Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Cerca negli script per "电力行业+股票+11年涨幅"

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

Moving Averages & Bollinger Bands with ForecastsMoving Averages & Bollinger Bands with Forecasts

11 Moving Averages

SMA, EMA, WMA

Highly Customizable

Linear Regression Forecast

Bollonger Bands

Personal Setup: Add indicator twice

1st indicator = SMA using #4, 7, 10, 11 (20, 50, 100, 200 SMAs) with bollonger bands on 20.

2nd indicator = EMA using #1, 2, 3, 5, 6, 8, 9 (5, 8, 13, 21 ,34, 55, 89 EMAs).

This allows easy toggling between SMAs/Bolls and Fib EMAs

Thank you to yatrader2 for the forecast code

[astropark] MACD, RSI+, AO, DMI, ADX, OBV, ADI//******************************************************************************

// Copyright by astropark v4.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV, ADI

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

// 14/01/2019 Added Accelerator Decelerator Indicator (ADI)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV//******************************************************************************

// Copyright by astropark v4.0.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX, OBV

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Oscillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

// 14/01/2019 Added On Balance Volume (OBV)

//******************************************************************************

[astropark] MACD, RSI+, Awesome Oscillator, DMI with ADX//******************************************************************************

// Copyright by astropark v3.1.0

// MACD, RSI+, Awesome Oscillator, DMI, ADX

// 24/10/2018 Added RSI with Center line to have clear glue of current trend

// 10/12/2018 Added MACD

// 13/12/2018 Added multiplier for MACD in order to make it clearly visible over RSI graph

// 11/01/2019 Added Awesome Ascillator (AO)

// 11/01/2019 Added Directional Movement Index (DMI) with ADX

//******************************************************************************

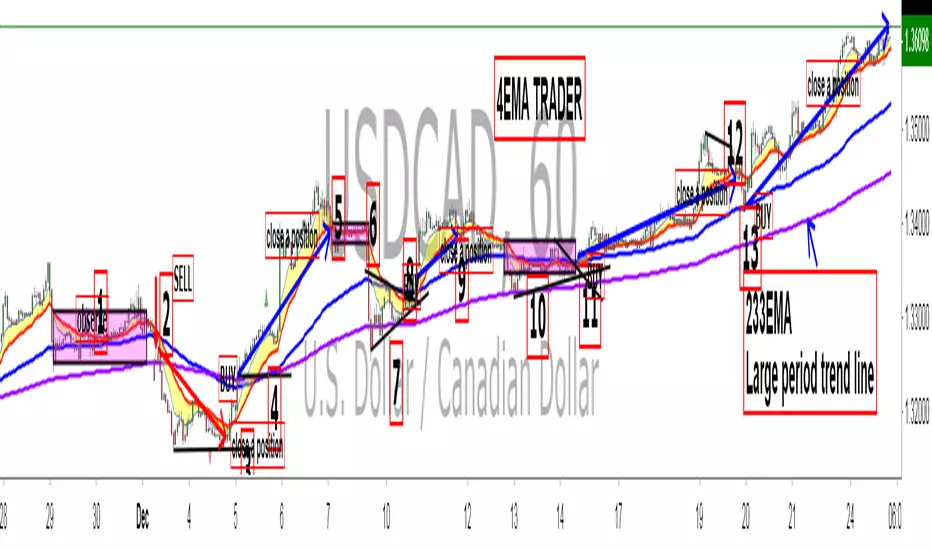

King 4EMA TraderKing 4EMA trader 8/21/89EMA+(233)V3.3

Explain the application of moving averages through the disk surface:

When the price runs above 89, it only looks for the buy signal.

When the price runs below 89, it only looks for sell signals.

The first step up through the 89 moving average after the first confirmation can buy homeoply,

The first pull down after crossing the 89 moving average for the first time confirms that it can be sold in line with the trend.

Price horizontal finishing, moving average frequently across the field observation.

The yellow area in the interval from 8 to 21 is the homeopathic warehouse addition signal.

When the price is above the 89 moving average, the k-line closes below the 21-day moving average as a callback signal

Prices below the 89 ema close above the 21 - day ema as a rebound signal

After the correction and rebound signals come out, we should make half of the profit and the other half of the stop loss in the break-even place.

Moving average is very suitable for the trend of strong varieties, is not suitable for volatile market.

Only at the end of the shock market moving average upward or downward divergent when it is possible to be used.

1. Repeatedly entangle the mean line of horizontal disk stage and observe it from the field

2. Sell the three EMA moving averages when they can't exceed 89EMA with downward crossing

3, many times can not break the new low when prices go sideways profit

4. Buy when the price reaches 89EMA after the convergence of triangle 3 is broken

5, the Angle of price rise slowed and closed below the 21 moving average when profit

6. Left field observation during transverse oscillation.

Sit tight while news or data cause prices to fall quickly

8. Buy when the price triangle breaks through the 89 moving average upward

9, the price does not rise to slow down when the horizontal closed below the 21 moving average when profit

10, price horizontal shock finishing at the same time the average line also transverse finishing field observation

11, the price of the triangle after finishing through the 89 moving average to buy.At this point all the averages have turned up

12, the second time can not break through the new high when the negative line can profit

13, the price of the first time in the same period of time through 89 after the first step back can be re-bought.

通过盘面讲解均线运用:

价格在89上面运行时时只找买入信号、

价格在89下面运行时只寻找卖出信号、

第一次向上穿过89均线后的第一次回踩确认可以顺势买入、

第一次向下穿过89均线后的第一次回抽确认可以顺势卖出、

价格横盘整理,均线频繁穿越时离场观察。

8-21区间里面黄色区域为顺势加仓信号,

价格在89均线上面时K线收盘在21天均线下面时为回调信号

价格在89均线下面时K线收盘在21天均线上面时为反弹信号

在回调和反弹信号出来之后我们应该获利一半的头寸,另外一半止损放到盈亏平衡的地方。

均线非常适合趋势性很强的品种,并不适合震荡行情。

只有在震荡行情结束时均线向上或向下发散时才有被运用的可能。

1、横盘阶段均线反复纠缠,离场观察

2、三条EMA均线向下交叉回抽无法超越89EMA时卖出

3、多次不能破新低时价格走横时获利

4、价格在3处三角形收敛被突破后站上了89EMA时买入

5、价格上涨角度变缓并收盘在21均线下面时获利

6、横盘震荡时离场观察。

7、见死不救新闻或数据导致价格快速下跌时观望

8、价格三角形向上突破时穿过89均线时买入

9、价格不升减速走横时收盘于21均线下面时获利

10、价格横盘震荡整理同时均线也横向整理时离场观察

11、价格突破三角形整理后重新穿过89均线时买入。此时所有均线已经向上翘头

12、第二次不能突破新高时收阴线可以获利

13、价格在同一个时间周期内第一次穿过89以后的第一次回踩可以重新买入。

Bitfinex Longs/Shorts Multi-Coin [acatwithcharts]This script plots the longs/shorts ratio derived from Bitfinex for BTCUSDLONGS, BTCUSDSHORTS, and similar for 11 top cryptocurrencies chosen selected based on marketcap, trading volume on Bitfinex, and the maximum number of times that TradingView would let me call the "security" function in one script. Included coins:

BTC, ETH, LTC, BCH, XRP, EOS, IOT (IOTA), ETC, ZEC, NEO, XMR

In addition to just plotting the ratios for the individual coins, this script also calculates for a customizable selection of the 11 coins both the average ratio and a weighted average weighted by (USD price of coin * sum of long and short positions).

I wrote it both to use both for a big picture overview of leveraged positions across major coins and to use as a Swiss army knife of longs/shorts ratio indicators for individual coins, most of which do not currently have individual scripts published.

I'm an amateur and you definitely shouldn't take anything I say or use any of my scripts as financial advice. I'd appreciate any feedback.

Stochastic Momentum IndexStochastic Momentum Index indicator script. This indicator was originally developed by William Blau (Stocks & Commodities V. 11:1 (11-18)).

67Major Market Trading Hours

New York Stock Exchange (NYSE)

Open: 9:30 AM (ET)

Close: 4:00 PM (ET)

Pre-Market: 4:00 AM – 9:30 AM (ET)

After Hours: 4:00 PM – 8:00 PM (ET)

Nasdaq

Open: 9:30 AM (ET)

Close: 4:00 PM (ET)

Pre-Market: 4:00 AM – 9:30 AM (ET)

After Hours: 4:00 PM – 8:00 PM (ET)

London Stock Exchange (LSE)

Open: 8:00 AM (GMT)

Close: 4:30 PM (GMT)

Tokyo Stock Exchange (TSE)

Open: 9:00 AM (JST)

Lunch Break: 11:30 AM – 12:30 PM (JST)

Close: 3:00 PM (JST)

Hong Kong Stock Exchange (HKEX)

Open: 9:30 AM (HKT)

Lunch Break: 12:00 PM – 1:00 PM (HKT)

Close: 4:00 PM (HKT)

If you'd like anything bigger, bold, color‑coded, or reorganized, just tell me and I’ll adjust it!

Crypto Signals & Overlays –29-11-2025Nebula Crypto Signals & Overlays

Nebula is a multi-timeframe trend and momentum indicator designed for high-cap crypto pairs (BTC, ETH, SOL, DOGE, etc.).

