Indicator Functions with Factor and HeikinAshiHello all,

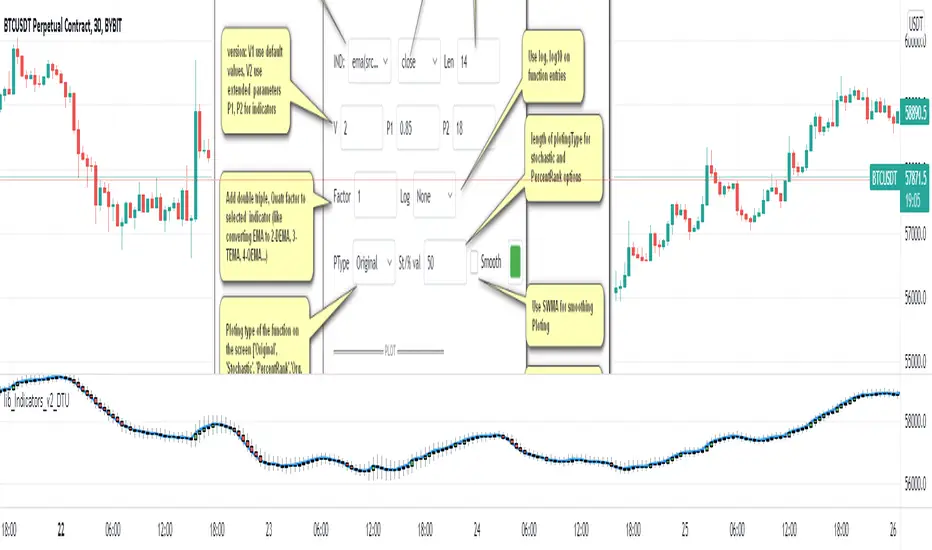

This indicator returns below selected indicators values with entered parameters.

Also you can add factorization, functions candles, function HeikinAshi and more to the plot.

VERSION:

Version 1: returns series only source and Length with already defined default values

Version 2: returns series with source, Length, p1 and p2 parameters according to the indicator definition (ex: )

PARAMETERS p1 p2

for defining multi arguments (See indicators list) indicator input value usable with verison=V2 selected.. ex: for alma( src , len ,offset=0.85,sigma=6), set source=source, len=length, p1=0.85 an p2=6

FACTOR:

Add double triple, Quadruple factors to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

1-Original

2-Double

3-Triple

4-Quadruple

LOG

Log: Use log, log10 on function entries

PLOTTING:

PType: Plotting type of the function on the screen

Original :use original values

Org. Range (-1,1): usable for indicators between range -1 and 1

Stochastic: Convert indicator values by using stochastic calculation between -1 & 1. (use AT/% length to better view)

PercentRank: Convert indicator values by using Percent Rank calculation between -1 & 1. (use AT/% length to better view)

ST/%: length for plotting Type for stochastic and Percent Rank options

Smooth: Use SWMA for smoothing the function

DISPLAY TYPES

Plot Candles: Display the selected indicator as candle by implementing values

Plot Ind: Display result of indicator with selected source

HeikinAshi: Display Selected indicator candles with Heikin Ashi calculation

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma( src , len ,offset=0.85,sigma=6)', // Arnaud Legoux Moving Average

ama = 'ama( src , len ,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', // Accumulation/distribution index.

cma = 'cma( src , len )', //Corrective Moving average

dema = 'dema( src , len )', // Double EMA (Same as EMA with 2 factor)

ema = 'ema( src , len )', // Exponential Moving Average

gmma = 'gmma( src , len )', //Geometric Mean Moving Average

hghst = 'highest( src , len )', //Highest value for a given number of bars back.

hl2ma = 'hl2ma( src , len )', //higest lowest moving average

hma = 'hma( src , len )', // Hull Moving Average .

lgAdt = 'lagAdapt( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre( src , len )', //Ehler's Laguerre filter

lsrcp = 'lesrcp( src , len )', //lowest exponential esrcpanding moving line

lexp = 'lexp( src , len )', //lowest exponential expanding moving line

linrg = 'linreg( src , len ,loffset=1)', // Linear regression

lowst = 'lowest( src , len )', //Lovest value for a given number of bars back.

pcnl = 'percntl( src , len )', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli( src , len )', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema( src , len )', //Range EMA (REMA)

rma = 'rma( src , len )', //Moving average used in RSI . It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma( src , len )', // Smoothed Moving Average

smma = 'smma( src , len )', // Smoothed Moving Average

supr2 = 'super2( src , len )', //Ehler's super smoother, 2 pole

supr3 = 'super3( src , len )', //Ehler's super smoother, 3 pole

strnd = 'supertrend( src , len ,period=3)', //Supertrend indicator

swma = 'swma( src , len )', //Sine-Weighted Moving Average

tema = 'tema( src , len )', // Triple EMA (Same as EMA with 3 factor)

tma = 'tma( src , len )', //Triangular Moving Average

vida = 'vida( src , len )', // Variable Index Dynamic Average

vwma = 'vwma( src , len )', // Volume Weigted Moving Average

wma = 'wma( src , len )', //Weigted Moving Average

angle = 'angle( src , len )', //angle of the series (Use its Input as another indicator output)

atr = 'atr( src , len )', // average true range . RMA of true range.

bbr = 'bbr( src , len ,mult=1)', // bollinger %%

bbw = 'bbw( src , len ,mult=2)', // Bollinger Bands Width . The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci( src , len )', // commodity channel index

cctbb = 'cctbbo( src , len )', // CCT Bollinger Band Oscilator

chng = 'change( src , len )', //Difference between current value and previous, source - source.

cmo = 'cmo( src , len )', // Chande Momentum Oscillator . Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog( src , len )', //The cog (center of gravity ) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve( src , len )', // Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl( src , len )', // Correlation coefficient . Describes the degree to which two series tend to deviate from their ta. sma values.

count = 'count( src , len )', //green avg - red avg

dev = 'dev( src , len )', //ta.dev() Measure of difference between the series and it's ta. sma

fall = 'falling( src , len )', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr( src , len ,mult=2)', // Keltner Channels Range

kcw = 'kcw( src , len ,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd( src , len )', // macd

mfi = 'mfi( src , len )', // Money Flow Index

nvi = 'nvi()', // Negative Volume Index

obv = 'obv()', // On Balance Volume

pvi = 'pvi()', // Positive Volume Index

pvt = 'pvt()', // Price Volume Trend

rise = 'rising( src , len )', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc( src , len )', // Rate of Change

rsi = 'rsi( src , len )', // Relative strength Index

smosc = 'smi_osc( src , len ,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig( src , len ,fast=5, slow=34)', //smi Signal

stdev = 'stdev( src , len )', //Standart deviation

trix = 'trix( src , len )' , //the rate of change of a triple exponentially smoothed moving average .

tsi = 'tsi( src , len )', //True Strength Index

vari = 'variance( src , len )', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta. sma ), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc( src , len )', // Williams %R

wad = 'wad()', // Williams Accumulation/Distribution .

wvad = 'wvad()' //Williams Variable Accumulation/Distribution

I will update the indicator list when I will update the library

Thanks to tradingview, @RodrigoKazuma for their open source indicators

Cerca negli script per "Exponential"

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

Multiple EMAAn exponential moving average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points. The exponential moving average is also referred to as the exponentially weighted moving average. An exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average (SMA), which applies an equal weight to all observations in the period.

The EMA is a moving average that places a greater weight and significance on the most recent data points.

Like all moving averages, this technical indicator is used to produce buy and sell signals based on crossovers and divergences from the historical average.

Traders often use several different EMA lengths, such as 10-day, 50-day, and 200-day moving averages.

Points to remember:

Exponential moving averages are more sensitive to the recent price

EMA can signal good trades, but it can also keep you out of bad trades

EMA offers dynamic support and resistance levels, which is good for trailing Stop Loss

The EMA slope shape has hidden secrets

The rules for the EMA trading strategy can be modified to fit your own trading needs. We don’t claim this to be hard rules, but they are good on their own to make for a great trading strategy. Make sure you first test out the EMA strategy on a paper trading account before you risk any of your hard-earned money

MLMatrixLibOverview

MLMatrixLib is a comprehensive Pine Script v6 library implementing machine learning algorithms using native matrix operations. This library provides traders and developers with a toolkit of statistical and ML methods for building quantitative trading systems, performing data analysis, and creating adaptive indicators.

How It Works

The library leverages Pine Script's native matrix type to perform efficient linear algebra operations. Each algorithm is implemented from first principles, using matrix decomposition, iterative optimization, and statistical estimation techniques. All functions are designed for numerical stability with careful handling of edge cases.

---

Library Contents (34 Sections)

Section 1: Utility Functions & Matrix Operations

Core building blocks including:

• identity(n) - Creates n×n identity matrix

• diagonal(values) - Creates diagonal matrix from array

• ones(rows, cols) / zeros(rows, cols) - Matrix constructors

• frobeniusNorm(m) / l1Norm(m) - Matrix norm calculations

• hadamard(m1, m2) - Element-wise multiplication

• columnMeans(m) / rowMeans(m) - Statistical aggregations

• standardize(m) - Z-score normalization (zero mean, unit variance)

• minMaxNormalize(m) - Scale values to range

• fitStandardScaler(m) / fitMinMaxScaler(m) - Reusable scaler parameters

• addBiasColumn(m) - Prepend column of ones for regression

• arrayMedian(arr) / arrayPercentile(arr, p) - Array statistics

Section 2: Activation Functions

Numerically stable implementations:

• sigmoid(x) / sigmoidMatrix(m) - Logistic function with overflow protection

• tanhActivation(x) / tanhMatrix(m) - Hyperbolic tangent

• relu(x) / reluMatrix(m) - Rectified Linear Unit

• leakyRelu(x, alpha) - Leaky ReLU with configurable slope

• elu(x, alpha) - Exponential Linear Unit

• Derivatives for backpropagation: sigmoidDerivative, tanhDerivative, reluDerivative

Section 3: Linear Regression (OLS)

Ordinary Least Squares implementation using the normal equation (X'X)⁻¹X'y:

• fitLinearRegression(X, y) - Fits model, returns coefficients, R², standard error

• fitSimpleLinearRegression(x, y) - Single-variable regression

• predictLinear(model, X) - Generate predictions

• predictionInterval(model, X, confidence) - Confidence intervals using t-distribution

• Model type stores: coefficients, R-squared, residuals, standard error

Section 4: Weighted Linear Regression

Generalized least squares with observation weights:

• fitWeightedLinearRegression(X, y, weights) - Solves (X'WX)⁻¹X'Wy

• Useful for downweighting outliers or emphasizing recent data

Section 5: Polynomial Regression

Fits polynomials of arbitrary degree:

• fitPolynomialRegression(x, y, degree) - Constructs Vandermonde matrix

• predictPolynomial(model, x) - Evaluate polynomial at points

Section 6: Ridge Regression (L2 Regularization)

Adds penalty term λ||β||² to prevent overfitting:

• fitRidgeRegression(X, y, lambda) - Solves (X'X + λI)⁻¹X'y

• Lambda parameter controls regularization strength

Section 7: LASSO Regression (L1 Regularization)

Coordinate descent algorithm for sparse solutions:

• fitLassoRegression(X, y, lambda, maxIter, tolerance) - Iterative soft-thresholding

• Produces sparse coefficients by driving some to exactly zero

• softThreshold(x, lambda) - Core shrinkage operator

Section 8: Elastic Net (L1 + L2 Regularization)

Combines LASSO and Ridge penalties:

• fitElasticNet(X, y, lambda, alpha, maxIter, tolerance)

• Alpha balances L1 vs L2: alpha=1 is LASSO, alpha=0 is Ridge

Section 9: Huber Robust Regression

Iteratively Reweighted Least Squares (IRLS) for outlier resistance:

• fitHuberRegression(X, y, delta, maxIter, tolerance)

• Delta parameter defines transition between L1 and L2 loss

• Downweights observations with large residuals

Section 10: Quantile Regression

Estimates conditional quantiles using linear programming approximation:

• fitQuantileRegression(X, y, tau, maxIter, tolerance)

• Tau specifies quantile (0.5 = median, 0.25 = lower quartile, etc.)

Section 11: Logistic Regression (Binary Classification)

Gradient descent optimization of cross-entropy loss:

• fitLogisticRegression(X, y, learningRate, maxIter, tolerance)

• predictProbability(model, X) - Returns probabilities

• predictClass(model, X, threshold) - Returns binary predictions

Section 12: Linear SVM (Support Vector Machine)

Sub-gradient descent with hinge loss:

• fitLinearSVM(X, y, C, learningRate, maxIter)

• C parameter controls regularization (higher = harder margin)

• predictSVM(model, X) - Returns class predictions

Section 13: Recursive Least Squares (RLS)

Online learning with exponential forgetting:

• createRLSState(nFeatures, lambda, delta) - Initialize state

• updateRLS(state, x, y) - Update with new observation

• Lambda is forgetting factor (0.95-0.99 typical)

• Useful for adaptive indicators that update incrementally

Section 14: Covariance and Correlation

Matrix statistics:

• covarianceMatrix(m) - Sample covariance

• correlationMatrix(m) - Pearson correlations

• pearsonCorrelation(x, y) - Single correlation coefficient

• spearmanCorrelation(x, y) - Rank-based correlation

Section 15: Principal Component Analysis (PCA)

Dimensionality reduction via eigendecomposition:

• fitPCA(X, nComponents) - Power iteration method

• transformPCA(X, model) - Project data onto principal components

• Returns components, explained variance, and mean

Section 16: K-Means Clustering

Lloyd's algorithm with k-means++ initialization:

• fitKMeans(X, k, maxIter, tolerance) - Cluster data points

• predictCluster(model, X) - Assign new points to clusters

• withinClusterVariance(model) - Measure cluster compactness

Section 17: Gaussian Mixture Model (GMM)

Expectation-Maximization algorithm:

• fitGMM(X, k, maxIter, tolerance) - Soft clustering with probabilities

• predictProbaGMM(model, X) - Returns membership probabilities

• Models data as mixture of Gaussian distributions

Section 18: Kalman Filter

Linear state estimation:

• createKalman1D(processNoise, measurementNoise, ...) - 1D filter

• createKalman2D(processNoise, measurementNoise) - Position + velocity tracking

• kalmanStep(state, measurement) - Predict-update cycle

• Optimal filtering for noisy measurements

Section 19: K-Nearest Neighbors (KNN)

Instance-based learning:

• fitKNN(X, y) - Store training data

• predictKNN(model, X, k) - Classify by majority vote

• predictKNNRegression(model, X, k) - Average of k neighbors

• predictKNNWeighted(model, X, k) - Distance-weighted voting

Section 20: Neural Network (Feedforward)

Multi-layer perceptron:

• createNeuralNetwork(architecture) - Define layer sizes

• trainNeuralNetwork(nn, X, y, learningRate, epochs) - Backpropagation

• predictNN(nn, X) - Forward pass

• Supports configurable hidden layers

Section 21: Naive Bayes Classifier

Gaussian Naive Bayes:

• fitNaiveBayes(X, y) - Estimate class-conditional distributions

• predictNaiveBayes(model, X) - Maximum a posteriori classification

• Assumes feature independence given class

Section 22: Anomaly Detection

Statistical outlier detection:

• fitAnomalyDetector(X, contamination) - Mahalanobis distance-based

• detectAnomalies(model, X) - Returns anomaly scores

• isAnomaly(model, X, threshold) - Binary classification

Section 23: Dynamic Time Warping (DTW)

Time series similarity:

• dtw(series1, series2) - Compute DTW distance

• Handles sequences of different lengths

• Useful for pattern matching

Section 24: Markov Chain / Regime Detection

Discrete state transitions:

• fitMarkovChain(states, nStates) - Estimate transition matrix

• predictNextState(transitionMatrix, currentState) - Most likely next state

• stationaryDistribution(transitionMatrix) - Long-run probabilities

Section 25: Hidden Markov Model (Simple)

Baum-Welch algorithm:

• fitHMM(observations, nStates, maxIter) - EM training

• viterbi(model, observations) - Most likely state sequence

• Useful for regime detection

Section 26: Exponential Smoothing & Holt-Winters

Time series smoothing:

• exponentialSmooth(data, alpha) - Simple exponential smoothing

• holtWinters(data, alpha, beta, gamma, seasonLength) - Triple smoothing

• Captures trend and seasonality

Section 27: Entropy and Information Theory

Information measures:

• entropy(probabilities) - Shannon entropy in bits

• conditionalEntropy(jointProbs, marginalProbs) - H(X|Y)

• mutualInformation(probsX, probsY, jointProbs) - I(X;Y)

• kldivergence(p, q) - Kullback-Leibler divergence

Section 28: Hurst Exponent

Long-range dependence measure:

• hurstExponent(data) - R/S analysis

• H < 0.5: mean-reverting, H = 0.5: random walk, H > 0.5: trending

Section 29: Change Detection (CUSUM)

Cumulative sum control chart:

• cusumChangeDetection(data, threshold, drift) - Detect regime changes

• cusumOnline(value, prevCusumPos, prevCusumNeg, target, drift) - Streaming version

Section 30: Autocorrelation

Serial dependence analysis:

• autocorrelation(data, maxLag) - ACF for all lags

• partialAutocorrelation(data, maxLag) - PACF via Durbin-Levinson

• Useful for time series model identification

Section 31: Ensemble Methods

Model combination:

• baggingPredict(models, X) - Average predictions

• votingClassify(models, X) - Majority vote

• Improves robustness through aggregation

Section 32: Model Evaluation Metrics

Performance assessment:

• mse(actual, predicted) / rmse / mae / mape - Regression metrics

• accuracy(actual, predicted) - Classification accuracy

• precision / recall / f1Score - Binary classification metrics

• confusionMatrix(actual, predicted, nClasses) - Multi-class evaluation

• rSquared(actual, predicted) / adjustedRSquared - Goodness of fit

Section 33: Cross-Validation

Model validation:

• trainTestSplit(X, y, trainRatio) - Random split

• Foundation for walk-forward validation

Section 34: Trading Convenience Functions

Trading-specific utilities:

• priceMatrix(length) - OHLC data as matrix

• logReturns(length) - Log return series

• rollingSlope(src, length) - Linear trend strength

• kalmanFilter(src, processNoise, measurementNoise) - Filtered price

• kalmanFilter2D(src, ...) - Price with velocity estimate

• adaptiveMA(src, sensitivity) - Kalman-based adaptive moving average

• volAdjMomentum(src, length) - Volatility-normalized momentum

• detectSRLevels(length, nLevels) - K-means based S/R detection

• buildFeatures(src, lengths) - Multi-timeframe feature construction

• technicalFeatures(length) - Standard indicator feature set (RSI, MACD, BB, ATR, etc.)

• lagFeatures(src, lags) - Time-lagged features

• sharpeRatio(returns) - Risk-adjusted return measure

• sortinoRatio(returns) - Downside risk-adjusted return

• maxDrawdown(equity) - Maximum peak-to-trough decline

• calmarRatio(returns, equity) - Return/drawdown ratio

• kellyCriterion(winRate, avgWin, avgLoss) - Optimal position sizing

• fractionalKelly(...) - Conservative Kelly sizing

• rollingBeta(assetReturns, benchmarkReturns) - Market exposure

• fractalDimension(data) - Market complexity measure

---

Usage Example

```

import YourUsername/MLMatrixLib/1 as ml

// Create feature matrix

matrix X = ml.priceMatrix(50)

X := ml.standardize(X)

// Fit linear regression

ml.LinearRegressionModel model = ml.fitLinearRegression(X, y)

float prediction = ml.predictLinear(model, X_new)

// Kalman filter for smoothing

float smoothedPrice = ml.kalmanFilter(close, 0.01, 1.0)

// Detect support/resistance levels

array levels = ml.detectSRLevels(100, 3)

// K-means clustering for regime detection

ml.KMeansModel km = ml.fitKMeans(features, 3)

int cluster = ml.predictCluster(km, newFeature)

```

---

Technical Notes

• All matrix operations use Pine Script's native matrix type

• Numerical stability ensured through:

- Clamping exponential arguments to prevent overflow

- Division by zero protection with epsilon thresholds

- Iterative algorithms with convergence tolerance

• Designed for bar-by-bar execution in Pine Script's event-driven model

• Compatible with Pine Script v6

---

Disclaimer

This library provides mathematical tools for quantitative analysis. It does not constitute financial advice. Past performance of any algorithm does not guarantee future results. Users are responsible for validating models on their specific use cases and understanding the limitations of each method.

Uptrick: Logarithmic Crypto Bands

Description :

Introduction

The `Uptrick: Logarithmic Crypto Bands` indicator introduces an innovative approach to technical analysis tailored specifically for the cryptocurrency markets. By leveraging logarithmic transformations combined with dynamic exponential bands, this indicator offers a sophisticated method for identifying critical support and resistance levels, assessing market trends, and evaluating volatility. Its unique approach stands out from traditional indicators by addressing the specific challenges of high volatility and erratic price movements inherent in cryptocurrency trading.

Originality and Usefulness

** 1. Unique Logarithmic Transformation: **

- Innovation : Unlike traditional indicators that often use raw price data, the Uptrick: Logarithmic Crypto Bands applies a logarithmic transformation to the closing prices: logPrice = math.log(close). This approach is original because it reduces the impact of extreme price fluctuations, providing a smoother and more stable price series. This transformation addresses a common issue in cryptocurrency markets where large price swings can obscure true market trends.

- Advantage : The logarithmic transformation compresses the price range, which allows traders to better identify long-term trends and reduce the noise caused by outlier price movements. This results in a more reliable basis for analysis and enhances the ability to detect meaningful market patterns.

**2. Dynamic Exponential Bands :**

- Innovation : The indicator employs exponential calculations to derive dynamic support and resistance levels based on a central base line : baseLine * math.pow(multiplier, n). Unlike static bands that remain fixed regardless of market conditions, these bands adjust dynamically according to market volatility.

- Advantage : The dynamic nature of the bands provides a more responsive and adaptive tool for traders. As market volatility changes, the bands widen or narrow accordingly, offering a more accurate reflection of potential support and resistance levels. This adaptability improves the tool's effectiveness in varying market conditions compared to static or traditional bands.

Detailed Description and Substantiation

**1. Logarithmic Price Calculation :**

- Code : ` logPrice = math.log(close)

- Description : This calculation converts the closing price into its logarithmic value. By compressing the price range, it minimizes the distortion caused by extreme price movements, which can be particularly pronounced in the volatile cryptocurrency markets.

- Purpose : To provide a stabilized price series that facilitates more accurate trend analysis and reduces the influence of erratic price fluctuations.

**2. Moving Averages of Logarithmic Prices :**

- ** Long-Term Moving Average :**

- Code : maLongLogPrice = ta.sma(logPrice, longLength)

longLength = 2000

- ** Description : A simple moving average of the logarithmic price over a long period. This average helps filter out short-term noise and provides insight into the long-term market trend.

- Purpose : To offer a perspective on the overall market direction, making it easier to identify enduring trends and distinguish them from short-term price movements.

- Short-Term Moving Average :

- Code : maShortLogPrice = ta.sma(logPrice, shortLength) shortLength = 900

- Description : A simple moving average of the logarithmic price over a shorter period. This component captures more immediate price trends and potential reversal points.

- Purpose : To detect short-term trends and changes in market direction, allowing traders to make timely trading decisions based on recent price action.

**3. Base Line Calculation :**

- Code : baseLine = math.exp(maShortLogPrice)

- Description : Converts the short-term moving average of the logarithmic price back to the original price scale. This base line serves as the central reference point for calculating the surrounding bands.

- Purpose : To establish a benchmark level from which the exponential bands are calculated, providing a central reference for assessing potential support and resistance levels.

**4. Band Calculation and Plotting :**

- ** Code :**

- Band 1: plot(baseLine * math.pow(multiplier, 1), color=color.new(color.yellow, 20), linewidth=1, title="Band 1")

- Band 2: plot(baseLine * math.pow(multiplier, 2), color=color.new(color.yellow, 20), linewidth=1, title="Band 2")

- Band 3: plot(baseLine * math.pow(multiplier, 3), color=color.new(color.yellow, 20), linewidth=1, title="Band 3")

- Band 4: plot(baseLine * math.pow(multiplier, 4), color=color.new(color.yellow, 20), linewidth=1, title="Band 4")

- Band 5: plot(baseLine * math.pow(multiplier, 5), color=color.new(color.yellow, 10), linewidth=1, title="Band 5")

- Band 6: plot(baseLine * math.pow(multiplier, 6), color=color.new(color.yellow, 0), linewidth=1, title="Band 6")

- * Multiplier : Set at 1.3, adjusts the spacing between bands to accommodate varying levels of market volatility.

- Description : Bands are plotted at exponential intervals from the base line. Each band represents a potential support or resistance level, with the spacing between them increasing exponentially. The color opacity of each band indicates its level of significance, with closer bands being more relevant for immediate trading decisions.

** How to Use the Indicator :**

**1. Identifying Support and Resistance Levels :**

- Support Levels : The lower bands, closer to the base line, can act as potential support levels. When the price approaches these bands from above, they may indicate areas where the price could stabilize or reverse direction.

- Resistance Levels : The upper bands, further from the base line, serve as resistance levels. When the price nears these bands from below, they can act as barriers to price movement, potentially leading to reversals or stalls.

**2. Confirming Trends :**

- Uptrend Confirmation : When the price consistently remains above the base line and moves towards higher bands, it signals a strong bullish trend. This confirmation helps traders capitalize on upward price movements.

- Downtrend Confirmation : When the price stays below the base line and approaches lower bands, it indicates a bearish trend. This confirmation assists traders in acting on downward price movements.

3. Analyzing Volatility :

- Wide Bands : Wider spacing between bands reflects higher market volatility. This indicates a more turbulent trading environment, where price movements are less predictable. Traders may need to adjust their strategies to handle increased volatility.

- Narrow Bands : Narrower bands suggest lower volatility and a more stable market environment. This can result in more predictable price movements and clearer trading signals.

**4. Entry and Exit Points :**

- Entry Points : Consider buying when the price bounces off the base line or a band, which could signal support in an uptrend.

- Exit Points : Evaluate selling or taking profits when the price nears upper bands or shows signs of reversal at these levels. This approach helps in locking in gains or minimizing losses during a downtrend.

**Chart Example:**

Here you can see how the price reacted getting closer to this level. All green circles show a bounce-off. So just from looking at the chart we can see a potential bounce again pretty soon.

** Disclosure :**

- ** Performance Claims :** The `Uptrick: Logarithmic Crypto Bands` indicator is designed to assist traders in analyzing price levels and trends. It is important to understand that this tool provides historical data analysis and does not guarantee future performance. The features and benefits described are based on historical market behavior and should not be seen as a prediction of future results. Traders should use this indicator as part of a broader trading strategy and consider other factors before making trading decisions.

[AIO] Multi Collection Moving Averages 140 MA TypesAll In One Multi Collection Moving Averages.

Since signing up 2 years ago, I have been collecting various Сollections.

I decided to get it into a decent shape and make it one of the biggest collections on TV, and maybe the entire internet.

And now I'm sharing my collection with you.

140 Different Types of Moving Averages are waiting for you.

Specifically :

"

AARMA | Adaptive Autonomous Recursive Moving Average

ADMA | Adjusted Moving Average

ADXMA | Average Directional Moving Average

ADXVMA | Average Directional Volatility Moving Average

AHMA | Ahrens Moving Average

ALF | Ehler Adaptive Laguerre Filter

ALMA | Arnaud Legoux Moving Average

ALSMA | Adaptive Least Squares

ALXMA | Alexander Moving Average

AMA | Adaptive Moving Average

ARI | Unknown

ARSI | Adaptive RSI Moving Average

AUF | Auto Filter

AUTL | Auto-Line

BAMA | Bryant Adaptive Moving Average

BFMA | Blackman Filter Moving Average

CMA | Corrected Moving Average

CORMA | Correlation Moving Average

COVEMA | Coefficient of Variation Weighted Exponential Moving Average

COVNA | Coefficient of Variation Weighted Moving Average

CTI | Coral Trend Indicator

DEC | Ehlers Simple Decycler

DEMA | Double EMA Moving Average

DEVS | Ehlers - Deviation Scaled Moving Average

DONEMA | Donchian Extremum Moving Average

DONMA | Donchian Moving Average

DSEMA | Double Smoothed Exponential Moving Average

DSWF | Damped Sine Wave Weighted Filter

DWMA | Double Weighted Moving Average

E2PBF | Ehlers 2-Pole Butterworth Filter

E2SSF | Ehlers 2-Pole Super Smoother Filter

E3PBF | Ehlers 3-Pole Butterworth Filter

E3SSF | Ehlers 3-Pole Super Smoother Filter

EDMA | Exponentially Deviating Moving Average (MZ EDMA)

EDSMA | Ehlers Dynamic Smoothed Moving Average

EEO | Ehlers Modified Elliptic Filter Optimum

EFRAMA | Ehlers Modified Fractal Adaptive Moving Average

EHMA | Exponential Hull Moving Average

EIT | Ehlers Instantaneous Trendline

ELF | Ehler Laguerre filter

EMA | Exponential Moving Average

EMARSI | EMARSI

EPF | Edge Preserving Filter

EPMA | End Point Moving Average

EREA | Ehlers Reverse Exponential Moving Average

ESSF | Ehlers Super Smoother Filter 2-pole

ETMA | Exponential Triangular Moving Average

EVMA | Elastic Volume Weighted Moving Average

FAMA | Following Adaptive Moving Average

FEMA | Fast Exponential Moving Average

FIBWMA | Fibonacci Weighted Moving Average

FLSMA | Fisher Least Squares Moving Average

FRAMA | Ehlers - Fractal Adaptive Moving Average

FX | Fibonacci X Level

GAUS | Ehlers - Gaussian Filter

GHL | Gann High Low

GMA | Gaussian Moving Average

GMMA | Geometric Mean Moving Average

HCF | Hybrid Convolution Filter

HEMA | Holt Exponential Moving Average

HKAMA | Hilbert based Kaufman Adaptive Moving Average

HMA | Harmonic Moving Average

HSMA | Hirashima Sugita Moving Average

HULL | Hull Moving Average

HULLT | Hull Triple Moving Average

HWMA | Henderson Weighted Moving Average

IE2 | Early T3 by Tim Tilson

IIRF | Infinite Impulse Response Filter

ILRS | Integral of Linear Regression Slope

JMA | Jurik Moving Average

KA | Unknown

KAMA | Kaufman Adaptive Moving Average & Apirine Adaptive MA

KIJUN | KIJUN

KIJUN2 | Kijun v2

LAG | Ehlers - Laguerre Filter

LCLSMA | 1LC-LSMA (1 line code lsma with 3 functions)

LEMA | Leader Exponential Moving Average

LLMA | Low-Lag Moving Average

LMA | Leo Moving Average

LP | Unknown

LRL | Linear Regression Line

LSMA | Least Squares Moving Average / Linear Regression Curve

LTB | Unknown

LWMA | Linear Weighted Moving Average

MAMA | MAMA - MESA Adaptive Moving Average

MAVW | Mavilim Weighted Moving Average

MCGD | McGinley Dynamic Moving Average

MF | Modular Filter

MID | Median Moving Average / Percentile Nearest Rank

MNMA | McNicholl Moving Average

MTMA | Unknown

MVSMA | Minimum Variance SMA

NLMA | Non-lag Moving Average

NWMA | Dürschner 3rd Generation Moving Average (New WMA)

PKF | Parametric Kalman Filter

PWMA | Parabolic Weighted Moving Average

QEMA | Quadruple Exponential Moving Average

QMA | Quick Moving Average

REMA | Regularized Exponential Moving Average

REPMA | Repulsion Moving Average

RGEMA | Range Exponential Moving Average

RMA | Welles Wilders Smoothing Moving Average

RMF | Recursive Median Filter

RMTA | Recursive Moving Trend Average

RSMA | Relative Strength Moving Average - based on RSI

RSRMA | Right Sided Ricker MA

RWMA | Regressively Weighted Moving Average

SAMA | Slope Adaptive Moving Average

SFMA | Smoother Filter Moving Average

SMA | Simple Moving Average

SSB | Senkou Span B

SSF | Ehlers - Super Smoother Filter P2

SSMA | Super Smooth Moving Average

STMA | Unknown

SWMA | Self-Weighted Moving Average

SW_MA | Sine-Weighted Moving Average

TEMA | Triple Exponential Moving Average

THMA | Triple Exponential Hull Moving Average

TL | Unknown

TMA | Triangular Moving Average

TPBF | Three-pole Ehlers Butterworth

TRAMA | Trend Regularity Adaptive Moving Average

TSF | True Strength Force

TT3 | Tilson (3rd Degree) Moving Average

VAMA | Volatility Adjusted Moving Average

VAMAF | Volume Adjusted Moving Average Function

VAR | Vector Autoregression Moving Average

VBMA | Variable Moving Average

VHMA | Vertical Horizontal Moving Average

VIDYA | Variable Index Dynamic Average

VMA | Volume Moving Average

VSO | Unknown

VWMA | Volume Weighted Moving Average

WCD | Unknown

WMA | Weighted Moving Average

XEMA | Optimized Exponential Moving Average

ZEMA | Zero Lag Moving Average

ZLDEMA | Zero-Lag Double Exponential Moving Average

ZLEMA | Ehlers - Zero Lag Exponential Moving Average

ZLTEMA | Zero-Lag Triple Exponential Moving Average

ZSMA | Zero-Lag Simple Moving Average

"

Don't forget that you can use any Moving Average not only for the chart but also for any of your indicators without affecting the code as in my example.

But remember that some MAs are not designed to work with anything other than a chart.

All MA and Code lists are sorted strictly alphabetically by short name (A-Z).

Each MA has its own number (ID) by which you can display the Moving Average you need.

Next to the ID selection there are tooltips with short names and their numbers. Use them.

The panel below will help you to read the Name of the selected MA.

Because of the size of the collection I think this is the optimal and most convenient use. Correct me if this is not the case.

Unknown - Some MAs I collected so long ago that I lost the full real name and couldn't find the authors. If you recognize them, please let me know.

I have deliberately simplified all MAs to input just Source and Length.

Because the collection is so large, it would be quite inconvenient and difficult to customize all MA functions (multipliers, offset, etc.).

If you need or like any MA you will still have to take it from my collection for your code.

I tried to leave the basic MA settings inside function in first strings.

I have tried to list most of the authors, but since the bulk of the collection was created a long time ago and was not intended for public publication I could not find all of them.

Some of the features were created from scratch or may have been slightly modified, so please be careful.

If you would like to improve this collection, please write to me in PM.

Also Credits, Likes, Awards, Loves and Thanks to :

@alexgrover

@allanster

@andre_007

@auroagwei

@blackcat1402

@bsharpe

@cheatcountry

@CrackingCryptocurrency

@Duyck

@ErwinBeckers

@everget

@glaz

@gotbeatz26107

@HPotter

@io72signals

@JacobAmos

@JoshuaMcGowan

@KivancOzbilgic

@LazyBear

@loxx

@LuxAlgo

@MightyZinger

@nemozny

@NGBaltic

@peacefulLizard50262

@RicardoSantos

@StalexBot

@ThiagoSchmitz

@TradingView

— 𝐀𝐧𝐝 𝐎𝐭𝐡𝐞𝐫𝐬 !

So just a Big Thank You to everyone who has ever and anywhere shared their codes.

Machine Learning: SuperTrend Strategy TP/SL [YinYangAlgorithms]The SuperTrend is a very useful Indicator to display when trends have shifted based on the Average True Range (ATR). Its underlying ideology is to calculate the ATR using a fixed length and then multiply it by a factor to calculate the SuperTrend +/-. When the close crosses the SuperTrend it changes direction.

This Strategy features the Traditional SuperTrend Calculations with Machine Learning (ML) and Take Profit / Stop Loss applied to it. Using ML on the SuperTrend allows for the ability to sort data from previous SuperTrend calculations. We can filter the data so only previous SuperTrends that follow the same direction and are within the distance bounds of our k-Nearest Neighbour (KNN) will be added and then averaged. This average can either be achieved using a Mean or with an Exponential calculation which puts added weight on the initial source. Take Profits and Stop Losses are then added to the ML SuperTrend so it may capitalize on Momentum changes meanwhile remaining in the Trend during consolidation.

By applying Machine Learning logic and adding a Take Profit and Stop Loss to the Traditional SuperTrend, we may enhance its underlying calculations with potential to withhold the trend better. The main purpose of this Strategy is to minimize losses and false trend changes while maximizing gains. This may be achieved by quick reversals of trends where strategic small losses are taken before a large trend occurs with hopes of potentially occurring large gain. Due to this logic, the Win/Loss ratio of this Strategy may be quite poor as it may take many small marginal losses where there is consolidation. However, it may also take large gains and capitalize on strong momentum movements.

Tutorial:

In this example above, we can get an idea of what the default settings may achieve when there is momentum. It focuses on attempting to hit the Trailing Take Profit which moves in accord with the SuperTrend just with a multiplier added. When momentum occurs it helps push the SuperTrend within it, which on its own may act as a smaller Trailing Take Profit of its own accord.

We’ve highlighted some key points from the last example to better emphasize how it works. As you can see, the White Circle is where profit was taken from the ML SuperTrend simply from it attempting to switch to a Bullish (Buy) Trend. However, that was rejected almost immediately and we went back to our Bearish (Sell) Trend that ended up resulting in our Take Profit being hit (Yellow Circle). This Strategy aims to not only capitalize on the small profits from SuperTrend to SuperTrend but to also capitalize when the Momentum is so strong that the price moves X% away from the SuperTrend and is able to hit the Take Profit location. This Take Profit addition to this Strategy is crucial as momentum may change state shortly after such drastic price movements; and if we were to simply wait for it to come back to the SuperTrend, we may lose out on lots of potential profit.

If you refer to the Yellow Circle in this example, you’ll notice what was talked about in the Summary/Overview above. During periods of consolidation when there is little momentum and price movement and we don’t have any Stop Loss activated, you may see ‘Signal Flashing’. Signal Flashing is when there are Buy and Sell signals that keep switching back and forth. During this time you may be taking small losses. This is a normal part of this Strategy. When a signal has finally been confirmed by Momentum, is when this Strategy shines and may produce the profit you desire.

You may be wondering, what causes these jagged like patterns in the SuperTrend? It's due to the ML logic, and it may be a little confusing, but essentially what is happening is the Fast Moving SuperTrend and the Slow Moving SuperTrend are creating KNN Min and Max distances that are extreme due to (usually) parabolic movement. This causes fewer values to be added to and averaged within the ML and causes less smooth and more exponential drastic movements. This is completely normal, and one of the perks of using k-Nearest Neighbor for ML calculations. If you don’t know, the Min and Max Distance allowed is derived from the most recent(0 index of data array) to KNN Length. So only SuperTrend values that exhibit distances within these Min/Max will be allowed into the average.

Since the KNN ML logic can cause these exponential movements in the SuperTrend, they likewise affect its Take Profit. The Take Profit may benefit from this movement like displayed in the example above which helped it claim profit before then exhibiting upwards movement.

By default our Stop Loss Multiplier is kept quite low at 0.0000025. Keeping it low may help to reduce some Signal Flashing while not taking extra losses more so than not using it at all. However, if we increase it even more to say 0.005 like is shown in the example above. It can really help the trend keep momentum. Please note, although previous results don’t imply future results, at 0.0000025 Stop Loss we are currently exhibiting 69.27% profit while at 0.005 Stop Loss we are exhibiting 33.54% profit. This just goes to show that although there may be less Signal Flashing, it may not result in more profit.

We will conclude our Tutorial here. Hopefully this has given you some insight as to how Machine Learning, combined with Trailing Take Profit and Stop Loss may have positive effects on the SuperTrend when turned into a Strategy.

Settings:

SuperTrend:

ATR Length: ATR Length used to create the Original Supertrend.

Factor: Multiplier used to create the Original Supertrend.

Stop Loss Multiplier: 0 = Don't use Stop Loss. Stop loss can be useful for helping to prevent false signals but also may result in more loss when hit and less profit when switching trends.

Take Profit Multiplier: Take Profits can be useful within the Supertrend Strategy to stop the price reverting all the way to the Stop Loss once it's been profitable.

Machine Learning:

Only Factor Same Trend Direction: Very useful for ensuring that data used in KNN is not manipulated by different SuperTrend Directional data. Please note, it doesn't affect KNN Exponential.

Rationalized Source Type: Should we Rationalize only a specific source, All or None?

Machine Learning Type: Are we using a Simple ML Average, KNN Mean Average, KNN Exponential Average or None?

Machine Learning Smoothing Type: How should we smooth our Fast and Slow ML Datas to be used in our KNN Distance calculation? SMA, EMA or VWMA?

KNN Distance Type: We need to check if distance is within the KNN Min/Max distance, which distance checks are we using.

Machine Learning Length: How far back is our Machine Learning going to keep data for.

k-Nearest Neighbour (KNN) Length: How many k-Nearest Neighbours will we account for?

Fast ML Data Length: What is our Fast ML Length?? This is used with our Slow Length to create our KNN Distance.

Slow ML Data Length: What is our Slow ML Length?? This is used with our Fast Length to create our KNN Distance.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Moving Average Compendium RefurbishedThis is my effort to bring together in a single script the widest range of moving averages possible.

I aggregated the calculation of averages within a library.

For more information about the library follow the link:

Basically this indicator is the visual result of this library.

You can choose the moving average and the script updates the chart as per the type.

The unique parameters of certain moving averages remain at their default values.

To have a rainbow of moving averages I also made an indicator:

Available moving averages:

AARMA = 'Adaptive Autonomous Recursive Moving Average'

ADEMA = '* Alpha-Decreasing Exponential Moving Average'

AHMA = 'Ahrens Moving Average'

ALMA = 'Arnaud Legoux Moving Average'

ALSMA = 'Adaptive Least Squares'

AUTOL = 'Auto-Line'

CMA = 'Corrective Moving average'

CORMA = 'Correlation Moving Average Price'

COVWEMA = 'Coefficient of Variation Weighted Exponential Moving Average'

COVWMA = 'Coefficient of Variation Weighted Moving Average'

DEMA = 'Double Exponential Moving Average'

DONCHIAN = 'Donchian Middle Channel'

EDMA = 'Exponentially Deviating Moving Average'

EDSMA = 'Ehlers Dynamic Smoothed Moving Average'

EFRAMA = '* Ehlrs Modified Fractal Adaptive Moving Average'

EHMA = 'Exponential Hull Moving Average'

EMA = 'Exponential Moving Average'

EPMA = 'End Point Moving Average'

ETMA = 'Exponential Triangular Moving Average'

EVWMA = 'Elastic Volume Weighted Moving Average'

FAMA = 'Following Adaptive Moving Average'

FIBOWMA = 'Fibonacci Weighted Moving Average'

FISHLSMA = 'Fisher Least Squares Moving Average'

FRAMA = 'Fractal Adaptive Moving Average'

GMA = 'Geometric Moving Average'

HKAMA = 'Hilbert based Kaufman\'s Adaptive Moving Average'

HMA = 'Hull Moving Average'

JURIK = 'Jurik Moving Average'

KAMA = 'Kaufman\'s Adaptive Moving Average'

LC_LSMA = '1LC-LSMA (1 line code lsma with 3 functions)'

LEOMA = 'Leo Moving Average'

LINWMA = 'Linear Weighted Moving Average'

LSMA = 'Least Squares Moving Average'

MAMA = 'MESA Adaptive Moving Average'

MCMA = 'McNicholl Moving Average'

MEDIAN = 'Median'

REGMA = 'Regularized Exponential Moving Average'

REMA = 'Range EMA'

REPMA = 'Repulsion Moving Average'

RMA = 'Relative Moving Average'

RSIMA = 'RSI Moving average'

RVWAP = '* Rolling VWAP'

SMA = 'Simple Moving Average'

SMMA = 'Smoothed Moving Average'

SRWMA = 'Square Root Weighted Moving Average'

SW_MA = 'Sine-Weighted Moving Average'

SWMA = '* Symmetrically Weighted Moving Average'

TEMA = 'Triple Exponential Moving Average'

THMA = 'Triple Hull Moving Average'

TREMA = 'Triangular Exponential Moving Average'

TRSMA = 'Triangular Simple Moving Average'

TT3 = 'Tillson T3'

VAMA = 'Volatility Adjusted Moving Average'

VIDYA = 'Variable Index Dynamic Average'

VWAP = '* VWAP'

VWMA = 'Volume-weighted Moving Average'

WMA = 'Weighted Moving Average'

WWMA = 'Welles Wilder Moving Average'

XEMA = 'Optimized Exponential Moving Average'

ZEMA = 'Zero-Lag Exponential Moving Average'

ZSMA = 'Zero-Lag Simple Moving Average'

Moving Averages RefurbishedIntroduction

This is a collection of multiple moving averages, where you can have a rainbow of moving averages with different types that can be defined by the user.

There are already other indicators in this rainbow style, however certain averages are absent in certain indicators and present in others,

needing the merge to have a more complete solution.

Resources

Here there is the possibility to individually define each moving average.

In addition, it is possible to adjust some details, such as themes, coloring and periods.

Regarding the calculation of averages, credit goes to the following authors.

What I've done here is to group these averages together and allow them to combine.

Credits

TradingView

PineCoders

CrackingCryptocurrency

MightyZinger

Alex Orekhov (everget)

alexgrover

paragjyoti2012

Moving averages available

1. Exponential Moving Average

2. Simple Moving Average

3. Relative Moving Average

4. Weighted Moving Average

5. Ehlers Dynamic Smoothed Moving Average

6. Double Exponential Moving Average

7. Triple Exponential Moving Average

8. Smoothed Moving Average

9. Hull Moving Average

10. Fractal Adaptive Moving Average

11. Kaufman's Adaptive Moving Average

12. Volatility Adjusted Moving Average

13. Jurik Moving Average

14. Optimized Exponential Moving Average

15. Exponential Hull Moving Average

16. Arnaud Legoux Moving Average

17. Coefficient of Variation Weighted Exponential Moving Average

18. Coefficient of Variation Weighted Moving Average

19. * Ehlrs Modified Fractal Adaptive Moving Average

20. Exponential Triangular Moving Average

21. Least Squares Moving Average

22. RSI Moving average

23. Simple Triangular Moving Average

24. Triple Hull Moving Average

25. Variable Index Dynamic Average

26. Volume-weighted Moving Average

27. Zero-Lag Exponential Moving Average

28. Zero-Lag Simple Moving Average

29. Elastic Volume Weighted Moving Average

30. Tillson T3

31. Geometric Moving Average

32. Welles Wilder Moving Average

33. Adjusted Moving Average

34. Corrective Moving average

35. Exponentially Deviating Moving Average

36. EMA Range

37. Sine-Weighted Moving Average

38. Adaptive Moving Average TABLE

39. Following Adaptive Moving Average

40. Hilbert based Kaufman's Adaptive Moving Average

41. Median

42. * VWAP

43. * Rolling VWAP

44. Triangular Simple Moving Average

45. Triangular Exponential Moving Average

46. Moving Average Price Correlation

47. Regularized Exponential Moving Average

48. Repulsion Moving Average

49. * Symmetrically Weighted Moving Average

* fixed period averages

MyLibraryLibrary "MyLibrary"

This library contains various trading strategies and utility functions for Pine Script.

simple_moving_average(src, length)

simple_moving_average

@description Calculates the Simple Moving Average (SMA) of a given series.

Parameters:

src (float) : (series float) The input series (e.g., close prices).

length (int) : (int) The number of periods to use for the SMA calculation.

Returns: (series float) The calculated SMA series.

exponential_moving_average(src, length)

exponential_moving_average

@description Calculates the Exponential Moving Average (EMA) of a given series.

Parameters:

src (float) : (series float) The input series (e.g., close prices).

length (simple int) : (int) The number of periods to use for the EMA calculation.

Returns: (series float) The calculated EMA series.

safe_division(numerator, denominator)

safe_division

@description Performs division with error handling for division by zero.

Parameters:

numerator (float) : (float) The numerator for the division.

denominator (float) : (float) The denominator for the division.

Returns: (float) The result of the division, or na if the denominator is zero.

strategy_moving_average_crossover(shortLength, longLength)

strategy_moving_average_crossover

@description Implements a Moving Average Crossover strategy.

Parameters:

shortLength (int) : (int) The length for the short period SMA.

longLength (int) : (int) The length for the long period SMA.

Returns: (series float, series float, series bool, series bool) The short SMA, long SMA, crossover signals, and crossunder signals.

strategy_rsi(rsiLength, overbought, oversold)

strategy_rsi

@description Implements an RSI-based trading strategy.

Parameters:

rsiLength (simple int) : (int) The length for the RSI calculation.

overbought (float) : (float) The overbought threshold.

oversold (float) : (float) The oversold threshold.

Returns: (series float, series bool, series bool) The RSI values, long signals, and short signals.

ichimoku_cloud(convPeriod, basePeriod, spanBPeriod, laggingSpanPeriod)

ichimoku_cloud

@description Computes Ichimoku Cloud components.

Parameters:

convPeriod (int) : (int) The conversion line period.

basePeriod (int) : (int) The base line period.

spanBPeriod (int)

laggingSpanPeriod (int)

Returns: (series float, series float, series float, series float, series float) The conversion line, base line, leading span A, leading span B, and lagging span.

strategy_ichimoku_conversion_baseline()

strategy_ichimoku_conversion_baseline

@description Implements an Ichimoku Conversion Line and Baseline strategy.

Returns: (series float, series float, series bool, series bool) The conversion line, baseline, crossover signals, and crossunder signals.

debug_print(labelText, value, barIndex)

debug_print

@description Prints values to the chart for debugging purposes.

Parameters:

labelText (string) : (string) The label text.

value (float) : (float) The value to display.

barIndex (int) : (int) The bar index where the label should be displayed.

BAERMThe Bitcoin Auto-correlation Exchange Rate Model: A Novel Two Step Approach

THIS IS NOT FINANCIAL ADVICE. THIS ARTICLE IS FOR EDUCATIONAL AND ENTERTAINMENT PURPOSES ONLY.

If you enjoy this software and information, please consider contributing to my lightning address

Prelude

It has been previously established that the Bitcoin daily USD exchange rate series is extremely auto-correlated

In this article, we will utilise this fact to build a model for Bitcoin/USD exchange rate. But not a model for predicting the exchange rate, but rather a model to understand the fundamental reasons for the Bitcoin to have this exchange rate to begin with.

This is a model of sound money, scarcity and subjective value.

Introduction

Bitcoin, a decentralised peer to peer digital value exchange network, has experienced significant exchange rate fluctuations since its inception in 2009. In this article, we explore a two-step model that reasonably accurately captures both the fundamental drivers of Bitcoin’s value and the cyclical patterns of bull and bear markets. This model, whilst it can produce forecasts, is meant more of a way of understanding past exchange rate changes and understanding the fundamental values driving the ever increasing exchange rate. The forecasts from the model are to be considered inconclusive and speculative only.

Data preparation

To develop the BAERM, we used historical Bitcoin data from Coin Metrics, a leading provider of Bitcoin market data. The dataset includes daily USD exchange rates, block counts, and other relevant information. We pre-processed the data by performing the following steps:

Fixing date formats and setting the dataset’s time index

Generating cumulative sums for blocks and halving periods

Calculating daily rewards and total supply

Computing the log-transformed price

Step 1: Building the Base Model

To build the base model, we analysed data from the first two epochs (time periods between Bitcoin mining reward halvings) and regressed the logarithm of Bitcoin’s exchange rate on the mining reward and epoch. This base model captures the fundamental relationship between Bitcoin’s exchange rate, mining reward, and halving epoch.

where Yt represents the exchange rate at day t, Epochk is the kth epoch (for that t), and epsilont is the error term. The coefficients beta0, beta1, and beta2 are estimated using ordinary least squares regression.

Base Model Regression

We use ordinary least squares regression to estimate the coefficients for the betas in figure 2. In order to reduce the possibility of over-fitting and ensure there is sufficient out of sample for testing accuracy, the base model is only trained on the first two epochs. You will notice in the code we calculate the beta2 variable prior and call it “phaseplus”.

The code below shows the regression for the base model coefficients:

\# Run the regression

mask = df\ < 2 # we only want to use Epoch's 0 and 1 to estimate the coefficients for the base model

reg\_X = df.loc\ [mask, \ \].shift(1).iloc\

reg\_y = df.loc\ .iloc\

reg\_X = sm.add\_constant(reg\_X)

ols = sm.OLS(reg\_y, reg\_X).fit()

coefs = ols.params.values

print(coefs)

The result of this regression gives us the coefficients for the betas of the base model:

\

or in more human readable form: 0.029, 0.996869586, -0.00043. NB that for the auto-correlation/momentum beta, we did NOT round the significant figures at all. Since the momentum is so important in this model, we must use all available significant figures.

Fundamental Insights from the Base Model

Momentum effect: The term 0.997 Y suggests that the exchange rate of Bitcoin on a given day (Yi) is heavily influenced by the exchange rate on the previous day. This indicates a momentum effect, where the price of Bitcoin tends to follow its recent trend.

Momentum effect is a phenomenon observed in various financial markets, including stocks and other commodities. It implies that an asset’s price is more likely to continue moving in its current direction, either upwards or downwards, over the short term.

The momentum effect can be driven by several factors:

Behavioural biases: Investors may exhibit herding behaviour or be subject to cognitive biases such as confirmation bias, which could lead them to buy or sell assets based on recent trends, reinforcing the momentum.

Positive feedback loops: As more investors notice a trend and act on it, the trend may gain even more traction, leading to a self-reinforcing positive feedback loop. This can cause prices to continue moving in the same direction, further amplifying the momentum effect.

Technical analysis: Many traders use technical analysis to make investment decisions, which often involves studying historical exchange rate trends and chart patterns to predict future exchange rate movements. When a large number of traders follow similar strategies, their collective actions can create and reinforce exchange rate momentum.

Impact of halving events: In the Bitcoin network, new bitcoins are created as a reward to miners for validating transactions and adding new blocks to the blockchain. This reward is called the block reward, and it is halved approximately every four years, or every 210,000 blocks. This event is known as a halving.

The primary purpose of halving events is to control the supply of new bitcoins entering the market, ultimately leading to a capped supply of 21 million bitcoins. As the block reward decreases, the rate at which new bitcoins are created slows down, and this can have significant implications for the price of Bitcoin.

The term -0.0004*(50/(2^epochk) — (epochk+1)²) accounts for the impact of the halving events on the Bitcoin exchange rate. The model seems to suggest that the exchange rate of Bitcoin is influenced by a function of the number of halving events that have occurred.

Exponential decay and the decreasing impact of the halvings: The first part of this term, 50/(2^epochk), indicates that the impact of each subsequent halving event decays exponentially, implying that the influence of halving events on the Bitcoin exchange rate diminishes over time. This might be due to the decreasing marginal effect of each halving event on the overall Bitcoin supply as the block reward gets smaller and smaller.

This is antithetical to the wrong and popular stock to flow model, which suggests the opposite. Given the accuracy of the BAERM, this is yet another reason to question the S2F model, from a fundamental perspective.

The second part of the term, (epochk+1)², introduces a non-linear relationship between the halving events and the exchange rate. This non-linear aspect could reflect that the impact of halving events is not constant over time and may be influenced by various factors such as market dynamics, speculation, and changing market conditions.

The combination of these two terms is expressed by the graph of the model line (see figure 3), where it can be seen the step from each halving is decaying, and the step up from each halving event is given by a parabolic curve.

NB - The base model has been trained on the first two halving epochs and then seeded (i.e. the first lag point) with the oldest data available.

Constant term: The constant term 0.03 in the equation represents an inherent baseline level of growth in the Bitcoin exchange rate.

In any linear or linear-like model, the constant term, also known as the intercept or bias, represents the value of the dependent variable (in this case, the log-scaled Bitcoin USD exchange rate) when all the independent variables are set to zero.

The constant term indicates that even without considering the effects of the previous day’s exchange rate or halving events, there is a baseline growth in the exchange rate of Bitcoin. This baseline growth could be due to factors such as the network’s overall growth or increasing adoption, or changes in the market structure (more exchanges, changes to the regulatory environment, improved liquidity, more fiat on-ramps etc).

Base Model Regression Diagnostics

Below is a summary of the model generated by the OLS function

OLS Regression Results

\==============================================================================

Dep. Variable: logprice R-squared: 0.999

Model: OLS Adj. R-squared: 0.999

Method: Least Squares F-statistic: 2.041e+06

Date: Fri, 28 Apr 2023 Prob (F-statistic): 0.00

Time: 11:06:58 Log-Likelihood: 3001.6

No. Observations: 2182 AIC: -5997.

Df Residuals: 2179 BIC: -5980.

Df Model: 2

Covariance Type: nonrobust

\==============================================================================

coef std err t P>|t| \

\------------------------------------------------------------------------------

const 0.0292 0.009 3.081 0.002 0.011 0.048

logprice 0.9969 0.001 1012.724 0.000 0.995 0.999

phaseplus -0.0004 0.000 -2.239 0.025 -0.001 -5.3e-05

\==============================================================================

Omnibus: 674.771 Durbin-Watson: 1.901

Prob(Omnibus): 0.000 Jarque-Bera (JB): 24937.353

Skew: -0.765 Prob(JB): 0.00

Kurtosis: 19.491 Cond. No. 255.

\==============================================================================

Below we see some regression diagnostics along with the regression itself.

Diagnostics: We can see that the residuals are looking a little skewed and there is some heteroskedasticity within the residuals. The coefficient of determination, or r2 is very high, but that is to be expected given the momentum term. A better r2 is manually calculated by the sum square of the difference of the model to the untrained data. This can be achieved by the following code:

\# Calculate the out-of-sample R-squared

oos\_mask = df\ >= 2

oos\_actual = df.loc\

oos\_predicted = df.loc\

residuals\_oos = oos\_actual - oos\_predicted

SSR = np.sum(residuals\_oos \*\* 2)

SST = np.sum((oos\_actual - oos\_actual.mean()) \*\* 2)

R2\_oos = 1 - SSR/SST

print("Out-of-sample R-squared:", R2\_oos)

The result is: 0.84, which indicates a very close fit to the out of sample data for the base model, which goes some way to proving our fundamental assumption around subjective value and sound money to be accurate.

Step 2: Adding the Damping Function