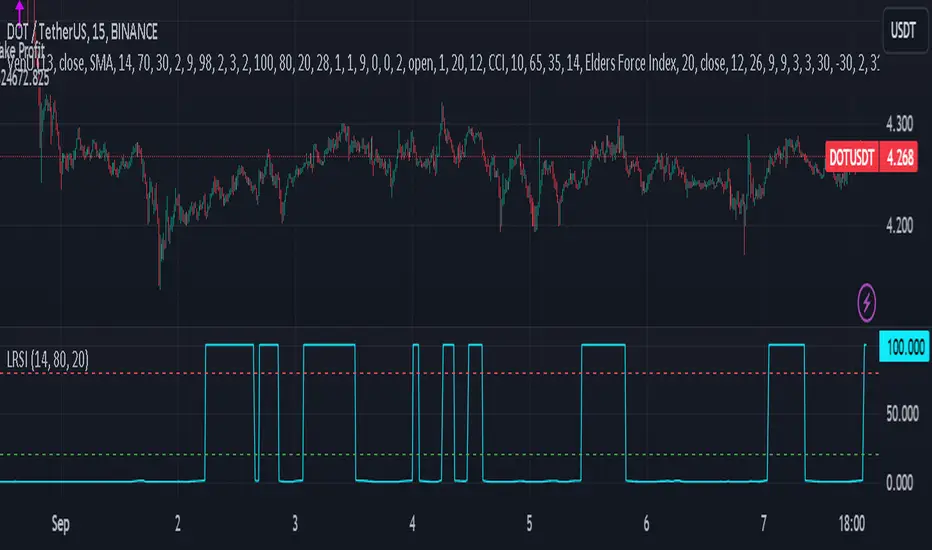

Laguerre RSILaguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI.

Change alpha coefficient to increase/decrease lag and smoothness.

Buy when Laguerre RSI crosses upwards above 20.

Sell when Laguerre RSI crosses down below 80.

While indicator runs flat above 80 level, it means that an uptrend is strong.

While indicator runs flat below 20 level, it means that a downtrend is strong.

Developer: John EHLERS

Author: KivancOzbilgic

Cerca negli script per "Laguerre RSI"

Laguerre RSI (Self Adjusting Alpha with Fractals Energy)Laguerre RSI (Self Adjusting Alpha with Fractals Energy) indicator script. I adopted idea from www.prorealcode.com and

If you disable `Apply Fractals Energy` option, you will get the original Laguerre RSI.

Laguerre RSI by KivancOzbilgic STRATEGYBacktesting.

" Laguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI .

Change alpha coefficient to increase/decrease lag and smoothness.

Buy when Laguerre RSI crosses upwards above 20.

Sell when Laguerre RSI crosses down below 80.

While indicator runs flat above 80 level, it means that an uptrend is strong.

While indicator runs flat below 20 level, it means that a downtrend is strong. "

Developer: John EHLERS

Author: KivancOzbilgic

Laguerre RSI - non repaintingIt seems that the traditional Laguerre* functions repaint due to the gamma parameter.

That goes even for the editorial pick here.

But one could use calculation period instead of "gamma" parameter. This gives us a non-repainting Laguerre RSI fit for scalping trends.

At first glance, I haven't seen anyone do this with a pine script, but I could be wrong because it's not a big deal.

So here is a variation of Laguerre RSI, without repainting. It's a little bit more insensitive, but this is not of great importance, since only the extreme values are used for confirmation.

( * Laguerre RSI is based on John EHLERS' Laguerre Filter to avoid the noise of RSI.)

And if you implement this indicator into a strategy (like I do) I can give you a trick.

Traditionaly the condition is at follows:

LaRSI = cd == 0 ? 100 : cu / (cu + cd)

(this is the final part of the indicator before the plotting)

LongLaguerre= LaRSIupb

It's fine for the short (ot exit long), but for the long is better to make a swich between the CD and CU parameters, as follows:

LaRSI1 = cd == 0 ? 100 : cu / (cu + cd)

LaRSI2 = cu == 0 ? 100 : cu / (cu + cd)

LongLaguerre= LaRSI2upb

Laguerre RSI Multi-Time FrameThe Laguerre RSI Indicator is a modification of the well-known relative strength indicator or RSI. John F. Ehlers, the famous trader who created the Laguerre RSI, tried to avoid whipsaws (noise) and lag produced by smoothing technical indicators by applying a filter and some changes to the original relative strength indicator. The result is a technical indicator that is more responsive and has much less noise than the original RSI indicator.

The multi-time frame LRSI is used to have multiple RSI oscillators on the screen at once that are derived from different intervals. This allows the trader to see setups in multiple time frames.

ATR-Adaptive, Smoothed Laguerre RSI [Loxx]ATR-Adaptive, Smoothed Laguerre RSI is an adaptive Laguerre RSI indicator with smoothing to reduce noise

What is Laguerre RSI?

The Laguerre RSI indicator created by John F. Ehlers is described in his book "Cybernetic Analysis for Stocks and Futures".

This version:

Instead of using fixed periods for Laguerre RSI calculation, this indicator uses an ATR (average True Range) adapting method to adjust the calculation period. This makes the RSI more responsive in some periods (periods of high volatility), and smoother in order periods (periods of low volatility). Also this indicator adds an option to have smoothed source input including Loxx's Expanded Source Types.

Included

-Loxx's Expanded Source Types

-Bar coloring

[blackcat] L2 Ehlers Laguerre RSI IndicatorLevel: 2

Background

John F. Ehlers introuced Laguerre RSI Indicator in his "Cybernetic Analysis for Stocks and Futures" chapter 14 on 2004.

Function

“Truth and science always triumph over ignorance and superstition.” said by Dr. Ehlers. We can generate superior smoothing with very short filters, it follows that we should be able to create superior indicators using very short data lengths also. The use of shorter data lengths means that we can make the indicators more responsive to changes in the price. The Laguerre RSI will be used as an example.

Key Signal

RSI ---> Laguerre RSI Indicator fast line

RSI(1) ---> Laguerre RSI Indicator slow line

Pros and Cons

100% John F. Ehlers definition translation of original work, even variable names are the same. This help readers who would like to use pine to read his book. If you had read his works, then you will be quite familiar with my code style.

Remarks

The 34th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Soheil PKO's 5 min Hitman Scalp - 3MA + Laguerre RSI + ADX [Pt]Someone sent me this strategy found on YouTube. It is Soheil PKO's "The Best and Most Profitable Scalping Strategy" Best way to find out is to code it =)

This strategy uses Moving Average Ribbon, Laguerre RSI, and ADX. This script only displays the MA ribbon, you will need to add Laguerre RSI and ADX separately.

Long Entry Criteria:

- 16 EMA > 48 EMA > 200 SMA

- Laguerre RSI > 80

- ADX > 20

Long Exit Criterion:

- 16 EMA < 48 EMA

Short Entry Criteria:

- 16 EMA < 48 EMA < 200 SMA

- Laguerre RSI < 20

- ADX > 20

Short Exit Criterion:

- 16 EMA > 48 EMA

As mentioned in the video, risk management is very important, especially for scalping strategies. Therefore, I've added option for setting Stop Loss and Price Target in the options for you guys to play with.

All parameters are configurable.

Enjoy~~

Trend-Following Combo-SuperTrend, EMA, Aroon, DMI, Laguerre RSIThis is a trend-following indicator which condenses two SuperTrend indicators -- one based on analysis over a shorter period of time (1.5, 7), and one based on analysis over a longer period of time (1.65, 100) -- into a single indicator which appears on your chart only when both the shorter- and longer-term analysis indicates a "SuperTrend" in the same direction.

Additionally, potential trade entry indicators are displayed in the form of up and down arrows when (by default) three of the following five indicators suggest that the market is trending in the same direction as both the shorter- and longer-term SuperTrend indicators:

EMA Crossover (8, 15)

Aroon Indicator (8)

Aroon Oscillator (8)

Directional Movement Index (DI +/-) (8)

Laguerre RSI (13)

You may update the parameters of any of the indicators to match your own preferences.

Additionally, you may also adjust the "Threshold" of indicators that must be in agreement with the SuperTrend to show a potential trade entry arrow. Bear in mind that if you set the Indicator Threshold too low, you will see more frequent trade entry arrows, many of which will not be profitable if taken. Similarly, set this value too high, and you will see fewer trade entry arrows that may not appear until after most of the "juice" in the trend has evaporated. Ideal values for the threshold seem to be between 2-4, depending on the symbol you are trading.

The following image shows all of the indicators referenced above on a 5-minute chart of the SPY during a single trading day:

And, here is the same period of time showing only the Trend-Following Combo indicator with default settings:

This indicator would not have been possible save for work contributed by the following:

SuperTrend by Rajandran R

Aroon w/ crossovers highlighted by seiglerj

Aroon Oscillator by jcrewolinsky

Directional Movement Index by TradingView

Laguerre RSI (Self Adjusting Alpha with Fractals Energy) by everget

LRSI-TTM Squeeze - AynetThis Pine Script code creates an indicator called LRSI-TTM Squeeze , which combines two key concepts to analyze momentum, squeeze conditions, and price movements in the market:

Laguerre RSI (LaRSI): A modified version of RSI used to identify trend reversals in price movements.

TTM Squeeze: Identifies market compressions (low volatility) and potential breakouts from these squeezes.

Functionality and Workflow of the Code

1. Laguerre RSI (LaRSI)

Purpose:

Provides a smoother and less noisy version of RSI to track price movements.

Calculation:

The script uses a filtering coefficient (alpha) to process price data through four levels (L0, L1, L2, L3).

Movement differences between these levels calculate buying pressure (cu) and selling pressure (cd).

The ratio of these pressures forms the Laguerre RSI:

bash

Kodu kopyala

LaRSI = cu / (cu + cd)

The LaRSI value indicates:

Below 20: Oversold condition (potential buy signal).

Above 80: Overbought condition (potential sell signal).

2. TTM Squeeze

Purpose:

Analyzes the relationship between Bollinger Bands (BB) and Keltner Channels (KC) to determine whether the market is compressed (low volatility) or expanded (high volatility).

Calculation:

Bollinger Bands:

Calculated based on the moving average (SMA) of the price, with an upper and lower band.

Keltner Channels:

Created using the Average True Range (ATR) to calculate an upper and lower band.

Squeeze States:

Squeeze On: BB is within KC.

Squeeze Off: BB is outside KC.

Other States (No Squeeze): Neither of the above applies.

3. Momentum Calculation

Momentum is computed using the linear regression of the difference between the price and its SMA. This helps anticipate the direction and strength of price movements when the squeeze ends.

Visuals on the Chart

Laguerre RSI Line:

An RSI indicator scaled to 0-100 is plotted.

The line's color changes based on its movement:

Green line: RSI is rising.

Red line: RSI is falling.

Key levels:

20 level: Oversold condition (buy signal can be triggered).

80 level: Overbought condition (sell signal can be triggered).

Momentum Histogram:

Displays momentum as histogram bars with colors based on its direction and strength:

Lime (light green): Positive momentum increasing.

Green: Positive momentum decreasing.

Red: Negative momentum decreasing.

Maroon (dark red): Negative momentum increasing.

Squeeze Status Indicator:

A marker is plotted on the zero line to indicate the squeeze state:

Yellow: Squeeze On (compression active).

Blue: Squeeze Off (compression ended, movement expected).

Gray: No Squeeze.

Information Table

A table is displayed in the top-right corner of the chart, showing closing prices for different timeframes (e.g., 1 minute, 5 minutes, 1 hour, etc.). Each timeframe is color-coded.

Alerts

LaRSI Alerts:

Crosses above 20: Exiting oversold condition (buy signal).

Crosses below 80: Exiting overbought condition (sell signal).

Squeeze Alerts:

When the squeeze ends: Indicates a potential price move.

When the squeeze starts: Indicates volatility is decreasing.

Summary

This indicator is a powerful tool for determining market trends, momentum, and squeeze conditions. It helps users identify periods when the market is likely to move or remain stagnant, providing alerts based on these analyses to support trading strategies.

STD-Filtered, ATR-Adaptive Laguerre Filter [Loxx]STD-Filtered, ATR-Adaptive Laguerre Filter is a standard Laguerre Filter that is first made ATR-adaptive and the passed through a standard deviation filter. This helps reduce noise and refine the output signal. Can apply the standard deviation filter to the price, signal, both or neither.

What is the Laguerre Filter?

The Laguerre RSI indicator created by John F. Ehlers is described in his book "Cybernetic Analysis for Stocks and Futures". The Laguerre Filter is a smoothing filter which is based on Laguerre polynomials. The filter requires the current price, three prior prices, a user defined factor called Alpha to fill its calculation. Adjusting the Alpha coefficient is used to increase or decrease its lag and it's smoothness.

Included:

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

Minimal Godmode 2.1// Acknowledgments:

// Original Godmode Authors:

// @Legion, @LazyBear, @Ni6HTH4wK, @xSilas

// Drop a line if you use or modify this code.

// Godmode 3.1.4: @SNOW_CITY

// Godmode 3.2: @sco77m4r7in and @oh92

// Godmode3.2+LSMA: @scilentor

// Godmode 4.0.0-4.0.1: @chrysopoetics

// Jurik Moving Average: @everget

// Constance Brown Composite Index RSI: @LazyBear

// Wavetrend Oscillator: @fskrypt

// TTM Squeeze: @Greeny

// True TSI/RSI: @cI8DH and @chrysopoetics

// Laguerre RSI (Self-Adjusting Alpha with Fractals Energy): @everget

// RSI Shaded: @mortdiggiddy

// Minimal Godmode v2.0:

// 6 BTC pairs/exchanges (instead of 11) to reduce loading time from the pinescript security() function

// Volume Composite for engine calculation

// TTM Squeeze on Wavetrend Signal

// Constance Brown Composite Index RSI (CBCI)

// TrueTSI (Godmode 4.0.0 implementation)

// Laguerre RSI (LRSI)

// Minimal Godmode v2.1:

// Removed TTM Squeeze and Volume Composite

// EMA for Wavetrend Signal

// Multi-exchange for BTC no longer the default

// mg engine toggle for CBCI, Laguerre RSI, and TTSI

// Wavetrend Histogram component toggle

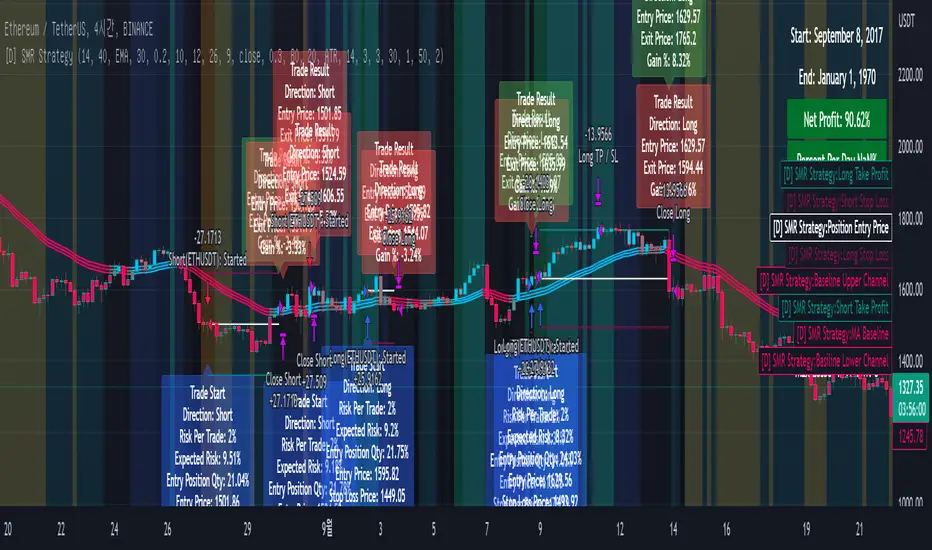

[DuDu95] SSL 4C MACD Laugerre RSI StrategyHello Guys! Nice to meet you all!

Before I start, my nickname has changed to 'DuDu95'!!

This is the Strategy introduced by youtube channel.

I made this based on the open source indicator by kevinmck100, vkno422, KivancOzbilgic. Thank you All!

### Entry Logic

1. Long Entry Logic

- close > SSL Hybrid baseline upper k (keltner channel)

- macd signal > 0 and current MACD value > previous MACD value

- Laguerre RSI < overbought Line.

2. short Entry Logic

- close < SSL Hybrid baseline lower k (keltner channel)

- macd signal < 0 and current MACD value < previous MACD value

- Laguerre RSI > overbought Line.

### Exit Logic

1. Long Exit Logic

- close < SSL Hybrid baseline lower k (keltner channel)

- macd signal < 0

2. short Entry Logic

- close > SSL Hybrid baseline upper k (keltner channel)

- macd signal > 0

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

FREE INDICATOR: Laguerre RSIAbout:

Averages, and the way they are compared and calculated make up a large amount of the indicators out there, so the fun thing about new averages, is how they open up a whole new group of indicators.

Usage:

This is Laguerre RSI. You'll notice it acts a little different than your normal RSI, and it can be traded in different ways. It can be used as a switch, or to view bursts of momentum. Combine with your style and see if you notice anything. It might just be what you were looking for! Stay tuned for more scripts & ideas by following me on TradingView.

Grab the source code here: pastebin.com

Installation video by @ChrisMoody here : blog.tradingview.com

░░░░░░░░░░░░░░░ Feel free to follow me to keep up with my latest scripts! ░░░░░░░░░░░░░░░

░░░░░░░░░░░░ PLEASE THUMB UP OR STAR IF YOU LIKE THIS INDICATOR! ░░░░░░░░░░░░

I'd like as many people as possible to get it :)

NormalizedOscillatorsLibrary "NormalizedOscillators"

Collection of some common Oscillators. All are zero-mean and normalized to fit in the -1..1 range. Some are modified, so that the internal smoothing function could be configurable (for example, to enable Hann Windowing, that John F. Ehlers uses frequently). Some are modified for other reasons (see comments in the code), but never without a reason. This collection is neither encyclopaedic, nor reference, however I try to find the most correct implementation. Suggestions are welcome.

rsi2(upper, lower) RSI - second step

Parameters:

upper : Upwards momentum

lower : Downwards momentum

Returns: Oscillator value

Modified by Ehlers from Wilder's implementation to have a zero mean (oscillator from -1 to +1)

Originally: 100.0 - (100.0 / (1.0 + upper / lower))

Ignoring the 100 scale factor, we get: upper / (upper + lower)

Multiplying by two and subtracting 1, we get: (2 * upper) / (upper + lower) - 1 = (upper - lower) / (upper + lower)

rms(src, len) Root mean square (RMS)

Parameters:

src : Source series

len : Lookback period

Based on by John F. Ehlers implementation

ift(src) Inverse Fisher Transform

Parameters:

src : Source series

Returns: Normalized series

Based on by John F. Ehlers implementation

The input values have been multiplied by 2 (was "2*src", now "4*src") to force expansion - not compression

The inputs may be further modified, if needed

stoch(src, len) Stochastic

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

ssstoch(src, len) Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the January 2014 issue of Stocks and Commodities

This is not an implementation of MESA Stochastic, as it is based on Highpass filter not present in the function (but you can construct it)

This implementation is scaled by 0.95, so that Super Smoother does not exceed 1/-1

I do not know, if this the right way to fix this issue, but it works for now

netKendall(src, len) Noise Elimination Technology by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the December 2020 issue of Stocks and Commodities

Uses simplified Kendall correlation algorithm

Implementation by @QuantTherapy:

rsi(src, len, smooth) RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

vrsi(src, len, smooth) Volume-scaled RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

This is my own version of RSI. It scales price movements by the proportion of RMS of volume

mrsi(src, len, smooth) Momentum RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

rrsi(src, len, smooth) Rocket RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

Does not include Fisher Transform of the original implementation, as the output must be normalized

Does not include momentum smoothing length configuration, so always assumes half the lookback length

mfi(src, len, smooth) Money Flow Index

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

lrsi(src, in_gamma, len) Laguerre RSI by John F. Ehlers

Parameters:

src : Source series

in_gamma : Damping factor (default is -1 to generate from len)

len : Lookback period (alternatively, if gamma is not set)

Returns: Oscillator series

The original implementation is with gamma. As it is impossible to collect gamma in my system, where the only user input is length,

an alternative calculation is included, where gamma is set by dividing len by 30. Maybe different calculation would be better?

fe(len) Choppiness Index or Fractal Energy

Parameters:

len : Lookback period

Returns: Oscillator series

The Choppiness Index (CHOP) was created by E. W. Dreiss

This indicator is sometimes called Fractal Energy

er(src, len) Efficiency ratio

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Based on Kaufman Adaptive Moving Average calculation

This is the correct Efficiency ratio calculation, and most other implementations are wrong:

the number of bar differences is 1 less than the length, otherwise we are adding the change outside of the measured range!

For reference, see Stocks and Commodities June 1995

dmi(len, smooth) Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Based on the original Tradingview algorithm

Modified with inspiration from John F. Ehlers DMH (but not implementing the DMH algorithm!)

Only ADX is returned

Rescaled to fit -1 to +1

Unlike most oscillators, there is no src parameter as DMI works directly with high and low values

fdmi(len, smooth) Fast Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Same as DMI, but without secondary smoothing. Can be smoothed later. Instead, +DM and -DM smoothing can be configured

doOsc(type, src, len, smooth) Execute a particular Oscillator from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Chande Momentum Oscillator (CMO) is RSI without smoothing. No idea, why some authors use different calculations

LRSI with Fractal Energy is a combo oscillator that uses Fractal Energy to tune LRSI gamma, as seen here: www.prorealcode.com

doPostfilter(type, src, len) Execute a particular Oscillator Postfilter from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

Returns: Oscillator series

RSI Shaded - MTF

Non-repainting multiple time frame RSI with shading of overbought and oversold levels.

Includes option for simple moving average smooth of the RSI (Larry Connors)

Includes option to plot the EMA of the RSI

Related to RSI Shaded .

For other multiple time frame indicators see:

Adaptive ATR-ADX Trend

Fisher Transform MTF

ADX-DI MTF

Laguerre RSI MTF

Professional MSTI+ Trading Indicator"Professional MSTI+ Trading Indicator" is a comprehensive technical analysis tool that combines over 20 indicators to generate high-quality trading signals and assess market sentiment. The script integrates standard indicators (MACD, RSI, Bollinger Bands, Stochastic, Simple Moving Averages, and Volume Analysis) with advanced components (Squeeze Momentum, Fisher Transform, True Strength Index, Heikin-Ashi, Laguerre RSI, Hull MA) and further includes metrics such as ADX, Chaikin Money Flow, Williams %R, VWAP, and EMA for in-depth market analysis.

Key Features:

Multiple Presets for Different Trading Styles:

Choose from optimal configurations like Professional, Swing Trading, Day Trading, Scalping, or Reversal Hunter. Note that the presets may not work perfectly on all pairs, and manual calibration might be required. This flexibility allows you to fine-tune the settings to align with your unique strategies and signals.

Multi-Layered Signal Filtering:

Filters based on trend, volume, and volatility help eliminate false signals, enhancing the accuracy of market entries.

Comprehensive Fear & Greed Index:

The indicator aggregates data from RSI, volatility, momentum, trend, and volume to gauge overall market sentiment, providing an additional layer of market context.

Dynamic Information Panel:

Displays detailed status updates for each component (e.g., MACD, RSI, Laguerre RSI, TSI, Fisher Transform, Squeeze, Hull MA, etc.) along with a visual strength bar that represents the intensity of the trading signal.

Signal Generation:

Buy and sell signals are generated when a predefined number of conditions are met and confirmed over multiple bars. These signals are clearly displayed on the chart with arrows, making it easier to spot potential entry and exit points.

Alert Setup:

Built-in alert conditions allow you to receive real-time notifications when trading signals are generated, helping you stay on top of market movements.

"Professional MSTI+ Trading Indicator" is designed to enhance your trading strategy by providing a multi-faceted market analysis and an intuitive visual interface. While the presets offer a robust starting point, they may require manual calibration on certain pairs, giving you the flexibility to configure your own unique strategies and signals.

ADX-DI Multi-TimeframePlots the multiple time frame version of the classic ADX-DI indicoator.

ADX

DI+ and DI-

ADX Threshold

DI Histogram difference with 2 threshold lookback values

For a similar multiple time frame indicator see the following scripts. They both use the historical + projection approach to yield non-repainting indicators.

Fisher Transform Multi-Timeframe

Laguerre RSI Multi-Timeframe

Adaptive Oscillator constructor [lastguru]Adaptive Oscillators use the same principle as Adaptive Moving Averages. This is an experiment to separate length generation from oscillators, offering multiple alternatives to be combined. Some of the combinations are widely known, some are not. Note that all Oscillators here are normalized to -1..1 range. This indicator is based on my previously published public libraries and also serve as a usage demonstration for them. I will try to expand the collection (suggestions are welcome), however it is not meant as an encyclopaedic resource , so you are encouraged to experiment yourself: by looking on the source code of this indicator, I am sure you will see how trivial it is to use the provided libraries and expand them with your own ideas and combinations. I give no recommendation on what settings to use, but if you find some useful setting, combination or application ideas (or bugs in my code), I would be happy to read about them in the comments section.

The indicator works in three stages: Prefiltering, Length Adaptation and Oscillators.

Prefiltering is a fast smoothing to get rid of high-frequency (2, 3 or 4 bar) noise.

Adaptation algorithms are roughly subdivided in two categories: classic Length Adaptations and Cycle Estimators (they are also implemented in separate libraries), all are selected in Adaptation dropdown. Length Adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle Estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly).

Chande (Price) - based on Chande's Dynamic Momentum Index (CDMI or DYMOI), which is dynamic RSI with this length

Chande (Volume) - a variant of Chande's algorithm, where volume is used instead of price

VIDYA - based on VIDYA algorithm. The period oscillates from the Lower Bound up (slow)

VIDYA-RS - based on Vitali Apirine's modification of VIDYA algorithm (he calls it Relative Strength Moving Average). The period oscillates from the Upper Bound down (fast)

Kaufman Efficiency Scaling - based on Efficiency Ratio calculation originally used in KAMA

Deviation Scaling - based on DSSS by John F. Ehlers

Median Average - based on Median Average Adaptive Filter by John F. Ehlers

Fractal Adaptation - based on FRAMA by John F. Ehlers

MESA MAMA Alpha - based on MESA Adaptive Moving Average by John F. Ehlers

MESA MAMA Cycle - based on MESA Adaptive Moving Average by John F. Ehlers , but unlike Alpha calculation, this adaptation estimates cycle period

Pearson Autocorrelation* - based on Pearson Autocorrelation Periodogram by John F. Ehlers

DFT Cycle* - based on Discrete Fourier Transform Spectrum estimator by John F. Ehlers

Phase Accumulation* - based on Dominant Cycle from Phase Accumulation by John F. Ehlers

Length Adaptation usually take two parameters: Bound From (lower bound) and To (upper bound). These are the limits for Adaptation values. Note that the Cycle Estimators marked with asterisks(*) are very computationally intensive, so the bounds should not be set much higher than 50, otherwise you may receive a timeout error (also, it does not seem to be a useful thing to do, but you may correct me if I'm wrong).

The Cycle Estimators marked with asterisks(*) also have 3 checkboxes: HP (Highpass Filter), SS (Super Smoother) and HW (Hann Window). These enable or disable their internal prefilters, which are recommended by their author - John F. Ehlers . I do not know, which combination works best, so you can experiment.

Chande's Adaptations also have 3 additional parameters: SD Length (lookback length of Standard deviation), Smooth (smoothing length of Standard deviation) and Power ( exponent of the length adaptation - lower is smaller variation). These are internal tweaks for the calculation.

Oscillators section offer you a choice of Oscillator algorithms:

Stochastic - Stochastic

Super Smooth Stochastic - Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

CMO - Chande Momentum Oscillator

RSI - Relative Strength Index

Volume-scaled RSI - my own version of RSI. It scales price movements by the proportion of RMS of volume

Momentum RSI - RSI of price momentum

Rocket RSI - inspired by RocketRSI by John F. Ehlers (not an exact implementation)

MFI - Money Flow Index

LRSI - Laguerre RSI by John F. Ehlers

LRSI with Fractal Energy - a combo oscillator that uses Fractal Energy to tune LRSI gamma

Fractal Energy - Fractal Energy or Choppiness Index by E. W. Dreiss

Efficiency ratio - based on Kaufman Adaptive Moving Average calculation

DMI - Directional Movement Index (only ADX is drawn)

Fast DMI - same as DMI, but without secondary smoothing

If no Adaptation is selected (None option), you can set Length directly. If an Adaptation is selected, then Cycle multiplier can be set.

Before an Oscillator, a High Pass filter may be executed to remove cyclic components longer than the provided Highpass Length (no High Pass filter, if Highpass Length = 0). Both before and after the Oscillator a Moving Average can be applied. The following Moving Averages are included: SMA, RMA, EMA, HMA , VWMA, 2-pole Super Smoother, 3-pole Super Smoother, Filt11, Triangle Window, Hamming Window, Hann Window, Lowpass, DSSS. For more details on these Moving Averages, you can check my other Adaptive Constructor indicator:

The Oscillator output may be renormalized and postprocessed with the following Normalization algorithms:

Stochastic - Stochastic

Super Smooth Stochastic - Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

Inverse Fisher Transform - Inverse Fisher Transform

Noise Elimination Technology - a simplified Kendall correlation algorithm "Noise Elimination Technology" by John F. Ehlers

Except for Inverse Fisher Transform, all Normalization algorithms can have Length parameter. If it is not specified (set to 0), then the calculated Oscillator length is used.

More information on the algorithms is given in the code for the libraries used. I am also very grateful to other TradingView community members (they are also mentioned in the library code) without whom this script would not have been possible.

FRACHTALS"FRACHTALS" - A practical example of taking a joke entirely way, way too far

Speaking of which - Moon when?

#REKT

Credits/Acknowledgements/References:

Fractal detection + other functions (@RicardoSantos)

Laguerre RSI w/ self-Adjusting Alpha (@everget)