages: FRAMA (Fractal Adaptive Moving Average), VIDYA (Variable Index Dynamic Average), and a Hamming windowed Volume-Weighted Moving Average (VWMA).

Key Features:

FRAMA Calculation:

FRAMA adapts to market volatility by dynamically adjusting its smoothing factor based on the fractal dimension of price movement. This allows it to be more responsive during trending periods while filtering out noise in sideways markets. The FRAMA is calculated for both short and long periods

VIDYA with CMO:

The VIDYA (Variable Index Dynamic Average) is based on a Chande Momentum Oscillator (CMO), which adjusts the smoothing factor dynamically depending on the momentum of the market. Higher momentum periods result in more responsive averages, while low momentum periods lead to smoother averages. Like FRAMA, VIDYA is calculated for both short and long periods.

Hamming Windowed VWMA:

This VWMA variation applies a Hamming window to smooth the weighting of volume across the calculation period. This method emphasizes central data points and reduces noise, making the VWMA more adaptive to volume fluctuations. The Hamming VWMA is calculated for short and long periods, offering another layer of adaptability to the hybrid moving average.

Hybrid Moving Averages:

Dynamic Coloring and Filling:

The script uses dynamic color transitions to visually distinguish between bullish and bearish conditions:

Hybrid Moving Average - Market TrendHybrid Moving Average Market Trend System - , designed to visualize market trends using a combination of three moving averages: FRAMA (Fractal Adaptive Moving Average), VIDYA (Variable Index Dynamic Average), and a Hamming windowed Volume-Weighted Moving Average (VWMA).

Key Features:

FRAMA Calculation:

FRAMA adapts to market volatility by dynamically adjusting its smoothing factor based on the fractal dimension of price movement. This allows it to be more responsive during trending periods while filtering out noise in sideways markets. The FRAMA is calculated for both short and long periods

VIDYA with CMO:

The VIDYA (Variable Index Dynamic Average) is based on a Chande Momentum Oscillator (CMO), which adjusts the smoothing factor dynamically depending on the momentum of the market. Higher momentum periods result in more responsive averages, while low momentum periods lead to smoother averages. Like FRAMA, VIDYA is calculated for both short and long periods.

Hamming Windowed VWMA:

This VWMA variation applies a Hamming window to smooth the weighting of volume across the calculation period. This method emphasizes central data points and reduces noise, making the VWMA more adaptive to volume fluctuations. The Hamming VWMA is calculated for short and long periods, offering another layer of adaptability to the hybrid moving average.

Hybrid Moving Averages:

Dynamic Coloring and Filling:

The script uses dynamic color transitions to visually distinguish between bullish and bearish conditions:

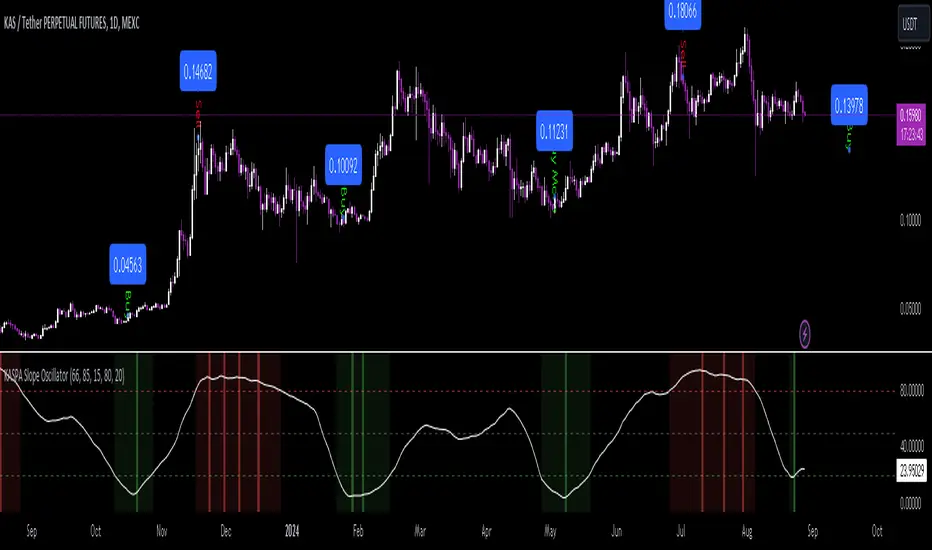

KASPA Slope OscillatorKASPA Slope Oscillator for analyzing KASPA on the 1D (daily) chart.