• Uses 21/50/200 EMAs + higher-timeframe EMA for trend filtering

• RSI and Bollinger Bands for momentum and squeeze detection

• Generates BUY/SELL labels on trend-side pullbacks

• ATR line as a dynamic stop/target guide, plus pivot-based support/resistance zones

• Background colors: green = bullish regime, red = bearish regime, yellow = low-volatility squeeze

Not financial advice. Always backtest and use proper risk management before trading live.

MA均线全仓回测//@version=5

strategy("39日MA均线全仓交易策略 (2017-2025)",

overlay=true,

initial_capital=1000,

commission_type=strategy.commission.percent,

commission_value=0.1,

pyramiding=0)

// 策略参数

startDate = input.time(timestamp("2017-08-01T00:00:00"), title="回测开始日期")

endDate = input.time(timestamp("2025-11-11T23:59:59"), title="回测结束日期")

maLength = input.int(39, title="MA周期", minval=1)

useSMA = input.bool(true, title="使用SMA(简单移动平均)")

// 计算移动平均线

maValue = useSMA ? ta.sma(close, maLength) : ta.ema(close, maLength)

// 绘制MA线

plot(maValue, color=color.new(color.blue, 0), linewidth=2, title="39日MA")

// 确定是否在回测时间范围内

inDateRange = time >= startDate and time <= endDate

// 交易逻辑 - 全仓交易

if inDateRange

// 生成交易信号:价格上穿MA时全仓买入,下穿MA时全仓卖出

longCondition = ta.crossover(close, maValue)

shortCondition = ta.crossunder(close, maValue)

// 执行交易 - 全仓操作

if longCondition

strategy.entry("全仓买入", strategy.long, qty=strategy.equity/close)

if shortCondition

strategy.close("全仓买入", comment="全仓卖出")

// 在回测时间范围外显示背景色

bgcolor(inDateRange ? color.new(color.green, 95) : na, title="回测期间背景")

// 添加性能统计和资金曲线

var float totalReturn = 0.0

if barstate.islast and inDateRange

totalReturn := ((strategy.netprofit + 1000) / 1000 - 1) * 100

label.new(bar_index, high,

text="回测结果:\n初始资金: 1000 USDT\n最终权益: " + str.tostring(strategy.netprofit + 1000, "#.##") + " USDT\n总收益率: " + str.tostring(totalReturn, "#.##") + "%\n总交易次数: " + str.tostring(strategy.closedtrades) + "次",

style=label.style_label_down, color=color.new(color.blue, 80), textcolor=color.white, size=size.normal)

// 绘制权益曲线

plot(strategy.equity, title="资金曲线", color=color.new(color.purple, 0), linewidth=1, trackprice=true)

BybitMinOrderSizeBybit Order Quantity Compliance Library

This library provides all utility functions required for TradingView strategies

that execute orders on Bybit via webhooks.

Problem:

Bybit enforces two strict rules on every order submitted:

Minimum Order Size – each symbol has its own minimum quantity.

Quantity Precision – each symbol requires rounding to the correct number of decimals.

TradingView does not expose this metadata, so strategies can easily submit

quantities that Bybit rejects as invalid.

Solution (This Library):

This library embeds full Bybit contract metadata, including:

A complete mapping of Bybit symbols → minimum order size

A complete mapping of Bybit symbols → allowed precision (decimal places)

A helper to normalize tickers (removing `.P` suffix for Bybit perpetuals)

It also exposes utility functions to automatically make your quantities valid:

`normalizeTicker()` — removes `.P` for consistent lookup

`getMinOrderSize()` — returns the correct minimum order size

`getPrecisionForTicker()` — returns required quantity precision

`floorQty()` — floors quantities to valid minimum increments

`roundQty()` — rounds quantities to valid decimal precision

Use Cases:

Ensuring webhook strategies never send too-small orders

Rounding limit/market orders correctly before execution

Making Pine strategies execution-accurate for Bybit

Avoiding "order rejected: qty too small / invalid precision" errors

This library is recommended for:

Live trading via TradingView → Bybit webhooks

Backtesting strategies that simulate real Bybit constraints

Source: www.bybit.com

Updated: 2025-11-25 — Bybit contract metadata

normalizeTicker(symbol)

Normalizes Bybit perpetual tickers by removing the ".P" suffix.

precisionFromMinOrder(minOrder)

Derives precision (decimal places) from minimum order size.

getMinOrderSize(symbol)

Retrieves the minimum order size for the current or given symbol.

getPrecisionForTicker(symbol)

Retrieves the required quantity precision (decimal places) for a given Bybit symbol.

floorQty(qty, symbol)

Rounds a quantity down to the nearest valid minimum order size for a given symbol.

roundQty(qty, symbol)

Rounds a quantity to the valid precision for the specified symbol.

Kernel Regression Trend LineKTrend – Non-Repainting Kernel Regression Trend (2025 Clean Version)

Ultra-clean, powerful, and completely non-repainting trend-following tool based on advanced Kernel regression (Rational Quadratic + Gaussian blend).

How it works:

• Uses two different kernel estimates with smart lag to detect genuine trend reversals

• Plots a thick, beautifully colored trend line (teal when rising, deep red when falling)

• Places precise, locked-in Bullish Flip (green triangle below bar) and Bearish Flip (red triangle above bar) signals only on confirmed bar close – zero repaint, ever

• Optional smoothing mode for even cleaner visuals

Features

✓ 100% non-repainting signals and line

✓ Minimal lag while staying extremely responsive

✓ Clean aesthetic – perfect for BTC, ETH, stocks, forex, any timeframe

✓ Built-in alerts for Bullish & Bearish flips

✓ Fully open source (MPL 2.0)

Default settings are already battle-tested and loved by thousands:

- Lookback Window: 11

- Relative Weighting: 8.0

- Regression Level: 25

- Lag: 2

Great on 1H–Daily charts, especially crypto and indices.

Credits: Original kernel library by jdehorty, cleaned & enhanced flip logic by HighlanderOne.

Enjoy the smoothest, most reliable kernel trend tool on TradingView – completely free!

BTC Energy + HR + Longs + M2

BTC Energy Ratio + Hashrate + Longs + M2

The #1 Bitcoin Macro Weapon on TradingView 🚀🔥

If you’re tired of getting chopped by fakeouts, ETF noise, and Twitter hopium — this is the one chart that finally puts you on the right side of every major move.

What you’re looking at:

Orange line → Bitcoin priced in real-world mining energy (Oil × Gas + Uranium × Coal) × 1000

→ The true fundamental floor of BTC

Blue line → Scaled hashrate trend (miner strength & capex lag)

Green line → Bitfinex longs EMA (leveraged bull sentiment)

Purple line → Global M2 money supply (US+EU+CN+JP) with 10-week lead (the liquidity wave BTC rides)

Why this indicator prints money:

Most tools react to price.

This one predicts where price is going based on energy, miners, leverage, and liquidity — the only four things that actually drive Bitcoin long-term.

It has nailed:

2022 bottom at ~924 📉

2024 breakout above 12,336 🚀

2025 top at 17,280 🏔️

And right now it’s flashing generational accumulation at ~11,500 (Nov 2025)

13 permanent levels with right-side labels — no guessing what anything means:

20,000 → 2021 Bull ATH

17,280 → 2025 ATH

15,000 → 2024 High Resist

14,000 → Overvalued Zone

13,000 → 2024 Breakout

12,336 → Bull/Bear Line (the most important level)

12,000 → 2024 Volume POC

10,930 → Key Support 2024

9,800 → Strong Buy Fib

8,000 → Deep Support 2023

6,000 → 2021 Mid-Cycle

4,500 → 2023 Accum Low

924 → 2022 Bear Low

Live dashboard tells you exactly what to do — no thinking required:

Current ratio (updates live)

Hashrate + 24H %

Longs trend

Risk Mode → Orange vs Hashrate (RISK ON / RISK OFF)

180-day correlation

RSI

13-tier Zone + SIGNAL (STRONG BUY / ACCUMULATE / HOLD / DISTRIBUTE / EXTREME SELL)

Dead-simple rules that actually work:

Weekly timeframe = cleanest view

Blue peaking + orange holding support → miner pain = next leg up

Green spiking + orange failing → overcrowded longs = trim

Purple rising → liquidity coming in = ride the wave

Risk Mode = RISK OFF → price is cheap vs miners → buy

Set these 3 alerts and walk away:

Ratio > 12,336 → Bull confirmed → add

Ratio > 14,000 → Start scaling out

Ratio < 9,800 → Generational buy → back up the truck

No repainting • Fully open-source • Forced daily data • Works on any TF

Energy is the only real backing Bitcoin has.

Hashrate lag is the best leading indicator.

Longs show greed.

M2 is the tide.

This chart combines all four — and right now it’s screaming ACCUMULATE.

Load it. Trust it.

Stop trading hope. Start trading reality.

