Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Cerca negli script per "涨幅超过60日均线的股票"

Constance Brown RSI with Composite IndexConstance Brown RSI with Composite Index

Overview

This indicator combines Constance Brown's RSI interpretation methodology with a Composite Index and ATR Distance to VWAP measurement to provide a comprehensive trading tool. It helps identify trends, momentum shifts, overbought/oversold conditions, and potential reversal points.

Key Features

Color-coded RSI zones for immediate trend identification

Composite Index for momentum analysis and divergence detection

ATR Distance to VWAP for identifying extreme price deviations

Automatic divergence detection for early reversal warnings

Pre-configured alerts for key trading signals

How to Use This Indicator

Trend Identification

The RSI line changes color based on its position:

Blue zone (RSI > 50): Bullish trend - look for buying opportunities

Purple zone (RSI < 50): Bearish trend - look for selling opportunities

Gray zone (RSI 40-60): Neutral/transitional market - prepare for potential breakout

The 40-50 area (light blue fill) acts as support during uptrends, while the 50-60 area (light purple fill) acts as resistance during downtrends.

// From the code:

upTrendZone = rsiValue > 50 and rsiValue <= 90

downTrendZone = rsiValue < 50 and rsiValue >= 10

neutralZone = rsiValue > 40 and rsiValue < 60

rsiColor = neutralZone ? neutralRSI : upTrendZone ? upTrendRSI : downTrendRSI

Momentum Analysis

The Composite Index (fuchsia line) provides momentum confirmation:

Values above 50 indicate positive momentum

Values below 40 indicate negative momentum

Crossing above/below these thresholds signals potential momentum shifts

// From the code:

compositeIndexRaw = rsiChange / ta.stdev(rsiValue, rsiLength)

compositeIndex = ta.sma(compositeIndexRaw, compositeSmoothing)

compositeScaled = compositeIndex * 10 + 50 // Scaled to fit 0-100 range

Overbought/Oversold Detection

The ATR Distance to VWAP table in the top-right corner shows how far price has moved from VWAP in terms of ATR units:

Extreme positive values (orange/red): Potentially overbought

Extreme negative values (purple/red): Potentially oversold

Near zero (gray): Price near average value

// From the code:

priceDistance = (close - vwapValue) / ta.atr(atrPeriod)

// Color coding based on distance value

Divergence Trading

The indicator automatically detects divergences between the Composite Index and price:

Bullish divergence: Price makes lower low but Composite Index makes higher low

Bearish divergence: Price makes higher high but Composite Index makes lower high

// From the code:

divergenceBullish = ta.lowest(compositeIndex, rsiLength) > ta.lowest(close, rsiLength)

divergenceBearish = ta.highest(compositeIndex, rsiLength) < ta.highest(close, rsiLength)

Trading Strategies

Trend Following

1. Identify the trend using RSI color:

Blue = Uptrend, Purple = Downtrend

2. Wait for pullbacks to support/resistance zones:

In uptrends: Buy when RSI pulls back to 40-50 zone and bounces

In downtrends: Sell when RSI rallies to 50-60 zone and rejects

3. Confirm with Composite Index:

Uptrends: Composite Index stays above 50 or quickly returns above it

Downtrends: Composite Index stays below 50 or quickly returns below it

4. Manage risk using ATR Distance:

Take profits when ATR Distance reaches extreme values

Place stops beyond recent swing points

Reversal Trading

1. Look for divergences

Bullish: Price makes lower low but Composite Index makes higher low

Bearish: Price makes higher high but Composite Index makes lower high

2. Confirm with ATR Distance:

Extreme readings suggest potential reversals

3. Wait for RSI zone transition:

Bullish: RSI crosses above 40 (purple to neutral/blue)

Bearish: RSI crosses below 60 (blue to neutral/purple)

4. Enter after confirmation:

Use candlestick patterns for precise entry

Place stops beyond the divergence point

Four pre-configured alerts are available:

Momentum High: Composite Index above 50

Momentum Low: Composite Index below 40

Bullish Divergence: Composite Index higher low

Bearish Divergence: Composite Index lower high

Customization

Adjust these parameters to optimize for your trading style:

RSI Length: Default 14, lower for more sensitivity, higher for fewer signals

Composite Index Smoothing: Default 10, lower for quicker signals, higher for less noise

ATR Period: Default 14, affects the ATR Distance to VWAP calculation

This indicator works well across various markets and timeframes, though the default settings are optimized for daily charts. Adjust parameters for shorter or longer timeframes as needed.

Happy trading!

RSI3M3+ v.1.8RSI3M3+ v.1.8 Indicator

This script is an advanced trading indicator based on Walter J. Bressert's cycle analysis methodology, combined with an RSI (Relative Strength Index) variation. Let me break it down and explain how it works.

Core Concepts

The RSI3M3+ indicator combines:

A short-term RSI (3-period)

A 3-period moving average to smooth the RSI

Bressert's cycle analysis principles to identify optimal trading points

RSI3M3+ Indicator VisualizationImage Walter J. Bressert's Cycle Analysis Concepts

Walter Bressert was a pioneer in cycle analysis trading who believed markets move in cyclical patterns that can be measured and predicted. His key principles integrated into this indicator include:

Trading Cycles: Markets move in cycles with measurable time spans from low to low

Timing Bands: Projected periods when the next cyclical low or high is anticipated

Oscillator Use: Using oscillators like RSI to confirm cycle position

Entry/Exit Rules: Specific rules for trade entry and exit based on cycle position

Key Parameters in the Script

Basic RSI Parameters

Required bars: Minimum number of bars needed (default: 20)

Overbought region: RSI level considered overbought (default: 70)

Oversold region: RSI level considered oversold (default: 30)

Bressert-Specific Parameters

Cycle Detection Length: Lookback period for cycle identification (default: 30)

Minimum/Maximum Cycle Length: Expected cycle duration in days (default: 15-30)

Buy Line: Lower threshold for buy signals (default: 40)

Sell Line: Upper threshold for sell signals (default: 60)

How the Indicator Works

RSI3M3 Calculation:

Calculates a 3-period RSI (sRSI)

Smooths it with a 3-period moving average (sMA)

Cycle Detection:

Identifies bottoms: When the RSI is below the buy line (40) and starting to turn up

Identifies tops: When the RSI is above the sell line (60) and starting to turn down

Records these points to calculate cycle lengths

Timing Bands:

Projects when the next cycle bottom or top should occur

Creates visual bands on the chart showing these expected time windows

Signal Generation:

Buy signals occur when the RSI turns up from below the oversold level (30)

Sell signals occur when the RSI turns down from above the overbought level (70)

Enhanced by Bressert's specific timing rules

Bressert's Five Trading Rules (Implemented in the Script)

Cycle Timing: The low must be 15-30 market days from the previous Trading Cycle bottom

Prior Top Validation: A Trading Cycle high must have occurred with the oscillator above 60

Oscillator Behavior: The oscillator must drop below 40 and turn up

Entry Trigger: Entry is triggered by a rise above the price high of the upturn day

Protective Stop: Place stop slightly below the Trading Cycle low (implemented as 99% of bottom price)

How to Use the Indicator

Reading the Chart

Main Plot Area:

Green line: 3-period RSI

Red line: 3-period moving average of the RSI

Horizontal bands: Oversold (30) and Overbought (70) regions

Dotted lines: Buy line (40) and Sell line (60)

Yellow vertical bands: Projected timing windows for next cycle bottom

Signals:

Green up arrows: Buy signals

Red down arrows: Sell signals

Trading Strategy

For Buy Signals:

Wait for the RSI to drop below the buy line (40)

Look for an upturn in the RSI from below this level

Enter the trade when price rises above the high of the upturn day

Place a protective stop at 99% of the Trading Cycle low

For Sell Signals:

Wait for the RSI to rise above the sell line (60)

Look for a downturn in the RSI from above this level

Consider exiting or taking profits when a sell signal appears

Alternative exit: When price moves below the low of the downturn day

Cycle Timing Enhancement:

Pay attention to the yellow timing bands

Signals occurring within these bands have higher probability of success

Signals outside these bands may be less reliable

Practical Tips for Using RSI3M3+

Timeframe Selection:

The indicator works best on daily charts for intermediate-term trading

Can be used on weekly charts for longer-term position trading

On intraday charts, adjust cycle lengths accordingly

Market Applicability:

Works well in trending markets with clear cyclical behavior

Less effective in choppy, non-trending markets

Consider additional indicators for trend confirmation

Parameter Adjustment:

Different markets may have different natural cycle lengths

You may need to adjust the min/max cycle length parameters

Higher volatility markets may need wider overbought/oversold levels

Trade Management:

Enter trades when all Bressert's conditions are met

Use the protective stop as defined (99% of cycle low)

Consider taking partial profits at the projected cycle high timing

Advanced Techniques

Multiple Timeframe Analysis:

Confirm signals with the same indicator on higher timeframes

Enter in the direction of the larger cycle when smaller and larger cycles align

Divergence Detection:

Look for price making new lows while RSI makes higher lows (bullish)

Look for price making new highs while RSI makes lower highs (bearish)

Confluence with Price Action:

Combine with support/resistance levels

Use with candlestick patterns for confirmation

Consider volume confirmation of cycle turns

This RSI3M3+ indicator combines the responsiveness of a short-term RSI with the predictive power of Bressert's cycle analysis, offering traders a sophisticated tool for identifying high-probability trading opportunities based on market cycles and momentum shifts.

THANK YOU FOR PREVIOUS CODER THAT EFFORT TO CREATE THE EARLIER VERSION THAT MAKE WALTER J BRESSERT CONCEPT IN TRADINGVIEW @ADutchTourist

JL - DWM OHLCThis indicator plots the following price levels on your chart automatically AND will not show up if you are using a timeframe bigger than 60 minutes, 1 day, or 1 week.

Here are the price levels that are automatically plotted for you, and so you know the styling is different for Daily, Weekly, Monthly levels so you can easily distinguish between them:

- Prior Day: High / Low / Close

- Current Day: Open

- Prior Week: High / Low / Close

- Current Week: Open

- Prior Month: High / Low / Close

- Current Month: Open

These plots are timeframe dependent and will not plot on subsequently higher timeframes, here is how they work:

Daily Price Levels are only shown on timeframes that are smaller than 60 minutes.

Weekly Price Levels are only shown on timeframes smaller than 1 Day.

Monthly Price Levels are only shown on timeframes smaller than 1 Week.

This way, you can turn on the indicator and not have to think about turning off certain price levels if you switch to a larger / longer timeframe than what you typically use.

For example, Daily OHLC price levels will quickly clutter the 60 minute chart, and likely you don't need to know the HLC of the Prior Day if you are looking at the 60 minute chart. Therefor it may be helpful to automatically hide the Daily price level plots, and only show the Weekly and Monthly plots on the 60 minute timeframe.

I hope you find this indicator helpful, thanks for reading.

Simultaneous INSIDE Bar Break IndicatorSimultaneous Inside Bar Break Indicator (SIBBI) for The Strat Community

Overview:

The Simultaneous Inside Bar Break Indicator (SIBBI) is designed to help traders using The Strat methodology identify one of the most powerful breakout patterns: the Simultaneous Inside Bar Break across multiple symbols. This indicator detects when all four user-selected symbols form inside bars on the previous candle and then break those inside bars in the same direction (either bullish or bearish) on the current candle.

Inside bars represent consolidation periods where price action does not break the high or low of the previous candle. When a simultaneous break occurs across multiple symbols, this often signals a strong move in the market, making this a key actionable signal in The Strat trading strategy.

Key Features:

Multi-Symbol Analysis: You can track up to four different symbols simultaneously. By default, the indicator comes with SPY, QQQ, IWM, and DIA, but you can modify these to track any other assets or symbols.

Inside Bar Detection: The indicator checks whether all four symbols have inside bars on the previous candle. It only triggers when all symbols meet this condition, making it a highly specific and reliable signal.

Simultaneous Break Detection: Once all symbols have inside bars, the indicator waits for a breakout in the same direction across all four symbols. A simultaneous bullish break (prices breaking above the previous candle’s high) triggers a green label, while a simultaneous bearish break (prices breaking below the previous candle’s low) triggers a red label.

Dynamic Label Timeframe: The indicator dynamically adjusts the timeframe in the label based on the user’s selected timeframe. This allows traders to know precisely which timeframe the break is occurring on. If the user selects "Chart Timeframe," the indicator will evolve with the current chart's timeframe, making it more versatile.

Timeframe Flexibility: The indicator can be set to analyze any timeframe—15-minute, 30-minute, 60-minute, daily, weekly, and so on. It only works for the specific timeframe you set it to in the settings. If set to "Chart Timeframe," the label will adapt dynamically based on the timeframe you are currently viewing.

Customizable Labels: The user can choose the size of the labels (tiny, small, or normal), ensuring that the visual output is tailored to individual preferences and chart layouts.

Best Use Case:

The Simultaneous Inside Bar Break Indicator is particularly powerful when applied to multiple timeframes. Here’s how to use it for maximum impact:

Multi-Timeframe Setup: Set the indicator on various timeframes (e.g., 15-minute, 30-minute, 60-minute, and daily) across multiple charts. This allows you to monitor different timeframes and identify when lower timeframe breaks trigger potential moves on higher timeframes.

Anticipating Strong Moves: When a simultaneous inside bar break occurs on one timeframe (e.g., 30-minute), keep an eye on the higher timeframes (e.g., 60-minute or daily) to see if those timeframes also break. This stacking of inside bar breaks can signal powerful market moves.

Higher Conviction Signals: The indicator is designed to provide high-conviction signals. Since it requires all four symbols to break in the same direction simultaneously, it reduces false signals and focuses on higher probability setups, which is crucial for traders using The Strat to time their trades effectively.

How the Indicator Works:

Inside Bar Formation: The indicator first checks that all four selected symbols had inside bars in the previous bar (i.e., the current high and low are contained within the previous bar’s high and low).

Simultaneous Break Detection: After detecting inside bars, the indicator checks if all four symbols break out in the same direction—bullish (breaking above the previous bar’s high) or bearish (breaking below the previous bar’s low).

Label Display: When a simultaneous inside bar break occurs, a label is plotted on the chart—either green for a bullish break (below the candle) or red for a bearish break (above the candle). The label will display the timeframe you set in the settings (e.g., "IBSB 60" for a 60-minute break).

Chart Timeframe Option: If you prefer, you can set the indicator to evolve with the chart’s current timeframe. In this mode, the label will not show a specific timeframe but will still display the simultaneous inside bar break when it occurs.

Recommendations for Usage:

Focus on Multiple Timeframes: The Strat methodology is all about understanding the relationship between different timeframes. Use this indicator on multiple timeframes to get a better picture of potential moves.

Pair with Other Strat Techniques: This indicator is most powerful when combined with other Strat tools, such as broadening formations, timeframe continuity, and actionable signals (e.g., 2-2 reversals). The simultaneous inside bar break can help confirm or invalidate other signals.

Customize Symbols and Timeframes: Although the default symbols are SPY, QQQ, IWM, and DIA, feel free to replace them with symbols more relevant to your trading. This indicator works well across equities, indices, futures, and forex pairs.

How to Set It Up:

Select Symbols: Choose four symbols that you want to track. These can be index ETFs (like SPY and QQQ), individual stocks, or any other tradable instruments.

Set Timeframe: In the indicator’s settings, choose a specific timeframe (e.g., 15-minute, 30-minute, daily). The label will reflect the selected timeframe, making it clear which time-based break you are seeing.

Optional - Chart Timeframe Mode: If you want the indicator to adapt to the chart’s current timeframe, select the "Chart Timeframe" option in the settings. The indicator will plot the breaks without showing a specific timeframe in the label.

Customize Label Size: Depending on your chart layout and personal preference, you can adjust the size of the labels (tiny, small, or normal) in the settings.

Conclusion:

The Simultaneous Inside Bar Break Indicator is a powerful tool for traders using The Strat methodology, offering a highly specific and reliable signal that can indicate potential large market moves. By monitoring multiple symbols and timeframes, you can gain deeper insight into the market's behavior and act with greater confidence. This indicator is ideal for traders looking to catch high-conviction moves and align their trades with broader market continuity.

Note: The indicator works best when paired with multi-timeframe analysis, allowing you to see how breaks on lower timeframes might influence larger trends. For traders who prefer simplicity, setting it to the "Chart Timeframe" mode offers flexibility while maintaining the core benefits of this indicator.

Financial Radar Chart by zdmreRadar chart is often used when you want to display data across several unique dimensions. Although there are exceptions, these dimensions are usually quantitative, and typically range from zero to a maximum value. Each dimension’s range is normalized to one another, so that when we draw our spider chart, the length of a line from zero to a dimension’s maximum value will be the similar for every dimension.

This Charts are useful for seeing which variables are scoring high or low within a dataset, making them ideal for displaying performance.

How is the score formed?

