3Commas Bollinger StrategyThis strategy is intended for use as a way of backtesting various parameters available on 3commas.io composite bot using a bollinger band type trading strategy. While it's primary intention is to provide users a way of backtesting bot parameters, it can also be used to trigger a deal start by either using the {{strategy.open.alert_message}} field in your alert and providing the bot details in the configuration screen for the strategy or by including the usual deal start message provided by 3commas. You can find more information about how to do this from help.3commas.io

The primary inputs for the strategy are:

// USER INPUTS

Short MA Window - The length of the Short moving average

Long MA Window - The length of the Long moving average

Upper Band Offset - The offset to use for the upper bollinger offset

Lower Band Offset - The offset to use for the lower bollinger offset

Long Stop Loss % - The stop loss percentage to test

Long Take Profit % - The Take profit percentage to test

Initial SO Deviation % - The price deviation percentage required to place to first safety order

Safety Order Vol Step % - The volume scale to test

3Commas Bot ID - (self explanatory)

Bot Email Token - Found in the deal start message for your bot (see link in previous section for details)

3Commas Bot Trading Pair - The pair to include for composite bot start deals (should match format of 3commas, not TradingView IE. USDT_BTC not BTCUSDT)

Start Date, Month, Year and End Date, Month and Year all apply to the backtesting window. By default it will use as much data as it can given the current period select (there is less historical data available for periods below 1H) back as far as 2016 (there appears to be no historical data on Trading view much before this). If you would like to test a different period of time, just change these values accordingly.

Known Issues

Currently there are a couple of issues with this strategy that you should be aware of. I may fix them at some point in the future but they don't really bug me so this is more for informational purposes than a promise that they may one day be fixed.

Does not test trailing take profit

Number of safety orders and Safety Order Step Scale are currently not user configurable (must edit source code)

Using the user configuration to generate deal start message assumes you are triggering a composite bot, not a simple bot.

Cerca negli script per "如何用wind搜索股票的发行价和份数"

Gann Fan Analysis v 3.0The openness of this community is amazing and I have gained a lot from being a member. Hopefully you think this is useful so I can give something back.

This indicator constructs a reference framework of Support and Resistance levels based on Gann Fan ratios. Two fans are created: Support or Bullish fan, and a Resistance or Bearish fan. The origin of the analysis is the lowest pivot in the analysis window set by the length input. The upper bound of the analysis is the highest pivot in the analysis window. This is the only user input that affects the fan calculation. The remaining user input controls the visualization of the fans. The fan calculations are updated as the high and low within the analysis window change. The resistance fan range is based on an assumed 70% retracement.

Indicator also highlights the active Support and Resistance lines of each fan. An alert is also included, based on the price crossing one of these active levels.

Currently I can't figure out how to get the analysis to extend beyond 278 or so bars (not sure what the limitation is) so it isn't really useful for intraday timeframes, but it is reliable on daily and above. I use it on a Weekly view with the analysis length set to 52, and on a daily timeframe with the length set to 260.

I included fractal visualization using Ricardo Santos' Fractals v9 script as a means of confirming the Gann Fan pivots. The two methods seems to correlate well, in my opinion.

The coding is terrible, I'm sure, so please overlook that as this my first complex effort. I'm a total amateur!

Matrix Library (Linear Algebra, incl Multiple Linear Regression)What's this all about?

Ever since 1D arrays were added to Pine Script, many wonderful new opportunities have opened up. There has been a few implementations of matrices and matrix math (most notably by TradingView-user tbiktag in his recent Moving Regression script: ). However, so far, no comprehensive libraries for matrix math and linear algebra has been developed. This script aims to change that.

I'm not math expert, but I like learning new things, so I took it upon myself to relearn linear algebra these past few months, and create a matrix math library for Pine Script. The goal with the library was to make a comprehensive collection of functions that can be used to perform as many of the standard operations on matrices as possible, and to implement functions to solve systems of linear equations. The library implements matrices using arrays, and many standard functions to manipulate these matrices have been added as well.

The main purpose of the library is to give users the ability to solve systems of linear equations (useful for Multiple Linear Regression with K number of independent variables for example), but it can also be used to simulate 2D arrays for any purpose.

So how do I use this thing?

Personally, what I do with my private Pine Script libraries is I keep them stored as text-files in a Libraries folder, and I copy and paste them into my code when I need them. This library is quite large, so I have made sure to use brackets in comments to easily hide any part of the code. This helps with big libraries like this one.

The parts of this script that you need to copy are labeled "MathLib", "ArrayLib", and "MatrixLib". The matrix library is dependent on the functions from these other two libraries, but they are stripped down to only include the functions used by the MatrixLib library.

When you have the code in your script (pasted somewhere below the "study()" call), you can create a matrix by calling one of the constructor functions. All functions in this library start with "matrix_", and all constructors start with either "create" or "copy". I suggest you read through the code though. The functions have very descriptive names, and a short description of what each function does is included in a header comment directly above it. The functions generally come in the following order:

Constructors: These are used to create matrices (empy with no rows or columns, set shape filled with 0s, from a time series or an array, and so on).

Getters and setters: These are used to get data from a matrix (like the value of an element or a full row or column).

Matrix manipulations: These functions manipulate the matrix in some way (for example, functions to append columns or rows to a matrix).

Matrix operations: These are the matrix operations. They include things like basic math operations for two indices, to transposing a matrix.

Decompositions and solvers: Next up are functions to solve systems of linear equations. These include LU and QR decomposition and solvers, and functions for calculating the pseudo-inverse or inverse of a matrix.

Multiple Linear Regression: Lastly, we find an implementation of a multiple linear regression, including all the standard statistics one can expect to find in most statistical software packages.

Are there any working examples of how to use the library?

Yes, at the very end of the script, there is an example that plots the predictions from a multiple linear regression with two independent (explanatory) X variables, regressing the chart data (the Y variable) on these X variables. You can look at this code to see a real-world example of how to use the code in this library.

Are there any limitations?

There are no hard limiations, but the matrices uses arrays, so the number of elements can never exceed the number of elements supported by Pine Script (minus 2, since two elements are used internally by the library to store row and column count). Some of the operations do use a lot of resources though, and as a result, some things can not be done without timing out. This can vary from time to time as well, as this is primarily dependent on the available resources from the Pine Script servers. For instance, the multiple linear regression cannot be used with a lookback window above 10 or 12 most of the time, if the statistics are reported. If no statistics are reported (and therefore not calculated), the lookback window can usually be extended to around 60-80 bars before the servers time out the execution.

Hopefully the dev-team at TradingView sees this script and find ways to implement this functionality diretly into Pine Script, as that would speed up many of the operations and make things like MLR (multiple linear regression) possible on a bigger lookback window.

Some parting words

This library has taken a few months to write, and I have taken all the steps I can think of to test it for bugs. Some may have slipped through anyway, so please let me know if you find any, and I'll try my best to fix them when I have time to do so. This library is intended to help the community. Therefore, I am releasing the library as open source, in the hopes that people may improving on it, or using it in their own work. If you do make something cool with this, or if you find ways to improve the code, please let me know in the comments.