DYOR • NFA • For entertainment purposes only 😎

#bitcoin #macro #energy #hashrate #m2 #cycle #riskon #riskoff

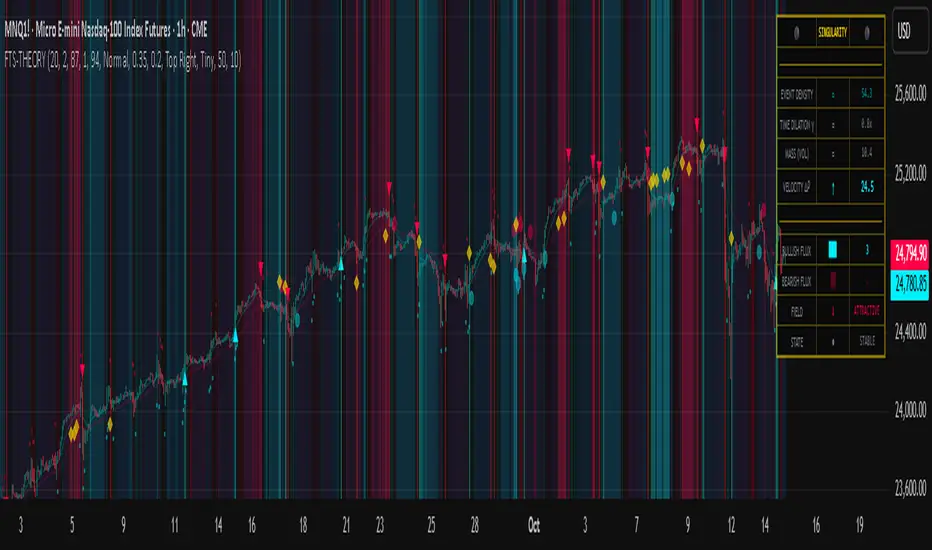

Flux-Tensor Singularity [FTS]Flux-Tensor Singularity - Multi-Factor Market Pressure Indicator

The Flux-Tensor Singularity (FTS) is an advanced multi-factor oscillator that combines volume analysis, momentum tracking, and volatility-weighted normalization to identify critical market inflection points. Unlike traditional single-factor indicators, FTS synthesizes price velocity, volume mass, and volatility context into a unified framework that adapts to changing market regimes.

This indicator identifies extreme market conditions (termed "singularities") where multiple confirming factors converge, then uses a sophisticated scoring system to determine directional bias. It is designed for traders seeking high-probability setups with built-in confluence requirements.

THEORETICAL FOUNDATION

The indicator is built on the premise that market time is not constant - different market conditions contain varying levels of information density. A 1-minute bar during a major news event contains far more actionable information than a 1-minute bar during overnight low-volume trading. Traditional indicators treat all bars equally; FTS does not.

The theoretical framework draws conceptual parallels to physics (purely as a mental model, not literal physics):

Volume as Mass: Large volume represents significant market participation and "weight" behind price moves. Just as massive objects have stronger gravitational effects, high-volume moves carry more significance.

Price Change as Velocity: The rate of price movement through price space represents momentum and directional force.

Volatility as Time Dilation: When volatility is high relative to its historical norm, the "information density" of each bar increases. The indicator weights these periods more heavily, similar to how time dilates near massive objects in physics.

This is a pedagogical metaphor to create a coherent mental model - the underlying mathematics are standard financial calculations combined in a novel way.

MATHEMATICAL FRAMEWORK

The indicator calculates a composite singularity value through four distinct steps:

Step 1: Raw Singularity Calculation

S_raw = (ΔP × V) × γ²

Where:

ΔP = Price Velocity = close - close

V = Volume Mass = log(volume + 1)

γ² = Time Dilation Factor = (ATR_local / ATR_global)²

Volume Transformation: Volume is log-transformed because raw volume can have extreme outliers (10x-100x normal). The logarithm compresses these spikes while preserving their significance. This is standard practice in volume analysis.

Volatility Weighting: The ratio of short-term ATR (5 periods) to long-term ATR (user-defined lookback) is squared to create a volatility amplification factor. When local volatility exceeds global volatility, this ratio increases, amplifying the raw singularity value. This makes the indicator regime-aware.

Step 2: Normalization

The raw singularity values are normalized to a 0-100 scale using a stochastic-style calculation:

S_normalized = ((S_raw - S_min) / (S_max - S_min)) × 100

Where S_min and S_max are the lowest and highest raw singularity values over the lookback period.

Step 3: Epsilon Compression

S_compressed = 50 + ((S_normalized - 50) / ε)

This is the critical innovation that makes the sensitivity control functional. By applying compression AFTER normalization, the epsilon parameter actually affects the final output:

ε < 1.0: Expands range (more signals)

ε = 1.0: No change (default)

ε > 1.0: Compresses toward 50 (fewer, higher-quality signals)

For example, with ε = 2.0, a normalized value of 90 becomes 70, making threshold breaches rarer and more significant.

Step 4: Smoothing

S_final = EMA(S_compressed, smoothing_period)

An exponential moving average removes high-frequency noise while preserving trend.

SIGNAL GENERATION LOGIC

When the tensor crosses above the upper threshold (default 90) or below the lower threshold (default 10), an extreme event is detected. However, the indicator does NOT immediately generate a buy or sell signal. Instead, it analyzes market context through a multi-factor scoring system:

Scoring Components:

Price Structure (+1 point): Current bar bullish/bearish

Momentum (+1 point): Price higher/lower than N bars ago

Trend Context (+2 points): Fast EMA above/below slow EMA (weighted heavier)

Acceleration (+1 point): Rate of change increasing/decreasing

Volume Multiplier (×1.5): If volume > average, multiply score

The highest score (bullish vs bearish) determines signal direction. This prevents the common indicator failure mode of "overbought can stay overbought" by requiring directional confirmation.

Signal Conditions:

A BUY signal requires:

Extreme event detection (tensor crosses threshold)

Bullish score > Bearish score

Price confirmation: Bullish candle (optional, user-controlled)

Volume confirmation: Volume > average (optional, user-controlled)

Momentum confirmation: Positive momentum (optional, user-controlled)

A SELL signal requires the inverse conditions.

INPUTS EXPLAINED - Core Parameters:

Global Horizon (Context): Default 20. Lookback period for normalization and volatility comparison. Higher values = smoother but less responsive. Lower values = more signals but potentially more noise.

Tensor Smoothing: Default 3. EMA period applied to final output. Removes "quantum foam" (high-frequency noise). Range 1-20.

Singularity Threshold: Default 90. Values above this (or below 100-threshold) trigger extreme event detection. Higher = rarer, stronger signals.

Signal Sensitivity (Epsilon): Default 1.0. Post-normalization compression factor. This is the key innovation - it actually works because it's applied AFTER normalization. Range 0.1-5.0.

Signal Interpreter Toggles:

Require Price Confirmation: Default ON. Only generates buy signals on bullish candles, sell signals on bearish candles. Reduces false signals but may delay entry.

Require Volume Confirmation: Default ON. Only signals when volume > average. Critical for stocks/crypto, less important for forex (unreliable volume data).

Use Momentum Filter: Default ON. Requires momentum agreement with signal direction. Prevents counter-trend signals.

Momentum Lookback: Default 5. Number of bars for momentum calculation. Shorter = more responsive, longer = trend-following bias.

Visual Controls:

Colors: Customizable colors for bullish flux, bearish flux, background, and event horizon.

Visual Transparency: Default 85. Master control for all visual elements (accretion disk, field lines, particles, etc.). Range 50-99. Signals and dashboard have separate controls.

Visibility Toggles: Individual on/off switches for:

Gravitational field lines (trend EMAs)

Field reversals (trend crossovers)

Accretion disk (background gradient)

Singularity diamonds (neutral extreme events)

Energy particles (volume bursts)

Event horizon flash (extreme event background)

Signal background flash

Signal Size: Tiny/Small/Normal triangle size

Signal Offsets: Separate controls for buy and sell signal vertical positioning (percentage of price)

Dashboard Settings:

Show Dashboard: Toggle on/off

Position: 9 placement options (all corners, centers, middles)

Text Size: Tiny/Small/Normal/Large

Background Transparency: 0-50, separate from visual transparency

VISUAL ELEMENTS EXPLAINED

1. Accretion Disk (Background Gradient):

A three-layer gradient background that intensifies as the tensor approaches extremes. The outer disk appears at any non-neutral reading, the inner disk activates above 70 or below 30, and the core layer appears above 85 or below 15. Color indicates direction (cyan = bullish, red = bearish). This provides instant visual feedback on market pressure intensity.

2. Gravitational Field Lines (EMAs):

Two trend-following EMAs (10 and 30 period) visualized as colored lines. These represent the "curvature" of market trend - when they diverge, trend is strong; when they converge, trend is weakening. Crossovers mark potential trend reversals.

3. Field Reversals (Circles):

Small circles appear when the fast EMA crosses the slow EMA, indicating a potential trend change. These are distinct from extreme events and appear at normal market structure shifts.

4. Singularity Diamonds:

Small diamond shapes appear when the tensor reaches extreme levels (>90 or <10) but doesn't meet the full signal criteria. These are "watch" events - extreme pressure exists but directional confirmation is lacking.

5. Energy Particles (Dots):

Tiny dots appear when volume exceeds 2× average, indicating significant participation. Color matches bar direction. These highlight genuine high-conviction moves versus low-volume drifts.

6. Event Horizon Flash:

A golden background flash appears the instant any extreme threshold is breached, before directional analysis. This alerts you to pay attention.

7. Signal Background Flash:

When a full buy/sell signal is confirmed, the background flashes cyan (buy) or red (sell). This is your primary alert that all conditions are met.

8. Signal Triangles:

The actual buy (▲) and sell (▼) markers. These only appear when ALL selected confirmation criteria are satisfied. Position is offset from bars to avoid overlap with other indicators.

