Periodic CycleAllows visualizing a periodic cycle based on startdate, cycle period and part of cycle to be highlighed.Indicatore Pine Script®di estyles_tvr151

Bitcoin Halving Cycle Profit (with info table)English Indicator Description: Based on the original indicator by @KevinSvenson_ A table with dates was added for study purposes, however the resulting dates are not validated. The Halving Cycle Profit indicator represents a fixed, recurring profit-taking cycle that begins with each Bitcoin halving event. Functionality Explained: After every halving event, there has historically been a fixed number of weeks that marked the area of highest profitability for taking profits. • 40 weeks post-halving = Start of the optimal profit-taking zone. • 80 weeks post-halving = “Last call” for profit-taking before the bear market. • 135 weeks post-halving = Optimal area to begin Dollar-Cost Averaging (DCA). Indicatore Pine Script®di WhaleScout26

Economic Cycle ScoreCalculation -Combine Business Cycle with Liquidity Cycle by applying Z-Score -Rescale Z-Score to 0-100 -Smooth it with ema -0-15 is oversold -85-100 is overbought Use Case -Identify when risk asset (Bitcoin) is overbought/oversold -Use this indicator together with other confluences ***USE ON MONTHLY CHART ONLY (due to the economic date release frequency)Indicatore Pine Script®di MoneyPrintingCompany13

Time Cycle linesTime cycles are recurring patterns or intervals in which market movements tend to repeat. Traders use them to identify potential turning points in price action. By analyzing historical highs, lows, and key time intervals, time cycles help forecast future market behavior and improve timing for entries and exits.Indicatore Pine Script®di CasperTheTraderAggiornato 1146

Global PMI CycleGlobal business-cycle proxy derived from PMI/ISM dynamics, designed to contextualise macro regimes alongside Bitcoin and risk assets.Indicatore Pine Script®di Malcs11

Crypto Cycle Radar (TOTAL / TOTAL2 / TOTAL3 / BTC.D / USDT.D)Crypto Cycle Radar (TOTAL / TOTAL2 / TOTAL3 / BTC.D / USDT.D)Indicatore Pine Script®di nickrick1087

Pi Cycle PersonalizadoYou can adjust it for any crypto asset to help identify each cycle’s peaks. Example: Cardano → Fast SMA: 150 Slow SMA: 350 Ethereum → Fast SMA: 250 Slow SMA: 625Indicatore Pine Script®di fernandoriv2

Gronk-Style Lunar Cycle Projection (fixed 30m base)Based on the lunar cycle timing provided by Gronko Polo - A Bromance in FinanceIndicatore Pine Script®di ledgineer18

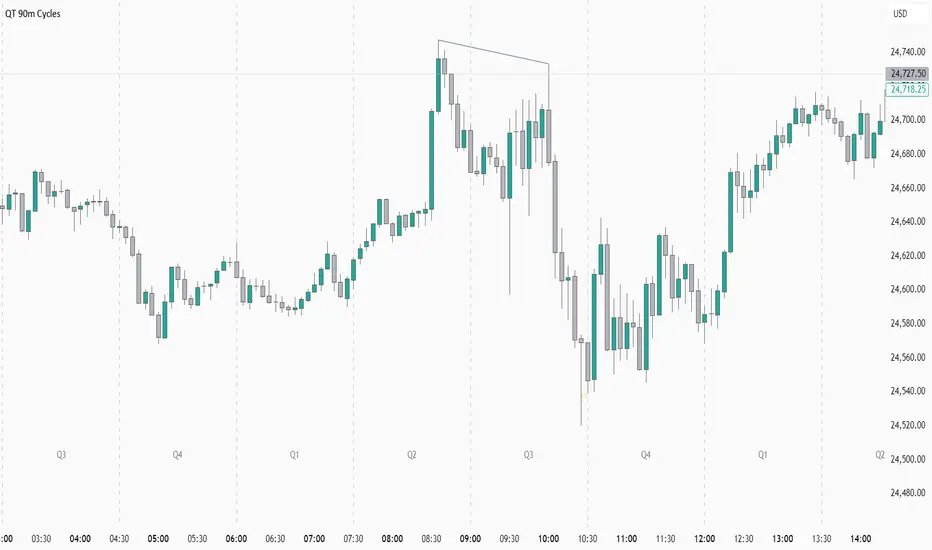

Quarterly Theory - 90m Cycles This Indicator Give you the Exact 90 mins cycles for the market and add background colors to each session over it.Indicatore Pine Script®di gbgb1bgbg122

Market Time Cycle (Expo)█ Time Cycles Overview Time cycles are a fascinating and powerful concept in the world of trading and investing. They are all about understanding and predicting the timing of market moves based on the premise that market events and price movements are not random, but instead occur in repeatable, cyclical patterns. The Concept of Time Cycles: The foundation of time cycles lies in the belief that historical market patterns tend to repeat themselves over specific periods. These periods or cycles could be influenced by a myriad of factors like economic data releases, earnings reports, geopolitical events, or even natural human behavior. For example, some traders observe increased market activity around the start and end of a trading day, which is a form of intraday time cycle. Understanding time cycles can provide traders with a roadmap, helping them anticipate potential trend shifts and make more informed decisions about when to buy or sell. █ Indicator Overview The Market Time Cycle (Expo) is designed to help traders track and analyze market cycles and generate signals for potential trading opportunities. It uses mathematical techniques to analyze market cycles and detect possible turning points. It does this by projecting the estimated cycle timeline and providing visual indications of cyclical phases through the use of color-coded lines and sine wave cycles. Time cycles offer a compelling way to forecast market trends and time your trades better. By adding time cycles to your trading toolbox, you could potentially gain a new perspective on market movements and refine your trading strategy further. The indicator generates trading signals based on the sine wave's behavior. When the sine wave crosses certain thresholds, the indicator generates a signal suggesting a potential trading opportunity based on cycle behavior. █ How to use This indicator can be a valuable tool to help traders understand and predict market trends and time their trades more accurately. By visualizing the cyclic nature of markets, traders can better anticipate potential turning points and adjust their trading strategies accordingly. It helps traders to spot ideal entry and exit points based on the cyclical nature of financial markets. █ Settings You can customize the number of bars (NumbOfBars) that are taken into consideration for the cycle. Including a higher number of bars will provide more data, which can be helpful for analyzing long-term trends. ----------------- Disclaimer The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information. All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs. My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes! Indicatore Pine Script®di Zeiierman1111 1.1 K

