Summer 2020/2021The Pine Script indicator you are examining is designed to enhance your trading chart by visually demarcating specific seasonal periods known as summer for the years 2020 and 2021. This indicator achieves this by employing background shading to indicate these defined summer periods, providing traders with a visual reference to help in analyzing seasonal trends and making informed decisions.

The script operates with precision by defining two critical summer periods: one for the year 2020 and another for the year 2021. The summer period, in this context, is identified as the time span between June 21 and September 22 of each specified year. The script utilizes the Pine Script timestamp function to create exact date and time boundaries for these periods, marking June 21 as the start of summer and September 22 as the end of summer for each year.

In detail, the indicator sets up two distinct background colors to represent the summer periods of 2020 and 2021. Specifically, it employs a semi-transparent blue color to signify the summer period of 2020, and a semi-transparent green color to denote the summer period of 2021. This differentiation in colors allows for easy visual distinction between the two years on the chart.

To achieve this visual effect, the script continuously evaluates the current bar's timestamp against the defined summer periods. If the current bar falls within the summer range of 2020, the background is shaded with the specified blue hue. Conversely, if the current bar is within the summer range of 2021, the background is shaded with the green hue. This approach ensures that the chart background reflects the specific summer periods accurately and distinctly.

By incorporating this indicator into your TradingView chart, you gain the ability to visually distinguish between different summer periods of consecutive years. This can be particularly useful for analyzing how market behavior or price movements vary during these specific times, facilitating better trend analysis and decision-making based on historical seasonal patterns.

Overall, this indicator serves as a practical tool for enhancing your chart's clarity and providing a seasonal context that can aid in the evaluation of trading strategies and historical market trends during the summer months of 2020 and 2021.

Cerca negli script per "宁德时代2021年净利润+资产负债率"

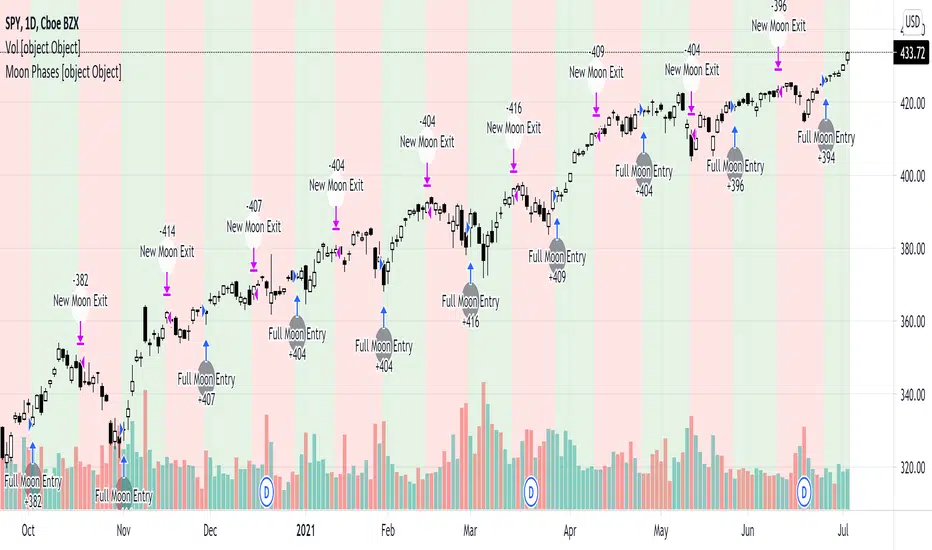

Moon Phases Strategy 2015 till 2021Moon Phases Strategy

Thank you to Author: Dustin Drummond for allowing me to use his Moon Phase strategy code and modify it. I wanted to test out the accuracy of the moon phase. And I could not have done it without his code

It was created to test the Moon Phase theory compared to just a buy and hold strategy.

It buys on full Moon and sells on the new moon. I also have added the ability to add stop loss and target profit if anyone wants to tinker with it. This strategy uses hard-coded dates from 1/1/2015 until 12/31/2021 only! Any dates outside of that range need to be added manually in the code or it will not work.

I may or may not update this so please don't be upset if it stops working after 12/31/2021.

Feel free to use any part of this code and please let me know if you can improve on this strategy.

Result:

50% accurate using data from 2015 till today.

I find a buy and hold strategy to have outperformed the moon phase.

It does have its value. It might be used as a confluence with other established indicators.

Monthly Options Expiration 2021Monthly options expiration for the year 2021.

Also you can set a flag X no. of days before the expiration date. I use it at as marker to take off existing positions in expiration week or roll to next expiration date or to place new trades.

Happy new year 2021 in advance and all the best traders.

[2021] SISIv SCALPER V1/0script of a scalping crypto strategy

aim to capture very short reversal on low timeframe

TASC 2021.10 - MAD Moving Average DifferencePresented here is code for the "Moving Average Difference" indicator originally conceived by John Ehlers, also referred to as MAD. This is one of TradingView's first code releases published in the October 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

This indicator has a companion indicator that is discussed in the article entitled Cycle/Trend Analytics And The MAD Indicator , authored by John Ehlers. He's providing an innovative double dose of indicator code for the month of October 2021.

John Ehlers generally describes it as a "thinking man's" MACD . MAD has similar, yet distinct, intended operation. For those of you familiar with the MACD indicator operation, you will find MACD adjustments having defaults of 12 and 26, while MAD has comparable adjustments with defaults of 8 and 23. These are intended for adjustment, same as any other oscillator.

The MAD indicator can be basically described as two simple moving averages applied within a "rate of change" (ROC) calculation.

Further Related Information

• SMA

• ROC

Join TradingView!

TASC 2021.10 - Cycle/Trend AnalyticsPresented here is code for the "Cycle/Trend Analytics" indicator originally conceived by John Ehlers. This is another one of TradingView's first code releases published in the October 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

This indicator, referred to as "CTA" in later explanations, has a companion indicator that is discussed in the article entitled MAD Moving Average Difference , authored by John Ehlers. He's providing an innovative double dose of indicator code for the month of October 2021.

Modes of Operation

CTA has two modes defined as "trend" and "cycle". Ehlers' intention from what can be gathered from the article is to portray "the strength of the trend" in trend mode on real data. Cycle mode exhibits the response of the bank of calculations when a hypothetical sine wave is utilized as price. When cycle mode is chosen, two other lines will be displayed that are not shown in trend mode. A more detailed explanation of the indicator's technical functionality and intention can be found in the original Cycle/Trend Analytics And The MAD Indicator article, which requires a subscription.

Computational Functionality

The CTA indicator only has one adjustment in the indicator "Settings" for choice of modes. The default mode of operation is "trend". Trend mode applies raw price data to the bank of plots, while the cycle mode employs a sinusoidal oscillator set to a cycle period of 30 bars. These are passed to multiple SMAs, which are then subtracted from the original source data. The result is a fascinating display of plots embellished with vivid array of gradient color on real data or the hypothetical sine wave.

Related Information

• SMA

• color.rgb()

Join TradingView

Forex Dogs Moving Averages with Distance TableThis is an indicator based on the book【Forex】ForexDog’s Vacuum Zone Trading 2021: Trading Strategy to “not lose” based on Experience and Logic written by Forex Dog (yes, this is his author name on Amazon; he is a trader popular mostly in Japan). It consists of simple moving averages which should somewhat correspond to the higher timeframes moving averages. The original was traded on a 15m chart and the periods are as follows: 5, 20, 40, 50, 80, 100, 200, 400, 640, 1600, 1920, 3200.

Then, there is a big table with a distances overview. This should give you an idea of how far each average is in ticks. The minus in front of the ticks_total signifies direction.

I expect some feedback on this because I don't think the user convenience is very with tables being so bright. My goal is to create a system that limits the number of "noodles" on the chart but still carries the information via the tables on the side.

Moving Average Length is not adjustable by design. The book says to use these quite explicitly, although the logic would work just fine with some other levels, it would not be the original strategy.

Good luck!

SWING for GOLD / BITCOIN Hey everyone

I want to share my swing trading system with you.Based on two moving averages coupled to RSI

The options

Shows current trends and entries for trades. Average trade retention 15-20 days

Entries for trades with a crossover of two lines

The percentage of successful test deals XAU/USD for 2010-2021: 69%

BTC Perpetual Futures Premium [Morty]Version 1.0, 20210409

This is an oscillator indicator that shows the premium between BTC perpetual futures and spot prices.

The prices of futures and spot are weighted average prices, weighted by the exchange's trading volume.

When the indicator is in the upper half of the region, the funding rate of perpetual contracts is relatively high, and the market trend is bullish.

When the indicator is in the upper half of the region, the funding rate of perpetual contracts is relatively high, and the market trend is bearish.

You can set the upper and lower limits of the premium. When the indicator exceeds the upper or lower limit, the trend usually reverses.

Buy the dip, Sell the high.

----------------------------------------------------------

Version 1.0, 20210409

这是一个振荡器指标,它显示了BTC永续期货和现货之间的溢价。

期货和现货的价格是加权平均价格,由交易所的交易量加权。

当指标在上半部区域时,永续合约的资金费率相对较高,市场趋势是牛市。

当指标在上半部区域时,永续合约的资金费率相对较高,市场趋势是熊市。

您可以设置溢价的上限和下限。当指标超过上限或者下限,通常会趋势反转。

Buy the dip, Sell the high.

Bitcoin Regression Price BoundariesTLDR

DCA into BTC at or below the blue line. DCA out of BTC when price approaches the red line. There's a setting to toggle the future extrapolation off/on.

INTRODUCTION

Regression analysis is a fundamental and powerful data science tool, when applied CORRECTLY . All Bitcoin regressions I've seen (Rainbow Log, Stock-to-flow, and non-linear models), have glaring flaws ... Namely, that they have huge drift from one cycle to the next.

Presented here, is a canonical application of this statistical tool. "Canonical" meaning that any trained analyst applying the established methodology, would arrive at the same result. We model 3 lines:

Upper price boundary (red) - Predicted the April 2021 top to within 1%

Lower price boundary (green)- Predicted the Dec 2022 bottom within 10%

Non-bubble best fit line (blue) - Last update was performed on Feb 28 2024.

NOTE: The red/green lines were calculated using solely data from BEFORE 2021.

"I'M INTRUIGED, BUT WHAT EXACTLY IS REGRESSION ANALYSIS?"

Quite simply, it attempts to draw a best-fit line over some set of data. As you can imagine, there are endless forms of equations that we might try. So we need objective means of determining which equations are better than others. This is where statistical rigor is crucial.

We check p-values to ensure that a proposed model is better than chance. When comparing two different equations, we check R-squared and Residual Standard Error, to determine which equation is modeling the data better. We check residuals to ensure the equation is sufficiently complex to model all the available signal. We check adjusted R-squared to ensure the equation is not *overly* complex and merely modeling random noise.

While most people probably won't entirely understand the above paragraph, there's enough key terminology in for the intellectually curious to research.

DIVING DEEPER INTO THE 3 REGRESSION LINES ABOVE

WARNING! THIS IS TECHNICAL, AND VERY ABBREVIATED

We prefer a linear regression, as the statistical checks it allows are convenient and powerful. However, the BTCUSD dataset is decidedly non-linear. Thus, we must log transform both the x-axis and y-axis. At the end of this process, we'll use e^ to transform back to natural scale.

Plotting the log transformed data reveals a crucial visual insight. The best fit line for the blowoff tops is different than for the lower price boundary. This is why other models have failed. They attempt to model ALL the data with just one equation. This causes drift in both the upper and lower boundaries. Here we calculate these boundaries as separate equations.

Upper Boundary (in red) = e^(3.24*ln(x)-15.8)

Lower Boundary (green) = e^(0.602*ln^2(x) - 4.78*ln(x) + 7.17)

Non-Bubble best fit (blue) = e^(0.633*ln^2(x) - 5.09*ln(x) +8.12)

* (x) = The number of days since July 18 2010

Anyone familiar with Bitcoin, knows it goes in cycles where price goes stratospheric, typically measured in months; and then a lengthy cool-off period measured in years. The non-bubble best fit line methodically removes the extreme upward deviations until the residuals have the closest statistical semblance to normal data (bell curve shaped data).

Whereas the upper/lower boundary only gets re-calculated in hindsight (well after a blowoff or capitulation occur), the Non-Bubble line changes ever so slightly with each new datapoint. The last update to this line was made on Feb 28, 2024.

