Multi-Timeframe RSI Table# Multi-Timeframe RSI Table

## Overview

This indicator displays RSI (Relative Strength Index) values across multiple timeframes in a convenient table format, allowing traders to quickly assess momentum conditions across different time horizons without switching charts.

## Features

• *7 Timeframes*: 5m, 15m, 1h, 4h, Daily, Weekly, Monthly

• *Color-coded RSI Values*:

- 🔴 Red: Overbought (≥70)

- 🟢 Green: Oversold (≤30)

- 🟠 Orange: Bullish momentum (50-70)

- 🟡 Yellow: Bearish momentum (30-50)

• *Clean Table Display*: Positioned in top-right corner for easy viewing

• *Customizable Settings*: Adjustable RSI length and overbought/oversold levels

## How to Use

1. Add the indicator to your chart

2. The table automatically displays current RSI values for all timeframes

3. Use color coding to quickly identify:

- *Buying opportunities* when multiple timeframes show green (oversold)

- *Selling opportunities* when multiple timeframes show red (overbought)

- *Trend alignment* when higher timeframes match your trading direction

## Trading Applications

• *Multi-timeframe analysis*: Confirm signals across different time horizons

• *Entry timing*: Find optimal entry points when shorter timeframes align with longer trends

• *Risk management*: Avoid trades when higher timeframes show opposite momentum

• *Swing trading*: Identify when daily/weekly RSI supports your position direction

## Settings

• *RSI Length*: Default 14 periods (standard RSI calculation)

• *Overbought Level*: Default 70 (customizable)

• *Oversold Level*: Default 30 (customizable)

## Best Practices

• Look for alignment across multiple timeframes for stronger signals

• Use higher timeframe RSI to determine overall trend direction

• Combine with price action and support/resistance levels

• Avoid trading against strong momentum shown in higher timeframes

Perfect for day traders, swing traders, and anyone who needs quick multi-timeframe RSI analysis without constantly switching chart timeframes.

Cerca negli script per "30年国债收益率"

Active PMI Support/Resistance Levels [EdgeTerminal]The PMI Support & Resistance indicator revolutionizes traditional technical analysis by using Pointwise Mutual Information (PMI) - a statistical measure from information theory - to objectively identify support and resistance levels. Unlike conventional methods that rely on visual pattern recognition, this indicator provides mathematically rigorous, quantifiable evidence of price levels where significant market activity occurs.

- The Mathematical Foundation: Pointwise Mutual Information

Pointwise Mutual Information measures how much more likely two events are to occur together compared to if they were statistically independent. In our context:

Event A: Volume spikes occurring (high trading activity)

Event B: Price being at specific levels

The PMI formula calculates: PMI = log(P(A,B) / (P(A) × P(B)))

Where:

P(A,B) = Probability of volume spikes occurring at specific price levels

P(A) = Probability of volume spikes occurring anywhere

P(B) = Probability of price being at specific levels

High PMI scores indicate that volume spikes and certain price levels co-occur much more frequently than random chance would predict, revealing genuine support and resistance zones.

- Why PMI Outperforms Traditional Methods

Subjective interpretation: What one trader sees as significant, another might ignore

Confirmation bias: Tendency to see patterns that confirm existing beliefs

Inconsistent criteria: No standardized definition of "significant" volume or price action

Static analysis: Doesn't adapt to changing market conditions

No strength measurement: Can't quantify how "strong" a level truly is

PMI Advantages:

✅ Objective & Quantifiable: Mathematical proof of significance, not visual guesswork

✅ Statistical Rigor: Levels backed by information theory and probability

✅ Strength Scoring: PMI scores rank levels by statistical significance

✅ Adaptive: Automatically adjusts to different market volatility regimes

✅ Eliminates Bias: Computer-calculated, removing human interpretation errors

✅ Market Structure Aware: Reveals the underlying order flow concentrations

- How It Works

Data Processing Pipeline:

Volume Analysis: Identifies volume spikes using configurable thresholds

Price Binning: Divides price range into discrete levels for analysis

Co-occurrence Calculation: Measures how often volume spikes happen at each price level

PMI Computation: Calculates statistical significance for each price level

Level Filtering: Shows only levels exceeding minimum PMI thresholds

Dynamic Updates: Refreshes levels periodically while maintaining historical traces

Visual System:

Current Levels: Bright, thick lines with PMI scores - your actionable levels

Historical Traces: Faded previous levels showing market structure evolution

Strength Tiers: Line styles indicate PMI strength (solid/dashed/dotted)

Color Coding: Green for support, red for resistance

Info Table: Real-time display of strongest levels with scores

- Indicator Settings:

Core Parameters

Lookback Period (Default: 200)

Lower (50-100): More responsive to recent price action, catches short-term levels

Higher (300-500): Focuses on major historical levels, more stable but less responsive

Best for: Day trading (100-150), Swing trading (200-300), Position trading (400-500)

Volume Spike Threshold (Default: 1.5)

Lower (1.2-1.4): More sensitive, catches smaller volume increases, more levels detected

Higher (2.0-3.0): Only major volume surges count, fewer but stronger signals

Market dependent: High-volume stocks may need higher thresholds (2.0+), low-volume stocks lower (1.2-1.3)

Price Bins (Default: 50)

Lower (20-30): Broader price zones, less precise but captures wider areas

Higher (70-100): More granular levels, precise but may be overly specific

Volatility dependent: High volatility assets benefit from more bins (70+)

Minimum PMI Score (Default: 0.5)

Lower (0.2-0.4): Shows more levels including weaker ones, comprehensive view

Higher (1.0-2.0): Only statistically strong levels, cleaner chart

Progressive filtering: Start with 0.5, increase if too cluttered

Max Levels to Show (Default: 8)

Fewer (3-5): Clean chart focusing on strongest levels only

More (10-15): Comprehensive view but may clutter chart

Strategy dependent: Scalpers prefer fewer (3-5), swing traders more (8-12)

Historical Tracking Settings

Update Frequency (Default: 20 bars)

Lower (5-10): More frequent updates, captures rapid market changes

Higher (50-100): Less frequent updates, focuses on major structural shifts

Timeframe scaling: 1-minute charts need lower frequency (5-10), daily charts higher (50+)

Show Historical Levels (Default: True)

Enables the "breadcrumb trail" effect showing evolution of support/resistance

Disable for cleaner charts focusing only on current levels

Max Historical Marks (Default: 50)

Lower (20-30): Less memory usage, shorter history

Higher (100-200): Longer historical context but more resource intensive

Fade Strength (Default: 0.8)

Lower (0.5-0.6): Historical levels more visible

Higher (0.9-0.95): Historical levels very subtle

Visual Settings

Support/Resistance Colors: Choose colors that contrast well with your chart theme Line Width: Thicker lines (3-4) for better visibility on busy charts Show PMI Scores: Toggle labels showing statistical strength Label Size: Adjust based on screen resolution and chart zoom level

- Most Effective Usage Strategies

For Day Trading:

Setup: Lookback 100-150, Volume Threshold 1.8-2.2, Update Frequency 10-15

Use PMI levels as bounce/rejection points for scalp entries

Higher PMI scores (>1.5) offer better probability setups

Watch for volume spike confirmations at levels

For Swing Trading:

Setup: Lookback 200-300, Volume Threshold 1.5-2.0, Update Frequency 20-30

Enter on pullbacks to high PMI support levels

Target next resistance level with PMI score >1.0

Hold through minor levels, exit at major PMI levels

For Position Trading:

Setup: Lookback 400-500, Volume Threshold 2.0+, Update Frequency 50+

Focus on PMI scores >2.0 for major structural levels

Use for portfolio entry/exit decisions

Combine with fundamental analysis for timing

- Trading Applications:

Entry Strategies:

PMI Bounce Trades

Price approaches high PMI support level (>1.0)

Wait for volume spike confirmation (orange triangles)

Enter long on bullish price action at the level

Stop loss just below the PMI level

Target: Next PMI resistance level

PMI Breakout Trades

Price consolidates near high PMI level

Volume increases (watch for orange triangles)

Enter on decisive break with volume

Previous resistance becomes new support

Target: Next major PMI level

PMI Rejection Trades

Price approaches PMI resistance with momentum

Watch for rejection signals and volume spikes

Enter short on failure to break through

Stop above the PMI level

Target: Next PMI support level

Risk Management:

Stop Loss Placement

Place stops 0.1-0.5% beyond PMI levels (adjust for volatility)

Higher PMI scores warrant tighter stops

Use ATR-based stops for volatile assets

Position Sizing

Larger positions at PMI levels >2.0 (highest conviction)

Smaller positions at PMI levels 0.5-1.0 (lower conviction)

Scale out at multiple PMI targets

- Key Warning Signs & What to Watch For

Red Flags:

🚨 Very Low PMI Scores (<0.3): Weak statistical significance, avoid trading

🚨 No Volume Confirmation: PMI level without recent volume spikes may be stale

🚨 Overcrowded Levels: Too many levels close together suggests poor parameter tuning

🚨 Outdated Levels: Historical traces are reference only, not tradeable

Optimization Tips:

✅ Regular Recalibration: Adjust parameters monthly based on market regime changes

✅ Volume Context: Always check for recent volume activity at PMI levels

✅ Multiple Timeframes: Confirm PMI levels across different timeframes

✅ Market Conditions: Higher thresholds during high volatility periods

Interpreting PMI Scores

PMI Score Ranges:

0.5-1.0: Moderate statistical significance, proceed with caution

1.0-1.5: Good significance, reliable for most trading strategies

1.5-2.0: Strong significance, high-confidence trade setups

2.0+: Very strong significance, institutional-grade levels

Historical Context: The historical trace system shows how support and resistance evolve over time. When current levels align with multiple historical traces, it indicates persistent market memory at those prices, significantly increasing the level's reliability.

