SPX Weekly Expected Moves# SPX Weekly Expected Moves Indicator

A professional Pine Script indicator for TradingView that displays weekly expected move levels for SPX based on real options data, with integrated Fibonacci retracement analysis and intelligent alerting system.

## Overview

This indicator helps options and equity traders visualize weekly expected move ranges for the S&P 500 Index (SPX) by plotting historical and current week expected move boundaries derived from weekly options pricing. Unlike theoretical volatility calculations, this indicator uses actual market-based expected move data that you provide from options platforms.

## Key Features

### 📈 **Expected Move Visualization**

- **Historical Lines**: Display past weeks' expected moves with configurable history (10, 26, or 52 weeks)

- **Current Week Focus**: Highlighted current week with extended lines to present time

- **Friday Close Reference**: Orange baseline showing the previous Friday's close price

- **Timeframe Independent**: Works consistently across all chart timeframes (1m to 1D)

### 🎯 **Fibonacci Integration**

- **Five Fibonacci Levels**: 23.6%, 38.2%, 50%, 61.8%, 76.4% between Friday close and expected move boundaries

- **Color-Coded Levels**:

- Red: 23.6% & 76.4% (outer levels)

- Blue: 38.2% & 61.8% (golden ratio levels)

- Black: 50% (midpoint - most critical level)

- **Current Week Only**: Fibonacci levels shown only for active trading week to reduce clutter

### 📊 **Real-Time Information Table**

- **Current SPX Price**: Live market price

- **Expected Move**: ±EM value for current week

- **Previous Close**: Friday close price (baseline for calculations)

- **100% EM Levels**: Exact upper and lower boundary prices

- **Current Location**: Real-time position within the EM structure (e.g., "Above 38.2% Fib (upper zone)")

### 🚨 **Intelligent Alert System**

- **Zone-Aware Alerts**: Separate alerts for upper and lower zones

- **Key Level Breaches**: Alerts for 23.6% and 76.4% Fibonacci level crossings

- **Bar Close Based**: Alerts trigger on confirmed bar closes, not tick-by-tick

- **Customizable**: Enable/disable alerts through settings

## How It Works

### Data Input Method

The indicator uses a **manual data entry approach** where you input actual expected move values obtained from options platforms:

```pinescript

// Add entries using the options expiration Friday date

map.put(expected_moves, 20250613, 91.244) // Week ending June 13, 2025

map.put(expected_moves, 20250620, 95.150) // Week ending June 20, 2025

```

### Weekly Structure

- **Monday 9:30 AM ET**: Week begins

- **Friday 4:00 PM ET**: Week ends

- **Lines Extend**: From Monday open to Friday close (historical) or current time + 5 bars (current week)

- **Timezone Handling**: Uses "America/New_York" for proper DST handling

### Calculation Logic

1. **Base Price**: Previous Friday's SPX close price

2. **Expected Move**: Market-derived ±EM value from weekly options

3. **Upper Boundary**: Friday Close + Expected Move

4. **Lower Boundary**: Friday Close - Expected Move

5. **Fibonacci Levels**: Proportional levels between Friday close and EM boundaries

## Setup Instructions

### 1. Data Collection

Obtain weekly expected move values from options platforms such as:

- **ThinkOrSwim**: Use thinkBack feature to look up weekly expected moves

- **Tastyworks**: Check weekly options expected move data

- **CBOE**: Reference SPX weekly options data

- **Manual Calculation**: (ATM Call Premium + ATM Put Premium) × 0.85

### 2. Data Entry

After each Friday close, update the indicator with the next week's expected move:

```pinescript

// Example: On Friday June 7, 2025, add data for week ending June 13

map.put(expected_moves, 20250613, 91.244) // Actual EM value from your platform

```

### 3. Configuration

Customize the indicator through the settings panel:

#### Visual Settings

- **Show Current Week EM**: Toggle current week display

- **Show Past Weeks**: Toggle historical weeks display

- **Max Weeks History**: Choose 10, 26, or 52 weeks of history

- **Show Fibonacci Levels**: Toggle Fibonacci retracement levels

- **Label Controls**: Customize which labels to display

#### Colors

- **Current Week EM**: Default yellow for active week

- **Past Weeks EM**: Default gray for historical weeks

- **Friday Close**: Default orange for baseline

- **Fibonacci Levels**: Customizable colors for each level type

#### Alerts

- **Enable EM Breach Alerts**: Master toggle for all alerts

- **Specific Alerts**: Four alert types for Fibonacci level breaches

## Trading Applications

### Options Trading

- **Straddle/Strangle Positioning**: Visualize breakeven levels for neutral strategies

- **Directional Plays**: Assess probability of reaching target levels

- **Earnings Plays**: Compare actual vs. expected move outcomes

### Equity Trading

- **Support/Resistance**: Use EM boundaries and Fibonacci levels as key levels

- **Breakout Trading**: Monitor for moves beyond expected ranges

- **Mean Reversion**: Look for reversals at extreme Fibonacci levels

### Risk Management

- **Position Sizing**: Gauge likely price ranges for the week

- **Stop Placement**: Use Fibonacci levels for logical stop locations

- **Profit Targets**: Set targets based on EM structure probabilities

## Technical Implementation

### Performance Features

- **Memory Managed**: Configurable history limits prevent memory issues

- **Timeframe Independent**: Uses timestamp-based calculations for consistency

- **Object Management**: Automatic cleanup of drawing objects prevents duplicates

- **Error Handling**: Robust bounds checking and NA value handling

### Pine Script Best Practices

- **v6 Compliance**: Uses latest Pine Script version features

- **User Defined Types**: Structured data management with WeeklyEM type

- **Efficient Drawing**: Smart line/label creation and deletion

- **Professional Standards**: Clean code organization and comprehensive documentation

## Customization Guide

### Adding New Weeks

```pinescript

// Add after market close each Friday

map.put(expected_moves, YYYYMMDD, EM_VALUE)

```

### Color Schemes

Customize colors for different trading styles:

- **Dark Theme**: Use bright colors for visibility

- **Light Theme**: Use contrasting dark colors

- **Minimalist**: Use single color with transparency

### Label Management

Control label density:

- **Show Current Week Labels Only**: Reduce clutter for active trading

- **Show All Labels**: Full information for analysis

- **Selective Display**: Choose specific label types

## Troubleshooting

### Common Issues

1. **No Lines Appearing**: Check that expected move data is entered for current/recent weeks

2. **Wrong Time Display**: Ensure "America/New_York" timezone is properly handled

3. **Duplicate Lines**: Restart indicator if drawing objects appear duplicated

4. **Missing Fibonacci Levels**: Verify "Show Fibonacci Levels" is enabled

### Data Validation

- **Expected Move Format**: Use positive numbers (e.g., 91.244, not ±91.244)

- **Date Format**: Use YYYYMMDD format (e.g., 20250613)

- **Reasonable Values**: Verify EM values are realistic (typically 50-200 for SPX)

## Version History

### Current Version

- **Pine Script v6**: Latest version compatibility

- **Fibonacci Integration**: Five-level retracement analysis

- **Zone-Aware Alerts**: Upper/lower zone differentiation

- **Dynamic Line Management**: Smart current week extension

- **Professional UI**: Comprehensive information table

### Future Enhancements

- **Multiple Symbols**: Extend beyond SPX to other indices

- **Automated Data**: Integration with options data APIs

- **Statistical Analysis**: Success rate tracking for EM predictions

- **Additional Levels**: Custom percentage levels beyond Fibonacci

## License & Usage

This indicator is designed for educational and trading purposes. Users are responsible for:

- **Data Accuracy**: Ensuring correct expected move values

- **Risk Management**: Proper position sizing and risk controls

- **Market Understanding**: Comprehending options-based expected move concepts

## Support

For questions, issues, or feature requests related to this indicator, please refer to the code comments and documentation within the Pine Script file.

---

**Disclaimer**: This indicator is for informational purposes only. Trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results.

Cerca negli script per "摩根标普500指数基金的收益如何"

A+ Trade CheckList with Comprehensive Relative StrengthThe indicator designed for traders who need real-time market assessment across multiple timeframes and benchmarks. This comprehensive tool combines traditional technical analysis with sophisticated relative strength measurements to provide a complete market picture in one convenient table display.

The indicator tracks essential trading levels including:

QQQ and SPY trend analysis using exponential moving averages

Previous day and week high/low levels for key support and resistance

Market open levels from the first 5 and 15 minutes of trading (9:30 AM ET)

VWAP positioning for institutional price reference

Short-term EMA positioning for momentum assessment

Advanced Relative Strength Analysis

The standout feature of this indicator is its comprehensive 8-metric relative strength scoring system that compares your current ticker against both QQQ (Nasdaq-100) and SPY (S&P 500) benchmarks.

The 4-Metric Relative Strength System Explained

Metric 1: Relative Strength Ratio (RSR)

Purpose: Measures whether your ticker is outperforming or underperforming relative to its historical relationship with the benchmarks.

How it works:

Calculates the ratio of your ticker's price to QQQ/SPY prices

Compares current ratio to a 20-period moving average of the ratio

Scores +1 if ratio is above average (relative strength), -1 if below (relative weakness)

Trading significance: Identifies when a stock is breaking out of its normal correlation pattern with major indices.

Metric 2: Percentage-Based Relative Performance

Purpose: Compares short-term percentage changes to identify immediate relative momentum.

How it works:

Calculates 5-day percentage change for your ticker and benchmarks

Subtracts benchmark performance from ticker performance

Scores +1 if outperforming by >1%, -1 if underperforming by >1%, 0 for neutral

Trading significance: Captures recent momentum shifts and identifies stocks moving independently of market direction.

Metric 3: Beta-Adjusted Relative Strength (Alpha)

Purpose: Measures risk-adjusted performance by accounting for the ticker's natural volatility relationship with benchmarks.

How it works:

Calculates rolling beta (correlation and variance relationship)

Determines expected returns based on benchmark moves and beta

Measures alpha (excess returns above/below expectations)

Scores based on whether alpha is consistently positive or negative

Trading significance: Identifies stocks generating returns beyond what their risk profile would suggest, indicating fundamental strength or weakness.

Metric 4: Volume-Weighted Relative Strength

Purpose: Incorporates volume analysis to validate price-based relative strength signals.

How it works:

Compares VWAP-based percentage changes between ticker and benchmarks

Applies volume weighting factor based on relative volume strength

Enhances score when high relative volume confirms price movements

Trading significance: Distinguishes between genuine institutional-driven moves and low-volume price action that may not sustain.

Combined Scoring System

The indicator generates 8 individual scores (4 metrics × 2 benchmarks) that combine into a single strength assessment:

Score Interpretation

Strong (4-8 points): Ticker significantly outperforming both benchmarks across multiple methodologies

Moderate Strong (1-3 points): Ticker showing good relative strength with some mixed signals

Neutral (0 points): Balanced performance relative to benchmarks

Moderate Weak (-1 to -3 points): Ticker showing relative weakness with some mixed signals

Weak (-4 to -8 points): Ticker significantly underperforming both benchmarks

Display Format

The indicator shows results as: "Strong (6/8)" indicating the ticker scored 6 out of 8 possible points.

Rolling VWAP Channel [LuxAlgo]The Rolling VWAP Channel indicator creates a channel by analyzing a large number of Volume Weighted Average Prices (VWAPs) and determining a Channel based on percentile linear interpolation throughout the VWAPs.

🔶 USAGE

In this indicator, we have formed a Channel by first calculating multiple VWAPs, each with their respective anchor, then locating prices using "Percentile Linear Interpolation".

Note: Percentile Linear Interpolation locates the price point at which a specified percentage of VWAPs fall below it.

For example, a percentile of 50% would mean that 50% of the VWAP values fall below this price.

This method of analysis is important since the VWAPs are not often evenly distributed; therefore, we are able to draw importance to different levels by analyzing in percentiles.

When visualized, there is typically clustering of the VWAP values, which occurs at any given time, as seen below.

The channel can be tailored to each individual, with full control of each percentile represented in the channel. That being said, a general concept is that these clustered areas are clear results of sideways price action, which would lead us to believe that after interactions at these levels, we should expect to see a directional decision made by the market closely after.

🔶 DETAILS

The Rolling VWAP calculation calculates a user-specified number of VWAPs (up to 500), each anchored to a unique starting point in the chart based on the start of a new timeframe.

Each new timeframe that occurs causes a new VWAP to initialize. When the total number of desired VWAPs is reached, the oldest VWAP is removed and re-initialized, anchored to the current bar. Hence, the name " Rolling " VWAPs

This method allows us to automatically generate and manage large amounts of VWAPs without the need for user interaction.

After we have generated these VWAPs, we are able to run analyses on their returned values, such as the "Percentile Linear Interpolation" mentioned in the section above.

🔶 SETTINGS

Anchor Period: Choose which time period to use as the anchor point to initialize new VWAPs from.

VWAP Source: Choose the source for your VWAPs to calculate.

VWAP Amount: Sets the number of VWAPs to use. After this amount is on the chart, the oldest will be rolled.

🔹 Channel Lines

Toggle: Enable the associated VWAP Channel percentile line.

Percentile: Adjust each line's percentile independently for your needs.

Width: Adjust the width of the associated percentile line.

🔹 Calculation

Calculated Bars: Tells the indicator how many bars to calculate on, for faster calculations with less history, use a lower value. Setting this to 0 will remove the bar constraint.

BACAP PRICE STRUCTURE 21 EMA TREND21dma-STRUCTURE

Overview

The 21dma-STRUCTURE indicator is a sophisticated overlay indicator that visualizes price action relative to a triple 21-period exponential moving average structure. Originally developed by BalarezoCapital and enhanced by PrimeTrading, this indicator provides clear visual cues for trend direction and momentum through dynamic bar coloring and EMA structure analysis.

Key Features

Triple EMA Structure

- 21 EMA High: Tracks the exponential moving average of high prices

- 21 EMA Close: Tracks the exponential moving average of closing prices

- 21 EMA Low: Tracks the exponential moving average of low prices

- Dynamic Cloud: Gray fill between high and low EMAs for visual structure reference

Smart Bar Coloring System

- Blue Bars: Price closes above all three EMAs (strong bullish momentum)

- Pink Bars: Daily high falls below the lowest EMA (strong bearish signal)

- Gray Bars: Neutral conditions or transitional phases

- Color Memory: Maintains previous color until new condition is met

Dynamic Center Line

- Trend-Following Color: Green when all EMAs are rising, red when all are falling

- Color Persistence: Maintains trend color during sideways movement

- Visual Clarity: Thicker center line for easy trend identification

Customizable Visual Elements

- Adjustable line thickness for all EMA plots

- Customizable colors for bullish and bearish conditions

- Configurable trend colors for uptrend and downtrend phases

- Optional bar color changes with toggle control

How to Use

Trend Identification

- Rising Green Center Line: All EMAs trending upward (bullish structure)

- Falling Red Center Line: All EMAs trending downward (bearish structure)

- Flat Center Line: Maintains last trend color during consolidation

Momentum Analysis

- Blue Bars: Strong bullish momentum with price above entire EMA structure

- Pink Bars: Strong bearish momentum with high below lowest EMA

- Gray Bars: Neutral or transitional momentum phases

Entry and Exit Signals

- Bullish Setup: Look for blue bars during green center line periods

- Bearish Setup: Look for pink bars during red center line periods

- Exit Consideration: Watch for color changes as potential momentum shifts

Structure Trading

- Support/Resistance: Use EMA cloud as dynamic support and resistance zones

- Breakout Confirmation: Bar color changes can confirm structure breakouts

- Trend Continuation: Color persistence suggests ongoing momentum

Settings

Visual Customization

- Change Bar Color: Toggle to enable/disable bar coloring

- Line Size: Adjust thickness of EMA lines (default: 3)

- Bullish Candle Color: Customize blue bar color

- Bearish Candle Color: Customize pink bar color

Trend Colors

- Uptrend Color: Color for rising EMA center line (default: green)

- Downtrend Color: Color for falling EMA center line (default: red)

- Cloud Color: Fill color between high and low EMAs (default: gray)

Advanced Features

Modified Bar Logic

Unlike traditional EMA systems, this indicator uses refined conditions:

- Bullish signals require close above ALL three EMAs

- Bearish signals require high below the LOWEST EMA

- Enhanced precision reduces false signals compared to single EMA systems

Trend Memory System

- Intelligent color persistence during sideways movement

- Reduces noise from minor EMA fluctuations

- Maintains trend context during consolidation periods

Performance Optimization

- Efficient calculation methods for real-time performance

- Clean visual design that doesn't clutter charts

- Compatible with all timeframes and instruments

Best Practices

Multi-Timeframe Analysis

- Use higher timeframes to identify overall trend direction

- Apply on multiple timeframes for confluence

- Combine with weekly/monthly charts for position trading

Risk Management

- Use bar color changes as early warning signals

- Consider position sizing based on EMA structure strength

- Set stops relative to EMA support/resistance levels

Combination Strategies

- Pair with volume indicators for confirmation

- Use alongside RSI or MACD for momentum confirmation

- Combine with key support/resistance levels

Market Context

- More effective in trending markets than choppy conditions

- Consider overall market environment and sector strength

- Adjust expectations during high volatility periods

Technical Specifications

- Based on 21-period exponential moving averages

- Uses Pine Script v6 for optimal performance

- Overlay indicator that works with any chart type

- Maximum 500 lines for clean performance

Ideal Applications

- Swing trading on daily charts

- Position trading on weekly charts

- Intraday momentum trading (adjust timeframe accordingly)

- Trend following strategies

- Structure-based trading approaches

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis, proper risk management, and consider your individual trading plan and risk tolerance.