ENOUGH NERD TALK! HOW CAN I APPLY THIS?

In the simplest terms, anything below the blue line is a statistical buying opportunity. The closer you approach the green line (the lower boundary) the more statistically strong that opportunity is. As price approaches the red line, is a growing statistical likelyhood/danger of an imminent blowoff top.

So a wise trader would DCA (dollar cost average) into Bitcoin below the blue line; and would DCA out of Bitcoin as it approaches the red line. Historically, you may or may not have a large time-window during points of maximum opportunity. So be vigilant! Anything within 10-20% of the boundary should be regarded as extreme opportunity.

Note: You can toggle the future extrapolation of these lines in the settings (default on).

CLOSING REMARKS

Keep in mind this is a pure statistical analysis. It's likely that this model is probing a complex, real economic process underlying the Bitcoin price. Statistical models like this are most accurate during steady state conditions, where the prevailing fundamentals are stable. (The astute observer will note, that the regression boundaries held despite the economic disruption of 2020).

Thus, it cannot be understated: Should some drastic fundamental change occur in the underlying economic landscape of cryptocurrency, Bitcoin itself, or the broader economy, this model could drastically deviate, and become significantly less accurate.

Furthermore, the upper/lower boundaries cross in the year 2037. THIS MODEL WILL EVENTUALLY BREAK DOWN. But for now, given that Bitcoin price moves on the order of 2000% from bottom to top, it's truly remarkable that, using SOLELY pre-2021 data, this model was able to nail the top/bottom within 10%.

Ehlers Two-Pole Predictor [Loxx]Ehlers Two-Pole Predictor is a new indicator by John Ehlers . The translation of this indicator into PineScript™ is a collaborative effort between @cheatcountry and I.

The following is an excerpt from "PREDICTION" , by John Ehlers

Niels Bohr said “Prediction is very difficult, especially if it’s about the future.”. Actually, prediction is pretty easy in the context of technical analysis . All you have to do is to assume the market will behave in the immediate future just as it has behaved in the immediate past. In this article we will explore several different techniques that put the philosophy into practice.

LINEAR EXTRAPOLATION

Linear extrapolation takes the philosophical approach quite literally. Linear extrapolation simply takes the difference of the last two bars and adds that difference to the value of the last bar to form the prediction for the next bar. The prediction is extended further into the future by taking the last predicted value as real data and repeating the process of adding the most recent difference to it. The process can be repeated over and over to extend the prediction even further.

Linear extrapolation is an FIR filter, meaning it depends only on the data input rather than on a previously computed value. Since the output of an FIR filter depends only on delayed input data, the resulting lag is somewhat like the delay of water coming out the end of a hose after it supplied at the input. Linear extrapolation has a negative group delay at the longer cycle periods of the spectrum, which means water comes out the end of the hose before it is applied at the input. Of course the analogy breaks down, but it is fun to think of it that way. As shown in Figure 1, the actual group delay varies across the spectrum. For frequency components less than .167 (i.e. a period of 6 bars) the group delay is negative, meaning the filter is predictive. However, the filter has a positive group delay for cycle components whose periods are shorter than 6 bars.

Figure 1

Here’s the practical ramification of the group delay: Suppose we are projecting the prediction 5 bars into the future. This is fine as long as the market is continued to trend up in the same direction. But, when we get a reversal, the prediction continues upward for 5 bars after the reversal. That is, the prediction fails just when you need it the most. An interesting phenomenon is that, regardless of how far the extrapolation extends into the future, the prediction will always cross the signal at the same spot along the time axis. The result is that the prediction will have an overshoot. The amplitude of the overshoot is a function of how far the extrapolation has been carried into the future.

But the overshoot gives us an opportunity to make a useful prediction at the cyclic turning point of band limited signals (i.e. oscillators having a zero mean). If we reduce the overshoot by reducing the gain of the prediction, we then also move the crossing of the prediction and the original signal into the future. Since the group delay varies across the spectrum, the effect will be less effective for the shorter cycles in the data. Nonetheless, the technique is effective for both discretionary trading and automated trading in the majority of cases.

EXPLORING THE CODE

Before we predict, we need to create a band limited indicator from which to make the prediction. I have selected a “roofing filter” consisting of a High Pass Filter followed by a Low Pass Filter. The tunable parameter of the High Pass Filter is HPPeriod. Think of it as a “stone wall filter” where cycle period components longer than HPPeriod are completely rejected and cycle period components shorter than HPPeriod are passed without attenuation. If HPPeriod is set to be a large number (e.g. 250) the indicator will tend to look more like a trending indicator. If HPPeriod is set to be a smaller number (e.g. 20) the indicator will look more like a cycling indicator. The Low Pass Filter is a Hann Windowed FIR filter whose tunable parameter is LPPeriod. Think of it as a “stone wall filter” where cycle period components shorter than LPPeriod are completely rejected and cycle period components longer than LPPeriod are passed without attenuation. The purpose of the Low Pass filter is to smooth the signal. Thus, the combination of these two filters forms a “roofing filter”, named Filt, that passes spectrum components between LPPeriod and HPPeriod.

Since working into the future is not allowed in EasyLanguage variables, we need to convert the Filt variable to the data array XX. The data array is first filled with real data out to “Length”. I selected Length = 10 simply to have a convenient starting point for the prediction. The next block of code is the prediction into the future. It is easiest to understand if we consider the case where count = 0. Then, in English, the next value of the data array is equal to the current value of the data array plus the difference between the current value and the previous value. That makes the prediction one bar into the future. The process is repeated for each value of count until predictions up to 10 bars in the future are contained in the data array. Next, the selected prediction is converted from the data array to the variable “Prediction”. Filt is plotted in Red and Prediction is plotted in yellow.

The Predict Extrapolation indicator is shown below for the Emini S&P Futures contract using the default input parameters. Filt is plotted in red and Predict is plotted in yellow. The crossings of the Predict and Filt lines provide reliable buy and sell timing signals. There is some overshoot for the shorter cycle periods, for example in February and March 2021, but the only effect is a late timing signal. Further reducing the gain and/or reducing the BarsFwd inputs would provide better timing signals during this period.

Figure 2. Predict Extrapolation Provides Reliable Timing Signals

I have experimented with other FIR filters for predictions, but found none that had a significant advantage over linear extrapolation.

