Ichimoku Cloud Score v1.0This script calculates a simple Ichimoku Score based on the signals documented here , with a few additions. Each of the score components can be individually weighted via the script inputs . The output is a plot of the normalized Ichimoku score, in the range of -100 to 100.

This script has been heavily modified from 'Ichimoku Cloud Signal Score v2.0.0 '. Credit to user 'dashed' for the initial implementation.

This has been modified with several refinements:

Clean/Organized Code

Simplified Inputs

Improved Style

Scores normalized to a range (-100, 100)

Bugfixes and Improvements

Script Inputs: i.imgur.com

Cerca negli script per "100万新币等于多少人民币"

Volume RatioDefinition:

Volume ratio can be obtained in a similar way to RSI.

Volume Ratio (%) = 100 - 100/(1+vr)

The parameter "vr" is defined as

vr=(A+U/2)/(D+U/2)

A=Total volume of the periods when the price advanced

D=Total volume of the periods when the price declined

U=Total volume of the periods when the price unchanged

After substitution, following expression can be derived and the denominator represents total volume of all periods.

Volume Ratio (%) = 100 x (A+U/2)/(A+D+U)

Notes:

A similar method to interpret RSI can be employed.

1) Overbought level over 70% and oversold level under 30%. These levels need to be adjusted according to the periods, time frames and issues.

2) Bullish picture over 50% line and bearish picture under 50% line.

3) Crossing oversold level to the upside can be taken as a confirmation of bullish reversal. - and vice versa for a bearish reversal.

4) After a long-term bearish market, the increase of volume can happen in the early stage of a bullish market.

5) Buying opportunity can be suggested when the volume ratio is declining and the price is either advancing or leveling off.

CCI with Volume Weighted EMA Here is an attempt to improve on the CCI using a volume weighted ema which is then plugged into the CCI formula.

Use:

The CCI with VW EMA is an oscillator that gives readings between -100 and +100. The usual use is to 'go long' with values over +100 and short on values less than -100.

Another use of this oscillator is a countertrend indicator where one sells at crosses under +100 and buys on crosses over -100.

Multi-Functional Fisher Transform MTF with MACDL TRIGGERWhat this indicator gives you is a true signal when price is exhausted and ready for a fast turnaround. Fisher Transform is set for multi-time frame and also allows the user to change the length. This way a user can compare two or more time spans and lengths to look for these MACDL divergent triggers after a Fisher exhaustion. With so many indicators, it's probably best to merge these indicators and change the Fisher and Trigger colors so you can still have a look at price action (remember to scale right after merger). I've noticed from time to time when you have Fisher 34 100 and 300 up and running on two different time frames such as 5 and 15 min charts, with MACDL triggers on the 100/300 or 34/100 you get a high probability trade trigger. However, there are rare exceptions such as when price moves in a parabolic state up or down for a long period where this indication does not work. Ideally this indicator works best in a sideways market or slow rising/descending moving market.

This indicator was worked on by Glaz, nmike and myself

LazyBear also introduced the MACDL indicator

CCI Crossover AlertThis very simple indicator will give you a blue background where the CCI crossed from below -100 to above -100, and a red background where it crossed from above 100 to below 100.

SMC Statistical Liquidity Walls [PhenLabs]📊 SMC Statistical Liquidity Walls

Version: PineScript™ v6

📌 Description

The SMC Statistical Liquidity Walls indicator is designed to visualize market volatility and potential reversal zones using advanced statistical modeling. Unlike traditional Bollinger Bands that use simple lines, this script utilizes an “Inverted Sigmoid” opacity function to create a “fog of war” effect. This visualizes the density of liquidity: the further price moves from the equilibrium (mean), the “harder” the liquidity wall becomes.

This tool solves the problem of over-trading in low-probability areas. By automatically mapping “Premium” (Resistance) and “Discount” (Support) zones based on Standard Deviation (SD), traders can instantly see when price is overextended. The result is a clean, intuitive overlay that helps you identify high-probability mean reversion setups without cluttering your chart with manual drawings.

🚀 Points of Innovation

Inverted Sigmoid Logic: A custom mathematical function maps Standard Deviation to opacity, creating a realistic “wall” density effect rather than linear gradients.

Dynamic “Solidity”: The indicator is transparent at the center (Equilibrium) and becomes visually solid at the edges, mimicking physical resistance.

Separated Directional Bias: distinct Red (Premium) and Green (Discount) coding helps SMC traders instantly recognize expensive vs. cheap pricing.

Smart “Safe” Deviation: Includes fallback logic to handle calculation errors if deviation hits zero, ensuring the indicator never crashes during data gaps.

🔧 Core Components

Basis Calculation: Uses a Simple Moving Average (SMA) to determine the market’s equilibrium point.

Standard Deviation Zones: Calculates 1SD, 2SD, and 3SD levels to define the statistical extremes of price action.

Sigmoid Alpha Calculation: Converts the SD distance into a transparency value (0-100) to drive the visual gradient.

🔥 Key Features

Automated Premium/Discount Zones: Red zones indicate overbought (Premium) areas; Green zones indicate oversold (Discount) areas.

Customizable Density: Users can adjust the “Steepness” and “Midpoint” of the sigmoid curve to control how fast the walls become solid.

Integrated Alerts: Built-in alert conditions trigger when price hits the “Solid” wall (2SD or higher), perfect for automated trading or notifications.

Visual Clarity: The center of the chart remains clear (high transparency) to keep focus on price action where it matters most.

🎨 Visualization

Equilibrium Line: A gray line representing the mean price.

Gradient Fills: The space between bands fills with color that increases in opacity as it moves outward.

Premium Wall: Upper zones fade from transparent red to solid red.

Discount Wall: Lower zones fade from transparent green to solid green.

📖 Usage Guidelines

Range Period: Default 20. Controls the lookback period for the SMA and Standard Deviation calculation.

Source: Default Close. The price data used for calculations.

Center Transparency: Default 100 (Clear). Controls how transparent the middle of the chart is.

Edge Transparency: Default 45 (Solid). Controls the opacity of the outermost liquidity wall.

Wall Steepness: Default 2.5. Adjusts how aggressively the gradient transitions from clear to solid.

Wall Start Point: Default 1.5 SD. The deviation level where the gradient shift begins to accelerate.

✅ Best Use Cases

Mean Reversion Trading: Enter trades when price hits the solid 2SD or 3SD wall and shows rejection wicks.

Take Profit Targets: Use the Equilibrium (Gray Line) as a logical first target for reversal trades.

Trend Filtering: Do not initiate new long positions when price is deep inside the Red (Premium) wall.

⚠️ Limitations

Lagging Nature: As a statistical tool based on Moving Averages, the walls react to past price data and may lag during sudden volatility spikes.

Trending Markets: In strong parabolic trends, price can “ride” the bands for extended periods; mean reversion should be used with caution in these conditions.

💡 What Makes This Unique

Physics-Based Visualization: We treat liquidity as a physical barrier that gets denser the deeper you push, rather than just a static line on a chart.

🔬 How It Works

Step 1: The script calculates the mean (SMA) and the Standard Deviation (SD) of the source price.

Step 2: It defines three zones above and below the mean (1SD, 2SD, 3SD).

Step 3: The custom `get_inverted_sigmoid` function calculates an Alpha (transparency) value based on the SD distance.

Step 4: Plot fills are colored dynamically, creating a seamless gradient that hardens at the extremes to visualize the “Liquidity Wall.”

💡 Note

For best results, combine this indicator with Price Action confirmation (such as pin bars or engulfing candles) when price touches the solid walls.

MTF RSI Stacked + AI + Gradient MTF RSI Stacked + AI + Gradient

Quick-start guide & best-practice rules

What the indicator does

Multi-Time-Frame RSI in one pane

• 10 time-frames (1 m → 1 M) are stacked 100 points apart (0, 100, 200 … 900).

• Each RSI is plotted with a smooth red-yellow-green gradient:

– Red = RSI below 30 (oversold)

– Yellow = RSI near 50

– Green = RSI above 70 (overbought)

• Grey 30-70 bands are drawn for every TF so you can see extremities at a glance.

Built-in AI (KNN) signal

• On every close of the chosen AI-time-frame the script:

– Takes the last 14-period RSI + normalised ATR as “features”

– Compares them to the last N bars (default 1 000)

– Votes of the k = 5 closest neighbours → BUY / SELL / NEUTRAL

• Confidence % is shown in the badge (top-right).

• A thick vertical line (green/red) is printed once when the signal flips.

How to read it

• Gradient colour tells you instantly which TFs are overbought/obove sold.

• When all or most gradients are green → broad momentum up; look for shorts only on lower-TF pullbacks.

• When most are red → broad momentum down; favour longs only on lower-TF bounces.

• Use the AI signal as a confluence filter, not a stand-alone entry:

– If AI = BUY and 3+ higher-TF RSIs just crossed > 50 → consider long.

– If AI = SELL and 3+ higher-TF RSIs just crossed < 50 → consider short.

• Divergences: price makes a higher high but 1 h/4 h RSI (gradient) makes a lower high → possible reversal.

Settings you can tweak

AI timeframe – leave empty = same as chart, or pick a higher TF (e.g. “15” or “60”) to slow the signal down.

Training bars – 500-2 000 is the sweet spot; bigger = slower but more stable.

K neighbours – 3-7; lower = more signals, higher = smoother.

RSI length – 14 is standard; 9 gives earlier turns, 21 gives fewer false swings.

Practical trading workflow

Open the symbol on your execution TF (e.g. 5 m).

Set AI timeframe to 3-5× execution TF (e.g. 15 m or 30 m) so the signal survives market noise.

Wait for AI signal to align with gradient extremes on at least one higher TF.

Enter on the first gradient reversal inside the 30-70 band on the execution TF.

Place stop beyond the swing that caused the gradient flip; target next opposing 70/30 level on the same TF or trail with structure.

Colour cheat-sheet

Bright green → RSI ≥ 70 (overbought)

Bright red → RSI ≤ 30 (oversold)

Muted colours → RSI near 50 (neutral, momentum pause)

That’s it—one pane, ten time-frames, colour-coded extremes and an AI confluence layer.

Keep the chart clean, use price action for precise entries, and let the gradient tell you when the wind is at your back.

CCI Threshold HistogramSynopsis

The Custom CCI Indicator by Simon20cent enhances traditional CCI analysis with adjustable smoothing and a momentum-based histogram. The histogram highlights key thresholds, turning green above +100 and red below –100 to clearly identify strong bullish or bearish momentum. Both the CCI and smoothed CCI lines can be toggled for a cleaner view, making this tool effective for spotting momentum shifts, breakout conditions, and potential entry zones with improved clarity.

GainzAlgo V2 [Alpha]// © GainzAlgo

//@version=5

indicator('GainzAlgo V2 ', overlay=true, max_labels_count=500)

show_tp_sl = input.bool(true, 'Display TP & SL', group='Techical', tooltip='Display the exact TP & SL price levels for BUY & SELL signals.')

rrr = input.string('1:2', 'Risk to Reward Ratio', group='Techical', options= , tooltip='Set a risk to reward ratio (RRR).')

tp_sl_multi = input.float(1, 'TP & SL Multiplier', 1, group='Techical', tooltip='Multiplies both TP and SL by a chosen index. Higher - higher risk.')

tp_sl_prec = input.int(2, 'TP & SL Precision', 0, group='Techical')

candle_stability_index_param = 0.7

rsi_index_param = 80

candle_delta_length_param = 10

disable_repeating_signals_param = input.bool(true, 'Disable Repeating Signals', group='Techical', tooltip='Removes repeating signals. Useful for removing clusters of signals and general clarity.')

GREEN = color.rgb(29, 255, 40)

RED = color.rgb(255, 0, 0)

TRANSPARENT = color.rgb(0, 0, 0, 100)

label_size = input.string('huge', 'Label Size', options= , group='Cosmetic')

label_style = input.string('text bubble', 'Label Style', , group='Cosmetic')

buy_label_color = input(GREEN, 'BUY Label Color', inline='Highlight', group='Cosmetic')

sell_label_color = input(RED, 'SELL Label Color', inline='Highlight', group='Cosmetic')

label_text_color = input(color.white, 'Label Text Color', inline='Highlight', group='Cosmetic')

stable_candle = math.abs(close - open) / ta.tr > candle_stability_index_param

rsi = ta.rsi(close, 14)

atr = ta.atr(14)

bullish_engulfing = close < open and close > open and close > open

rsi_below = rsi < rsi_index_param

decrease_over = close < close

var last_signal = ''

var tp = 0.

var sl = 0.

bull_state = bullish_engulfing and stable_candle and rsi_below and decrease_over and barstate.isconfirmed

bull = bull_state and (disable_repeating_signals_param ? (last_signal != 'buy' ? true : na) : true)

bearish_engulfing = close > open and close < open and close < open

rsi_above = rsi > 100 - rsi_index_param

increase_over = close > close

bear_state = bearish_engulfing and stable_candle and rsi_above and increase_over and barstate.isconfirmed

bear = bear_state and (disable_repeating_signals_param ? (last_signal != 'sell' ? true : na) : true)

round_up(number, decimals) =>

factor = math.pow(10, decimals)

math.ceil(number * factor) / factor

if bull

last_signal := 'buy'

dist = atr * tp_sl_multi

tp_dist = rrr == '2:3' ? dist / 2 * 3 : rrr == '1:2' ? dist * 2 : rrr == '1:4' ? dist * 4 : dist

tp := round_up(close + tp_dist, tp_sl_prec)

sl := round_up(close - dist, tp_sl_prec)

if label_style == 'text bubble'

label.new(bar_index, low, 'BUY', color=buy_label_color, style=label.style_label_up, textcolor=label_text_color, size=label_size)

else if label_style == 'triangle'

label.new(bar_index, low, 'BUY', yloc=yloc.belowbar, color=buy_label_color, style=label.style_triangleup, textcolor=TRANSPARENT, size=label_size)

else if label_style == 'arrow'

label.new(bar_index, low, 'BUY', yloc=yloc.belowbar, color=buy_label_color, style=label.style_arrowup, textcolor=TRANSPARENT, size=label_size)

label.new(show_tp_sl ? bar_index : na, low, 'TP: ' + str.tostring(tp) + '\nSL: ' + str.tostring(sl), yloc=yloc.price, color=color.gray, style=label.style_label_down, textcolor=label_text_color)

if bear

last_signal := 'sell'

dist = atr * tp_sl_multi

tp_dist = rrr == '2:3' ? dist / 2 * 3 : rrr == '1:2' ? dist * 2 : rrr == '1:4' ? dist * 4 : dist

tp := round_up(close - tp_dist, tp_sl_prec)

sl := round_up(close + dist, tp_sl_prec)

if label_style == 'text bubble'

label.new(bear ? bar_index : na, high, 'SELL', color=sell_label_color, style=label.style_label_down, textcolor=label_text_color, size=label_size)

else if label_style == 'triangle'

label.new(bear ? bar_index : na, high, 'SELL', yloc=yloc.abovebar, color=sell_label_color, style=label.style_triangledown, textcolor=TRANSPARENT, size=label_size)

else if label_style == 'arrow'

label.new(bear ? bar_index : na, high, 'SELL', yloc=yloc.abovebar, color=sell_label_color, style=label.style_arrowdown, textcolor=TRANSPARENT, size=label_size)

label.new(show_tp_sl ? bar_index : na, low, 'TP: ' + str.tostring(tp) + '\nSL: ' + str.tostring(sl), yloc=yloc.price, color=color.gray, style=label.style_label_up, textcolor=label_text_color)

alertcondition(bull or bear, 'BUY & SELL Signals', 'New signal!')

alertcondition(bull, 'BUY Signals (Only)', 'New signal: BUY')

alertcondition(bear, 'SELL Signals (Only)', 'New signal: SELL')

NQ-VIX Expected Move LevelsNQ -VIX Daily Price Bands

This indicator plots dynamic intraday price bands for NQ futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Open + (NQ Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily Open - (NQ Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's open.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's open

Lower band (red) contracts from the current day's open

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Information table displaying:

Current NQ price and VIX level

Daily Open

Expected move

NQ-VIX Expected Move LTF LevelsNQ -VIX LTF Price Bands

This indicator plots dynamic intraday price bands for NQ futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = (Input TF Open) + (NQ Price × VIX x √(Input TF ÷ (23h in min) ) ÷ 100

Lower Band = Daily Open - (NQ Price × VIX x √(Input TF ÷ (23h in min) ) ÷ 100

The calculation uses the square root of Input TF ÷ (23h in min) to convert annualized VIX volatility into an expected TF move, then scales it as a percentage adjustment from the current TF input's open.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current TF's open

Lower band (red) contracts from the current TF's open

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Information table displaying:

Current input TF

Current NQ price and VIX level

Current input TF Open

Expected move

Viprasol Elite Advanced Pattern Scanner# 🚀 Viprasol Elite Advanced Pattern Scanner

## Overview

The **Viprasol Elite Advanced Pattern Scanner** is a sophisticated technical analysis tool designed to identify high-probability double bottom (DISCOUNT) and double top (PREMIUM) patterns with unprecedented accuracy. Unlike basic pattern detectors, this elite scanner employs an AI-powered quality scoring system to filter out false signals and highlight only the most reliable trading opportunities.

