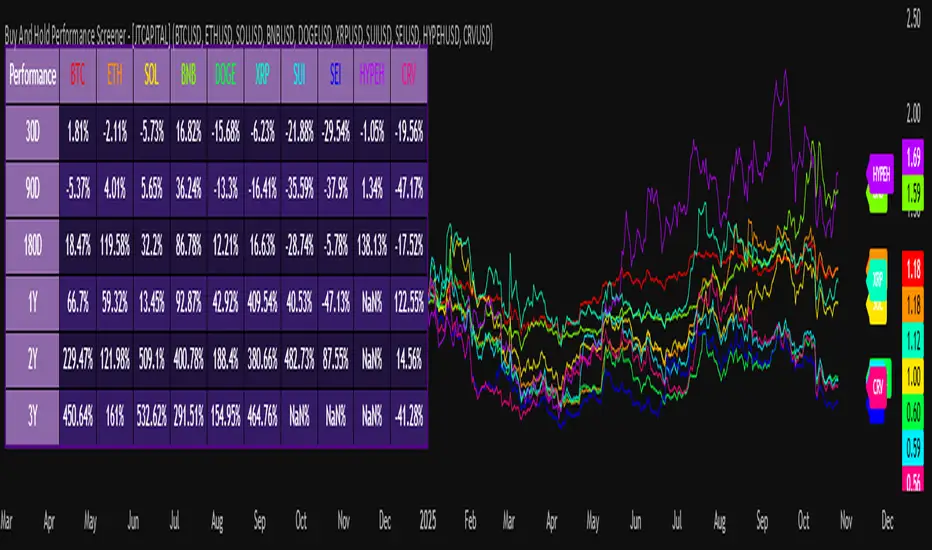

Buy And Hold Performance Screener - [JTCAPITAL]Buy And Hold Performance Screener – is a script designed to track and display multi-asset “buy and hold” performance curves and performance statistics over defined timeframes for selected symbols. It doesn’t attempt to time entries or exits; rather, it shows what would happen if one simply bought the asset at the defined start date and held it.

The indicator works by calculating in the following steps:

Start Date Definition

The script begins by reading an input for the start date. This defines the bar from which the equity curves begin.

Symbol Definitions & Close Price Retrieval

The script allows the user to specify up to ten tickers. For each ticker it uses request.security() on the “1D” timeframe to retrieve the daily close price of that symbol.

Plot Enable Inputs

For each ticker there is an input boolean controlling whether the equity curve for that ticker should be plotted.

Asset Name Cleaning

The helper function clean_name(string asset) => … takes the asset string (e.g., “CRYPTO:SOLUSD”) and manipulates it (via string splitting and replacements) to derive a cleaned short name (e.g., “SOL”). This name is used for visuals (labels, table headers).

Equity Curve Calculation (“HODL”)

The helper function f_HODL(closez) defines a variable equity that assumes a starting equity of 1 unit at the start date and then multiplies by the ratio of each bar’s close to the prior bar’s close: i.e. daily compounding of returns.

Performance Metrics Calculation

The helper function f_performance(closez) calculates, for each symbol’s close series, the percentage change of the current close relative to its close 30 days ago, 90 days ago, 180 days ago, 1 year ago (365 days), 2 years ago (730 days) and 3 years ago (1095 days).

Equity Curve Plots

For each ticker, if the corresponding plot input is true, the script assigns a plotted variable equal to the equity curve value. Its then drawing each selected equity curve on the chart, each in a distinct color.

Table Construction

If the plottable input is true, the script constructs a table and populates it with rows and column corresponding to the assigned tickers and the set 6 timeframes used for display.

Buy and Sell Conditions:

Since this is strictly a “buy-and-hold” performance screener, there are no explicit buy or sell signals generated or plotted. The script assumes: buy at the defined start_date, hold continuously to present. There are no filters, no exit logic, no take-profit or stop-loss. The benefit of this approach is to provide a clean benchmark of how selected assets would have performed if one simply adopted a passive “buy & hold” approach from a given start date.

Features and Parameters:

start_date (input.time) : Defines the date from which performance and equity curves begin.

ticker1 … ticker10 (input.symbol) : User-selectable asset symbols to include in the screener.

plot1 … plot10 (input.bool) : Boolean flags to enable/disable plotting of each asset’s equity curve.

plottable (input.bool) : Flag to enable/disable drawing the performance table.

Colored plotting + Labels for identifying each asset curve on the chart.

Specifications:

Here is a detailed breakdown of every calculation/variable/function used in the script and what each part means:

start_date

This is defined via input.time(timestamp("1 Jan 2025"), title = "Start Date"). It allows the user to pick a specific calendar date from which the equity curves and performance calculations will start.

ticker1 … ticker10

These inputs allow the user to select up to ten different assets (symbols) to monitor. The script uses each of these to fetch daily close prices.

plot1 … plot10

Boolean inputs controlling which of the ten asset equity curves are plotted. If plotX is true, the equity curve for ticker X will be visible; otherwise it will be not plotted. This gives the user flexibility to include or exclude specific assets on the chart.

Returns the cleaned asset short name.

This provides friendly text labels like “BTC”, “ETH”, “SOL”, etc., instead of full symbol codes.

The choice of distinct colours for each asset helps differentiate curves visually when multiple assets are overlaid.

Colour definitions

Variables color1…color10 are explicitly defined via color.rgb(r,g,b) to give each asset a unique colour (e.g., red, orange, yellow, green, cyan, blue, purple, pink, etc.).

What are the benefits of combining these calculations?

By computing equity curves for multiple assets from the same start date and overlaying them, you can visualise comparative performance of different assets under a uniform “buy & hold” assumption.

The performance table adds multi-horizon returns (30 D, 90 D, 180 D, 1 Y, 2 Y, 3 Y) which helps the user see both short-term and longer-term performance without having to manually compute returns.

The use of daily close data via request.security(..., "1D") removes dependency on the chart’s timeframe, thereby standardising the comparison across assets.

The equity curve and table together provide both visual (curve) and numerical (table) summaries of performance, making it easier to spot trends, divergences, and cross-asset comparisons at a glance.

Because it uses compounding (equity := equity * (closez / closez )), the curves reflect the real growth of a 1-unit investment held over time, rather than only simple returns.

The labelling of curves and the color-coding make the multi-asset overlay easier to interpret.

Using a clean start date ensures that all curves begin at the same point (1 unit at start_date), making relative performance intuitive.

Because of this, the script is useful as a benchmarking tool: rather than trying to pick entries or exit points, you can simply compare “what if I had held these assets since Jan 1 2025” (or your chosen date), and see which assets out-/under-performed in that period. It helps an investor or trader evaluate the long-term benefits of passive vs. active management, or of allocation decisions.