Non-Lagging Longevity Zones [BigBeluga]🔵 OVERVIEW

A clean, non-lagging system for identifying price zones that persist over time—ranking them visually based on how long they survive without being invalidated.

Non-Lagging Longevity Zones uses non-lagging pivots to automatically build upper and lower zones that reflect key resistance and support. These zones are kept alive as long as price respects them and are instantly removed when invalidated. The indicator assigns a unique lifespan label to each zone in Days (D), Months (M), or Years (Y), providing instant context for historical relevance.

🔵 CONCEPTS

Non-Lag Pivot Detection: Detects upper and lower pivots using non-lagging swing identification (highest/lowest over length period).

h = ta.highest(len)

l = ta.lowest(len)

high_pivot = high == h and high < h

low_pivot = low == l and low > l

Longevity Ranking: Zones are preserved as long as price doesn't breach them. Levels that remain intact grow in visual intensity.

Time-Based Weighting: Each zone is labeled with its lifespan in days , emphasizing how long it has survived.

duration = last_bar_index - start

days_ = int(duration*(timeframe.in_seconds("")/60/60/24))

days = days_ >= 365 ? int(days_ / 365) : days_ >= 30 ? int(days_ / 30) : days_

marker = days_ >= 365 ? " Y" : days_ >= 30 ? " M" : " D"

Dynamic Coloring: Older zones are drawn with stronger fill, while newer ones appear fainter—making it easy to assess significance.

Self-Cleaning Logic: If price invalidates a zone, it’s instantly removed, keeping the chart clean and focused.

🔵 FEATURES

Upper and Lower Zones: Auto-detects valid high/low pivots and plots horizontal zones with ATR-based thickness.

Real-Time Validation: Zones are extended only if price stays outside them—giving precise control zones.

Gradient Fill Intensity: The longer a level survives, the more opaque the fill becomes.

Duration-Based Labeling: Time alive is shown at the root of each zone:

• D – short-term zones

• M – medium-term structure

• Y – long-term legacy levels

Smart Zone Clearing: Zones are deleted automatically once invalidated by price, keeping the display accurate.

Efficient Memory Handling: Keeps only the 10 most recent valid levels per side for optimal performance.

🔵 HOW TO USE

Track durable S/R zones that survived price tests without being breached.

Use longer-lived zones as high-confidence confluence areas for entries or targets.

Observe fill intensity to judge structural importance at a glance .

Layer with volume or momentum tools to confirm bounce or breakout probability.

Ideal for swing traders, structure-based traders, or macro analysis.

🔵 CONCLUSION

Non-Lagging Longevity Zones lets the market speak for itself—by spotlighting levels with proven survival over time. Whether you're trading trend continuation, mean reversion, or structure-based reversals, this tool equips you with an immediate read on what price zones truly matter—and how long they've stood the test of time.

Smart Directional Fib Zone (Selectable Session)🎯 Overview

This indicator plots a dynamic Fibonacci zone between the 0.5 and 0.618 levels , calculated from the previous day’s price action , and is designed specifically for intraday traders.

It visually highlights key retracement or reaction areas where the market often pauses or reverses.

🔍 How it works

At the start of each day, the script automatically captures:

the previous day’s open (pdo),

high (pdh),

low (pdl),

and close (pdc).

It then determines if the previous day was bullish (Close > Open) or bearish (Close < Open).

Based on that:

If the previous day was bullish, it projects the Fibonacci levels down from the high (typical for expecting retracements).

If bearish, it projects them up from the low.

The two key levels are:

0.5 (50%) retracement / projection

0.618 (61.8%) retracement / projection

A colored zone is plotted between these levels to act as a leading guide for intraday setups.

⏰ Time filtering & session customization

A unique feature is the dynamic session filtering:

By default, the zone is only plotted during active market hours, keeping your chart clean outside trading hours.

The script provides a dropdown selector so you can quickly switch between:

India session (9:15 to 15:30)

Europe session (9:00 to 17:30)

US session (9:30 to 16:00)

Or even define your own custom session times.

This makes it ideal for intraday traders in any region.

🎨 Visual features

The fill zone changes color based on the previous day’s sentiment:

Green zone if the previous day was bullish

Red zone if the previous day was bearish

🚨 Alerts

The script includes an alert condition, so you can easily set up TradingView alerts to notify you when:

Price enters the Fibonacci zone.

This is extremely helpful for catching retracements or reversals without staring at the screen all day.

⚙️ How to use

✅ Works on any intraday timeframe (1 min, 5 min, 15 min, etc.).

✅ Simply add it to your chart, pick your session in the dropdown, and watch the Fibonacci zone automatically adjust to your selected market hours.

Use it as a confluence tool alongside other indicators like VWAP, EMAs, Bollinger Bands, or price action patterns to time entries and exits.

💪 Why this is powerful

This is more than a simple Fib retracement tool:

It dynamically adapts to the previous day’s sentiment, helping you trade in alignment with recent market psychology.

The session filtering ensures your charts are focused only on the periods

Relative Measured Volatility (RMV)RMV • Volume-Sensitive Consolidation Indicator

A lightweight Pine Script that highlights true low-volatility, low-volume bars in a single squeeze measure.

What it does

Calculates each bar’s raw High-Low range.

Down-weights bars where volume is below its 30-day average, emphasizing genuine quiet periods.

Normalizes the result over the prior 15 bars (excluding the current bar), scaling from 0 (tightest) to 100 (most volatile).

Draws the series as a step plot, shades true “tight” bars below the user threshold, and marks sustained squeezes with a small arrow.

Key inputs

Lookback (bars): Number of bars to use for normalization (default 15).

Tight Threshold: RMV value under which a bar is considered squeezed (default 15).

Volume SMA Period: Period for the volume moving average benchmark (default 30).

How it works

Raw range: barRange = high - low

Volume ratio: volRatio = min(volume / sma(volume,30), 1)

Weighted range: vwRange = barRange * volRatio

Rolling min/max (prior 15 bars): exclude today so a new low immediately registers a 0.

Normalize: rmv = clamp(100 * (vwRange - min) / (max - min), 0, 100)

Visualization & signals

Step line for exact bar-by-bar values.

Shaded background when RMV < threshold.

Consecutive-bar filter ensures arrows only appear when tightness lasts at least two bars, cutting noise.

Why use it

Quickly spot consolidation zones that combine narrow price action with genuine dry volume—ideal for swing entries ahead of breakouts.

Simple Market Kill-Zones + Open (UTC)What it does

This Pine v6 indicator highlights the “kill-zones” around the big session opens—Asian (23:00–03:00 UTC), London (07:00–09:00 UTC) and New York (13:30–15:30 UTC)—by reading each bar’s actual UTC timestamp. It also draws dashed vertical lines at exactly 23:00, 07:00 and 13:30 UTC, so you never miss the liquidity ramps. Because it uses raw UTC hours/minutes, it stays accurate even when exchanges pause (e.g. Nano-BTC’s daily halt) or your chart’s display timezone changes.

Key Inputs

Show Asia/London/NY Kill Zone – toggle each shaded band on/off

Zone Colors – pick your own semi-transparent hues

Show Session-Open Lines – enable dashed verticals at the exact open times

Line Colors – customize the line opacity and style

How to use

Apply on your favorite timeframe (15 min–1 h is a sweet spot).

Toggle the zones you care about and pick readable colors.

Use the dashed lines as entry triggers or as visual bookmarks.

In your own Pine strategies, wrap order logic with the zone booleans to only trade when liquidity’s alive.

F&O Time Zones – Final Fixed📌 This indicator highlights high-probability intraday time zones used in Indian F&O (Futures & Options) strategies. Ideal for scalping, breakout setups, and trap avoidance.

