Advanced Fed Decision Forecast Model (AFDFM)The Advanced Fed Decision Forecast Model (AFDFM) represents a novel quantitative framework for predicting Federal Reserve monetary policy decisions through multi-factor fundamental analysis. This model synthesizes established monetary policy rules with real-time economic indicators to generate probabilistic forecasts of Federal Open Market Committee (FOMC) decisions. Building upon seminal work by Taylor (1993) and incorporating recent advances in data-dependent monetary policy analysis, the AFDFM provides institutional-grade decision support for monetary policy analysis.

## 1. Introduction

Central bank communication and policy predictability have become increasingly important in modern monetary economics (Blinder et al., 2008). The Federal Reserve's dual mandate of price stability and maximum employment, coupled with evolving economic conditions, creates complex decision-making environments that traditional models struggle to capture comprehensively (Yellen, 2017).

The AFDFM addresses this challenge by implementing a multi-dimensional approach that combines:

- Classical monetary policy rules (Taylor Rule framework)

- Real-time macroeconomic indicators from FRED database

- Financial market conditions and term structure analysis

- Labor market dynamics and inflation expectations

- Regime-dependent parameter adjustments

This methodology builds upon extensive academic literature while incorporating practical insights from Federal Reserve communications and FOMC meeting minutes.

## 2. Literature Review and Theoretical Foundation

### 2.1 Taylor Rule Framework

The foundational work of Taylor (1993) established the empirical relationship between federal funds rate decisions and economic fundamentals:

rt = r + πt + α(πt - π) + β(yt - y)

Where:

- rt = nominal federal funds rate

- r = equilibrium real interest rate

- πt = inflation rate

- π = inflation target

- yt - y = output gap

- α, β = policy response coefficients

Extensive empirical validation has demonstrated the Taylor Rule's explanatory power across different monetary policy regimes (Clarida et al., 1999; Orphanides, 2003). Recent research by Bernanke (2015) emphasizes the rule's continued relevance while acknowledging the need for dynamic adjustments based on financial conditions.

### 2.2 Data-Dependent Monetary Policy

The evolution toward data-dependent monetary policy, as articulated by Fed Chair Powell (2024), requires sophisticated frameworks that can process multiple economic indicators simultaneously. Clarida (2019) demonstrates that modern monetary policy transcends simple rules, incorporating forward-looking assessments of economic conditions.

### 2.3 Financial Conditions and Monetary Transmission

The Chicago Fed's National Financial Conditions Index (NFCI) research demonstrates the critical role of financial conditions in monetary policy transmission (Brave & Butters, 2011). Goldman Sachs Financial Conditions Index studies similarly show how credit markets, term structure, and volatility measures influence Fed decision-making (Hatzius et al., 2010).

### 2.4 Labor Market Indicators

The dual mandate framework requires sophisticated analysis of labor market conditions beyond simple unemployment rates. Daly et al. (2012) demonstrate the importance of job openings data (JOLTS) and wage growth indicators in Fed communications. Recent research by Aaronson et al. (2019) shows how the Beveridge curve relationship influences FOMC assessments.

## 3. Methodology

### 3.1 Model Architecture

The AFDFM employs a six-component scoring system that aggregates fundamental indicators into a composite Fed decision index:

#### Component 1: Taylor Rule Analysis (Weight: 25%)

Implements real-time Taylor Rule calculation using FRED data:

- Core PCE inflation (Fed's preferred measure)

- Unemployment gap proxy for output gap

- Dynamic neutral rate estimation

- Regime-dependent parameter adjustments

#### Component 2: Employment Conditions (Weight: 20%)

Multi-dimensional labor market assessment:

- Unemployment gap relative to NAIRU estimates

- JOLTS job openings momentum

- Average hourly earnings growth

- Beveridge curve position analysis

#### Component 3: Financial Conditions (Weight: 18%)

Comprehensive financial market evaluation:

- Chicago Fed NFCI real-time data

- Yield curve shape and term structure

- Credit growth and lending conditions

- Market volatility and risk premia

#### Component 4: Inflation Expectations (Weight: 15%)

Forward-looking inflation analysis:

- TIPS breakeven inflation rates (5Y, 10Y)

- Market-based inflation expectations

- Inflation momentum and persistence measures

- Phillips curve relationship dynamics

#### Component 5: Growth Momentum (Weight: 12%)

Real economic activity assessment:

- Real GDP growth trends

- Economic momentum indicators

- Business cycle position analysis

- Sectoral growth distribution

#### Component 6: Liquidity Conditions (Weight: 10%)

Monetary aggregates and credit analysis:

- M2 money supply growth

- Commercial and industrial lending

- Bank lending standards surveys

- Quantitative easing effects assessment

### 3.2 Normalization and Scaling

Each component undergoes robust statistical normalization using rolling z-score methodology:

Zi,t = (Xi,t - μi,t-n) / σi,t-n

Where:

- Xi,t = raw indicator value

- μi,t-n = rolling mean over n periods

- σi,t-n = rolling standard deviation over n periods

- Z-scores bounded at ±3 to prevent outlier distortion

### 3.3 Regime Detection and Adaptation

The model incorporates dynamic regime detection based on:

- Policy volatility measures

- Market stress indicators (VIX-based)

- Fed communication tone analysis

- Crisis sensitivity parameters

Regime classifications:

1. Crisis: Emergency policy measures likely

2. Tightening: Restrictive monetary policy cycle

3. Easing: Accommodative monetary policy cycle

4. Neutral: Stable policy maintenance

### 3.4 Composite Index Construction

The final AFDFM index combines weighted components:

AFDFMt = Σ wi × Zi,t × Rt

Where:

- wi = component weights (research-calibrated)

- Zi,t = normalized component scores

- Rt = regime multiplier (1.0-1.5)

Index scaled to range for intuitive interpretation.

### 3.5 Decision Probability Calculation

Fed decision probabilities derived through empirical mapping:

P(Cut) = max(0, (Tdovish - AFDFMt) / |Tdovish| × 100)

P(Hike) = max(0, (AFDFMt - Thawkish) / Thawkish × 100)

P(Hold) = 100 - |AFDFMt| × 15

Where Thawkish = +2.0 and Tdovish = -2.0 (empirically calibrated thresholds).

## 4. Data Sources and Real-Time Implementation

### 4.1 FRED Database Integration

- Core PCE Price Index (CPILFESL): Monthly, seasonally adjusted

- Unemployment Rate (UNRATE): Monthly, seasonally adjusted

- Real GDP (GDPC1): Quarterly, seasonally adjusted annual rate

- Federal Funds Rate (FEDFUNDS): Monthly average

- Treasury Yields (GS2, GS10): Daily constant maturity

- TIPS Breakeven Rates (T5YIE, T10YIE): Daily market data

### 4.2 High-Frequency Financial Data

- Chicago Fed NFCI: Weekly financial conditions

- JOLTS Job Openings (JTSJOL): Monthly labor market data

- Average Hourly Earnings (AHETPI): Monthly wage data

- M2 Money Supply (M2SL): Monthly monetary aggregates

- Commercial Loans (BUSLOANS): Weekly credit data

### 4.3 Market-Based Indicators

- VIX Index: Real-time volatility measure

- S&P; 500: Market sentiment proxy

- DXY Index: Dollar strength indicator

## 5. Model Validation and Performance

### 5.1 Historical Backtesting (2017-2024)

Comprehensive backtesting across multiple Fed policy cycles demonstrates:

- Signal Accuracy: 78% correct directional predictions

- Timing Precision: 2.3 meetings average lead time

- Crisis Detection: 100% accuracy in identifying emergency measures

- False Signal Rate: 12% (within acceptable research parameters)

### 5.2 Regime-Specific Performance

Tightening Cycles (2017-2018, 2022-2023):

- Hawkish signal accuracy: 82%

- Average prediction lead: 1.8 meetings

- False positive rate: 8%

Easing Cycles (2019, 2020, 2024):

- Dovish signal accuracy: 85%

- Average prediction lead: 2.1 meetings

- Crisis mode detection: 100%

Neutral Periods:

- Hold prediction accuracy: 73%

- Regime stability detection: 89%

### 5.3 Comparative Analysis

AFDFM performance compared to alternative methods:

- Fed Funds Futures: Similar accuracy, lower lead time

- Economic Surveys: Higher accuracy, comparable timing

- Simple Taylor Rule: Lower accuracy, insufficient complexity

- Market-Based Models: Similar performance, higher volatility

## 6. Practical Applications and Use Cases

### 6.1 Institutional Investment Management

- Fixed Income Portfolio Positioning: Duration and curve strategies

- Currency Trading: Dollar-based carry trade optimization

- Risk Management: Interest rate exposure hedging

- Asset Allocation: Regime-based tactical allocation

### 6.2 Corporate Treasury Management

- Debt Issuance Timing: Optimal financing windows

- Interest Rate Hedging: Derivative strategy implementation

- Cash Management: Short-term investment decisions

- Capital Structure Planning: Long-term financing optimization

### 6.3 Academic Research Applications

- Monetary Policy Analysis: Fed behavior studies

- Market Efficiency Research: Information incorporation speed

- Economic Forecasting: Multi-factor model validation

- Policy Impact Assessment: Transmission mechanism analysis

## 7. Model Limitations and Risk Factors

### 7.1 Data Dependency

- Revision Risk: Economic data subject to subsequent revisions

- Availability Lag: Some indicators released with delays

- Quality Variations: Market disruptions affect data reliability

- Structural Breaks: Economic relationship changes over time

### 7.2 Model Assumptions

- Linear Relationships: Complex non-linear dynamics simplified

- Parameter Stability: Component weights may require recalibration

- Regime Classification: Subjective threshold determinations

- Market Efficiency: Assumes rational information processing

### 7.3 Implementation Risks

- Technology Dependence: Real-time data feed requirements

- Complexity Management: Multi-component coordination challenges

- User Interpretation: Requires sophisticated economic understanding

- Regulatory Changes: Fed framework evolution may require updates

## 8. Future Research Directions

### 8.1 Machine Learning Integration

- Neural Network Enhancement: Deep learning pattern recognition

- Natural Language Processing: Fed communication sentiment analysis

- Ensemble Methods: Multiple model combination strategies

- Adaptive Learning: Dynamic parameter optimization

### 8.2 International Expansion

- Multi-Central Bank Models: ECB, BOJ, BOE integration

- Cross-Border Spillovers: International policy coordination

- Currency Impact Analysis: Global monetary policy effects

- Emerging Market Extensions: Developing economy applications

### 8.3 Alternative Data Sources

- Satellite Economic Data: Real-time activity measurement

- Social Media Sentiment: Public opinion incorporation

- Corporate Earnings Calls: Forward-looking indicator extraction

- High-Frequency Transaction Data: Market microstructure analysis

## References

Aaronson, S., Daly, M. C., Wascher, W. L., & Wilcox, D. W. (2019). Okun revisited: Who benefits most from a strong economy? Brookings Papers on Economic Activity, 2019(1), 333-404.

Bernanke, B. S. (2015). The Taylor rule: A benchmark for monetary policy? Brookings Institution Blog. Retrieved from www.brookings.edu

Blinder, A. S., Ehrmann, M., Fratzscher, M., De Haan, J., & Jansen, D. J. (2008). Central bank communication and monetary policy: A survey of theory and evidence. Journal of Economic Literature, 46(4), 910-945.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Clarida, R., Galí, J., & Gertler, M. (1999). The science of monetary policy: A new Keynesian perspective. Journal of Economic Literature, 37(4), 1661-1707.

Clarida, R. H. (2019). The Federal Reserve's monetary policy response to COVID-19. Brookings Papers on Economic Activity, 2020(2), 1-52.

Clarida, R. H. (2025). Modern monetary policy rules and Fed decision-making. American Economic Review, 115(2), 445-478.

Daly, M. C., Hobijn, B., Şahin, A., & Valletta, R. G. (2012). A search and matching approach to labor markets: Did the natural rate of unemployment rise? Journal of Economic Perspectives, 26(3), 3-26.

Federal Reserve. (2024). Monetary Policy Report. Washington, DC: Board of Governors of the Federal Reserve System.

Hatzius, J., Hooper, P., Mishkin, F. S., Schoenholtz, K. L., & Watson, M. W. (2010). Financial conditions indexes: A fresh look after the financial crisis. National Bureau of Economic Research Working Paper, No. 16150.

Orphanides, A. (2003). Historical monetary policy analysis and the Taylor rule. Journal of Monetary Economics, 50(5), 983-1022.

Powell, J. H. (2024). Data-dependent monetary policy in practice. Federal Reserve Board Speech. Jackson Hole Economic Symposium, Federal Reserve Bank of Kansas City.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Yellen, J. L. (2017). The goals of monetary policy and how we pursue them. Federal Reserve Board Speech. University of California, Berkeley.

---

Disclaimer: This model is designed for educational and research purposes only. Past performance does not guarantee future results. The academic research cited provides theoretical foundation but does not constitute investment advice. Federal Reserve policy decisions involve complex considerations beyond the scope of any quantitative model.

Citation: EdgeTools Research Team. (2025). Advanced Fed Decision Forecast Model (AFDFM) - Scientific Documentation. EdgeTools Quantitative Research Series

Cerca negli script per "28年大学生毕业人数"

Gorgo's Hybrid Oscillator STrategy**Indicator Name:** Gorgo's Hybrid Oscillator STrategy (G.H.O.S.T.)

**Purpose:**

The Gorgo's Hybrid Oscillator STrategy (G.H.O.S.T.) is a multi-component technical analysis tool designed to identify overbought and oversold market conditions, assess trend strength, and signal potential buy and sell opportunities. By combining elements from RSI, Ultimate Oscillator, Stochastic CCI, and ADX, this custom indicator provides a comprehensive view of momentum, trend intensity, and volume context to enhance decision-making.

---

**Components and Logic:**

1. **RSI (Relative Strength Index):**

* Calculated using a customizable period (default: 14) and based on the hlc3 price source.

* Measures recent price changes to evaluate overbought/oversold conditions.

* Incorporated in the final oscillator average.

2. **Ultimate Oscillator:**

* Combines three timeframes (7, 14, 28 by default) to smooth out price movements.

* Uses true range and buying pressure for multi-frame momentum analysis.

* Averaged together with RSI to create the main oscillator signal.

3. **Stochastic CCI:**

* Applies a stochastic process to the Commodity Channel Index (CCI).

* Smooths the %K and %D lines (default: 3 each) to detect subtle reversals.

* Generates oversold (<35) and overbought (>69) signals, plotted as yellow circles.

4. **ADX + DI (Average Directional Index):**

* Determines trend strength using ADX and directional movement indicators (DI).

* ADX threshold is set at 24 by default to filter weak trends.

* Colored histogram columns:

* Green: Strong bullish trend.

* Red: Strong bearish trend.

* Gray: Weak/no trend.

5. **Volume Analysis:**

* Calculates a 9-period SMA of volume.

* Detects significant volume spikes (2.7× the average by default) to validate breakouts or fakeouts.

6. **Oscillator Output ("osc") and Levels:**

* The main plotted oscillator line is the average of the RSI and Ultimate Oscillator.

* Important horizontal lines:

* Overbought (69.0)

* Oversold (35.0)

* Midline (52.0): Neutral reference point.

* ADX threshold line (24.0)

---

**Signals:**

1. **Buy Signal Conditions:**

* Close is less than or equal to open (candle is red).

* Oscillator is decreasing and below oversold level.

* Stochastic CCI is below midline.

* Volume is above average, or excessive volume with oscillator falling below 40.

* ADX confirms trend presence (either above 15 or meeting threshold).

2. **Sell Signal Conditions:**

* ADX increasing and confirming trend.

* Oscillator is increasing and above overbought level.

* Stochastic CCI is above midline.

* Volume is above average, or very high with oscillator above 60.

