2022 Model ICT Entry Strategy [TradingFinder] One Setup For Life🔵 Introduction

The ICT 2022 model, introduced by Michael Huddleston, is an advanced trading strategy rooted in liquidity and price imbalance, where time and price serve as the core elements. This ICT 2022 trading strategy is an algorithmic approach designed to analyze liquidity and imbalances in the market. It incorporates concepts such as Fair Value Gap (FVG), Liquidity Sweep, and Market Structure Shift (MSS) to help traders identify liquidity movements and structural changes in the market, enabling them to determine optimal entry and exit points for their trades.

This Full ICT Day Trading Model empowers traders to pinpoint the Previous Day High/Low as well as the highs and lows of critical sessions like the London and New York sessions. These levels act as Liquidity Zones, which are frequently swept prior to a market structure shift (MSS) or a retracement to areas such as Optimal Trade Entry (OTE).

Bullish :

Bearish :

🔵 How to Use

The ICT 2022 model is a sophisticated trading strategy that focuses on identifying key liquidity levels and price movements. It operates based on two main principles. In the first phase, the price approaches liquidity zones and sweeps critical levels such as the previous day’s high or low and key session levels.

This movement is known as a Liquidity Sweep. In the second phase, following the sweep, the price retraces to areas like the FVG (Fair Value Gap), creating ideal entry points for trades. Below is a detailed explanation of how to apply this strategy in bullish and bearish setups.

🟣 Bullish ICT 2022 Model Setup

To use the ICT 2022 model in a bullish setup, start by identifying the Previous Day High/Low or key session levels, such as those of the London or New York sessions. In a bullish setup, the price usually moves downward first, sweeping the Liquidity Low. This move, known as a Liquidity Sweep, reflects the collection of buy orders by major market participants.

After the liquidity sweep, the price should shift market structure and start moving upward; this shift, referred to as Market Structure Shift (MSS), signals the beginning of an upward trend. Following MSS, areas like FVG, located within the Discount Zone, are identified. At this stage, the trader waits for the price to retrace to these zones. Once the price returns, a long trade is executed.

Finally, the stop-loss should be set below the liquidity low to manage risk, while the take-profit target is usually placed above the previous day’s high or other identified liquidity levels. This structure enables traders to take advantage of the upward price movement after the liquidity sweep.

🟣 Bearish ICT 2022 Model Setup

To identify a bearish setup in the ICT 2022 model, begin by marking the Previous Day High/Low or key session levels, such as the London or New York sessions. In this scenario, the price typically moves upward first, sweeping the Liquidity High. This move, known as a Liquidity Sweep, signifies the collection of sell orders by key market players.

After the liquidity sweep, the price should shift market structure downward. This movement, called the Market Structure Shift (MSS), indicates the start of a downtrend. Following MSS, areas such as FVG, found within the Premium Zone, are identified. At this stage, the trader waits for the price to retrace to these areas. Once the price revisits these zones, a short trade is executed.

In this setup, the stop-loss should be placed above the liquidity high to control risk, while the take-profit target is typically set below the previous day’s low or another defined liquidity level. This approach allows traders to capitalize on the downward price movement following the liquidity sweep.

🔵 Settings

Swing period : You can set the swing detection period.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

FVG Length : Default is 120 Bar.

MSS Length : Default is 80 Bar.

FVG Filter : This refines the number of identified FVG areas based on a specified algorithm to focus on higher quality signals and reduce noise.

Types of FVG filters :

Very Aggressive Filter: Adds a condition where, for an upward FVG, the last candle's highest price must exceed the middle candle's highest price, and for a downward FVG, the last candle's lowest price must be lower than the middle candle's lowest price. This minimally filters out FVGs.

Aggressive Filter: Builds on the Very Aggressive mode by ensuring the middle candle is not too small, filtering out more FVGs.

Defensive Filter: Adds criteria regarding the size and structure of the middle candle, requiring it to have a substantial body and specific polarity conditions, filtering out a significant number of FVGs.

Very Defensive Filter: Further refines filtering by ensuring the first and third candles are not small-bodied doji candles, retaining only the highest quality signals.

🔵 Conclusion

The ICT 2022 model is a comprehensive and advanced trading strategy designed around key concepts such as liquidity, price imbalance, and market structure shifts (MSS). By focusing on the sweep of critical levels such as the previous day’s high/low and important trading sessions like London and New York, this strategy enables traders to predict market movements with greater precision.

The use of tools like FVG in this model helps traders fine-tune their entry and exit points and take advantage of bullish and bearish trends after liquidity sweeps. Moreover, combining this strategy with precise timing during key trading sessions allows traders to minimize risk and maximize returns.

In conclusion, the ICT 2022 model emphasizes the importance of time and liquidity, making it a powerful tool for both professional and novice traders. By applying the principles of this model, you can make more informed trading decisions and seize opportunities in financial markets more effectively.

Cerca negli script per "2022年+美股英伟达+交易税费+计算方法"

Monthly Options Expiration 2022Monthly options expiration for the year 2022.

Also you can set a flag X no. of days before the expiration date. I use it at as marker to take off existing positions in expiration week or roll to next expiration date or to place new trades.

Happy new year 2022 in advance and all the best traders.

MACD-V (Volatility-Normalised Momentum) — Spiroglou, 2022Volatility-normalized MACD per Alex Spiroglou (2022):

MACD-V = (EMA12 − EMA26) / ATR26 × 100, so momentum is expressed in ATR units and stays comparable across assets/timeframes.

What you get

• Trend-colored line: green when price ≥ EMA200, red otherwise.

• Guides: ±50 / ±100 / 0; Extremes: ±140 (editable).

• Regime shading: OB ≥ +140 shaded red; OS ≤ −140 shaded green.

• Clean, on-curve markers: small circles on the MACD-V line at the four edge events — OB (enter ≥ +threshold), OBX (cross back down), OS (enter ≤ −threshold), OSX (cross back up).

• Text labels are off by default; optional toggle only for OB/OBX.

• Signal & histogram: EMA(9) of MACD-V and (MACD-V − Signal) columns.

• Alerts: OB/OS entries & exits included.

How to use

• Favor longs when MACD-V > 0 (ideally > +50); respect OB for possible exhaustion.

• Favor shorts when MACD-V < 0 (ideally < −50); respect OS for possible exhaustion.

• Because it’s ATR-normalized, thresholds transfer well across symbols and timeframes.

ICT NY Futures Indices Session Model - YT New York MentorshipThis indicator plots out the time periods and open lines as outlined in ICT's 2022 Mentorship and is designed specifically for the New York futures trading session.

Time zone is set to GMT-4 (NY) by default but can be changed for accommodate daylight saving in the menu.

Please note this indicator is to be used only on the 30min timeframe and below.

Here are its features:

The background color shows the morning session, in two parts (8.30am to 9.30am and 9.30am to 11.30am), then a two hour gap for lunch (ICT calls this "Dead time") and finally, the afternoon session, also to two (1.30pm to 3pm and 3pm to 4pm).

It not only shows the current killzones, but future zones as well.

These times are important; trades can be framed within these zones as taught in the mentorship.

Next are the open lines. These lines are automatically plotted and can be areas for price to react off of; they are the opening price of a candle at these times:

00.00 (New York Midnight, also known as "True Day Open")

8.30am (New York Equities pre-open)

9.30am (New York Equities open)

2.00am (London Stock Exchange open)

And lastly, London's trading session High and Low are projected forward onto the New York trading session.

These two price points are areas of liquidity that were pooled during London, but they can also often set the high or low of the day.

Please let me know if there are any bugs or if you have suggestions for the next update.

[2022] MACD Cross Strategy (version 1)Early workings of a macd crossover. User inputs, strategy parameters, use on forex, crypto, stocks, etc,..

On Balance Volume Trend© 2022, CryptoNaut1000

An extension to "On Balance Volume Momentum (OBV Momentum)".

"OBV Trend" is a trend strength indicator, that can be used to identify strong trends and also trend changes based on volume.

High positive values indicate strong volume on the buy side, high negative values indicate strong volume on the sell side.

An increasing OBV trend indicates a strengthening buy trend or a weakening sell trend,

decreasing OBV trend indicates a strengthening sell trend or weakening buy trend.

OBV trend is calculated by plotting a short vs. a long moving average and filling the difference in volume.

OBV trend metric is absolute volume.

[2022]Volume Flow v3 with alertsIndicators are an essential part of technical analysis of cryptocurrency. Their main function is to predict market direction based on historic price, cryptocurrency volume and other information. There are several types of crypto indicators illustrating various parameters (trend, volatility, volume, momentum, etc.) but in this article we will look at volume indicators.

Volume indicators demonstrate changing of trading volume over time. This information is very useful as crypto trading volume displays how strong the current trend is. For example, if the price goes up and the volume is high then the trend is strong and will more likely last longer. There are various volume indicators, but we’ll talk about the most popular ones, such as:

On Balance Volume

Accumulation/Distribution Line

Money Flow Index

Chaikin Oscillator

Chaikin Money Flow

Ease of Movement

Financial Astrology Crypto ML Daily TrendThis daily trend indicator is based on financial astrology cycles detected with advanced machine learning techniques for the crypto-currencies research portfolio: ADA, BAT, BNB, BTC, DASH, EOS, ETC, ETH, LINK, LTC, XLM, XMR, XRP, ZEC and ZRX. The daily price trend is forecasted through this planets cycles (angular aspects, speed, declination), fast ones are based on Moon, Mercury, Venus and Sun and Mid term cycles are based on Mars, Vesta and Ceres. The combination of all this cycles produce a daily price trend prediction that is encoded into a PineScript array using binary format "0 or 1" that represent sell and buy signals respectively. The indicator provides signals since 2021-01-01 to 2022-12-31, the past months signals purpose is to support backtesting of the indicator combined with other technical indicator entries like MAs, RSI or Stochastic. For future predictions besides 2022 a machine learning models re-train phase will be required.

The resolution of this indicator is 1D, you can tune a parameter where you can determine how many future bars of daily trend are plotted and adjust an hours shift to anticipate future signals into current bar in order to produce a leading indicator effect to anticipate the trend changes with some hours of anticipation. Combined with technical analysis indicators this daily trend is very powerful because can help to produce approximately 60% of profitable signals based on the backtesting results. You can look at our open source Github repositories to validate accuracy using the backtesting strategies we have implemented in Jesse Crypto Trading Framework as proof of concept of the predictive potential of this indicator. Alternatively, we have implemented a PineScript strategy that use this indicator, just consider that we are pending to do signals update to the period July 2021 to December 2022: This strategy have accumulated more than 110 likes and many traders have validated the predictive power of Financial Astrology.

DISCLAIMER: This indicator is experimental and don’t provide financial or investment advice, the main purpose is to demonstrate the predictive power of financial astrology. Any allocation of funds following the documented machine learning model prediction is a high-risk endeavour and it’s the users responsibility to practice healthy risk management according to your situation.

Noa: Z-distance from VWAP with Kalman Smoother

Title: Noa: Z-distance from VWAP with Kalman Smoother

Description:

The "Z-distance from VWAP with Kalman Smoother" is a tool constructed on the premise that price evolves in distinct stages: normal or extreme trends (upward or downward) and transitional periods, termed as 'flips'. The Volume Weighted Average Price (VWAP) serves as a benchmark, representing the market's expectation of a fair value over a given time frame. However, since each stock trades on its unique price scale, direct comparisons are not feasible. This script introduces a standardized method, using the Z-score from the VWAP, to understand and compare these relationships across diverse scales.

Core Principles:

Stages of Price Movement:

- Prices don't move purely randomly; while they contain a random element, they oscillate in discernible patterns or stages—either maintaining a trend (normal or extreme) or undergoing transition (flip).

- VWAP as Fair Value: VWAP offers a dynamic representation of what the market perceives as fair value for a stock over a specific period.

- Standardizing Price Relations: Given the varied scales at which different stocks trade, a model was imperative to standardize these relations. The Z-score from the VWAP fulfills this role, offering a normalized measure of how far the price deviates from its perceived fair value.

Features:

Z-score Levels:

The indicator demarcates various stages of price movements, offering clarity on potential overbought or oversold conditions.

- Extreme Up Trend: Indicated when the Z-score surpasses the upper limit.

- Normal Up Trend: Represented when the Z-score lies between the flip upper and the upper limit.

- Transition (Flip): Recognized when the Z-score oscillates within the flip range.

- Normal Down Trend: Denoted when the Z-score is between the flip lower and the lower limit.

- Extreme Down Trend: Marked when the Z-score falls below the lower limit.

Visual Aids:

- Color-coded regions between specific Z-score levels and the Z-score plot itself elucidate the current market state.

- Kalman Filter: By incorporating a Kalman filter, the indicator offers a less noisy and smoother representation of the Z-score, enhancing its interpretability.

Usage:

Trend Analysis:

- The Z-score states and the color-coded plot facilitate a nuanced understanding of the prevailing market trend.

- Potential Reversal Points: Extremely positive or negative Z-scores might hint at impending reversals.

- Buy/Sell Signals: Z-score's interactions with the flip level can be interpreted as potential trading signals.

Example (for illustration purposes only):

AAPL since April 2022: The stock exited from a normal uptrend and transitioned potentially towards a downtrend. By the end of April, AAPL flipped twice before transitioning to a normal downtrend. By early May, the stock moved into an aggressive downtrend. Market buyers were able to counter this downtrend by June, but selling pressure persisted, pushing the stock back into an aggressive downtrend. By the end of June, buyers halted the aggressive selling and transitioned the stock from an aggressive to normal downtrend, then to a flip, and finally to a normal uptrend by the end of August. AAPL briefly peaked into an aggressive uptrend before being pressured back to a normal downtrend. The rest of 2022 saw AAPL attempting several short-lived uptrend flips. However, 2023 brought a change, with AAPL flipping into a normal uptrend by the end of January, maintaining it until August of that year.

Credits:

This script, inspired by Z distance from VWAP by LazyBear and Kalman Smoother by alexgrover, was revamped and enriched by nord-ouestadvisors to embed these core principles and heighten its usability. A special acknowledgment to ChatGPT by OpenAI for the guidance.

Smoothed Heikin Ashi Trend on Chart - TraderHalai BACKTESTSmoothed Heikin Ashi Trend on chart - Backtest

This is a backtest of the Smoothed Heikin Ashi Trend indicator, which computes the reverse candle close price required to flip a Heikin Ashi trend from red to green and vice versa. The original indicator can be found in the scripts section of my profile.

This particular back test uses this indicator with a Trend following paradigm with a percentage-based stop loss.

Note, that backtesting performance is not always indicative of future performance, but it does provide some basis for further development and walk-forward / live testing.