🕒 Covered Time Zones:

• 9:15 – 9:21 AM → Flash Trades (first 1-minute volatility)

• 9:21 – 9:30 AM → Smart Money Trap (VWAP fakeouts)

• 9:30 – 9:50 AM → Fake Breakout Zone

• 9:50 – 10:15 AM → Institutional Entry Timing

• 10:15 – 10:45 AM → VWAP Range Scalps

• 10:45 – 11:15 AM → Second Trap Zone

• 11:15 – 1:00 PM → Trend Continuation Window

• 1:00 – 1:45 PM → Volatility Compression

• 1:45 – 2:15 PM → Institutional Exit Phase 1

• 2:15 – 2:45 PM → Trend Acceleration / Reversals

• 2:45 – 3:15 PM → Expiry Scalping Zone

• 3:15 – 3:30 PM → Dead Zone (square-off time)

🔧 Features:

✓ Clean vertical lines per zone

✓ Optional label positions (top or bottom)

✓ Adjustable line style, width, and color

🧠 Best used on: NIFTY, BANKNIFTY, FINNIFTY (5-min or lower)

---

🔒 **Disclaimer**:

This script is for **educational purposes only**. It is not financial advice. Trading involves risk. Please consult a professional or do your own research before taking any positions.

—

👤 Script by: **JoanJagan**

🛠️ Built in Pine Script v5

Aetherium Institutional Market Resonance EngineAetherium Institutional Market Resonance Engine (AIMRE)

A Three-Pillar Framework for Decoding Institutional Activity

🎓 THEORETICAL FOUNDATION

The Aetherium Institutional Market Resonance Engine (AIMRE) is a multi-faceted analysis system designed to move beyond conventional indicators and decode the market's underlying structure as dictated by institutional capital flow. Its philosophy is built on a singular premise: significant market moves are preceded by a convergence of context , location , and timing . Aetherium quantifies these three dimensions through a revolutionary three-pillar architecture.

This system is not a simple combination of indicators; it is an integrated engine where each pillar's analysis feeds into a central logic core. A signal is only generated when all three pillars achieve a state of resonance, indicating a high-probability alignment between market organization, key liquidity levels, and cyclical momentum.

⚡ THE THREE-PILLAR ARCHITECTURE

1. 🌌 PILLAR I: THE COHERENCE ENGINE (THE 'CONTEXT')

Purpose: To measure the degree of organization within the market. This pillar answers the question: " Is the market acting with a unified purpose, or is it chaotic and random? "

Conceptual Framework: Institutional campaigns (accumulation or distribution) create a non-random, organized market environment. Retail-driven or directionless markets are characterized by "noise" and chaos. The Coherence Engine acts as a filter to ensure we only engage when institutional players are actively steering the market.

Formulaic Concept:

Coherence = f(Dominance, Synchronization)

Dominance Factor: Calculates the absolute difference between smoothed buying pressure (volume-weighted bullish candles) and smoothed selling pressure (volume-weighted bearish candles), normalized by total pressure. A high value signifies a clear winner between buyers and sellers.

Synchronization Factor: Measures the correlation between the streams of buying and selling pressure over the analysis window. A high positive correlation indicates synchronized, directional activity, while a negative correlation suggests choppy, conflicting action.

The final Coherence score (0-100) represents the percentage of market organization. A high score is a prerequisite for any signal, filtering out unpredictable market conditions.

2. 💎 PILLAR II: HARMONIC LIQUIDITY MATRIX (THE 'LOCATION')

Purpose: To identify and map high-impact institutional footprints. This pillar answers the question: " Where have institutions previously committed significant capital? "

Conceptual Framework: Large institutional orders leave indelible marks on the market in the form of anomalous volume spikes at specific price levels. These are not random occurrences but are areas of intense historical interest. The Harmonic Liquidity Matrix finds these footprints and consolidates them into actionable support and resistance zones called "Harmonic Nodes."

Algorithmic Process:

Footprint Identification: The engine scans the historical lookback period for candles where volume > average_volume * Institutional_Volume_Filter. This identifies statistically significant volume events.

Node Creation: A raw node is created at the mean price of the identified candle.

Dynamic Clustering: The engine uses an ATR-based proximity algorithm. If a new footprint is identified within Node_Clustering_Distance (ATR) of an existing Harmonic Node, it is merged. The node's price is volume-weighted, and its magnitude is increased. This prevents chart clutter and consolidates nearby institutional orders into a single, more significant level.

Node Decay: Nodes that are older than the Institutional_Liquidity_Scanback period are automatically removed from the chart, ensuring the analysis remains relevant to recent market dynamics.

3. 🌊 PILLAR III: CYCLICAL RESONANCE MATRIX (THE 'TIMING')

Purpose: To identify the market's dominant rhythm and its current phase. This pillar answers the question: " Is the market's immediate energy flowing up or down? "

Conceptual Framework: Markets move in waves and cycles of varying lengths. Trading in harmony with the current cyclical phase dramatically increases the probability of success. Aetherium employs a simplified wavelet analysis concept to decompose price action into short, medium, and long-term cycles.

Algorithmic Process:

Cycle Decomposition: The engine calculates three oscillators based on the difference between pairs of Exponential Moving Averages (e.g., EMA8-EMA13 for short cycle, EMA21-EMA34 for medium cycle).

Energy Measurement: The 'energy' of each cycle is determined by its recent volatility (standard deviation). The cycle with the highest energy is designated as the "Dominant Cycle."

Phase Analysis: The engine determines if the dominant cycles are in a bullish phase (rising from a trough) or a bearish phase (falling from a peak).

Cycle Sync: The highest conviction timing signals occur when multiple cycles (e.g., short and medium) are synchronized in the same direction, indicating broad-based momentum.

🔧 COMPREHENSIVE INPUT SYSTEM

Pillar I: Market Coherence Engine

Coherence Analysis Window (10-50, Default: 21): The lookback period for the Coherence Engine.

Lower Values (10-15): Highly responsive to rapid shifts in market control. Ideal for scalping but can be sensitive to noise.

Balanced (20-30): Excellent for day trading, capturing the ebb and flow of institutional sessions.

Higher Values (35-50): Smoother, more stable reading. Best for swing trading and identifying long-term institutional campaigns.

Coherence Activation Level (50-90%, Default: 70%): The minimum market organization required to enable signal generation.

Strict (80-90%): Only allows signals in extremely clear, powerful trends. Fewer, but potentially higher quality signals.

Standard (65-75%): A robust filter that effectively removes choppy conditions while capturing most valid institutional moves.

Lenient (50-60%): Allows signals in less-organized markets. Can be useful in ranging markets but may increase false signals.

Pillar II: Harmonic Liquidity Matrix

Institutional Liquidity Scanback (100-400, Default: 200): How far back the engine looks for institutional footprints.

Short (100-150): Focuses on recent institutional activity, providing highly relevant, immediate levels.

Long (300-400): Identifies major, long-term structural levels. These nodes are often extremely powerful but may be less frequent.

Institutional Volume Filter (1.3-3.0, Default: 1.8): The multiplier for detecting a volume spike.

High (2.5-3.0): Only registers climactic, undeniable institutional volume. Fewer, but more significant nodes.

Low (1.3-1.7): More sensitive, identifying smaller but still relevant institutional interest.

Node Clustering Distance (0.2-0.8 ATR, Default: 0.4): The ATR-based distance for merging nearby nodes.

High (0.6-0.8): Creates wider, more consolidated zones of liquidity.

Low (0.2-0.3): Creates more numerous, precise, and distinct levels.

Pillar III: Cyclical Resonance Matrix

Cycle Resonance Analysis (30-100, Default: 50): The lookback for determining cycle energy and dominance.

Short (30-40): Tunes the engine to faster, shorter-term market rhythms. Best for scalping.

Long (70-100): Aligns the timing component with the larger primary trend. Best for swing trading.

Institutional Signal Architecture

Signal Quality Mode (Professional, Elite, Supreme): Controls the strictness of the three-pillar confluence.

Professional: Loosest setting. May generate signals if two of the three pillars are in strong alignment. Increases signal frequency.

Elite: Balanced setting. Requires a clear, unambiguous resonance of all three pillars. The recommended default.

Supreme: Most stringent. Requires perfect alignment of all three pillars, with each pillar exhibiting exceptionally strong readings (e.g., coherence > 85%). The highest conviction signals.

Signal Spacing Control (5-25, Default: 10): The minimum bars between signals to prevent clutter and redundant alerts.

🎨 ADVANCED VISUAL SYSTEM

The visual architecture of Aetherium is designed not merely for aesthetics, but to provide an intuitive, at-a-glance understanding of the complex data being processed.

Harmonic Liquidity Nodes: The core visual element. Displayed as multi-layered, semi-transparent horizontal boxes.

Magnitude Visualization: The height and opacity of a node's "glow" are proportional to its volume magnitude. More significant nodes appear brighter and larger, instantly drawing the eye to key levels.

Color Coding: Standard nodes are blue/purple, while exceptionally high-magnitude nodes are highlighted in an accent color to denote critical importance.

🌌 Quantum Resonance Field: A dynamic background gradient that visualizes the overall market environment.