Debt Paying Ability

if Debt_to_Equity < %10 : 100

elif < 20% : 90

elif < 30% : 80

elif < 40% : 70

elif < 50% : 60

elif < 60% : 50

elif < 70% : 40

elif < 80% : 30

elif < 90% : 20

elif < 100% : 10

else: 0

ROIC

if Return_on_Invested_Capital > %50 : 100

elif > 40% : 90

elif > 30% : 80

elif > 20% : 70

elif > 10% : 50

elif > 5% : 20

else: 0

ROE

if Return_on_Equity > %50 : 100

elif > 40% : 90

elif > 30% : 80

elif > 20% : 70

elif > 10% : 50

elif > 5% : 20

else: 0

Operating Ability

if Operating_Margin > %50 : 100

elif > 30% : 90

elif > 20% : 80

elif > 15% : 60

elif > 10% : 40

elif > 0 : 20

else: 0

EV/EBITDA

if Enterprise_Value_to_EBITDA < 3 : 100

elif < 5 : 80

elif < 7 : 70

elif < 8 : 60

elif < 10 : 40

elif < 12 : 20

else: 0

FREE CASH Ability

if Price_to_Free_Cash_Flow < 5 : 100

elif < 7 : 90

elif < 10 : 80

elif < 16 : 60

elif < 18 : 50

elif < 20 : 40

elif < 22 : 30

elif < 30 : 20

elif < 40 : 15

elif < 50 : 10

elif < 60 : 5

else: 0

GROWTH Ability

if Revenue_One_Year_Growth > %20 : 100

elif > 16% : 90

elif > 14% : 80

elif > 12% : 70

elif > 10% : 50

elif > 7% : 40

elif > 4% : 30

elif > 2% : 20

elif > 0 : 10

else: 0

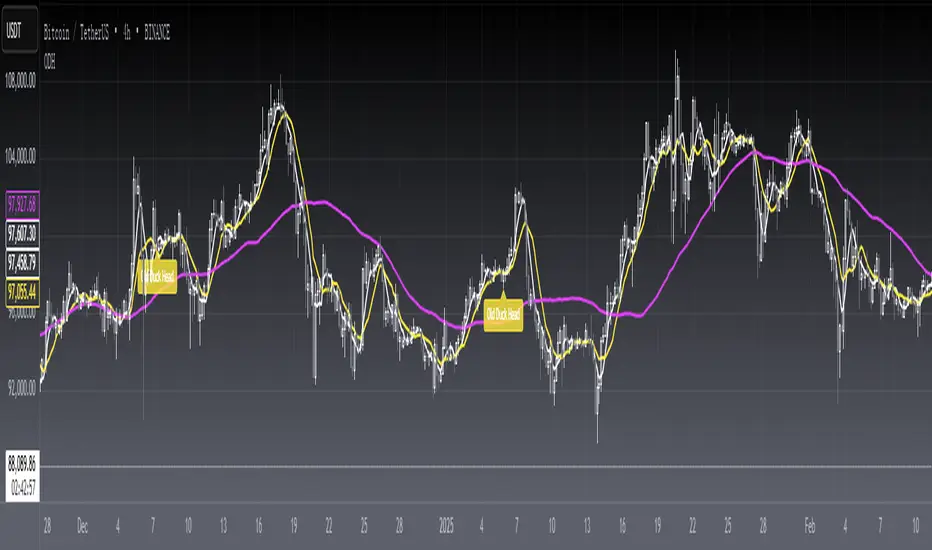

[blackcat] L1 Old Duck HeadLevel 1

Background

The old duck head is a classic form formed by a series of behaviors such as bankers opening positions, washing dishes, and pulling over the top of the duck head.

Function

A form of stock candles:

(1) Moving averages using 5, 10 and 60 parameters. When the 5-day and 10-day moving averages crossed the 60-day moving average, a duck neck was formed.

(2) The high point when the stock price fell back formed a duck head.

(3) When the stock price fell back soon, the 5-day and 10-day moving averages again turned up to form a duckbill.

(4) Duck nose refers to the hole formed when the 5-day moving average crosses the 10-day moving average and the two lines cross again.

Market significance:

(1) When the dealer starts to collect chips, the stock price rises slowly, and the 5-day and 10-day moving averages cross the 60-day moving average, forming a duck neck.

(2) When the stock price of the banker shakes the position and starts to pull back, the high point of the stock price forms the top of the duck's head.

(3) When the dealer builds a position again to collect chips, the stock price rises again, forming a duck bill.

Operation method:

(1) Buy when the 5-day and 10-day moving averages cross the 60-day moving average and form a duck neck.

(2) Buy on dips near the sesame point of trading volume near the duckbill.

(3) Intervene when the stock price crosses the top of the duck's head in heavy volume.

The top of the duck’s head should be a little far away from the 60-day moving average, otherwise it means that the dealer is not willing to open a position at this old duck’s head, and the bottom of the old duck’s head must be heavy. Small is better, nothing is the strongest! There must be a lot of sesame dots under the nostrils of the duck, otherwise it means that the dealer has poor control. There must be ventilation under the duck bill, the higher the ventilation, the better!

Remarks

Feedbacks are appreciated.

Edge of MomentumThe script was designed for the purpose of catching the rocket portion of a move (the edge of momentum).

Long

--When RSI closes over 60, take long order 1 tick above that bar. The closed bar above RSI 60 will be colored "green" or whatever color the user chooses. (RSI > 60)

--On a long position, exit will be a closed bar below the ema (low, 10) . The closed bar below the ema will be colored "yellow." (Price < ema)

--Note: On a long position there is no need to exit when a closed bar is colored "purple." RSI is just below 60 but above 40. Pullback or chop

Short

--When RSI closes below 40, take a short order 1 tick below that bar. The closed bar below RSI 40 will be colored "red." RSI<40)

--On a short position, exit will be a closed bar above the ema (low, 10). The closed bar above the ema will be colored "purple." (Price > ema)

--Note: On a short position there is no need to exit when a closed bar is colored "yellow."

Note: You may see a series of purple and yellow bars, that is simply chop. I define chop as RSI moving between 60 and 40.

Trade should only be taken above green colored candle(long) and below red colored candle (short). No position should be taken off yellow or purple candle (chop)

Again this is designed to catch the momentum part of a move, and to help reduce some entries during chop. It is a simple systems that beginning traders can use and profit from.

Note: I don't no shit about coding scripts I just learn from reading others.

Enjoy. If you decide to use please drop me a line...suggestions/comments, etc.

Best of luck in all you do.

3 Duck's Trading System from Babypips.comThe 3 Duck's Trading System from Babypips.com

The 3 Duck's Trading System is the most popular and active trading system thread on the the babypips.com forum. It is a system that is mainly for beginners because it teaches you discipline, learning to cope with price moving against your position and learning to stay in a trade and keep profits running. For the thread and more info on the 3 Duck's Trading System click here

How does it work?

The system is a very simple enter/exit based on the 60 SMA of 3 different time frames: 4 hour, 1 hour and 5 minute.

The Rules, er, the Ducks! The Ducks must all be in a row for a trade to take place!

Duck 1 - To go long, price must be above the 60 SMA on the 4 hour chart.

Duck 2 - To go long, price must be above the 60 SMA on the 1 hour chart.

Duck 3 - To go long, price must cross above the 60 SMA on the 5 minute chart and the 60 SMA of the 5 minute chart must be below that of the 4 hour and 1 hour chart. (obviously the reverse for shorting)

YOU MUST USE THIS SYSTEM ONLY ON THE 5 MINUTE CHART.

I say this because I have already charted all of the Ducks into the 5 minute chart so you don't have to flip back and forth.

I have also added some inputs for profit targets, stop targets, trailing stops and times to trade for backtesting.

If you have any questions or comments, please let me know! If you see I messed up on something, please let me know!

Also a VERY special thanks to the babypips.com user Captain_Currency . He wrote this strategy 10 years ago (2007 was 10 years ago?!) and he is still active on the thread and posting results and offering help!

VWAP MA HLOC securities Jayy update fix This version replaces previous versions that stopped functioning as a result of a TradingView script update.

This script complies with the current script syntax.

for intraday securities default is 9:30 am to 4 pm Eastern Other session choices are provided in the format dialogue box.

script plots VWAP, yesterday's high, low, open and close (HLOC), the day befores HLOC - if desired, today's open and todays high and low.

Also signals inside bars (high is less than or equal to the previous

bar's high and the low is greater than or equal to

the previous low) the : true inside bars have a maroon triangle below the bar as well as a ">" above the bar.

If subsequent bars are inside the last bar before the last true inside bar they also are marked with an ">"

Also plots the 20 ema for different time periods (as per Al Brooks), If you trade the 5 min then you will

likely be interested in the 20 ema for 15 mins and 60 mins

the following is a list of the higher timeframe 20 emas

1 minute 5, 15, 60 period 20 ema

5 minute 15, 60 period 20 ema

15 minute 60, 120 , 240 period 20 ema

60 minute 120, 240 period 20 ema

120 minute 240, D period 20 ema

240 minute D period 20 ema

Jayy

Liquidity Sweep + FVG Entry Model//@version=5

indicator("Liquidity Sweep + FVG Entry Model", overlay = true, max_labels_count = 500, max_lines_count = 500)

// Just to confirm indicator is loaded, always plot close:

plot(close, color = color.new(color.white, 0))

// ─────────────────────────────────────────────

// PARAMETERS

// ─────────────────────────────────────────────

len = input.int(5, "Liquidity Lookback")

tpMultiplier = input.float(2.0, "TP Distance Multiplier")

// ─────────────────────────────────────────────

// LIQUIDITY SWEEP DETECTION

// ─────────────────────────────────────────────

lowestPrev = ta.lowest(low, len)

highestPrev = ta.highest(high, len)

sweepLow = low < lowestPrev and close > lowestPrev

sweepHigh = high > highestPrev and close < highestPrev

// Plot liquidity levels

plot(lowestPrev, "Liquidity Low", color = color.new(color.blue, 40), style = plot.style_line)

plot(highestPrev, "Liquidity High", color = color.new(color.red, 40), style = plot.style_line)

// ─────────────────────────────────────────────

// DISPLACEMENT DETECTION

// ─────────────────────────────────────────────

bullDisp = sweepLow and close > open and close > close

bearDisp = sweepHigh and close < open and close < close

// ─────────────────────────────────────────────

// FAIR VALUE GAP (FVG)

// ─────────────────────────────────────────────

bullFVG = low > high

bearFVG = high < low

// we’ll store the last FVG lines

var line fvgTop = na

var line fvgBottom = na

// clear old FVG lines when new one appears

if bullFVG or bearFVG

if not na(fvgTop)

line.delete(fvgTop)

if not na(fvgBottom)

line.delete(fvgBottom)

// Bullish FVG box

if bullFVG

fvgTop := line.new(bar_index , high , bar_index, high , extend = extend.right, color = color.new(color.green, 60))

fvgBottom := line.new(bar_index , low, bar_index, low, extend = extend.right, color = color.new(color.green, 60))

// Bearish FVG box

if bearFVG

fvgTop := line.new(bar_index , low , bar_index, low , extend = extend.right, color = color.new(color.red, 60))

fvgBottom := line.new(bar_index , high, bar_index, high, extend = extend.right, color = color.new(color.red, 60))

// ─────────────────────────────────────────────

// ENTRY, SL, TP CONDITIONS

// ─────────────────────────────────────────────

var line slLine = na

var line tp1Line = na

var line tp2Line = na

f_deleteLineIfExists(line_id) =>

if not na(line_id)

line.delete(line_id)

if bullDisp and bullFVG

sl = low

tp1 = close + (close - sl) * tpMultiplier

tp2 = close + (close - sl) * (tpMultiplier * 1.5)

f_deleteLineIfExists(slLine)

f_deleteLineIfExists(tp1Line)

f_deleteLineIfExists(tp2Line)

slLine := line.new(bar_index, sl, bar_index + 1, sl, extend = extend.right, color = color.red)

tp1Line := line.new(bar_index, tp1, bar_index + 1, tp1, extend = extend.right, color = color.green)

tp2Line := line.new(bar_index, tp2, bar_index + 1, tp2, extend = extend.right, color = color.green)

label.new(bar_index, close, "BUY Entry\nFVG Retest\nSL Below Sweep",

style = label.style_label_up, color = color.new(color.green, 0), textcolor = color.white)

if bearDisp and bearFVG

sl = high

tp1 = close - (sl - close) * tpMultiplier

tp2 = close - (sl - close) * (tpMultiplier * 1.5)

f_deleteLineIfExists(slLine)

f_deleteLineIfExists(tp1Line)

f_deleteLineIfExists(tp2Line)

slLine := line.new(bar_index, sl, bar_index + 1, sl, extend = extend.right, color = color.red)

tp1Line := line.new(bar_index, tp1, bar_index + 1, tp1, extend = extend.right, color = color.green)

tp2Line := line.new(bar_index, tp2, bar_index + 1, tp2, extend = extend.right, color = color.green)

label.new(bar_index, close, "SELL Entry\nFVG Retest\nSL Above Sweep",

style = label.style_label_down, color = color.new(color.red, 0), textcolor = color.white)

Mirpapa_Lib_BoxLibrary "Mirpapa_Lib_Box"

GetHTFrevised(_tf, _case)

GetHTFrevised

@description Retrieve a specific bar value from a Higher Time Frame (HTF) series.

Parameters:

_tf (string) : string The target HTF string (examples: "60", "1D").

_case (string) : string Case string determining which OHLC value to request.

@return float Returns the requested HTF value or na if _case does not match.

GetHTFrevised(_tf)

Parameters:

_tf (string)

GetHTFoffsetToLTFoffset(_offset, _chartTf, _htfTf)

GetHTFoffsetToLTFoffset

@description Adjust an HTF offset to an LTF offset by calculating the ratio of timeframes.

Parameters:

_offset (int) : int The HTF bar offset (0 means current HTF bar).

_chartTf (string) : string The current chart's timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string The High Time Frame string (e.g., "60", "1D").

@return int The corresponding LTF bar index. Returns 0 if the result is negative.

GetHtfFromLabel(_label)

GetHtfFromLabel

@description Convert a Korean HTF label into a Pine Script timeframe string.

Parameters:

_label (string) : string The Korean label (e.g., "5분", "1시간").

@return string Returns the corresponding Pine Script timeframe (e.g., "5", "60").

IsChartTFcomparisonHTF(_chartTf, _htfTf)

IsChartTFcomparisonHTF

@description Determine whether a given HTF is greater than or equal to the current chart timeframe.

Parameters:

_chartTf (string) : string Current chart timeframe (e.g., "5", "15", "1D").

_htfTf (string) : string HTF timeframe (e.g., "60", "1D").

@return bool True if HTF ≥ chartTF, false otherwise.

IsCondition(_boxType, _isBull, _pricePrev, _priceNow)

IsCondition

@description FOB, FVG 조건 체크.\

_boxType: "fob"(Fair Order Block) 또는 "fvg"(Fair Value Gap).\

_isBull: true(상승 패턴), false(하락 패턴).\

상승 시 현재 가격이 이전 가격보다 높으면 true, 하락 시 이전 가격이 현재 가격보다 높으면 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("fob", "fvg")

_isBull (bool) : 상승(true) 또는 하락(false)

_pricePrev (float) : 이전 가격

_priceNow (float) : 현재 가격

Returns: bool 조건 만족 여부

IsCondition(_boxType, _high2, _high1, _high0, _low2, _low1, _low0)

IsCondition

@description Sweep 조건 체크 (Swing High/Low 동시 발생).\

_boxType: "sweep" 또는 "breachBoth".\

조건: high2 < high1 > high0 (Swing High) AND low2 > low1 < low0 (Swing Low).\

중간 캔들이 양쪽보다 높고 낮은 지점을 동시에 형성할 때 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("sweep", "breachBoth")

_high2 (float)

_high1 (float)

_high0 (float)

_low2 (float)

_low1 (float)

_low0 (float)

Returns: bool 조건 만족 여부

IsCondition(_boxType, _isBull, _open1, _close1, _high1, _low1, _open0, _close0, _low2, _low3, _high2, _high3)

IsCondition

@description RB (Rejection Block) 조건 체크.\

_boxType: "rb" (Rejection Block).\

상승 RB: candle1=음봉, candle0=양봉, low3>low1 AND low2>low1, close1*1.001>open0, open1close0.\

이전 캔들의 거부 후 현재 캔들이 반대 방향으로 전환될 때 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("rb")

_isBull (bool) : 상승(true) 또는 하락(false)

_open1 (float)

_close1 (float)

_high1 (float)

_low1 (float)

_open0 (float)

_close0 (float)

_low2 (float)

_low3 (float)

_high2 (float)

_high3 (float)

Returns: bool 조건 만족 여부

IsCondition(_boxType, _isBull, _open2, _close1, _open1, _close0)

IsCondition

@description SOB (Strong Order Block) 조건 체크.\

_boxType: "sob" (Strong Order Block).\

상승 SOB: 양봉2 => 음봉1 => 양봉0, open2 > close1 AND open1 < close0.\

하락 SOB: 음봉2 => 양봉1 => 음봉0, open2 < close1 AND open1 > close0.\

3개 캔들 패턴으로 강한 주문 블록 형성 시 true 반환.

Parameters:

_boxType (string) : 박스 타입 ("sob")

_isBull (bool) : 상승(true) 또는 하락(false)

_open2 (float) : 2개 이전 캔들 open

_close1 (float) : 1개 이전 캔들 close

_open1 (float) : 1개 이전 캔들 open

_close0 (float) : 현재 캔들 close

Returns: bool 조건 만족 여부

CreateBox(_boxType, _boxState, _breachModeStart, _breachModeEnd, _isBull, _leftTime, _rightTime, _top, _bottom, _useLine, _colorBG, _colorBD, _colorText, _customText)

CreateBox

@description 박스 생성 (값 전달 방식 - 모든 좌표 직접 지정).\

호출자가 모든 좌표와 시간을 계산하여 전달.\

HTF/LTF 구분 불필요, tf/cache 계산 없음.\

Parameters:

_boxType (string) : 박스 타입 ("sob", "fob", "rb", "custom" 등)

_boxState (string) : 박스 상태 ("pending", "start", "extension")

_breachModeStart (string) : 시작 돌파 처리 방식

_breachModeEnd (string) : 종료 돌파 처리 방식

_isBull (bool) : 상승(true) 또는 하락(false)

_leftTime (int) : 박스 시작 시간

_rightTime (int) : 박스 종료 시간

_top (float) : 박스 상단 가격

_bottom (float) : 박스 하단 가격

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_customText (string) : 커스텀 텍스트

Returns: 성공 여부와 박스 데이터

CreateBox(_boxType, _boxState, _tf, _isBull, _useLine, _colorBG, _colorBD, _colorText, _cache)

CreateBox (자동 계산 방식)

@description 박스 생성 (tf/cache 기반 자동 좌표 계산).\

라이브러리가 boxType에 따라 좌표를 자동 계산.\

Parameters:

_boxType (string) : 박스 타입

_boxState (string) : 박스 상태 ("pending", "start", "extension")

_tf (string) : 시간대

_isBull (bool) : 상승(true) 또는 하락(false)

_useLine (bool) : 중간선 표시 여부

_colorBG (color) : 박스 배경색

_colorBD (color) : 박스 테두리색

_colorText (color) : 텍스트 색상

_cache (HTFCache) : HTF 캐시 데이터

Returns: 성공 여부와 박스 데이터

ProcessBoxDatas(_openBoxes, _closedBoxes, _useMidLine, _closeCount, _baseColor, _pendingTransparency, _startTransparency, _endTransparency, _currentBarIndex, _currentLow, _currentHigh, _currentClose, _currentTime)

ProcessBoxDatas

@description 박스 확장 및 상태별 돌파 처리.\

열린 박스들을 현재 bar까지 확장하고, 상태별 돌파 조건 체크.\

PENDING: 시작 조건 체크 → START 전환\

START: 종료 조건 체크 → END 전환\

EXTENSION: 무한 확장\

종료된 박스는 _closedBoxes로 이동하고 _colorClose 색상 적용.\

Parameters:

_openBoxes (array) : 열린 박스 배열

_closedBoxes (array) : 닫힌 박스 배열

_useMidLine (bool) : 중간선 표시 여부

_closeCount (int) : 돌파 카운트 (이 횟수만큼 돌파 시 종료)

_baseColor (color) : 기본 색상

_pendingTransparency (int) : 대기 상태 불투명도

_startTransparency (int) : 시작 상태 불투명도

_endTransparency (int) : 종료 상태 불투명도

_currentBarIndex (int) : 현재 bar_index

_currentLow (float) : 현재 low

_currentHigh (float) : 현재 high

_currentClose (float) : 현재 close

_currentTime (int) : 현재 time

Returns: bool 항상 true

BoxType

BoxType

Fields:

FOB (series string)

FVG (series string)

IFVG (series string)

SOB (series string)

RB (series string)

BB (series string)

MB (series string)

SWEEP (series string)

CUSTOM (series string)

BreachMode

BreachMode

Fields:

BOTH_HIGH_LOW (series string)

BOTH_CLOSE (series string)

DIRECTIONAL_HIGH_LOW (series string)

DIRECTIONAL_CLOSE (series string)

NEAR_HIGH (series string)

NEAR_CLOSE (series string)

NEAR_LOW (series string)

FAR_HIGH (series string)

FAR_CLOSE (series string)

FAR_LOW (series string)

BoxState

BoxState

Fields:

PENDING (series string)

START (series string)

END (series string)

EXTENSION (series string)

BoxData

BoxData

Fields:

_type (series string) : 박스 타입

_breachModeStart (series string) : 시작 돌파 처리 방식

_breachModeEnd (series string) : 종료 돌파 처리 방식

_boxState (series string) : 박스 상태

_isBull (series bool) : 상승(true) 또는 하락(false) 방향

_box (series box)

_line (series line)

_boxTop (series float)

_boxBot (series float)

_boxMid (series float)

_topBreached (series bool)

_bottomBreached (series bool)

_breakCount (series int)

HTFCache

Fields:

_timeframe (series string)

_lastBarIndex (series int)

_isNewBar (series bool)

_barIndex (series int)

_open (series float)

_high (series float)

_low (series float)

_close (series float)

_open1 (series float)

_close1 (series float)

_high1 (series float)

_low1 (series float)

_open2 (series float)

_close2 (series float)

_high2 (series float)

_low2 (series float)

_high3 (series float)

_low3 (series float)

_time1 (series int)

_time2 (series int)

猛の掟・本物っぽいTradingViewスクリーナー 完全版//@version=5

indicator("猛の掟・本物っぽいTradingViewスクリーナー 完全版", overlay=false, max_labels_count=500, max_lines_count=500)

// =============================

// 入力パラメータ

// =============================

emaLenShort = input.int(5, "短期EMA", minval=1)

emaLenMid = input.int(13, "中期EMA", minval=1)

emaLenLong = input.int(26, "長期EMA", minval=1)

macdFastLen = input.int(12, "MACD Fast", minval=1)

macdSlowLen = input.int(26, "MACD Slow", minval=1)

macdSignalLen = input.int(9, "MACD Signal", minval=1)

macdZeroTh = input.float(0.2, "MACDゼロライン近辺とみなす許容値", step=0.05)

volMaLen = input.int(5, "出来高平均日数", minval=1)

volMinRatio = input.float(1.3, "出来高倍率(初動判定しきい値)", step=0.1)

volStrongRatio = input.float(1.5, "出来高倍率(本物/三点シグナル用)", step=0.1)

highLookback = input.int(60, "直近高値の参照本数", minval=10)

pullbackMin = input.float(5.0, "押し目最小 ", step=0.5)

pullbackMax = input.float(15.0, "押し目最大 ", step=0.5)

breakLookback = input.int(15, "レジブレ後とみなす本数", minval=1)

wickBodyMult = input.float(2.0, "ピンバー:下ヒゲが実体の何倍以上か", step=0.5)

// 表示設定

showPanel = input.bool(true, "下パネルにスコアを表示する")

showTable = input.bool(true, "右上に8条件チェック表を表示する")

// =============================

// 基本指標計算

// =============================

emaShort = ta.ema(close, emaLenShort)

emaMid = ta.ema(close, emaLenMid)

emaLong = ta.ema(close, emaLenLong)

= ta.macd(close, macdFastLen, macdSlowLen, macdSignalLen)

volMa = ta.sma(volume, volMaLen)

volRatio = volMa > 0 ? volume / volMa : 0.0

recentHigh = ta.highest(high, highLookback)

prevHigh = ta.highest(high , highLookback)

pullbackPct = recentHigh > 0 ? (recentHigh - close) / recentHigh * 100.0 : 0.0

// ローソク足要素

body = math.abs(close - open)

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

// =============================

// A:トレンド条件

// =============================

emaUp = emaShort > emaShort and emaMid > emaMid and emaLong > emaLong

goldenOrder = emaShort > emaMid and emaMid > emaLong

aboveEma2 = close > emaLong and close > emaLong

trendOK = emaUp and goldenOrder and aboveEma2

// =============================

// B:MACD条件

// =============================

macdGC = ta.crossover(macdLine, macdSignal)

macdNearZero = math.abs(macdLine) <= macdZeroTh

macdUp = macdLine > macdLine

macdOK = macdGC and macdNearZero and macdUp

// =============================

// C:出来高条件

// =============================

volInitOK = volRatio >= volMinRatio // 8条件用

volStrongOK = volRatio >= volStrongRatio // 三点シグナル用

volumeOK = volInitOK

// =============================

// D:ローソク足パターン

// =============================

isBullPinbar = lowerWick > wickBodyMult * body and lowerWick > upperWick and close >= open

isBullEngulf = close > open and open < close and close > open

isBigBullCross = close > emaShort and close > emaMid and open < emaShort and open < emaMid and close > open

candleOK = isBullPinbar or isBullEngulf or isBigBullCross

// =============================

// E:価格帯(押し目&レジブレ)

// =============================

pullbackOK = pullbackPct >= pullbackMin and pullbackPct <= pullbackMax

isBreakout = close > prevHigh and close <= prevHigh

barsSinceBreak = ta.barssince(isBreakout)

afterBreakZone = barsSinceBreak >= 0 and barsSinceBreak <= breakLookback

afterBreakPullbackOK = afterBreakZone and pullbackOK and close > emaShort

priceOK = pullbackOK and afterBreakPullbackOK

// =============================

// 8条件の統合

// =============================

allRulesOK = trendOK and macdOK and volumeOK and candleOK and priceOK

// =============================

// 最終三点シグナル

// =============================

longLowerWick = lowerWick > wickBodyMult * body and lowerWick > upperWick

macdGCAboveZero = ta.crossover(macdLine, macdSignal) and macdLine > 0

volumeSpike = volStrongOK

finalThreeSignal = longLowerWick and macdGCAboveZero and volumeSpike

buyConfirmed = allRulesOK and finalThreeSignal

// =====================================================

// スクリーナー用スコア(0=なし, 1=猛, 2=確)

// =====================================================

score = buyConfirmed ? 2 : (allRulesOK ? 1 : 0)

// 色分け(1行で安全な書き方)

col = score == 2 ? color.new(color.yellow, 0) : score == 1 ? color.new(color.lime, 0) : color.new(color.gray, 80)

// -----------------------------------------------------

// ① 視覚用:下パネルのカラム表示

// -----------------------------------------------------

plot(showPanel ? score : na,

title = "猛スコア(0=なし,1=猛,2=確)",

style = plot.style_columns,

color = col,

linewidth = 2)

hline(0, "なし", color=color.new(color.gray, 80))

hline(1, "猛", color=color.new(color.lime, 60))

hline(2, "確", color=color.new(color.yellow, 60))

// -----------------------------------------------------

// ② Data Window 用出力(スクリーナー風)

// -----------------------------------------------------

plot(score, title="Score_0なし1猛2確", color=color.new(color.white, 100), display=display.data_window)

plot(allRulesOK ? 1 : 0, title="A_Trend_OK", color=color.new(color.white, 100), display=display.data_window)

plot(macdOK ? 1 : 0, title="B_MACD_OK", color=color.new(color.white, 100), display=display.data_window)

plot(volumeOK ? 1 : 0, title="C_Volume_OK", color=color.new(color.white, 100), display=display.data_window)

plot(candleOK ? 1 : 0, title="D_Candle_OK", color=color.new(color.white, 100), display=display.data_window)

plot(priceOK ? 1 : 0, title="E_Price_OK", color=color.new(color.white, 100), display=display.data_window)

plot(longLowerWick ? 1 : 0, title="F_Pin下ヒゲ_OK", color=color.new(color.white, 100), display=display.data_window)

plot(macdGCAboveZero ? 1 : 0, title="G_MACDゼロ上", color=color.new(color.white, 100), display=display.data_window)

plot(volumeSpike ? 1 : 0, title="H_出来高1.5倍", color=color.new(color.white, 100), display=display.data_window)

// -----------------------------------------------------

// ③ 右上に「8条件チェック表」を表示(最終バーのみ)

// -----------------------------------------------------

var table info = table.new(position.top_right, 2, 9,

border_width = 1,

border_color = color.new(color.white, 60))

// 1行分の表示用ヘルパー

fRow(string label, bool cond, int row) =>

color bg = cond ? color.new(color.lime, 70) : color.new(color.red, 80)

string txt = cond ? "達成" : "未達"

// 左列:条件名

table.cell(info, 0, row, label, text_color = color.white, bgcolor = color.new(color.black, 0))

// 右列:結果(達成 / 未達)

table.cell(info, 1, row, txt, text_color = color.white, bgcolor = bg)

if barstate.islast and showTable

// ヘッダー(2列とも黒背景)

table.cell(info, 0, 0, "猛の掟 8条件チェック", text_color = color.white, bgcolor = color.new(color.black, 0))

table.cell(info, 1, 0, "", text_color = color.white, bgcolor = color.new(color.black, 0))

fRow("A: トレンド", trendOK, 1)

fRow("B: MACD", macdOK, 2)

fRow("C: 出来高", volumeOK, 3)

fRow("D: ローソク", candleOK, 4)

fRow("E: 押し目/レジブレ", priceOK, 5)

fRow("三点: ヒゲ", longLowerWick, 6)

fRow("三点: MACDゼロ上", macdGCAboveZero,7)

fRow("三点: 出来高1.5倍", volumeSpike, 8)

Adaptive Genesis Engine [AGE]ADAPTIVE GENESIS ENGINE (AGE)

Pure Signal Evolution Through Genetic Algorithms

Where Darwin Meets Technical Analysis

🧬 WHAT YOU'RE GETTING - THE PURE INDICATOR

This is a technical analysis indicator - it generates signals, visualizes probability, and shows you the evolutionary process in real-time. This is NOT a strategy with automatic execution - it's a sophisticated signal generation system that you control .

What This Indicator Does:

Generates Long/Short entry signals with probability scores (35-88% range)

Evolves a population of up to 12 competing strategies using genetic algorithms

Validates strategies through walk-forward optimization (train/test cycles)

Visualizes signal quality through premium gradient clouds and confidence halos

Displays comprehensive metrics via enhanced dashboard

Provides alerts for entries and exits

Works on any timeframe, any instrument, any broker

What This Indicator Does NOT Do:

Execute trades automatically

Manage positions or calculate position sizes

Place orders on your behalf

Make trading decisions for you

This is pure signal intelligence. AGE tells you when and how confident it is. You decide whether and how much to trade.

🔬 THE SCIENCE: GENETIC ALGORITHMS MEET TECHNICAL ANALYSIS

What Makes This Different - The Evolutionary Foundation

Most indicators are static - they use the same parameters forever, regardless of market conditions. AGE is alive . It maintains a population of competing strategies that evolve, adapt, and improve through natural selection principles:

Birth: New strategies spawn through crossover breeding (combining DNA from fit parents) plus random mutation for exploration

Life: Each strategy trades virtually via shadow portfolios, accumulating wins/losses, tracking drawdown, and building performance history

Selection: Strategies are ranked by comprehensive fitness scoring (win rate, expectancy, drawdown control, signal efficiency)

Death: Weak strategies are culled periodically, with elite performers (top 2 by default) protected from removal

Evolution: The gene pool continuously improves as successful traits propagate and unsuccessful ones die out

This is not curve-fitting. Each new strategy must prove itself on out-of-sample data through walk-forward validation before being trusted for live signals.

🧪 THE DNA: WHAT EVOLVES

Every strategy carries a 10-gene chromosome controlling how it interprets market data:

Signal Sensitivity Genes

Entropy Sensitivity (0.5-2.0): Weight given to market order/disorder calculations. Low values = conservative, require strong directional clarity. High values = aggressive, act on weaker order signals.

Momentum Sensitivity (0.5-2.0): Weight given to RSI/ROC/MACD composite. Controls responsiveness to momentum shifts vs. mean-reversion setups.

Structure Sensitivity (0.5-2.0): Weight given to support/resistance positioning. Determines how much price location within swing range matters.

Probability Adjustment Genes

Probability Boost (-0.10 to +0.10): Inherent bias toward aggressive (+) or conservative (-) entries. Acts as personality trait - some strategies naturally optimistic, others pessimistic.

Trend Strength Requirement (0.3-0.8): Minimum trend conviction needed before signaling. Higher values = only trades strong trends, lower values = acts in weak/sideways markets.

Volume Filter (0.5-1.5): Strictness of volume confirmation. Higher values = requires strong volume, lower values = volume less important.

Risk Management Genes

ATR Multiplier (1.5-4.0): Base volatility scaling for all price levels. Controls whether strategy uses tight or wide stops/targets relative to ATR.

Stop Multiplier (1.0-2.5): Stop loss tightness. Lower values = aggressive profit protection, higher values = more breathing room.

Target Multiplier (1.5-4.0): Profit target ambition. Lower values = quick scalping exits, higher values = swing trading holds.

Adaptation Gene

Regime Adaptation (0.0-1.0): How much strategy adjusts behavior based on detected market regime (trending/volatile/choppy). Higher values = more reactive to regime changes.

The Magic: AGE doesn't just try random combinations. Through tournament selection and fitness-weighted crossover, successful gene combinations spread through the population while unsuccessful ones fade away. Over 50-100 bars, you'll see the population converge toward genes that work for YOUR instrument and timeframe.

📊 THE SIGNAL ENGINE: THREE-LAYER SYNTHESIS

Before any strategy generates a signal, AGE calculates probability through multi-indicator confluence:

Layer 1 - Market Entropy (Information Theory)

Measures whether price movements exhibit directional order or random walk characteristics:

The Math:

Shannon Entropy = -Σ(p × log(p))

Market Order = 1 - (Entropy / 0.693)

What It Means:

High entropy = choppy, random market → low confidence signals

Low entropy = directional market → high confidence signals

Direction determined by up-move vs down-move dominance over lookback period (default: 20 bars)

Signal Output: -1.0 to +1.0 (bearish order to bullish order)

Layer 2 - Momentum Synthesis

Combines three momentum indicators into single composite score:

Components:

RSI (40% weight): Normalized to -1/+1 scale using (RSI-50)/50

Rate of Change (30% weight): Percentage change over lookback (default: 14 bars), clamped to ±1

MACD Histogram (30% weight): Fast(12) - Slow(26), normalized by ATR

Why This Matters: RSI catches mean-reversion opportunities, ROC catches raw momentum, MACD catches momentum divergence. Weighting favors RSI for reliability while keeping other perspectives.