## 🎯 Key Features

### Advanced Pattern Detection

- **DISCOUNT Patterns** (Double Bottoms): Identifies bullish reversal zones where price may bounce

- **PREMIUM Patterns** (Double Tops): Detects bearish reversal zones where price may decline

- Multi-point validation system (5-point structure)

- Symmetry analysis with customizable tolerance

### 🤖 AI Quality Scoring System

Each pattern receives a quality score (0-100) based on:

- **Symmetry Analysis** (32% weight): How closely the two bottoms/tops match

- **Trend Context** (22% weight): Strength of the preceding trend using ADX

- **Volume Profile** (22% weight): Volume confirmation at key points

- **Pattern Depth** (16% weight): Significance of the pattern's price range

- **Structure Quality** (16% weight): Overall pattern formation quality

Quality Grades:

- ⭐ **ELITE** (88-100): Highest probability setups

- ✨ **VERY STRONG** (77-87): Strong trade opportunities

- ✓ **STRONG** (67-76): Valid patterns with good potential

- ○ **VALID** (65-66): Acceptable patterns meeting minimum criteria

### 🎯 Intelligent Target System

Three target modes per pattern direction:

- **Conservative**: 0.618 Fibonacci extension (safer, closer targets)

- **Balanced**: 1.0 extension (moderate risk/reward)

- **Aggressive**: 1.618 extension (higher risk/reward)

Targets automatically adjust based on pattern quality score.

### 🔧 Advanced Filtering Options

- **Volatility Filter (ATR)**: Excludes patterns during extreme volatility

- **Momentum Filter (ADX)**: Ensures sufficient trend strength

- **Liquidity Filter (Volume)**: Confirms adequate trading volume

### 📊 Pattern Lifecycle Management

- Real-time neckline tracking with extension multiplier

- Pattern invalidation after extended wait period

- Breakout/breakdown confirmation

- Reversal detection (pattern failure scenarios)

- Target achievement tracking

### 🌈 Premium Visual System

- Color-coded quality levels

- Cyber-themed color scheme (Neon Green/Hot Pink/Purple/Cyan)

- Transparent fills for pattern zones

- Dynamic labels with pattern information

- Elite dashboard showing live pattern stats

## 📈 How To Use

### Basic Setup

1. Add indicator to your chart

2. Enable desired patterns (DISCOUNT and/or PREMIUM)

3. Adjust quality threshold (default: 65) - higher = fewer but better signals

4. Set your preferred target mode

### Trading DISCOUNT Patterns (Bullish)

1. Wait for pattern detection (labeled points 1-4)

2. Check quality score on dashboard

3. Entry on breakout above neckline (point 5)

4. Stop loss below the lowest bottom

5. Target shown automatically based on your mode

6. ⚠️ Watch for pattern failure (break below bottoms = SHORT signal)

### Trading PREMIUM Patterns (Bearish)

1. Wait for pattern detection (labeled points 1-4)

2. Check quality score on dashboard

3. Entry on breakdown below neckline (point 5)

4. Stop loss above the highest top

5. Target shown automatically based on your mode

6. ⚠️ Watch for pattern failure (break above tops = LONG signal)

## ⚙️ Input Settings Guide

### 🔍 Detection Engine

- **Left/Right Pivots**: Higher = fewer but cleaner patterns (default: 6/4)

- **Min Pattern Width**: Minimum bars between bottoms/tops (default: 12)

- **Symmetry Tolerance**: Max % difference allowed between levels (default: 1.8%)

- **Extension Multiplier**: How long to wait for breakout (default: 2.2x pattern width)

### ⭐ Quality AI

- **Min Quality Score**: Only show patterns above this score (default: 65)

- **Weight Distribution**: Customize what matters most (symmetry/trend/volume/depth/structure)

### 🔧 Filters

- **Volatility Filter**: Avoid choppy markets (recommended: ON)

- **Momentum Filter**: Ensure trend strength (recommended: ON)

- **Liquidity Filter**: Volume confirmation (recommended: ON)

### 💎 Target System

- Choose target aggression for each pattern type and direction

- Higher quality patterns get adjusted targets automatically

## 🎨 Visual Customization

- Adjust colors for DISCOUNT/PREMIUM patterns

- Set quality-based color coding

- Customize label sizes

- Toggle dashboard visibility and position

- Show/hide historical patterns

## 🚨 Alert System

Set up TradingView alerts for:

- 🚀 **LONG Signals**: DISCOUNT breakout, PREMIUM failure

- 📉 **SHORT Signals**: PREMIUM breakdown, DISCOUNT failure

- ✅ **Target Achievement**: When price hits your target

## 💡 Pro Tips

1. **Higher Timeframes = Better Signals**: Patterns on 4H, Daily, Weekly are more reliable

2. **Quality Over Quantity**: Focus on ELITE and VERY STRONG grades

3. **Combine with Trend**: DISCOUNT in uptrend, PREMIUM in downtrend = best results

4. **Watch Pattern Failures**: Failed patterns often provide strong counter-trend signals

5. **Adjust for Your Style**: Intraday traders use Conservative, swing traders use Aggressive

## 🔒 Pattern Invalidation

Patterns become invalid if:

- No breakout/breakdown within extension period

- Support/resistance levels are broken prematurely

- Pattern shown in faded colors = no longer active

## ⚠️ Risk Disclaimer

This indicator is a tool for technical analysis and does not guarantee profitable trades. Always:

- Use proper risk management

- Combine with other analysis methods

- Never risk more than you can afford to lose

- Past performance does not indicate future results

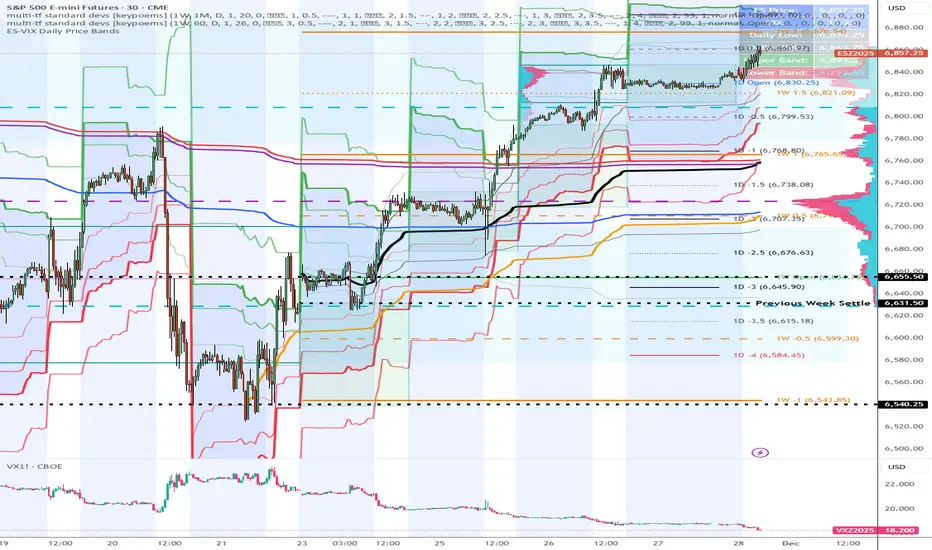

ES-VIX Expected Move LTF LevelsES-VIX LTF Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = (Input TF Open) + (ES Price × VIX x √(Input TF ÷ (23h in min) ) ÷ 100

Lower Band = Daily Open - (ES Price × VIX x √(Input TF ÷ (23h in min) ) ÷ 100

The calculation uses the square root of Input TF ÷ (23h in min) to convert annualized VIX volatility into an expected TF move, then scales it as a percentage adjustment from the current TF input's open.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current TF's open

Lower band (red) contracts from the current TF's open

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Information table displaying:

Current input TF

Current ES price and VIX level

Current input TF Open

Expected move

Hurst Exponent - Detrended Fluctuation AnalysisIn stochastic processes, chaos theory and time series analysis, detrended fluctuation analysis (DFA) is a method for determining the statistical self-affinity of a signal. It is useful for analyzing time series that appear to be long-memory processes and noise.