Compatible with Pine Script v6 | Works on all timeframes | Optimized for trending markets

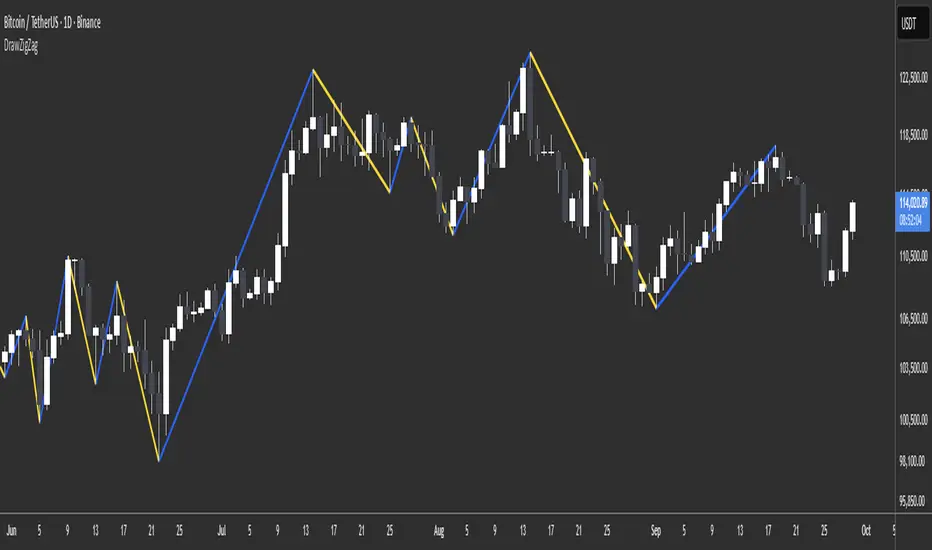

DrawZigZag🟩 OVERVIEW

This library draws zigzag lines for existing pivots. It is designed to be simple to use. If your script creates pivots and you want to join them up while handling edge cases, this library does that quickly and efficiently. If you want your pivots created for you, choose one of the many other zigzag libraries that do that.

🟩 HOW TO USE

Pine Script libraries contain reusable code for importing into indicators. You do not need to copy any code out of here. Just import the library and call the function you want.

For example, for version 1 of this library, import it like this:

import SimpleCryptoLife/DrawZigZag/1

See the EXAMPLE USAGE sections within the library for examples of calling the functions.

For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script User Manual.

🟩 WHAT IT DOES

I looked at every zigzag library on TradingView, after finishing this one. They all seemed to fall into two groups in terms of functionality:

• Create the pivots themselves, using a combination of Williams-style pivots and sometimes price distance.

• Require an array of pivot information, often in a format that uses user-defined types.

My library takes a completely different approach.

Firstly, it only does the drawing. It doesn't calculate the pivots for you. This isn't laziness. There are so many ways to define pivots and that should be up to you. If you've followed my work on market structure you know what I think of Williams pivots.

Secondly, when you pass information about your pivots to the library function, you only need the minimum of pivot information -- whether it's a High or Low pivot, the price, and the bar index. Pass these as normal variables -- bools, ints, and floats -- on the fly as your pivots confirm. It is completely agnostic as to how you derive your pivots. If they are confirmed an arbitrary number of bars after they happen, that's fine.

So why even bother using it if all it does it draw some lines?

Turns out there is quite some logic needed in order to connect highs and lows in the right way, and to handle edge cases. This is the kind of thing one can happily outsource.

🟩 THE RULES

• Zigs and zags must alternate between Highs and Lows. We never connect a High to a High or a Low to a Low.

• If a candle has both a High and Low pivot confirmed on it, the first line is drawn to the end of the candle that is the opposite to the previous pivot. Then the next line goes vertically through the candle to the other end, and then after that continues normally.

• If we draw a line up from a Low to a High pivot, and another High pivot comes in higher, we *extend* the line up, and the same for lines down. Yes this is a form of repainting. It is in my opinion the only way to end up with a correct structure.

• We ignore lower highs on the way up and higher lows on the way down.

🟩 WHAT'S COOL ABOUT THIS LIBRARY

• It's simple and lightweight: no exported user-defined types, no helper methods, no matrices.

• It's really fast. In my profiling it runs at about ~50ms, and changing the options (e.g., trimming the array) doesn't make very much difference.

• You only need to call one function, which does all the calculations and draws all lines.

• There are two variations of this function though -- one simple function that just draws lines, and one slightly more advanced method that modifies an array containing the lines. If you don't know which one you want, use the simpler one.

🟩 GEEK STUFF

• There are no dependencies on other libraries.

• I tried to make the logic as clear as I could and comment it appropriately.

• In the `f_drawZigZags` function, the line variable is declared using the `var` keyword *inside* the function, for simplicity. For this reason, it persists between function calls *only* if the function is called from the global scope or a local if block. In general, if a function is called from inside a loop , or multiple times from different contexts, persistent variables inside that function are re-initialised on each call. In this case, this re-initialisation would mean that the function loses track of the previous line, resulting in incorrect drawings. This is why you cannot call the `f_drawZigZags` function from a loop (not that there's any reason to). The `m_drawZigZagsArray` does not use any internal `var` variables.

• The function itself takes a Boolean parameter `_showZigZag`, which turns the drawings on and off, so there is no need to call the function conditionally. In the examples, we do call the functions from an if block, purely as an illustration of how to increase performance by restricting the amount of code that needs to be run.

🟩 BRING ON THE FUNCTIONS

f_drawZigZags(_showZigZag, _isHighPivot, _isLowPivot, _highPivotPrice, _lowPivotPrice, _pivotIndex, _zigzagWidth, _lineStyle, _upZigColour, _downZagColour)

This function creates or extends the latest zigzag line. Takes real-time information about pivots and draws lines. It does not calculate the pivots. It must be called once per script and cannot be called from a loop.

Parameters:

_showZigZag (bool) : Whether to show the zigzag lines.

_isHighPivot (bool) : Whether the current bar confirms a high pivot. Note that pivots are confirmed after the bar in which they occur.

_isLowPivot (bool) : Whether the current bar confirms a low pivot.

_highPivotPrice (float) : The price of the high pivot that was confirmed this bar. It is NOT the high price of the current bar.

_lowPivotPrice (float) : The price of the low pivot that was confirmed this bar. It is NOT the low price of the current bar.

_pivotIndex (int) : The bar index of the pivot that was confirmed this bar. This is not an offset. It's the `bar_index` value of the pivot.

_zigzagWidth (int) : The width of the zigzag lines.

_lineStyle (string) : The style of the zigzag lines.

_upZigColour (color) : The colour of the up zigzag lines.

_downZagColour (color) : The colour of the down zigzag lines.

Returns: The function has no explicit returns. As a side effect, it draws or updates zigzag lines.

method m_drawZigZagsArray(_a_zigZagLines, _showZigZag, _isHighPivot, _isLowPivot, _highPivotPrice, _lowPivotPrice, _pivotIndex, _zigzagWidth, _lineStyle, _upZigColour, _downZagColour, _trimArray)

Namespace types: array

Parameters:

_a_zigZagLines (array)

_showZigZag (bool) : Whether to show the zigzag lines.

_isHighPivot (bool) : Whether the current bar confirms a high pivot. Note that pivots are usually confirmed after the bar in which they occur.

_isLowPivot (bool) : Whether the current bar confirms a low pivot.

_highPivotPrice (float) : The price of the high pivot that was confirmed this bar. It is NOT the high price of the current bar.

_lowPivotPrice (float) : The price of the low pivot that was confirmed this bar. It is NOT the low price of the current bar.

_pivotIndex (int) : The bar index of the pivot that was confirmed this bar. This is not an offset. It's the `bar_index` value of the pivot.

_zigzagWidth (int) : The width of the zigzag lines.

_lineStyle (string) : The style of the zigzag lines.

_upZigColour (color) : The colour of the up zigzag lines.

_downZagColour (color) : The colour of the down zigzag lines.

_trimArray (bool) : If true, the array of lines is kept to a maximum size of two lines (the line elements are not deleted). If false (the default), the array is kept to a maximum of 500 lines (the maximum number of line objects a single Pine script can display).

Returns: This function has no explicit returns but it modifies a global array of zigzag lines.

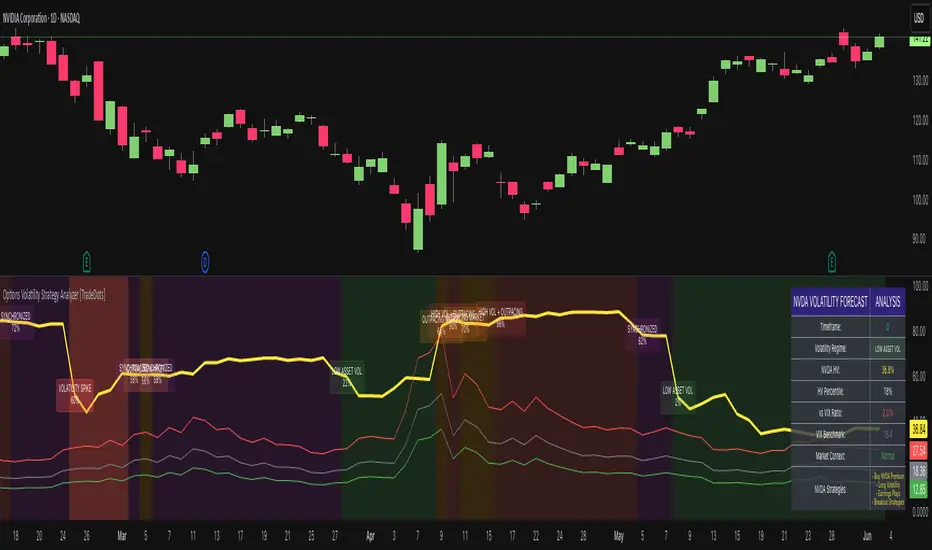

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Regression Channel (Interactive)Weighted Interactive Regression Channel (WIRC)

Overview

The Weighted Interactive Regression Channel improves on traditional regression channels by emphasizing key price points through intelligent weighting. Instead of treating all candles equally, WIRC adapts to market dynamics for better trend detection and channel accuracy.