MESA

MESA is an acronym for Maximum Entropy Spectral Analysis. Conceptually, it removes spectral components until the residual is left with maximum entropy. It does this by forming an all-pole filter whose order is determined by the selected number of coefficients. It maximally addresses the data within the selected window and ignores all other data. Its resolution is determined only by the number of filter coefficients selected. Since the resulting filter is an IIR filter, a prediction can be formed simply by convolving the filter coefficients with the data. MESA is one of the few, if not the only way to practically determine the coefficients of a higher order IIR filter. Discussion of MESA is beyond the scope of this article.

TWO POLE IIR FILTER

While the coefficients of a higher order IIR filter are difficult to compute without MESA, it is a relatively simple matter to compute the coefficients of a two pole IIR filter.

(Skip this paragraph if you don’t care about DSP) We can locate the conjugate pole positions parametrically in the Z plane in polar coordinates. Let the radius be QQ and the principal angle be 360 / P2Period. The first order component is 2*QQ*Cosine(360 / P2Period) and the second order component is just QQ2. Therefore, the transfer response becomes:

H(z) = 1 / (1 - 2*QQ*Cosine(360 / P2Period)*Z-1 + QQ2*Z-2)

By mixing notation we can easily convert the transfer response to code.

Output / Input = 1 / (1 - 2*QQ*Cosine(360 / P2Period)* + QQ2* )

Output - 2*QQ*Cosine(360 / P2Period)*Output + QQ2*Output = Input

Output = Input + 2*QQ*Cosine(360 / P2Period)*Output - QQ2*Output

The Two Pole Predictor starts by computing the same “roofing filter” design as described for the Linear Extrapolation Predictor. The HPPeriod and LPPeriod inputs adjust the roofing filter to obtain the desired appearance of an indicator. Since EasyLanguage variables cannot be extended into the future, the prediction process starts by loading the XX data array with indicator data up to the value of Length. I selected Length = 10 simply to have a convenient place from which to start the prediction. The coefficients are computed parametrically from the conjugate pole positions and are normalized to their sum so the IIR filter will have unity gain at zero frequency.

The prediction is formed by convolving the IIR filter coefficients with the historical data. It is easiest to see for the case where count = 0. This is the initial prediction. In this case the new value of the XX array is formed by successively summing the product of each filter coefficient with its respective historical data sample. This process is significantly different from linear extrapolation because second order curvature is introduced into the prediction rather than being strictly linear. Further, the prediction is adaptive to market conditions because the degree of curvature depends on recent historical data. The prediction in the data array is converted to a variable by selecting the BarsFwd value. The prediction is then plotted in yellow, and is compared to the indicator plotted in red.

The Predict 2 Pole indicator is shown above being applied to the Emini S&P Futures contract for most of 2021. The default parameters for the roofing filter and predictor were used. By comparison to the Linear Extrapolation prediction of Figure 2, the Predict 2 Pole indicator has a more consistent prediction. For example, there is little or no overshoot in February or March while still giving good predictions in April and May.

Input parameters can be varied to adjust the appearance of the prediction. You will find that the indicator is relatively insensitive to the BarsFwd input. The P2Period parameter primarily controls the gain of the prediction and the QQ parameter primarily controls the amount of prediction lead during trending sections of the indicator.

TAKEAWAYS

1. A more or less universal band limited “roofing filter” indicator was used to demonstrate the predictors. The HPPeriod input parameter is used to control whether the indicator looks more like a trend indicator or more like a cycle indicator. The LPPeriod input parameter is used to control the smoothness of the indicator.

2. A linear extrapolation predictor is formed by adding the difference of the two most recent data bars to the value of the last data bar. The result is considered to be a real data point and the process is repeated to extend the prediction into the future. This is an FIR filter having a one bar negative group delay at zero frequency, but the group delay is not constant across the spectrum. This variable group delay causes the linear extrapolation prediction to be inconsistent across a range of market conditions.

3. The degree of prediction by linear extrapolation can be controlled by varying the gain of the prediction to reduce the overshoot to be about the same amplitude as the peak swing of the indicator.

4. I was unable to experimentally derive a higher order FIR filter predictor that had advantages over the simple linear extrapolation predictor.

5. A Two Pole IIR predictor can be created by parametrically locating the conjugate pole positions.

6. The Two Pole predictor is a second order filter, which allows curvature into the prediction, thus mitigating overshoot. Further, the curvature is adaptive because the prediction depends on previously computed prediction values.

7. The Two Pole predictor is more consistent over a range of market conditions.

ADDITIONS

Loxx's Expanded source types:

Library for expanded source types:

Explanation for expanded source types:

Three different signal types: 1) Prediction/Filter crosses; 2) Prediction middle crosses; and, 3) Filter middle crosses.

Bar coloring to color trend.

Signals, both Long and Short.

Alerts, both Long and Short.

FII and DII Data

Greetings to All of you.

The script is plotting FII & DII activity of buying or selling on Daily TimeFrame of Nifty Spot.

Will display only on Nifty 50 Spot on Daily TimeFrame . Codes are hardcoded because novice to PineScripting.

Data is collected from NSE website on daily basis, it's an manual process.

Observation:

Start date of observation is 16th Nov., 2021. FII bought worth 14,240 & kept buying for next 2 days & bought stocks worth 17,760 crores. But market kept falling as we can see in the chart.

Now FII's started selling & in next 5 days they sold stocks worth 18,698 crores. What makes sense from this is might have cut their losses early. FII's kept selling & Nifty made an low of 16410.

FII had sold stocks worth -21,954 crores.

FII are negative & the top green box which you see is FII & DII activity from 19th Oct 2021 when Nifty Spot made an High of 18604.45.

As of 14th Jan.,2022 they are still Negative & DII are extremely positive.

NOTE: DII have not sold any thing yet. They are PLUS +74,428 Crore . Now if they start selling we need to take care of our portfolio.

Hope the information might help in someway.

Take Care & Stay Safe why because Health is Wealth.

PS: If you have any better way to improve the hard coded codes please enlighten. Thank you in advance

Simple Moon Phases StrategySimple Moon Phases Strategy

This strategy is very basic and needs some filters to improve results. It was created to test the Moon Phase theory compared to just a buy and hold strategy and it did not beat the buy and hold. However, if you flip the entry and exit signals to the opposite signals it performs a lot worse, so there might be some validity to the Moon Phases having an effect on the markets. I might try to add some filters and increase hold times with trailing stops in a separate version.

