TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

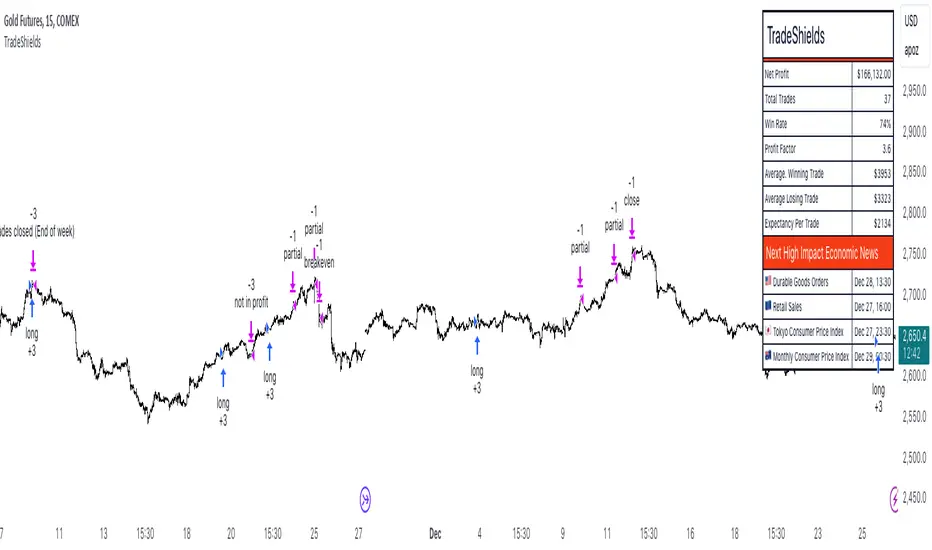

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

Cerca negli script per "algo"

Auto Harmonic Pattern - Backtester [Trendoscope]We are finally here with the implementation of backtesting tool for Auto-Harmonic-Pattern-UltimateX .

CAUTION: THIS IS NOT A STRATEGY AND SHOULD NOT BE FOLLOWED BLINDLY. WE ENCOURAGE USERS TO UTILISE THIS AS BACKTESTING TOOL FOR BUILDING THEIR STRATEGY BASED ON HARMONIC PATTERNS

This script is based on our premium indicator - Auto-Harmonic-Pattern-UltimateX . In this script, along with implementation of scanning harmonic patterns, we provide various options via settings which enables users to build their own strategy based on harmonic patterns, use them with custom coded filters, backtest them on various tickers and timeframes.

Harmonic Patterns is concept and we can trade harmonic pattern in many ways. While general interest around harmonic patterns is to find reversal zones and use them for short term swing trades. But, using it along trend following strategies can also be very rewarding. Here is one of the educational idea I shared about using harmonic patterns for trend following. These are just few possibilities where users can explore further on how they want to trade this. The settings of this script are crafted in such a way that it enables users to explore all these possibilities.

🎲 Components

Chart components of this script is lighter compared to Auto Harmonic Pattern - UltimateX. This is because we want to keep lighter interface in order to support seamless execution of emulator. Since pine strategy framework does most of the things such as calculating profitability, keeping track of trades and results etc, display with respect to - "Closed Trade Stats" are removed from this script and "Open Trade Stats" are made lighter.

🎲 Settings

🎯 Trade Settings : Few important settings under this section are

Due to pine limitations, we will not be able to support both long and short in a same setup. Hence, users need to chose either long or short trade setup.

Entry/Base/Target play important role in defining your strategy.

Confluence is another important factor which lets users use multiple patterns at once as confirmation.

🎯 Zigzag Settings : Zigzag settings determine the size of patterns being formed.

Please note that smaller patterns may not yield very good results and larger patterns may take time to complete trade. Similarly higher depth can cause runtime issues. Recursive zigzag option is alternative to deep search algorithm.

🎯 Filters :

Filters enable users to select trades based on specific conditions. Ability to use external filter even allows writing and using custom filters to be used with this algorithm. Here is a video which explains how this can be done. HOW-TO-Use-external-filters

Pattern filters allow users to pick and chose patterns they want to trade. This can be done either individually or based on category

🎯 Alerts :

Apart from strategy specific alerts, the script also implements customisable alerts via pine alert() function. Alerts can be configured to send upon three conditions

When new pattern is created

When an existing pattern updates entry/stop/target due to safe repaint of D (Only happens when Trail Entry Price is selected)

When a pattern in trade closes either due to hitting stop or target

Important Note: Alerts fired via this method may not match the trades shown on chart as trades which are controlled via pine strategy emulator depends on various other factors such as pyramiding.

Alert template is customisable and users can make use of available placeholders to get dynamic data in alerts. Valid placeholders are

{alertType} - Alert type - New/Update/Close

{id} - Pattern Id

{ticker} - Ticker

{timeframe} - Chart timeframe

{price} - Current price

{patterns} - Identified pattern names

{direction} - Direction - Long/Short

{entry} - Entry Price

{stop} - Stop Price

{target} - Target Price

{orderType} - Limit/Stop - applicable for only New and Update types

{status} - Trade status. Valid values are Pending/Cancelled/Stopped/Success

Template is common for all custom alert types. Hence, updating the template will impact all custom alerts - New/Update/Close

{

"alert" : "{alertType}",

"id" : {id},

"ticker" : "{ticker}",

"timeframe" : "{timeframe}",

"price" : {price},

"patterns" : "{patterns}",

"direction" : "{direction}",

"entry" : {entry},

"stop" : {stop},

"target" : {target},

"orderType" : {orderType}

"status" : {status}

}

Here is a video on how to customise the alerts using templates and placeholders - HOW-TO-Customize-Alerts-With-Placeholders

🎯 Miscellaneous :

These are simple settings to control display and backtest bars. If you are running alerts, we suggest turning of Open Trades and Drawings and limit backtest to minimal value in order to improve efficiency of

🎯 Backtest Engine Parameters :

Default settings are optimised for trend following. Users are encouraged to play around with settings and filters to build strategy out of this tool.

Position sizing is not leveraged. Margin settings makes sure that trades cannot exceed capital.

All measures are taken to avoid repainting. Script does not use request.security and real time bars. This drastically reduces the risk of repainting in scripts.

If you are premium user, please select "Bar Magnifier".

gangood bot for FinandyGangood is a mean reversion algorithm currently optimized for trading the ETH/USDT pair on the 1 hour chart time frame. All indicator inputs use the closing price of the period, and all trades are executed at the open of the period following the period in which the trading signal was generated.

To take into account slippage, the commission costs 0.15%.

Backtest result from 2020.

