Gaussian Weighted Moving Average with Forecast [CHE]Presentation for TradingView: Gaussian Weighted Moving Average with Forecast

Introduction

Welcome to our presentation on the "Gaussian Weighted Moving Average with Forecast" (GWMA). This script, written in Pine Script™, offers an enhanced method for analyzing and predicting price movements on TradingView. The script combines Gaussian Weighted Moving Averages and polynomial regression to provide accurate and customizable forecasts.

Overview

Title: Gaussian Weighted Moving Average with Forecast

Author: chervolino

License: Mozilla Public License 2.0

Main Features

1. Gaussian Weighted Moving Average (GWMA):

- Calculates a weighted moving average using a Gaussian weighting function.

- Parameters for length and standard deviation allow fine-tuning of the smoothing effect.

2. Polynomial Regression with Forecast:

- Creates a model to predict future price movements.

- Adjustable length and degree of polynomial regression.

- Option to extrapolate predictions and visualize them.

3. Visual Representation:

- Uses lines and colors to depict trend changes.

- Customizable colors for upward and downward trends.

Input Parameters

Length: Length of the moving average (default: 50)

Standard Deviation: Standard deviation for Gaussian weighting (default: 10.0)

Width: Width of the plotted lines (default: 1)

Colors: Customizable colors for upward and downward trends

Forecast Length: Length of the forecast period (default: 20)

Extrapolate Length: Length of the extrapolation (default: 50)

Polynomial Degree: Degree of the polynomial regression (default: 3)

Lock Forecast: Option to lock and stabilize the forecast

Core Algorithms

1. Gaussian Weight Calculation:

gaussian_weight(x, std_dev) =>

1 / (std_dev * math.sqrt(2 * math.pi)) * math.exp(-0.5 * math.pow(x / std_dev, 2))

2. GWMA Calculation:

calculate_gwma(length, std_dev) =>

// Algorithm to calculate the weighted moving average

3. Initialize Lines for Polynomial Regression:

initialize_lines_array(extrapolate, length) =>

// Initialize array lines

4. Create Design Matrix for Polynomial Regression:

get_design_matrix(length, degree) =>

// Create the design matrix

5. Calculate and Plot Polynomial Regression:

calculate_polynomial_regression(src, length, degree, extrapolate, lines_arr, lock, width, upward_color, downward_color) =>

// Algorithm to calculate polynomial regression and plot the forecast

Combining Indicators: Originality and Usefulness

The combination of Gaussian Weighted Moving Average and polynomial regression provides traders with a robust tool for trend analysis and prediction. The GWMA smooths out price data while emphasizing recent prices, making it sensitive to short-term trends. Polynomial regression, on the other hand, offers a mathematical approach to model and forecast future prices based on historical data. By integrating these two methodologies, traders can achieve a more comprehensive view of market trends and potential future movements, making the tool highly valuable for decision-making.

Explanation for Users

Most TradingView users are not familiar with Pine Script, so a clear description is essential for understanding how to use the script.

Gaussian Weighted Moving Average (GWMA): This indicator calculates a moving average using Gaussian weights, which gives more importance to recent prices. The length and standard deviation parameters allow users to control the sensitivity and smoothness of the average.

Polynomial Regression with Forecast: This feature uses polynomial regression to model the price trend and predict future movements. Users can adjust the length of the historical data used, the degree of the polynomial, and the length of the forecast. The script plots these predictions, making it easier for traders to visualize potential future price paths.

Visualization of Results

1. GWMA Plotting:

plot(gaussian_ma_result, title="GWMA", color=line_color, linewidth=width_input)

2. Forecast Extrapolation:

plot(forecast_val, 'Extrapolation', offset=extrapolate_setting, linewidth=width_input, style=plot.style_circles)

Conclusion

The "Gaussian Weighted Moving Average with Forecast" script provides a powerful tool for analyzing and predicting price movements on TradingView. By combining Gaussian weighting and polynomial regression, it offers a precise and customizable method for trend analysis and forecasting.

Thank you for your attention! For any questions or further information, please feel free to reach out.

Cerca negli script per "algo"

Venit A.I Trading V1RSI indicatorThis indicator is designed to provide buy and sell signals based on the Relative Strength Index (RSI). Here's a breakdown of its components and functionality:

1. **Input Parameters**:

- `Period`: This parameter allows the user to adjust the period used in calculating the RSI.

- `Upper Threshold` and `Lower Threshold`: These parameters define the overbought and oversold levels for the RSI.

- `Imverse Algorithm`: This parameter allows the user to toggle between different algorithms for generating buy and sell signals.

- `Show Lines`: This parameter toggles the visibility of lines on the chart indicating buy and sell signals.

- `Show Labels`: This parameter toggles the visibility of labels on the chart indicating buy and sell signals.

2. **RSI Calculation**:

- The RSI is calculated using the specified period (`myPeriod`), typically representing the closing prices of the asset.

3. **Buy and Sell Conditions**:

- Buy conditions are determined based on whether the RSI crosses below the lower threshold (`myThresholdDn`), indicating potential oversold conditions.

- Sell conditions are determined based on whether the RSI crosses above the upper threshold (`myThresholdUp`), indicating potential overbought conditions.

- The choice of buy and sell conditions can be toggled using the `Imverse Algorithm` parameter.

4. **Position Tracking**:

- The indicator maintains a variable `myPosition` to track the current position (buy or sell) based on the generated signals.

- If a buy signal occurs (`buy` condition is true), `myPosition` is set to 0. If a sell signal occurs (`sell` condition is true) or the previous position was a buy, `myPosition` is set to 1. Otherwise, `myPosition` remains unchanged.

5. **Visualization**:

- Buy and sell signals are plotted on the chart using shapes (`plotshape`) based on the `myLineToggle` and `myLabelToggle` parameters.

- Lines are drawn on the chart to visually represent buy and sell signals.

- Labels are placed on the chart indicating buy and sell signals.

6. **Alerts**:

- The indicator provides alerts for buy and sell signals using the `alertcondition` function.

Overall, this indicator aims to provide traders with signals based on RSI movements, helping them identify potential buying and selling opportunities in the market. The flexibility in parameters allows users to customize the indicator based on their trading preferences and strategies.

DNA GRAVITY PRICE V1 PINESCRIPTLABSWe can observe that this indicator displays the range within which the asset fluctuates around the average price, and its behavior depends on the parameters of amplitude and angular frequency. "price_mas" is a measure calculated as part of the indicator. It is derived by adding an adjusted amplitude (A_mas) multiplied by the cosine of the combination of angular frequency (w), time, and a phase shift (phi) to the average price (P0). This calculated value oscillates around the actual asset price and is used to identify potential turning points and the range where the price has established itself within the specified lookback period.

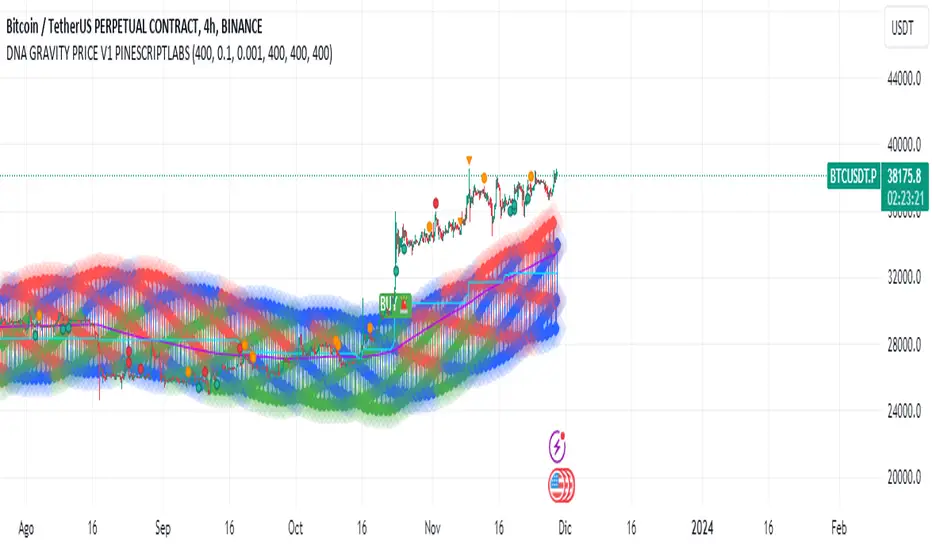

2.- At its core, the indicator utilizes the innovative concept of 'price_mas,' a calculated metric visualized in three essential colors: green to indicate low levels, blue for medium levels, and red for high levels. These colors reflect the position of the price in relation to a range determined by historical highs and lows.

In the context of the "DNA GRAVITY PRICE V1 " indicator, low, medium, and high levels specifically refer to the calculated value of 'price_mas,' which is a derived measure within the indicator. They do not directly refer to the actual asset price but rather to a calculated value that the indicator uses to analyze and predict the behavior of the asset's price.

This algorithm stands out for its ability to capture the 'strength' of the price through the 'price_mas' zones. Once the price exits the zones marked by the 'price_mas' (red, blue, and green plots), it tends to return with significant force.

Buy & Sell Signals:

Buy Signal: If the price and the Donchian lines cross above the high threshold, visually represented by red diamonds, it indicates a strong bullish momentum. This not only shows that the price is rising but also that the trend is strong enough to push the Donchian lines, which represent price extremes over a certain period, above the threshold. This convergence of movements, marked by the crossing over the red diamonds, suggests a higher probability of the bullish trend continuing.

Sell Signal: Similarly, if the price and the Donchian lines fall below the low threshold, visualized as green diamonds, this signals a significant bearish momentum. The simultaneous decline of the price and the Donchian lines below this threshold, marked by the green diamonds, indicates that not only is the price decreasing, but the bearish trend is strong enough to influence the price extremes calculated by the Donchian lines.

Configuration:

-The "Initial Dynamic Length of MAS Price" parameter controls the smoothness and sensitivity of the indicator. A high value smooths the Simple Moving Average (SMA), making the indicator less responsive to short-term price fluctuations. On the other hand, a low value makes the indicator more sensitive to short-term price fluctuations, generating faster and more volatile signals

-This parameter, "MAS Amplitude Percentage," determines the amplitude as a percentage. Increasing the Initial Dynamic Price will result in a larger amplitude relative to the price, leading to wider ranges for the indicator. Decreasing this value will have the opposite effect, reducing the amplitude relative to the price. Increasing "A_mas_pct" can make signals more extreme and less frequent, while decreasing it will make signals smoother and more frequent.

-This parameter, "Angular Frequency of MAS," affects the frequency of oscillations in the calculation of the "Initial Dynamic Price." A higher value of "w" will make the oscillations faster and more frequent, which means that the indicator will be more responsive to abrupt price changes. Conversely, a lower value will make the oscillations slower and smoother, making the indicator less sensitive to rapid price changes. Modifying ""Angular Frequency of MAS,"" directly impacts the frequency of oscillations in the indicator.

Español:

Podemos observar que este indicador muestra el rango en el cual el activo fluctúa alrededor del precio promedio y su comportamiento depende de los parámetros de amplitud y frecuencia angular. "price_mas" es una medida calculada como parte del indicador. Se deriva al sumar una amplitud ajustada (A_mas) multiplicada por el coseno de la combinación de frecuencia angular (w), tiempo y un desplazamiento de fase (phi) al precio promedio (P0). Este valor calculado oscila alrededor del precio real del activo y se utiliza para identificar posibles puntos de giro y el rango donde el precio se ha establecido dentro del período de búsqueda especificado.

En su núcleo, el indicador utiliza el innovador concepto de 'price_mas', una métrica calculada visualizada en tres colores esenciales: verde para indicar niveles bajos, azul para niveles medios y rojo para niveles altos. Estos colores reflejan la posición del precio en relación con un rango determinado por los máximos y mínimos históricos.

En el contexto del indicador "DNA GRAVITY PRICE V1", los niveles bajos, medios y altos se refieren específicamente al valor calculado de 'price_mas', que es una medida derivada dentro del indicador. No se refieren directamente al precio real del activo, sino a un valor calculado que el indicador utiliza para analizar y predecir el comportamiento del precio del activo.

Este algoritmo se destaca por su capacidad para capturar la 'fortaleza' del precio a través de las zonas de 'price_mas'. Una vez que el precio sale de las zonas marcadas por 'price_mas' (trazas rojas, azules y verdes), tiende a regresar con una fuerza significativa. Este comportamiento es crucial para los operadores, ya que proporciona oportunidades tanto para capitalizar las retracciones de precios como para anticipar posibles cambios de tendencia.

Señales de Compra y Venta:

Señal de Compra: Si el precio y las líneas Donchian cruzan por encima del umbral alto, visualmente representado por diamantes rojos, indica un fuerte impulso alcista. Esto no solo muestra que el precio está aumentando, sino que la tendencia es lo suficientemente fuerte como para empujar las líneas Donchian, que representan los extremos de precio durante un período determinado, por encima del umbral. Esta convergencia de movimientos, marcada por el cruce sobre los diamantes rojos, sugiere una mayor probabilidad de que la tendencia alcista continúe.

Señal de Venta: De manera similar, si el precio y las líneas Donchian caen por debajo del umbral bajo, visualizado como diamantes verdes, esto señala un fuerte impulso bajista. La caída simultánea del precio y las líneas Donchian por debajo de este umbral, marcada por los diamantes verdes, indica que no solo el precio está disminuyendo, sino que la tendencia bajista es lo suficientemente fuerte como para influir en los extremos de precio calculados por las líneas Donchian.

Configuración:

El parámetro "Longitud Dinámica Inicial de MAS Price" controla la suavidad y la sensibilidad del indicador. Un valor alto suaviza el Promedio Móvil Simple (SMA), lo que hace que el indicador sea menos sensible a las fluctuaciones de precio a corto plazo. Por otro lado, un valor bajo hace que el indicador sea más sensible a las fluctuaciones de precio a corto plazo, generando señales más rápidas y volátiles.

Este parámetro, "Porcentaje de Amplitud de MAS," determina la amplitud como un porcentaje. Aumentar el valor de "Longitud Dinámica Inicial de MAS Price" dará como resultado una amplitud más grande en relación con el precio, lo que conducirá a rangos más amplios para el indicador. Disminuir este valor tendrá el efecto contrario, reduciendo la amplitud en relación con el precio. Aumentar "Porcentaje de A_mas" puede hacer que las señales sean más extremas y menos frecuentes, mientras que disminuirlo hará que las señales sean más suaves y más frecuentes.

Este parámetro, "Frecuencia Angular de MAS," afecta la frecuencia de las oscilaciones en el cálculo del "Precio Móvil Simple Inicial." Un valor más alto de "w" hará que las oscilaciones sean más rápidas y frecuentes, lo que significa que el indicador será más receptivo a cambios abruptos en el precio. Por otro lado, un valor más bajo hará que las oscilaciones sean más lentas y suaves, haciendo que el indicador sea menos sensible a cambios rápidos en el precio. Modificar "Frecuencia Angular de MAS" afecta directamente la frecuencia de las oscilaciones en el indicador.

IPDA Standard Deviations [DexterLab x TFO x toodegrees]> Introduction and Acknowledgements

The IPDA Standard Deviations tool encompasses the Time and price relationship as studied by @TraderDext3r .

I am not the creator of this Theory, and I do not hold the answers to all the questions you may have; I suggest you to study it from Dexter's tweets, videos, and material.

This tool was born from a collaboration between @TraderDext3r, @tradeforopp and I, with the objective of bringing a comprehensive IPDA Standard Deviations tool to Tradingview.

> Tool Description

This is purely a graphical aid for traders to be able to quickly determine Fractal IPDA Time Windows, and trace the potential Standard Deviations of the moves at their respective high and low extremes.

The disruptive value of this tool is that it allows traders to save Time by automatically adapting the Time Windows based on the current chart's Timeframe, as well as providing customizations to filter and focus on the appropriate Standard Deviations.

> IPDA Standard Deviations by TraderDext3r

The underlying idea is based on the Interbank Price Delivery Algorithm's lookback windows on the daily chart as taught by the Inner Circle Trader:

IPDA looks at the past three months of price action to determine how to deliver price in the future.

Additionally, the ICT concept of projecting specific manipulation moves prior to large displacement upwards/downwards is used to navigate and interpret the priorly mentioned displacement move. We pay attention to specific Standard Deviations based on the current environment and overall narrative.

Dexter being one of the most prominent Inner Circle Trader students, harnessed the fractal nature of price to derive fractal IPDA Lookback Time Windows for lower Timeframes, and studied the behaviour of price at specific Deviations.

For Example:

The -1 to -2 area can initiate an algorithmic retracement before continuation.

The -2 to -2.5 area can initiate an algorithmic retracement before continuation, or a Smart Money Reversal.

The -4 area should be seen as the ultimate objective, or the level at which the displacement will slow down.

Given that these ideas stem from ICT's concepts themselves, they are to be used hand in hand with all other ICT Concepts (PD Array Matrix, PO3, Institutional Price Levels, ...).

> Fractal IPDA Time Windows

The IPDA Lookbacks Types identified by Dexter are as follows:

Monthly – 1D Chart: one widow per Month, highlighting the past three Months.

Weekly – 4H to 8H Chart: one window per Week, highlighting the past three Weeks.

Daily – 15m to 1H Chart: one window per Day, highlighting the past three Days.

Intraday – 1m to 5m Chart: one window per 4 Hours highlighting the past 12 Hours.

Inside these three respective Time Windows, the extreme High and Low will be identified, as well as the prior opposing short term market structure point. These represent the anchors for the Standard Deviation Projections.

> Tool Settings

The User is able to plot any type of Standard Deviation they want by inputting them in the settings, in their own line of the text box. They will always be plotted from the Time Windows extremes.

As previously mentioned, the User is also able to define their own Timeframe intervals for the respective IPDA Lookback Types. The specific Timeframes on which the different Lookback Types are plotted are edge-inclusive. In case of an overlap, the higher Timeframe Lookback will be prioritized.

Finally the User is able to filter and remove Standard Deviations in two ways:

"Remove Once Invalidated" will automatically delete a Deviation once its outer anchor extreme is traded through.

Manual Toggles will allow to remove the Upward or Downward Deviation of each Time Window at the discretion of the User.

Major shoutout to Dexter and TFO for their Time, it was a pleasure to collaborate and create this tool with them.

GLGT!

Machine Learning Momentum Oscillator [ChartPrime]The Machine Learning Momentum Oscillator brings together the K-Nearest Neighbors (KNN) algorithm and the predictive strength of the Tactical Sector Indicator (TSI) Momentum. This unique oscillator not only uses the insights from TSI Momentum but also taps into the power of machine learning therefore being designed to give traders a more comprehensive view of market momentum.

At its core, the Machine Learning Momentum Oscillator blends TSI Momentum with the capabilities of the KNN algorithm. Introducing KNN logic allows for better handling of noise in the data set. The TSI Momentum is known for understanding how strong trends are and which direction they're headed, and now, with the added layer of machine learning, we're able to offer a deeper perspective on market trends. This is a fairly classical when it comes to visuals and trading.

Green bars show the trader when the asset is in an uptrend. On the flip side, red bars mean things are heading down, signaling a bearish movement driven by selling pressure. These color cues make it easier to catch the sentiment and direction of the market in a glance.

Yellow boxes are also displayed by the oscillator. These boxes highlight potential turning points or peaks. When the market comes close to these points, they can provide a heads-up about the possibility of changes in momentum or even a trend reversal, helping a trader make informed choices quickly. These can be looked at as possible reversal areas simply put.

Settings:

Users can adjust the number of neighbours in the KNN algorithm and choose the periods they prefer for analysis. This way, the tool becomes a part of a trader's strategy, adapting to different market conditions as they see fit. Users can also adjust the smoothing used by the oscillator via the smoothing input.

SimilarityMeasuresLibrary "SimilarityMeasures"

Similarity measures are statistical methods used to quantify the distance between different data sets

or strings. There are various types of similarity measures, including those that compare:

- data points (SSD, Euclidean, Manhattan, Minkowski, Chebyshev, Correlation, Cosine, Camberra, MAE, MSE, Lorentzian, Intersection, Penrose Shape, Meehl),

- strings (Edit(Levenshtein), Lee, Hamming, Jaro),

- probability distributions (Mahalanobis, Fidelity, Bhattacharyya, Hellinger),

- sets (Kumar Hassebrook, Jaccard, Sorensen, Chi Square).

---

These measures are used in various fields such as data analysis, machine learning, and pattern recognition. They

help to compare and analyze similarities and differences between different data sets or strings, which

can be useful for making predictions, classifications, and decisions.

