Dark Cloud Backtest This is a bearish reversal pattern formed by two candlesticks within a uptrend.

Consists of an up candlestick followed by a down candlestick which opens lower

than the prior candlestick and closes below the midrange of the prior candlestick.

It is the reverse of the Piercing Line.

WARNING:

- For purpose educate only

- This script to change bars colors.

Cerca negli script per "algo"

Bullish Harami Backtest This is a bullish reversal pattern formed by two candlesticks in which a small

real body is contained within the prior session's unusually large real body.

Usually the second real body is the opposite color of the first real body.

The Harami pattern is the reverse of the Engulfing pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

Bearish Harami Backtest This is a bearish reversal pattern formed by two candlesticks in which a short

real body is contained within the prior session's long real body. Usually the

second real body is the opposite color of the first real body. The Harami pattern

is the reverse of the Engulfing pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

AI-Based Strategy on Renko Chart V.1This is a Strategy based on Artificial Intelligence (AI) algorithms which can be used as a decision support system.

How to use:

1- Select the Renko chart.

2- Set "ATR Length" on settings window to "1". Settings can be seen after right click on the chart.

3- Use arbitrary time frame.

HATbot v1 Automation Script and Indicator [Backtest]This is the debut release of HATbot.

HATbot is a terrible name for a new trend following indicator and strategy script.

Backtest window: 2018-01-01 to 2019-01-01.

Initial capital: $1000

Shorting: enabled

TB!G-Scalp Strategy [Backtest]Scalping Crypto Assets Made Easy

TB!G-Scalp is a TradingView based alert and accompanying strategy PineV3 Script.

Backtest vs Realtime

When designing the algorithms for this strategy our focus was primarily on ease of use.This results in a beautiful yet easy to use scalping strategy. As input it takes a chart period and only one extra parameter for fine tuning. The backtest results are an accurate representation of it’s real-time behaviour.

What makes it tick?

Over the last 2 years we collected a lot of market data regarding Bull and Bear behaviours. This previous market behaviour echo’s into the current market trend.

By recognising these echo’s we are able to anticipate an upcoming micro reversal which eventually end up being a scalping strategy.

Interested

Access is provided to a limited amount of people and for the duration that is determined by it’s Alpha Decay Rate.

This ADR is expected to become problematic after 2.3 year of usage on a lot of 150 users.

Megalodon Pro Automated Trader BackTester

Why Megalodon?

We believe that enlightening others is an incredible way to make this world a better place. That's why we created the tools you need to stop worrying about your investments and focus on what really matters in your life.

What is Megalodon?

Megalodon uses Artificial Intelligence that combines 574 back-tested indicators and 2674 back-tested setups, simultaneously.

Megalodon works with any kind of asset , market state and time frame .

What is the win rate?

Megalodon is extremely accurate and offers insane profits as long as the fundamental analysis is done right .

Backtesting results can be found on our social media or down below .

How to use Megalodon Pro Automated Trader?

Simply, orange rectangles are buy signals and purple rectangles are sell signals .

Green clouds show buy signals and red clouds show sell signals.

Yellow line shows the difference between buy and sell counts.

How to set alarms on Megalodon Pro Automated Trader?

Click on Alert, select Megalodon Pro Automated Trader and click on Buy-Signal or Sell-Signal. More details can be found on our social media.

You may also watch our Megalodon Investing Tutorials on Youtube for more information.

How to purchase?

Megalodon is totally FREE .

You may upgrade to Megalodon Pro for the most important features , including automizing your trading on any asset profitably, setting up alarms to get notified , joining to our VIP telegram channel to get daily updates and our VIP telegram group to interact with the community. Simply go to our website on our TradingView page for learning more and joining us for free.

Some of the backtesting results are:

BTC/USD for longer time frame trading in the bear market for the last year.

APPLE for longer time frame trading in the bull market for the last 10 years.

EURO/USD for day trading in the neutral market for the last month.

BTC/USD for day trading in the bull market for the last 15 days.

APPLE for day trading in the neutral market for the last 2 days and 6 hours.

AI-Based Strategy V.1

This is a Strategy based on Artificial Intelligence (AI) algorithms which can be used (alone or along with other strategies) as a decision support system.