Key Differences from Standard Channels

Weighted vs. Equal: Prioritizes significant events over uniform weighting

Dynamic vs. Static: Adapts in real time to market changes

Accurate vs. Basic: Reduces noise, enhances signal clarity

Customizable vs. Fixed: Full control over weights and visuals

Weighting Methods

Direction Change – Highlights reversal points via local peaks/troughs

Volume-Based – Emphasizes high-volume candles, ideal for breakouts

Price Range – Weights wide-range candles to capture volatility

Time Decay – Prioritizes recent data for current market relevance

Interactive Features

Data Range: Set channel start/end over 1–500 bars

Visuals: Line styles, color coding, fill options, reference lines

Stats: Slope, R², standard deviation, point count, weight method

Technical Implementation

Weighted Regression Formula: Uses weights for slope, intercept, and deviation

Channel Lines: Center = weighted regression; bounds = ± deviation × multiplier

Usage Scenarios

Trend Analysis: Use Direction Change + longer range

Breakouts: Use Volume weighting + fill + boundary watching

Volatility: Apply Price Range weighting + monitor standard deviation

Current Market: Use Time Decay + shorter ranges + stat display

Parameter Tips

Channel Width:

Narrow (1.0–1.5): Responsive

Standard (1.5–2.0): Balanced

Wide (2.0–3.0+): Conservative

Weighting Intensity:

Conservative (1.5–2.0)

Moderate (2.0–3.0)

Aggressive (3.0+)

Advanced Use

Multi-Timeframe: Use different weightings per timeframe

Market Structure: Detect swings, institutional zones

Risk Management: Dynamic S/R levels, volatility-driven sizing

Best Practices

Start with Direction Change

Test different ranges

Monitor stats

Combine with other indicators

Adjust to market context

Recalibrate regularly

Conclusion

WIRC delivers a smarter, more adaptive view of price action than standard regression tools. With real-time customization and multiple weighting options, it’s ideal for traders seeking precision across strategies—trend tracking, breakout confirmation, or volatility insight.

Daily ADR TableDaily ADR Table Indicator

The Daily Average Daily Range (ADR) Table displays real-time volatility statistics directly on your chart. It shows both the current day's range and the historical average daily range as percentages of the current price, providing essential volatility metrics for trading decisions.

The indicator tracks today's range in real-time throughout the trading session using session-based calculations to ensure accuracy. It compares this against a customizable historical average (default 20 days, adjustable from 1-500 days) to help traders assess whether current volatility is above or below normal levels.

All values are displayed as percentages for easy comparison across different price levels and formatted to two decimal places for precision. The table position, text size, alignment, and colors are fully customizable with nine position options and professional default styling optimized for readability.

This indicator is valuable for day traders, swing traders, and market analysts who need to quickly assess current market volatility relative to historical norms. It assists in position sizing decisions, setting stop losses, and identifying potential breakout or consolidation scenarios based on range expansion or contraction.

Symbol vs Benchmark Performance & Volatility TableThis tool puts the current symbol’s performance and volatility side-by-side with any benchmark —NASDAQ, S&P 500, NIFTY or a custom index of your choice.

A quick glance shows whether the stock is outperforming, lagging, or just moving with the market.

⸻

Features

• ✅ Returns over 1W, 1M, 3M, 6M, 12M

• 🔄 Benchmark comparison with optional difference row

• ⚡ Volatility snapshot (20D, 60D, or 252D)

• 🎛️ Fully customizable:

• Show/hide rows and timeframes

• Switch between default or custom benchmarks

• Pick position, size, and colors

Built to answer a simple, everyday question — “How’s this really doing compared to the broader market?”

Thanks to @BeeHolder, whose performance table originally inspired this.

Hope it makes your analysis a little easier and quicker.

RRC Sniper SetupRRC Sniper Setup, this looks at candles this way:

Go to Market Scanner

Create New Scan → "RRC Sniper Setup"

Add filters listed below with timeframe logic (e.g. 1m/5m)

Run scan on:

Your Watchlist

SPY 500

QQQ 100

AI/Momentum names

1. Reclaim Filter

Find price breaking back above a key level (VWAP or EMA113)

Last 1m Close > EMA 113 (1m)

OR

Last 5m Close > VWAP

2. Retrace Filter

Price pulls back into the zone and holds within a tight range

Current Price < VWAP * 1.0025

AND

Current Price > VWAP * 0.9975

AND

Volume (Current Candle) < Volume (Previous Candle)

✅ 3. Confirm Filter

Price begins moving back up with confirmation candle and volume

Last Candle Close > Last Candle Open

AND

Volume (Current Candle) > Volume (Previous Candle)

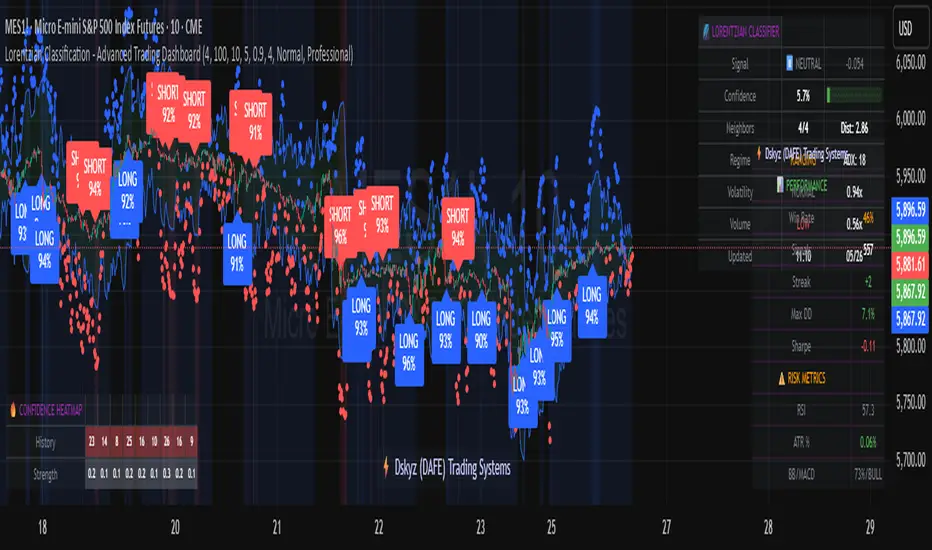

Lorentzian Classification - Advanced Trading DashboardLorentzian Classification - Relativistic Market Analysis

A Journey from Theory to Trading Reality

What began as fascination with Einstein's relativity and Lorentzian geometry has evolved into a practical trading tool that bridges theoretical physics and market dynamics. This indicator represents months of wrestling with complex mathematical concepts, debugging intricate algorithms, and transforming abstract theory into actionable trading signals.

The Theoretical Foundation

Lorentzian Distance in Market Space

Traditional Euclidean distance treats all feature differences equally, but markets don't behave uniformly. Lorentzian distance, borrowed from spacetime geometry, provides a more nuanced similarity measure:

d(x,y) = Σ ln(1 + |xi - yi|)

This logarithmic formulation naturally handles:

Scale invariance: Large price moves don't overwhelm small but significant patterns

Outlier robustness: Extreme values are dampened rather than dominating

Non-linear relationships: Captures market behavior better than linear metrics

K-Nearest Neighbors with Relativistic Weighting

The algorithm searches historical market states for patterns similar to current conditions. Each neighbor receives weight inversely proportional to its Lorentzian distance:

w = 1 / (1 + distance)

This creates a "gravitational" effect where closer patterns have stronger influence on predictions.

The Implementation Challenge

Creating meaningful market features required extensive experimentation:

Price Features: Multi-timeframe momentum (1, 2, 3, 5, 8 bar lookbacks) Volume Features: Relative volume analysis against 20-period average

Volatility Features: ATR and Bollinger Band width normalization Momentum Features: RSI deviation from neutral and MACD/price ratio

Each feature undergoes min-max normalization to ensure equal weighting in distance calculations.

The Prediction Mechanism

For each current market state:

Feature Vector Construction: 12-dimensional representation of market conditions

Historical Search: Scan lookback period for similar patterns using Lorentzian distance

Neighbor Selection: Identify K nearest historical matches

Outcome Analysis: Examine what happened N bars after each match

Weighted Prediction: Combine outcomes using distance-based weights

Confidence Calculation: Measure agreement between neighbors

Technical Hurdles Overcome

Array Management: Complex indexing to prevent look-ahead bias

Distance Calculations: Optimizing nested loops for performance

Memory Constraints: Balancing lookback depth with computational limits

Signal Filtering: Preventing clustering of identical signals

Advanced Dashboard System

Main Control Panel

The primary dashboard provides real-time market intelligence:

Signal Status: Current prediction with confidence percentage

Neighbor Analysis: How many historical patterns match current conditions

Market Regime: Trend strength, volatility, and volume analysis

Temporal Context: Real-time updates with timestamp

Performance Analytics

Comprehensive tracking system monitors:

Win Rate: Percentage of successful predictions

Signal Count: Total predictions generated

Streak Analysis: Current winning/losing sequence

Drawdown Monitoring: Maximum equity decline

Sharpe Approximation: Risk-adjusted performance estimate

Risk Assessment Panel

Multi-dimensional risk analysis:

RSI Positioning: Overbought/oversold conditions

ATR Percentage: Current volatility relative to price

Bollinger Position: Price location within volatility bands

MACD Alignment: Momentum confirmation

Confidence Heatmap

Visual representation of prediction reliability:

Historical Confidence: Last 10 periods of prediction certainty

Strength Analysis: Magnitude of prediction values over time

Pattern Recognition: Color-coded confidence levels for quick assessment

Input Parameters Deep Dive

Core Algorithm Settings

K Nearest Neighbors (1-20): More neighbors create smoother but less responsive signals. Optimal range 5-8 for most markets.