Goertzel Cycle Composite Wave [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Cycle Composite Wave indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading. *** To decrease the load time of this indicator, only XX many bars back will render to the chart. You can control this value with the setting "Number of Bars to Render". This doesn't have anything to do with repainting or the indicator being endpointed*** █ Brief Overview of the Goertzel Cycle Composite Wave The Goertzel Cycle Composite Wave is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions. The Goertzel Cycle Composite Wave is considered a non-repainting and endpointed indicator. This means that once a value has been calculated for a specific bar, that value will not change in subsequent bars, and the indicator is designed to have a clear start and end point. This is an important characteristic for indicators used in technical analysis, as it allows traders to make informed decisions based on historical data without the risk of hindsight bias or future changes in the indicator's values. This means traders can use this indicator trading purposes. The repainting version of this indicator with forecasting, cycle selection/elimination options, and data output table can be found here: Goertzel Browser The primary purpose of this indicator is to: 1. Detect and analyze the dominant cycles present in the price data. 2. Reconstruct and visualize the composite wave based on the detected cycles. To achieve this, the indicator performs several tasks: 1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components. 2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength. 3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength. 4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the cycles. The color of the lines indicates whether the wave is increasing or decreasing. This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements, the indicator aims to assist traders in making more informed decisions. █ What is the Goertzel Algorithm? The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics. The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as: 1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed. 2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments. 3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear. 4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues. The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT: 1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases. 2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing. 3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest. 4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential. The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics. █ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications The Goertzel algorithm, initially designed for signal processing in telecommunications, has gained significant traction in the financial industry due to its efficient frequency detection capabilities. In quantitative finance, the Goertzel algorithm has been utilized for uncovering hidden market cycles, developing data-driven trading strategies, and optimizing risk management. This section delves deeper into the applications of the Goertzel algorithm in finance, particularly within the context of quantitative trading and analysis. Unveiling Hidden Market Cycles: Market cycles are prevalent in financial markets and arise from various factors, such as economic conditions, investor psychology, and market participant behavior. The Goertzel algorithm's ability to detect and isolate specific frequencies in price data helps trader analysts identify hidden market cycles that may otherwise go unnoticed. By examining the amplitude, phase, and periodicity of each cycle, traders can better understand the underlying market structure and dynamics, enabling them to develop more informed and effective trading strategies. Developing Quantitative Trading Strategies: The Goertzel algorithm's versatility allows traders to incorporate its insights into a wide range of trading strategies. By identifying the dominant market cycles in a financial instrument's price data, traders can create data-driven strategies that capitalize on the cyclical nature of markets. For instance, a trader may develop a mean-reversion strategy that takes advantage of the identified cycles. By establishing positions when the price deviates from the predicted cycle, the trader can profit from the subsequent reversion to the cycle's mean. Similarly, a momentum-based strategy could be designed to exploit the persistence of a dominant cycle by entering positions that align with the cycle's direction. Enhancing Risk Management: The Goertzel algorithm plays a vital role in risk management for quantitative strategies. By analyzing the cyclical components of a financial instrument's price data, traders can gain insights into the potential risks associated with their trading strategies. By monitoring the amplitude and phase of dominant cycles, a trader can detect changes in market dynamics that may pose risks to their positions. For example, a sudden increase in amplitude may indicate heightened volatility, prompting the trader to adjust position sizing or employ hedging techniques to protect their portfolio. Additionally, changes in phase alignment could signal a potential shift in market sentiment, necessitating adjustments to the trading strategy. Expanding Quantitative Toolkits: Traders can augment the Goertzel algorithm's insights by combining it with other quantitative techniques, creating a more comprehensive and sophisticated analysis framework. For example, machine learning algorithms, such as neural networks or support vector machines, could be trained on features extracted from the Goertzel algorithm to predict future price movements more accurately. Furthermore, the Goertzel algorithm can be integrated with other technical analysis tools, such as moving averages or oscillators, to enhance their effectiveness. By applying these tools to the identified cycles, traders can generate more robust and reliable trading signals. The Goertzel algorithm offers invaluable benefits to quantitative finance practitioners by uncovering hidden market cycles, aiding in the development of data-driven trading strategies, and improving risk management. By leveraging the insights provided by the Goertzel algorithm and integrating it with other quantitative techniques, traders can gain a deeper understanding of market dynamics and devise more effective trading strategies. █ Indicator Inputs src: This is the source data for the analysis, typically the closing price of the financial instrument. detrendornot: This input determines the method used for detrending the source data. Detrending is the process of removing the underlying trend from the data to focus on the cyclical components. The available options are: hpsmthdt: Detrend using Hodrick-Prescott filter centered moving average. zlagsmthdt: Detrend using zero-lag moving average centered moving average. logZlagRegression: Detrend using logarithmic zero-lag linear regression. hpsmth: Detrend using Hodrick-Prescott filter. zlagsmth: Detrend using zero-lag moving average. DT_HPper1 and DT_HPper2: These inputs define the period range for the Hodrick-Prescott filter centered moving average when detrendornot is set to hpsmthdt. DT_ZLper1 and DT_ZLper2: These inputs define the period range for the zero-lag moving average centered moving average when detrendornot is set to zlagsmthdt. DT_RegZLsmoothPer: This input defines the period for the zero-lag moving average used in logarithmic zero-lag linear regression when detrendornot is set to logZlagRegression. HPsmoothPer: This input defines the period for the Hodrick-Prescott filter when detrendornot is set to hpsmth. ZLMAsmoothPer: This input defines the period for the zero-lag moving average when detrendornot is set to zlagsmth. MaxPer: This input sets the maximum period for the Goertzel algorithm to search for cycles. squaredAmp: This boolean input determines whether the amplitude should be squared in the Goertzel algorithm. useAddition: This boolean input determines whether the Goertzel algorithm should use addition for combining the cycles. useCosine: This boolean input determines whether the Goertzel algorithm should use cosine waves instead of sine waves. UseCycleStrength: This boolean input determines whether the Goertzel algorithm should compute the cycle strength, which is a normalized measure of the cycle's amplitude. WindowSizePast: These inputs define the window size for the composite wave. FilterBartels: This boolean input determines whether Bartel's test should be applied to filter out non-significant cycles. BartNoCycles: This input sets the number of cycles to be used in Bartel's test. BartSmoothPer: This input sets the period for the moving average used in Bartel's test. BartSigLimit: This input sets the significance limit for Bartel's test, below which cycles are considered insignificant. SortBartels: This boolean input determines whether the cycles should be sorted by their Bartel's test results. StartAtCycle: This input determines the starting index for selecting the top N cycles when UseCycleList is set to false. This allows you to skip a certain number of cycles from the top before selecting the desired number of cycles. UseTopCycles: This input sets the number of top cycles to use for constructing the composite wave when UseCycleList is set to false. The cycles are ranked based on their amplitudes or cycle strengths, depending on the UseCycleStrength input. SubtractNoise: This boolean input determines whether to subtract the noise (remaining cycles) from the composite wave. If set to true, the composite wave will only include the top N cycles specified by UseTopCycles. █ Exploring Auxiliary Functions The following functions demonstrate advanced techniques for analyzing financial markets, including zero-lag moving averages, Bartels probability, detrending, and Hodrick-Prescott filtering. This section examines each function in detail, explaining their purpose, methodology, and applications in finance. We will examine how each function contributes to the overall performance and effectiveness of the indicator and how they work together to create a powerful analytical tool. Zero-Lag Moving Average: The zero-lag moving average function is designed to minimize the lag typically associated with moving averages. This is achieved through a two-step weighted linear regression process that emphasizes more recent data points. The function calculates a linearly weighted moving average (LWMA) on the input data and then applies another LWMA on the result. By doing this, the function creates a moving average that closely follows the price action, reducing the lag and improving the responsiveness of the indicator. The zero-lag moving average function is used in the indicator to provide a responsive, low-lag smoothing of the input data. This function helps reduce the noise and fluctuations in the data, making it easier to identify and analyze underlying trends and patterns. By minimizing the lag associated with traditional moving averages, this function allows the indicator to react more quickly to changes in market conditions, providing timely signals and improving the overall effectiveness of the indicator. Bartels Probability: The Bartels probability function calculates the probability of a given cycle being significant in a time series. It uses a mathematical test called the Bartels test to assess the significance of cycles detected in the data. The function calculates coefficients for each detected cycle and computes an average amplitude and an expected amplitude. By comparing these