Please note:

The script assumes continuous daily data and does not account for dividends, fees, slippage, or tax implications.

It does not attempt to optimise timing or provide trading signals.

Returns prior to the start date are ignored (equity only begins once time >= start_date).

For newly listed assets with fewer than 365 or 730 or 1095 days of history, the longer-horizon returns may return na or misleading values.

Because it uses request.security() without specifying lookahead, and on “1D” timeframe, it complies with standard usage but you should verify there is no look-ahead bias in your particular setup.

ENJOY!

Cerca negli script per "文华财经tick价格"

Outside Candle Session Breakout [CHE]Outside Candle Session Breakout

Session - anchored HTF levels for clear market-structure and precise breakout context

Summary

This indicator is a relevant market-structure tool. It anchors the session to the first higher-timeframe bar, then activates only when the second bar forms an outside condition. Price frequently reacts around these anchors, which provides precise breakout context and a clear overview on both lower and higher timeframes. Robustness comes from close-based validation, an adaptive volatility and tick buffer, first-touch enforcement, optional retest, one-signal-per-session, cooldown, and an optional trend filter.

Pine version: v6. Overlay: true.

Motivation: Why this design?

Short-term breakout tools often trigger during noise, duplicate within the same session, or drift when volatility shifts. The core idea is to gate signals behind a meaningful structure event: a first-bar anchor and a subsequent outside bar on the session timeframe. This narrows attention to structurally important breaks while adaptive buffering and debouncing reduce false or mid-run triggers.

What’s different vs. standard approaches?

Baseline: Simple high-low breaks or fixed buffers without session context.

Architecture: Session-anchored first-bar high/low; outside-bar gate; close-based confirmation with an adaptive ATR and tick buffer; first-touch enforcement; optional retest window; one-signal-per-session and cooldown; optional EMA trend and slope filter; higher-timeframe aggregation with lookahead disabled; themeable visuals and a range fill between levels.

Practical effect: Cleaner timing at structurally relevant levels, fewer redundant or late triggers, and better multi-timeframe situational awareness.

How it works (technical)

The chart timeframe is mapped to an analysis timeframe and a session timeframe.

The first session bar defines the anchor high and low. The setup becomes active only after the next bar forms an outside range relative to that first bar.

While active, the script tracks these anchors and checks for a breakout beyond a buffered threshold, using closing prices or wicks by preference.

The buffer scales with volatility and is limited by a minimum tick floor. First-touch enforcement avoids mid-run confirmations.

Optional retest requires a pullback to the raw anchor followed by a new close beyond the buffered level within a user window.

Optional trend gating uses an EMA on the analysis timeframe, including an optional slope requirement and price-location check.

Higher-timeframe data is requested with lookahead disabled. Values can update during a forming higher-timeframe bar; waiting and confirmation mitigate timing shifts.

Parameter Guide

Enable Long / Enable Short — Direction toggles. Default: true / true. Reduces unwanted side.

Wait Candles — Minimum bars after outside confirmation before entries. Default: five. More waiting increases stability.

Close-based Breakout — Confirm on candle close beyond buffer. Default: true. For wick sensitivity, disable.

ATR Buffer — Enables adaptive volatility buffer. Default: true.

ATR Multiplier — Buffer scaling. Default: zero point two. Increase to reduce noise.

Ticks Buffer — Minimum buffer in ticks. Default: two. Protects in quiet markets.

Cooldown Bars — Blocks new signals after a trigger. Default: three.

One Signal per Session — Prevents duplicates within a session. Default: true.

Require Retest — Pullback to raw anchor before confirming. Default: false.

Retest Window — Bars allowed for retest completion. Default: five.

HTF Trend Filter — EMA-based gating. Default: false.

EMA Length — EMA period. Default: two hundred.

Slope — Require EMA slope direction. Default: true.

Price Above/Below EMA — Require price location relative to EMA. Default: true.

Show Levels / Highlight Session / Show Signals — Visual controls. Default: true.

Color Theme — “Blue-Green” (default), “Monochrome”, “Earth Tones”, “Classic”, “Dark”.

Time Period Box — Visibility, size, position, and colors for the info box. (Optional)

Reading & Interpretation

The two level lines represent the session’s first-bar high and low. The filled band illustrates the active session range.

“OUT” marks that the outside condition is confirmed and the setup is live.

“LONG” or “SHORT” appears only when the breakout clears buffer, debounce, and optional gates.

Background tint indicates sessions where the setup is valid.

Alerts fire on confirmed long or short breakout events.

Practical Workflows & Combinations

Trend-following: Keep close-based validation, ATR buffer near the default, one-signal-per-session enabled; add EMA trend and slope for directional bias.

Retest confirmation: Enable retest with a short window to prioritize cleaner continuation after a pullback.

Lower-timeframe scalping: Reduce waiting and cooldown slightly; keep a small tick buffer to filter micro-whips.

Swing and position context: Increase ATR multiplier and waiting; maintain once-per-session to limit duplicates.

Timeframe Tiers and Trader Profiles

The script adapts its internal mapping based on the chart timeframe:

Under fifteen minutes → Analysis: one minute; Session: sixty minutes. Useful for scalpers and high-frequency intraday reads.

Between fifteen and under sixty minutes → Analysis: fifteen minutes; Session: one day. Suits day traders who need intraday alignment to the daily session.

Between sixty minutes and under one day → Analysis: sixty minutes; Session: one week. Serves intraday-to-swing transitions and end-of-day planning.

Between one day and under one week → Analysis: two hundred forty minutes; Session: two weeks. Fits swing traders who monitor multi-day structure.

Between one week and under thirty days → Analysis: one day; Session: three months. Supports position traders seeking quarterly context.

Thirty days and above → Analysis: one day; Session: twelve months. Provides a broad annual anchor for macro context.

These tiers are designed to keep anchors meaningful across regimes while preserving responsiveness appropriate to the trader profile.

Behavior, Constraints & Performance

Signals can be validated on closed bars through close-based logic; enabling this reduces intrabar flicker.

Higher-timeframe values may evolve during a forming bar; waiting parameters and the outside-bar gate reduce, but do not remove, this effect.

Resource footprint is light; the script uses standard indicators and a single higher-timeframe request per stream.

Known limits: rare setups during very quiet periods, sensitivity to gaps, and reduced reliability on illiquid symbols.

Sensible Defaults & Quick Tuning

Start with close-based validation on, ATR buffer on with a multiplier near zero point two, tick buffer two, cooldown three, once-per-session on.

Too many flips: increase the ATR multiplier and cooldown; consider enabling the EMA filter and slope.

Too sluggish: reduce the ATR multiplier and waiting; disable retest.

Choppy conditions: keep close-based validation, increase tick buffer, shorten the retest window.