Historical Lookback (50-500): Deeper history improves pattern recognition but reduces adaptability. 100-200 bars optimal for most timeframes.

Feature Window (5-30): Longer windows capture more context but reduce sensitivity. Match to your trading timeframe.

Feature Selection

Price Changes: Essential for momentum and reversal detection Volume Profile: Critical for institutional activity recognition Volatility Measures: Key for regime change detection Momentum Indicators: Vital for trend confirmation

Signal Generation

Prediction Horizon (1-20): How far ahead to predict. Shorter horizons for scalping, longer for swing trading.

Signal Threshold (0.5-0.9): Confidence required for signal generation. Higher values reduce false signals but may miss opportunities.

Smoothing (1-10): EMA applied to raw predictions. More smoothing reduces noise but increases lag.

Visual Design Philosophy

Color Themes

Professional: Corporate blue/red for institutional environments Neon: Cyberpunk cyan/magenta for modern aesthetics

Matrix: Green/red hacker-inspired palette Classic: Traditional trading colors

Information Hierarchy

The dashboard system prioritizes information by importance:

Primary Signals: Largest, most prominent display

Confidence Metrics: Secondary but clearly visible

Supporting Data: Detailed but unobtrusive

Historical Context: Available but not distracting

Trading Applications

Signal Interpretation

Long Signals: Prediction > threshold with high confidence

Look for volume confirmation

- Check trend alignment

- Verify support levels

Short Signals: Prediction < -threshold with high confidence

Confirm with resistance levels

- Check for distribution patterns

- Verify momentum divergence

- Market Regime Adaptation

Trending Markets: Higher confidence in directional signals

Ranging Markets: Focus on reversal signals at extremes

Volatile Markets: Require higher confidence thresholds

Low Volume: Reduce position sizes, increase caution

Risk Management Integration

Confidence-Based Sizing: Larger positions for higher confidence signals

Regime-Aware Stops: Wider stops in volatile regimes

Multi-Timeframe Confirmation: Align signals across timeframes

Volume Confirmation: Require volume support for major signals

Originality and Innovation

This indicator represents genuine innovation in several areas:

Mathematical Approach

First application of Lorentzian geometry to market pattern recognition. Unlike Euclidean-based systems, this naturally handles market non-linearities.

Feature Engineering

Sophisticated multi-dimensional feature space combining price, volume, volatility, and momentum in normalized form.

Visualization System

Professional-grade dashboard system providing comprehensive market intelligence in intuitive format.

Performance Tracking

Real-time performance analytics typically found only in institutional trading systems.

Development Journey

Creating this indicator involved overcoming numerous technical challenges:

Mathematical Complexity: Translating theoretical concepts into practical code

Performance Optimization: Balancing accuracy with computational efficiency

User Interface Design: Making complex data accessible and actionable

Signal Quality: Filtering noise while maintaining responsiveness

The result is a tool that brings institutional-grade analytics to individual traders while maintaining the theoretical rigor of its mathematical foundation.

Best Practices

- Parameter Optimization

- Start with default settings and adjust based on:

Market Characteristics: Volatile vs. stable

Trading Timeframe: Scalping vs. swing trading

Risk Tolerance: Conservative vs. aggressive

Signal Confirmation

Never trade on Lorentzian signals alone:

Price Action: Confirm with support/resistance

Volume: Verify with volume analysis

Multiple Timeframes: Check higher timeframe alignment

Market Context: Consider overall market conditions

Risk Management

Position Sizing: Scale with confidence levels

Stop Losses: Adapt to market volatility

Profit Targets: Based on historical performance

Maximum Risk: Never exceed 2-3% per trade

Disclaimer

This indicator is for educational and research purposes only. It does not constitute financial advice or guarantee profitable trading results. The Lorentzian classification system reveals market patterns but cannot predict future price movements with certainty. Always use proper risk management, conduct your own analysis, and never risk more than you can afford to lose.

Market dynamics are inherently uncertain, and past performance does not guarantee future results. This tool should be used as part of a comprehensive trading strategy, not as a standalone solution.

Bringing the elegance of relativistic geometry to market analysis through sophisticated pattern recognition and intuitive visualization.

Thank you for sharing the idea. You're more than a follower, you're a leader!

@vasanthgautham1221

Trade with precision. Trade with insight.

— Dskyz , for DAFE Trading Systems

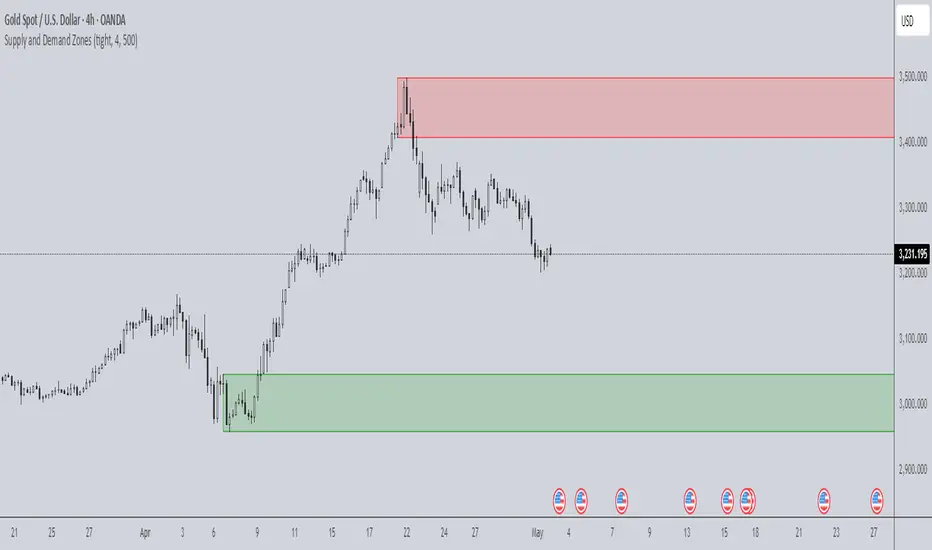

Supply and Demand Zones🔍 Supply and Demand Zones

by The_Forex_Steward

This indicator automatically identifies Supply and Demand Zones based on aggregated synthetic candles, helping traders pinpoint potential reversal or breakout levels with clarity and precision.

🧠 How It Works:

This tool aggregates price data over a set number of candles (defined by the Aggregation Factor ) to create "synthetic candles" that smooth out noise and highlight significant institutional price activity. These candles are then analyzed to detect bullish or bearish order blocks , which are visualized as zones:

-Demand Zones (Green) : Formed when price breaks above the high of a previous bearish synthetic candle.

-Supply Zones (Red) : Formed when price breaks below the low of a previous bullish synthetic candle.

These areas often represent key institutional interest where price is likely to react.

⚙️ Key Features:

-Aggregation Factor : Groups candles to form larger, synthetic ones. Higher values smooth price and reduce noise.

-Custom Zone Length : Define how far zones extend forward (up to 500 bars).

-Mitigation Logic : Choose whether to auto-delete zones once price breaks through them.

-Visual Customization : Customize zone colors and borders to suit your charting style.

-Alerts : Get notified when new Supply or Demand zones are formed.

📈 How to Use It:

1. Trend Trading : Use zones as dynamic support/resistance to enter with trend pullbacks.

2. Reversals : Look for price reactions at untested zones for potential counter-trend setups.

3. Breakouts : Monitor for zone breaks that signal strong momentum or shifts in market structure.

4. Confluence : Combine with other indicators (like RSI or volume) for more robust trade setups.

🔔 Alerts:

Receive alerts when new demand or supply zones are formed so you can take action in real time.

✅ Recommended Settings:

For intraday trading : Use lower aggregation values (e.g., 3–5).

For swing/position trading : Higher values (e.g., 6–10) may give better structure.

RTH Session Highs & LowsA Pine Script indicator designed to track and plot the Regular Trading Hours (RTH) session highs and lows on a chart, typically for U.S. equity markets (e.g., S&P 500, Nasdaq, etc.), which operate from 9:30 AM to 4:00 PM Eastern Time.

Session High & Low Lines:

During the RTH session, the indicator draws green and red horizontal lines that represent the highest and lowest price seen so far within that trading session.

These levels help traders identify intraday support (low) and resistance (high) levels.

New High/Low Markers:

Small triangle markers are placed:

Above the bar when a new intraday high is made (green triangle).

Below the bar when a new intraday low is made (red triangle).

This visually flags when momentum may be building or reversing.

Intraday Strategy Support:

Use the session high/low as dynamic support/resistance for scalping or breakout strategies.

For example:

Breakouts above session highs may indicate bullish strength.

Breakdowns below session lows may suggest bearish momentum.

Mean Reversion Tactics:

Prices approaching these lines and then rejecting can be used for mean reversion setups.