Testing was performed on Bitcoin , as this is a primary target market for me to use this kind of strategy.

Sample Backtesting results as of 10th June 2022:

Backtesting parameters:

Position size: 10% of equity

Long stop: 1% below entry

Short stop: 1% above entry

Repainting: Off

Smoothing: SMA

Period: 10

8 Hour:

Number of Trades: 1046

Gross Return: 249.27 %

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 28.01 %

Profit Factor (Expectancy): 2.019

Average Loss: 0.33 %

Average Win: 1.69 %

Average Time for Loss: 1 day

Average Time for Win: 5.33 days

1 Day:

Number of Trades: 429

Gross Return: 458.4 %

CAGR Return: 15.76 %

Max Drawdown: 6.37 %

Profit Factor (Expectancy): 2.804

Average Loss: 0.8 %

Average Win: 7.2 %

Average Time for Loss: 3 days

Average Time for Win: 16 days

5 Day:

Number of Trades: 69

Gross Return: 1614.9 %

CAGR Return: 26.7 %

Max Drawdown: 5.7 %

Profit Factor (Expectancy): 10.451

Average Loss: 3.64 %

Average Win: 81.17 %

Average Time for Loss: 15 days

Average Time for Win: 85 days

Analysis:

The strategy is typical amongst trend following strategies with a less regular win rate, but where profits are more significant than losses. Most of the losses are in sideways, low volatility markets. This strategy performs better on higher timeframes, where it shows a positive expectancy of the strategy.

The average win was positively impacted by Bitcoin’s earlier smaller market cap, as the percentage wins earlier were higher.

Overall the strategy shows potential for further development and may be suitable for walk-forward testing and out of sample analysis to be considered for a demo trading account.

Note in an actual trading setup, you may wish to use this with volatility filters, combined with support resistance zones for a better setup.

As always, this post/indicator/strategy is not financial advice, and please do your due diligence before trading this live.

Original indicator links:

On chart version -

Oscillator version -

Update - 27/06/2022

Unfortunately, It appears that the original script had been taken down due to auto-moderation because of concerns with no slippage / commission. I have since adjusted the backtest, and re-uploaded to include the following to address these concerns, and show that I am genuinely trying to give back to the community and not mislead anyone:

1) Include commission of 0.1% - to match Binance's maker fees prior to moving to a fee-less model.

2) Include slippage of 10 ticks (This is a realistic slippage figure from searching online for most crypto exchanges)

3) Adjust account balance to 10,000 - since most of us are not millionaires.

The rest of the backtesting parameters are comparable to previous results:

Backtesting parameters:

Initial capital: 10000 dollars

Position size: 10% of equity

Long stop: 2% below entry

Short stop: 2% above entry

Repainting: Off

Smoothing: SMA

Period: 10

Slippage: 10 ticks

Commission: 0.1%

This script still remains to shows viability / profitablity on higher term timeframes (with slightly higher drawdown), and I have included the backtest report below to document my findings:

8 Hour:

Number of Trades: 1082

Gross Return: 233.02%

CAGR Return: 14.04 %

Max Drawdown: 7.9 %

Win percentage: 25.6%

Profit Factor (Expectancy): 1.627

Average Loss: 0.46 %

Average Win: 2.18 %

Average Time for Loss: 1.33 day

Average Time for Win: 7.33 days

Once again, please do your own research and due dillegence before trading this live. This post is for education and information purposes only, and should not be taken as financial advice.

Price Correction to fix data manipulation and mispricingPrice Correction corrects for index and security mispricing to the extent possible in TradingView on both daily and intraday charts. Price correction addresses mispricing issues for specific securities with known issues, or the user can build daily candles from intraday data instead of relying on exchange reported daily OHLC prices, which can include both legitimate special auction and off-exchange trades or illegitimate mispricing. The user can also detect daily OHLC prices that don’t reflect the intraday price action within a specified percent deviation. Price Correction functions as normal candles or bars for any time frame when correction is not needed.

On the 4th of October 2022, the AMEX exchange, owned by the New York Stock Exchange, decided to misprice the daily OHLC data for the SPY, the world’s largest ETF fund. The exchange eliminated the overnight gap that should have occurred in the daily chart that represents regular trading hours by showing a wick connecting near the close of the previous day. Neither the SPX, the SP500 cash index that the SPY ETF tracks, nor other SPX ETFs such as VOO or IVV show such a wick because significant price action at that level never occurred. The intraday SPY chart never shows the price drop below 372.31 that day, but there is a wick that extends to 366.57. On the 6th of October, they continued this practice of using a wick that connects with the close of the previous day to eliminate gaps in daily price action. The objective of this indicator is to fix such inconsistent mispricing practices in the SPY, NYA, and other indices or securities.

Price Correction corrects for the daily mispricing in the SPY to agree with the price action that actually occurred in the SPX index it tracks, as well as the other SPX ETFs, by using intraday data. The chart below compares the Price Correction of the SPY (top) to the SPX (middle) and the original mispriced SPY (bottom) with incorrect wicks. Price correction (top) removes those incorrect wicks (bottom) to match the SPX (middle).

The daily mispricing of the SPY follows after the successful deployment of the NYSE Composite Index mispricing, NYA, an index that represents all common stocks within the New York Stock Exchange, the largest exchange in the world. The importance of the NYA should not be understated. It is the price counterpart to NYSE’s market internals or statistics. Beginning in 2021, the New York Stock Exchange eliminated gaps in daily OHLC data for the NYA by using the close of the previous day as the open for the following day, in violation of their own NYSE Index Series Methodology. The Methodology states for the opening price that “The first index level is calculated and published around 09:30 ET, when the U.S. equity markets open for their regular trading session. The calculation of that level utilizes the most updated prices available at that moment.” You can verify for yourself that this is simply not the case. The first update of the NYA price for each day matches the close of the previous day, not the “most updated prices available at that moment”, causing data providers to often represent the first intraday bar with a huge sudden price change when an overnight price change occurred instead. For example, on 13 Jun 2022, TradingView shows a one-minute bar drop 2.3%. With a market capitalization of roughly 23 trillion dollars, the NYSE composite capitalization did not suddenly drop a half-trillion dollars in just one minute as the intraday chart data would have you believe. All major US indices, index ETFs, and even foreign indices like the Toronto TAX, the Australian ASXAL, the Bombay SENSEX, and German DAX had down gaps that day, except for the mispriced NYSE index. Price Correction corrects for this mispricing in daily OHLC data, as shown in the main chart at the top of this page comparing the original NYA (top) to the Price Corrected NYA (bottom).

Price Correction also corrects for the intraday mispricing in the NYA. The chart below shows how the Price Correction (top) replaces the incorrect first one-minute candles with gaps (bottom) from 22 Sep 2022 to 29 Sep 2022. TradingView is inconsistent in how intraday data is reported for overnight gaps by sometimes connecting the first intraday bar of the day to the close of the previous day, and other times not. This inconsistency may be due to manually changing the intraday data based on user support tickets. For example, after reporting the lack of a major gap in the NYA daily OHLC prices that existed intraday for 13 Jun 2022, TradingView opted to remove the true gap in intraday prices by creating a 2.3% half-a-trillion-dollar one-minute bar that connected the close of the previous day to show a sudden drop in price that didn’t occur, instead of adding the gap in the daily OHLC data that actually took place from overnight price action.