values, the Bartels probability is derived, indicating the likelihood of a cycle's significance. This information can help in identifying and analyzing dominant cycles in financial markets. The Bartels probability function is incorporated into the indicator to assess the significance of detected cycles in the input data. By calculating the Bartels probability for each cycle, the indicator can prioritize the most significant cycles and focus on the market dynamics that are most relevant to the current trading environment. This function enhances the indicator's ability to identify dominant market cycles, improving its predictive power and aiding in the development of effective trading strategies. Detrend Logarithmic Zero-Lag Regression: The detrend logarithmic zero-lag regression function is used for detrending data while minimizing lag. It combines a zero-lag moving average with a linear regression detrending method. The function first calculates the zero-lag moving average of the logarithm of input data and then applies a linear regression to remove the trend. By detrending the data, the function isolates the cyclical components, making it easier to analyze and interpret the underlying market dynamics. The detrend logarithmic zero-lag regression function is used in the indicator to isolate the cyclical components of the input data. By detrending the data, the function enables the indicator to focus on the cyclical movements in the market, making it easier to analyze and interpret market dynamics. This function is essential for identifying cyclical patterns and understanding the interactions between different market cycles, which can inform trading decisions and enhance overall market understanding. Bartels Cycle Significance Test: The Bartels cycle significance test is a function that combines the Bartels probability function and the detrend logarithmic zero-lag regression function to assess the significance of detected cycles. The function calculates the Bartels probability for each cycle and stores the results in an array. By analyzing the probability values, traders and analysts can identify the most significant cycles in the data, which can be used to develop trading strategies and improve market understanding. The Bartels cycle significance test function is integrated into the indicator to provide a comprehensive analysis of the significance of detected cycles. By combining the Bartels probability function and the detrend logarithmic zero-lag regression function, this test evaluates the significance of each cycle and stores the results in an array. The indicator can then use this information to prioritize the most significant cycles and focus on the most relevant market dynamics. This function enhances the indicator's ability to identify and analyze dominant market cycles, providing valuable insights for trading and market analysis. Hodrick-Prescott Filter: The Hodrick-Prescott filter is a popular technique used to separate the trend and cyclical components of a time series. The function applies a smoothing parameter to the input data and calculates a smoothed series using a two-sided filter. This smoothed series represents the trend component, which can be subtracted from the original data to obtain the cyclical component. The Hodrick-Prescott filter is commonly used in economics and finance to analyze economic data and financial market trends. The Hodrick-Prescott filter is incorporated into the indicator to separate the trend and cyclical components of the input data. By applying the filter to the data, the indicator can isolate the trend component, which can be used to analyze long-term market trends and inform trading decisions. Additionally, the cyclical component can be used to identify shorter-term market dynamics and provide insights into potential trading opportunities. The inclusion of the Hodrick-Prescott filter adds another layer of analysis to the indicator, making it more versatile and comprehensive. Detrending Options: Detrend Centered Moving Average: The detrend centered moving average function provides different detrending methods, including the Hodrick-Prescott filter and the zero-lag moving average, based on the selected detrending method. The function calculates two sets of smoothed values using the chosen method and subtracts one set from the other to obtain a detrended series. By offering multiple detrending options, this function allows traders and analysts to select the most appropriate method for their specific needs and preferences. The detrend centered moving average function is integrated into the indicator to provide users with multiple detrending options, including the Hodrick-Prescott filter and the zero-lag moving average. By offering multiple detrending methods, the indicator allows users to customize the analysis to their specific needs and preferences, enhancing the indicator's overall utility and adaptability. This function ensures that the indicator can cater to a wide range of trading styles and objectives, making it a valuable tool for a diverse group of market participants. The auxiliary functions functions discussed in this section demonstrate the power and versatility of mathematical techniques in analyzing financial markets. By understanding and implementing these functions, traders and analysts can gain valuable insights into market dynamics, improve their trading strategies, and make more informed decisions. The combination of zero-lag moving averages, Bartels probability, detrending methods, and the Hodrick-Prescott filter provides a comprehensive toolkit for analyzing and interpreting financial data. The integration of advanced functions in a financial indicator creates a powerful and versatile analytical tool that can provide valuable insights into financial markets. By combining the zero-lag moving average, █ In-Depth Analysis of the Goertzel Cycle Composite Wave Code The Goertzel Cycle Composite Wave code is an implementation of the Goertzel Algorithm, an efficient technique to perform spectral analysis on a signal. The code is designed to detect and analyze dominant cycles within a given financial market data set. This section will provide an extremely detailed explanation of the code, its structure, functions, and intended purpose. Function signature and input parameters: The Goertzel Cycle Composite Wave function accepts numerous input parameters for customization, including source data (src), the current bar (forBar), sample size (samplesize), period (per), squared amplitude flag (squaredAmp), addition flag (useAddition), cosine flag (useCosine), cycle strength flag (UseCycleStrength), past sizes (WindowSizePast), Bartels filter flag (FilterBartels), Bartels-related parameters (BartNoCycles, BartSmoothPer, BartSigLimit), sorting flag (SortBartels), and output buffers (goeWorkPast, cyclebuffer, amplitudebuffer, phasebuffer, cycleBartelsBuffer). Initializing variables and arrays: The code initializes several float arrays (goeWork1, goeWork2, goeWork3, goeWork4) with the same length as twice the period (2 * per). These arrays store intermediate results during the execution of the algorithm. Preprocessing input data: The input data (src) undergoes preprocessing to remove linear trends. This step enhances the algorithm's ability to focus on cyclical components in the data. The linear trend is calculated by finding the slope between the first and last values of the input data within the sample. Iterative calculation of Goertzel coefficients: The core of the Goertzel Cycle Composite Wave algorithm lies in the iterative calculation of Goertzel coefficients for each frequency bin. These coefficients represent the spectral content of the input data at different frequencies. The code iterates through the range of frequencies, calculating the Goertzel coefficients using a nested loop structure. Cycle strength computation: The code calculates the cycle strength based on the Goertzel coefficients. This is an optional step, controlled by the UseCycleStrength flag. The cycle strength provides information on the relative influence of each cycle on the data per bar, considering both amplitude and cycle length. The algorithm computes the cycle strength either by squaring the amplitude (controlled by squaredAmp flag) or using the actual amplitude values. Phase calculation: The Goertzel Cycle Composite Wave code computes the phase of each cycle, which represents the position of the cycle within the input data. The phase is calculated using the arctangent function (math.atan) based on the ratio of the imaginary and real components of the Goertzel coefficients. Peak detection and cycle extraction: The algorithm performs peak detection on the computed amplitudes or cycle strengths to identify dominant cycles. It stores the detected cycles in the cyclebuffer array, along with their corresponding amplitudes and phases in the amplitudebuffer and phasebuffer arrays, respectively. Sorting cycles by amplitude or cycle strength: The code sorts the detected cycles based on their amplitude or cycle strength in descending order. This allows the algorithm to prioritize cycles with the most significant impact on the input data. Bartels cycle significance test: If the FilterBartels flag is set, the code performs a Bartels cycle significance test on the detected cycles. This test determines the statistical significance of each cycle and filters out the insignificant cycles. The significant cycles are stored in the cycleBartelsBuffer array. If the SortBartels flag is set, the code sorts the significant cycles based on their Bartels significance values. Waveform calculation: The Goertzel Cycle Composite Wave code calculates the waveform of the significant cycles for specified time windows. The windows are defined by the WindowSizePast parameters, respectively. The algorithm uses either cosine or sine functions (controlled by the useCosine flag) to calculate the waveforms for each cycle. The useAddition flag determines whether the waveforms should be added or subtracted. Storing waveforms in a matrix: The calculated waveforms for the cycle is stored in the matrix - goeWorkPast. This matrix holds the waveforms for the specified time windows. Each row in the matrix represents a time window position, and each column corresponds to a cycle. Returning the number of cycles: The Goertzel Cycle Composite Wave function returns the total number of detected cycles (number_of_cycles) after processing the input data. This information can be used to further analyze the results or to visualize the detected cycles. The Goertzel Cycle Composite Wave code is a comprehensive implementation of the Goertzel Algorithm, specifically designed for detecting and analyzing dominant cycles within financial market data. The code offers a high level of customization, allowing users to fine-tune the algorithm based on their specific needs. The Goertzel Cycle Composite Wave's combination of preprocessing, iterative calculations, cycle extraction, sorting, significance testing, and waveform calculation makes it a powerful tool for understanding cyclical components in financial data. █ Generating and Visualizing Composite Waveform The indicator calculates and visualizes the composite waveform for specified time windows based on the detected cycles. Here's a detailed explanation of this process: Updating WindowSizePast: The WindowSizePast is updated to ensure they are at least twice the MaxPer (maximum period). Initializing matrices and arrays: The matrix goeWorkPast is initialized to store the Goertzel results for specified time windows. Multiple arrays are also initialized to store cycle, amplitude, phase, and Bartels information. Preparing the source data (srcVal) array: The source data is copied