---

References:

en.wikipedia.org

cran.r-project.org

numerics.mathdotnet.com

github.com

github.com

github.com

Encyclopedia of Distances, doi.org

ssd(p, q)

Sum of squared difference for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the squared euclidean distance.

euclidean(p, q)

Euclidean distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of distance that calculates the straight-line (or Euclidean).

manhattan(p, q)

Manhattan distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of absolute differences between both points.

minkowski(p, q, p_value)

Minkowsky Distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

p_value (float) : `float` P value, default=1.0(1: manhatan, 2: euclidean), does not support chebychev.

Returns: Measure of similarity in the normed vector space.

chebyshev(p, q)

Chebyshev distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

correlation(p, q)

Correlation distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Measure of maximum absolute difference.

cosine(p, q)

Cosine distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Cosine distance between vectors `p` and `q`.

---

angiogenesis.dkfz.de

camberra(p, q)

Camberra distance for N dimensions.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Weighted measure of absolute differences between both points.

mae(p, q)

Mean absolute error is a normalized version of the sum of absolute difference (manhattan).

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean absolute error of vectors `p` and `q`.

mse(p, q)

Mean squared error is a normalized version of the sum of squared difference.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Mean squared error of vectors `p` and `q`.

lorentzian(p, q)

Lorentzian distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Lorentzian distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

intersection(p, q)

Intersection distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Intersection distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

penrose(p, q)

Penrose Shape distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Penrose shape distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

meehl(p, q)

Meehl distance between provided vectors.

Parameters:

p (float ) : `array` Vector with first numeric distribution.

q (float ) : `array` Vector with second numeric distribution.

Returns: Meehl distance of vectors `p` and `q`.

---

angiogenesis.dkfz.de

edit(x, y)

Edit (aka Levenshtein) distance for indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Number of deletions, insertions, or substitutions required to transform source string into target string.

---

generated description:

The Edit distance is a measure of similarity used to compare two strings. It is defined as the minimum number of

operations (insertions, deletions, or substitutions) required to transform one string into another. The operations

are performed on the characters of the strings, and the cost of each operation depends on the specific algorithm

used.

The Edit distance is widely used in various applications such as spell checking, text similarity, and machine

translation. It can also be used for other purposes like finding the closest match between two strings or

identifying the common prefixes or suffixes between them.

---

github.com

www.red-gate.com

planetcalc.com

lee(x, y, dsize)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

dsize (int) : `int` Dictionary size.

Returns: Distance between two strings by accounting for dictionary size.

---

www.johndcook.com

hamming(x, y)

Distance between two indexed strings of equal length.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Length of different components on both sequences.

---

en.wikipedia.org

jaro(x, y)

Distance between two indexed strings.

Parameters:

x (int ) : `array` Indexed array.

y (int ) : `array` Indexed array.

Returns: Measure of two strings' similarity: the higher the value, the more similar the strings are.

The score is normalized such that `0` equates to no similarities and `1` is an exact match.

---

rosettacode.org

mahalanobis(p, q, VI)

Mahalanobis distance between two vectors with population inverse covariance matrix.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

VI (matrix) : `matrix` Inverse of the covariance matrix.

Returns: The mahalanobis distance between vectors `p` and `q`.

---

people.revoledu.com

stat.ethz.ch

docs.scipy.org

fidelity(p, q)

Fidelity distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya Coefficient between vectors `p` and `q`.

---

en.wikipedia.org

bhattacharyya(p, q)

Bhattacharyya distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Bhattacharyya distance between vectors `p` and `q`.

---

en.wikipedia.org

hellinger(p, q)

Hellinger distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The hellinger distance between vectors `p` and `q`.

---

en.wikipedia.org

jamesmccaffrey.wordpress.com

kumar_hassebrook(p, q)

Kumar Hassebrook distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Kumar Hassebrook distance between vectors `p` and `q`.

---

github.com

jaccard(p, q)

Jaccard distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Jaccard distance between vectors `p` and `q`.

---

github.com

sorensen(p, q)

Sorensen distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

Returns: The Sorensen distance between vectors `p` and `q`.

---

people.revoledu.com

chi_square(p, q, eps)

Chi Square distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Chi Square distance between vectors `p` and `q`.

---

uw.pressbooks.pub

stats.stackexchange.com

www.itl.nist.gov

kulczynsky(p, q, eps)

Kulczynsky distance between provided vectors.

Parameters:

p (float ) : `array` 1D Vector.

q (float ) : `array` 1D Vector.

eps (float)

Returns: The Kulczynsky distance between vectors `p` and `q`.

---

github.com

Hybrid EMA AlgoLearner⭕️Innovative trading indicator that utilizes a k-NN-inspired algorithmic approach alongside traditional Exponential Moving Averages (EMAs) for more nuanced analysis. While the algorithm doesn't actually employ machine learning techniques, it mimics the logic of the k-Nearest Neighbors (k-NN) methodology. The script takes into account the closest 'k' distances between a short-term and long-term EMA to create a weighted short-term EMA. This combination of rule-based logic and EMA technicals offers traders a more sophisticated tool for market analysis.

⭕️Foundational EMAs: The script kicks off by generating a 50-period short-term EMA and a 200-period long-term EMA. These EMAs serve a dual purpose: they provide the basic trend-following capability familiar to most traders, akin to the classic EMA 50 and EMA 200, and set the stage for more intricate calculations to follow.

⭕️k-NN Integration: The indicator distinguishes itself by introducing k-NN (k-Nearest Neighbors) logic into the mix. This machine learning technique scans prior market data to find the closest 'neighbors' or distances between the two EMAs. The 'k' closest distances are then picked for further analysis, thus imbuing the indicator with an added layer of data-driven context.

⭕️Algorithmic Weighting: After the k closest distances are identified, they are utilized to compute a weighted EMA. Each of the k closest short-term EMA values is weighted by its associated distance. These weighted values are summed up and normalized by the sum of all chosen distances. The result is a weighted short-term EMA that packs more nuanced information than a simple EMA would.

[blackcat] L1 TradingView Array and Series ConversionsLevel 1

Background

It just so happens that I need some functions that can convert between the Series data type and the Array data type.

Function

Series is a unique data type of TradingView. By operating Series data, the algorithm can be simplified, which is very convenient. However, in high-level languages, Array is a basic data type that provides great flexibility and can be used to develop advanced algorithms. This is why TradingView introduces the Array data type. This script simply demonstrates how to convert between these two data types.

s2a function: Convert a TV series into an array.

a2s function: Convert an array into a TV series

Finally, Courtesy of Electrified for his "Average Lib":

Remarks

Feedbacks are appreciated.

Discrete Fourier Transform Overlay [wbburgin]The discrete Fourier transform (DFT) overlay uses a discrete Fourier transform algorithm to identify trend direction. This is a simpler interpretation that only uses the magnitude of the first frequency component obtained from the DFT algorithm, but can be useful for visualization purposes. I haven't seen many Fourier scripts on TradingView that actually have the magnitude plotted on the chart (some have lines, for instance, but that makes it difficult to look into the past or to see previous lines).