Combine with volume or candlestick patterns for confirmation.

Risk Management:

Set stops or targets relative to session highs/lows.

For instance, use session high as a stop-loss level in a short position.

Volatility Gauge:

Tracking how frequently new highs/lows are formed can help assess intraday volatility or range expansion.

Complement with Indicators:

Combine this with our "McGinley Dynamic Channel with Directional Shading" indicator or our "EMA Crossover with Shading" indicator to add context to breakouts or rejections.

Index Futures vs Cash ArbitrageThis indicator measures the statistical spread between major stock index futures and their corresponding cash indices (e.g., ES vs SPX, NQ vs NDX) using Z-score normalization. It automatically detects commonly traded index pairs (S&P 500, Nasdaq, Dow Jones, Russell 2000) and calculates a smoothed spread between futures and spot prices. A Z-score is then derived from this spread to highlight potential overpricing or underpricing conditions.

Traders can use customizable thresholds to identify mean-reversion opportunities where the futures contract may be temporarily overvalued or undervalued relative to the index. The histogram highlights the direction of the Z-score (green = futures > index, red = futures < index), while built-in alerts notify users of key threshold breaches or zero-line crosses.

This tool is designed for discretionary traders, pairs traders, or anyone exploring statistical arbitrage strategies between futures and spot markets. It is not a buy/sell signal by itself and should be used with additional confluence or risk management techniques.

HILo Ema Double Squeeze BandsHILo Ema Double Squeeze Bands

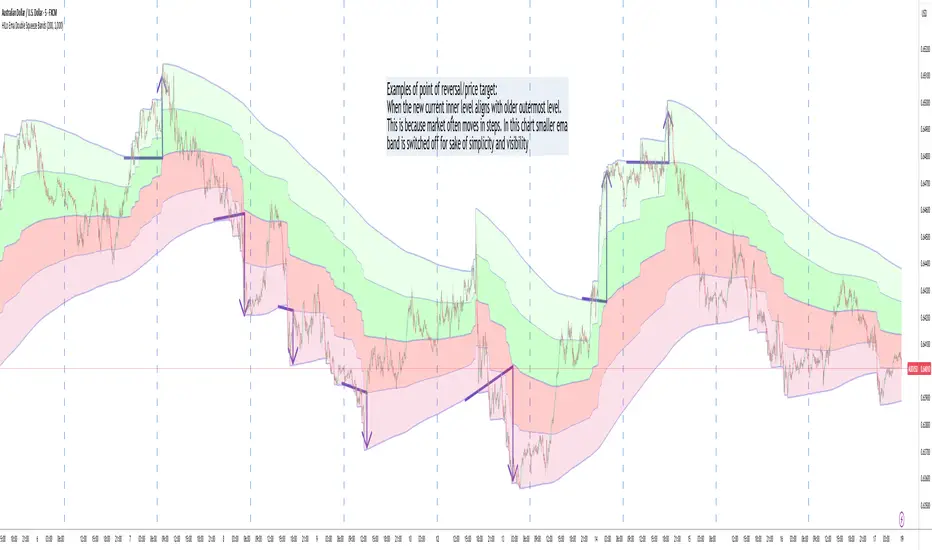

This advanced technical indicator is a powerful variation of "HiLo Ema squeeze bands" that combines the best elements of Donchian channels and EMAs. It's specially designed to identify price squeezes before significant market moves while providing dynamic support/resistance levels and predictive price targets.

Indicator Concept:

The indicator initializes EMAs at each new high or low - the upper EMA tracks highs while the lower EMA tracks lows. The price range between upper and lower bands is divided into 4 equal zones by these lines:

Upper2 (uppermost line)

Upper1 (upper quartile)

Middle (center line)

Lower1 (lower quartile)

Lower2 (lowermost line)

This creates a more trend-responsive alternative to traditional Donchian channels with clearly defined zones for trade planning.

Key Features:

Dual EMA Band System: Utilizes both short-term and long-term EMAs to create adaptive price channels that respond to different market cycles

Quartile Divisions: Each band set includes middle lines and quartile divisions for more precise entry and exit points

Customizable Parameters: Easily adjust EMA periods and display options to suit your trading style and timeframe

Visual Color Zones: Clear color-coded zones help quickly identify bullish and bearish areas

Optional Extra Divisions: Add more granular internal lines (eighth divisions) for enhanced precision with longer EMA periods

Price Labels Option: Display exact price values for key levels directly on the chart

Price Target Prediction:

One of the most valuable features of this indicator is its ability to help predict potential reversal points:

When price breaks above the Upper2 level, look for potential reversals when the new Upper1 or Middle line aligns with previous Upper2 levels

When price breaks below the Lower2 level, look for potential reversals when the new Lower1 or Middle line aligns with previous Lower2 levels

Settings Guide:

Recommended Settings: 200 for Short EMA, 1000 for Long EMA works extremely well across most timeframes and symbols

Display options allow you to show/hide either band system based on your analysis preferences

The new option to divide the long EMA range into 8 parts instead of 4 is particularly useful when:

Long EMA period is >500

Short EMA is switched off and long EMA is used independently

Perfect for swing traders and position traders looking for a more sophisticated volatility-based overlay that adapts to changing market conditions and provides predictive reversal levels.

Note: This indicator works well across multiple timeframes but is especially effective on H4, Daily and Weekly charts for trend trading.

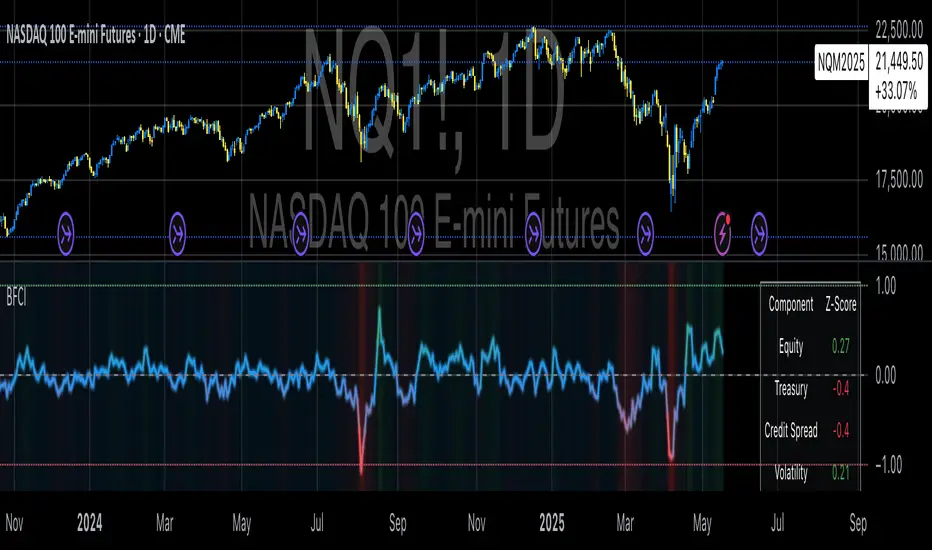

Bloomberg Financial Conditions Index (Proxy)The Bloomberg Financial Conditions Index (BFCI): A Proxy Implementation

Financial conditions indices (FCIs) have become essential tools for economists, policymakers, and market participants seeking to quantify and monitor the overall state of financial markets. Among these measures, the Bloomberg Financial Conditions Index (BFCI) has emerged as a particularly influential metric. Originally developed by Bloomberg L.P., the BFCI provides a comprehensive assessment of stress or ease in financial markets by aggregating various market-based indicators into a single, standardized value (Hatzius et al., 2010).

The original Bloomberg Financial Conditions Index synthesizes approximately 50 different financial market variables, including money market indicators, bond market spreads, equity market valuations, and volatility measures. These variables are normalized using a Z-score methodology, weighted according to their relative importance to overall financial conditions, and then aggregated to produce a composite index (Carlson et al., 2014). The resulting measure is centered around zero, with positive values indicating accommodative financial conditions and negative values representing tighter conditions relative to historical norms.

As Angelopoulou et al. (2014) note, financial conditions indices like the BFCI serve as forward-looking indicators that can signal potential economic developments before they manifest in traditional macroeconomic data. Research by Adrian et al. (2019) demonstrates that deteriorating financial conditions, as measured by indices such as the BFCI, often precede economic downturns by several months, making these indices valuable tools for predicting changes in economic activity.

Proxy Implementation Approach

The implementation presented in this Pine Script indicator represents a proxy of the original Bloomberg Financial Conditions Index, attempting to capture its essential features while acknowledging several significant constraints. Most critically, while the original BFCI incorporates approximately 50 financial variables, this proxy version utilizes only six key market components due to data accessibility limitations within the TradingView platform.

These components include:

Equity market performance (using SPY as a proxy for S&P 500)

Bond market yields (using TLT as a proxy for 20+ year Treasury yields)

Credit spreads (using the ratio between LQD and HYG as a proxy for investment-grade to high-yield spreads)

Market volatility (using VIX directly)

Short-term liquidity conditions (using SHY relative to equity prices as a proxy)

Each component is transformed into a Z-score based on log returns, weighted according to approximated importance (with weights derived from literature on financial conditions indices by Brave and Butters, 2011), and aggregated into a composite measure.

