Trend Following Strategy with KNN

### 1. Strategy Features

This strategy combines the K-Nearest Neighbors (KNN) algorithm with a trend-following strategy to predict future price movements by analyzing historical price data. Here are the main features of the strategy:

1. **Dynamic Parameter Adjustment**: Uses the KNN algorithm to dynamically adjust parameters of the trend-following strategy, such as moving average length and channel length, to adapt to market changes.

2. **Trend Following**: Captures market trends using moving averages and price channels to generate buy and sell signals.

3. **Multi-Factor Analysis**: Combines the KNN algorithm with moving averages to comprehensively analyze the impact of multiple factors, improving the accuracy of trading signals.

4. **High Adaptability**: Automatically adjusts parameters using the KNN algorithm, allowing the strategy to adapt to different market environments and asset types.

### 2. Simple Introduction to the KNN Algorithm

The K-Nearest Neighbors (KNN) algorithm is a simple and intuitive machine learning algorithm primarily used for classification and regression problems. Here are the basic concepts of the KNN algorithm:

1. **Non-Parametric Model**: KNN is a non-parametric algorithm, meaning it does not make any assumptions about the data distribution. Instead, it directly uses training data for predictions.

2. **Instance-Based Learning**: KNN is an instance-based learning method that uses training data directly for predictions, rather than generating a model through a training process.

3. **Distance Metrics**: The core of the KNN algorithm is calculating the distance between data points. Common distance metrics include Euclidean distance, Manhattan distance, and Minkowski distance.

4. **Neighbor Selection**: For each test data point, the KNN algorithm finds the K nearest neighbors in the training dataset.

5. **Classification and Regression**: In classification problems, KNN determines the class of a test data point through a voting mechanism. In regression problems, KNN predicts the value of a test data point by calculating the average of the K nearest neighbors.

### 3. Applications of the KNN Algorithm in Quantitative Trading Strategies

The KNN algorithm can be applied to various quantitative trading strategies. Here are some common use cases:

1. **Trend-Following Strategies**: KNN can be used to identify market trends, helping traders capture the beginning and end of trends.

2. **Mean Reversion Strategies**: In mean reversion strategies, KNN can be used to identify price deviations from the mean.

3. **Arbitrage Strategies**: In arbitrage strategies, KNN can be used to identify price discrepancies between different markets or assets.

4. **High-Frequency Trading Strategies**: In high-frequency trading strategies, KNN can be used to quickly identify market anomalies, such as price spikes or volume anomalies.

5. **Event-Driven Strategies**: In event-driven strategies, KNN can be used to identify the impact of market events.

6. **Multi-Factor Strategies**: In multi-factor strategies, KNN can be used to comprehensively analyze the impact of multiple factors.

### 4. Final Considerations

1. **Computational Efficiency**: The KNN algorithm may face computational efficiency issues with large datasets, especially in real-time trading. Optimize the code to reduce access to historical data and improve computational efficiency.

2. **Parameter Selection**: The choice of K value significantly affects the performance of the KNN algorithm. Use cross-validation or other methods to select the optimal K value.

3. **Data Standardization**: KNN is sensitive to data standardization and feature selection. Standardize the data to ensure equal weighting of different features.

4. **Noisy Data**: KNN is sensitive to noisy data, which can lead to overfitting. Preprocess the data to remove noise.

5. **Market Environment**: The effectiveness of the KNN algorithm may be influenced by market conditions. Combine it with other technical indicators and fundamental analysis to enhance the robustness of the strategy.

Cerca negli script per "algo"

[Pandora] Error Function Treasure Trove - ERF/ERFI/Sigmoids+PRAISE:

At this time, I have to graciously thank the wonderful minds behind the new "Pine Profiler Mode" (PPM). Directly prior to this release, it allowed me to ascertain script performance even more. While I usually write mostly in highly optimized Pine code, PPM visually identified a few bottlenecks that would otherwise be hard to identify. Anyone who contributed to PPMs creation and testing before release... BRAVO!!! I commend all of those who assisted in it's state-of-the-art engineering and inception, well done!

BACKSTORY:

This script is specifically being released in defense of another member, an exceptionally unique PhD. It was brought to my attention that a script-mod-event occurred, regarding the publishing of a measly antiquated error function (ERF) calculation within his script. This sadly resulted in the now former member jumping ship after receiving unmannerly responses amidst his curious inquiries as to why his erf() was modded. To forbid rusty and rudimentary formulations because a mod-on-duty is temporally offended by a non-nefarious release of code, is in MY opinion an injustice to principles of perpetuating open-source code intended to benefit thousands to millions of community members. While Pine is the heart and soul of TV, the mathematical concepts contributed from the minds of members is the inspirational fuel of curiosity that powers it's pertinent reason to exist and evolve.

It is an indisputable fact that most members are not greatly skilled Pine Poets. Many members may be incapable of innovating robust function code in Pine, even if they have one or more PhDs. We ALL come from various disciplines of mathematical comprehension and education. Some mathematicians are not greatly skilled at coding, while some coders are not exceptional at math. So... what am I to do to attempt to resolve this circumstantial challenge??? Those who know me best are aware that I will always side with "the right side of history" in order to accomplish my primary self-defined missions I choose to accept. Serving as an algorithmic advocate, I felt compelled to intercede by compiling numerous error functions into elegant code of very high caliber that any and every TV member may choose to employ, so this ERROR never happens again.

After weeks of contemplation into algorithms I knew little about, I prioritized myself to resolve an unanticipated matter by creating advanced formulas of exquisitely crafted error functions refined to the best of my current abilities. My aversion for unresolved problems motivated me to eviscerate error function insufficiencies with many more rigid formulations beyond what is thought to exist. ERF needed a proper algorithmic exorcism anyways. In my furiosity, I contemplated an array of madMAXimum diplomatic demolition methods, choosing the chain saw massacre technique to slaughter dysfunctionalities I encountered on a battered ERF roadway. This resulted in prolific solutions that should assuredly endure the test of time. Poetically, as you will come to see, I am ripping the lid off of Pandora's box of error functions in this case to correct wrongs into a splendid bundle of rights for members.

INTENTION:

Error function (ERF) enthusiasts... PREPARE FOR GLORY!! The specific purpose of this script is to deprecate classic error functions with the creation of a fierce and formidable army of superior formulations, each having varying attributes of computational complexity with differing absolute error ranges in their results for multiple compute scenarios. This is NOT an indicator... It is intended to allow members to embark on endeavors to advance the profound knowledge base of this growing worldwide community of 60+ million inquisitive minds. For those of you who believe computational mathematics and statistics is near completion at its finest; I am here to inform you, this is ridiculous to ponder. We are no where near statistical excellence that can and will exist eventually. At this time, metaphorically speaking, we are merely scratching microns off of the surface of the skin of a statistical apple Isaac Newton once pondered.

THIS RELEASE:

Following weeks of pondering methodical experiments beyond the ordinary, I am liberating these wild notions of my error function explorations to the entire globe as copyleft code, not just Pine. This Pandora's basket of ERFs is being openly disclosed for the sake of the sanctity of mathematics, empirical science (not the garbage we are told by CONTROLocrats to blindly trust), revolutionary cutting edge engineering, cosmology, physics, information technology, artificial intelligence, and EVERY other mathematical branch of human knowledge being discovered over centuries. I do believe James Glaisher would favor my aims concerning ERF aspirations embracing the "Power of Pine".

The included functions are intended for TV members to use in any way they see fit. This is a gift to ALL members to foster future innovative excellence on this platform. Any attempt to moderate this code without notification of "self-evident clear and just cause" will be considered an irrevocable egregious action. The original foundational PURPOSE of establishing script moderation (I clearly remember) was primarily to maintain active vigilance over a growing community against intentional nefarious actions and/or behaviors in blatant disrespect to other author's works AND also thwart rampant copypasting bandit operations, all while accommodating balanced principles of fairness for an educational community cause via open source publishing that should support future algorithmic inventions well beyond my lifespan.

APPLICATIONS:

The related error functions are used in probability theory, statistics, and numerous and engineering scientific disciplines. Its key characteristics and applications are innumerable in computational realms. Its versatility and significance make it a fundamental tool in arenas of quantitative analysis and scientific research...

Probability Theory - Is widely used in probability theory to calculate probabilities and quantiles of the normal distribution.

Statistics - It's related to the Gaussian integral and plays a crucial role in statistics, especially in hypothesis testing and confidence interval calculations.

Physics - In physics, it arises in the study of diffusion equations, quantum mechanics, and heat conduction problems.

Engineering - Applications exist in engineering disciplines such as signal processing, control theory, and telecommunications.

Error Analysis - It's employed in error analysis and uncertainty quantification.

Numeric Approximations - Due to its lack of a closed-form expression, numerical methods are often employed to approximate erf/erfi().

AI, LLMs, & MACHINE LEARNING:

The error function (ERF) is indispensable to various AI applications, particularly due to its relation to Gaussian distributions and error analysis. It is used in Gaussian processes for regression and classification, probabilistic inference for Bayesian networks, soft margin computation in SVMs, neural networks involving Gaussian activation functions or noise, and clustering algorithms like Gaussian Mixture Models. Improved ERF approximations can enhance precision in these applications, reduce computational complexity, handle outliers and noise better, and improve optimization and convergence, possibly leading to more accurate, efficient, and robust AI systems.

BONUS ALGORITHMS:

While ERFs are versatile, its opposite also exists in the form of inverse error functions (ERFIs). I have also included a modified form of the inverse fisher transform along side MY sigmoid (sigmyod). I am uncertain what sigmyod() may be used for, but it's a culmination of my examinations deep into "sigmoid domains", something I am fascinated by. Whatever implications it may possess, I am unveiling it along with it's cousin functions. For curious minds, this quality of composition seen here is ideally what underlies what I would term "Pandora functionality" that empowers my Pandora indication. I go through hordes of formulations, testing, and inspection to find what appears to be the most beneficial logical/mathematical equation to apply...

SCRIPT OPERATION:

To showcase the characteristics and performance of my ERF/ERFI formulations, I devised a multi-modal script. By using bar_index , I generated a broad sequence of numeric values to input into the first ERF/ERFI parameter. These sequences allow you to inspect the contours of the error function's outputs for both ERF and ERFI. When combined with compute-intensive precision functions (CIPFs), the polynomial function output values can be subtracted from my CIPFs to obtain results of absolute error, displaying the accuracy of the many polynomial estimation functions I tuned in testing for Pine's float environment.

A host of numeric input settings are wildly adjustable to inspect values/curvatures across the range of numeric input sequences. Very large numbers, such as Divisor:100,000,100/Offset:200,000,000 for ERF modes or... Divisor:100,000,100/Offset:100,000,000 for ERFI modes, will display miniscule output values calculated from input values in close proximity to 0.0 for the various estimates, similar to a microscope. ERFI approximations very near in proximity to +/-1.0 will always yield large deviations of absolute error. Dragging/zooming your chart or using the Offset input will aid with visually clipping off those ERFI extremes where float precision functions cannot suffice.

NOTICE:

perf() and perfi() are intended for precision computation (as good as it basically gets) in a float environment. However, they are CPU intensive (especially perfi). I wouldn't recommend these being used in ANY Pine script unless it's an "absolute necessity" to do so to accomplish your goal. I only built them to obtain "absolute error curvatures" of the error functions for the polynomial approximations. These are visible in the accuracy modes in the indicator Settings.

Bogdan Ciocoiu - Code runnerDescription

The Code Runner is a hybrid indicator that leverages other pre-configured, integrated open-source algorithms to help traders spot regular and continuation divergences.

The Code Runner specialises in integrating some of the most popular oscillators well known for their accuracy when scalping using divergence strategies.

Uniqueness

The Code Runner stands out as a one-stop-shop pack of oscillator algorithms that traders can further customise to spot divergences.

The indicator's uniqueness stands from its capability to recast each algorithm to apply to the same scale. This feature is achieved by manually adjusting the outputs of each algorithm to fit on a scale between +100 and -100.

Another benefit of the Code Runner comes from its standardisation of outputs, mainly consisting of lines. Showing lines enables traders to draw potential regular and continuation divergences quickly.

The indicator has been pre-configured to support scalping at 1-5 minutes.

Open-source

The Code Runner uses the following open-source scripts and algorithms:

www.tradingview.com

www.tradingview.com

www.tradingview.com

www.tradingview.com

www.tradingview.com

www.tradingview.com

www.tradingview.com

www.tradingview.com

These algorithms are available in the public domain either in TradingView space or outside (given their popularity in the financial markets industry).

Adaptive Average Vortex Index [lastguru]As a longtime fan of ADX, looking at Vortex Indicator I often wondered, where is the third line. I have rarely seen that anybody is calculating it. So, here it is: Average Vortex Index - an ADX calculated from Vortex Indicator. I interpret it similarly to the ADX indicator: higher values show stronger trend. If you discover other interpretation or have suggestions, comments are welcome.

Both VI+ and VI- lines are also drawn. As I use adaptive length calculation in my other scripts (based on the libraries I've developed and published), I have also included the possibility to have an adaptive length here, so if you hate the idea of calculating ADX from VI, you can disable that line and just look at the adaptive Vortex Indicator.

Note that as with all my oscillators, all the lines here are renormalized to -1..1 range unlike the original Vortex Indicator computation. To do that for VI+ and VI- lines, I subtract 1 from their values. It does not change the shape or the amplitude of the lines.

Adaptation algorithms are roughly subdivided in two categories: classic Length Adaptations and Cycle Estimators (they are also implemented in separate libraries), all are selected in Adaptation dropdown. Length Adaptation used in the Adaptive Moving Averages and the Adaptive Oscillators try to follow price movements and accelerate/decelerate accordingly (usually quite rapidly with a huge range). Cycle Estimators, on the other hand, try to measure the cycle period of the current market, which does not reflect price movement or the rate of change (the rate of change may also differ depending on the cycle phase, but the cycle period itself usually changes slowly).

VIDYA - based on VIDYA algorithm. The period oscillates from the Lower Bound up (slow)

VIDYA-RS - based on Vitali Apirine's modification of VIDYA algorithm (he calls it Relative Strength Moving Average). The period oscillates from the Upper Bound down (fast)

Kaufman Efficiency Scaling - based on Efficiency Ratio calculation originally used in KAMA

Fractal Adaptation - based on FRAMA by John F. Ehlers

MESA MAMA Cycle - based on MESA Adaptive Moving Average by John F. Ehlers

Pearson Autocorrelation* - based on Pearson Autocorrelation Periodogram by John F. Ehlers

DFT Cycle* - based on Discrete Fourier Transform Spectrum estimator by John F. Ehlers

Phase Accumulation* - based on Dominant Cycle from Phase Accumulation by John F. Ehlers

Length Adaptation usually take two parameters: Bound From (lower bound) and To (upper bound). These are the limits for Adaptation values. Note that the Cycle Estimators marked with asterisks(*) are very computationally intensive, so the bounds should not be set much higher than 50, otherwise you may receive a timeout error (also, it does not seem to be a useful thing to do, but you may correct me if I'm wrong).

The Cycle Estimators marked with asterisks(*) also have 3 checkboxes: HP (Highpass Filter), SS (Super Smoother) and HW (Hann Window). These enable or disable their internal prefilters, which are recommended by their author - John F. Ehlers . I do not know, which combination works best, so you can experiment.

If no Adaptation is selected ( None option), you can set Length directly. If an Adaptation is selected, then Cycle multiplier can be set.

The oscillator also has the option to configure the internal smoothing function with Window setting. By default, RMA is used (like in ADX calculation). Fast Default option is using half the length for smoothing. Triangle , Hamming and Hann Window algorithms are some better smoothers suggested by John F. Ehlers.

After the oscillator a Moving Average can be applied. The following Moving Averages are included: SMA , RMA, EMA , HMA , VWMA , 2-pole Super Smoother, 3-pole Super Smoother, Filt11, Triangle Window, Hamming Window, Hann Window, Lowpass, DSSS.

Postfilter options are applied last:

Stochastic - Stochastic

Super Smooth Stochastic - Super Smooth Stochastic (part of MESA Stochastic ) by John F. Ehlers

Inverse Fisher Transform - Inverse Fisher Transform

Noise Elimination Technology - a simplified Kendall correlation algorithm "Noise Elimination Technology" by John F. Ehlers

Momentum - momentum (derivative)

Except for Inverse Fisher Transform , all Postfilter algorithms can have Length parameter. If it is not specified (set to 0), then the calculated Slow MA Length is used. If Filter/MA Length is less than 2 or Postfilter Length is less than 1, they are calculated as a multiplier of the calculated oscillator length.

More information on the algorithms is given in the code for the libraries used. I am also very grateful to other TradingView community members (they are also mentioned in the library code) without whom this script would not have been possible.

Keltner Channel Enhanced [DCAUT]█ Keltner Channel Enhanced

📊 ORIGINALITY & INNOVATION

The Keltner Channel Enhanced represents an important advancement over standard Keltner Channel implementations by introducing dual flexibility in moving average selection for both the middle band and ATR calculation. While traditional Keltner Channels typically use EMA for the middle band and RMA (Wilder's smoothing) for ATR, this enhanced version provides access to 25+ moving average algorithms for both components, enabling traders to fine-tune the indicator's behavior to match specific market characteristics and trading approaches.

Key Advancements:

Dual MA Algorithm Flexibility: Independent selection of moving average types for middle band (25+ options) and ATR smoothing (25+ options), allowing optimization of both trend identification and volatility measurement separately

Enhanced Trend Sensitivity: Ability to use faster algorithms (HMA, T3) for middle band while maintaining stable volatility measurement with traditional ATR smoothing, or vice versa for different trading strategies

Adaptive Volatility Measurement: Choice of ATR smoothing algorithm affects channel responsiveness to volatility changes, from highly reactive (SMA, EMA) to smoothly adaptive (RMA, TEMA)

Comprehensive Alert System: Five distinct alert conditions covering breakouts, trend changes, and volatility expansion, enabling automated monitoring without constant chart observation

Multi-Timeframe Compatibility: Works effectively across all timeframes from intraday scalping to long-term position trading, with independent optimization of trend and volatility components

This implementation addresses key limitations of standard Keltner Channels: fixed EMA/RMA combination may not suit all market conditions or trading styles. By decoupling the trend component from volatility measurement and allowing independent algorithm selection, traders can create highly customized configurations for specific instruments and market phases.

📐 MATHEMATICAL FOUNDATION

Keltner Channel Enhanced uses a three-component calculation system that combines a flexible moving average middle band with ATR-based (Average True Range) upper and lower channels, creating volatility-adjusted trend-following bands.

Core Calculation Process:

1. Middle Band (Basis) Calculation:

The basis line is calculated using the selected moving average algorithm applied to the price source over the specified period:

basis = ma(source, length, maType)

Supported algorithms include EMA (standard choice, trend-biased), SMA (balanced and symmetric), HMA (reduced lag), WMA, VWMA, TEMA, T3, KAMA, and 17+ others.

2. Average True Range (ATR) Calculation:

ATR measures market volatility by calculating the average of true ranges over the specified period:

trueRange = max(high - low, abs(high - close ), abs(low - close ))

atrValue = ma(trueRange, atrLength, atrMaType)

ATR smoothing algorithm significantly affects channel behavior, with options including RMA (standard, very smooth), SMA (moderate smoothness), EMA (fast adaptation), TEMA (smooth yet responsive), and others.

3. Channel Calculation:

Upper and lower channels are positioned at specified multiples of ATR from the basis:

upperChannel = basis + (multiplier × atrValue)

lowerChannel = basis - (multiplier × atrValue)

Standard multiplier is 2.0, providing channels that dynamically adjust width based on market volatility.

Keltner Channel vs. Bollinger Bands - Key Differences:

While both indicators create volatility-based channels, they use fundamentally different volatility measures:

Keltner Channel (ATR-based):

Uses Average True Range to measure actual price movement volatility

Incorporates gaps and limit moves through true range calculation

More stable in trending markets, less prone to extreme compression

Better reflects intraday volatility and trading range

Typically fewer band touches, making touches more significant

More suitable for trend-following strategies

Bollinger Bands (Standard Deviation-based):

Uses statistical standard deviation to measure price dispersion

Based on closing prices only, doesn't account for intraday range

Can compress significantly during consolidation (squeeze patterns)

More touches in ranging markets

Better suited for mean-reversion strategies

Provides statistical probability framework (95% within 2 standard deviations)

Algorithm Combination Effects:

The interaction between middle band MA type and ATR MA type creates different indicator characteristics:

Trend-Focused Configuration (Fast MA + Slow ATR): Middle band uses HMA/EMA/T3, ATR uses RMA/TEMA, quick trend changes with stable channel width, suitable for trend-following

Volatility-Focused Configuration (Slow MA + Fast ATR): Middle band uses SMA/WMA, ATR uses EMA/SMA, stable trend with dynamic channel width, suitable for volatility trading

Balanced Configuration (Standard EMA/RMA): Classic Keltner Channel behavior, time-tested combination, suitable for general-purpose trend following

Adaptive Configuration (KAMA + KAMA): Self-adjusting indicator responding to efficiency ratio, suitable for markets with varying trend strength and volatility regimes

📊 COMPREHENSIVE SIGNAL ANALYSIS

Keltner Channel Enhanced provides multiple signal categories optimized for trend-following and breakout strategies.

Channel Position Signals:

Upper Channel Interaction:

Price Touching Upper Channel: Strong bullish momentum, price moving more than typical volatility range suggests, potential continuation signal in established uptrends

Price Breaking Above Upper Channel: Exceptional strength, price exceeding normal volatility expectations, consider adding to long positions or tightening trailing stops

Price Riding Upper Channel: Sustained strong uptrend, characteristic of powerful bull moves, stay with trend and avoid premature profit-taking

Price Rejection at Upper Channel: Momentum exhaustion signal, consider profit-taking on longs or waiting for pullback to middle band for reentry

Lower Channel Interaction:

Price Touching Lower Channel: Strong bearish momentum, price moving more than typical volatility range suggests, potential continuation signal in established downtrends

Price Breaking Below Lower Channel: Exceptional weakness, price exceeding normal volatility expectations, consider adding to short positions or protecting against further downside

Price Riding Lower Channel: Sustained strong downtrend, characteristic of powerful bear moves, stay with trend and avoid premature covering

Price Rejection at Lower Channel: Momentum exhaustion signal, consider covering shorts or waiting for bounce to middle band for reentry

Middle Band (Basis) Signals:

Trend Direction Confirmation:

Price Above Basis: Bullish trend bias, middle band acts as dynamic support in uptrends, consider long positions or holding existing longs

Price Below Basis: Bearish trend bias, middle band acts as dynamic resistance in downtrends, consider short positions or avoiding longs

Price Crossing Above Basis: Potential trend change from bearish to bullish, early signal to establish long positions

Price Crossing Below Basis: Potential trend change from bullish to bearish, early signal to establish short positions or exit longs

Pullback Trading Strategy:

Uptrend Pullback: Price pulls back from upper channel to middle band, finds support, and resumes upward, ideal long entry point

Downtrend Bounce: Price bounces from lower channel to middle band, meets resistance, and resumes downward, ideal short entry point

Basis Test: Strong trends often show price respecting the middle band as support/resistance on pullbacks

Failed Test: Price breaking through middle band against trend direction signals potential reversal

Volatility-Based Signals:

Narrow Channels (Low Volatility):

Consolidation Phase: Channels contract during periods of reduced volatility and directionless price action

Breakout Preparation: Narrow channels often precede significant directional moves as volatility cycles

Trading Approach: Reduce position sizes, wait for breakout confirmation, avoid range-bound strategies within channels

Breakout Direction: Monitor for price breaking decisively outside channel range with expanding width

Wide Channels (High Volatility):

Trending Phase: Channels expand during strong directional moves and increased volatility

Momentum Confirmation: Wide channels confirm genuine trend with substantial volatility backing

Trading Approach: Trend-following strategies excel, wider stops necessary, mean-reversion strategies risky

Exhaustion Signs: Extreme channel width (historical highs) may signal approaching consolidation or reversal

Advanced Pattern Recognition:

Channel Walking Pattern:

Upper Channel Walk: Price consistently touches or exceeds upper channel while staying above basis, very strong uptrend signal, hold longs aggressively

Lower Channel Walk: Price consistently touches or exceeds lower channel while staying below basis, very strong downtrend signal, hold shorts aggressively

Basis Support/Resistance: During channel walks, price typically uses middle band as support/resistance on minor pullbacks

Pattern Break: Price crossing basis during channel walk signals potential trend exhaustion

Squeeze and Release Pattern:

Squeeze Phase: Channels narrow significantly, price consolidates near middle band, volatility contracts

Direction Clues: Watch for price positioning relative to basis during squeeze (above = bullish bias, below = bearish bias)

Release Trigger: Price breaking outside narrow channel range with expanding width confirms breakout

Follow-Through: Measure squeeze height and project from breakout point for initial profit targets

Channel Expansion Pattern:

Breakout Confirmation: Rapid channel widening confirms volatility increase and genuine trend establishment

Entry Timing: Enter positions early in expansion phase before trend becomes overextended

Risk Management: Use channel width to size stops appropriately, wider channels require wider stops

Basis Bounce Pattern:

Clean Bounce: Price touches middle band and immediately reverses, confirms trend strength and entry opportunity

Multiple Bounces: Repeated basis bounces indicate strong, sustainable trend

Bounce Failure: Price penetrating basis signals weakening trend and potential reversal

Divergence Analysis:

Price/Channel Divergence: Price makes new high/low while staying within channel (not reaching outer band), suggests momentum weakening

Width/Price Divergence: Price breaks to new extremes but channel width contracts, suggests move lacks conviction

Reversal Signal: Divergences often precede trend reversals or significant consolidation periods

Multi-Timeframe Analysis:

Keltner Channels work particularly well in multi-timeframe trend-following approaches:

Three-Timeframe Alignment:

Higher Timeframe (Weekly/Daily): Identify major trend direction, note price position relative to basis and channels

Intermediate Timeframe (Daily/4H): Identify pullback opportunities within higher timeframe trend

Lower Timeframe (4H/1H): Time precise entries when price touches middle band or lower channel (in uptrends) with rejection

Optimal Entry Conditions:

Best Long Entries: Higher timeframe in uptrend (price above basis), intermediate timeframe pulls back to basis, lower timeframe shows rejection at middle band or lower channel

Best Short Entries: Higher timeframe in downtrend (price below basis), intermediate timeframe bounces to basis, lower timeframe shows rejection at middle band or upper channel

Risk Management: Use higher timeframe channel width to set position sizing, stops below/above higher timeframe channels

🎯 STRATEGIC APPLICATIONS

Keltner Channel Enhanced excels in trend-following and breakout strategies across different market conditions.

Trend Following Strategy:

Setup Requirements:

Identify established trend with price consistently on one side of basis line

Wait for pullback to middle band (basis) or brief penetration through it

Confirm trend resumption with price rejection at basis and move back toward outer channel

Enter in trend direction with stop beyond basis line

Entry Rules:

Uptrend Entry:

Price pulls back from upper channel to middle band, shows support at basis (bullish candlestick, momentum divergence)

Enter long on rejection/bounce from basis with stop 1-2 ATR below basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Downtrend Entry:

Price bounces from lower channel to middle band, shows resistance at basis (bearish candlestick, momentum divergence)

Enter short on rejection/reversal from basis with stop 1-2 ATR above basis

Aggressive: Enter on first touch; Conservative: Wait for confirmation candle

Trend Management:

Trailing Stop: Use basis line as dynamic trailing stop, exit if price closes beyond basis against position

Profit Taking: Take partial profits at opposite channel, move stops to basis

Position Additions: Add to winners on subsequent basis bounces if trend intact

Breakout Strategy:

Setup Requirements:

Identify consolidation period with contracting channel width

Monitor price action near middle band with reduced volatility

Wait for decisive breakout beyond channel range with expanding width

Enter in breakout direction after confirmation

Breakout Confirmation:

Price breaks clearly outside channel (upper for longs, lower for shorts), channel width begins expanding from contracted state

Volume increases significantly on breakout (if using volume analysis)

Price sustains outside channel for multiple bars without immediate reversal

Entry Approaches:

Aggressive: Enter on initial break with stop at opposite channel or basis, use smaller position size

Conservative: Wait for pullback to broken channel level, enter on rejection and resumption, tighter stop

Volatility-Based Position Sizing:

Adjust position sizing based on channel width (ATR-based volatility):

Wide Channels (High ATR): Reduce position size as stops must be wider, calculate position size using ATR-based risk calculation: Risk / (Stop Distance in ATR × ATR Value)

Narrow Channels (Low ATR): Increase position size as stops can be tighter, be cautious of impending volatility expansion

ATR-Based Risk Management: Use ATR-based risk calculations, position size = 0.01 × Capital / (2 × ATR), use multiples of ATR (1-2 ATR) for adaptive stops

Algorithm Selection Guidelines:

Different market conditions benefit from different algorithm combinations:

Strong Trending Markets: Middle band use EMA or HMA, ATR use RMA, capture trends quickly while maintaining stable channel width

Choppy/Ranging Markets: Middle band use SMA or WMA, ATR use SMA or WMA, avoid false trend signals while identifying genuine reversals

Volatile Markets: Middle band and ATR both use KAMA or FRAMA, self-adjusting to changing market conditions reduces manual optimization

Breakout Trading: Middle band use SMA, ATR use EMA or SMA, stable trend with dynamic channels highlights volatility expansion early

Scalping/Day Trading: Middle band use HMA or T3, ATR use EMA or TEMA, both components respond quickly

Position Trading: Middle band use EMA/TEMA/T3, ATR use RMA or TEMA, filter out noise for long-term trend-following

📋 DETAILED PARAMETER CONFIGURATION

Understanding and optimizing parameters is essential for adapting Keltner Channel Enhanced to specific trading approaches.

Source Parameter:

Close (Most Common): Uses closing price, reflects daily settlement, best for end-of-day analysis and position trading, standard choice

HL2 (Median Price): Smooths out closing bias, better represents full daily range in volatile markets, good for swing trading

HLC3 (Typical Price): Gives more weight to close while including full range, popular for intraday applications, slightly more responsive than HL2

OHLC4 (Average Price): Most comprehensive price representation, smoothest option, good for gap-prone markets or highly volatile instruments

Length Parameter:

Controls the lookback period for middle band (basis) calculation:

Short Periods (10-15): Very responsive to price changes, suitable for day trading and scalping, higher false signal rate

Standard Period (20 - Default): Represents approximately one month of trading, good balance between responsiveness and stability, suitable for swing and position trading

Medium Periods (30-50): Smoother trend identification, fewer false signals, better for position trading and longer holding periods

Long Periods (50+): Very smooth, identifies major trends only, minimal false signals but significant lag, suitable for long-term investment

Optimization by Timeframe: 1-15 minute charts use 10-20 period, 30-60 minute charts use 20-30 period, 4-hour to daily charts use 20-40 period, weekly charts use 20-30 weeks.

ATR Length Parameter:

Controls the lookback period for Average True Range calculation, affecting channel width:

Short ATR Periods (5-10): Very responsive to recent volatility changes, standard is 10 (Keltner's original specification), may be too reactive in whipsaw conditions

Standard ATR Period (10 - Default): Chester Keltner's original specification, good balance between responsiveness and stability, most widely used

Medium ATR Periods (14-20): Smoother channel width, ATR 14 aligns with Wilder's original ATR specification, good for position trading

Long ATR Periods (20+): Very smooth channel width, suitable for long-term trend-following

Length vs. ATR Length Relationship: Equal values (20/20) provide balanced responsiveness, longer ATR (20/14) gives more stable channel width, shorter ATR (20/10) is standard configuration, much shorter ATR (20/5) creates very dynamic channels.

Multiplier Parameter:

Controls channel width by setting ATR multiples:

Lower Values (1.0-1.5): Tighter channels with frequent price touches, more trading signals, higher false signal rate, better for range-bound and mean-reversion strategies

Standard Value (2.0 - Default): Chester Keltner's recommended setting, good balance between signal frequency and reliability, suitable for both trending and ranging strategies

Higher Values (2.5-3.0): Wider channels with less frequent touches, fewer but potentially higher-quality signals, better for strong trending markets

Market-Specific Optimization: High volatility markets (crypto, small-caps) use 2.5-3.0 multiplier, medium volatility markets (major forex, large-caps) use 2.0 multiplier, low volatility markets (bonds, utilities) use 1.5-2.0 multiplier.

MA Type Parameter (Middle Band):

Critical selection that determines trend identification characteristics:

EMA (Exponential Moving Average - Default): Standard Keltner Channel choice, Chester Keltner's original specification, emphasizes recent prices, faster response to trend changes, suitable for all timeframes

SMA (Simple Moving Average): Equal weighting of all data points, no directional bias, slower than EMA, better for ranging markets and mean-reversion

HMA (Hull Moving Average): Minimal lag with smooth output, excellent for fast trend identification, best for day trading and scalping

TEMA (Triple Exponential Moving Average): Advanced smoothing with reduced lag, responsive to trends while filtering noise, suitable for volatile markets

T3 (Tillson T3): Very smooth with minimal lag, excellent for established trend identification, suitable for position trading

KAMA (Kaufman Adaptive Moving Average): Automatically adjusts speed based on market efficiency, slow in ranging markets, fast in trends, suitable for markets with varying conditions

ATR MA Type Parameter:

Determines how Average True Range is smoothed, affecting channel width stability:

RMA (Wilder's Smoothing - Default): J. Welles Wilder's original ATR smoothing method, very smooth, slow to adapt to volatility changes, provides stable channel width

SMA (Simple Moving Average): Equal weighting, moderate smoothness, faster response to volatility changes than RMA, more dynamic channel width

EMA (Exponential Moving Average): Emphasizes recent volatility, quick adaptation to new volatility regimes, very responsive channel width changes

TEMA (Triple Exponential Moving Average): Smooth yet responsive, good balance for varying volatility, suitable for most trading styles

Parameter Combination Strategies:

Conservative Trend-Following: Length 30/ATR Length 20/Multiplier 2.5, MA Type EMA or TEMA/ATR MA Type RMA, smooth trend with stable wide channels, suitable for position trading

Standard Balanced Approach: Length 20/ATR Length 10/Multiplier 2.0, MA Type EMA/ATR MA Type RMA, classic Keltner Channel configuration, suitable for general purpose swing trading

Aggressive Day Trading: Length 10-15/ATR Length 5-7/Multiplier 1.5-2.0, MA Type HMA or EMA/ATR MA Type EMA or SMA, fast trend with dynamic channels, suitable for scalping and day trading

Breakout Specialist: Length 20-30/ATR Length 5-10/Multiplier 2.0, MA Type SMA or WMA/ATR MA Type EMA or SMA, stable trend with responsive channel width

Adaptive All-Conditions: Length 20/ATR Length 10/Multiplier 2.0, MA Type KAMA or FRAMA/ATR MA Type KAMA or TEMA, self-adjusting to market conditions

Offset Parameter:

Controls horizontal positioning of channels on chart. Positive values shift channels to the right (future) for visual projection, negative values shift left (past) for historical analysis, zero (default) aligns with current price bars for real-time signal analysis. Offset affects only visual display, not alert conditions or actual calculations.

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Keltner Channel Enhanced provides improvements over standard implementations while maintaining proven effectiveness.

Response Characteristics:

Standard EMA/RMA Configuration: Moderate trend lag (approximately 0.4 × length periods), smooth and stable channel width from RMA smoothing, good balance for most market conditions

Fast HMA/EMA Configuration: Approximately 60% reduction in trend lag compared to EMA, responsive channel width from EMA ATR smoothing, suitable for quick trend changes and breakouts

Adaptive KAMA/KAMA Configuration: Variable lag based on market efficiency, automatic adjustment to trending vs. ranging conditions, self-optimizing behavior reduces manual intervention

Comparison with Traditional Keltner Channels:

Enhanced Version Advantages:

Dual Algorithm Flexibility: Independent MA selection for trend and volatility vs. fixed EMA/RMA, separate tuning of trend responsiveness and channel stability

Market Adaptation: Choose configurations optimized for specific instruments and conditions, customize for scalping, swing, or position trading preferences

Comprehensive Alerts: Enhanced alert system including channel expansion detection

Traditional Version Advantages:

Simplicity: Fewer parameters, easier to understand and implement

Standardization: Fixed EMA/RMA combination ensures consistency across users

Research Base: Decades of backtesting and research on standard configuration

When to Use Enhanced Version: Trading multiple instruments with different characteristics, switching between trending and ranging markets, employing different strategies, algorithm-based trading systems requiring customization, seeking optimization for specific trading style and timeframe.

When to Use Standard Version: Beginning traders learning Keltner Channel concepts, following published research or trading systems, preferring simplicity and standardization, wanting to avoid optimization and curve-fitting risks.

Performance Across Market Conditions:

Strong Trending Markets: EMA or HMA basis with RMA or TEMA ATR smoothing provides quicker trend identification, pullbacks to basis offer excellent entry opportunities

Choppy/Ranging Markets: SMA or WMA basis with RMA ATR smoothing and lower multipliers, channel bounce strategies work well, avoid false breakouts

Volatile Markets: KAMA or FRAMA with EMA or TEMA, adaptive algorithms excel by automatic adjustment, wider multipliers (2.5-3.0) accommodate large price swings

Low Volatility/Consolidation: Channels narrow significantly indicating consolidation, algorithm choice less impactful, focus on detecting channel width contraction for breakout preparation

Keltner Channel vs. Bollinger Bands - Usage Comparison:

Favor Keltner Channels When: Trend-following is primary strategy, trading volatile instruments with gaps, want ATR-based volatility measurement, prefer fewer higher-quality channel touches, seeking stable channel width during trends.

Favor Bollinger Bands When: Mean-reversion is primary strategy, trading instruments with limited gaps, want statistical framework based on standard deviation, need squeeze patterns for breakout identification, prefer more frequent trading opportunities.

Use Both Together: Bollinger Band squeeze + Keltner Channel breakout is powerful combination, price outside Bollinger Bands but inside Keltner Channels indicates moderate signal, price outside both indicates very strong signal, Bollinger Bands for entries and Keltner Channels for trend confirmation.

Limitations and Considerations:

General Limitations:

Lagging Indicator: All moving averages lag price, even with reduced-lag algorithms

Trend-Dependent: Works best in trending markets, less effective in choppy conditions

No Direction Prediction: Indicates volatility and deviation, not future direction, requires confirmation

Enhanced Version Specific Considerations:

Optimization Risk: More parameters increase risk of curve-fitting historical data

Complexity: Additional choices may overwhelm beginning traders

Backtesting Challenges: Different algorithms produce different historical results

Mitigation Strategies:

Use Confirmation: Combine with momentum indicators (RSI, MACD), volume, or price action

Test Parameter Robustness: Ensure parameters work across range of values, not just optimized ones

Multi-Timeframe Analysis: Confirm signals across different timeframes

Proper Risk Management: Use appropriate position sizing and stops

Start Simple: Begin with standard EMA/RMA before exploring alternatives

Optimal Usage Recommendations:

For Maximum Effectiveness:

Start with standard EMA/RMA configuration to understand classic behavior

Experiment with alternatives on demo account or paper trading

Match algorithm combination to market condition and trading style

Use channel width analysis to identify market phases

Combine with complementary indicators for confirmation

Implement strict risk management using ATR-based position sizing

Focus on high-quality setups rather than trading every signal

Respect the trend: trade with basis direction for higher probability

Complementary Indicators:

RSI or Stochastic: Confirm momentum at channel extremes

MACD: Confirm trend direction and momentum shifts

Volume: Validate breakouts and trend strength

ADX: Measure trend strength, avoid Keltner signals in weak trends

Support/Resistance: Combine with traditional levels for high-probability setups

Bollinger Bands: Use together for enhanced breakout and volatility analysis

USAGE NOTES

This indicator is designed for technical analysis and educational purposes. Keltner Channel Enhanced has limitations and should not be used as the sole basis for trading decisions. While the flexible moving average selection for both trend and volatility components provides valuable adaptability across different market conditions, algorithm performance varies with market conditions, and past characteristics do not guarantee future results.

Key considerations:

Always use multiple forms of analysis and confirmation before entering trades

Backtest any parameter combination thoroughly before live trading

Be aware that optimization can lead to curve-fitting if not done carefully

Start with standard EMA/RMA settings and adjust only when specific conditions warrant

Understand that no moving average algorithm can eliminate lag entirely

Consider market regime (trending, ranging, volatile) when selecting parameters

Use ATR-based position sizing and risk management on every trade

Keltner Channels work best in trending markets, less effective in choppy conditions

Respect the trend direction indicated by price position relative to basis line

The enhanced flexibility of dual algorithm selection provides powerful tools for adaptation but requires responsible use, thorough understanding of how different algorithms behave under various market conditions, and disciplined risk management.

[blackcat] L1 Net Volume DifferenceOVERVIEW

The L1 Net Volume Difference indicator serves as an advanced analytical tool designed to provide traders with deep insights into market sentiment by examining the differential between buying and selling volumes over precise timeframes. By leveraging these volume dynamics, it helps identify trends and potential reversal points more accurately, thereby supporting well-informed decision-making processes. The key focus lies in dissecting intraday changes that reflect short-term market behavior, offering critical input for both swing and day traders alike. 📊

Key benefits encompass:

• Precise calculation of net volume differences grounded in real-time data.

• Interactive visualization elements enhancing interpretability effortlessly.

• Real-time generation of buy/sell signals driven by dynamic volume shifts.

TECHNICAL ANALYSIS COMPONENTS

📉 Volume Accumulation Mechanisms:

Monitors cumulative buy/sell volumes derived from comparative closing prices.

Periodically resets accumulation counters aligning with predefined intervals (e.g., 5-minute bars).

Facilitates identification of directional biases reflecting underlying market forces accurately.

🕵️♂️ Sentiment Detection Algorithms:

Employs proprietary logic distinguishing between bullish/bearish sentiments dynamically.

Ensures consistent adherence to predefined statistical protocols maintaining accuracy.

Supports adaptive thresholds adjusting sensitivities based on changing market conditions flexibly.

🎯 Dynamic Signal Generation:

Detects transitions indicating dominance shifts between buyers/sellers promptly.

Triggers timely alerts enabling swift reactions to evolving market dynamics effectively.

Integrates conditional logic reinforcing signal validity minimizing erroneous activations.

INDICATOR FUNCTIONALITY

🔢 Core Algorithms:

Utilizes moving averages along with standardized deviation formulas generating precise net volume measurements.

Implements Arithmetic Mean Line Algorithm (AMLA) smoothing techniques improving interpretability.

Ensures consistent alignment with established statistical principles preserving fidelity.

🖱️ User Interface Elements:

Dedicated plots displaying real-time net volume markers facilitating swift decision-making.

Context-sensitive color coding distinguishing positive/negative deviations intuitively.

Background shading highlighting proximity to key threshold activations enhancing visibility.

STRATEGY IMPLEMENTATION

✅ Entry Conditions:

Confirm bullish/bearish setups validated through multiple confirmatory signals.

Validate entry decisions considering concurrent market sentiment factors.

Assess alignment between net volume readings and broader trend directions ensuring coherence.

🚫 Exit Mechanisms:

Trigger exits upon hitting predetermined thresholds derived from historical analyses.

Monitor continuous breaches signifying potential trend reversals promptly executing closures.

Execute partial/total closes contingent upon cumulative loss limits preserving capital efficiently.

PARAMETER CONFIGURATIONS

🎯 Optimization Guidelines:

Reset Interval: Governs responsiveness versus stability balancing sensitivity/stability.

Price Source: Dictates primary data series driving volume calculations selecting relevant inputs accurately.

💬 Customization Recommendations:

Commence with baseline defaults; iteratively refine parameters isolating individual impacts.

Evaluate adjustments independently prior to combined modifications minimizing disruptions.

Prioritize minimizing erroneous trigger occurrences first optimizing signal fidelity.

Sustain balanced risk-reward profiles irrespective of chosen settings upholding disciplined approaches.

ADVANCED RISK MANAGEMENT

🛡️ Proactive Risk Mitigation Techniques:

Enforce strict compliance with pre-defined maximum leverage constraints adhering strictly to guidelines.

Mandatorily apply trailing stop-loss orders conforming to script outputs reinforcing discipline.

Allocate positions proportionately relative to available capital reserves managing exposures prudently.

Conduct periodic reviews gauging strategy effectiveness rigorously identifying areas needing refinement.

⚠️ Potential Pitfalls & Solutions:

Address frequent violations arising during heightened volatility phases necessitating manual interventions judiciously.

Manage false alerts warranting immediate attention avoiding adverse consequences systematically.

Prepare contingency plans mitigating margin call possibilities preparing proactive responses effectively.

Continuously assess automated system reliability amidst fluctuating conditions ensuring seamless functionality.

PERFORMANCE AUDITS & REFINEMENTS

🔍 Critical Evaluation Metrics:

Assess win percentages consistently across diverse trading instruments gauging reliability.

Calculate average profit ratios per successful execution measuring profitability efficiency accurately.

Measure peak drawdown durations alongside associated magnitudes evaluating downside risks comprehensively.

Analyze signal generation frequencies revealing hidden patterns potentially skewing outcomes uncovering systematic biases.

📈 Historical Data Analysis Tools:

Maintain comprehensive records capturing every triggered event meticulously documenting results.

Compare realized profits/losses against backtested simulations benchmarking actual vs expected performances accurately.

Identify recurrent systematic errors demanding corrective actions implementing iterative refinements steadily.

Document evolving performance metrics tracking progress dynamically addressing identified shortcomings proactively.

PROBLEM SOLVING ADVICE

🔧 Frequent Encountered Challenges:

Unpredictable behaviors emerging within thinly traded markets requiring filtration processes.

Latency issues manifesting during abrupt price fluctuations causing missed opportunities.

Overfitted models yielding suboptimal results post-extensive tuning demanding recalibrations.

Inaccuracies stemming from incomplete/inaccurate data feeds necessitating verification procedures.

💡 Effective Resolution Pathways:

Exclude low-liquidity assets prone to erratic movements enhancing signal integrity.

Introduce buffer intervals safeguarding major news/event impacts mitigating distortions effectively.

Limit ongoing optimization attempts preventing model degradation maintaining optimal performance levels consistently.

Verify reliable connections ensuring uninterrupted data flows guaranteeing accurate interpretations reliably.

USER ENGAGEMENT SEGMENT

🤝 Community Contributions Welcome

Highly encourage active participation sharing experiences & recommendations!

THANKS

Heartfelt acknowledgment extends to all developers contributing invaluable insights about volume-based trading methodologies! ✨

Forex Pips Tracker PinescriptlabsThis algorithm is exclusively designed for the Forex market 🌐 and serves as a tool to measure volatility, helping to determine on average how many pips positions move per hour. With this information, a trader can place take profit and stop loss orders with greater certainty, since they know the average pip movement range during each hour of the day.

What does it do and how does it work?

• Volatility measurement in pips 📊:

The algorithm calculates the size of the movement (or range) of each candle expressed in pips. To do this, it takes the difference between the highest and lowest price of each candle and converts it into pips.

👉

• Time zone adjustment ⏰:

It allows you to configure the time zone so that the data aligns with your desired schedule. This is especially useful for comparing movements at different times based on the trader's location.

• Analysis by time intervals 🕒:

The algorithm’s logic organizes the information for each hour of the day. It stores data for the current day, the previous day, weekly, and historically (200 candles). This allows you to see how volatility varies across different periods, providing a dynamic view of market behavior.

👉

• Directionality of movement 🔄:

In addition to averaging the pip range, the algorithm determines the predominant direction of each candle (bullish or bearish). This translates into visual indicators (like arrows) that help identify whether, on average, the movement during that hour tends to go up or down.

• Table visualization 📈:

Finally, the information is presented in an integrated table on the chart. Each row corresponds to an hour of the day and shows the average number of pips and the direction (bullish, bearish, or neutral) for each analyzed period. This table makes it easy to quickly and practically interpret the volatility data.

By combining these features, the algorithm becomes an essential tool for traders looking to better understand market dynamics and optimize their trading strategies! 💼✨

Español:

Este algoritmo está diseñado exclusivamente para el mercado Forex 🌐 y sirve como una herramienta para medir la volatilidad, ayudando a determinar en promedio cuántos pips se mueven las posiciones por hora. Con esta información, un trader puede colocar el take profit y el stop loss con mayor certeza, ya que conoce el rango promedio de movimiento en pips durante cada hora del día.

¿Qué hace y cómo funciona?

• Medición de volatilidad en pips 📊:

El algoritmo calcula el tamaño del movimiento (o rango) de cada vela expresado en pips. Para ello, toma la diferencia entre el precio máximo y el mínimo de cada vela y la convierte a pips.

👉

• Ajuste de zona horaria ⏰:

Permite configurar la zona horaria para que los datos se ajusten al horario deseado. Esto es especialmente útil para comparar movimientos durante distintas horas en función de la localización del trader.

• Análisis por intervalos de tiempo 🕒:

La lógica del algoritmo organiza la información por cada hora del día. Guarda datos para el día actual, el día anterior, a nivel semanal e histórico (200 velas). Esto permite ver cómo varía la volatilidad en diferentes periodos, proporcionando una visión dinámica del comportamiento del mercado.

👉

• Direccionalidad del movimiento 🔄:

Además de promediar el rango en pips, el algoritmo determina la dirección predominante de cada vela (alcista o bajista). Esto se traduce en indicadores visuales (como flechas) que permiten identificar si, en promedio, el movimiento en esa hora tiende a subir o bajar.

• Visualización en tabla 📈:

Finalmente, la información se presenta en una tabla integrada en el gráfico. Cada fila corresponde a una hora del día y muestra el promedio de pips y la dirección (alcista, bajista o neutral) para cada uno de los periodos analizados. Esta tabla facilita la interpretación rápida y práctica de los datos de volatilidad.

Al combinar estas funciones, el algoritmo se convierte en una herramienta esencial para traders que buscan entender mejor la dinámica del mercado y optimizar sus estrategias de trading! 💼✨

[Pandora] Vast Volatility Treasure TroveINTRODUCTION:

Volatility enthusiasts, prepare for VICTORY on this day of July 4th, 2024! This is my "Vast Volatility Treasure Trove," intended mostly for educational purposes, yet these functions will also exhibit versatility when combined with other algorithms to garner statistical excellence. Once again, I am now ripping the lid off of Pandora's box... of volatility. Inside this script is a 'vast' collection of volatility estimators, reflecting the indicators name. Whether you are a seasoned trader destined to navigate financial strife or an eagerly curious learner, this script offers a comprehensive toolkit for a broad spectrum of volatility analysis. Enjoy your journey through the realm of market volatility with this code!

WHAT IS MARKET VOLATILITY?:

Market volatility refers to various fluctuations in the value of a financial market or asset over a period of time, often characterized by occasional rapid and significant deviations in price. During periods of greater market volatility, evolving conditions of prices can move rapidly in either direction, creating uncertainty for investors with results of sharp declines as well as rapid gains. However, market volatility is a typical aspect expected in financial markets that can also present opportunities for informed decision-making and potential benefits from the price flux.

SCRIPT INTENTION:

Volatility is assuredly omnipresent, waxing and waning in magnitude, and some readers have every intention of studying and/or measuring it. This script serves as an all-in-one armada of volatility estimators for TradingView members. I set out to provide a diverse set of tools to analyze and interpret market volatility, offering volatile insights, and aid with the development of robust trading indicators and strategies.

In today's fast-paced financial markets, understanding and quantifying volatility is informative for both seasoned traders and novice investors. This script is designed to empower users by equipping them with a comprehensive suite of volatility estimators. Each function within this script has been meticulously crafted to address various aspects of volatility, from traditional methods like Garman-Klass and Parkinson to more advanced techniques like Yang-Zhang and my custom experimental algorithms.

Ultimately, this script is more than just a collection of functions. It is a gateway to a deeper understanding of market volatility and a valuable resource for anyone committed to mastering the complexities of financial markets.

SCRIPT CONTENTS:

This script includes a variety of functions designed to measure and analyze market volatility. Where applicable, an input checkbox option provides an unbiased/biased estimate. Below is a brief description of each function in the original order they appear as code upon first publish:

Parkinson Volatility - Estimates volatility emphasizing the high and low range movements.

Alternate Parkinson Volatility - Simpler version of the original Parkinson Volatility that I realized.

Garman-Klass Volatility - Estimates volatility based on high, low, open, and close prices using a formula that adjusts for biases in price dynamics.

Rogers-Satchell-Yoon Volatility #1 - Estimates volatility based on logarithmic differences between high, low, open, and close values.

Rogers-Satchell-Yoon Volatility #2 - Similar estimate to Rogers-Satchell with the same result via an alternate formulation of volatility.

Yang-Zhang Volatility - An advanced volatility estimate combining both strengths of the Garman-Klass and Rogers-Satchell estimators, with weights determined by an alpha parameter.

Yang-Zhang (Modified) Volatility - My experimental modification slightly different from the Yang-Zhang formula with improved computational efficiency.

Selectable Volatility - Basic customizable volatility calculation based on the logarithmic difference between selected numerator and denominator prices (e.g., open, high, low, close).

Close-to-Close Volatility - Estimates volatility using the logarithmic difference between consecutive closing prices. Specifically applicable to data sources without open, high, and low prices.

Open-to-Close Volatility - (Overnight Volatility): Estimates volatility based on the logarithmic difference between the opening price and the last closing price emphasizing overnight gaps.

Hilo Volatility - Estimates volatility using a method similar to Parkinson's method, which considers the logarithm of the high and low prices.

Vantage Volatility - My experimental custom 'vantage' method to estimate volatility similar to Yang-Zhang, which incorporates various factors (Alpha, Beta, Gamma) to generate a weighted logarithmic calculation. This may be a volatility advantage or disadvantage, hence it's name.

Schwert Volatility - Estimates volatility based on arithmetic returns.

Historical Volatility - Estimates volatility considering logarithmic returns.

Annualized Historical Volatility - Estimates annualized volatility using logarithmic returns, adjusted for the number of trading days in a year.

If I omitted any other known varieties, detailed requests for future consideration can be made below for their inclusion into this script within future versions...

BONUS ALGORITHMS:

This script also includes several experimental and bonus functions that push the boundaries of volatility analysis as I understand it. These functions are designed to provide additional insights and also are my ideal notions for traders looking to explore other methods of volatility measurement.

VOLATILITY APPLICATIONS:

Volatility estimators serve a common role across various facets of trading and financial analysis, offering insights into market behavior. These tools are already in instrumental with enhancing risk management practices by providing a deeper understanding of market dynamics and the inherent uncertainty in asset prices. With volatility estimators, traders can effectively quantifying market risk and adjust their strategies accordingly, optimizing portfolio performance and mitigating potential losses. Additionally, volatility estimations may serve as indication for detecting overbought or oversold market conditions, offering probabilistic insights that could inform strategic decisions at turning points. This script

distinctly offers a variety of volatility estimators to navigate intricate financial terrains with informed judgment to address challenges of strategic planning.

CODE REUSE:

You don't have to ask for my permission to use/reuse these functions in your published scripts, simply because I have better things to do than answer requests for the reuse of these functions.

Notice: Unfortunately, I will not provide any integration support into member's projects at all. I have my own projects that require way too much of my day already.

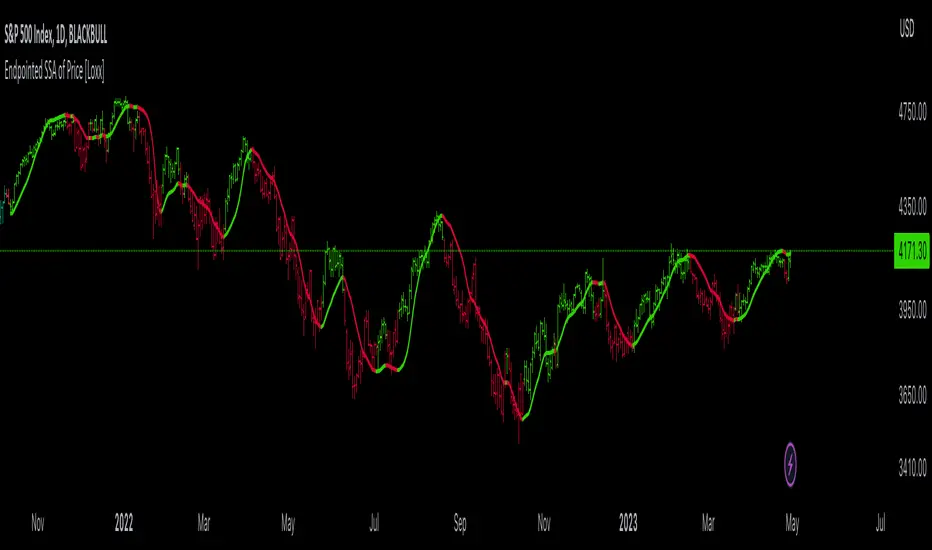

Endpointed SSA of Price [Loxx]The Endpointed SSA of Price: A Comprehensive Tool for Market Analysis and Decision-Making

The financial markets present sophisticated challenges for traders and investors as they navigate the complexities of market behavior. To effectively interpret and capitalize on these complexities, it is crucial to employ powerful analytical tools that can reveal hidden patterns and trends. One such tool is the Endpointed SSA of Price, which combines the strengths of Caterpillar Singular Spectrum Analysis, a sophisticated time series decomposition method, with insights from the fields of economics, artificial intelligence, and machine learning.

The Endpointed SSA of Price has its roots in the interdisciplinary fusion of mathematical techniques, economic understanding, and advancements in artificial intelligence. This unique combination allows for a versatile and reliable tool that can aid traders and investors in making informed decisions based on comprehensive market analysis.

The Endpointed SSA of Price is not only valuable for experienced traders but also serves as a useful resource for those new to the financial markets. By providing a deeper understanding of market forces, this innovative indicator equips users with the knowledge and confidence to better assess risks and opportunities in their financial pursuits.

█ Exploring Caterpillar SSA: Applications in AI, Machine Learning, and Finance

Caterpillar SSA (Singular Spectrum Analysis) is a non-parametric method for time series analysis and signal processing. It is based on a combination of principles from classical time series analysis, multivariate statistics, and the theory of random processes. The method was initially developed in the early 1990s by a group of Russian mathematicians, including Golyandina, Nekrutkin, and Zhigljavsky.

Background Information:

SSA is an advanced technique for decomposing time series data into a sum of interpretable components, such as trend, seasonality, and noise. This decomposition allows for a better understanding of the underlying structure of the data and facilitates forecasting, smoothing, and anomaly detection. Caterpillar SSA is a particular implementation of SSA that has proven to be computationally efficient and effective for handling large datasets.

Uses in AI and Machine Learning:

In recent years, Caterpillar SSA has found applications in various fields of artificial intelligence (AI) and machine learning. Some of these applications include:

1. Feature extraction: Caterpillar SSA can be used to extract meaningful features from time series data, which can then serve as inputs for machine learning models. These features can help improve the performance of various models, such as regression, classification, and clustering algorithms.

2. Dimensionality reduction: Caterpillar SSA can be employed as a dimensionality reduction technique, similar to Principal Component Analysis (PCA). It helps identify the most significant components of a high-dimensional dataset, reducing the computational complexity and mitigating the "curse of dimensionality" in machine learning tasks.

3. Anomaly detection: The decomposition of a time series into interpretable components through Caterpillar SSA can help in identifying unusual patterns or outliers in the data. Machine learning models trained on these decomposed components can detect anomalies more effectively, as the noise component is separated from the signal.

4. Forecasting: Caterpillar SSA has been used in combination with machine learning techniques, such as neural networks, to improve forecasting accuracy. By decomposing a time series into its underlying components, machine learning models can better capture the trends and seasonality in the data, resulting in more accurate predictions.

Application in Financial Markets and Economics:

Caterpillar SSA has been employed in various domains within financial markets and economics. Some notable applications include:

1. Stock price analysis: Caterpillar SSA can be used to analyze and forecast stock prices by decomposing them into trend, seasonal, and noise components. This decomposition can help traders and investors better understand market dynamics, detect potential turning points, and make more informed decisions.

2. Economic indicators: Caterpillar SSA has been used to analyze and forecast economic indicators, such as GDP, inflation, and unemployment rates. By decomposing these time series, researchers can better understand the underlying factors driving economic fluctuations and develop more accurate forecasting models.

3. Portfolio optimization: By applying Caterpillar SSA to financial time series data, portfolio managers can better understand the relationships between different assets and make more informed decisions regarding asset allocation and risk management.

Application in the Indicator:

In the given indicator, Caterpillar SSA is applied to a financial time series (price data) to smooth the series and detect significant trends or turning points. The method is used to decompose the price data into a set number of components, which are then combined to generate a smoothed signal. This signal can help traders and investors identify potential entry and exit points for their trades.

The indicator applies the Caterpillar SSA method by first constructing the trajectory matrix using the price data, then computing the singular value decomposition (SVD) of the matrix, and finally reconstructing the time series using a selected number of components. The reconstructed series serves as a smoothed version of the original price data, highlighting significant trends and turning points. The indicator can be customized by adjusting the lag, number of computations, and number of components used in the reconstruction process. By fine-tuning these parameters, traders and investors can optimize the indicator to better match their specific trading style and risk tolerance.

Caterpillar SSA is versatile and can be applied to various types of financial instruments, such as stocks, bonds, commodities, and currencies. It can also be combined with other technical analysis tools or indicators to create a comprehensive trading system. For example, a trader might use Caterpillar SSA to identify the primary trend in a market and then employ additional indicators, such as moving averages or RSI, to confirm the trend and generate trading signals.

In summary, Caterpillar SSA is a powerful time series analysis technique that has found applications in AI and machine learning, as well as financial markets and economics. By decomposing a time series into interpretable components, Caterpillar SSA enables better understanding of the underlying structure of the data, facilitating forecasting, smoothing, and anomaly detection. In the context of financial trading, the technique is used to analyze price data, detect significant trends or turning points, and inform trading decisions.

█ Input Parameters

This indicator takes several inputs that affect its signal output. These inputs can be classified into three categories: Basic Settings, UI Options, and Computation Parameters.

Source: This input represents the source of price data, which is typically the closing price of an asset. The user can select other price data, such as opening price, high price, or low price. The selected price data is then utilized in the Caterpillar SSA calculation process.

Lag: The lag input determines the window size used for the time series decomposition. A higher lag value implies that the SSA algorithm will consider a longer range of historical data when extracting the underlying trend and components. This parameter is crucial, as it directly impacts the resulting smoothed series and the quality of extracted components.

Number of Computations: This input, denoted as 'ncomp,' specifies the number of eigencomponents to be considered in the reconstruction of the time series. A smaller value results in a smoother output signal, while a higher value retains more details in the series, potentially capturing short-term fluctuations.

SSA Period Normalization: This input is used to normalize the SSA period, which adjusts the significance of each eigencomponent to the overall signal. It helps in making the algorithm adaptive to different timeframes and market conditions.

Number of Bars: This input specifies the number of bars to be processed by the algorithm. It controls the range of data used for calculations and directly affects the computation time and the output signal.

Number of Bars to Render: This input sets the number of bars to be plotted on the chart. A higher value slows down the computation but provides a more comprehensive view of the indicator's performance over a longer period. This value controls how far back the indicator is rendered.

Color bars: This boolean input determines whether the bars should be colored according to the signal's direction. If set to true, the bars are colored using the defined colors, which visually indicate the trend direction.

Show signals: This boolean input controls the display of buy and sell signals on the chart. If set to true, the indicator plots shapes (triangles) to represent long and short trade signals.

Static Computation Parameters:

The indicator also includes several internal parameters that affect the Caterpillar SSA algorithm, such as Maxncomp, MaxLag, and MaxArrayLength. These parameters set the maximum allowed values for the number of computations, the lag, and the array length, ensuring that the calculations remain within reasonable limits and do not consume excessive computational resources.

█ A Note on Endpionted, Non-repainting Indicators

An endpointed indicator is one that does not recalculate or repaint its past values based on new incoming data. In other words, the indicator's previous signals remain the same even as new price data is added. This is an important feature because it ensures that the signals generated by the indicator are reliable and accurate, even after the fact.