Signal Output: -1.0 to +1.0 (strong bearish to strong bullish)

Layer 3 - Structure Analysis

Evaluates price position within swing range (default: 50-bar lookback):

Position Classification:

Bottom 20% of range = Support Zone → bullish bounce potential

Top 20% of range = Resistance Zone → bearish rejection potential

Middle 60% = Neutral Zone → breakout/breakdown monitoring

Signal Logic:

At support + bullish candle = +0.7 (strong buy setup)

At resistance + bearish candle = -0.7 (strong sell setup)

Breaking above range highs = +0.5 (breakout confirmation)

Breaking below range lows = -0.5 (breakdown confirmation)

Consolidation within range = ±0.3 (weak directional bias)

Signal Output: -1.0 to +1.0 (bearish structure to bullish structure)

Confluence Voting System

Each layer casts a vote (Long/Short/Neutral). The system requires minimum 2-of-3 agreement (configurable 1-3) before generating a signal:

Examples:

Entropy: Bullish, Momentum: Bullish, Structure: Neutral → Signal generated (2 long votes)

Entropy: Bearish, Momentum: Neutral, Structure: Neutral → No signal (only 1 short vote)

All three bullish → Signal generated with +5% probability bonus

This is the key to quality. Single indicators give too many false signals. Triple confirmation dramatically improves accuracy.

📈 PROBABILITY CALCULATION: HOW CONFIDENCE IS MEASURED

Base Probability:

Raw_Prob = 50% + (Average_Signal_Strength × 25%)

Then AGE applies strategic adjustments:

Trend Alignment:

Signal with trend: +4%

Signal against strong trend: -8%

Weak/no trend: no adjustment

Regime Adaptation:

Trending market (efficiency >50%, moderate vol): +3%

Volatile market (vol ratio >1.5x): -5%

Choppy market (low efficiency): -2%

Volume Confirmation:

Volume > 70% of 20-bar SMA: no change

Volume below threshold: -3%

Volatility State (DVS Ratio):

High vol (>1.8x baseline): -4% (reduce confidence in chaos)

Low vol (<0.7x baseline): -2% (markets can whipsaw in compression)

Moderate elevated vol (1.0-1.3x): +2% (trending conditions emerging)

Confluence Bonus:

All 3 indicators agree: +5%

2 of 3 agree: +2%

Strategy Gene Adjustment:

Probability Boost gene: -10% to +10%

Regime Adaptation gene: scales regime adjustments by 0-100%

Final Probability: Clamped between 35% (minimum) and 88% (maximum)

Why These Ranges?

Below 35% = too uncertain, better not to signal

Above 88% = unrealistic, creates overconfidence

Sweet spot: 65-80% for quality entries

🔄 THE SHADOW PORTFOLIO SYSTEM: HOW STRATEGIES COMPETE

Each active strategy maintains a virtual trading account that executes in parallel with real-time data:

Shadow Trading Mechanics

Entry Logic:

Calculate signal direction, probability, and confluence using strategy's unique DNA

Check if signal meets quality gate:

Probability ≥ configured minimum threshold (default: 65%)

Confluence ≥ configured minimum (default: 2 of 3)

Direction is not zero (must be long or short, not neutral)

Verify signal persistence:

Base requirement: 2 bars (configurable 1-5)

Adapts based on probability: high-prob signals (75%+) enter 1 bar faster, low-prob signals need 1 bar more

Adjusts for regime: trending markets reduce persistence by 1, volatile markets add 1

Apply additional filters:

Trend strength must exceed strategy's requirement gene

Regime filter: if volatile market detected, probability must be 72%+ to override

Volume confirmation required (volume > 70% of average)

If all conditions met for required persistence bars, enter shadow position at current close price

Position Management:

Entry Price: Recorded at close of entry bar

Stop Loss: ATR-based distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit: ATR-based distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Position: +1 (long) or -1 (short), only one at a time per strategy

Exit Logic:

Check if price hit stop (on low) or target (on high) on current bar

Record trade outcome in R-multiples (profit/loss normalized by ATR)

Update performance metrics:

Total trades counter incremented

Wins counter (if profit > 0)

Cumulative P&L updated

Peak equity tracked (for drawdown calculation)

Maximum drawdown from peak recorded

Enter cooldown period (default: 8 bars, configurable 3-20) before next entry allowed

Reset signal age counter to zero

Walk-Forward Tracking:

During position lifecycle, trades are categorized:

Training Phase (first 250 bars): Trade counted toward training metrics

Testing Phase (next 75 bars): Trade counted toward testing metrics (out-of-sample)

Live Phase (after WFO period): Trade counted toward overall metrics

Why Shadow Portfolios?

No lookahead bias (uses only data available at the bar)

Realistic execution simulation (entry on close, stop/target checks on high/low)

Independent performance tracking for true fitness comparison

Allows safe experimentation without risking capital

Each strategy learns from its own experience

🏆 FITNESS SCORING: HOW STRATEGIES ARE RANKED

Fitness is not just win rate. AGE uses a comprehensive multi-factor scoring system:

Core Metrics (Minimum 3 trades required)

Win Rate (30% of fitness):

WinRate = Wins / TotalTrades

Normalized directly (0.0-1.0 scale)

Total P&L (30% of fitness):

Normalized_PnL = (PnL + 300) / 600

Clamped 0.0-1.0. Assumes P&L range of -300R to +300R for normalization scale.

Expectancy (25% of fitness):

Expectancy = Total_PnL / Total_Trades

Normalized_Expectancy = (Expectancy + 30) / 60

Clamped 0.0-1.0. Rewards consistency of profit per trade.

Drawdown Control (15% of fitness):

Normalized_DD = 1 - (Max_Drawdown / 15)

Clamped 0.0-1.0. Penalizes strategies that suffer large equity retracements from peak.

Sample Size Adjustment

Quality Factor:

<50 trades: 1.0 (full weight, small sample)

50-100 trades: 0.95 (slight penalty for medium sample)

100 trades: 0.85 (larger penalty for large sample)

Why penalize more trades? Prevents strategies from gaming the system by taking hundreds of tiny trades to inflate statistics. Favors quality over quantity.

Bonus Adjustments

Walk-Forward Validation Bonus:

if (WFO_Validated):

Fitness += (WFO_Efficiency - 0.5) × 0.1

Strategies proven on out-of-sample data receive up to +10% fitness boost based on test/train efficiency ratio.

Signal Efficiency Bonus (if diagnostics enabled):

if (Signals_Evaluated > 10):

Pass_Rate = Signals_Passed / Signals_Evaluated

Fitness += (Pass_Rate - 0.1) × 0.05

Rewards strategies that generate high-quality signals passing the quality gate, not just profitable trades.

Final Fitness: Clamped at 0.0 minimum (prevents negative fitness values)

Result: Elite strategies typically achieve 0.50-0.75 fitness. Anything above 0.60 is excellent. Below 0.30 is prime candidate for culling.

🔬 WALK-FORWARD OPTIMIZATION: ANTI-OVERFITTING PROTECTION

This is what separates AGE from curve-fitted garbage indicators.

The Three-Phase Process

Every new strategy undergoes a rigorous validation lifecycle:

Phase 1 - Training Window (First 250 bars, configurable 100-500):

Strategy trades normally via shadow portfolio

All trades count toward training performance metrics

System learns which gene combinations produce profitable patterns

Tracks independently: Training_Trades, Training_Wins, Training_PnL

Phase 2 - Testing Window (Next 75 bars, configurable 30-200):

Strategy continues trading without any parameter changes

Trades now count toward testing performance metrics (separate tracking)

This is out-of-sample data - strategy has never seen these bars during "optimization"

Tracks independently: Testing_Trades, Testing_Wins, Testing_PnL

Phase 3 - Validation Check:

Minimum_Trades = 5 (configurable 3-15)

IF (Train_Trades >= Minimum AND Test_Trades >= Minimum):

WR_Efficiency = Test_WinRate / Train_WinRate

Expectancy_Efficiency = Test_Expectancy / Train_Expectancy

WFO_Efficiency = (WR_Efficiency + Expectancy_Efficiency) / 2

IF (WFO_Efficiency >= 0.55): // configurable 0.3-0.9

Strategy.Validated = TRUE

Strategy receives fitness bonus

ELSE:

Strategy receives 30% fitness penalty

ELSE:

Validation deferred (insufficient trades in one or both periods)

What Validation Means

Validated Strategy (Green "✓ VAL" in dashboard):

Performed at least 55% as well on unseen data compared to training data

Gets fitness bonus: +(efficiency - 0.5) × 0.1

Receives priority during tournament selection for breeding

More likely to be chosen as active trading strategy

Unvalidated Strategy (Orange "○ TRAIN" in dashboard):

Failed to maintain performance on test data (likely curve-fitted to training period)

Receives 30% fitness penalty (0.7x multiplier)

Makes strategy prime candidate for culling

Can still trade but with lower selection probability

Insufficient Data (continues collecting):

Hasn't completed both training and testing periods yet

OR hasn't achieved minimum trade count in both periods

Validation check deferred until requirements met

Why 55% Efficiency Threshold?

If a strategy earned 10R during training but only 5.5R during testing, it still proved an edge exists beyond random luck. Requiring 100% efficiency would be unrealistic - market conditions change between periods. But requiring >50% ensures the strategy didn't completely degrade on fresh data.