What this indicator is—and isn’t

This is a visualization and signal layer for session-anchored breakouts with stability gates. It is not a complete trading system, risk framework, or predictive engine. Combine it with structured analysis, position sizing, and disciplined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Free Stock ScreenerMissing great trade opportunities is annoying, and unless you have 12 screens or only trade one market, you are missing a lot of trades. To fix that, we created this free stock screener so you get notified instantly of potential great trading conditions in real time, right on your chart.

You get notified of trading benchmarks being met by the value being displayed on the scanner as well as a color change so that it grabs your attention and makes you aware that you should take a look at the other market and look for a potential trade. It also has built in alerts so you can have an alert notification go off when any of your trading conditions are met instead of needing to watch the scanner for color changes.

The screener will change the ticker symbol background color to red green when price is above or below the previous daily range and above or below both VWAPs. This signals that the ticker is trending, which typically means it is a great time to trade that market and follow the trend.

This free stock screener allows you to scan up to 10 different markets at the same time for various different conditions so you always know what is going on with your favorite trading symbols. If you want to scan more tickers, just add the indicator to your chart again and change the table position to the other side of the screen and update the tickers on the 2nd screener, allowing you to have 20 tickers at a time.

The scanner can be fully customized by changing the markets that it screens and turning on or off as many of them as you would like. You can also turn on or off any of the different data sets so that you only get information about trading conditions that matter to you.

The screener can provide data on any type of market, such as stocks, crypto, futures, forex and more. Each ticker can be adjusted to whatever market you would like it to scan for data in the settings panel, the only limitation is that it will not provide data for the VWAP and volume trend score if the ticker you are screening does not provide volume data.

Screener Features

The scanner will provide the following types of data for each ticker that is turned on:

Volume - Provides a volume score compared to the average volume and notifies you of higher than normal volume and volume spikes on individual bars by changing colors.

Volatility - Provides a volatility score compared to the average volatility and notifies you of higher than normal volatility by changing colors.

Oscillator - Choose between the RSI or CCI. The value of that oscillator will be displayed and will notify you when values are in extreme ranges such as overbought or oversold conditions according to the threshold values you enter in the settings panel. When those thresholds have been breached, you will be notified by it changing color.

Big Candles - Compares the current candle to average previous candle sizes, and changes color to notify you of big candles including a big top wick, big bottom wick, big candle body and big candle high to low range.

Daily Level Touches & Trends - Calculates and displays various daily candle and intraday open price levels that act as support and resistance. Notifies you when price is touching any of the daily levels that are turned on. The levels you can have on are as follows: previous day high, previous day low or previous day open. It also will notify you when price is touching the current day’s open, NY 930am open, Asia 8pm open, London 2am open and NY midnight 12am open. It will also say “Above” if price is above the previous day’s high or it will say “Below” if price is below the previous day’s low. The color of the cell will also change when a level touch is happening or price is above the previous day high or below the previous day low.

VWAP - Choose from 2 different VWAP lengths, default settings are daily and weekly VWAPs. You will get notified if price touches either of the VWAPs and they will also say “Above” or “Below” if price is currently above or below each VWAP.

How To Use The Screener To Help You Trade

The main purpose of the screener is to scan other markets and notify you of potential good trading opportunities such as price bouncing off of the daily levels or VWAPs. It can also be used to know when price is trending according to the VWAPs and daily levels. Lastly, you can use it to know how the volume and volatility trends are currently which gives you more confidence in taking a trade with this data when volume and volatility are present.

Volume Score

When volume is high, this represents a good time to trade because there are many market participants and price is likely to be volatile while there is high volume which can present a lot of good trade setups for you to take.

The volume score shown on the screener measures the current volume trend compared to previous volume trends and calculates that into a score based on 100 being the same as the previous volume trend. So any value above 100 means it is high volume and any value less than 100 means it is lower volume than normal.

In the settings panel, you can adjust the volume threshold that needs to be met for a volume notification to show up. The default setting is at 120, so you will get notified when the current volume trend score is 120 or higher or you can adjust that threshold value to whatever value you prefer.

It also will notify you when there is a volume spike on the current bar. This is determined by calculating an average of the recent volume totals and then checking to see if the current bar is greater than or equal to that average multiplied by 3. So if a single bar has volume that is greater than 3 times what the average volume is, then you will get a notification that says “Spike” to make you aware of that volume spike.

The volume trend threshold, volume spike multiplier and lookback length for the average volume used in volume spike calculations can all be adjusted in the settings panel to fit your desired preferences.

Volatility Score

High volatility can mean it is a great time to trade because the market is moving quickly and providing large enough movements that you can get in and out in a short amount of time, while still accruing decent sized trade PnL.

The volatility score will calculate the current volatility for each market compared to previous conditions and then divide the current volatility by the average volatility to give you a volatility score. Anything over 100 means the market is decently volatile and you should look at that market to find potential trade setups to execute on. Anything below 100 means the market is not very volatile and it is usually best to just wait until volatility returns before you start trading again.

The screener will notify you when the volatility score is above the threshold you set. The default value is set to 90, but can be adjusted to your preference. Pay attention to any market that shows an alert and take a look at that chart because the high volatility may present a good trade setup for you in the near future.

Oscillator Score

The oscillator data can be switched between Relative Strength Index(RSI) and Commodity Channel Index(CCI).

The RSI provides a value between 0 and 100 that indicates the momentum and strength of the recent price action. Many traders use the extremes of the 0-100 range to signal overbought or oversold conditions and use that as a sign to look for price to reverse in the near future. The typical values used for this and the default settings to provide notifications are: 70 for overbought and 30 for oversold. The scanner will notify you when the RSI value is considered overbought or oversold so you know to take a look at the chart and analyze if it is ready for a trade to be taken.

The CCI provides a value that can be used to determine the trend strength of the underlying asset when the oscillator moves above 100 or below -100. These extreme values are outside of the normal accumulation range and signify that price is moving strongly in that direction so it may be a good time to take a trade in the direction of the trend. The scanner will show you the value of the CCI for each market and notify you if that value is above 100 or below -100.

Both RSI and CCI settings can be adjusted in the settings panel to your desired settings so you have the exact oscillator settings you prefer to use as well as the exact values that you want to use for being notified.

Big Candles

Big candles can mean that many traders are buying or selling at the same time and many times indicate a good signal to trade in that same direction. That is why we included this calculation in the screener, so you are always aware when a large candle prints.

It calculates the average size of the recent candles and then uses that average as the benchmark to determine if the current candle is considered big and worthy of notifying you to take a look at that chart.

You can adjust the multiplier used for the big candle threshold to whatever you desire, but the default setting is 3 which means the candle will be considered big and notify you if it is 3 times as large as an average candle.

The big candles data will track the following candle values and notify you with these labels:

High to Low candle size = HL

Candle Body from open to close candle size = OC

Top Wick size = TW

Bottom Wick size = BW

Daily Level Touches & Trend

Daily level touches are excellent levels to watch for price to bounce because they often act as support and resistance levels for intraday trading. The scanner will track each market and notify you when the current candle is touching any of the daily levels that you have turned on in the settings panel.

The main levels that are turned on by default and are useful for all markets and how they will be labeled on the scanner are as follows:

Previous Day High = High

Previous Day Low = Low

Previous Day Open = < Open

Previous Day Close = Close

Current Day Open = Open

We also included some extra levels that are useful for futures traders. They are as follows:

NY 930am Open = 930am

NY 12am Midnight Open = 12am

Asia Open at 8pm NY time = Asia

London Open at 2am NY Time = London

Watch how price reacts to these levels and then trade the bounces off of these levels if the price action confirms that it is going to respect that level.

When price is currently above the previous day high, the scanner will say “Above” and show a green color, indicating a bullish trend and that price is above the previous daily candle’s high.

When price is currently below the previous day low, the scanner will say “Below” and show a red color, indicating a bearish trend and that price is below the previous daily candle’s low.

Pay attention to when price is trending above or below the previous daily candle as those trends can provide excellent trend trading opportunities.

The daily levels that you have turned on in the settings will also show as lines on the chart and include a label next to them, identifying each level so you know what each line represents. You can turn on or off all of the lines shown on the chart in the main settings or turn them off one by one in the style panel of the settings. Labels can also be turned on or off for all of the lines in the main settings panel. You can adjust the label positioning in the Label Offset section of the settings panel.

VWAP Touches & Trend

VWAP stands for volume weighted average price and is a very popular tool that traders use to determine trend direction based on volume as well as an excellent level to trade price bounces off of.

The typical VWAP time period used is Daily, which means the volume weighted average price will reset at the beginning of a new day. We set the first VWAP to be the daily VWAP by default and the second one to be the weekly VWAP. You can adjust both of the time periods to be any of the provided time lengths that you choose.

The screener will show “Above” with a green background color when price is above the VWAP, indicating a bullish trend. It will show “Below” with a red background color when price is below the VWAP, indicating a bearish trend. When both VWAPs are showing Above or Below, you can expect price to trend in that direction, so look for pullbacks you can trade in the direction of the trend. If the VWAPs are showing different directions, then you should expect to bounce back and forth between the VWAPs, but be careful and watch out for price to break beyond either one and start a trend.

When the current candle is touching the VWAP, the scanner will change colors and say VWAP to notify you that price is touching the VWAP and you should look at that chart and analyze the market for a potential bounce off of the VWAP to trade.

Trending Market Signals

Strong trends are excellent markets to trade and can many times provide excellent trading opportunities that don’t require expert price action reading skills to be able to take winning trades from. That is why we included a signal to notify you of a strong trending market.

The strong trending market will show up as a green or red background color for the ticker name. If the color of the ticker name is green, it is notifying you that the price is above the previous daily high, above VWAP 1 and above VWAP 2 and is a good market to look for bullish trend trades. If the color of the ticker name is red, it is notifying you that the price is below the previous daily low, below VWAP 1 and below VWAP 2 and is a good market to look for bearish trend trades.

Changing The Tickers It Scans

To change the tickers that the indicator scans, scroll near the bottom of the settings panel and select the ticker symbol you want to update and then search for the exact symbol you want to use. If you want to scan less tickers, then just turn some of the tickers off that you don’t need.

Scanning More Than 10 Tickers

If you want to scan more than 10 tickers, you can add the scanner to your chart again and then just change the table position to the other side of the screen. This will allow you to scan 10 more tickers that will show up separately. Then if you want even more, just add the indicator to your chart again and update the table position until you have as many markets as you want. The table position setting can be found at the bottom of the main settings panel.

Alerts

The screener has alerts that can be used to notify you when any of the data set thresholds have been met or if price is touching one of the levels. You can set alerts for the following events:

Bullish Trend Alert - Price is above the previous daily high and above both VWAPs.

Bearish Trend Alert - Price is below the previous daily low and below both VWAPs.

High Volume Alert - Volume is higher than the threshold or a volume spike is detected.

High Volatility Alert - Volatility is higher than the threshold.

Oscillator Is Extended Alert - Oscillator value has exceeded the upper or lower threshold.

Big Candle Alert - A big candle has been detected.

Daily Level Touch Alert - One of the daily levels that is turned on is being touched.

VWAP Touch Alert - One of the 2 VWAPs are being touched.

An alert will trigger when any one of tickers on your scanner meets the alert conditions, so when you see the alert, you will need to go to your chart and look at the scanner to see which ticker it was and then navigate to that chart to look for potential trade setups.

The alerts will use the exact same settings you have configured in the settings panel to send you alert notifications. With normal settings, this could give you a lot of alerts, so if you only want alerts to fire when abnormal conditions are being met, try setting up a second screener on your chart that has very high threshold values and only has the most important level touches on. Then turn the setting "Do Not Show The Screener On The Chart" to off so the calculations will still run and fire alerts, but won't clog up your charts. This way you can only get alert notifications when major events happen but still have your normal screener settings available on your chart.

Markets This Can Be Used On

This screener uses the price action and volume data so you can use it to scan any type of market you would like as long as the ticker you are scanning has price and volume data feeds. If a market does not have volume data, then it will just show NaN in the volume row and the VWAP rows will not show anything.

real_time_candlesIntroduction

The Real-Time Candles Library provides comprehensive tools for creating, manipulating, and visualizing custom timeframe candles in Pine Script. Unlike standard indicators that only update at bar close, this library enables real-time visualization of price action and indicators within the current bar, offering traders unprecedented insight into market dynamics as they unfold.

This library addresses a fundamental limitation in traditional technical analysis: the inability to see how indicators evolve between bar closes. By implementing sophisticated real-time data processing techniques, traders can now observe indicator movements, divergences, and trend changes as they develop, potentially identifying trading opportunities much earlier than with conventional approaches.

Key Features

The library supports two primary candle generation approaches:

Chart-Time Candles: Generate real-time OHLC data for any variable (like RSI, MACD, etc.) while maintaining synchronization with chart bars.

Custom Timeframe (CTF) Candles: Create candles with custom time intervals or tick counts completely independent of the chart's native timeframe.

Both approaches support traditional candlestick and Heikin-Ashi visualization styles, with options for moving average overlays to smooth the data.

Configuration Requirements

For optimal performance with this library:

Set max_bars_back = 5000 in your script settings

When using CTF drawing functions, set max_lines_count = 500, max_boxes_count = 500, and max_labels_count = 500

These settings ensure that you will be able to draw correctly and will avoid any runtime errors.

Usage Examples

Basic Chart-Time Candle Visualization

// Create real-time candles for RSI

float rsi = ta.rsi(close, 14)

Candle rsi_candle = candle_series(rsi, CandleType.candlestick)

// Plot the candles using Pine's built-in function

plotcandle(rsi_candle.Open, rsi_candle.High, rsi_candle.Low, rsi_candle.Close,

"RSI Candles", rsi_candle.candle_color, rsi_candle.candle_color)

Multiple Access Patterns

The library provides three ways to access candle data, accommodating different programming styles:

// 1. Array-based access for collection operations

Candle candles = candle_array(source)

// 2. Object-oriented access for single entity manipulation

Candle candle = candle_series(source)

float value = candle.source(Source.HLC3)

// 3. Tuple-based access for functional programming styles

= candle_tuple(source)

Custom Timeframe Examples

// Create 20-second candles with EMA overlay

plot_ctf_candles(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 20,

timezone = -5,

tied_open = true,

ema_period = 9,

enable_ema = true

)

// Create tick-based candles (new candle every 15 ticks)

plot_ctf_tick_candles(

source = close,

candle_type = CandleType.heikin_ashi,

number_of_ticks = 15,

timezone = -5,

tied_open = true

)

Advanced Usage with Custom Visualization

// Get custom timeframe candles without automatic plotting

CandleCTF my_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 30

)

// Apply custom logic to the candles

float ema_values = my_candles.ctf_ema(14)

// Draw candles and EMA using time-based coordinates

my_candles.draw_ctf_candles_time()

ema_values.draw_ctf_line_time(line_color = #FF6D00)

Library Components

Data Types

Candle: Structure representing chart-time candles with OHLC, polarity, and visualization properties

CandleCTF: Extended candle structure with additional time metadata for custom timeframes

TickData: Structure for individual price updates with time deltas

Enumerations

CandleType: Specifies visualization style (candlestick or Heikin-Ashi)

Source: Defines price components for calculations (Open, High, Low, Close, HL2, etc.)

SampleType: Sets sampling method (Time-based or Tick-based)

Core Functions

get_tick(): Captures current price as a tick data point

candle_array(): Creates an array of candles from price updates

candle_series(): Provides a single candle based on latest data

candle_tuple(): Returns OHLC values as a tuple

ctf_candles_array(): Creates custom timeframe candles without rendering

Visualization Functions

source(): Extracts specific price components from candles

candle_ctf_to_float(): Converts candle data to float arrays

ctf_ema(): Calculates exponential moving averages for candle arrays

draw_ctf_candles_time(): Renders candles using time coordinates

draw_ctf_candles_index(): Renders candles using bar index coordinates

draw_ctf_line_time(): Renders lines using time coordinates

draw_ctf_line_index(): Renders lines using bar index coordinates

Technical Implementation Notes

This library leverages Pine Script's varip variables for state management, creating a sophisticated real-time data processing system. The implementation includes:

Efficient tick capturing: Samples price at every execution, maintaining temporal tracking with time deltas

Smart state management: Uses a hybrid approach with mutable updates at index 0 and historical preservation at index 1+

Temporal synchronization: Manages two time domains (chart time and custom timeframe)

The tooltip implementation provides crucial temporal context for custom timeframe visualizations, allowing users to understand exactly when each candle formed regardless of chart timeframe.

Limitations

Custom timeframe candles cannot be backtested due to Pine Script's limitations with historical tick data

Real-time visualization is only available during live chart updates

Maximum history is constrained by Pine Script's array size limits

Applications

Indicator visualization: See how RSI, MACD, or other indicators evolve in real-time

Volume analysis: Create custom volume profiles independent of chart timeframe

Scalping strategies: Identify short-term patterns with precisely defined time windows

Volatility measurement: Track price movement characteristics within bars

Custom signal generation: Create entry/exit signals based on custom timeframe patterns

Conclusion

The Real-Time Candles Library bridges the gap between traditional technical analysis (based on discrete OHLC bars) and the continuous nature of market movement. By making indicators more responsive to real-time price action, it gives traders a significant edge in timing and decision-making, particularly in fast-moving markets where waiting for bar close could mean missing important opportunities.

Whether you're building custom indicators, researching price patterns, or developing trading strategies, this library provides the foundation for sophisticated real-time analysis in Pine Script.

Implementation Details & Advanced Guide

Core Implementation Concepts

The Real-Time Candles Library implements a sophisticated event-driven architecture within Pine Script's constraints. At its heart, the library creates what's essentially a reactive programming framework handling continuous data streams.

Tick Processing System

The foundation of the library is the get_tick() function, which captures price updates as they occur:

export get_tick(series float source = close, series float na_replace = na)=>

varip float price = na

varip int series_index = -1

varip int old_time = 0

varip int new_time = na

varip float time_delta = 0

// ...

This function:

Samples the current price

Calculates time elapsed since last update

Maintains a sequential index to track updates

The resulting TickData structure serves as the fundamental building block for all candle generation.

State Management Architecture

The library employs a sophisticated state management system using varip variables, which persist across executions within the same bar. This creates a hybrid programming paradigm that's different from standard Pine Script's bar-by-bar model.

For chart-time candles, the core state transition logic is:

// Real-time update of current candle

candle_data := Candle.new(Open, High, Low, Close, polarity, series_index, candle_color)

candles.set(0, candle_data)

// When a new bar starts, preserve the previous candle

if clear_state

candles.insert(1, candle_data)

price.clear()

// Reset state for new candle

Open := Close

price.push(Open)

series_index += 1

This pattern of updating index 0 in real-time while inserting completed candles at index 1 creates an elegant solution for maintaining both current state and historical data.

Custom Timeframe Implementation

The custom timeframe system manages its own time boundaries independent of chart bars:

bool clear_state = switch settings.sample_type

SampleType.Ticks => cumulative_series_idx >= settings.number_of_ticks

SampleType.Time => cumulative_time_delta >= settings.number_of_seconds

This dual-clock system synchronizes two time domains:

Pine's execution clock (bar-by-bar processing)

The custom timeframe clock (tick or time-based)

The library carefully handles temporal discontinuities, ensuring candle formation remains accurate despite irregular tick arrival or market gaps.

Advanced Usage Techniques

1. Creating Custom Indicators with Real-Time Candles

To develop indicators that process real-time data within the current bar:

// Get real-time candles for your data

Candle rsi_candles = candle_array(ta.rsi(close, 14))

// Calculate indicator values based on candle properties

float signal = ta.ema(rsi_candles.first().source(Source.Close), 9)

// Detect patterns that occur within the bar

bool divergence = close > close and rsi_candles.first().Close < rsi_candles.get(1).Close

2. Working with Custom Timeframes and Plotting

For maximum flexibility when visualizing custom timeframe data:

// Create custom timeframe candles

CandleCTF volume_candles = ctf_candles_array(

source = volume,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 60

)

// Convert specific candle properties to float arrays

float volume_closes = volume_candles.candle_ctf_to_float(Source.Close)

// Calculate derived values

float volume_ema = volume_candles.ctf_ema(14)

// Create custom visualization

volume_candles.draw_ctf_candles_time()

volume_ema.draw_ctf_line_time(line_color = color.orange)

3. Creating Hybrid Timeframe Analysis

One powerful application is comparing indicators across multiple timeframes:

// Standard chart timeframe RSI

float chart_rsi = ta.rsi(close, 14)

// Custom 5-second timeframe RSI

CandleCTF ctf_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 5

)

float fast_rsi_array = ctf_candles.candle_ctf_to_float(Source.Close)

float fast_rsi = fast_rsi_array.first()

// Generate signals based on divergence between timeframes

bool entry_signal = chart_rsi < 30 and fast_rsi > fast_rsi_array.get(1)

Final Notes

This library represents an advanced implementation of real-time data processing within Pine Script's constraints. By creating a reactive programming framework for handling continuous data streams, it enables sophisticated analysis typically only available in dedicated trading platforms.

The design principles employed—including state management, temporal processing, and object-oriented architecture—can serve as patterns for other advanced Pine Script development beyond this specific application.

------------------------

Library "real_time_candles"

A comprehensive library for creating real-time candles with customizable timeframes and sampling methods.

Supports both chart-time and custom-time candles with options for candlestick and Heikin-Ashi visualization.

Allows for tick-based or time-based sampling with moving average overlay capabilities.

get_tick(source, na_replace)

Captures the current price as a tick data point

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

na_replace (float) : Optional - Value to use when source is na

Returns: TickData structure containing price, time since last update, and sequential index

candle_array(source, candle_type, sync_start, bullish_color, bearish_color)

Creates an array of candles based on price updates

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

sync_start (simple bool) : Optional - Whether to synchronize with the start of a new bar

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of Candle objects ordered with most recent at index 0

candle_series(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides a single candle based on the latest price data

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: A single Candle object representing the current state

candle_tuple(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides candle data as a tuple of OHLC values

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Tuple representing current candle values

method source(self, source, na_replace)

Extracts a specific price component from a Candle

Namespace types: Candle

Parameters:

self (Candle)

source (series Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

na_replace (float) : Optional - Value to use when source value is na

Returns: The requested price value from the candle

method source(self, source)

Extracts a specific price component from a CandleCTF

Namespace types: CandleCTF

Parameters:

self (CandleCTF)

source (simple Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

Returns: The requested price value from the candle as a varip

method candle_ctf_to_float(self, source)

Converts a specific price component from each CandleCTF to a float array

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

Returns: Array of float values extracted from the candles, ordered with most recent at index 0

method ctf_ema(self, ema_period)

Calculates an Exponential Moving Average for a CandleCTF array

Namespace types: array

Parameters:

self (array)

ema_period (simple float) : Period for the EMA calculation

Returns: Array of float values representing the EMA of the candle data, ordered with most recent at index 0

method draw_ctf_candles_time(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar time coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using time-based x-coordinates

method draw_ctf_candles_index(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar index coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using index-based x-coordinates

method draw_ctf_line_time(self, source, line_size, line_color)

Renders a line representing a price component from the candles using time coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_time(self, line_size, line_color)

Renders a line from a varip float array using time coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_index(self, source, line_size, line_color)

Renders a line representing a price component from the candles using index coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

method draw_ctf_line_index(self, line_size, line_color)

Renders a line from a varip float array using index coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots tick-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots tick-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots time-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots time-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_candles(source, candle_type, sample_type, number_of_ticks, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, enable_ema, line_width, ema_color, use_time_indexing)

Unified function for plotting candles with comprehensive options

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Optional - Type of candle chart to display

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

ema_period (simple float) : Optional - Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

enable_ema (bool) : Optional - Whether to display the EMA overlay

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with optional EMA overlay

ctf_candles_array(source, candle_type, sample_type, number_of_ticks, number_of_seconds, tied_open, bullish_color, bearish_color)

Creates an array of custom timeframe candles without rendering them

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to create (candlestick or Heikin-Ashi)

sample_type (simple SampleType) : Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of CandleCTF objects ordered with most recent at index 0

Candle

Structure representing a complete candle with price data and display properties

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

candle_color (series color) : Color to use when rendering the candle

ready (series bool) : Boolean indicating if candle data is valid and ready for use

TickData

Structure for storing individual price updates

Fields:

price (series float) : The price value at this tick

time_delta (series float) : Time elapsed since the previous tick in milliseconds

series_index (series int) : Sequential index identifying this tick

CandleCTF

Structure representing a custom timeframe candle with additional time metadata

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

open_time (series int) : Timestamp marking when the candle was opened (in Unix time)

time_delta (series float) : Duration of the candle in milliseconds

candle_color (series color) : Color to use when rendering the candle

Ultra Trade JournalThe Ultra Trade Journal is a powerful TradingView indicator designed to help traders meticulously document and analyze their trades. Whether you're a novice or an experienced trader, this tool offers a clear and organized way to visualize your trading strategy, monitor performance, and make informed decisions based on detailed trade metrics.

Detailed Description

The Ultra Trade Journal indicator allows users to input and visualize critical trade information directly on their TradingView charts.

.........

User Inputs

Traders can specify entry and exit prices , stop loss levels, and up to four take profit targets.

.....

Dynamic Plotting

Once the input values are set, the indicator automatically plots horizontal lines for entry, exit, stop loss, and each take profit level on the chart. These lines are visually distinct, using different colors and styles (solid, dashed, dotted) to represent each element clearly.

.....

Live Position Tracking

If enabled, the indicator can adjust the exit price in real-time based on the current market price, allowing traders to monitor live positions effectively.

.....

Tick Calculations

The script calculates the number of ticks between the entry price and each exit point (stop loss and take profits). This helps in understanding the movement required for each target and assessing the potential risk and reward.

.....

Risk-Reward Ratios

For each take profit level, the indicator computes the risk-reward (RR) ratio by comparing the ticks at each target against the stop loss ticks. This provides a quick view of the potential profitability versus the risk taken.

.....

Comprehensive Table Display

A customizable table is displayed on the chart, summarizing all key trade details. This includes the entry and exit prices, stop loss and take profit levels, tick counts, and their respective RR ratios.

Users can adjust the table's Position and text color to suit their preferences.

.....

Visual Enhancements

The indicator uses adjustable background shading between entry and stop loss/take profit lines to visually represent potential trade outcomes. This shading adjusts based on whether the trade is long or short, providing an intuitive understanding of trade performance.

.........

Overall, the Ultra Trade Journal combines visual clarity with detailed analytics, enabling traders to keep a well-organized record of their trades and enhance their trading strategies through insightful data.

US Sentiment Index [CryptoSea]The US Sentiment Index is an advanced analytical tool designed for traders seeking to uncover patterns, correlations, and potential leading signals across key market tickers. This indicator surpasses traditional sentiment measures, providing a data-driven approach that offers deeper insights compared to conventional indices like the Fear and Greed Index.

Key Features

Multi-Ticker Analysis: Integrates data from a diverse set of market indicators, including gold, S&P 500, U.S. Dollar Index, Volatility Index, and more, to create a comprehensive view of market sentiment.

Customisable Sensitivity Settings: Allows users to adjust the moving average period to fine-tune the sensitivity of sentiment calculations, adapting the tool to various market conditions and trading strategies.

Detailed Sentiment Scaling: Utilises a 0-100 scale to quantify sentiment strength, with colour gradients that visually represent bearish, neutral, and bullish conditions, aiding in quick decision-making.

Below is an example where the sentiment index can give leading signals. We see a first sign of wekaness in the index as it drops below its moving average. Shortly after we see it dip below our median 50 level, another sign of weakeness. We see the SPX price action to take a hit following the sentiment index decrease.

Tickers Used and Their Impact on Sentiment

The impact of each ticker on sentiment can be bullish or bearish, depending on their behaviour:

Gold (USGD): Typically seen as a safe-haven asset, rising gold prices often indicate increased market fear or bearish sentiment. Conversely, falling gold prices can signal reduced fear and a shift towards bullish sentiment in riskier assets.

S&P 500 (SPX): A rising S&P 500 is usually a sign of bullish sentiment, reflecting confidence in economic growth and market stability. A decline, however, suggests bearish sentiment and a potential move towards risk aversion.

U.S. Dollar Index (DXY): A strengthening U.S. Dollar can be a sign of fear as investors seek safety in the dollar, which is bearish for risk assets. A weakening dollar, on the other hand, can signal bullish sentiment as capital flows into riskier assets.

Volatility Index (VIX): Known as the "fear gauge," a rising VIX indicates increased market fear and bearish sentiment. A falling VIX suggests a calm, bullish market environment.

Junk Bonds (JNK): Rising junk bond prices often reflect bullish sentiment as investors take on more risk for higher returns. Conversely, falling junk bond prices signal increased fear and bearish sentiment.

Long-Term Treasury Bonds (TLT): Higher prices for long-term treasuries usually indicate a flight to safety, reflecting bearish sentiment. Lower prices suggest a shift towards riskier assets, indicating bullish sentiment.

Financial Sector ETF (XLF): Strength in the financial sector is typically bullish, indicating confidence in economic conditions. Weakness in this sector can reflect bearish sentiment and concerns about financial stability.

Unemployment Rate (USUR): A rising unemployment rate is a bearish signal, indicating economic weakness. A declining unemployment rate is bullish, reflecting economic strength and job growth.

U.S. Interest Rates (USINTR, USIRYY): Higher interest rates can be bearish, as they increase borrowing costs and reduce spending. Lower rates are generally bullish, promoting economic growth and risk-taking.

How it Works

Sentiment Calculation: The US Sentiment Index combines data from multiple tickers, calculating sentiment by scaling the distance from their respective moving averages. Each asset's behaviour is interpreted within the context of market fear or greed, providing a refined sentiment reading that adjusts dynamically.

Market Strength Analysis: When the index is above 50 and also above its moving average, it indicates particularly strong or bullish market conditions, driven by greed. Conversely, when the index is below 50 and under its moving average, it signals bearish or weak market conditions, associated with fear.

Correlation and Pattern Detection: The indicator analyses correlations among the included assets to detect patterns that might signal potential market movements, giving traders a leading edge over simpler sentiment measures.

Adaptive Background Colouring: Utilises a colour gradient that dynamically adjusts based on sentiment values, highlighting extreme fear, neutral, and extreme greed levels directly on the chart.

Flexible Display Options: Offers settings to toggle the moving average plot and adjust its period, giving users the ability to tailor the indicator's sensitivity and display to their specific needs.

In this example below, we can see the Sentiment rise above the Moving Average (MA). Price action goes on to follow this, although there is an instance where it dips below the MA, it quickly rises back above again as a sign of strength.

Another way you can use this index is by simply using the MA, if its trending up, we know the macro sentiment is bullish.

Application

Data-Driven Insights: Offers traders a detailed, data-driven approach to sentiment analysis, incorporating a broad spectrum of market indicators to deliver actionable insights.

Pattern Recognition: Helps identify patterns and correlations that may lead to market reversals or continuations, providing a nuanced view that goes beyond simple sentiment gauges.

Enhanced Decision-Making: Equips traders with a robust tool to validate trading strategies and make informed decisions based on comprehensive sentiment analysis.

The US Sentiment Index by is an essential addition to the toolkit of any trader looking to navigate market complexities with precision and confidence. Its advanced features and data-driven approach offer unparalleled insights into market sentiment, setting it apart from conventional sentiment indicators.

Z-Score Probability IndicatorThis is the Z-Score Probability indicator. As many people like my original Z-Score indicator and have expressed more interest in the powers of the Z, I decided to make this indicator which shows additional powers of the Z-Score.

Z-Score is not only useful for measuring a ticker or any other variable’s distance from the mean, it is also useful to calculate general probability in a normal distribution set. Not only can it calculate probability in a dataset, but it can also calculate the variables within said dataset by using the Standard Deviation and the Mean of the dataset.

Using these 2 aspects of the Z-Score, you can, In principle, have an indicator that operates similar to Fibonacci retracement levels with the added bonus of being able to actually ascertain the realistic probability of said retracement.

Let’s take a look at an example:

This is a chart showing SPY on the daily timeframe. If we look at the current Z-Score level, we can see that SPY is pushing into the 2 to 3 Z-Score range. We can see two things from this:

1. We can see that a retracement to a Z-Score of 2 would correspond to a price of 425.26 based on the current dataset. And

2. We can see that the probability that SPY retraces to a Z-Score of 2 is around 0.9800 or 98%.

To take it one step further, we can look at the various other variables in the distribution. If we were to bet on SPY retracing back to -1 SDs, that would correspond to a price of around 397.15, with a probability of around 0.1600 or 16% (see image below):

Let’s say, we thought SPY would go to $440. Well, we can see that the probability SPY goes to 434.64 currently is pretty low. How do we know? Because the Z-Score table shows us the probability of values falling BELOW that Z-score level in the current distribution. So if we look at this example below:

We can see that 0.9998 or roughly 99% of values in the current SPY distribution will fall below 434.64. Thus, it may be unrealistic, at this point in time, to target said value.

So what is a Z-Score Table?

Well, I need to disclose/clarify that the Z-Score Table being displayed in this indicator does Z-Score probability a HUGE injustice. However, with the constraints what is realistic to fit into an indicator, I had to make it far more succinct. Let’s take a look at an actual Z-Score Table below:

Above is a look an the actual Z-Score table. How it works is you first identify you’re Z-Score and then find the corresponding value that relates to your score. The number displayed in the dataset represents the number of variables in the dataset/density distribution that fall BELOW that particular Z-score.

So, for example, if we have a Z-Score of -2.31, we can consult that table, go to the -2.3 then scroll across to the 0.01 to represent -2.31. We would see that this Z-Score corresponds to a 0.0104 probability zone (or essentially 1%) indicating that the majority of the variables in the distribution fall below that mean Z-score. In terms of tickers and stocks, that would mean it would theoretically be “overbought”.

So what does the indicator Z-Table tell us?

I have averaged out the data for the purposes of this indicator. However, you can also reference a manual Z-Table to get the exact probability for the current precise Z-Score. However, the reality is it doesn’t necessarily matter to be exact when it comes to tickers. The reason being, ticker’s are in constant flux, and by the time you identify that probability, the ticker will already be at a different level. So generalizations are okay in these circumstances, you just need to get the “gist” of where the distribution lies.

So how do I use the indicator?

Using the indicator is pretty straightforward. Once launched, you will see the current Z-Score of the ticker, the current levels based on the distribution and the summarized Z-Table.

The Z-Table will turn gray to indicate the zone the ticker is currently in. In this case, we can see that SPY currently is in the 2 SD Zone, meaning that 0.98 or 98% of the current dataset being shown falls below the price we are at:

When we launch the settings, we can see a few inputs.

Lookback Length: This determines the number of candles back we want to calculate the distribution for. It is defaulted to 75, but you can adjust it to whichever length you want.

SMA Length: The SMA is optional but defaults to on. If you want to see the smoothed trend of the Z-Score, this will do the trick. It does not need to be set to the same

length as the Z-Score lookback. Thus, if you want a more or less responsive SMA with, say, a larger dataset, then you can reduce the SMA length yourself.

Distribution Probability Fills: This simply colour codes the distribution zones / probability zones on the indicator.

Show Z-Table: This will display the summarized Z-Table.

Show SMA: As I indicated, the SMA is optional, you can toggle it on or off to see the overall Z-Score trend.

Concluding Remarks:

And that my friends is the Z-Score Probability Indicator.

I hope you all enjoy it and find it helpful. As always leave your comments, questions and suggestions below.

Safe trades to all and take care!

Limit Order + ATR Stop-Loss [TANHEF]This indicator enables interactive placement of limit or stop-limit orders with a trailing ATR stop-loss and optional profit target (with alerts). Refer to the images below for further clarification.

Why use a trailing stop-loss?

A trailing stop-loss serves as an exit strategy when price moves against you, while also allowing you to adjust the exit point further into profit when price moves favorably. The ATR (Average True Range), a reliable measure of volatility, acts as an effective risk management tool, functioning as a trailing stop-loss.

Indicator Explanation

Initial indicator placement: Select Long Limit or Long-Stop Limit order.

Change Entry Type: Switch between Long and Short within settings.

Modify entry price: Drag circle, adjust in settings, or re-add indicator to chart.

Optional Profit Target: Use Risk/Reward ratio or specify price.

Entry anticipation: Estimated ATR stop-loss and profit target as blue circles (fluctuates with volatility changes).

Entry triggered: Actual ATR stop-loss and profit target plotted.

Exit conditions: Stop-loss or profit target hit, exit entry.

Update Frequency: Continuously, Bar Open, or Bar Open on entry then continuously.

ATR Overlap: no entry occurs if the ATR overlaps with price (stop-loss 'hit' already on entry bar)

Table: Displays input settings selected.

Show Only On Ticker: Ability to hide indicator on other tickers.

Long Limit

Long Stop-Limit

Short Limit

Short Stop-Limit

Alerts

1. 'Check' alerts to use within indicator settings (entry, trailing stop hit, profit target hit, and failed entry).

2. Select 'Create Alert'

3. Set the condition to 'Limit Order + ATR Stop-Loss''

4. Select create.

Additional details can be added to the alert message using these words in between Curly (Brace) Brackets:

{{trail}} = ATR trailing stop-loss (price)

{{target}} = Price target (price)

{{type}} = Long or Short stop-loss (word)

{{traildistance}} = Trailing Distance (%)

{{targetdistance}} = Target Distance (%)

{{starttime}} = Start time of position (day:hr:min)

{{maxdrawdown}} = max loss

{{maxprofit}} = max profit

{{update}} = stoploss update frequency

{{entrysource}} = entry as 1st bar source (yes/no)

{{triggerentry}} = Wick/Close Trigger entry input

{{triggerexit}} = Wick/Close Trigger exit input

{{triggertarget}} = Wick/Close Trigger target input

{{atrlength}} = ATR length input

{{atrmultiplier}} = ATR multiplier input

{{atrtype}} = ATR type input

{{ticker}} = Ticker of chart (word)

{{exchange}} = Exchange of chart (word)

{{description}} = Description of ticker (words)

{{close}} = Bar close (price)

{{open}} = Bar open (price)

{{high}} = Bar high (price)

{{low}} = Bar low (price)

{{hl2}} = Bar HL2 (price)

{{volume}} = Bar volume (value)

{{time}} = Current time (day:hr:min)

{{interval}} = Chart timeframe

{{newline}} = New line for text

Leveraged Share Conversion IndicatorHello everyone,

Releasing my leveraged share conversion indicator.

I noticed that the option traders have all the fun and resources but the share traders don't really have many resources in terms of adjusting or profits on leveraged and inverse shares. So, I decided to change that this this indicator!

What it does:

In a nut shell, the calculator converts one share to the price of another through the use of a regression based analysis.

There are multiple pre-stored libraries available in the indicator, including IWM, SPY, BTC and QQQ.

However, if the ticker you want to convert is not in one of the pre-defined libraries, you can select "Use Alternative Ticker" and indicate the stock you wish to convert.

Using Libraries:

If the conversion you want is available in one of the libraries, simply select the conversion you would like. For example, if you want to convert SPY to SPXU, select that conversion. The indicator will then launch up the conversion results which it will display in a dashboard to the right and will also display the plotted conversion on a chart (see imagine below:

In the dashboard, the indicator will show you:

a) The conversion result: This is the most likely price based on the analysis