About the Discrete Fourier Transform

The DFT is a mathematical transformation that decomposes a time-domain signal into its constituent frequency components. By applying the DFT to OHLC data, we can interpret the periodicities and trends present in the market. I've designed the overlay so that you can choose your source for the Fourier transform, as well as the length.

Settings and Configuration

The "Fourier Period" is the transform length of the DFT algorithm. This input indicates the number of data points considered for the DFT calculation. For example, if this input is set to 20, the DFT will be performed on the most recent 20 data points of the input series. The transform length affects the resolution and accuracy of the frequency analysis. A shorter transform length may provide a broader frequency range but with less detail, while a longer transform length can provide finer frequency resolution but may be computationally more intensive (I recommend using under 100 - anything above that might take too much time to load on the platform).

The "Fourier X Series" is the source you want the Fourier transform to be applied to. I have it set in default to the close.

"Kernel Smoothing" is the bar-start of the rational quadratic kernel used to smooth the frequency component. Think of it just like a normal moving average if you are unfamiliar with the concept, it functions similarly to the "length" value of a moving average.

Aggregate Medians [wbburgin]This indicator recursively finds the average of all high/low medians under your chosen length. This can be very, very helpful for analyzing trends where a moving average or a normal median would produce a bunch of false signals.

Settings:

The "Length" setting is the maximum median that you want the algorithm to add into the sum. The "Start at Period" setting is the the minimum median that you want the algorithm to take into account. Starting at a higher period means that the faster, more sensitive medians of lower lengths are not included, and will smooth out your curve.

I haven't seen many recursive algorithms on TradingView so feel free to use this script as inspiration for any of your ideas. In theory, you can essentially replace the median function with any other function - a moving average, a supertrend, or anything else.

The start must be lower than the length, because this is a sum from the start to the length of all medians in between.

MLExtensionsLibrary "MLExtensions"

normalizeDeriv(src, quadraticMeanLength)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src : The input series (i.e., the first-order derivative for price).

quadraticMeanLength : The length of the quadratic mean (RMS).

Returns: nDeriv The normalized derivative of the input series.

normalize(src, min, max)

Rescales a source value with an unbounded range to a target range.

Parameters:

src : The input series

min : The minimum value of the unbounded range

max : The maximum value of the unbounded range

Returns: The normalized series

rescale(src, oldMin, oldMax, newMin, newMax)

Rescales a source value with a bounded range to anther bounded range

Parameters:

src : The input series

oldMin : The minimum value of the range to rescale from

oldMax : The maximum value of the range to rescale from

newMin : The minimum value of the range to rescale to

newMax : The maximum value of the range to rescale to

Returns: The rescaled series

color_green(prediction)

Assigns varying shades of the color green based on the KNN classification

Parameters:

prediction : Value (int|float) of the prediction

Returns: color

color_red(prediction)

Assigns varying shades of the color red based on the KNN classification

Parameters:

prediction : Value of the prediction

Returns: color

tanh(src)

Returns the the hyperbolic tangent of the input series. The sigmoid-like hyperbolic tangent function is used to compress the input to a value between -1 and 1.

Parameters:

src : The input series (i.e., the normalized derivative).

Returns: tanh The hyperbolic tangent of the input series.

dualPoleFilter(src, lookback)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src : The input series (i.e., the hyperbolic tangent).

lookback : The lookback window for the smoothing.

Returns: filter The smoothed hyperbolic tangent of the input series.

tanhTransform(src, smoothingFrequency, quadraticMeanLength)

Returns the tanh transform of the input series.

Parameters:

src : The input series (i.e., the result of the tanh calculation).

smoothingFrequency

quadraticMeanLength

Returns: signal The smoothed hyperbolic tangent transform of the input series.

n_rsi(src, n1, n2)

Returns the normalized RSI ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the RSI calculation).

n1 : The length of the RSI.

n2 : The smoothing length of the RSI.

Returns: signal The normalized RSI.

n_cci(src, n1, n2)

Returns the normalized CCI ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the CCI calculation).

n1 : The length of the CCI.

n2 : The smoothing length of the CCI.

Returns: signal The normalized CCI.

n_wt(src, n1, n2)

Returns the normalized WaveTrend Classic series ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the WaveTrend Classic calculation).

n1

n2

Returns: signal The normalized WaveTrend Classic series.

n_adx(highSrc, lowSrc, closeSrc, n1)

Returns the normalized ADX ideal for use in ML algorithms.

Parameters:

highSrc : The input series for the high price.

lowSrc : The input series for the low price.

closeSrc : The input series for the close price.

n1 : The length of the ADX.

regime_filter(src, threshold, useRegimeFilter)

Parameters:

src

threshold

useRegimeFilter

filter_adx(src, length, adxThreshold, useAdxFilter)

filter_adx

Parameters:

src : The source series.

length : The length of the ADX.

adxThreshold : The ADX threshold.

useAdxFilter : Whether to use the ADX filter.

Returns: The ADX.

filter_volatility(minLength, maxLength, useVolatilityFilter)

filter_volatility

Parameters:

minLength : The minimum length of the ATR.

maxLength : The maximum length of the ATR.

useVolatilityFilter : Whether to use the volatility filter.

Returns: Boolean indicating whether or not to let the signal pass through the filter.

backtest(high, low, open, startLongTrade, endLongTrade, startShortTrade, endShortTrade, isStopLossHit, maxBarsBackIndex, thisBarIndex)

Performs a basic backtest using the specified parameters and conditions.

Parameters:

high : The input series for the high price.

low : The input series for the low price.

open : The input series for the open price.

startLongTrade : The series of conditions that indicate the start of a long trade.`

endLongTrade : The series of conditions that indicate the end of a long trade.

startShortTrade : The series of conditions that indicate the start of a short trade.

endShortTrade : The series of conditions that indicate the end of a short trade.

isStopLossHit : The stop loss hit indicator.

maxBarsBackIndex : The maximum number of bars to go back in the backtest.

thisBarIndex : The current bar index.

Returns: A tuple containing backtest values

init_table()

init_table()

Returns: tbl The backtest results.

update_table(tbl, tradeStatsHeader, totalTrades, totalWins, totalLosses, winLossRatio, winrate, stopLosses)

update_table(tbl, tradeStats)

Parameters:

tbl : The backtest results table.

tradeStatsHeader : The trade stats header.

totalTrades : The total number of trades.

totalWins : The total number of wins.

totalLosses : The total number of losses.

winLossRatio : The win loss ratio.

winrate : The winrate.

stopLosses : The total number of stop losses.

Returns: Updated backtest results table.

WaveTrend 3D█ OVERVIEW

WaveTrend 3D (WT3D) is a novel implementation of the famous WaveTrend (WT) indicator and has been completely redesigned from the ground up to address some of the inherent shortcomings associated with the traditional WT algorithm.

█ BACKGROUND

The WaveTrend (WT) indicator has become a widely popular tool for traders in recent years. WT was first ported to PineScript in 2014 by the user @LazyBear, and since then, it has ascended to become one of the Top 5 most popular scripts on TradingView.