DASHBOARD METRICS EXPLAINED

The dashboard displays real-time calculated values:

Event Density: Current tensor value (0-100). Above 90 or below 10 = critical. Icon changes: 🔥 (extreme high), ❄️ (extreme low), ○ (neutral).

Time Dilation (γ): Current volatility ratio squared. Values >2.0 indicate extreme volatility environments. >1.5 = elevated, >1.0 = above average. Icon: ⚡ (extreme), ⚠ (elevated), ○ (normal).

Mass (Vol): Log-transformed volume value. Compared to volume ratio (current/average). Icon: ● (>2× avg), ◐ (>1× avg), ○ (below avg).

Velocity (ΔP): Raw price change. Direction arrow indicates momentum direction. Shows the actual price delta value.

Bullish Flux: Current bullish context score. Displayed as both a bar chart (visual) and numeric value. Brighter when bullish score dominates.

Bearish Flux: Current bearish context score. Same visualization as bullish flux. These scores compete - the winner determines signal direction.

Field: Trend direction based on EMA relationship. "Repulsive" (uptrend), "Attractive" (downtrend), "Neutral" (ranging). Icon: ⬆⬇↔

State: Current market condition:

🚀 EJECTION: Buy signal active

💥 COLLAPSE: Sell signal active

⚠ CRITICAL: Extreme event, no directional confirmation

● STABLE: Normal market conditions

HOW TO USE THE INDICATOR

1. Wait for Extreme Events:

The indicator is designed to be selective. Don't trade every fluctuation - wait for tensor to reach >90 or <10. This alone is not a signal.

2. Check Context Scores:

Look at the Bullish Flux vs Bearish Flux in the dashboard. If scores are close (within 1-2 points), the market is indecisive - skip the trade.

3. Confirm with Signals:

Only act when a full triangle signal appears (▲ or ▼). This means ALL your selected confirmation criteria have been met.

4. Use with Price Structure:

Combine with support/resistance levels. A buy signal AT support is higher probability than a buy signal in the middle of nowhere.

5. Respect the Dashboard State:

When State shows "CRITICAL" (⚠), it means extreme pressure exists but direction is unclear. These are the most dangerous moments - wait for resolution.

6. Volume Matters:

Energy particles (dots) and the Mass metric tell you if institutions are participating. Signals without volume confirmation are lower probability.

MARKET AND TIMEFRAME RECOMMENDATIONS

Scalping (1m-5m):

Lookback: 10-14

Smoothing: 5-7

Threshold: 85

Epsilon: 0.5-0.7

Note: Expect more noise. Confirm with Level 2 data. Best on highly liquid instruments.

Intraday (15m-1h):

Lookback: 20-30 (default settings work well)

Smoothing: 3-5

Threshold: 90

Epsilon: 1.0

Note: Sweet spot for the indicator. High win rate on liquid stocks, forex majors, and crypto.

Swing Trading (4h-1D):

Lookback: 30-50

Smoothing: 3

Threshold: 90-95

Epsilon: 1.5-2.0

Note: Signals are rare but high conviction. Combine with higher timeframe trend analysis.

Position Trading (1D-1W):

Lookback: 50-100

Smoothing: 5-7

Threshold: 95

Epsilon: 2.0-3.0

Note: Extremely rare signals. Only trade the most extreme events. Expect massive moves.

Market-Specific Settings:

Forex (EUR/USD, GBP/USD, etc.):

Volume data is unreliable (spot forex has no centralized volume)

Disable "Require Volume Confirmation"

Focus on momentum and trend filters

News events create extreme singularities

Best on 15m-1h timeframes

Stocks (High-Volume Equities):

Volume confirmation is CRITICAL - keep it ON

Works excellently on AAPL, TSLA, SPY, etc.

Morning session (9:30-11:00 ET) shows highest event density

Earnings announcements create guaranteed extreme events

Best on 5m-1h for day trading, 1D for swing trading

Crypto (BTC, ETH, major alts):

Reduce threshold to 85 (crypto has constant high volatility)

Volume spikes are THE primary signal - keep volume confirmation ON

Works exceptionally well due to 24/7 trading and high volatility

Epsilon can be reduced to 0.7-0.8 for more signals

Best on 15m-4h timeframes

Commodities (Gold, Oil, etc.):

Gold responds to macro events (Fed announcements, geopolitical events)

Oil responds to supply shocks

Use daily timeframe minimum

Increase lookback to 50+

These are slow-moving markets - be patient

Indices (SPX, NDX, etc.):

Institutional volume matters - keep volume confirmation ON

Opening hour (9:30-10:30 ET) = highest singularity probability

Strong correlation with VIX - high VIX = more extreme events

Best on 15m-1h for day trading

WHAT MAKES THIS INDICATOR UNIQUE

1. Post-Normalization Sensitivity Control:

Unlike most oscillators where sensitivity controls don't actually work (they're applied before normalization, which then rescales everything), FTS applies epsilon compression AFTER normalization. This means the sensitivity parameter genuinely affects signal frequency. This is a novel implementation not found in standard oscillators.

2. Multi-Factor Confluence Requirement:

The indicator doesn't just detect "overbought" or "oversold" - it detects extreme conditions AND THEN analyzes context through five separate factors (price structure, momentum, trend, acceleration, volume). Most indicators are single-factor; FTS requires confluence.

3. Volatility-Weighted Normalization:

By squaring the ATR ratio (local/global), the indicator adapts to changing market regimes. A 1% move in a low-volatility environment is treated differently than a 1% move in a high-volatility environment. Traditional indicators treat all moves equally regardless of context.

4. Volume Integration at the Core:

Volume isn't an afterthought or optional filter - it's baked into the fundamental equation as "mass." The log transformation handles outliers elegantly while preserving significance. Most price-based indicators completely ignore volume.

5. Adaptive Scoring System:

Rather than fixed buy/sell rules ("RSI >70 = sell"), FTS uses competitive scoring where bullish and bearish evidence compete. The winner determines direction. This solves the classic problem of "overbought markets can stay overbought during strong uptrends."

6. Comprehensive Visual Feedback:

The multi-layer visualization system (accretion disk, field lines, particles, flashes) provides instant intuitive feedback on market state without requiring dashboard reading. You can see pressure building before extreme thresholds are hit.

7. Separate Extreme Detection and Signal Generation:

"Singularity diamonds" show extreme events that don't meet full criteria, while "signal triangles" only appear when ALL conditions are met. This distinction helps traders understand when pressure exists versus when it's actionable.

COMPARISON TO EXISTING INDICATORS

vs. RSI/Stochastic:

These normalize price relative to recent range. FTS normalizes (price change × log volume × volatility ratio) - a composite metric, not just price position.

vs. Chaikin Money Flow:

CMF combines price and volume but lacks volatility context and doesn't use adaptive normalization or post-normalization compression.

vs. Bollinger Bands + Volume:

Bollinger Bands show volatility but don't integrate volume or create a unified oscillator. They're separate components, not synthesized.

vs. MACD:

MACD is pure momentum. FTS combines momentum with volume weighting and volatility context, plus provides a normalized 0-100 scale.

The specific combination of log-volume weighting, squared volatility amplification, post-normalization epsilon compression, and multi-factor directional scoring is unique to this indicator.

LIMITATIONS AND PROPER DISCLOSURE

Not a Holy Grail:

No indicator is perfect. This tool identifies high-probability setups but cannot predict the future. Losses will occur. Use proper risk management.

Requires Confirmation:

Best used in conjunction with price action analysis, support/resistance levels, and higher timeframe trend. Don't trade signals blindly.

Volume Data Dependency:

On forex (spot) and some low-volume instruments, volume data is unreliable or tick-volume only. Disable volume confirmation in these cases.

Lagging Components:

The EMA smoothing and trend filters are inherently lagging. In extremely fast moves, signals may appear after the initial thrust.

Extreme Event Rarity:

With conservative settings (high threshold, high epsilon), signals can be rare. This is by design - quality over quantity. If you need more frequent signals, reduce threshold to 85 and epsilon to 0.7.

Not Financial Advice:

This indicator is an analytical tool. All trading decisions and their consequences are solely your responsibility. Past performance does not guarantee future results.

BEST PRACTICES

Don't trade every singularity - wait for context confirmation

Higher timeframes = higher reliability

Combine with support/resistance for entry refinement

Volume confirmation is CRITICAL for stocks/crypto (toggle off only for forex)

During major news events, singularities are inevitable but direction may be uncertain - use wider stops

When bullish and bearish flux scores are close, skip the trade

Test settings on your specific instrument/timeframe before live trading

Use the dashboard actively - it contains critical diagnostic information

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Mars Signals - Ultimate Institutional Suite v3.0(Joker)Comprehensive Trading Manual

Mars Signals – Ultimate Institutional Suite v3.0 (Joker)

## Chapter 1 – Philosophy & System Architecture

This script is not a simple “buy/sell” indicator.

Mars Signals – UIS v3.0 (Joker) is designed as an institutional-style analytical assistant that layers several methodologies into a single, coherent framework.

The system is built on four core pillars:

1. Smart Money Concepts (SMC)

- Detection of Order Blocks (professional demand/supply zones).

- Detection of Fair Value Gaps (FVGs) (price imbalances).

2. Smart DCA Strategy

- Combination of RSI and Bollinger Bands

- Identifies statistically discounted zones for scaling into spot positions or exiting shorts.

3. Volume Profile (Visible Range Simulation)

- Distribution of volume by price, not by time.

