Anchored Darvas Box## ANCHORED DARVAS BOX

---

### OVERVIEW

**Anchored Darvas Box** lets you drop a single timestamp on your chart and build a Darvas-style consolidation zone forward from that exact candle. The indicator freezes the first user-defined number of bars to establish the range, verifies that price respects that range for another user-defined number of bars, then waits for the first decisive breakout. The resulting rectangle captures every tick of the accumulation phase and the exact moment of expansion—no manual drawing, complete timestamp precision.

---

### HISTORICAL BACKGROUND

Nicolas Darvas’s 1950s box theory tracked institutional accumulation by hand-drawing rectangles around tight price ranges. A trade was triggered only when price escaped the rectangle.

The anchored version preserves Darvas’s logic but pins the entire sequence to a user-chosen candle: perfect for analysing a market open, an earnings release, FOMC minute, or any other catalytic bar.

---

### ALGORITHM DETAIL

1. **ANCHOR BAR**

*You provide a timestamp via the settings panel.* The script waits until the chart reaches that bar and records its index as **startBar**.

2. **RANGE DEFINITION — BARS 1-7**

• `rangeHigh` = highest high of bars 1-7 plus optional tolerance.

• `rangeLow` = lowest low of bars 1-7 minus optional tolerance.

3. **RANGE VALIDATION — BARS 8-14**

• Price must stay inside ` `.

• Any violation aborts the test; no box is created.

4. **ARMED STATE**

• If bars 8-14 hold the range, two live guide-lines appear:

– **Green** at `rangeHigh`

– **Red** at `rangeLow`

• The script is now “armed,” waiting indefinitely for the first true breakout.

5. **BREAKOUT & BOX CREATION**

• **Up breakout** =`high > rangeHigh` → rectangle drawn in **green**.

• **Down breakout**=`low < rangeLow` → rectangle drawn in **red**.

• Box extends from **startBar** to the breakout bar and never updates again.

• Optional labels print the dollar and percentage height of the box at its left edge.

6. **OPTIONAL COOLDOWN**

• After the box is painted the script can stay silent for a user-defined number of bars, letting you study the fallout without another range immediately arming on top of it.

---

### INPUT PARAMETERS

• **ANCHOR TIME** – Precise yyyy-mm-dd HH:MM:SS that seeds the sequence.

• **BARS TO DEFINE RANGE** – Default 7; affects both definition and validation windows.

• **OPTIONAL TOLERANCE** – Absolute price buffer to ignore micro-wicks.

• **COOLDOWN BARS AFTER BREAKOUT** – Pause length before the indicator is allowed to re-anchor (set to zero to disable).

• **SHOW BOX DISTANCE LABELS** – Toggle to print Δ\$ and Δ% on every completed box.

---

### USER WORKFLOW

1. Add the indicator, open settings, and set **ANCHOR TIME** to the candle you care about (e.g., “2025-04-23 09:30:00” for NYSE open).

2. Watch live as the script:

– Paints the seven-bar range.

– Draws validation lines.

– Locks in the box on breakout.

3. Use the box boundaries as structural stops, targets, or context for further trades.

---

### PRACTICAL APPLICATIONS

• **OPENING RANGE BREAKOUTS** – Anchor at the first second of the session; capture the initial 7-bar range and trade the first clean break.

• **EVENT STUDIES** – Anchor at a news candle to measure immediate post-event volatility.

• **VOLUME PROFILE FUSION** – Combine the anchored box with VPVR to see if the breakout occurs at a high-volume node or a low-liquidity pocket.

• **RISK DISCIPLINE** – Stop-loss can sit just inside the opposite edge of the anchored range, enforcing objective risk.

---

### ADVANCED CUSTOMISATION IDEAS

• **MULTIPLE ANCHORS** – Clone the indicator and anchor several boxes (e.g., London open, New York open).

• **DYNAMIC WINDOW** – Switch the 7-bar fixed length to a volatility-scaled length (ATR percentile).

• **STRATEGY WRAPPER** – Turn the indicator into a `strategy{}` script and back-test anchored boxes on decades of data.

---

### FINAL THOUGHTS

Anchored Darvas Boxes give you Darvas’s timeless range-break methodology anchored to any candle of interest—perfect for dissecting openings, economic releases, or your own bespoke “important” bars with laboratory precision.

Cerca negli script per "雷迪克2025年最新财务数据(营业收入、净利润、市盈率、市净率)"

EMA Trend Pro: Dynamic Clouds & ColorsEMA Trend Pro is your ultimate trend companion, built for traders who want clarity, precision, and confidence in their entries.

This script fuses dynamic EMA cloud zones with breakout and pullback signals — giving you real-time insights into market structure and momentum. Whether you're trading crypto, forex, stocks, or futures, EMA Trend Pro adapts to your style.

🔧 Key Features:

✅ EMA Stack Clouds with Folding Sensitivity (9/21/48/200)

✅ Bullish / Bearish trend labels with real-time dashboard

✅ Volume strength analysis (High, Normal, Low)

✅ Breakout signal alerts (momentum-based)

✅ Pullback signal alerts (trend resumption)

✅ Fully customizable: EMA lengths, signal visibility, cloud opacity

✅ Works across all assets and timeframes

🛠️ Designed for scalping, swing trading, and intraday setups.

🔔 Built-in alerts make automation seamless — no guesswork.

💡 Usage Tips:

Use clouds and trend labels to identify structure and bias

Trade breakouts when EMAs align and volume confirms

Look for pullbacks into the EMA zone and enter on resumption

📅 Market Hours Filter: Keeps signals relevant during core trading hours (9:30 AM–4 PM ET).

👤 Developed by @glapougbaegarmondeh

🧠 Version 1.0 | 📆 Released: April 24, 2025

Express Generator StrategyExpress Generator Strategy

Pine Script™ v6

The Express Generator Strategy is an algorithmic trading system that harnesses confluence from multiple technical indicators to optimize trade entries and dynamic risk management. Developed in Pine Script v6, it is designed to operate within a user-defined backtesting period—ensuring that trades are executed only during chosen historical windows for targeted analysis.

How It Works:

- Entry Conditions:

The strategy relies on a dual confirmation approach:- A moving average crossover system where a fast (default 9-period SMA) crossing above or below a slower (default 21-period SMA) average signals a potential trend reversal.

- MACD confirmation; trades are only initiated when the MACD line crosses its signal line in the direction of the moving average signal.

- An RSI filter refines these signals by preventing entries when the market might be overextended—ensuring that long entries only occur when the RSI is below an overbought level (default 70) and short entries when above an oversold level (default 30).

- Risk Management & Dynamic Position Sizing:

The strategy takes a calculated approach to risk by enabling the adjustment of position sizes using:- A pre-defined percentage of equity risk per trade (default 1%, adjustable between 0.5% to 3%).

- A stop-loss set in pips (default 100 pips, with customizable ranges), which is then adjusted by market volatility measured through the ATR.

- Trailing stops (default 50 pips) to help protect profits as the market moves favorably.

This combination of volatility-adjusted risk and equity-based position sizing aims to harmonize trade exposure with prevailing market conditions.

- Backtest Period Flexibility:

Users can define the start and end dates for backtesting (e.g., January 1, 2020 to December 31, 2025). This ensures that the strategy only opens trades within the intended analysis window. Moreover, if the strategy is still holding a position outside this period, it automatically closes all trades to prevent unwanted exposure.

- Visual Insights:

For clarity, the strategy plots the fast (blue) and slow (red) moving averages directly on the chart, allowing for visual confirmation of crossovers and trend shifts.