The Protection: Strategies that work great on historical data but fail on new data are automatically identified and penalized. This prevents the population from being polluted by overfitted strategies that would fail in live trading.

🌊 DYNAMIC VOLATILITY SCALING (DVS): ADAPTIVE STOP/TARGET PLACEMENT

AGE doesn't use fixed stop distances. It adapts to current volatility conditions in real-time.

Four Volatility Measurement Methods

1. ATR Ratio (Simple Method):

Current_Vol = ATR(14) / Close

Baseline_Vol = SMA(Current_Vol, 100)

Ratio = Current_Vol / Baseline_Vol

Basic comparison of current ATR to 100-bar moving average baseline.

2. Parkinson (High-Low Range Based):

For each bar: HL = log(High / Low)

Parkinson_Vol = sqrt(Σ(HL²) / (4 × Period × log(2)))

More stable than close-to-close volatility. Captures intraday range expansion without overnight gap noise.

3. Garman-Klass (OHLC Based):

HL_Term = 0.5 × ²

CO_Term = (2×log(2) - 1) × ²

GK_Vol = sqrt(Σ(HL_Term - CO_Term) / Period)

Most sophisticated estimator. Incorporates all four price points (open, high, low, close) plus gap information.

4. Ensemble Method (Default - Median of All Three):

Ratio_1 = ATR_Current / ATR_Baseline

Ratio_2 = Parkinson_Current / Parkinson_Baseline

Ratio_3 = GK_Current / GK_Baseline

DVS_Ratio = Median(Ratio_1, Ratio_2, Ratio_3)

Why Ensemble?

Takes median to avoid outliers and false spikes

If ATR jumps but range-based methods stay calm, median prevents overreaction

If one method fails, other two compensate

Most robust approach across different market conditions

Sensitivity Scaling

Scaled_Ratio = (Raw_Ratio) ^ Sensitivity

Sensitivity 0.3: Cube root - heavily dampens volatility impact

Sensitivity 0.5: Square root - moderate dampening

Sensitivity 0.7 (Default): Balanced response to volatility changes

Sensitivity 1.0: Linear - full 1:1 volatility impact

Sensitivity 1.5: Exponential - amplified response to volatility spikes

Safety Clamps: Final DVS Ratio always clamped between 0.5x and 2.5x baseline to prevent extreme position sizing or stop placement errors.

How DVS Affects Shadow Trading

Every strategy's stop and target distances are multiplied by the current DVS ratio:

Stop Loss Distance:

Stop_Distance = ATR × ATR_Mult (gene) × Stop_Mult (gene) × DVS_Ratio

Take Profit Distance:

Target_Distance = ATR × ATR_Mult (gene) × Target_Mult (gene) × DVS_Ratio

Example Scenario:

ATR = 10 points

Strategy's ATR_Mult gene = 2.5

Strategy's Stop_Mult gene = 1.5

Strategy's Target_Mult gene = 2.5

DVS_Ratio = 1.4 (40% above baseline volatility - market heating up)

Stop = 10 × 2.5 × 1.5 × 1.4 = 52.5 points (vs. 37.5 in normal vol)

Target = 10 × 2.5 × 2.5 × 1.4 = 87.5 points (vs. 62.5 in normal vol)

Result:

During volatility spikes: Stops automatically widen to avoid noise-based exits, targets extend for bigger moves

During calm periods: Stops tighten for better risk/reward, targets compress for realistic profit-taking

Strategies adapt risk management to match current market behavior

🧬 THE EVOLUTIONARY CYCLE: SPAWN, COMPETE, CULL

Initialization (Bar 1)

AGE begins with 4 seed strategies (if evolution enabled):

Seed Strategy #0 (Balanced):

All sensitivities at 1.0 (neutral)

Zero probability boost

Moderate trend requirement (0.4)

Standard ATR/stop/target multiples (2.5/1.5/2.5)

Mid-level regime adaptation (0.5)

Seed Strategy #1 (Momentum-Focused):

Lower entropy sensitivity (0.7), higher momentum (1.5)

Slight probability boost (+0.03)

Higher trend requirement (0.5)

Tighter stops (1.3), wider targets (3.0)

Seed Strategy #2 (Entropy-Driven):

Higher entropy sensitivity (1.5), lower momentum (0.8)

Slight probability penalty (-0.02)

More trend tolerant (0.6)

Wider stops (1.8), standard targets (2.5)

Seed Strategy #3 (Structure-Based):

Balanced entropy/momentum (0.8/0.9), high structure (1.4)

Slight probability boost (+0.02)

Lower trend requirement (0.35)

Moderate risk parameters (1.6/2.8)

All seeds start with WFO validation bypassed if WFO is disabled, or must validate if enabled.

Spawning New Strategies

Timing (Adaptive):

Historical phase: Every 30 bars (configurable 10-100)

Live phase: Every 200 bars (configurable 100-500)

Automatically switches to live timing when barstate.isrealtime triggers

Conditions:

Current population < max population limit (default: 8, configurable 4-12)

At least 2 active strategies exist (need parents)

Available slot in population array

Selection Process:

Run tournament selection 3 times with different seeds

Each tournament: randomly sample active strategies, pick highest fitness

Best from 3 tournaments becomes Parent 1

Repeat independently for Parent 2

Ensures fit parents but maintains diversity

Crossover Breeding:

For each of 10 genes:

Parent1_Fitness = fitness

Parent2_Fitness = fitness

Weight1 = Parent1_Fitness / (Parent1_Fitness + Parent2_Fitness)

Gene1 = parent1's value

Gene2 = parent2's value

Child_Gene = Weight1 × Gene1 + (1 - Weight1) × Gene2

Fitness-weighted crossover ensures fitter parent contributes more genetic material.

Mutation:

For each gene in child:

IF (random < mutation_rate):

Gene_Range = GENE_MAX - GENE_MIN

Noise = (random - 0.5) × 2 × mutation_strength × Gene_Range

Mutated_Gene = Clamp(Child_Gene + Noise, GENE_MIN, GENE_MAX)

Historical mutation rate: 20% (aggressive exploration)

Live mutation rate: 8% (conservative stability)

Mutation strength: 12% of gene range (configurable 5-25%)

Initialization of New Strategy:

Unique ID assigned (total_spawned counter)

Parent ID recorded

Generation = max(parent generations) + 1

Birth bar recorded (for age tracking)

All performance metrics zeroed

Shadow portfolio reset

WFO validation flag set to false (must prove itself)

Result: New strategy with hybrid DNA enters population, begins trading in next bar.

Competition (Every Bar)

All active strategies:

Calculate their signal based on unique DNA

Check quality gate with their thresholds

Manage shadow positions (entries/exits)

Update performance metrics

Recalculate fitness score

Track WFO validation progress

Strategies compete indirectly through fitness ranking - no direct interaction.

Culling Weak Strategies

Timing (Adaptive):

Historical phase: Every 60 bars (configurable 20-200, should be 2x spawn interval)

Live phase: Every 400 bars (configurable 200-1000, should be 2x spawn interval)

Minimum Adaptation Score (MAS):

Initial MAS = 0.10

MAS decays: MAS × 0.995 every cull cycle

Minimum MAS = 0.03 (floor)

MAS represents the "survival threshold" - strategies below this fitness level are vulnerable.

Culling Conditions (ALL must be true):

Population > minimum population (default: 3, configurable 2-4)

At least one strategy has fitness < MAS

Strategy's age > culling interval (prevents premature culling of new strategies)

Strategy is not in top N elite (default: 2, configurable 1-3)

Culling Process:

Find worst strategy:

For each active strategy:

IF (age > cull_interval):

Fitness = base_fitness

IF (not WFO_validated AND WFO_enabled):

Fitness × 0.7 // 30% penalty for unvalidated

IF (Fitness < MAS AND Fitness < worst_fitness_found):

worst_strategy = this_strategy

worst_fitness = Fitness

IF (worst_strategy found):

Count elite strategies with fitness > worst_fitness

IF (elite_count >= elite_preservation_count):

Deactivate worst_strategy (set active flag = false)

Increment total_culled counter

Elite Protection:

Even if a strategy's fitness falls below MAS, it survives if fewer than N strategies are better. This prevents culling when population is generally weak.

Result: Weak strategies removed from population, freeing slots for new spawns. Gene pool improves over time.

Selection for Display (Every Bar)

AGE chooses one strategy to display signals:

Best fitness = -1

Selected = none

For each active strategy:

Fitness = base_fitness

IF (WFO_validated):

Fitness × 1.3 // 30% bonus for validated strategies

IF (Fitness > best_fitness):

best_fitness = Fitness

selected_strategy = this_strategy

Display selected strategy's signals on chart

Result: Only the highest-fitness (optionally validated-boosted) strategy's signals appear as chart markers. Other strategies trade invisibly in shadow portfolios.

🎨 PREMIUM VISUALIZATION SYSTEM