Differences from the Original BFCI

The methodology employed in this proxy differs from the original BFCI in several important ways. First, the variable selection is necessarily limited compared to Bloomberg's comprehensive approach. Second, the proxy relies on ETFs and publicly available indices rather than direct market rates and spreads used in the original. Third, the weighting scheme, while informed by academic literature, is simplified compared to Bloomberg's proprietary methodology, which may employ more sophisticated statistical techniques such as principal component analysis (Kliesen et al., 2012).

These differences mean that while the proxy BFCI captures the general direction and magnitude of financial conditions, it may not perfectly replicate the precision or sensitivity of the original index. As Aramonte et al. (2013) suggest, simplified proxies of financial conditions indices typically capture broad movements in financial conditions but may miss nuanced shifts in specific market segments that more comprehensive indices detect.

Practical Applications and Limitations

Despite these limitations, research by Arregui et al. (2018) indicates that even simplified financial conditions indices constructed from a limited set of variables can provide valuable signals about market stress and future economic activity. The proxy BFCI implemented here still offers significant insight into the relative ease or tightness of financial conditions, particularly during periods of market stress when correlations among financial variables tend to increase (Rey, 2015).

In practical applications, users should interpret this proxy BFCI as a directional indicator rather than an exact replication of Bloomberg's proprietary index. When the index moves substantially into negative territory, it suggests deteriorating financial conditions that may precede economic weakness. Conversely, strongly positive readings indicate unusually accommodative financial conditions that might support economic expansion but potentially also signal excessive risk-taking behavior in markets (López-Salido et al., 2017).

The visual implementation employs a color gradient system that enhances interpretation, with blue representing neutral conditions, green indicating accommodative conditions, and red signaling tightening conditions—a design choice informed by research on optimal data visualization in financial contexts (Few, 2009).

References

Adrian, T., Boyarchenko, N. and Giannone, D. (2019) 'Vulnerable Growth', American Economic Review, 109(4), pp. 1263-1289.

Angelopoulou, E., Balfoussia, H. and Gibson, H. (2014) 'Building a financial conditions index for the euro area and selected euro area countries: what does it tell us about the crisis?', Economic Modelling, 38, pp. 392-403.

Aramonte, S., Rosen, S. and Schindler, J. (2013) 'Assessing and Combining Financial Conditions Indexes', Finance and Economics Discussion Series, Federal Reserve Board, Washington, D.C.

Arregui, N., Elekdag, S., Gelos, G., Lafarguette, R. and Seneviratne, D. (2018) 'Can Countries Manage Their Financial Conditions Amid Globalization?', IMF Working Paper No. 18/15.

Brave, S. and Butters, R. (2011) 'Monitoring financial stability: A financial conditions index approach', Economic Perspectives, Federal Reserve Bank of Chicago, 35(1), pp. 22-43.

Carlson, M., Lewis, K. and Nelson, W. (2014) 'Using policy intervention to identify financial stress', International Journal of Finance & Economics, 19(1), pp. 59-72.

Few, S. (2009) Now You See It: Simple Visualization Techniques for Quantitative Analysis. Analytics Press, Oakland, CA.

Hatzius, J., Hooper, P., Mishkin, F., Schoenholtz, K. and Watson, M. (2010) 'Financial Conditions Indexes: A Fresh Look after the Financial Crisis', NBER Working Paper No. 16150.

Kliesen, K., Owyang, M. and Vermann, E. (2012) 'Disentangling Diverse Measures: A Survey of Financial Stress Indexes', Federal Reserve Bank of St. Louis Review, 94(5), pp. 369-397.

López-Salido, D., Stein, J. and Zakrajšek, E. (2017) 'Credit-Market Sentiment and the Business Cycle', The Quarterly Journal of Economics, 132(3), pp. 1373-1426.

Rey, H. (2015) 'Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence', NBER Working Paper No. 21162.

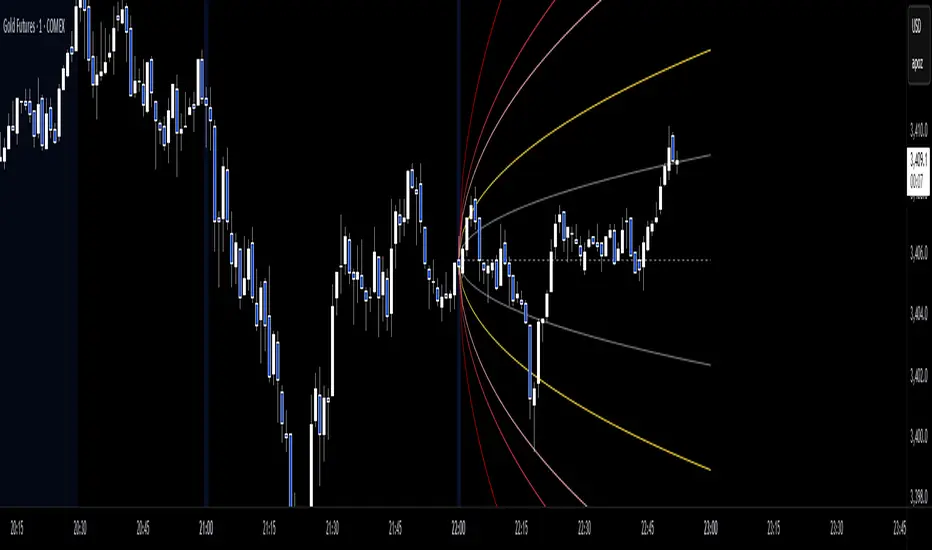

Anchored Probability Cone by TenozenFirst of all, credit to @nasu_is_gaji for the open source code of Log-Normal Price Forecast! He teaches me alot on how to use polylines and inverse normal distribution from his indicator, so check it out!

What is this indicator all about?

This indicator draws a probability cone that visualizes possible future price ranges with varying levels of statistical confidence using Inverse Normal Distribution , anchored to the start of a selected timeframe (4h, W, M, etc.)

Feutures:

Anchored Cone: Forecasts begin at the first bar of each chosen higher timeframe, offering a consistent point for analysis.

Drift & Volatility-Based Forecast: Uses log returns to estimate market volatility (smoothed using VWMA) and incorporates a trend angle that users can set manually.

Probabilistic Price Bands: Displays price ranges with 5 customizable confidence levels (e.g., 30%, 68%, 87%, 99%, 99,9%).

Dynamic Updating: Recalculates and redraws the cone at the start of each new anchor period.

How to use:

Choose the Anchored Timeframe (PineScript only be able to forecast 500 bars in the future, so if it doesn't plot, try adjusting to a lower anchored period).

You can set the Model Length, 100 sample is the default. The higher the sample size, the higher the bias towards the overall volatility. So better set the sample size in a balanced manner.

If the market is inside the 30% conifidence zone (gray color), most likely the market is sideways. If it's outside the 30% confidence zone, that means it would tend to trend and reach the other probability levels.

Always follow the trend, don't ever try to trade mean reversions if you don't know what you're doing, as mean reversion trades are riskier.

That's all guys! I hope this indicator helps! If there's any suggestions, I'm open for it! Thanks and goodluck on your trading journey!

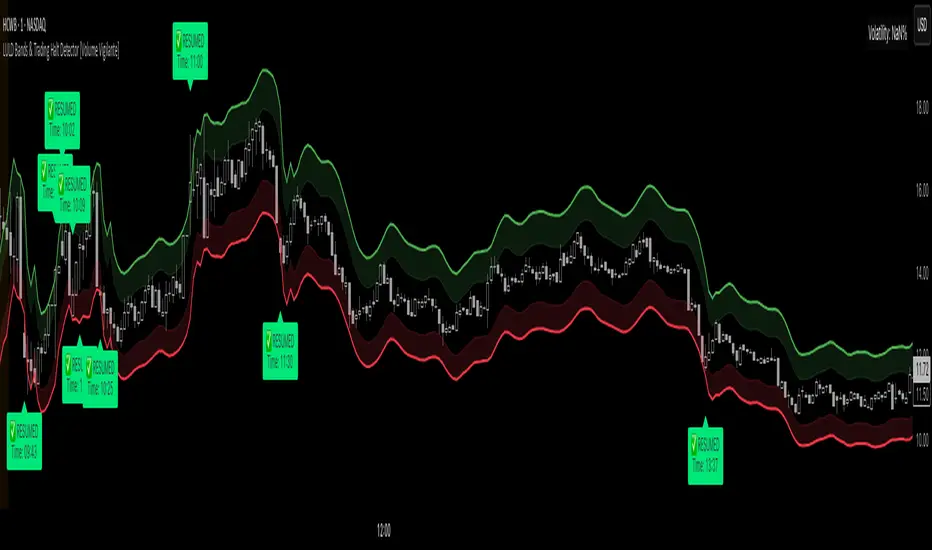

LULD Bands & Trading Halt Detector [Volume Vigilante]📖 LULD Bands & Trading Halt Detector

This advanced tool visualizes official Limit Up / Limit Down (LULD) price bands and detects regulatory trading halts and resumptions based on SEC and NASDAQ rules. It is engineered for high accuracy by anchoring all calculations to the 1-minute timeframe, ensuring reliable signals across any chart resolution.

📌 What Does This Script Do?

- Draws real-time LULD price band estimations and optional buffer (caution) zones directly on the chart.

- Detects trading halt resumptions by monitoring time gaps between candles and other regulatory criteria. (Note: Due to Pine Script limitations, halts cannot be detected in real-time, only resumptions after they occur.)