WARNING: This strategy uses hard-coded dates from 1/1/2015 until 12/31/2021 only! Any dates outside of that range need to be added manually in the code or it will not work. I may or may not update this so please don't be upset if it stops working after 12/31/2021.

Feel free to use any part of this code and please let me know if you can improve on this strategy.

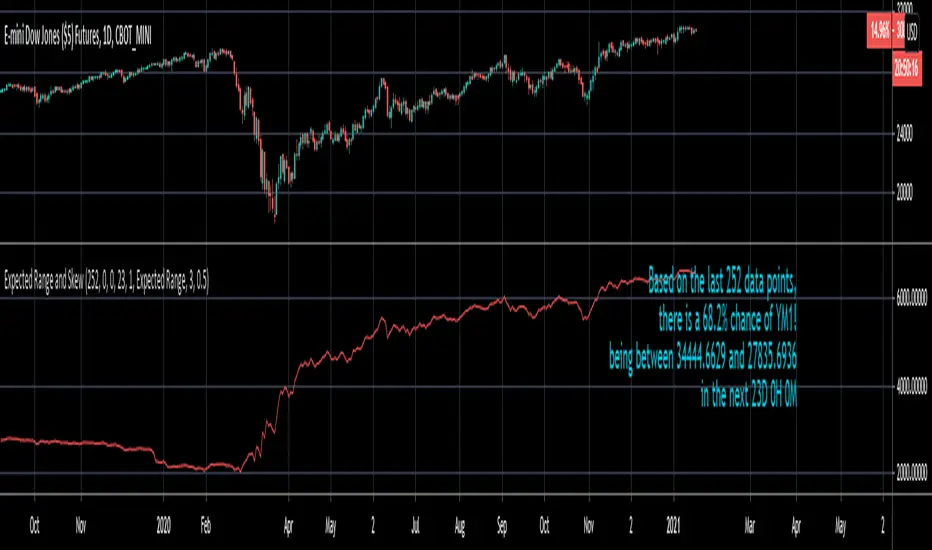

Expected Range and SkewThis is an open source and updated version of my previous "Confidence Interval" script. This script provides you with the expected range over a given time period in the future and the skew of that range. For example, if you wanted to know the expected 1 standard deviation range of MSFT over the next 20 days, this will tell you that. Additionally, this script will also tell you the skew of the expected range.

How to use this script:

1) Enter the length, this will determine the number of data points used in the calculation of the expected range.

2) Enter the amount of time you want projected forward in minutes, hours, and days.

3) Input standard deviation of the expected range.

4) Pick the type of data you want shown from the dropdown menu. Your choices are either the expected range or the skew of the expected range.

5) Enter the x and y coordinates of the label (optional). This is useful so it doesn't impede your view of the plot.

Here are a few notes about this script:

First, the expected range line gives you the width of said range (upper bound - lower bound), and the label will tell you specifically what the upper and lower bounds of the expected range are.

Second, this script will work on any of the default timeframes, but you need to be careful with how far out you try to project the expected range depending on the timeframe you're using. For example, if you're using the 1min timeframe, it probably won't do you any good trying to project the expected range over the next 20 days; or if you're using the daily timeframe it doesn't make sense to try to project the expected range for the next 5 hours. You can tell if the time horizon you're trying to project doesn't work well with the chart timeframe you're using if the current price is outside of either the upper or lower bounds provided in the label. If the current price is within the upper and lower bounds provided in the label, then the time horizon that you're projecting over is reasonable for the chart timeframe you're using.

Third, this script does not countdown automatically, so the time provided in the label will stay the same. For example, in the picture above, the expected range of Dow Futures over the next 23 days from January 12th, 2021 is calculated. But when tomorrow comes it won't count down to 22 days, instead it will show the range over the next 23 days from January 13th, 2021. So if you want the time horizon to change as time goes on you will have to update this yourself manually.

Lastly, if you try to set an alert on this script, you will get a warning about it possibly repainting. This is because of the label, not the plot itself. The label constantly updates itself, which triggers the warning. I tested setting alerts on this script both with and without the inclusion of the label, and without the label the repainting warning did not occur. So remember, if you set an alert on this script you will get a warning about it possibly repainting, but this is because of the label constantly updating, not the plot itself.

WTT Volume Trend [Morty]WTT Volume Trend by Morty

Inspired by Natural Trading Theory

It is a colored volume indicator based on the strength of single candlestick pattern.

It also paints two weighted volume SMA, which shows the strength and trend of the market.

Version 1.0, Updated at 20210327

Features:

- Colored volume bars (Optional)

- Weighted Bullish volume SMA trend lines according to candlestick pattern

- Weighted Bearish volume SMA trend lines according to candlestick pattern

- Adjustable volume SMA length

- Adjustable weighting factors

- Filling the background between volume SMA trend lines

Multiple Alerts by MortyMultiple Alerts by Morty

Version 1.0, Updated at 20210322

When the following signals meet the conditions, alerts will be triggered.

close price cross SMA

SMA_fast cross SMA_slow

MACD cross signal

RSI overbought and oversold

close price cross Bollinger Bands

Momentum cross 0 level

This script will also plot two MAs, EMA default ( SMA optional ).

CDC ActionZone BF for ETHUSD-1D © PRoSkYNeT-EE

Based on improvements from "Kitti-Playbook Action Zone V.4.2.0.3 for Stock Market"

Based on improvements from "CDC Action Zone V3 2020 by piriya33"

Based on Triple MACD crossover between 9/15, 21/28, 15/28 for filter error signal (noise) from CDC ActionZone V3

MACDs generated from the execution of millions of times in the "Brute Force Algorithm" to backtest data from the past 5 years. ( 2017-08-21 to 2022-08-01 )

Released 2022-08-01

***** The indicator is used in the ETHUSD 1 Day period ONLY *****

Recommended Stop Loss : -4 % (execute stop Loss after candlestick has been closed)

Backtest Result ( Start $100 )

Winrate 63 % (Win:12, Loss:7, Total:19)

Live Days 1,806 days

B : Buy

S : Sell

SL : Stop Loss

2022-07-19 07 - 1,542 : B 6.971 ETH

2022-04-13 07 - 3,118 : S 8.98 % $10,750 12,7,19 63 %

2022-03-20 07 - 2,861 : B 3.448 ETH

2021-12-03 07 - 4,216 : SL -8.94 % $9,864 11,7,18 61 %

2021-11-30 07 - 4,630 : B 2.340 ETH

2021-11-18 07 - 3,997 : S 13.71 % $10,832 11,6,17 65 %

2021-10-05 07 - 3,515 : B 2.710 ETH

2021-09-20 07 - 2,977 : S 29.38 % $9,526 10,6,16 63 %

2021-07-28 07 - 2,301 : B 3.200 ETH

2021-05-20 07 - 2,769 : S 50.49 % $7,363 9,6,15 60 %

2021-03-30 07 - 1,840 : B 2.659 ETH

2021-03-22 07 - 1,681 : SL -8.29 % $4,893 8,6,14 57 %

2021-03-08 07 - 1,833 : B 2.911 ETH

2021-02-26 07 - 1,445 : S 279.27 % $5,335 8,5,13 62 %

2020-10-13 07 - 381 : B 3.692 ETH

2020-09-05 07 - 335 : S 38.43 % $1,407 7,5,12 58 %

2020-07-06 07 - 242 : B 4.199 ETH

2020-06-27 07 - 221 : S 28.49 % $1,016 6,5,11 55 %

2020-04-16 07 - 172 : B 4.598 ETH

2020-02-29 07 - 217 : S 47.62 % $791 5,5,10 50 %

2020-01-12 07 - 147 : B 3.644 ETH

2019-11-18 07 - 178 : S -2.73 % $536 4,5,9 44 %

2019-11-01 07 - 183 : B 3.010 ETH

2019-09-23 07 - 201 : SL -4.29 % $551 4,4,8 50 %

2019-09-18 07 - 210 : B 2.740 ETH

2019-07-12 07 - 275 : S 63.69 % $575 4,3,7 57 %

2019-05-03 07 - 168 : B 2.093 ETH

2019-04-28 07 - 158 : S 29.51 % $352 3,3,6 50 %

2019-02-15 07 - 122 : B 2.225 ETH

2019-01-10 07 - 125 : SL -6.02 % $271 2,3,5 40 %

2018-12-29 07 - 133 : B 2.172 ETH

2018-05-22 07 - 641 : S 5.95 % $289 2,2,4 50 %

2018-04-21 07 - 605 : B 0.451 ETH

2018-02-02 07 - 922 : S 197.42 % $273 1,2,3 33 %

2017-11-11 07 - 310 : B 0.296 ETH

2017-10-09 07 - 297 : SL -4.50 % $92 0,2,2 0 %

2017-10-07 07 - 311 : B 0.309 ETH

2017-08-22 07 - 310 : SL -4.02 % $96 0,1,1 0 %

2017-08-21 07 - 323 : B 0.310 ETH

TASC 2021.11 MADH Moving Average Difference, Hann█ OVERVIEW

Presented here is code for the "Moving Average Difference, Hann" indicator originally conceived by John Ehlers. The code is also published in the November 2021 issue of Trader's Tips by Technical Analysis of Stocks & Commodities (TASC) magazine.

█ CONCEPTS

By employing a Hann windowed finite impulse response filter (FIR), John Ehlers has enhanced the Moving Average Difference (MAD) to provide an oscillator with exceptional smoothness.

Of notable mention, the wave form of MADH resembles Ehlers' "Reverse EMA" Indicator, formerly revealed in the September 2017 issue of TASC. Many variations of the "Reverse EMA" were published in TradingView's Public Library.

█ FEATURES

Three values in the script's "Settings/Inputs" provide control over the oscillators behavior:

• The price source

• A "Short Length" with a default of 8, to manage the lower band edge of the oscillator

• The "Dominant Cycle", originally set at 27, which appears to be a placeholder for an adaptive control mechanism

Two coloring options are provided for the line's fill:

• "ZeroCross", the default, uses the line's position above/below the zero level. This is the mode used in the top version of MADH on this chart.

• "Momentum" uses the line's up/down state, as shown in the bottom version of the indicator on the chart.

█ NOTES

Calculations

The source price is used in two independent Hann windowed FIR filters having two different periods (lengths) of historical observation for calculation, one being a "Short Length" and the other termed "Dominant Cycle". These are then passed to a "rate of change" calculation and then returned by the reusable function. The secret sauce is that a "windowed Hann FIR filter" is superior tp a generic SMA filter, and that ultimately reveals Ehlers' clever enhancement. We'll have to wait and see what ingenuities Ehlers has next to unleash. Stay tuned...

The `madh()` function code was optimized for computational efficiency in Pine, differing visibly from Ehlers' original formula, but yielding the same results as Ehlers' version.

Background

This indicator has a sibling indicator discussed in the "The MAD Indicator, Enhanced" article by Ehlers. MADH is an evolutionary update from the prior MAD indicator code published in the October 2021 issue of TASC.

Sibling Indicators

• Moving Average Difference (MAD)

• Cycle/Trend Analytics

Related Information

• Cycle/Trend Analytics And The MAD Indicator

• The Reverse EMA Indicator

• Hann Window

• ROC

Join TradingView!

FIR Hann Window Indicator (Ehlers)From Ehlers' Windowing article:

"A still-smoother weighting function that is easy to program is called the Hann window. The Hann window is often described as a “sine squared” distribution, although it is easier to program as a cosine subtracted from unity. The shape of the coefficient outline looks like a sinewave whose valleys are at the ends of the array and whose peak is at the center of the array. This configuration offers a smooth window transition from the smallest coefficient amplitude to the largest coefficient amplitude."

Ported from: { TASC SEP 2021 FIR Hann Window Indicator } (C) 2021 John F. Ehlers

Stocks & Commodities V. 39:09 (8–14, 23): Windowing by John F. Ehlers

Original code found here: traders.com

FIR Chart: traders.com

ROC Chart: traders.com

Ehlers style implementation mostly maintained for easy verification.

Added optional ROC display.

Style and efficiency updates + Hann windowing as a function coming soon.

Indicator added twice to chart show both FIR and ROC.

