VIX-VXV-Ratio-Buschi

English:

This script shows the ratio between the VIX (implied volatility of SPX options over the next month) and the VXV (implied volatility of SPX options over the next three months). Since in normal "Contango" mode, the VXV should be higher than the VIX, the crossing under 1.0 or maybe 0.95 after a volatility spike could be a sign for a calming market or at least a calming volatility.

Deutsch:

Dieses Skript zeigt das Verhältnis zwischen dem VIX (implizite Volatilität der SPX-Optionen über den nächsten Monat) und dem VXV (implizite Volatilität der SPX-Optionen über die nächsten drei Monate). Da im normalen "Contango"-Modus der VXV höher als der VIX liegen sollte, kann das Abfallen unter 1,0 oder 0,95 nach einer Volatilitätsspitze ein Anzeichen für einen ruhiger werdenden Markt oder zumindest eine ruhiger werdende Volatilität sein.

Cerca negli script per "Implied volatility"

OHLC Volatility Estimators by @Xel_arjonaDISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is by Creative-Commons as TradingView's regulations. Any use, copy or re-use of this code should mention it's origin as it's authorship.

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED AS DEBUGING CODE The models included in the function have been taken from openly sources on the web so they could have some errors as in the calculation scheme and/or in it's programatic scheme. Debugging are welcome.

WHAT'S THIS?

Here's a full collection of candle based (compressed tick) Volatility Estimators given as a function, openly available for free, it can print IMPLIED VOLATILITY by an external symbol ticker like INDEX:VIX.

Models included in the volatility calculation function:

CLOSE TO CLOSE: This is the classic estimator by rule, sometimes referred as HISTORICAL VOLATILITY and is the must common, accepted and widely used out there. Is based on traditional Standard Deviation method derived from the logarithm return of current close from yesterday's.

ELASTIC WEIGHTED MOVING AVERAGE: This estimator has been used by RiskMetriks®. It's calculation is based on an ElasticWeightedMovingAverage Standard Deviation method derived from the logarithm return of current close from yesterday's. It can be viewed or named as an EXPONENTIAL HISTORICAL VOLATILITY model.

PARKINSON'S: The Parkinson number, or High Low Range Volatility, developed by the physicist, Michael Parkinson, in 1980 aims to estimate the Volatility of returns for a random walk using the high and low in any particular period. IVolatility.com calculates daily Parkinson values. Prices are observed on a fixed time interval. n=10, 20, 30, 60, 90, 120, 150, 180 days.

ROGERS-SATCHELL: The Rogers-Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a Geometric Brownian Motion (GBM) with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, this Rogers-Satchell estimator does not account for jumps in price (Gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

YANG-ZHANG: Yang and Zhang were the first to derive an historical volatility estimator that has a minimum estimation error, is independent of the drift, and independent of opening gaps. This estimator is maximally 14 times more efficient than the close-to-close estimator.

LOGARITHMIC GARMAN-KLASS: The former is a pinescript transcript of the model defined as in iVolatility . The metric used is a combination of the overnight, high/low and open/close range. Such a volatility metric is a more efficient measure of the degree of volatility during a given day. This metric is always positive.

Option Range Projector PRO (with Alerts)Indicator Name: Option Range Projector PRO (with Alerts)

Short Description

This is a powerful and flexible tool for traders that visualizes expected price movement ranges based on option pricing principles and statistical deviations. The indicator plots standard deviation levels (Sigmas) and boundaries calculated from the price of an options Straddle, providing a unique insight into market volatility expectations.

It is ideal for options traders, as well as those who trade futures or spot assets and want to gain an edge by understanding where the market anticipates price boundaries on a specific date.

Core Concepts

The indicator is based on three key ideas:

Standard Deviation (Sigma, σ): In statistics, this is a measure of value dispersion. In trading, when applied to prices, standard deviation levels show the probable range within which the price is expected to remain until a specific date (expiration).

±1σ (1 Sigma): Approximately 68.2% probability that the price will stay within this range.

±2σ (2 Sigmas): Approximately 95.4% probability. These levels often act as strong support/resistance.

±3σ (3 Sigmas): Approximately 99.7% probability. Reaching these levels is a statistically rare event.

Implied Volatility (IV): This is a key component. IV is the market's forecast of the asset's future volatility. It is derived from current option prices and reflects how significant the price movements are expected to be by traders. The higher the IV, the wider the calculated ranges will be.

Straddle-Based Levels: A straddle is an options strategy involving the simultaneous purchase of a Call and a Put option with the same strike price and expiration date. The cost of this combination (Call + Put) directly reflects the market's expected price movement in points. Our indicator uses this value to construct alternative, highly accurate boundaries of the expected range.

Key Features

Flexible Expiration Choice: Easily switch between standard contracts (Weekly, Monthly, Quarterly) or set any custom number of days to expiration (DTE).

Dual Volatility Calculation Mode: Use automatic calculation based on historical data or enter a precise IV value manually (e.g., from your broker's terminal) for maximum accuracy.

Two Types of Predictive Levels: Visualize classic standard deviations (Sigmas) and/or levels calculated from the Straddle price for a comprehensive analysis.

Expiration Comparison: Enable the display of additional levels for a different expiration date to visually compare short-term and long-term market expectations.

"Greeks" Calculation: The indicator calculates and displays key option Greeks (Delta, Gamma, Theta, Vega), helping to deepen the understanding of an option position's characteristics.

Informative Table: All key data—ATM price, IV, DTE, level prices, Greeks, and option prices—are consolidated into one clear table for quick analysis.

Customizable Alerts: Get instant notifications directly in TradingView when the price crosses any of the important levels (±1σ, ±2σ, ±3σ).

Full Visual Customization: Control colors, line thickness, labels, and zone fills to adapt the indicator to your trading style.

How to Use (Settings)

Price Settings:

Auto-detect ATM Price: When enabled, the indicator will use the current closing price as the At-The-Money (ATM) price.

Manual ATM Price: If auto mode is disabled, you can set a precise ATM price manually.

Volatility Settings:

Auto-calculate IV: Calculates historical volatility over a specified period. Useful if you don't have access to real-time IV.

Manual IV Value: (Recommended for accuracy). Enter the Implied Volatility (IV) value for the desired strike from your brokerage terminal or analytical services here.

Expiration:

Contract Type: Choose one of the standard terms (Weekly, Monthly, Quarterly) or "Custom" to use a manual day input.

Days to Expiration: Active only for the "Custom" type.

Show Multiple Expirations: Enables a second set of levels with a different term for comparison.

Straddle Boundaries:

Use Manual Input: Allows you to enter the precise Call and Put Settle prices from the official exchange summary (e.g., from the CME website). This provides the most accurate boundaries based on real market prices.

Trading Ideas and Application

Mean Reversion Trading: The ±2σ and ±3σ levels often act as strong overbought/oversold zones. A price reaching these extreme values has a high statistical probability of reversing or correcting back towards the central ATM price.

Trend Confirmation and Breakouts: A confident close outside the ±1σ range can indicate the beginning of a strong directional move.

Risk Management: Use the levels to set stop-losses or determine profit targets. For example, when opening a trade near the +1σ level, you might consider a target at +2σ and place a stop-loss behind the ATM level.

Volatility Analysis: By comparing the width of the ranges for different expirations, you can assess how the market is pricing short-term versus long-term risks. A narrow range suggests low expectations, while a wide range indicates high ones.

Disclaimer: This indicator is an analysis tool and does not provide direct financial advice or trading signals. All trading decisions are your own. Use this indicator in conjunction with other analysis methods.

ATR 3x Multiplier StrategyBeta version

Volatility and Candle Spikes in Trading

Volatility

Volatility refers to the degree of variation in the price of a financial asset over time. It measures how much the price fluctuates and is often associated with risk and uncertainty in the market. High volatility means larger price swings, while low volatility indicates more stable price movements.

Key aspects of volatility:

Measured using indicators like Average True Range (ATR), Bollinger Bands, and Implied Volatility (IV).

Influenced by factors such as market news, economic events, and liquidity.

Higher volatility increases both risk and potential profit opportunities.

Candle Spikes

A candle spike (or wick) refers to a sudden price movement that forms a long shadow or wick on a candlestick chart. These spikes can indicate strong buying or selling pressure, liquidity hunts, or stop-loss triggers.

Types of candle spikes:

Bullish Spike (Long Lower Wick): Indicates buyers rejected lower prices, pushing the price higher.

Bearish Spike (Long Upper Wick): Suggests sellers rejected higher prices, pushing the price lower.

Stop-Loss Hunt: Market makers may trigger stop-losses by creating artificial spikes before reversing the price.

News-Induced Spikes: Economic data releases or unexpected events can cause sudden price jumps.

Understanding volatility and candle spikes can help traders manage risk, spot entry/exit points, and avoid false breakouts. 🚀📈

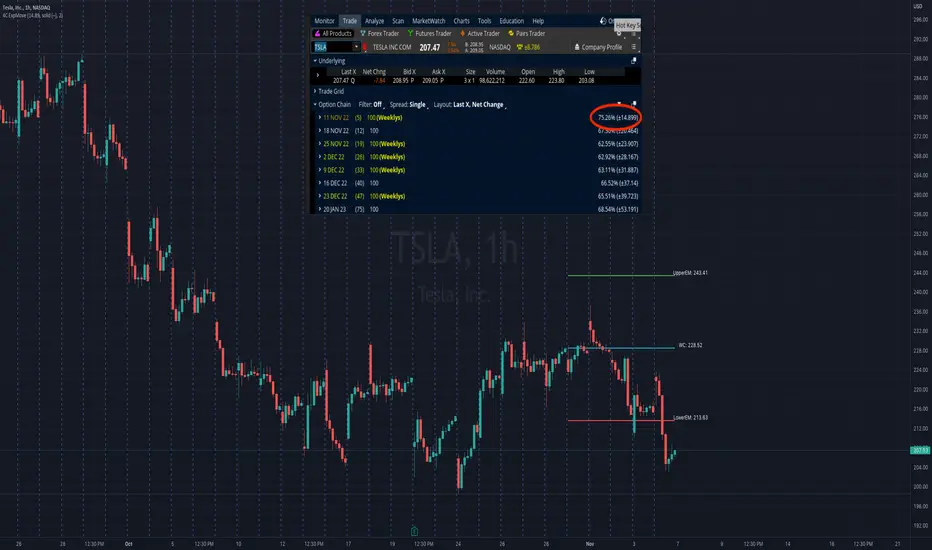

4C Options Expected Move (Weekly + 0DTE)This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) Daily options, for a quick visual reference.

Please Note: This indicator is different from our original "4C Expected Move (Weekly Options)" indicator, as it now packages the ability to ALSO plot 0DTE options expected moves along with Weekly expected moves. Many other newer features have also been implemented.

Background Information

The Expected Move (EM) is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of options pricing and implied volatility.

This range can be viewed as possible support and resistance, or, once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

About the Indicator

This indicator plots the calculated Expected Move for BOTH Weekly and Zero Dated Expiration (0DTE) options, for a quick visual reference.

For the weekly EM, the range is based on the Weekly close of the prior week.

For the Daily EM based on 0DTE options, the range is based on the Daily close of the prior day.

The indicator will automatically start a new weekly EM plot at the beginning of the week, and a new daily EM at the beginning of each day.

The EM values must be updated weekly and/or daily.

Features

Plots the EM for the week

Plots the EM for the day, for symbols that offer daily expiration options

Plots the 2 Standard Deviation EM for both the weekly and daily EM

Labels with calculated values are plotted near the levels for quick visual aid

Settings

Can toggle weekly EM on/off

Can toggle Daily EM on/off

Can toggle 2 Standard Deviation lines on/off

Can toggle labels for all EM on/off

Robust line settings

Can adjust label location left/right based on personal preference

Can enter symbol into settings as a reference

Handy instructions in the settings

How To Set Up The Indicator

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Usually, you can look at the stock's option chain to find the weekly expected move.

You will have to do your own research to find where this information is displayed depending on your broker. You may also need to find the information elsewhere if your broker does not have this information.

You can also do your calculation of the EM using the following formula (please do your own research):

Expected Move = Option Price x Implied Volatility x Square Root of Time

See screenshot example below

This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM are on the right side of the option chain.

The Expected Move is circled in blue. Use the +- number in parentheses, NOT the % value.

For the weekly EM, input the number that corresponds to the weekly option into the indicator. This must be done on a weekly basis, and It is typically best to use the EM for the next week expiration that is generated AFTER the Friday close and/or before the Monday open of the upcoming week.

For the daily EM, input the number that corresponds to the daily 0DTE option into the indicator. This must be done on a daily basis, and it is typically best to use the EM value for the 0DTE option that is generated the night before (after market close), or before the market opens for that 0DTE. .

vol_premiaThis script shows the volatility risk premium for several instruments. The premium is simply "IV30 - RV20". Although Tradingview doesn't provide options prices, CBOE publishes 30-day implied volatilities for many instruments (most of which are VIX variations). CBOE calculates these in a standard way, weighting at- and out-of-the-money IVs for options that expire in 30 days, on average. For realized volatility, I used the standard deviation of log returns. Since there are twenty trading periods in 30 calendar days, IV30 can be compared to RV20. The "premium" is the difference, which reflects market participants' expectation for how much upcoming volatility will over- or under-shoot recent volatility.

The script loads pretty slow since there are lots of symbols, so feel free to delete the ones you don't care about. Hopefully the code is straightforward enough. I won't list the meaning of every symbols here, since I might change them later, but you can type them into tradingview for data, and read about their volatility index on CBOE's website. Some of the more well-known ones are:

ES: S&P futures, which I prefer to the SPX index). Its implied volatility is VIX.

USO: the oil ETF representing WTI future prices. Its IV is OVX.

GDX: the gold miner's ETF, which is usually more volatile than gold. Its IV is VXGDX.

FXI: a china ETF, whose volatility is VXFXI.

And so on. In addition to the premium, the "percentile" column shows where this premium ranks among the previous 252 trading days. 100 = the highest premium, 0 = the lowest premium.

Tempo V | QuantEdgeB📊 Tempo V | QuantEdgeB

🔍 What is Tempo V?

Tempo V by QuantEdgeB is a volatility resonance framework that fuses multiple volatility models into a single adaptive signal. It acts like a seismograph for market energy, detecting shifts in pressure, flow, and agitation before they erupt into full-blown volatility waves.

Rather than just measure price range, Tempo V decodes the texture of volatility — layering Z-Score logic over 7 elite volatility and energy signals to create a unified tempo pulse.

💡 Think of Tempo V as your market EQ meter, identifying when price is humming calmly or vibrating toward breakout chaos.

⚙️ Core Components

✅ Multi-Model Volatility Stack

Tempo V blends the most statistically robust volatility estimators:

• IMI – Measures price "thrust" or intraday initiation.

• RVI – Detects directional volatility flow.

• ATR – True range of price breathing.

• Rogers-Satchell – Captures variance with directional drift.

• Parkinson – Focuses on high–low spread efficiency.

• Yang-Zhang – A hybrid volatility estimator ideal for crypto assets.

• Garman-Klass – Captures OHLC variance with tight math.

Each signal is z-scored, scaled, and dynamically smoothed into a composite value — the aggZ.

✅ Z-Blend Aggregation

• aggZ = The heartbeat of Tempo V — a weighted blend of all enabled signals.

• It’s like a volatility weather report: positive means upside risk building, negative means downside storm clouds.

✅ Adaptive EMA Trendline

• Tempo V includes a dynamically responsive trendline that changes pace depending on market tempo.

• This tracks the momentum of volatility, not price — a major edge in fast-moving environments.

🎯 Signal & Stage Interpretation

🧭 Z-Score Based Stage Labels

At every candle, Tempo V identifies the current volatility stage:

1.Value ≥ +1.25 ==> 🔺 High Upside Volatility

2.Value +0.5 to +1.25 ==> ⚡ Volatile-Up Phase

3.Value -0.5 to +0.5 ==> ⏸️ Stable Range / Balance

4.Value -1.25 to -0.5 ==> ⚠️ Volatile-Down Phase

5.Value ≤ -1.25 ==> 🔻 High Downside Volatility

These insights allow you to act preemptively on upcoming breakouts, fades, or quiet zones.

🖼️ Visual Overlay Engine

• Column Chart – aggZ plotted as a histogram, easily trackable.

• Trend Line – Responsive smoothing that visualizes volatility shift.

• Background Color Zones – Highlighting extreme tempo levels.

• Bar Coloring (Optional) – Syncs chart bars with volatility phase.

🧠 Why Use Tempo V?

Tempo V is designed for traders who want to:

• Detect volatility pressure before price erupts

• Combine multiple models into one actionable score

• Visualize tempo stages without overwhelming charts

• Spot shifts in energy, flow, and agitation — not just direction

💼 Ideal Use Cases

• Breakout Traders: Anticipate volatility surges

• Mean-Reversion Setups: Fade extremes after tempo climax

• Options Traders: Identify implied volatility zones visually

• Trend Traders: Use rising aggZ as confirmation of commitment

🧬 Default Settings

• Z-Score Length: 45

• Smooth Length: 5

• Active Models: All 7 enabled by default

• Upper/Lower Bounds: ±1.25

🧬 In Summary

Tempo V | QuantEdgeB is not just a volatility measure — it’s a volatility intelligence framework, distilling 7 elite metrics into one real-time pulse of market agitation.

It’s smart, fast, and narrates market rhythm so you can trade with anticipation instead of reaction.

📌 Navigate the Pulse of Volatility | Powered by QuantEdgeB

🔹 Disclaimer: Past performance is not indicative of future results.

🔹 Strategic Advice: Always tune the z-lengths and smoothing to fit your asset and timeframe volatility. Backtest thoroughly.

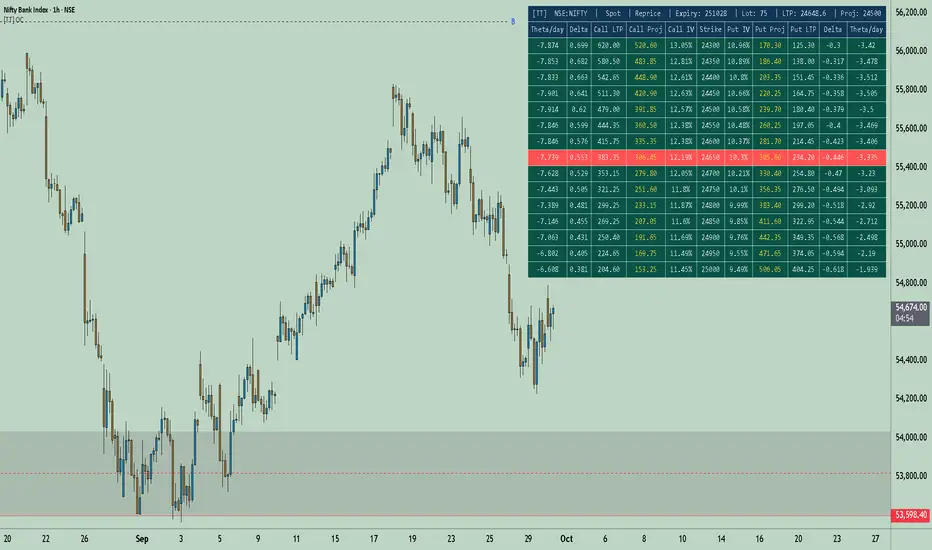

[TT] Option Chain✅Option Geeks for NSE India

Option Geeks is a powerful tool designed for options traders on the NSE (National Stock Exchange of India). It provides real-time visualization and insights based on key option greeks such as Delta, Gamma, Theta, and Implied Volatility (IV) — enabling traders to make more informed decisions when analyzing option chains and positions.

✅What This Script Does:

Calculates and displays the main option greeks for both Call and Put options.

Highlights sensitivity of option prices to changes in:

Underlying price (Delta, Gamma)

Time decay (Theta)

Implied Volatility Calculation.

Tracks live changes in IV and allows comparison across strikes and expiries.

Helps identify favorable option setups and hedging opportunities.

Designed for Bank Nifty, Nifty 50, and top NSE FnO stocks.

✅ How It Works (Conceptually):

Uses a simplified Black-Scholes model adapted for Indian markets.

Takes into account underlying price, strike, days to expiry, interest rate, and volatility to compute the Greeks. Plots real-time values on chart

Manually You need to input the ATM Strike and nearest expiry to update Greeks accordingly.