By integrating multiple technical indicators with robust risk management and adaptable position sizing, the Express Generator Strategy provides a comprehensive framework for capturing trending moves while prudently managing downside risk. It’s ideally suited for traders looking to combine systematic entries with a disciplined and dynamic risk approach.

Clenow MomentumClenow Momentum Method

The Clenow Momentum Method, developed by Andreas Clenow, is a systematic, quantitative trading strategy focused on capturing medium- to long-term price trends in financial markets. Popularized through Clenow’s book, Stocks on the Move: Beating the Market with Hedge Fund Momentum Strategies, the method leverages momentum—an empirically observed phenomenon where assets that have performed well in the recent past tend to continue performing well in the near future.

Theoretical Foundation

Momentum investing is grounded in behavioral finance and market inefficiencies. Investors often exhibit herding behavior, underreact to new information, or chase trends, causing prices to trend beyond fundamental values. Clenow’s method builds on academic research, such as Jegadeesh and Titman (1993), which demonstrated that stocks with high returns over 3–12 months outperform those with low returns over similar periods.

Clenow’s approach specifically uses **annualized momentum**, calculated as the rate of return over a lookback period (typically 90 days), annualized to reflect a yearly percentage. The formula is:

Momentum=(((Close N periods agoCurrent Close)^N252)−1)×100

- Current Close: The most recent closing price.

- Close N periods ago: The closing price N periods back (e.g., 90 days).

- N: Lookback period (commonly 90 days).

- 252: Approximate trading days in a year for annualization.

This metric ranks stocks by their momentum, prioritizing those with the strongest upward trends. Clenow’s method also incorporates risk management, diversification, and volatility adjustments to enhance robustness.

Methodology

The Clenow Momentum Method involves the following steps:

1. Universe Selection:

- A broad universe of liquid stocks is chosen, often from major indices (e.g., S&P 500, Nasdaq 100) or global exchanges.

- Filters should exclude illiquid stocks (e.g., low average daily volume) or those with extreme volatility.

2. Momentum Calculation:

- Stocks are ranked based on their annualized momentum over a lookback period (typically 90 days, though 60–120 days can be common tests).

- The top-ranked stocks (e.g., top 10–20%) are selected for the portfolio.

3. Volatility Adjustment (Optional):

- Clenow sometimes adjusts momentum scores by volatility (e.g., dividing by the standard deviation of returns) to favor stocks with smoother trends.

- This reduces exposure to erratic price movements.

4. Portfolio Construction:

- A diversified portfolio of 10–25 stocks is constructed, with equal or volatility-weighted allocations.

- Position sizes are often adjusted based on risk (e.g., 1% of capital per position).

5. Rebalancing:

- The portfolio is rebalanced periodically (e.g., weekly or monthly) to maintain exposure to high-momentum stocks.

- Stocks falling below a momentum threshold are replaced with higher-ranked candidates.

6. Risk Management:

- Stop-losses or trailing stops may be applied to limit downside risk.

- Diversification across sectors reduces concentration risk.

Implementation in TradingView

Key features include:

- Customizable Lookback: Users can adjust the lookback period in pinescript (e.g., 90 days) to align with Clenow’s methodology.

- Visual Cues: Background colors (green for positive, red for negative momentum) and a zero line help identify trend strength.

- Integration with Screeners: TradingView’s stock screener can filter high-momentum stocks, which can then be analyzed with the custom indicator.

Strengths

1. Simplicity: The method is straightforward, relying on a single metric (momentum) that’s easy to calculate and interpret.

2. Empirical Support: Backed by decades of academic research and real-world hedge fund performance.

3. Adaptability: Applicable to stocks, ETFs, or other asset classes, with flexible lookback periods.

4. Risk Management: Diversification and periodic rebalancing reduce idiosyncratic risk.

5. TradingView Integration: Pine Script implementation enables real-time visualization, enhancing decision-making for stocks like NVDA or SPY.

Limitations

1. Mean Reversion Risk: Momentum can reverse sharply in bear markets or during sector rotations, leading to drawdowns.

2. Transaction Costs: Frequent rebalancing increases trading costs, especially for retail traders with high commissions. This is not as prevalent with commission free trading becoming more available.

3. Overfitting Risk: Over-optimizing lookback periods or filters can reduce out-of-sample performance.

4. Market Conditions: Underperforms in low-momentum or highly volatile markets.

Practical Applications

The Clenow Momentum Method is ideal for:

Retail Traders: Use TradingView’s screener to identify high-momentum stocks, then apply the Pine Script indicator to confirm trends.

Portfolio Managers: Build diversified momentum portfolios, rebalancing monthly to capture trends.

Swing Traders: Combine with volume filters to target short-term breakouts in high-momentum stocks.

Cross-Platform Workflow: Integrate with Python scanners to rank stocks, then visualize on TradingView for trade execution.

Comparison to Other Strategies

Vs. Minervini’s VCP: Clenow’s method is purely quantitative, while Minervini’s Volatility Contraction Pattern (your April 11, 2025 query) combines momentum with chart patterns. Clenow is more systematic but less discretionary.

Vs. Mean Reversion: Momentum bets on trend continuation, unlike mean reversion strategies that target oversold conditions.

Vs. Value Investing: Momentum outperforms in bull markets but may lag value strategies in recovery phases.

Conclusion

The Clenow Momentum Method is a robust, evidence-based strategy that capitalizes on price trends while managing risk through diversification and rebalancing. Its simplicity and adaptability make it accessible to retail traders, especially when implemented on platforms like TradingView with custom Pine Script indicators. Traders must be mindful of transaction costs, mean reversion risks, and market conditions. By combining Clenow’s momentum with volume filters and alerts, you can optimize its application for swing or position trading.

Market Open & Pre-Open Linesversion 1.0 2025-04-23

Stated vertical line for market open and pre-market open. Market option include US, EU, UK, JP and AU. This line do auto-defined during daylight saving time. This help for those trade during market open and benefit for those doing backtest on it.

Bullish and Bearish Breakout Alert for Gold Futures PullbackBelow is a Pine Script (version 6) for TradingView that includes both bullish and bearish breakout conditions for my intraday trading strategy on micro gold futures (MGC). The strategy focuses on scalping two-legged pullbacks to the 20 EMA or key levels with breakout confirmation, tailored for the Apex Trader Funding $300K challenge. The script accounts for the Daily Sentiment Index (DSI) at 87 (overbought, favoring pullbacks). It generates alerts for placing stop-limit orders for 175 MGC contracts, ensuring compliance with Apex’s rules ($7,500 trailing threshold, $20,000 profit target, 4:59 PM ET close).

Script Requirements

Version: Pine Script v6 (latest for TradingView, April 2025).

Purpose:

Bullish: Alert when price breaks above a rejection candle’s high after a two-legged pullback to the 20 EMA in a bullish trend (price above 20 EMA, VWAP, higher highs/lows).

Bearish: Alert when price breaks below a rejection candle’s low after a two-legged pullback to the 20 EMA in a bearish trend (price below 20 EMA, VWAP, lower highs/lows).

Context: 5-minute MGC chart, U.S. session (8:30 AM–12:00 PM ET), avoiding overbought breakouts above $3,450 (DSI 87).

Output: Alerts for stop-limit orders (e.g., “Buy: Stop=$3,377, Limit=$3,377.10” or “Sell: Stop=$3,447, Limit=$3,446.90”), quantity 175 MGC.