How to use:

1- The default values of Input 1, Input 2, R, and T for ETHUSDT are “Close”, “ohlc4”, 180, and 0.1325 respectively. They can be changed to achieve the best performance for ETHUSDT or other symbols.

2- Use one of the time frames 15 to 3m.

3. When the background is green buy, and when the background is red sell.

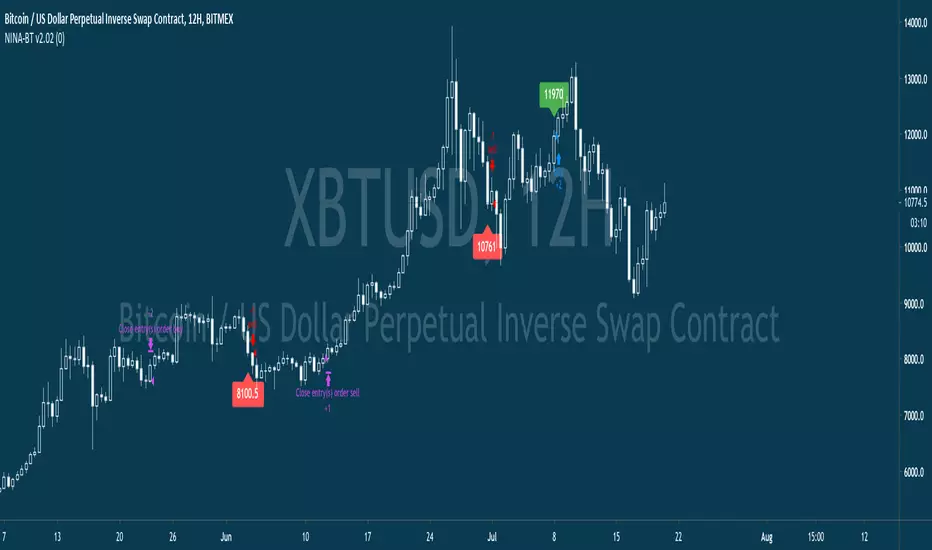

NINA-BTHello Fellow Traders !

KikingAlgo has produced another amazing tool which is now fully operational and ready.

This Algo is called NINA-BT ( Backtesting + Multi Time Frame ) and is based on mathematical formula over 11 timeframes to create trend signals based on the current market conditions.

The Algo can operate on any market, any pair in any timeframe and shows a clear trend direction and strength.

This is a PRO BT version of NINA - drop private message for details.

Regards

KikingAlgo

Bullish Engulfing Backtest This is a bullish reversal pattern formed by two candlesticks. Following a downtrend,

the first candlestick is a down candlestick which is followed by an up candlestick

which has a long real body that engulfs or contains the real body of the prior bar.

The Engulfing pattern is the reverse of the Harami pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

Bearish Engulfing Backtest This is a bearish candlestick reversal pattern formed by two candlesticks.

Following an uptrend, the first candlestick is a up candlestick which is

followed by a down candlestick which has a long real body that engulfs or

contains the real body of the prior bar. The Engulfing pattern is the reverse

of the Harami pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

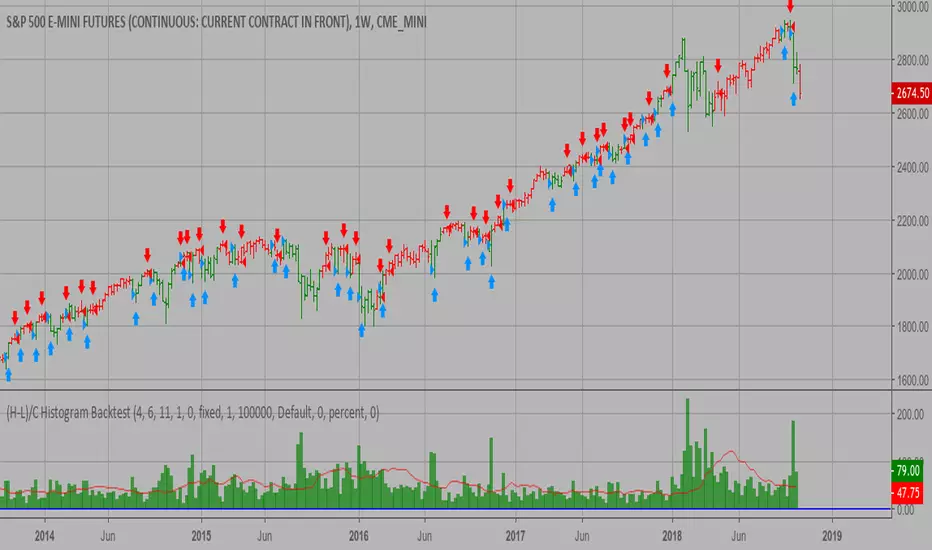

(H-L)/C Histogram Backtest This histogram displays (high-low)/close

Can be applied to any time frame.