- Identification of POC (Point of Control) and high-/low-volume areas.

4. Wyckoff Helper – Spring

- Detection of bear traps, liquidity grabs, and sharp bullish reversals.

All four pillars feed into a Confluence Engine (Scoring System).

The final output is presented in the Dashboard, with a clear, human-readable signal:

- STRONG LONG 🚀

- WEAK LONG ↗

- NEUTRAL / WAIT

- WEAK SHORT ↘

- STRONG SHORT 🩸

This allows the trader to see *how many* and *which* layers of the system support a bullish or bearish bias at any given time.

## Chapter 2 – Settings Overview

### 2.1 General & Dashboard Group

- Show Dashboard Panel (`show_dash`)

Turns the dashboard table in the corner of the chart ON/OFF.

- Show Signal Recommendation (`show_rec`)

- If enabled, the textual signal (STRONG LONG, WEAK SHORT, etc.) is displayed.

- If disabled, you only see feature status (ON/OFF) and the current price.

- Dashboard Position (`dash_pos`)

Determines where the dashboard appears on the chart:

- `Top Right`

- `Bottom Right`

- `Top Left`

### 2.2 Smart Money (SMC) Group

- Enable SMC Strategy (`show_smc`)

Globally enables or disables the Order Block and FVG logic.

- Order Block Pivot Lookback (`ob_period`)

Main parameter for detecting key pivot highs/lows (swing points).

- Default value: 5

- Concept:

A bar is considered a pivot low if its low is lower than the lows of the previous 5 and the next 5 bars.

Similarly, a pivot high has a high higher than the previous 5 and the next 5 bars.

These pivots are used as anchors for Order Blocks.

- Increasing `ob_period`:

- Fewer levels.

- But levels tend to be more significant and reliable.

- In highly volatile markets (major news, war events, FOMC, etc.),

using values 7–10 is recommended to filter out weak levels.

- Show Fair Value Gaps (`show_fvg`)

Enables/disables the drawing of FVG zones (imbalances).

- Bullish OB Color (`c_ob_bull`)

- Color of Bullish Order Blocks (Demand Zones).

- Default: semi-transparent green (transparency ≈ 80).

- Bearish OB Color (`c_ob_bear`)

- Color of Bearish Order Blocks (Supply Zones).

- Default: semi-transparent red.

- Bullish FVG Color (`c_fvg_bull`)

- Color of Bullish FVG (upward imbalance), typically yellow.

- Bearish FVG Color (`c_fvg_bear`)

- Color of Bearish FVG (downward imbalance), typically purple.

### 2.3 Smart DCA Strategy Group

- Enable DCA Zones (`show_dca`)

Enables the Smart DCA logic and visual labels.

- RSI Length (`rsi_len`)

Lookback period for RSI (default: 14).

- Shorter → more sensitive, more noise.

- Longer → fewer signals, higher reliability.

- Bollinger Bands Length (`bb_len`)

Moving average period for Bollinger Bands (default: 20).

- BB Multiplier (`bb_mult`)

Standard deviation multiplier for Bollinger Bands (default: 2.0).

- For extremely volatile markets, values like 2.5–3.0 can be used so that only extreme deviations trigger a DCA signal.

### 2.4 Volume Profile (Visible Range Sim) Group

- Show Volume Profile (`show_vp`)

Enables the simulated Volume Profile bars on the right side of the chart.

- Volume Lookback Bars (`vp_lookback`)

Number of bars used to compute the Volume Profile (default: 150).

- Higher values → broader historical context, heavier computation.

- Row Count (`vp_rows`)

Number of vertical price segments (rows) to divide the total price range into (default: 30).

- Width (%) (`vp_width`)

Relative width of each volume bar as a percentage.

In the code, bar widths are scaled relative to the row with the maximum volume.

> Technical note: Volume Profile calculations are executed only on the last bar (`barstate.islast`) to keep the script performant even on higher timeframes.

### 2.5 Wyckoff Helper Group

- Show Wyckoff Events (`show_wyc`)

Enables detection and plotting of Wyckoff Spring events.

- Volume MA Length (`vol_ma_len`)

Length of the moving average on volume.

A bar is considered to have Ultra Volume if its volume is more than 2× the volume MA.

## Chapter 3 – Smart Money Strategy (Order Blocks & FVG)

### 3.1 What Is an Order Block?

An Order Block (OB) represents the footprint of large institutional orders:

- Bullish Order Block (Demand Zone)

The last selling region (bearish candle/cluster) before a strong upward move.

- Bearish Order Block (Supply Zone)

The last buying region (bullish candle/cluster) before a strong downward move.

Institutions and large players place heavy orders in these regions. Typical price behavior:

- Price moves away from the zone.

- Later returns to the same zone to fill unfilled orders.

- Then continues the larger trend.

In the script:

- If `pl` (pivot low) forms → a Bullish OB is created.

- If `ph` (pivot high) forms → a Bearish OB is created.

The box is drawn:

- From `bar_index ` to `bar_index`.

- Between `low ` and `high `.

- `extend=extend.right` extends the OB into the future, so it acts as a dynamic support/resistance zone.

- Only the last 4 OB boxes are kept to avoid clutter.

### 3.2 Order Block Color Guide

- Semi-transparent Green (`c_ob_bull`)

- Represents a Bullish Order Block (Demand Zone).

- Interpretation: a price region with a high probability of bullish reaction.

- Semi-transparent Red (`c_ob_bear`)

- Represents a Bearish Order Block (Supply Zone).

- Interpretation: a price region with a high probability of bearish reaction.

Overlap (Multiple OBs in the Same Area)

When two or more Order Blocks overlap:

- The shared area appears visually denser/stronger.

- This suggests higher order density.

- Such zones can be treated as high-priority levels for entries, exits, and stop-loss placement.

### 3.3 Demand/Supply Logic in the Scoring Engine

is_in_demand = low <= ta.lowest(low, 20)

is_in_supply = high >= ta.highest(high, 20)

- If current price is near the lowest lows of the last 20 bars, it is considered in a Demand Zone → positive impact on score.

- If current price is near the highest highs of the last 20 bars, it is considered in a Supply Zone → negative impact on score.

This logic complements Order Blocks and helps the Dashboard distinguish whether:

- Market is currently in a statistically cheap (long-friendly) area, or

- In a statistically expensive (short-friendly) area.

### 3.4 Fair Value Gaps (FVG)

#### Concept

When the market moves aggressively:

- Some price levels are skipped and never traded.

- A gap between wicks/shadows of consecutive candles appears.

- These regions are called Fair Value Gaps (FVGs) or Imbalances.

The market generally “dislikes” imbalance and often:

- Returns to these zones in the future.

- Fills the gap (rebalance).

- Then resumes its dominant direction.

#### Implementation in the Code

Bullish FVG (Yellow)

fvg_bull_cond = show_smc and show_fvg and low > high and close > high

if fvg_bull_cond

box.new(bar_index , high , bar_index, low, ...)

Core condition:

`low > high ` → the current low is above the high of two bars ago; the space between them is an untraded gap.

Bearish FVG (Purple)

fvg_bear_cond = show_smc and show_fvg and high < low and close < low

if fvg_bear_cond

box.new(bar_index , low , bar_index, high, ...)

Core condition:

`high < low ` → the current high is below the low of two bars ago; again a price gap exists.

#### FVG Color Guide

- Transparent Yellow (`c_fvg_bull`) – Bullish FVG

Often acts like a magnet for price:

- Price tends to retrace into this zone,

- Fill the imbalance,

- And then continue higher.

- Transparent Purple (`c_fvg_bear`) – Bearish FVG

Price tends to:

- Retrace upward into the purple area,

- Fill the imbalance,

- And then resume downward movement.

#### Trading with FVGs

- FVGs are *not* standalone entry signals.

They are best used as:

- Targets (take-profit zones), or

- Reaction areas where you expect a pause or reversal.

Examples:

- If you are long, a bearish FVG above is often an excellent take-profit zone.

- If you are short, a bullish FVG below is often a good cover/exit zone.

### 3.5 Core SMC Trading Templates

#### Reversal Long

1. Price trades down into a green Order Block (Demand Zone).

2. A bullish confirmation candle (Close > Open) forms inside or just above the OB.

3. If this zone is close to or aligned with a bullish FVG (yellow), the signal is reinforced.

4. Entry:

- At the close of the confirmation candle, or

- Using a limit order near the upper boundary of the OB.

5. Stop-loss:

- Slightly below the OB.

- If the OB is broken decisively and price consolidates below it, the zone loses validity.

6. Targets:

- The next FVG,

- Or the next red Order Block (Supply Zone) above.

#### Reversal Short

The mirror scenario:

- Price rallies into a red Order Block (Supply).

- A bearish confirmation candle forms (Close < Open).

- FVG/premium structure above can act as a confluence.

- Stop-loss goes above the OB.

- Targets: lower FVGs or subsequent green OBs below.

## Chapter 4 – Smart DCA Strategy (RSI + Bollinger Bands)

### 4.1 Smart DCA Concept

- Classic DCA = buying at fixed time intervals regardless of price.

- Smart DCA = scaling in only when:

- Price is statistically cheaper than usual, and

- The market is in a clear oversold condition.

Code logic:

rsi_val = ta.rsi(close, rsi_len)

= ta.bb(close, bb_len, bb_mult)

dca_buy = show_dca and rsi_val < 30 and close < bb_lower

dca_sell = show_dca and rsi_val > 70 and close > bb_upper

Conditions:

- DCA Buy – Smart Scale-In Zone

- RSI < 30 → oversold.

- Close < lower Bollinger Band → price has broken below its typical volatility envelope.

- DCA Sell – Overbought/Distribution Zone

- RSI > 70 → overbought.

- Close > upper Bollinger Band → price is extended far above the mean.

### 4.2 Visual Representation on the Chart

- Green “DCA” Label Below Candle

- Shape: `labelup`.

- Color: lime background, white text.

- Meaning: statistically attractive level for laddered spot entries or short exits.

- Red “SELL” Label Above Candle

- Warning that the market is in an extended, overbought condition.

- Suitable for profit-taking on longs or considering short entries (with proper confluence and risk management).

- Light Green Background (`bgcolor`)

- When `dca_buy` is true, the candle background turns very light green (high transparency).

- This helps visually identify DCA Zones across the chart at a glance.

### 4.3 Practical Use in Trading

#### Spot Trading

Used to build a better average entry price:

- Every time a DCA label appears, allocate a fixed portion of capital (e.g., 2–5%).

- Combining DCA signals with:

- Green OBs (Demand Zones), and/or

- The Volume Profile POC

makes the zone structurally more important.

#### Futures Trading

- Longs

- Use DCA Buy signals as low-risk zones for opening or adding to longs when:

- Price is inside a green OB, or

- The Dashboard already leans LONG.

- Shorts

- Use DCA Sell signals as:

- Exit zones for longs, or

- Areas to initiate shorts with stops above structural highs.

## Chapter 5 – Volume Profile (Visible Range Simulation)

### 5.1 Concept

Traditional volume (histogram under the chart) shows volume over time.

Volume Profile shows volume by price level:

- At which prices has the highest trading activity occurred?

- Where did buyers and sellers agree the most (High Volume Nodes – HVNs)?

- Where did price move quickly due to low participation (Low Volume Nodes – LVNs)?

### 5.2 Implementation in the Script

Executed only when `show_vp` is enabled and on the last bar:

1. The last `vp_lookback` bars (default 150) are processed.

2. The minimum low and maximum high over this window define the price range.

3. This price range is divided into `vp_rows` segments (e.g., 30 rows).

4. For each row:

- All bars are scanned.

- If the mid-price `(high + low ) / 2` falls inside a row, that bar’s volume is added to the row total.

5. The row with the greatest volume is stored as `max_vol_idx` (the POC row).

6. For each row, a volume box is drawn on the right side of the chart.

### 5.3 Color Scheme

- Semi-transparent Orange

- The row with the maximum volume – the Point of Control (POC).

- Represents the strongest support/resistance level from a volume perspective.

- Semi-transparent Blue

- Other volume rows.

- The taller the bar → the higher the volume → the stronger the interest at that price band.

### 5.4 Trading Applications

- If price is above POC and retraces back into it:

→ POC often acts as support, suitable for long setups.

- If price is below POC and rallies into it:

→ POC often acts as resistance, suitable for short setups or profit-taking.

HVNs (Tall Blue Bars)

- Represent areas of equilibrium where the market has spent time and traded heavily.

- Price tends to consolidate here before choosing a direction.

LVNs (Short or Nearly Empty Bars)

- Represent low participation zones.

- Price often moves quickly through these areas – useful for targeting fast moves.

## Chapter 6 – Wyckoff Helper – Spring

### 6.1 Spring Concept

In the Wyckoff framework:

- A Spring is a false break of support.

- The market briefly trades below a well-defined support level, triggers stop losses,

then sharply reverses upward as institutional buyers absorb liquidity.

This movement:

- Clears out weak hands (retail sellers).

- Provides large players with liquidity to enter long positions.

- Often initiates a new uptrend.

### 6.2 Code Logic

Conditions for a Spring:

1. The current low is lower than the lowest low of the previous 50 bars

→ apparent break of a long-standing support.

2. The bar closes bullish (Close > Open)

→ the breakdown was rejected.

3. Volume is significantly elevated:

→ `volume > 2 × volume_MA` (Ultra Volume).

When all conditions are met and `show_wyc` is enabled:

- A pink diamond is plotted below the bar,

- With the label “Spring” – one of the strongest long signals in this system.

### 6.3 Trading Use

- After a valid Spring, markets frequently enter a meaningful bullish phase.

- The highest quality setups occur when:

- The Spring forms inside a green Order Block, and

- Near or on the Volume Profile POC.

Entries:

- At the close of the Spring bar, or

- On the first pullback into the mid-range of the Spring candle.

Stop-loss:

- Slightly below the Spring’s lowest point (wick low plus a small buffer).

## Chapter 7 – Confluence Engine & Dashboard

### 7.1 Scoring Logic

For each bar, the script:

1. Resets `score` to 0.

2. Adjusts the score based on different signals.

SMC Contribution

if show_smc

if is_in_demand

score += 1

if is_in_supply

score -= 1

- Being in Demand → `+1`

- Being in Supply → `-1`

DCA Contribution

if show_dca

if dca_buy

score += 2

if dca_sell

score -= 2

- DCA Buy → `+2` (strong, statistically driven long signal)

- DCA Sell → `-2`

Wyckoff Spring Contribution

if show_wyc

if wyc_spring

score += 2

- Spring → `+2` (entry of strong money)

### 7.2 Mapping Score to Dashboard Signal

- score ≥ 2 → STRONG LONG 🚀

Multiple bullish conditions aligned.

- score = 1 → WEAK LONG ↗

Some bullish bias, but only one layer clearly positive.

- score = 0 → NEUTRAL / WAIT

Rough balance between buying and selling forces; staying flat is usually preferable.

- score = -1 → WEAK SHORT ↘

Mild bearish bias, suited for cautious or short-term plays.

- score ≤ -2 → STRONG SHORT 🩸

Convergence of several bearish signals.

### 7.3 Dashboard Structure

The dashboard is a two-column table:

- Row 0

- Column 0: `"Mars Signals"` – black background, white text.

- Column 1: `"UIS v3.0"` – black background, yellow text.

- Row 1

- Column 0: `"Price:"` (light grey background).

- Column 1: current closing price (`close`) with a semi-transparent blue background.

- Row 2

- Column 0: `"SMC:"`

- Column 1:

- `"ON"` (green) if `show_smc = true`

- `"OFF"` (grey) otherwise.

- Row 3

- Column 0: `"DCA:"`

- Column 1:

- `"ON"` (green) if `show_dca = true`

- `"OFF"` (grey) otherwise.

- Row 4

- Column 0: `"Signal:"`

- Column 1: signal text (`status_txt`) with background color `status_col`

(green, red, teal, maroon, etc.)

- If `show_rec = false`, these cells are cleared.

## Chapter 8 – Visual Legend (Colors, Shapes & Actions)

For quick reading inside TradingView, the visual elements are described line by line instead of a table.

Chart Element: Green Box

Color / Shape: Transparent green rectangle

Core Meaning: Bullish Order Block (Demand Zone)

Suggested Trader Response: Look for longs, Smart DCA adds, closing or reducing shorts.

Chart Element: Red Box

Color / Shape: Transparent red rectangle

Core Meaning: Bearish Order Block (Supply Zone)

Suggested Trader Response: Look for shorts, or take profit on existing longs.

Chart Element: Yellow Area

Color / Shape: Transparent yellow zone

Core Meaning: Bullish FVG / upside imbalance

Suggested Trader Response: Short take-profit zone or expected rebalance area.

Chart Element: Purple Area

Color / Shape: Transparent purple zone

Core Meaning: Bearish FVG / downside imbalance

Suggested Trader Response: Long take-profit zone or temporary supply region.

Chart Element: Green "DCA" Label

Color / Shape: Green label with white text, plotted below the candle

Core Meaning: Smart ladder-in buy zone, DCA buy opportunity

Suggested Trader Response: Spot DCA entry, partial short exit.

Chart Element: Red "SELL" Label

Color / Shape: Red label with white text, plotted above the candle

Core Meaning: Overbought / distribution zone

Suggested Trader Response: Take profit on longs, consider initiating shorts.

Chart Element: Light Green Background (bgcolor)

Color / Shape: Very transparent light-green background behind bars

Core Meaning: Active DCA Buy zone

Suggested Trader Response: Treat as a discount zone on the chart.

Chart Element: Orange Bar on Right

Color / Shape: Transparent orange horizontal bar in the volume profile

Core Meaning: POC – price with highest traded volume

Suggested Trader Response: Strong support or resistance; key reference level.

Chart Element: Blue Bars on Right

Color / Shape: Transparent blue horizontal bars in the volume profile

Core Meaning: Other volume levels, showing high-volume and low-volume nodes

Suggested Trader Response: Use to identify balance zones (HVN) and fast-move corridors (LVN).

Chart Element: Pink "Spring" Diamond

Color / Shape: Pink diamond with white text below the candle

Core Meaning: Wyckoff Spring – liquidity grab and potential major bullish reversal

Suggested Trader Response: One of the strongest long signals in the suite; look for high-quality long setups with tight risk.

Chart Element: STRONG LONG in Dashboard

Color / Shape: Green background, white text in the Signal row

Core Meaning: Multiple bullish layers in confluence

Suggested Trader Response: Consider initiating or increasing longs with strict risk management.

Chart Element: STRONG SHORT in Dashboard

Color / Shape: Red background, white text in the Signal row

Core Meaning: Multiple bearish layers in confluence

Suggested Trader Response: Consider initiating or increasing shorts with a logical, well-placed stop.

## Chapter 9 – Timeframe-Based Trading Playbook

### 9.1 Timeframe Selection

- Scalping

- Timeframes: 1M, 5M, 15M

- Objective: fast intraday moves (minutes to a few hours).

- Recommendation: focus on SMC + Wyckoff.

Smart DCA on very low timeframes may introduce excessive noise.

- Day Trading

- Timeframes: 15M, 1H, 4H

- Provides a good balance between signal quality and frequency.

- Recommendation: use the full stack – SMC + DCA + Volume Profile + Wyckoff + Dashboard.

- Swing Trading & Position Investing

- Timeframes: Daily, Weekly

- Emphasis on Smart DCA + Volume Profile.

- SMC and Wyckoff are used mainly to fine-tune swing entries within larger trends.

### 9.2 Scenario A – Scalping Long

Example: 5-Minute Chart

1. Price is declining into a green OB (Bullish Demand).

2. A candle with a long lower wick and bullish close (Pin Bar / Rejection) forms inside the OB.

3. A Spring diamond appears below the same candle → very strong confluence.

4. The Dashboard shows at least WEAK LONG ↗, ideally STRONG LONG 🚀.

5. Entry:

- On the close of the confirmation candle, or

- On the first pullback into the mid-range of that candle.

6. Stop-loss:

- Slightly below the OB.

7. Targets:

- Nearby bearish FVG above, and/or

- The next red OB.

### 9.3 Scenario B – Day-Trading Short

Recommended Timeframes: 1H or 4H

1. The market completes a strong impulsive move upward.

2. Price enters a red Order Block (Supply).

3. In the same zone, a purple FVG appears or remains unfilled.

4. On a lower timeframe (e.g., 15M), RSI enters overbought territory and a DCA Sell signal appears.

5. The main timeframe Dashboard (1H) shows WEAK SHORT ↘ or STRONG SHORT 🩸.

Trade Plan

- Open a short near the upper boundary of the red OB.

- Place the stop above the OB or above the last swing high.

- Targets:

- A yellow FVG lower on the chart, and/or

- The next green OB (Demand) below.

### 9.4 Scenario C – Swing / Investment with Smart DCA

Timeframes: Daily / Weekly

1. On the daily or weekly chart, each time a green “DCA” label appears:

- Allocate a fixed fraction of your capital (e.g., 3–5%) to that asset.

2. Check whether this DCA zone aligns with the orange POC of the Volume Profile:

- If yes → the quality of the entry zone is significantly higher.

3. If the DCA signal sits inside a daily green OB, the probability of a medium-term bottom increases.

4. Always build the position laddered, never all-in at a single price.

Exits for investors:

- Near weekly red OBs or large purple FVG zones.

- Ideally via partial profit-taking rather than closing 100% at once.

### 9.5 Case Study 1 – BTCUSDT (15-Minute)

- Context: Price has sold off down towards 65,000 USD.

- A green OB had previously formed at that level.

- Near the lower boundary of this OB, a partially filled yellow FVG is present.

- As price returns to this region, a Spring appears.

- The Dashboard shifts from NEUTRAL / WAIT to WEAK LONG ↗.

Plan

- Enter a long near the OB low.

- Place stop below the Spring low.

- First target: a purple FVG around 66,200.

- Second (optional) target: the first red OB above that level.

### 9.6 Case Study 2 – Meme Coin (PEPE – 4H)

- After a strong pump, price enters a corrective phase.

- On the 4H chart, RSI drops below 30; price breaks below the lower Bollinger Band → a DCA label prints.

- The Volume Profile shows the POC at approximately the same level.

- The Dashboard displays STRONG LONG 🚀.

Plan

- Execute laddered buys in the combined DCA + POC zone.

- Place a protective stop below the last significant swing low.

- Target: an expected 20–30% upside move towards the next red OB or purple FVG.

## Chapter 10 – Risk Management, Psychology & Advanced Tuning

### 10.1 Risk Management

No signal, regardless of its strength, replaces risk control.

Recommendations:

- In futures, do not expose more than 1–3% of account equity to risk per trade.

- Adjust leverage to the volatility of the instrument (lower leverage for highly volatile altcoins).

- Place stop-losses in zones where the idea is clearly invalidated:

- Below/above the relevant Order Block or Spring, not randomly in the middle of the structure.

### 10.2 Market-Specific Parameter Tuning

- Calmer Markets (e.g., major FX pairs)

- `ob_period`: 3–5.

- `bb_mult`: 2.0 is usually sufficient.

- Highly Volatile Markets (Crypto, news-driven assets)

- `ob_period`: 7–10 to highlight only the most robust OBs.

- `bb_mult`: 2.5–3.0 so that only extreme deviations trigger DCA.

- `vol_ma_len`: increase (e.g., to ~30) so that Spring triggers only on truly exceptional

volume spikes.

### 10.3 Trading Psychology

- STRONG LONG 🚀 does not mean “risk-free”.

It means the probability of a successful long, given the model’s logic, is higher than average.

- Treat Mars Signals as a confirmation and context system, not a full replacement for your own decision-making.

- Example of disciplined thinking:

- The Dashboard prints STRONG LONG,

- But price is simultaneously testing a multi-month macro resistance or a major negative news event is imminent,

- In such cases, trade smaller, widen stops appropriately, or skip the trade.

## Chapter 11 – Technical Notes & FAQ

### 11.1 Does the Script Repaint?

- Order Blocks and Springs are based on completed pivot structures and confirmed candles.

- Until a pivot is confirmed, an OB does not exist; after confirmation, behavior is stable under classic SMC assumptions.

- The script is designed to be structurally consistent rather than repainting signals arbitrarily.

### 11.2 Computational Load of Volume Profile

- On the last bar, the script processes up to `vp_lookback` bars × `vp_rows` rows.

- On very low timeframes with heavy zooming, this can become demanding.

- If you experience performance issues:

- Reduce `vp_lookback` or `vp_rows`, or

- Temporarily disable Volume Profile (`show_vp = false`).

### 11.3 Multi-Timeframe Behavior

- This version of the script is not internally multi-timeframe.

All logic (OB, DCA, Spring, Volume Profile) is computed on the active timeframe only.

- Practical workflow:

- Analyze overall structure and key zones on higher timeframes (4H / Daily).

- Use lower timeframes (15M / 1H) with the same tool for timing entries and exits.

## Conclusion

Mars Signals – Ultimate Institutional Suite v3.0 (Joker) is a multi-layer trading framework that unifies:

- Price structure (Order Blocks & FVG),

- Statistical behavior (Smart DCA via RSI + Bollinger),

- Volume distribution by price (Volume Profile with POC, HVN, LVN),

- Liquidity events (Wyckoff Spring),

into a single, coherent system driven by a transparent Confluence Scoring Engine.

The final output is presented in clear, actionable language:

> STRONG LONG / WEAK LONG / NEUTRAL / WEAK SHORT / STRONG SHORT

The system is designed to support professional decision-making, not to replace it.

Used together with strict risk management and disciplined execution,

Mars Signals – UIS v3.0 (Joker) can serve as a central reference manual and operational guide

for your trading workflow, from scalping to swing and investment positioning.

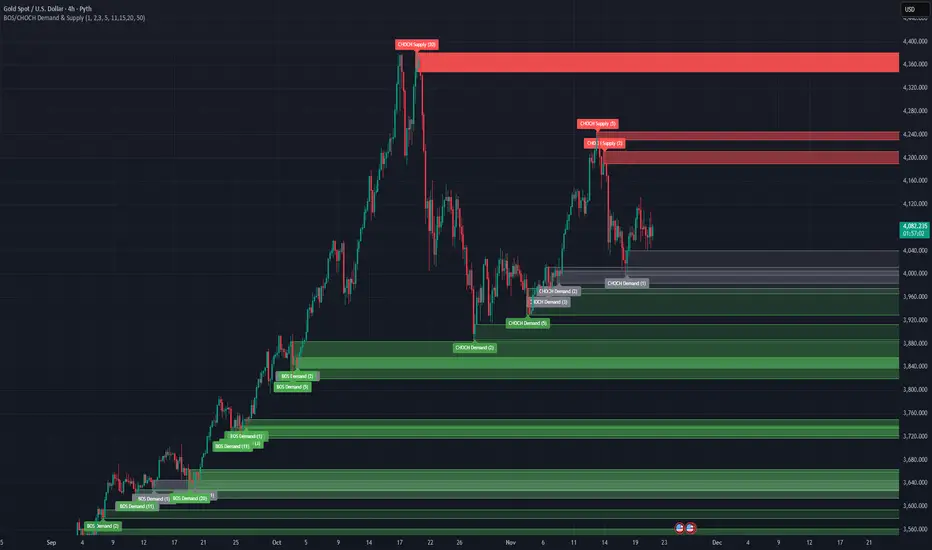

BOS/CHOCH Demand & SupplyThis indicator automatically identifies and plots Supply and Demand zones based on Smart Money Concepts (SMC) methodology. It detects structural breaks in price action and marks the origin zones that initiated these moves.

How It Works (Technical Methodology)

1. Swing Point Detection

The indicator uses Pine Script's ta.pivothigh() and ta.pivotlow() functions to identify swing highs and lows. Users can input multiple lookback periods (e.g., 1, 2, 3, 5, 11, 15, 20) to detect structure across different timeframe perspectives simultaneously.

2. Break of Structure (BOS) Detection

A Bullish BOS is confirmed when:

Current candle closes above the last swing high

Previous candle's high was still below that swing high

The current swing high is higher than the previous swing high (trend continuation)

A Bearish BOS is confirmed when:

Current candle closes below the last swing low

Previous candle's low was still above that swing low

The current swing low is lower than the previous swing low (trend continuation)

3. Change of Character (CHOCH) Detection

A Bullish CHOCH is confirmed when:

Price breaks above the last swing high

But that swing high was lower than the previous swing high (potential reversal signal)

A Bearish CHOCH is confirmed when:

Price breaks below the last swing low

But that swing low was higher than the previous swing low (potential reversal signal)

4. Inducement / Liquidity Grab Filter (Optional)

When enabled, zones are only drawn if the swing point that created them first grabbed liquidity from the previous swing:

For Demand zones: The swing low must have traded below the previous swing low before the bullish break

For Supply zones: The swing high must have traded above the previous swing high before the bearish break

This filter helps identify higher-probability zones where stop-losses were likely triggered before the move.

5. Zone Construction

Demand Zone (Bullish):

Top boundary: max(open, close) of the swing low candle

Bottom boundary: low of the swing low candle

Supply Zone (Bearish):

Top boundary: high of the swing high candle

Bottom boundary: min(open, close) of the swing high candle

This captures the candle body-to-wick range where institutional orders likely reside.

6. Zone Lifecycle Management

Active Zone: Displayed in green (demand) or red (supply)

Mitigated Zone: When price touches the zone but doesn't break it, the zone turns gray (indicating partial fill)

Broken Zone: When price fully breaks through the zone, it is automatically deleted from the chart

How to Use

Demand Zones (Green): Look for long entries when price returns to these zones. The zone represents where buying pressure previously overcame selling.

Supply Zones (Red): Look for short entries when price returns to these zones. The zone represents where selling pressure previously overcame buying.

BOS Zones: Indicate trend continuation - trade in the direction of the break.

CHOCH Zones: Indicate potential reversal - these are early warning signals of trend change.

Enable "Require Inducement" for higher-quality setups where liquidity was grabbed before the structural break.

Multi-Lookback Periods: Using multiple values helps identify zones across different structural levels. Smaller values catch minor structure; larger values catch major structure.

Disclaimer

This indicator is a technical analysis tool and should be used in conjunction with other forms of analysis. Past performance does not guarantee future results. Always use proper risk management.

oct25libLibrary of technical indicators for use in scripts.

1) salmav3(src, length, smooth, mult, sd_len)

Parameters:

src (float)

length (int)

smooth (simple int)

mult(float)

sd_len(int)

2) boltzman(src, length, T, alpha, smoothLen)

Parameters:

src (float)

length (int)

T(float)

Alpha(float)

smoothLen (simple int)

3) shannon(src, vol, len, bc, vc, smooth)

Parameters:

src (float)

vol (float)

len (int)

bc (bool)

vc (bool)

smooth (simple int)

4) vama(src, baseLen, volLen, beta)

Parameters:

src (float)

baseLen (int)

volLen (int)

beta (float)

5) fwma(src, period, lambda, smooth)

Parameters:

src (float)

period (int)

lambda (float)

smooth (simple int)

6) savitzky(srcc, srch, srcl, length)

Parameters:

srcc (float)

srch (float)

srcl (float)

length (int)

7) butterworth(src, length, poles, smooth)

Parameters:

src (float)

length (int)

poles (int)

smooth (simple int)

8) rti(src, trend_data_count, trend_sensitivity_percentage, midline, smooth)

Parameters:

src (float)

trend_data_count (int)

trend_sensitivity_percentage (int)

midline (int)

smooth (simple int)

9) chandemo(src, length, smooth)

Parameters:

src (float)

length (int)

smooth (simple int)

10) hsma(assetClose, length, emalen, midline)

Parameters:

assetClose (float)

length (int)

emalen (simple int)

midline (float)

11) rsi(src, rsiLengthInput, rsiemalen, midline)

Parameters:

src (float)

rsiLengthInput (simple int)

rsiemalen (simple int)

midline (float)

12) lacoca(src, lookback, malen, matype)

Parameters:

src (float)

lookback (int)

malen (simple int)

matype (string)

Luxy Sector & Industry RS AnalyzerEver wonder why some stocks soar while others in the same sector barely move? Or why your perfectly timed entry still loses money? Possibly the answer can be found in Relative Strength.

The Luxy Sector & Industry RS Analyzer solves a critical problem that most traders overlook: picking strong stocks in strong sectors AND strong industries . It's not enough for a stock to go up - you want stocks that are crushing their competition at both the sector AND industry level. This indicator does the heavy lifting by automatically comparing your stock against its sector ETF, industry ETF, the broader market, sector leader, and industry leader, giving you a complete multi-level picture of relative performance.

What makes this different?

- Automatic sector AND industry detection - no manual setup required

- Multi-level hierarchy analysis: Market → Sector → Industry → Stock

- Multi-timeframe analysis (1 month to 1 year) in one glance

- Industry ETF mapping (30+ industries covered)

- Clear 0-100 scoring system with letter grades (A+ to F)

- Works on stocks, crypto, forex, and commodities

- Real-time updates with anti-repaint protection

Think of it as your performance dashboard - instantly showing you if you're trading a champion or a laggard at every level of the market hierarchy.

METHODOLOGY & ATTRIBUTION

This indicator is based on classical Relative Strength (RS) analysis principles from technical analysis. RS methodology compares an asset's price performance against a benchmark to identify relative outperformance or underperformance. This concept has been used by professional traders and institutions for decades.

Key Concepts Used:

Relative Strength (RS) - Classical technical analysis concept measuring comparative performance

Multi-Level Hierarchy Analysis - Market → Sector → Industry → Stock comparison

Sector Rotation Analysis - Identifying which sectors are leading or lagging the market

Industry Rotation Analysis - Identifying which industries are leading within their sectors

Multi-period Performance Analysis - Evaluating strength across multiple timeframes

Beta Calculation - Standard statistical measure of volatility relative to a benchmark

DISCLAIMER: This indicator is for educational and informational purposes only. It should not be considered financial advice or a recommendation to buy or sell. Past performance does not guarantee future results. Trading involves risk and may not be suitable for all investors. Always do your own research and consult with a financial advisor before making investment decisions.

with all rows visible - capture when stock has strong RS score (70+) so users can see what a "good" setup looks like]

WHAT THE INDICATOR SHOWS

1. AUTOMATIC ASSET TYPE DETECTION

The indicator automatically identifies what you're analyzing and adjusts accordingly:

Stocks - Compares to sector ETF (XLK, XLF, XLV, etc.) and SPY

Crypto - Compares to Total Crypto Market Cap and Bitcoin

Forex - Compares to relevant currency index (DXY, EXY, etc.)

Commodities - Compares to Gold (GLD) as benchmark

Indices - Compares to broader market indices

How it works: The indicator reads your chart's asset type and ticker, then automatically maps it to the correct sector or benchmark. For stocks, it uses intelligent sector detection (looking at the sector field) to match you with the right sector ETF. For example:

- Technology stocks get compared to XLK (Technology Select Sector SPDR)

- Financial stocks get compared to XLF (Financial Select Sector SPDR)

- Healthcare stocks get compared to XLV (Health Care Select Sector SPDR)

This happens instantly when you add the indicator to any chart - no configuration needed.

2. SECTOR & MARKET BENCHMARKS

What is a Sector ETF?

A sector ETF is an exchange-traded fund that tracks a specific industry group. For example, XLK contains all major technology companies. By comparing your stock to its sector ETF, you can see if your stock is outperforming or underperforming its peers.

The indicator shows three key comparison points:

Stock vs Sector (Benchmark)

This tells you how your stock performs compared to companies in the same industry. Positive numbers mean your stock is beating the sector average. Negative numbers mean it's lagging behind.

Stock vs Market (SPY)

This shows performance against the broader S&P 500 index. This is important because even if a stock beats its sector, the entire sector might be weak. You want stocks that beat both their sector AND the market.

Sector vs Market

This reveals "sector rotation" - whether money is flowing into or out of this sector. When this number is positive, the whole sector is hot and leading the market. This is powerful because strong sectors tend to lift all boats, making it easier to find winners.

3. MULTI-PERIOD PERFORMANCE ANALYSIS

The indicator calculates performance across four timeframes simultaneously:

1 Month (1M) - Recent short-term momentum

3 Months (3M) - Medium-term trend strength

6 Months (6M) - Longer-term positioning

1 Year (1Y) - Full-cycle performance view

Why multiple periods matter:

A stock might look great over 1 month but terrible over 6 months - that's a red flag. The best stocks show consistent strength across all timeframes . When you see positive RS (Relative Strength) values across all four periods, you've found a stock with sustained outperformance.

Each row in the table shows:

- Raw performance percentage for that period

- RS value (the difference compared to benchmark)

- Color coding: Green for positive, red for negative, white for neutral

4. SECTOR LEADER COMPARISON

The indicator automatically identifies and compares your stock to the sector leader - the dominant stock in that industry.