Radar RiderThe Radar Rider indicator is a powerful tool that combines multiple technical indicators into a single spider plot, providing traders with a comprehensive view of market conditions. This article will delve into the workings of each built-in indicator and their arrangement within the spider plot. To better understand the structure of the script, let's first examine some of the primary functions and how they are utilized in the script.

Normalize Function: normalize(close, len)

The normalize function takes the close price and a length as arguments and normalizes the price data by scaling it between 0 and 1, making it easier to compare different indicators.

Exponential Moving Average (EMA) Filter: bes(source, alpha)

The EMA filter is used to smooth out data using an exponential moving average, with the given alpha value defining the level of smoothing. This helps reduce noise and enhance the trend-following characteristics of the indicators.

Maximum and Minimum Functions: max(src) and min(src)

These functions find the maximum and minimum values of the input data over a certain period, respectively. These values are used in the normalization process and can help identify extreme conditions in the market.

Min-Max Function: min_max(src)

The min-max function scales the input data between 0 and 100 by dividing the difference between the data point and the minimum value by the range between the maximum and minimum values. This standardizes the data, making it easier to compare across different indicators.

Slope Function: slope(source, length, n_len, pre_smoothing = 0.15, post_smoothing = 0.7)

The slope function calculates the slope of a given data source over a specified length, and then normalizes it using the provided normalization length. Pre-smoothing and post-smoothing values can be adjusted to control the level of smoothing applied to the data before and after calculating the slope.

Percent Function: percent(x, y)

The percent function calculates the percentage difference between two values, x and y. This is useful for comparing the relative change in different indicators.

In the given code, there are multiple indicators included. Here, we will discuss each of them in detail.

EMA Diff:

The Exponential Moving Average (EMA) Diff is the difference between two EMA values of different lengths. The EMA is a type of moving average that gives more weight to recent data points. The EMA Diff helps traders identify trends and potential trend reversals. In the code, the EMA Diff is calculated using the ema_diff() function, which takes length, close, filter, and len_norm as parameters.

Percent Rank EMA Diff:

The Percent Rank EMA Diff is the percentage rank of the EMA Diff within a given range. It helps traders identify overbought or oversold conditions in the market. In the code, the Percent Rank EMA Diff is calculated using the percent_rank_ema_diff() function, which takes length, close, filter, and len_norm as parameters.

EMA Diff Longer:

The EMA Diff Longer is the difference between two EMA values of different lengths, similar to EMA Diff but with a longer period. In the code, the EMA Diff Longer is calculated using the ema_diff_longer() function, which takes length, close, filter, and len_norm as parameters.

RSI Filter:

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. The RSI Filter is the RSI value passed through a filter to smooth out the data. In the code, the RSI Filter is calculated using the rsi_filter() function, which takes length, close, and filter as parameters.

RSI Diff Normalized:

The RSI Diff Normalized is the normalized value of the derivative of the RSI. It helps traders identify potential trend reversals in the market. In the code, the RSI Diff Normalized is calculated using the rsi_diff_normalized() function, which takes length, close, filter, len_mad, and len_norm as parameters.

Z Score:

The Z Score is a statistical measurement that describes a value's relationship to the mean of a group of values. In the context of the code, the Z Score is calculated for the closing price of a security. The z_score() function takes length, close, filter, and len_norm as parameters.

EMA Normalized:

The EMA Normalized is the normalized value of the EMA, which helps traders identify trends and potential trend reversals in the market. In the code, the EMA Normalized is calculated using the ema_normalized() function, which takes length, close, filter, and len_norm as parameters.

WMA Volume Normalized:

The Weighted Moving Average (WMA) Volume Normalized is the normalized value of the WMA of the volume. It helps traders identify volume trends and potential trend reversals in the market. In the code, the WMA Volume Normalized is calculated using the wma_volume_normalized() function, which takes length, volume, filter, and len_norm as parameters.

EMA Close Diff Normalized:

The EMA Close Diff Normalized is the normalized value of the derivative of the EMA of the closing price. It helps traders identify potential trend reversals in the market. In the code, the EMA Close Diff Normalized is calculated using the ema_close_diff_normalized() function, which takes length, close, filter, len_mad, and len_norm as parameters.

Momentum Normalized:

The Momentum Normalized is the normalized value of the momentum, which measures the rate of change of a security's price. It helps traders identify trends and potential trend reversals in the market. In the code, the Momentum Normalized is calculated using the momentum_normalized() function, which takes length, close, filter, and len_norm as parameters.

Slope Normalized:

The Slope Normalized is the normalized value of the slope, which measures the rate of change of a security's price over a specified period. It helps traders identify trends and potential trend reversals in the market. In the code, the Slope Normalized is calculated using the slope_normalized() function, which takes length, close, filter, and len_norm as parameters.

Trend Intensity:

Trend Intensity is a measure of the strength of a security's price trend. It is based on the difference between the average of price increases and the average of price decreases over a given period. The trend_intensity() function in the code calculates the Trend Intensity by taking length, close, filter, and len_norm as parameters.

Volatility Ratio:

The Volatility Ratio is a measure of the volatility of a security's price, calculated as the ratio of the True Range (TR) to the Exponential Moving Average (EMA) of the TR. The volatility_ratio() function in the code calculates the Volatility Ratio by taking length, high, low, close, and filter as parameters.

Commodity Channel Index (CCI):

The Commodity Channel Index (CCI) is a momentum-based oscillator used to help determine when an investment vehicle is reaching a condition of being overbought or oversold. The CCI is calculated as the difference between the mean price of a security and its moving average, divided by the mean absolute deviation (MAD) of the mean price. In the code, the CCI is calculated using the cci() function, which takes length, high, low, close, and filter as parameters.

These indicators are combined in the code to create a comprehensive trading strategy that considers multiple factors such as trend strength, momentum, volatility, and overbought/oversold conditions. The combined analysis provided by these indicators can help traders make informed decisions and improve their chances of success in the market.

The Radar Rider indicator is a powerful tool that combines multiple technical indicators into a single, easy-to-read visualization. By understanding the inner workings of each built-in indicator and their arrangement within the spider plot, traders can better interpret market conditions and make informed trading decisions.

Cerca negli script per "TAKE"

Crypto Uptrend Script + Pullback//Volume CandlesDescription: his is an adaption of my Pullback candle - This works on all timeframes and Markets (Forex//Stocks//)

Crypto Uptrend Script with Pullback Candle allows traders to get into a trend when the price is at end of a pullback and entering a balance phase in the market (works on all markets). The use of Moving averages to help identify a Trends and the use of Key levels to help traders be aware of where strong areas are in the market.

This script can work really well in Crypto Bull Runs when used on HTF and with confluences

The script has key support and resistance zones which are made up of quarterly data. Price reacts to these areas but patience is required as price will take time to come into these areas

I have updated the Pullback Candle with the use of Volume to filter out the weak Pullback Candles -

There are new candles to the script.

The First candle is the Bullish Volume Candle - This candle is set to a multiplier of 2x with a crossover of 50/100 on Volume - this then will paint a purple candle.

Uses of the Bullish Volume Candle:

Breakthrough of key areas // special chart patterns

Rejection of key areas

End of a impulse wave (Profit Takers)

The second candle is a Hammer - I prefer using the Hammers on Higher Timeframes however they do work on all timeframes. .

The third candle is a Exhaustion of impulse downward move.

Uses of this candle - can denote a new trend but has to be with confluence to a demand area // support area or with any use of technical analysis - using this alone is not advised

The fourth candle is a indecision candle in the shape of a Doji - this candle can help identify if the trend is in a continuation or a reversal

This script can work really well in Crypto Bull Runs

Disclaimer: There will be Pullbacks with High Volume (Breakouts) and not go the way as intended but this script is to allow traders to get into trends at good price levels. The script can paint signals in areas where price is too expensive so please do your own due diligence on the markets as this script is to help get into good areas of price

Please leave a thumbs up if you like this script and message me for information on how to use the script.

peterzorve-libraryLibrary "library"

is_bullish_engulfing()

is_bearish_engulfing()

is_hammer(fib_level)

Parameters:

fib_level (float)

is_shooting_star(fib_level)

Parameters:

fib_level (float)

is_hammer_and_star(fib_level)

Parameters:

fib_level (float)

is_star_and_hammer(fib_level)

Parameters:

fib_level (float)

is_dogi(dogi_body_ratio)

Parameters:

dogi_body_ratio (float)

is_bear_bear_bullish_engulf()

is_atr_stoploss_takeprofit(atr_multiplier, atr_length, reward_ratio)

Parameters:

atr_multiplier (float)

atr_length (simple int)

reward_ratio (float)

is_fixed_stoploss_takeprofit(stoploss_pips, reward_ratio)

Parameters:

stoploss_pips (float)

reward_ratio (float)

is_step_trailing_stoploss(stoploss_pips)

Parameters:

stoploss_pips (float)

is_atr_trailing_stoploss(atr_multiplier, break_even_pip)

Parameters:

atr_multiplier (float)

break_even_pip (int)

is_pull_back_strategy(length)

Parameters:

length (simple int)

is_trade_statistics(condition, entrypoint, stoploss, takeprofit)

Parameters:

condition (bool)

entrypoint (float)

stoploss (float)

takeprofit (float)

is_table_of_statistics(win_trades, lost_trades, even_trades, pips_won, pips_lost)

Parameters:

win_trades (int)

lost_trades (int)

even_trades (int)

pips_won (float)

pips_lost (float)

is_pine_info(lotsize, stoploss, takeprofit)

Parameters:

lotsize (float)

stoploss (float)

takeprofit (float)

is_support_and_resistance_strategy(look_back, look_forward)

Parameters:

look_back (int)

look_forward (int)

is_choral_strategy(smoothing_period, constant_d)

Parameters:

smoothing_period (int)

constant_d (float)

is_bollinger_band_strategy(length, dev_entry, dev_stoploss, dev_takeprofit)

Parameters:

length (int)

dev_entry (simple float)

dev_stoploss (simple float)

dev_takeprofit (simple float)

Strategy: Range BreakoutWhat?

In the price action, levels have a significant role to play. Based on the price moving above/below the levels - the underlying instrument shows some price-action in the direction of breakout/breakdown.

There are plenty of ways level can be determined. Levels are the decision point to take a trade or not. But if we make the level derivation complex, then the execution may get hamper.

This strategy script, developed in PineScript v5, is our attempt at solving this problem at the core by providing this simple, yet elegant solution to this problem.

It's essentially an attempt to Trade Simple by drawing logical (horizontal) lines in the chart and take actions, after multiple associated parameters confirmation, on the breakout / breakdown of the levels.

How?

Let us explain how we are drawing the levels.

We are depending on some of the parameters as described below:

Open Range : During intraday movement, often if prices move beyond a particular level, it exibits more movement in the same swing in same direction. We found out, through our back testing for Indian Indices like NSE:NIFTY , NSE:BANKNIFTY or NSE:CNXFINANCE the first 15m (i.e 09:15 AM to 09:30 AM, IST) is one of such range. For Indian stocks, it is 9:15 to 9:45. And for MCX MCX:CRUDEOIL1! it's 5:00 pm to 6:00 pm. There are our first levels.

PDHCL : Previous Day High, Close, Low. This is our next level

VWAP : The rolling VWAP (volume weighted average price)

In the breakout/breakdown of the Open Range and Previous Day High/Low, we are taking the trade decisions as follows using CEST principle:

C onditions :

If current bar's (say you are in 5m timeframe) closing is broken out the Open Range High or Previous Day High, taken a Buy/Long decision (let's say buying a Call Option CE or selling a Put Option PE or buying the future or cash).

If current bar's (say you are in 5m timeframe) closing is broken down the Open Range Low or Previous Day Low, taken a Sell/Short decision (let's say buying a Put Option CE or selling a Call Option PE or selling the future or cash).

Additionally, and optionally (default ON, one can turn off): we are checking various other associated multiple confirmations as follows:

1. Momentum : Checking 14-period RSI value is more than 50 or less than 50 (all parameters like period, OB, OS ranges are configurable through settings)

2. Current bar's volume is more than the last 20 bars volume average. How much more - that multiplier is also configurable. (default is 1)

3. The breakout candle is bullish (green) or bearish (red).

E ntry :

All of these happens only on the closing of the candle . Means: Non Repainting! .

Clearly in the chart we are showing as green up arrow BO (breakout for buy) and red down arrow BD (breakdown for sell) to take your decision process smooth.

So, on the closing of the decision BO/BD candle we are entering the trade (with a thumping heart and nail biting ...)

S top Loss :

We are relying on the time tasted (last 40 years) mechanism of Average True Range (ATR) of default 14 period. This default period is also configurable.

So for Long trades: the 14 period ATR low band is the SL.

For Short trades: the 14 period ATR high band is the SL.

T arget :

We are depending on the thump rule of 1:2 Risk Reward. It's simple and effective. No fancy thing. We are closing the trade on double the favorable price movement compared to the SL placed. Of course, this RR ratio is confiurable from the settings, as usual.

What's Unqiue in it?

The utter simplicity of this trading mechanism. No fancy things like complex chart pattern, OI data, multiple candlestick patterns, Order flow analysis etc.

Simple level determination,

Marking clearly in the chart.

Making each parameter configurable in Settings and showing tooltip adjacent to the parameter to make you understand it better for your customization,

Wait for the candle close, thus eliminating the chances of repainting menace (as much as possible)

Additional momentum and volume check to trade entry confirmation.

Works with normal candlestick (nothing special ones like HA ...)

Showing everything as a Summary Table (which, again can be turned off optionally) overlaying at the bottom-right corner of the chart,

Optionally the Summary Table can be configured to alert you back (say you get it notified in your email or SMS).

That way, a single, simple, effective trade setup will ease your journey as smooth sail as possible.

Mentions

There are plenty of friends from whom time to time we borrowed some of the ideas while working closely together over last one year.

From tradingview community, we took the spirit of @zzzcrypto123 awesome work done long back (in 2020) as the indicator "ORB - Opening Range Breakout". (We tried to reach him for his explicit consent, unable to catch hold of him).

Some other publicly available materials we have consulted to get the additional checks (like RSI, volume).

Lat word

Use it please and thank you for your constant patronage in following us in this awesome platform. Let's keep growing together.

Disclaimer :

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

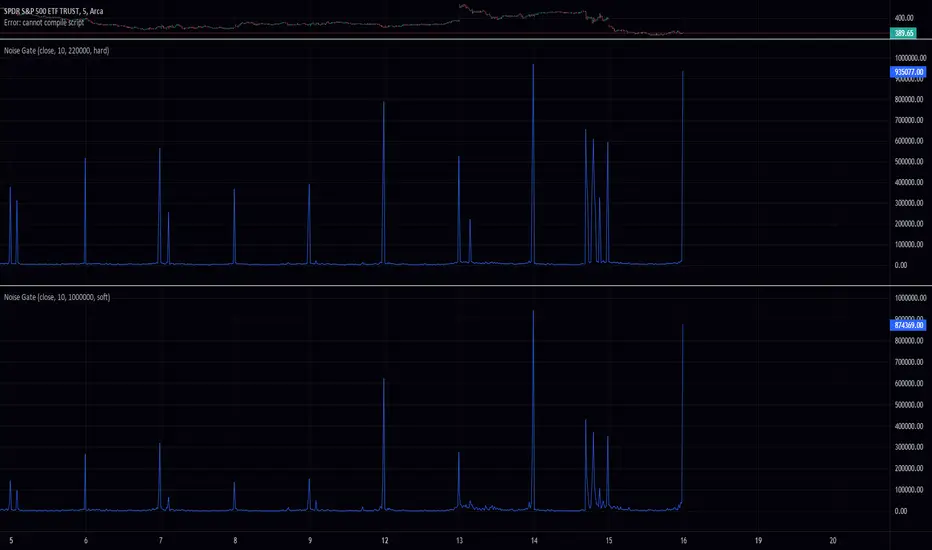

Noise GateThis Pine Script code defines an indicator called "Noise Gate" which filters out "noise" from a given signal. The indicator takes four input parameters: source, length, ratio, and level. The source parameter specifies the source data for the indicator (e.g., close prices), the length parameter specifies the length of a moving average, the ratio parameter specifies the attenuation ratio, and the level parameter specifies the threshold for attenuating the signal.

The core of the indicator is the noise_gate function, which takes three input parameters: signal, ratio, and level. The signal parameter represents the input signal that needs to be filtered. The ratio parameter specifies the amount by which the signal will be attenuated (reduced in amplitude) if it falls below the level parameter. The level parameter is a threshold that determines whether the signal will be attenuated or not.

The noise_gate function first calculates the absolute value of the signal using the math.abs() function. This is done because the filtering only applies to the magnitude of the signal, not its sign (positive or negative value).

The function then checks if the absolute value of the signal is above the level threshold using an if statement. If it is, the signal is returned as is. If the absolute value of the signal is below the level threshold, the function calculates a value called soft_knee_ratio using the formula 1 - (level - abs_signal) / level. This value represents the amount by which the signal will be attenuated. The signal is then reduced in amplitude by this soft_knee_ratio and the resulting value is returned as the output of the function.

The noise_gate function applies the transformation symmetrically to both positive and negative values of the signal parameter. This is because the transformation only depends on the absolute value of the signal, not its sign. The transformation first calculates the absolute value of the signal using the math.abs() function and then applies the filtering based on the magnitude of the signal. The sign of the signal is not taken into account in this process. As a result, the transformation is applied symmetrically to both positive and negative values of the signal.

The noise_gate function can be a valuable tool for anyone looking to filter out noise or unwanted variations from a signal. It is flexible and easy to use, and can be applied to a wide range of situations where signal noise reduction is needed. For example, it can be used to smooth out financial time series data or to remove background noise from an audio recording.

The noise_gate function in this code has been modified to include an additional input parameter called knee_type, which allows the user to specify whether to use a hard knee or a soft knee. A hard knee means that the compressor triggers simply at the threshold, whereas a soft knee means that the compressor triggers smoothly, gradually increasing the attenuation as the signal falls further below the threshold.

To use a hard knee, the user can set the knee_type parameter to "hard". To use a soft knee, the user can set the knee_type parameter to "soft". The default value for the knee_type parameter is "soft", so if the user does not specify a value for knee_type, the noise_gate function will use a soft knee by default.

The noise_gate function includes a check for the value of the knee_type parameter and applies the appropriate knee type. If the knee_type parameter is set to "hard", the function applies a hard knee by simply triggering at the threshold and dividing the input by the ratio if the signal falls below the threshold. If the knee_type parameter is set to "soft" (or if it is not specified and the default value is used), the function applies a soft knee by gradually increasing the attenuation of the signal as it falls further below the threshold.

The noise_gate function can be a valuable tool for anyone looking to filter out noise or unwanted variations from a signal. It is flexible and easy to use, and can be applied to a wide range of situations where signal noise reduction is needed. For example, it can be used to smooth out financial time series data or to remove background noise from an audio recording.

kNNLibrary "kNN"

Collection of experimental kNN functions. This is a work in progress, an improvement upon my original kNN script:

The script can be recreated with this library. Unlike the original script, that used multiple arrays, this has been reworked with the new Pine Script matrix features.

To make a kNN prediction, the following data should be supplied to the wrapper:

kNN : filter type. Right now either Binary or Percent . Binary works like in the original script: the system stores whether the price has increased (+1) or decreased (-1) since the previous knnStore event (called when either long or short condition is supplied). Percent works the same, but the values stored are the difference of prices in percents. That way larger differences in prices would give higher scores.

k : number k. This is how many nearest neighbors are to be selected (and summed up to get the result).

skew : kNN minimum difference. Normally, the prediction is done with a simple majority of the neighbor votes. If skew is given, then more than a simple majority is needed for a prediction. This also means that there are inputs for which no prediction would be given (if the majority votes are between -skew and +skew). Note that in Percent mode more profitable trades will have higher voting power.

depth : kNN matrix size limit. Originally, the whole available history of trades was used to make a prediction. This not only requires more computational power, but also neglects the fact that the market conditions are changing. This setting restricts the memory matrix to a finite number of past trades.

price : price series

long : long condition. True if the long conditions are met, but filters are not yet applied. For example, in my original script, trades are only made on crossings of fast and slow MAs. So, whenever it is possible to go long, this value is set true. False otherwise.

short : short condition. Same as long , but for short condition.

store : whether the inputs should be stored. Additional filters may be applied to prevent bad trades (for example, trend-based filters), so if you only need to consult kNN without storing the trade, this should be set to false.

feature1 : current value of feature 1. A feature in this case is some kind of data derived from the price. Different features may be used to analyse the price series. For example, oscillator values. Not all of them may be used for kNN prediction. As the current kNN implementation is 2-dimensional, only two features can be used.

feature2 : current value of feature 2.

The wrapper returns a tuple: [ longOK, shortOK ]. This is a pair of filters. When longOK is true, then kNN predicts a long trade may be taken. When shortOK is true, then kNN predicts a short trade may be taken. The kNN filters are returned whenever long or short conditions are met. The trade is supposed to happen when long or short conditions are met and when the kNN filter for the desired direction is true.

Exported functions :

knnStore(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are binary: up/down

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnStorePercent(knn, p1, p2, src, maxrows)

Store the previous trade; buffer the current one until results are in. Results are in percents

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

src : current price

maxrows : limit the matrix size to this number of rows (0 of no limit)

Returns: modified knn matrix

knnGet(distance, result)

Get neighbours by getting k results with the smallest distances

Parameters:

distance : distance array

result : result array

Returns: array slice of k results

knnDistance(knn, p1, p2)

Create a distance array from the two given parameters

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

Returns: distance array

knnSum(knn, p1, p2, k)

Make a prediction, finding k nearest neighbours and summing them up

Parameters:

knn : knn matrix

p1 : feature 1 value

p2 : feature 2 value

k : sum k nearest neighbors

Returns: sum of k nearest neighbors

doKNN(kNN, k, skew, depth, price, long, short, store, feature1, feature2)

execute kNN filter

Parameters:

kNN : filter type

k : number k

skew : kNN minimum difference

depth : kNN matrix size limit

price : series

long : long condition

short : short condition

store : store the supplied features (if false, only checks the results without storage)

feature1 : feature 1 value

feature2 : feature 2 value

Returns: filter output

Balgat EkibiBands are calculated with the std error and variance of the price actions. So if price cross up or cross down the variance bands, you could expect a reversal movement.

So if price cross up with the bands and after that there is a reversal candle movement, a short position could be taken.

If price cross down to the bands and after that there is a reversal candle movement, a long positon could be taken.

All risk management and money management is up to you.

X48 - Strategy | MA Type Cross + TPSL | Future&Spot | V.2Thank You For Open Source Code, This Strategy Ref. By 1.Simple Strategy Like MA Crossover For Long/Short or Spot Trade, 2. CDC Action Zone V.2 for BarPaint

This Strategy Mixing With MA Crossover Strategy and BarPaint By CDC Action Zone and TP/SL by Varbara

### How To Use Strategy : Setting EMA/SMA Crossover EMA/SMA, Any Value If You Want

For Long Position : Cross Up

For Short Position : Cross Down

Can Use With Spot Trade : Cross Up = Buy, Cross Down = Sell

TP/SL When Your OrderSize Change From any % Of Your TP/SL Value

### In Strategy Setting

Intitial Capital = Ex. 200

Order Size = Should Be Money Management Not Use 100% of Capital Ex. 10% of Capital (200$) = Order Size 20$

StopLoss and Take Profit = If You Run Trend TF 4H+ or 1D+ You Can Change TP% = 1,000% for nonlimit and Stop Loss 5 - 20% from your order size

Ex. Stoploss 15% = OrderSize / 100 x %SL = 20$/100 x 15% = 3$ Loss from order size 20$ (if you not set stop loss.)

Base Currency = (Your Currency) # Ex. USD

Commission = (Your Trading Fee) # Ex. Future Fee Can Check At Binance Fee Rate > www.binance.com > Choose Your Fee Type, Ex. USD M Future (Regular User) = 0.02 (Maker), 0.04 (Taker)

Commission Symbol Type = % # (Ref. By Binance Fee Rate)

### Notice ####

Default Setting It's Realistic From Normal Life Ex. Capital 200$ / Ordersize 20$ (10%)/ Commission 0.1% (Buy+Sell) / Slippage = 2 / TP = 1000% (nonlimit) / SL = 15%/OrderSize

Low Risk But High Return, Good Luck

### Bot Auto Trade by X4815162342 ###

if you wanna try my bot auto trade X48-3in1-bot : Contact My Line ID : x4815x

Full Command Alert For This Strategy If You Wanna See It's

'{"ex":"'+markettype+'","side": "'+longcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

'{"ex":"'+markettype+'","side": "'+shortcommand+'", "amount": "@{{strategy.order.contracts}}", "symbol": "{{ticker}}", "passphrase": "'+passphrase+'","leverage":"'+str.tostring(leveragex)+'"}'

But Easy Than Full Command Just Use Thisssssss !! Strategy Be Manage Auto Long and Short or TPSL Position

You Don't Do Anything Just Use This Message to Alerts Message

{{strategy.order.alert_message}}

### If you don't use bot but just looking for strategy test ####

Just Pass Bot Setting Function It's Nothing Effect For Strategy !!!!!!

Let's Enjoy With Your Strategy BackTest 😁

Remember Beware Max drawdown%. I'm Recommend Lower Than 10% It's Very Good.

Joker Trailing TP BotTrailing Take Profit is used by the traders to increase their gains when the prices moves in a favorable direction. Let’s have a look at what is Trailing Take Profit and how it works.

What Is a Trailing Take Profit?

Trailing Take Profit is a term largely used in crypto, whereas you may encounter the term Trailing Stop in traditional trading describing almost the same thing, So what’s the difference between Trailing Take Profit and Trailing Stop? Trailing Stop is a type of Stop Loss automatically moving in the same direction as the asset’s price. Trailing Take Profit is nothing else than Trailing Stop activated after initial Take Profit is reached.

The main difference between these two is that Trailing Take Profit takes the profit in any case (altough it might be later annihilated by Trailing Stop). Thus, Trailing Take Profit reduces the risks that might’ve occurred using Trailing Stop alone. Trailing Take Profit is bound to the maximum of Take Profit price instead of just a price increase/decrease.

As you might notice, the terms Trailing Take Profit and Stop Loss are quite similar. To avoid confusion, in this article we will be talking about Trailing Take Profit as defined above.

Trailing Take Profit only moves in one direction. It is designed to lock in profit and limit losses. The trailing profit only moves up (in case of a long strategy) once the price has surpassed previous high and a new high has been established. If the trailing take profit moves up, it cannot move back down, thus securing the profit and preventing losses.

Trailing Take Profit allows the trade to remain open and continue to profit as long as the price is moving in the investor’s favor. If the price changes direction and the change surpasses the previously set percentage the order will be closed.

How Does it Work?

For example if you buy BTC at the price of 10000, if you set a Take Profit at 11000 and a Trailing Take Profit at 5% :

If the price goes up to 10500, nothing happens because the Take Profit at 11000 has not been reached.

Then if the BTC price goes up top 11000, a Stop Order at 10450 will be set.

Then if the BTC price goes down to 10500, the Stop Order stays at 104500.

Then if the BTC price goes up to 12000, the Stop Order moves to 11400.

Then if the BTC price goes down to 11000, the Stop Order at 11400 is executed.

You see that without Trailing Take Profit, the buy order would have been sold at 11000. Thus, a trader would miss an earning opportunity at 11400.

Divergence Macd+RSI Fast[RSU] -- No RepaintThis indicator combines the divergence of rsi and macd and displays it on the candlestick chart.

RSI:

1. When rsi is at a high point, once it falls by 1 k line, it will detect the divergence from the previous high point. This can quickly find the divergence that has taken effect and help you quickly capture the trend before a sharp decline or rise.

The difference between other RSI divergence indicators: the official divergence indicator is to detect the 5 and the k line, which may lead to a large amount of decline.

2. This indicator detects the previous high and the previous low of 5, 10, 20 lengths at the same time, instead of only detecting a fixed length, so that more deviations can be found.

MACD:

1. When MACD-diff line(orange color) is at a high point, once it falls by 1 k line, it will detect the divergence from the previous high point. This can quickly find the divergence that has taken effect and help you quickly capture the trend before a sharp decline or rise.

2. This indicator detects the previous high and the previous low of 5, 10, 20, 40 , 60 lengths at the same time, instead of only detecting a fixed length, so that more divergences can be found.

Notice:

Because it is a quick divergence detection, it is recommended to confirm that the divergence takes effect after the current k is completely closed first. I have identified this state in the indicator as "k not end".

Disadvantages and Risks:

Since it is a quick discovery, there will be error identification. Error divergences will recolor to grey.

Suggestion:

Use Alert catching divergence occurrences.

Please do not:

Don't go short in the uptrend, don't go long in the downtrend.

Top divergences that occur because of a strong uptrend are usually only temporary pullbacks. Bottom divergences in persistent declines are also temporary rallies. Do not attempt to trade such low-return trades.

It is recommended to use the divergence indicator when the stock price has made a new high and retraced, and once again made a new high, because this often leads to the end of the trend.

Divergence how to use:

1. After the previous candlestick was completely closed, a bottom divergence was found.

2. Open an long order at the beginning of the second bar, or as close to the bottom as possible (because the stop loss will be smaller).

3. Break the stop loss price below the previous low where the divergence occurred, which already means that the divergence is wrong.

Villa Dinamic Pivot Supertrend StrategyThis strategy works better on AUD/USD in the 15 min timeframe. It uses the Pivot Supertrend to enter trades based on different filters such as:

- Simple EMA filter: that the 3 EMAs should be in order

- DEMA angle: you can choose the DEMA Angle threshold and the look back to check the angle to just trade trades with DEMA at a certain angle

- Simple DEMA filter: just check if close is above or below DEMA

- Take Every Supertrend Signal: this means to take every normal supertrend signal to not just wait for a pivot supertrend signal to enter a trade (specially on long pivot supertrend periods)

- Stop Loss at Supertrend: this means that the stop loss will be at the Normal Supertrend, if false the stop loss will be placed at the ATR level selected.

- 2 Steps Take Profit: this means if you want to close a percentage of position as soon as the normal supertrend crosses the entry price, you can select the % on the "2 Steps TP qty" input

- Stop Loss ATR Multiplier: if Stop Loss at Supertrend is off this will be the stoploss based on the atr

- Take Profit ATR Multiplier: if Stop Loss at Supertrend is off this will be the takeprofit based on the atr (you have to keep in mind that the ratio between this two will make the Risk to reward ratio of the take profit when the Stop Loss at Supertrend)

- Testing: to avoid overfitting, you can select date ranges for backtesting and forwardtesting and select which testing you wanna do

Measure Volume, Momentum, Trend, VolatilityThis script displays the following indicators in one pane to quickly determine several important factors regarding price action. It allows the user to quickly see all of most important factors surrounding price action in one pane with one quick glance. This should be incredibly helpful and allow things like double divergence and trend confirmation to be spotted much more quickly. I personally use the data in this indicator to replace four separate indicators and it has brought my win rate and profit factor significantly higher. I hadn't seen any place where all of the best J. Welles Wilder indicators such as RSI, Parabolic SAR, and DMI/ADX were brought into one easy to use interface. This is my attempt at fixing that gap. For a much deeper understanding of how to use these indicators, I recommend reading New Concepts in Technical Trading Systems written by J. Welles Wilder.

Momentum via RSI (Relative Strength Index)

Volume via MFI (Money Flow Index)

Volatility via DMI/ADX (Direction Movement Index/Average Directional Index)

Trend via Parabolic SAR (Parabolic Stop and Reverse)

It is worth noting that DMI/ADX and Parabolic SAR can both help determine trend strength and volatility.

The Volatility mechanism is measured by DMI and ADX and displayed at the top of the pane using circles. The top, tiny circles reflect if show if positive DI or negative DI has a higher value. The small circles directly underneath indicate whether or not the ADX is above 20 (configurable, some may choose to increase this to 25 or even 30).

The Momentum mechanism is shown as standard RSI with the default being a white line and default period of 14, which is all configurable.

The Volume mechanism is shown as standard MFI with the default being a fuchsia line and default period of 14, which is also configurable.

The momentum and volume oscillators should be used in conjunction to help spot whether the trend is strong or weak using divergences and the middle, overbought, and oversold levels. These levels are also configurable.

The Trend mechanism is measured by Parabolic SAR and displayed at the bottom of the pane using diamonds. The default is red diamonds when in a bear trend, green when in an uptrend which is configurable. When price is above the Parabolic SAR, it is considered to be an uptrend. When price is below the Parabolic SAR, it is considered to be a downtrend. The way price is measured is also configurable (i.e. open, close, ohlc4, hlc3, etc.). When price crossed above or below the Parabolic SAR, the diamonds will change colors.

All the indicators displayed should be used in a well rounded strategy. For instance, I only trade when ADX is above 20 and rarely trade against the trend shown via PSAR. When trend shifts and divergences helped indicate a trend shift would occur using the RSI and MFI, it can be a great spot to take an entry. RSI/MFI can also confirm the trend is strong when they are not showing divergences and inline with price action. All of this data should be used in conjunction with good fundamental data and technical levels. Divergences with RSI and MFI on double tops or bottoms can also be incredibly powerful. There is no right or wrong way to use all the data displayed in this indicator, however using all four pillars of trading (Momentum, Volume, Trend, Volatility) will help ensure only the best trades are taken.

VIX SPX & XJOVix is a volatility indicator that lets traders know when to be cautious.

This indicator shows the volatility for the US market as well as the Australian market on seperate lines.

Blue lines are Vix for SPX (S&P 500)

If blue indicator goes above 30, high volatility is present and caution should be taken.

Green lines are Vix for XJO (ASX 200)

If green indicator goes above 20, high volatility is present and caution should be taken.

Swing Trades Validator - The One TraderThis swing trading strategy validator is built on the original strategy taught in my bootcamp for swing traders.

The strategy is simple and follows a trend trading pattern on prices reacting to Exponential Moving Averages over a multiple time-frame analysis.

The details of the strategy are as follows:

- Holding Period : Upto a couple of months

- Time-frames to be analysed : Month - Week - Day

- Trade Execution : Daily Time-frame

Analysis Details:

Step 1 : On the Monthly time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the month.

Step 2 : The price needs to be above the 8ema on the Monthly time-frame.

Step 3 : The 8ema must be above the 20ema on the Monthly time-frame.

The above steps indicate a bullish strength in the instrument on the Monthly time-frame.

Step 4 : On the Weekly time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the week.

Step 5 : The price needs to be above the 8ema on the Weekly time-frame.

Step 6 : The 8ema must be above the 20ema on the Weekly time-frame.

The above steps indicate a bullish strength in the instrument on the Weekly time-frame.

Step 7 : On the Daily time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the day.

Step 8 : The price needs to be above the 8ema on the Daily time-frame.

Step 9 : The 8ema must be above the 20ema on the Daily time-frame.

The above steps indicate a bullish strength in the instrument on the Daily time-frame.

Step 10 : While the 8ema is above the 20ema on the Daily time-frame, the price must be allowed to rise before a pullback is seen towards the moving averages, indicating a bearish move trying to change the trend.

Step 11 : These pullback candles need to form a pattern called the Ring Low with the second pullback candle having a lower high and lower low and the low of the last pullback candle being lesser than or equal to the fat ema on the Daily time-frame.

Step 12 : If the stock is still bullish and the trend is displaying a strength in the underlying bullish direction, then there will be a resumption candle that will have a closing price higher than the previous day's high price.

This trend continuation signal is a confirmation that the instrument will continue in the underlying trend direction and we will be able to enter if this condition is satisfied.

The profit and loss percentages are set at a default 10% as this can be a minimum risk : reward for swing trades on average, but the inputs have been made available to the users in order to adjust the risk : reward to find the most optimum breathing room for each individual stock or instrument. This will give the user a highly custom overview of the strategy on individual instruments based on their volatility and price movements.

The strategy tester will auto back-test this strategy historically and find all the trades that were taken based on this strategy and populate a performance summary.

The most important data in V1.0 of this script are as follows:

1. No. of Trades Taken : We want to see many trades being taken on this strategy in that particular instrument. This shows us a healthy report on the number of winning vs. losing trades.

2. Percentage Profitable : We want to see that this strategy has worked out in the past and is giving us a high probability of return. This in no way an indication that the strategy will definitely work out in the future as well, but gives us an idea of whether or not we should enter this trade.

3. No. of Winning Trades vs. Losing Trades : We would like to see a significantly higher number of winning trades.

4. Avg. # of bars in a trade : This gives us an idea of how long on average we might have to wait to see the results of this strategy either in favor of our reward or against our desired direction. Some trades can be completed in around 15-20 bars on average and some trades have shown to take upto 45 days to reach desired reward. This is in line with our planned holding period, but gives the trader a sense of time and increased level of patience.

The future updates will have more utility of the various elements of the strategy tester and the entire exit strategy will be integrated into the script.

This script is not to be used as a standalone method and must be studied well in order to execute trades. I have not hidden visibility on other time-frames, but since order execution is done on the Daily time-frame, the script must run on the Daily time-frame only.

There are many other factors to be taken into consideration before entering a trade and proper risk management and position sizing rules must be followed.

Our bootcamp participants will use this strategy tester in conjunction with the invite-only Trading Toolkit assigned to them.

The development of this script will be ongoing and all comments and feedback are welcome.

Supertrend + Stoch StrategyA strategy using ema , supertrend and stochastic .

Long entry conditions:

1. EMA 25 > EMA 50 and EMA 100 > EMA 100.

2. Supertrend indicator is green.

3. Stochastic k line cross over d line.

Long stop: the lowest price of the last k

Ichimoku Kinko Hyo [DM]Ichimoku Kinko Hyo PineV5

Definition

The Ichimoku Cloud is a package of multiple technical indicators that signal support, resistance, market trend, and market momentum. It is one of the few indicators out there that attempts to convey a number of meaningful insights into one. For that reason it can be hard to understand at first glance, but is commonly used among professional traders and market participants.

History

In the late 1960s, Goichi Hosada introduced the Ichimoku Cloud. It took several years for its adoption and understanding to take off, but today it is commonly known and used as an indicator in the field of technical analysis.

Calculations

The Ichimoku Cloud can be calculated in several different ways. It depends on your timeframe, needs, and expertise in technical analysis.

Takeaways

The Cloud is an integral part of the technical indicator as a whole and helps traders and investors identify the specific calculations made to the chart. Price below the cloud indicates a downward trend, whereas price above the cloud indicates an uptrend. These trend signals can strengthen if both the cloud and the price are moving in the same direction. Similarly, the signals can weaken if the cloud is moving in the opposite direction.

What to look for

By using various averages, the Ichimoku Cloud indicator gives traders and investors key and extensive data information. Trends are high when price is above the cloud, weak when price is below the cloud, or transitioning when price is seen inside the cloud.

As was mentioned in the Calculation section above, when Leading Span A falls below Leading Span B, we can confirm a downtrend. The cloud, in this case, displays a red hue. When Leading Span A is above Leading Span B, we can confirm an uptrend. The cloud, in this case, displays a green hue.

The Ichimoku cloud can be used with other technical indicators in order to better assess risk. By looking at larger trends, with the help of multiple indicators, traders are able to see how smaller trends can fit within the general market picture as a whole.

Limitations

With all of the lines and cloud shading and data points, the chart can look a little crowded and stuffy. In order to work through this, there’s software that can hide these lines so the chart looks cleaner for traders and all the information you’d like to see is at the forefront of the chart. At TradingView, we have special features available for all our users. Anyone using our platform can pick which lines and backgrounds they’d like shown and can also customize the color, line thickness, and opacity with a simple click.

more info: ichimoku.org

MACD AdvancedHello traders!

As you know, MACD is one of the oldest and the most popular indicators for trading. It seems to be a «Hello world indicator» of most technical analysis beginners. It’s easy to interpret and rather useful for many styles of trading. There are many arguments about its accuracy but in my opinion, this indicator can show very good results. However, you should squeeze every drop of its opportunities and we'll help you with it. We invented this script to make the lives of both professionals and freshmen easier.

Our new indicator uses all the opportunities that MACD gives. It takes into consideration divergencies, crossovers, the MACD, and signal line location. It seems to be rather difficult to take into consideration all MACD signals when you don’t use algorithmic trading, but it’ll be trivial using our script. We have integrated some innovations that’ll make traders’ staff easier. As you know, the crossover is considered to be a false signal in conjunction with hidden divergence which predicts another movement. Thus, we catch all types of divergencies and if it’s hidden of another «value» we skip it. However, if there's a crossover with bullish divergence or cross under with bearish, the signal seems to be strong and accurate. In this case, divergence is playing for us and makes the point of entrance more trustable. Our script takes into consideration this case and the innovative divergence chaser doesn’t give any mistakes. Moreover, if crossover takes place above zero line and crosses under bellow it, these signals are considered to be false too. It’s a trivial task comparing with the previous, thus it’s extremely simple for our script. We called it MACD Advanced cause it uses all the power of MACD with the power of invasive divergence chasers. The usage of it is trivial. Just add it to the chart, tune the parameters like MACD and tune the divergence chaser and get very accurate signals. We decided not to draw the bars to make signals more visible. It seems to be very nice!

I hope guys you'll enjoy it and it'll become a part of your trading staff.

EMA pullback strategyA solid EMA pullback strategy for cryptos 15 min chart that uses EMA crossing as signal and pullback as stop loss.

EMA1: shortest period for finding crossing (I find period = 33 profitable for BTCUSD, you can adjust it for other cryptos)

EMA2: 5x period of EMA1, for filtering out some trend reversals

EMA3: 11x period of EMA1, for determining trend direction

Rules are:

Long:

close price > EMA3

EMA1 > EMA3

close price pullbacks below EMA1 and then crosses up EMA1, enter at the first close price above EMA1

lowest pullback close price < EMA2 at the cross up

Short:

close price < EMA3

EMA1 < EMA3

close price pullbacks above EMA1 and then crosses down EMA1, enter at the first close price below EMA1

highest pullback close price > EMA2 at the cross down

Stop-loss at lowest/highest pullback price for long/short

Take profit = 2x stop-loss

Risk management: risk range can be set in the inspector. If the risk is lower than the range, the trade is not taken. if the risk is higher than the range, the position size is adjusted to keep the risk within range.

BTC VIP EMA CROSS Buy/Sell (GC & DC)EMA cross 5&10 standard-setting with add on of BUY/SELL signal ( GC & DC) which will make the traders have an indication of buy and sell easily and clearly.

An exponential moving average strategy, or EMA strategy, is used to identify the predominant trend in the market. It can also provide the support and resistance level to execute your trade. Indicators: v4 (default setting), EMA 5 10 Crossover (default setting)

Preferred Time Frame(s):15-Minute, 30-Minute, 1-Hour, 4-Hour, 1-Day

Strategy

Long Entry Rules

Enter a buy in the market if the following indicator or chart pattern takes center stage:

If the blue upward pointing arrow of the EMA 5 10 Crossover custom indicator gets aligned just somewhat below the candlesticks as seen in Fig. 1.0, the market sentiment is said to be bullish, hence a trigger to go long on the pair of interest.

If the light blue line of the custom indicator gets outlined just below price bars as illustrated in Fig. 1.0, price is said to be pushed somewhat higher i.e. a trigger to buy the asset of focus.

Exit Strategy/Take Profit for Buy Entry

Exit or take profit if the following rules or conditions takes precedence:

If the red downward pointing arrow of the EMA 5 10 Crossover custom indicator forms above price bars as depicted in Fig. 1.0 while a buy signal is ongoing in the market, a possible price dip is said to be looming, as such an exit or take profit is advised.

If the red line of the custom indicator forms above the candlestick during a bullish trend, it is a pointer to a possible price dip, hence an exit or take profit is advised.

SMT - Smart Money Thursday Boxes

The Smart Money Trading Thursday - is a very specific trading system. You only trade it on a Thursday.

The script/indicator will color Thursdays as two boxes. If you just want one color, use same color for

both boxes. The boxes is there to indicate London/New York sessions.

SETTINGS

In the setting you find a numeric value as 1700-0400:5

The "5" indicate Thursday. You can change that if you prefer to color another specific day.

For example "4" would indicate Wednesday. And you can change the hours to fit your

sessions and trading style.

You can also use the 2 boxes on different days. If you for example would like to color up

London for Wednesday and Thursday. Then set hours to fit London session and adjust the

:5 to 4 on the 1st box and 5 on the 2nd.

HOW TO USE IT?

The Smart Money works in a way retail trading does not. Smart Money has an objective

to locate retail patterns, where there will be a lot of stop loss volume to be grabbed.

So when a retail trader see a setup like a "Double Top / Bottom". The Institutional

will see $$$ of dumb money, ready to be taken. The best moves happen on a Thursday

but if you are a skilled trader, you can see the move also occur on Wednesday or Friday.

The first thing that will happen, is that the Smart Money Breaks out of session. Meaning

they will leave the current weeks high/low range. To start collect negative contracts

of the retail volume.

When you see that happen. And you see a breakout that consist of 4 in a row 1 hour

chart candles. Then you have your first rule meet.

#1 Thursday breakout of current weeks high/low. And the move is a clean 4 hour move

as 4x H1 candles. The move can start within range. But must end clearly outside.

Visual Example:

#2 Next, we await an engulf at peak or near peak. That is where Institutional

may have problem to match any more contracts, and since they used their own

money to make this move. They must now mitigate orders, and return back to

the original retail pattern as most retail traders are now stopped out.

(Normally this is a long/clear candle out of range. they rarely go lower

then retail traders entry in the 1st push. This to not save any souls :)

#3 Price returns back to where the breakout from the retail happens.

You can now take your profit as a Smart Money Trader. Trading with less risk,

you can take profit of the return of that latest 4x H1 candle move. (Order

Block)

CONCLUSION

The best trade is when you can combine a retail pattern, followed by a

breakout which holds 4x 1 hour candles in the outbreak direction.

2nd best is when you have the 4x H1 breakout and really no clear retail

pattern. Still is the same game. Just not as clear as the one above.

Study the steps in this image and you see what to look after:

Good Luck with your trading!

Regards,

The Hunter Trading Group

CCI Strategy v2This was a strategy I found based on MT4. It takes CCI readings, then transforms them into a weighted moving average illustration. This is represented as:

Red Line - A six period moving average taken from CCI (NOT PRICE)

Green Line - A sixty-six period moving average taken from CCI (NOT PRICE)

Blue Line - CCI plotted

I have also added some levels and bollinger bands to highlight changes in activity.

The strategy is:

BUY - When the red line crosses upwards over green line.

SELL - When the red line crosses downwards over green line.

Extra confirmation is available by watching the blue line, it should be above red to buy, below red to sell. If the blue line drops in the opposite direction, this may be an opportunity to buy on a pull back.

If you wish for any modications to be applied, please do not hesitate to contact me.

Delta Volume Columns Pro [LucF]█ OVERVIEW

This indicator displays volume delta information calculated with intrabar inspection on historical bars, and feed updates when running in realtime. It is designed to run in a pane and can display either stacked buy/sell volume columns or a signal line which can be calculated and displayed in many different ways.

Five different models are offered to reveal different characteristics of the calculated volume delta information. Many options are offered to visualize the calculations, giving you much leeway in morphing the indicator's visuals to suit your needs. If you value delta volume information, I hope you will find the time required to master Delta Volume Columns Pro well worth the investment. I am confident that if you combine a proper understanding of the indicator's information with an intimate knowledge of the volume idiosyncrasies on the markets you trade, you can extract useful market intelligence using this tool.

█ WARNINGS

1. The indicator only works on markets where volume information is available,

Please validate that your symbol's feed carries volume information before asking me why the indicator doesn't plot values.

2. When you refresh your chart or re-execute the script on the chart, the indicator will repaint because elapsed realtime bars will then recalculate as historical bars.

3. Because the indicator uses different modes of calculation on historical and realtime bars, it's critical that you understand the differences between them. Details are provided further down.

4. Calculations using intrabar inspection on historical bars can only be done from some chart timeframes. See further down for a list of supported timeframes.

If the chart's timeframe is not supported, no historical volume delta will display.

█ CONCEPTS

Chart bars

Three different types of bars are used in charts:

1. Historical bars are bars that have already closed when the script executes on them.

2. The realtime bar is the current, incomplete bar where a script is running on an open market. There is only one active realtime bar on your chart at any given time.

The realtime bar is where alerts trigger.

3. Elapsed realtime bars are bars that were calculated when they were realtime bars but have since closed.

When a script re-executes on a chart because the browser tab is refreshed or some of its inputs are changed, elapsed realtime bars are recalculated as historical bars.

Why does this indicator use two modes of calculation?

Historical bars on TradingView charts contain OHLCV data only, which is insufficient to calculate volume delta on them with any level of precision. To mine more detailed information from those bars we look at intrabars , i.e., bars from a smaller timeframe (we call it the intrabar timeframe ) that are contained in one chart bar. If your chart Is running at 1D on a 24x7 market for example, most 1D chart bars will contain 24 underlying 1H bars in their dilation. On historical bars, this indicator looks at those intrabars to amass volume delta information. If the intrabar is up, its volume goes in the Buy bin, and inversely for the Sell bin. When price does not move on an intrabar, the polarity of the last known movement is used to determine in which bin its volume goes.

In realtime, we have access to price and volume change for each update of the chart. Because a 1D chart bar can be updated tens of thousands of times during the day, volume delta calculations on those updates is much more precise. This precision, however, comes at a price:

— The script must be running on the chart for it to keep calculating in realtime.

— If you refresh your chart you will lose all accumulated realtime calculations on elapsed realtime bars, and the realtime bar.

Elapsed realtime bars will recalculate as historical bars, i.e., using intrabar inspection, and the realtime bar's calculations will reset.

When the script recalculates elapsed realtime bars as historical bars, the values on those bars will change, which means the script repaints in those conditions.

— When the indicator first calculates on a chart containing an incomplete realtime bar, it will count ALL the existing volume on the bar as Buy or Sell volume,

depending on the polarity of the bar at that point. This will skew calculations for that first bar. Scripts have no access to the history of a realtime bar's previous updates,

and intrabar inspection cannot be used on realtime bars, so this is the only to go about this.

— Even if alerts only trigger upon confirmation of their conditions after the realtime bar closes, they are repainting alerts

because they would perhaps not have calculated the same way using intrabar inspection.

— On markets like stocks that often have different EOD and intraday feeds and volume information,

the volume's scale may not be the same for the realtime bar if your chart is at 1D, for example,

and the indicator is using an intraday timeframe to calculate on historical bars.

— Any chart timeframe can be used in realtime mode, but plots that include moving averages in their calculations may require many elapsed realtime bars before they can calculate.

You might prefer drastically reducing the periods of the moving averages, or using the volume columns mode, which displays instant values, instead of the line.

Volume Delta Balances

This indicator uses a variety of methods to evaluate five volume delta balances and derive other values from those balances. The five balances are:

1 — On Bar Balance : This is the only balance using instant values; it is simply the subtraction of the Sell volume from the Buy volume on the bar.

2 — Average Balance : Calculates a distinct EMA for both the Buy and Sell volumes, and subtracts the Sell EMA from the Buy EMA.

3 — Momentum Balance : Starts by calculating, separately for both Buy and Sell volumes, the difference between the same EMAs used in "Average Balance" and

an SMA of double the period used for the "Average Balance" EMAs. The difference for the Sell side is subtracted from the difference for the Buy side,

and an RSI of that value is calculated and brought over the −50/+50 scale.

4 — Relative Balance : The reference values used in the calculation are the Buy and Sell EMAs used in the "Average Balance".

From those, we calculate two intermediate values using how much the instant Buy and Sell volumes on the bar exceed their respective EMA — but with a twist.

If the bar's Buy volume does not exceed the EMA of Buy volume, a zero value is used. The same goes for the Sell volume with the EMA of Sell volume.

Once we have our two intermediate values for the Buy and Sell volumes exceeding their respective MA, we subtract them. The final "Relative Balance" value is an ALMA of that subtraction.

The rationale behind using zero values when the bar's Buy/Sell volume does not exceed its EMA is to only take into account the more significant volume.

If both instant volume values exceed their MA, then the difference between the two is the signal's value.

The signal is called "relative" because the intermediate values are the difference between the instant Buy/Sell volumes and their respective MA.

This balance flatlines when the bar's Buy/Sell volumes do not exceed their EMAs, which makes it useful to spot areas where trader interest dwindles, such as consolidations.

The smaller the period of the final value's ALMA, the more easily you will see the balance flatline. These flat zones should be considered no-trade zones.

5 — Percent Balance : This balance is the ALMA of the ratio of the "On Bar Balance" value, i.e., the volume delta balance on the bar (which can be positive or negative),

over the total volume for that bar.

From the balances and marker conditions, two more values are calculated:

1 — Marker Bias : It sums the up/down (+1/‒1) occurrences of the markers 1 to 4 over a period you define, so it ranges from −4 to +4, times the period.

Its calculation will depend on the modes used to calculate markers 3 and 4.

2 — Combined Balances : This is the sum of the bull/bear (+1/−1) states of each of the five balances, so it ranges from −5 to +5.

█ FEATURES

The indicator has two main modes of operation: Columns and Line .

Columns

• In Columns mode you can display stacked Buy/Sell volume columns.

• The buy section always appears above the centerline, the sell section below.

• The top and bottom sections can be colored independently using eight different methods.

• The EMAs of the Buy/Sell values can be displayed (these are the same EMAs used to calculate the "Average Balance").

Line

• Displays one of seven signals: the five balances or one of two complementary values, i.e., the "Marker Bias" or the "Combined Balances".

• You can color the line and its fill using independent calculation modes to pack more information in the display.

You can thus appraise the state of 3 different values using the line itself, its color and the color of its fill.

• A "Divergence Levels" feature will use the line to automatically draw expanding levels on divergence events.

Default settings

Using the indicator's default settings, this is the information displayed:

• The line is calculated on the "Average Balance".

• The line's color is determined by the bull/bear state of the "Percent Balance".

• The line's fill gradient is determined by the advances/declines of the "Momentum Balance".

• The orange divergence dots are calculated using discrepancies between the polarity of the "On Bar Balance" and the chart's bar.

• The divergence levels are determined using the line's level when a divergence occurs.

• The background's fill gradient is calculated on advances/declines of the "Marker Bias".

• The chart bars are colored using advances/declines of the "Relative Balance". Divergences are shown in orange.

• The intrabar timeframe is automatically determined from the chart's timeframe so that a minimum of 50 intrabars are used to calculate volume delta on historical bars.

Alerts

The configuration of the marker conditions explained further is what determines the conditions that will trigger alerts created from this script. Note that simply selecting the display of markers does not create alerts. To create an alert on this script, you must use ALT-A from the chart. You can create multiple alerts triggering on different conditions from this same script; simply configure the markers so they define the trigger conditions for each alert before creating the alert. The configuration of the script's inputs is saved with the alert, so from then on you can change them without affecting the alert. Alert messages will mention the marker(s) that triggered the specific alert event. Keep in mind, when creating alerts on small chart timeframes, that discrepancies between alert triggers and markers displayed on your chart are to be expected. This is because the alert and your chart are running two distinct instances of the indicator on different servers and different feeds. Also keep in mind that while alerts only trigger on confirmed conditions, they are calculated using realtime calculation mode, which entails that if you refresh your chart and elapsed realtime bars recalculate as historical bars using intrabar inspection, markers will not appear in the same places they appeared in realtime. So it's important to understand that even though the alert conditions are confirmed when they trigger, these alerts will repaint.

Let's go through the sections of the script's inputs.

Columns

The size of the Buy/Sell columns always represents their respective importance on the bar, but the coloring mode for tops and bottoms is independent. The default setup uses a standard coloring mode where the Buy/Sell columns are always in the bull/bear color with a higher intensity for the winning side. Seven other coloring modes allow you to pack more information in the columns. When choosing to color the top columns using a bull/bear gradient on "Average Balance", for example, you will have bull/bear colored tops. In order for the color of the bottom columns to continue to show the instant bar balance, you can then choose the "On Bar Balance — Dual Solid Colors" coloring mode to make those bars the color of the winning side for that bar. You can display the averages of the Buy and Sell columns. If you do, its coloring is controlled through the "Line" and "Line fill" sections below.

Line and Line fill

You can select the calculation mode and the thickness of the line, and independent calculations to determine the line's color and fill.

Zero Line

The zero line can display dots when all five balances are bull/bear.

Divergences

You first select the detection mode. Divergences occur whenever the up/down direction of the signal does not match the up/down polarity of the bar. Divergences are used in three components of the indicator's visuals: the orange dot, colored chart bars, and to calculate the divergence levels on the line. The divergence levels are dynamic levels that automatically build from the line's values on divergence events. On consecutive divergences, the levels will expand, creating a channel. This implementation of the divergence levels corresponds to my view that divergences indicate anomalies, hesitations, points of uncertainty if you will. It precludes any attempt to identify a directional bias to divergences. Accordingly, the levels merely take note of divergence events and mark those points in time with levels. Traders then have a reference point from which they can evaluate further movement. The bull/bear/neutral colors used to plot the levels are also congruent with this view in that they are determined by the line's position relative to the levels, which is how I think divergences can be put to the most effective use. One of the coloring modes for the line's fill uses advances/declines in the line after divergence events.

Background

The background can show a bull/bear gradient on six different calculations. As with other gradients, you can adjust its brightness to make its importance proportional to how you use it in your analysis.

Chart bars

Chart bars can be colored using seven different methods. You have the option of emptying the body of bars where volume does not increase, as does my TLD indicator, and you can choose whether you want to show divergences.

Intrabar Timeframe

This is the intrabar timeframe that will be used to calculate volume delta using intrabar inspection on historical bars. You can choose between four modes. The three "Auto-steps" modes calculate, from the chart's timeframe, the intrabar timeframe where the said number of intrabars will make up the dilation of chart bars. Adjustments are made for non-24x7 markets. "Fixed" mode allows you to select the intrabar timeframe you want. Checking the "Show TF" box will display in the lower-right corner the intrabar timeframe used at any given moment. The proper selection of the intrabar timeframe is important. It must achieve maximal granularity to produce precise results while not unduly slowing down calculations, or worse, causing runtime errors. Note that historical depth will vary with the intrabar timeframe. The smaller the timeframe, the shallower historical plots you will be.

Markers

Markers appear when the required condition has been confirmed on a closed bar. The configuration of the markers when you create an alert is what determines when the alert will trigger. Five markers are available:

• Balances Agreement : All five balances are either bullish or bearish.

• Double Bumps : A double bump is two consecutive up/down bars with +/‒ volume delta, and rising Buy/Sell volume above its average.

• Divergence confirmations : A divergence is confirmed up/down when the chosen balance is up/down on the previous bar when that bar was down/up, and this bar is up/down.

• Balance Shifts : These are bull/bear transitions of the selected signal.

• Marker Bias Shifts : Marker bias shifts occur when it crosses into bull/bear territory.

Periods

Allows control over the periods of the different moving averages used to calculate the balances.

Volume Discrepancies

Stock exchanges do not report the same volume for intraday and daily (or higher) resolutions. Other variations in how volume information is reported can also occur in other markets, namely Forex, where volume irregularities can even occur between different intraday timeframes. This will cause discrepancies between the total volume on the bar at the chart's timeframe, and the total volume calculated by adding the volume of the intrabars in that bar's dilation. This does not necessarily invalidate the volume delta information calculated from intrabars, but it tells us that we are using partial volume data. A mechanism to detect chart vs intrabar timeframe volume discrepancies is provided. It allows you to define a threshold percentage above which the background will indicate a difference has been detected.

Other Settings

You can control here the display of the gray dot reminder on realtime bars, and the display of error messages if you are using a chart timeframe that is not greater than the fixed intrabar timeframe, when you use that mode. Disabling the message can be useful if you only use realtime mode at chart timeframes that do not support intrabar inspection.

█ RAMBLINGS

On Volume Delta

Volume is arguably the best complement to interpret price action, and I consider volume delta to be the most effective way of processing volume information. In periods of low-volatility price consolidations, volume will typically also be lower than normal, but slight imbalances in the trend of the buy/sell volume balance can sometimes help put early odds on the direction of the break from consolidation. Additionally, the progression of the volume imbalance can help determine the proximity of the breakout. I also find volume delta and the number of divergences very useful to evaluate the strength of trends. In trends, I am looking for "slow and steady", i.e., relatively low volatility and pauses where price action doesn't look like world affairs are being reassessed. In my personal mythology, this type of trend is often more resilient than high-volatility breakouts, especially when volume balance confirms the general agreement of traders signaled by the low-volatility usually accompanying this type of trend. The volume action on pauses will often help me decide between aggressively taking profits, tightening a stop or going for a longer-term movement. As for reversals, they generally occur in high-volatility areas where entering trades is more expensive and riskier. While the identification of counter-trend reversals fascinates many traders to no end, they represent poor opportunities in my view. Volume imbalances often precede reversals, but I prefer to use volume delta information to identify the areas following reversals where I can confirm them and make relatively low-cost entries with better odds.

On "Buy/Sell" Volume

Buying or selling volume are misnomers, as every unit of volume transacted is both bought and sold by two different traders. While this does not keep me from using the terms, there is no such thing as “buy only” or “sell only” volume. Trader lingo is riddled with peculiarities.

Divergences