Color: Shifts from cool blues/purples (low coherence) to energetic greens/cyans (high coherence and organization), providing instant context.

Intensity: The brightness and opacity of the field are influenced by total market energy (a composite of coherence, momentum, and volume), making powerful market states visually apparent.

💎 Crystalline Lattice Matrix: A geometric web of lines projected from a central moving average.

Mathematical Basis: Levels are projected using multiples of the Golden Ratio (Phi ≈ 1.618) and the ATR. This visualizes the natural harmonic and fractal structure of the market. It is not arbitrary but is based on mathematical principles of market geometry.

🧠 Synaptic Flow Network: A dynamic particle system visualizing the engine's "thought process."

Node Density & Activation: The number of particles and their brightness/color are tied directly to the Market Coherence score. In high-coherence states, the network becomes a dense, bright, and organized web. In chaotic states, it becomes sparse and dim.

⚡ Institutional Energy Waves: Flowing sine waves that visualize market volatility and rhythm.

Amplitude & Speed: The height and speed of the waves are directly influenced by the ATR and volume, providing a feel for market energy.

📊 INSTITUTIONAL CONTROL MATRIX (DASHBOARD)

The dashboard is the central command console, providing a real-time, quantitative summary of each pillar's status.

Header: Displays the script title and version.

Coherence Engine Section:

State: Displays a qualitative assessment of market organization: ◉ PHASE LOCK (High Coherence), ◎ ORGANIZING (Moderate Coherence), or ○ CHAOTIC (Low Coherence). Color-coded for immediate recognition.

Power: Shows the precise Coherence percentage and a directional arrow (↗ or ↘) indicating if organization is increasing or decreasing.

Liquidity Matrix Section:

Nodes: Displays the total number of active Harmonic Liquidity Nodes currently being tracked.

Target: Shows the price level of the nearest significant Harmonic Node to the current price, representing the most immediate institutional level of interest.

Cycle Matrix Section:

Cycle: Identifies the currently dominant market cycle (e.g., "MID ") based on cycle energy.

Sync: Indicates the alignment of the cyclical forces: ▲ BULLISH , ▼ BEARISH , or ◆ DIVERGENT . This is the core timing confirmation.

Signal Status Section:

A unified status bar that provides the final verdict of the engine. It will display "QUANTUM SCAN" during neutral periods, or announce the tier and direction of an active signal (e.g., "◉ TIER 1 BUY ◉" ), highlighted with the appropriate color.

🎯 SIGNAL GENERATION LOGIC

Aetherium's signal logic is built on the principle of strict, non-negotiable confluence.

Condition 1: Context (Coherence Filter): The Market Coherence must be above the Coherence Activation Level. No signals can be generated in a chaotic market.

Condition 2: Location (Liquidity Node Interaction): Price must be actively interacting with a significant Harmonic Liquidity Node.

For a Buy Signal: Price must be rejecting the Node from below (testing it as support).

For a Sell Signal: Price must be rejecting the Node from above (testing it as resistance).

Condition 3: Timing (Cycle Alignment): The Cyclical Resonance Matrix must confirm that the dominant cycles are synchronized with the intended trade direction.

Signal Tiering: The Signal Quality Mode input determines how strictly these three conditions must be met. 'Supreme' mode, for example, might require not only that the conditions are met, but that the Market Coherence is exceptionally high and the interaction with the Node is accompanied by a significant volume spike.

Signal Spacing: A final filter ensures that signals are spaced by a minimum number of bars, preventing over-alerting in a single move.

🚀 ADVANCED TRADING STRATEGIES

The Primary Confluence Strategy: The intended use of the system. Wait for a Tier 1 (Elite/Supreme) or Tier 2 (Professional/Elite) signal to appear on the chart. This represents the alignment of all three pillars. Enter after the signal bar closes, with a stop-loss placed logically on the other side of the Harmonic Node that triggered the signal.

The Coherence Context Strategy: Use the Coherence Engine as a standalone market filter. When Coherence is high (>70%), favor trend-following strategies. When Coherence is low (<50%), avoid new directional trades or favor range-bound strategies. A sharp drop in Coherence during a trend can be an early warning of a trend's exhaustion.

Node-to-Node Trading: In a high-coherence environment, use the Harmonic Liquidity Nodes as both entry points and profit targets. For example, after a BUY signal is generated at one Node, the next Node above it becomes a logical first profit target.

⚖️ RESPONSIBLE USAGE AND LIMITATIONS

Decision Support, Not a Crystal Ball: Aetherium is an advanced decision-support tool. It is designed to identify high-probability conditions based on a model of institutional behavior. It does not predict the future.

Risk Management is Paramount: No indicator can replace a sound risk management plan. Always use appropriate position sizing and stop-losses. The signals provided are probabilistic, not certainties.

Past Performance Disclaimer: The market models used in this script are based on historical data. While robust, there is no guarantee that these patterns will persist in the future. Market conditions can and do change.

Not a "Set and Forget" System: The indicator performs best when its user understands the concepts behind the three pillars. Use the dashboard and visual cues to build a comprehensive view of the market before acting on a signal.

Backtesting is Essential: Before applying this tool to live trading, it is crucial to backtest and forward-test it on your preferred instruments and timeframes to understand its unique behavior and characteristics.

🔮 CONCLUSION

The Aetherium Institutional Market Resonance Engine represents a paradigm shift from single-variable analysis to a holistic, multi-pillar framework. By quantifying the abstract concepts of market context, location, and timing into a unified, logical system, it provides traders with an unprecedented lens into the mechanics of institutional market operations.

It is not merely an indicator, but a complete analytical engine designed to foster a deeper understanding of market dynamics. By focusing on the core principles of institutional order flow, Aetherium empowers traders to filter out market noise, identify key structural levels, and time their entries in harmony with the market's underlying rhythm.

"In all chaos there is a cosmos, in all disorder a secret order." - Carl Jung

— Dskyz, Trade with insight. Trade with confluence. Trade with Aetherium.

Open Range Breakout (ORB) with Alerts

🚀 ChartsAlgo – Open Range Breakout (ORB) with Alerts

The Open Range Breakout (ORB) Indicator by ChartsAlg is designed for intraday traders looking to capitalize on price movements after the market’s opening range. This tool is especially effective for futures (MNQ, MES) and high-volatility stocks or crypto where initial volatility sets the tone for the session.

This indicator identifies a user-defined opening range window, plots the high/low lines of that range, and visually alerts users when price breaks out above or below the range — with options to customize breakout repetitions, background fill, and alerts.

💡 What is an Open Range Breakout (ORB)?

The opening range represents the high and low established during the first few minutes of the trading session — usually 15 or 30 minutes. Many intraday strategies are based on the idea that breaking out of this initial range often signals strong momentum and trend continuation.

Traders often enter:

Long when price breaks above the range high.

Short when price breaks below the range low.

⚙️ How It Works

You define a session window (e.g., 09:30–09:45 EST).

The indicator tracks the high and low during this time.

Once the session ends, the high and low become your range breakout levels.

The indicator then:

Plots lines for visual clarity

Optionally fills background between the range

Triggers breakout signals if price crosses the levels

Provides alerts when breakouts occur

🛠️ Settings Breakdown

🔹 Session Settings

Range Session: Set your preferred window (e.g., 0930–0945). Can be premarket, first 30 mins, or any custom time.

Time zone: Use "America/New York" for EST (default) or change to "GMT+0" for international traders.

🔹 Breakout Settings

Bullish Breakout Signals: Number of allowed breakout alerts above the range.

Bearish Breakout Signals: Number of allowed breakout alerts below the range.

This prevents repeated alerts once breakout has been confirmed.

🔹 Display Settings

Show Background Fill: Fills area between high/low of the range for easier visual analysis.

Show Breakout Signals: Triangle markers plotted on the chart when breakouts happen.

Only Show Today’s Range: Keeps the chart clean by showing only the most current day’s range.

🔹 Color Settings

Range High/Low Line Colors: Choose any color for clarity.

Range Fill Color: Customize the highlight area for your chart style.

📊 Chart Features

Range High/Low Lines: Automatically plotted after range session ends.

Visual Fill Box: Optional background shading between the opening range.

Triangle Breakout Markers: Appear at the breakout candle.

Alerts: Can be used with TradingView’s alert system to notify you of breakouts in real-time.

🔔 Alerts

Two alert conditions are built in:

Bullish Breakout: Triggers when price breaks above the high of the range.

Bearish Breakout: Triggers when price breaks below the low of the range.

Example Alert Message:

📈 “Bullish Breakout above Open Range on AAPL!”

To activate:

Click “🔔 Alerts” on TradingView.

Set condition to this script.

Choose “ORB Breakout Up” or “ORB Breakout Down”.

Choose alert frequency and notification method.

⚠️ DISCLAIMER

ChartsAlgo tools are for informational and educational purposes only.

They are not financial advice or signals. Past performance does not guarantee future results. Use at your own risk and always implement solid risk management.