✅ Who Should Use It:

Options traders seeking deeper insight beyond price charts.

Scalpers and positional traders looking to understand how their trades react to time, price, and volatility.

Anyone trading on NSE’s F&O segment who wants to make smarter trades based on calculated risk metrics

SPX Expected MoveThis indicator plots the "expected move" of SPX for today's trading session. Expected move is the amount that SPX is predicted to increase or decrease from its current price, based on the current level of implied volatility. The implied volatility in this indicator is computed from the current value of the VIX (or one of several volatility symbols available on Trading view). The computation is done using standard formula. The resulting plots are labeled as 1 and 2 standard deviations. The default values are to use VIX as well as 252 trading days in the years.

Use the square root of (days to expiration, or in this case a fraction of the day remaining) divided but the square root of (252, or number of trading days in a year).

timeRemaining = math.sqrt(DTE) / math.sqrt(252)

Standard deviation move = SPX bar closing price * (VIX/100) * timeRemaining

[blackcat] L1 Visual Volatility IndicatorHey there! Let's get into the details about dynamic rate indicators, how they work, their importance, usage, and benefits in trading.

Dynamic rate indicators are essential in trading as they help traders assess the volatility and risk level of the market, so they can make the right trading strategies and risk management measures.

When it comes to the importance of dynamic rate indicators, they provide critical information about market volatility, which is super important for traders. Traders can use this information to understand the risk level of the market, determine market stability and instability, and adjust trading strategies based on volatility changes.

Now let's talk about the usage of dynamic rate indicators. They have different usage times for different trading strategies and market environments. Generally, when market volatility is low, traders can take advantage of the opportunity to do trend tracking or oscillating trades. When market volatility is high, traders can take a more conservative approach, such as using stop-loss orders or reducing position sizes.

Using dynamic rate indicators can bring several benefits. First, they can help traders evaluate the risk level of the market, so they can develop suitable risk management strategies. Traders can adjust stop-loss and take-profit levels based on changes in volatility to control risk. Second, dynamic rate indicators provide information about market trends and price fluctuations, helping traders make wiser trading decisions. Traders can determine entry and exit points based on the signals of dynamic rate indicators. Lastly, dynamic rate indicators play a significant role in option pricing. Implied volatility helps traders evaluate option prices and market expectations for future volatility, so they can carry out option trades or hedging operations.

In conclusion, dynamic rate indicators are essential for traders as they help assess market volatility and risk levels, develop suitable trading strategies and risk management measures, and increase trading success and profitability. Remember that different indicators are suitable for different types of markets, so it is essential to choose the right one for your specific trading needs.

This indicator is a powerful tool for traders who want to stay ahead of the market and make informed trading decisions. By analyzing trends in volatility, this indicator can provide valuable insights into market sentiment and help traders identify potential trading opportunities.

One of the key advantages of the L1 Visual Volatility Indicator is its ability to adapt to changing market conditions. The channel structure it constructs based on ATR characteristics provides a framework for tracking volatility that can be adjusted to different timeframes and asset classes. This allows traders to customize the indicator to their specific needs and trading style, making it a versatile tool for a wide range of trading strategies.

Another advantage of this indicator is its use of gradient colors to differentiate between Bullish and Bearish volatility. This provides a visual representation of market sentiment that can help traders quickly identify potential trading opportunities and make informed decisions. Additionally, the use of Fibonacci's long-term moving average to define the sideways consolidation area provides a reliable framework for identifying key levels of support and resistance, further enhancing the indicator's usefulness in trading.

In conclusion, the L1 Visual Volatility Indicator is a powerful tool for traders looking to stay ahead of the market and make informed trading decisions. Its ability to adapt to changing market conditions and use of gradient colors to differentiate between Bullish and Bearish volatility make it a versatile and effective tool for a wide range of trading strategies. By incorporating this indicator into their trading arsenal, traders can gain valuable insights into market sentiment and improve their chances of success in the markets.

Realized Volatility (StdDev of Returns, %)📌 Realized Volatility (StdDev of Returns, %)

This indicator measures realized volatility directly from price returns, instead of the common but misleading approach of calculating standard deviation around a moving average.

🔹 How it works:

Computes close-to-close log returns (the most common way volatility is measured in finance).

Calculates the standard deviation of these returns over a chosen lookback period (default = 200 bars).

Converts results into percentages for easier interpretation.

Provides three key volatility measures:

Daily Realized Vol (%) – raw standard deviation of returns.

Annualized Vol (%) – scaled by √250 trading days (market convention).

Horizon Vol (%) – volatility over a custom horizon (default = 5 days, i.e. weekly).

🔹 Why use this indicator?

Shows true realized volatility from historical returns.

More accurate than measuring deviation around a moving average.

Useful for traders analyzing risk, position sizing, and comparing realized vs implied volatility.

⚠️ Note:

It is best used on the Daily Chart!

By default, this uses log returns (which are additive and standard in quant finance).

If you prefer, you can easily switch to simple % returns in the code.

Volatility estimates depend on your chosen lookback length and may vary across timeframes.

4C Expected Move (Weekly Options)This indicator plots the Expected Move (EM) calculated from weekly options pricing, for a quick visual reference.

The EM is the amount that a stock is predicted to increase or decrease from its current price, based on the current level of implied volatility.

This range can be viewed as support and resistance, or once price gets outside of the range, institutional hedging actions can accelerate the move in that direction.

The EM range is based on the Weekly close of the prior week.

It can be useful to know what the weekly EM range is for a stock to understand the probabilities of the overall distance, direction and volatility for the week.

To use this indicator you must have access to a broker with options data (not available on Tradingview).

Look at the stock's option chain and find the weekly expected move. You will have to do your own research to find where this information is displayed depending on your broker.

See screenshot example on the chart. This is the Thinkorswim platform's option chain, and the Implied Volatility % and the calculated EM is circled in red. Use the +- number in parentheses, NOT the % value.

Input that number into the indicator on a weekly basis, ideally on the weekend sometime after the cash market close on Friday, and before the Market open at the beginning of the trading week.

The indicator must be manually updated each week.

It will automatically start over at the beginning of the week.

Compare Crypto Bollinger Bands//This is not financial advice, I am not a financial advisor.

//What are volatility tokens?

//Volatility tokens are ERC-20 tokens that aim to track the implied volatility of crypto markets.

//Volatility tokens get their exposure to an asset’s implied volatility using FTX MOVE contracts.

//There are currently two volatility tokens: BVOL and IBVOL.

//BVOL targets tracking the daily returns of being 1x long the implied volatility of BTC

//IBVOL targets tracking the daily returns of being 1x short the implied volatility of BTC.

/////////////////////////////////////////////////////////////////

CAN USE ON ANY CRYPTO CHART AS BINANCE:BTCUSD is still the most dominant crypto, positive volatility for BTC is positive for all.

/////////////////////////////////////////////////////////////////

//The Code.

//The blue line (ChartLine) is the current chart plotted on in Bollinger

//The red line (BVOLLine) plots the implied volatility of BTC

//The green line (IBVOLLine) plot the inverse implied volatility of BTC

//The orange line (TOTALLine) plots how well the crypto market is performing on the Bolling scale. The higher the number the better.

//There are 2 horizontal lines, 0.40 at the bottom & 0.60 at the top

/////////To Buy

//1. The blue line (ChartLine) must be higher than the green line (IBVOLLine)

//2. The green line (IBVOLLine) must be higher than the red line (BVOLLine)

//3. The red line (BVOLLine) must be less than 0.40 // This also acts as a trendsetter

//4. The orange line (TOTALLine) MUST be greater than the red line. This means that the crypto market is positive.

//5.IF THE BLUE LINE (ChartLine) IS GREATER THAN THE ORANGE LINE (TOTALLine) IT MEANS YOUR CRYPTO IS OUTPERFOMING THE MARKET {good for short term explosive bars}

//6. If the orange line (TOTALLine) is higher than your current chart, say BTCUSD. And BTC is going up to. It just means BTC is going up slowly. it's fine as long as they are moving in the same position.

//5. I use this on the 4hr, 1D, 1W timeframes

///////To Exit

//1.If the blue line (ChartLine) crosses under the green line (IBVOLLine) exit{ works best on 4hr,1D, 1W to avoid fakes}

//2.If the red line crosses over the green line when long. {close positions, or watch positions} It means negative volatility is wining

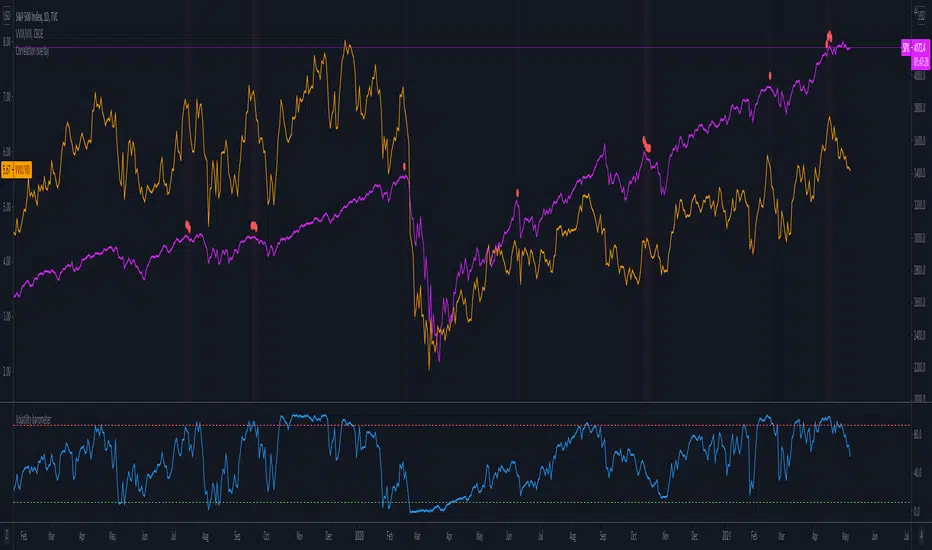

Volatility barometerIt is the indicator that analyzes the behaviour of VIX against CBOE volaility indices (VIX3M, VIX6M and VIX1Y) and VIX futures (next contract to the front one - VX!2). Because VIX is a derivate of SPX, the indicator shall be used on the SPX chart (or equivalent like SPY).

When the readings get above 90 / below 10, it means the market is overbought / oversold in terms of implied volatility. However, it does not mean it will reverse - if the price go higher along with the indicator readings then everything is fine. There is an alarming situation when the SPX is diverging - e.g. the price go higher, the readings lower. It means the SPX does not play in the same team as IVOL anymore and might reverse.

You can use it in conjunction with other implied volatility indicators for stronger signals: the Correlation overlay ( - the indicator that measures the correlation between VVIX and VIX) and VVIX/VIX ratio (it generates a signal the ratio makes 50wk high).

Volatility SkewThis indicator measure the historical skew of actual volatility for an individual security. It measure the volatility of up moves versus down moves over the period and gives a ratio. When the indicator is greater than one, it indicators that volatility is greater to the upside, when it is below 1 it indicates that volatility is skewed to the downside.

This is not comparable to the SKEW index, since that measures the implied volatility across option strikes, rather than using historical volatility.

(JS)S&P 500 Volatility Oscillator For Options 2.0I am going to start taking requests to open source my indicators and they will also be updated to Version 4 of Pinescript.

I added some features to the original code such the ability to smooth the oscillator and select the look back periods for the historical volatility.

Link to original:

Original post:

"The idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX ). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX ) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility . (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M ) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX , SPY , even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Feb 17, 2019

Release Notes: Cosmetic update for a much cleaner look:

-Replaced the "HIGH IV" with a simlple "H"

-Now the white line is constantly showing you the relationship between VIX and VIX3M - when VIX is greater than VIX3M the background still goes red

-However, now when VIX drops below Historical Volatility, the background is bright green

-When both above are true - it's dark green

-The Average True Range on the bottom is now a series of crosses"

Options Greeks AnalyzerOptions Greeks Analyzer (Training & Learning Guide)

________________________________________

1. Introduction

Options trading is advanced compared to regular stock trading, and one of the most important aspects is Options Greeks. Greeks are mathematical values that measure how the price of an option will react to changes in various factors such as the underlying asset’s price, volatility, interest rates, and time to expiry.

This Options Greeks Analyzer tool is built using TradingView Pine Script v5. It serves as a real time training and analysis dashboard that helps learners visualize how options greeks behave, how option prices change, and how traders can make informed decisions.

📌 Educational Disclaimer:

This tool is only for training and learning purposes. It is not a financial advice tool nor to be used for live trading decisions. The data shown is theoretical Black Scholes model calculations, which may differ from actual option market prices.

________________________________________

2. How the Tool Works

The Options Greeks Analyzer is divided into different modules. Below is a step by step walkthrough:

________________________________________

Step 1: User Inputs

• Implied Volatility (IV%) — You can manually enter volatility, which is the most important factor in option pricing. Higher IV = higher option premium.

• Expiry Selection — Choose from preset durations like 7D, 14D, 30D etc. Days to expiry directly affect time decay (Theta).

• Strike Price Mode — You can select either:

o ATM (At-the-Money = Current price of stock/index)

o Custom strike (Enter your own strike price)

• Risk-Free Rate (%) — A small interest rate factor (like government bond yield) used for theoretical valuation.

• Table Customization — Choose table size, position, and whether to show price lines for easy visibility.

________________________________________

Step 2: Market Data & Volatility

• The tool takes the current market price (Spot Price) as input.

• It calculates realized volatility from historical price fluctuations (using past 30 bars/log returns).