The indicator is plotted in a separate pane below the price chart and uses a mathematical approach to calculate and visualize the momentum or "slope" of KASPA's price movements.

Input Parameters:

Slope Window (days):

Defines the period (66 days by default) over which the slope is calculated.

Normalization Window (days):

The window size (85 days) for normalizing the slope values between 0 and 100.

Smoothing Period:

The number of days (15 days) over which the slope values are smoothed to reduce noise.

Overbought and Oversold Levels:

Threshold levels set at 80 (overbought) and 20 (oversold), respectively.

Calculation of the Slope:

Logarithmic Price Calculation:

Converts the close price of KASPA into a logarithmic scale to account for exponential growth or decay.

Rolling Slope:

Computes the rate of change in logarithmic prices over the defined slope window.

Normalization:

The slope is normalized between 0 and 100, allowing easier identification of extreme values.

Smoothing and Visualization:

Smoothing the Slope:

A Simple Moving Average (SMA) is applied to the normalized slope for the specified smoothing period.

Plotting the Oscillator:

The smoothed slope is plotted on the oscillator chart. Horizontal lines indicate overbought (80), oversold (20), and the mid-level (50).

Background Color Indications:

Background colors (red or green) indicate when the slope crosses above the overbought or below the oversold levels, respectively, signaling potential buy or sell conditions.

Detection of Local Maxima and Minima:

The code identifies local peaks (maxima) above the overbought level and troughs (minima) below the oversold level.

Vertical background lines are highlighted in red or green at these points, signaling potential reversals.

Short Summary:

The oscillator line fluctuates between 0 and 100, representing the normalized momentum of the price.

Red background areas indicate periods when the oscillator is above the overbought level (80), suggesting a potential overbought condition or a sell signal.

Green background areas indicate periods when the oscillator is below the oversold level (20), suggesting a potential oversold condition or a buy signal.

The vertical lines on the background mark local maxima and minima where price reversals may occur.

(I also want to thank @ForgoWork for optimizing visuality and cleaning up the source code)

Option Pair ZigzagOptions Pair Zigzag:

Though we can split the chart window and view multiple charts, this indicator is useful when we view options charts.

How this indicator works:

The indicator works in non-overlay mode.

The indicator will find other option pair symbol and load it’s chart in indicator window. It will also draw a zigzag on both the charts. It will also fetch the SPOT symbol and display SPOT Close price of latest candle.

Useful information:

A. Support resistance: Higher High (HH) and Lower Low (LL) markings can be treated as strong support and or resistance and LH, HL markings can be treated as weak support and or resistance.

B. Trend identification: Easy identification of trend based on trend lines and trend markings i.e. Higher High (HH), Lower Low (LL), Lower High (LH), Higher Low (HL)

C. Use of Rate of change (ROC )– Labels drawn on swing points are equipped with ROC% between swing points. ROC% between Call and Put option charts can be compared and used to identify strong and weak moves.

Example:

1. User loads a call option chart of ‘NIFTY240620C23500’ (NIFTY 50 INDEX OPTIONS 20 JUN 2024 CALL 23500)

2. Since user has selected CALL Option, Indicator rules/logic will find PUT Option symbol of same strike and expiry

3. PUT Option chart would then shown in the indicator window

4. Draw zigzag on both the charts

5. Plot labels on both the charts

6. Labels are equipped with a tooltip showing rate of change between 2 pivot points

Input Parameters:

Left bars – Parameter required for plotting zigzag

Right bars – Parameter required for plotting zigzag

Plot HHLL Labels – Enable/disable plotting of labels

Use cases:

Refer to chart snapshots:

1. Buy Call Option or Sell Put Option - How one can trade on formation of a consolidation range

2. Breakdown of Swing structure - One can observe Swing structure (Zigzag) formed on a SPOT chart and trade on break of swing structure

3. Triangle formation - Observe the patterns formed on the SPOT chart and trade either Call or Put options. Example snapshot shows trade based on triangle pattern

Chart Snapshot:

One can split chart window and load base symbol chart which will help to review bases symbol and options chart at the same time.