█ OVERVIEW

We have introduced the concept of Hurst Exponent in our previous open indicator Hurst Exponent (Simple). It is an indicator that measures market state from autocorrelation. However, we apply a more advanced and accurate way to calculate Hurst Exponent rather than simple approximation. Therefore, we recommend using this version of Hurst Exponent over our previous publication going forward. The method we used here is called detrended fluctuation analysis. (For folks that are not interested in the math behind the calculation, feel free to skip to "features" and "how to use" section. However, it is recommended that you read it all to gain a better understanding of the mathematical reasoning).

█ Detrend Fluctuation Analysis

Detrended Fluctuation Analysis was first introduced by by Peng, C.K. (Original Paper) in order to measure the long-range power-law correlations in DNA sequences . DFA measures the scaling-behavior of the second moment-fluctuations, the scaling exponent is a generalization of Hurst exponent.

The traditional way of measuring Hurst exponent is the rescaled range method. However DFA provides the following benefits over the traditional rescaled range method (RS) method:

• Can be applied to non-stationary time series. While asset returns are generally stationary, DFA can measure Hurst more accurately in the instances where they are non-stationary.

• According the the asymptotic distribution value of DFA and RS, the latter usually overestimates Hurst exponent (even after Anis- Llyod correction) resulting in the expected value of RS Hurst being close to 0.54, instead of the 0.5 that it should be. Therefore it's harder to determine the autocorrelation based on the expected value. The expected value is significantly closer to 0.5 making that threshold much more useful, using the DFA method on the Hurst Exponent (HE).

• Lastly, DFA requires lower sample size relative to the RS method. While the RS method generally requires thousands of observations to reduce the variance of HE, DFA only needs a sample size greater than a hundred to accomplish the above mentioned.

█ Calculation

DFA is a modified root-mean-squares (RMS) analysis of a random walk. In short, DFA computes the RMS error of linear fits over progressively larger bins (non-overlapped “boxes” of similar size) of an integrated time series.

Our signal time series is the log returns. First we subtract the mean from the log return to calculate the demeaned returns. Then, we calculate the cumulative sum of demeaned returns resulting in the cumulative sum being mean centered and we can use the DFA method on this. The subtraction of the mean eliminates the “global trend” of the signal. The advantage of applying scaling analysis to the signal profile instead of the signal, allows the original signal to be non-stationary when needed. (For example, this process converts an i.i.d. white noise process into a random walk.)

We slice the cumulative sum into windows of equal space and run linear regression on each window to measure the linear trend. After we conduct each linear regression. We detrend the series by deducting the linear regression line from the cumulative sum in each windows. The fluctuation is the difference between cumulative sum and regression.

We use different windows sizes on the same cumulative sum series. The window sizes scales are log spaced. Eg: powers of 2, 2,4,8,16... This is where the scale free measurements come in, how we measure the fractal nature and self similarity of the time series, as well as how the well smaller scale represent the larger scale.

As the window size decreases, we uses more regression lines to measure the trend. Therefore, the fitness of regression should be better with smaller fluctuation. It allows one to zoom into the “picture” to see the details. The linear regression is like rulers. If you use more rulers to measure the smaller scale details you will get a more precise measurement.

The exponent we are measuring here is to determine the relationship between the window size and fitness of regression (the rate of change). The more complex the time series are the more it will depend on decreasing window sizes (using more linear regression lines to measure). The less complex or the more trend in the time series, it will depend less. The fitness is calculated by the average of root mean square errors (RMS) of regression from each window.

Root mean Square error is calculated by square root of the sum of the difference between cumulative sum and regression. The following chart displays average RMS of different window sizes. As the chart shows, values for smaller window sizes shows more details due to higher complexity of measurements.

The last step is to measure the exponent. In order to measure the power law exponent. We measure the slope on the log-log plot chart. The x axis is the log of the size of windows, the y axis is the log of the average RMS. We run a linear regression through the plotted points. The slope of regression is the exponent. It's easy to see the relationship between RMS and window size on the chart. Larger RMS equals less fitness of the regression. We know the RMS will increase (fitness will decrease) as we increases window size (use less regressions to measure), we focus on the rate of RMS increasing (how fast) as window size increases.

If the slope is < 0.5, It means the rate of of increase in RMS is small when window size increases. Therefore the fit is much better when it's measured by a large number of linear regression lines. So the series is more complex. (Mean reversion, negative autocorrelation).

If the slope is > 0.5, It means the rate of increase in RMS is larger when window sizes increases. Therefore even when window size is large, the larger trend can be measured well by a small number of regression lines. Therefore the series has a trend with positive autocorrelation.

If the slope = 0.5, It means the series follows a random walk.

█ FEATURES

• Sample Size is the lookback period for calculation. Even though DFA requires a lower sample size than RS, a sample size larger > 50 is recommended for accurate measurement.

• When a larger sample size is used (for example = 1000 lookback length), the loading speed may be slower due to a longer calculation. Date Range is used to limit numbers of historical calculation bars. When loading speed is too slow, change the data range "all" into numbers of weeks/days/hours to reduce loading time. (Credit to allanster)

• “show filter” option applies a smoothing moving average to smooth the exponent.

• Log scale is my work around for dynamic log space scaling. Traditionally the smallest log space for bars is power of 2. It requires at least 10 points for an accurate regression, resulting in the minimum lookback to be 1024. I made some changes to round the fractional log space into integer bars requiring the said log space to be less than 2.

• For a more accurate calculation a larger "Base Scale" and "Max Scale" should be selected. However, when the sample size is small, a larger value would cause issues. Therefore, a general rule to be followed is: A larger "Base Scale" and "Max Scale" should be selected for a larger the sample size. It is recommended for the user to try and choose a larger scale if increasing the value doesn't cause issues.

The following chart shows the change in value using various scales. As shown, sometimes increasing the value makes the value itself messy and overshoot.

When using the lowest scale (4,2), the value seems stable. When we increase the scale to (8,2), the value is still alright. However, when we increase it to (8,4), it begins to look messy. And when we increase it to (16,4), it starts overshooting. Therefore, (8,2) seems to be optimal for our use.

█ How to Use

Similar to Hurst Exponent (Simple). 0.5 is a level for determine long term memory.

• In the efficient market hypothesis, market follows a random walk and Hurst exponent should be 0.5. When Hurst Exponent is significantly different from 0.5, the market is inefficient.

• When Hurst Exponent is > 0.5. Positive Autocorrelation. Market is Trending. Positive returns tend to be followed by positive returns and vice versa.

• Hurst Exponent is < 0.5. Negative Autocorrelation. Market is Mean reverting. Positive returns trends to follow by negative return and vice versa.

However, we can't really tell if the Hurst exponent value is generated by random chance by only looking at the 0.5 level. Even if we measure a pure random walk, the Hurst Exponent will never be exactly 0.5, it will be close like 0.506 but not equal to 0.5. That's why we need a level to tell us if Hurst Exponent is significant.

So we also computed the 95% confidence interval according to Monte Carlo simulation. The confidence level adjusts itself by sample size. When Hurst Exponent is above the top or below the bottom confidence level, the value of Hurst exponent has statistical significance. The efficient market hypothesis is rejected and market has significant inefficiency.

The state of market is painted in different color as the following chart shows. The users can also tell the state from the table displayed on the right.

An important point is that Hurst Value only represents the market state according to the past value measurement. Which means it only tells you the market state now and in the past. If Hurst Exponent on sample size 100 shows significant trend, it means according to the past 100 bars, the market is trending significantly. It doesn't mean the market will continue to trend. It's not forecasting market state in the future.

However, this is also another way to use it. The market is not always random and it is not always inefficient, the state switches around from time to time. But there's one pattern, when the market stays inefficient for too long, the market participants see this and will try to take advantage of it. Therefore, the inefficiency will be traded away. That's why Hurst exponent won't stay in significant trend or mean reversion too long. When it's significant the market participants see that as well and the market adjusts itself back to normal.