into an array, srcVal, and detrended using one of the selected methods (hpsmthdt, zlagsmthdt, logZlagRegression, hpsmth, or zlagsmth). Goertzel function call: The Goertzel function is called to analyze the detrended source data and extract cycle information. The output, number_of_cycles, contains the number of detected cycles. Initializing arrays for waveforms: The goertzel array is initialized to store the endpoint Goertzel. Calculating composite waveform (goertzel array): The composite waveform is calculated by summing the selected cycles (either from the user-defined cycle list or the top cycles) and optionally subtracting the noise component. Drawing composite waveform (pvlines): The composite waveform is drawn on the chart using solid lines. The color of the lines is determined by the direction of the waveform (green for upward, red for downward). To summarize, this indicator generates a composite waveform based on the detected cycles in the financial data. It calculates the composite waveforms and visualizes them on the chart using colored lines. █ Enhancing the Goertzel Algorithm-Based Script for Financial Modeling and Trading The Goertzel algorithm-based script for detecting dominant cycles in financial data is a powerful tool for financial modeling and trading. It provides valuable insights into the past behavior of these cycles. However, as with any algorithm, there is always room for improvement. This section discusses potential enhancements to the existing script to make it even more robust and versatile for financial modeling, general trading, advanced trading, and high-frequency finance trading. Enhancements for Financial Modeling Data preprocessing: One way to improve the script's performance for financial modeling is to introduce more advanced data preprocessing techniques. This could include removing outliers, handling missing data, and normalizing the data to ensure consistent and accurate results. Additional detrending and smoothing methods: Incorporating more sophisticated detrending and smoothing techniques, such as wavelet transform or empirical mode decomposition, can help improve the script's ability to accurately identify cycles and trends in the data. Machine learning integration: Integrating machine learning techniques, such as artificial neural networks or support vector machines, can help enhance the script's predictive capabilities, leading to more accurate financial models. Enhancements for General and Advanced Trading Customizable indicator integration: Allowing users to integrate their own technical indicators can help improve the script's effectiveness for both general and advanced trading. By enabling the combination of the dominant cycle information with other technical analysis tools, traders can develop more comprehensive trading strategies. Risk management and position sizing: Incorporating risk management and position sizing functionality into the script can help traders better manage their trades and control potential losses. This can be achieved by calculating the optimal position size based on the user's risk tolerance and account size. Multi-timeframe analysis: Enhancing the script to perform multi-timeframe analysis can provide traders with a more holistic view of market trends and cycles. By identifying dominant cycles on different timeframes, traders can gain insights into the potential confluence of cycles and make better-informed trading decisions. Enhancements for High-Frequency Finance Trading Algorithm optimization: To ensure the script's suitability for high-frequency finance trading, optimizing the algorithm for faster execution is crucial. This can be achieved by employing efficient data structures and refining the calculation methods to minimize computational complexity. Real-time data streaming: Integrating real-time data streaming capabilities into the script can help high-frequency traders react to market changes more quickly. By continuously updating the cycle information based on real-time market data, traders can adapt their strategies accordingly and capitalize on short-term market fluctuations. Order execution and trade management: To fully leverage the script's capabilities for high-frequency trading, implementing functionality for automated order execution and trade management is essential. This can include features such as stop-loss and take-profit orders, trailing stops, and automated trade exit strategies. While the existing Goertzel algorithm-based script is a valuable tool for detecting dominant cycles in financial data, there are several potential enhancements that can make it even more powerful for financial modeling, general trading, advanced trading, and high-frequency finance trading. By incorporating these improvements, the script can become a more versatile and effective tool for traders and financial analysts alike. █ Understanding the Limitations of the Goertzel Algorithm While the Goertzel algorithm-based script for detecting dominant cycles in financial data provides valuable insights, it is important to be aware of its limitations and drawbacks. Some of the key drawbacks of this indicator are: Lagging nature: As with many other technical indicators, the Goertzel algorithm-based script can suffer from lagging effects, meaning that it may not immediately react to real-time market changes. This lag can lead to late entries and exits, potentially resulting in reduced profitability or increased losses. Parameter sensitivity: The performance of the script can be sensitive to the chosen parameters, such as the detrending methods, smoothing techniques, and cycle detection settings. Improper parameter selection may lead to inaccurate cycle detection or increased false signals, which can negatively impact trading performance. Complexity: The Goertzel algorithm itself is relatively complex, making it difficult for novice traders or those unfamiliar with the concept of cycle analysis to fully understand and effectively utilize the script. This complexity can also make it challenging to optimize the script for specific trading styles or market conditions. Overfitting risk: As with any data-driven approach, there is a risk of overfitting when using the Goertzel algorithm-based script. Overfitting occurs when a model becomes too specific to the historical data it was trained on, leading to poor performance on new, unseen data. This can result in misleading signals and reduced trading performance. Limited applicability: The Goertzel algorithm-based script may not be suitable for all markets, trading styles, or timeframes. Its effectiveness in detecting cycles may be limited in certain market conditions, such as during periods of extreme volatility or low liquidity. While the Goertzel algorithm-based script offers valuable insights into dominant cycles in financial data, it is essential to consider its drawbacks and limitations when incorporating it into a trading strategy. Traders should always use the script in conjunction with other technical and fundamental analysis tools, as well as proper risk management, to make well-informed trading decisions. █ Interpreting Results The Goertzel Cycle Composite Wave indicator can be interpreted by analyzing the plotted lines. The indicator plots two lines: composite waves. The composite wave represents the composite wave of the price data. The composite wave line displays a solid line, with green indicating a bullish trend and red indicating a bearish trend. Interpreting the Goertzel Cycle Composite Wave indicator involves identifying the trend of the composite wave lines and matching them with the corresponding bullish or bearish color. █ Conclusion The Goertzel Cycle Composite Wave indicator is a powerful tool for identifying and analyzing cyclical patterns in financial markets. Its ability to detect multiple cycles of varying frequencies and strengths make it a valuable addition to any trader's technical analysis toolkit. However, it is important to keep in mind that the Goertzel Cycle Composite Wave indicator should be used in conjunction with other technical analysis tools and fundamental analysis to achieve the best results. With continued refinement and development, the Goertzel Cycle Composite Wave indicator has the potential to become a highly effective tool for financial modeling, general trading, advanced trading, and high-frequency finance trading. Its accuracy and versatility make it a promising candidate for further research and development. █ Footnotes What is the Bartels Test for Cycle Significance? The Bartels Cycle Significance Test is a statistical method that determines whether the peaks and troughs of a time series are statistically significant. The test is named after its inventor, George Bartels, who developed it in the mid-20th century. The Bartels test is designed to analyze the cyclical components of a time series, which can help traders and analysts identify trends and cycles in financial markets. The test calculates a Bartels statistic, which measures the degree of non-randomness or autocorrelation in the time series. The Bartels statistic is calculated by first splitting the time series into two halves and calculating the range of the peaks and troughs in each half. The test then compares these ranges using a t-test, which measures the significance of the difference between the two ranges. If the Bartels statistic is greater than a critical value, it indicates that the peaks and troughs in the time series are non-random and that there is a significant cyclical component to the data. Conversely, if the Bartels statistic is less than the critical value, it suggests that the peaks and troughs are random and that there is no significant cyclical component. The Bartels Cycle Significance Test is particularly useful in financial analysis because it can help traders and analysts identify significant cycles in asset prices, which can in turn inform investment decisions. However, it is important to note that the test is not perfect and can produce false signals in certain situations, particularly in noisy or volatile markets. Therefore, it is always recommended to use the test in conjunction with other technical and fundamental indicators to confirm trends and cycles. Deep-dive into the Hodrick-Prescott Fitler The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world. The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend. The HP filter works by minimizing the following objective function: Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences) Where: 1. The first term represents the deviation of the data from the trend. 2. The second term represents the smoothness of the trend. 3. λ is a smoothing parameter that determines the degree of smoothness of the trend. The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend. The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency. However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series. Despite these limitations, the HP filter remains a valuable tool for analyzing economic and financial data. It is widely used by central banks and financial institutions to monitor long-term trends in the economy, and it can be used to identify turning points in the business cycle. The filter can also be used to analyze asset prices, exchange rates, and other financial variables. The Hodrick-Prescott filter is a powerful tool for analyzing economic and financial data. It separates a time series into a trend component and a cyclical component, allowing for easy identification of long-term trends and turning points in the business cycle. While it has some limitations, it remains a valuable tool for economists, central banks, and financial institutions around the world.Indicatore Pine Script®di loxx33376