The WT algorithm appears to have origins in a lesser-known proprietary algorithm called Trading Channel Index (TCI), created by AIQ Systems in 1986 as an integral part of their commercial software suite, TradingExpert Pro. The software’s reference manual states that “TCI identifies changes in price direction” and is “an adaptation of Donald R. Lambert’s Commodity Channel Index (CCI)”, which was introduced to the world six years earlier in 1980. Interestingly, a vestige of this early beginning can still be seen in the source code of LazyBear’s script, where the final EMA calculation is stored in an intermediate variable called “tci” in the code.

█ IMPLEMENTATION DETAILS

WaveTrend 3D is an alternative implementation of WaveTrend that directly addresses some of the known shortcomings of the indicator, including its unbounded extremes, susceptibility to whipsaw, and lack of insight into other timeframes.

In the canonical WT approach, an exponential moving average (EMA) for a given lookback window is used to assess the variability between price and two other EMAs relative to a second lookback window. Since the difference between the average price and its associated EMA is essentially unbounded, an arbitrary scaling factor of 0.015 is typically applied as a crude form of rescaling but still fails to capture 20-30% of values between the range of -100 to 100. Additionally, the trigger signal for the final EMA (i.e., TCI) crossover-based oscillator is a four-bar simple moving average (SMA), which further contributes to the net lag accumulated by the consecutive EMA calculations in the previous steps.

The core idea behind WT3D is to replace the EMA-based crossover system with modern Digital Signal Processing techniques. By assuming that price action adheres approximately to a Gaussian distribution, it is possible to sidestep the scaling nightmare associated with unbounded price differentials of the original WaveTrend method by focusing instead on the alteration of the underlying Probability Distribution Function (PDF) of the input series. Furthermore, using a signal processing filter such as a Butterworth Filter, we can eliminate the need for consecutive exponential moving averages along with the associated lag they bring.

Ideally, it is convenient to have the resulting probability distribution oscillate between the values of -1 and 1, with the zero line serving as a median. With this objective in mind, it is possible to borrow a common technique from the field of Machine Learning that uses a sigmoid-like activation function to transform our data set of interest. One such function is the hyperbolic tangent function (tanh), which is often used as an activation function in the hidden layers of neural networks due to its unique property of ensuring the values stay between -1 and 1. By taking the first-order derivative of our input series and normalizing it using the quadratic mean, the tanh function performs a high-quality redistribution of the input signal into the desired range of -1 to 1. Finally, using a dual-pole filter such as the Butterworth Filter popularized by John Ehlers, excessive market noise can be filtered out, leaving behind a crisp moving average with minimal lag.

Furthermore, WT3D expands upon the original functionality of WT by providing:

First-class support for multi-timeframe (MTF) analysis

Kernel-based regression for trend reversal confirmation

Various options for signal smoothing and transformation

A unique mode for visualizing an input series as a symmetrical, three-dimensional waveform useful for pattern identification and cycle-related analysis

█ SETTINGS

This is a summary of the settings used in the script listed in roughly the order in which they appear. By default, all default colors are from Google's TensorFlow framework and are considered to be colorblind safe.

Source: The input series. Usually, it is the close or average price, but it can be any series.

Use Mirror: Whether to display a mirror image of the source series; for visualizing the series as a 3D waveform similar to a soundwave.

Use EMA: Whether to use an exponential moving average of the input series.

EMA Length: The length of the exponential moving average.

Use COG: Whether to use the center of gravity of the input series.

COG Length: The length of the center of gravity.

Speed to Emphasize: The target speed to emphasize.

Width: The width of the emphasized line.

Display Kernel Moving Average: Whether to display the kernel moving average of the signal. Like PCA, an unsupervised Machine Learning technique whereby neighboring vectors are projected onto the Principal Component.

Display Kernel Signal: Whether to display the kernel estimator for the emphasized line. Like the Kernel MA, it can show underlying shifts in bias within a more significant trend by the colors reflected on the ribbon itself.

Show Oscillator Lines: Whether to show the oscillator lines.

Offset: The offset of the emphasized oscillator plots.

Fast Length: The length scale factor for the fast oscillator.

Fast Smoothing: The smoothing scale factor for the fast oscillator.

Normal Length: The length scale factor for the normal oscillator.

Normal Smoothing: The smoothing scale factor for the normal frequency.

Slow Length: The length scale factor for the slow oscillator.

Slow Smoothing: The smoothing scale factor for the slow frequency.

Divergence Threshold: The number of bars for the divergence to be considered significant.

Trigger Wave Percent Size: How big the current wave should be relative to the previous wave.

Background Area Transparency Factor: Transparency factor for the background area.

Foreground Area Transparency Factor: Transparency factor for the foreground area.

Background Line Transparency Factor: Transparency factor for the background line.

Foreground Line Transparency Factor: Transparency factor for the foreground line.

Custom Transparency: Transparency of the custom colors.

Total Gradient Steps: The maximum amount of steps supported for a gradient calculation is 256.

Fast Bullish Color: The color of the fast bullish line.

Normal Bullish Color: The color of the normal bullish line.

Slow Bullish Color: The color of the slow bullish line.

Fast Bearish Color: The color of the fast bearish line.

Normal Bearish Color: The color of the normal bearish line.

Slow Bearish Color: The color of the slow bearish line.

Bullish Divergence Signals: The color of the bullish divergence signals.

Bearish Divergence Signals: The color of the bearish divergence signals.

█ ACKNOWLEDGEMENTS

@LazyBear - For authoring the original WaveTrend port on TradingView

@PineCoders - For the beautiful color gradient framework used in this indicator

@veryfid - For the inspiration of using mirrored signals for cycle analysis and using multiple lookback windows as proxies for other timeframes

Improved Chaikin Money FlowChaikin Money Flow is a well-known Indicator for gauging buying/selling pressure. Marc Chaikin intended this to be used on the daily timeframe to capture the behavior of price action at or near the daily close when larger-scale actors influence the market. The calculation is straight forward as described within the built-in TradingView "CMF" indicator:

1. Period Money Flow Multiplier = ((Close - Low) - (High - Close)) /(High - Low)

2. Period Money Flow Volume = Period Money Flow Multiplier x Volume for the Period

3. Chaikin Money Flow = 21 Period Sum of Money Flow Volume / 21 Period Sum of Volume

There is, however, a problem with this algorithm: it does not account for daily gaps in price action. This leads to the indicator sometimes moving out-of-sync with price action and/or an under-emphasis of the magnitude change of the indicator relative to the change in price action. This is a significant problem for someone trying to read divergences against an underlying.

Note: I have never seen a published attempt to improve this indicator which is why I decided that there had to be a way to do it.

In order to mitigate this issue, I have taken the basic script provided by TradingView and made a key modification. If the open of a candle is outside the range of the previous candle, then the close of the previous candle is used as the "high" for the current candle (in the case of a gap down) or the "low" for the current candle (in the case of a gap up). However, if the close of the current candle exceeds the previous close, highs and lows for the current candle are calculated as normal. I believe this accounts for gaps in price action without significantly altering the original intent of the indicator.

