Moon+Lunar Cycle Vertical Delineation & Projection

Automatically highlights the exact candle in which Moonphase shifts occur.

Optionally including shifts within the Microphases of the total Lunar Cycle.

This allow traders to pre-emptively identify time-based points of volatility,

focusing on mean-reversion; further simplified via the use of projections.

Projections are calculated via candle count, values displayed in "Debug";

these are useful in understanding the function & underlying mechanics.

Cerca negli script per "Cycle"

CCI with Signals & Divergence [AIBitcoinTrend]👽 CCI with Signals & Divergence (AIBitcoinTrend)

The Hilbert Adaptive CCI with Signals & Divergence takes the traditional Commodity Channel Index (CCI) to the next level by dynamically adjusting its calculation period based on real-time market cycles using Hilbert Transform Cycle Detection. This makes it far superior to standard CCI, as it adapts to fast-moving trends and slow consolidations, filtering noise and improving signal accuracy.

Additionally, the indicator includes real-time divergence detection and an ATR-based trailing stop system, helping traders identify potential reversals and manage risk effectively.

👽 What Makes the Hilbert Adaptive CCI Unique?

Unlike the traditional CCI, which uses a fixed-length lookback period, this version automatically adjusts its lookback period using Hilbert Transform to detect the dominant cycle in the market.

✅ Hilbert Transform Adaptive Lookback – Dynamically detects cycle length to adjust CCI sensitivity.

✅ Real-Time Divergence Detection – Instantly identifies bullish and bearish divergences for early reversal signals.

✅ Implement Crossover/Crossunder signals tied to ATR-based trailing stops for risk management

👽 The Math Behind the Indicator

👾 Hilbert Transform Cycle Detection

The Hilbert Transform estimates the dominant market cycle length based on the frequency of price oscillations. It is computed using the in-phase and quadrature components of the price series:

tp = (high + low + close) / 3

smooth = (tp + 2 * tp + 2 * tp + tp ) / 6

detrender = smooth - smooth

quadrature = detrender - detrender

inPhase = detrender + quadrature

outPhase = quadrature - inPhase

instPeriod = 0.0

deltaPhase = math.abs(inPhase - inPhase ) + math.abs(outPhase - outPhase )

instPeriod := nz(3.25 / deltaPhase, instPeriod )

dominantCycle = int(math.min(math.max(instPeriod, cciMinPeriod), 500))

Where:

In-Phase & Out-Phase Components are derived from a detrended version of the price series.

Instantaneous Frequency measures the rate of cycle change, allowing the CCI period to adjust dynamically.

The result is bounded within a user-defined min/max range, ensuring stability.

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while CCI forms a higher low.

Buy signal is confirmed when CCI shows upward momentum.

Bearish Divergence Setup:

Price makes a higher high, while CCI forms a lower high.

Sell signal is confirmed when CCI shows downward momentum.

👾 Trailing Stop & Signal-Based Trading

Bullish Setup:

✅ CCI crosses above -100 → Buy signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if the price crosses below the stop.

Bearish Setup:

✅ CCI crosses below 100 → Sell signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if the price crosses above the stop.

👽 Why It’s Useful for Traders

Hilbert Adaptive Period Calculation – No more fixed-length periods; the indicator dynamically adapts to market conditions.

Real-Time Divergence Alerts – Helps traders anticipate market reversals before they occur.

ATR-Based Risk Management – Stops automatically adjust based on volatility.

Works Across Multiple Markets & Timeframes – Ideal for stocks, forex, crypto, and futures.

👽 Indicator Settings

Min & Max CCI Period – Defines the adaptive range for Hilbert-based lookback.

Smoothing Factor – Controls the degree of smoothing applied to CCI.

Enable Divergence Analysis – Toggles real-time divergence detection.

Lookback Period – Defines the number of bars for detecting pivot points.

Enable Crosses Signals – Turns on CCI crossover-based trade signals.

ATR Multiplier – Adjusts trailing stop sensitivity.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

Altcoins vs BTC Market Cap HeatmapAltcoins vs BTC Market Cap Heatmap

"Ground control to major Tom" 🌙 👨🚀 🚀

This indicator provides a visual heatmap for tracking the relationship between the market cap of altcoins (TOTAL3) and Bitcoin (BTC). The primary goal is to identify potential market cycle tops and bottoms by analyzing how the TOTAL3 market cap (all cryptocurrencies excluding Bitcoin and Ethereum) compares to Bitcoin’s market cap.

Key Features:

• Market Cap Ratio: Plots the ratio of TOTAL3 to BTC market caps to give a clear visual representation of altcoin strength versus Bitcoin.

• Heatmap: Colors the background red when altcoins are overheating (TOTAL3 market cap equals or exceeds BTC) and blue when altcoins are cooling (TOTAL3 market cap is half or less than BTC).

• Threshold Levels: Includes horizontal lines at 1 (Overheated), 0.75 (Median), and 0.5 (Cooling) for easy reference.

• Alerts: Set alert conditions for when the ratio crosses key levels (1.0, 0.75, and 0.5), enabling timely notifications for potential market shifts.

How It Works:

• Overheated (Ratio ≥ 1): Indicates that the altcoin market cap is on par or larger than Bitcoin's, which could signal a top in the cycle.

• Cooling (Ratio < 0.5): Suggests that the altcoin market cap is half or less than Bitcoin's, potentially signaling a market bottom or cooling phase.

• Median (Ratio ≈ 0.75): A midpoint that provides insight into the market's neutral zone.

Use this tool to monitor market extremes and adjust your strategy accordingly when the altcoin market enters overheated or cooling phases.

Adaptive, Double Jurik Filter Moving Average (AJFMA) [Loxx]Adaptive, Double Jurik Filter Moving Average (AJFMA) is moving average like Jurik Moving Average but with the addition of double smoothing and adaptive length (Autocorrelation Periodogram Algorithm) and power/volatility {Juirk Volty) inputs to further reduce noise and identify trends.

What is Jurik Volty?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

That's why investors, banks and institutions worldwide ask for the Jurik Research Moving Average ( JMA ). You may apply it just as you would any other popular moving average. However, JMA's improved timing and smoothness will astound you.

What is adaptive Jurik volatility?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers , 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average ( KAMA ) and Tushar Chande’s variable index dynamic average ( VIDYA ) adapt to changes in volatility . By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic , relative strength index ( RSI ), commodity channel index ( CCI ), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

- Double calculation of AJFMA for even smoother results

Adaptive Look-back/Volatility Phase Change Index on Jurik [Loxx]Adaptive Look-back, Adaptive Volatility Phase Change Index on Jurik is a Phase Change Index but with adaptive length and volatility inputs to reduce phase change noise and better identify trends. This is an invese indicator which means that small values on the oscillator indicate bullish sentiment and higher values on the oscillator indicate bearish sentiment

What is the Phase Change Index?

Based on the M.H. Pee's TASC article "Phase Change Index".

Prices at any time can be up, down, or unchanged. A period where market prices remain relatively unchanged is referred to as a consolidation. A period that witnesses relatively higher prices is referred to as an uptrend, while a period of relatively lower prices is called a downtrend.

The Phase Change Index (PCI) is an indicator designed specifically to detect changes in market phases.

This indicator is made as he describes it with one deviation: if we follow his formula to the letter then the "trend" is inverted to the actual market trend. Because of that an option to display inverted (and more logical) values is added.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

That's why investors, banks and institutions worldwide ask for the Jurik Research Moving Average ( JMA ). You may apply it just as you would any other popular moving average. However, JMA's improved timing and smoothness will astound you.

What is adaptive Jurik volatility

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is an adaptive cycle, and what is Ehlers Autocorrelation Periodogram Algorithm?

From his Ehlers' book Cycle Analytics for Traders Advanced Technical Trading Concepts by John F. Ehlers, 2013, page 135:

"Adaptive filters can have several different meanings. For example, Perry Kaufman’s adaptive moving average (KAMA) and Tushar Chande’s variable index dynamic average (VIDYA) adapt to changes in volatility. By definition, these filters are reactive to price changes, and therefore they close the barn door after the horse is gone.The adaptive filters discussed in this chapter are the familiar Stochastic, relative strength index (RSI), commodity channel index (CCI), and band-pass filter.The key parameter in each case is the look-back period used to calculate the indicator. This look-back period is commonly a fixed value. However, since the measured cycle period is changing, it makes sense to adapt these indicators to the measured cycle period. When tradable market cycles are observed, they tend to persist for a short while.Therefore, by tuning the indicators to the measure cycle period they are optimized for current conditions and can even have predictive characteristics.

The dominant cycle period is measured using the Autocorrelation Periodogram Algorithm. That dominant cycle dynamically sets the look-back period for the indicators. I employ my own streamlined computation for the indicators that provide smoother and easier to interpret outputs than traditional methods. Further, the indicator codes have been modified to remove the effects of spectral dilation.This basically creates a whole new set of indicators for your trading arsenal."

Included

-Your choice of length input calculation, either fixed or adaptive cycle

-Invert the signal to match the trend

-Bar coloring to paint the trend

Happy trading!

Obsidians Gold RevengeMany traders (including institutional desks) track lunar cycles on Gold (XAUUSD) because of the psychological impact on market sentiment. The common theory—often attributed to methods like Gann analysis—is:

🌑 New Moon: Often correlates with Market Bottoms (Buy Signals) or "New Beginnings."

🌕 Full Moon: Often correlates with Market Tops (Sell Signals) or "Exhaustion."

Here is a script that mathematically calculates the Moon Phase based on the lunar synodic month (approx. 29.53 days). It will plot these events on your chart so you can visually backtest if Gold respects these cycles.

How to use this for testing

Add it to your Chart: Apply it to the XAUUSD (Gold) chart.

Timeframe: This works best on 4-Hour (4H) or Daily (1D) charts. (On 15m charts, the moon phase covers many candles, so the label will appear on the specific candle where the phase officially "switched").

What to look for:

Look at the Dark Blue (New Moon) areas. Did price form a bottom or start a rally there?

Look at the Yellow (Full Moon) areas. Did price peak and reverse downward there?

Note: Lunar cycles are considered a "timing tool" rather than a directional indicator. They often indicate when a reversal might happen, but you should combine this with your Institutional Candle zones to confirm the direction!

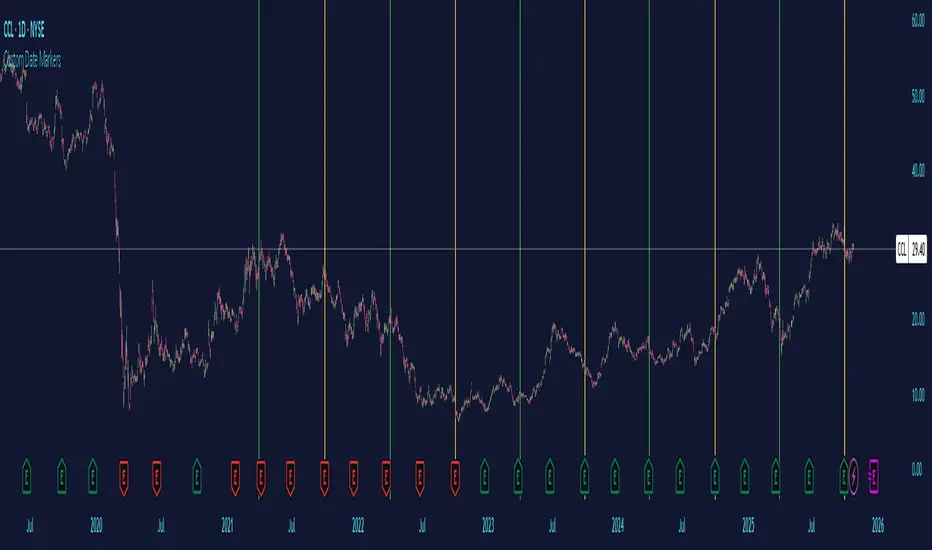

Custom Date MarkersCustom Date Markers - Pine Script Indicator

This indicator provides a powerful visual tool for technical and pattern analysis by allowing traders to mark up to 10 specific historical dates with customizable vertical lines on any chart. Each date can be assigned its own unique color, making it easy to categorize and distinguish between different types of events or market catalysts.

Primary Use Cases:

The indicator excels at identifying cyclical patterns and recurring market behavior. By marking significant dates such as earnings announcements, Federal Reserve meetings, dividend ex-dates, or seasonal events, traders can quickly visualize whether stocks consistently react in similar ways around these recurring dates. This is particularly valuable for discovering hidden patterns that might not be obvious from price action alone.

Practical Applications:

Earnings Analysis: Mark historical earnings dates to see if a stock tends to rally or sell-off before/after announcements

Macro Events: Identify how assets respond to FOMC meetings, CPI releases, or other economic data

Seasonal Patterns: Track dates that show recurring volatility or directional moves (like tax deadline periods, end-of-quarter re balancing, etc.)

Event Studies: Analyze the impact of company-specific events like product launches, FDA approvals, or leadership changes

Advanced Insights:

What makes this tool particularly interesting is its ability to reveal non-obvious correlations. For example, you might discover that a retail stock consistently experiences volume spikes 2-3 weeks before Black Friday across multiple years, or that certain tech stocks show weakness during specific conference dates. The color-coding feature allows you to layer multiple event types simultaneously—perhaps using red for bearish catalysts and green for bullish ones—creating a visual heat map of historical market reactions.

The indicator's 6-month default spacing (covering 4.5 years) is strategically designed to capture multiple business cycles while maintaining clarity on the chart. This timeframe is long enough to identify genuine patterns rather than coincidences, yet focused enough to remain relevant to current market conditions.

Pro Tip: Combine this indicator with volume analysis or other technical indicators to validate whether the patterns you observe are accompanied by meaningful market participation or if they're statistical noise.

Path of the Planets🪐 Path of the Planets

Path of the Planets is an open-source Pine Script™ v6 indicator. It is inspired by W.D. Gann’s Path of Planets chart, specifically the Chart 5-9 artistic replica by Patrick Mikula "shown below". The script visualizes planetary positions so you can explore possible correlations with price. It overlays geocentric and heliocentric longitudes and declinations using the AstroLib library and includes an optional positions table that shows, at a glance, each body’s geocentric longitude, heliocentric longitude, and declination. This is an educational tool only and not trading advice.

Key Features

Start point: Choose a date and time to begin plotting so studies can align with market events.

Adjustments: Mirror longitudes and shift by 360° multiples to re-frame cycles.

Planets: Toggle geocentric and heliocentric longitudes and declinations for Sun, Mercury, Venus, Earth, Mars, Jupiter, Saturn, Uranus, Neptune, and Pluto. Moon declination is available.

Positions table: Optional color-coded table (bottom-right) with three columns labeled Geo, Helio, and Dec. Values show degrees with the zodiac sign for the longitudes and degrees for declinations.

Visualization: Solid lines for geocentric longitudes, circles for heliocentric longitudes, and columns for declinations. Includes a zero-declination reference line.

How It Works

Converts bar timestamps to Julian days via AstroLib.

Fetches positions with AstroLib types: geocentric (0), heliocentric (1), and declination (3).

Normalizes longitudes to the −180° to +180° range, applies optional mirroring and 360° shifts, and converts longitudes to zodiac sign labels for the table.

Plots and the table update only on and after the selected start time.

Usage Tips

Apply on daily or higher timeframes when studying broader cycles. For degrees, use the left scale.

Limitations at the moment: default latitude, longitude, and timezone are set to 0; aspects and retrogrades are not included; the focus is on raw paths.

License and Credits

Dependency: @BarefootJoey Astrolib

Contributions and observations are welcome.

HSI - Halving Seasonality Index for Bitcoin (BTC) [Logue]Halving Seasonality Index (HSI) for Bitcoin (BTC) - The HSI takes advantage of the consistency of BTC cycles. Past cycles have formed macro tops around 538 days after each halving. Past cycles have formed macro bottoms every 948 days after each halving. Therefore, a linear "risk" curve can be created between the bottom and top dates to measure how close BTC might be to a bottom or a top. The default triggers are set at 98% risk for tops and 5% risk for bottoms. Extensions are also added as defaults to allow easy identification of the dates of the next top or bottom according to the HSI.

CSI - Calendar Seasonality Index for Bitcoin (BTC) [Logue]Calendar Seasonality Index (CSI) for Bitcoin (BTC) - The CSI takes advantage of the consistency of BTC cycles. Past cycles have formed macro tops every four years near November 21st, starting from in 2013. Past cycles have formed macro bottoms every four years near January 15th, starting from 2011. Therefore, a linear "risk" curve can be created between the bottom and top dates to measure how close BTC might be to a bottom or a top. The default triggers are at 98% risk for tops and 5% risk for bottoms. Extensions are also added as defaults to allow easy identification of the dates of the next top or bottom according to the CSI.

Triple Ehlers Market StateClear trend identification is an important aspect of finding the right side to trade, another is getting the best buying/selling price on a pullback, retracement or reversal. Triple Ehlers Market State can do both.

Three is always better

Ehlers’ original formulation produces bullish, bearish and trendless signals. The indicator presented here gate stages three correlation cycles of adjustable lengths and degree thresholds, displaying a more refined view of bullish, bearish and trendless markets, in a compact and novel way.

Stick with the default settings, or experiment with the cycle period and threshold angle of each cycle, then choose whether ‘Recent trend weighting’ is included in candle colouring.

John Ehlers is a highly respected trading maths head who may need no introduction here. His idea for Market State was published in TASC June 2020 Traders Tips. The awesome interpretation of Ehlers’ work on which Triple Ehlers Market State’s correlation cycle calculations are based can be found at:

DISCLAIMER: None of this is financial advice.

Mission Control Dashboard (AI, Crypto, Liquidity) FASTCONCEPT Price is a lagging indicator. Liquidity is a leading indicator. "Mission Control Dashboard (AI, Crypto, Liquidity) FAST" is a sophisticated macroeconomic dashboard designed to audit the "plumbing" of the financial system in real-time. Unlike standard indicators that rely solely on price action, this tool pulls data from the Federal Reserve (FRED), Treasury Statements, Corporate Financials (10-K/10-Q), and On-Chain Stablecoin metrics to visualize the structural flows driving the market.

THE "UNIFIED FIELD" SOLVER One of the hardest challenges in cross-asset scripting is "Time Dilation"—synchronizing 24/7 Crypto markets (Bitcoin) with Mon-Fri Traditional markets (Stocks/Bonds).

Standard scripts fail on weekends, showing mismatched data.

This engine uses a Weekly Anchor system. It calculates all momentum and liquidity metrics based on "Week-to-Date" or "Month-Ago" anchors. This ensures that a "Liquidity Drain" looks identical whether you are viewing a Bitcoin chart on Saturday or an Apple chart on Monday.

THE CHRONOS LOGIC The dashboard is sorted by Time Sensitivity (Speed of impact), from fast-twitch tactical signals to slow-moving structural fundamentals.

1. TACTICAL (Reacts in 24–48h)

Stablecoin Flight: Measures the immediate flow of capital from Volatile Assets to Stablecoins (USDT/USDC). A spike (>0.5%) indicates fear/sidelining.

Liquidity Alpha: Calculates the efficiency of capital. It subtracts "Friction" (Dollar Strength + Yields) from "Flow" (Liquidity Beta). High Alpha means money is flowing easily into risk assets.

Alt Euphoria: Tracks the overheating of the Altcoin market (TOTAL3). Green indicates sustainable growth; Red (>45%) warns of a "blow-off top."

Retail FOMO: A sentiment gauge comparing Coinbase Stock ( NASDAQ:COIN ) performance vs. Bitcoin ( CRYPTOCAP:BTC ). When Retail outperforms the Asset, local tops often follow.

2. LIQUIDITY & MACRO (Reacts in 1–4 Weeks)

Debt Wall (10Y): The Rate-of-Change of the US 10-Year Treasury Yield. Spiking yields act as gravity on risk assets.

Liquidity Beta: The raw "Quantity of Money." Tracks the 4-week change in Net Liquidity (Fed Balance Sheet - TGA + Stablecoins).

TGA Balance: The Critical Monitor. Tracks the Treasury General Account. When the TGA rises (Red), the government is draining liquidity from the banking system. When it falls (Green), it releases cash.

Note: This script includes an auto-scaler to handle TGA data in both Billions and Millions.

3. STRUCTURAL (Reacts in 3–12 Months)

AI Capex (YoY & QoQ): The "Floor" of the 2025/2026 cycle. Tracks the Capital Expenditure of the Hyperscalers (MSFT, GOOGL, AMZN, META). As long as this remains high (>30%), the infrastructure boom supports the tech narrative.

PMI Manufacturing: Tracks the ISM Manufacturing cycle. Contraction (<50) often forces Fed intervention.

Micron Inventory: A lead indicator for the hardware cycle.

HOW TO USE

Status Colors: The traffic light system helps you assess risk at a glance.

🟢 GREEN (Healthy): Flow is positive, friction is low, fundamentals are strong.

🔴 RED (Danger): Liquidity is draining (TGA spike), yields are shock-rising, or FOMO is excessive.

Zero Configuration: The script auto-detects asset classes and scales units (Billions/Trillions) automatically.

DATA SOURCES

Federal Reserve Economic Data (FRED)

Daily Treasury Statement (DTS)

CryptoCap (TradingView)

Nasdaq/Corporate Financials

Disclaimer: This tool is for informational purposes only and does not constitute financial advice. Macro data feeds are subject to reporting delays.

350DMA bands + Z-score (V2)This script extends the classic 350-day moving average (350DMA) by building dynamic valuation bands and a Z-Score framework to evaluate how far price deviates from its long-term mean.

Features

350DMA Anchor: Uses the 350-day simple moving average as the baseline reference.

Fixed Multipliers: Key bands plotted at ×0.625, ×1.0, ×1.6, ×2.0, and ×2.5 of the 350DMA — historically significant levels for cycle analysis.

Z-Score Mapping: Price is converted into a Z-Score on a scale from +2 (deep undervaluation) to –2 (extreme overvaluation), using log-space interpolation for accuracy.

Custom Display: HUD panel and on-chart label show the current Z-Score in real time.

Clamp Option: Users can toggle between raw Z values or capped values (±2).

How to Use

Valuation Context: The 350DMA is often considered a “fair value” anchor; large deviations identify cycles of under- or over-valuation.

Z-Score Insight:

Positive Z values suggest favorable accumulation zones where price is below long-term average.

Negative Z values highlight zones of stretched valuation, often associated with distribution or profit-taking.

Strategic Application: This is not a standalone trading system — it works best in confluence with other indicators, cycle models, or macro analysis.

Originality

Unlike a simple DMA overlay, this script:

Provides multiple cycle-based bands derived from the 350DMA.

Applies a logarithmic Z-Score mapping for more precise long-term scaling.

Adds an integrated HUD and labeling system for quick interpretation.

HHT Signal Analyzer (Refined)HHT Signal Analyzer

The HHT Signal Analyzer provides a real-time, smoothed approximation of the Hilbert-Huang Transform (HHT), designed to reveal adaptive cycles and phase changes in price action. It emulates Intrinsic Mode Functions (IMFs) using a double exponential moving average (EMA) filter to extract short-term oscillatory signals from price.

This indicator is helpful for identifying subtle shifts in market behavior, such as when a trend is transitioning or weakening, and is especially effective when paired with trend-based tools like GRJMOM.

How it works:

Applies a double EMA to the price (EMA of EMA)

Calculates the difference between the fast and slow EMA to emulate IMF behavior

Amplifies the signal for clear visual feedback

Highlights cycle slope changes with background coloring (green = rising, red = falling)

Use Cases:

Use slope direction to detect early phase shifts in the market

Combine with trend indicators to confirm or fade moves

Helps visualize when the market is entering a cycle crest or trough

Best for:

Traders looking to capture short-term reversals, cycle timing, or divergence with smooth and adaptive signals

Can be used on any timeframe

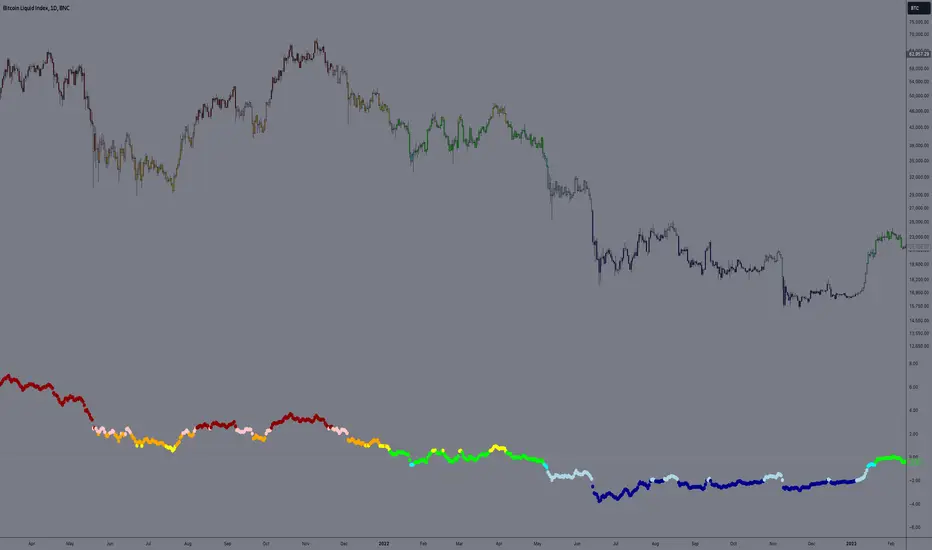

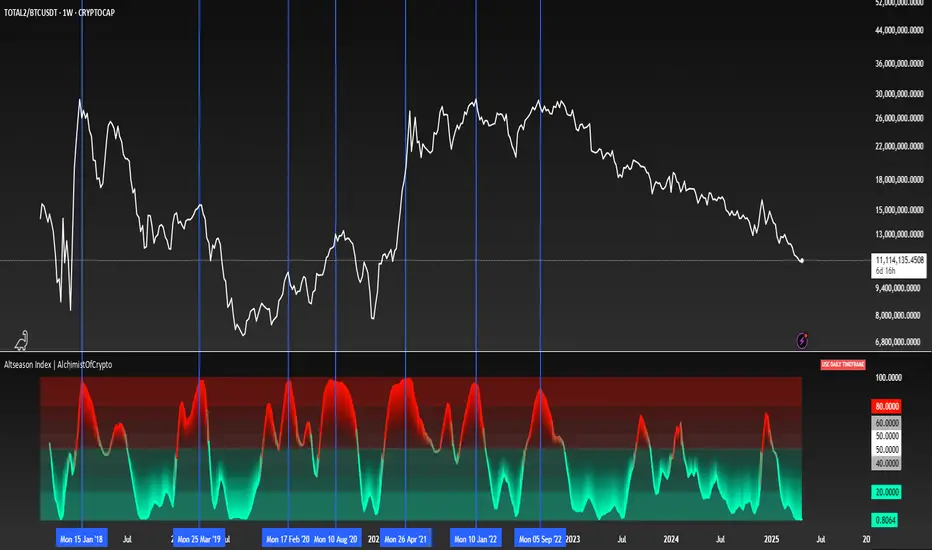

Altseason Index | AlchimistOfCrypto

🌈 Altseason Index | AlchimistOfCrypto – Revealing Bitcoin-Altcoin Dominance Cycles 🌈

"The Altseason Index, engineered through advanced mathematical methodology, visualizes the probabilistic distribution of capital flows between Bitcoin and altcoins within a multi-cycle paradigm. This indicator employs statistical normalization principles where ratio coefficients create mathematical boundaries that define dominance transitions between cryptographic asset classes. Our implementation features algorithmically enhanced rainbow visualization derived from extensive market cycle analysis, creating a dynamic representation of value flow with adaptive color gradients that highlight critical phase transitions in the cyclical evolution of the crypto market."

📊 Professional Trading Application

The Altseason Index transcends traditional sentiment models with a sophisticated multi-band illumination system that reveals the underlying structure of crypto sector rotation. Scientifically calibrated across different ratios (TOTAL2/BTC, OTHERS/BTC) and featuring seamless daily visualization, it enables investors to perceive capital transitions between Bitcoin and altcoins with unprecedented clarity.

- Visual Theming 🎨

Scientifically designed rainbow gradient optimized for market cycle recognition:

- Green-Blue: Altcoin accumulation zones with highest capital flow potential

- Neutral White: Market equilibrium zone representing balanced capital distribution

- Yellow-Red: Bitcoin dominance regions indicating defensive capital positioning

- Gradient Transitions: Mathematical inflection points for strategic reallocation

- Market Phase Detection 🔍

- Precise zone boundaries demarcating critical sentiment shifts in the crypto ecosystem

- Daily timeframe calculation ensuring consistent signal reliability

- Multiple ratio analysis revealing the probabilistic nature of market capital flows

🚀 How to Use

1. Identify Market Phase ⏰: Locate the current index relative to colored zones

2. Understand Capital Flow 🎚️: Monitor transitions between Bitcoin and altcoin dominance

3. Assess Mathematical Value 🌈: Determine optimal allocation based on zone location

4. Adjust Investment Strategy 🔎: Modulate position sizing based on dominance assessment

5. Prepare for Rotation ✅: Anticipate capital shifts when approaching extreme zones

6. Invest with Precision 🛡️: Accumulate altcoins in lower zones, reduce in upper zones

7. Manage Risk Dynamically 🔐: Scale portfolio allocations based on index positioning

Smart Trend Tracker Name: Smart Trend Tracker

Description:

The Smart Trend Tracker indicator is designed to analyze market cycles and identify key trend reversal points. It automatically marks support and resistance levels based on price dynamics, helping traders better navigate market structure.

Application:

Trend Analysis: The indicator helps determine when a trend may be nearing a reversal, which is useful for making entry or exit decisions.

Support and Resistance Levels: Automatically marks key levels, simplifying chart analysis.

Reversal Signals: Provides visual signals for potential reversal points, which can be used for counter-trend trading strategies.

How It Works:

Candlestick Sequence Analysis: The indicator tracks the number of consecutive candles in one direction (up or down). If the price continues to move N bars in a row in one direction, the system records this as an impulse phase.

Trend Exhaustion Detection: After a series of directional bars, the market may reach an overbought or oversold point. If the price continues to move in the same direction but with weakening momentum, the indicator records a possible trend slowdown.

Chart Display: The indicator marks potential reversal points with numbers or special markers. It can also display support and resistance levels based on key cycle points.

Settings:

Cycle Length: The number of bars after which the possibility of a reversal is assessed.

Trend Sensitivity: A parameter that adjusts sensitivity to trend movements.

Dynamic Levels: Setting for displaying key levels.

Название: Smart Trend Tracker

Описание:

Индикатор Smart Trend Tracker предназначен для анализа рыночных циклов и выявления ключевых точек разворота тренда. Он автоматически размечает уровни поддержки и сопротивления, основываясь на динамике цены, что помогает трейдерам лучше ориентироваться в структуре рынка.

Применение:

Анализ трендов: Индикатор помогает определить моменты, когда тренд может быть близок к развороту, что полезно для принятия решений о входе или выходе из позиции.

Определение уровней поддержки и сопротивления: Автоматически размечает ключевые уровни, что упрощает анализ графика.

Сигналы разворота: Индикатор предоставляет визуальные сигналы о возможных точках разворота, что может быть использовано для стратегий, основанных на контртрендовой торговле.

Как работает:

Анализ последовательности свечей: Индикатор отслеживает количество последовательных свечей в одном направлении (вверх или вниз). Если цена продолжает движение N баров подряд в одном направлении, система фиксирует это как импульсную фазу.

Выявление истощения тренда: После серии направленных баров рынок может достичь точки перегрева. Если цена продолжает двигаться в том же направлении, но с ослаблением импульса, индикатор фиксирует возможное замедление тренда.

Отображение на графике: Индикатор отмечает точки потенциального разворота номерами или специальными маркерами. Также возможен вывод уровней поддержки и сопротивления, основанных на ключевых точках цикла.

Настройки:

Длина цикла (Cycle Length): Количество баров, после которых оценивается возможность разворота.

Фильтрация тренда (Trend Sensitivity): Параметр, регулирующий чувствительность к трендовым движениям.

Уровни поддержки/сопротивления (Dynamic Levels): Настройка для отображения ключевых уровней.

BTC - Liquisync: Macro Pulse & Desync EngineLiquisync: Macro Pulse & Desync Engine | RM

Strategic Context: The Macro Fuel Tank

Why compare Global Liquidity to Bitcoin? Because Bitcoin acts as a "Global M2 Sponge." As central banks expand their balance sheets, this "Fuel" filters into the system, taking roughly 56 to 70 days to reach Bitcoin's price. Liquisync measures this lead-lag relationship to determine if the "Engine" (Price) is properly supported by the "Fuel" (M2).

How the Model Differs: Liquisync vs. Standard Macro Composites

Many existing macro scripts focus on a Linear Sum of indicators—adding up M2, Spread, and Copper/Gold into a single Z-score. While useful for general sentiment, these "Composite" models often suffer from Directional Blindness. They tell you if the environment is "Risk-On," but they cannot tell you if the Price is currently lying about the Liquidity.

The Liquisync Edge:

• Conflict Detection: Unlike composites that simply turn red or green, Liquisync identifies Desync.

• Velocity Normalization: Instead of Z-scoring absolute values, we measure the Acceleration (Slope) of the move, allowing us to see "Decay" before the trend actually flips.

How the Model Works

1. Pulse Velocity Mapping (The Dual-Slope Architecture)

The engine utilizes a Dual-Slope Architecture to measure the "Dynamic Force" behind the market. By calculating the Linear Regression Slope for both Global Liquidity and BTC Price, we are measuring Acceleration.

• Liquidity Slope (The Fuel): Measures the speed at which central banks are expanding or contracting the money supply.

• Price Slope (The Engine): Measures the speed at which the market is repricing Bitcoin in response to that money (or due to other factors).

The Mathematical Bridge: We don't just plot these lines independently; we normalize them. Because Global M2 is measured in Trillions and BTC in Thousands of Dollars, we transform both into a unified Relative Pulse Score (-100 to +100).

Liquisync: The 4 Macro Scenarios (Directional Matrix) By measuring the interconnectivity of these two pulses, the engine identifies four distinct market regimes:

Scenario A: Institutional Expansion (Harmony) Liquidity Slope (+ rising) | Price Slope (+ rising) Harmony. The trend is "True." The price increase is fully supported by global money. (Scenario Jan 2023)

Scenario B: The Bear Trap (Desync / "Open Mouth") Liquidity Slope (+ rising) | Price Slope (- falling) The Core Edge. Liquidity is filling up, but price is dropping due to short-term panic. Because the fuel is there, the price must eventually snap upward to catch up with the liquidity reality. (Scenario Jun 2020)

Scenario C: The Bull Trap (Desync / "Open Mouth") Liquidity Slope (- falling) | Price Slope (+ rising) The Danger Zone. Price is climbing on "Empty Fuel." Retail FOMO is driving the market while liquidity is being pulled. Highly unstable. (Scenario Jul 2022)

Scenario D: Macro Contraction (Harmony) Liquidity Slope (- falling) | Price Slope (- falling) The Drain. Global liquidity is shrinking and price is following. A fundamental bear market. (Scenario Nov/Dec 2021)

2. Directional Desync (The Conflict Filter)

Liquisync is a Conflict Filter. It ignores "Synchronous" phases where both lines move together and focuses 100% of its visual energy on the Desync scenarios (Bear Trap or Bull Trap). When the lines travel in opposite directions, the indicator generates Cyan Columns. The height of these columns tells you the intensity of the conflict. When the pulses move in Harmony (Scenario A & D), the desync value remains at zero. This creates a 'Visual Silence' on the chart, signaling that the current price trend is structurally healthy and macro-supported.

3. Liquisync Extreme (The Snap-Back Star ✦)

This triggers when the "Open Mouth" (the Liquidity Pulse (Golden Line) and the Price Pulse (White Area) pull in diametrically opposite directions) desync reaches 85% of its 1-year historical record. This is a generational signal identifying the absolute limits of market irrationality relative to the macro reality (Price up, M2 down or vice versa).

How to Read the Chart

• Golden Pulse: The Liquidity Slope

• White Area: The Price Slope

• Harmony (No Columns): Price and Liquidity are in sync. Trend-following is safe.

• Open Mouth (Cyan Columns): These are not momentum bars; they are Conflict Bars . They only appear when the Price and Liquidity are traveling in opposite directions. The taller the column, the more "stretched" the macro rubber band has become.

• Magenta Stars: The desync is at a statistical limit. Expect a violent Macro Snap-Back toward the Golden Liquidity line.

The 60-Day Lead-Lag Principle: Why the Delay?

The Liquisync engine utilizes a specific forward-lag (defaulted to 60–80 days or 9 weeks, to be parametrized by the user) based on the Monetary Transmission Mechanism. Research into global liquidity cycles shows that central bank injections (M2 expansion) do not impact high-beta risk assets instantaneously. Capital follows a "Waterfall Effect": it moves first into primary dealer banks, then into credit markets and equities, and finally—once the "liquidity tide" has sufficiently risen—into the cryptocurrency ecosystem. Statistical correlation studies confirm that the peak relationship between Global M2 and Bitcoin historically occurs with a 56 to 63-day delay. By shifting the liquidity data forward, we align the "Macro Cause" with its "Market Effect," revealing a clearer predictive map that standard, unlagged indicators miss.

Settings & Calibration: Tuning the Liquisync Engine

The Liquisync engine is a precision instrument that requires specific calibration to align the "Macro Fuel" with the "Price Engine."

Slope Lookback defines the sensitivity of our acceleration measurement; a setting of 6 (Weekly) or 30 (Daily) ensures we capture structural shifts while filtering out intraday noise

Liquidity Lag is perhaps the most critical setting, as it shifts the M2 data forward to account for the standard 60–80 day (or 9-week) transmission delay—the time it takes for central bank liquidity to actually hit the crypto order books.

Extreme Window establishes our statistical benchmark; by default, this is set to 52 (representing one full year on the Weekly timeframe), allowing the engine to identify "Magenta Star" signals by comparing the current directional desync against the highest records of the last 365 days.

Recommended Calibration :

• Daily (1D): Set Lag to 60–80 and Lookback to 30 .

• Weekly (1W): Set Lag to 9 (9 weeks) and Lookback to 6 . The 1W chart is the preferred filter for macro cycles.

Detailed Script Calculations

The script aggregates liquidity from the FED, RRP, TGA, PBoC, ECB, and BoJ using request.security. We calculate the ta.linreg slope of this aggregate, normalize it via EMA-smoothed RSI mapping (-100 to +100), and apply a ta.change filter to identify directional opposition. The "Extreme" signal is derived from a rolling ta.highest window of the desync intensity.

The Liquisync engine calculates the Linear Regression Slope (m) over a user-defined window:

m =

Where:

• Δy = The distance between the current linear regression end-point and the previous bar.

• Δx = The defined bar-count (Lookback).

Risk Disclaimer & Credits

The Liquisync is a thematic macro tool. Global liquidity data is subject to reporting delays (Note: Because central bank M2 data is typically reported with a lag, the Golden Pulse represents the most recently available macro data, not a real-time high-frequency feed.). This is not financial advice; it is a statistical model for institutional education. Rob Maths is not liable for losses incurred via use of this model.

Tags:

indicator, bitcoin, btc, macro, liquidity, desync, liquisync, institutional, m2, robmaths, Rob Maths

Fast Fourier Transform [ScorsoneEnterprises]The SCE Fast Fourier Transform (FFT) is a tool designed to analyze periodicities and cyclical structures embedded in price. This is a Fourier analysis to transform price data from the time domain into the frequency domain, showing the rhythmic behaviors that are otherwise invisible on standard charts.

Instead of merely observing raw prices, this implementation applies the FFT on the logarithmic returns of the asset:

Log Return(𝑚) = log(close / close )

This ensures stationarity and stabilizes variance, making the analysis statistically robust and less influenced by trends or large price swings.

For a user-defined lookback window 𝑁:

Each frequency component 𝑘 is computed by summing real and imaginary projections of log-returns multiplied by complex exponential functions:

𝑒^−𝑖𝜃 = cos(𝜃)−𝑖sin(𝜃)

where:

θ = 2πkm / N

he result is the magnitude spectrum, calculated as:

Magnitude(𝑘) = sqrt(Real_Sum(𝑘)^2 + Imag_Sum(𝑘)^2)

This spectrum represents the strength of oscillations at each frequency over the lookback period, helping traders identify dominant cycles.

Visual Analysis & Interpretation

To give traders context for the FFT spectrum’s values, this script calculates:

25th Percentile (Purple Line)

Represents relatively low cyclical intensity.

Values below this threshold may signal quiet, noisy, or trendless periods.

75th Percentile (Red Line)

Represents heightened cyclical dominance.

Values above this threshold may indicate significant periodic activity and potential trend formation or rhythm in price action.

The FFT magnitude of the lowest frequency component (index 0) is plotted directly on the chart in teal. Observing how this signal fluctuates relative to its percentile bands provides a dynamic measure of cyclical market activity.

Chart examples

In this NYSE:CL chart, we see the regime of the price accurately described in the spectral analysis. We see the price above the 75th percentile continue to trend higher until it breaks back below.

In long trending markets like NYSE:PL has been, it can give a very good explanation of the strength. There was confidence to not switch regimes as we never crossed below the 75th percentile early in the move.

The script is also usable on the lower timeframes. There is no difference in the usability from the different timeframes.

Script Parameters

Lookback Value (N)

Default: 30

Defines how many bars of data to analyze. Larger N captures longer-term cycles but may smooth out shorter-term oscillations.

Trend Condition [TradersPro]

OVERVIEW

The Trend Condition Indicator measures the strength of the bullish or bearish trend by using a ribbon pattern of exponential moving averages and scoring system. Trend cycles naturally expand and contract as a normal part of the cycle. It is the rhythm of the market. Perpetual expansion and contraction of trend.

As trend cycles develop the indicator shows a compression of the averages. These compression zones are key locations as trends typically expand from there. The expansion of trend can be up or down.

As the trend advances the ribbon effect of the indicator can be seen as each average expands with the price action. Once they have “fanned” the probability of the current trend slowing is high.

This can be used to recognize a powerful trend may be concluding. Traders can tighten stops, exit positions or utilize other prudent strategies.

CONCEPTS

Each line will display green if it is higher than the prior period and red if it is lower than the prior period. If the average is green it is considered bullish and will score one point in the bullish display. Red lines are considered bearish and will score one point in the bearish display.

The indicator can then be used at a quick glance to see the number of averages that are bullish and the number that are bearish.

A trader may use these on any tradable instrument. They can be helpful in stock portfolio management when used with an index like the S&P 500 to determine the strength of the current market trend. This may affect trade decisions like possession size, stop location and other risk factors.

Phase-Accumulation Adaptive EMA w/ Expanded Source Types [Loxx]Phase-Accumulation Adaptive EMA w/ Expanded Source Types is a Phase Accumulation Adaptive Exponential Moving Average with Loxx's Expanded Source Types. This indicator is meant to better capture trend movements using dominant cycle inputs. Alerts are included.

What is Phase Accumulation?

The phase accumulation method of computing the dominant cycle is perhaps the easiest to comprehend. In this technique, we measure the phase at each sample by taking the arctangent of the ratio of the quadrature component to the in-phase component. A delta phase is generated by taking the difference of the phase between successive samples. At each sample we can then look backwards, adding up the delta phases.When the sum of the delta phases reaches 360 degrees, we must have passed through one full cycle, on average.The process is repeated for each new sample.

The phase accumulation method of cycle measurement always uses one full cycle’s worth of historical data.This is both an advantage and a disadvantage.The advantage is the lag in obtaining the answer scales directly with the cycle period.That is, the measurement of a short cycle period has less lag than the measurement of a longer cycle period. However, the number of samples used in making the measurement means the averaging period is variable with cycle period. longer averaging reduces the noise level compared to the signal.Therefore, shorter cycle periods necessarily have a higher out- put signal-to-noise ratio.

Included:

-Toggle on/off bar coloring

-Alerts

Regime MapRegime Map — Volatility State Detector

This indicator is a PineScript friendly approximation of a more advanced Python regime-analysis engine.

The original backed identifies market regimes using structural break detection, Hidden-Markov Models, wavelet decomposition, and long-horizon volatility clustering. Since Pine Script cannot execute these statistical models directly, this version implements a lightweight, real-time proxy using realised volatility and statistical thresholds.

The purpose is to provide a clear visual map of evolving volatility conditions without requiring any heavy offline computation.

________________________________________

Mathematical Basis: Python vs Pine

1. Volatility Estimation

Python (Realised Volatility):

RVₜ = √N × stdev( log(Pₜ) − log(Pₜ₋₁) )

Pine Approximation:

RVₜ = stdev( log(Pₜ) − log(Pₜ₋₁), lookback )

Rationale:

Realised volatility captures volatility clustering — a key characteristic of regime transitions.

________________________________________

2. Regime Classification

Python (HMM Volatility States):

Volatility is modelled as belonging to hidden states with different means and variances:

State μ₁, σ₁

State μ₂, σ₂

State μ₃, σ₃

with state transitions determined by a probability matrix.

Pine Approximation (Z-Score Regimes):

Zₜ = ( RVₜ − mean(RV) ) / stdev(RV)

Regime assignment:

• Regime 0 (Low Vol): Zₜ < Zₗₒw

• Regime 1 (Normal): Zₗₒw ≤ Zₜ ≤ Zₕᵢgh

• Regime 2 (High Vol): Zₜ > Zₕᵢgh

Rationale:

Z-scores provide clean statistical boundaries that behave similarly to HMM state separation but are computable in real time.

________________________________________

3. Structural Break Detection vs Rolling Windows

Python (Bai–Perron Structural Breaks):

Segments the volatility series into periods with distinct statistical properties by minimising squared error over multiple regimes.

Pine Approximation:

Rolling mean and rolling standard deviation of volatility over a long window.

Rationale:

When structural breaks are not available, long-window smoothing approximates slow regime changes effectively.

________________________________________

4. Multi-Scale Cycles

Python (Wavelet Decomposition):

Volatility decomposed into long-cycle (A₄) and short-cycle components (D bands).

Pine Approximation:

Single-scale smoothing using long-horizon averages of RV.

Rationale:

Wavelets reveal multi-frequency behaviour; Pine captures the dominant low-frequency component.

________________________________________

Indicator Output

The background colour reflects the active volatility regime:

• Low Volatility (Green): trending behaviour, cleaner directional movement

• Normal Volatility (Yellow): balanced environment

• High Volatility (Red): sharp swings, traps, mean-reversion phases

Regime labels appear on the chart, with a status panel displaying the current regime.

________________________________________

Operational Logic

1. Compute log returns

2. Calculate short-horizon realised volatility

3. Compute long-horizon mean and standard deviation

4. Derive volatility Z-score

5. Assign regime classification

6. Update background colour and labels

This provides a stable, real-time map of market state transitions.

________________________________________

Practical Applications

Intraday Trading

• Low-volatility regimes favour trend and breakout continuation

• High-volatility regimes favour mean reversion and wide stop placement

Swing Trading

• Compression phases often precede multi-day trending moves

• Volatility expansions accompany distribution or panic events

Risk Management

• Enables volatility-adjusted position sizing

• Helps avoid leverage during expansion regimes

________________________________________

Notes

• Does not repaint

• Fully configurable thresholds and lookbacks

• Works across indices, stocks, FX, crypto

• Designed for real-time volatility regime identification

________________________________________

Disclaimer

This script is intended solely for educational and research purposes.

It does not constitute financial advice or a recommendation to buy or sell any instrument.

Trading involves risk, and past volatility patterns do not guarantee future outcomes.

Users are responsible for their own trading decisions, and the author assumes no liability for financial loss.

Transfer Function Filter [theUltimator5]The Transfer Function Filter is an engineering style approach to transform the price action on a chart into a frequency, then filter out unwanted signals using Butterworth-style filter approach.

This indicator allows you to analyze market structure by isolating or removing different frequency components of price movement—similar to how engineers filter signals in control systems and electrical circuits.

🔎 Features

Four Filter Types

1) Low Pass Filter – Smooths price data, highlighting long-term trends while filtering out short-term noise. This filter acts similar to an EMA, removing noisy signals, resulting in a smooth curve that follows the price of the stock relative to the filter cutoff settings.

Real world application for low pass filter - Used in power supplies to provide a clean, stable power level.

2) High Pass Filter – Removes slow-moving trends to emphasize short-term volatility and rapid fluctuations. The high pass filter removes the "DC" level of the chart, removing the average price moves and only outputting volatility.

Real world application for high pass filter - Used in audio equalizers to remove low-frequency noise (like rumble) while allowing higher frequencies to pass through, improving sound clarity.

3) Band Pass Filter – Allows signals to plot only within a band of bar ranges. This filter removes the low pass "DC" level and the high pass "high frequency noise spikes" and shows a signal that is effectively a smoothed volatility curve. This acts like a moving average for volatility.

Real world application for band pass filter - Radio stations only allow certain frequency bands so you can change your radio channel by switching which frequency band your filter is set to.

4) Band Stop Filter – Suppresses specific frequency bands (cycles between two cutoffs). This filter allows through the base price moving average, but keeps the high frequency volatility spikes. It allows you to filter out specific time interval price action.

Real world application for band stop filter - If there is prominent frequency signal in the area which can cause unnecessary noise in your system, a band stop filter can cancel out just that frequency so you get everything else

Configurable Parameters

• Cutoff Periods – Define the cycle lengths (in bars) to filter. This is a bit counter-intuitive with the numbering since the higher the bar count on the low-pass filter, the lower the frequency cutoff is. The opposite holds true for the high pass filter.

• Filter Order – Adjust steepness and responsiveness (higher order = sharper filtering, but with more delay).

• Overlay Option – Display Low Pass & Band Stop outputs directly on the price chart, or in a separate pane. This is enabled by default, plotting the filters that mimic moving averages directly onto the chart.

• Source Selection – Apply filters to close, open, high, low, or custom sources.

Histograms for Comparison

• BS–LP Histogram – Shows distance between Band Stop and Low Pass filters.

• BP–HP Histogram – Highlights differences between Band Pass and High Pass filters.

Histograms give the visualization of a pseudo-MACD style indicator

Visual & Informational Aids

• Customizable colors for each filter line.

• Optional zero-line for histogram reference.

• On-chart info table summarizing active filters, cutoff settings, histograms, and filter order.

📊 Use Cases

Trend Detection – Use the Low Pass filter to smooth noise and follow underlying market direction.

Volatility & Cycle Analysis – Apply High Pass or Band Pass to capture shorter-term patterns.

Noise Suppression – Deploy Band Stop to remove specific choppy frequencies.

Momentum Insight – Watch the histograms to spot divergences and relative filter strength.

E9 PLRRThe E9 PLRR (Power Law Residual Ratio) is a custom-built indicator designed to evaluate the overvaluation or undervaluation of an asset, specifically by utilizing logarithmic price data and a power law-based model. It leverages a dynamic regression technique to assess the deviation of the current price from its expected value, giving insights into how much the price deviates from its long-term trend.

This indicator is primarily used to detect market extremes and cycles, often used in the analysis of long-term price movements in assets like Bitcoin, where cyclical behavior and significant price deviations are common.

This chart is back from 2019 and shows (From left to right) 2018 Bear market bottom at $3.5k (Dark Blue) , following a peak at 12k (dark red) before the Covid crash back down to EUROTLX:4K (Dark blue)

Key Components

Logarithmic Price Data:

The indicator works with logarithmic price data (ohlc4), which represents the average of open, high, low, and close prices. The logarithmic transformation is crucial in financial modeling, especially when analyzing long-term price data, as it normalizes exponential price growth patterns.

Dynamic Exponent 𝑘:

The model calculates a dynamic exponent k using regression, which defines the power law relationship between time and price. This exponent is essential in determining the expected power law price return and how far the current price deviates from that expected trend.

Power Law Price Return:

The power law price return is computed using the dynamic exponent

k over a defined period, such as 365 days (1 year). It represents the theoretical price return based on a power law relationship, which is used to compare against the actual logarithmic price data.

Risk-Free Rate:

The indicator incorporates an adjustable risk-free rate, allowing users to model the opportunity cost of holding an asset compared to risk-free alternatives. By default, the risk-free rate is set to 0%, but this can be modified depending on the user's requirements.

Volatility Adjustment:

A key feature of the PLRR is its ability to adjust for price volatility. The indicator smooths out short-term price fluctuations using a moving average, helping to detect longer-term cycles and trends.

PLRR Calculation:

The core of the indicator is the calculation of the Power Law Residual Ratio (PLRR). This is derived by subtracting the expected power law price return and risk-free rate from the logarithmic price return, then multiplying the result by a user-defined multiplier.

Color Gradient:

The PLRR values are represented visually using a color gradient. This gradient helps the user quickly identify whether the asset is in an undervalued, fair value, or overvalued state:

Dark Blue to Light Blue: Indicates undervaluation, with increasing blue tones representing a higher degree of undervaluation.

Green to Yellow: Represents fair value, where the price is aligned with the expected power law return.

Orange to Dark Red: Indicates overvaluation, with increasing red tones representing a higher degree of overvaluation.

Zero Line:

A zero line is plotted on the indicator chart, serving as a reference point. Values above the zero line suggest potential overvaluation, while values below indicate potential undervaluation.

Dots Visualization:

The PLRR is plotted using dots, with each dot color-coded based on the PLRR value. This dot-based visualization makes it easier to spot significant changes or reversals in market sentiment without overwhelming the user with continuous lines.

Bar Coloring:

The chart’s bars are colored in accordance with the PLRR value at each point in time, making it visually clear when an asset is potentially overvalued or undervalued.

Indicator Functionality

Cycle Identification : The E9 PLRR is especially useful for identifying cyclical market behavior. In assets like Bitcoin, which are known for their boom-bust cycles, the PLRR can help pinpoint when the market is likely entering a peak (overvaluation) or a trough (undervaluation).

Overvaluation and Undervaluation Detection: By comparing the current price to its expected power law return, the PLRR helps traders assess whether an asset is trading above or below its fair value. This is critical for long-term investors seeking to enter the market at undervalued levels and exit during periods of overvaluation.

Trend Following: The indicator helps users identify the broader trend by smoothing out short-term volatility. This makes it useful for both momentum traders looking to ride trends and contrarian traders seeking to capitalize on market extremes.

Customization

The E9 PLRR allows users to fine-tune several parameters based on their preferences or specific market conditions:

Lookback Period:

The user can adjust the lookback period (default: 100) to modify how the moving average and regression are calculated.

Risk-Free Rate:

Adjusting the risk-free rate allows for more realistic modeling of the opportunity cost of holding the asset.

Multiplier:

The multiplier (default: 5.688) amplifies the sensitivity of the PLRR, allowing users to adjust how aggressively the indicator responds to price movements.

This indicator was inspired by the works of Ashwin & PlanG and their work around powerLaw. Thank you. I hall be working on the calculation of this indicator moving forward to make improvements and optomisations.