Apex Compliance: 175-contract limit, stop-losses, one-directional news trading, close by 4:59 PM ET.

How to Use the Script in TradingView

1. Add Script:

Open TradingView (tradingview.com).

Go to “Pine Editor” (bottom panel).

Copy the script from the content.

Click “Add to Chart” to apply to your MGC 5-minute chart .

2. Configure Chart:

Symbol: MGC (Micro Gold Futures, CME, via Tradovate/Apex data feed).

Timeframe: 5-minute (entries), 15-minute (trend confirmation, manually check).

Indicators: Script plots 20 EMA and VWAP; add RSI (14) and volume manually if needed .

3. Set Alerts:

Click the “Alert” icon (bell).

Add two alerts:

Bullish Breakout: Condition = “Bullish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Bearish Breakout: Condition = “Bearish Breakout Alert for Gold Futures Pullback,” trigger = “Once Per Bar Close.”

Customize messages (default provided) and set notifications (e.g., TradingView app, SMS).

Example: Bullish alert at $3,377 prompts “Stop=$3,377, Limit=$3,377.10, Quantity=175 MGC” .

4. Execute Orders:

Bullish:

Alert triggers (e.g., stop $3,377, limit $3,377.10).

In TradingView’s “Order Panel,” select “Stop-Limit,” set:

Stop Price: $3,377.

Limit Price: $3,377.10.

Quantity: 175 MGC.

Direction: Buy.

Confirm via Tradovate.

Add bracket order (OCO):

Stop-loss: Sell 175 at $3,376.20 (8 ticks, $1,400 risk).

Take-profit: Sell 87 at $3,378 (1:1), 88 at $3,379 (2:1) .

Bearish:

Alert triggers (e.g., stop $3,447, limit $3,446.90).

Select “Stop-Limit,” set:

Stop Price: $3,447.

Limit Price: $3,446.90.

Quantity: 175 MGC.

Direction: Sell.

Confirm via Tradovate.

Add bracket order:

Stop-loss: Buy 175 at $3,447.80 (8 ticks, $1,400 risk).

Take-profit: Buy 87 at $3,446 (1:1), 88 at $3,445 (2:1) .

5. Monitor:

Green triangles (bullish) or red triangles (bearish) confirm signals.

Avoid bullish entries above $3,450 (DSI 87, overbought) or bearish entries below $3,296 (support) .

Close trades by 4:59 PM ET (set 4:50 PM alert) .

Aesthetic RSI [AlchimistOfCrypto]🌌 Aesthetic RSI – Unveiling the Fractal Forces of Markets 🌌

Category: Momentum Indicators 📈

"The RSI oscillator, formalized through an advanced mathematical prism, reveals the underlying fractal structures of price movements. This indicator draws inspiration from quantum principles of divergence-convergence where the probability of a return to equilibrium increases proportionally to the distance from the median point. Our implementation employs sophisticated algorithmic smoothing to filter out the stochastic noise inherent in financial markets, allowing visualization of the true momentum forces according to thermodynamic entropy principles applied to trading systems."

📊 Professional Trading Application

The Aesthetic RSI is a visually stunning and mathematically refined take on the classic Relative Strength Index. With customizable settings, advanced smoothing, and eight unique visual palettes, it empowers traders to detect momentum shifts and divergences with unparalleled clarity.

⚙️ Indicator Configuration

- Length 📏

The core parameter (default: 20) that determines the calculation period.

- Lower values (8-14): Increase sensitivity for short-term trading.

- Higher values (21-34): Provide stronger signals for position trading.

- OverBought/OverSold Thresholds 🎯

Customizable boundaries (default: 75/25) to identify extreme market conditions.

- Calibrate based on asset volatility: Higher volatility assets may need wider thresholds (80/20) to reduce false signals.

- Style 🎨

Eight meticulously crafted visual palettes optimized for pattern recognition:

- Miami Vice (default): High-contrast cyan/magenta scheme for spotting divergences.

- Cyberpunk: Yellow/purple combo to highlight momentum shifts.

- Classic: Traditional green/red for conventional analysis.

- High Contrast: Maximum visual separation for traders with visual impairments.

- Specialized palettes (Forest, Ocean, Fire, Monochrome): Tailored for diverse market conditions.

- Mode Selection 🔄

- Full: Displays a complete gradient spectrum across the RSI range, emphasizing momentum transitions between 35-65.

- OverZone: Focuses on actionable extreme zones, reducing noise in ranging markets.

🚀 How to Use

1. Adjust Length ⏰: Set the period based on your trading style (short-term or long-term).

2. Fine-Tune Thresholds 🎚️: Customize overbought/oversold levels to match the asset’s volatility.

3. Select a Palette 🌈: Choose a visual style that enhances your pattern recognition.

4. Choose Mode 🔍: Use "Full" for detailed momentum analysis or "OverZone" for extreme zone focus.

5. Spot Divergences ✅: Look for price-RSI divergences to anticipate reversals.

6. Trade with Precision 🛡️: Combine with other indicators for high-probability setups.

📅 Release Notes (April 2025)

Aesthetic RSI blends quantum-inspired mathematics with artistic visualization, redefining momentum analysis. Stay tuned for future enhancements! ✨

🏷️ Tags

#Trading #TechnicalAnalysis #RSI #Momentum #Divergence #MultiTimeframe #TradingStrategy #RiskManagement #Forex #Stocks #Crypto #Bitcoin #AlgoTrading #DayTrading #SwingTrading #TheAlchimist #QuantumTrading #VisualTrading #PatternRecognition

SPDR Sectors TableThis script generates an interactive and customizable SPDR Sectors Table designed to monitor and analyze the performance of the 11 main sectors of the S&P 500 via sector-specific ETFs. It offers a dynamic overview of daily or periodic sector movements, making it a valuable tool for traders, analysts, and investors implementing sector rotation strategies.

█ DEFINITIONS

SPDR Sectors ETFs are exchange-traded funds managed by State Street Global Advisors, which divide the S&P 500 into the following 11 sectors:

- Communication Services (XLC)

- Consumer Discretionary (XLY)

- Consumer Staples (XLP)

- Energy (XLE)

- Financials (XLF)

- Health Care (XLV)

- Industrials (XLI)

- Materials (XLB)

- Real Estate (XLRE)

- Technology (XLK)

- Utilities (XLU)

These ETFs aim to replicate the performance of their respective sectors as defined by the Global Industry Classification Standard (GICS). The funds are periodically rebalanced to match changes in the S&P 500 composition, offering an accurate snapshot of sectoral trends.

█ INDICATOR

The table displays each sector's ticker and full name, following official GICS terminology and SPDR color coding. It also shows percentage performance, calculated daily on intraday charts or based on the selected time frame.

Users can sort the table by either percentage performance or the relative weight of each ETF in the S&P 500. The default weight values reflect data updated as of 17 April 2025, and can be manually adjusted based on the most recent sector weightings available on the official SPDR website.

[Kpt-Ahab] PnL-calculatorThe PnL-Cal shows how much you’re up or down in your own currency, based on the current exchange rate.

Let’s say your home currency is EUR.

On October 10, 2022, you bought 10 Tesla stocks at $219 apiece.

Back then, with an exchange rate of 0.9701, you spent €2,257.40.

If you sold the 10 Tesla shares on April 17, 2025 for $241.37 each, that’s around a 10% gain in USD.

But if you converted the USD back to EUR on the same day at an exchange rate of 1.1398, you’d actually end up with an overall loss of about 6.2%.

Right now, only a single entry point is supported.