By using this indicator, you agree that you are solely responsible for any trades or decisions made based on the information provided.

Multi-Confluence Swing Hunter V1# Multi-Confluence Swing Hunter V1 - Complete Description

Overview

The Multi-Confluence Swing Hunter V1 is a sophisticated low timeframe scalping strategy specifically optimized for MSTR (MicroStrategy) trading. This strategy employs a comprehensive point-based scoring system that combines optimized technical indicators, price action analysis, and reversal pattern recognition to generate precise trading signals on lower timeframes.

Performance Highlight:

In backtesting on MSTR 5-minute charts, this strategy has demonstrated over 200% profit performance, showcasing its effectiveness in capturing rapid price movements and volatility patterns unique to MicroStrategy's trading behavior.

The strategy's parameters have been fine-tuned for MSTR's unique volatility characteristics, though they can be optimized for other high-volatility instruments as well.

## Key Innovation & Originality

This strategy introduces a unique **dual scoring system** approach:

- **Entry Scoring**: Identifies swing bottoms using 13+ different technical criteria

- **Exit Scoring**: Identifies swing tops using inverse criteria for optimal exit timing

Unlike traditional strategies that rely on simple indicator crossovers, this system quantifies market conditions through a weighted scoring mechanism, providing objective, data-driven entry and exit decisions.

## Technical Foundation

### Optimized Indicator Parameters

The strategy utilizes extensively backtested parameters specifically optimized for MSTR's volatility patterns:

**MACD Configuration (3,10,3)**:

- Fast EMA: 3 periods (vs standard 12)

- Slow EMA: 10 periods (vs standard 26)

- Signal Line: 3 periods (vs standard 9)

- **Rationale**: These faster parameters provide earlier signal detection while maintaining reliability, particularly effective for MSTR's rapid price movements and high-frequency volatility

**RSI Configuration (21-period)**:

- Length: 21 periods (vs standard 14)

- Oversold: 30 level

- Extreme Oversold: 25 level

- **Rationale**: The 21-period RSI reduces false signals while still capturing oversold conditions effectively in MSTR's volatile environment

**Parameter Adaptability**: While optimized for MSTR, these parameters can be adjusted for other high-volatility instruments. Faster-moving stocks may benefit from even shorter MACD periods, while less volatile assets might require longer periods for optimal performance.

### Scoring System Methodology

**Entry Score Components (Minimum 13 points required)**:

1. **RSI Signals** (max 5 points):

- RSI < 30: +2 points

- RSI < 25: +2 points

- RSI turning up: +1 point

2. **MACD Signals** (max 8 points):

- MACD below zero: +1 point

- MACD turning up: +2 points

- MACD histogram improving: +2 points

- MACD bullish divergence: +3 points

3. **Price Action** (max 4 points):

- Long lower wick (>50%): +2 points

- Small body (<30%): +1 point

- Bullish close: +1 point

4. **Pattern Recognition** (max 8 points):

- RSI bullish divergence: +4 points

- Quick recovery pattern: +2 points

- Reversal confirmation: +4 points

**Exit Score Components (Minimum 13 points required)**:

Uses inverse criteria to identify swing tops with similar weighting system.

## Risk Management Features

### Position Sizing & Risk Control

- **Single Position Strategy**: 100% equity allocation per trade

- **No Overlapping Positions**: Ensures focused risk management

- **Configurable Risk/Reward**: Default 5:1 ratio optimized for volatile assets

### Stop Loss & Take Profit Logic

- **Dynamic Stop Loss**: Based on recent swing lows with configurable buffer

- **Risk-Based Take Profit**: Calculated using risk/reward ratio

- **Clean Exit Logic**: Prevents conflicting signals

## Default Settings Optimization

### Key Parameters (Optimized for MSTR/Bitcoin-style volatility):

- **Minimum Entry Score**: 13 (ensures high-conviction entries)

- **Minimum Exit Score**: 13 (prevents premature exits)

- **Risk/Reward Ratio**: 5.0 (accounts for volatility)

- **Lower Wick Threshold**: 50% (identifies true hammer patterns)

- **Divergence Lookback**: 8 bars (optimal for swing timeframes)

### Why These Defaults Work for MSTR:

1. **Higher Score Thresholds**: MSTR's volatility requires more confirmation

2. **5:1 Risk/Reward**: Compensates for wider stops needed in volatile markets

3. **Faster MACD**: Captures momentum shifts quickly in fast-moving stocks

4. **21-period RSI**: Reduces noise while maintaining sensitivity

## Visual Features

### Score Display System

- **Green Labels**: Entry scores ≥10 points (below bars)

- **Red Labels**: Exit scores ≥10 points (above bars)

- **Large Triangles**: Actual trade entries/exits

- **Small Triangles**: Reversal pattern confirmations

### Chart Cleanliness

- Indicators plotted in separate panes (MACD, RSI)

- TP/SL levels shown only during active positions

- Clear trade markers distinguish signals from actual trades

## Backtesting Specifications

### Realistic Trading Conditions

- **Commission**: 0.1% per trade

- **Slippage**: 3 points

- **Initial Capital**: $1,000

- **Account Type**: Cash (no margin)

### Sample Size Considerations

- Strategy designed for 100+ trade sample sizes

- Recommended timeframes: 4H, 1D for swing trading

- Optimal for trending/volatile markets

## Strategy Limitations & Considerations

### Market Conditions

- **Best Performance**: Trending markets with clear swings

- **Reduced Effectiveness**: Highly choppy, sideways markets

- **Volatility Dependency**: Optimized for moderate to high volatility assets

### Risk Warnings

- **High Allocation**: 100% position sizing increases risk

- **No Diversification**: Single position strategy

- **Backtesting Limitation**: Past performance doesn't guarantee future results

## Usage Guidelines

### Recommended Assets & Timeframes

- **Primary Target**: MSTR (MicroStrategy) - 5min to 15min timeframes

- **Secondary Targets**: High-volatility stocks (TSLA, NVDA, COIN, etc.)

- **Crypto Markets**: Bitcoin, Ethereum (with parameter adjustments)

- **Timeframe Optimization**: 1min-15min for scalping, 30min-1H for swing scalping

### Timeframe Recommendations

- **Primary Scalping**: 5-minute and 15-minute charts

- **Active Monitoring**: 1-minute for precise entries

- **Swing Scalping**: 30-minute to 1-hour timeframes

- **Avoid**: Sub-1-minute (excessive noise) and above 4-hour (reduces scalping opportunities)

## Technical Requirements

- **Pine Script Version**: v6

- **Overlay**: Yes (plots on price chart)

- **Additional Panes**: MACD and RSI indicators

- **Real-time Compatibility**: Confirmed bar signals only

## Customization Options

All parameters are fully customizable through inputs:

- Indicator lengths and levels

- Scoring thresholds

- Risk management settings

- Visual display preferences

- Date range filtering

## Conclusion

This scalping strategy represents a comprehensive approach to low timeframe trading that combines multiple technical analysis methods into a cohesive, quantified system specifically optimized for MSTR's unique volatility characteristics. The optimized parameters and scoring methodology provide a systematic way to identify high-probability scalping setups while managing risk effectively in fast-moving markets.

The strategy's strength lies in its objective, multi-criteria approach that removes emotional decision-making from scalping while maintaining the flexibility to adapt to different instruments through parameter optimization. While designed for MSTR, the underlying methodology can be fine-tuned for other high-volatility assets across various markets.

**Important Disclaimer**: This strategy is designed for experienced scalpers and is optimized for MSTR trading. The high-frequency nature of scalping involves significant risk. Past performance does not guarantee future results. Always conduct your own analysis, consider your risk tolerance, and be aware of commission/slippage costs that can significantly impact scalping profitability.

Adaptive RSI (ARSI)# Adaptive RSI (ARSI) - Dynamic Momentum Oscillator

Adaptive RSI is an advanced momentum oscillator that dynamically adjusts its calculation period based on real-time market volatility and cycle analysis. Unlike traditional RSI that uses fixed periods, ARSI continuously adapts to market conditions, providing more accurate overbought/oversold signals and reducing false signals during varying market phases.

## How It Works

At its core, ARSI calculates an adaptive period ranging from 8 to 28 bars using two key components: volatility measurement through Average True Range (ATR) and cycle detection via price momentum analysis. The logic is straightforward:

- **High volatility periods** trigger shorter calculation periods for enhanced responsiveness to rapid price movements

- **Low volatility periods** extend the calculation window for smoother, more reliable signals

- **Market factor** combines volatility and cycle analysis to determine optimal RSI period in real-time

When RSI crosses above 70, the market enters overbought territory. When it falls below 30, oversold conditions emerge. The indicator also features extreme levels at 80/20 for stronger reversal signals and midline crossovers at 50 for trend confirmation.

The adaptive mechanism ensures the oscillator remains sensitive during critical market movements while filtering out noise during consolidation phases, making it superior to static RSI implementations across different market conditions.