Result since 2019 2,500,000%, maximum drawdown 18%

This bot uses 11 indicators:

1) ADX

2) RANGE FILTER

3) SAR

4) RSI

5) TWAP

6) JMA

7) MACD

8) VOLUME DELTA

9) VOLUME WEIGHT

10) MA

11) TSI

Pattern 1:

There are 3 main components that make up Gangood: I. Trend Filter. The algorithm uses a version of the ADX indicator as a trend filter to only trade during certain time periods when price is most likely to be range-bound (i.e., average retracement). This indicator consists of a fast ADX and a slow ADX both using the same lookback period.

The ADX is smoothed with a 6-period EMA and the slow ADX is smoothed with a 12-period EMA. When the fast ADX is above the slow ADX , the algorithm does not trade because it indicates that the price is most likely trending, which is bad for a mean reversion system. Conversely, when the fast ADX is below the slow ADX, the price is likely to be in a range, so this is the only time the algorithm is allowed to trade. II. Bollinger Bands When the trend filter allows trading, the algorithm uses Bollinger Bands.

Indicator for opening long and short positions. The Bolliger Bands indicator has a 20 lookback period and a 1.5 standard deviation for both the upper and lower bands. When the price crosses the lower band, a buy signal is generated and a long position is opened. When the price crosses the upper band, a sell signal is generated and a short position is opened.

Pattern 2:

Based on RSI which is commonly used as a trend reversal indicator. However, here it is used as a trend-setting indicator, often with great success. This pattern only takes long trades, which is quite successful in a bull market.

Pattern 3:

Long or short trades are determined by the intersection of the fast EMA with the slow EMA for long positions and vice versa for short positions. Trades should only occur close to intersections. We then use the MACD for the long position. an indicator with a 10-minute time frame where we look for high peaks in negative values for longs and vice versa for shorts. They should be significantly higher than the other peaks.

Capital Management:

The maximum leverage in this strategy, I would recommend 2x, in order to trade without unnecessary risks and keep your nerves in order.

Bot setup:

I use the Finandy terminal, in which you can easily trade with this strategy.

1. We go to binance and turn on the hedging mode, this is necessary so that if tradingview sends a webhook for buying later than for selling.

2. Adding a new signal to Finandy

2.1. Open tab

2.1.1. "Order side" Strategy

2.1.2. "Amount" Balance% x Leverage

2.1.3. We set the percentage of the order two times less than the one you want

2.1.4. "Shoulder" is twice as large as the one you want

2.2.Close tab

2.2.1. "Enebaled" tick

2.2.2. "Reverse / Close" Disable

3. Set a notification for this strategy.

4. Copy "Signal URL" and paste it into webhook on tradingview

5. Copy "Signal Message" and paste it into the message on tradingview

CryptoNite - Machine Learning Strategy (15Min Timeframe)Greeting Traders! I am back with another ML strategy. :D I kept my word with combining my machine learning algorithms from Python and integrating them into Tradingview. Thanks to Tradingview's new release of Pinescript v5 it is now possible. This strategy respects the Sortino Ratio and was created using 2 years of data for 50 different cryptocurrencies. That is a total of 100 years of data and 44,849 trades to create this strategy. Now let me tell you, my computer and I are exhausted. We both been at it non-stop for about two months everyday. I refine the strategy, and the computer runs 24/7 for a few days to spit out the best results into the terminal. It's been a good run so my computer will finally get some sleep tonight.

So let's talk a little about the features of the strategy. In the settings window, you'll see the Stoploss, Take Profit Parameters, and Date Range. You can change the Date Range, but I recommend to leave the SL/TP parameters how they are because the machine learning algo chose those input. If you wish to change them you are always welcome to do so but backtest results will change. For the Take Profit parameters you'll see on the left side you something labeled time duration(displayed in minutes) and on the right side you'll see take profit values. Let's talk a little bit how they work.

TP_values = {

"0": 0.102,

"133": 0.051,

"431": 0.039,

"963": 0

}

In python, the table looks like this but it is quite easy to understand in Tradingview.

From 0-133 minutes, the strategy is looking to the reach target point 1 at 10.2% profit.

From 133-431 minutes, the strategy is looking to the reach target point 2 at 5.1% profit.

From 431-963 minutes, the strategy is looking to the reach target point 3 at 3.9% profit.

From 963+ minutes, the strategy is looking to break even at 0% profit on target point 4.

Through each target point a sell trigger is active. It will look for the best time to sell even if TP has not been reached.

This helps the trade not stay open too long.

The last thing I need to mention is the textbox displayed on the right side of your chart. This textbox displays the current Take Profit value in dollar amount. So when you're in a trade you'll know what TP target has to be reached when the open trade is active. Throughout time, the target price changes depending how long the trade has been open. If you have any questions feel free to comment down below, and enjoy this strategy!

hamster-bot HD preset_2presets for users

// DESCRIPTION OF STRATEGY ver. 2

HiDeep Strategy

Author foresterufa

This is a counter-trend strategy that is gradually gaining a position against the trend at the best price.

A prerequisite for completing a position is the price exit from the internal channel on the chart and the appearance of the HiDeep indicator.

The condition for closing the position is touching the opposite side of the internal channel.

A condition for facilitating closure along the middle line of the channel, with high price volatility , is that the price touches the border of the external channel.

Input signals are generated by HiDeep indicators. Closing a position by moving averages.

HigherHigh LowerLow RATALGOHi Traders,

This is Trend following strategy.

This strategy calculates the higher high or lower low of a look back period. If the previous high or low is breached, a signal to enter market is given.

This strategy works well with regular candles and line charts if you find the right settings and chart time frame.

Give it a try with your settings & post your feedback and suggestion if any for improvement.

I had automate this strategy with broker using Trading view Alert feature to get some live results on NSE:Banknifty1!

MTF - Box Trading StrategyMultiTime Frame - Box Trading Strategies (MTF-BT))

How does it work ? The code uses dynamic levels and crossovers on higher time frames to identify trade calls.

Model 1 (Default) Uses a low risk model and Model 2 (Optional) Uses an aggressive model

How to Deploy / Use

As part of the Indicator there are a few choices the user can opt for

Box Resolution - The resolution of the higher time frame for analysis , typically set at 90 , can be customized by the users.