The Hurst Exponent can be used as a mean reverting oscillator itself. In a liquid market, the value tends to return back inside the confidence interval after significant moves(In smaller markets, it could stay inefficient for a long time). So when Hurst Exponent shows significant values, the market has just entered significant trend or mean reversion state. However, when it stays outside of confidence interval for too long, it would suggest the market might be closer to the end of trend or mean reversion instead.

Larger sample size makes the Hurst Exponent Statistics more reliable. Therefore, if the user want to know if long term memory exist in general on the selected ticker, they can use a large sample size and maximize the log scale. Eg: 1024 sample size, scale (16,4).

Following Chart is Bitcoin on Daily timeframe with 1024 lookback. It suggests the market for bitcoin tends to have long term memory in general. It generally has significant trend and is more inefficient at it's early stage.

Expected Move BandsExpected move is the amount that an asset is predicted to increase or decrease from its current price, based on the current levels of volatility.

In this model, we assume asset price follows a log-normal distribution and the log return follows a normal distribution.

Note: Normal distribution is just an assumption, it's not the real distribution of return

Settings:

"Estimation Period Selection" is for selecting the period we want to construct the prediction interval.

For "Current Bar", the interval is calculated based on the data of the previous bar close. Therefore changes in the current price will have little effect on the range. What current bar means is that the estimated range is for when this bar close. E.g., If the Timeframe on 4 hours and 1 hour has passed, the interval is for how much time this bar has left, in this case, 3 hours.

For "Future Bars", the interval is calculated based on the current close. Therefore the range will be very much affected by the change in the current price. If the current price moves up, the range will also move up, vice versa. Future Bars is estimating the range for the period at least one bar ahead.

There are also other source selections based on high low.

Time setting is used when "Future Bars" is chosen for the period. The value in time means how many bars ahead of the current bar the range is estimating. When time = 1, it means the interval is constructing for 1 bar head. E.g., If the timeframe is on 4 hours, then it's estimating the next 4 hours range no matter how much time has passed in the current bar.

Note: It's probably better to use "probability cone" for visual presentation when time > 1

Volatility Models :

Sample SD: traditional sample standard deviation, most commonly used, use (n-1) period to adjust the bias

Parkinson: Uses High/ Low to estimate volatility, assumes continuous no gap, zero mean no drift, 5 times more efficient than Close to Close

Garman Klass: Uses OHLC volatility, zero drift, no jumps, about 7 times more efficient

Yangzhang Garman Klass Extension: Added jump calculation in Garman Klass, has the same value as Garman Klass on markets with no gaps.

about 8 x efficient

Rogers: Uses OHLC, Assume non-zero mean volatility, handles drift, does not handle jump 8 x efficient

EWMA: Exponentially Weighted Volatility. Weight recently volatility more, more reactive volatility better in taking account of volatility autocorrelation and cluster.

YangZhang: Uses OHLC, combines Rogers and Garmand Klass, handles both drift and jump, 14 times efficient, alpha is the constant to weight rogers volatility to minimize variance.

Median absolute deviation: It's a more direct way of measuring volatility. It measures volatility without using Standard deviation. The MAD used here is adjusted to be an unbiased estimator.

Volatility Period is the sample size for variance estimation. A longer period makes the estimation range more stable less reactive to recent price. Distribution is more significant on a larger sample size. A short period makes the range more responsive to recent price. Might be better for high volatility clusters.

Standard deviations:

Standard Deviation One shows the estimated range where the closing price will be about 68% of the time.

Standard Deviation two shows the estimated range where the closing price will be about 95% of the time.

Standard Deviation three shows the estimated range where the closing price will be about 99.7% of the time.

Note: All these probabilities are based on the normal distribution assumption for returns. It's the estimated probability, not the actual probability.

Manually Entered Standard Deviation shows the range of any entered standard deviation. The probability of that range will be presented on the panel.

People usually assume the mean of returns to be zero. To be more accurate, we can consider the drift in price from calculating the geometric mean of returns. Drift happens in the long run, so short lookback periods are not recommended. Assuming zero mean is recommended when time is not greater than 1.

When we are estimating the future range for time > 1, we typically assume constant volatility and the returns to be independent and identically distributed. We scale the volatility in term of time to get future range. However, when there's autocorrelation in returns( when returns are not independent), the assumption fails to take account of this effect. Volatility scaled with autocorrelation is required when returns are not iid. We use an AR(1) model to scale the first-order autocorrelation to adjust the effect. Returns typically don't have significant autocorrelation. Adjustment for autocorrelation is not usually needed. A long length is recommended in Autocorrelation calculation.

Note: The significance of autocorrelation can be checked on an ACF indicator.

ACF

The multimeframe option enables people to use higher period expected move on the lower time frame. People should only use time frame higher than the current time frame for the input. An error warning will appear when input Tf is lower. The input format is multiplier * time unit. E.g. : 1D

Unit: M for months, W for Weeks, D for Days, integers with no unit for minutes (E.g. 240 = 240 minutes). S for Seconds.

Smoothing option is using a filter to smooth out the range. The filter used here is John Ehler's supersmoother. It's an advance smoothing technique that gets rid of aliasing noise. It affects is similar to a simple moving average with half the lookback length but smoother and has less lag.

Note: The range here after smooth no long represent the probability

Panel positions can be adjusted in the settings.

X position adjusts the horizontal position of the panel. Higher X moves panel to the right and lower X moves panel to the left.

Y position adjusts the vertical position of the panel. Higher Y moves panel up and lower Y moves panel down.

Step line display changes the style of the bands from line to step line. Step line is recommended because it gets rid of the directional bias of slope of expected move when displaying the bands.

Warnings:

People should not blindly trust the probability. They should be aware of the risk evolves by using the normal distribution assumption. The real return has skewness and high kurtosis. While skewness is not very significant, the high kurtosis should be noticed. The Real returns have much fatter tails than the normal distribution, which also makes the peak higher. This property makes the tail ranges such as range more than 2SD highly underestimate the actual range and the body such as 1 SD slightly overestimate the actual range. For ranges more than 2SD, people shouldn't trust them. They should beware of extreme events in the tails.

Different volatility models provide different properties if people are interested in the accuracy and the fit of expected move, they can try expected move occurrence indicator. (The result also demonstrate the previous point about the drawback of using normal distribution assumption).

Expected move Occurrence Test

The prediction interval is only for the closing price, not wicks. It only estimates the probability of the price closing at this level, not in between. E.g., If 1 SD range is 100 - 200, the price can go to 80 or 230 intrabar, but if the bar close within 100 - 200 in the end. It's still considered a 68% one standard deviation move.

ES-VIX Expected Move - Open basedES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Open + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily Open - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's open.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's open

Lower band (red) contracts from the current day's open

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Information table displaying:

Current ES price and VIX level

Daily Open

Expected move

AlphaRank MA Lens – Multi-Timeframe Moving Average MapAlphaRank MA Lens – Multi-Timeframe Moving Average Map

AlphaRank MA Lens is a clean, open-source moving-average overlay that turns price action into an easy-to-read trend map. It focuses on structure and context only — no signals, no backtest, no hype — just a clear view of where price sits relative to key moving averages.

The script plots the 10 / 20 / 50 / 100 / 150 / 200 / 730 moving averages with full color control and a single “MA Type” switch, so you can flip the whole stack between SMA and EMA in one click. Instead of loading multiple separate MA indicators, this puts the full trend stack in one tool.

An optional background highlight lets you choose a reference MA (for example the 200 MA) and softly shade the chart:

Green when price is above that MA

Red when price is below it

This makes trend regime changes easy to see at a glance.

How traders typically use it (education only):

10/20/50 MAs → short-term trend and momentum.

100/150/200/730 MAs → bigger structural trend and “where price lives” in the long-term range.

Many traders consider conditions healthier when price and the short MAs are stacked above the longer MAs, and weaker when price trades below them.

Follow my work: AlphaRank

This script is for educational and analytical purposes only and does not provide trading advice or performance promises. Always combine it with your own judgment, testing, and risk management.