If you bought shares on different days with different exchange rates, you’ll unfortunately have to enter an average for now.

For viewing on a phone, the table can be simplified.

Moving Average Shift WaveTrend StrategyMoving Average Shift WaveTrend Strategy

🧭 Overview

The Moving Average Shift WaveTrend Strategy is a trend-following and momentum-based trading system designed to be overlayed on TradingView charts. It executes trades based on the confluence of multiple technical conditions—volatility, session timing, trend direction, and oscillator momentum—to deliver logical and systematic trade entries and exits.

🎯 Strategy Objectives

Enter trades aligned with the prevailing long-term trend

Exit trades on confirmed momentum reversals

Avoid false signals using session timing and volatility filters

Apply structured risk management with automatic TP, SL, and trailing stops

⚙️ Key Features

Selectable MA types: SMA, EMA, SMMA (RMA), WMA, VWMA

Dual-filter logic using a custom oscillator and moving averages

Session and volatility filters to eliminate low-quality setups

Trailing stop, configurable Take Profit / Stop Loss logic

“In-wave flag” prevents overtrading within the same trend wave

Visual clarity with color-shifting candles and entry/exit markers

📈 Trading Rules

✅ Long Entry Conditions:

Price is above the selected MA

Oscillator is positive and rising

200-period EMA indicates an uptrend

ATR exceeds its median value (sufficient volatility)

Entry occurs between 09:00–17:00 (exchange time)

Not currently in an active wave

🔻 Short Entry Conditions:

Price is below the selected MA

Oscillator is negative and falling

200-period EMA indicates a downtrend

All other long-entry conditions are inverted

❌ Exit Conditions:

Take Profit or Stop Loss is hit

Opposing signals from oscillator and MA

Trailing stop is triggered

🛡️ Risk Management Parameters

Pair: ETH/USD

Timeframe: 4H

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pips

Risk per Trade: 2% of account equity (adjustable)

Total Trades: 224

Backtest Period: May 24, 2016 — April 7, 2025

Note: Risk parameters are fully customizable to suit your trading style and broker conditions.

🔧 Trading Parameters & Filters

Time Filter: Trades allowed only between 09:00–17:00 (exchange time)

Volatility Filter: ATR must be above its median value

Trend Filter: Long-term 200-period EMA

📊 Technical Settings

Moving Average

Type: SMA

Length: 40

Source: hl2

Oscillator

Length: 15

Threshold: 0.5

Risk Management

Take Profit: 1.5%

Stop Loss: 1.0%

Trailing Stop: 1.0%

👁️ Visual Support

MA and oscillator color changes indicate directional bias

Clear chart markers show entry and exit points

Trailing stops and risk controls are transparently managed

🚀 Strategy Improvements & Uniqueness

In-wave flag avoids repeated entries within the same trend phase

Filtering based on time, volatility, and trend ensures higher-quality trades

Dynamic high/low tracking allows precise trailing stop placement

Fully rule-based execution reduces emotional decision-making

💡 Inspirations & Attribution

This strategy is inspired by the excellent concept from:

ChartPrime – “Moving Average Shift”

It expands on the original idea with advanced trade filters and trailing logic.

Source reference:

📌 Summary

The Moving Average Shift WaveTrend Strategy offers a rule-based, reliable approach to trend trading. By combining trend and momentum filters with robust risk controls, it provides a consistent framework suitable for various market conditions and trading styles.

⚠️ Disclaimer

This script is for educational purposes only. Trading involves risk. Always use proper backtesting and risk evaluation before applying in live markets.

MA Deviation// -----------------------------------------------------------------------------

// MA Deviation Marking & Alert (MA Divergence)

// -----------------------------------------------------------------------------

// Short Title: MA Deviation Radar

// Author: zhipeng luo

// Version: 1.0

// Date: 2025-04-11

// -----------------------------------------------------------------------------

// Overview:

// This indicator identifies and highlights price bars where the closing price

// deviates significantly from its Simple Moving Average (SMA) by a user-defined

// percentage. It visually marks these bars on the chart and provides

// configurable alert conditions for threshold breaches.

//

// How it Works:

// 1. Calculates the Simple Moving Average (SMA) based on the 'MA Period' input.

// 2. Computes the percentage deviation of the closing price from the SMA value.

// Formula: `((Close - SMA) / SMA) * 100`

// 3. Compares the calculated deviation percentage against the positive and

// negative 'Threshold (%)' input values.

// 4. Marks the background of the price bars when a threshold is exceeded:

// - Red Background: Price deviation is greater than the positive threshold.

// - Green Background: Price deviation is less than the negative threshold.

// 5. Includes an optional, non-visible plot of the MA line itself.

// 6. Offers three distinct alert conditions for automation and notifications.

//

// Features:

// - Customizable Simple Moving Average period.

// - Adjustable deviation threshold percentage.

// - Clear visual signals using background colors on the main chart.

// - Built-in Alert Conditions:

// - MA Positive Deviation Alert (Triggers when price > MA + Threshold %)

// - MA Negative Deviation Alert (Triggers when price < MA - Threshold %)

// - MA Deviation Alert - Any (Triggers on either positive or negative breach)

//

// How to Use:

// - Identify Potential Extremes: Useful for spotting potential overbought (large

// positive deviation) or oversold (large negative deviation) conditions

// which might precede price corrections or mean reversion.

// - Gauge Trend Extension: Extreme deviations can sometimes indicate that a

// trend is overextended and might be due for a pause or reversal.

// - Parameter Tuning: Adjust the 'MA Period' and '(Threshold %)' settings to

// suit the specific asset, timeframe, and volatility characteristics you

// are analyzing. Lower thresholds yield more signals; higher thresholds

// focus on more significant deviations.

// - Alerts: Set up alerts via the TradingView alert menu using the provided

// conditions ("MA Positive Deviation Alert", "MA Negative Deviation Alert",

// "MA Deviation Alert - Any") to get notified of potential setups.

//

// Parameters:

// - MA Period (Default: 200): The lookback period for the SMA calculation.

// - (Threshold %) (Default: 7.0): The percentage deviation (positive and

// negative) from the MA required to trigger a background signal and alert.

//

// Alerts & Important Note:

// Three alert conditions corresponding to the signals are available:

// 1. "MA Positive Deviation Alert"

// 2. "MA Negative Deviation Alert"

// 3. "MA Deviation Alert - Any"

//

// ***Please Note:*** The value shown after "( {{plot_0}}%)" or

// "( {{plot_0}}%)" in the default alert message refers to the

// **Moving Average value** (`plot_0`), not the actual deviation percentage.

// The alert *triggers correctly* based on the deviation percentage crossing

// the threshold, but the number displayed by the `{{plot_0}}` placeholder

// in the message is the MA's value at that time due to the script's

// internal plot order.

//

// Disclaimer: This indicator is provided for informational and analytical

// purposes only. It does not constitute financial advice or a recommendation

// to buy or sell any asset. Always conduct your own research and use proper

// risk management. Trading involves significant risk.

// -----------------------------------------------------------------------------

OverUnder Yield Spread🗺️ OverUnder is a structural regime visualizer , engineered to diagnose the shape, tone, and trajectory of the yield curve. Rather than signaling trades directly, it informs traders of the world they’re operating in. Yield curve steepening or flattening, normalizing or inverting — each regime reflects a macro pressure zone that impacts duration demand, liquidity conditions, and systemic risk appetite. OverUnder abstracts that complexity into a color-coded compression map, helping traders orient themselves before making risk decisions. Whether you’re in bonds, currencies, crypto, or equities, the regime matters — and OverUnder makes it visible.