## Features

- **True Adaptive Calculation**: Dynamic period adjustment from 8-28 bars based on market volatility

- **Multiple Signal Types**: Overbought/oversold, extreme reversals, and midline crossovers

- **Configurable Parameters**: RSI length, adaptive sensitivity, ATR period, min/max bounds

- **Smart Smoothing**: Adjustable EMA smoothing from 1-21 periods to reduce noise

- **Visual Clarity**: Gradient colors, area fills, and signal dots for immediate trend recognition

- **Real-time Information**: Live data table showing current RSI, adaptive period, and market factor

- **Flexible Source Input**: Apply to any price source (close, hl2, ohlc4, etc.)

- **Professional Alerts**: Six built-in alert conditions for automated trading systems

## Signal Generation

ARSI generates multiple signal types for comprehensive market analysis:

**Primary Signals**: RSI crosses above 70 (overbought) or below 30 (oversold) - most reliable entry/exit points

**Extreme Signals**: RSI reaches 80+ (extreme overbought) or 20- (extreme oversold) - potential reversal zones

**Trend Signals**: RSI crosses above/below 50 midline - confirms directional momentum

**Reversal Signals**: Price action contradicts extreme RSI levels - early turning point detection

The adaptive period changes provide additional confirmation - signals accompanied by significant period shifts often carry higher probability of success.

## Visual Implementation

The indicator employs sophisticated visual elements for instant market comprehension:

- **Gradient RSI Line**: Color intensity reflects both value and momentum direction

- **Dynamic Zones**: Overbought/oversold areas with customizable fill colors

- **Signal Markers**: Triangular indicators mark key reversal and continuation points

- **Information Panel**: Real-time display of RSI value, adaptive period, market factor, and signal status

- **Background Coloring**: Subtle fills indicate current market state without chart clutter

## Parameter Configuration

**RSI Settings**:

- RSI Length: Base calculation period (default: 14)

- Adaptive Sensitivity: Response aggressiveness to volatility changes (default: 1.0)

- ATR Length: Volatility measurement period (default: 14)

- Min/Max Period: Adaptive calculation boundaries (default: 8/28)

- Smoothing Length: Final noise reduction filter (default: 3)

**Level Settings**:

- Overbought/Oversold: Standard signal levels (default: 70/30)

- Extreme Levels: Enhanced reversal zones (default: 80/20)

- Midline Display: 50-level trend confirmation toggle

**Visual Settings**:

- Line Width: RSI line thickness (1-5)

- Area Fills: Zone highlighting toggle

- Gradient Colors: Dynamic color intensity

- Signal Dots: Entry/exit marker display

## Alerts

ARSI includes six comprehensive alert conditions:

- **ARSI Overbought** - RSI crosses above overbought level

- **ARSI Oversold** - RSI crosses below oversold level

- **ARSI Bullish Cross** - RSI crosses above 50 midline

- **ARSI Bearish Cross** - RSI crosses below 50 midline

- **ARSI Extreme Bull** - Potential bullish reversal from extreme oversold

- **ARSI Extreme Bear** - Potential bearish reversal from extreme overbought

## Use Cases

**Trend Following**: Adaptive periods naturally adjust during trend acceleration and consolidation phases

**Mean Reversion**: Enhanced overbought/oversold signals with volatility-based confirmation

**Breakout Trading**: Extreme level breaches often precede significant directional moves

**Risk Management**: Multiple signal types allow for layered entry/exit strategies

**Multi-Timeframe Analysis**: Works effectively across various timeframes and asset classes

## Trading Applications

**Swing Trading**: Excels during trend transitions with adaptive sensitivity to changing conditions

**Day Trading**: Enhanced responsiveness during volatile sessions while filtering consolidation noise

**Position Trading**: Longer smoothing periods provide stable signals for broader market analysis

**Scalping**: Minimal smoothing with high sensitivity captures short-term momentum shifts

The indicator performs well across stocks, forex, commodities, and cryptocurrencies, though parameter optimization may be required for specific market characteristics.

## Settings Summary

**Display Settings**:

- RSI Length: Moving average baseline period

- Adaptive Sensitivity: Volatility response factor

- ATR Length: Volatility measurement window

- Min/Max Period: Adaptive calculation boundaries

- Smoothing Length: Noise reduction filter

**Level Configuration**:

- Overbought/Oversold: Primary signal thresholds

- Extreme Levels: Secondary reversal zones

- Midline Display: Trend confirmation toggle

**Visual Options**:

- Line Width: RSI line appearance

- Area Fills: Zone highlighting

- Gradient Colors: Dynamic visual feedback

- Signal Dots: Entry/exit markers

## Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice. Trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. Always conduct thorough testing and risk assessment before live implementation. The adaptive nature of this indicator requires understanding of its behavior across different market conditions for optimal results.

Mark4ex vWapMark4ex VWAP is a precision session-anchored Volume Weighted Average Price (VWAP) indicator crafted for intraday traders who want clean, reliable VWAP levels that reset daily to match a specific market session.

Unlike the built-in continuous VWAP, this version anchors each day to your chosen session start and end time, most commonly aligned with the New York Stock Exchange Open (9:30 AM EST) through the market close (4:00 PM EST). This ensures your VWAP reflects only intraday price action within your active trading window — filtering out irrelevant overnight moves and providing clearer mean-reversion signals.

Key Features:

Fully configurable session start & end times — adapt it for NY session or any other market.

Anchored VWAP resets daily for true session-based levels.

Built for the New York Open Range Breakout strategy: see how price interacts with VWAP during the volatile first 30–60 minutes of the US market.

Plots a clean, dynamic line that updates tick-by-tick during the session and disappears outside trading hours.

Designed to help you spot real-time support/resistance, intraday fair value zones, and liquidity magnets used by institutional traders.

How to Use — NY Open Range Breakout:

During the first hour of the New York session, institutional traders often define an “Opening Range” — the high and low formed shortly after the bell. The VWAP in this zone acts as a dynamic pivot point:

When price is above the session VWAP, bulls are in control — the level acts as a support floor for pullbacks.

When price is below the session VWAP, bears dominate — the level acts as resistance against bounces.

Breakouts from the opening range often test the VWAP for confirmation or rejection.

Traders use this to time entries for breakouts, retests, or mean-reversion scalps with greater confidence.

⚙️ Recommended Settings:

Default: 9:30 AM to 4:00 PM New York time — standard US equities session.

Adjust hours/minutes to match your target market’s open and close.

👤 Who is it for?

Scalpers, day traders, prop traders, and anyone trading the NY Open, indices like the S&P 500, or highly liquid stocks during US cash hours.

🚀 Why use Mark4ex VWAP?

Because a properly anchored VWAP is a trader’s real-time institutional fair value, giving you better context than static moving averages. It adapts live to volume shifts and helps you follow smart money footprints.

This indicator will reconfigure every day, anchored to the New York Open, it will also leave historical NY Open VWAP for study purpose.

S&P Power Hour Liquidity Sweep StrategyThis indicator is designed for intraday traders who want to take advantage of liquidity grabs, break of structure (BOS), and optimal entry points during the most volatile hours of the trading day: the NYSE Power Hours (09:30–10:30 AM and 02:30–04:00 PM EST).

Key Features:

Power Hour Detection:

Automatically identifies the two most liquid hours of the trading session.

Liquidity Sweep Detection:

Highlights when price sweeps a recent swing high or low — a common trap before reversals.

Break of Structure (BOS):

Confirms trend shift after a liquidity sweep with smart money-style BOS markers.

Fair Value Gap (FVG) Highlighting: (Optional)

Spot institutional imbalances between candles to fine-tune trade entries.

How It Works:

Wait for price to sweep a swing high or low during the power hours.

Look for a break of structure (BOS) in the opposite direction.

Enter on the next candle or FVG retest.

The indicator will plot a yellow circle for entry, a red line for stop, and a green line for the target (based on your RR setting).

Customizable Inputs:

Swing sensitivity (lookback bars)

Risk-to-reward ratio

Optional FVG visibility

Best Used With:

Higher timeframe bias (15m/1H)

Order blocks or volume analysis

Avoiding major news events

Whether you're a scalper or precision-based intraday trader, this tool helps you spot high-probability reversal setups with clean visuals and clear confirmations.