WARNING:

- For purpose educate only

- This script to change bars colors.

CMO & WMA Backtest ver 2.0 This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.

Trend Trader Bands Backtest This is plots the indicator developed by Andrew Abraham

in the Trading the Trend article of TASC September 1998

It was modified, result values wass averages.

And draw two bands above and below TT line.

Trend Trader AVR Backtest This is plots the indicator developed by Andrew Abraham

in the Trading the Trend article of TASC September 1998

It was modified, result values wass averages.

Ichimoku Backtest Ichimoku Strategy

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Quantitative R-Difference Trading Strategy/SystemWorks extremely well with many stocks.

This strategy was tested on all components of the Dow since 1987. It averaged 22% a year. Slippage and commission were accounted for. 70% of the trades were profitable. The average maximum drawdown was around 15%.

This strategy has also been tested against random. The results indicate that this strategy's results are not due to random chance, but rather it has an edge in the stock market.

Does not repaint, and is not a curve fitted strategy.

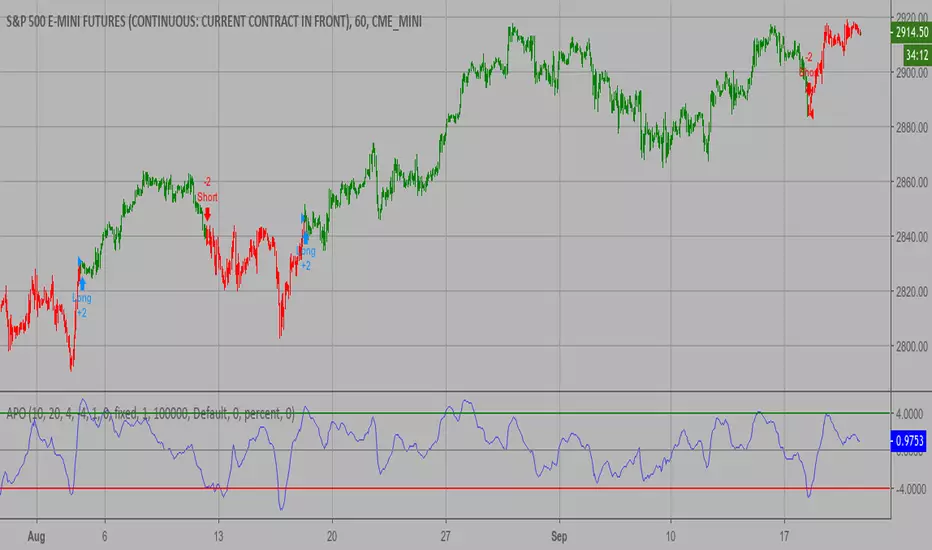

Absolute Price Oscillator (APO) Backtest 2.0 The Absolute Price Oscillator displays the difference between two exponential

moving averages of a security's price and is expressed as an absolute value.

How this indicator works

APO crossing above zero is considered bullish, while crossing below zero is bearish.

A positive indicator value indicates an upward movement, while negative readings

signal a downward trend.

Divergences form when a new high or low in price is not confirmed by the Absolute Price

Oscillator (APO). A bullish divergence forms when price make a lower low, but the APO

forms a higher low. This indicates less downward momentum that could foreshadow a bullish

reversal. A bearish divergence forms when price makes a higher high, but the APO forms a

lower high. This shows less upward momentum that could foreshadow a bearish reversal.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Market Facilitation Index (MFI) Backtest The Market Facilitation Index is an indicator that relates price range to

volume and measures the efficency of price movement. Use the indicator to

determine if the market is trending. If the Market Facilitation Index increased,

then the market is facilitating trade and is more efficient, implying that the

market is trending. If the Market Facilitation Index decreased, then the market

is becoming less efficient, which may indicate a trading range is developing that

may be a trend reversal.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Keltner Channel Backtest The Keltner Channel, a classic indicator

of technical analysis developed by Chester Keltner in 1960.