🧠 Core Logic

Built to show the slope and intent of a selected rate pair, the OverUnder Yield Spread defaults to 🇺🇸US10Y-US2Y, but can just as easily compare global sovereign curves or even dislocated monetary systems. This value is continuously monitored and passed through a debounce filter to determine whether the curve is:

• Inverted, or

• Steepening

If the curve is flattening below zero: the world is bracing for contraction. Policy lags. Risk appetite deteriorates. Duration gets bid, but only as protection. Stocks and speculative assets suffer, regardless of positioning.

📍 Curve Regimes in Bull and Bear Contexts

• Flattening occurs when the short and long ends compress . In a bull regime, flattening may reflect long-end demand or fading growth expectations. In a bear regime, flattening often precedes or confirms central bank tightening.

• Steepening indicates expanding spread . In a bull context, this may signal healthy risk appetite or early expansion. In a bear or crisis context, it may reflect aggressive front-end cuts and dislocation between short- and long-term expectations.

• If the curve is steepening above zero: the world is rotating into early expansion. Risk assets behave constructively. Bond traders position for normalization. Equities and crypto begin trending higher on rising forward expectations.

🖐️ Dynamically Colored Spread Line Reflects 1 of 4 Regime States

• 🟢 Normal / Steepening — early expansion or reflation

• 🔵 Normal / Flattening — late-cycle or neutral slowdown

• 🟠 Inverted / Steepening — policy reversal or soft landing attempt

• 🔴 Inverted / Flattening — hard contraction, credit stress, policy lag

🍋 The Lemon Label

At every bar, an anchored label floats directly on the spread line. It displays the active regime (in plain English) and the precise spread in percent (or basis points, depending on resolution). Colored lemon yellow, neither green nor red, the label is always legible — a design choice to de-emphasize bias and center the data .

🎨 Fill Zones

These bands offer spatial, persistent views of macro compression or inversion depth.

• Blue fill appears above the zero line in normal (non-inverted) conditions

• Red fill appears below the zero line during inversion

🧪 Sample Reading: 1W chart of TLT

OverUnder reveals a multi-year arc of structural inversion and regime transition. From mid-2021 through late 2023, the spread remains decisively inverted, signaling persistent flattening and credit stress as bond prices trended sharply lower. This prolonged inversion aligns with a high-volatility phase in TLT, marked by lower highs and an accelerating downtrend, confirming policy lag and macro tightening conditions.

As of early 2025, the spread has crossed back above the zero baseline into a “Normal / Steepening” regime (annotated at +0.56%), suggesting a macro inflection point. Price action remains subdued, but the shift in yield structure may foreshadow a change in trend context — particularly if follow-through in steepening persists.

🎭 Different Traders Respond Differently:

• Bond traders monitor slope change to anticipate policy pivots or recession signals.

• Equity traders use regime shifts to time rotations, from growth into defense, or from contraction into reflation.

• Currency traders interpret curve steepening as yield compression or divergence depending on region.

• Crypto traders treat inversion as a liquidity vacuum — and steepening as an early-phase risk unlock.

🛡️ Can It Compare Different Bond Markets?

Yes — with caveats. The indicator can be used to compare distinct sovereign yield instruments, for example:

• 🇫🇷FR10Y vs 🇩🇪DE10Y - France vs Germany

• 🇯🇵JP10Y vs 🇺🇸US10Y - BoJ vs Fed policy curves

However:

🙈 This no longer visualizes the domestic yield curve, but rather the differential between rate expectations across regions

🙉 The interpretation of “inversion” changes — it reflects spread compression across nations , not within a domestic yield structure

🙊 Color regimes should then be viewed as relative rate positioning , not absolute curve health

🙋🏻 Example: OverUnder compares French vs German 10Y yields

1. 🇫🇷 Change the long-duration ticker to FR10Y

2. 🇩🇪 Set the short-duration ticker to DE10Y

3. 🤔 Interpret the result as: “How much higher is France’s long-term borrowing cost vs Germany’s?”

You’ll see steepening when the spread rises (France decoupling), flattening when the spread compresses (convergence), and inversions when Germany yields rise above France’s — historically rare and meaningful.

🧐 Suggested Use

OverUnder is not a signal engine — it’s a context map. Its value comes from situating any trade idea within the prevailing yield regime. Use it before entries, not after them.

• On the 1W timeframe, OverUnder excels as a macro overlay. Yield regime shifts unfold over quarters, not days. Weekly structure smooths out rate volatility and reveals the true curvature of policy response and liquidity pressure. Use this view to orient your portfolio, define directional bias, or confirm long-duration trend turns in assets like TLT, SPX, or BTC.

• On the 1D timeframe, the indicator becomes tactically useful — especially when aligning breakout setups or trend continuations with steepening or flattening transitions. Daily views can also identify early-stage regime cracks that may not yet be visible on the weekly.

• Avoid sub-daily use unless you’re anchoring a thesis already built on higher timeframe structure. The yield curve is a macro construct — it doesn’t oscillate cleanly at intraday speeds. Shorter views may offer clarity during event-driven spikes (like FOMC reactions), but they do not replace weekly context.

Ultimately, OverUnder helps you decide: What kind of world am I trading in? Use it to confirm macro context, avoid fighting the curve, and lean into trades aligned with the broader pressure regime.

Nifty Advance/Decline Ratio - First 20 StocksNifty 20 Advance/Decline Ratio Indicator

This Pine Script tracks the Advance/Decline Ratio of the top 20 Nifty stocks (by weightage as of March 31, 2025). It helps gauge the market's strength by comparing the number of advancing vs. declining stocks among major Nifty heavyweights. The script calculates and plots the ratio, with a reference line at 1 (neutral point). This indicator resets daily and provides insights into overall market trends based on the performance of the top Nifty stocks.

Key Features:

Tracks advance/decline movements of top 20 Nifty stocks.

Plots the Advance/Decline Ratio on the chart.

Resets daily for fresh analysis.

Donchian Breakout Strategy📈 Donchian Breakout Strategy (Inspired by Way of the Turtle)

This strategy is a modern adaptation of the legendary Turtle Trading system as taught in Way of the Turtle by Curtis Faith — re-engineered for the crypto market’s volatility, 24/7 nature, and frequent fakeouts.

⸻

🐢 Original Inspiration

The original Turtle system, created by Richard Dennis and William Eckhardt, used:

• Breakouts of Donchian Channels (20-day for entry, 10-day for exit)

• Volatility-based position sizing using ATR (N)

• Simple rules, big trend exposure, and pyramiding to grow winners

It was built for futures and commodities, trading daily bars, assuming stable trading hours and regulated markets.

⸻

🚀 What’s Different in This Strategy?

✅ Optimized for Crypto

• Adapts to constant volatility and price manipulation common in crypto

• Adds commission modeling for realistic results (0.045% default)

✅ Improved Entry Filtering

• Uses EMA filter to align with trend direction

• Adds RSI momentum check to avoid early or weak breakouts

• Optional volatility and volume filters to reduce false signals

✅ Smarter Exits

• ATR-based volatility stop loss, not just Donchian reversal

• Avoids pyramiding to reduce risk from sudden reversals

✅ Backtest-Friendly

• Default backtest window starts from 2025-01-01

• Fully configurable: long/short toggle, filter control, stop loss multiplier

⸻

🧪 Use Case

• Best on trending coins with strong directional moves

• Avoids chop via filters, preserving capital

• Can be tuned for aggressive or conservative setups with just a few tweaks

Gold Opening 15-Min ORB INDICATOR by AdéThis indicator is designed for trading Gold (XAUUSD) during the first 15 minutes of major market openings: Asian, European, and US sessions. It highlights these key time windows, plots the high and low ranges of each session, and generates breakout-based buy/sell signals. Ideal for traders focusing on volatility at market opens.