JPMorgan G7 Volatility IndexThe JPMorgan G7 Volatility Index: Scientific Analysis and Professional Applications

Introduction

The JPMorgan G7 Volatility Index (G7VOL) represents a sophisticated metric for monitoring currency market volatility across major developed economies. This indicator functions as an approximation of JPMorgan's proprietary volatility indices, providing traders and investors with a normalized measurement of cross-currency volatility conditions (Clark, 2019).

Theoretical Foundation

Currency volatility is fundamentally defined as "the statistical measure of the dispersion of returns for a given security or market index" (Hull, 2018, p.127). In the context of G7 currencies, this volatility measurement becomes particularly significant due to the economic importance of these nations, which collectively represent more than 50% of global nominal GDP (IMF, 2022).

According to Menkhoff et al. (2012, p.685), "currency volatility serves as a global risk factor that affects expected returns across different asset classes." This finding underscores the importance of monitoring G7 currency volatility as a proxy for global financial conditions.

Methodology

The G7VOL indicator employs a multi-step calculation process:

Individual volatility calculation for seven major currency pairs using standard deviation normalized by price (Lo, 2002)

- Weighted-average combination of these volatilities to form a composite index

- Normalization against historical bands to create a standardized scale

- Visual representation through dynamic coloring that reflects current market conditions

The mathematical foundation follows the volatility calculation methodology proposed by Bollerslev et al. (2018):

Volatility = σ(returns) / price × 100

Where σ represents standard deviation calculated over a specified timeframe, typically 20 periods as recommended by the Bank for International Settlements (BIS, 2020).

Professional Applications

Professional traders and institutional investors employ the G7VOL indicator in several key ways:

1. Risk Management Signaling

According to research by Adrian and Brunnermeier (2016), elevated currency volatility often precedes broader market stress. When the G7VOL breaches its high volatility threshold (typically 1.5 times the 100-period average), portfolio managers frequently reduce risk exposure across asset classes. As noted by Borio (2019, p.17), "currency volatility spikes have historically preceded equity market corrections by 2-7 trading days."

2. Counter-Cyclical Investment Strategy

Low G7 volatility periods (readings below the lower band) tend to coincide with what Shin (2017) describes as "risk-on" environments. Professional investors often use these signals to increase allocations to higher-beta assets and emerging markets. Campbell et al. (2021) found that G7 volatility in the lowest quintile historically preceded emerging market outperformance by an average of 3.7% over subsequent quarters.

3. Regime Identification

The normalized volatility framework enables identification of distinct market regimes:

- Readings above 1.0: Crisis/high volatility regime

- Readings between -0.5 and 0.5: Normal volatility regime

- Readings below -1.0: Unusually calm markets

According to Rey (2015), these regimes have significant implications for global monetary policy transmission mechanisms and cross-border capital flows.

Interpretation and Trading Applications

G7 currency volatility serves as a barometer for global financial conditions due to these currencies' centrality in international trade and reserve status. As noted by Gagnon and Ihrig (2021, p.423), "G7 currency volatility captures both trade-related uncertainty and broader financial market risk appetites."

Professional traders apply this indicator in multiple contexts:

- Leading indicator: Research from the Federal Reserve Board (Powell, 2020) suggests G7 volatility often leads VIX movements by 1-3 days, providing advance warning of broader market volatility.

- Correlation shifts: During periods of elevated G7 volatility, cross-asset correlations typically increase what Brunnermeier and Pedersen (2009) term "correlation breakdown during stress periods." This phenomenon informs portfolio diversification strategies.

- Carry trade timing: Currency carry strategies perform best during low volatility regimes as documented by Lustig et al. (2011). The G7VOL indicator provides objective thresholds for initiating or exiting such positions.

References

Adrian, T. and Brunnermeier, M.K. (2016) 'CoVaR', American Economic Review, 106(7), pp.1705-1741.

Bank for International Settlements (2020) Monitoring Volatility in Foreign Exchange Markets. BIS Quarterly Review, December 2020.

Bollerslev, T., Patton, A.J. and Quaedvlieg, R. (2018) 'Modeling and forecasting (un)reliable realized volatilities', Journal of Econometrics, 204(1), pp.112-130.

Borio, C. (2019) 'Monetary policy in the grip of a pincer movement', BIS Working Papers, No. 706.

Brunnermeier, M.K. and Pedersen, L.H. (2009) 'Market liquidity and funding liquidity', Review of Financial Studies, 22(6), pp.2201-2238.

Campbell, J.Y., Sunderam, A. and Viceira, L.M. (2021) 'Inflation Bets or Deflation Hedges? The Changing Risks of Nominal Bonds', Critical Finance Review, 10(2), pp.303-336.

Clark, J. (2019) 'Currency Volatility and Macro Fundamentals', JPMorgan Global FX Research Quarterly, Fall 2019.

Gagnon, J.E. and Ihrig, J. (2021) 'What drives foreign exchange markets?', International Finance, 24(3), pp.414-428.

Hull, J.C. (2018) Options, Futures, and Other Derivatives. 10th edn. London: Pearson.

International Monetary Fund (2022) World Economic Outlook Database. Washington, DC: IMF.

Lo, A.W. (2002) 'The statistics of Sharpe ratios', Financial Analysts Journal, 58(4), pp.36-52.

Lustig, H., Roussanov, N. and Verdelhan, A. (2011) 'Common risk factors in currency markets', Review of Financial Studies, 24(11), pp.3731-3777.

Menkhoff, L., Sarno, L., Schmeling, M. and Schrimpf, A. (2012) 'Carry trades and global foreign exchange volatility', Journal of Finance, 67(2), pp.681-718.

Powell, J. (2020) Monetary Policy and Price Stability. Speech at Jackson Hole Economic Symposium, August 27, 2020.

Rey, H. (2015) 'Dilemma not trilemma: The global financial cycle and monetary policy independence', NBER Working Paper No. 21162.

Shin, H.S. (2017) 'The bank/capital markets nexus goes global', Bank for International Settlements Speech, January 15, 2017.

Price Correction to fix data manipulation and mispricingPrice Correction corrects for index and security mispricing to the extent possible in TradingView on both daily and intraday charts. Price correction addresses mispricing issues for specific securities with known issues, or the user can build daily candles from intraday data instead of relying on exchange reported daily OHLC prices, which can include both legitimate special auction and off-exchange trades or illegitimate mispricing. The user can also detect daily OHLC prices that don’t reflect the intraday price action within a specified percent deviation. Price Correction functions as normal candles or bars for any time frame when correction is not needed.