Buy Call Option or Sell Put Option

Breakdown of Swing structure

Triangle formation

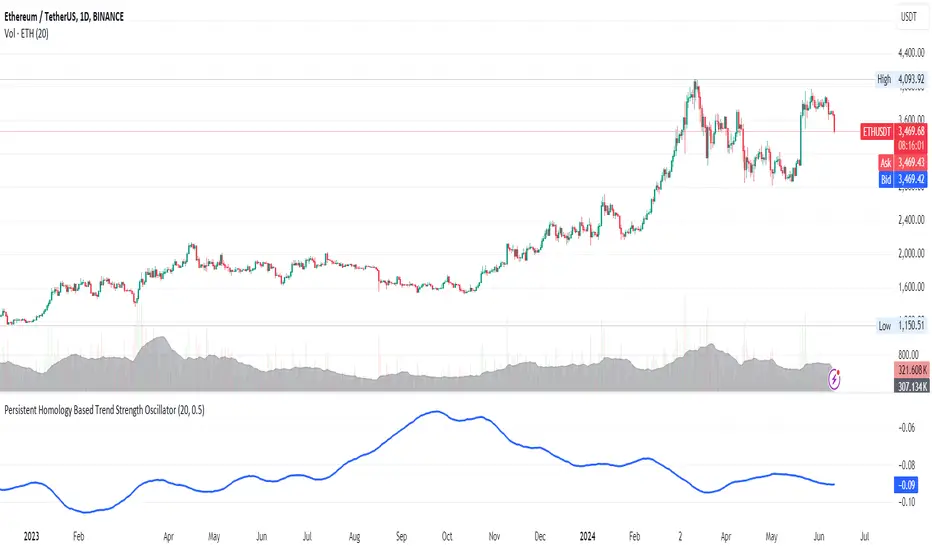

Persistent Homology Based Trend Strength OscillatorPersistent Homology Based Trend Strength Oscillator

The Persistent Homology Based Trend Strength Oscillator is a unique and powerful tool designed to measure the persistence of market trends over a specified rolling window. By applying the principles of persistent homology, this indicator provides traders with valuable insights into the strength and stability of uptrends and downtrends, helping to inform better trading decisions.

What Makes This Indicator Original?

This indicator's originality lies in its application of persistent homology , a method from topological data analysis, to financial markets. Persistent homology examines the shape and features of data across multiple scales, identifying patterns that persist as the scale changes. By adapting this concept, the oscillator tracks the persistence of uptrends and downtrends in price data, offering a novel approach to trend analysis.

Concepts Underlying the Calculations:

Persistent Homology: This method identifies features such as clusters, holes, and voids that persist as the scale changes. In the context of this indicator, it tracks the duration and stability of price trends.

Rolling Window Analysis: The oscillator uses a specified window size to calculate the average length of uptrends and downtrends, providing a dynamic view of trend persistence over time.

Threshold-Based Trend Identification: It differentiates between uptrends and downtrends based on specified thresholds for price changes, ensuring precision in trend detection.

How It Works:

The oscillator monitors consecutive changes in closing prices to identify uptrends and downtrends.

An uptrend is detected when the closing price increase exceeds a specified positive threshold.

A downtrend is detected when the closing price decrease exceeds a specified negative threshold.

The lengths of these trends are recorded and averaged over the chosen window size.

The Trend Persistence Index is calculated as the difference between the average uptrend length and the average downtrend length, providing a measure of trend persistence.

How Traders Can Use It:

Identify Trend Strength: The Trend Persistence Index offers a clear measure of the strength and stability of uptrends and downtrends. A higher value indicates stronger and more persistent uptrends, while a lower value suggests stronger and more persistent downtrends.

Spot Trend Reversals: Significant shifts in the Trend Persistence Index can signal potential trend reversals. For instance, a transition from positive to negative values might indicate a shift from an uptrend to a downtrend.

Confirm Trends: Use the Trend Persistence Index alongside other technical indicators to confirm the strength and duration of trends, enhancing the accuracy of your trading signals.

Manage Risk: Understanding trend persistence can help traders manage risk by identifying periods of high trend stability versus periods of potential volatility. This can be crucial for timing entries and exits.

Example Usage:

Default Settings: Start with the default settings to get a feel for the oscillator’s behavior. Observe how the Trend Persistence Index reacts to different market conditions.

Adjust Thresholds: Fine-tune the positive and negative thresholds based on the asset's volatility to improve trend detection accuracy.

Combine with Other Indicators: Use the Persistent Homology Based Trend Strength Oscillator in conjunction with other technical indicators such as moving averages, RSI, or MACD for a comprehensive analysis.

Backtesting: Conduct backtesting to see how the oscillator would have performed in past market conditions, helping you to refine your trading strategy.

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)

Volume Zone Oscillator with EMA smoothing

Parameters:

src (float) : Source series

len (simple int) : Length parameter for EMA

Returns: VZO value

vzo_sma(src, len)

Volume Zone Oscillator with SMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for SMA

Returns: VZO value

vzo_wma(src, len)

Volume Zone Oscillator with WMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for WMA

Returns: VZO value

alma2(series, windowsize, offset, sigma)

Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float) : Input series

windowsize (int) : Size of the moving average window

offset (float) : Offset parameter

sigma (float) : Sigma parameter

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Aproxiates srt using Discrete wavelet transform.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

Wavelet_std(src, len, offset, mag)

Aproxiates srt using Discrete wavelet transform with standard deviation as a magnitude.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (float) : Offset parameter for ALMA

mag (int) : Magnitude parameter for standard deviation

Returns: Wavelet-transformed series

LaplaceTransform(xval, N, a)

Original Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

Returns: Aproxiated source value

NLaplaceTransform(xval, N, a, repeat)

Y repetirions on Original Laplace Transform over N set of close prices, each time N-k set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformsum(xval, N, a, b)

Sum of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiff(xval, N, a, b, repeat)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiff(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, with dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiff(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor, dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiffFrom2(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

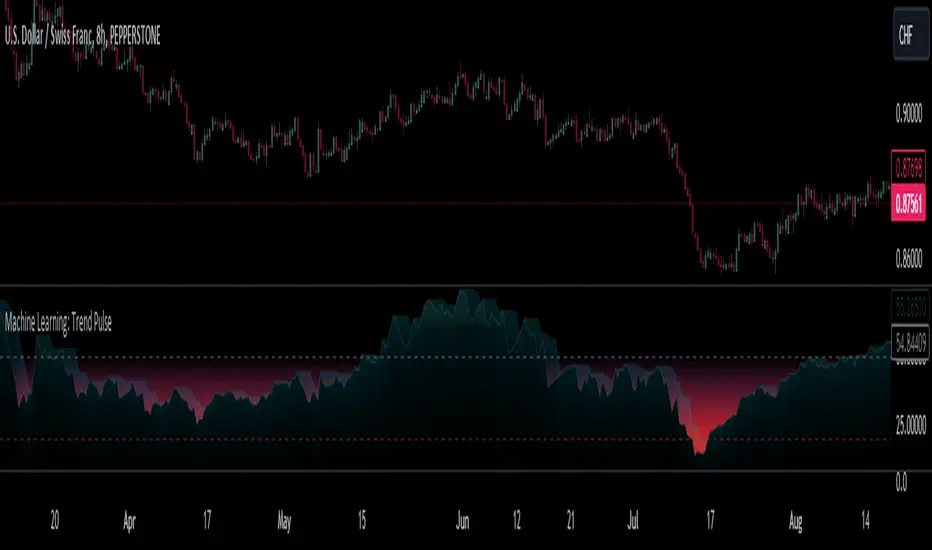

Machine Learning: Trend Pulse⚠️❗ Important Limitations: Due to the way this script is designed, it operates specifically under certain conditions:

Stocks & Forex : Only compatible with timeframes of 8 hours and above ⏰

Crypto : Only works with timeframes starting from 4 hours and higher ⏰

❗Please note that the script will not work on lower timeframes.❗

Feature Extraction : It begins by identifying a window of past price changes. Think of this as capturing the "mood" of the market over a certain period.

Distance Calculation : For each historical data point, it computes a distance to the current window. This distance measures how similar past and present market conditions are. The smaller the distance, the more similar they are.

Neighbor Selection : From these, it selects 'k' closest neighbors. The variable 'k' is a user-defined parameter indicating how many of the closest historical points to consider.

Price Estimation : It then takes the average price of these 'k' neighbors to generate a forecast for the next stock price.

Z-Score Scaling: Lastly, this forecast is normalized using the Z-score to make it more robust and comparable over time.

Inputs:

histCap (Historical Cap) : histCap limits the number of past bars the script will consider. Think of it as setting the "memory" of model—how far back in time it should look.

sampleSpeed (Sampling Rate) : sampleSpeed is like a time-saving shortcut, allowing the script to skip bars and only sample data points at certain intervals. This makes the process faster but could potentially miss some nuances in the data.

winSpan (Window Size) : This is the size of the "snapshot" of market data the script will look at each time. The window size sets how many bars the algorithm will include when it's measuring how "similar" the current market conditions are to past conditions.