• Implied Volatility (manual input) is then compared to realized vol:

o If IV > Historical Volatility → Market pricing is “expensive” (HIGH IV RANK).

o If IV < Historical Volatility → Market is “cheap” (LOW IV RANK).

o Otherwise, it’s MEDIUM.

📌 Why it matters?

Traders can decide whether buying or selling options is favorable. Beginners learn that timing entry with volatility is more critical than just looking at market direction.

________________________________________

Step 3: Black-Scholes Formula

The core engine uses the Black-Scholes model, a mathematical formula widely used to compute option fair prices.

It uses the following inputs:

• Current price (Spot)

• Strike Price

• Time to Expiry (T)

• Risk Free Rate (r)

• Implied Volatility (σ)

This produces:

• Call Option Price

• Put Option Price

📌 This teaches learners how premiums are derived theoretically and why the same strike can have different values depending on IV and time.

________________________________________

Step 4: Option Greeks Calculation

The tool computes the first order Greeks:

• Delta → Measures how much the option price changes when the underlying stock moves by 1 point.

(Call Delta ranges 0–1, Put Delta ranges -1 to 0).

• Gamma → Sensitivity of Delta to price change. A measure of volatility risk.

• Theta → Time decay. Shows how much value option loses as each day passes. Calls and Puts have negative Theta (decay).

• Vega → Measures how sensitive option price is to volatility changes.

• Rho → Interest rate sensitivity. Mostly minor in equity options but important for training.

📌 New traders learn how each factor impacts profits/losses. Instead of random guessing, they see mathematical impact in numbers.

________________________________________

Step 5: Dashboard & Visualization

The tool builds a professional dashboard table on the chart.

It shows categories such as:

1. Asset Info — Spot, Strike, DTE (days to expiry), IV%, IV Rank, 1-Day Trend, Moneyness (ATM/OTM/ITM).

2. Option Prices — Call, Put, Break-even levels, Time Value, Expected Move (%), Realized vs Implied Vol.

3. Greeks with Visual Progress Bars — Easily shows Delta, Gamma, Vega, Theta, Rho in intuitive graphical representations.

4. Status Bar — Suggests theoretical bias like:

o HIGH IV → Favor Option Selling

o LOW IV → Favor Option Buying

o MEDIUM → Neutral observation

5. Recommendation Line — Offers training-based suggestions like “Buy Straddles”, “Sell Call Spreads”, etc. These are not signals, but scenarios to learn strategies.

________________________________________

3. How It Helps Beginners

1. Learn Greeks in Action:

Beginners often memorize formulas but never see real-time changes. This dashboard updates every bar to show how Greeks change dynamically.

2. Compare Volatilities:

Traders understand difference between historical vs implied volatility and why option premiums behave differently.

3. Understand Risk Levels:

The tool highlights when Gamma risk is high (danger for sellers) or when Theta is most favorable.

4. Training Mode for Strategies:

Helps beginners experiment by changing IV, strike, expiry and seeing how straddles, spreads, naked options would behave theoretically.

5. Prepares Before Live Trading:

Safe environment to practice option analysis without risking capital.

________________________________________

4. Educational Use Cases

• Scenario 1: Change expiry from 7D to 30D — see how Theta becomes slower for longer expiries.

• Scenario 2: Increase IV from 25% to 80% — watch how option premiums inflate, and recommendation changes from “Buy” to “Sell”.

• Scenario 3: Select OTM vs ITM strikes — check how delta moves from near 0 to near 1.

By running these scenarios, learners understand why professional traders hedge Greeks instead of directional gambling.

________________________________________

5. Disclaimer

This Options Greeks Analyzer is built strictly for educational and training purposes.

• It uses theoretical formulas (Black-Scholes) that may not match actual option market prices.

• The recommendations are for learning strategy logic only, not real-world execution signals.

• Trading in options carries significant risks and may result in capital loss.

📌 Always consult with a financial advisor before applying real strategies.

________________________________________

✅ Summary

This Options Greeks Analyzer:

• Teaches how Greeks, IV, and premiums work.

• Provides a real-time interactive dashboard for training.

• Helps beginners practice option scenarios safely.

• Is meant strictly for learning and not live trading execution.

________________________________________

________________________________________

Disclaimer from aiTrendview

This script and its trading signals are provided for training and educational purposes only. They do not constitute financial advice or a guaranteed trading system. Trading involves substantial risk, and there is the potential to lose all invested capital. Users should perform their own analysis and consult with qualified financial professionals before making any trading decisions. aiTrendview disclaims any liability for losses incurred from using this code or trading based on its signals. Use this tool responsibly, and trade only with risk capital.

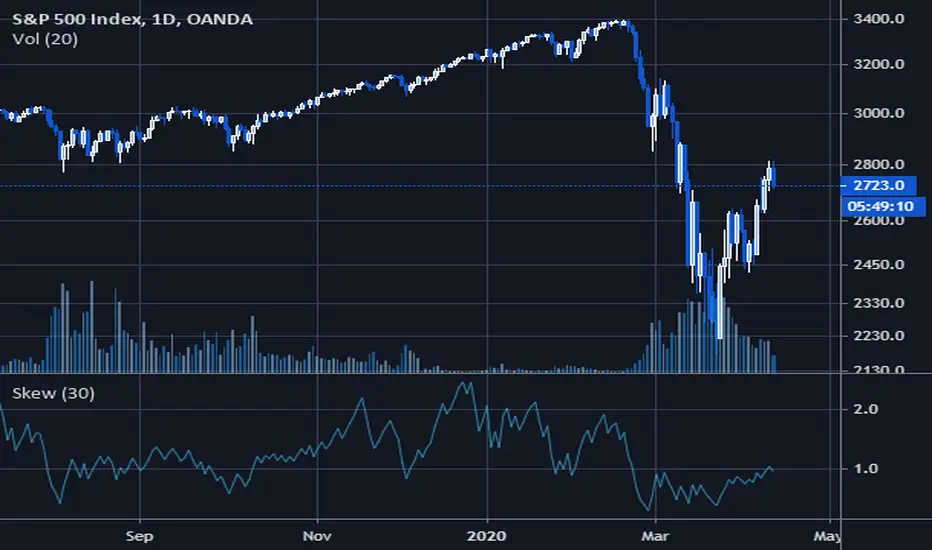

(JS) S&P 500 Volatility Oscillator For OptionsThe idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility. (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX, SPY, even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Boyle Trinomial Options Pricing Model [Loxx]Boyle Trinomial Options Pricing Model is an options pricing indicator that builds an N-order trinomial tree to price American and European options. This is different form the Binomial model in that the Binomial assumes prices can only go up and down wheres the Trinomial model assumes prices can go up, down, or sideways (shoutout to the "crab" market enjoyers). This method also allows for dividend adjustment.

The Trinomial Tree via VinegarHill Finance Labs

A two-jump process for the asset price over each discrete time step was developed in the binomial lattice. Boyle expanded this frame of reference and explored the feasibility of option valuation by allowing for an extra jump in the stochastic process. In keeping with Black Scholes, Boyle examined an asset (S) with a lognormal distribution of returns. Over a small time interval, this distribution can be approximated by a three-point jump process in such a way that the expected return on the asset is the riskless rate, and the variance of the discrete distribution is equal to the variance of the corresponding lognormal distribution. The three point jump process was introduced by Phelim Boyle (1986) as a trinomial tree to price options and the effect has been momentous in the finance literature. Perhaps shamrock mythology or the well-known ballad associated with Brendan Behan inspired the Boyle insight to include a third jump in lattice valuation. His trinomial paper has spawned a huge amount of ground breaking research. In the trinomial model, the asset price S is assumed to jump uS or mS or dS after one time period (dt = T/n), where u > m > d. Joshi (2008) point out that the trinomial model is characterized by the following five parameters: (1) the probability of an up move pu, (2) the probability of an down move pd, (3) the multiplier on the stock price for an up move u, (4) the multiplier on the stock price for a middle move m, (5) the multiplier on the stock price for a down move d. A recombining tree is computationally more efficient so we require:

ud = m*m

M = exp (r∆t),

V = exp (σ 2∆t),

dt or ∆t = T/N

where where N is the total number of steps of a trinomial tree. For a tree to be risk-neutral, the mean and variance across each time steps must be asymptotically correct. Boyle (1986) chose the parameters to be:

m = 1, u = exp(λσ√ ∆t), d = 1/u

pu =( md − M(m + d) + (M^2)*V )/ (u − d)(u − m) ,

pd =( um − M(u + m) + (M^2)*V )/ (u − d)(m − d)

Boyle suggested that the choice of value for λ should exceed 1 and the best results were obtained when λ is approximately 1.20. One approach to constructing trinomial trees is to develop two steps of a binomial in combination as a single step of a trinomial tree. This can be engineered with many binomials CRR(1979), JR(1979) and Tian (1993) where the volatility is constant.

Further reading:

A Lattice Framework for Option Pricing with Two State

Trinomial tree via wikipedia

Inputs

Spot price: select from 33 different types of price inputs

Calculation Steps: how many iterations to be used in the Trinomial model. In practice, this number would be anywhere from 5000 to 15000, for our purposes here, this is limited to 220.

Strike Price: the strike price of the option you're wishing to model

Market Price: this is the market price of the option; choose, last, bid, or ask to see different results

Historical Volatility Period: the input period for historical volatility ; historical volatility isn't used in the Trinomial model, this is to serve as a comparison, even though historical volatility is from price movement of the underlying asset where as implied volatility is the volatility of the option

Historical Volatility Type: choose from various types of implied volatility , search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

Included

Option pricing panel

Loxx's Expanded Source Types

Related indicators

Implied Volatility Estimator using Black Scholes

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model

Institutional Orderflow - CT Institutional Orderflow - CT

Overview

This indicator translates VIX futures dynamics into equity price implications, revealing institutional hedging flows and vol pricing's gravitational pull on price, where overpriced volatility signals compression and upside support, while underpriced levels flag expansion risks and downside pressure.

It maps VX deviations to equity levels via historical correlations, anchored by the Bull Bear Bias (BBB), a contango midpoint concept from Matt Cowart at Rocketscooter that sets VX1! fair value as the midpoint between front-month (VX1!) and second-month (VX2!) contracts at monthly rolls.

VX itself quantifies the distribution of options strikes around the underlying price over time, essentially the market's priced-in dispersion of potential outcomes, tied to expiration distance, with volatility inversely proportional to liquidity (fewer transactions in high-vol environments reduce flow and amplify moves).

Interpretation

- VX1! (Front-Month VIX Futures) : Gauges 30-day (±7 days, or 23-37 days to expiration) SPX implied volatility via forward options pricing, capturing medium-term hedging landscapes. Dealers, managing gamma exposure from longer-dated options, hedge by delta-adjusting underlying positions; rising VX1! reflects widening strike distributions (higher fear), prompting protective equity sales that pressure prices; falls toward BBB indicate narrowing distributions (calm), easing hedges and fostering liquidity-driven rallies as transaction frequency rises.

- VIX1D (1-Day Expected Volatility) : Focuses on ultra-short-dated (e.g., 0DTE) P.M.-settled options, measuring immediate strike clustering and gamma intensity near expiration. Closer-dated options heighten dealer sensitivity; spikes signal concentrated hedging bursts, eroding liquidity and fueling intraday volatility with sharp price reversals; declines promote hedging unwind, boosting transaction flow and short-term stability.

- VVIX (Volatility of VIX) : Assesses the implied volatility of VIX options (the "vol of vol"), revealing uncertainty in the vol forecast itself. Elevated VVIX denotes aggressive dealer repositioning across VIX strikes, forecasting erratic VX swings and reduced equity liquidity; subdued levels imply stable distributions, enhancing flow and trend persistence. BBB projections adjust dynamically: low VVIX (<80) constrains overshoots for reversion trades, while high (>110) expands them amid panic hedging.

- BBB Relationship : VX1! above BBB highlights over-distributed (expensive) vol, where dealers unwind hedges as time decays, inverting low liquidity into upside momentum; below BBB warns of under-distributed (cheap) vol, with sparse transactions amplifying expansion risks. Shorter tenors (VIX1D) drive tactical, gamma-fueled price action, contrasting VX1!'s strategic horizon, with VVIX scaling the intensity.

Key Features

- Target Line (Anchored) : Locks at swing violations as enduring support (green, below price) or resistance (red, above), fusing BBB's vol equilibrium with technical anchors to spotlight dealer hedge confluences in strike distributions.

- Magnet Line (Dynamic) : Mirrors live VX1!/BBB shifts, plotting "implied fair" price (blue above for unwind pull; orange below for hedge drag), linking term structure evolution to liquidity-driven gravity.

- Fear Scenario Line : Forecasts price erosion from a 10%+ VX1! surge above BBB, calibrated by VVIX for vol-of-vol amplification, defining dealer panic thresholds where low-liquidity spikes cascade.

- Overshoot Projection : Predicts interim extensions past targets, modulated by VIX1D (near-term gamma flares) and VVIX (distribution uncertainty), relating expiration proximity to heightened swings before time-decay reversion.

- Candle Coloring and SMA Trends : Tracks near-term VX1!/VVIX/VIX1D flows via gradient-colored candles (strong/medium/weak bullish/bearish based on SMA deviations), visualizing realtime options dynamics; green shades signal hedging unwind (rising liquidity, upside bias), red indicates expansion (dealer sales, downside drag). Recommended: VX1! Trend for long-term confluences (Tue-Thu swings); VIX1D Trend or VX1! + VIX1D for short-term (Mon/Fri scalps); add VVIX for regime shifts.

- Swing Boxes : Denote aggressive VX spikes (fear hedging bets) or de-escalations (position realizations), highlighting gamma-driven reversals where dealers rebalance, often preceding liquidity surges or drains in price action.

- Table Metrics : Condenses VX1!/BBB skew, VVIX regimes, VIX1D pulses, and contango cues, correlating options tenor gradients to price flow and hedging mechanics.

Multiple Rate Of ChangeConvergence of Multiple period Rates of Change near the Zero line shows contraction in volatility.

Soon we can expect expansion in volatility.

Ideal strategy would be to buy ATM Straddles when different period ROCs converge near Zero line.

(Also check implied volatility of options before going for this strategy)

IV Rank (tasty-style) — VIXFix / HV ProxyIV Rank (tasty-style) — VIXFix / HV Proxy

Overview

This indicator replicates tastytrade’s IV Rank calculation—but built entirely inside TradingView.

Because TradingView does not expose live option-chain implied volatility, the script lets you choose between two widely used price-based IV proxies:

VIXFix (Williams VIX Fix): a fast-reacting volatility estimate derived from price extremes.

HV(30): 30-day annualized historical volatility of daily log returns.

The goal is to approximate the “rich vs. cheap” option volatility environment that traders use to decide whether to sell or buy premium.

Formula

IV Rank answers the question: Where is current implied volatility relative to its own 1-year range?

𝐼

𝑉

𝑅

=

𝐼

𝑉

𝑐

𝑢

𝑟

𝑟

𝑒

𝑛

𝑡

−

𝐼

𝑉

1

𝑦

𝐿

𝑜

𝑤

𝐼

𝑉

1

𝑦

𝐻

𝑖

𝑔

ℎ

−

𝐼

𝑉

1

𝑦

𝐿

𝑜

𝑤

×

100

IVR=

IV

1yHigh

−IV

1yLow

IV

current

−IV

1yLow

×100

IVcurrent: Current value of the chosen IV proxy.

IV1yHigh/Low: Highest and lowest proxy values over the user-defined lookback (default 252 trading days ≈ 1 year).

IVR = 0 → Current IV equals its 1-year low

IVR = 100 → Current IV equals its 1-year high

IVR ≈ 50 → Current IV sits mid-range

How to Use

High IV Rank (≥50–60%)

Options are relatively expensive → short-premium strategies (credit spreads, iron condors, straddles) may be more attractive.

Low IV Rank (≤20%)

Options are relatively cheap → long-premium strategies (debit spreads, calendars, diagonals) may offer better risk/reward.

Combine with your own analysis, liquidity checks, and risk management.

Inputs & Customization

IV Source: Choose “VIXFix” or “HV(30)” as the volatility proxy.

IVR Lookback: Rolling window for 1-year high/low (default 252 trading days).

VIXFix Parameters: Length and stdev multiplier to fine-tune sensitivity.

Info Label: Optional on-chart label displays current IV proxy, 1-year high/low, and IV Rank.

Alerts: Optional alerts when IVR crosses 50, falls below 20, or rises above 80.

Notes & Limitations

This indicator does not pull real option-chain IV.

It provides a close structural analogue to tastytrade’s IV Rank using price-derived proxies for markets where options data is not directly available.

For live option IV, use broker platforms or third-party data feeds alongside this script.

Tags: IV Rank, Implied Volatility, Tastytrade, VIXFix, Historical Volatility, Options, Premium Selling, Debit Spreads, Market Volatility

Weekly Covered Calls Strategy with IV & Delta LogicWhat Does the Indicator Do?

this is interactive you must use it with your options chain to input data based on the contract you want to trade.

Visualize three strike price levels for covered calls based on:

Aggressive (closest to price, riskier).

Moderate (mid-range, balanced).

Low Delta (farthest, safer).

Incorporate Implied Volatility (IV) from the options chain to make strike predictions more realistic and aligned with market sentiment. Adjust the risk tolerance by modifying Delta inputs and IV values. Risk is defined for example .30 delta means 30% chance of your shares being assigned. If you want to generate steady income with your shares you might want to lower the risk of them being assigned to .05 or 5% etc.

How to Use the Indicator with the Options Chain

Start with the Options Chain:

Look for the following data points from your options chain:

Implied Volatility (IV Mid): Average IV for a particular strike price.

Delta:

~0.30 Delta: Closest strike (Aggressive).

~0.15–0.20 Delta: Mid-range strike (Moderate).

~0.05–0.10 Delta: Far OTM, safer (Low Delta).

Strike Price: Identify strike prices for the desired Deltas.

Open Interest: Check liquidity; higher OI ensures tighter spreads.

Input IV into the Indicator:

Enter the IV Mid value (e.g., 0.70 for 70%) from the options chain into the Implied Volatility field of the indicator.

Adjust Delta Inputs Based on Risk Tolerance:

Aggressive Delta: Increase if you want strikes closer to the current price (riskier, higher premium).

Default: 0.2 (20% chance of shares being assigned).

Moderate Delta: Balanced risk/reward.

Default: 0.12 (12%)

Low Delta: Decrease for safer, farther OTM strikes.

Default: 0.05 (5%)

Visualize the Chart:

Once inputs are updated:

Red Line: Aggressive Strike (closest, riskiest, higher premium).

Blue Line: Moderate Strike (mid-range).

Green Line: Low Delta Strike (farthest, safer).

Step-by-Step Workflow Example

Open the options chain and note:

Implied Volatility (IV Mid): Example 71.5% → input as 0.715.

Delta for desired strikes:

Aggressive: 0.30 Delta → Closest strike ~ $455.

Moderate: 0.15 Delta → Mid-range strike ~ $470.

Low Delta: 0.05 Delta → Farther strike ~ $505.

Open the indicator and adjust:

IV Mid: Enter 0.715.

Aggressive Delta: Leave at 0.12 (or adjust to bring strikes closer).

Moderate Delta: Leave at 0.18.

Low Delta: Adjust to 0.25 for safer, farther strikes.

View the chart:

Compare the indicator's strikes (red, blue, green) with actual options chain strikes.

Use the visualization to: Validate the risk/reward for each strike.

Align strikes with technical trends, support/resistance.

Adjusting Inputs Based on Risk Tolerance

Higher Risk: Increase Aggressive Delta (e.g., 0.15) for closer strikes.

Use higher IV values for volatile stocks.

Moderate Risk: Use default values (0.12–0.18 Delta).

Balance premiums and probability.

Lower Risk: Increase Low Delta (e.g., 0.30) for farther, safer strikes.

Focus on higher IV stocks with good open interest.

Key Benefits

Simplifies Strike Selection: Visualizes the three risk levels directly on the chart.

Aligns with Market Sentiment: Incorporates IV for realistic forecasts.

Customizable for Risk: Adjust inputs to match personal risk tolerance.

By combining the options chain (IV, Delta, and liquidity) with the technical chart, you get a powerful, visually intuitive tool for covered call strategies.