SMT Cycles by AlgoKingsSMT Cycles by AlgoKings RISK DISCLAIMER: This indicator is an analytical tool for educational purposes only, not financial advice. Trading carries substantial risk of loss. This tool does not guarantee profitable trades. Always use proper risk management and never risk more than you can afford to lose. WHAT ARE SMT CYCLES? This indicator identifies Smart Money Technique divergences using cycle-based analysis rather than standard timeframes. Cycles represent natural market rhythms (sessions, 90-minute institutional windows, true daily periods) that better align with institutional trading patterns than arbitrary timeframe bars. Example: During the London session, NQ makes a new high but ES fails to follow = Bearish SMT divergence within the London cycle UNDERLYING METHODOLOGY This indicator combines four analytical layers: 1. AUTOMATIC CORRELATION MAPPING Built-in correlation intelligence for 40+ pairs (identical to SMT Custom): - Futures: NQ, ES, YM cross-correlation | GC/SI | 6E/6B - Forex: EURUSD/GBPUSD/DXY(inverse) | AUDUSD/NZDUSD - Stocks: MAG7 (META, NVDA, MSFT, etc.) vs NDX - Crypto: BTCUSD/ETHUSD Algorithm automatically mirrors contract types and exchange prefixes using regex-based parsing for futures contracts and micro variants. 2. CYCLE-BASED PERIOD DETECTION Unlike standard timeframe analysis, this indicator uses market structure cycles: SWING CYCLES (Position Trading): - Yearly: 12-month institutional rebalancing periods - Quarterly: 3-month earnings and fund rotation cycles - Monthly: Calendar month institutional flows - Weekly: 7-day swing trading cycles - Daily: Standard 18:00-18:00 EST bars - TrueDay: 00:00-00:00 EST for 24-hour markets (futures, forex, crypto) INTRADAY CYCLES (Day Trading): - Session: Asia (18:00-02:00), London (02:00-08:30), NY AM (08:30-12:00), NY PM (12:00-17:00) EST - 90m: Three 90-minute windows per trading day (02:00-03:30, 03:30-05:00, etc.) - 30m: 30-minute institutional order flow windows - 10m, 3m, 1m: Scalping cycles for precise entry timing Technical implementation: - TrueDay calculation: Detects candle closes at exactly 00:00 EST using time modulo arithmetic on 24-hour markets. Differs from standard Daily bars which use futures settlement times (18:00 EST). - Session detection: Regex pattern matching on hour/minute timestamps to identify cycle boundaries (e.g., h==2 and m==0 triggers Asia session end) - 90m hierarchy: Groups sub-90m cycles (30m, 10m, 3m, 1m) under their parent 90m window using group timestamp tracking (gx field) - Intermediate accumulation: For multi-bar cycles (TrueDay, Sessions, 90m), maintains running high/low (nh1, nl1) across constituent bars until cycle completion 3. MULTI-TIMEFRAME CYCLE ANALYSIS Proprietary cycle synchronization: - Tracks price structure across up to 11 configurable cycles simultaneously - Maintains independent high/low tracking for each symbol pair using request.security() - Compares previous cycle extremes (high , low ) across correlated pairs - Timestamps divergence formations at chart timeframe precision - Implements adaptive purge logic (1min to 12M) based on cycle type 4. DIVERGENCE CLASSIFICATION SYSTEM Bullish SMT: Chart symbol makes lower low within cycle, correlated pair does NOT = Institutional buying pressure Bearish SMT: Chart symbol makes higher high within cycle, correlated pair does NOT = Institutional selling pressure Advanced features include level tracking (monitors when extremes are revisited), automatic extension until both levels violated, 90m hierarchy overlap filtering (hides sub-90m SMT within parent 90m window), and inverse correlation support for DXY relationships. WHY CLOSED-SOURCE? This script protects proprietary algorithms: - Cycle boundary detection: Custom logic for TrueDay calculation (00:00 EST candle close detection using modulo arithmetic on 24h markets), Session identification (time-based regex for Asia/London/NY periods), and 90m window calculation (minute offset from 02:00 EST baseline) - Intermediate cycle accumulation: Complex state management for multi-bar cycles (Sessions, 90m, TrueDay) that build complete cycle values across constituent bars before finalizing - 90m hierarchy system: Proprietary grouping algorithm (gtype, gca, gx fields) that links sub-90m cycles to parent windows for intelligent overlap filtering - Automatic symbol mapping: Custom logic for 40+ correlation pairs including futures contract recognition and exchange inheritance - Adaptive purge system: Cycle-specific memory management (1S to 12M) optimized through backtesting - Multi-level tracking: Simultaneous monitoring of multiple active divergences across different cycle types with state management for "taken" levels Standard SMT indicators use fixed timeframes. This script analyzes institutional cycles that don't align with standard bar periods, requiring complex time arithmetic and multi-bar aggregation logic. TECHNICAL COMPONENTS Core structures: - Cycle Object: Tracks high/low/time for each cycle type with intermediate values (nh1, nl1) for multi-bar cycles and complete cycle values (h1, l1, t1) upon cycle completion - CycleType Enum: Defines 11 cycle types (year, quarter, month, week, day, trueday, session, m90, m30, m10, m3, m1) with associated period strings and purge thresholds - Point Object: Stores divergence formation data for chart symbol level and correlated symbol level with "taken" status tracking - SMT Object: Visual representation with line extension, tooltip showing formation time (EST), and optional 90m group timestamp (gx) for hierarchy filtering Cycle detection logic: - TrueDay: Tests if hour==0, minute==0 at candle close OR day-of-week changes (with Monday exception for markets closed weekends) - Session: Matches specific hour:minute combinations (16:30=Void, 02:00=Asia end, 06:30=London end, 11:00=NY AM end, 15:30=NY PM end) - 90m: Calculates (hour*60 + minute - 120) % 90 == 0 to detect 90-minute boundaries from 02:00 EST baseline HOW TO USE Setup (Automatic Mode - Recommended): 1. Apply to chart of supported pair (see correlation list above) 2. Indicator automatically detects optimal comparison symbols 3. Enable/disable specific cycle categories (Swing or Intraday) in settings 4. Enable/disable individual cycles within each category 5. Adjust visual preferences (colors, line styles, labels) Setup (Manual Mode): 1. Uncheck "Automatic Symbol Mode" in settings 2. Enter "Manual Symbol #1" (e.g., ES1! when chart shows NQ1!) 3. Optional: Enter "Manual Symbol #2" for three-way comparison 4. Check "Invert" if symbol is inversely correlated (e.g., DXY vs EURUSD) Chart Timeframe Requirements: - Swing cycles: Chart TF must be <= cycle period (e.g., Daily cycle requires 1H or lower chart) - Intraday cycles: Chart TF must divide evenly into cycle (e.g., 90m cycle requires 30m, 15m, 10m, 5m, or lower chart) - TrueDay: Automatically selected for 1H and below chart TF on 24-hour markets (futures, forex, crypto) Interpretation: - Blue lines = Bullish SMT (chart made lower low within cycle, correlated pair held higher). Potential reversal up. - Red lines = Bearish SMT (chart made higher high within cycle, correlated pair stayed lower). Potential reversal down. - Dots in labels = Multiple SMT signals overlap. Hover to see all cycles showing divergence. SETTINGS EXPLAINED Symbols: - Automatic Symbol Mode: Uses built-in correlation intelligence (recommended) - Manual Symbol #1/2: Override automatic selection - Invert: For inverse correlations (DXY vs majors) - Hide Exact Overlap: Removes duplicate signals with identical start/end times - Hide 90m Hierarchy Overlap: Hides sub-90m SMT (30m, 10m, 3m, 1m) when contained within parent 90m window - Hide All Overlap: Hides lower precedence SMT when start/end points overlap higher precedence SMT Intraday Cycles (Enable/Disable per symbol): - Session: Asia (18:00-02:00), London (02:00-08:30), NY AM (08:30-12:00), NY PM (12:00-17:00) EST - 90m: Three 90-minute institutional windows per day - 30m: 30-minute cycles - 10m, 3m, 1m: Scalping cycles - Each cycle has two checkboxes: left for Symbol #1, right for Symbol #2 Swing Cycles (Enable/Disable per symbol): - Yearly: 12-month cycles - Quarterly: 3-month cycles - Monthly: Calendar month cycles - Weekly: 7-day cycles - Daily: Standard daily bars (18:00-18:00 EST) OR TrueDay (00:00-00:00 EST on 1H and below chart TF for 24h markets) - Each cycle has two checkboxes: left for Symbol #1, right for Symbol #2 Display: - Bull/Bear: Enable/disable directional signals - Line colors, styles (solid/dashed/dotted), widths - Label: Show/hide text labels with color and size options - SMT formation time: Displays timestamp in tooltip (New York time) UPDATES This script is actively maintained. Updates released through TradingView's native update system. For technical questions, use the comment section below.Indicatore Pine Script®di AlgoKings_Official6