Features:Session Windows:

Asian: 1:00–1:15 AM Barcelona time (23:00–23:15 UTC, CEST-adjusted).

European: 9:00–9:15 AM Barcelona time (07:00–07:15 UTC).

US: 3:30–3:45 PM Barcelona time (13:30–13:45 UTC).

Marked with yellow (Asian), green (Europe), and blue (US) triangles below bars.

High/Low Ranges:Plots horizontal lines showing the highest high and lowest low of each session’s first 15 minutes.Lines appear after each session ends and persist until the next day, color-coded to match the sessions.Breakout Signals:Buy (Long): Triggers when the closing price breaks above the highest high of the previous 5 bars during a session window (lime triangle above bar).Sell (Short): Triggers when the closing price breaks below the lowest low of the previous 5 bars during a session window (red triangle below bar).

Signals are restricted to the 15-minute session periods for focused trading.Usage:Timeframe: Optimized for 1-minute XAUUSD charts.Timezone: Set your chart to UTC for accurate session timing (script uses UTC internally, based on Barcelona CEST, UTC+2 in April).Strategy:

Use buy/sell signals for breakout trades during volatile market opens, with session ranges as support/resistance levels.Customization: Adjust the lookback variable (default: 5) to tweak signal sensitivity.Notes:Tested for April 2025 (CEST, UTC+2).

Adjust timestamp values if using outside daylight saving time (CET, UTC+1) or for different broker timezones.Best for scalping or short-term trades during high-volatility periods. Combine with other indicators for confirmation if desired.How to Use:Apply to a 1-minute XAUUSD chart.Watch for session markers (triangles) and breakout signals during the 15-minute windows.Use the high/low lines to gauge potential breakout targets or reversals.

Larry Williams POIV A/D [tradeviZion]Larry Williams' POIV A/D - Release Notes v1.0

=================================================

Release Date: 01 April 2025

OVERVIEW

--------

The Larry Williams POIV A/D (Price, Open Interest, Volume Accumulation/Distribution) indicator implements Williams' original formula while adding advanced divergence detection capabilities. This powerful tool combines price movement, open interest, and volume data to identify potential trend reversals and continuations.

FEATURES

--------

- Implements Larry Williams' original POIV A/D formula

- Divergence detection system:

* Regular divergences for trend reversal signals

* Hidden divergences for trend continuation signals

- Fast Mode option for earlier pivot detection

- Customizable sensitivity for divergence filtering

- Dynamic color visualization based on indicator direction

- Adjustable smoothing to reduce noise

- Automatic fallback to OBV when Open Interest is unavailable

FORMULA

-------

POIV A/D = CumulativeSum(Open Interest * (Close - Close ) / (True High - True Low)) + OBV

Where:

- Open Interest: Current period's open interest

- Close - Close : Price change from previous period

- True High - True Low: True Range

- OBV: On Balance Volume

DIVERGENCE TYPES

---------------

1. Regular Divergences (Reversal Signals):

- Bullish: Price makes lower lows while indicator makes higher lows

- Bearish: Price makes higher highs while indicator makes lower highs

2. Hidden Divergences (Continuation Signals):

- Bullish: Price makes higher lows while indicator makes lower lows

- Bearish: Price makes lower highs while indicator makes higher highs

REQUIREMENTS

-----------

- Works best with futures and other instruments that provide Open Interest data

- Automatically adapts to work with any instrument by using OBV when OI is unavailable

USAGE GUIDE

-----------

1. Apply the indicator to any chart

2. Configure settings:

- Adjust sensitivity for divergence detection

- Enable/disable Fast Mode for earlier signals

- Customize visual settings as needed

3. Look for divergence signals:

- Regular divergences for potential trend reversals

- Hidden divergences for trend continuation opportunities

4. Use the alerts system for automated divergence detection

KNOWN LIMITATIONS

----------------

- Requires Open Interest data for full functionality

- Fast Mode may generate more signals but with lower reliability

ACKNOWLEDGEMENTS

---------------

This indicator is based on Larry Williams' work on Open Interest analysis. The implementation includes additional features for divergence detection while maintaining the integrity of the original formula.

Gold Futures vs Spot (Candlestick + Line Overlay)📝 Script Description: Gold Futures vs Spot

This script was developed to compare the price movements between Gold Futures and Spot Gold within a specific time frame. The primary goals of this script are:

To analyze the price spread between Gold Futures and Spot

To identify potential arbitrage opportunities caused by price discrepancies

To assist in decision-making and enhance the accuracy of gold market analysis

🔧 Key Features:

Fetches price data from both Spot and Futures markets (from APIs or chart sources)

Converts and aligns data for direct comparison

Calculates the price spread (Futures - Spot)

Visualizes the spread over time or exports the data for further analysis

📅 Date Created:

🧠 Additional Notes:

This script is ideal for investors, gold traders, or analysts who want to understand the relationship between the Futures and Spot markets—especially during periods of high volatility. Unusual spreads may signal shifts in market sentiment or the actions of institutional players.

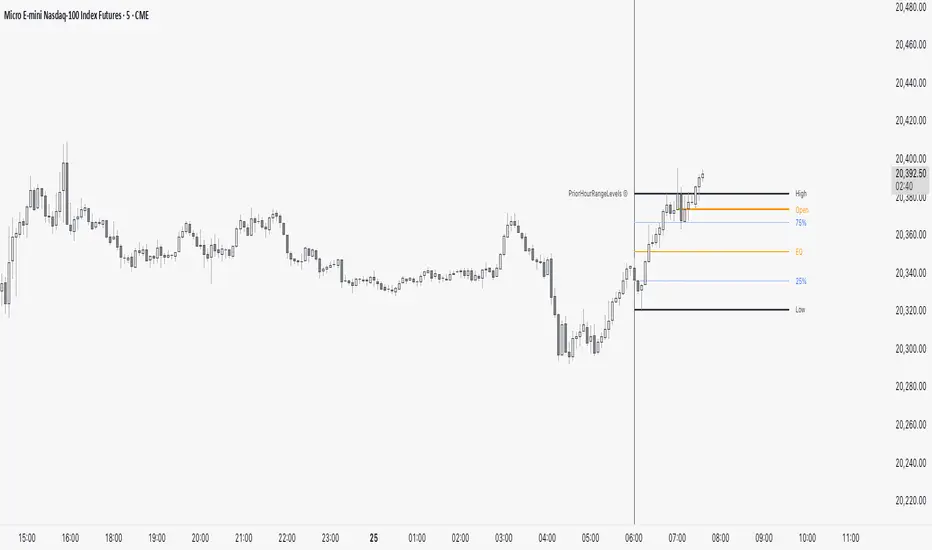

PriorHourRangeLevels_v0.1PriorHourRangeLevels_v0.1

Created by dc_77 | © 2025 | Mozilla Public License 2.0

Overview

"PriorHourRangeLevels_v0.1" is a versatile Pine Script™ indicator designed to help traders visualize and analyze price levels based on the prior hour’s range. It overlays key levels—High, Low, 75%, 50% (EQ), and 25%—from the previous hour onto the current price chart, alongside the current hour’s opening price. With customizable display options and time zone support, it’s ideal for intraday traders looking to identify support, resistance, and breakout zones.