Abu Basel IQOption 2m Signals//@version=5

indicator("Abu Basel IQOption 2m Signals", overlay = true, timeframe = "", timeframe_gaps = true)

//========================

// الإعدادات

//========================

emaFastLen = input.int(9, "EMA سريع (9)")

emaSlowLen = input.int(21, "EMA بطيء (21)")

rsiLen = input.int(14, "RSI Length", minval = 2)

rsiBuyLevel = input.float(50.0, "RSI حد الشراء (أعلى من)", minval = 0, maxval = 100)

rsiSellLevel= input.float(50.0, "RSI حد البيع (أقل من)", minval = 0, maxval = 100)

bbLen = input.int(20, "Bollinger Length")

bbMult = input.float(2.0, "Bollinger Deviation")

showSignals = input.bool(true, "إظهار الأسهم (CALL / PUT)")

showBg = input.bool(true, "تلوين الخلفية عند الإشارات")

//========================

// المؤشرات الأساسية

//========================

emaFast = ta.ema(close, emaFastLen)

emaSlow = ta.ema(close, emaSlowLen)

basis = ta.sma(close, bbLen)

dev = bbMult * ta.stdev(close, bbLen)

bbUpper = basis + dev

bbLower = basis - dev

rsi = ta.rsi(close, rsiLen)

// رسم المتوسطات والبولينجر

plot(emaFast, title = "EMA 9", linewidth = 2)

plot(emaSlow, title = "EMA 21", linewidth = 2)

plot(basis, title = "BB Basis", linewidth = 1)

plot(bbUpper, title = "BB Upper", linewidth = 1, style = plot.style_line)

plot(bbLower, title = "BB Lower", linewidth = 1, style = plot.style_line)

//========================

// دوال أشكال الشموع الانعكاسية

//========================

bodySize = math.abs(close - open)

fullRange = high - low

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

isSmallBody = bodySize <= fullRange * 0.3

// Hammer صاعدة (ذيل سفلي طويل)

bullHammer() =>

lowerWick > bodySize * 2 and upperWick <= bodySize and close > open

// Shooting Star هابطة (ذيل علوي طويل)

bearShootingStar() =>

upperWick > bodySize * 2 and lowerWick <= bodySize and close < open

// Bullish Engulfing

bullEngulfing() =>

close > open and close < open and close > open and open < close

// Bearish Engulfing

bearEngulfing() =>

close < open and close > open and close < open and open > close

// تجميع أنماط صعود/هبوط

bullPattern = bullHammer() or bullEngulfing()

bearPattern = bearShootingStar() or bearEngulfing()

//========================

// شروط الدخول

//========================

// تقاطع المتوسطات

bullCross = ta.crossover(emaFast, emaSlow) // صعود

bearCross = ta.crossunder(emaFast, emaSlow) // هبوط

// شروط شراء CALL:

// 1) تقاطع EMA9 فوق EMA21

// 2) السعر فوق خط وسط البولنجر

// 3) RSI أعلى من 50

// 4) شمعة انعكاسية صاعدة (Hammer أو Engulfing)

callCond = bullCross and close > basis and rsi > rsiBuyLevel and bullPattern

// شروط بيع PUT:

// 1) تقاطع EMA9 تحت EMA21

// 2) السعر تحت خط وسط البولنجر

// 3) RSI أقل من 50

// 4) شمعة انعكاسية هابطة (Shooting Star أو Bearish Engulfing)

putCond = bearCross and close < basis and rsi < rsiSellLevel and bearPattern

//========================

// رسم الإشارات على الشارت

//========================

plotshape(showSignals and callCond, title="CALL 2m",

style=shape.labelup, location=location.belowbar,

text="CALL\n2m", size=size.tiny)

plotshape(showSignals and putCond, title="PUT 2m",

style=shape.labeldown, location=location.abovebar,

text="PUT\n2m", size=size.tiny)

// تلوين الخلفية عند الإشارات

bgcolor(showBg and callCond ? color.new(color.green, 85) :

showBg and putCond ? color.new(color.red, 85) : na)

//========================

// شروط التنبيه (Alerts)

//========================

alertcondition(callCond, title="CALL 2m Signal",

message="Abu Basel Signal: CALL 2m on {{ticker}} at {{close}}")

alertcondition(putCond, title="PUT 2m Signal",

message="Abu Basel Signal: PUT 2m on {{ticker}} at {{close}}")

ADX Forecast Colorful [DiFlip]ADX Forecast Colorful

Introducing one of the most advanced ADX indicators available — a fully customizable analytical tool that integrates forward-looking forecasting capabilities. ADX Forecast Colorful is a scientific evolution of the classic ADX, designed to anticipate future trend strength using linear regression. Instead of merely reacting to historical data, this indicator projects the future behavior of the ADX, giving traders a strategic edge in trend analysis.

⯁ Real-Time ADX Forecasting

For the first time, a public ADX indicator incorporates linear regression (least squares method) to forecast the future behavior of ADX. This breakthrough approach enables traders to anticipate trend strength changes based on historical momentum. By applying linear regression to the ADX, the indicator plots a projected trendline n periods ahead — helping users make more accurate and timely trading decisions.

⯁ Highly Customizable

The indicator adapts seamlessly to any trading style. It offers a total of 26 long entry conditions and 26 short entry conditions, making it one of the most configurable ADX tools on TradingView. Each condition is fully adjustable, enabling the creation of statistical, quantitative, and automated strategies. You maintain full control over the signals to align perfectly with your system.

⯁ Innovative and Science-Based

This is the first public ADX indicator to apply least-squares predictive modeling to ADX dynamics. Technically, it embeds machine learning logic into a traditional trend-strength indicator. Using linear regression as a predictive engine adds powerful statistical rigor to the ADX, turning it into an intelligent, forward-looking signal generator.

⯁ Scientific Foundation: Linear Regression

Linear regression is a fundamental method in statistics and machine learning used to model the relationship between a dependent variable y and one or more independent variables x. The basic formula for simple linear regression is:

y = β₀ + β₁x + ε

Where:

y = predicted value (e.g., future ADX)

x = explanatory variable (e.g., bar index or time)

β₀ = intercept

β₁ = slope (rate of change)

ε = random error term

The goal is to estimate β₀ and β₁ by minimizing the sum of squared errors. This is achieved using the least squares method, ensuring the best linear fit to historical data. Once the coefficients are calculated, the model extends the regression line forward, generating the ADX projection based on recent trends.

⯁ Least Squares Estimation

To minimize the error, the regression coefficients are calculated as:

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

Σ = summation

x̄ and ȳ = means of x and y

i ranges from 1 to n (number of data points)

These formulas provide the best linear unbiased estimator under Gauss-Markov conditions — assuming constant variance and linearity.

⯁ Linear Regression in Machine Learning

Linear regression is a foundational algorithm in supervised learning. Its power in producing quantitative predictions makes it essential in AI systems, predictive analytics, time-series forecasting, and automated trading. Applying it to the ADX essentially places an intelligent forecasting engine inside a classic trend tool.

⯁ Visual Interpretation

Imagine an ADX time series like this:

Time →

ADX →

The regression line smooths these values and projects them n periods forward, creating a predictive trajectory. This forecasted ADX line can intersect with the actual ADX, offering smarter buy and sell signals.

⯁ Summary of Scientific Concepts

Linear Regression: Models variable relationships with a straight line.

Least Squares: Minimizes prediction errors for best fit.

Time-Series Forecasting: Predicts future values using historical data.

Supervised Learning: Trains models to predict outcomes from inputs.

Statistical Smoothing: Reduces noise and highlights underlying trends.

⯁ Why This Indicator Is Revolutionary

Scientifically grounded: Based on rigorous statistical theory.

Unprecedented: First public ADX using least-squares forecast modeling.

Smart: Uses machine learning logic.

Forward-Looking: Generates predictive, not just reactive, signals.

Customizable: Flexible for any strategy or timeframe.

⯁ Conclusion

By merging ADX and linear regression, this indicator enables traders to predict market momentum rather than merely follow it. ADX Forecast Colorful is not just another indicator — it’s a scientific leap forward in technical analysis. With 26 fully configurable entry conditions and smart forecasting, this open-source tool is built for creating cutting-edge quantitative strategies.

⯁ Example of simple linear regression with one independent variable

This example demonstrates how a basic linear regression works when there is only one independent variable influencing the dependent variable. This type of model is used to identify a direct relationship between two variables.

⯁ In linear regression, observations (red) are considered the result of random deviations (green) from an underlying relationship (blue) between a dependent variable (y) and an independent variable (x)

This concept illustrates that sampled data points rarely align perfectly with the true trend line. Instead, each observed point represents the combination of the true underlying relationship and a random error component.

⯁ Visualizing heteroscedasticity in a scatterplot with 100 random fitted values using Matlab

Heteroscedasticity occurs when the variance of the errors is not constant across the range of fitted values. This visualization highlights how the spread of data can change unpredictably, which is an important factor in evaluating the validity of regression models.

⯁ The datasets in Anscombe’s quartet were designed to have nearly the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but look very different when plotted

This classic example shows that summary statistics alone can be misleading. Even with identical numerical metrics, the datasets display completely different patterns, emphasizing the importance of visual inspection when interpreting a model.

⯁ Result of fitting a set of data points with a quadratic function

This example illustrates how a second-degree polynomial model can better fit certain datasets that do not follow a linear trend. The resulting curve reflects the true shape of the data more accurately than a straight line.

⯁ What is the ADX?

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ How to use the ADX?

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

Strong Trend: When the ADX is above 25, indicating a strong trend.

Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

Neutral Zone: Between 20 and 25, where the trend strength is unclear.

⯁ Entry Conditions

Each condition below is fully configurable and can be combined to build precise trading logic.

📈 BUY

🅰️ Signal Validity: The signal will remain valid for X bars .

🅰️ Signal Sequence: Configurable as AND or OR .

🅰️ +DI > -DI

🅰️ +DI < -DI

🅰️ +DI > ADX

🅰️ +DI < ADX

🅰️ -DI > ADX

🅰️ -DI < ADX

🅰️ ADX > Threshold

🅰️ ADX < Threshold

🅰️ +DI > Threshold

🅰️ +DI < Threshold

🅰️ -DI > Threshold

🅰️ -DI < Threshold

🅰️ +DI (Crossover) -DI

🅰️ +DI (Crossunder) -DI

🅰️ +DI (Crossover) ADX

🅰️ +DI (Crossunder) ADX

🅰️ +DI (Crossover) Threshold

🅰️ +DI (Crossunder) Threshold

🅰️ -DI (Crossover) ADX

🅰️ -DI (Crossunder) ADX

🅰️ -DI (Crossover) Threshold

🅰️ -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

📉 SELL

🅰️ Signal Validity: The signal will remain valid for X bars .

🅰️ Signal Sequence: Configurable as AND or OR .

🅰️ +DI > -DI

🅰️ +DI < -DI

🅰️ +DI > ADX

🅰️ +DI < ADX

🅰️ -DI > ADX

🅰️ -DI < ADX

🅰️ ADX > Threshold

🅰️ ADX < Threshold

🅰️ +DI > Threshold

🅰️ +DI < Threshold

🅰️ -DI > Threshold

🅰️ -DI < Threshold

🅰️ +DI (Crossover) -DI

🅰️ +DI (Crossunder) -DI

🅰️ +DI (Crossover) ADX

🅰️ +DI (Crossunder) ADX

🅰️ +DI (Crossover) Threshold

🅰️ +DI (Crossunder) Threshold

🅰️ -DI (Crossover) ADX

🅰️ -DI (Crossunder) ADX

🅰️ -DI (Crossover) Threshold

🅰️ -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

🤖 Automation

All BUY and SELL conditions are compatible with TradingView alerts, making them ideal for fully or semi-automated systems.

⯁ Unique Features

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

Superior-Range Bound Renko - Strategy - 11-29-25 - SignalLynxSuperior-Range Bound Renko Strategy with Advanced Risk Management Template

Signal Lynx | Free Scripts supporting Automation for the Night-Shift Nation 🌙

1. Overview

Welcome to Superior-Range Bound Renko (RBR) — a volatility-aware, structure-respecting swing-trading system built on top of a full Risk Management (RM) Template from Signal Lynx.

Instead of relying on static lookbacks (like “14-period RSI”) or plain MA crosses, Superior RBR:

Adapts its range definition to market volatility in real time

Emulates Renko Bricks on a standard, time-based chart (no Renko chart type required)

Uses a stack of Laguerre Filters to detect genuine impulse vs. noise

Adds an Adaptive SuperTrend powered by a small k-means-style clustering routine on volatility

Under the hood, this script also includes the full Signal Lynx Risk Management Engine:

A state machine that separates “Signal” from “Execution”

Layered exit tools: Stop Loss, Trailing Stop, Staged Take Profit, Advanced Adaptive Trailing Stop (AATS), and an RSI-style stop (RSIS)

Designed for non-repainting behavior on closed candles by basing execution-critical logic on previous-bar data

We are publishing this as an open-source template so traders and developers can leverage a professional-grade RM engine while integrating their own signal logic if they wish.

2. Quick Action Guide (TL;DR)

Best Timeframe:

4 Hours (H4) and above. This is a high-conviction swing-trading system, not a scalper.

Best Assets:

Volatile instruments that still respect market structure:

Bitcoin, Ethereum, Gold (XAUUSD), high-volatility Forex pairs (e.g., GBPJPY), indices with clean ranges.

Strategy Type:

Volatility-Adaptive Trend Following + Impulse Detection.

It hunts for genuine expansion out of ranges, not tiny mean-reversion nibbles.

Key Feature:

Renko Emulation on time-based candles.

We mathematically model Renko Bricks and overlay them on your standard chart to define:

“Equilibrium” zones (inside the brick structure)

“Breakout / impulse” zones (when price AND the impulse line depart from the bricks)

Repainting:

Designed to be non-repainting on closed candles.

All RM execution logic uses confirmed historical data (no future bars, no security() lookahead). Intrabar flicker during formation is allowed, but once a bar closes the engine’s decisions are stable.

Core Toggles & Filters:

Enable Longs and Shorts independently

Optional Weekend filter (block trades on Saturday/Sunday)

Per-module toggles: Stop Loss, Trailing Stop, Staged Take Profits, AATS, RSIS

3. Detailed Report: How It Works

A. The Strategy Logic: Superior RBR

Superior RBR builds its entry signal from multiple mathematical layers working together.

1) Adaptive Lookback (Volatility Normalization)

Instead of a fixed 100-bar or 200-bar range, the script:

Computes ATR-based volatility over a user-defined period.

Normalizes that volatility relative to its recent min/max.

Maps the normalized value into a dynamic lookback window between a minimum and maximum (e.g., 4 to 100 bars).

High Volatility:

The lookback shrinks, so the system reacts faster to explosive moves.

Low Volatility:

The lookback expands, so the system sees a “bigger picture” and filters out chop.

All the core “Range High/Low” and “Range Close High/Low” boundaries are built on top of this adaptive window.

2) Range Construction & Quick Ranges

The engine constructs several nested ranges:

Outer Range:

rangeHighFinal – dynamic highest high

rangeLowFinal – dynamic lowest low

Inner Close Range:

rangeCloseHighFinal – highest close

rangeCloseLowFinal – lowest close

Quick Ranges:

“Half-length” variants of those, used to detect more responsive changes in structure and volatility.

These ranges define:

The macro box price is trading inside

Shorter-term “pressure zones” where price is coiling before expansion

3) Renko Emulation (The Bricks)

Rather than using the Renko chart type (which discards time), this script emulates Renko behavior on your normal candles:

A “brick size” is defined either:

As a standard percentage move, or

As a volatility-driven (ATR) brick, optionally inhibited by a minimum standard size

The engine tracks a base value and derives:

brickUpper – top of the emulated brick

brickLower – bottom of the emulated brick

When price moves sufficiently beyond those levels, the brick “shifts”, and the directional memory (renkoDir) updates:

renkoDir = +2 when bricks are advancing upward

renkoDir = -2 when bricks are stepping downward

You can think of this as a synthetic Renko tape overlaid on time-based candles:

Inside the brick: equilibrium / consolidation

Breaking away from the brick: momentum / expansion

4) Impulse Tracking with Laguerre Filters

The script uses multiple Laguerre Filters to smooth price and brick-derived data without traditional lag.

Key filters include:

LagF_1 / LagF_W: Based on brick upper/lower baselines

LagF_Q: Based on HLCC4 (high + low + 2×close)/4

LagF_Y / LagF_P: Complex averages combining brick structures and range averages

LagF_V (Primary Impulse Line):

A smooth, high-level impulse line derived from a blend of the above plus the outer ranges

Conceptually:

When the impulse line pushes away from the brick structure and continues in one direction, an impulse move is underway.

When its direction flips and begins to roll over, the impulse is fading, hinting at mean reversion back into the range.