Price Correction allows users to detect daily OHLC data that does not reflect the intraday price action within a certain percent difference by changing the color of those candles or bars that deviate. The chart below clearly shows the start of the NYSE disinformation campaign for NYA that started in 2021 by painting blue those candles with daily OHLC values that deviated from the intraday values by 0.1%. Before 2021, the number of deviating candles is relatively sparse, but beginning in 2021, the chart is littered with deviating candles.

If there are other index or security mispricing or data issues you are aware of that can be incorporated into Price Correction, please let me know. Accurate financial data is indispensable in making accurate financial decisions. Assert your right to accurate financial data by reporting incorrect data and mispricing issues.

How to use the Price Correction

Simply add this “indicator” to your chart and remove the mispriced default candles or bars by right clicking on the chart, selecting Settings, and de-selecting Body, Wick, and Border under the Symbol tab. The Presets settings automatically takes care of mispricing in the NYA and SPY to the extent possible in TradingView. The user can also build their own daily candles based off of intraday data to address other securities that may have mispricing issues.

Williams Vix Fix ultra complete indicator (Tartigradia)Williams VixFix is a realized volatility indicator developed by Larry Williams, and can help in finding market bottoms.

Indeed, as Williams describe in his paper, markets tend to find the lowest prices during times of highest volatility, which usually accompany times of highest fear. The VixFix is calculated as how much the current low price statistically deviates from the maximum within a given look-back period.

Although the VixFix originally only indicates market bottoms, its inverse may indicate market tops. As masa_crypto writes : "The inverse can be formulated by considering "how much the current high value statistically deviates from the minimum within a given look-back period." This transformation equates Vix_Fix_inverse. This indicator can be used for finding market tops, and therefore, is a good signal for a timing for taking a short position." However, in practice, the Inverse VixFix is much less reliable than the classical VixFix, but is nevertheless a good addition to get some additional context.

For more information on the Vix Fix, which is a strategy published under public domain:

* The VIX Fix, Larry Williams, Active Trader magazine, December 2007, web.archive.org

* Fixing the VIX: An Indicator to Beat Fear, Amber Hestla-Barnhart, Journal of Technical Analysis, March 13, 2015, ssrn.com

* Replicating the CBOE VIX using a synthetic volatility index trading algorithm, Dayne Cary and Gary van Vuuren, Cogent Economics & Finance, Volume 7, 2019, Issue 1, doi.org

Created By ChrisMoody on 12-26-2014...

V3 MAJOR Update on 1-05-2014

tista merged LazyBear's Black Dots filter in 2020:

Extended by Tartigradia in 10-2022:

* Can select a symbol different from current to calculate vixfix, allows to select SP:SPX to mimic the original VIX index.

* Inverse VixFix (from masa_crypto and web.archive.org)

* VixFix OHLC Bars plot

* Price / VixFix Candles plot (Pro Tip: draw trend lines to find good entry/exit points)

* Add ADX filtering, Minimaxis signals, Minimaxis filtering (from samgozman )

* Convert to pinescript v5

* Allow timeframe selection (MTF)

* Skip off days (more accurate reproduction of original VIX)

* Reorganized, cleaned up code, commented out parts, commented out or removed unused code (eg, some of the KC calculations)

* Changed default Bollinger Band settings to reduce false positives in crypto markets.

Set Index symbol to SPX, and index_current = false, and timeframe Weekly, to reproduce the original VIX as close as possible by the VIXFIX (use the Add Symbol option, because you want to plot CBOE:VIX on the same timeframe as the current chart, which may include extended session / weekends). With the Weekly timeframe, off days / extended session days should not change much, but with lower timeframes this is important, because nights and weekends can change how the graph appears and seemingly make them different because of timing misalignment when in reality they are not when properly aligned.

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

S&P 500 Quandl Data & RatiosTradingView has a little-known integration that allows you to pull in 3rd party data-sets from Nasdaq Data Link, also known as Quandl. Today, I am open-sourcing for the community an indicator that uses the Quandl integration to pull in historical data and ratios on the S&P500. I originally coded this to study macro P/E ratios during peaks and troughs of boom/bust cycles.

The indicator pulls in each of the following datasets, as defined and provided by Quandl. The user can select which datasets to pull in using the indicator settings:

Dividend Yield : S&P 500 dividend yield (12 month dividend per share)/price. Yields following June 2022 (including the current yield) are estimated based on 12 month dividends through June 2022, as reported by S&P. Sources: Standard & Poor's for current S&P 500 Dividend Yield. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Dividend Yields.

Price Earning Ratio : Price to earnings ratio, based on trailing twelve month as reported earnings. Current PE is estimated from latest reported earnings and current market price. Source: Robert Shiller and his book Irrational Exuberance for historic S&P 500 PE Ratio.

CAPE/Shiller PE Ratio : Shiller PE ratio for the S&P 500. Price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio (CAPE Ratio), Shiller PE Ratio, or PE 10 FAQ. Data courtesy of Robert Shiller from his book, Irrational Exuberance.

Earnings Yield : S&P 500 Earnings Yield. Earnings Yield = trailing 12 month earnings divided by index price (or inverse PE) Yields following March, 2022 (including current yield) are estimated based on 12 month earnings through March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Book Ratio : S&P 500 price to book value ratio. Current price to book ratio is estimated based on current market price and S&P 500 book value as of March, 2022 the latest reported by S&P. Source: Standard & Poor's

Price Sales Ratio : S&P 500 Price to Sales Ratio (P/S or Price to Revenue). Current price to sales ratio is estimated based on current market price and 12 month sales ending March, 2022 the latest reported by S&P. Source: Standard & Poor's

Inflation Adjusted SP500 : Inflation adjusted SP500. Other than the current price, all prices are monthly average closing prices. Sources: Standard & Poor's Robert Shiller and his book Irrational Exuberance for historic S&P 500 prices, and historic CPIs.

Revenue Per Share : Trailing twelve month S&P 500 Sales Per Share (S&P 500 Revenue Per Share) non-inflation adjusted current dollars. Source: Standard & Poor's

Earnings Per Share : S&P 500 Earnings Per Share. 12-month real earnings per share inflation adjusted, constant August, 2022 dollars. Sources: Standard & Poor's for current S&P 500 Earnings. Robert Shiller and his book Irrational Exuberance for historic S&P 500 Earnings.

Disclaimer: This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Singular and Cumulative Volume Delta (SVD+CVD)This a Volume Delta indicator with Cumulative Volume Delta.

I have been studying Volume Delta and CVD trading strategies and indicator styles.

This implementation was developed to test a basic trailing window / oscillator approach.

Script has been republished as public and searchable.

Changelog from private era follows.

Jun 9 (2022)

Release Notes:

Added option to use EMA/SMA based cumulation. This will not scale well with singular data, so default view is still SUM.

Jun 9 (2022)

Release Notes:

Outdated comment correction.

Jun 9 (2022)

Release Notes:

Added default option to normalilze visual scale of MA cumulation types. The averaging creates a singular value sized results, instead of a range-sums. This multiples that candle result by the range length to get a range-sum sized result.

Added option to scale the cumulation size relative to the volume size. 1-to-1 scaling creates singular deltas that can be hard to see with all options on. This allows you to beef them up for visual or weighting purposes.

Jun 15 (2022)

Release Notes: * Added break even level for current delta. Tells where current delta must land for cumulative delta to stay flat.

* Added comparison of historical cumulative levels to current level. The historical levels are the initial values going into current accumulation window.

* Changed title of indicator to be more generic, clear, and searchable.

Jun 15 (2022)

Release Notes: * Added option to have the cumulation cutoff line AFTER or OVER the end of the cumulation window. This change is to ensure the indicator clearly documents it's behavior and avoids confusion on this / last cumulation window semantics.

* Bugfix: Initial levels were pulled from cumulation line which was AFTER end of window. This has been changed to the initial values INSIDE the cumulation window.

* Code cleanup.

June 17th (2022)

Release Notes: Marked as beta because TV confirmed they no longer allow private scripts to be changed to public. (Despite lingering documentation that says otherwise.

June 17th (2022)

Re-published as public.

ICT Master Suite [Trading IQ]Hello Traders!

We’re excited to introduce the ICT Master Suite by TradingIQ, a new tool designed to bring together several ICT concepts and strategies in one place.

The Purpose Behind the ICT Master Suite

There are a few challenges traders often face when using ICT-related indicators:

Many available indicators focus on one or two ICT methods, which can limit traders who apply a broader range of ICT related techniques on their charts.

There aren't many indicators for ICT strategy models, and we couldn't find ICT indicators that allow for testing the strategy models and setting alerts.

Many ICT related concepts exist in the public domain as indicators, not strategies! This makes it difficult to verify that the ICT concept has some utility in the market you're trading and if it's worth trading - it's difficult to know if it's working!

Some users might not have enough chart space to apply numerous ICT related indicators, which can be restrictive for those wanting to use multiple ICT techniques simultaneously.

The ICT Master Suite is designed to offer a comprehensive option for traders who want to apply a variety of ICT methods. By combining several ICT techniques and strategy models into one indicator, it helps users maximize their chart space while accessing multiple tools in a single slot.

Additionally, the ICT Master Suite was developed as a strategy . This means users can backtest various ICT strategy models - including deep backtesting. A primary goal of this indicator is to let traders decide for themselves what markets to trade ICT concepts in and give them the capability to figure out if the strategy models are worth trading!

What Makes the ICT Master Suite Different

There are many ICT-related indicators available on TradingView, each offering valuable insights. What the ICT Master Suite aims to do is bring together a wider selection of these techniques into one tool. This includes both key ICT methods and strategy models, allowing traders to test and activate strategies all within one indicator.

Features

The ICT Master Suite offers:

Multiple ICT strategy models, including the 2022 Strategy Model and Unicorn Model, which can be built, tested, and used for live trading.

Calculation and display of key price areas like Breaker Blocks, Rejection Blocks, Order Blocks, Fair Value Gaps, Equal Levels, and more.

The ability to set alerts based on these ICT strategies and key price areas.

A comprehensive, yet practical, all-inclusive ICT indicator for traders.

Customizable Timeframe - Calculate ICT concepts on off-chart timeframes

Unicorn Strategy Model

2022 Strategy Model

Liquidity Raid Strategy Model

OTE (Optimal Trade Entry) Strategy Model

Silver Bullet Strategy Model

Order blocks

Breaker blocks

Rejection blocks

FVG

Strong highs and lows

Displacements

Liquidity sweeps

Power of 3

ICT Macros

HTF previous bar high and low

Break of Structure indications

Market Structure Shift indications

Equal highs and lows

Swings highs and swing lows

Fibonacci TPs and SLs

Swing level TPs and SLs

Previous day high and low TPs and SLs

And much more! An ongoing project!

How To Use

Many traders will already be familiar with the ICT related concepts listed above, and will find using the ICT Master Suite quite intuitive!

Despite this, let's go over the features of the tool in-depth and how to use the tool!

The image above shows the ICT Master Suite with almost all techniques activated.

ICT 2022 Strategy Model

The ICT Master suite provides the ability to test, set alerts for, and live trade the ICT 2022 Strategy Model.

The image above shows an example of a long position being entered following a complete setup for the 2022 ICT model.

A liquidity sweep occurs prior to an upside breakout. During the upside breakout the model looks for the FVG that is nearest 50% of the setup range. A limit order is placed at this FVG for entry.

The target entry percentage for the range is customizable in the settings. For instance, you can select to enter at an FVG nearest 33% of the range, 20%, 66%, etc.

The profit target for the model generally uses the highest high of the range (100%) for longs and the lowest low of the range (100%) for shorts. Stop losses are generally set at 0% of the range.

The image above shows the short model in action!

Whether you decide to follow the 2022 model diligently or not, you can still set alerts when the entry condition is met.

ICT Unicorn Model

The image above shows an example of a long position being entered following a complete setup for the ICT Unicorn model.

A lower swing low followed by a higher swing high precedes the overlap of an FVG and breaker block formed during the sequence.

During the upside breakout the model looks for an FVG and breaker block that formed during the sequence and overlap each other. A limit order is placed at the nearest overlap point to current price.

The profit target for this example trade is set at the swing high and the stop loss at the swing low. However, both the profit target and stop loss for this model are configurable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

For Longs, the selectable stop losses are:

Swing Low

Bottom of FVG or breaker block

The image above shows the short version of the Unicorn Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

For Shorts, the selectable stop losses are:

Swing High

Top of FVG or breaker block

The image above shows the profit target and stop loss options in the settings for the Unicorn Model.

Optimal Trade Entry (OTE) Model

The image above shows an example of a long position being entered following a complete setup for the OTE model.

Price retraces either 0.62, 0.705, or 0.79 of an upside move and a trade is entered.

The profit target for this example trade is set at the -0.5 fib level. This is also adjustable in the settings.

For Longs, the selectable profit targets are:

Swing High

Fib -0.5

Fib -1

Fib -2

The image above shows the short version of the OTE Model in action!

For Shorts, the selectable profit targets are:

Swing Low

Fib -0.5

Fib -1

Fib -2

Liquidity Raid Model

The image above shows an example of a long position being entered following a complete setup for the Liquidity Raid Modell.

The user must define the session in the settings (for this example it is 13:30-16:00 NY time).

During the session, the indicator will calculate the session high and session low. Following a “raid” of either the session high or session low (after the session has completed) the script will look for an entry at a recently formed breaker block.

If the session high is raided the script will look for short entries at a bearish breaker block. If the session low is raided the script will look for long entries at a bullish breaker block.

For Longs, the profit target options are:

Swing high

User inputted Lib level

For Longs, the stop loss options are:

Swing low

User inputted Lib level

Breaker block bottom

The image above shows the short version of the Liquidity Raid Model in action!

For Shorts, the profit target options are:

Swing Low

User inputted Lib level

For Shorts, the stop loss options are:

Swing High

User inputted Lib level

Breaker block top

Silver Bullet Model

The image above shows an example of a long position being entered following a complete setup for the Silver Bullet Modell.

During the session, the indicator will determine the higher timeframe bias. If the higher timeframe bias is bullish the strategy will look to enter long at an FVG that forms during the session. If the higher timeframe bias is bearish the indicator will look to enter short at an FVG that forms during the session.

For Longs, the profit target options are:

Nearest Swing High Above Entry

Previous Day High

For Longs, the stop loss options are:

Nearest Swing Low

Previous Day Low

The image above shows the short version of the Silver Bullet Model in action!

For Shorts, the profit target options are:

Nearest Swing Low Below Entry

Previous Day Low

For Shorts, the stop loss options are:

Nearest Swing High

Previous Day High

Order blocks

The image above shows indicator identifying and labeling order blocks.

The color of the order blocks, and how many should be shown, are configurable in the settings!

Breaker Blocks

The image above shows indicator identifying and labeling order blocks.

The color of the breaker blocks, and how many should be shown, are configurable in the settings!

Rejection Blocks

The image above shows indicator identifying and labeling rejection blocks.

The color of the rejection blocks, and how many should be shown, are configurable in the settings!

Fair Value Gaps

The image above shows indicator identifying and labeling fair value gaps.

The color of the fair value gaps, and how many should be shown, are configurable in the settings!

Additionally, you can select to only show fair values gaps that form after a liquidity sweep. Doing so reduces "noisy" FVGs and focuses on identifying FVGs that form after a significant trading event.

The image above shows the feature enabled. A fair value gap that occurred after a liquidity sweep is shown.

Market Structure

The image above shows the ICT Master Suite calculating market structure shots and break of structures!

The color of MSS and BoS, and whether they should be displayed, are configurable in the settings.

Displacements

The images above show indicator identifying and labeling displacements.

The color of the displacements, and how many should be shown, are configurable in the settings!

Equal Price Points

The image above shows the indicator identifying and labeling equal highs and equal lows.

The color of the equal levels, and how many should be shown, are configurable in the settings!

Previous Custom TF High/Low

The image above shows the ICT Master Suite calculating the high and low price for a user-defined timeframe. In this case the previous day’s high and low are calculated.

To illustrate the customizable timeframe function, the image above shows the indicator calculating the previous 4 hour high and low.

Liquidity Sweeps

The image above shows the indicator identifying a liquidity sweep prior to an upside breakout.

The image above shows the indicator identifying a liquidity sweep prior to a downside breakout.

The color and aggressiveness of liquidity sweep identification are adjustable in the settings!

Power Of Three

The image above shows the indicator calculating Po3 for two user-defined higher timeframes!

Macros

The image above shows the ICT Master Suite identifying the ICT macros!

ICT Macros are only displayable on the 5 minute timeframe or less.

Strategy Performance Table

In addition to a full-fledged TradingView backtest for any of the ICT strategy models the indicator offers, a quick-and-easy strategy table exists for the indicator!

The image above shows the strategy performance table in action.

Keep in mind that, because the ICT Master Suite is a strategy script, you can perform fully automatic backtests, deep backtests, easily add commission and portfolio balance and look at pertinent metrics for the ICT strategies you are testing!

Lite Mode

Traders who want the cleanest chart possible can toggle on “Lite Mode”!

In Lite Mode, any neon or “glow” like effects are removed and key levels are marked as strict border boxes. You can also select to remove box borders if that’s what you prefer!

Settings Used For Backtest

For the displayed backtest, a starting balance of $1000 USD was used. A commission of 0.02%, slippage of 2 ticks, a verify price for limit orders of 2 ticks, and 5% of capital investment per order.

A commission of 0.02% was used due to the backtested asset being a perpetual future contract for a crypto currency. The highest commission (lowest-tier VIP) for maker orders on many exchanges is 0.02%. All entered positions take place as maker orders and so do profit target exits. Stop orders exist as stop-market orders.

A slippage of 2 ticks was used to simulate more realistic stop-market orders. A verify limit order settings of 2 ticks was also used. Even though BTCUSDT.P on Binance is liquid, we just want the backtest to be on the safe side. Additionally, the backtest traded 100+ trades over the period. The higher the sample size the better; however, this example test can serve as a starting point for traders interested in ICT concepts.

Community Assistance And Feedback

Given the complexity and idiosyncratic applications of ICT concepts amongst its proponents, the ICT Master Suite’s built-in strategies and level identification methods might not align with everyone's interpretation.

That said, the best we can do is precisely define ICT strategy rules and concepts to a repeatable process, test, and apply them! Whether or not an ICT strategy is trading precisely how you would trade it, seeing the model in action, taking trades, and with performance statistics is immensely helpful in assessing predictive utility.

If you think we missed something, you notice a bug, have an idea for strategy model improvement, please let us know! The ICT Master Suite is an ongoing project that will, ideally, be shaped by the community.

A big thank you to the @PineCoders for their Time Library!

Thank you!

ISODateTimeLibrary "ISODateTime"

getDateParts(dateStr)

Get year, month, day from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getTimeParts(dateStr)

Get hour, minute, seconds from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getUTCTimezone(dateStr)

Get UTC timezone.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: string UTC timezone

CDC ActionZone BF for ETHUSD-1D © PRoSkYNeT-EE

Based on improvements from "Kitti-Playbook Action Zone V.4.2.0.3 for Stock Market"

Based on improvements from "CDC Action Zone V3 2020 by piriya33"

Based on Triple MACD crossover between 9/15, 21/28, 15/28 for filter error signal (noise) from CDC ActionZone V3

MACDs generated from the execution of millions of times in the "Brute Force Algorithm" to backtest data from the past 5 years. ( 2017-08-21 to 2022-08-01 )

Released 2022-08-01

***** The indicator is used in the ETHUSD 1 Day period ONLY *****

Recommended Stop Loss : -4 % (execute stop Loss after candlestick has been closed)

Backtest Result ( Start $100 )

Winrate 63 % (Win:12, Loss:7, Total:19)

Live Days 1,806 days

B : Buy

S : Sell

SL : Stop Loss

2022-07-19 07 - 1,542 : B 6.971 ETH

2022-04-13 07 - 3,118 : S 8.98 % $10,750 12,7,19 63 %

2022-03-20 07 - 2,861 : B 3.448 ETH

2021-12-03 07 - 4,216 : SL -8.94 % $9,864 11,7,18 61 %

2021-11-30 07 - 4,630 : B 2.340 ETH

2021-11-18 07 - 3,997 : S 13.71 % $10,832 11,6,17 65 %

2021-10-05 07 - 3,515 : B 2.710 ETH

2021-09-20 07 - 2,977 : S 29.38 % $9,526 10,6,16 63 %

2021-07-28 07 - 2,301 : B 3.200 ETH

2021-05-20 07 - 2,769 : S 50.49 % $7,363 9,6,15 60 %

2021-03-30 07 - 1,840 : B 2.659 ETH

2021-03-22 07 - 1,681 : SL -8.29 % $4,893 8,6,14 57 %

2021-03-08 07 - 1,833 : B 2.911 ETH

2021-02-26 07 - 1,445 : S 279.27 % $5,335 8,5,13 62 %

2020-10-13 07 - 381 : B 3.692 ETH

2020-09-05 07 - 335 : S 38.43 % $1,407 7,5,12 58 %

2020-07-06 07 - 242 : B 4.199 ETH

2020-06-27 07 - 221 : S 28.49 % $1,016 6,5,11 55 %

2020-04-16 07 - 172 : B 4.598 ETH

2020-02-29 07 - 217 : S 47.62 % $791 5,5,10 50 %

2020-01-12 07 - 147 : B 3.644 ETH

2019-11-18 07 - 178 : S -2.73 % $536 4,5,9 44 %

2019-11-01 07 - 183 : B 3.010 ETH

2019-09-23 07 - 201 : SL -4.29 % $551 4,4,8 50 %

2019-09-18 07 - 210 : B 2.740 ETH

2019-07-12 07 - 275 : S 63.69 % $575 4,3,7 57 %

2019-05-03 07 - 168 : B 2.093 ETH

2019-04-28 07 - 158 : S 29.51 % $352 3,3,6 50 %

2019-02-15 07 - 122 : B 2.225 ETH

2019-01-10 07 - 125 : SL -6.02 % $271 2,3,5 40 %

2018-12-29 07 - 133 : B 2.172 ETH

2018-05-22 07 - 641 : S 5.95 % $289 2,2,4 50 %

2018-04-21 07 - 605 : B 0.451 ETH

2018-02-02 07 - 922 : S 197.42 % $273 1,2,3 33 %

2017-11-11 07 - 310 : B 0.296 ETH

2017-10-09 07 - 297 : SL -4.50 % $92 0,2,2 0 %

2017-10-07 07 - 311 : B 0.309 ETH

2017-08-22 07 - 310 : SL -4.02 % $96 0,1,1 0 %

2017-08-21 07 - 323 : B 0.310 ETH

Linear EDCA v1.2Strategy Description:

Linear EDCA (Linear Enhanced Dollar Cost Averaging) is an enhanced version of the DCA fixed investment strategy. It has the following features:

1. Take the 1100-day SMA as a reference indicator, enter the buy range below the moving average, and enter the sell range above the moving average

2. The order to buy and sell is carried out at different "speed", which are set with two linear functions, and you can change the slope of the linear function to achieve different trading position control purposes

3. This fixed investment is a low-frequency strategy and only works on a daily level cycle

----------------

Strategy backtest performance:

BTCUSD (September 2014~September 2022): Net profit margin 26378%, maximum floating loss 47.12% (2015-01-14)

ETHUSD (August 2018~September 2022): Net profit margin 1669%, maximum floating loss 49.63% (2018-12-14)

----------------

How the strategy works:

Buying Conditions:

The closing price of the day is below the 1100 SMA, and the ratio of buying positions is determined by the deviation of the closing price from the moving average and the buySlope parameter

Selling Conditions:

The closing price of the day is above the 1100 SMA, and the ratio of the selling position is determined by the deviation of the closing price and the moving average and the sellSlope parameter

special case:

When the sellOffset parameter>0, it will maintain a small buy within a certain range above the 1100 SMA to avoid prematurely starting to sell

The maximum ratio of a single buy position does not exceed defInvestRatio * maxBuyRate

The maximum ratio of a single sell position does not exceed defInvestRatio * maxSellRate

----------------

Version Information:

Current version v1.2 (the first officially released version)

v1.2 version setting parameter description:

defInvestRatio: The default fixed investment ratio, the strategy will calculate the position ratio of a single fixed investment based on this ratio and a linear function. The default 0.025 represents 2.5% of the position

buySlope: the slope of the linear function of the order to buy, used to control the position ratio of a single buy

sellSlope: the slope of the linear function of the order to sell, used to control the position ratio of a single sell

sellOffset: The offset of the order to sell. If it is greater than 0, it will keep a small buy within a certain range to avoid starting to sell too early

maxSellRate: Controls the maximum sell multiple. The maximum ratio of a single sell position does not exceed defInvestRatio * maxSellRate

maxBuyRate: Controls the maximum buy multiple. The maximum ratio of a single buy position does not exceed defInvestRatio * maxBuyRate

maPeriod: the length of the moving average, 1100-day MA is used by default

smoothing: moving average smoothing algorithm, SMA is used by default

useDateFilter: Whether to specify a date range when backtesting

settleOnEnd: If useDateFilter==true, whether to close the position after the end date

startDate: If useDateFilter==true, specify the backtest start date

endDate: If useDateFilter==true, specify the end date of the backtest

investDayofweek: Invest on the day of the week, the default is to close on Monday

intervalDays: The minimum number of days between each invest. Since it is calculated on a weekly basis, this number must be 7 or a multiple of 7

The v1.2 version data window indicator description (only important indicators are listed):

MA: 1100-day SMA

RoR%: floating profit and loss of the current position

maxLoss%: The maximum floating loss of the position. Note that this floating loss represents the floating loss of the position, and does not represent the floating loss of the overall account. For example, the current position is 1%, the floating loss is 50%, the overall account floating loss is 0.5%, but the position floating loss is 50%

maxGain%: The maximum floating profit of the position. Note that this floating profit represents the floating profit of the position, and does not represent the floating profit of the overall account.

positionPercent%: position percentage

positionAvgPrice: position average holding cost

--------------------------------

策略说明:

Linear EDCA(Linear Enhanced Dollar Cost Averaging)是一个DCA定投策略的增强版本,它具有如下特性:

1. 以1100日SMA均线作为参考指标,在均线以下进入定买区间,在均线以上进入定卖区间

2. 定买和定卖以不同的“速率”进行,它们用两条线性函数设定,并且你可以通过改变线性函数的斜率,以达到不同的买卖仓位控制的目的

3. 本定投作为低频策略,只在日级别周期工作

----------------

策略回测表现:

BTCUSD(2014年09月~2022年09月):净利润率26378%,最大浮亏47.12%(2015-01-14)

ETHUSD(2018年08~2022年09月):净利润率1669%,最大浮亏49.63%(2018-12-14)

----------------

策略工作原理:

买入条件:

当日收盘价在 1100 SMA 之下,由收盘价和均线的偏离度,以及buySlope参数决定买入仓位比例

卖出条件:

当日收盘价在 1100 SMA之上,由收盘价和均线的偏离度,以及sellSlope参数决定卖出仓位比例

特例:

当sellOffset参数>0,则在 1100 SMA以上一定范围内还会保持小幅买入,避免过早开始卖出

单次买入仓位比例最大不超过 defInvestRatio * maxBuyRate

单次卖出仓位比例最大不超过 defInvestRatio * maxSellRate

----------------

版本信息:

当前版本v1.2(第一个正式发布的版本)

v1.2版本设置参数说明:

defInvestRatio: 默认定投比例,策略会根据此比例和线性函数计算得出单次定投的仓位比例。默认0.025代表2.5%仓位

buySlope: 定买的线性函数斜率,用来控制单次买入的仓位倍率

sellSlope: 定卖的线性函数斜率,用来控制单次卖出的仓位倍率

sellOffset: 定卖的偏移度,如果大于0,则在一定范围内还会保持小幅买入,避免过早开始卖出

maxSellRate: 控制最大卖出倍率。单次卖出仓位比例最大不超过 defInvestRatio * maxSellRate

maxBuyRate: 控制最大买入倍率。单次买入仓位比例最大不超过 defInvestRatio * maxBuyRate

maPeriod: 均线长度,默认使用1100日MA

smoothing: 均线平滑算法,默认使用SMA

useDateFilter: 回测时是否要指定日期范围

settleOnEnd: 如果useDateFilter==true,在结束日之后是否平仓所持有的仓位平仓

startDate: 如果useDateFilter==true,指定回测开始日期

endDate: 如果useDateFilter==true,指定回测结束日期

investDayofweek: 每次在周几定投,默认在每周一收盘

intervalDays: 每次定投之间的最小间隔天数,由于是按周计算,所以此数字必须是7或7的倍数

v1.2版本数据窗口指标说明(只列出重要指标):

MA:1100日SMA

RoR%: 当前仓位的浮动盈亏

maxLoss%: 仓位曾经的最大浮动亏损,注意此浮亏代表持仓仓位的浮亏情况,并不代表整体账户浮亏情况。例如当前仓位是1%,浮亏50%,整体账户浮亏是0.5%,但仓位浮亏是50%

maxGain%: 仓位曾经的最大浮动盈利,注意此浮盈代表持仓仓位的浮盈情况,并不代表整体账户浮盈情况。

positionPercent%: 仓位持仓占比

positionAvgPrice: 仓位平均持仓成本

Quantitative Easing and Tightening PeriodsQuantitative Easing (QE) and Quantitative Tightening (QT) periods based on historical events from the Federal Reserve:

Quantitative Easing (QE) Periods:

QE1:

Start: November 25, 2008

End: March 31, 2010

Description: The Federal Reserve initiated QE1 in response to the financial crisis, purchasing mortgage-backed securities and Treasuries.

QE2:

Start: November 3, 2010

End: June 29, 2011

Description: QE2 involved the purchase of $600 billion in U.S. Treasury bonds to further stimulate the economy.

QE3:

Start: September 13, 2012

End: October 29, 2014

Description: QE3 was an open-ended bond-buying program with monthly purchases of $85 billion in Treasuries and mortgage-backed securities.

QE4 (COVID-19 Pandemic Response):

Start: March 15, 2020

End: March 10, 2022

Description: The Federal Reserve engaged in QE4 in response to the economic impact of the COVID-19 pandemic, purchasing Treasuries and MBS in an effort to provide liquidity.

Quantitative Tightening (QT) Periods:

QT1:

Start: October 1, 2017

End: August 1, 2019

Description: The Federal Reserve began shrinking its balance sheet in 2017, gradually reducing its holdings of U.S. Treasuries and mortgage-backed securities. This period ended in August 2019 when the Fed decided to stop reducing its balance sheet.

QT2:

Start: June 1, 2022

End: Ongoing (as of March 2025)

Description: The Federal Reserve started QT again in June 2022, reducing its holdings of U.S. Treasuries and MBS in response to rising inflation. The Fed has continued this tightening cycle.

These periods are key moments in U.S. monetary policy, where the Fed either injected liquidity into the economy (QE) or reduced its balance sheet by not reinvesting maturing securities (QT). The exact dates and nature of these policies may vary based on interpretation and adjustments to the Fed's actions during those times.

Customizable BTC Seasonality StrategyThis strategy leverages intraday seasonality effects in Bitcoin, specifically targeting hours of statistically significant returns during periods when traditional financial markets are closed. Padysak and Vojtko (2022) demonstrate that Bitcoin exhibits higher-than-average returns from 21:00 UTC to 23:00 UTC, a period in which all major global exchanges, such as the New York Stock Exchange (NYSE), Tokyo Stock Exchange, and London Stock Exchange, are closed. The absence of competing trading activity from traditional markets during these hours appears to contribute to these statistically significant returns.

The strategy proceeds as follows:

Entry Time: A long position in Bitcoin is opened at a user-specified time, which defaults to 21:00 UTC, aligning with the beginning of the identified high-return window.

Holding Period: The position is held for two hours, capturing the positive returns typically observed during this period.

Exit Time: The position is closed at a user-defined time, defaulting to 23:00 UTC, allowing the strategy to exit as the favorable period concludes.

This simple seasonality strategy aims to achieve a 33% annualized return with a notably reduced volatility of 20.93% and maximum drawdown of -22.45%. The results suggest that investing only during these high-return hours is more stable and less risky than a passive holding strategy (Padysak & Vojtko, 2022).

References

Padysak, M., & Vojtko, R. (2022). Seasonality, Trend-following, and Mean reversion in Bitcoin.

Economic Calendar (Import from Spreadsheet)This script draws vertical lines to mark Economic Calendar Events.

Datetime of events is defined by user in Settings via a standardized line of text.

Motivation for coding this script:

All traders should be aware of economic calendar events. At times, when you really need to pay attention to an upcoming major event, you might even decide to use the vertical-line drawing tool to mark it. However, this takes manual effort.

This script provides a solution to performing mundane tasks such as drawing vertical lines and dragging them ever so slightly, just to have them approximately aligned with exact time.

Parameters:

(1) Source data - String representation of collection of datetime referencing to Economic Calendar Events

(2) Line color, & (3) Width of line - For displaying vertical lines drawn by script.

Standardized format for Source Data :

Example:

If 'GMT;2022,6,1,14,0,0;2022,6,2,12,15,0;' is provided to PineScript, then two vertical lines will be drawn on June 6, 2022 according to the exact time in 'YYYY,MM,DD,hh,mm,ss' format at the specified timezone (GMT in this case).

Template for Source Data :

Included here, link below, is a shared Google Sheet that systematically processes Economic Calendar data provided in the 'Raw Data' tab.

drive.google.com

Users are advised to use their preferred methods* to format the string (for source data param.), and apply their own criteria to sort down the Events. (ie. only include Events of High Impact, etc.)

* Preferred methods (as mentioned above) does not mean being limited to using the template as provided in this post.

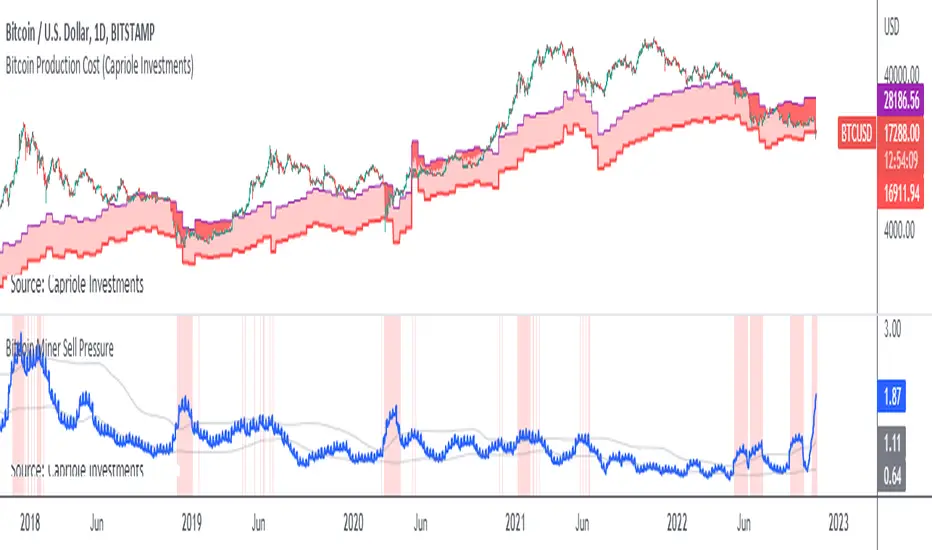

Bitcoin Miner Sell PressureBitcoin miners are in pain and now (November 2022) selling more than they have in almost 5 years!

Introducing: Bitcoin Miner Sell Pressure.

A free, open-source indicator which tracks on-chain data to highlight when Bitcoin miners are selling more of their reserves than usual.

The indicator tracks the ratio of on-chain miner Bitcoin outflows to miner Bitcoin reserves.

- Higher = more selling than usual

- Lower = less selling than usual

- Red = extraordinary sell pressure

Today , it's red.

What can we see now ?

Miners are not great at treasury management. They tend to sell most when they are losing money (like today). But there have been times when they sold well into high profit, such as into the 2017 $20K top and in early 2021 when Bitcoin breached $40K.

Bitcoin Miner Sell Pressure identifies industry stress, excess and miner capitulation.

Unsurprisingly, there is a high correlation with Bitcoin Production Cost; giving strong confluence to both.

In some instances, BMSP spots capitulation before Hash Ribbons. Such as today!