Use Long Strategy 1 - This would add long trades based on Model1 Algorithm for the users

Use Short Strategy 1 - This would add short trades based on Model1 Algorithm for the users

Use Long Strategy 2 - This would add long trades based on Model2 Algorithm for the users

Use Short Strategy 2 - This would add short trades based on Model2 Algorithm for the users

Check Range Val Validate the width of the channel on higher timeframe and trade only when the channel is wider than the value provided ,

The value of 0.14 is determined using series of back test across various assets

Use Stop Loss : Flag to check if Stop Loss should be done by the strategy

Stop Loss Limit : Stop Loss in Absolute terms

Use Profit Booking : Flag to check if Profit Booking should be done by the strategy

Stop Loss Limit : Profit Target in Absolute terms

Do Intraday Exit :Flag to check if trade should be taken as an Intraday only

Exit Window : Session time during which the trade should be closed , like 15:00 - 15:30 for NSE , 22:30 - 23:00 for MCX etc ,

it should be wide enough to accommodate the resolution the use has on the screen

Visual Checks - The user could manually validate the back test results on various assets they would like to use this strategy on before putting it live.

Usage/Markets : Index Trading / Equities and also well with Commodities and Currencies

Time Frame : works well between 3 and 30 , keep the Box resolution to at least 45 for 3/5 mins TF and you could move upto 180 (3 hrs ) for a 30 mins TF.

Strategy Settings Used/Assumed : All of this values are provided in the Properties Tab of the Indicator Settings

and the users can customize it to suit the broker or the product they are charting it against

Initial Capital : 100 000

Order Size : 10 Quantities for Equities , you may change it to 1 lot for Future contracts based on capital deployed

Commission : is set at 0.05%

Slippage : 20 ticks

Recalculate Option : After the Order is filled is selected by default

Disclaimer : There could be scenarios when the breakout/breakdown candle is rejected , especially when it is long one

so it is always recommended to have a confirmation candle that open-closes above the breakout candle / open-closes below the breakdown candle

If you like it and find it useful or if you find a defect or bug , Please let us know in the comments .. that would encouraging !! for us to develop it further

Thank you and have a beautiful and Profitable trading session !

How to get access

Please click on the link / email in the signature or send me a private message to get access

Feedback

Please click on the link/email in the signature or send me a private message for suggestions/feedbacks

GreenCrypto Strategy

This strategy majorly uses MA, Tilson and S&R. MA is used for predicting the trend, Instead of normal cross-over of the MA, we are calculating the trend of the MA itself (whether MA is moving upward or downward by comparing the previous and current value of MA), along with MA we also use Tilson to calculate the MA.

Once we have MA and Tilson we take average and merge both MA and Tilson MA to get a double confirmation on the trend of the market. for entry and exit we use S&R with the merged MA, if the trend change is at the support or resistance level we go for LONG/SHORT respectively. Here we are doing continuous LONG+SHORT position, this provides more opportunity to capture unexpected market trend.

Enter a Long Trade when the script shows "Long" and exit either when you get "Short" signal or when it meets your target.

Parameters:

"Use 1:EST, 2:SST, 3:HST ?" : Select EMA , SMA or HullMA (works best on HullMA)

Length: Length of the EMA / SMA /HullmA

Factor: Used for calculation of Tilson and the Support and resistance .

Date/month/day : for selecting the right backtesting the period (currently it set to Jan 2018 to current day )

for this backtesting i have used 1000$ capital and 0.02% commission for each trade.

This strategy works best on 4H time fram but you can also use it on 1 day or higher timeframe charts

The default config present in this script is designed for ETH but it will also work with other coins)

Config for Specific Crypto coins (Please feel free to try out other configs also) :

ADA, BNB, EOS : "Use 1:EST, 2:SST, 3:HST ?" = 3

"Length" = 8

"Factor" = 0.9

ETC, XLM : "Use 1:EST, 2:SST, 3:HST ?" = 3

"Length" = 8

"Factor" = 0.85

Please DM me if you would like to tryout 7 Days free trail.

The Profit Gate | Tier 1 Script | v1.0.0This script is used to optimized the trend of the stock based on volume , and many kind of moving average. You can use this to swing, or get the idea of long hold play. This work for Crypto as well as penny stock.

This script is best for Penny Stock, Big Cap, Crypto. It is generally based on the idea of averaging move of previous candles as well as current volume . This means if we have our candles at 15m, it will capture bunch of previous candles up to 10 years ahead to get an average move. This will give us a prediction of whether or not a stock will move up (Buy), or go down (Sell).

General Buy|Sell Tier 1

This script is used to optimized the trend of the stock based on volume , and many kind of moving average. You can use this to swing, or get the idea of long hold play. This work for Crypto as well as penny stock.

This script is best for Penny Stock, Big Cap, Crypto. It is generally based on the idea of averaging move of previous candles as well as current volume . This means if we have our candles at 15m, it will capture bunch of previous candles up to 10 years ahead to get an average move. This will give us a prediction of whether or not a stock will move up (Buy), or go down (Sell).

We also use Binary entropy function to optimize the original MACD .

This indicator should be able to tell you where to get in, out, or start to set trailing stop loss on the current position. I will constantly update this algorithm.

Trend analysis, This is ridge model that take in past data from the nearest certain number of candles then predict the next trend by an algorithm.

We also have standard deviation so we can apply it to find the best strike price with the highest probability to get ITM

Please DM me for access to this script

TC Chart Score StrategyThis is My Call Confidence Strategy

The Strategy is designed to help confirm a bullish reversal after a downtrend.

This uses custom weighted algorithm

The Algorithm combines directional movement, volume over average, and moving averages to formulate a score.

The score is then used in conjunction with a smoothed score of the same criteria to initiate a buy signal on a cross over.

The settings are designed to help you customize how you weight directional movement, and the moving averages to further finetune the algorithm to your timelines.

The default settings are designed to be used on a 1 hour time frame.

You can change the settings for other time frames to further increase effectiveness.

This script will be updated as needed if a better algorithm is designed.

RAT Moving Average Crossover StrategyThis is based on general moving average crossovers but some modifications made to generate buy sell signals.

[B] hamster-bot ZZ Breakout reversal strategyAttention! This is a beta version of the strategy script >> <<

A backtest should only be done if you understand how the options work. Otherwise, do a test in the release version

Wildfire [v1]Lower time frame trading strategy with a very simple algorithm and adjustable parameters.

Backtest result shown is from 1st Jan 2018.

Tested with BTCUSD 30m Bitfinex and ETHUSD 30m. Approaches to addressing the drawdown are in development, however the algo in general seems very workable. Prelim tests in other markets encouraging. I have another bot called WARBASTARD which operates in higher timeframes (4hrs) and has far more acceptable drawdown figures.

Invite only, sorry.

Trend Flow & Breakout Professional [Strategy]Description:

🌪️ Overview

Stop guessing. Start following the flow.

The Trend Flow & Breakout Professional is a high-precision visual trading system designed to solve the biggest problem traders face: Choppy Markets & Fakeouts.

Instead of relying on lagging indicators that generate false signals, this engine uses a proprietary "Momentum Alignment Algorithm" to identify when price action is entering a genuine expansion phase. It transforms complex trend data into a clean, easy-to-read visual roadmap, allowing you to catch the meat of the move while filtering out the noise.

🔮 Key Features

1. The "Traffic Light" Visual System Trading is 90% psychology. This script reduces mental fatigue by coloring the chart background to reflect the dominant market state:

🟢 Green Zone (Bullish Flow): Momentum is accelerating upwards. The system suggests holding long positions and ignoring minor pullbacks.

🔴 Red Zone (Bearish Flow): Structure has broken down. The system suggests defensive measures or short entries.

Note: The background remains active as long as the trend structure holds, preventing you from exiting trades too early.

2. Smart Noise Filtering Unlike standard crossover strategies that get destroyed in sideways ranges, this system includes a Multi-Layer Trend Filter. It only triggers a signal when:

Short-term momentum aligns perfectly with the medium-term direction.

Volatility expands significantly (breakout confirmation).

Price successfully clears key long-term structural resistance (The "Blue Sky" Zone).

3. Built-in "Smart Strategy" Backtester We have integrated a professional-grade position management module. You can customize how the strategy executes trades in the settings:

Mode A: Sniper (Trend Reversal): Enters heavily on the first confirmed breakout and holds until the trend reverses. Ideal for swing traders.

Mode B: Builder (Pyramiding): Adds to the position incrementally as the trend confirms its strength, maximizing profit during strong runs.

4. Cooldown Mechanism To prevent over-trading, the algorithm includes a smart "Cooldown Period" that prevents signal spamming during high-volatility consolidations.

⚙️ How to Trade This System

Wait for the Signal:

Look for the "Buy" / "Sell" labels accompanied by a bright Neon Candle.

Ensure the background color shifts (e.g., from Grey/Red to Green).

Ride the Zone:

Do not exit just because of one red candle. As long as the Background remains Green, the trend is healthy.

The background color acts as your "psychological anchor," helping you let profits run.

Exit / Reversal:

A complete background color flip (e.g., Green to Red) indicates a structural trend failure. This is your signal to close positions or flip directions.

⚠️ Disclaimer

This tool is for educational and technical analysis purposes only. Past performance does not guarantee future results. Always use proper risk management.

GraalSTRATEGY DESCRIPTION — “GRAAL”

GRAAL is an advanced algorithmic crypto-trading strategy designed for trend and semi-trend market conditions. It combines ATR-based trend/flat detection, dynamic Stop-Loss and multi-level Take-Profit, break-even (BE) logic, an optional trailing stop, and a “lock-on-trend” mechanism to hold positions until the market structure truly reverses.

The strategy is optimized for Binance, OKX and Bybit (USDT-M and USDC-M futures), but can also be used on spot as an indicator.

Core Logic

Trend Detection — dynamic trend zones built using ATR and local high/low structure.

Entry Logic — positions are opened only after trend confirmation and a momentum-based local trigger.

Exit Logic:

fixed TP levels (TP1/TP2/TP3),

dynamic ATR-based SL,

break-even move after TP1 or TP2,

optional trailing stop.

Lock-on-Trend — positions remain open until an opposite trend signal appears.

Noise Protection — flat filter disables entries during low-volatility conditions.

Key Advantages

Sophisticated and reliable risk-management system.

Minimal false entries due to robust trend filtering.

Optional trailing logic to maximize profit during strong directional moves.

Works well on BTC, ETH and major altcoins.

Easily adaptable for various timeframes (1m–4h).

Supports full automation via OKX / WunderTrading / 3Commas JSON alerts.

Recommended Use Cases

Crypto futures (USDT-M / USDC-M).

Intraday trading (5m–15m–1h).

Swing trading (4h–1D).

Fully automated signal-bot execution.

Important Notes

This is an algorithmic strategy, not financial advice.

Strategy Tester performance may differ from real execution due to liquidity, slippage and fees.

Always backtest and optimize parameters for your specific market and asset.

Recommended Settings: LONG only, no TP, no SL, Flat Policy: Hold, TP3 Mode: Trend, Trailing Stop 1.2%, Fixed size 100 USD, Leverage 10×, ATR=14, HH/LL=36.

RastaRasta — Educational Strategy (Pine v5)

Momentum · Smoothing · Trend Study

Overview

The Rasta Strategy is a visual and educational framework designed to help traders study momentum transitions using the interaction between a fast-reacting EMA line and a slower smoothed reference line.

It is not a signal generator or profit system; it’s a learning tool for understanding how smoothing, crossovers, and filters interact under different market conditions.

The script displays:

A primary EMA line (the fast reactive wave).

A Smoothed line (using your chosen smoothing method).

Optional fog zones between them for quick visual context.

Optional DNA rungs connecting both lines to illustrate volatility compression and expansion.

Optional EMA 8 / EMA 21 trend filter to observe higher-time-frame alignment.

Core Idea

The Rasta model focuses on wave interaction. When the fast EMA crosses above the smoothed line, it reflects a shift in short-term momentum relative to background trend pressure. Cross-unders suggest weakening or reversal.

Rather than treating this as a trading “signal,” use it to observe structure, study trend alignment, and test how smoothing type affects reaction speed.

Smoothing Types Explained

The script lets you experiment with multiple smoothing techniques:

Type Description Use Case

SMA (Simple Moving Average) Arithmetic mean of the last n values. Smooth and steady, but slower. Trend-following studies; filters noise on higher time frames.

EMA (Exponential Moving Average) Weights recent data more. Responds faster to new price action. Momentum or reactive strategies; quick shifts and reversals.

RMA (Relative Moving Average) Used internally by RSI; smooths exponentially but slower than EMA. Momentum confirmation; balanced response.

WMA (Weighted Moving Average) Linear weights emphasizing the most recent data strongly. Intraday scalping; crisp but potentially noisy.

None Disables smoothing; uses the EMA line alone. Raw comparison baseline.

Each smoothing method changes how early or late the strategy reacts:

Faster smoothing (EMA/WMA) = more responsive, good for scalping.

Slower smoothing (SMA/RMA) = more stable, good for trend following.

Modes of Study

🔹 Scalper Mode

Use short EMA lengths (e.g., 3–5) and fast smoothing (EMA or WMA).

Focus on 1 min – 15 min charts.

Watch how quick crossovers appear near local tops/bottoms.

Fog and rung compression reveal volatility contraction before bursts.

Goal: study short-term rhythm and liquidity pulses.

🔹 Momentum Mode

Use moderate EMA (5–9) and RMA smoothing.

Ideal for 1 H–4 H charts.

Observe how the fog color aligns with trend shifts.

EMA 8 / 21 filter can act as macro bias; “Enter” labels will appear only in its direction when enabled.