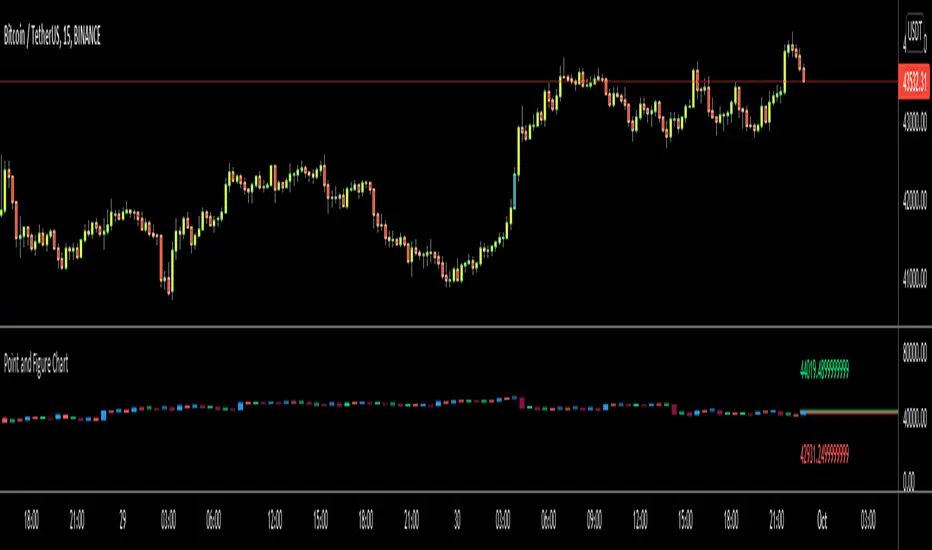

Point and Figure Chart - LiveHello Traders,

This is "Point and Figure Chart (PnF)" script that run in separated window in real time. The separated PnF chart window is timeless, so no relation with the time on the chart. PnF chart consist of "X" and "O" columns. While "X" columns represents rising prices, "O" column represents a falling price. If you have no idea about what PnF charting is then you should search for "Point and Figure Charting" on the net and get some info before using this script.

Now lets talk about details. PnF Chart requires at least two variables to be set => Box size and Reversal. Box size represents the size of each X/O in PnF chart and the reversal is used to calculate new X/O or reversal. for example if currrent column is X column then for new "X", "box size * 1" move is needed and for new "O" column or reversal, "box size * revelsal" move is needed. in the script I use lines as X/O columns.

In the options you can set "Box Size Assingment Method". you have 3 options Traditional, ATR, Percentage . what are they?

Traditional: user-defined box size, means you can set the box size as you wish, using the option . if you use this option then you should set it accordingly.

ATR : that's dynamic box size scaling and on each columns it's calculated once, you can set length for ATR

Percentage: that's also dynamic box size scaling according to closing price when new column appeared. if you use this option then you should set it accordingly.

Reversal: The reversal is typically 3 but you can change it as you wish

"Change Bar Color by PnF Trend": if you enable this option then bar color changes by PnF columns, by default it's not enabled

"Change Column Color When Breakout Occurs": PnF color changes if Double Top/Bottom breakout accours. enabled by default and you can set the colors as you wish using the options

"Change Bar Color When Breakout Occurs": bar colors changed if Double Top/Bottom breakout accours. enabled by default and you can set the colors as you wish using the options

the script checks only Double Top/Bottom breakouts at the moment. there are many other breakouts such Triple/Quadruple, Ascending/Descending Triple Top/Bottom breakouts, Catapult etc.

Also the script shows new X/O level and reversal Levels in PnF window. An example:

If you enable "Change Bar Color by PnF Trend" option:

An example if you disable the option "Change Column Color When Breakout Occurs

You may want to see my another/older "Point and Point Chart" script as well. you can find it in my profile/published scripts and in the Public Library. I use same PnF calculation algorithm in both scripts.

Enjoy!

Smooth First Derivative IndicatorIntroducing the Smooth First Derivative indicator. For each time step, the script numerically differentiates the price data using prior datapoints from the look-back window. The resulting time derivative (the rate of price change over time) is presented as a centered oscillator.

A first derivative is a versatile tool used in functional data analysis. When applied to price data, it can be applied to analyze momentum, confirm trend direction, and identify pivot points.

Model Description:

The model assumes that, within the look-back window, price data can be well approximated by a smooth differentiable function. The first derivative can then be computed numerically using a noise-robust one-sided differentiator. The current version of the script employs smooth differentiators developed by P. Holoborodko (www.holoborodko.com). Note that the Indicator should not be confused with Constance Brown's Derivative Oscillator.

Input parameter:

The Bandwidth parameter sets the number of points in the moving look-back window and thus determines the smoothness of the first derivative curve. Note that a smoother Indicator shows a greater lag.

Interpretation:

When using this Indicator, one should recall that the first derivative can simply be interpreted as the slope of the curve:

- The maximum (minimum) in the Indicator corresponds to the point at which the market experiences the maximum upward (downward) slope, i.e., the inflection point. The steeper the slope, the greater the Indicator value.

- The positive-to-negative zero-crossing in the Indicator suggests that the market has formed a local maximum (potential start of a downtrend or a period of consolidation). Likewise, a zero-crossing from negative to positive is a potential bullish signal.

[R&D] Moving CentroidThis script utilizes this concept. Instead of weighting by volume, it weights by amount of price action on every close price of the rolling window. I assume it can be used as an additional reference point for price mode and price antimode.

it is directly connected with Market (not volume) profile, or TPO charts.

The algorithm:

1) takes a rolling window of, for example, 50 data points of close prices:

2) for each of this closing prices, the algorithm will check how many bars touched this close price.

3) then: sum of datapoints * weights/sum of weights

Since the logic is implemented in pretty non-efficient way, the script sometimes can take time to make calculations. Moreover, it calculates the centroid taking into account only close prices, not every tick. of a given rolling window That's why it's still experimental.

5min ORB - HenryJ5min ORB, for ICT trading

Strategy Implementation: The main goal is to identify and visually mark the trading range established during the first 5 minutes of the regular trading session.

Time Definition: It measures the Highest High and Lowest Low recorded from the session open (minute 0) up to the close of the 5th minute.

Visual Marking: It draws two distinct horizontal line segments on the chart:

One line marks the High of the 5-minute Opening Range.

One line marks the Low of the 5-minute Opening Range.

Drawing Window: The lines are intentionally drawn starting from the 6th minute (after the range is fully established) and extend up to the 60th minute of the trading session. This ensures the lines are available to guide trades for the first hour after the opening volatility subsides.

Labeling: It includes a "5min ORB" text label placed near the high line, clearly identifying the range.

BY Henry J

CANDLE_TIME_RDThis tool displays the time of each candle directly on the chart by placing a label below

the bar with an upward-pointing arrow for clear visual alignment. It helps traders quickly

identify the exact timestamp of any candle during fast intraday analysis or historical review.

OVERVIEW

The script extracts the hour and minute of each bar, formats the timestamp according to the

user’s preference, and prints it beneath the candle. This removes the need to rely on the

data window or crosshair for time inspection. It is ideal for ITI evaluation, timestamp

journaling, and precise replay study.

FEATURES

- Prints the time under each candle or every N-th candle using a simple step input.

- Supports both AM/PM and military time through a toggle input.

- Builds all hour and minute text manually to ensure consistent formatting.

- Uses label.style_label_up to draw an arrow pointing toward the candle.

- Positions labels with yloc.belowbar so they do not overlap price bars.

USE CASES

- Reviewing setups with ChatGPT where exact candle timing matters.

- Studying EMA touches, VWAP interactions, or momentum shifts that occur at specific times.

- Journaling entries and exits with precise timestamps.

- Quickly identifying candle times without zooming or opening data windows.

This script is designed for clarity and convenience, improving workflow for structured

intraday traders and replay analysts.

Ultimate Multi-Asset Correlation System by able eiei Ultimate Multi-Asset Correlation System - User Guide

Overview

This advanced TradingView indicator combines WaveTrend oscillator analysis with comprehensive multi-asset correlation tracking. It helps traders understand market relationships, identify regime changes, and spot high-probability trading opportunities across different asset classes.