The indicator is a bit like Bollinger Bands and Envelopes.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

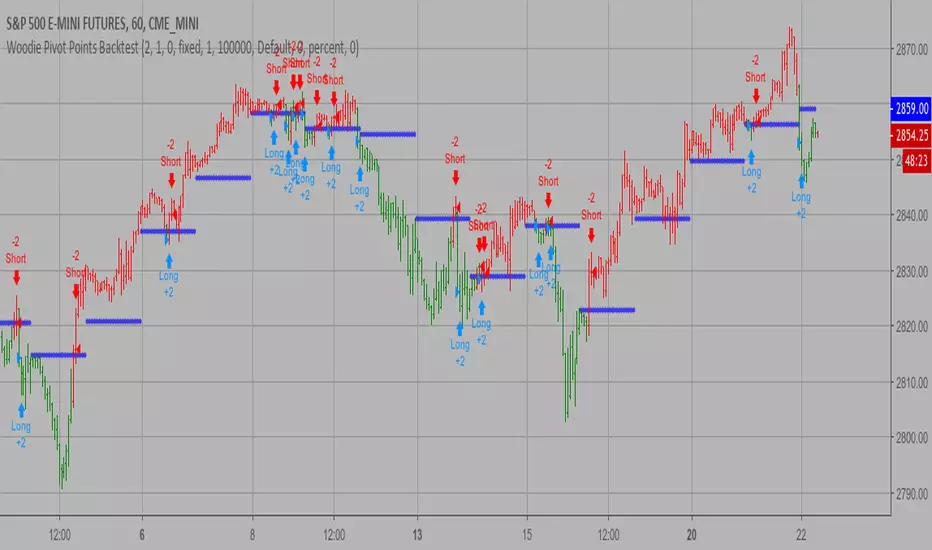

Woodie Pivot Points Backtest Simply input the vales of the high, low and closing price of the previous

period to calculate the Woodie pivot point and the associated resistance

and support levels for the present period.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Volatility Backtest The Volatility function measures the market volatility by plotting a

smoothed average of the True Range. It returns an average of the TrueRange

over a specific number of bars, giving higher weight to the TrueRange of

the most recent bar.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

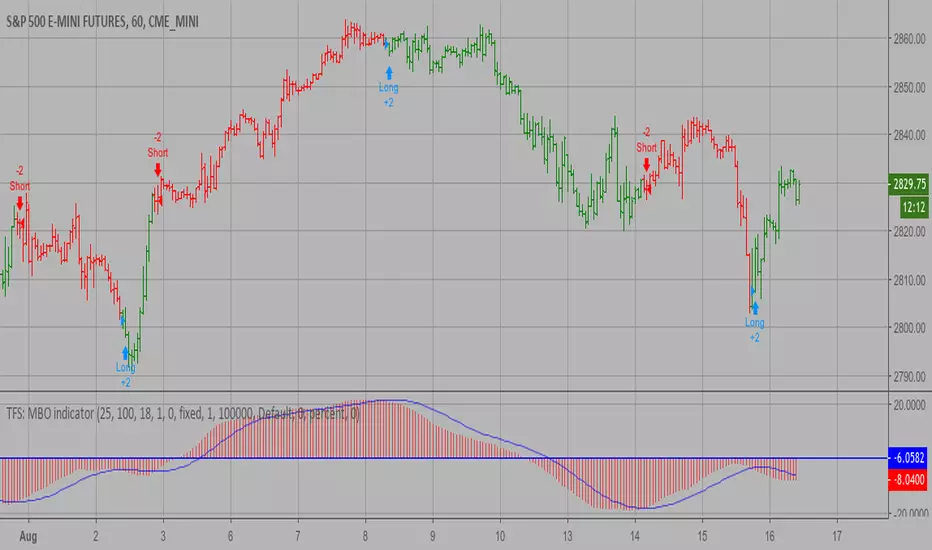

TFS: MBO Backtest MBO indicator is the third component of TFS trading system. This indicator

was developed by Bryan Strain and Mark Whitley.

The idea of MBO is similar to moving average convergence/divergence (MACD)

indicator. It is calculated by subtracting the 200-day moving average from

the 25-day moving average.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.