- Triggers real-time alerts for:

- Trading Resumptions (Limit Up & Limit Down)

- LULD Zone Entries (Caution Zone)

- Band Breaches (Limit Up and Limit Down)

- Plots historical halt resumption markers to analyse past events.

📐 How It Works:

- Implements official SEC/NASDAQ LULD rules for Tier 1 and Tier 2 securities.

- Applies special band adjustments for the final 25 minutes of trading (after 3:35 PM ET).

- Anchors all logic to the 1-minute timeframe for precise calculations, even on higher timeframe charts.

- Includes adjustable volume and volatility filters to eliminate false signals (ghost halts) on low-- liquidity assets, especially Tier 2 securities when TradingView fails to print candles.

⚙️ How to Use It:

1.) Apply the script to any asset or timeframe.

2.) Adjust Volume and Volatility Filters to reduce noise. (Recommended: 500,000+ volume, 10%+ volatility.)

3.) Enable or disable visual components like bands, buffer zones, and halt resumption labels.

4.) Configure alerts directly from the script settings panel.

5.) Apply alerts to individual assets via "Add Alert On..." or to entire watchlists using "Add Alert on the List."

🧩 What Makes This Script Unique?

- True 1-Minute Anchored Calculations: Ensures alerts and visuals match official trading halt criteria regardless of chart timeframe.

- Customisable Buffered Zones: Visualise proximity to regulatory price limits and avoid volatility traps.

- Combines halt resumption detection, limit up/down band visualisation, and real-time alerts into one clean, modular tool.

📚 Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Use at your own discretion and consult a licensed financial advisor before making trading decisions based on it.

Official Resources:

- NASDAQ LULD Regulations (FAQ):

www.nasdaqtrader.com

Current Nasdaq Trading Halts:

www.nasdaqtrader.com

Divergence Macro Sentiment Indicator (DMSI)The Divergence Macro Sentiment Indicator (DMSI)

Think of DMSI as your daily “mood ring” for the markets. It boils down the tug-of-war between growth assets (S&P 500, copper, oil) and safe havens (gold, VIX) into one clear histogram—so you instantly know if the bulls have broad backing or are charging ahead with one foot tied behind.

🔍 What You’re Seeing

Green bars (above zero): Risk-on conviction.

Equities and commodities are rallying while gold and volatility retreat.

Red bars (below zero): Risk-off caution.

Gold or VIX are climbing even as stocks rise—or stocks aren’t fully joined by oil/copper.

Zero line: The line in the sand between “full-steam ahead” and “proceed with care.”

📈 How to Read It

Cross-Zero Signals

Bullish trigger: DMSI flips up through zero after a red stretch → fresh long entries.

Bearish trigger: DMSI tumbles below zero from green territory → tighten stops or go defensive.

Divergence Warnings

If SPX makes new highs but DMSI is rolling over (lower green bars or red), that’s your early red flag—rallies may fizzle.

Strength Confirmation

On pullbacks, only buy dips when DMSI ≥ 0. When DMSI is deeply positive, you can be more aggressive on position size or add leverage.

💡 Trade Guidance & Use Cases

Trend Filter: Only take your S&P or sector-ETF long setups when DMSI is non-negative—avoids hollow rallies.

Macro Pair Trades:

Deep red DMSI: go long gold or gold miners (GLD, GDX).

Strong green DMSI: lean into cyclicals, industrials, even energy names.

Risk Management:

Scale out as DMSI fades into negative territory mid-trade.

Scale in or add to winners when it stays bullish.

Swing Confirmation: Overlay on any oscillator or price-pattern system—accept signals only when the macro tide is flowing in your favour.

🚀 Why It Works

Markets don’t move in a vacuum. When stocks rally but the “real-economy” metals and volatility aren’t cooperating, something’s off under the hood. DMSI catches those cross-asset cracks before price alone can—and gives you an early warning system for smarter entries, tighter risk, and bigger gains when the macro trend really kicks in.

CAN INDICATORCAN Moving Averages Indicator - Feature Guide

1. Multiple Moving Averages (20 MAs)

- Supports up to 20 individual moving averages

- Each MA can be independently configured:

- Enable/Disable toggle

- Length (period) setting

- Type selection (SMA, EMA, DEMA, VWMA, RMA, WMA)

- Color customization

- Individual timeframe settings when global timeframe is disabled

Pre-configured MA Settings:

1. MA1-8: SMA type

- Lengths: 20, 50, 100, 200, 365, 489, 600, 1460

2. MA9-20: EMA type

- Lengths: 30, 60, 120, 240, 300, 400, 500, 700, 800, 900, 1000, 2000

2. Global Timeframe Settings

Location: Global Settings group

Features:

- Use Global Timeframe: Toggle to use one timeframe for all MAs

- Global Timeframe: Select the timeframe to apply globally

3. Label Display Options

Location: Main Inputs section

Controls:

- Show MA Type: Display MA type (SMA, EMA, etc.)

- Show MA Length: Display period length

- Show Resolution: Display timeframe

- Label Offset: Adjust label position

4. Cross Alerts System

Location: Cross Alerts group

Features:

1. Price Crosses:

- Alerts when price crosses any selected MA

- Select MA to monitor (1-20)

- Triggers on crossover/crossunder

2. MA Crosses:

- Alerts when one MA crosses another

- Select fast MA (1-20)

- Select slow MA (1-20)

- Triggers on crossover/crossunder

5. Relative Strength (RS) Analysis

Location: Relative Strength group

Features:

- Select any MA to monitor (1-20)

- Compares MA to its own average

- Adjustable RS Length (default 14)

- Visual feedback via background color:

- Green: MA above its average (uptrend)

- Red: MA below its average (downtrend)

- Customizable colors and transparency

6. Moving Average Types Available

1. **SMA** (Simple Moving Average)

- Equal weight to all prices

2. **EMA** (Exponential Moving Average)

- More weight to recent prices

3. **DEMA** (Double Exponential Moving Average)

- Reduced lag compared to EMA

4. **VWMA** (Volume Weighted Moving Average)

- Incorporates volume data

5. **RMA** (Running Moving Average)

- Smoother than EMA

6. **WMA** (Weighted Moving Average)

- Linear weight distribution

Usage Tips

1. **For Trend Following:**

- Enable longer-period MAs (MA4-MA8)

- Use cross alerts between long-term MAs

- Monitor RS for trend strength

2. **For Short-term Trading:**

- Focus on shorter-period MAs (MA1-MA3, MA9-MA11)

- Enable price cross alerts

- Use multiple timeframe analysis

3. **For Multiple Timeframe Analysis:**

- Disable global timeframe

- Set different timeframes for each MA

- Compare MA relationships across timeframes

4. **For Performance:**

- Disable unused MAs

- Limit active alerts to necessary pairs

- Use RS selectively on key MAs

ETH to RTH Gap DetectorETH to RTH Gap Detector

What It Does

This indicator identifies and tracks custom-defined gaps that form between Extended Trading Hours (ETH) and Regular Trading Hours (RTH). Unlike traditional gap definitions, this indicator uses a specialized approach - defining up gaps as the space between previous session close high to current session initial balance low, and down gaps as the space from previous session close low to current session initial balance high. Each detected gap is monitored until it's touched by price.

Key Features

Detects custom-defined ETH-RTH gaps based on previous session close and current session initial balance

Automatically identifies both up gaps and down gaps

Visualizes gaps with color-coded boxes that extend until touched

Tracks when gaps are filled (when price touches the gap area)

Offers multiple display options for filled gaps (color change, border only, pattern, or delete)

Provides comprehensive statistics including total gaps, up/down ratio, and touched gap percentage

Includes customizable alert system for real-time gap filling notifications

Features toggle options for dashboard visibility and weekend sessions

Uses time-based box coordinates to avoid common TradingView drawing limitations

How To Use It

Configure Session Times : Set your preferred RTH hours and timezone (default 9:30-16:00 America/New York)

Set Initial Balance Period : Adjust the initial balance period (default 30 minutes) for gap detection sensitivity

Monitor Gap Formation : The indicator automatically detects gaps between the previous session close and current session IB

Watch For Gap Fills : Gaps change appearance or disappear when price touches them, based on your selected style

Check Statistics : View the dashboard to see total gaps, directional distribution, and touched percentage

Set Alerts : Enable alerts to receive notifications when gaps are filled

Settings Guide

RTH Settings : Configure the start/end times and timezone for Regular Trading Hours

Initial Balance Period : Controls how many minutes after market open to calculate the initial balance (1-240 minutes)

Display Settings : Toggle gap boxes, extension behavior, and dashboard visibility

Filled Box Style : Choose how filled gaps appear - Filled (color change), Border Only, Pattern, or Delete

Color Settings : Customize colors for up gaps, down gaps, and filled gaps

Alert Settings : Control when and how alerts are triggered for gap fills

Weekend Session Toggle : Option to include or exclude weekend trading sessions

Technical Details

The indicator uses time-based coordinates (xloc.bar_time) to prevent "bar index too far" errors

Gap boxes are intelligently limited to avoid TradingView's 500-bar drawing limitation

Box creation and fill detection use proper range intersection logic for accuracy

Session detection is handled using TradingView's session string format for reliability

Initial balance detection is precisely calculated based on time difference

Statistics calculations exclude zero-division scenarios for stability