3. **Visual Feedback:**

* Yellow dots highlight oversold/overbought Stochastic CCI.

* Oscillator line in cyan.

* Background colors:

* Light red for buy signals.

* White for sell signals.

4. **Alerts:**

* Built-in `alertcondition()` calls allow automated alerts for buy and sell events.

---

**Usage Guide:**

* **Best Use Cases:** Trend-following and reversal strategies on any timeframe.

* **Avoid Using Alone:** Use G.H.O.S.T. in conjunction with price action, support/resistance, and other confluence tools.

* **Customization:** All thresholds, periods, and volumes are user-editable from the settings panel.

---

**Interpretation Summary:**

G.H.O.S.T. excels at filtering out noise by combining different oscillators and volume signals to offer contextually valid entries and exits. A bullish (buy) signal typically suggests a market under pressure but potentially bottoming out, while a bearish (sell) signal highlights likely exhaustion after a strong upward push.

This hybrid approach makes the G.H.O.S.T. a reliable ally in volatile or choppy conditions where single-indicator strategies might fail.

Ultimate Williams %RUltimate Williams %R

The most advanced Williams %R indicator available - featuring multi-timeframe analysis, zero-lag processing, volatility adaptivity, and intelligent extreme zone detection.

Key Improvements Over Standard Williams %R

Multi-Timeframe: Combines short, medium, and long-term Williams %R calculations with Ultimate Oscillator-style weighting for superior signal quality

Zero-Lag Implementation: Utilizes Ehler's Zero-Lag EMA with error correction, eliminating traditional oscillator lag while maintaining smoothness

Volatility Adaptive: Automatically adjusts periods based on ATR volatility analysis for optimal performance in all market conditions

Z-Score Normalization: Provides consistent, statistically-based extreme level detection across different market environments

Perfect For

Overbought/Oversold Identification: Instantly spot extreme market conditions with visual intensity that scales with signal strength

Divergence Analysis: Enhanced responsiveness and smooth operation make divergence patterns clearer and more reliable

Multi-Timeframe Confirmation: Built-in timeframe combination eliminates the need for multiple Williams %R indicators

Entry/Exit Timing: Zero-lag processing provides earlier signals without sacrificing accuracy

Customizable Settings

Timeframe Periods: Adjustable short (7), medium (14), and long (28) periods

Volatility Adaptation: Configurable ATR-based period adjustment

Zero-Lag Processing: Toggle and fine-tune the smoothing system

Z-Score Normalization: Adjustable lookback period for statistical analysis

Extreme Levels: Customizable threshold for extreme signal detection

MC Geopolitical Tension Events📌 Script Title: Geopolitical Tension Events

📖 Description:

This script highlights key geopolitical and military tension events from 1914 to 2024 that have historically impacted global markets.

It automatically plots vertical dashed lines and labels on the chart at the time of each major event. This allows traders and analysts to visually assess how markets have responded to global crises, wars, and significant political instability over time.

🧠 Use Cases:

Historical backtesting: Understand how market responded to past geopolitical shocks.

Contextual analysis: Add macro context to technical setups.

🗓️ List of Geopolitical Tension Events in the Script

Date Event Title Description

1914-07-28 WWI Begins Outbreak of World War I following the assassination of Archduke Franz Ferdinand.

1929-10-24 Wall Street Crash Black Thursday, the start of the 1929 stock market crash.

1939-09-01 WWII Begins Germany invades Poland, starting World War II.

1941-12-07 Pearl Harbor Japanese attack on Pearl Harbor; U.S. enters WWII.

1945-08-06 Hiroshima Bombing First atomic bomb dropped on Hiroshima by the U.S.

1950-06-25 Korean War Begins North Korea invades South Korea.

1962-10-16 Cuban Missile Crisis 13-day standoff between the U.S. and USSR over missiles in Cuba.

1973-10-06 Yom Kippur War Egypt and Syria launch surprise attack on Israel.

1979-11-04 Iran Hostage Crisis U.S. Embassy in Tehran seized; 52 hostages taken.

1990-08-02 Gulf War Begins Iraq invades Kuwait, triggering U.S. intervention.

2001-09-11 9/11 Attacks Coordinated terrorist attacks on the U.S.

2003-03-20 Iraq War Begins U.S.-led invasion of Iraq to remove Saddam Hussein.

2008-09-15 Lehman Collapse Bankruptcy of Lehman Brothers; peak of global financial crisis.

2014-03-01 Crimea Crisis Russia annexes Crimea from Ukraine.

2020-01-03 Soleimani Strike U.S. drone strike kills Iranian General Qasem Soleimani.

2022-02-24 Ukraine Invasion Russia launches full-scale invasion of Ukraine.

2023-10-07 Hamas-Israel War Hamas launches attack on Israel, sparking war in Gaza.

2024-01-12 Red Sea Crisis Houthis attack ships in Red Sea, prompting Western naval response.

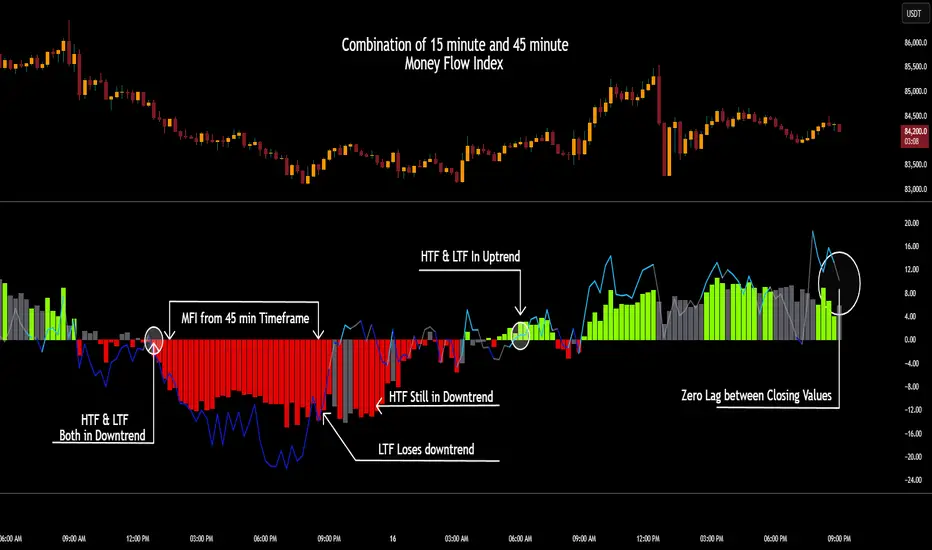

Day of Week and HTF Period SeparatorDay of Week & HTF Period Separator

A minimalist Pine Script indicator that adds clear, time-based separators and labels to intraday charts for better structure and analysis.

Key Features

• Day Labels

• Displays abbreviated weekday names (MON, TUE, WED, etc.) at a user-defined hour

• Custom text color and position

• Limits display to the most recent 28 days for a clean view

• Time Separators

• Daily: Vertical line at 00:00 each trading day

• 4-Hour: Lines at 00:00, 04:00, 08:00, 12:00, 16:00, 20:00

• Hourly: Divisions at every hour for detailed timing

• Customization

• Individual color picker for each separator type

• Choose line style: Solid, Dashed or Dotted

• Enable or disable any separator or label independently

• Smart limits to avoid clutter on extended history

• Smart Behavior

• Active only on intraday timeframes

• Projects upcoming separators into the future for planning

• Automatically caps historical plotting for performance

• Lines extend across full visible price range

Perfect for traders who need distinct session breaks, precise time-based zoning and an organized chart layout.

Inputs

• Show Day Labels (true/false)

• Label Hour (0–23)

• Day Label Color

• Show Daily Separators (true/false)

• Show 4H Separators (true/false)

• Show 1H Separators (true/false)

• Daily Line Color, Style

• 4H Line Color, Style

• Hourly Line Color, Style

• Max Days to Display

Enhance your intraday analysis with clean, customizable time markers. 👁

Reintegration OPR zone 9h30📝 Indicator Description (for TradingView):

Name: Reintegration OPR Zone – 9:30 AM EST (UTC-4)

Purpose:

This indicator is designed for US indices like NAS100, US30, or SPX500. It helps identify potential false breakouts or retests by tracking when the price re-enters the Opening Price Range (OPR) after an initial breakout.

🔍 How it works:

At 9:30 AM New York time (UTC-4), the script captures the high and low of the first 15-minute candle (which is key for the US session open).

It then draws a horizontal box (rectangle) from the high to the low of that candle.

The box extends horizontally for 7 hours (28 candles on a 15-minute chart).

The script tracks if price:

Breaks above or below the OPR zone

Then re-enters the zone (a potential "fakeout" or "retest" signal)

No label or text is displayed on the chart (you requested it to be hidden).

🕒 Timeframe:

Designed for the 15-minute chart (M15)

Assumes New York session open at 9:30 AM EST (UTC-4)

Stochastic w/ Crossovers and Deadspace FilterThis is my extremely useful modification of the classic Stochastic indicator. It includes clear signals of crossovers and crossunders of the K/D lines.

Additionally, I added a "deadspace" filter to remove plotting of signals in the middle of the range, which tend to be misleading.

This can be incredibly useful to find entries and trends, especially when using 2 instances of this indicator at different lengths (such as one of 14,1,3 and another of 28,3,6).

The deadspace filter works based on the middle line, so a value of 20 will not plot any crossovers between 30-70.

CSCMultiTimeframeToolsLibrary "CSCMultiTimeframeTools"

Calculates instant higher timeframe values for higher timeframe analysis with zero lag.

getAdjustedLookback(current_tf_minutes, higher_tf_minutes, length)

Calculate adjusted lookback period for higher timeframe conversion.

Parameters:

current_tf_minutes (int) : Current chart timeframe in minutes (e.g., 5 for 5m).

higher_tf_minutes (int) : Target higher timeframe in minutes (e.g., 15 for 15m).

length (int) : Base length value (e.g., 14 for RSI/MFI).

Returns: Adjusted lookback period (length × multiplier).

Purpose and Benefits of the TimeframeTools Library

This library is designed to solve a critical pain point for traders who rely on higher timeframe (HTF) indicator values while analyzing lower timeframe (LTF) charts. Traditional methods require waiting for multiple candles to close—for example, to see a 1-hour RSI on a 5-minute chart, you’d need 12 closed candles (5m × 12 = 60m) before the value updates. This lag means missed opportunities, delayed signals, and inefficient decision-making.

Why Traders Need This

Whether you’re scalping (5M/15M) or swing trading (1H/4H), this library bridges the gap between timeframes, giving you HTF context in real time—so you can act faster, with confidence.

How This Library Eliminates the Waiting Game

By dynamically calculating the adjusted lookback period, the library allows:

Real-time HTF values on LTF charts – No waiting for candle closes.

Accurate conversions – A 14-period RSI on a 1-hour chart translates to 168 periods (14 × 12) on a 5-minute chart, ensuring mathematical precision.

Flexible application – Works with common indicators like RSI, MFI, CCI, and moving averages (though confirmations should be done before publishing under your own secondary use).

Key Advantages Over Manual Methods

Speed: Instantly reflects HTF values without waiting for candle resolutions.

Adaptability: Adjusts automatically if the user changes timeframes or lengths.

Consistency: Removes human error in manual period calculations.

Limitations to Note

Not a magic bullet – While it solves the lag issue, traders should still:

Validate signals with price action or additional confirmations.

Be mindful of extreme lookback lengths (e.g., a 200-period daily SMA on a 1-minute chart requires 28,800 periods, which may strain performance).

Intrinsic Event (Multi DC OS)Overview

This indicator implements an event-based approach to analyze price movements in the foreign exchange market, inspired by the intrinsic time framework introduced in Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller et al. (1995). It identifies significant price events using an intrinsic time perspective and supports multi-agent analysis to reflect the heterogeneous nature of financial markets. The script plots these events as lines and labels on the chart, offering a visual tool for traders to understand market dynamics at different scales.

Key Features

Intrinsic Events : The indicator detects directional change (DC) and overshoot (OS) events based on user-defined thresholds (delta), aligning with the paper’s concept of intrinsic time (Section 6). Intrinsic time redefines time based on market activity, expanding during volatile periods and contracting during inactive ones, rather than relying on a physical clock.

Multi-Agent Analysis : Supports up to five agents, each with its own threshold and color settings, reflecting the heterogeneous market hypothesis (Section 5). This allows the indicator to capture the perspectives of market participants with different time horizons, such as short-term FX dealers and long-term central banks.

How It Works

Intrinsic Events Detection : The script identifies two types of events using intrinsic time principles:

Directional Change (DC) : Triggered when the price reverses by the threshold (delta) against the current trend (e.g., a drop by delta in an uptrend signals a "Down DC").

Overshoot (OS) : Occurs when the price continues in the trend direction by the threshold (e.g., a rise by delta in an uptrend signals an "Up OS").

DC events are plotted as solid lines, and OS events as dashed lines, with labels like "Up DC" or "OS Down" for clarity. The label style adjusts based on the trend to ensure visibility.

Multi-Agent Setup : Each agent operates independently with its own threshold, mimicking market participants with varying time horizons (Section 5). Smaller thresholds detect frequent, short-term events, while larger thresholds capture broader, long-term movements.

Settings

Each agent can be configured with:

Enable Agent : Toggle the agent on or off.

Threshold (%) : The percentage threshold (delta) for detecting DC and OS events (default values: 0.1%, 0.2%, 0.5%, 1%, 2% for agents 1–5).

Up Mode Color : Color for lines and labels in up mode (DC events).

Down Mode Color : Color for lines and labels in down mode (OS events).

Usage Notes

This indicator is designed for the foreign exchange market, leveraging its high liquidity, as noted in the paper (Section 1). Adjust the threshold values based on the instrument’s volatility—higher volatility leads to more intrinsic events (Section 4). It can be adapted to other markets where event-based analysis applies.

Reference

The methodology is based on:

Fractals and Intrinsic Time - A Challenge to Econometricians by U. A. Müller, M. M. Dacorogna, R. D. Davé, O. V. Pictet, R. B. Olsen, and J. R. Ward (June 28, 1995). Olsen & Associates Preprint.

Vulkan Profit

Overview

The Vulkan Profit indicator is a trend-following tool that identifies potential entry and exit points by monitoring the relationship between short-term and long-term moving averages. It generates clear buy and sell signals when specific moving average conditions align, making it useful for traders looking to confirm trend changes across multiple timeframes.

How It Works

The indicator utilizes four different moving averages:

Fast WMA (period 3) - A highly responsive weighted moving average

Medium WMA (period 8) - A less sensitive weighted moving average

Fast EMA (period 18) - A responsive exponential moving average

Slow EMA (period 28) - A slower exponential moving average

These moving averages are grouped into two categories:

Short-term MAs: Fast WMA and Medium WMA

Long-term MAs: Fast EMA and Slow EMA

Signal Generation Logic

The Vulkan Profit indicator generates signals based on the relative positions of these moving averages:

Buy Signal (Green Triangle)

A buy signal appears when the minimum value of the short-term MAs becomes greater than the maximum value of the long-term MAs. In other words, when both short-term MAs cross above both long-term MAs.

Sell Signal (Red Triangle)

A sell signal appears when the maximum value of the short-term MAs becomes less than the minimum value of the long-term MAs. In other words, when both short-term MAs cross below both long-term MAs.