I have made four other minor tweaks:

1. Default style is color coded area above and below the Zero Line

2. Range scaled to +/-100 instead of +/-1 (displays better on graph)

3. Set timeframe to Daily (as that is the timeframe for which this indicator was intended by Chaikin)

4. Length defaults to 21 (which is what Chaikin uses)

Extreme Trend Reversal Points [HeWhoMustNotBeNamed]Using moving average crossover for identifying the change in trend is very common. However, this method can give lots of false signals during the ranging markets. In this algorithm, we try to find the extreme trend by looking at fully aligned multi-level moving averages and only look at moving average crossover when market is in the extreme trend - either bullish or bearish. These points can mean long term downtrend or can also cause a small pullback before trend continuation. In this discussion, we will also check how to handle different scenarios.

🎲 Components

🎯 Recursive Multi Level Moving Averages

Multi level moving average here refers to applying moving average on top of base moving average on multiple levels. For example,

Level 1 SMA = SMA(source, length)

Level 2 SMA = SMA(Level 1 SMA, length)

Level 3 SMA = SMA(Level 2 SMA, length)

..

..

..

Level n SMA = SMA(Level (n-1) SMA, length)

In this script, user can select how many levels of moving averages need to be calculated. This is achieved through " recursive moving average " algorithm. Requirement for building such algorithm was initially raised by @loxx

While I was able to develop them in minimal code with the help of some of the existing libraries built on arrays and matrix , I also thought why not extend this to find something interesting.

Note that since we are using variable levels - we will not be able to plot all the levels of moving average. (This is because plotting cannot be done in the loop). Hence, we are using lines to display the latest moving average levels in front of the last candle. Lines are color coded in such a way that least numbered levels are greener and higher levels are redder.

🎯 Finding the trend and range

Strength of fully aligned moving average is calculated based on position of each level with respect to other levels.

For example, in a complete uptrend, we can find

source > L(1)MA > L(2)MA > L(3)MA ...... > L(n-1)MA > L(n)MA

Similarly in a complete downtrend, we can find

source < L(1)MA < L(2)MA < L(3)MA ...... < L(n-1)MA < L(n)MA

Hence, the strength of trend here is calculated based on relative positions of each levels. Due to this, value of strength can range from 0 to Level*(Level-1)/2

0 represents the complete downtrend

Level*(Level-1)/2 represents the complete uptrend.

Range and Extreme Range are calculated based on the percentile from median. The brackets are defined as per input parameters - Range Percentile and Extreme Range Percentile by using Percentile History as reference length.

Moving average plot is color coded to display the trend strength.

Green - Extreme Bullish

Lime - Bullish

Silver - range

Orange - Bearish

Red - Extreme Bearish

🎯 Finding the trend reversal

Possible trend reversals are when price crosses the moving average while in complete trend with all the moving averages fully aligned. Triangle marks are placed in such locations which can help observe the probable trend reversal points. But, there are possibilities of trend overriding these levels. An example of such thing, we can see here:

In order to overcome this problem, we can employ few techniques.

1. After the signal, wait for trend reversal (moving average plot color to turn silver) before placing your order.

2. Place stop orders on immediate pivot levels or support resistance points instead of opening market order. This way, we can also place an order in the direction of trend. Whichever side the price breaks out, will be the direction to trade.

3. Look for other confirmations such as extremely bullish and bearish candles before placing the orders.

🎯 An example of using stop orders

Let us take this scenario where there is a signal on possible reversal from complete uptrend.

Create a box joining high and low pivots at reasonable distance. You can also chose to add 1 ATR additional distance from pivots.

Use the top of the box as stop-entry for long and bottom as stop-entry for short. The other ends of the box can become stop-losses for each side.

After few bars, we can see that few more signals are plotted but, the price is still within the box. There are some candles which touched the top of the box. But, the candlestick patterns did not represent bullishness on those instances. If you have placed stop orders, these orders would have already filled in. In that case, just wait for position to hit either stop or target.

For bullish side, targets can be placed at certain risk reward levels. In this case, we just use 1:1 for bullish (trend side) and 1:1.5 for bearish side (reversal side)

In this case, price hit the target without any issue:

Wait for next reversal signal to appear before placing another order :)

American Approximation Bjerksund & Stensland 2002 [Loxx]American Approximation Bjerksund & Stensland 2002 is an American Options pricing model. This indicator also includes numerical greeks. You can compare the output of the American Approximation to the Black-Scholes-Merton value on the output of the options panel.

The Bjerksund & Stensland (2002) Approximation

The Bjerksund and Stensland (2002) approximation divides the time to maturity into two parts, each with a separate flat exercise boundary. It is thus a straightforward generalization of the Bjerksund-Stensland 1993 algorithm. The method is fast and efficient and should be more accurate than the Barone-Adesi and Whaley (1987) and the Bjerksund and Stensland (1993b) approximations. The algorithm requires an accurate cumulative bivariate normal approximation. Several approximations that are described in the literature are not sufficiently accurate, but the Genze algorithm works.

C = alpha2*S^B - alpha2*phi(S, t1, B, I2, I2)

+ phi(S, t1, I2, I2) - phi(S, t1, I, I1, I2)

- X*phi(S, t1, 0, I2, I2) + X*phi(S, t1, 0, I1, I2)

+ alpha1*phi(X, t1, B, I1, I2) - alpha1*psi*St, T, B, I1, I2, I1, t1)

+ psi(S, T, 1, I1, I2, I1, t1) - psi(S, T, 1, X, I2, I1, t1)

- X*psi(S, T, 0, I1, I2, I1, t1) + psi(S, T, 0 ,X, I2, I1, t1)

where

alpha1 = (I1 - X)*I1^-B

alpha2 = (I2 - X)*I2^-B

B = (1/2 - b/v^2) + ((b/v^2 - 1/2)^2 + 2*(r/v^2))^0.5

The function psi(S, T, y, H, I) is given by

psi(S, T, gamma, H, I) = e^lambda * S^gamma * (N(-d) - (I/S)^k * N(-d2))

d = (log(S/H) + (b + (gamma - 1/2) * v^2) * T) / (v * T^0.5)

d2 = (log(I^2/(S*H)) + (b + (gamma - 1/2) * v^2) * T) / (v * T^0.5)

lambda = -r + gamma * b + 1/2 * gamma * (gamma - 1) * v^2

k = 2*b/v^2 + (2 * gamma - 1)

and the trigger price I is defined as

I1 = B0 + (B(+infi) - B0) * (1 - e^h1)

I2 = B0 + (B(+infi) - B0) * (1 - e^h2)

h1 = -(b*t1 + 2*v*t1^0.5) * (X^2 / ((B(+infi) - B0))*B0)

h2 = -(b*T + 2*v*T^0.5) * (X^2 / ((B(+infi) - B0))*B0)

t1 = 1/2 * (5^0.5 - 1) * T

B(+infi) = (B / (B - 1)) * X

B0 = max(X, (r / (r - b)) * X)

Moreover, the function psi(S, T, gamma, H, I2, I1, t1) is given by

psi(S, T, gamma, H, I2, I1, t1, r, b, v) = e^(lambda * T) * S^gamma * (M(-e1, -f1, rho) - (I2/S)^k * M(-e2, -f2, rho)

- (I1/S)^k * M(-e3, -f3, -rho) + (I1/I2)^k * M(-e4, -f4, -rho))

where (see screenshot for e and f values)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

cbnd3(x) = Cumulative Bivariate Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Nadaraya-Watson CombineThis is a combination of the Lux Algo Nadaraya-Watson Estimator and Envelope. Please note the repainting issue.

In addition, I've added a plot of the actual values of the current barstate of

the Nadaraya-Watson windows as they are computed (lines 92-95). It only plots values for the current data at

each time update. It is interesting to compare the trajectory of the end points of the Estimator and

Envelope to the smoothing function at each time update. Due to the kernel smoothing at each update the

history is lost at each update (repaint).

I've added a feature to allow adjustment to the kernel smoothing algorithm as suggested by thomsonraja (line 59).

The settings and usage are repeated from Lux Algo below.

Settings

Window Size: Determines the number of recent price observations to be used to fit the Nadaraya-Watson Estimator.

Bandwidth: Controls the degree of smoothness of the envelopes , with higher values returning smoother results.

Mult: Controls the envelope width.

Src: Input source of the indicator.

Kernel power: See line 59, adjusts the exponential power (powh) as suggested by thomsonraja

Kernel denominator: See line 59, adjusts the denominator (den) as suggested by thomsonraja

Usage

This tool outlines extremes made by the prices within the selected window size.

This is achieved by estimating the underlying trend in the price using kernel smoothing,

calculating the mean absolute deviations from it, and adding/subtracting it

from the estimated underlying trend.

I repeat Lux Algo's caution: 'we do not recommend this tool to be used alone

or solely for real time applications.'

End-Pointed SSA of Normalized Price Corridor [Loxx]End-Pointed SSA of Normalized Price Corridor is an end-pointed SSA of normalized input price to output a smoothed normalized oscillator of price. Corridors are added in attempt to decipher larger trend direction of price. These corridor trend lines are based on highs and lows of price. Due to the SSA algorithm, this indicator takes some time load on the chat, so be patient. You can adjust the lag parameter downward to speed up the indicator load time but this will also degrade the signal. There are many different ways to use this indicator. It is also Renko chart friendly.

An example of emerging trends (these do not repaint)

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA . This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA . The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA , one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA , the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

Included

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

End-pointed SSA of Williams %R [Loxx]End-pointed SSA of Williams %R is an indicator that runes Williams %R SSA calculation through a Singular Spectrum Analysis (SSA) algorithm to derive a smoother final output. The reduction in noise from the traditional Williams %R is significant.

What is Williams %R?

Williams %R , also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA . This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA . The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA , one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA , the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

Included:

Bar coloring

[*Alerts

[*Signals

[*Loxx's Expanded Source Types

Related Williams %R Indicators

Williams %R on Chart w/ Dynamic Zones

Williams %R w/ Bollinger Bands

Intermediate Williams %R w/ Discontinued Signal Lines

Related SSA Indicators

End-pointed SSA of FDASMA

End-pointed SSA of Normalized Price Oscillator

SSA of Price [Loxx]SSA of Price ris an indicator that runs an SSA calculation on price to derive final output. This indicator also serves to introduce the concept of SSA to the Pine Coder community. The data returned from this algorithm is an array of modeled values on past X bars. Unlike the end-pointed SSA posted previously, this version pulls the modeled data from the output array and draws a line backward from the current bar. This indicator recalculates so past observations aren't very useful, but the current observation is since the current bar is index 0 of the output array which means it's the endpointed value.

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA . This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA . The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA , one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA , the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

End-pointed SSA of Normalized Price Oscillator [Loxx]End-pointed SSA of Normalized Price Oscillator is an indicator that converts source price into a normalized oscillator and runs an SSA calculation to derived a smoother final output. This indicator also serves to introduce the concept of SSA to the Pine Coder community. The data returned from this algorithm is an array of modeled values on past X bars. We could use this data but it's not useful, so instead we use the end-pointed value which is the first value of the array at index 0.

What is Singular Spectrum Analysis (SSA)?

Singular spectrum analysis (SSA) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition (SVD) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.

For our purposes here, we are only concerned with the "Caterpillar" SSA. This methodology was developed in the former Soviet Union independently (the ‘iron curtain effect’) of the mainstream SSA. The main difference between the main-stream SSA and the "Caterpillar" SSA is not in the algorithmic details but rather in the assumptions and in the emphasis in the study of SSA properties. To apply the mainstream SSA, one often needs to assume some kind of stationarity of the time series and think in terms of the "signal plus noise" model (where the noise is often assumed to be ‘red’). In the "Caterpillar" SSA, the main methodological stress is on separability (of one component of the series from another one) and neither the assumption of stationarity nor the model in the form "signal plus noise" are required.

"Caterpillar" SSA

The basic "Caterpillar" SSA algorithm for analyzing one-dimensional time series consists of:

Transformation of the one-dimensional time series to the trajectory matrix by means of a delay procedure (this gives the name to the whole technique);

Singular Value Decomposition of the trajectory matrix;

Reconstruction of the original time series based on a number of selected eigenvectors.

This decomposition initializes forecasting procedures for both the original time series and its components. The method can be naturally extended to multidimensional time series and to image processing.

The method is a powerful and useful tool of time series analysis in meteorology, hydrology, geophysics, climatology and, according to our experience, in economics, biology, physics, medicine and other sciences; that is, where short and long, one-dimensional and multidimensional, stationary and non-stationary, almost deterministic and noisy time series are to be analyzed.

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

Itakura-Saito Autoregressive Extrapolation of Price [Loxx]Itakura-Saito Autoregressive Extrapolation of Price is an indicator that uses an autoregressive analysis to predict future prices. This is a linear technique that was originally derived or speech analysis algorithms.

What is Itakura-Saito Autoregressive Analysis?

The technique of linear prediction has been available for speech analysis since the late 1960s (Itakura & Saito, 1973a, 1970; Atal & Hanauer, 1971), although the basic principles were established long before this by Wiener (1947). Linear predictive coding, which is also known as autoregressive analysis, is a time-series algorithm that has applications in many fields other than speech analysis (see, e.g., Chatfield, 1989).

Itakura and Saito developed a formulation for linear prediction analysis using a lattice form for the inverse filter. The Itakura–Saito distance (or Itakura–Saito divergence) is a measure of the difference between an original spectrum and an approximation of that spectrum. Although it is not a perceptual measure it is intended to reflect perceptual (dis)similarity. It was proposed by Fumitada Itakura and Shuzo Saito in the 1960s while they were with NTT. The distance is defined as: The Itakura–Saito distance is a Bregman divergence, but is not a true metric since it is not symmetric and it does not fulfil triangle inequality.

read more: Selected Methods for Improving Synthesis Speech Quality Using Linear Predictive Coding: System Description, Coefficient Smoothing and Streak

Data inputs