Key Features

1. WaveTrend Oscillator

Main Signal Lines: WT1 (blue) and WT2 (red) plot momentum and its moving average

Overbought/Oversold Zones: Default levels at +60/-60

Cross Signals:

🟢 Bullish: WT1 crosses above WT2 in oversold territory

🔴 Bearish: WT1 crosses below WT2 in overbought territory

Higher Timeframe (HTF) Analysis: Shows WT1 from 4H, Daily, and Weekly timeframes for trend confirmation

2. Multi-Asset Correlation Tracking

Monitors relationships between:

Major Assets: Gold (XAUUSD), Dollar Index (DXY), US 10-Year Yield, S&P 500

Crypto Assets: Bitcoin, Ethereum, Solana, BNB

Cross-Asset Analysis: Correlation between traditional markets and crypto

3. Market Regime Detection

Automatically identifies market conditions:

Risk-On: High correlation + positive sentiment (🟢 Green background)

Risk-Off: High correlation + negative sentiment (🔴 Red background)

Crypto-Risk-On: Strong crypto correlations (🟠 Orange background)

Low-Correlation: Divergent market behavior (⚪ Gray background)

Neutral: Mixed signals (🟡 Yellow background)

How to Use

Basic Setup

Add to Chart: Apply the indicator to any chart (works on all timeframes)

Choose Display Mode (Display Options):

All: Shows everything (recommended for comprehensive analysis)

WaveTrend Only: Focus on momentum signals

Correlation Only: View market relationships

Heatmap Only: Simplified correlation view

Enable Asset Groups:

✅ Major Assets: Traditional markets (stocks, bonds, commodities)

✅ Crypto Assets: Digital currencies

Mix and match based on your trading focus

Reading the Charts

WaveTrend Section (Bottom Panel)

Above 0 = Bullish momentum

Below 0 = Bearish momentum

Above +60 = Overbought (potential reversal)

Below -60 = Oversold (potential bounce)

Lighter lines = Higher timeframe trends

Correlation Histogram (Colored Bars)

Blue bars: Major asset correlations

Orange bars: Crypto correlations

Purple bars: Cross-asset correlations

Bar height: Correlation strength (-50 to +50 scale)

Background Color

Intensity reflects correlation strength

Color shows market regime

Dashboard Elements

🎯 Market Regime Analysis (Top Left)

Current Regime: Overall market condition

Average Correlation: Strength of relationships (0-1 scale)

Risk Sentiment: -100% (risk-off) to +100% (risk-on)

HTF Alignment: Multi-timeframe trend agreement

Signal Quality: Confidence level for current signals

📊 Correlation Matrix (Top Right)

Shows correlation values between asset pairs:

1.00: Perfect positive correlation

0.75+: Strong correlation (🟢 Green)

0.50+: Medium correlation (🟡 Yellow)

0.25+: Weak correlation (🟠 Orange)

Below 0.25: Negative/no correlation (🔴 Red)

🔥 Correlation Heatmap (Bottom Right)

Visual matrix showing:

Gold vs. DXY, BTC, ETH

DXY vs. BTC, ETH

BTC vs. ETH

Color-coded strength

📈 Performance Tracker (Bottom Left)

Tracks individual asset momentum:

WT1 Values: Current momentum reading

Status: OB (overbought) / OS (oversold) / Normal

Trading Strategies

1. High-Probability Trend Following

✅ Entry Conditions:

WaveTrend bullish/bearish cross

HTF Alignment matches signal direction

Signal Quality > 70%

Correlation supports direction

2. Regime Change Trading

🎯 Watch for regime shifts:

Risk-Off → Risk-On = Consider long positions

High correlation → Low correlation = Reduce position size

Crypto-Risk-On = Focus on crypto longs

3. Divergence Trading

🔍 Look for:

Strong correlation breakdown = Potential volatility

Cross-asset correlation surge = Follow the leader

Volume-price correlation extremes = Trend confirmation

4. Overbought/Oversold Reversals

⚡ Trade reversals when:

WT crosses in extreme zones (-60/+60)

HTF alignment shows opposite trend weakening

Correlation confirms mean reversion setup

Customization Tips

Fine-Tuning Parameters

WaveTrend Core:

Channel Length (10): Lower = more sensitive, Higher = smoother

Average Length (21): Adjust for your timeframe

Correlation Settings:

Length (50): Longer = more stable, Shorter = more responsive

Smoothing (5): Reduce noise in correlation readings

Market Regime:

Risk-On Threshold (0.6): Lower = earlier regime signals

High Correlation Threshold (0.75): Adjust sensitivity

Custom Asset Selection

Replace default symbols with your preferred markets:

Major Assets: Any forex, indices, bonds

Crypto: Any digital currencies

Must use correct exchange prefix (e.g., BINANCE:BTCUSDT)

Alert System

Enable "Advanced Alerts" to receive notifications for:

✅ Market regime changes

✅ Correlation breakdowns/surges

✅ Strong signals with high correlation

✅ Extreme volume-price correlation

✅ Complete HTF alignment

Correlation Interpretation Guide

ValueMeaningTrading Implication+0.75 to +1.0Strong positiveAssets move together+0.5 to +0.75Moderate positiveGenerally aligned+0.25 to +0.5Weak positiveLoose relationship-0.25 to +0.25No correlationIndependent movements-0.5 to -0.25Weak negativeSlight inverse relationship-0.75 to -0.5Moderate negativeTend to move opposite-1.0 to -0.75Strong negativeStrongly inversely correlated

Best Practices

Use Multiple Timeframes: Check HTF alignment before trading

Confirm with Correlation: Strong signals work best with supportive correlations

Watch Regime Changes: Adjust strategy based on market conditions

Volume Matters: Enable volume-price correlation for confirmation

Quality Over Quantity: Trade only high-quality setups (>70% signal quality)

Common Patterns to Watch

🔵 Risk-On Environment:

Gold-BTC positive correlation

DXY negative correlation with risk assets

High crypto correlations

🔴 Risk-Off Environment:

Flight to safety (Gold up, stocks down)

DXY strength

Correlation breakdowns

🟡 Transition Periods:

Low correlation across assets

Mixed HTF signals

Use caution, reduce position sizes

Technical Notes

Calculation Period: Uses HLC3 (average of high, low, close)

Correlation Window: Rolling correlation over specified length

HTF Data: Accurately calculated using security() function

Performance: Optimized for real-time calculation on all timeframes

Support

For optimal performance:

Use on 15-minute to daily timeframes

Enable only needed asset groups

Adjust correlation length based on trading style

Combine with your existing strategy for confirmation

Enjoy comprehensive multi-asset analysis! 🚀

Kernel Regression Trend LineKTrend – Non-Repainting Kernel Regression Trend (2025 Clean Version)

Ultra-clean, powerful, and completely non-repainting trend-following tool based on advanced Kernel regression (Rational Quadratic + Gaussian blend).

How it works:

• Uses two different kernel estimates with smart lag to detect genuine trend reversals

• Plots a thick, beautifully colored trend line (teal when rising, deep red when falling)

• Places precise, locked-in Bullish Flip (green triangle below bar) and Bearish Flip (red triangle above bar) signals only on confirmed bar close – zero repaint, ever

• Optional smoothing mode for even cleaner visuals

Features

✓ 100% non-repainting signals and line

✓ Minimal lag while staying extremely responsive

✓ Clean aesthetic – perfect for BTC, ETH, stocks, forex, any timeframe

✓ Built-in alerts for Bullish & Bearish flips

✓ Fully open source (MPL 2.0)

Default settings are already battle-tested and loved by thousands:

- Lookback Window: 11

- Relative Weighting: 8.0

- Regression Level: 25

- Lag: 2

Great on 1H–Daily charts, especially crypto and indices.

Credits: Original kernel library by jdehorty, cleaned & enhanced flip logic by HighlanderOne.

Enjoy the smoothest, most reliable kernel trend tool on TradingView – completely free!

Advanced Time Dividers & Killzones IndicatorOverview

A comprehensive Pine Script v6 indicator that displays customizable time period dividers and trading session killzones on your chart. Perfect for intraday traders who need clear visual separation of time periods and want to identify key trading sessions.