Multi Cycles Slope-Fit System MLMulti Cycles Predictive System : A Slope-Adaptive Ensemble Executive Summary: The MCPS-Slope (Multi Cycles Slope-Fit System) represents a paradigm shift from static technical analysis to adaptive, probabilistic market modeling. Unlike traditional indicators that rely on a single algorithm with fixed settings, this system deploys a "Mixture of Experts" (MoE) ensemble comprising 13 distinct cycle and trend algorithms. Using a Gradient-Based Memory (GBM) learning engine, the system dynamically solves the "Cycle Mode" problem by real-time weighting. It aggressively curve-fits the Slope of component cycles to the Slope of the price action, rewarding algorithms that successfully predict direction while suppressing those that fail. This is a non-repainting, adaptive oscillator designed to identify market regimes, pinpoint high-probability reversals via OB/OS logic, and visualize the aggregate consensus of advanced signal processing mathematics. 1. The Core Philosophy: Why "Slope" Matters: In technical analysis, most traders focus on Levels (Price is above X) or Values (RSI is at 70). However, the primary driver of price action is Momentum, which is mathematically defined as the Rate of Change, or the Slope. This script introduces a novel approach: Slope Fitting. Instead of asking "Is the cycle high or low?", this system asks: "Is the trajectory (Slope) of this cycle matching the trajectory of the price?" The Dual-Functionality of the Normalized Oscillator The final output is a normalized oscillator bounded between -1.0 and +1.0. This structure serves two critical functions simultaneously: Directional Bias (The Slope): When the Combined Cycle line is rising (Positive Slope), the aggregate consensus of the 13 algorithms suggests bullish momentum. When falling (Negative Slope), it suggests bearish momentum. The script measures how well these slopes correlate with price action over a rolling lookback window to assign confidence weights. Overbought / Oversold (OB/OS) Identification: Because the output is mathematically clipped and normalized: Approaching +1.0 (Overbought): Indicates that the top-weighted algorithms have reached their theoretical maximum amplitude. This is a statistical extreme, often preceding a mean reversion or trend exhaustion. Approaching -1.0 (Oversold): Indicates the aggregate cycle has reached maximum bearish extension, signaling a potential accumulation zone. Zero Line (0.0): The equilibrium point. A cross of the Zero Line is the most traditional signal of a trend shift. 2. The "Mixture of Experts" (MoE) Architecture: Markets are dynamic. Sometimes they trend (Trend Following works), sometimes they chop (Mean Reversion works), and sometimes they cycle cleanly (Signal Processing works). No single indicator works in all regimes. This system solves that problem by running 13 Algorithms simultaneously and voting on the outcome. The 13 "Experts" Inside the Code: All algorithms have been engineered to be Non-Repainting. Ehlers Bandpass Filter: Extracts cycle components within a specific frequency bandwidth. Schaff Trend Cycle: A double-smoothed stochastic of the MACD, excellent for cycle turning points. Fisher Transform: Normalizes prices into a Gaussian distribution to pinpoint turning points. Zero-Lag EMA (ZLEMA): Reduces lag to track price changes faster than standard MAs. Coppock Curve: A momentum indicator originally designed for long-term market bottoms. Detrended Price Oscillator (DPO): Removes trend to isolate short-term cycles. MESA Adaptive (Sine Wave): Uses Phase accumulation to detect cycle turns. Goertzel Algorithm: Uses Digital Signal Processing (DSP) to detect the magnitude of specific frequencies. Hilbert Transform: Measures the instantaneous position of the cycle. Autocorrelation: measures the correlation of the current price series with a lagged version of itself. SSA (Simplified): Singular Spectrum Analysis approximation (Lag-compensated, non-repainting). Wavelet (Simplified): Decomposes price into approximation and detail coefficients. EMD (Simplified): Empirical Mode Decomposition approximation using envelope theory. 3. The Adaptive "GBM" Learning Engine This is the "Machine Learning" component of the script. It does not use pre-trained weights; it learns live on your chart. How it works: Fitting Window: On every bar, the system looks back 20 days (configurable). Slope Correlation: It calculates the correlation between the Slope of each of the 13 algorithms and the Slope of the Price. Directional Bonus: It checks if the algorithm is pointing in the same direction as the price. Weight Optimization: Algorithms that match the price direction and correlation receive a higher "Fit Score." Algorithms that diverge from price action are penalized. A "Softmax" style temperature function and memory decay allow the weights to shift smoothly but aggressively. The Result: If the market enters a clean sine-wave cycle, the Ehlers and Goertzel weights will spike. If the market explodes into a linear trend, ZLEMA and Schaff will take over, suppressing the cycle indicators that would otherwise call for a premature top. 4. How to Read the Interface: The visual interface is designed for maximum information density without clutter. The Dashboard (Bottom Left - GBM Stats) Combined Fit: A percentage score (0-100%). High values (>70%) mean the system is "Locked In" and tracking price accurately. Low values suggest market chaos/noise. Entropy: A measure of disorder. High entropy means the algorithms disagree (Neutral/Chop). Low entropy means the algorithms are unanimous (Strong Trend). Top 1 / Top 3 Weight: Shows how concentrated the decision is. If Top 1 Weight is 50%, one algorithm is dominating the decision. The Matrix (Bottom Right - Weight Table) This table lifts the hood on the engine. Fit Score: How well this specific algo is performing right now. Corr/Dir: Raw correlation and Direction Match stats. Weight: The actual percentage influence this algorithm has on the final line. Cycle: The current value of that specific algorithm. Regime: Identifies if the consensus is Bullish, Bearish, or Neutral. The Chart Overlay The Line: The Gradient-Colored line is the Weighted Ensemble Prediction. Green: Bullish Slope. Red: Bearish Slope. Triangles: Zero-Cross signals (Bullish/Bearish). "STRONG" Labels: Appears when the cycle sustains a value above +0.5 or below -0.5, indicating strong momentum. Background Color: Changes subtly to reflect the aggregate Regime (Strong Up, Bullish, Neutral, Bearish, Strong Down). 5. Trading Strategies: A. The Slope Reversal (OB/OS Fade) Concept: Catching tops and bottoms using the -1/+1 normalization. Signal: Wait for the Combined Cycle to reach extreme values (>0.8 or <-0.8). Trigger: The entry is taken not when it hits the level, but when the Slope flips. Short: Cycle hits +0.9, color turns from Green to Red (Slope becomes negative). Long: Cycle hits -0.9, color turns from Red to Green (Slope becomes positive). B. The Zero-Line Trend Join Concept: Joining an established trend after a correction. Signal: Price is trending, but the Cycle pulls back to the Zero line. Trigger: A "Triangle" signal appears as the cycle crosses Zero in the direction of the higher timeframe trend. C. Divergence Analysis Concept: Using the "Fit Score" to identify weak moves. Signal: Price makes a Higher High, but the Combined Cycle makes a Lower High. Confirmation: Check the GBM Stats table. If "Combined Fit" is dropping while price is rising, the trend is decoupling from the cycle logic. This is a high-probability reversal warning. 6. Technical Configuration: Fitting Window (Default: 20): The number of bars the ML engine looks back to judge algorithm performance. Lower (10-15) for scalping/quick adaptation. Higher (30-50) for swing trading and stability. GBM Learning Rate (Default: 0.25): Controls how fast weights change. High (>0.3): The system reacts instantly to new behaviors but may be "jumpy." Low (<0.15): The system is very smooth but may lag in regime changes. Max Single Weight (Default: 0.55): Prevents one single algorithm from completely hijacking the system, ensuring an ensemble effect remains. Slope Lookback: The period over which the slope (velocity) is calculated. 7. Disclaimer & Notes: Repainting: This indicator utilizes closed bar data for calculations and employs non-repainting approximations of SSA, EMD, and Wavelets. It does not repaint historical signals. Calculations: The "ML" label refers to the adaptive weighting algorithm (Gradient-based optimization), not a neural network black box. Risk: No indicator guarantees future performance. The "Fit Score" is a backward-looking metric of recent performance; market regimes can shift instantly. Always use proper risk management. Author's Note The MCPS-Slope was built to solve the frustration of "indicator shopping." Instead of switching between an RSI, a MACD, and a Stochastic depending on the day, this system mathematically determines which one is working best right now and presents you with a single, synthesized data stream. If you find this tool useful, please leave a Boost and a Comment below! Indicatore Pine Script®di jaydesaigu39

SMT Divergence - Time & Calendar CyclesOverview This indicator is a tool designed to detect SMT Divergences across multiple market structures. It operates on a Dual-Layer Logic, which filters, ranks, and renders divergences based on specific, adjustable Time Cycles (e.g., 90-minute, or 30-minute rolling windows) and Calendar Cycles (e.g., Daily, or Weekly structure). 1. Core Concept: Automated SMT Detection SMT Divergences occur when correlated instruments fail to confirm each other's price action at key structural pivots. For example, if the Nasdaq (NQ) makes a higher high while the S&P 500 (ES) fails to do so, that can be considered a SMT Divergence , this discrepancy in correlation could indicate a potential shift in structural momentum and a weakening of the prevailing trend. This indicator automates this analysis by comparing the Main Chart against up to three user-defined Comparison Symbols. It supports: Direct Correlation: Identifies standard divergences between positively correlated assets where one fails to confirm the other's new high or low (e.g., NQ vs. ES). Inverse Correlation: Accounts for negative correlation to detect failures in symmetry, such as when the Main Chart makes a Higher High but the Inverse Symbol fails to make the expected Lower Low (e.g., EURUSD vs. DXY). Cross Symbol vs. Symbol: Logic that cross-verifies comparison symbols against each other to find internal market weakness, even if the main chart is currently neutral (e.g., Symbol 1 vs. Symbol 2). 2. How It Works: Technical Architecture To accurately map market structure, the indicator uses a specific technical method to handle data synchronization and structure storage: A. Data Synchronization The tool utilizes 'request.security' targeting the current chart's resolution (native timeframe) to retrieve comparison data of the other symbol. This method enforces strict bar-by-bar alignment between the main symbol and the comparison symbol, preventing the access of future data (lookahead bias) and ensuring historical data integrity. B. Pivot Arrays The script identifies significant swing points and stores them in custom arrays. It iterates through these arrays to compare the current price structure against historical structures stored in memory. The array storage and comparison logic operates in two distinct modes depending on the cycle type: 2.1 Time Cycles (Intraday Analysis) Targeting specific, adjustable time windows like 90-minute or 30-minute cycles. Session Bound: These cycles are strictly bound to a user-defined trading session (e.g., 09:30 - 16:00). Continuous Roll: They repeat continuously throughout the window until the session ends. Session Reset: At the start of every new session, calculation data resets to ensure signals reflect only the current session, while preserving all historical lines on the chart. 2.2 Calendar Cycles (Macro Analysis) Targeting Higher Timeframe (HTF) structural analysis (Daily, Weekly, Monthly, Quarterly, and Yearly). Persistent Data: Unlike Time Cycles, Calendar Cycles utilize persistent data arrays that survive session resets. Calculation Mode: "Exchange Session" prevents ghost lines on Futures, while "Input Timezone" enforces strict midnight resets for Crypto/CFDs. 3. The Unified SMT Visualization The indicator provides a Composite Visualization , unifying micro (Intraday) and macro (Calendar) analysis by simultaneously projecting divergence signals onto a single chart view. Live vs. Historical Logic: The Live Feed (Dynamic State): This is the only component where repainting occurs. Signals within the current active cycle are temporary and self-correcting: Updates: If the price pushes to a new extreme within the open cycle, the SMT line automatically redraws to the new High/Low. Invalidation: If the Comparison Symbol eventually breaks its structure ("catches up") before the cycle closes, the divergence is no longer valid, and the signal is removed. Example: In a 90-minute Time Cycle, a signal might form at minute 30. If the Comparison Symbol confirms the move at minute 45, the signal is invalidated. If the divergence holds until minute 90, it becomes permanent. The Historian (Permanent Record): Once a cycle closes, the final state is locked. Validated signals are transferred to the historical array and will never change (non-repainting). 4. Key Features & Capabilities 4.1 Multi-Symbol & Correlation Triple-Check Logic: Capable of comparing the Main Chart against Symbol 1, Symbol 2, and Symbol 3 simultaneously. Cross-Symbol Check: The script can optionally validate Symbol 1 against Symbol 2 (e.g., checking ES vs. YM) and plot the result on your main chart, providing a broader market view. 4.2 Structural Range Validation The script includes strict validation logic to ensure high-quality data. It automatically verifies that the detected highs and lows are the true extremes of the cycle range. Lookback Cycles: Users define the exact number of preceding historical cycles the current structure must be compared against (e.g., comparing against the last 9 cycles), allowing for customization of structural depth. 4.3 Professional Drawing & Chart Management Visual Collision Detection: The script uses Coordinate Tracking to store the start and end points of every rendered divergence. If a lower timeframe cycle attempts to draw over an existing higher-priority structure, the logic compares their coordinates and suppresses the lower-priority signal to prevent visual clutter. Data Integrity: The script automatically validates cycle duration to ensure signals do not span across abnormal time gaps or missing data. Memory Optimization: The script actively manages internal memory to prevent execution limits, allowing for deep backtesting history even on lower timeframes. 4.4 Structural Parameters Furthest / Nearest Mode: Determines which specific pivot to target when multiple candidates exist within the same search window. Furthest: Targets the extreme point furthest back in time within the cycle range (captures the widest possible structure). Nearest: Targets the most recent valid pivot (captures the tightest, most immediate structure). Anchor Mode: Controls exactly where the divergence line connects: Structural: Always connects to the Main Chart's pivot High/Low. Snap to Aggressor: The precision method. The line "snaps" to the exact candle where the structure was broken first, whether on the Main Chart or the Comparison Symbol. Cycle Boundary Overlap: Controls how the transition candle is handled between time cycles (Overlap On vs. Clean Start). 4.5 Full Customization Adaptive & Custom Coloring: Labels automatically adjust to background brightness for optimal readability. Includes a manual override for user-defined color preferences. Visual Control: Fully customizable line styles, widths, and colors for every individual cycle. 5. How To Use This Tool Configuration: Set your Timezone and Session Start/End times in the settings. This ensures "Time Cycles" align with your specific market. Select Symbols: Input your comparison symbols (e.g., ES, YM, or inversely DXY). Crucial: Ensure the "Inverse" toggle is checked for negatively correlated assets. Cycle Selection: Enable the specific cycles relevant to your strategy (e.g., Daily + 90-minutes). Render History: Scroll the chart back to the beginning of your available price history after loading the indicator or changing timeframes to process maximum historical data. Interpretation: Bearish SMT: Price makes a Higher High, but the correlated asset makes a Lower High. This divergence could indicate a potential shift in structural momentum and a weakening of the prevailing uptrend. Bullish SMT: Price makes a Lower Low, but the correlated asset makes a Higher Low. This divergence could indicate a potential shift in structural momentum and a weakening of the prevailing downtrend. Disclaimer This indicator is designed for educational purposes only. It does not constitute financial advice or a recommendation to trade. Trading involves risk, and past performance does not guarantee future results.Indicatore Pine Script®di TimeLabsAlgoAggiornato 2234