5) Fib-Based Structure & Swaps

The system also layers in Fib levels derived from the adaptive ranges:

Standard levels (12%, 23.6%, 38.2%, 50%, 61%, 76.8%, 88%) from the main range

A secondary “swap” set derived from close-range dynamics (fib12Swap, fib23Swap, etc.)

These Fibs are used to:

Bucket price into structural zones (below 12, between 23–38, etc.)

Detect breakouts when price and Laguerre move beyond key Fib thresholds

Drive zSwap logic (where a secondary Fib set becomes the active structure once certain conditions are met)

6) Adaptive SuperTrend with K-Means-Style Volatility Clustering

Under the hood, the script uses a small k-means-style clustering routine on ATR:

ATR is measured over a fixed period

The range of ATR values is split into Low, Medium, High volatility centroids

Current ATR is assigned to the nearest centroid (cluster)

From that, a SuperTrend variant (STK) is computed with dynamic sensitivity:

In quiet markets, SuperTrend can afford to be tighter

In wild markets, it widens appropriately to avoid constant whipsaw

This SuperTrend-based oscillator (LagF_K and its signals) is then combined with the brick and Laguerre stack to confirm valid trend regimes.

7) Final Baseline Signals (+2 / -2)

The “brain” of Superior RBR lives in the Baseline & Signal Generation block:

Two composite signals are built: B1 and B2:

They combine:

Fib breakouts

Renko direction (renkoDir)

Expansion direction (expansionQuickDir)

Multiple Laguerre alignments (LagF_Q, LagF_W, LagF_Y, LagF_Z, LagF_P, LagF_V)

They also factor in whether Fib structures are expanding or contracting.

A user toggle selects the “Baseline” signal:

finalSig = B2 (default) or B1 (alternate baseline)

finalSig is then filtered through the RM state machine and only when everything aligns, we emit:

+2 = Long / Buy signal

-2 = Short / Sell signal

0 = No new trade

Those +2 / -2 values are what feed the Risk Management Engine.

B. The Risk Management (RM) Engine

This script features the Signal Lynx Risk Management Engine, a proprietary state machine built to separate Signal from Execution.

Instead of firing orders directly on indicator conditions, we:

Convert the raw signal into a clean integer (Fin = +2 / -2 / 0)

Feed it into a Trade State Machine that understands:

Are we flat?

Are we in a long or short?

Are we in a closing sequence?

Should we permit re-entry now or wait?

Logic Injection / Template Concept:

The RM engine expects a simple integer:

+2 → Buy

-2 → Sell

Everything else (0) is “no new trade”

This makes the script a template:

You can remove the Superior RBR block

Drop in your own logic (RSI, MACD, price action, etc.)

As long as you output +2 or -2 into the same signal channel, the RM engine can drive all exits and state transitions.

Aggressive vs Conservative Modes:

The input AgressiveRM (Aggressive RM) governs how we interpret signals:

Conservative Mode (Aggressive RM = false):

Uses a more filtered internal signal (AF) to open trades

Effectively waits for a clean trend flip / confirmation before new entries

Minimizes whipsaw at the cost of fewer trades

Aggressive Mode (Aggressive RM = true):

Reacts directly to the fresh alert (AO) pulses

Allows faster re-entries in the same direction after RM-based exits

Still respects your pyramiding setting; this script ships with pyramiding = 0 by default, so it will not stack multiple positions unless you change that parameter in the strategy() call.

The state machine enforces discipline on top of your signal logic, reducing double-fires and signal spam.

C. Advanced Exit Protocols (Layered Defense)

The exit side is where this template really shines. Instead of a single “take profit or stop loss,” it uses multiple, cooperating layers.

1) Hard Stop Loss

A classic percentage-based Stop Loss (SL) relative to the entry price.

Acts as a final “catastrophic protection” layer for unexpected moves.

2) Standard Trailing Stop

A percentage-based Trailing Stop (TS) that:

Activates only after price has moved a certain percentage in your favor (tsActivation)

Then trails price by a configurable percentage (ts)

This is a straightforward, battle-tested trailing mechanism.

3) Staged Take Profits (Three Levels)

The script supports three staged Take Profit levels (TP1, TP2, TP3):

Each stage has:

Activation percentage (how far price must move in your favor)

Trailing amount for that stage

Position percentage to close

Example setup:

TP1:

Activate at +10%

Trailing 5%

Close 10% of the position

TP2:

Activate at +20%

Trailing 10%

Close another 10%

TP3:

Activate at +30%

Trailing 5%

Close the remaining 80% (“runner”)

You can tailor these quantities for partial scaling out vs. letting a core position ride.

4) Advanced Adaptive Trailing Stop (AATS)

AATS is a sophisticated volatility- and structure-aware stop:

Uses Hirashima Sugita style levels (HSRS) to model “floors” and “ceilings” of price:

Dungeon → Lower floors → Mid → Upper floors → Penthouse

These levels classify where current price sits within a long-term distribution.

Combines HSRS with Bollinger-style envelopes and EMAs to determine:

Is price extended far into the upper structure?

Is it compressed near the lower ranges?

From this, it computes an adaptive factor that controls how tight or loose the trailing level (aATS / bATS) should be:

High Volatility / Penthouse areas:

Stop loosens to avoid getting wicked out by inevitable spikes.

Low Volatility / compressed structure:

Stop tightens to lock in and protect profit.

AATS is designed to be the “smart last line” that responds to context instead of a single fixed percentage.

5) RSI-Style Stop (RSIS)

On top of AATS, the script includes a RSI-like regime filter:

A McGinley Dynamic mean of price plus ATR bands creates a dynamic channel.

Crosses above the top band and below the lower band change a directional state.

When enabled (UseRSIS):

RSIS can confirm or veto AATS closes:

For longs: A shift to bearish RSIS can force exits sooner.

For shorts: A shift to bullish RSIS can do the same.

This extra layer helps avoid over-reactive stops in strong trends while still respecting a regime change when it happens.

D. Repainting Protection

Many strategies look incredible in the Strategy Tester but fail in live trading because they rely on intrabar values or future-knowledge functions.

This template is built with closed-candle realism in mind:

The Risk Management logic explicitly uses previous bar data (open , high , low , close ) for the key decisions on:

Trailing stop updates

TP triggers

SL hits

RM state transitions

No security() lookahead or future-bar access is used.

This means:

Backtest behavior is designed to match what you can actually get with TradingView alerts and live automation.

Signals may “flicker” intrabar while the candle is forming (as with any strategy), but on closed candles, the RM decisions are stable and non-repainting.

4. For Developers & Modders

We strongly encourage you to mod this script.

To plug your own strategy into the RM engine:

Look for the section titled:

// BASELINE & SIGNAL GENERATION

You will see composite logic building B1 and B2, and then selecting:

baseSig = B2

altSig = B1

finalSig = sigSwap ? baseSig : altSig

You can replace the content used to generate baseSig / altSig with your own logic, for example:

RSI crosses

MACD histogram flips

Candle pattern detectors

External condition flags

Requirements are simple:

Your final logic must output:

2 → Buy signal

-2 → Sell signal

0 → No new trade

That output flows into the RM engine via finalSig → AlertOpen → state machine → Fin.

Once you wire your signals into finalSig, the entire Risk Management system (Stops, TPs, AATS, RSIS, re-entry logic, weekend filters, long/short toggles) becomes available for your custom strategy without re-inventing the wheel.

This makes Superior RBR not just a strategy, but a reference architecture for serious Pine dev work.

5. About Signal Lynx

Automation for the Night-Shift Nation 🌙

Signal Lynx focuses on helping traders and developers bridge the gap between indicator logic and real-world automation. The same RM engine you see here powers multiple internal systems and templates, including other public scripts like the Super-AO Strategy with Advanced Risk Management.

We provide this code open source under the Mozilla Public License 2.0 (MPL-2.0) to:

Demonstrate how Adaptive Logic and structured Risk Management can outperform static, one-layer indicators

Give Pine Script users a battle-tested RM backbone they can reuse, remix, and extend

If you are looking to automate your TradingView strategies, route signals to exchanges, or simply want safer, smarter strategy structures, please keep Signal Lynx in your search.

License: Mozilla Public License 2.0 (Open Source).

If you make beneficial modifications, please consider releasing them back to the community so everyone can benefit.

Single AHR DCA (HM) — AHR Pane (customized quantile)Customized note

The log-regression window LR length controls how long a long-term fair value path is estimated from historical data.