✨ Features

Time Period Dividers

Weekly Lines: Vertical lines marking the start of each week

Monthly Lines: Vertical lines marking the start of each month

Quarterly Lines: Vertical lines marking the start of each quarter (Q1, Q2, Q3, Q4)

Yearly Lines: Vertical lines marking the start of each year

Trading Session Killzones

London Session: 2:00-5:00 GMT (Blue shaded box)

New York Session: 7:00-10:00 GMT (Green shaded box)

London Close: 10:00-12:00 GMT (Orange shaded box)

Asia Session: 20:00-00:00 GMT (Pink shaded box)

🎨 Customization Options

Display Controls

Toggle each time divider type individually

Toggle each killzone individually

Adjust historical and future display range

Show/hide labels on dividers and killzones

Style Customization

Line Styles: Choose between Solid, Dashed, or Dotted lines

Line Width: Adjustable from 1 to 5 pixels

Colors: Fully customizable colors for each element with transparency control

Label Size: Choose from Tiny, Small, Normal, or Large

Period Settings

Control how many bars to display in the past (0-5000)

Control how many bars to display in the future (0-1000)

📋 Usage Instructions

Add to Chart: Add the indicator to any chart

Select Timeframe: Works best on intraday timeframes (1H, 15min, 5min) for killzones

Customize: Open settings to enable/disable features and customize colors

Trading: Use the dividers to identify time periods and killzones to spot high-liquidity sessions

💡 Trading Applications

Time Dividers

Weekly/Monthly Analysis: Identify major time period transitions

Market Structure: Analyze how price behaves at period boundaries

Event Correlation: Align with economic calendar events

Killzones

High Liquidity Periods: Trade during peak market activity

ICT Strategy: Follows Inner Circle Trader killzone concepts

Session-Based Trading: Focus on specific trading sessions

Volatility Windows: Identify when major moves typically occur

⚙️ Technical Details

Version: Pine Script v6

Type: Overlay indicator

Max Lines: 500 (optimized performance)

Max Boxes: 500 (for killzone visualization)

Timezone: GMT/UTC for killzones

Memory Efficient: Automatic cleanup of old objects

🎯 Best Practices

Combine with Price Action: Use dividers to frame your analysis

Focus on Killzones: Most significant price moves occur during these sessions

Adjust Transparency: Find the right balance between visibility and chart clarity

Use Labels Wisely: Toggle labels on/off based on your needs

Timeframe Selection: Use lower timeframes (≤1H) to see killzones clearly

📝 Notes

Killzone times are in GMT/UTC timezone

Works on all instruments (Forex, Crypto, Stocks, Futures)

Optimized for performance with automatic memory management

Fully compatible with other indicators

🔄 Updates & Support

This indicator is actively maintained. Feel free to suggest improvements or report issues in the comments.

DCA Position vs Cash HoldingThis indicator visualizes the performance of a simulated dollar-cost averaging (DCA) strategy compared to simply holding cash. It models the cumulative position size and value of buying a fixed dollar amount of the asset per candle over a configurable lookback period.

🔍 What It Shows:

Simulates buying $1 (or any amount) of the asset per candle

Tracks the total units accumulated and their current market value

Plots the difference between the DCA position value and total cash spent

Highlights when DCA buyers are underwater — a potential contrarian buy zone

📈 How to Use:

Values above zero indicate DCA outperformance vs cash

Values below zero signal structural drawdown — often a high-conviction bulk-buy opportunity

Use as a sentiment overlay to time discretionary adds or confirm regime shifts

⚙️ Inputs:

Lookback Window: Number of candles used to simulate DCA accumulation

DCA Amount: Dollar value purchased per candle

This tool is ideal for traders seeking to quantify accumulation efficiency, identify cycle inflection points, and visualize sentiment-weighted cost basis dynamics.

MA SMART Angle

### 📊 WHAT IS MA SMART ANGLE?

**MA SMART Angle** is an advanced momentum and trend detection indicator that analyzes the angles (slopes) of multiple moving averages to generate clear, non-repainting BUY and SELL signals.

**Original Concept Credit:** This indicator builds upon the "MA Angles" concept originally created by **JD** (also known as Duyck). The core angle calculation methodology and Jurik Moving Average (JMA) implementation by **Everget** are preserved from the original open-source work. The angle calculation formula was contributed by **KyJ**. This enhanced version is published with respect to the open-source nature of the original indicator.

Original indicator reference: "ma angles - JD" by Duyck

---

## 🎯 ORIGINALITY & VALUE PROPOSITION

### **What Makes This Different from the Original:**

While the original "MA Angles" by **JD** provided excellent angle visualization, it lacked actionable entry signals. **MA SMART Angle** addresses this by adding:

**1. Clear Entry/Exit Signals**

- Explicit BUY/SELL arrows based on angle crossovers, momentum confirmation, and MA alignment

- No guessing when to enter trades - the indicator tells you exactly when conditions align

**2. Non-Repainting Logic**

- All signals use confirmed historical data (shifted by 2 bars minimum)

- Critical for backtesting reliability and live trading confidence

- Original indicator could repaint signals on current bar

**3. Dual Signal System**

- **Simple Mode:** More frequent signals based on angle crossovers + momentum (for active traders)

- **Strict Mode:** Requires full multi-MA alignment + momentum confirmation (for conservative traders)

- Adaptable to different trading styles and risk tolerances

**4. Smart Signal Filtering**

- **Anti-spam cooldown:** Prevents duplicate signals within configurable bar count

- **No-trade zone detection:** Filters out low-conviction sideways markets automatically

- **Multi-timeframe MA alignment:** Ensures all moving averages agree on direction before signaling

**5. Enhanced Visualization**

- Large, clear BUY/SELL arrows with descriptive labels

- Color-coded backgrounds for market states (trending vs. ranging)

- Momentum histogram showing acceleration/deceleration in real-time

- Live status table displaying trend strength, angle value, momentum, and MA alignment

**6. Professional Alert System**

- Four distinct alert conditions: BUY Signal, SELL Signal, Strong BUY, Strong SELL

- Enables automated trade notifications and strategy integration

**7. Modified MA Periods**

- Original used EMA(27), EMA(83), EMA(278)

- Enhanced version uses faster EMA(3), EMA(8), EMA(13) for more responsive signals

- Better suited for modern volatile markets and shorter timeframes

---

## 📐 HOW IT WORKS - TECHNICAL EXPLANATION

### **Core Methodology:**

The indicator calculates angles (slopes) for five key moving averages:

- **JMA (Jurik Moving Average)** - Smooth, lag-reduced trend line (original implementation by **Everget**)

- **JMA Fast** - Responsive momentum indicator with higher power parameter

- **MA27 (EMA 3)** - Primary fast-moving average for signal generation

- **MA83 (EMA 8)** - Medium-term trend confirmation

- **MA278 (EMA 13)** - Slower trend filter

### **Angle Calculation Formula (by KyJ):**

```

angle = arctan((MA - MA ) / ATR(14)) × (180 / π)

```

**Why ATR normalization?**

- Makes angles comparable across different instruments (forex, stocks, crypto)

- Makes angles comparable across different timeframes

- Accounts for volatility - a 10-point move in different assets has different significance

**Angle Interpretation:**

- **> 15°** = Strong trend (momentum accelerating)

- **0° to 15°** = Weak trend (momentum present but moderate)

- **-2° to +2°** = No-trade zone (sideways/choppy market)

- **< -15°** = Strong downtrend

### **Signal Generation Logic:**

#### **BUY Signal Conditions:**

1. MA27 angle crosses above 0° (upward momentum initiates)

2. All three EMAs (3, 8, 13) pointing upward (trend alignment confirmed)

3. Momentum is positive for 2+ bars (acceleration, not deceleration)

4. Angle exceeds minimum threshold (not in no-trade zone)

5. Cooldown period passed (prevents signal spam)

#### **SELL Signal Conditions:**

1. MA27 angle crosses below 0° (downward momentum initiates)

2. All three EMAs pointing downward (downtrend alignment)

3. Momentum is negative for 2+ bars

4. Angle below negative threshold (not in no-trade zone)

5. Cooldown period passed

#### **Strong BUY+ / SELL+ Signals:**

Additional entry opportunities when JMA Fast crosses JMA Slow while maintaining strong directional angle - indicates momentum acceleration within established trend.

---

## 🔧 HOW TO USE

### **Recommended Settings by Trading Style:**

**Scalpers / Day Traders:**

- Signal Type: **Simple**

- Minimum Angle: **3-5°**

- Cooldown Bars: **3-5 bars**

- Timeframes: 1m, 5m, 15m

**Swing Traders:**

- Signal Type: **Strict**

- Minimum Angle: **7-10°**

- Cooldown Bars: **8-12 bars**

- Timeframes: 1H, 4H, Daily

**Position Traders:**

- Signal Type: **Strict**

- Minimum Angle: **10-15°**

- Cooldown Bars: **15-20 bars**

- Timeframes: Daily, Weekly

### **Parameter Descriptions:**

**1. Source** (default: OHLC4)

- Price data used for MA calculations

- OHLC4 provides smoothest angles

- Close is more responsive but noisier

**2. Threshold for No-Trade Zones** (default: 2°)

- Angles below this are considered sideways/ranging

- Increase for stricter filtering of choppy markets

- Decrease to allow signals in quieter trending periods

**3. Signal Type** (Simple vs. Strict)

- **Simple:** Angle crossover OR (trend + momentum)

- **Strict:** Angle crossover AND all MAs aligned AND momentum confirmed

- Start with Simple, switch to Strict if too many false signals

**4. Minimum Angle for Signal** (default: 5°)

- Only generate signals when angle exceeds this threshold

- Higher values = stronger trends required

- Lower values = more sensitive to momentum changes

**5. Cooldown Bars** (default: 5)

- Minimum bars between consecutive signals

- Prevents spam during volatile chop

- Scale with your timeframe (higher TF = more bars)

**6. Color Bars** (default: true)

- Colors chart bars based on signal state

- Green = bullish conditions, Red = bearish conditions

- Can disable if you prefer clean price bars

**7. Background Colors**

- **Yellow background** = No-trade zone (low angle, ranging market)

- **Green flash** = BUY signal generated

- **Red flash** = SELL signal generated

- All customizable or can be disabled

---

## 📊 INTERPRETING THE INDICATOR

### **Visual Elements:**

**Main Chart Window:**

- **Thick Lime/Fuchsia Line** = MA27 angle (primary signal line)

- **Medium Green/Red Line** = MA83 angle (trend confirmation)

- **Thin Green/Red Line** = MA278 angle (slow trend filter)

- **Aqua/Orange Line** = JMA Fast (momentum detector)

- **Green/Red Area** = JMA slope (overall trend context)

- **Blue/Purple Histogram** = Momentum (angle acceleration/deceleration)

**Signal Arrows:**

- **Large Green ▲ "BUY"** = Primary buy signal (all conditions met)

- **Small Green ▲ "BUY+"** = Strong momentum buy (JMA fast cross)

- **Large Red ▼ "SELL"** = Primary sell signal (all conditions met)

- **Small Red ▼ "SELL+"** = Strong momentum sell (JMA fast cross)

**Status Table (Top Right):**

- **Angle:** Current MA27 angle in degrees

- **Trend:** Classification (STRONG UP/DOWN, UP/DOWN, FLAT)

- **Momentum:** Acceleration state (ACCEL UP/DN, Up/Down)

- **MAs:** Alignment status (ALL UP/DOWN, Mixed)

- **Zone:** Trading zone status (ACTIVE vs. NO TRADE)

- **Last:** Bars since last signal

### **Trading Strategies:**

**Strategy 1: Pure Signal Following**

- Enter LONG on BUY signal

- Exit on SELL signal

- Use stop-loss at recent swing low/high

- Works best on trending instruments

**Strategy 2: Confirmation with Price Action**

- Wait for BUY signal + bullish candlestick pattern

- Wait for SELL signal + bearish candlestick pattern

- Increases win rate by filtering premature signals

- Recommended for beginners

**Strategy 3: Momentum Acceleration**

- Use BUY+/SELL+ signals for adding to positions

- Only take these in direction of primary signal

- Scalp quick moves during momentum spikes

- For experienced traders

**Strategy 4: Mean Reversion in No-Trade Zones**

- When status shows "NO TRADE", fade extremes

- Wait for angle to exit no-trade zone for reversal

- Contrarian approach for range-bound markets

- Requires tight stops

---

## ⚠️ LIMITATIONS & DISCLAIMERS

**What This Indicator DOES:**

✅ Measures momentum direction and strength via angle analysis

✅ Generates signals when multiple conditions align

✅ Filters out low-conviction sideways markets

✅ Provides visual clarity on trend state

**What This Indicator DOES NOT:**

❌ Predict future price movements with certainty

❌ Guarantee profitable trades (no indicator can)

❌ Work equally well on all instruments/timeframes

❌ Replace proper risk management and position sizing

**Known Limitations:**

- **Lagging Nature:** Like all moving averages, signals occur after momentum begins

- **Whipsaw Risk:** Can generate false signals in volatile, directionless markets

- **Optimization Required:** Parameters need adjustment for different assets

- **Not a Complete System:** Should be combined with risk management, position sizing, and other analysis

**Best Performance Conditions:**

- Strong trending markets (crypto bull runs, stock breakouts)

- Liquid instruments (major forex pairs, large-cap stocks)

- Appropriate timeframe selection (match to trading style)

- Used alongside support/resistance and volume analysis

---

## 🔔 ALERT SETUP

The indicator includes four alert conditions:

**1. BUY SIGNAL**

- Message: "MA SMART Angle: BUY SIGNAL! Angle crossed up with momentum"

- Use for: Primary long entries

**2. SELL SIGNAL**

- Message: "MA SMART Angle: SELL SIGNAL! Angle crossed down with momentum"

- Use for: Primary short entries or long exits

**3. Strong BUY**

- Message: "MA SMART Angle: Strong BUY momentum - JMA fast crossed up"

- Use for: Adding to longs or aggressive entries

**4. Strong SELL**

- Message: "MA SMART Angle: Strong SELL momentum - JMA fast crossed down"

- Use for: Adding to shorts or aggressive exits

**Setting Up Alerts:**

1. Right-click indicator → "Add Alert on MA SMART Angle"

2. Select desired condition from dropdown

3. Choose notification method (popup, email, webhook)

4. Set alert expiration (typically "Once Per Bar Close")

---

## 📚 EDUCATIONAL VALUE

This indicator serves as an excellent learning tool for understanding:

**1. Angle-Based Momentum Analysis**

- Traditional indicators show MA crossovers

- This shows the *rate of change* (velocity) of MAs

- Teaches traders to think in terms of momentum acceleration

**2. Multi-Timeframe Confirmation**

- Shows how fast, medium, and slow MAs interact

- Demonstrates importance of trend alignment

- Helps develop patience for high-probability setups

**3. Signal Quality vs. Quantity Tradeoff**

- Simple mode = more signals, more noise

- Strict mode = fewer signals, higher quality

- Teaches discretionary filtering skills

**4. Market State Recognition**

- Visual distinction between trending and ranging markets

- Helps traders avoid trading choppy conditions

- Develops "market context" awareness

---

## 🔄 DIFFERENCES FROM OTHER MA INDICATORS

**vs. Traditional MA Crossovers:**

- Measures momentum (angle) rather than just price crossing MA

- Provides earlier signals as angles change before price crosses

- Filters better for sideways markets using no-trade zones

**vs. MACD:**

- Uses multiple MAs instead of just two

- ATR normalization makes it universal across instruments

- Visual angle representation more intuitive than histogram

**vs. Supertrend:**

- Not based on ATR bands but on MA slope analysis

- Provides graduated strength indication (not just binary trend)

- Less prone to whipsaw in low volatility

**vs. Original "MA Angles" by JD:**

- Adds explicit entry/exit signals (original had none)

- Implements no-repaint logic for reliability

- Includes signal filtering and quality controls

- Provides dual signal systems (Simple/Strict)

- Enhanced visualization and status monitoring

- Uses faster MA periods (3/8/13 vs 27/83/278) for modern markets

---

## 📖 CODE STRUCTURE (for Pine Script learners)

This indicator demonstrates:

**Advanced Pine Script Techniques:**

- Custom function implementation (JMA, angle calculation)

- Var declarations for stateful tracking

- Table creation for HUD display

- Multi-condition signal logic

- Alert system integration

- Proper use of historical references for no-repaint

**Code Organization:**

- Modular function definitions (JMA, angle)

- Clear separation of concerns (inputs, calculations, plotting, alerts)

- Extensive commenting for maintainability

- Best practices for Pine Script v5

**Learning Resources:**

- Study the JMA function to understand adaptive smoothing

- Examine angle calculation for ATR normalization technique

- Review signal logic for multi-condition confirmation patterns

- Analyze anti-spam filtering for state management

The code is open-source - feel free to study, modify, and improve upon it!

---

## 🙏 CREDITS & ATTRIBUTION

**Original Concepts:**

- **"ma angles - JD" by JD (Duyck)** - Core angle calculation methodology and indicator concept

Original open-source indicator on TradingView Community Scripts

- **JMA (Jurik Moving Average) implementation by Everget** - Smooth, low-lag moving average function

Acknowledged in original JD indicator code

- **Angle Calculation formula by KyJ** - Mathematical formula for converting MA slope to degrees using ATR normalization

Acknowledged in original JD indicator code comments

**Enhancements in This Version:**

- Signal generation logic - Original implementation for this indicator

- No-repaint confirmation system - Original implementation

- Dual signal modes (Simple/Strict) - Original implementation

- Visual enhancements and status table - Original implementation

- Alert system and signal filtering - Original implementation

- Modified MA periods (3/8/13 instead of 27/83/278) - Optimization for modern markets

**Open Source Philosophy:**

This indicator follows the open-source spirit of TradingView and the Pine Script community. The original "ma angles - JD" by JD (Duyck) was published as open-source, enabling this enhanced version. Similarly, this code is published as open-source to allow further community improvements.

---

## ⚡ QUICK START GUIDE

**For New Users:**

1. Add indicator to chart

2. Start with default settings (Simple mode)

3. Wait for BUY signal (green arrow)

4. Observe how price behaves after signal

5. Check status table to understand market state

6. Adjust parameters based on your instrument/timeframe

**For Experienced Traders:**

1. Switch to Strict mode for higher quality signals

2. Increase cooldown bars to reduce frequency

3. Raise minimum angle threshold for stronger trends

4. Combine with your existing strategy for confirmation

5. Set up alerts for desired signal types

6. Backtest on your preferred instruments

---

## 🎓 RECOMMENDED COMBINATIONS

**Works Well With:**

- **Volume Analysis:** Confirm signals with volume spikes

- **Support/Resistance:** Take signals near key levels

- **RSI/Stochastic:** Avoid overbought/oversold extremes

- **ATR:** Size positions based on volatility

- **Price Action:** Wait for candlestick confirmation

**Complementary Indicators:**

- Order Flow / Footprint (for institutional confirmation)

- Volume Profile (for identifying value areas)

- VWAP (for intraday mean reversion reference)

- Fibonacci Retracements (for target setting)

---

## 📈 PERFORMANCE EXPECTATIONS

**Realistic Win Rates:**

- Simple Mode: 45-55% (higher frequency, moderate accuracy)

- Strict Mode: 55-65% (lower frequency, higher accuracy)

- Combined with price action: 60-70%

**Best Asset Classes:**

1. **Cryptocurrencies** (strong trends, clear signals)

2. **Forex Major Pairs** (smooth price action, good angles)

3. **Large-Cap Stocks** (trending behavior, liquid)

4. **Index Futures** (trending instruments)

**Challenging Conditions:**

- Low volatility consolidation periods

- News-driven erratic movements

- Thin/illiquid instruments

- Counter-trending markets

---

## 🛡️ RISK DISCLAIMER

**IMPORTANT LEGAL NOTICE:**

This indicator is for **educational and informational purposes only**. It is **NOT financial advice** and does not constitute a recommendation to buy or sell any financial instrument.

**Trading Risks:**

- Trading carries substantial risk of loss

- Past performance does not guarantee future results

- No indicator can predict market movements with certainty

- You can lose more than your initial investment (especially with leverage)

**User Responsibilities:**

- Conduct your own research and due diligence

- Understand the instruments you trade

- Never risk more than you can afford to lose

- Use proper position sizing and risk management

- Consider consulting a licensed financial advisor

**Indicator Limitations:**

- Signals are based on historical data only

- No guarantee of accuracy or profitability

- Parameters must be optimized for your specific use case

- Results vary significantly by market conditions

By using this indicator, you acknowledge and accept all trading risks. The author is not responsible for any financial losses incurred through use of this indicator.

---

## 📧 SUPPORT & FEEDBACK

**Found a bug?** Please report it in the comments with:

- Chart symbol and timeframe

- Parameter settings used

- Description of unexpected behavior

- Screenshot if possible

**Have suggestions?** Share your ideas for improvements!

**Enjoying the indicator?** Leave a like and follow for updates!

VWAP – Pivot Pairs (SECONDS‑BASED RESET)VWAP – Pivot Pairs (SECONDS-BASED RESET) is a Pine Script v6 indicator for TradingView that combines pivot-based breakout detection with resettable VWAP (Volume Weighted Average Price) calculations over user-defined rolling time periods in seconds.It identifies high and low swing pivots via breakout logic, then calculates two VWAP lines per anchor:One using high/low as the price source,

One using close as the price source.

These form "pivot pairs" that reset automatically at the start of each custom-duration period (e.g., every 300 seconds), starting from a user-defined UTC time of day (default: 09:30 UTC).Visuals include:Colored VWAP lines (high pair: red, low pair: green),

Semi-transparent fill zones between each pair,

Optional toggles to show/hide high or low pairs.

Use CasesUse Case

Description

Intraday Scalping (1–15 min charts)

Use 60–300 second resets to capture micro-trends within larger sessions. VWAP pairs act as dynamic support/resistance after breakouts.

High-Frequency / Algo Validation

Backtest strategies on tick/second charts where traditional session resets fail. Align resets with exchange micro-sessions or volatility windows.

Opening Range Breakout (ORB) Enhancement

Set period_seconds = 1800 (30 min) and start time = 09:30 UTC → VWAP builds only on first 30 mins post-open, then floats. Pairs show deviation from ORB mean.

Range-Bound Market Analysis

In choppy markets, VWAP pairs converge near fair value. Divergence signals potential breakout. Fill color intensity shows conviction.

Multi-Timeframe Confluence

Overlay on 1-second chart with 300s reset → matches 5-minute structure. Use close-based VWAP for entries, high/low-based for stops.

Key Features SummaryFeature

Function

period_seconds

Rolling window length in seconds (e.g., 300 = 5 min)

period_start_time

UTC time-of-day anchor (default: 09:30)

new_period logic

Triggers full reset of pivots + VWAP on exact second boundary

breakingHigher / breakingLower

Detects confirmed breakouts (not just close above high)

Dual VWAP per anchor

ta.vwap(high) and ta.vwap(close) for range-aware mean

Fill zones

Visual value area between high/close VWAPs

Toggle visibility

Independently show/hide high or low pivot pairs

How It Works – Step-by-StepTime Engine Converts user inputs → milliseconds

Calculates current period start time using integer division from epoch

Detects exact bar when new period begins (new_period = true)

On New Period Resets both high/low anchors to current bar’s h and l

Forces VWAP recalculation from this bar forward

Breakout Detection Only triggers on strong candles (rising/falling, non-doji)

Requires open/close beyond prior pivot → avoids wicks-only breaks

VWAP Accumulation ta.vwap(source, reset_condition) restarts when anchor resets

Two sources per side → shows where volume clustered (at highs vs closes)

Plotting Four lines + two fills

Clean, customizable, overlay-friendly

Pro TipsUse on Heikin Ashi for smoother breakout signals.

Combine with volume profile to validate VWAP clusters.

For crypto, set period_start_time = 0 (00:00 UTC) for clean 4-hour resets.

Add alerts on new_period or breakingHigher for automation.

In short: This is a precision VWAP tool for time-boxed, pivot-driven mean reversion and breakout trading, ideal for scalpers, day traders, and algo developers needing sub-session granularity.

GTI BGTI: RSI Suite (Standard • Stochastic • Smoothed)

A three-layer momentum and trend toolkit that combines Standard RSI, Stochastic RSI, and a Smoothed/“Macro” RSI to help you read intraday swings, trend transitions, and high-probability reversal/continuation spots.

All in one pane with intuitive coloring and optional divergence markers and alerts.

Why this works

* Stochastic RSI (K/D) visualizes fast momentum swings and timing.

* Standard RSI moves more gradually, helping confirm trend transitions that may span several Stochastic cycles.

* Smoothed RSI (Average → Macro) adds a second-pass filter and slope persistence to reveal the macro direction while suppressing noise.

Used together, Stochastic guides entries/exits around local highs/lows, while the RSI layers improve confidence when a small swing is likely part of a larger turn.

What you’ll see

* Standard RSI (yellow; pink above Bull line, aqua below Bear line).

* Stochastic RSI (K/D) with contextual colors:

* Greens when RSI is weak/oversold (bearish conditions → watch for bullish reversals/continuations).

* Reds when RSI is strong/overbought (bullish conditions → watch for bearish reversals/continuations).

* Smoothed (Macro) RSI with trend color:

* Red when macro is ascending (bullish),

* Aqua when macro is descending (bearish).

* Divergences (optional markers):

* Bearish: RSI Lower High + Price Higher High (red ⬇).

* Bullish: RSI Higher Low + Price Lower Low (green ⬆).

* No repaint: pivots confirm after the chosen right-bars window.

How to use it

* Bullish Reversal

* Macro RSI is reversing at a higher low after price has been in a overall downtrend

* Stochastic RSI is switching from green to red in an overall downtrend

* Bullish Oversold

* Macro RSI is reversing from a significantly low level after price has a short but strong dip during an overall uptrend

* Stochastic RSI is switching from green to red in an overall uptrend

* Bullish Continuation

* Macro RSI is ascending with a strong slope or forming a higher low above the 50 line

* Stochastic RSI is reaching a bottom but still painted red

* Bearish Reversal

* Macro RSI is reversing at a lower high after price has been in a overall uptrend

* Stochastic RSI is switching from red to green in an overall uptrend

* Bearish Overbought

* Macro RSI is reversing from a significantly high level after price has a short but strong jump during an overall downtrend

* Stochastic RSI is switching from red to green in an overall downtrend

* Bearish Continuation

* Macro RSI is descending with a strong slope or forming a lower high below the 50 line

* Stochastic RSI is reaching a top but still painted green

* Divergences: Use as signals of exhaustion—best when aligned with Macro RSI color/slope and key levels (e.g., Bull/Bear lines, 50 midline).

*** IMPORTANT ***

* Stack confluence, don’t single-signal trade. Look for:

* 1) Macro RSI color & slope (red = ascending/bullish, aqua = descending/bearish)

* 2) Standard RSI location (above/below Bull/Bear lines or 50)

* 3) Stoch flip + direction

* 4) Price structure (HH/HL vs LH/LL)

* 5) Divergence type (regular vs hidden) at meaningful levels

* Trade with the macro

* Prioritize longs when Macro RSI is red or just flipped up

* Prioritize shorts when Macro RSI is aqua or just flipped down

* Counter-trend setups = smaller size and faster management.

* Location > signal

* The same crossover/divergence is higher quality near Bull (~60)/Bear(~40) or extremes than in the mid-range chop around 50.

* Early vs confirmed

* Use the early pivot heads-up for anticipation, but scale in only after the confirmed pivot (right-bars complete). If early signal fails to confirm, stand down.

* Define invalidation upfront

* For divergence entries, place stops beyond the pivot extreme (LL/HH). If Macro RSI flips against your trade or RSI breaks back through 50 with slope, exit or tighten.

* Multi-timeframe alignment

* Best results come when entry timeframe (e.g., 1H) aligns with higher-TF macro (e.g., 4H/D). If they disagree, treat it as mean-reversion only.

* Avoid common traps

* Skip: isolated Stochastic flips without RSI support, divergences without price HH/LL confirmation, and serial divergences when Macro RSI slope is strong against the idea.

* Parameter guidance

* Start with defaults; then tune: confirmBars 3–7, minSlope 0.05–0.15 RSI pts/bar, pivot left/right tighter for faster but noisier signals, wider for cleaner but fewer.

* Alerts = workflow, not auto-trades

* Use Macro Flip + Divergence alerts as a checklist trigger; enter only when your confluence rules are met and risk is defined.

Key inputs (tweak to your market/timeframe)

* RSI / Stochastic lengths and K/D smoothing.

* Bull / Bear Lines (default 61.1 / 43.6).

* Average RSI Method/Length (SMA/EMA/RMA/WMA) + Macro Smooth Length.

* Trend confirmation: bars of persistence and minimum slope to reduce flip noise.

* Pivot look-back (left/right) for divergence confirmation strictness.

Alerts included

* Macro Flip Up / Down (Smoothed RSI regime change).

* RSI Bullish/Bearish Divergence (confirmed at pivot).

* Stochastic RSI continuation/divergence (optional).

Tips

* Level + Slope matter. High/low RSI level flags conditions; slope confirms impulse/continuation.

* Let Stochastic time the swing; let Macro RSI filter the trend.

* Tighten or loosen pivot windows to trade fewer/cleaner vs. more/faster signals.

Scissors&Knifes V3.1✂️ The Scissors (PAG Chop V4 Engine)

🧠 Core idea

Scissors measure market compression and breakout readiness.

They use a modified Choppiness Index that looks at the relationship between:

True Range volatility (ATR × period length)

The total high–low range over the same window.

The smaller the ratio (sum of TR vs range), the more directional and impulsive the market is.

The higher the ratio, the more “sideways” the market trades.

This version smooths the result over PAG_SMOOTHLEN bars and applies several color bands that correspond to volatility states.

🎨 Color code meaning

Range State Color Interpretation

≤ 30 Strong Red #8B0000 Momentum exhaustion on downside, sellers dominating — about to reverse or already strong down-trend.

30 – 38 Brick Red #A52A2A Fading downside pressure; often the “bleeding edge” of a bearish climax.

38 – 55 Transparent black (α≈100) Neutral chop zone — indecision, range-building.

55 – 61.8 Yellow (optional) #DAA520 Early compression pocket where volatility starts contracting; the calm before a trend.

61.8 – 70 Bright Green #556B2F Energy release phase: volatility breaking out upward.

≥ 70 Strong Green #355E3B Sustained bullish drive, often continuation leg of a trend.

🪶 Secret nuance:

The transition bands (38–45 and 45–55) are treated as fully transparent to mark “dead zones.”

When PAG Chop sits here, all label activity pauses — the system resets its cluster memory so the next colored print begins a new “cluster”, letting you clearly see where fresh directional momentum starts.

🧩 Cluster logic

Every time a colored (non-transparent) reading appears, it belongs to a “color cluster.”

Grey labels (= count 1) mark the genesis of a new cluster, and following counts 2, 3, 4 … represent the internal continuity of that trend state.

You can optionally hide the first N grey or count 2 labels to reduce clutter on the initial stabilization bars.

✂️ Label meaning

Each label shows:

Emoji ✂️

Current count (e.g. ✂️ = 3 means 3 timeframes are simultaneously firing)

Optional list of the timeframes that contribute.

So a high count (e.g. 8–10) means many lower TFs are synchronizing volatility breakout — a multiframe alignment, often just before an acceleration burst.

🔪 The Knife (Mr Blonde V4 Engine)

🧠 Core idea

Mr Blonde converts the slope of a long EMA into an angle-of-attack metric — literally the “tilt” of market momentum.

It computes the EMA gradient relative to price span and rescales it into degrees (-5 ° to +5 °).

The steeper the angle, the stronger the directional push.

🎨 Color code meaning

Angle range Color Interpretation

≥ +5 ° Transparent (Black 1) Fully over-extended up move — wait for reset.

+3.57 – +5 ° Dark Red Strong upward slope, momentum apex.

+2.14 – +3.57 ° Orange Medium upward slope, trend acceleration zone.

+0.71 – +2.14 ° Light Orange Mild upward bias, pre-momentum phase.

0 to -0.71 ° Yellow Neutral transition.

-0.71 – -2.14 ° Olive Green Soft bearish slope.

-2.14 – -3.57 ° Olive Drab Building bearish momentum.

-3.57 – -5 ° Hunter Green Strong downward angle, aggressive push.

≤ -5 ° Transparent (Black 2) Oversold/over-tilted — likely exhaustion.

🪶 Secret nuance:

Mr Blonde uses a “span normalization” factor that divides EMA slope by the dynamic range of highs and lows.

This lets it compare angles fairly across assets with different volatility profiles (e.g. BTC vs ES) — it’s one of the rare EMA-angle implementations that self-scales properly.

🗡 Label meaning

Emoji 🔪

Count = how many TFs share the same momentum angle bias.

When many TFs show the same slope polarity (e.g. knife = 8), you’re in a deep momentum cascade — a “knife trend.”

💫 Yellow knife

The yellow state marks neutrality or slope flattening.

If you enable yellow visibility (mb_show_yellow), you can see where momentum cools off — often the earliest reversal hint.

⚙️ Shared mechanics between ✂️ and 🔪

Multi-timeframe sweep

The script cycles through 1 m → 10 m by default, running both engines once per TF.

Each returning true adds +1 to the count.

So:

sc_hits = count of timeframes where PAG fires + 1

knife_hits = count of timeframes where MB fires + 1

That “+1 shift” means there’s always at least 1, letting count = 1 represent the local TF itself.

Cluster limiter

If Limit max labels per cluster is on, you cap how many total symbols (both ✂️ & 🔪, including trails) can appear within one color phase — avoiding chart spam during extended trends.

Trails

Each printed label seeds a short-lived “trail” sequence — faded copies extending N bars forward.

Trails visualize the linger effect of the last signal, useful for visually connecting bursts in momentum.

Grey or count = 1 labels can have shorter or longer trails depending on your overrides (*_trail_bars_grey).

They’re purely visual and do not affect alerting.

Alerts

Alerts fire independently of whether you hide labels — unless you enable “respect filters”.

This guarantees you never miss a structural signal even if you suppress visuals for clarity.

🌈 Interpreting Both Together

Scenario Interpretation

✂️ = low (1–2) + 🔪 rising (red/orange) Market just leaving chop, early thrust stage.

✂️ = high (≥ 5) + 🔪 green Fully aligned breakout continuation — trend in progress.

✂️ = yellow cluster + 🔪 yellow Volatility squeeze, energy buildup — next expansion near.

✂️ = green cluster → 🔪 turns red Cross-state conflict; likely transition or correction.

✂️ = grey + 🔪 grey Reset condition — both engines cooling; stand aside.

💡 Hidden edge:

Scissors signal potential, Knife measures kinetic force.

The perfect storm is when ✂️ goes from yellow→green one bar before 🔪 shifts from orange→green — it catches the birth of directional flow while volatility is still tight.

🧭 Reading the labels intuitively

Grey ✂️/🔪 = 1 → embryonic state, may fizzle or bloom.

✂️/🔪 = 2 or 3 → expansion taking hold.

✂️/🔪 ≥ 4 (mid black) → strong synchronized drive across TFs.

Transparent gap → cluster reset; prepare for new phase.

Trail lines → echo of previous cluster strength.

Final secret tip 🗝

Because both engines are mathematically uncorrelated (volatility vs EMA angle), when they agree in color polarity on multiple TFs, you have one of the cleanest probabilistic trend windows possible.

If you ever see ✂️ = 6 + 🔪 = 6 both pointing the same way — that’s a “knife-through-the-scissors” moment: volatility expansion and directional slope synchronized — those are the bars where institutional algorithms tend to add size.

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

Volume Surprise [LuxAlgo]The Volume Surprise tool displays the trading volume alongside the expected volume at that time, allowing users to spot unexpected trading activity on the chart easily.

The tool includes an extrapolation of the estimated volume for future periods, allowing forecasting future trading activity.

🔶 USAGE

We define Volume Surprise as a situation where the actual trading volume deviates significantly from its expected value at a given time.

Being able to determine if trading activity is higher or lower than expected allows us to precisely gauge the interest of market participants in specific trends.

A histogram constructed from the difference between the volume and expected volume is provided to easily highlight the difference between the two and may be used as a standalone.

The tool can also help quantify the impact of specific market events, such as news about an instrument. For example, an important announcement leading to volume below expectations might be a sign of market participants underestimating the impact of the announcement.

Like in the example above, it is possible to observe cases where the volume significantly differs from the expected one, which might be interpreted as an anomaly leading to a correction.

🔹 Detecting Rare Trading Activity

Expected volume is defined as the mean (or median if we want to limit the impact of outliers) of the volume grouped at a specific point in time. This value depends on grouping volume based on periods, which can be user-defined.

However, it is possible to adjust the indicator to overestimate/underestimate expected volume, allowing for highlighting excessively high or low volume at specific times.

In order to do this, select "Percentiles" as the summary method, and change the percentiles value to a value that is close to 100 (overestimate expected volume) or to 0 (underestimate expected volume).

In the example above, we are only interested in detecting volume that is excessively high, we use the 95th percentile to do so, effectively highlighting when volume is higher than 95% of the volumes recorded at that time.

🔶 DETAILS

🔹 Choosing the Right Periods

Our expected volume value depends on grouping volume based on periods, which can be user-defined.

For example, if only the hourly period is selected, volumes are grouped by their respective hours. As such, to get the expected volume for the hour 7 PM, we collect and group the historical volumes that occurred at 7 PM and average them to get our expected value at that time.

Users are not limited to selecting a single period, and can group volume using a combination of all the available periods.

Do note that when on lower timeframes, only having higher periods will lead to less precise expected values. Enabling periods that are too low might prevent grouping. Finally, enabling a lot of periods will, on the other hand, lead to a lot of groups, preventing the ability to get effective expected values.

In order to avoid changing periods by navigating across multiple timeframes, an "Auto Selection" setting is provided.

🔹 Group Length

The length setting allows controlling the maximum size of a volume group. Using higher lengths will provide an expected value on more historical data, further highlighting recurring patterns.

🔹 Recommended Assets

Obtaining the expected volume for a specific period (time of the day, day of the week, quarter, etc) is most effective when on assets showing higher signs of periodicity in their trading activity.

This is visible on stocks, futures, and forex pairs, which tend to have a defined, recognizable interval with usually higher trading activity.

Assets such as cryptocurrencies will usually not have a clearly defined periodic trading activity, which lowers the validity of forecasts produced by the tool, as well as any conclusions originating from the volume to expected volume comparisons.

🔶 SETTINGS

Length: Maximum number of records in a volume group for a specific period. Older values are discarded.

Smooth: Period of a SMA used to smooth volume. The smoothing affects the expected value.

🔹 Periods

Auto Selection: Automatically choose a practical combination of periods based on the chart timeframe.

Custom periods can be used if disabling "Auto Selection". Available periods include:

- Minutes

- Hours

- Days (can be: Day of Week, Day of Month, Day of Year)

- Months

- Quarters

🔹 Summary

Method: Method used to obtain the expected value. Options include Mean (default) or Percentile.

Percentile: Percentile number used if "Method" is set to "Percentile". A value of 50 will effectively use a median for the expected value.

🔹 Forecast

Forecast Window: Number of bars ahead for which the expected volume is predicted.

Style: Style settings of the forecast.

Simplified Percentile ClusteringSimplified Percentile Clustering (SPC) is a clustering system for trend regime analysis.

Instead of relying on heavy iterative algorithms such as k-means, SPC takes a deterministic approach: it uses percentiles and running averages to form cluster centers directly from the data, producing smooth, interpretable market state segmentation that updates live with every bar.