Multi-Timeframe High Low (@JP7FX)Multi-Timeframe High Low Levels (@JP7FX)

This Price Action indicator displays high and low levels from a selected timeframe on your current chart.

These levels COULD represent areas of potential liquidity, providing key price points where traders can target entries, reversals, or continuation trades.

Key Features:

Display high and low levels from a selected timeframe.

Customize line width, colors for high and low levels, and label text color.

Enable or disable the display of high levels, low levels, and labels.

Receive alerts when the price takes out high or low levels.

How to use:

It is important to note that using this indicator on it's own is not advisable. Instead, it should be combined with other tools and analysis for a more comprehensive trading strategy.

Possibly look to use my MTF Supply and Demand Indicator to look for zones to trade from at these levels?

If the price breaks above a high level, you might consider entering a long position, with the expectation that the price will continue to rise. Conversely, if the price breaks below a low level, you may think about entering a short position, anticipating further downward movement.

On the other hand, you can also use high or low levels to look for reversal trades, as these areas can represent attractive liquidity zones.

By identifying these key price points, you could take advantage of potential market reversals and capitalise on new trading opportunities.

Always remember to use this indicator in conjunction with other technical analysis tools for the best results.

Additionally, you can enable alerts to notify you when the price takes out high or low levels, helping you stay informed about significant price movements.

This indicator could be a valuable tool for traders looking to identify key price points for potential trading opportunities.

As always with the markets, Trade Safe :)

Cerca negli script per "TAKE"

The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)The Flash-Strategy (Momentum-RSI, EMA-crossover, ATR)

Are you tired of manually analyzing charts and trying to find profitable trading opportunities? Look no further! Our algorithmic trading strategy, "Flash," is here to simplify your trading process and maximize your profits.

Flash is an advanced trading algorithm that combines three powerful indicators to generate highly selective and accurate trading signals. The Momentum-RSI, Super-Trend Analysis and EMA-Strategy indicators are used to identify the strength and direction of the underlying trend.

The Momentum-RSI signals the strength of the trend and only generates trading signals in confirmed upward or downward trends. The Super-Trend Analysis confirms the trend direction and generates signals when the price breaks through the super-trend line. The EMA-Strategy is used as a qualifier for the generation of trading signals, where buy signals are generated when the EMA crosses relevant trend lines.

Flash is highly selective, as it only generates trading signals when all three indicators align. This ensures that only the highest probability trades are taken, resulting in maximum profits.

Our trading strategy also comes with two profit management options. Option 1 uses the so-called supertrend-indicator which uses the dynamic ATR as a key input, while option 2 applies pre-defined, fixed SL and TP levels.

The settings for each indicator can be customized, allowing you to adjust the length, limit value, factor, and source value to suit your preferences. You can also set the time period in which you want to run the backtest and how many dollar trades you want to open in each position for fully automated trading.

Choose your preferred trade direction and stop-loss/take-profit settings, and let Flash do the rest. Say goodbye to manual chart analysis and hello to consistent profits with Flash. Try it now!

General Comments

This Flash Strategy has been developed in cooperation between Baby_whale_to_moon and JS-TechTrading. Cudos to Baby_whale_to_moon for doing a great job in transforming sophisticated trading ideas into pine scripts.

Detailed Description

The “Flash” script considers the following indicators for the generation of trading signals:

1. Momentum-RSI

2. ‘Super-Trend’-Analysis

3. EMA-Strategy

1. Momentum-RSI

• This indicator signals the strength of the underlying upward- or downward-trend.

• The signal range of this indicator is from 0 to 100. Values > 60 indicate a confirmed upward- or downward-trend.

• The strategy will only generate trading signals in case the stock (or any other financial security) is in a confirmed upward- (long entry signals) or downward-trend (short entry signals).

• This indicator provides information with regards to the strength of the underlying trend and it does not give any insight with regard to the direction of the trend. Therefore, this strategy also considers other indicators which provide technical confirmation with regards to the direction of the underlying trend.

Graph 1 shows this concept:

• The Momentum-RSI indicator gives lower readings during consolidation phases and no trading signals are generated during these periods.

Example (graph 2):

2. Super-Trend Analysis

• The red line in the graph below represents the so-called super-trend-line. Trading signals are only generated in case the price action breaks through this super-trend-line indicating a new confirmed upward-trend (or downward-trend, respectively).

• If that happens, the super trend-line changes its color from red to green, giving confirmation that the trend changed from bearish to bullish and long-entries can be considered.

• The vice-versa approach can be considered for short entries.

Graph 3 explains this concept:

3. Exponential Moving Average / EMA-Strategy

The functionality of this EMA-element of the strategy has been programmed as follows:

• The exponential moving average and two other trend lines are being used as qualifiers for the generation of trading-signals.

• Buy-signals for long-entries are only considered in case the EMA (yellow line in the graph below) crosses the red line.

• Sell-signals for short-entries are only considered in case the EMA (yellow line in the graph below) crosses the green line.

An example is shown in graph 4 below:

We use this indicator to determine the new trend direction that may occur by using the data of the price's past movement.

4. Bringing it all together

This section describes in detail, how this strategy combines the Momentum-RSI, the super-trend analysis and the EMA-strategy.

The strategy only generates trading-signals in case all of the following conditions and qualifiers are being met:

1. Momentum-RSI is higher than the set value of this strategy. The standard and recommended value is 60 (graph 5):

2. The super-trend analysis needs to indicate a confirmed upward-trend (for long-entry signals) or a confirmed downward-trend (for short-entry signals), respectively.

3. The EMA-strategy needs to indicate that the stock or financial security is in a confirmed upward-trend (long-entries) or downward-trend (short-entries), respectively.

The strategy will only generate trading signals if all three qualifiers are being met. This makes this strategy highly selective and is the key secret for its success.

Example for Long-Entry (graph 6):

When these conditions are met, our Long position is opened.

Example for Short-Entry (graph 7):

Trade Management Options (graph 8)

Option 1

In this dynamic version, the so-called supertrend-indicator is being used for the trade exit management. This supertrend-indicator is a sophisticated and optimized methodology which uses the dynamic ATR as one of its key input parameters.

The following settings of the supertrend-indicator can be changed and optimized (graph 9):

The dynamic SL/TP-lines of the supertrend-indicator are shown in the charts. The ATR-length and the supertrend-factor result in a multiplier value which can be used to fine-tune and optimize this strategy based on the financial security, timeframe and overall market environment.

Option 2 (graph 10):

Option 2 applies pre-defined, fixed SL and TP levels which will appear as straight horizontal lines in the chart.

Settings options (graph 11):

The following settings can be changed for the three elements of this strategy:

1. (Length Mom-Rsi): Length of our Mom-RSI indicator.

2. Mom-RSI Limit Val: the higher this number, the more momentum of the underlying trend is required before the strategy will start creating trading signals.

3. The length and factor values of the super trend indicator can be adjusted:ATR Length SuperTrend and Factor Super Trend

4. You can set the source value used by the ema trend indicator to determine the ema line: Source Ema Ind

5. You can set the EMA length and the percentage value to follow the price: Length Ema Ind and Percent Ema Ind

6. The backtesting period can be adjusted: Start and End time of BackTest

7. Dollar cost per position: this is relevant for 100% fully automated trading.

8. Trade direction can be adjusted: LONG, SHORT or BOTH

9. As we explained above, we can determine our stop-loss and take-profit levels dynamically or statically. (Version 1 or Version 2 )

Display options on the charts graph 12):

1. Show horizontal lines for the Stop-Loss and Take-profit levels on the charts.

2. Display relevant Trend Lines, including color setting options for the supertrend functionality. In the example below, green lines indicate a confirmed uptrend, red lines indicate a confirmed downtrend.

Other comments

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

Volatility Percentile (H-LINES)A simple script that adjusts the Volatility Percentile Indicator visibly in order to better accommodate entries/exits and certain trading setups/strategies.

--------------------------------------------------------------------------------------------------------------------------------------------------------

TL;DR - Remember after a full reset, we are looking for initial crosses UP on the UpperSwingline and crosses DOWN on the LowerSwingline for primary and secondary signal derivation.

Vice versa also works great but the prior method mentioned is a little more consistent in my experience, but you should mess around and optimise this for your own setups and strategies anyway.

--------------------------------------------------------------------------------------------------------------------------------------------------------

ORIGINAL SCRIPT HERE:

^Click image for a redirect to that script.

ALL CREDIT GOES TO: www.tradingview.com

He wrote everything so give credit where it's due, good bit of kit this here script is.

--------------------------------------------------------------------------------------------------------------------------------------------------------

HOW I USE MY VISUALLY ALTERED VERSION OF THIS SCRIPT

First of all, the alterations I've made seem only to be consistently viable with renko charts though if you can get the sought after results using candles or any other chart type then perfect, but be wary. All my back-testing done only with LinReg, HMA and SWMA - ATR type settings exclusively on renko charts. The changes I've made to the original script essentially just turns it visibly into an oscillator and uses a couple horizontal lines to generate signals, very simple - absolutely nothing has changed in the actual code of calculating this indicator.

What I believe my adjustments have achieved is quite simple. A full reset/oscillation on the indicator tries to map the strongest parts of a move or at least the part of the move where volume and the rate of transactions is at its peak to even facilitate said move. *take this statement with a pinch of salt though I do believe it's interacting with accumulation/distribution patterns, which is expected of volatility*

For ease of communication let's refer to the area between the the first UpperSwingline cross to the subsequent LowerSwingline cross, as the primary move. Then afterwards when it crosses the UpperSwingline again to make the full reset, the area in between those two points referred to as the secondary move.

Though more interestingly/practically the indicator ends up giving you two signals. In order for this to work we have to first decide that a spike up in volatility which crosses the UpperSwingline implies a significant level of interest at that price level. Usually that means a reversal is brewing, if price has already moved, trended and is approaching a certain area of value; which causes a spike of new positions to be taken, then you know that this is a level where contrarians are looking to enter. Now here's the tricky part, when volatility crosses the LowerSwingline price action becomes a little more open for interpretation, the way I personally like to look at this secondary signal is the potential for an exhaustion period to prolong itself a little longer. I know that's not the perfect analysis for what's going on, a more in-depth look into what's going on would best be described using Elliott Wave Theory, if a cross on the UpperSwingline near a significant area of value gives us a reversal trade lets just assume for the sake of argument that a new Elliott Wave can begin forming here. Making the move from that initial UpperSwngline cross to the cross on the LowerSwingline, the area that encompasses those two points: the impulse wave. After this point my analogy kind of falls apart and sadly my knowledge just isn't what it needs to be in order for me to properly analyse what's going on here but I must digress. Price after crossing the LowerSwingline up until the point where it makes a full reset by crossing the UpperSwingline again, within this area price seems to do either one of two things:

Situation 1 - Most likely occurs after a major trend reversal from major support/resistance or area of value (price has trended to new territory, maybe spent time a little time consolidating but hasn't broken the key level, momentum shifts, price action breaks current structure and you get the signal that primary move is a reversal) = Exhaustion Period, price will continue in direction of primary move during the secondary move. This here is for our trend-followers, you wanna take a continuation trade? Just wait for the pullback/rally to hit a FiB retracement level and enter - or any other means to find a decent support/resistance to enter.

Situation 2 - Most likely occurs when market enters a range or consolidation (price was previously seen as being at either a discount or premium so Situation 1 could have already played out and now you're looking at a full reset after that, imagine this spot to be the centre line of a linear regression channel or bang in the middle of your range, could even occur if price breaks a key moving average and decides it ought to consolidate around it for a while. Basically at any point where a somewhat prolonged consolidation is expected and not a quick reversal) = Corrective Wave, price will move against the direction of primary move during the secondary move. Now you might be expecting me to say this ones for you reversal traders but not really, if this is occurring then there probably isn't a definitive direction the market has chosen so you can use this opportunity to take range trades in the direction or against the direction of whatever the current trend or latest trend was depending on whatever slight bias you may have. <--- Situation 2 is very useful for finding cleaner entries if you do have a trend bias, say price underwent Situation 1, is now at key moving average but your bias is that it will break and continue up, so you wait and allow the secondary move of Situation 2 to take your entry to a much better R:R before entering a position.

--------------------------------------------------------------------------------------------------------------------------------------------------------

Simple_RSI+PA+DCA StrategyThis strategy is a result of a study to understand better the workings of functions, for loops and the use of lines to visualize price levels. The strategy is a complete rewrite of the older RSI+PA+DCA Strategy with the goal to make it dynamic and to simplify the strategy settings to the bare minimum.

In case you are not familiar with the older RSI+PA+DCA Strategy, here is a short explanation of the idea behind the strategy:

The idea behind the strategy based on an RSI strategy of buying low. A position is entered when the RSI and moving average conditions are met. The position is closed when it reaches a specified take profit percentage. As soon as the first the position is opened multiple PA (price average) layers are setup based on a specified percentage of price drop. When the price hits the layer another position with the same position size is is opened. This causes the average cost price (the white line) to decrease. If the price drops more, another position is opened with another price average decrease as result. When the price starts rising again the different positions are separately closed when each reaches the specified take profit. The positions can be re-opened when the price drops again. And so on. When the price rises more and crosses over the average price and reached the specified Stop level (the red line) on top of it, it closes all the positions at once and cancels all orders. From that moment on it waits for another price dip before it opens a new position.

This is the old RSI+PA+DCA Strategy:

The reason to completely rewrite the code for this strategy is to create a more automated, adaptable and dynamic system. The old version is static and because of the linear use of code the amount of DCA levels were fixed to max 6 layers. If you want to add more DCA layers you manually need to change the script and add extra code. The big difference in the new version is that you can specify the amount of DCA layers in the strategy settings. The use of 'for loops' in the code gives the possibility to make this very dynamic and adaptable.

The RSI code is adapted, just like the old version, from the RSI Strategy - Buy The Dips by Coinrule and is used for study purpose. Any other low/dip finding indicator can be used as well

The distance between the DCA layers are calculated exponentially in a function. In the settings you can define the exponential scale to create the distance between the layers. The bigger the scale the bigger the distance. This calculation is not working perfectly yet and needs way more experimentation. Feel free to leave a comment if you have a better idea about this.

The idea behind generating DCA layers with a 'for loop' is inspired by the Backtesting 3commas DCA Bot v2 by rouxam .

The ideas for creating a dynamic position count and for opening and closing different positions separately based on a specified take profit are taken from the Simple_Pyramiding strategy I wrote previously.

This code is a result of a study and not intended for use as a full functioning strategy. To make the code understandable for users that are not so much introduced into pine script (like myself), every step in the code is commented to explain what it does. Hopefully it helps.

Enjoy!

Strategy for UT Bot Alerts indicator Using the UT Bot alerts indicator by @QuantNomad, this strategy was designed for showing an example of how this indicator could be used, also, it has the goal to help some people from a group that use to use this indicator for their trading. Under any circumstance I recommend to use it without testing it before in real time.

Backtesting context: 2020-02-05 to 2023-02-25 of BTCUSD 4H by Tvc. Commissions: 0.03% for each entry, 0.03% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 3 indicators are used:

UT Bot Alerts indicator by Quantnomad

One Ema of 200 periods for indicate the trend

Atr stop loss from Gatherio

Trade conditions:

For longs:

Close price is higher than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our long signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as buy (open long position)

The other half will be closed when close price is lower than Atr and Ema from UT Bot cross under Atr. This will be showed as cl buy (close long position)

For shorts:

Close price is lower than Atr from UT Bot

Ema from UT Bot cross over Atr from UT Bot.

This gives us our short signal. Stop loss will be determined by atr stop loss (white point), break even(blue point) by a risk/reward ratio of 0.75:1 and take profit of 3:1 where half position will be closed. This will be showed as sell (open short position)

The other half will be closed when close price is higher than Atr and Ema from UT Bot cross over Atr. This will be showed as cl sell (close short position)

Risk management

For calculate the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a long signal at price of 20,000 usd. The stop loss price from atr stop loss is 19,000. You calculate the distance in percent between 20,000 and 19,000. In this case, that distance would be of 5,0%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(5,0%) = 500usd. It means, you have to use 500 usd for risking 2.5% of your account.

We will use this risk management for apply compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital

---> Do not forget to deactivate Trades on chart option in style settings for a cleaner look of the chart <---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Strategies for trending markets use to have more looses than wins and it takes a long time to get profits, so do not forget to be patient and consistent !

---> The strategy can still be improved, you can change some parameters depending of the asset and timeframe like risk/reward for taking profits, for break even, also the main parameters of the UT Bot Alerts <----

Strat Dashboard [TFO]The Strat Dashboard tracks up to 10 signals while highlighting common strat reversal patterns, the SSS 50% rule, timeframe continuity, and some additional criteria with VWAP and moving averages.

With the strat, all price action bars/candles are simplified into 3 total possibilities: 1 (inside bar), 2 (a bar that takes the previous bar's high OR low), and 3 (outside bar). The first table column for Last X Candles shows the most recent candles according to this notation, for example, 1 - 2D - 2U. This would mean we had an inside bar, followed by a bar that took the previous bar's low, followed then by a bar that took the previous bar's high. Note that the colors in this column are set according to whether the current bar's close exceeds the previous bar's high/low. By default, these colors are green if above the previous bar's highs, or red if below the previous bar's lows. If the current close is in between the previous candle's high and low (even after already taking the prior high or low), no color will be applied.

The SSS 50% column shows a yes or no value for whether the current bar aligns with the SSS 50% rule, where a bar has taken either the previous high or low, and has since reversed to at least the midway point of the previous bar's height - essentially anticipating a 2 that may become a 3 (outside bar).

Timeframe continuity (TFC) shows a yes or no value for when the current candle on multiple timeframes are all green or red (above the open price or below the open price, respectively). For example, if you were looking at the current 15m, 1h, and 1D bars, and they were all above the open price, you could say there's TFC between all three timeframes. As of the initial release, you can select up to 3 different timeframes. The table values will only be true when all selected timeframes are in alignment. When setting alerts, first deselect the timeframes if you don't want TFC logic to impact alerts.

The "Last" column shows the last strat reversal pattern that was confirmed (after the last bar closes). Waiting for a candle close is the safer option since a 2 can turn into a 3; however for higher timeframes, it may be beneficial to make an update to this indicator in which you can have live alerts as well (not waiting for a candle close). You can select which strat reversals you want to be shown from the settings. Various strat reversals may be selected for alerts of type "Any"; for example, if setting up an alert for "Any" strat reversal on Symbol 1, then this alert will go off when any of the *selected* strat reversals occur for that specific symbol. Deselect any strat reversals that you don't want to be included in these alerts.

Lastly, the EMA and VWAP columns simply show whether price is above or below said value. This tracks the current candle close, and may repaint/change several times if the current bar is oscillating above and below these values.

Morning Option Pullback IndicatorI designed this indicator to help me identify Option CALL and PUT signals for the QQQ and SPY on the 1 min chart.

Summary of how it works

1. It identifies the Pre-Market channel High and Low and draws green and red lines for the day at these levels.

2. Waits for a morning or afternoon sessions breakout/breakdown of price out of that channel.

3. The buy a CALL or PUT signal is when price pulls back to the EMA Medium line after breaking out of the channel.

4. Settings allow adjusting of when the signal happens

5. EMA Short (5) and EMA Medium (20) must stay apart for a selectable number of bars

6. For a CALL signal, the Price and EMA Medium (20) must be above the Pre Market High line when price pulls back to EMA Medium (20) line

7. There is a selectable adjustment to allow the signal to trigger when the price comes within a close enough range of the EMA Medium and PM High lines

8. There is a TICK.US filter that you can use to only signal a CALL when the TICK.US 10 min chart shows the average of the EMA5 and EMA20 is over 100

9. It has Buy and Sell signal Alerts and user adjustable Stop Loss and Profit Taker settings.

10. EMA Settings are adjustable and can show up to 3 EMA's on the chart. I personally like the EMA5 and 20. Others may use something similar like 9 and 21. It's user selectable.

Big Poppa Code Strat & Momentum Strategy IndicatorThis indicator is a combination of a few things in order to work with a unique trading style gleaned from Callme100k, jrgreatness, TrustMyLevels , FaithInTheStrat, Rob Smith and Saty Mahajan.

This Indicator is created to help you day trade using, ATR Fibonacci Levels, Price Action and Momentum.

It displays Fibonacci Levels Based on ATR to indicate when a security is 0.236, 0.382 +- the Days Open, +- the Days Open, 0.618 +- the Days Open and 1.0 +- Days Open.

To understand this script you need to understand

Average True Range (ATR)

1 Bar Inside Bar

2 Bar Outside Bar (Break either the top or bottom)

3 Bar Engulfing Bar

Strat Setups - 212, 322, 312

Fibonacci - 0.236, 0.382, 0.618, 1.0

Moving Averages

A Trend is considered bullish when (green)

Current Price is greater than the Fast EMA Value (8)

Fast EMA is greater than PIVOT EMA Value (21)

Pivot EMA is greater than SLOW EMA Value (34)

OR Hull is trending up and the Price is above the Volume Weighted Moving Average and price is above VWAP

A trend is considered Bearish when (red)

Current Price is less than the Fast EMA Value (8)

Fast EMA is less than PIVOT EMA Value (21)

Pivot EMA is less than SLOW EMA Value (34)

OR Hull is trending down and the Price is below the Volume Weighted Moving Average and price is below VWAP

If these conditions are not met then the Momentum is in Conflict (orange)

The Momentum band will match the color of the current trend

The table that is present can be turned off at any time lets you see

1) If Moving Averages are showing bullish, bearish or in conflict

2) If There us Time Frame Continuity, (if 5 min up, are all the other timeframes up also)

3) How much of the ATR have we moved on the day

4) Are we in Call or Put range for the day based on ATR Fib Levels

The Ideal situation for entering a call

1) Momentum is Green

2) FTFC on Green

3) A Strat Actionable Signal is present

4) You are in the call range, 0.236 - 0.618 ATR + the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Ideal situation from entering a put

1) Momentum is red

2) FTFC on Red

3) A Strat Actionable Signal is present

4) You are in the put range, 0.236 - 0.618 ATR - the Price

5) The ATR still has room, I.e only 50% of the ATR has been run already

Exit the trade for these reasons you entered (for profit or loss)

1) ATR has no more room

2) FTFC is now in conflict

3) Momentum has shifted

Take Profit when

1) You reach a new ATR Level 0.618, 1.0 , -0.618, -1, etc

Passive Stop Loss

1) Open Price if you are aggressive

2) Next ATR Level Down or Up

Feel free to take profit and leave runners

This script does not give signals, you should do your own research, I am not a financial advisors, I am simply applying principles of seasoned veterans to code. You make all decisions about how you buy, sell and trade. The creator of this script makes no promises and takes no responsibility for your personal trading.

To research the methods described above look up

Rob Smith : The Strat

Saty Mahajan : ATR Levels

Fibonacci

Using the HULL Moving Average

Exponential Moving Averages

VWAP

VWMA

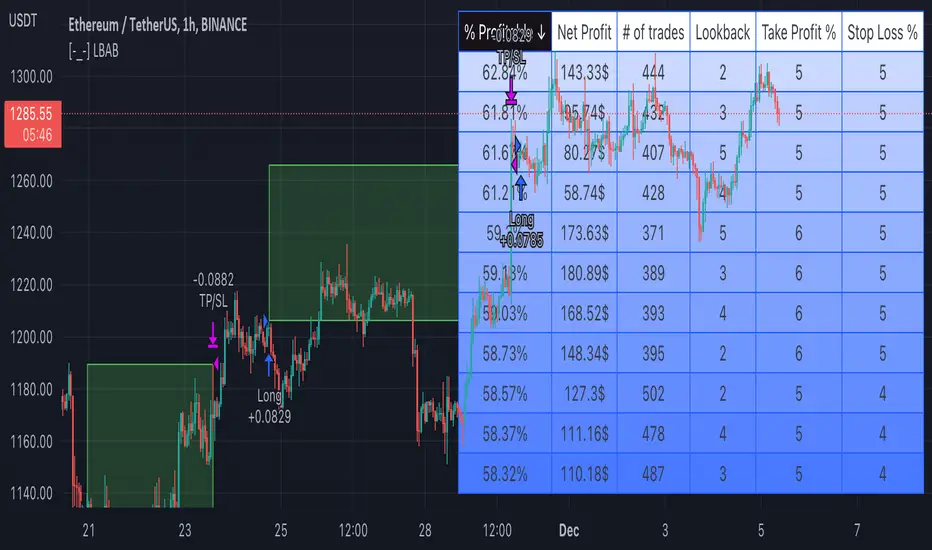

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

MA MomentumThis simple script takes two ma's sums them and takes the the difference between the current and previous data points. This gives a lovely smoothed momentum indicator. The way it works is if its green its good and if its red its bad. In other words, I take the smooth signal as a filter for the momentum. You can also spot divergences between the indicator and the price to make decisions. Some features include extra smoothing and adjustable ma's. I hope you find this script useful!

Thank you.

50 Pips A Day Strategy - Kaspricci50 Pips A Day Strategy

This strategy is designed to work on 1 hour timeframe. It is designed to capture the early market move of major forex pairs like EURUSD or GBPUSD. It takes the high and low of the first candle (7 a.m. GMT, London Stock Exchange opens) and places to pending orders at these prices levels.

High + additional gap in pips = buy stop pending order

Low + additional gap in pips = sell stop pending order

For both orders a stop loss of 15 pips and a take profit of 50 pips is used as a default. As soon as price triggers one pending order, the remaining pending order is cancelled. At the end of the configured session time all open and pending orders are closed / cancelled.

Settings

Trading Time - start and end time of session. It is configured for Monday to Friday only. At the beginning the first candle is used to define stop prices for pending orders.

Source for Buy Stop order - Default: high. Used to calculate buy stop order. You can add additional pips as a gap.

Source for Sell Stop order - Default: low. Used to calculate sell stop order. You can add additional pips as a gap.

Stop Loss in Pips - Default: 15. Used for both pending orders.

Take Profit in Pips - Default: 50. Used for both pending orders.

This strategy is for educational purposes only! It is not meant to be a financial recommendation.

(E)Moving Average Ribbon High/LowThis is a slight modification of the standard Moving Average Ribbon. This script will take the 200 EMA and SMA with source the high and low, not the close.

This band will act as a support and resistance zone and should be used as a confluence with other indicators or support/resistance lines.

I got inspired to create this one, by the YT video "FINALLY! The 200 EMA Confluence Trading Strategy You’ve Been Waiting For" by The Secret Mindset.

In his video he takes only the 200EMA, but this script will take by default also the SMA into account.

In the settings you still can adapt as you wish ;-)

Happy trading!

Tick StrategyTick Strategy:

Questions many pine coders/traders have is, How to enter/exit trade as soon as trade condition is met i.e. do not wait till candle completion to enter/exit the trade. This strategy will help you to understand one of the way to achieve it.

This is an educational strategy to demonstrate, how one can trade based on tick data. This being a strategy based on tick data, it can be tested only on real time candles. This strategy will not take any trades on historical candles and cannot be used for back testing. All the strategy trades taken on real time candles will disappear (repainting) once chart is refreshed and new trades will be entered on real time candles.

The strategy will do nothing during off market hours and will not take any trades.

The strategy has been designed based on rules/inputs below:

1. Count the ticks from start of a candle till end of candle

2. Bifurcate ticks as up-ticks and down-ticks. If tick price is above previous tick price the tick is considered as up-tick and vice versa

3. Count the successive up-ticks and successive down-ticks

Strategy rules:

1. Track candle type (green or red) continuously on each tick (green candle is when latest tick price > previous tick price)

2. Take a long trade if work in progress (WIP) candle is green candle and we get successive up-ticks equal to user input ticks for trade

3. Take a short trade if work in progress (WIP) candle is red candle and we get successive down-ticks equal to user input ticks for trade

4. Exit the trade when we get successive ticks equal to user input ticks in opposite direction

5. Optionally for trade entry, user can decide whether to calculate successive up-ticks/down-ticks from beginning of candle or successive up-ticks/down-ticks anytime during the candle formation

6. Optionally for trade exit/square off, user can decide whether to apply exit rules on the entry candle or only from subsequent candle

Strategy setting:

1. '' – This is just to describe when trades are entered. This parameter is not used for any calculation

2. 'No of successive ticks to enter the trade' – User input to decide, number of successive ticks for trade entry

3. 'Count successive ticks for trade only from start of candle' – check this to count successive ticks only from beginning of a candle

4. 'Exit if succussive ticks in opposite direction' - User input to decide, number of successive ticks in opposite direction for exiting the trade

5. 'Apply exit criteria on entry candle' – check to allow exit of trade on the entry candle, if un-checked, trade will not be exited on the entry candle i.e. opposite direction ticks will be counted from subsequent candle

Information below will be displayed continuously on the chart:

1. Candle no – Candles are counted from start of the trading session. This is current candle being formed on the chart

2. Candle now – This shows either ‘Green’ or ‘Red’ based on type of candle being formed

3. Tick count – This is current tick number being processed. Tick number starts from 1 for each new candle

4. Up-tick count – Number of up-ticks during formation of current candle

5. Down-tick count – Number of down-ticks during formation of current candle

6. Successive up-ticks – Current successive up-tick count

7. Successive down-ticks – Current successive down-tick count

8. Up-tick volume – Volume associated with up-ticks

9. Down-tick volume – Volume associated with down-ticks

10. Up-tick volume % - This is % of volume associated with up-ticks

11. Total volume – Candle volume till now. (Some times you might observe small difference between total volume and the volume shown by volume indicator. The difference could be because of refresh rate of your screen)

12. Candle completion % - This shows current candles completion %. This is candle progress from start of candle till close of candle

Bollinger Pair TradeNYSE:MA-1.6*NYSE:V

Revision: 1

Author: @ozdemirtrading

Revision 2 Considerations :

- Simplify and clean up plotting

Disclaimer: This strategy is currently working on the 5M chart. Change the length input to accommodate your needs.

For the backtesting of more than 3 months, you may need to upgrade your membership.

Description:

The general idea of the strategy is very straightforward: it takes positions according to the lower and upper Bollinger bands.

But I am mainly using this strategy for pair trading stocks. Do not forget that you will get better results if you trade with cointegrated pairs.

Bollinger band: Moving average & standard deviation are calculated based on 20 bars on the 1H chart (approx 240 bars on a 5m chart). X-day moving averages (20 days as default) are also used in the background in some of the exit strategy choices.

You can define position entry levels as the multipliers of standard deviation (for exp: mult2 as 2 * standard deviation).

There are 4 choices for the exit strategy:

SMA: Exit when touches simple moving average (SMA)

SKP: Skip SMA and do not stop if moving towards 20D SMA, and exit if it touches the other side of the band

SKPXDSMA: Skip SMA if moving towards 20D SMA, and exit if it touches 20D SMA

NoExit: Exit if it touches the upper & lower band only.

Options:

- Strategy hard stop: if trade loss reaches a point defined as a percent of the initial capital. Stop taking new positions. (not recommended for pair trade)

- Loss per trade: close position if the loss is at a defined level but keeps watching for new positions.

- Enable expected profit for trade (expected profit is calculated as the distance to SMA) (recommended for pair trade)

- Enable VIX threshold for the following options: (recommended for volatile periods)

- Stop trading if VIX for the previous day closes above the threshold

- Reverse active trade direction if VIX for the previous day is above the threshold

- Take reverse positions (assuming the Bollinger band is going to expand) for all trades

Backtesting:

Close positions after a defined interval: mark this if you want the close the final trade for backtesting purposes. Unmark it to get live signals.

Use custom interval: Backtest specific time periods.

Other Options:

- Use EMA: use an exponential moving average for the calculations instead of simple moving average

- Not against XDSMA: do not take a position against 20D SMA (if X is selected as 20) (recommended for pairs with a clear trend)

- Not in XDSMA 1 DEV: do not take a position in 20D SMA 1*standart deviation band (recommended if you need to decrease # of trades and increase profit for trade)

- Not in XDSMA 2 DEV: do not take a position in 20D SMA 2*standart deviation band

Session management:

- Not in session: Session start and end times can be defined here. If you do not want to trade in certain time intervals, mark that session.(helps to reduce slippage and get more realistic backtest results)

Simple and Profitable Scalping Strategy (ForexSignals TV)Strategy is based on the "SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV.

See video for a detailed explaination of the whole strategy.

I'm not entirely happy with the performance of this strategy yet however I do believe it has potential as the concept makes a lot of sense.

I'm open to any ideas people have on how it could be improved.

Strategy incorporates the following features:

Risk management:

Configurable X% loss per stop (default to 1%)

Configurable R:R ratio

Trade entry:

Based on stratgey conditions outlined below

Trade exit:

Based on stratgey conditions outlined below

Backtesting:

Configurable backtesting range by date

Trade drawings:

Each entry condition indicator can be turned on and off

TP/SL boxes drawn for all trades. Can be turned on and off

Trade exit information labels. Can be turned on and off

NOTE: Trade drawings will only be applicable when using overlay strategies

Debugging:

Includes section with useful debugging techniques

Strategy conditions

Trade entry:

LONG

C1: On higher timeframe trend EMAs, Fast EMA must be above Slow EMA

C2: On higher timeframe trend EMAs, price must be above Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be above Medium EMA and Medium EMA must be above Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in upward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the high of the last X candles (plus price buffer) to trigger entry (stop order entry)

SHORT

C1: On higher timeframe trend EMAs, Fast EMA must be below Slow EMA

C2: On higher timeframe trend EMAs, price must be below Fast EMA

C3: On current timeframe entry EMAs, Fast EMA must be below Medium EMA and Medium EMA must be below Slow EMA

C4: On current timeframe entry EMAs, all 3 EMA lines must have fanned out in downward direction for previous X candles (configurable)

C5: On current timeframe entry EMAs, previous candle must have closed above and not touched any EMA lines

C6: On current timeframe entry EMAs, current candle must have pulled back to touch the EMA line(s)

C7: Price must break through the low of the last X candles (plus price buffer) to trigger entry (stop order entry)

Trade entry:

Calculated position size based on risk tolerance

Entry price is a stop order set just above (buffer configurable) the recent swing high/low (long/short)

Trade exit:

Stop Loss is set just below (buffer configurable) trigger candle's low/high (long/short)

Take Profit calculated from Stop Loss using R:R ratio

Credits

"SIMPLE and PROFITABLE Forex Scalping Strategy" taken from YouTube channel ForexSignals TV

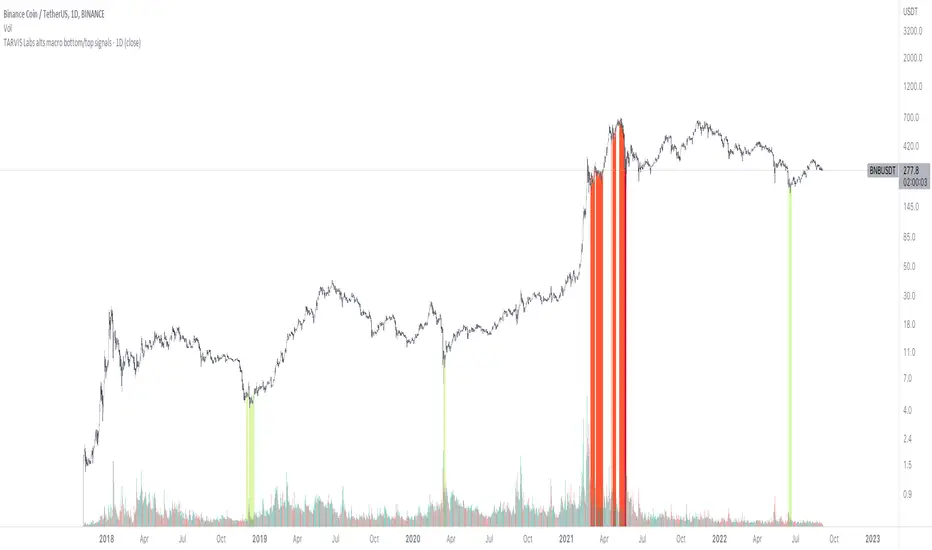

TARVIS Labs - Alts Macro Bottom/Top SignalsSCRIPT DESCRIPTION

PLEASE READ THROUGH THIS CAREFULLY.

This is a script specifically written to help provide indicators from a macro view for ALTS. This script needs to be run on the 1 day. It helps indicate when to accumulate alts, and when its in a bull run when this a bull run top beginning to form with warnings, and a indicator that a top is in. This is described further below.

NOTE - in order to accomodate most alts the script had to be broad enough in its indicators to cover many different scenarios. If you are trading a smaller altcoin I suggest taking a more conservative approach to accumulation.

FAQs:

1. Why is there no accumulation zone showing up before an uptrend?

This could be because the trend has been so strong for this coin that there hasn't been a strong enough signal to accumulate or this could be that the chart doesnt have enough historical data (needs over 2 years) for the indicators to flash green.

2. Why is there no tops shown for a chart Im looking at?

This is either because there isn't enough historical data (needs over 2 years) for the indicators to build or because the altcoin didnt perform as well as the rest of the market. The altcoin has to perform as well as the market over the length of the bull run in order for the signals to show. Typically an altcoin that shows sharp increases and sharp drops shortly after will not have signals show up.

3. The "Potential End of Bull Run Top Indicator" showed up but we weren't near the top yet, why is that?

The alts indicator has to work across many altcoins, and their trends are not all the same. This can lead to the indicator showing but not necessarily being the exact top. The data from the alts macro bottom/top signals should be paired with the "TARVIS Labs bitcoin macro bottom/top signals" indicator for BTC. The reasoning is because if the top is not showing that its in for Bitcoin its likely that the altcoin's top is also not in. You should use the two in tandem to know if the bull run top is very likely in.

ACCUMULATION ZONE INDICATOR - LIGHT GREEN

Description

When we look at the general crypto landscape, the 200d & 300d EMAs are extremely useful. We can use their cross and momentum in order to determine a bottom forming. If the price has fallen over 40% below the 200 day EMA and the 200 day EMA has crossed below the 300d EMA, its a downtrend with a steep fall, which could indicate a good time to accumulate. When we see the 200 day EMA's slope drop drastically (over 5% w/w) it is also a good signal to accumulate.

Strategy for Usage

For alts, the strategy can vary drastically. You need to take into account:

1. the market cap of the altcoin, is it a smaller market cap altcoin or a larger one?

2. historical trend, does it typically trend strongly with a smaller accumulation zone?

Once you've taken these into account you can form a strategy. For example, if the altcoin has had smaller accumulation zones historically you'll want to take advantage of the accumulation zones when they pop up and be more aggressive (say a 30 day accumulation). If the altcoin has historically had longer accumulation zones then you'll want to be more conservative with your strategy and potentially have a 100 day (or even longer) accumulation period. If the altcoin is a smaller market cap alt, you will want to also take that into account. You'll want to likely be more conservative,

STRONG BUY IN ACCUMULATION ZONE INDICATOR - DARK GREEN

Description

We can add to the bottoming signal by looking for strong downtrends inside the bottoming signal. We do this by seeing when the 36 day EMA has a slope decreasing by 2% day/day.

Strategy for Usage

These strong downtrend days can be used to add more to our accumulation strategy. We can add more on these days (ex. double what you were planning to on a typical accumulation day).

LOCAL TOP NEAR BULL RUN TOP INDICATOR - RED

Description

When the 100 week EMA is in a strong uptrend (4% increase w/w) we can look for significant loss of momentum in order to determine if a local top is in near a bull run top. This strategy uses a MACD with 9/36/9 config for the daily chart. We look for the signals momentum loss, when the slope becomes negative.

Strategy for Usage

Ideally the right strategy to use here is to exit the market when this indicator starts. When the indicator ends if the "Potential End of Bull Run Top Indicator" is not showing on the chart you can buy back into the market.

POTENTIAL END OF BULL RUN TOP INDICATOR - DARK RED

Description

When the 100 week EMA is in a strong uptrend (3% increase w/w), and a MACD config of 108/234/9 has a negative signal slope signifying a very large momentum loss, but the 1d 18 EMA is still above the 1d 63 EMA we show this signal.

Strategy for Usage

This is a strong indicator that the top is in, and it potentially being the bull run top. Because alts can vary strongly in their charts, this should be a strong warning but not necessarily a certainty that the bull run is over.

CCMA - Count Condition MA (560 Indicators In One) Do you like using moving averages?

Why do you think a pair of moving averages on a chart will help you?

What is the probability that once two moving averages have crossed, you will successfully enter the trade?

So why not use 100+ moving averages at once to increase the probability of a successful trade?

And all this can be seen in a single oscillator as a histogram!

I want to introduce you to a system that takes into account 560 moving averages movements. And that's just for a second, 560 potential indicators.

Specifically:

- 22 types of MA (EMA, SMA, RMA and others).

- 176 moving averages.

- 310 crossover checks.

- 252 checks of trend following.

The indicator makes the most of the opportunities provided by television. Therefore, it can take a long time to load it.

How does it work ?

In general, the indicator counts the number of fulfilled conditions.

It checks if MA #1 and MA #2 have crossed. If so, it adds +1 to the statistics. It also checks if price is above or below the moving average. There are a total of 560 such checks. (This is about the maximum the TV allowed me).

The default is 8 lengths of moving averages, I took the Fibonacci numbers thinking they were the optimal solution. You can take any of your favorites.

If the "Ratio MOD" feature is on. Then you can see how many MAs are showing signals to enter a long or short position.

You can also see the indication at the bottom as dots. They show which signals are longer/shorter. If the number of signals is the same, the dot will be yellow. The first line of dots counts the number of crossings. The second line counts the number of crossovers + checks whether the price is above or below the average slippage.

If the "Differ MOD" function is enabled. Then you can see the difference between long and short signals. With the same indication as in RATIO MOD.

If "Show all" is on, then the bar graph shows all 560 accounting options. If it is off, only the number of crossovers is displayed. (This does not apply to the display as points)

If the script shows an error, try to change the timeframe and go back. Or add it again.

You can also disable the histogram in the stats settings and leave only the points that help in determining the trend.

DMI StrategyThis strategy is based on DMI indicator. It helps me to identify base or top of the script. I mostly use this script to trade in Nifty bank options, even when the signal comes in nifty . It can be used to trade in other scripts as well. Pivot points can also be used to take entry. Long entry is taken when DI+(11) goes below 10 and DI-(11) goes above 40 , whereas short entry is taken when DI-(11) goes below 10 and DI+(11) goes above 40.

For bank nifty , I take the trade in the strike price for which the current premium is nearby 300, with the SL of 20%. If premium goes below 10% I buy one more lot to average, but exit if the premium goes below 20% of the first entry. If the trade moves in the correct direction, we need to start trailing our stoploss or exit at the pre-defined target.

As this a strategy, there is one problem. While we are in the phase of "long", if again the "long" phase comes, it will not be shown on chart until a "short" phase has come, and vice versa. This has been resolved by creating an indicator instead of strategy with the name of "DMI Buy-sell on chart". Please go through that to get more entry points.

Please have a look at strategy tester to back test

DMI StrategyThis strategy is based on DMI indicator. It helps me to identify base or top of the script. I mostly use this script to trade in Nifty bank options, even when the signal comes in nifty. It can be used to trade in other scripts as well. Pivot points can also be used to take entry. Long entry is taken when DI+(11) goes below 10 and DI-(11) goes above 40, whereas short entry is taken when DI-(11) goes below 10 and DI+(11) goes above 40.

For bank nifty, I take the trade in the strike price for which the current premium is nearby 300, with the SL of 20%. If premium goes below 10% I buy one more lot to average, but exit if the premium goes below 20% of the first entry. If the trade moves in the correct direction, we need to start trailing our stoploss or exit at the pre-defined target.

Please have a look at strategy tester to back test.

VHF-Adaptive T3 iTrend [Loxx]VHF-Adaptive T3 iTrend is an iTrend indicator with T3 smoothing and Vertical Horizontal Filter Adaptive period input. iTrend is used to determine where the trend starts and ends. You'll notice that the noise filter on this one is extreme. Adjust the period inputs accordingly to suit your take and your backtest requirements. This is also useful for scalping lower timeframes. Enjoy!

What is VHF Adaptive Period?

Vertical Horizontal Filter (VHF) was created by Adam White to identify trending and ranging markets. VHF measures the level of trend activity, similar to ADX DI. Vertical Horizontal Filter does not, itself, generate trading signals, but determines whether signals are taken from trend or momentum indicators. Using this trend information, one is then able to derive an average cycle length.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

Price-Filtered Spearman Rank Correl. w/ Floating Levels [Loxx]Price-Filtered Spearman Rank Correl. w/ Floating Levels is a Spearman Rank Correlation indicator with optional source filtering and floating levels.

What is Spearman rank correlation?

Spearman rank correlation, also known as Spearman coefficient is a formula used to identify the strength of the link between two datasets. This coefficient is a method that can be used to assess the strength of a relationship apart from the direction it takes. The formula, named after Charles Spearman, a mathematician, can only be used in circumstances where data can be categorized or put in order, for instance, the highest to the lowest.

For a better understanding of Spearman coefficient, it helps to get a sense of what monotonic function means. There’s a monotonic relationship under these circumstances:

– When the variable values rise together.

– When one variable value rises the other variable value lowers.

– The rate of movement of the variables need not necessarily be constant.

The Spearman correlation coefficient or rs, between +1 and -1, where +1 indicates a perfect strength between variables, while zero shows no association and -1 shows a perfect negative strength.

Spearman rank correlation theory:

A nonparametric (distribution-free) rank statistic proposed by Spearman in 1904 as a measure of the strength of the associations between two variables (Lehmann and D'Abrera 1998). The Spearman rank correlation coefficient can be used to give an R-estimate, and is a measure of monotone association that is used when the distribution of the data make Pearson's correlation coefficient undesirable or misleading.

Included:

Zero-line and signal cross options for bar coloring, signals, and alerts

Alerts

3 Signal types

Loxx's Expanded Source Types

Inverse MACD + DMI Scalping with Volatility Stop (By Coinrule)This script is focused on shorting during downtrends and utilises two strength based indicators to provide confluence that the start of a short-term downtrend has occurred - catching the opportunity as soon as possible.

This script can work well on coins you are planning to hodl for long-term and works especially well whilst using an automated bot that can execute your trades for you. It allows you to hedge your investment by allocating a % of your coins to trade with, whilst not risking your entire holding. This mitigates unrealised losses from hodling as it provides additional cash from the profits made. You can then choose to hodl this cash, or use it to reinvest when the market reaches attractive buying levels.

Alternatively, you can use this when trading contracts on futures markets where there is no need to already own the underlying asset prior to shorting it.

ENTRY

The trading system uses the Momentum Average Convergence Divergence (MACD) indicator and the Directional Movement Index (DMI) indicator to confirm when the best time is for selling. Combining these two indicators prevents trading during uptrends and reduces the likelihood of getting stuck in a market with low volatility.

The MACD is a trend following momentum indicator and provides identification of short-term trend direction. In this variation it utilises the 12-period as the fast and 26-period as the slow length EMAs, with signal smoothing set at 9.

The DMI indicates what way price is trending and compares prior lows and highs with two lines drawn between each - the positive directional movement line (+DI) and the negative directional movement line (-DI). The trend can be interpreted by comparing the two lines and what line is greater. When the negative DMI is greater than the positive DMI, there are more chances that the asset is trading in a sustained downtrend, and vice versa.

The system will enter trades when two conditions are met:

1) The MACD histogram turns bearish.

2) When the negative DMI is greater than the positive DMI.

EXIT

The strategy comes with a fixed take profit combined with a volatility stop, which acts as a trailing stop to adapt to the trend's strength. Depending on your long-term confidence in the asset, you can edit the fixed take profit to be more conservative or aggressive.

The position is closed when:

Take-Profit Exit: +8% price decrease from entry price.

OR

Stop-Loss Exit: Price crosses above the volatility stop.

In general, this approach suits medium to long term strategies. The backtesting for this strategy begins on 1 April 2022 to 18 July 2022 in order to demonstrate its results in a bear market. Back testing it further from the beginning of 2022 onwards further also produces good returns.

Pairs that produce very strong results include SOLUSDT on the 45m timeframe, MATICUSDT on the 2h timeframe, and AVAUSDT on the 1h timeframe. Generally, the back testing suggests that it works best on the 45m/1h timeframe across most pairs.

A trading fee of 0.1% is also taken into account and is aligned to the base fee applied on Binance.

Future PreviewFuture Preview

Calculate real-time future order profit with open price, leverage and commission fee. Simple and straight forward. If you need any additional feature, please leave a comment below. I am glad to help.

Usage:

When adding Future Preview to chart, it will ask order open time and open price on the chart by clicking with left mouse on the desired value. These value can be changed lately, as well as the leverage and commission fee. Default leverage is 10 and default commission fee is 0.06% (taker).

There will be two horizontal lines. The solid longer line is the open price line, it shows the order open price. The shorter line moving with real-time price is the current price line, it shows the current price. There will be preview data shows on top or below the price line. Open price line is red for short order and green for long order. The current price line is red when the order is losing and it is green when it profiting. The back ground color follows the color of current price line. Background color transparency and gain/loss color can be changed in options.

There will be one horizontal line on the left if the option of showing open time is on (default is on). It shows the time stamp when current order opened.

After adding Future Preview to chart, there is option to add Taking Profit(TP) or Stop Loss(SL) to the chart.

Font size can be changed in option