Wosabi Time Cycle Gann v1 This indicator is an auxiliary tool for drawing the five-year and ten-year cycle, as it draws vertical lines every 12 candles and for 12 minor cycles, so that a major cycle consists of 144 candles, which is the ten-year cycle. It helps to know whether the current trend will continue for the five-year cycle and whether it will complete the ten-year cycle or not The standard cycle assumes that the trend is from a bottom or a top, if it continues for more than 24 candles to 36 candles, then corrects and does not break the bottom or top, then the trend will continue at least to complete the five-year cycle, i.e. 72 candles, and if the trend continues and the seven-year cycle closes at the 82 candle above The price of the candle of the strategic line No. 42, there is a possibility to complete the ten-year cycle (you must have experience in the standard patterns of time cycles as explained by gan). The indicator also draws the digital gates in horizontal lines, and you have to select them manually and adjust the price difference from one currency to another from the settings. When adding the indicator for the first time, you must specify the candle of the beginning of the trend, whether at a bottom or a top, as well as specifying the highest or lowest price that is expected to reach five digital gates, and you can modify the gates later in the settings. You can show a horizontal line at the close of each minor cycle of 24 candles, and you can adjust the line length from the settings. You can also show lines on the vibration plugs. When the trend is up, the end price must be higher than the starting price, in order to draw the direction for the gates correctly, and when the trend is down, the end price must be lower than the starting price. Important note: This indicator depends on your experience in time cycles and will not give you any buy or sell signals. It is an indicator that saves you drawing for cycles and gates and depends on your personal experience in time cycles. هذا المؤشر اداة مساعدة لرسم دورة الخمس سنوات والعشر سنوات، فهو يرسم خطوط اعمده راسية كل 12 شمعة ولعدد 12 دورة صغرى لتتكون دورة كبرى من 144 شمعة وهي دورة العشر سنوات وهي تساعد لمعرفة هل الاتجاه الحالي سيستمر لدورة الخمس سنوات وهل سيكمل دورة العشر سنوات ام لا ، فالدورة القياسية تفترض ان الاتجاه من قاع او قمة اذا استمر لاكثر من 24 شمعة الى 36 شمعة ثم صحح ولم يكسر القاع او القمة فإن الاتجاه سيستمر على الاقل لاكمال دورة الخمس سنوات اي 72 شمعة ، واذا استمر الاتجاه واغلق دورة السبع سنوات عند الشمعة 82 فوق سعر شمعة خط الاستراتيجي رقم 42 فهنالك احتمالية لاكمال دورة العشر سنوات (يجب ان يكون ليك خبرة في الانماط القياسية للدورات الزمنية كما شرحها gan). كذلك يقوم المؤشر برسم البوابات الرقمية في خطوط افقية وعليك تحديدها بشكل يدوي وتعديل فارق السعر من عملة لاخرى من الاعدادات . عند اضافة المؤشر لاول مرة يجب تحديد شمعة بداية الاتجاه سواء عند قاع او قمة وكذلك تحديد السعر الاعلى او الادنى المتوقع ان تصل له خمس بوابات رقمية ويمكنك تعديل البوابات لاحقا من الاعدادات . يمكنك اظهار خط افقي عند اغلاق كل دورة صغرى لعدد 24 شمعة ويمكنك تعديل طول الخط من الاعدادات . يمكنك كذلك اظهار خطوط على شمعات الاهتزاز . عندما يكون الاتجاه صاعد يجب ان يكون سعر النهاية اعلى من سعر البداية ليتم رسم الاتتجاه للبوابات بشكل صحيح وعندما يكون الاتجاه هابط يجب ان يكون سعر النهاية ادنى من سعر البداية . ملاحظة هامة : هذا المؤشر يعتمد على خبرتك في الدورات الزمنية ولن يعطيك اي اشارات شراء او بيع فهو مؤشر يوفر عليك الرسم للدورات والبوابات ويعتمد على خبرتك الشخصية في الدورات الزمنية . Indicatore Pine Script®di AhmadWosabiAggiornato 66158