How It Works

Hourly Reset: The indicator detects the start of each hour based on your chosen time zone (e.g., "America/New_York" by default).

Prior Hour Range: It calculates the High and Low of the previous hour, then derives three additional levels:

75%: 75% of the range above the Low.

EQ (50%): The midpoint of the range.

25%: 25% of the range above the Low.

Current Hour Open: Displays the opening price of the current hour.

Projection: Lines extend forward (default: 24 bars) to project these levels into the future, aiding in real-time analysis.

Alerts: Triggers alerts when the price crosses any of the prior hour’s levels (High, 75%, EQ, 25%, Low).

Key Features

Time Zone Flexibility: Choose from options like UTC, New York, Tokyo, or London to align with your trading session.

Visual Customization:

Toggle visibility for each level (High, Low, 75%, EQ, 25%, Open, and Anchor).

Adjust line styles (Solid, Dashed, Dotted), colors, and widths.

Show or hide labels with adjustable sizes (Tiny, Small, Normal, Large).

Anchor Line: A vertical line marks the start of the prior hour, with optional labeling.

Alert Conditions: Set up notifications for price crossings to catch key moments without watching the chart.

Usage Tips

Use the High and Low as potential breakout levels, while 75%, EQ, and 25% act as intermediate support/resistance zones.

Trend Confirmation: Watch how price interacts with the EQ (50%) level to gauge momentum.

Session Planning: Adjust the time zone to match your market (e.g., "Europe/London" for FTSE trading).

Projection Offset: Extend or shorten the lines (via "Projection Offset") based on your chart timeframe.

Inputs

Time Zone: Select your preferred market time zone.

Anchor Settings: Show/hide the prior hour start line, style, color, width, and label.

Level Settings: Customize visibility, style, color, width, and labels for Open, High, 75%, EQ, 25%, and Low.

Display: Set projection length and label size.

Momentum Volume Divergence (MVD) EnhancedMomentum Volume Divergence (MVD) Enhanced is a powerful indicator that detects price-momentum divergences and momentum suppression for reversal trading. Optimized for XRP on 1D charts, it features dynamic lookbacks, ATR-adjusted thresholds, and SMA confirmation. Signals include strong divergences (triangles) and suppression warnings (crosses). Includes a detailed user guide—try it out and share your feedback!

Setup: Add to XRP 1D chart with defaults (mom_length_base=8, vol_length_base=10). Signals: Red triangle (sell), Green triangle (buy), Orange cross (bear warning), Yellow cross (bull warning). Confirm with 5-day SMA crossovers. See full guide for details!

Disclaimer: This indicator is for educational purposes only, not financial advice. Trading involves risk—use at your discretion.

Momentum Volume Divergence (MVD) Enhanced Indicator User Guide

Version: Pine Script v6

Designed for: TradingView

Recommended Use: XRP on 1-day (1D) chart

Date: March 18, 2025

Author: Herschel with assistance from Grok 3 (xAI)

Overview

The Momentum Volume Divergence (MVD) Enhanced indicator is a powerful tool for identifying price-momentum divergences and momentum suppression patterns on XRP’s 1-day (1D) chart. Plotted below the price chart, it provides clear visual signals to help traders spot potential reversals and trend shifts.

Purpose

Detect divergences between price and momentum for buy/sell opportunities.

Highlight momentum suppression as warnings of fading trends.

Offer actionable trading signals with intuitive markers.

Indicator Components

Main Plot

Volume-Weighted Momentum (vw_mom): Blue line showing momentum adjusted by volume.

Above 0 = bullish momentum.

Below 0 = bearish momentum.

Zero Line: Gray dashed line at 0, separating bullish/bearish zones.

Key Signals

Strong Bearish Divergence:

Marker: Red triangle at the top.

Meaning: Price makes a higher high, but momentum weakens, confirmed by a drop below the 5-day SMA.

Action: Potential sell/short signal.

Strong Bullish Divergence:

Marker: Green triangle at the bottom.

Meaning: Price makes a lower low, but momentum strengthens, confirmed by a rise above the 5-day SMA.

Action: Potential buy/long signal.

Bearish Suppression:

Marker: Orange cross at the top + red background.

Meaning: Strong bullish momentum with low volume in a volume downtrend, suggesting fading strength.

Action: Warning to avoid longs or exit early.

Bullish Suppression:

Marker: Yellow cross at the bottom + green background.

Meaning: Strong bearish momentum with low volume in a volume uptrend, suggesting fading weakness.

Action: Warning to avoid shorts or exit early.

Debug Plots (Optional)

Volume Ratio: Gray line (volume vs. its MA) vs. yellow line (threshold).

Momentum Threshold: Purple lines (positive/negative momentum cutoffs).

Smoothed Momentum: Orange line (raw momentum).

Confirmation SMA: Purple line (price trend confirmation).

Labels

Text labels (e.g., "Bear Div," "Bull Supp") mark detected patterns.

How to Use the Indicator

Step-by-Step Trading Process

1. Monitor the Chart

Load your XRP 1D chart with the indicator applied.

Observe the blue vw_mom line and signal markers.

2. Spot a Signal

Primary Signals: Look for red triangles (strong_bear) or green triangles (strong_bull).

Warnings: Note orange crosses (suppression_bear) or yellow crosses (suppression_bull).

3. Confirm the Signal

For Strong Bullish Divergence (Buy):

Green triangle appears.

Price closes above the 5-day SMA (purple line) and a recent swing high.

Optional: Volume ratio (gray line) exceeds the threshold (yellow line).

For Strong Bearish Divergence (Sell):

Red triangle appears.

Price closes below the 5-day SMA and a recent swing low.

Optional: Volume ratio (gray line) falls below the threshold (yellow line).

4. Enter the Trade

Long:

Buy at the close of the signal bar.

Stop loss: Below the recent swing low or 2 × ATR(14) below entry.

Short:

Sell/short at the close of the signal bar.

Stop loss: Above the recent swing high or 2 × ATR(14) above entry.

5. Manage the Trade

Take Profit:

Aim for a 2:1 or 3:1 risk-reward ratio (e.g., risk $0.05, target $0.10-$0.15).

Or exit when an opposite suppression signal appears (e.g., orange cross for longs).

Trailing Stop:

Move stop to breakeven after a 1:1 RR move.

Trail using the 5-day SMA or 2 × ATR(14).

Early Exit:

Exit if a suppression signal appears against your position (e.g., suppression_bull while short).

6. Filter Out Noise

Avoid trades if a suppression signal precedes a divergence within 2-3 days.

Optional: Add a 50-day SMA on the price chart:

Longs only if price > 50-SMA.

Shorts only if price < 50-SMA.

Example Trades (XRP 1D)

Bullish Trade

Signal: Green triangle (strong_bull) at $0.55.

Confirmation: Price closes above 5-SMA and $0.57 high.

Entry: Buy at $0.58.

Stop Loss: $0.53 (recent low).

Take Profit: $0.63 (2:1 RR) or exit on suppression_bear.

Outcome: Price hits $0.64, exit at $0.63 for profit.

Bearish Trade

Signal: Red triangle (strong_bear) at $0.70.

Confirmation: Price closes below 5-SMA and $0.68 low.

Entry: Short at $0.67.

Stop Loss: $0.71 (recent high).

Take Profit: $0.62 (2:1 RR) or exit on suppression_bull.

Outcome: Price drops to $0.61, exit at $0.62 for profit.

Tips for Success

Combine with Price Levels:

Use support/resistance zones (e.g., weekly pivots) to confirm entries.

Monitor Volume:

Rising volume (gray line above yellow) strengthens signals.

Adjust Sensitivity:

Too many signals? Increase div_strength_threshold to 0.7.

Too few signals? Decrease to 0.3.

Backtest:

Review 20-30 past signals on XRP 1D to assess performance.

Avoid Choppy Markets:

Skip signals during low volatility (tight price ranges).

Troubleshooting

No Signals:

Lower div_strength_threshold to 0.3 or mom_threshold_base to 0.2.

Check if XRP’s volatility is unusually low.

False Signals:

Increase sma_confirm_length to 7 or add a 50-SMA filter.

Indicator Not Loading:

Ensure the script compiles without errors.

Customization (Optional)

Change Colors: Edit color.* values (e.g., color.red to color.purple).

Add Alerts: Use TradingView’s alert menu for "Strong Bearish Divergence Confirmed," etc.

Test Other Assets: Experiment with BTC or ETH, adjusting inputs as needed.

Disclaimer

This indicator is for educational purposes only and not financial advice. Trading involves risk, and past performance does not guarantee future results. Use at your own discretion.

Setup: Use on XRP 1D with defaults (mom_length_base=8, vol_length_base=10). Signals: Red triangle (sell), Green triangle (buy), Orange cross (bear warning), Yellow cross (bull warning). Confirm with 5-day SMA cross. Stop: 2x ATR(14). Profit: 2:1 RR or suppression exit. Full guide available separately!

Quantitative Easing and Tightening PeriodsQuantitative Easing (QE) and Quantitative Tightening (QT) periods based on historical events from the Federal Reserve:

Quantitative Easing (QE) Periods:

QE1:

Start: November 25, 2008

End: March 31, 2010

Description: The Federal Reserve initiated QE1 in response to the financial crisis, purchasing mortgage-backed securities and Treasuries.

QE2:

Start: November 3, 2010

End: June 29, 2011

Description: QE2 involved the purchase of $600 billion in U.S. Treasury bonds to further stimulate the economy.

QE3:

Start: September 13, 2012

End: October 29, 2014

Description: QE3 was an open-ended bond-buying program with monthly purchases of $85 billion in Treasuries and mortgage-backed securities.

QE4 (COVID-19 Pandemic Response):

Start: March 15, 2020

End: March 10, 2022

Description: The Federal Reserve engaged in QE4 in response to the economic impact of the COVID-19 pandemic, purchasing Treasuries and MBS in an effort to provide liquidity.

Quantitative Tightening (QT) Periods:

QT1:

Start: October 1, 2017

End: August 1, 2019

Description: The Federal Reserve began shrinking its balance sheet in 2017, gradually reducing its holdings of U.S. Treasuries and mortgage-backed securities. This period ended in August 2019 when the Fed decided to stop reducing its balance sheet.

QT2:

Start: June 1, 2022

End: Ongoing (as of March 2025)

Description: The Federal Reserve started QT again in June 2022, reducing its holdings of U.S. Treasuries and MBS in response to rising inflation. The Fed has continued this tightening cycle.

These periods are key moments in U.S. monetary policy, where the Fed either injected liquidity into the economy (QE) or reduced its balance sheet by not reinvesting maturing securities (QT). The exact dates and nature of these policies may vary based on interpretation and adjustments to the Fed's actions during those times.

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

Multi-Ticker RS vs SPYThis Pine Script, titled "Multi-Ticker RS vs SPY," is a clean and efficient indicator designed for TradingView, enabling traders to monitor the relative strength (RS) of up to 10 ticker symbols compared to the S&P 500 ETF (SPY) on a single chart. Ideal for options traders, such as those managing a $1,400 account, it provides a simple way to assess which stocks are outperforming or underperforming the broader market. As of February 26, 2025, the script supports any chart timeframe, such as 5-minute or daily intervals, and calculates RS based on a user-defined lookback period, defaulting to 1 bar for real-time insights.

Users can input ticker symbols via customizable settings, with defaults set to popular stocks like AAPL, TSLA, NVDA, GOOGL, AMZN, MSFT, FB, NFLX, INTC, and PYPL. The script fetches closing prices for each ticker and SPY, computes their percentage changes over the lookback period, and determines RS as the ratio of each ticker’s change to SPY’s change, handling division by zero gracefully. It displays each ticker’s current RS score in a vertical column of labels on the chart’s top-left corner, updated on the last bar to avoid clutter. Users can adjust label size (tiny, small, normal, large) and text color for visibility, ensuring a tailored, error-free experience for quick market analysis.

MACD Divergence all in oneMACD Divergence all in one

It can also be named as MACD dual divergence detector pro !

A sophisticated yet user-friendly tool designed to identify both bullish and bearish divergences using the MACD (Moving Average Convergence Divergence) indicator. This advanced script helps traders spot potential trend reversals by detecting hidden momentum shifts in the market, offering a comprehensive solution for divergence trading.

🎯 Key Features:

• Automatic detection of bullish and bearish divergences

• Clear visual signals with color-coded lines (Green for bullish, Red for bearish)

• Smart filtering system to eliminate false signals

• Customizable parameters to match your trading style

• Clean, uncluttered chart presentation

• Optimized performance for real-time analysis

• Easy-to-read labels showing divergence types

• Built-in signal spacing to avoid clustering

📊 How it works:

The indicator uses an advanced algorithm to analyze the relationship between price action and MACD momentum to identify:

Bullish Divergences:

- Price makes higher lows while MACD shows lower lows

- Signals potential trend reversal from bearish to bullish

- Marked with green lines and upward labels

Bearish Divergences:

- Price makes lower highs while MACD shows higher highs

- Signals potential trend reversal from bullish to bearish

- Marked with red lines and downward labels

⚙️ Customizable Settings:

1. MACD Parameters:

- Fast Length (default: 12)

- Slow Length (default: 26)

- Signal Length (default: 9)

2. Divergence Detection:

- Left/Right Pivot Bars

- Divergence Lookback Period

- Minimum/Maximum Divergence Length

- Divergence Strength Filter

3. Visual Settings:

- Clear color coding for easy identification

- Adjustable line thickness

- Customizable label size

💡 Best Practices:

- Most effective on higher timeframes (1H, 4H, Daily)

- Combine with support/resistance levels

- Use with trend lines and price action

- Consider volume confirmation

- Best results during trending markets

- Use appropriate stop-loss levels

🎓 Trading Tips:

1. Look for bullish divergences near support levels

2. Watch for bearish divergences near resistance zones

3. Confirm signals with other technical indicators

4. Consider market context and overall trend

5. Use proper position sizing and risk management

⚠️ Important Notes:

- Past performance doesn't guarantee future results

- Always use proper risk management

- Test settings on historical data first

- Different timeframes may require parameter adjustments

- Not all divergences lead to reversals

Created by: Anmol-max-star

Last Updated: 2025-02-25 16:15:08 UTC

📌 Regular updates and improvements planned!

Disclaimer:

This indicator is for informational purposes only. Always conduct your own analysis and use proper risk management techniques. Trading involves risk of loss, and past performance does not guarantee future results.

🤝 Support:

Feel free to leave comments for:

- Suggestions

- Improvements

- Feature requests

- Bug reports

- General feedback

Your feedback helps make this tool better for everyone!

Happy Trading and May the Trends Be With You! 📈