On the 4th of October 2022, the AMEX exchange, owned by the New York Stock Exchange, decided to misprice the daily OHLC data for the SPY, the world’s largest ETF fund. The exchange eliminated the overnight gap that should have occurred in the daily chart that represents regular trading hours by showing a wick connecting near the close of the previous day. Neither the SPX, the SP500 cash index that the SPY ETF tracks, nor other SPX ETFs such as VOO or IVV show such a wick because significant price action at that level never occurred. The intraday SPY chart never shows the price drop below 372.31 that day, but there is a wick that extends to 366.57. On the 6th of October, they continued this practice of using a wick that connects with the close of the previous day to eliminate gaps in daily price action. The objective of this indicator is to fix such inconsistent mispricing practices in the SPY, NYA, and other indices or securities.

Price Correction corrects for the daily mispricing in the SPY to agree with the price action that actually occurred in the SPX index it tracks, as well as the other SPX ETFs, by using intraday data. The chart below compares the Price Correction of the SPY (top) to the SPX (middle) and the original mispriced SPY (bottom) with incorrect wicks. Price correction (top) removes those incorrect wicks (bottom) to match the SPX (middle).

The daily mispricing of the SPY follows after the successful deployment of the NYSE Composite Index mispricing, NYA, an index that represents all common stocks within the New York Stock Exchange, the largest exchange in the world. The importance of the NYA should not be understated. It is the price counterpart to NYSE’s market internals or statistics. Beginning in 2021, the New York Stock Exchange eliminated gaps in daily OHLC data for the NYA by using the close of the previous day as the open for the following day, in violation of their own NYSE Index Series Methodology. The Methodology states for the opening price that “The first index level is calculated and published around 09:30 ET, when the U.S. equity markets open for their regular trading session. The calculation of that level utilizes the most updated prices available at that moment.” You can verify for yourself that this is simply not the case. The first update of the NYA price for each day matches the close of the previous day, not the “most updated prices available at that moment”, causing data providers to often represent the first intraday bar with a huge sudden price change when an overnight price change occurred instead. For example, on 13 Jun 2022, TradingView shows a one-minute bar drop 2.3%. With a market capitalization of roughly 23 trillion dollars, the NYSE composite capitalization did not suddenly drop a half-trillion dollars in just one minute as the intraday chart data would have you believe. All major US indices, index ETFs, and even foreign indices like the Toronto TAX, the Australian ASXAL, the Bombay SENSEX, and German DAX had down gaps that day, except for the mispriced NYSE index. Price Correction corrects for this mispricing in daily OHLC data, as shown in the main chart at the top of this page comparing the original NYA (top) to the Price Corrected NYA (bottom).

Price Correction also corrects for the intraday mispricing in the NYA. The chart below shows how the Price Correction (top) replaces the incorrect first one-minute candles with gaps (bottom) from 22 Sep 2022 to 29 Sep 2022. TradingView is inconsistent in how intraday data is reported for overnight gaps by sometimes connecting the first intraday bar of the day to the close of the previous day, and other times not. This inconsistency may be due to manually changing the intraday data based on user support tickets. For example, after reporting the lack of a major gap in the NYA daily OHLC prices that existed intraday for 13 Jun 2022, TradingView opted to remove the true gap in intraday prices by creating a 2.3% half-a-trillion-dollar one-minute bar that connected the close of the previous day to show a sudden drop in price that didn’t occur, instead of adding the gap in the daily OHLC data that actually took place from overnight price action.

Price Correction allows users to detect daily OHLC data that does not reflect the intraday price action within a certain percent difference by changing the color of those candles or bars that deviate. The chart below clearly shows the start of the NYSE disinformation campaign for NYA that started in 2021 by painting blue those candles with daily OHLC values that deviated from the intraday values by 0.1%. Before 2021, the number of deviating candles is relatively sparse, but beginning in 2021, the chart is littered with deviating candles.

If there are other index or security mispricing or data issues you are aware of that can be incorporated into Price Correction, please let me know. Accurate financial data is indispensable in making accurate financial decisions. Assert your right to accurate financial data by reporting incorrect data and mispricing issues.

How to use the Price Correction

Simply add this “indicator” to your chart and remove the mispriced default candles or bars by right clicking on the chart, selecting Settings, and de-selecting Body, Wick, and Border under the Symbol tab. The Presets settings automatically takes care of mispricing in the NYA and SPY to the extent possible in TradingView. The user can also build their own daily candles based off of intraday data to address other securities that may have mispricing issues.

sm trend analyzer█ OVERVIEW

This script is intended to provide full time frame continuity information for almost all time frames (3, 5, 15, 30, 60, 4H, Day, Week, Month, Quarter, Year)

When added, the script provides a visual indicator/table to the bottom right of the screen to view the different performance at each time frame.

----------

Output

Time Frames: 3min, 5min, 15min, 30min, 60min, 4 Hour, Day, Week, Month Quarter, Year

Time Frame Labels: 3, 5, 15, 30, H, 4H, D, W, M, Q, Y

Colors: Will display the colors in RED if it's a down time frame (close/current < prior close) or a GREEN if it's a up time frame (close/current > prior close), the color will be more opaque/the opacity will increase the stronger it's levels are for the time frame.

Percentage: The percentages will also display, to give you a quick visual indicator or how strong a time frame is one way or the other.

Best Practices

----------

Had to decouple this from the other scripts because TV limits how much you can plot/show

May be a little slow at times, analyzing a lot of time periods/data be patient.

Used to indicate who is in control, buyers or sellers.

Jul 28, 2021

Release Notes: Fix study name, add some padding (high percentages are hard to get one the whole table)

Jul 28, 2021

Release Notes: Add more space... fix logic. It's open and close not close and prior close for FTC.

Jul 28, 2021

Release Notes: Set the width to ensure the whole percentage is shown. Also stack the cells (2 rows of 6) so it's more compressed and easier to read. Added in the 2H indicator as well.

Aug 2, 2021

Release Notes: Changes: added the ability to disable/hide each box and the ability to change the time frame of each box. The boxes are sequentially numbered, 1 - 12, left to right, top to bottom. So the first box, or 1, would be the top left, 2 would be the next box, all the way to 12 at the bottom right.