Advanced VWAP CalendarThe Advanced VWAP Calendar is a designed to plot Volume Weighted Average Price (VWAP) lines anchored to user-defined and preset time periods, including weekly, monthly, quarterly, and custom anchors. As of August 15, 2025, this indicator provides traders with a robust tool for analyzing price trends relative to volume-weighted averages, with clear labeling and extensive customization options. Below is a summary of its key features and functionality, with technical details and code references updated to focus on user-facing behavior and presentation, while preserving all other aspects of the original summary.

Key Features

Multiple Time Period VWAPs:

Weekly VWAPs: Supports up to five VWAPs for a user-selected month and year, starting at midnight each Monday (e.g., W1 Aug 2025, W2 Aug 2025). Enabled via a single toggle, with anchors automatically set to the first Monday of the chosen month.

Monthly VWAPs: Plots VWAPs for all 12 months of a selected year (e.g., Jan 2025, Feb 2025) or a single user-specified month/year. Labels use month abbreviations (e.g., "Aug 2025").

Quarterly VWAPs: Covers four quarters of a selected year (e.g., Q1 2025, Q2 2025), with options to enable all quarters or individual ones (Q1–Q4).

Legacy VWAPs: Provides monthly and quarterly VWAPs for a user-selected legacy year (e.g., 2024), labeled with a "Legacy" prefix (e.g., "Legacy Jan 2024," "Legacy Q1 2024"), with similar enablement options.

Custom VWAPs: Includes 10 fully customizable VWAPs, each with user-defined anchor times, labels (e.g., "Q1 2025"), colors, line widths (1–5), text colors, bubble styles, text sizes (8–40), and background options.

Clear and Dynamic Labeling:

Labels appear to the right of the chart, showing the VWAP value (e.g., "Q1 2025 123.45").

Weekly labels follow a "W# Month Year" format (e.g., "W1 Aug 2025").

Monthly labels use abbreviated months (e.g., "Aug 2025"), while quarterly labels use "Q# Year" (e.g., "Q3 2025").

Legacy labels include a "Legacy" prefix (e.g., "Legacy Q1 2024").

Labels support customizable text sizes (tiny to huge) and can be displayed with or without a background, with optional bubble styles.

Flexible Customization:

Each VWAP can be enabled or disabled independently, with user inputs for anchor times, labels, and visual properties.

Colors are predefined for weekly (red, orange, blue, green, purple), monthly (varied), quarterly (red, blue, green, yellow), and legacy VWAPs, but custom VWAPs allow any color selection.

Line widths and text sizes are adjustable, ensuring visual clarity and chart readability.

This indicator was a dual effort, code was heavily contributed in effort by AzDxB, major credit and THANKS goes to him www.tradingview.com

Cerca negli script per "特斯拉+2025年4月7日至2025年5月7日+股价走势"

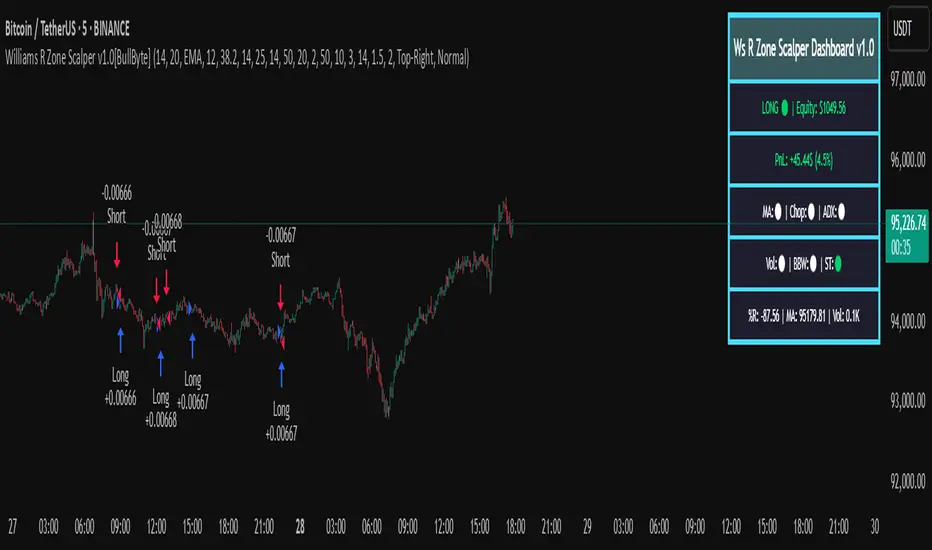

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.

- Forex majors : Raise `chopThr` to ~42.

- Stocks/high-beta : Enable `useBBW`.

- Enable SL/TP : Toggle `useSL`; stop-loss = 1.5×ATR, take-profit = 2×ATR apply automatically.

---

Common Questions

- * Why not trade every Williams R reversal?*

Raw Williams R whipsaws in sideways markets. Choppiness and volume filters reduce false entries.

- *Can I use on 1 min or 15 min?*

Yes—adjust ATR length or thresholds accordingly. Defaults target 5 min scalping.

- *What if all filters are on?*

Fewer arrows, higher-quality signals. Expect ~10 % boost in average win size.

---

Disclaimer & License

Trading carries risk of loss. Use this script “as is” under the Mozilla Public License 2.0 (mozilla.org). Always backtest, paper-trade, and adjust risk settings to your own profile.

---

Credits & References

- Pine Script v6, using TradingView’s built-in `ta.supertrend()`.

- TradingView House Rules: www.tradingview.com

Goodluck!

BullByte

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades