Systemic Net Liquidity (Macro Fuel for Crypto & Stocks)This indicator tracks Systemic Net Liquidity, the single most important macro factor for determining the long-term trend of risk assets like Bitcoin (BTC) and major indices (S&P 500). It measures the amount of actual cash available in the financial system to chase speculative assets, distinguishing between money that is circulating and money that is locked up at the Federal Reserve.

Mechanism (What It Measures)

The script uses direct data from the FRED (Federal Reserve Economic Data) to calculate the true state of market funding:

\text{Net Liquidity} = \text{Fed Assets (WALCL)} - \text{Treasury General Account (TGA)} - \text{Reverse Repo (RRP)}

1. Fed Assets (WALCL): The total balance sheet of the Fed (The overall supply of money).

2. Treasury General Account (TGA): Funds the US Treasury collects via bond issuance. When the TGA rises, liquidity is actively drained from the banking system (A major bearish pressure).

3. Overnight Reverse Repo (RRP): Cash parked by banks and money market funds at the Fed, effectively frozen and not contributing to market activity.

How to Interpret Signals

Treat the Net Liquidity line as the market's "Fuel Gauge":

📈 BULLISH SIGNAL (Liquidity Injection): When the Net Liquidity line is rising, money is flowing back into the system, signalling a tailwind for risk assets.

📉 BEARISH SIGNAL (Liquidity Drain): When the line is falling (often due to high TGA balances), cash is being removed. This signals major friction and pressure on price action.

⚠️ DIVERGENCE WARNING: A strong signal is generated when Price (e.g., BTC) rises, but Net Liquidity falls. This macro divergence strongly suggests a major trend reversal or correction is imminent.

Important Notes

Data Source: Data is directly sourced from FRED and updates daily/weekly. This tool is best used for macro analysis and identifying high-level cycles, not short-term scalping.

Disclaimer: Use this indicator as a confirmation tool within your broader strategy. It is not a standalone trading signal.

Cerca negli script per "Cycle"

Quantura - Average Intraday Candle VolumeIntroduction

“Quantura – Average Intraday Candle Volume” is a quantitative visualization tool that calculates and displays the average traded volume for each intraday time position based on a user-defined historical lookback period. It allows traders to analyze recurring intraday volume patterns, identify high-activity sessions, and detect liquidity shifts throughout the trading day.

Originality & Value

This indicator goes beyond standard volume averages by normalizing and aligning volume data according to the time of day. Instead of simply smoothing recent bars, it builds an intraday volume profile based on historical daily averages, enabling users to understand when during the day volume typically peaks or drops.

Its originality and usefulness come from:

Converting standard volume data into time-aligned intraday averages.

Visualization of historical intraday liquidity behavior, not just total daily volume.

Dynamic scaling using normalization and transparency to emphasize active and quiet periods.

Optional day-separator lines for precise intraday structure recognition.

Gradient-based coloring for better visual interpretation of volume intensity.

Functionality & Core Logic

The indicator divides each day into discrete intraday time positions (based on chart timeframe).

For each position, it stores and updates historical volume values across the selected number of days.

It calculates an average volume per time position by aggregating all stored values and dividing them by the number of valid days.

The result is plotted as a continuous histogram showing typical intraday volume distribution.

The bar colors and transparency dynamically reflect the relative intensity of volume at each point in the day.

Parameters & Customization

Number of Days for Averaging: Defines how many past days are included in the volume average calculation (default: 365).

UTC Offset: Allows synchronization of intraday cycles with local or exchange time zones.

Base Color: Sets the main color for plotted volume columns.

Color Mode: Choose between “Gradient” (transparency dynamically adjusts by intensity) or “Normal” (fixed opacity).

Day Line: Toggles dashed vertical lines marking the start of each trading day.

Visualization & Display

Volume is plotted as a series of histogram bars, each representing the average volume for a specific intraday time position.

A gradient color mode enhances readability by fading lower-intensity areas and highlighting high-volume regions.

Optional day-separator lines visually segment historical sessions for easy reference.

Works seamlessly across all chart timeframes that divide the 24-hour day into regular bar intervals.

Use Cases

Identify when trading activity typically peaks (e.g., session opens, news windows, or overlapping markets).

Compare current intraday volume to historical averages for early anomaly detection.

Enhance algorithmic or discretionary strategies that depend on volume-timing alignment.

Combine with volatility or price structure indicators to confirm market activity zones.

Evaluate session consistency across different time zones using the UTC offset parameter.

Limitations & Recommendations

The indicator requires intraday data (below 1D resolution) to function properly.

Volume behavior may vary across brokers and assets; adjust averaging period accordingly.

Does not predict price movement — it provides volume-based context for analysis.

Works best when combined with structure or momentum-based indicators.

Markets & Timeframes

Compatible with all intraday markets — including crypto, Forex, equities, and futures — and all intraday timeframes (from 1 minute to 4 hours). It is particularly valuable for analyzing assets with continuous 24-hour trading activity.

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Important

This description complies with TradingView’s Script Publishing and House Rules. It provides a clear explanation of the indicator’s originality, logic, and purpose, without any unrealistic performance or predictive claims.

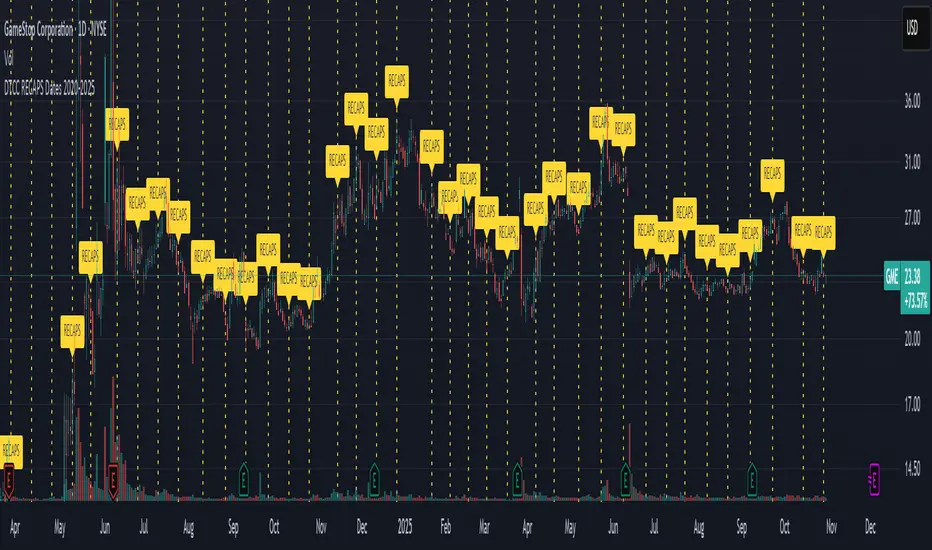

DTCC RECAPS Dates 2020-2025This is a simple indicator which marks the RECAPS dates of the DTCC, during the periods of 2020 to 2025.

These dates have marked clear settlement squeezes in the past, such as GME's squeeze of January 2021.

------------------------------------------------------------------------------------------------------------------

The Depository Trust & Clearing Corporation (DTCC) has published the 2025 schedule for its Reconfirmation and Re-pricing Service (RECAPS) through the National Securities Clearing Corporation (NSCC). RECAPS is a monthly process for comparing and re-pricing eligible equities, municipals, corporate bonds, and Unit Investment Trusts (UITs) that have aged two business days or more .

At its core, the Reconfirmation and Re-pricing Service (RECAPS) is a risk management tool used by the National Securities Clearing Corporation (NSCC), a subsidiary of the DTCC. Its primary purpose is to reduce the risks associated with aged, unsettled trades in the U.S. securities market .

When a trade is executed, it is sent to the NSCC for clearing and settlement. However, for various reasons, some trades may not settle on their scheduled date and become "aged." These unsettled trades create risk for both the trading parties and the clearinghouse (NSCC) because the value of the underlying securities can change over time. If a trade fails to settle and one of the parties defaults, the NSCC may have to step in to complete the transaction at the current market price, which could result in a loss.

RECAPS mitigates this risk by systematically re-pricing these aged, open trading obligations to the current market value. This process ensures that the financial obligations of the clearing members accurately reflect the present value of the securities, preventing the accumulation of significant, unmanaged market risk .

Detailed Mechanics: How Does it Work?

The RECAPS process revolves around two key dates you asked about: the RECAPS Date and the Settlement Date .

The RECAPS Date: On this day, the NSCC runs a process to identify all eligible trades that have remained unsettled for two business days or more. These "aged" trades are then re-priced to the current market value. This re-pricing is not just a simple recalculation; it generates new settlement instructions. The original, unsettled trade is effectively cancelled and replaced with a new one at the current market price. This is done through the NSCC's Obligation Warehouse.

The Settlement Date: This is typically the business day following the RECAPS date. On this date, the financial settlement of the re-priced trades occurs. The difference in value between the original trade price and the new, re-priced value is settled between the two trading parties. This "mark-to-market" adjustment is processed through the members' settlement accounts at the DTCC.

Essentially, the process ensures that any gains or losses due to price changes in the underlying security are realized and settled periodically, rather than being deferred until the trade is ultimately settled or cancelled.

Are These Dates Used to Check Margin Requirements?

Yes, indirectly, this process is closely tied to managing margin and collateral requirements for NSCC members. Here’s how:

The NSCC requires its members to post collateral to a clearing fund, which acts as a mutualized guarantee against defaults. The amount of collateral each member must provide is calculated based on their potential risk exposure to the clearinghouse.

By re-pricing aged trades to current market values through RECAPS, the NSCC gets a more accurate picture of each member's outstanding obligations and, therefore, their current risk profile. If a member has a large number of unsettled trades that have moved against them in value, the re-pricing will crystallize that loss, which will be settled the next day.

This regular re-pricing and settlement of aged trades prevent the build-up of large, unrealized losses that could increase a member's risk profile beyond what their posted collateral can cover. While RECAPS is not the only mechanism for calculating margin (the NSCC has a complex system for daily margin calls based on overall portfolio risk), it is a crucial component for managing the specific risk posed by aged, unsettled transactions. It ensures that the value of these obligations is kept current, which in turn helps ensure that collateral levels remain adequate.

--------------------------------------------------------------------------------------------------------------

Future dates of 2025:

- November 12, 2025 (Wed)

- November 25, 2025 (Tue)

- December 11, 2025 (Thu)

- December 29, 2025 (Mon)

The dates for 2026 haven't been published yet at this time.

The RECAPS process is essentially the industry's way of retrying the settlement of all unresolved FTDs, netting outstanding obligations, and gradually forcing resolution (either delivery or buy-in). Monitoring RECAPS cycles is one way to track the lifecycle, accumulation, and eventual resolution (or persistence) of failures to deliver in the U.S. market.

The US Stock market has become a game of settlement dates and FTDs, therefore this can be useful to track.

Squeeze Hour Frequency [CHE]Squeeze Hour Frequency (ATR-PR) — Standalone — Tracks daily squeeze occurrences by hour to reveal time-based volatility patterns

Summary

This indicator identifies periods of unusually low volatility, defined as squeezes, and tallies their frequency across each hour of the day over historical trading sessions. By aggregating counts into a sortable table, it helps users spot hours prone to these conditions, enabling better scheduling of trading activity to avoid or target specific intraday regimes. Signals gain robustness through percentile-based detection that adapts to recent volatility history, differing from fixed-threshold methods by focusing on relative lowness rather than absolute levels, which reduces false positives in varying market environments.

Motivation: Why this design?

Traders often face uneven intraday volatility, with certain hours showing clustered low-activity phases that precede or follow breakouts, leading to mistimed entries or overlooked calm periods. The core idea of hourly squeeze frequency addresses this by binning low-volatility events into 24 hourly slots and counting distinct daily occurrences, providing a historical profile of when squeezes cluster. This reveals time-of-day biases without relying on real-time alerts, allowing proactive adjustments to session focus.

What’s different vs. standard approaches?

- Reference baseline: Classical volatility tools like simple moving average crossovers or fixed ATR thresholds, which flag squeezes uniformly across the day.

- Architecture differences:

- Uses persistent arrays to track one squeeze per hour per day, preventing overcounting within sessions.

- Employs custom sorting on ratio arrays for dynamic table display, prioritizing top or bottom performers.

- Handles timezones explicitly to ensure consistent binning across global assets.

- Practical effect: Charts show a persistent table ranking hours by squeeze share, making intraday patterns immediately visible—such as a top hour capturing over 20 percent of total events—unlike static overlays that ignore temporal distribution, which matters for avoiding low-liquidity traps in crypto or forex.

How it works (technical)

The indicator first computes a rolling volatility measure over a specified lookback period. It then derives a relative ranking of the current value against recent history within a window of bars. A squeeze is flagged when this ranking falls below a user-defined cutoff, indicating the value is among the lowest in the recent sample.

On each bar, the local hour is extracted using the selected timezone. If a squeeze occurs and the bar has price data, the count for that hour increments only if no prior mark exists for the current day, using a persistent array to store the last marked day per hour. This ensures one tally per unique trading day per slot.

At the final bar, arrays compile counts and ratios for all 24 hours, where the ratio represents each hour's share of total squeezes observed. These are sorted ascending or descending based on display mode, and the top or bottom subset populates the table. Background shading highlights live squeezes in red for visual confirmation. Initialization uses zero-filled arrays for counts and negative seeds for day tracking, with state persisting across bars via variable declarations.

No higher timeframe data is pulled, so there is no repaint risk from external fetches; all logic runs on confirmed bars.

Parameter Guide

ATR Length — Controls the lookback for the volatility measure, influencing sensitivity to short-term fluctuations; shorter values increase responsiveness but add noise, longer ones smooth for stability — Default: 14 — Trade-offs/Tips: Use 10-20 for intraday charts to balance quick detection with fewer false squeezes; test on historical data to avoid over-smoothing in trending markets.

Percentile Window (bars) — Sets the history depth for ranking the current volatility value, affecting how "low" is defined relative to past; wider windows emphasize long-term norms — Default: 252 — Trade-offs/Tips: 100-300 bars suit daily cycles; narrower for fast assets like crypto to catch recent regimes, but risks instability in sparse data.

Squeeze threshold (PR < x) — Defines the cutoff for flagging low relative volatility, where values below this mark a squeeze; lower thresholds tighten detection for rarer events — Default: 10.0 — Trade-offs/Tips: 5-15 percent for conservative signals reducing false positives; raise to 20 for more frequent highlights in high-vol environments, monitoring for increased noise.

Timezone — Specifies the reference for hourly binning, ensuring alignment with market sessions — Default: Exchange — Trade-offs/Tips: Set to "America/New_York" for US assets; mismatches can skew counts, so verify against chart timezone.

Show Table — Toggles the results display, essential for reviewing frequencies — Default: true — Trade-offs/Tips: Disable on mobile for performance; pair with position tweaks for clean overlays.

Pos — Places the table on the chart pane — Default: Top Right — Trade-offs/Tips: Bottom Left avoids candle occlusion on volatile charts.

Font — Adjusts text readability in the table — Default: normal — Trade-offs/Tips: Tiny for dense views, large for emphasis on key hours.

Dark — Applies high-contrast colors for visibility — Default: true — Trade-offs/Tips: Toggle false in light themes to prevent washout.

Display — Filters table rows to focus on extremes or full list — Default: All — Trade-offs/Tips: Top 3 for quick scans of risky hours; Bottom 3 highlights safe low-squeeze periods.

Reading & Interpretation

Red background shading appears on bars meeting the squeeze condition, signaling current low relative volatility. The table lists hours as "H0" to "H23", with columns for daily squeeze counts, percentage share of total squeezes (summing to 100 percent across hours), and an arrow marker on the top hour. A summary row above details the peak count, its share, and the leading hour. A label at the last bar recaps total days observed, data-valid days, and top hour stats. Rising shares indicate clustering, suggesting regime persistence in that slot.

Practical Workflows & Combinations

- Trend following: Scan for hours with low squeeze shares to enter during stable regimes; confirm with higher highs or lower lows on the 15-minute chart, avoiding top-share hours post-news like tariff announcements.

- Exits/Stops: Tighten stops in high-share hours to guard against sudden vol spikes; use the table to shift to conservative sizing outside peak squeeze times.

- Multi-asset/Multi-TF: Defaults work across crypto pairs on 5-60 minute timeframes; for stocks, widen percentile window to 500 bars. Combine with volume oscillators—enter only if squeeze count is below average for the asset.

Behavior, Constraints & Performance

Logic executes on closed bars, with live bars updating counts provisionally but finalizing on confirmation; table refreshes only at the last bar, avoiding intrabar flicker. No security calls or higher timeframes, so no repaint from external data. Resources include a 5000-bar history limit, loops up to 24 iterations for sorting and totals, and arrays sized to 24 elements; labels and table are capped at 500 each for efficiency. Known limits: Skips hours without bars (e.g., weekends), assumes uniform data availability, and may undercount in sparse sessions; timezone shifts can alter profiles without warning.

Sensible Defaults & Quick Tuning

Start with ATR Length at 14, Percentile Window at 252, and threshold at 10.0 for broad crypto use. If too many squeezes flag (noisy table), raise threshold to 15.0 and narrow window to 100 for stricter relative lowness. For sluggish detection in calm markets, drop ATR Length to 10 and threshold to 5.0 to capture subtler dips. In high-vol assets, widen window to 500 and threshold to 20.0 for stability.

What this indicator is—and isn’t

This is a historical frequency tracker and visualization layer for intraday volatility patterns, best as a filter in multi-tool setups. It is not a standalone signal generator, predictive model, or risk manager—pair it with price action, news filters, and position sizing rules.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Thanks to Duyck

for the ma sorter

Nth Candle by exp3rtsThis lightweight and versatile TradingView indicator highlights every Xth candle on your chart, making it easy to spot cyclical price behavior or track specific intervals in the market.

- Custom Interval – Choose how often candles should be highlighted (e.g., every 5th, 10th, or

20th bar).

- Color Coding – Highlighted candles are shaded green if bullish and red if bearish, giving you

quick visual insights into momentum at those intervals.

- Clean Overlay – The indicator draws directly on your main chart without clutter, so you can

combine it with your favorite setups and strategies.

Use this tool to:

1) Identify repeating patterns and cycles

2) Mark periodic reference candles

3) Support discretionary trading decisions with clear visual cues

Global Liquidity Proxy vs BitcoinGlobal Liquidity Proxy vs Bitcoin. Helps to understand the cycles with liquidty.

US Presidents 1920–2024Description:

This indicator displays all U.S. presidential elections from 1920 to 2024 on your chart.

Features:

Vertical lines at the date of each presidential election.

Line color by party:

Red = Republican

Blue = Democrat

Gray = Other/None

Labels showing the name of each president.

Modern flag style: Presidents from 1900 onward are highlighted as modern, giving clear historical separation.

Fully overlayed on the price chart for timeline context.

Customizable: Label position (above/below bar) and line width.

Use case: Useful for analyzing modern U.S. presidential cycles, market reactions to elections, or quickly referencing recent presidents directly on charts.

Auto-Fit Growth Trendline# **Theoretical Algorithmic Principles of the Auto-Fit Growth Trendline (AFGT)**

## **🎯 What Does This Algorithm Do?**

The Auto-Fit Growth Trendline is an advanced technical analysis system that **automates the identification of long-term growth trends** and **projects future price levels** based on historical cyclical patterns.

### **Primary Functionality:**

- **Automatically detects** the most significant lows in regular periods (monthly, quarterly, semi-annually, annually)

- **Constructs a dynamic trendline** that connects these historical lows

- **Projects the trend into the future** with high mathematical precision

- **Generates Fibonacci bands** that act as dynamic support and resistance levels

- **Automatically adapts** to different timeframes and market conditions

### **Strategic Purpose:**

The algorithm is designed to identify **fundamental value zones** where price has historically found support, enabling traders to:

- Identify optimal entry points for long positions

- Establish realistic price targets based on mathematical projections

- Recognize dynamic support and resistance levels

- Anticipate long-term price movements

---

## **🧮 Core Mathematical Foundations**

### **Adaptive Temporal Segmentation Theory**

The algorithm is based on **dynamic temporal partition theory**, where time is divided into mathematically coherent uniform intervals. It uses modular transformations to create bijective mappings between continuous timestamps and discrete periods, ensuring each temporal point belongs uniquely to a specific period.

**What does this achieve?** It allows the algorithm to automatically identify natural market cycles (annual, quarterly, etc.) without manual intervention, adapting to the inherent periodicity of each asset.

The temporal mapping function implements a **discrete affine transformation** that normalizes different frequencies (monthly, quarterly, semi-annual, annual) to a space of unique identifiers, enabling consistent cross-temporal comparative analysis.

---

## **📊 Local Extrema Detection Theory**

### **Multi-Point Retrospective Validation Principle**

Local minima detection is founded on **relative extrema theory with sliding window**. Instead of using a simple minimum finder, it implements a cross-validation system that examines the persistence of the extremum across multiple historical periods.

**What problem does this solve?** It eliminates false minima caused by temporal volatility, identifying only those points that represent true historical support levels with statistical significance.

This approach is based on the **statistical confirmation principle**, where a minimum is only considered valid if it maintains its extremum condition during a defined observation period, significantly reducing false positives caused by transitory volatility.

---

## **🔬 Robust Interpolation Theory with Outlier Control**

### **Contextual Adaptive Interpolation Model**

The mathematical core uses **piecewise linear interpolation with adaptive outlier correction**. The key innovation lies in implementing a **contextual anomaly detector** that identifies not only absolute extreme values, but relative deviations to the local context.

**Why is this important?** Financial markets contain extreme events (crashes, bubbles) that can distort projections. This system identifies and appropriately weights them without completely eliminating them, preserving directional information while attenuating distortions.

### **Implicit Bayesian Smoothing Algorithm**

When an outlier is detected (deviation >300% of local average), the system applies a **simplified Kalman filter** that combines the current observation with a local trend estimation, using a weight factor that preserves directional information while attenuating extreme fluctuations.

---

## **📈 Stabilized Extrapolation Theory**

### **Exponential Growth Model with Dampening**

Extrapolation is based on a **modified exponential growth model with progressive dampening**. It uses multiple historical points to calculate local growth ratios, implements statistical filtering to eliminate outliers, and applies a dampening factor that increases with extrapolation distance.

**What advantage does this offer?** Long-term projections in finance tend to be exponentially unrealistic. This system maintains short-to-medium term accuracy while converging toward realistic long-term projections, avoiding the typical "exponential explosions" of other methods.

### **Asymptotic Convergence Principle**

For long-term projections, the algorithm implements **controlled asymptotic convergence**, where growth ratios gradually converge toward pre-established limits, avoiding unrealistic exponential projections while preserving short-to-medium term accuracy.

---

## **🌟 Dynamic Fibonacci Projection Theory**

### **Continuous Proportional Scaling Model**

Fibonacci bands are constructed through **uniform proportional scaling** of the base curve, where each level represents a linear transformation of the main curve by a constant factor derived from the Fibonacci sequence.

**What is its practical utility?** It provides dynamic resistance and support levels that move with the trend, offering price targets and profit-taking points that automatically adapt to market evolution.

### **Topological Preservation Principle**

The system maintains the **topological properties** of the base curve in all Fibonacci projections, ensuring that spatial and temporal relationships are consistently preserved across all resistance/support levels.

---

## **⚡ Adaptive Computational Optimization**

### **Multi-Scale Resolution Theory**

It implements **automatic multi-resolution analysis** where data granularity is dynamically adjusted according to the analysis timeframe. It uses the **adaptive Nyquist principle** to optimize the signal-to-noise ratio according to the temporal observation scale.

**Why is this necessary?** Different timeframes require different levels of detail. A 1-minute chart needs more granularity than a monthly one. This system automatically optimizes resolution for each case.

### **Adaptive Density Algorithm**

Calculation point density is optimized through **adaptive sampling theory**, where calculation frequency is adjusted according to local trend curvature and analysis timeframe, balancing visual precision with computational efficiency.

---

## **🛡️ Robustness and Fault Tolerance**

### **Graceful Degradation Theory**

The system implements **multi-level graceful degradation**, where under error conditions or insufficient data, the algorithm progressively falls back to simpler but reliable methods, maintaining basic functionality under any condition.

**What does this guarantee?** That the indicator functions consistently even with incomplete data, new symbols with limited history, or extreme market conditions.

### **State Consistency Principle**

It uses **mathematical invariants** to guarantee that the algorithm's internal state remains consistent between executions, implementing consistency checks that validate data structure integrity in each iteration.

---

## **🔍 Key Theoretical Innovations**

### **A. Contextual vs. Absolute Outlier Detection**

It revolutionizes traditional outlier detection by considering not only the absolute magnitude of deviations, but their relative significance within the local context of the time series.

**Practical impact:** It distinguishes between legitimate market movements and technical anomalies, preserving important events like breakouts while filtering noise.

### **B. Extrapolation with Weighted Historical Memory**

It implements a memory system that weights different historical periods according to their relevance for current prediction, creating projections more adaptable to market regime changes.

**Competitive advantage:** It automatically adapts to fundamental changes in asset dynamics without requiring manual recalibration.

### **C. Automatic Multi-Timeframe Adaptation**

It develops an automatic temporal resolution selection system that optimizes signal extraction according to the intrinsic characteristics of the analysis timeframe.

**Result:** A single indicator that functions optimally from 1-minute to monthly charts without manual adjustments.

### **D. Intelligent Asymptotic Convergence**

It introduces the concept of controlled asymptotic convergence in financial extrapolations, where long-term projections converge toward realistic limits based on historical fundamentals.

**Added value:** Mathematically sound long-term projections that avoid the unrealistic extremes typical of other extrapolation methods.

---

## **📊 Complexity and Scalability Theory**

### **Optimized Linear Complexity Model**

The algorithm maintains **linear computational complexity** O(n) in the number of historical data points, guaranteeing scalability for extensive time series analysis without performance degradation.

### **Temporal Locality Principle**

It implements **temporal locality**, where the most expensive operations are concentrated in the most relevant temporal regions (recent periods and near projections), optimizing computational resource usage.

---

## **🎯 Convergence and Stability**

### **Probabilistic Convergence Theory**

The system guarantees **probabilistic convergence** toward the real underlying trend, where projection accuracy increases with the amount of available historical data, following **law of large numbers** principles.

**Practical implication:** The more history an asset has, the more accurate the algorithm's projections will be.

### **Guaranteed Numerical Stability**

It implements **intrinsic numerical stability** through the use of robust floating-point arithmetic and validations that prevent overflow, underflow, and numerical error propagation.

**Result:** Reliable operation even with extreme-priced assets (from satoshis to thousand-dollar stocks).

---

## **💼 Comprehensive Practical Application**

**The algorithm functions as a "financial GPS"** that:

1. **Identifies where we've been** (significant historical lows)

2. **Determines where we are** (current position relative to the trend)

3. **Projects where we're going** (future trend with specific price levels)

4. **Provides alternative routes** (Fibonacci bands as alternative targets)

This theoretical framework represents an innovative synthesis of time series analysis, approximation theory, and computational optimization, specifically designed for long-term financial trend analysis with robust and mathematically grounded projections.

Adaptive MVRV & RSI Strategy V6 (Dynamic Thresholds)Strategy Explanation

This is an advanced Dollar-Cost Averaging (DCA) strategy for Bitcoin that aims to adapt to long-term market cycles and changing volatility. Instead of relying on fixed buy/sell signals, it uses a dynamic, weighted approach based on a combination of on-chain data and classic momentum.

Core Components:

Dual-Indicator Signal: The strategy combines two powerful indicators for a more robust signal:

MVRV Ratio: An on-chain metric to identify when Bitcoin is fundamentally over or undervalued relative to its historical cost basis.

Weekly RSI: A classic momentum indicator to gauge long-term market strength and identify overbought/oversold conditions.

Dynamic, Self-Adjusting Thresholds: The core innovation of this strategy is that it avoids fixed thresholds (e.g., "sell when RSI is 70"). Instead, the buy and sell zones are dynamically calculated based on a long-term (2-year) moving average and standard deviation of each indicator. This allows the strategy to automatically adapt to Bitcoin's decreasing volatility and changing market structure over time.

Weighted DCA (Scaling In & Out): The strategy doesn't just buy or sell a fixed amount. The size of its trades is scaled based on conviction:

Buying: As the MVRV and RSI fall deeper into their "undervalued" zones, the percentage of available cash used for each purchase increases.

Selling: As the indicators rise further into "overvalued" territory, the percentage of the current position sold also increases.

This creates an adaptive system that systematically accumulates during periods of fear and distributes during periods of euphoria, with the intensity of its actions directly tied to the extremity of market conditions.

ECG chart - mauricioofsousaMGO Primary – Matriz Gráficos ON

The Blockchain of Trading applied to price behavior

The MGO Primary is the foundation of Matriz Gráficos ON — an advanced graphical methodology that transforms market movement into a logical, predictable, and objective sequence, inspired by blockchain architecture and periodic oscillatory phenomena.

This indicator replaces emotional candlestick reading with a mathematical interpretation of price blocks, cycles, and frequency. Its mission is to eliminate noise, anticipate reversals, and clearly show where capital is entering or exiting the market.

What MGO Primary detects:

Oscillatory phenomena that reveal the true behavior of orders in the book:

RPA – Breakout of Bullish Pivot

RPB – Breakout of Bearish Pivot

RBA – Sharp Bullish Breakout

RBB – Sharp Bearish Breakout

Rhythmic patterns that repeat in medium timeframes (especially on 12H and 4H)

Wave and block frequency, highlighting critical entry and exit zones

Validation through Primary and Secondary RSI, measuring the real strength behind movements

Who is this indicator for:

Traders seeking statistical clarity and visual logic

Operators who want to escape the subjectivity of candlesticks

Anyone who values technical precision with operational discipline

Recommended use:

Ideal timeframes: 12H (high precision) and 4H (moderate intensity)

Recommended assets: indices (e.g., NASDAQ), liquid stocks, and futures

Combine with: structured risk management and macro context analysis

Real-world performance:

The MGO12H achieved a 92% accuracy rate in 2025 on the NASDAQ, outperforming the average performance of major global quantitative strategies, with a net score of over 6,200 points for the year.

BUY in HASH RibbonsHash Ribbons Indicator (BUY Signal)

A TradingView Pine Script v6 implementation for identifying Bitcoin miner capitulation (“Springs”) and recovery phases based on hash rate data. It marks potential low-risk buying opportunities by tracking short- and long-term moving averages of the network hash rate.

⸻

Key Features

• Hash Rate SMAs

• Short-term SMA (default: 30 days)

• Long-term SMA (default: 60 days)

• Phase Markers

• Gray circle: Short SMA crosses below long SMA (start of capitulation)

• White circles: Ongoing capitulation, with brighter white when the short SMA turns upward

• Yellow circle: Short SMA crosses back above long SMA (end of capitulation)

• Orange circle: Buy signal once hash rate recovery aligns with bullish price momentum (10-day price SMA crosses above 20-day price SMA)

• Display Modes

• Ribbons: Plots the two SMAs as colored bands—red for capitulation, green for recovery

• Oscillator: Shows the percentage difference between SMAs as a histogram (red for negative, blue for positive)

• Optional Overlays

• Bitcoin halving dates (2012, 2016, 2020, 2024) with dashed lines and labels

• Raw hash rate data in EH/s

• Alerts

• Configurable alerts for capitulation start, recovery, and buy signals

⸻

How It Works

1. Data Source: Fetches daily hash rate values from a selected provider (e.g., IntoTheBlock, Quandl).

2. Capitulation Detection: When the 30-day SMA falls below the 60-day SMA, miners are likely capitulating.

3. Recovery Identification: A rising 30-day SMA during capitulation signals miner recovery.

4. Buy Signal: Confirmed when the hash rate recovery coincides with a bullish shift in price momentum (10-day price SMA > 20-day price SMA).

⸻

Inputs

Hash Rate Short SMA: 30 days

Hash Rate Long SMA: 60 days

Plot Signals: On

Plot Halvings: Off

Plot Raw Hash Rate: Off

⸻

Considerations

• Timeframe: Best applied on daily charts to capture meaningful miner behavior.

• Data Reliability: Ensure the chosen hash rate source provides consistent, gap-free data.

• Risk Management: Use alongside other technical indicators (e.g., RSI, MACD) and fundamental analysis.

• Backtesting: Evaluate performance over different market cycles before live deployment.

Economy RadarEconomy Radar — Key US Macro Indicators Visualized

A handy tool for traders and investors to monitor major US economic data in one chart.

Includes:

Inflation: CPI, PCE, yearly %, expectations

Monetary policy: Fed funds rate, M2 money supply

Labor market: Unemployment, jobless claims, consumer sentiment

Economy & markets: GDP, 10Y yield, US Dollar Index (DXY)

Options:

Toggle indicators on/off

Customizable colors

Tooltips explain each metric (in Russian & English)

Perfect for spotting economic cycles and supporting trading decisions.

Add to your chart and get a clear macro picture instantly!

[Mustang Algo] Channel Strategy# Mustang Algo Channel Strategy - Universal Market Sentiment Oscillator

## 🎯 ORIGINAL CONCEPT

This strategy employs a unique market sentiment oscillator that works on ALL financial assets. It uses Bitcoin supply dynamics combined with stablecoin market capitalization as a macro sentiment indicator to generate universal timing signals across stocks, forex, commodities, indices, and cryptocurrencies.

## 🌐 UNIVERSAL APPLICATION

- **Any Asset Class:** Stocks, Forex, Commodities, Indices, Crypto, Bonds

- **Market-Wide Timing:** BTC/Stablecoin ratio serves as a global risk sentiment gauge

- **Cross-Market Signals:** Trade any instrument using macro liquidity conditions

- **Ecosystem Approach:** One oscillator for all financial markets

## 🧮 METHODOLOGY

**Core Calculation:** BTC Supply / (Combined Stablecoin Market Cap / BTC Price)

- **Data Sources:** DAI + USDT + USDC market capitalizations

- **Signal Generation:** RSI(14) applied to the ratio, double-smoothed with WMA

- **Timing Logic:** Crossover signals filtered by overbought/oversold zones

- **Multi-Timeframe:** Configurable timeframe analysis (default: Daily)

## 📈 TRADING STRATEGY

**LONG Entries:** Bullish crossover when market sentiment is oversold (<48)

**SHORT Entries:** Bearish crossover when market sentiment is overbought (>55)

**Universal Timing:** These macro signals apply to trading any financial instrument

## ⚙️ FLEXIBLE RISK MANAGEMENT

**Three SL/TP Calculation Modes:**

- **Percentage Mode:** Traditional % based (4% SL, 12% TP default)

- **Ticks Mode:** Precise tick-based calculation (50/150 ticks default)

- **Pips Mode:** Forex-style pip calculation (50/150 pips default)

**Realistic Parameters:**

- Commission: 0.1% (adjustable for different asset classes)

- Slippage: 2 ticks

- Position sizing: 10% of equity (conservative)

- No pyramiding (single position management)

## 📊 KEY ADVANTAGES

✅ **Universal Application:** One strategy for all asset classes

✅ **Macro Foundation:** Based on global liquidity and risk sentiment

✅ **False Signal Filtering:** Overbought/oversold zones reduce noise

✅ **Flexible Risk Management:** Multiple SL/TP calculation methods

✅ **No Lookahead Bias:** Clean backtesting with realistic results

✅ **Cross-Market Correlation:** Captures broad market risk cycles

## 🎛️ CONFIGURATION GUIDE

1. **Asset Selection:** Apply to stocks, forex, commodities, indices, crypto

2. **Timeframe Setup:** Daily recommended for swing trading

3. **Sentiment Bounds:** Adjust 48/55 levels based on market volatility

4. **Risk Management:** Choose appropriate SL/TP mode for your asset class

5. **Direction Filter:** Select Long Only, Short Only, or Both

## 📋 BACKTESTING STANDARDS

**Compliant with TradingView Guidelines:**

- ✅ Realistic commission structure (0.1% default)

- ✅ Appropriate slippage modeling (2 ticks)

- ✅ Conservative position sizing (10% equity)

- ✅ Sustainable risk ratios (1:3 SL/TP)

- ✅ No lookahead bias (proper historical simulation)

- ✅ Sufficient sample size potential (100+ trades possible)

## 🔬 ORIGINAL RESEARCH

This strategy introduces a revolutionary approach to financial markets by treating the BTC/Stablecoin ratio as a global risk sentiment gauge. Unlike traditional indicators that analyze individual asset price action, this oscillator captures macro liquidity flows that affect ALL financial markets - from stocks to forex to commodities.

## 🎯 MARKET APPLICATIONS

**Stocks & Indices:** Risk-on/risk-off sentiment timing

**Forex:** Global liquidity flow analysis for major pairs

**Commodities:** Risk appetite for inflation hedges

**Bonds:** Flight-to-safety vs. risk-seeking behavior

**Crypto:** Native application with direct correlation

## ⚠️ RISK DISCLOSURE

- Designed for intermediate to long-term trading across all timeframes

- Market sentiment can remain extreme longer than expected

- Always use appropriate position sizing for your specific asset class

- Adjust commission and slippage settings for different markets

- Past performance does not guarantee future results

## 🚀 INNOVATION SUMMARY

**What makes this strategy unique:**

- First to use BTC/Stablecoin ratio as universal market sentiment indicator

- Applies macro-economic principles to technical analysis across all assets

- Single oscillator provides timing signals for entire financial ecosystem

- Bridges traditional finance with digital asset insights

- Combines fundamental liquidity analysis with technical precision

RSI - PRIMARIO -mauricioofsousa

MGO Primary – Matriz Gráficos ON

The Blockchain of Trading applied to price behavior

The MGO Primary is the foundation of Matriz Gráficos ON — an advanced graphical methodology that transforms market movement into a logical, predictable, and objective sequence, inspired by blockchain architecture and periodic oscillatory phenomena.

This indicator replaces emotional candlestick reading with a mathematical interpretation of price blocks, cycles, and frequency. Its mission is to eliminate noise, anticipate reversals, and clearly show where capital is entering or exiting the market.

What MGO Primary detects:

Oscillatory phenomena that reveal the true behavior of orders in the book:

RPA – Breakout of Bullish Pivot

RPB – Breakout of Bearish Pivot

RBA – Sharp Bullish Breakout

RBB – Sharp Bearish Breakout

Rhythmic patterns that repeat in medium timeframes (especially on 12H and 4H)

Wave and block frequency, highlighting critical entry and exit zones

Validation through Primary and Secondary RSI, measuring the real strength behind movements

Who is this indicator for:

Traders seeking statistical clarity and visual logic

Operators who want to escape the subjectivity of candlesticks

Anyone who values technical precision with operational discipline

Recommended use:

Ideal timeframes: 12H (high precision) and 4H (moderate intensity)

Recommended assets: indices (e.g., NASDAQ), liquid stocks, and futures

Combine with: structured risk management and macro context analysis

Real-world performance:

The MGO12H achieved a 92% accuracy rate in 2025 on the NASDAQ, outperforming the average performance of major global quantitative strategies, with a net score of over 6,200 points for the year.

Sun Moon Conjunctions Trine Oppositions 2025this script is an astrological tool designed to overlay significant Sun-Moon aspect events for 2025 on a Bitcoin chart. It highlights key lunar phases and aspects—Conjunctions (New Moon) in blue, Squares in red, Oppositions (Full Moon) in purple, and Trines in green—using background colors and labeled markers. Users can toggle visibility for each aspect type and adjust label sizes via customizable inputs. The script accurately marks events from January through December 2025, with labels appearing once per event, making it a valuable resource for exploring potential correlations between lunar cycles and Bitcoin price movements.

Planetary Retrograde DashboardThe Retrograde Dashboard offers a quick overview of all planets and their historical and current retrograde statuses across various time frames.

How This Indicator Works

Custom Overlay: The indicator displays its own overlay, plotting the periods of planetary retrograde. This enables users to visually track all planetary retrogrades over time, both historically and in real-time.

When a planet is in retrograde, its symbol will show the ℞ retrograde symbol next to it.

When a planet is in direct motion, only the planetary symbol is visible.

The indicator adapts to different timeframes, allowing you to analyze whether a planet was in retrograde at any specific moment.

What is Retrograde Motion?

In astrology and astro-finance, retrograde motion occurs when a planet seems to move backward in the sky from Earth's perspective. Although this is an optical illusion due to differences in orbital speeds, many traders and analysts believe that planetary retrogrades can influence market behavior. Retrogrades are often linked with reassessment, reversals, and shifts in momentum, making them valuable for both historical and predictive market analysis.

Research & Discovery – Compare planetary retrograde cycles with historical market behavior to identify potential correlations.

Created using Astrolib by @BarefootJoey

[COG] Adaptive Squeeze Intensity 📊 Adaptive Squeeze Intensity (ASI) Indicator

🎯 Overview

The Adaptive Squeeze Intensity (ASI) indicator is an advanced technical analysis tool that combines the power of volatility compression analysis with momentum, volume, and trend confirmation to identify high-probability trading opportunities. It quantifies the degree of price compression using a sophisticated scoring system and provides clear entry signals for both long and short positions.

⭐ Key Features

- 📈 Comprehensive squeeze intensity scoring system (0-100)

- 📏 Multiple Keltner Channel compression zones

- 📊 Volume analysis integration

- 🎯 EMA-based trend confirmation

- 🎨 Proximity-based entry validation

- 📱 Visual status monitoring

- 🎨 Customizable color schemes

- ⚡ Clear entry signals with directional indicators

🔧 Components

1. 📐 Squeeze Intensity Score (0-100)

The indicator calculates a total squeeze intensity score based on four components:

- 📊 Band Convergence (0-40 points): Measures the relationship between Bollinger Bands and Keltner Channels

- 📍 Price Position (0-20 points): Evaluates price location relative to the base channels

- 📈 Volume Intensity (0-20 points): Analyzes volume patterns and thresholds

- ⚡ Momentum (0-20 points): Assesses price momentum and direction

2. 🎨 Compression Zones

Visual representation of squeeze intensity levels:

- 🔴 Extreme Squeeze (80-100): Red zone

- 🟠 Strong Squeeze (60-80): Orange zone

- 🟡 Moderate Squeeze (40-60): Yellow zone

- 🟢 Light Squeeze (20-40): Green zone

- ⚪ No Squeeze (0-20): Base zone

3. 🎯 Entry Signals

The indicator generates entry signals based on:

- ✨ Squeeze release confirmation

- ➡️ Momentum direction

- 📊 Candlestick pattern confirmation

- 📈 Optional EMA trend alignment

- 🎯 Customizable EMA proximity validation

⚙️ Settings

🔧 Main Settings

- Base Length: Determines the calculation period for main indicators

- BB Multiplier: Sets the Bollinger Bands deviation multiplier

- Keltner Channel Multipliers: Three separate multipliers for different compression zones

📈 Trend Confirmation

- Four customizable EMA periods (default: 21, 34, 55, 89)

- Optional trend requirement for entry signals

- Adjustable EMA proximity threshold

📊 Volume Analysis

- Customizable volume MA length

- Adjustable volume threshold for signal confirmation

- Option to enable/disable volume analysis

🎨 Visualization

- Customizable bullish/bearish colors

- Optional intensity zones display

- Status monitor with real-time score and state information

- Clear entry arrows and background highlights

💻 Technical Code Breakdown

1. Core Calculations

// Base calculations for EMAs

ema_1 = ta.ema(close, ema_length_1)

ema_2 = ta.ema(close, ema_length_2)

ema_3 = ta.ema(close, ema_length_3)

ema_4 = ta.ema(close, ema_length_4)

// Proximity calculation for entry validation

ema_prox_raw = math.abs(close - ema_1) / ema_1 * 100

is_close_to_ema_long = close > ema_1 and ema_prox_raw <= prox_percent

```

### 2. Squeeze Detection System

```pine

// Bollinger Bands setup

BB_basis = ta.sma(close, length)

BB_dev = ta.stdev(close, length)

BB_upper = BB_basis + BB_mult * BB_dev

BB_lower = BB_basis - BB_mult * BB_dev

// Keltner Channels setup

KC_basis = ta.sma(close, length)

KC_range = ta.sma(ta.tr, length)

KC_upper_high = KC_basis + KC_range * KC_mult_high

KC_lower_high = KC_basis - KC_range * KC_mult_high

```

### 3. Scoring System Implementation

```pine

// Band Convergence Score

band_ratio = BB_width / KC_width

convergence_score = math.max(0, 40 * (1 - band_ratio))

// Price Position Score

price_range = math.abs(close - KC_basis) / (KC_upper_low - KC_lower_low)

position_score = 20 * (1 - price_range)

// Final Score Calculation

squeeze_score = convergence_score + position_score + vol_score + mom_score

```

### 4. Signal Generation

```pine

// Entry Signal Logic

long_signal = squeeze_release and

is_momentum_positive and

(not use_ema_trend or (bullish_trend and is_close_to_ema_long)) and

is_bullish_candle

short_signal = squeeze_release and

is_momentum_negative and

(not use_ema_trend or (bearish_trend and is_close_to_ema_short)) and

is_bearish_candle

```

📈 Trading Signals

🚀 Long Entry Conditions

- Squeeze release detected

- Positive momentum

- Bullish candlestick

- Price above relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

🔻 Short Entry Conditions

- Squeeze release detected

- Negative momentum

- Bearish candlestick

- Price below relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

⚠️ Alert Conditions

- 🔔 Extreme squeeze level reached (score crosses above 80)

- 🚀 Long squeeze release signal

- 🔻 Short squeeze release signal

💡 Tips for Usage

1. 📱 Use the status monitor to track real-time squeeze intensity and state

2. 🎨 Pay attention to the color gradient for trend direction and strength

3. ⏰ Consider using multiple timeframes for confirmation

4. ⚙️ Adjust EMA and proximity settings based on your trading style

5. 📊 Use volume analysis for additional confirmation in liquid markets

📝 Notes

- 🔧 The indicator combines multiple technical analysis concepts for robust signal generation

- 📈 Suitable for all tradable markets and timeframes

- ⭐ Best results typically achieved in trending markets with clear volatility cycles

- 🎯 Consider using in conjunction with other technical analysis tools for confirmation

⚠️ Disclaimer

This technical indicator is designed to assist in analysis but should not be considered as financial advice. Always perform your own analysis and risk management when trading.

INTELLECT_city - US Presidential Elections Dates (USA)(EN)

It is interesting to compare Halvings Cycles and Presidential elections.

This indicator shows all presidential elections in the USA from the period 2008, and future ones to the date 2044. The indicator will automatically show all future dates of presidential elections.

--

To apply it to your chart it is very easy:

Select:

1) Exchange: BITSTAMP

2) Pair BTC \ USD (Without "T" at the end)

3) Timeframe 1 day

4) In the Browser, switch the chart to Logarithmic (on the right bottom, click the "L" button)

or on mobile, switch to "Logarithmic" we look on the chart: "Gear" - and switch to "Logarithmic"

------------------

(RU)

Интересно сопоставить Циклы Halvings и Президентские выборы.

Данный индикатор показывает все президентские выборы в США с периода 2008 года, и будущие к дате 2044 года. Индикатор будет автоматически показывать все будущие даты .

--

Что бы применить у себя на графике это очень легко:

Выберите:

1) Биржа: BITSTAMP

2) Пара BTC \ USD (Без "T" в конце)

3) Timeframe 1 дневной

4) В Браузере переключить график на Логарифмический (с право внизу кнопка "Л")

или на мобильно переключить на "Логарифмический" ищем на графике: "Шестеренку" — и переключаем на "Логарифмический"

-------------------

(DE)

Es ist interessant, die Halbierungszyklen und die Präsidentschaftswahlen zu vergleichen.

Dieser Indikator zeigt alle US-Präsidentschaftswahlen seit 2008 und zukünftige bis zum Datum 2044. Der Indikator zeigt automatisch alle zukünftigen Präsidentschaftswahltermine an.

--

Es ist sehr einfach, dies auf Ihr Diagramm anzuwenden:

Wählen:

1) Austausch: BITSTAMP

2) Paar BTC \ USD (Ohne das „T“ am Ende)

3) Zeitrahmen 1 Tag

4) Schalten Sie im Browser das Diagramm auf Logarithmisch um (die Schaltfläche „L“ unten rechts).

oder auf dem Mobilgerät auf „Logarithmisch“ umschalten, in der Grafik nach „Getriebe“ suchen – und auf „Logarithmisch“ umschalten

Vlad Waves█ CONCEPT

Acceleration Line (Blue)

The Acceleration Line is calculated as the difference between the 8-period SMA and the 20-period SMA.

This line helps to identify the momentum and potential turning points in the market.

Signal Line (Red)

The Signal Line is an 8-period SMA of the Acceleration Line.

This line smooths out the Acceleration Line to generate clearer signals.

Long-Term Average (Green)

The Long-Term Average is a 200-period SMA of the Acceleration Line.

This line provides a broader context of the market trend, helping to distinguish between long-term and short-term movements.

█ SIGNALS

Buy Mode

A buy signal occurs when the Acceleration Line crosses above the Signal Line while below the Long-Term Average. This indicates a potential bullish reversal in the market.

When the Signal Line crosses the Acceleration Line above the Long-Term Average, consider placing a stop rather than reversing the position to protect gains from potential pullbacks.

Sell Mode

A sell signal occurs when the Acceleration Line crosses below the Signal Line while above the Long-Term Average. This indicates a potential bearish reversal in the market.

When the Signal Line crosses the Acceleration Line below the Long-Term Average, consider placing a stop rather than reversing the position to protect gains from potential pullbacks.

█ UTILITY

This indicator is not recommended for standalone buy or sell signals. Instead, it is designed to identify market cycles and turning points, aiding in the decision-making process.

Entry signals are most effective when they occur away from the Long-Term Average, as this helps to avoid sideways movements.

Use larger timeframes, such as daily or weekly charts, for better accuracy and reliability of the signals.

█ CREDITS

The idea for this indicator came from Fabio Figueiredo (Vlad).

3x MTF MACD v3.0MACD's on 3 different Time Frames

Indicator Information

- Each Time Frame shows start of Trend and end of trend of the MACD vs the Signal Cross

- They are labled 1,2,3 with respective up or down triangle for possible direction.

User Inputs

- configure the indicator by specifying various inputs. These inputs include colors for bullish

and bearish conditions, the time frame to use, whether to show a Simple Moving Average

(SMA) line, and other parameters.

- Users can choose time frames for analysis (like 30 minutes, 1 hour, etc.)

but they must be in mintues.

- The code also allows users to customize how the indicator looks on the chart by providing

options for position and color.

Main Calculations

- The script calculates the Simple Moving Average (SMA) based on the user-defined time

frame.

- It then determines the color of the plot (line) based on certain conditions, such as whether

the SMA is rising or falling. These conditions help users quickly identify market trends.

Label Creation

- The code creates labels that can be displayed on the chart.

These labels indicate whether there's a bullish or bearish signal.

Level Detection

- The script determines and labels key levels or points of interest in the chart based on

certain conditions.

- It can show labels like "①" and "▲" for bullish conditions and "▼" for bearish conditions.

Table Display

- There's an option to show a table on the chart that displays information about the MACD

indicator Chosen and the NUmber Bubble assocated with that time frame

- The table can include information like which time frame is being analyzed, whether the SMA

line is shown, and other relevant data.

Plotting on the Chart

- The script plots the Simple Moving Average (SMA) on the chart. The color of this line

changes based on the calculated trend conditions.

ATR (Average True Range)

- The script also plots the Average True Range (ATR) on the chart. ATR is used to measure

market volatility.

"In essence, this script is a highly customizable MACD and SMA indicator for traders. It assists traders in comprehending market trends, offering insights into different MACD cycles concerning various timeframes.

Users can configure it to match their trading strategies, and it presents information in a user-friendly manner with colors, labels, and tables.

This simplifies market analysis, allowing traders to make more informed decisions without the distraction of multiple indicators."

Time Cycles IndicatorThis script is used to analyze the seasonality of any asset (commodities, stocks, indices).

To use the script select a timeframe D or W and select the months you are interested in the script settings. You will see all the candles that are part of those months highlighted in the chart.

You can use this script to understand if assets have a cyclical behavior in certain months of the year.

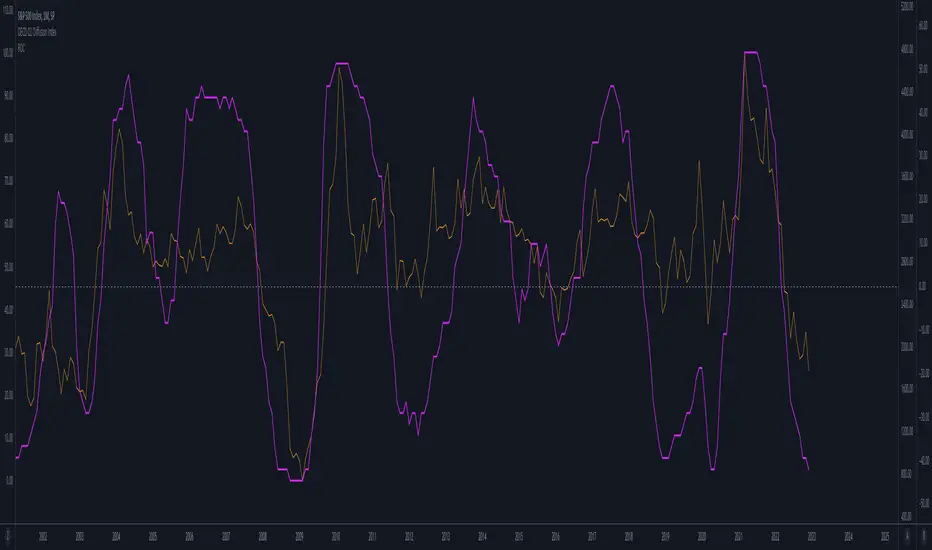

OECD CLI Diffusion IndexWhat does the indicator measure?

This is a macro indicator. It uses OECD's composite leading indicator - see details about the CLI below.

What it does it calculate YoY changes for CLI of 38 countries that are members or are associated with the OECD. Then it measures a percent of countries which CLI is rising.

How this can be used?

The positive slope of the curve means that there probably will be an economic growth among those countries within next 6 - 9 months. The negative slope means there probably will be an economic contraction.

Forward-looking economic growth is correlated with positive S&P 500 YoY growth (equity markets are also forward looking). The chart above presents the CLI diffusion index with overlayed S&P500 YoY rate of change.

The CLI is also correlated with ISM PMI - see example below:

What is a CLI?

"The OECD system of Composite Leading Indicators (CLIs) is designed to provide early signals of turning points in business cycles - fluctuation in the output gap, i.e. fluctuation of the economic activity around its long term potential level. This approach, focusing on turning points (peaks and troughs), results in CLIs that provide qualitative rather than quantitative information on short-term economic movements."

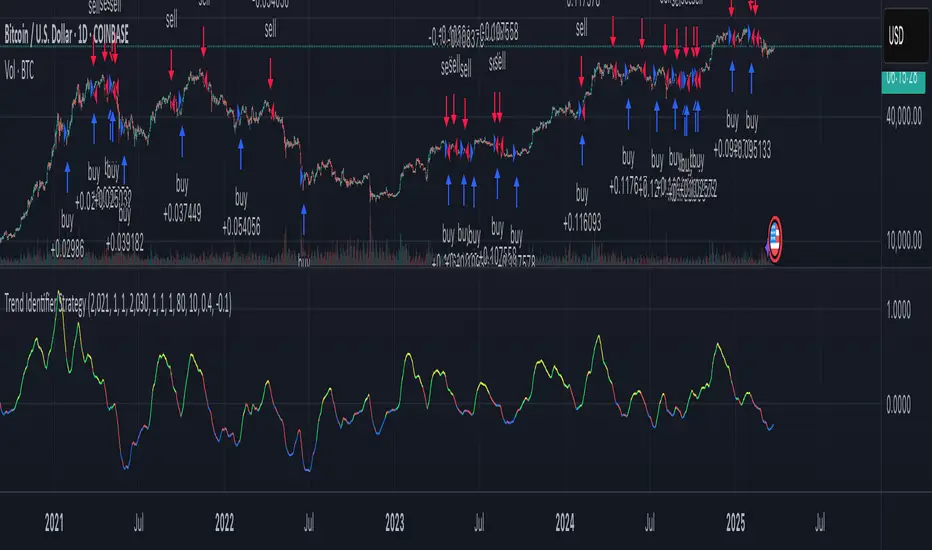

Trend Identifier StrategyTrend Identifier Strategy for 1D BTC.USD

The indicator smoothens a closely following moving average into a polynomial like plot and assumes 4 staged cycles based on the first and the second derivatives. This is an optimized strategy for long term buying and selling with a Sortino Ratio above 3. It is designed to be a more profitable alternative to HODLing. It can be combined with 'Accumulation/Distribution Bands & Signals' and 'Exponential Top and Bottom Finder'.