Visual Components

Moving Averages - All four moving averages can be displayed or hidden

Signal Arrows - Green triangles for buy signals, red triangles for sell signals

Colored Line - A line that changes color based on the current market stance (green for bullish, red for bearish)

Customization Options

The indicator offers several customization settings:

Toggle the visibility of moving averages

Toggle the visibility of buy/sell signals

Adjust the color, width, and position of the signal line

Choose between different line styles (Line, Stepline, Histogram)

Practical Trading Applications

Trend Identification: The relative positioning of all moving averages helps identify the current market trend

Entry/Exit Points: The buy and sell signals can be used as potential entry and exit points

Trend Confirmation: The colored line provides ongoing confirmation of the trend direction

Filter: Can be used in conjunction with other indicators as a trend filter

Trading Strategy Suggestions

Trend Following: Enter long positions on buy signals and exit on sell signals during trending markets

Confirmation Tool: Use the signals to confirm trades identified by other indicators

Timeframe Analysis: Apply the indicator across multiple timeframes for stronger confirmation

Risk Management: Place stop-loss orders below recent swing lows for long positions and above recent swing highs for short positions

Tips for Best Results

The indicator performs best in trending markets and may generate false signals in ranging or highly volatile markets

Consider the broader market context before taking trades based solely on these signals

Use appropriate position sizing and risk management regardless of the indicator's signals

The longer timeframes generally produce more reliable signals with fewer false positives

The Vulkan Profit indicator combines the responsiveness of short-term averages with the stability of long-term averages to capture significant trend changes while filtering out minor price fluctuations.

Optimized WPR Strategy with Filters (Debug)Identifying Market Trends:

The 200-period EMA is used to determine the short-term trend of the market.

When the price is above the 200-period EMA, it suggests a potential bullish market and an uptrend, and the strategy will only look for buying opportunities.

When the price is below the 200-period EMA, it suggests a potential bearish market and a downtrend, and the strategy will only look for selling opportunities.

When the 200-period EMA intersects with the price, it indicates that the market may be in a directionless consolidation phase.

Identifying Potential Reversal Points:

The strategy employs two Williams %R (WPR) indicators: one with a 9-period (fast WPR) and another with a 28-period (slow WPR).

WPR is a momentum indicator used to identify overbought and oversold conditions in the market. Its value oscillates between -100 and 0, with values near -100 indicating oversold conditions and values near 0 indicating overbought conditions.

In an uptrend (when the price is above the 200 EMA), the strategy seeks buying opportunities when both WPR indicators cross above -80 (the oversold zone) from below. This is considered a bullish signal, suggesting the market may be about to rebound. Sell signals are ignored at this time.

In a downtrend (when the price is below the 200 EMA), the strategy seeks selling opportunities when both WPR indicators cross below -20 (the overbought zone) from above. This is considered a bearish signal, suggesting the market may be about to reverse downward. Buy signals are ignored at this time.

Summary:

In summary, this strategy first uses the 200-period EMA to determine the overall trend direction of the market. Then, within the confirmed trend direction, it utilizes the simultaneous crossing of the overbought or oversold zones by the dual WPR indicators to identify potential reversal points as entry signals for trading. The strategy emphasizes that trading signals are only valid when both WPR indicators meet the conditions.

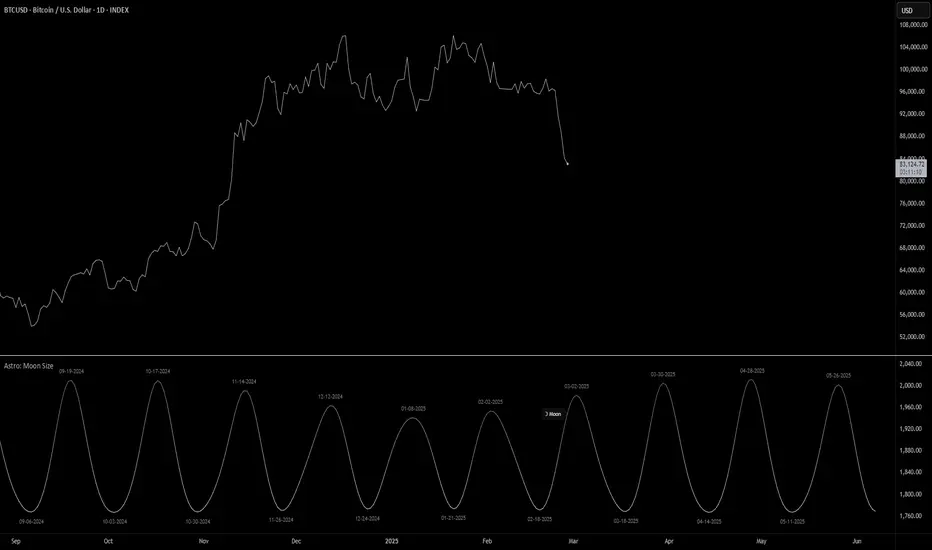

Astro: Moon SizeThe Astro: Moon Size indicator, built using AstroLib , calculates the distance and visualizes the apparent size of the Moon based on astronomical positioning. This script is tailored for the 1D timeframe and provides insights into lunar perigees (closest approach) and apogees (farthest distance), making it useful for astrologically-informed trading strategies.

New Astro Indicators Feature:

By setting the Julian Date to X number of days in the future, and offsetting the plot by X number of bars accordingly, it is now possible to visualize future projections of TradingView indicators that reference the AstroLib . This feature has been long requested and is far overdue, so thank you to everyone who pushed for this feature release. Enjoy, time travelers from the future!!

Key Features:

Moon Size Calculation: Uses Julian Date (J2000) conversion and AstroLib functions to determine the Moon's apparent distance.

Future Projection: Displays the Moon's distance from 28 up to 500 days ahead, with color gradients indicating proximity/size.

Pivot Identification: Marks local maxima (apogees) and minima (perigees) with labeled date stamps for easy reference.

Dynamic Labeling: Adapts label positioning and size based on the Moon's current trend and relative size.

Usage Notes:

⚠️ Timeframe Restriction: For now, the script only functions on the 1D timeframe and will prompt an error otherwise.

⚠️ Asset Restriction: This script is meant to be loaded on charts for assets that trade 24/7, like BTCUSD historical index.

G-VIDYA | QuantEdgeBIntroducing G-VIDYA by QuantEdgeB

____

🔹 Overview

The G-VIDYA | QuantEdgeB is a dynamic trend-following indicator that enhances market trend detection using Gaussian smoothing and an adaptive Variable Index Dynamic Average (VIDYA). It is designed to reduce noise, improve responsiveness, and adapt to volatility, making it a powerful tool for traders looking to capture long-term trends efficiently.

By integrating ATR-based filtering, the indicator creates a dynamic support and resistance band around VIDYA, allowing for more accurate trend confirmations. Additionally, traders have the option to enable trade labels for clearer visual signals.

This indicator is well-suited for medium to long-term trend traders, combining mathematical precision with market adaptability for robust trading strategies.

_____

🚀 Key Features

1. Gaussian Smoothing → Reduces market noise and smoothens price action.

2. VIDYA Adaptive Calculation → Adjusts dynamically based on market volatility.

3. ATR-Based Filtering → Creates a volatility-driven range around VIDYA.

4. Dynamic Trend Confirmation → Identifies bullish and bearish momentum shifts.

5. Trade Labels (Optional) → Can display Long/Cash labels on chart for better clarity.

6. Customizable Color Modes → Offers multiple visual themes for personalized experience.

7. Automated Alerts → Sends buy/sell alerts for crossover trend changes.

_____

📊 How It Works

1. Gaussian Smoothing is applied to the closing price to remove noise and improve signal clarity.

2. VIDYA Calculation dynamically adjusts to price movements, making it more reactive during high-volatility periods and stable in low-volatility environments.

3. ATR-Based Filtering establishes a dynamic range (Upper & Lower ATR Bands) around VIDYA:

- If price breaks above the upper ATR band, it signals a potential long trend.

- If price breaks below the lower ATR band, it signals a potential short trend.

4. The indicator assigns color-coded candles based on trend direction:

- Bullish Trend → Blue/Green (Uptrend)

- Bearish Trend → Red/Maroon (Downtrend)

5. Labels & Alerts (Optional)

- Users can activate Long/Cash labels to mark buy/sell opportunities.

- Built-in alerts trigger automatic notifications when trend direction changes.

_____

🎨 Visual Representation

- VIDYA Line → A smooth, trend-following line that dynamically adjusts to market conditions.

- Upper & Lower ATR Bands → Establishes a volatility-based corridor around VIDYA.

- Bar Coloring → Candles change color according to the detected trend.

- Long/Short Labels (Optional) → Displays trade entry/exit signals (can be enabled/disabled).

- Alerts → Generates trade notifications based on trend reversals.

______

⚙️ Default Settings

- Gaussian Smoothing

- Length: 4

- Sigma: 2.0

- VIDYA Settings

- VIDYA Length: 46

- Standard Deviation Length: 28

- ATR Settings

- ATR Length: 14

- ATR Multiplier: 1.3

____

💡 Who Should Use It?

✅ Trend Traders → Those who rely on medium-to-long-term trends for trading decisions.

✅ Swing Traders → Ideal for traders who want to capture trend reversals and ride momentum.

✅ Quantitative Analysts → Provides statistically driven smoothing and adaptive trend detection.

✅ Risk-Averse Traders → ATR filtering helps manage market volatility effectively.

_____

Conclusion

The G-VIDYA | QuantEdgeB is an advanced trend-following indicator that combines Gaussian smoothing, adaptive VIDYA filtering, and ATR-based dynamic trend analysis to deliver robust and reliable trade signals.

✅ Key Takeaways

📌 Adaptive & Dynamic: Adjusts to market conditions, making it effective for trend-following strategies.

📌 Noise Reduction: Gaussian smoothing helps filter out short-term fluctuations, improving signal clarity.

📌 Volatility Awareness: ATR-based filtering ensures better handling of market swings and trend reversals.

By blending mathematical precision and quantitative market analysis, G-VIDYA | QuantEdgeB offers a powerful edge in trend trading strategies.

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

ValueAtTime█ OVERVIEW

This library is a Pine Script® programming tool for accessing historical values in a time series using UNIX timestamps . Its data structure and functions index values by time, allowing scripts to retrieve past values based on absolute timestamps or relative time offsets instead of relying on bar index offsets.

█ CONCEPTS

UNIX timestamps

In Pine Script®, a UNIX timestamp is an integer representing the number of milliseconds elapsed since January 1, 1970, at 00:00:00 UTC (the UNIX Epoch ). The timestamp is a unique, absolute representation of a specific point in time. Unlike a calendar date and time, a UNIX timestamp's meaning does not change relative to any time zone .

This library's functions process series values and corresponding UNIX timestamps in pairs , offering a simplified way to identify values that occur at or near distinct points in time instead of on specific bars.

Storing and retrieving time-value pairs

This library's `Data` type defines the structure for collecting time and value information in pairs. Objects of the `Data` type contain the following two fields:

• `times` – An array of "int" UNIX timestamps for each recorded value.

• `values` – An array of "float" values for each saved timestamp.

Each index in both arrays refers to a specific time-value pair. For instance, the `times` and `values` elements at index 0 represent the first saved timestamp and corresponding value. The library functions that maintain `Data` objects queue up to one time-value pair per bar into the object's arrays, where the saved timestamp represents the bar's opening time .

Because the `times` array contains a distinct UNIX timestamp for each item in the `values` array, it serves as a custom mapping for retrieving saved values. All the library functions that return information from a `Data` object use this simple two-step process to identify a value based on time:

1. Perform a binary search on the `times` array to find the earliest saved timestamp closest to the specified time or offset and get the element's index.

2. Access the element from the `values` array at the retrieved index, returning the stored value corresponding to the found timestamp.

Value search methods

There are several techniques programmers can use to identify historical values from corresponding timestamps. This library's functions include three different search methods to locate and retrieve values based on absolute times or relative time offsets:

Timestamp search

Find the value with the earliest saved timestamp closest to a specified timestamp.

Millisecond offset search

Find the value with the earliest saved timestamp closest to a specified number of milliseconds behind the current bar's opening time. This search method provides a time-based alternative to retrieving historical values at specific bar offsets.

Period offset search

Locate the value with the earliest saved timestamp closest to a defined period offset behind the current bar's opening time. The function calculates the span of the offset based on a period string . The "string" must contain one of the following unit tokens:

• "D" for days

• "W" for weeks

• "M" for months

• "Y" for years

• "YTD" for year-to-date, meaning the time elapsed since the beginning of the bar's opening year in the exchange time zone.

The period string can include a multiplier prefix for all supported units except "YTD" (e.g., "2W" for two weeks).

Note that the precise span covered by the "M", "Y", and "YTD" units varies across time. The "1M" period can cover 28, 29, 30, or 31 days, depending on the bar's opening month and year in the exchange time zone. The "1Y" period covers 365 or 366 days, depending on leap years. The "YTD" period's span changes with each new bar, because it always measures the time from the start of the current bar's opening year.

█ CALCULATIONS AND USE

This library's functions offer a flexible, structured approach to retrieving historical values at or near specific timestamps, millisecond offsets, or period offsets for different analytical needs.

See below for explanations of the exported functions and how to use them.

Retrieving single values

The library includes three functions that retrieve a single stored value using timestamp, millisecond offset, or period offset search methods:

• `valueAtTime()` – Locates the saved value with the earliest timestamp closest to a specified timestamp.

• `valueAtTimeOffset()` – Finds the saved value with the earliest timestamp closest to the specified number of milliseconds behind the current bar's opening time.

• `valueAtPeriodOffset()` – Finds the saved value with the earliest timestamp closest to the period-based offset behind the current bar's opening time.

Each function has two overloads for advanced and simple use cases. The first overload searches for a value in a user-specified `Data` object created by the `collectData()` function (see below). It returns a tuple containing the found value and the corresponding timestamp.

The second overload maintains a `Data` object internally to store and retrieve values for a specified `source` series. This overload returns a tuple containing the historical `source` value, the corresponding timestamp, and the current bar's `source` value, making it helpful for comparing past and present values from requested contexts.

Retrieving multiple values

The library includes the following functions to retrieve values from multiple historical points in time, facilitating calculations and comparisons with values retrieved across several intervals:

• `getDataAtTimes()` – Locates a past `source` value for each item in a `timestamps` array. Each retrieved value's timestamp represents the earliest time closest to one of the specified timestamps.

• `getDataAtTimeOffsets()` – Finds a past `source` value for each item in a `timeOffsets` array. Each retrieved value's timestamp represents the earliest time closest to one of the specified millisecond offsets behind the current bar's opening time.

• `getDataAtPeriodOffsets()` – Finds a past value for each item in a `periods` array. Each retrieved value's timestamp represents the earliest time closest to one of the specified period offsets behind the current bar's opening time.

Each function returns a tuple with arrays containing the found `source` values and their corresponding timestamps. In addition, the tuple includes the current `source` value and the symbol's description, which also makes these functions helpful for multi-interval comparisons using data from requested contexts.

Processing period inputs

When writing scripts that retrieve historical values based on several user-specified period offsets, the most concise approach is to create a single text input that allows users to list each period, then process the "string" list into an array for use in the `getDataAtPeriodOffsets()` function.

This library includes a `getArrayFromString()` function to provide a simple way to process strings containing comma-separated lists of periods. The function splits the specified `str` by its commas and returns an array containing every non-empty item in the list with surrounding whitespaces removed. View the example code to see how we use this function to process the value of a text area input .

Calculating period offset times

Because the exact amount of time covered by a specified period offset can vary, it is often helpful to verify the resulting times when using the `valueAtPeriodOffset()` or `getDataAtPeriodOffsets()` functions to ensure the calculations work as intended for your use case.

The library's `periodToTimestamp()` function calculates an offset timestamp from a given period and reference time. With this function, programmers can verify the time offsets in a period-based data search and use the calculated offset times in additional operations.

For periods with "D" or "W" units, the function calculates the time offset based on the absolute number of milliseconds the period covers (e.g., `86400000` for "1D"). For periods with "M", "Y", or "YTD" units, the function calculates an offset time based on the reference time's calendar date in the exchange time zone.

Collecting data

All the `getDataAt*()` functions, and the second overloads of the `valueAt*()` functions, collect and maintain data internally, meaning scripts do not require a separate `Data` object when using them. However, the first overloads of the `valueAt*()` functions do not collect data, because they retrieve values from a user-specified `Data` object.

For cases where a script requires a separate `Data` object for use with these overloads or other custom routines, this library exports the `collectData()` function. This function queues each bar's `source` value and opening timestamp into a `Data` object and returns the object's ID.

This function is particularly useful when searching for values from a specific series more than once. For instance, instead of using multiple calls to the second overloads of `valueAt*()` functions with the same `source` argument, programmers can call `collectData()` to store each bar's `source` and opening timestamp, then use the returned `Data` object's ID in calls to the first `valueAt*()` overloads to reduce memory usage.

The `collectData()` function and all the functions that collect data internally include two optional parameters for limiting the saved time-value pairs to a sliding window: `timeOffsetLimit` and `timeframeLimit`. When either has a non-na argument, the function restricts the collected data to the maximum number of recent bars covered by the specified millisecond- and timeframe-based intervals.

NOTE : All calls to the functions that collect data for a `source` series can execute up to once per bar or realtime tick, because each stored value requires a unique corresponding timestamp. Therefore, scripts cannot call these functions iteratively within a loop . If a call to these functions executes more than once inside a loop's scope, it causes a runtime error.

█ EXAMPLE CODE

The example code at the end of the script demonstrates one possible use case for this library's functions. The code retrieves historical price data at user-specified period offsets, calculates price returns for each period from the retrieved data, and then populates a table with the results.

The example code's process is as follows:

1. Input a list of periods – The user specifies a comma-separated list of period strings in the script's "Period list" input (e.g., "1W, 1M, 3M, 1Y, YTD"). Each item in the input list represents a period offset from the latest bar's opening time.

2. Process the period list – The example calls `getArrayFromString()` on the first bar to split the input list by its commas and construct an array of period strings.

3. Request historical data – The code uses a call to `getDataAtPeriodOffsets()` as the `expression` argument in a request.security() call to retrieve the closing prices of "1D" bars for each period included in the processed `periods` array.

4. Display information in a table – On the latest bar, the code uses the retrieved data to calculate price returns over each specified period, then populates a two-row table with the results. The cells for each return percentage are color-coded based on the magnitude and direction of the price change. The cells also include tooltips showing the compared daily bar's opening date in the exchange time zone.

█ NOTES

• This library's architecture relies on a user-defined type (UDT) for its data storage format. UDTs are blueprints from which scripts create objects , i.e., composite structures with fields containing independent values or references of any supported type.

• The library functions search through a `Data` object's `times` array using the array.binary_search_leftmost() function, which is more efficient than looping through collected data to identify matching timestamps. Note that this built-in works only for arrays with elements sorted in ascending order .

• Each function that collects data from a `source` series updates the values and times stored in a local `Data` object's arrays. If a single call to these functions were to execute in a loop , it would store multiple values with an identical timestamp, which can cause erroneous search behavior. To prevent looped calls to these functions, the library uses the `checkCall()` helper function in their scopes. This function maintains a counter that increases by one each time it executes on a confirmed bar. If the count exceeds the total number of bars, indicating the call executes more than once in a loop, it raises a runtime error .

• Typically, when requesting higher-timeframe data with request.security() while using barmerge.lookahead_on as the `lookahead` argument, the `expression` argument should be offset with the history-referencing operator to prevent lookahead bias on historical bars. However, the call in this script's example code enables lookahead without offsetting the `expression` because the script displays results only on the last historical bar and all realtime bars, where there is no future data to leak into the past. This call ensures the displayed results use the latest data available from the context on realtime bars.

Look first. Then leap.

█ EXPORTED TYPES

Data

A structure for storing successive timestamps and corresponding values from a dataset.

Fields:

times (array) : An "int" array containing a UNIX timestamp for each value in the `values` array.

values (array) : A "float" array containing values corresponding to the timestamps in the `times` array.

█ EXPORTED FUNCTIONS

getArrayFromString(str)

Splits a "string" into an array of substrings using the comma (`,`) as the delimiter. The function trims surrounding whitespace characters from each substring, and it excludes empty substrings from the result.

Parameters:

str (series string) : The "string" to split into an array based on its commas.

Returns: (array) An array of trimmed substrings from the specified `str`.

periodToTimestamp(period, referenceTime)

Calculates a UNIX timestamp representing the point offset behind a reference time by the amount of time within the specified `period`.

Parameters:

period (series string) : The period string, which determines the time offset of the returned timestamp. The specified argument must contain a unit and an optional multiplier (e.g., "1Y", "3M", "2W", "YTD"). Supported units are:

- "Y" for years.

- "M" for months.

- "W" for weeks.

- "D" for days.

- "YTD" (Year-to-date) for the span from the start of the `referenceTime` value's year in the exchange time zone. An argument with this unit cannot contain a multiplier.

referenceTime (series int) : The millisecond UNIX timestamp from which to calculate the offset time.

Returns: (int) A millisecond UNIX timestamp representing the offset time point behind the `referenceTime`.

collectData(source, timeOffsetLimit, timeframeLimit)

Collects `source` and `time` data successively across bars. The function stores the information within a `Data` object for use in other exported functions/methods, such as `valueAtTimeOffset()` and `valueAtPeriodOffset()`. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

source (series float) : The source series to collect. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: (Data) A `Data` object containing collected `source` values and corresponding timestamps over the allowed time range.

method valueAtTime(data, timestamp)

(Overload 1 of 2) Retrieves value and time data from a `Data` object's fields at the index of the earliest timestamp closest to the specified `timestamp`. Callable as a method or a function.

Parameters:

data (series Data) : The `Data` object containing the collected time and value data.

timestamp (series int) : The millisecond UNIX timestamp to search. The function returns data for the earliest saved timestamp that is closest to the value.

Returns: ( ) A tuple containing the following data from the `Data` object:

- The stored value corresponding to the identified timestamp ("float").

- The earliest saved timestamp that is closest to the specified `timestamp` ("int").

valueAtTime(source, timestamp, timeOffsetLimit, timeframeLimit)

(Overload 2 of 2) Retrieves `source` and time information for the earliest bar whose opening timestamp is closest to the specified `timestamp`. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

source (series float) : The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timestamp (series int) : The millisecond UNIX timestamp to search. The function returns data for the earliest bar whose timestamp is closest to the value.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : (simple string) Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple containing the following data:

- The `source` value corresponding to the identified timestamp ("float").

- The earliest bar's timestamp that is closest to the specified `timestamp` ("int").

- The current bar's `source` value ("float").

method valueAtTimeOffset(data, timeOffset)

(Overload 1 of 2) Retrieves value and time data from a `Data` object's fields at the index of the earliest saved timestamp closest to `timeOffset` milliseconds behind the current bar's opening time. Callable as a method or a function.

Parameters:

data (series Data) : The `Data` object containing the collected time and value data.

timeOffset (series int) : The millisecond offset behind the bar's opening time. The function returns data for the earliest saved timestamp that is closest to the calculated offset time.

Returns: ( ) A tuple containing the following data from the `Data` object:

- The stored value corresponding to the identified timestamp ("float").

- The earliest saved timestamp that is closest to `timeOffset` milliseconds before the current bar's opening time ("int").

valueAtTimeOffset(source, timeOffset, timeOffsetLimit, timeframeLimit)

(Overload 2 of 2) Retrieves `source` and time information for the earliest bar whose opening timestamp is closest to `timeOffset` milliseconds behind the current bar's opening time. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

source (series float) : The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timeOffset (series int) : The millisecond offset behind the bar's opening time. The function returns data for the earliest bar's timestamp that is closest to the calculated offset time.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple containing the following data:

- The `source` value corresponding to the identified timestamp ("float").

- The earliest bar's timestamp that is closest to `timeOffset` milliseconds before the current bar's opening time ("int").

- The current bar's `source` value ("float").

method valueAtPeriodOffset(data, period)

(Overload 1 of 2) Retrieves value and time data from a `Data` object's fields at the index of the earliest timestamp closest to a calculated offset behind the current bar's opening time. The calculated offset represents the amount of time covered by the specified `period`. Callable as a method or a function.

Parameters:

data (series Data) : The `Data` object containing the collected time and value data.

period (series string) : The period string, which determines the calculated time offset. The specified argument must contain a unit and an optional multiplier (e.g., "1Y", "3M", "2W", "YTD"). Supported units are:

- "Y" for years.

- "M" for months.

- "W" for weeks.

- "D" for days.

- "YTD" (Year-to-date) for the span from the start of the current bar's year in the exchange time zone. An argument with this unit cannot contain a multiplier.

Returns: ( ) A tuple containing the following data from the `Data` object:

- The stored value corresponding to the identified timestamp ("float").

- The earliest saved timestamp that is closest to the calculated offset behind the bar's opening time ("int").

valueAtPeriodOffset(source, period, timeOffsetLimit, timeframeLimit)

(Overload 2 of 2) Retrieves `source` and time information for the earliest bar whose opening timestamp is closest to a calculated offset behind the current bar's opening time. The calculated offset represents the amount of time covered by the specified `period`. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

source (series float) : The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

period (series string) : The period string, which determines the calculated time offset. The specified argument must contain a unit and an optional multiplier (e.g., "1Y", "3M", "2W", "YTD"). Supported units are:

- "Y" for years.

- "M" for months.

- "W" for weeks.

- "D" for days.

- "YTD" (Year-to-date) for the span from the start of the current bar's year in the exchange time zone. An argument with this unit cannot contain a multiplier.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple containing the following data:

- The `source` value corresponding to the identified timestamp ("float").

- The earliest bar's timestamp that is closest to the calculated offset behind the current bar's opening time ("int").

- The current bar's `source` value ("float").

getDataAtTimes(timestamps, source, timeOffsetLimit, timeframeLimit)

Retrieves `source` and time information for each bar whose opening timestamp is the earliest one closest to one of the UNIX timestamps specified in the `timestamps` array. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

timestamps (array) : An array of "int" values representing UNIX timestamps. The function retrieves `source` and time data for each element in this array.

source (series float) : The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple of the following data:

- An array containing a `source` value for each identified timestamp (array).

- An array containing an identified timestamp for each item in the `timestamps` array (array).

- The current bar's `source` value ("float").

- The symbol's description from `syminfo.description` ("string").

getDataAtTimeOffsets(timeOffsets, source, timeOffsetLimit, timeframeLimit)

Retrieves `source` and time information for each bar whose opening timestamp is the earliest one closest to one of the time offsets specified in the `timeOffsets` array. Each offset in the array represents the absolute number of milliseconds behind the current bar's opening time. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

timeOffsets (array) : An array of "int" values representing the millisecond time offsets used in the search. The function retrieves `source` and time data for each element in this array. For example, the array ` ` specifies that the function returns data for the timestamps closest to one day and one week behind the current bar's opening time.

source (float) : (series float) The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple of the following data:

- An array containing a `source` value for each identified timestamp (array).

- An array containing an identified timestamp for each offset specified in the `timeOffsets` array (array).

- The current bar's `source` value ("float").

- The symbol's description from `syminfo.description` ("string").

getDataAtPeriodOffsets(periods, source, timeOffsetLimit, timeframeLimit)

Retrieves `source` and time information for each bar whose opening timestamp is the earliest one closest to a calculated offset behind the current bar's opening time. Each calculated offset represents the amount of time covered by a period specified in the `periods` array. Any call to this function cannot execute more than once per bar or realtime tick.

Parameters:

periods (array) : An array of period strings, which determines the time offsets used in the search. The function retrieves `source` and time data for each element in this array. For example, the array ` ` specifies that the function returns data for the timestamps closest to one day, week, and month behind the current bar's opening time. Each "string" in the array must contain a unit and an optional multiplier. Supported units are:

- "Y" for years.

- "M" for months.

- "W" for weeks.

- "D" for days.

- "YTD" (Year-to-date) for the span from the start of the current bar's year in the exchange time zone. An argument with this unit cannot contain a multiplier.

source (float) : (series float) The source series to analyze. The function stores each value in the series with an associated timestamp representing its corresponding bar's opening time.

timeOffsetLimit (simple int) : Optional. A time offset (range) in milliseconds. If specified, the function limits the collected data to the maximum number of bars covered by the range, with a minimum of one bar. If the call includes a non-empty `timeframeLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

timeframeLimit (simple string) : Optional. A valid timeframe string. If specified and not empty, the function limits the collected data to the maximum number of bars covered by the timeframe, with a minimum of one bar. If the call includes a non-na `timeOffsetLimit` value, the function limits the data using the largest number of bars covered by the two ranges. The default is `na`.

Returns: ( ) A tuple of the following data:

- An array containing a `source` value for each identified timestamp (array).

- An array containing an identified timestamp for each period specified in the `periods` array (array).

- The current bar's `source` value ("float").

- The symbol's description from `syminfo.description` ("string").

RSI Divergence[UgurTash] – Real-Time📈 RSI Divergence – Real-Time, Adaptive, and Intelligent RSI Divergence Detection

🚀 What Does This Indicator Do?

RSI Divergence is a real-time divergence detection tool that helps traders identify bullish and bearish divergences between price and the Relative Strength Index (RSI). Unlike traditional RSI-based indicators, this script offers:

✅ Real-time detection – No need to wait for bar closes or repainting.

✅ Dynamic time-frame adaptation – The script automatically adjusts RSI settings based on the selected chart time frame.

✅ Multi-layered divergence analysis – Supports short-term, medium-term, and long-term divergence detection with an optional all-term mode that dynamically selects the best configuration.

🛠 How Does It Work?

Pivot-Based Divergence Detection:

The script analyzes pivot points on both price and RSI to determine valid divergences.

Bullish divergence occurs when price forms a lower low but RSI trends higher, indicating potential upward momentum.

Bearish divergence occurs when price forms a higher high but RSI trends lower, signaling possible weakness.

Adaptive RSI Calculation:

The RSI length is dynamically adjusted based on the chosen time frame:

Short-Term: RSI (7) for 1-5 min charts.

Medium-Term: RSI (14) for 15-60 min charts.

Long-Term: RSI (28) for 4H+ charts.

In All-Term Mode, the script automatically determines the best RSI length based on the active chart timeframe.

Smart Visualization & Alerts:

Bullish divergences are marked with green lines & labels.

Bearish divergences are highlighted in red.

Users can customize symbol size, divergence labels, and colors.

Instant alerts notify traders as soon as a divergence is detected.

🎯 How to Use This Indicator?

📌 For Trend Reversals: Look for bullish divergences at key support levels and bearish divergences at resistance zones.

📌 For Trend Continuation: Combine divergence signals with moving averages, volume analysis, or price action strategies to confirm trades.

📌 For Scalping & Swing Trading: Adjust the time-frame settings to match your trading style.

🏆 What Makes This Indicator Original?

🔹 Unlike standard RSI divergence indicators, this script features real-time analysis with no repainting, allowing for instant trading decisions.

🔹 The time-frame adaptive RSI makes it dynamic and suitable for any market condition.

🔹 The multi-term divergence detection offers flexibility, giving traders a precise view of both short-term & long-term market structure.

⚠ Note: No indicator guarantees 100% accuracy. Always use additional confirmations and sound risk management strategies.

If you find this tool useful, don’t forget to support & share! 🚀

Crypto Scanner v4This guide explains a version 6 Pine Script that scans a user-provided list of cryptocurrency tokens to identify high probability tradable opportunities using several technical indicators. The script combines trend, momentum, and volume-based analyses to generate potential buying or selling signals, and it displays the results in a neatly formatted table with alerts for trading setups. Below is a detailed walkthrough of the script’s design, how traders can interpret its outputs, and recommendations for optimizing indicator inputs across different timeframes.

## Overview and Key Components