All these variables help to simplify and streamline the k-NN model, making it workable within limitations. You could see them as tuning knobs, letting you balance between computational efficiency and predictive accuracy.

Relative slopeRelative slope metric

Description:

I was in need to create a simple, naive and elegant metric that was able to tell how strong is the trend in a given rolling window. While abstaining from using more complicated and arguably more precise approaches, I’ve decided to use Linearly Weighted Linear Regression slope for this goal. Outright values are useful, but the problem was that I wasn’t able to use it in comparative analysis, i.e between different assets & different resolutions & different window sizes, because obviously the outputs are scale-variant.

Here is the asset-agnostic, resolution-agnostic and window size agnostic version of the metric.

I made it asset agnostic & resolution agnostic by including spread information to the formula. In our case it's weighted stdev over differenced data (otherwise we contaminate the spread with the trend info). And I made it window size agnostic by adding a non-linear relation of length to the output, so finally it will be aprox in (-1, 1) interval, by taking square root of length, nothing fancy. All these / 2 and * 2 in unexpected places all around the formula help us to return the data to it’s natural scale while keeping the transformations in place.

Peace TV

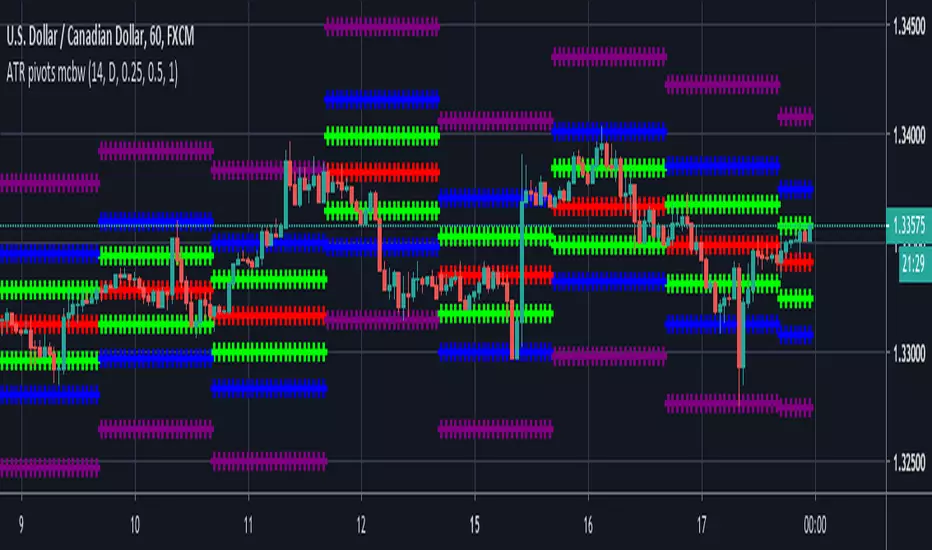

ATR based Pivots mcbwHey everyone this is an exciting new script I have prepared for you.

I was reading an old forex bulletin article some time ago when I came across this: solar.murty.net (or you can download the full bulletin with lots of other good articles here: www.forexfactory.com).

You can already buy this for metatrader (www.mql5.com) so I figured to make it for free for tradingview.

This bulletin suggested that you can reasonably predict daily volatility by adding or subtracting multiples of the daily ATR to the daily opening. Using this you can choose multiples to use as price targets and alternatively as stop losses. For example, if you already have a sense of market direction you can buy at market open place a stop loss at - 1 daily ATR and a profit target at + 3 ATRs for a risk to reward ratio of 3. If you are looking for smaller/quicker moves with a ratio of 3 you can have a stop loss at -0.25 ATR and a take profit at +0.75 ATR.

Alternatively this article also suggests to use this method to catch volatility breakouts. If price is higher than the + 1 ATR area then you can safely assume it will be going to the +2 ATR area so you can put a buy stop at + 1 ATR with a profit target at + 2 ATR with a stop loss at +0.5 ATR to catch a volatility breakout with a risk to reward ratio of 2!

Even further there are methods that you can use with ATRs of multiple window sizes, for example by opening two copies of this indicator and measuring recent volatility with a 1 week window and long term volatility within a 1 month window. If the short term volatility is crossing the long term volatility then there is a high probability chance that even more price movement will occur.

However I have found that this method is good for more than daily volatility , it can also be used to measure weekly volatility , and monthly volatility and use these multiples as good long term price targets.