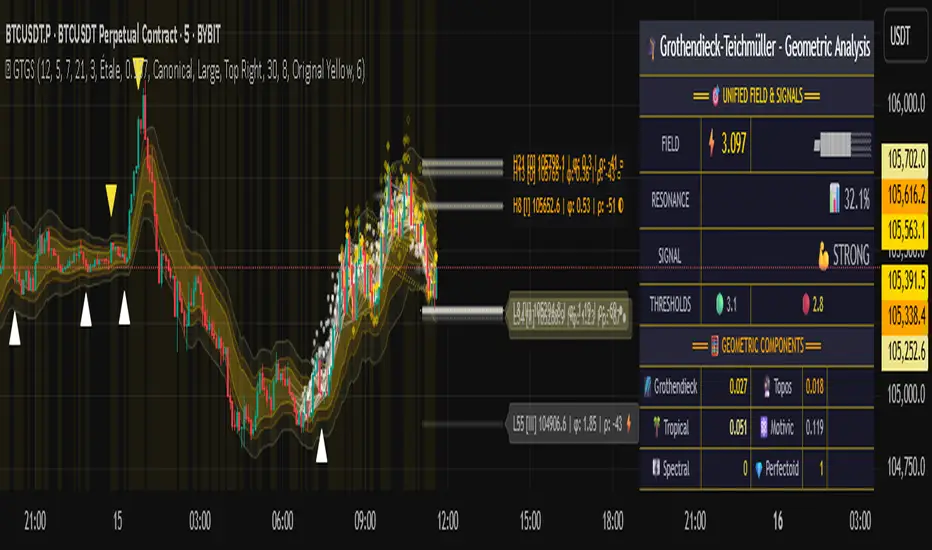

Grothendieck-Teichmüller Geometric SynthesisDskyz's Grothendieck-Teichmüller Geometric Synthesis (GTGS)

THEORETICAL FOUNDATION: A SYMPHONY OF GEOMETRIES

The 🎓 GTGS is built upon a revolutionary premise: that market dynamics can be modeled as geometric and topological structures. While not a literal academic implementation—such a task would demand computational power far beyond current trading platforms—it leverages core ideas from advanced mathematical theories as powerful analogies and frameworks for its algorithms. Each component translates an abstract concept into a practical market calculation, distinguishing GTGS by identifying deeper structural patterns rather than relying on standard statistical measures.

1. Grothendieck-Teichmüller Theory: Deforming Market Structure

The Theory : Studies symmetries and deformations of geometric objects, focusing on the "absolute" structure of mathematical spaces.

Indicator Analogy : The calculate_grothendieck_field function models price action as a "deformation" from its immediate state. Using the nth root of price ratios (math.pow(price_ratio, 1.0/prime)), it measures market "shape" stretching or compression, revealing underlying tensions and potential shifts.

2. Topos Theory & Sheaf Cohomology: From Local to Global Patterns

The Theory : A framework for assembling local properties into a global picture, with cohomology measuring "obstructions" to consistency.

Indicator Analogy : The calculate_topos_coherence function uses sine waves (math.sin) to represent local price "sections." Summing these yields a "cohomology" value, quantifying price action consistency. High values indicate coherent trends; low values signal conflict and uncertainty.

3. Tropical Geometry: Simplifying Complexity

The Theory : Transforms complex multiplicative problems into simpler, additive, piecewise-linear ones using min(a, b) for addition and a + b for multiplication.

Indicator Analogy : The calculate_tropical_metric function applies tropical_add(a, b) => math.min(a, b) to identify the "lowest energy" state among recent price points, pinpointing critical support levels non-linearly.

4. Motivic Cohomology & Non-Commutative Geometry

The Theory : Studies deep arithmetic and quantum-like properties of geometric spaces.

Indicator Analogy : The motivic_rank and spectral_triple functions compute weighted sums of historical prices to capture market "arithmetic complexity" and "spectral signature." Higher values reflect structured, harmonic price movements.

5. Perfectoid Spaces & Homotopy Type Theory

The Theory : Abstract fields dealing with p-adic numbers and logical foundations of mathematics.

Indicator Analogy : The perfectoid_conv and type_coherence functions analyze price convergence and path identity, assessing the "fractal dust" of price differences and price path cohesion, adding fractal and logical analysis.

The Combination is Key : No single theory dominates. GTGS ’s Unified Field synthesizes all seven perspectives into a comprehensive score, ensuring signals reflect deep structural alignment across mathematical domains.

🎛️ INPUTS: CONFIGURING THE GEOMETRIC ENGINE

The GTGS offers a suite of customizable inputs, allowing traders to tailor its behavior to specific timeframes, market sectors, and trading styles. Below is a detailed breakdown of key input groups, their functionality, and optimization strategies, leveraging provided tooltips for precision.

Grothendieck-Teichmüller Theory Inputs

🧬 Deformation Depth (Absolute Galois) :

What It Is : Controls the depth of Galois group deformations analyzed in market structure.

How It Works : Measures price action deformations under automorphisms of the absolute Galois group, capturing market symmetries.

Optimization :

Higher Values (15-20) : Captures deeper symmetries, ideal for major trends in swing trading (4H-1D).

Lower Values (3-8) : Responsive to local deformations, suited for scalping (1-5min).

Timeframes :

Scalping (1-5min) : 3-6 for quick local shifts.

Day Trading (15min-1H) : 8-12 for balanced analysis.

Swing Trading (4H-1D) : 12-20 for deep structural trends.

Sectors :

Stocks : Use 8-12 for stable trends.

Crypto : 3-8 for volatile, short-term moves.

Forex : 12-15 for smooth, cyclical patterns.

Pro Tip : Increase in trending markets to filter noise; decrease in choppy markets for sensitivity.

🗼 Teichmüller Tower Height :

What It Is : Determines the height of the Teichmüller modular tower for hierarchical pattern detection.

How It Works : Builds modular levels to identify nested market patterns.

Optimization :

Higher Values (6-8) : Detects complex fractals, ideal for swing trading.

Lower Values (2-4) : Focuses on primary patterns, faster for scalping.

Timeframes :

Scalping : 2-3 for speed.

Day Trading : 4-5 for balanced patterns.

Swing Trading : 5-8 for deep fractals.

Sectors :

Indices : 5-8 for robust, long-term patterns.

Crypto : 2-4 for rapid shifts.

Commodities : 4-6 for cyclical trends.

Pro Tip : Higher towers reveal hidden fractals but may slow computation; adjust based on hardware.

🔢 Galois Prime Base :

What It Is : Sets the prime base for Galois field computations.

How It Works : Defines the field extension characteristic for market analysis.

Optimization :

Prime Characteristics :

2 : Binary markets (up/down).

3 : Ternary states (bull/bear/neutral).

5 : Pentagonal symmetry (Elliott waves).

7 : Heptagonal cycles (weekly patterns).

11,13,17,19 : Higher-order patterns.

Timeframes :

Scalping/Day Trading : 2 or 3 for simplicity.

Swing Trading : 5 or 7 for wave or cycle detection.

Sectors :

Forex : 5 for Elliott wave alignment.

Stocks : 7 for weekly cycle consistency.

Crypto : 3 for volatile state shifts.

Pro Tip : Use 7 for most markets; 5 for Elliott wave traders.

Topos Theory & Sheaf Cohomology Inputs

🏛️ Temporal Site Size :

What It Is : Defines the number of time points in the topological site.

How It Works : Sets the local neighborhood for sheaf computations, affecting cohomology smoothness.

Optimization :

Higher Values (30-50) : Smoother cohomology, better for trends in swing trading.

Lower Values (5-15) : Responsive, ideal for reversals in scalping.

Timeframes :

Scalping : 5-10 for quick responses.

Day Trading : 15-25 for balanced analysis.

Swing Trading : 25-50 for smooth trends.

Sectors :

Stocks : 25-35 for stable trends.

Crypto : 5-15 for volatility.

Forex : 20-30 for smooth cycles.

Pro Tip : Match site size to your average holding period in bars for optimal coherence.

📐 Sheaf Cohomology Degree :

What It Is : Sets the maximum degree of cohomology groups computed.

How It Works : Higher degrees capture complex topological obstructions.

Optimization :

Degree Meanings :

1 : Simple obstructions (basic support/resistance).

2 : Cohomological pairs (double tops/bottoms).

3 : Triple intersections (complex patterns).

4-5 : Higher-order structures (rare events).

Timeframes :

Scalping/Day Trading : 1-2 for simplicity.

Swing Trading : 3 for complex patterns.

Sectors :

Indices : 2-3 for robust patterns.

Crypto : 1-2 for rapid shifts.

Commodities : 3-4 for cyclical events.

Pro Tip : Degree 3 is optimal for most trading; higher degrees for research or rare event detection.

🌐 Grothendieck Topology :

What It Is : Chooses the Grothendieck topology for the site.

How It Works : Affects how local data integrates into global patterns.

Optimization :

Topology Characteristics :

Étale : Finest topology, captures local-global principles.

Nisnevich : A1-invariant, good for trends.

Zariski : Coarse but robust, filters noise.

Fpqc : Faithfully flat, highly sensitive.

Sectors :

Stocks : Zariski for stability.

Crypto : Étale for sensitivity.

Forex : Nisnevich for smooth trends.

Indices : Zariski for robustness.

Timeframes :

Scalping : Étale for precision.

Swing Trading : Nisnevich or Zariski for reliability.

Pro Tip : Start with Étale for precision; switch to Zariski in noisy markets.

Unified Field Configuration Inputs

⚛️ Field Coupling Constant :

What It Is : Sets the interaction strength between geometric components.

How It Works : Controls signal amplification in the unified field equation.

Optimization :

Higher Values (0.5-1.0) : Strong coupling, amplified signals for ranging markets.

Lower Values (0.001-0.1) : Subtle signals for trending markets.

Timeframes :

Scalping : 0.5-0.8 for quick, strong signals.

Swing Trading : 0.1-0.3 for trend confirmation.

Sectors :

Crypto : 0.5-1.0 for volatility.

Stocks : 0.1-0.3 for stability.

Forex : 0.3-0.5 for balance.

Pro Tip : Default 0.137 (fine structure constant) is a balanced starting point; adjust up in choppy markets.

📐 Geometric Weighting Scheme :

What It Is : Determines the framework for combining geometric components.

How It Works : Adjusts emphasis on different mathematical structures.

Optimization :

Scheme Characteristics :

Canonical : Equal weighting, balanced.

Derived : Emphasizes higher-order structures.

Motivic : Prioritizes arithmetic properties.

Spectral : Focuses on frequency domain.

Sectors :

Stocks : Canonical for balance.

Crypto : Spectral for volatility.

Forex : Derived for structured moves.

Indices : Motivic for arithmetic cycles.

Timeframes :

Day Trading : Canonical or Derived for flexibility.

Swing Trading : Motivic for long-term cycles.

Pro Tip : Start with Canonical; experiment with Spectral in volatile markets.

Dashboard and Visual Configuration Inputs

📋 Show Enhanced Dashboard, 📏 Size, 📍 Position :

What They Are : Control dashboard visibility, size, and placement.

How They Work : Display key metrics like Unified Field , Resonance , and Signal Quality .

Optimization :

Scalping : Small size, Bottom Right for minimal chart obstruction.

Swing Trading : Large size, Top Right for detailed analysis.

Sectors : Universal across markets; adjust size based on screen setup.

Pro Tip : Use Large for analysis, Small for live trading.

📐 Show Motivic Cohomology Bands, 🌊 Morphism Flow, 🔮 Future Projection, 🔷 Holographic Mesh, ⚛️ Spectral Flow :

What They Are : Toggle visual elements representing mathematical calculations.

How They Work : Provide intuitive representations of market dynamics.

Optimization :

Timeframes :

Scalping : Enable Morphism Flow and Spectral Flow for momentum.

Swing Trading : Enable all for comprehensive analysis.

Sectors :

Crypto : Emphasize Morphism Flow and Future Projection for volatility.

Stocks : Focus on Cohomology Bands for stable trends.

Pro Tip : Disable non-essential visuals in fast markets to reduce clutter.

🌫️ Field Transparency, 🔄 Web Recursion Depth, 🎨 Mesh Color Scheme :

What They Are : Adjust visual clarity, complexity, and color.

How They Work : Enhance interpretability of visual elements.

Optimization :

Transparency : 30-50 for balanced visibility; lower for analysis.

Recursion Depth : 6-8 for balanced detail; lower for older hardware.

Color Scheme :

Purple/Blue : Analytical focus.

Green/Orange : Trading momentum.

Pro Tip : Use Neon Purple for deep analysis; Neon Green for active trading.

⏱️ Minimum Bars Between Signals :

What It Is : Minimum number of bars required between consecutive signals.

How It Works : Prevents signal clustering by enforcing a cooldown period.

Optimization :

Higher Values (10-20) : Fewer signals, avoids whipsaws, suited for swing trading.

Lower Values (0-5) : More responsive, allows quick reversals, ideal for scalping.

Timeframes :

Scalping : 0-2 bars for rapid signals.

Day Trading : 3-5 bars for balance.

Swing Trading : 5-10 bars for stability.

Sectors :

Crypto : 0-3 for volatility.

Stocks : 5-10 for trend clarity.

Forex : 3-7 for cyclical moves.

Pro Tip : Increase in choppy markets to filter noise.

Hardcoded Parameters

Tropical, Motivic, Spectral, Perfectoid, Homotopy Inputs : Fixed to optimize performance but influence calculations (e.g., tropical_degree=4 for support levels, perfectoid_prime=5 for convergence).

Optimization : Experiment with codebase modifications if advanced customization is needed, but defaults are robust across markets.

🎨 ADVANCED VISUAL SYSTEM: TRADING IN A GEOMETRIC UNIVERSE

The GTTMTSF ’s visuals are direct representations of its mathematics, designed for intuitive and precise trading decisions.

Motivic Cohomology Bands :

What They Are : Dynamic bands ( H⁰ , H¹ , H² ) representing cohomological support/resistance.

Color & Meaning : Colors reflect energy levels ( H⁰ tightest, H² widest). Breaks into H¹ signal momentum; H² touches suggest reversals.

How to Trade : Use for stop-loss/profit-taking. Band bounces with Dashboard confirmation are high-probability setups.

Morphism Flow (Webbing) :

What It Is : White particle streams visualizing market momentum.

Interpretation : Dense flows indicate strong trends; sparse flows signal consolidation.

How to Trade : Follow dominant flow direction; new flows post-consolidation signal trend starts.

Future Projection Web (Fractal Grid) :

What It Is : Fibonacci-period fractal projections of support/resistance.

Color & Meaning : Three-layer lines (white shadow, glow, colored quantum) with labels showing price, topological class, anomaly strength (φ), resonance (ρ), and obstruction ( H¹ ). ⚡ marks extreme anomalies.

How to Trade : Target ⚡/● levels for entries/exits. High-anomaly levels with weakening Unified Field are reversal setups.

Holographic Mesh & Spectral Flow :

What They Are : Visuals of harmonic interference and spectral energy.

How to Trade : Bright mesh nodes or strong Spectral Flow warn of building pressure before price movement.

📊 THE GEOMETRIC DASHBOARD: YOUR MISSION CONTROL

The Dashboard translates complex mathematics into actionable intelligence.

Unified Field & Signals :

FIELD : Master value (-10 to +10), synthesizing all geometric components. Extreme readings (>5 or <-5) signal structural limits, often preceding reversals or continuations.

RESONANCE : Measures harmony between geometric field and price-volume momentum. Positive amplifies bullish moves; negative amplifies bearish moves.

SIGNAL QUALITY : Confidence meter rating alignment. Trade only STRONG or EXCEPTIONAL signals for high-probability setups.

Geometric Components :

What They Are : Breakdown of seven mathematical engines.

How to Use : Watch for convergence. A strong Unified Field is reliable when components (e.g., Grothendieck , Topos , Motivic ) align. Divergence warns of trend weakening.

Signal Performance :

What It Is : Tracks indicator signal performance.

How to Use : Assesses real-time performance to build confidence and understand system behavior.

🚀 DEVELOPMENT & UNIQUENESS: BEYOND CONVENTIONAL ANALYSIS

The GTTMTSF was developed to analyze markets as evolving geometric objects, not statistical time-series.

Why This Is Unlike Anything Else :

Theoretical Depth : Uses geometry and topology, identifying patterns invisible to statistical tools.

Holistic Synthesis : Integrates seven deep mathematical frameworks into a cohesive Unified Field .

Creative Implementation : Translates PhD-level mathematics into functional Pine Script , blending theory and practice.

Immersive Visualization : Transforms charts into dynamic geometric landscapes for intuitive market understanding.

The GTTMTSF is more than an indicator; it’s a new lens for viewing markets, for traders seeking deeper insight into hidden order within chaos.

" Where there is matter, there is geometry. " - Johannes Kepler

— Dskyz , Trade with insight. Trade with anticipation.

Multi-Timeline 1.0Multi-TimeLines 1.0 - Comprehensive Description

WHAT IT DOES:

This indicator creates dynamic horizontal support/resistance lines based on opening prices captured at user-defined New York times. Unlike static horizontal lines, these levels automatically appear and disappear based on sophisticated session logic, providing traders with time-sensitive reference levels that adapt to market sessions.

HOW IT WORKS - TECHNICAL IMPLEMENTATION:

1.

Timezone Conversion Engine:

The script uses Pine Script's "America/New_York" timezone functions to ensure all time calculations are based on NY time, regardless of the user's chart timezone. This eliminates confusion and provides consistent behavior across global markets.

2.

Dual-Category Time Classification System:

The indicator employs a unique two-category classification system:

Category A (16:00-23:59 NY): Evening times that extend overnight until next day 15:59 NY

Category B (00:00-15:59 NY): Day times that extend until same day 15:59 NY

This classification handles the complex logic of overnight sessions and prevents lines from incorrectly resetting at midnight for evening times.

3. Price Capture Mechanism:

Uses precise time-hit detection with backup systems for edge cases (especially midnight 00:00). When a specified time occurs, the script captures the bar's opening price and stores it in persistent variables using Pine Script's var declarations.

4. Session-Aware Display Logic: