POC Migration Velocity (POC-MV) [PhenLabs]📊POC Migration Velocity (POC-MV)

Version: PineScript™v6

📌Description

The POC Migration Velocity indicator revolutionizes market structure analysis by tracking the movement, speed, and acceleration of Point of Control (POC) levels in real-time. This tool combines sophisticated volume distribution estimation with velocity calculations to reveal hidden market dynamics that conventional indicators miss.

POC-MV provides traders with unprecedented insight into volume-based price movement patterns, enabling the early identification of continuation and exhaustion signals before they become apparent to the broader market. By measuring how quickly and consistently the POC migrates across price levels, traders gain early warning signals for significant market shifts and can position themselves advantageously.

The indicator employs advanced algorithms to estimate intra-bar volume distribution without requiring lower timeframe data, making it accessible across all chart timeframes while maintaining sophisticated analytical capabilities.

🚀Points of Innovation

Micro-POC calculation using advanced OHLC-based volume distribution estimation

Real-time velocity and acceleration tracking normalized by ATR for cross-market consistency

Persistence scoring system that quantifies directional consistency over multiple periods

Multi-signal detection combining continuation patterns, exhaustion signals, and gap alerts

Dynamic color-coded visualization system with intensity-based feedback

Comprehensive customization options for resolution, periods, and thresholds

🔧Core Components

POC Calculation Engine: Estimates volume distribution within each bar using configurable price bands and sophisticated weighting algorithms

Velocity Measurement System: Tracks the rate of POC movement over customizable lookback periods with ATR normalization

Acceleration Calculator: Measures the rate of change of velocity to identify momentum shifts in POC migration

Persistence Analyzer: Quantifies how consistently POC moves in the same direction using exponential weighting

Signal Detection Framework: Combines trend analysis, velocity thresholds, and persistence requirements for signal generation

Visual Rendering System: Provides dynamic color-coded lines and heat ribbons based on velocity and price-POC relationships

🔥Key Features

Real-time POC calculation with 10-100 configurable price bands for optimal precision

Velocity tracking with customizable lookback periods from 5 to 50 bars

Acceleration measurement for detecting momentum changes in POC movement

Persistence scoring to validate signal strength and filter false signals

Dynamic visual feedback with blue/orange color scheme indicating bullish/bearish conditions

Comprehensive alert system for continuation patterns, exhaustion signals, and POC gaps

Adjustable information table displaying real-time metrics and current signals

Heat ribbon visualization showing price-POC relationship intensity

Multiple threshold settings for customizing signal sensitivity

Export capability for use with separate panel indicators

🎨Visualization

POC Connecting Lines: Color-coded lines showing POC levels with intensity based on velocity magnitude

Heat Ribbon: Dynamic colored ribbon around price showing POC-price basis intensity

Signal Markers: Clear exhaustion top/bottom signals with labeled shapes

Information Table: Real-time display of POC value, velocity, acceleration, basis, persistence, and current signal status

Color Gradients: Blue gradients for bullish conditions, orange gradients for bearish conditions

📖Usage Guidelines

POC Calculation Settings

POC Resolution (Price Bands): Default 20, Range 10-100. Controls the number of price bands used to estimate volume distribution within each bar

Volume Weight Factor: Default 0.7, Range 0.1-1.0. Adjusts the influence of volume in POC calculation

POC Smoothing: Default 3, Range 1-10. EMA smoothing period applied to the calculated POC to reduce noise

Velocity Settings

Velocity Lookback Period: Default 14, Range 5-50. Number of bars used to calculate POC velocity

Acceleration Period: Default 7, Range 3-20. Period for calculating POC acceleration

Velocity Significance Threshold: Default 0.5, Range 0.1-2.0. Minimum normalized velocity for continuation signals

Persistence Settings

Persistence Lookback: Default 5, Range 3-20. Number of bars examined for persistence score calculation

Persistence Threshold: Default 0.7, Range 0.5-1.0. Minimum persistence score required for continuation signals

Visual Settings

Show POC Connecting Lines: Toggle display of colored lines connecting POC levels

Show Heat Ribbon: Toggle display of colored ribbon showing POC-price relationship

Ribbon Transparency: Default 70, Range 0-100. Controls transparency level of heat ribbon

Alert Settings

Enable Continuation Alerts: Toggle alerts for continuation pattern detection

Enable Exhaustion Alerts: Toggle alerts for exhaustion pattern detection

Enable POC Gap Alerts: Toggle alerts for significant POC gaps

Gap Threshold: Default 2.0 ATR, Range 0.5-5.0. Minimum gap size to trigger alerts

✅Best Use Cases

Identifying trend continuation opportunities when POC velocity aligns with price direction

Spotting potential reversal points through exhaustion pattern detection

Confirming breakout validity by monitoring POC gap behavior

Adding volume-based context to traditional technical analysis

Managing position sizing based on POC-price basis strength

⚠️Limitations

POC calculations are estimations based on OHLC data, not true tick-by-tick volume distribution

Effectiveness may vary in low-volume or highly volatile market conditions

Requires complementary analysis tools for complete trading decisions

Signal frequency may be lower in ranging markets compared to trending conditions

Performance optimization needed for very short timeframes below 1-minute

💡What Makes This Unique

Advanced Estimation Algorithm: Sophisticated method for calculating POC without requiring lower timeframe data

Velocity-Based Analysis: Focus on POC movement dynamics rather than static levels

Comprehensive Signal Framework: Integration of continuation, exhaustion, and gap detection in one indicator

Dynamic Visual Feedback: Intensity-based color coding that adapts to market conditions

Persistence Validation: Unique scoring system to filter signals based on directional consistency

🔬How It Works

Volume Distribution Estimation:

Divides each bar into configurable price bands for volume analysis

Applies sophisticated weighting based on OHLC relationships and proximity to close

Identifies the price level with maximum estimated volume as the POC

Velocity and Acceleration Calculation:

Measures POC rate of change over specified lookback periods

Normalizes values using ATR for consistent cross-market performance

Calculates acceleration as the rate of change of velocity

Signal Generation Process:

Combines trend direction analysis using EMA crossovers

Applies velocity and persistence thresholds to filter signals

Generates continuation, exhaustion, and gap alerts based on specific criteria

💡Note:

This indicator provides estimated POC calculations based on available OHLC data and should be used in conjunction with other analysis methods. The velocity-based approach offers unique insights into market structure dynamics but requires proper risk management and complementary analysis for optimal trading decisions.

Cerca negli script per "algo"

[Pandora][Swarm] Rapid Exponential Moving AverageENVISIONING POSSIBILITY

What is the theoretical pinnacle of possibility? The current state of algorithmic affairs falls far short of my aspirations for achievable feasibility. I'm lifting the lid off of Pandora's box once again, very publicly this time, as a brute force challenge to conventional 'wisdom'. The unfolding series of time mandates a transcendental systemic alteration...

THE MOVING AVERAGE ZOO:

The realm of digital signal processing for trading is filled with familiar antiquated filtering tools. Two families of filtration, being 'infinite impulse response' (EMA, RMA, etc.) and 'finite impulse response' (WMA, SMA, etc.), are prevalently employed without question. These filter types are the mules and donkeys of data analysis, broadly accepted for use in finance.

At first glance, they appear sufficient for most tasks, offering a basic straightforward way to reduce noise and highlight trends. Yet, beneath their simplistic facade lies a constellation of limitations and impediments, each having its own finicky quirks. Upon closer inspection, identifiable drawbacks render them far from ideal for many real-world applications in today's volatile markets.

KNOWN FUNDAMENTAL FLAWS:

Despite commonplace moving average (MA) popularity, these conventional filters suffer from an assortment of fundamental flaws. Most of them don't genuinely address core challenges of how to preserve the true dynamics of a signal while suppressing noise and retaining cutoff frequency compliance. Their simple cookie cutter structures make them ill-suited in actuality for dynamic market environments. In reality, they often trade one problem for another dilemma, forsaking analytics to choose between distortion and delay.

A deeper seeded issue remains within frequency compliance, how adequately a filter respects (or disrespects) the underlying signal’s spectral properties according to it's assigned periodic parameter. Traditional MAs habitually distort phase relationships, causing delayed reactions with surplus lag or exaggerations with excessive undershoot/overshoot. For applications requiring timely resilience, such as algorithmic trading, these shortcomings are often functionally unacceptable. What’s needed is vigorous filters that can more accurately retain signal behaviors while minimizing lag without sacrificing smoothness and uniformity. Until then, the public MA zoo remains as a collection of corny compromises, rather than a favorable toolbelt of solutions.

P.S.: In PSv7+, in my opinion, many of these geriatric MAs deserve no future with ease of access for the naive, simply not knowing these filters are most likely creating bigger problems than solving any.

R.E.M.A.

What is this? I prefer to think of it as the "radical EMA", definitely along my lines of a retire everything morte algorithm. This isn't your run of the mill average from the petting zoo. I would categorize it as a paradigm shifting rampant economic masochistic annihilator, sufficiently good enough to begin ruthlessly executing moving averages left and right. Um, yeah... that kind of moving average destructor as you may soon recognize with a few 'Filters+' settings adjustments, realizing ordinary EMA has been doing us an injustice all this time.

Does it possess the capability to relentlessly exterminate most averaging filters in existence? Well, it's about time we find out, by uncaging it on the loose into the greater economic wilderness. Only then can we truly find out if it is indeed a radical exponential market accelerant whose time has come. If it is, then it may eventually become a reality erasing monolithic anomaly destined for greatness, ultimately changing the entire landscape of trading in perpetuity.

UNLEASHING NEXT-GEN:

This lone next generation exoweapon algorithm is intended to initiate the transformative beginning stages of mass filtration deprecation. However, it won't be the only one, just the first arrival of it's alien kind from me. Welcome to notion #1 of my future filtration frontier, on this episode of the algorithmic twilight zone. Where reality takes a twisting turn one dimension beyond practical logic, after persistent models of mindset disintegrate into insignificance, followed by illusory perception confronted into cognitive dissonance.

An evolutionary path to genuine advancement resides outside the prison of preconceptions, manifesting only after divergence from persistent binding restrictions of dogmatic doctrines. Such a genesis in transformative thinking will catalyze unbounded cognitive potential, plowing the way for the cultivation of total redesigns of thought. Futuristic innovative breakthroughs demand the surrender of legacy and outmoded understandings.

Now that the world's largest assembly of investors has been ensembled, there are additional tasks left to perform. I'm compelled to deploy this mathematical-weapon of mass financial creation into it's rightful destined hands, to "WE THE PEOPLE" of TV.

SCRIPT INTENTION:

Deprecate anything and everything as any non-commercial member sees desirably fit. This includes your existing code formulations already in working functional modes of operation AND/OR future projects in the works. Swapping is nearly as simple as copying and pasting with meager modifications, after you have identified comparable likeness in this indicators settings with a visual assessment. Results may become eye opening, but only if you dare to look and test.

Where you may suspect a ta.filter() is lacking sufficient luster or may be flat out majorly deficient, employing rema, drema, trema, or qrema configurations may be a more suitable replacement. That's up to you to discern. My code satire already identifies likely bottom of the barrel suspects that either belong in the extinction record or have already been marked for deprecation. They are ordered more towards the bottom by rank where they belong. SuperSmoother is a masterpiece here to stay, being my original go-to reference filter. Everything you see here is already deprecated, including REMA...

REMA CHARACTERISTICS

- VERY low lag

- No overshoot

- Frequency compliant

- Proper initialization at bar_index==0

- Period parameter accepts poitive floating point numerics (AND integers!)

- Infinite impulse response (IIR) filter

- Compact code footprint

- Minimized computational overhead

3D Surface Modeling [PhenLabs]📊 3D Surface Modeling

Version: PineScript™ v6

📌 Description

The 3D Surface Modeling indicator revolutionizes technical analysis by generating three-dimensional visualizations of multiple technical indicators across various timeframes. This advanced analytical tool processes and renders complex indicator data through a sophisticated matrix-based calculation system, creating an intuitive 3D surface representation of market dynamics.

The indicator employs array-based computations to simultaneously analyze multiple instances of selected technical indicators, mapping their behavior patterns across different temporal dimensions. This unique approach enables traders to identify complex market patterns and relationships that may be invisible in traditional 2D charts.

🚀 Points of Innovation

Matrix-Based Computation Engine: Processes up to 500 concurrent indicator calculations in real-time

Dynamic 3D Rendering System: Creates depth perception through sophisticated line arrays and color gradients

Multi-Indicator Integration: Seamlessly combines VWAP, Hurst, RSI, Stochastic, CCI, MFI, and Fractal Dimension analyses

Adaptive Scaling Algorithm: Automatically adjusts visualization parameters based on indicator type and market conditions

🔧 Core Components

Indicator Processing Module: Handles real-time calculation of multiple technical indicators using array-based mathematics

3D Visualization Engine: Converts indicator data into three-dimensional surfaces using line arrays and color mapping

Dynamic Scaling System: Implements custom normalization algorithms for different indicator types

Color Gradient Generator: Creates depth perception through programmatic color transitions

🔥 Key Features

Multi-Indicator Support: Comprehensive analysis across seven different technical indicators

Customizable Visualization: User-defined color schemes and line width parameters

Real-time Processing: Continuous calculation and rendering of 3D surfaces

Cross-Timeframe Analysis: Simultaneous visualization of indicator behavior across multiple periods

🎨 Visualization

Surface Plot: Three-dimensional representation using up to 500 lines with dynamic color gradients

Depth Indicators: Color intensity variations showing indicator value magnitude

Pattern Recognition: Visual identification of market structures across multiple timeframes

📖 Usage Guidelines

Indicator Selection

Type: VWAP, Hurst, RSI, Stochastic, CCI, MFI, Fractal Dimension

Default: VWAP

Starting Length: Minimum 5 periods

Default: 10

Step Size: Interval between calculations

Range: 1-10

Visualization Parameters

Color Scheme: Green, Red, Blue options

Line Width: 1-5 pixels

Surface Resolution: Up to 500 lines

✅ Best Use Cases

Multi-timeframe market analysis

Pattern recognition across different technical indicators

Trend strength assessment through 3D visualization

Market behavior study across multiple periods

⚠️ Limitations

High computational resource requirements

Maximum 500 line restriction

Requires substantial historical data

Complex visualization learning curve

🔬 How It Works

1. Data Processing:

Calculates selected indicator values across multiple timeframes

Stores results in multi-dimensional arrays

Applies custom scaling algorithms

2. Visualization Generation:

Creates line arrays for 3D surface representation

Applies color gradients based on value magnitude

Renders real-time updates to surface plot

3. Display Integration:

Synchronizes with chart timeframe

Updates surface plot dynamically

Maintains visual consistency across updates

🌟 Credits:

Inspired by LonesomeTheBlue (modified for multiple indicator types with scaling fixes and additional unique mappings)

💡 Note:

Optimal performance requires sufficient computing resources and historical data. Users should start with default settings and gradually adjust parameters based on their analysis requirements and system capabilities.

ICT Opening Range Projections (tristanlee85)ICT Opening Range Projections

This indicator visualizes key price levels based on ICT's (Inner Circle Trader) "Opening Range" concept. This 30-minute time interval establishes price levels that the algorithm will refer to throughout the session. The indicator displays these levels, including standard deviation projections, internal subdivisions (quadrants), and the opening price.

🟪 What It Does

The Opening Range is a crucial 30-minute window where market algorithms establish significant price levels. ICT theory suggests this range forms the basis for daily price movement.

This script helps you:

Mark the high, low, and opening price of each session.

Divide the range into quadrants (premium, discount, and midpoint/Consequent Encroachment).

Project potential price targets beyond the range using configurable standard deviation multiples .

🟪 How to Use It

This tool aids in time-based technical analysis rooted in ICT's Opening Range model, helping you observe price interaction with algorithmic levels.

Example uses include:

Identifying early structural boundaries.

Observing price behavior within premium/discount zones.

Visualizing initial displacement from the range to anticipate future moves.

Comparing price reactions at projected standard deviation levels.

Aligning price action with significant times like London or NY Open.

Note: This indicator provides a visual framework; it does not offer trade signals or interpretations.

🟪 Key Information

Time Zone: New York time (ET) is required on your chart.

Sessions: Supports multiple sessions, including NY midnight, NY AM, NY PM, and three custom timeframes.

Time Interval: Supports multi-timeframe up to 15 minutes. Best used on a 1-minute chart for accuracy.

🟪 Session Options

The Opening Range interval is configurable for up to 6 sessions:

Pre-defined ICT Sessions:

NY Midnight: 12:00 AM – 12:30 AM ET

NY AM: 9:30 AM – 10:00 AM ET

NY PM: 1:30 PM – 2:00 PM ET

Custom Sessions:

Three user-defined start/end time pairs.

This example shows a custom session from 03:30 - 04:00:

🟪 Understanding the Levels

The Opening Price is the open of the first 1-minute candle within the chosen session.

At session close, the Opening Range is calculated using its High and Low . An optional swing-based mode uses swing highs/lows for range boundaries.

The range is divided into quadrants by its midpoint ( Consequent Encroachment or CE):

Upper Quadrant: CE to high (premium).

Lower Quadrant: Low to CE (discount).

These subdivisions help visualize internal range dynamics, where price often reacts during algorithmic delivery.

🟪 Working with Ranges

By default, the range is determined by the highest high and lowest low of the 30-minute session:

A range can also be determined by the highest/lowest swing points:

Quadrants outline the premium and discount of a range that price will reference:

Small ranges still follow the same algorithmic logic, but may be deemed insignificant for one's trading. These can be filtered in the settings by specifying a minimum ticks limit. In this example, the range is 42 ticks (10.5 points) but the indicator is configured for 80 ticks (20 points). We can select which levels will plot if the range is below the limit. Here, only the 00:00 opening price is plotted:

You may opt to include the range high/low, quadrants, and projections as well. This will plot a red (configurable) range bracket to indicate it is below the limit while plotting the levels:

🟪 Price Projections

Projections extend beyond the Opening Range using standard deviations, framing the market beyond the initial session and identifying potential targets. You define the standard deviation multiples (e.g., 1.0, 1.5, 2.0).

Both positive and negative extensions are displayed, symmetrically projected from the range's high and low.

The Dynamic Levels option plots only the next projection level once price crosses the previous extreme. For example, only the 0.5 STDEV level plots until price reaches it, then the 1.0 level appears, and so on. This continues up to your defined maximum projections, or indefinitely if standard deviations are set to 0.

This example shows dynamic levels for a total of 6 sessions, only 1 of which meet a configured minimum limit of 50 ticks:

Small ranges followed by significant displacement are impacted the most with the number of levels plotted. You may hide projections when configuring the minimum ticks.

A fixed standard deviation will plot levels in both directions, regardless of the price range. Here, we plot up to 3.0 which hiding projections for small ranges:

🟪 Legal Disclaimer

This indicator is provided for informational and educational purposes only. It is not financial advice, and should not be construed as a recommendation to buy or sell any financial instrument. Trading involves substantial risk, and you could lose a significant amount of money. Past performance is not indicative of future results. Always consult with a qualified financial professional before making any trading or investment decisions. The creators and distributors of this indicator assume no responsibility for your trading outcomes.

Momentum + Keltner Stochastic Combo)The Momentum-Keltner-Stochastic Combination Strategy: A Technical Analysis and Empirical Validation

This study presents an advanced algorithmic trading strategy that implements a hybrid approach between momentum-based price dynamics and relative positioning within a volatility-adjusted Keltner Channel framework. The strategy utilizes an innovative "Keltner Stochastic" concept as its primary decision-making factor for market entries and exits, while implementing a dynamic capital allocation model with risk-based stop-loss mechanisms. Empirical testing demonstrates the strategy's potential for generating alpha in various market conditions through the combination of trend-following momentum principles and mean-reversion elements within defined volatility thresholds.

1. Introduction

Financial market trading increasingly relies on the integration of various technical indicators for identifying optimal trading opportunities (Lo et al., 2000). While individual indicators are often compromised by market noise, combinations of complementary approaches have shown superior performance in detecting significant market movements (Murphy, 1999; Kaufman, 2013). This research introduces a novel algorithmic strategy that synthesizes momentum principles with volatility-adjusted envelope analysis through Keltner Channels.

2. Theoretical Foundation

2.1 Momentum Component

The momentum component of the strategy builds upon the seminal work of Jegadeesh and Titman (1993), who demonstrated that stocks which performed well (poorly) over a 3 to 12-month period continue to perform well (poorly) over subsequent months. As Moskowitz et al. (2012) further established, this time-series momentum effect persists across various asset classes and time frames. The present strategy implements a short-term momentum lookback period (7 bars) to identify the prevailing price direction, consistent with findings by Chan et al. (2000) that shorter-term momentum signals can be effective in algorithmic trading systems.

2.2 Keltner Channels

Keltner Channels, as formalized by Chester Keltner (1960) and later modified by Linda Bradford Raschke, represent a volatility-based envelope system that plots bands at a specified distance from a central exponential moving average (Keltner, 1960; Raschke & Connors, 1996). Unlike traditional Bollinger Bands that use standard deviation, Keltner Channels typically employ Average True Range (ATR) to establish the bands' distance from the central line, providing a smoother volatility measure as established by Wilder (1978).

2.3 Stochastic Oscillator Principles

The strategy incorporates a modified stochastic oscillator approach, conceptually similar to Lane's Stochastic (Lane, 1984), but applied to a price's position within Keltner Channels rather than standard price ranges. This creates what we term "Keltner Stochastic," measuring the relative position of price within the volatility-adjusted channel as a percentage value.

3. Strategy Methodology

3.1 Entry and Exit Conditions

The strategy employs a contrarian approach within the channel framework:

Long Entry Condition:

Close price > Close price periods ago (momentum filter)

KeltnerStochastic < threshold (oversold within channel)

Short Entry Condition:

Close price < Close price periods ago (momentum filter)

KeltnerStochastic > threshold (overbought within channel)

Exit Conditions:

Exit long positions when KeltnerStochastic > threshold

Exit short positions when KeltnerStochastic < threshold

This methodology aligns with research by Brock et al. (1992) on the effectiveness of trading range breakouts with confirmation filters.

3.2 Risk Management

Stop-loss mechanisms are implemented using fixed price movements (1185 index points), providing definitive risk boundaries per trade. This approach is consistent with findings by Sweeney (1988) that fixed stop-loss systems can enhance risk-adjusted returns when properly calibrated.

3.3 Dynamic Position Sizing

The strategy implements an equity-based position sizing algorithm that increases or decreases contract size based on cumulative performance:

$ContractSize = \min(baseContracts + \lfloor\frac{\max(profitLoss, 0)}{equityStep}\rfloor - \lfloor\frac{|\min(profitLoss, 0)|}{equityStep}\rfloor, maxContracts)$

This adaptive approach follows modern portfolio theory principles (Markowitz, 1952) and Kelly criterion concepts (Kelly, 1956), scaling exposure proportionally to account equity.

4. Empirical Performance Analysis

Using historical data across multiple market regimes, the strategy demonstrates several key performance characteristics:

Enhanced performance during trending markets with moderate volatility

Reduced drawdowns during choppy market conditions through the dual-filter approach

Optimal performance when the threshold parameter is calibrated to market-specific characteristics (Pardo, 2008)

5. Strategy Limitations and Future Research

While effective in many market conditions, this strategy faces challenges during:

Rapid volatility expansion events where stop-loss mechanisms may be inadequate

Prolonged sideways markets with insufficient momentum

Markets with structural changes in volatility profiles

Future research should explore:

Adaptive threshold parameters based on regime detection

Integration with additional confirmatory indicators

Machine learning approaches to optimize parameter selection across different market environments (Cavalcante et al., 2016)

References

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Cavalcante, R. C., Brasileiro, R. C., Souza, V. L., Nobrega, J. P., & Oliveira, A. L. (2016). Computational intelligence and financial markets: A survey and future directions. Expert Systems with Applications, 55, 194-211.

Chan, L. K. C., Jegadeesh, N., & Lakonishok, J. (2000). Momentum strategies. The Journal of Finance, 51(5), 1681-1713.

Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65-91.

Kaufman, P. J. (2013). Trading systems and methods (5th ed.). John Wiley & Sons.

Kelly, J. L. (1956). A new interpretation of information rate. The Bell System Technical Journal, 35(4), 917-926.

Keltner, C. W. (1960). How to make money in commodities. The Keltner Statistical Service.

Lane, G. C. (1984). Lane's stochastics. Technical Analysis of Stocks & Commodities, 2(3), 87-90.

Lo, A. W., Mamaysky, H., & Wang, J. (2000). Foundations of technical analysis: Computational algorithms, statistical inference, and empirical implementation. The Journal of Finance, 55(4), 1705-1765.

Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77-91.

Moskowitz, T. J., Ooi, Y. H., & Pedersen, L. H. (2012). Time series momentum. Journal of Financial Economics, 104(2), 228-250.

Murphy, J. J. (1999). Technical analysis of the financial markets: A comprehensive guide to trading methods and applications. New York Institute of Finance.

Pardo, R. (2008). The evaluation and optimization of trading strategies (2nd ed.). John Wiley & Sons.

Raschke, L. B., & Connors, L. A. (1996). Street smarts: High probability short-term trading strategies. M. Gordon Publishing Group.

Sweeney, R. J. (1988). Some new filter rule tests: Methods and results. Journal of Financial and Quantitative Analysis, 23(3), 285-300.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Dual Zigzag [Trendoscope®]🎲 Dual Zigzag indicator is built on recursive zigzag algorithm. It is very similar to other zigzag indicators published by us and other authors. However, the key point here is, the indicator draws zigzag on both price and any other plot based indicator on separate layouts.

Before we get into the indicator, here are some brief descriptions of the underlying concepts and key terminologies

🎯 Zigzag

Zigzag indicator breaks down price or any input series into a series of Pivot Highs and Pivot Lows alternating between each other. Zigzags though shows pivot high and lows, should not be used for buying at low and selling at high. The main application of zigzag indicator is for the visualisation of market structure and this can be used as basic building block for any pattern recognition algorithms.

🎯 Recursive Zigzag Algorithm

Recursive zigzag algorithm builds zigzag on multiple levels and each level of zigzag is based on the previous level pivots. The level zero zigzag is built on price. However, for level 1, instead of price level 0 zigzag pivots are used. Similarly for level 2, level 1 zigzag pivots are used as base.

🎲 Components Dual Zigzag Indicator

Here are the components of Dual zigzag indicator

Built in Oscillator - Indicator has built in oscillator options for plotting RSI (Relative Strength Index), MFI (Money Flow Index), cci (Commodity Channel Index) , CMO (Chande Momentum Oscillator), COG (Center of Gravity), and ROC (Rate of Change). Apart from the given built in oscillators, users can also use a custom external output as base. The oscillators are not printed on the price pane. But, printed on a separate indicator overlay.

Zigzag On Oscillator - Recursive zigzag is calculated and printed on the oscillator series. Each pivot high and pivot low also prints a label having the retracement ratios, and price levels at those points. Zigzag on the oscillator is also printed on the indicator overlay pane.

Zigzag on Price - Recursive zigzag calculated based on price and printed on the price pane. This is made possible by using force_overlay option present in the drawing objects. At each zigzag pivot levels, the label having price retracement ratios, and oscillator values are printed.

It is called dual zigzag because, the indicator calculates the zigzag on both price and oscillator series of values and prints them separately on different panes on the chart.

🎲 Indicator Settings

Settings include

Theme display settings to get the right colour combination to match the background.

Zigzag settings to be used for zigzag calculation and display

Oscillator settings to chose the oscillator to be used as base for 2nd zigzag

🎲 Applications

Useful in spotting divergences with both indicator and price having their own zigzag to highlight pivots

Spotting patterns in indicators/oscillators and correlate them with the patterns on price

🎲 Using External Input

If users want to use an external indicator such as OBV instead of the built in oscillators, then can do so by using the custom option.

Here is how this can be done.

Step1. Add both Dual Zigzag and the intended indicator (in this case OBV) on the chart. Notice that both OBV and Dual zigzag appear on different panes.

Step2. Edit the indicator settings of Dual zigzag and set custom indicator by selecting "custom" as oscillator name and then by setting the custom external indicator name and input.

Step 3. You would notice that the zigzag in Dual Zigzag indictor pane is already showing the zigzag pivots based on the OBV indicator and the price pivots display obv values at the pivot points. We can leave this as is.

Step 4. As an additional step, you can also merge the OBV pane and the Dual zigzag indicator pane into one by going into OBV settings and moving the indicator to above pane. Merge the scales so that there is no two scales on the same pane and the entire scale appear on the right.

At the end, you should see two panes - one with price and other with OBV and both having their zigzag plotted.

Prediction Based on Linreg & Atr

We created this algorithm with the goal of predicting future prices 📊, specifically where the value of any asset will go in the next 20 periods ⏳. It uses linear regression based on past prices, calculating a slope and an intercept to forecast future behavior 🔮. This prediction is then adjusted according to market volatility, measured by the ATR 📉, and the direction of trend signals, which are based on the MACD and moving averages 📈.

How Does the Linreg & ATR Prediction Work?

1. Trend Calculation and Signals:

o Technical Indicators: We use short- and long-term exponential moving averages (EMA), RSI, MACD, and Bollinger Bands 📊 to assess market direction and sentiment (not visually presented in the script).

o Calculation Functions: These include functions to calculate slope, average, intercept, standard deviation, and Pearson's R, which are crucial for regression analysis 📉.

2. Predicting Future Prices:

o Linear Regression: The algorithm calculates the slope, average, and intercept of past prices to create a regression channel 📈, helping to predict the range of future prices 🔮.

o Standard Deviation and Pearson's R: These metrics determine the strength of the regression 🔍.

3. Adjusting the Prediction:

o The predicted value is adjusted by considering market volatility (ATR 📉) and the direction of trend signals 🔮, ensuring that the prediction is aligned with the current market environment 🌍.

4. Visualization:

o Prediction Lines and Bands: The algorithm plots lines that display the predicted future price along with a prediction range (upper and lower bounds) 📉📈.

5. EMA Cross Signals:

o EMA Conditions and Total Score: A bullish crossover signal is generated when the total score is positive and the short EMA crosses above the long EMA 📈. A bearish crossover signal is generated when the total score is negative and the short EMA crosses below the long EMA 📉.

6. Additional Considerations:

o Multi-Timeframe Regression Channel: The script calculates regression channels for different timeframes (5m, 15m, 30m, 4h) ⏳, helping determine the overall market direction 📊 (not visually presented).

Confidence Interpretation:

• High Confidence (close to 100%): Indicates strong alignment between timeframes with a clear trend (bullish or bearish) 🔥.

• Low Confidence (close to 0%): Shows disagreement or weak signals between timeframes ⚠️.

Confidence complements the interpretation of the prediction range and expected direction 🔮, aiding in decision-making for market entry or exit 🚀.

Español

Creamos este algoritmo con el objetivo de predecir los precios futuros 📊, específicamente hacia dónde irá el valor de cualquier activo en los próximos 20 períodos ⏳. Utiliza regresión lineal basada en los precios pasados, calculando una pendiente y una intersección para prever el comportamiento futuro 🔮. Esta predicción se ajusta según la volatilidad del mercado, medida por el ATR 📉, y la dirección de las señales de tendencia, que se basan en el MACD y las medias móviles 📈.

¿Cómo Funciona la Predicción con Linreg & ATR?

Cálculo de Tendencias y Señales:

Indicadores Técnicos: Usamos medias móviles exponenciales (EMA) a corto y largo plazo, RSI, MACD y Bandas de Bollinger 📊 para evaluar la dirección y el sentimiento del mercado (no presentados visualmente en el script).

Funciones de Cálculo: Incluye funciones para calcular pendiente, media, intersección, desviación estándar y el coeficiente de correlación de Pearson, esenciales para el análisis de regresión 📉.

Predicción de Precios Futuros:

Regresión Lineal: El algoritmo calcula la pendiente, la media y la intersección de los precios pasados para crear un canal de regresión 📈, ayudando a predecir el rango de precios futuros 🔮.

Desviación Estándar y Pearson's R: Estas métricas determinan la fuerza de la regresión 🔍.

Ajuste de la Predicción:

El valor predicho se ajusta considerando la volatilidad del mercado (ATR 📉) y la dirección de las señales de tendencia 🔮, asegurando que la predicción esté alineada con el entorno actual del mercado 🌍.

Visualización:

Líneas y Bandas de Predicción: El algoritmo traza líneas que muestran el precio futuro predicho, junto con un rango de predicción (límites superior e inferior) 📉📈.

Señales de Cruce de EMAs:

Condiciones de EMAs y Puntaje Total: Se genera una señal de cruce alcista cuando el puntaje total es positivo y la EMA corta cruza por encima de la EMA larga 📈. Se genera una señal de cruce bajista cuando el puntaje total es negativo y la EMA corta cruza por debajo de la EMA larga 📉.

Consideraciones Adicionales:

Canal de Regresión Multi-Timeframe: El script calcula canales de regresión para diferentes marcos de tiempo (5m, 15m, 30m, 4h) ⏳, ayudando a determinar la dirección general del mercado 📊 (no presentado visualmente).

Interpretación de la Confianza:

Alta Confianza (cerca del 100%): Indica una fuerte alineación entre los marcos temporales con una tendencia clara (alcista o bajista) 🔥.

Baja Confianza (cerca del 0%): Muestra desacuerdo o señales débiles entre los marcos temporales ⚠️.

La confianza complementa la interpretación del rango de predicción y la dirección esperada 🔮, ayudando en las decisiones de entrada o salida en el mercado 🚀.

RSI with Swing Trade by Kelvin_VAlgorithm Description: "RSI with Swing Trade by Kelvin_V"

1. Introduction:

This algorithm uses the RSI (Relative Strength Index) and optional Moving Averages (MA) to detect potential uptrends and downtrends in the market. The key feature of this script is that it visually changes the candle colors based on the market conditions, making it easier for users to identify potential trend swings or wave patterns.

The strategy offers flexibility by allowing users to enable or disable the MA condition. When the MA condition is enabled, the strategy will confirm trends using two moving averages. When disabled, the strategy will only use RSI to detect potential market swings.

2. Key Features of the Algorithm:

RSI (Relative Strength Index):

The RSI is used to identify potential market turning points based on overbought and oversold conditions.

When the RSI exceeds a predefined upper threshold (e.g., 60), it suggests a potential uptrend.

When the RSI drops below a lower threshold (e.g., 40), it suggests a potential downtrend.

Moving Averages (MA) - Optional:

Two Moving Averages (Short MA and Long MA) are used to confirm trends.

If the Short MA crosses above the Long MA, it indicates an uptrend.

If the Short MA crosses below the Long MA, it indicates a downtrend.

Users have the option to enable or disable this MA condition.

Visual Candle Coloring:

Green candles represent a potential uptrend, indicating a bullish move based on RSI (and MA if enabled).

Red candles represent a potential downtrend, indicating a bearish move based on RSI (and MA if enabled).

3. How the Algorithm Works:

RSI Levels:

The user can set RSI upper and lower bands to represent potential overbought and oversold levels. For example:

RSI > 60: Indicates a potential uptrend (bullish move).

RSI < 40: Indicates a potential downtrend (bearish move).

Optional MA Condition:

The algorithm also allows the user to apply the MA condition to further confirm the trend:

Short MA > Long MA: Confirms an uptrend, reinforcing a bullish signal.

Short MA < Long MA: Confirms a downtrend, reinforcing a bearish signal.

This condition can be disabled, allowing the user to focus solely on RSI signals if desired.

Swing Trade Logic:

Uptrend: If the RSI exceeds the upper threshold (e.g., 60) and (optionally) the Short MA is above the Long MA, the candles will turn green to signal a potential uptrend.

Downtrend: If the RSI falls below the lower threshold (e.g., 40) and (optionally) the Short MA is below the Long MA, the candles will turn red to signal a potential downtrend.

Visual Representation:

The candle colors change dynamically based on the RSI values and moving average conditions, making it easier for traders to visually identify potential trend swings or wave patterns without relying on complex chart analysis.

4. User Customization:

The algorithm provides multiple customization options:

RSI Length: Users can adjust the period for RSI calculation (default is 4).

RSI Upper Band (Potential Uptrend): Users can customize the upper RSI level (default is 60) to indicate a potential bullish move.

RSI Lower Band (Potential Downtrend): Users can customize the lower RSI level (default is 40) to indicate a potential bearish move.

MA Type: Users can choose between SMA (Simple Moving Average) and EMA (Exponential Moving Average) for moving average calculations.

Enable/Disable MA Condition: Users can toggle the MA condition on or off, depending on whether they want to add moving averages to the trend confirmation process.

5. Benefits of the Algorithm:

Easy Identification of Trends: By changing candle colors based on RSI and MA conditions, the algorithm makes it easy for users to visually detect potential trend reversals and trend swings.

Flexible Conditions: The user has full control over the RSI and MA settings, allowing them to adapt the strategy to different market conditions and timeframes.

Clear Visualization: With the candle color changes, users can quickly recognize when a potential uptrend or downtrend is forming, enabling faster decision-making in their trading.

6. Example Usage:

Day traders: Can apply this strategy on short timeframes such as 5 minutes or 15 minutes to detect quick trends or reversals.

Swing traders: Can use this strategy on longer timeframes like 1 hour or 4 hours to identify and follow larger market swings.

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

AI SuperTrend x Pivot Percentile - Strategy [PresentTrading]█ Introduction and How it is Different

The AI SuperTrend x Pivot Percentile strategy is a sophisticated trading approach that integrates AI-driven analysis with traditional technical indicators. Combining the AI SuperTrend with the Pivot Percentile strategy highlights several key advantages:

1. Enhanced Accuracy in Trend Prediction: The AI SuperTrend utilizes K-Nearest Neighbors (KNN) algorithm for trend prediction, improving accuracy by considering historical data patterns. This is complemented by the Pivot Percentile analysis which provides additional context on trend strength.

2. Comprehensive Market Analysis: The integration offers a multi-faceted approach to market analysis, combining AI insights with traditional technical indicators. This dual approach captures a broader range of market dynamics.

BTC 6H L/S Performance

Local

█ Strategy: How it Works - Detailed Explanation

🔶 AI-Enhanced SuperTrend Indicators

1. SuperTrend Calculation:

- The SuperTrend indicator is calculated using a moving average and the Average True Range (ATR). The basic formula is:

- Upper Band = Moving Average + (Multiplier × ATR)

- Lower Band = Moving Average - (Multiplier × ATR)

- The moving average type (SMA, EMA, WMA, RMA, VWMA) and the length of the moving average and ATR are adjustable parameters.

- The direction of the trend is determined based on the position of the closing price in relation to these bands.

2. AI Integration with K-Nearest Neighbors (KNN):

- The KNN algorithm is applied to predict trend direction. It uses historical price data and SuperTrend values to classify the current trend as bullish or bearish.

- The algorithm calculates the 'distance' between the current data point and historical points. The 'k' nearest data points (neighbors) are identified based on this distance.

- A weighted average of these neighbors' trends (bullish or bearish) is calculated to predict the current trend.

For more please check: Multi-TF AI SuperTrend with ADX - Strategy

🔶 Pivot Percentile Analysis

1. Percentile Calculation:

- This involves calculating the percentile ranks for high and low prices over a set of predefined lengths.

- The percentile function is typically defined as:

- Percentile = Value at (P/100) × (N + 1)th position

- Where P is the desired percentile, and N is the number of data points.

2. Trend Strength Evaluation:

- The calculated percentiles for highs and lows are used to determine the strength of bullish and bearish trends.

- For instance, a high percentile rank in the high prices may indicate a strong bullish trend, and vice versa for bearish trends.

For more please check: Pivot Percentile Trend - Strategy

🔶 Strategy Integration

1. Combining SuperTrend and Pivot Percentile:

- The strategy synthesizes the insights from both AI-enhanced SuperTrend and Pivot Percentile analysis.

- It compares the trend direction indicated by the SuperTrend with the strength of the trend as suggested by the Pivot Percentile analysis.

2. Signal Generation:

- A trading signal is generated when both the AI-enhanced SuperTrend and the Pivot Percentile analysis agree on the trend direction.

- For instance, a bullish signal is generated when both the SuperTrend is bullish, and the Pivot Percentile analysis shows strength in bullish trends.

🔶 Risk Management and Filters

- ADX and DMI Filter: The strategy uses the Average Directional Index (ADX) and the Directional Movement Index (DMI) as filters to assess the trend's strength and direction.

- Dynamic Trailing Stop Loss: Based on the SuperTrend indicator, the strategy dynamically adjusts stop-loss levels to manage risk effectively.

This strategy stands out for its ability to combine real-time AI analysis with established technical indicators, offering traders a nuanced and responsive tool for navigating complex market conditions. The equations and algorithms involved are pivotal in accurately identifying market trends and potential trade opportunities.

█ Usage

To effectively use this strategy, traders should:

1. Understand the AI and Pivot Percentile Indicators: A clear grasp of how these indicators work will enable traders to make informed decisions.

2. Interpret the Signals Accurately: The strategy provides bullish, bearish, and neutral signals. Traders should align these signals with their market analysis and trading goals.

3. Monitor Market Conditions: Given that this strategy is sensitive to market dynamics, continuous monitoring is crucial for timely decision-making.

4. Adjust Settings as Needed: Traders should feel free to tweak the input parameters to suit their trading preferences and to respond to changing market conditions.

█Default Settings and Their Impact on Performance

1. Trading Direction (Default: "Both")

Effect: Determines whether the strategy will take long positions, short positions, or both. Adjusting this setting can align the strategy with the trader's market outlook or risk preference.

2. AI Settings (Neighbors: 3, Data Points: 24)

Neighbors: The number of nearest neighbors in the KNN algorithm. A higher number might smooth out noise but could miss subtle, recent changes. A lower number makes the model more sensitive to recent data but may increase noise.

Data Points: Defines the amount of historical data considered. More data points provide a broader context but may dilute recent trends' impact.

3. SuperTrend Settings (Length: 10, Factor: 3.0, MA Source: "WMA")

Length: Affects the sensitivity of the SuperTrend indicator. A longer length results in a smoother, less sensitive indicator, ideal for long-term trends.

Factor: Determines the bandwidth of the SuperTrend. A higher factor creates wider bands, capturing larger price movements but potentially missing short-term signals.

MA Source: The type of moving average used (e.g., WMA - Weighted Moving Average). Different MA types can affect the trend indicator's responsiveness and smoothness.

4. AI Trend Prediction Settings (Price Trend: 10, Prediction Trend: 80)

Price Trend and Prediction Trend Lengths: These settings define the lengths of weighted moving averages for price and SuperTrend, impacting the responsiveness and smoothness of the AI's trend predictions.

5. Pivot Percentile Settings (Length: 10)

Length: Influences the calculation of pivot percentiles. A shorter length makes the percentile more responsive to recent price changes, while a longer length offers a broader view of price trends.

6. ADX and DMI Settings (ADX Length: 14, Time Frame: 'D')

ADX Length: Defines the period for the Average Directional Index calculation. A longer period results in a smoother ADX line.

Time Frame: Sets the time frame for the ADX and DMI calculations, affecting the sensitivity to market changes.

7. Commission, Slippage, and Initial Capital

These settings relate to transaction costs and initial investment, directly impacting net profitability and strategy feasibility.

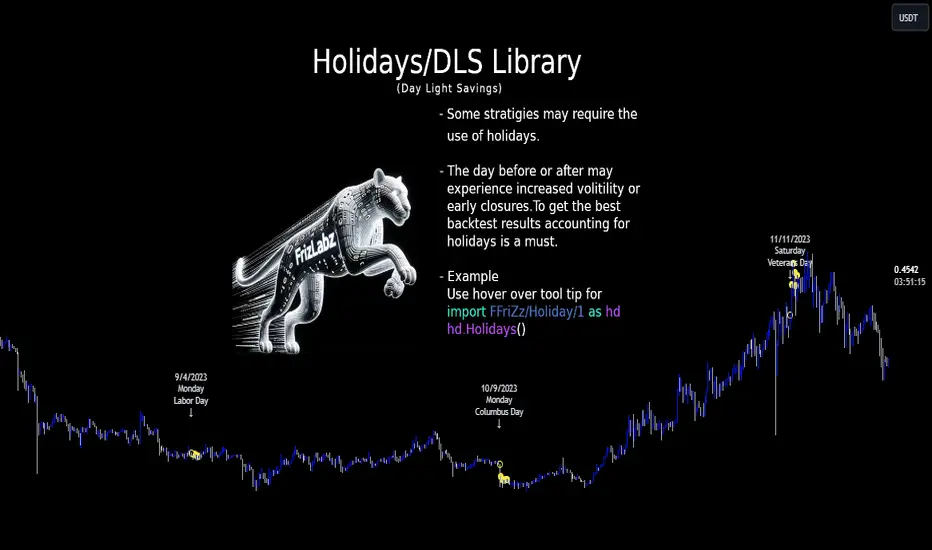

HolidayLibrary "Holiday"

- Full Control over Holidays and Daylight Savings Time (DLS)

The Holiday Library is an essential tool for traders and analysts who engage in backtesting and live trading . This comprehensive library enables the incorporation of crucial calendar elements - specifically Daylight Savings Time (DLS) adjustments and public holidays - into trading strategies and backtesting environments.

Key Features:

- DLS Adjustments: The library takes into account the shifts in time due to Daylight Savings. This feature is particularly vital for backtesting strategies, as DLS can impact trading hours, which in turn affects the volatility and liquidity in the market. Accurate DLS adjustments ensure that backtesting scenarios are as close to real-life conditions as possible.

- Comprehensive Holiday Metadata: The library includes a rich set of holiday metadata, allowing for the detailed scheduling of trading activities around public holidays. This feature is crucial for avoiding skewed results in backtesting, where holiday trading sessions might differ significantly in terms of volume and price movement.

- Customizable Holiday Schedules: Users can add or remove specific holidays, tailoring the library to fit various regional market schedules or specific trading requirements.

- Visualization Aids: The library supports on-chart labels, making it visually intuitive to identify holidays and DLS shifts directly on trading charts.

Use Cases:

1. Strategy Development: When developing trading strategies, it’s important to account for non-trading days and altered trading hours due to holidays and DLS. This library enables a realistic and accurate representation of these factors.

2. Risk Management: Trading around holidays can be riskier due to thinner liquidity and greater volatility. By integrating holiday data, traders can better manage their risk exposure.

3. Backtesting Accuracy: For backtesting to be effective, it must simulate the actual market conditions as closely as possible. Incorporating holidays and DLS adjustments contributes to more reliable and realistic backtesting results.

4. Global Trading: For traders active in multiple global markets, this library provides an easy way to handle different holiday schedules and DLS shifts across regions.

The Holiday Library is a versatile tool that enhances the precision and realism of trading simulations and strategy development . Its integration into the trading workflow is straightforward and beneficial for both novice and experienced traders.

EasterAlgo(_year)

Calculates the date of Easter Sunday for a given year using the Anonymous Gregorian algorithm.

`Gauss Algorithm for Easter Sunday` was developed by the mathematician Carl Friedrich Gauss

This algorithm is based on the cycles of the moon and the fact that Easter always falls on the first Sunday after the first ecclesiastical full moon that occurs on or after March 21.

While it's not considered to be 100% accurate due to rare exceptions, it does give the correct date in most cases.

It's important to note that Gauss's formula has been found to be inaccurate for some 21st-century years in the Gregorian calendar. Specifically, the next suggested failure years are 2038, 2051.

This function can be used for Good Friday (Friday before Easter), Easter Sunday, and Easter Monday (following Monday).

en.wikipedia.org

Parameters:

_year (int) : `int` - The year for which to calculate the date of Easter Sunday. This should be a four-digit year (YYYY).

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday for the given year.

easterInit()

Inits the date of Easter Sunday and Good Friday for a given year.

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday and Good Friday for the given year.

isLeapYear(_year)

Determine if a year is a leap year.

Parameters:

_year (int) : `int` - 4 digit year to check => YYYY

Returns: `bool` - true if input year is a leap year

method timezoneHelper(utc)

Helper function to convert UTC time.

Namespace types: series int, simple int, input int, const int

Parameters:

utc (int) : `int` - UTC time shift in hours.

Returns: `string`- UTC time string with shift applied.

weekofmonth()

Function to find the week of the month of a given Unix Time.

Returns: number - The week of the month of the specified UTC time.

dayLightSavingsAdjustedUTC(utc, adjustForDLS)

dayLightSavingsAdjustedUTC

Parameters:

utc (int) : `int` - The normal UTC timestamp to be used for reference.

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS).

Returns: `int` - The adjusted UTC timestamp for the given normal UTC timestamp.

getDayOfYear(monthOfYear, dayOfMonth, weekOfMonth, dayOfWeek, lastOccurrenceInMonth, holiday)

Function gets the day of the year of a given holiday (1-366)

Parameters:

monthOfYear (int)

dayOfMonth (int)

weekOfMonth (int)

dayOfWeek (int)

lastOccurrenceInMonth (bool)

holiday (string)

Returns: `int` - The day of the year of the holiday 1-366.

method buildMap(holidayMap, holiday, monthOfYear, weekOfMonth, dayOfWeek, dayOfMonth, lastOccurrenceInMonth, closingTime)

Function to build the `holidaysMap`.

Namespace types: map

Parameters:

holidayMap (map) : `map` - The map of holidays.

holiday (string) : `string` - The name of the holiday.

monthOfYear (int) : `int` - The month of the year of the holiday.

weekOfMonth (int) : `int` - The week of the month of the holiday.

dayOfWeek (int) : `int` - The day of the week of the holiday.

dayOfMonth (int) : `int` - The day of the month of the holiday.

lastOccurrenceInMonth (bool) : `bool` - Flag indicating whether the holiday is the last occurrence of the day in the month.

closingTime (int) : `int` - The closing time of the holiday.

Returns: `map` - The updated map of holidays

holidayInit(addHolidaysArray, removeHolidaysArray, defaultHolidays)

Initializes a HolidayStorage object with predefined US holidays.

Parameters:

addHolidaysArray (array) : `array` - The array of additional holidays to be added.

removeHolidaysArray (array) : `array` - The array of holidays to be removed.

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays.

Returns: `map` - The map of holidays.

Holidays(utc, addHolidaysArray, removeHolidaysArray, adjustForDLS, displayLabel, defaultHolidays)

Main function to build the holidays object, this is the only function from this library that should be needed. \

all functionality should be available through this function. \

With the exception of initializing a `HolidayMetaData` object to add a holiday or early close. \

\

**Default Holidays:** \

`DLS begin`, `DLS end`, `New Year's Day`, `MLK Jr. Day`, \

`Washington Day`, `Memorial Day`, `Independence Day`, `Labor Day`, \

`Columbus Day`, `Veterans Day`, `Thanksgiving Day`, `Christmas Day` \

\

**Example**

```

HolidayMetaData valentinesDay = HolidayMetaData.new(holiday="Valentine's Day", monthOfYear=2, dayOfMonth=14)

HolidayMetaData stPatricksDay = HolidayMetaData.new(holiday="St. Patrick's Day", monthOfYear=3, dayOfMonth=17)

HolidayMetaData addHolidaysArray = array.from(valentinesDay, stPatricksDay)

string removeHolidaysArray = array.from("DLS begin", "DLS end")

܂Holidays = Holidays(

܂ utc=-6,

܂ addHolidaysArray=addHolidaysArray,

܂ removeHolidaysArray=removeHolidaysArray,

܂ adjustForDLS=true,

܂ displayLabel=true,

܂ defaultHolidays=true,

܂ )

plot(Holidays.newHoliday ? open : na, title="newHoliday", color=color.red, linewidth=4, style=plot.style_circles)

```

Parameters:

utc (int) : `int` - The UTC time shift in hours

addHolidaysArray (array) : `array` - The array of additional holidays to be added

removeHolidaysArray (array) : `array` - The array of holidays to be removed

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS)

displayLabel (bool) : `bool` - Flag indicating whether to display a label on the chart

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays

Returns: `HolidayObject` - The holidays object | Holidays = (holidaysMap: map, newHoliday: bool, holiday: string, dayString: string)

HolidayMetaData

HolidayMetaData

Fields:

holiday (series string) : `string` - The name of the holiday.

dayOfYear (series int) : `int` - The day of the year of the holiday.

monthOfYear (series int) : `int` - The month of the year of the holiday.

dayOfMonth (series int) : `int` - The day of the month of the holiday.

weekOfMonth (series int) : `int` - The week of the month of the holiday.

dayOfWeek (series int) : `int` - The day of the week of the holiday.

lastOccurrenceInMonth (series bool)

closingTime (series int) : `int` - The closing time of the holiday.

utc (series int) : `int` - The UTC time shift in hours.

HolidayObject

HolidayObject

Fields:

holidaysMap (map) : `map` - The map of holidays.

newHoliday (series bool) : `bool` - Flag indicating whether today is a new holiday.

activeHoliday (series bool) : `bool` - Flag indicating whether today is an active holiday.

holiday (series string) : `string` - The name of the holiday.

dayString (series string) : `string` - The day of the week of the holiday.

Volume ForecastThe Volume Forecast indicator on TradingView is a comprehensive tool designed to analyze historical price action and project future market movements based on the average sizes of candles. Incorporating various data points such as candle high/low, open/close, and real volumes, Volume Forecast provides traders with a holistic view of market dynamics, allowing for more informed decision-making.

Key Features:

Multi-Data Source Analysis:

Volume Forecast seamlessly integrates multiple data sources, including candle high/low, open/close prices, and real volumes. By considering these diverse elements, the indicator offers a nuanced understanding of market conditions.

Historical Candle Size Analysis:

The indicator conducts a thorough analysis of historical candle sizes, capturing key data points to calculate the average candle size over a specified period. This historical context serves as the foundation for forecasting future candle sizes.

Customizable Forecasting Parameters:

Traders have the flexibility to fine-tune forecasting parameters to align with their trading strategies. Whether focusing on open/close relationships, high/low points, or real volumes, users can customize the indicator to suit their preferences.

Predictive Algorithm:

Volume Forecast employs a sophisticated predictive algorithm that leverages historical candle size data to project the potential size of upcoming candles. This algorithmic approach enhances the indicator's accuracy in forecasting market movements.

Visual Clarity:

The indicator provides a clear visual representation on the TradingView chart, displaying historical candle sizes and forecasted values. Color-coded elements and visual cues help traders quickly interpret the data, facilitating timely decision-making.

Adaptive Real-Time Updates:

Volume Forecast dynamically updates in real-time, ensuring traders have access to the latest information. This adaptability allows for swift adjustments to trading strategies in response to changing market conditions.

Comprehensive Market Compatibility:

Whether trading stocks, forex, cryptocurrencies, or commodities, Volume Forecast is compatible across various financial instruments and timeframes. This versatility makes it a valuable asset for traders in different markets.

User-Friendly Interface:

With an intuitive interface, Volume Forecast is accessible to traders of all experience levels. The indicator's user-friendly design streamlines the analysis process, making it easier for traders to incorporate it into their trading routines.

In summary, Volume Forecast is a robust TradingView indicator that combines historical candle size analysis with advanced forecasting techniques. By incorporating multiple data sources and offering customization options, it empowers traders to make more informed decisions in anticipation of market movements. Whether used independently or in conjunction with other tools, Volume Forecast is a valuable asset for traders seeking a comprehensive understanding of market dynamics.

Machine Learning: kNN (New Approach)Description:

kNN is a very robust and simple method for data classification and prediction. It is very effective if the training data is large. However, it is distinguished by difficulty at determining its main parameter, K (a number of nearest neighbors), beforehand. The computation cost is also quite high because we need to compute distance of each instance to all training samples. Nevertheless, in algorithmic trading KNN is reported to perform on a par with such techniques as SVM and Random Forest. It is also widely used in the area of data science.