Goal: study sustained motion between pullbacks and acceleration waves.

🔹 Trend-Follower Mode

Use longer EMA (13–21) with SMA smoothing.

Great for daily/weekly charts.

Focus on periods where fog stays unbroken for long stretches — these illustrate clear trend dominance.

Watch rung spacing: tight clusters often precede consolidations; wide rungs signal expanding volatility.

Goal: visualize slow-motion trend transitions and filter whipsaw conditions.

Components

EMA Line (Red): Fast-reacting short-term direction.

Smoothed Line (Yellow): Reference trend baseline.

Fog Zone: Green when EMA > Smoothed (up-momentum), red when below.

DNA Rungs: Thin connectors showing volatility structure.

EMA 8 / 21 Filter (optional):

When enabled, the strategy will only allow Enter events if EMA 8 > EMA 21.

Use this to study higher-trend gating effects.

Educational Applications

Momentum Visualization: Observe how the fast EMA “breathes” around the smoothed baseline.

Trend Transitions: Compare different smoothing types to see how early or late reversals are detected.

Noise Filtering: Experiment with fog opacity and smoothing lengths to understand trade-off between responsiveness and stability.

Risk Concept Simulation: Includes a simple fixed stop-loss parameter (default 13%) for educational demonstrations of position management in the Strategy Tester.

How to Use

Add to Chart → “Strategy.”

Works on any timeframe and instrument.

Adjust Parameters:

Length: base EMA speed.

Smoothing Type: choose SMA, EMA, RMA, or WMA.

Smoothing Length: controls delay and smoothness.

EMA 8 / 21 Filter: toggles trend gating.

Fog & Rungs: visual study options only.

Study Behavior:

Use Strategy Tester → List of Trades for entry/exit context.

Observe how different smoothing types affect early vs. late “Enter” points.

Compare trend periods vs. ranging periods to evaluate efficiency.

Combine with External Tools:

Overlay RSI, MACD, or Volume for deeper correlation analysis.

Use replay mode to visualize crossovers in live sequence.

Interpreting the Labels

Enter: Marks where fast EMA crosses above the smoothed line (or when filter flips positive).

Exit: Marks where fast EMA crosses back below.

These are purely analytical markers — they do not represent trade advice.

Educational Value

The Rasta framework helps learners explore:

Reaction time differences between moving-average algorithms.

Impact of smoothing on signal clarity.

Interaction of local and global trends.

Visualization of volatility contraction (tight DNA rungs) and expansion (wide fog zones).

It’s a sandbox for studying price structure, not a promise of profit.

Disclaimer

This script is provided for educational and research purposes only.

It does not constitute financial advice, trading signals, or performance guarantees. Past market behavior does not predict future outcomes.

Users are encouraged to experiment responsibly, record observations, and develop their own understanding of price behavior.

Author: Michael Culpepper (mikeyc747)

License: Educational / Open for study and modification with credit.

Philosophy:

“Learning the rhythm of the market is more valuable than chasing its profits.” — Rasta

Strategy Builder v1.0.0 [BigBeluga]🔵 OVERVIEW

The Strategy Builder combines advanced price-action logic, smart-money concepts, and volatility-adaptive momentum signals to automate high-quality entries and exits across any market. It blends trend recognition, market structure shifts, order block reactions, imbalance (FVG) signals, liquidity sweeps, candlestick confirmations, and oscillator-powered divergences into one cohesive engine.

Whether used as a full automation workflow or as a structured confirmation framework, this strategy provides a disciplined, rules-driven method to trade with logic — not emotion.

🔵 BACKTEST WINDOW CONTROL

This module allows you to restrict strategy execution to a specific historical period.

Ideal for performance isolation, regime testing, and forward-walk validation.

Limit Backtest Window

Enabling this option activates custom date filters for the backtest engine.

Start — Define the starting date & time for backtesting

End — Define the ending date & time for backtesting

Only trades and signals inside this window are executed

Reduces computation load on large datasets

Useful for testing specific market environments (e.g., bull cycles, crash periods, sideways regimes)

🔵 SIGNAL GLOSSARY (Advanced Technical Explanation)

Traders can build long and short setups using up to 6 configurable entry conditions for each direction.

Every condition can be set as Bullish or Bearish and mapped to any signal source — allowing deep customization

Below is the full internal logic overview of every signal available in the Strategy Builder.

Signals are based on trend models, volatility structures, liquidity logic, oscillator behavior, and market structure mapping.

Trend Signals (Low-Lag Trend Engine)

Uses a proprietary low-lag baseline + momentum gradient model to detect directional bias.

Trend Signal — Momentum breaks above/below adaptive trend baseline.

Trend Signal+ — Stronger trend confirmation using volatility-weighted momentum.

Trend Signal Any — Triggers when any bullish/bearish trend signal appears.

SmartBand & Retests (Adaptive Volatility Bands)

Dynamic envelope that contracts/expands with volatility & trend strength.

SmartBand Retest — Price retests dynamic band and rejects, confirming continuation.

ActionWave Signals (Impulse-Pullback Engine)

Tracks wave behavior, acceleration and deceleration in price.

ActionWave — Detects directional impulse strength vs pullback weakness.

ActionWave Cross — Momentum acceleration threshold crossed → trend ignition.

Magnet Signals (Liquidity Gravity + Mean Reversion Bias)

Detects zones where price is being drawn due to liquidity voids or imbalance.

Magnet — Trend and liquidity pressure align, creating directional “pull.”

MagnetBar Low Momentum — Low-volatility compression → pre-breakout condition.

Flow Trend (Directional Flow State + ATR Envelope)

Higher-timeframe bias confirmation + dynamic volatility filter.

FlowTrend — Confirms major directional bias (uptrend or downtrend).

FlowTrend Retest — Price tests HTF flow band and rejects → trend resume.

Voltix (Volatility Expansion Pulse)

Detects regime shift from quiet accumulation → trending expansion.

Voltix — Breakout volatility signature, trend acceleration trigger.

Candlestick Pattern (Algorithmic Price Action Recognition)

Auto-recognizes meaningful reversal or continuation candle formations.

Candlestick Pattern — Confirms momentum reversal/continuation via candle logic.

OrderBlock Logic (Institutional Footprint System)

Institutional demand/supply zone tracking with mitigation logic.

Order Block Touch — Price taps institutional zone → reaction filter.

Order Block Break — OB invalidation → institutional flow shift.

Market Structure Engine (Swing Logic + Volume Confirmation)

Tracks major swing breaks and structural reversals.

BoS — Break of Structure in trend direction (continuation bias).

ChoCh — Change of Character — early reversal marker.

Fair Value Gaps (Imbalance & Volume Displacement)

Identifies inefficiencies caused by rapid displacement moves.

FVG Created — Price leaves inefficiency behind.

FVG Retest — Price returns to rebalance inefficiency → reaction zone.

Liquidity Events (Stop-Run & Reversal Logic)

Detects stop-hunt events and liquidity sweeps.

SFP — Swing failure & wick sweep → reversal confirmation.

Liquidity Created — New equal highs/lows form liquidity pool.

Liquidity Grab — Sweep through liquidity line followed by rejection.

Support / Resistance Break Logic

Adaptive zone recognition + momentum confirmation.

Support/Resistance Cross — Zone decisively broken → structural shift.

Pattern Breakouts (Market Geometry Engine)

Tracks breakout from compression & expansion formations.

Channel Break — Channel breakout → trend acceleration.

Wedge Break — Break from contraction wedge → burst of momentum.

Session Logic (Opening Range Behavior)

Session-based volatility trigger.

Session Break — Break above/below session opening range.

Momentum / Reversal Oscillator Suite

Oscillator-driven exhaustion & reversal signals.

Nautilus Signals — Momentum reversal signature (oscillator shift).

Nautilus Peak — Momentum peak → exhaustion risk.

OverSold/Overbought ❖ — Extreme exhaustion zones → reversal setup.

DipX Signals ✦ — Dip buy / Dip sell timing, micro-reversal engine.

Advanced Divergence Engine

Momentum/price disagreement layer with multi-trigger confirmation.

Normal Divergence — Classic divergence reversal.

Hidden Divergence — Trend continuation divergence.

Multiple Divergence — Multiple divergence confirmations stacked → high confidence.

🔧 Adjustable Signal Logic

Some signals in this system can be additionally refined through the strategy settings panel.

This allows traders to tune internal behavior for different market regimes, assets, and volatility conditions.

🔵 LONG / SHORT EXIT CONDITIONS

This section allows you to automate exits using the same advanced market conditions available for entries.

Each exit rule consists of:

Toggle — Enable/disable individual exit rule.

Direction Filter — Trigger exit only if selected market bias appears (Bullish/Bearish).

Signal Type — Choose which market event triggers the exit (same list as entry conditions).

When the active conditions are met, the strategy automatically closes the current position — ensuring emotion-free risk management and systematic trade control.

🔵 TAKE PROFIT & STOP LOSS SYSTEM

This strategy builder provides a fully dynamic risk-management engine designed for both systematic traders and discretionary confirmation users.

Take Profit Logic

Scale out of trades progressively or exit fully using algorithmic TP levels.

Up to 3 Take-Profit targets available

Choose TP calculation method:

• ATR-based distance (volatility-adaptive targets)

• %-based distance (fixed percentage from entry)

Define Size — ATR multiplier or % value

Custom Exit Size per TP (e.g., 25% / 25% / 50%)

Visual TP plotting on chart for clarity

Stop Loss Logic

Automated protection logic for every trade.

Two SL Modes:

• Fixed Stop Loss — static SL from entry

• Trailing Stop Loss — SL follows price as trade progresses

Distance options:

• ATR multiplier (adapts to volatility)

• %-based from entry (fixed distance)

SL dynamically draws on chart for transparency

Trailing SL behavior:

Follows price only in profitable direction

Never moves against the trade

Locks profits as trend develops

🔵 Strategy Dashboard

A compact on-chart performance dashboard is included to help monitor live trade status and backtest results in real time.

It displays key metrics:

Start Capital — Initial account balance used in simulation.

Position Size — % of capital allocated per trade based on user settings (It changes if the trade hits take profits, when more than one take profit is selected).

Current Trade — Shows active trade direction (Long / Short) and real-time % return from entry.

Closed Trades — Counter of completed positions, useful for reading sample size during testing.

🔵 CONCLUSION

The Strategy Builder brings together a powerful suite of smart-money and momentum-driven signals, allowing traders to automate robust trade logic built on modern market structure concepts. With access to trend filters, order blocks, liquidity events, divergence signals, volatility cues, and session-based triggers, it provides a deeply adaptive trade engine capable of fitting many market environments.

Mario vr SIT MC Utilizar en el gráfico

4

1

55

🧠 Market Structure Pro System – MVR

Market Structure Pro System – MVR is an advanced trading strategy designed to detect key reversal and trend-break zones with high precision.

It combines multiple professional tools within a single algorithm — integrating market structure, dynamic channels, volatility filters, and trend confirmations — making it ideal for scalping and swing trading across different markets (Forex, indices, cryptocurrencies, or stocks).

⚙️ How it works

The algorithm performs a complete structural analysis of the market through several technical layers:

🔹 1. Price Structure (BOS, Supply & Demand)

The system automatically detects:

Order Blocks

Supply and Demand Zones

Break of Structure (BOS) to identify market structure shifts

This allows traders to recognize where price is likely to react or break a trend, anticipating major market movements.

🔹 2. Keltner Channels and Linear Regression

The strategy uses multiple Keltner Channels with different settings to measure volatility expansion and contraction.

In combination, a dynamic linear regression line shows the overall market direction, helping confirm whether price is trending or ranging.

🔹 3. Volatility and Trend Filters

It integrates several complementary systems:

ATR (Average True Range): measures the strength and volatility of price movement.

PSAR (Parabolic SAR): identifies potential trend reversals.

Supertrend: acts as the main trend filter and confirmation tool.

These filters work together to avoid false signals in ranging or low-volatility conditions.

🔹 4. Swing Highs / Lows and Dynamic Lines

The indicator also marks swing high and low points, helping visualize dynamic support and resistance levels and potential price reversal areas.

📈 Signal Interpretation

BUY signals:

Occur when price breaks a demand zone or bearish structure, while trend filters (Supertrend / PSAR) confirm bullish direction.

SELL signals:

Trigger when price breaks a supply zone or bullish structure, with bearish confirmation from the trend filters.

These conditions can be further validated by visual confirmations from the Keltner Channel or a color change in the linear regression.

Script protegido

Este script se publica como código cerrado. Sin embargo, puede utilizarlo libremente y sin limitaciones: obtenga más información aquí.

mariovr_usd

Exención de responsabilidad

La información y las publicaciones que ofrecemos, no implican ni constituyen un asesoramiento financiero, ni de inversión, trading o cualquier otro tipo de consejo o recomendación emitida o respaldada por TradingView. Puede obtener información adicional en las Condiciones de uso.

1 comentario

AI-JX Strategy### 🤖 Core Features

AI-JX v3.3 is an AI-powered comprehensive trading strategy system developed with PineScript v6, integrating multiple advanced technical analysis tools and machine learning algorithms.

### 📊 Main Functional Modules 1. AI Learning System

- Adaptive Parameter Optimization : Automatically learns and adjusts trading parameters

- Three Strategy Modes : Conservative (ranging markets), Aggressive (trending markets), Balanced (universal)

- Dynamic Weight Adjustment : Intelligently allocates weights to different strategies based on market conditions

- Learning Memory Mechanism : Records historical trading data for continuous strategy optimization 2. Technical Indicator System

- SuperTrend Indicator : ATR-based trend following system

- Heikin Ashi Smoothing : Reduces market noise for clearer trend signals

- Standard Deviation Channels : Multi-level support and resistance analysis

- Trend Distribution Profile : Visualizes price distribution and trend strength

- Multi-Timeframe Analysis : Comprehensive analysis across 5m, 15m, and 1h timeframes 3. Intelligent Signal Generation

- Traditional Signals : Classic buy/sell signals based on SuperTrend

- AI Smart Signals : Comprehensive scoring system combining RSI, MACD, and ATR

- False Breakout Detection : Identifies and filters fake breakout signals

- Price Confirmation Mechanism : Ensures signal validity and reliability 4. Risk Management System

- Dynamic Stop Loss/Take Profit : Long 3% TP/1.5% SL, Short 2:1 risk-reward ratio

- Slippage Monitoring : Real-time market slippage risk assessment

- Volatility Filtering : Adjusts trading strategy based on ATR

- Position Management : Smart capital allocation and risk control 5. Visualization Panels

- Statistics Panel : Displays key data like trade count, win rate, current strategy

- AI Learning Panel : Shows strategy weights and learning progress

- Prediction Panel : Real-time AI analysis and trading recommendations

- Chart Markers : Clear buy/sell signals and trend line displays 6. Alert System

- Multiple Alert Types : Buy, sell, take profit, and stop loss notifications

- Personalized Messages : Fun "WangWang" themed alert messages

- Real-time Notifications : Precise alerts with maximum one per bar frequency

### 🎯 Key Advantages

- AI-Driven : Machine learning optimization for better performance

- Multi-Strategy : Adapts to different market conditions automatically

- Risk-Controlled : Comprehensive risk management with dynamic adjustments

- User-Friendly : Intuitive interface with detailed visualization panels

- Highly Customizable : Extensive parameter settings for different trading styles

TTE Elite Market SignalsWelcome to TTE Elite Market Signals Your very own personal trading assistant

Trading today demands more than intuition—it requires exclusive access to elite-level market intelligence and the discipline to act on high-probability signals. Every professional trader seeks that decisive advantage: the clarity and confidence that separates consistent profitability from market uncertainty. The financial markets show no mercy, demanding precision, logic, and strategy grounded in institutional-grade analysis.

Human judgment, while powerful, can be compromised by fatigue and emotion, leading to costly trading errors. This is precisely where TTE Elite Market Signals excels. Our sophisticated platform combines proven trading methodologies with advanced signal generation technology, delivering market intelligence that empowers you to identify optimal entry and exit opportunities while maintaining complete control over your trading decisions.

Revolutionary Signal Intelligence

TTE Elite Market Signals features adaptive learning technology that evolves with market conditions. It continuously refines its analysis, helping you identify higher-probability setups while providing the market intelligence needed for superior risk management.

Elite Analysis Modes

Our platform adapts its signal generation to match market personalities:

- Institutional Flow Mode (MM-hybrid): Identifies manipulation patterns and tracks smart money movement with exclusive institutional-grade precision

- Momentum Adaptive Mode: Rapidly adjusts analysis when volatility and momentum shift

- Conservative Precision Mode: Steady, risk-conscious signals for consistent performance

- Adaptive Intelligence Mode: Self-refining system that enhances signal quality over time from past trades (long term of use)

Comprehensive Signal Intelligence

TTE Elite Market Signals integrates multiple sophisticated analytical systems:

- Volume Profile analysis for exclusive institutional-level market insights

- Pattern recognition enhanced by machine learning algorithms

- Intelligent exit timing that identifies optimal profit-taking opportunities

- Protection against market manipulation tactics

- Position sizing guidance that scales with trading success

- Fibonacci based reversal logic

Perfect for Your Trading Evolution

Experienced traders appreciate our sophisticated market intelligence and institutional-grade analytics that provide genuine competitive advantages.

Developing traders benefit from intelligent signal analysis that handles complex market calculations while teaching professional-level market interpretation and risk management principles via visuals on chart and descriptive panel.

All timeframes supported—from scalping to swing trading, TTE Elite Market Signals adapts to your preferred trading style via several user input selections.

Two Elite Service Modes

1. Signal Intelligence Mode: Real-time market signals with AI-driven analysis and detailed trade rationale

2. Alert Precision Mode: High-probability setup notifications with comprehensive market context and risk parameters

The Exclusive Learning Advantage

What makes TTE Elite Market Signals exceptional: it maintains a comprehensive trade memory and identifies the highest-probability signals, adapts to changing volatility patterns, and continuously refines(does not repaint) its analysis to enhance your profit potential and trading accuracy.

Built-in Professional Protection

- Advanced manipulation detection safeguards against institutional market maker(MM) tactics

- Intelligent risk assessment adjusts signal confidence based on market conditions

- Progressive scaling guidance maximizes winners while minimizing losses(educational)

- Comprehensive oversight with customizable risk parameters

Experience the Elite Difference

TTE gives you visuals on the chart of past trades and live metrics results to see what actually work and what fails, to minimize unrealistic expectations. Just sit back and watch sophisticated algorithms work tirelessly on your behalf, identifying opportunities that others miss and alerting you as signals are generated. Transforming the stressful, emotional battlefield of trading into a systematic analytical approach.

Let the System Do the Heavy Lifting

While others struggle with analysis paralysis and emotional decision-making, you'll have access to signals that have already processed hundreds of data points, identified institutional patterns, and calculated optimal risk-reward scenarios for a far less stressful trading experience.

What Elite Traders Should Know

TTE Elite Market Signals represents cutting-edge signal generation technology designed for serious market education and skill development, but it is not a black box, nor perfect for all markets. It must be adjusted to yield optimal results. While our advanced capabilities and institutional-grade features provide significant analytical advantages, trading success requires discipline and proper execution. Markets evolve, and optimal results demand understanding of signal context.

Success with TTE Elite Market Signals comes from mastering our analytical modes and using the proper entry types such as breakout entry, machine learning(ML) entry etc, utilizing and selecting the most effective risk control to optimize it, and maintaining disciplined risk management.

Join the Elite Trading Revolution

This isn't just another signal service—it equips you with the tools to do proper market analysis displaying price movement and volume profile designed for serious traders who understand that consistent profitability comes from discipline, superior market intelligence and proper interpretation, not luck.

Trade smart, stay profitable, and achieve trading excellence.

Best TTE Settings

Trade Entry Types:

1st Best Breakout Entry(out perform all others when used alone)

2nd Best ML Entry by itself or + Pattern Entry Combined

Risk Management:

ATR Multiplier 2

Enable Master Size Control

Master Size Mode

Max Risk Per Trade % 2.5

Max Multiplier Cap 1.5

Enable Growth Scaling

Growth Scaling Mode-set to Time Based or Performance

Risk Management System- set to Hybrid

Enable ML System

ML Mode-set to Auto or Quantum Learning

ML Application Strategy-set to Universal All Entries

Enable Trend Continuation

Mode- Set to Standard

Independent Entry-stays unchecked(off)

Best Performing Instruments on TTE (will update list as more are adjusted and tested)

NVDA

AMD

AMZN

TSLA

SPY

QQQ

PLTR

Setup: Smooth Gaussian + Adaptive Supertrend (Manual Vol)Overview

This strategy combines two powerful trend-based tools originally developed by Algo Alpha: the Smooth Gaussian Trend (simulated) and the Adaptive Supertrend. The objective is to capture sustained bullish movements in periods of controlled volatility by filtering for high-probability entries.

Entry Logic

Long Entry Conditions:

The closing price is above the Smooth Gaussian Trend line (with length = 75), and

The volatility setting from the Adaptive Supertrend is manually defined as either 2 or 3

Exit Condition:

The closing price falls below the Smooth Gaussian Trend line

This script uses a simulated version of the Gaussian Trend line via double-smoothed SMA, as the original Algo Alpha indicator is protected and cannot be accessed directly in code.

Features

Plots entry and exit signals directly on the chart

Manual toggle to enable or disable the volatility filter

Lightweight design to allow flexible backtesting even without access to proprietary indicators

Important Note

This strategy does not connect to the actual Adaptive Supertrend from Algo Alpha. Users must manually input the volatility level based on what they observe on the chart when the original indicator is also applied. The Smooth Gaussian Trend is approximated and may differ slightly from the original.

Suggested Use

Recommended timeframes: 1H, 4H, or Daily

Best used alongside the original indicators displayed on the chart

Consider incorporating additional structure, momentum, or volume filters to enhance performance

If you have suggestions or would like to contribute improvements, feel free to reach out or fork the script.

Long-Leg Doji Breakout StrategyThe Long-Leg Doji Breakout Strategy is a sophisticated technical analysis approach that capitalizes on market psychology and price action patterns.

Core Concept: The strategy identifies Long-Leg Doji candlestick patterns, which represent periods of extreme market indecision where buyers and sellers are in equilibrium. These patterns often precede significant price movements as the market resolves this indecision.

Pattern Recognition: The algorithm uses strict mathematical criteria to identify authentic Long-Leg Doji patterns. It requires the candle body to be extremely small (≤0.1% of the total range) while having long wicks on both sides (at least 2x the body size). An ATR filter ensures the pattern is significant relative to recent volatility.

Trading Logic: Once a Long-Leg Doji is identified, the strategy enters a "waiting mode," monitoring for a breakout above the doji's high (long signal) or below its low (short signal). This confirmation approach reduces false signals by ensuring the market has chosen a direction.

Risk Management: The strategy allocates 10% of equity per trade and uses a simple moving average crossover for exits. Visual indicators help traders understand the pattern identification and trade execution process.

Psychological Foundation: The strategy exploits the natural market cycle where uncertainty (represented by the doji) gives way to conviction (the breakout), creating high-probability trading opportunities.

The strength of this approach lies in its ability to identify moments when market sentiment shifts from confusion to clarity, providing traders with well-defined entry and exit points while maintaining proper risk management protocols.

How It Works

The strategy operates on a simple yet powerful principle: identify periods of market indecision, then trade the subsequent breakout when the market chooses direction.

Step 1: Pattern Detection

The algorithm scans for Long-Leg Doji candles, which have three key characteristics:

Tiny body (open and close prices nearly equal)

Long upper wick (significant rejection of higher prices)

Long lower wick (significant rejection of lower prices)

Step 2: Confirmation Wait

Once a doji is detected, the strategy doesn't immediately trade. Instead, it marks the high and low of that candle and waits for a definitive breakout.

Step 3: Trade Execution

Long Entry: When price closes above the doji's high

Short Entry: When price closes below the doji's low

Step 4: Exit Strategy

Positions are closed when price crosses back through a 20-period moving average, indicating potential trend reversal.

Market Psychology Behind It

A Long-Leg Doji represents a battlefield between bulls and bears that ends in a stalemate. The long wicks show that both sides tried to push price in their favor but failed. This creates a coiled spring effect - when one side finally gains control, the move can be explosive as trapped traders rush to exit and momentum traders jump aboard.

Key Parameters

Doji Body Threshold (0.1%): Ensures the body is truly small relative to the candle's range

Wick Ratio (2.0): Both wicks must be at least twice the body size

ATR Filter: Uses Average True Range to ensure the pattern is significant in current market conditions

Position Size: 10% of equity per trade for balanced risk management

Pros:

High Probability Setups: Doji patterns at key levels often lead to significant moves as they represent genuine shifts in market sentiment.

Clear Rules: Objective criteria for entry and exit eliminate emotional decision-making and provide consistent execution.

Risk Management: Built-in position sizing and exit rules help protect capital during losing trades.

Market Neutral: Works equally well for long and short positions, adapting to market direction rather than fighting it.

Visual Confirmation: The strategy provides clear visual cues, making it easy to understand when patterns are forming and trades are triggered.

Cons:

False Breakouts: In choppy or ranging markets, price may break the doji levels only to quickly reverse, creating whipsaws.

Patience Required: Traders must wait for both pattern formation and breakout confirmation, which can test discipline during active market periods.

Simple Exit Logic: The moving average exit may be too simplistic, potentially cutting profits short during strong trends or holding losers too long during reversals.

Volatility Dependent: The strategy relies on sufficient volatility to create meaningful doji patterns - it may underperform in extremely quiet markets.

Lagging Entries: Waiting for breakout confirmation means missing the very beginning of moves, reducing potential profit margins.

Best Market Conditions

The strategy performs optimally during periods of moderate volatility when markets are making genuine directional decisions rather than just random noise. It works particularly well around key support/resistance levels where the market's indecision is most meaningful.

Optimization Considerations

Consider combining with additional confluence factors like volume analysis, support/resistance levels, or other technical indicators to improve signal quality. The exit strategy could also be enhanced with trailing stops or multiple profit targets to better capture extended moves while protecting gains.

Best for Index option,

Enjoy !!

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions