Strategy Builder Pro [ChartPrime]ChartPrime Strategy Creator Overview

The ChartPrime Strategy Builder offers traders an innovative, structured approach to building and testing strategies. The Strategy Creator allows users to combine, test, and automate complex strategies with many parameters.

Key Features of the ChartPrime Strategy Builder

1. Customizable Buy and Sell Conditions

The Strategy Creator provides flexibility in establishing entry and exit rules, with separate sections for long and short strategies. Traders can combine multiple conditions in each section to fine-tune when positions are opened or closed. For instance, they might choose to only buy when the indicator signals a buy and the Dynamic Reactor (a low lag filter) indicator shows a bullish trend. Users are able to pick, mix and match the following list of features:

Signal Mode: Select the type of assistive signals you are requiring. Provided are both trend following signals with self optimization using backtest results as well as reversal signals, aiming to provide real time tops and bottoms in markets. Both these signal modes can be fine tuned using the tuning input to refine signals to a trader's liking. ChartPrime Trend Signals leverage audio engineering inspired techniques and low-pass filters in order to achieve and attempt to produce lower lag response times and therefore are designed to have a uniqueness when compared to more classical trend following approaches.

The Dynamic Reactor: provides a simple band passing through the chart. This can provide assistance in support and resistance locations as well as identifying the trend direction expressed via green and red colors. Taking a moving average and applying unique adaptivity calculations gives this plot a unique and fast behavior.

Candlestick structures: analyze candlestick formation putting a spin on classical candlestick patterns and provide the most relevant formations on the chart. These are not classical and are filtered by further analyzing market activity. A trader's classic with a spin.

The Prime Trend Assistant: provides a trend following dynamic support and resistance level. This makes it perfect to use in confluence or as a filter for other supporting indicators. This is an adaptive trend following system designed to handle volatility leveraging filter kernels as opposed to low pass filters.

Money Flow: with further filters applied for early response to money flow changes in the market. This can be a great filter in trends.

Oscillator reversals: are built in leveraging an oscillator focusing on market momentum allowing users to enter based on market shifts and trends along with reversals.

Volume-Inspired Signals: determine overbought and oversold conditions, adding another layer of analysis to the oscillator. These appear as orange labels, providing a simple reading into a possible reversal.

The Volume Matrix: is a volume oscillator that shows whether money is flowing into or out of the market. Green suggests an uptrend with buyers in control, while red indicates a majority of sellers. By incorporating smoothed volume analysis, it distinguishes between bullish and bearish volumes, offering an early indication of potential trend reversals.

The True 7: is a middle-ranking system that evaluates the strength of a move and the overall trend, offering a numeric or visual representation of trend strength. It can also indicate when a trend is starting to reverse, providing leading signals for potential market shifts. Rather than using an oscillator, this offers the unique edge of falling into set categories, making understanding it simple. This can be a great confluence point when designing a strategy.

Take profits: These offer real-time suggestions from our algorithm on when it might be a good time to take profit. Using these as part of a strategy allows for great entries at bottoms and tops of trends.

Using features such as the Dynamic reactor have dual purposes. Traders can use this as both a filter and an entry condition. This allows for true interoperability when using the Strategy Builder. The above conditions are duplicated for short entries too allowing for symmetrical trading systems. By disabling all of the entry conditions on either long or short areas of the settings will create a strategy that only takes a single type of position. For example; a trader that just wants to take longs can disable all short options.

2. Layered Entries

Layered entries, a feature to enhance the uniqueness in the tool. It allows traders to average into positions as the market moves, rather than committing all capital at once. This feature is particularly useful for volatile markets where prices may fluctuate substantially. The Strategy Builder lets users adjust the number of layered entries, which can help in managing risk and optimizing entry points as well as the aggressiveness of the safety orders. With each safety order placed the system will automatically and dynamically scale into positions reducing the average entry price and hence dynamically adjust the potential take profits. Due to the potential complexities of exiting during multiple orders, a smart system is employed to automatically take profits on the layered system aiming to take profits at peaks of trends.

Users are able to override this smart TP system at the bottom of the settings instead targeting percentage profits for both short and long positions.

Entries lowering average buy price

The ability to adjust how quickly the system layers into positions can also be adjusted via the layered entries drop down between fast and slow mode where the slow mode will be more cautious when producing new orders.

3. Flexible Take Profit (TP) and Stop Loss (SL) Options

Traders can set their TP and SL levels according to various parameters, including ATR (Average True Range), risk-reward ratio, trailing stops, or specific price changes. If layered entries are active, an automatic TP method is applied by default, though traders can manually specify TP values if they prefer. This setup allows for precise control over trade exits, tailored to the strategy’s risk profile.

Provided options

The ability to use external take profits and stop losses is also provided. By loading an indicator of your choice the plots will be added to the chart. By navigating to the external sources area of the settings, users can select this plot and use it as part of a wider trading system.

Example: Let’s say a user has entries based on the inbuilt trend signals and wishes to exit whenever the RSI crosses above 70, they can add RSI to the chart, select crossing up and enter the value of 70.

4. Integrated Reinvestment for Compounding Gains

The reinvestment option allows traders to reinvest a portion of their gains into future trades, increasing trade size over time and benefiting from compounding. For example, a user might set 30% of each trade's profit to reinvest, with the remaining 70% allocated for risk management or additional safety orders. This approach can enhance long-term growth while balancing risk.

Generally in trading it can be a good approach to take profits so we suggest a healthy balance. This setting is generally best used for slow steady strategies with the long term aim of accumulating as much of the asset as possible.

5. Leverage and Position Sizing

Users can configure leverage and position sizing to simulate varying risk levels and capital allocations. A dashboard on the interface displays margin requirements based on the selected leverage, allowing traders to estimate trade sizes relative to their available capital. Whenever using leverage especially with layered entries it’s important to keep a close eye on the position sizes to avoid potential liquidations.

6. Pre-Configured Strategies for Immediate Testing

For users seeking a starting point, ChartPrime includes a range of preset strategies. These were developed and backtested by ChartPrime’s team. This allows traders to start with a stable base and adapt it to their own preferences. It is vital to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. These pre-built configurations offer a structured way and base to design strategies off of. These are also subject to changing results as new price action arrives and they become outdated. They serve the purpose of simply being example use cases.

7. In-Depth Specific Backtesting Ranges

The Strategy Builder includes backtesting capabilities, providing a clear view of how different setups would have performed over specified time periods. Traders can select date ranges to target specific market conditions, then review results on TradingView to see how their strategies perform across different market trends.

Example Use Case: Developing a Strategy

Consider a trader who is focused on long positions only and prefers a lower-risk strategy (note these tools can be used for all assets; we are using an undisclosed asset as an example). Using the Strategy Builder, they could:

- Disable short conditions.

- Set long entry rules to trigger when both the ChartPrime oscillator and Quantum Reactor indicators show bullish signals.

- Enable layered entries to improve average entry prices by adding to positions during market dips.

- Run a backtest over a two-year period to see historical performance trends, making adjustments as needed.

The backtest will show where entries and exits would have occurred and how layered entries may have impacted profitability.

8. Iterative design

Strategy builders and creating a strategy is often an iterative process. By experimenting and using logic; a trader can arrive at a more sustainable system. Analyzing the shortcomings of your strategy and iteratively designing and filtering them out is the goal. For example; let’s say a strategy has high drawdown, a user would want to tighten stop losses for example to reduce this and find a balance point between optimizing winning trades and reducing the drawdown. When designing a strategy there are generally tradeoffs and optimizing taking into consideration a wide range of factors is key. This also applies to filtering techniques, entries and exits and every variable in the strategy.

Let’s say a strategy was taking too many long positions in a downtrend and after you’ve analyzed the data, you come to the conclusion this needs to be solved. Filtering these using built in trend following tools can be a great approach and refining with logic is a great approach.

The Strategy Builder also takes into consideration those who seek to automate especially via reinvesting and leverage features.

Considerations

The ChartPrime Strategy Builder aims to help traders build clear, rule-based strategies without excessive complexity. As with all backtesting tools, it's crucial to understand that historical performance doesn't guarantee future success, and traders should be mindful of overfitting. This tool offers a structured way to test strategies against various market conditions, helping traders refine their approaches with data-driven insights. Traders should also ensure they enter the correct fees when designing strategies and ensure usage on standard candle types.

Cerca negli script per "algo"

Smart Fib StrategySmart Fibonacci Strategy

This advanced trading strategy combines the power of adaptive SMA entries with Fibonacci-based exit levels to create a comprehensive trend-following system that self-optimizes based on historical market conditions. Credit goes to Julien_Eche who created the "Best SMA Finder" which received an Editors Pick award.

Strategy Overview

The Smart Fibonacci Strategy employs a two-pronged approach to trading:

1. Intelligent Entries: Uses a self-optimizing SMA (Simple Moving Average) to identify optimal entry points. The system automatically tests multiple SMA lengths against historical data to determine which period provides the most robust trading signals.

2. Fibonacci-Based Exits: Implements ATR-adjusted Fibonacci bands to establish precise exit targets, with risk-management options ranging from conservative to aggressive.

This dual methodology creates a balanced system that adapts to changing market conditions while providing clear visual reference points for trade management.

Key Features

- **Self-Optimizing Entries**: Automatically calculates the most profitable SMA length based on historical performance

- **Adjustable Risk Parameters**: Choose between low-risk and high-risk exit targets

- **Directional Flexibility**: Trade long-only, short-only, or both directions

- **Visualization Tools**: Customizable display of entry lines and exit bands

- **Performance Statistics**: Comprehensive stats table showing key metrics

- **Smoothing Option**: Reduces noise in the Fibonacci bands for cleaner signals

Trading Rules

Entry Signals

- **Long Entry**: When price crosses above the blue center line (optimal SMA)

- **Short Entry**: When price crosses below the blue center line (optimal SMA)

### Exit Levels

- **Low Risk Option**: Exit at the first Fibonacci band (1.618 * ATR)

- **High Risk Option**: Exit at the second Fibonacci band (2.618 * ATR)

Strategy Parameters

Display Settings

- Toggle visibility of the stats table and indicator components

Strategy Settings

- Select trading direction (long, short, or both)

- Choose exit method (low risk or high risk)

- Set minimum trades threshold for SMA optimization

SMA Settings

- Option to use auto-optimized or fixed-length SMA

- Customize SMA length when using fixed option

Fibonacci Settings

- Adjust ATR period and SMA basis for Fibonacci bands

- Enable/disable smoothing function

- Customize Fibonacci ratio multipliers

Appearance Settings

- Modify colors, line widths, and transparency

Optimization Methodology

The strategy employs a sophisticated optimization algorithm that:

1. Tests multiple SMA lengths against historical data

2. Evaluates performance based on trade count, profit factor, and win rate

3. Calculates a "robustness score" that balances profitability with statistical significance

4. Selects the SMA length with the highest robustness score

This ensures that the strategy's entry signals are continuously adapting to the most effective parameters for current market conditions.

Risk Management

Position sizing is fixed at $2,000 per trade, allowing for consistent exposure across all trading setups. The Fibonacci-based exit system provides two distinct risk management approaches:

- **Conservative Approach**: Using the first Fibonacci band for exits produces more frequent but smaller wins

- **Aggressive Approach**: Using the second Fibonacci band allows for larger potential gains at the cost of increased volatility

Ideal Usage

This strategy is best suited for:

- Trending markets with clear directional moves

- Timeframes from 4H to Daily for most balanced results

- Instruments with moderate volatility (stocks, forex, commodities)

Traders can further enhance performance by combining this strategy with broader market analysis to confirm the prevailing trend direction.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

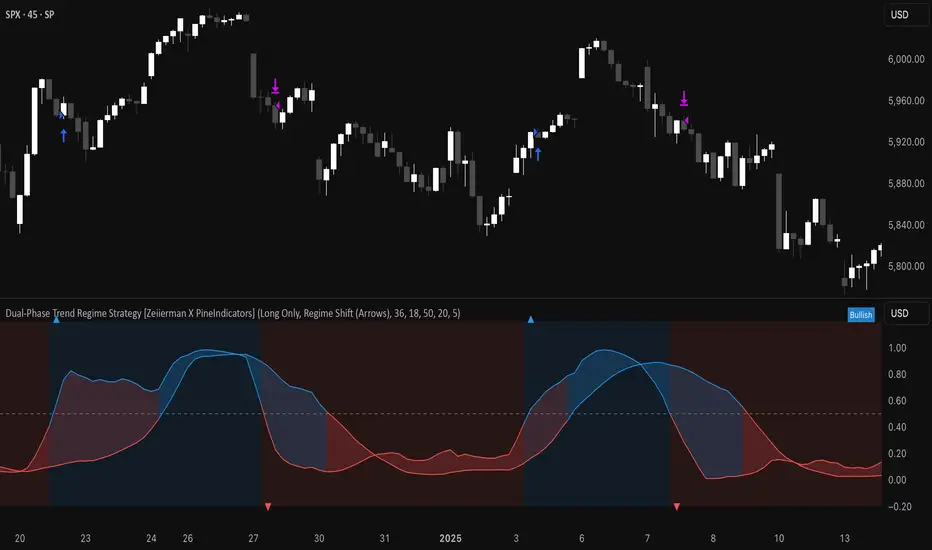

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

External Signals Strategy Tester v5External Signals Strategy Tester v5 – User Guide (English)

1. Purpose

This Pine Script strategy is a universal back‑tester that lets you plug in any external buy/sell series (for example, another indicator, webhook feed, or higher‑time‑frame condition) and evaluate a rich set of money‑management rules around it – with a single click on/off workflow for every module.

2. Core Workflow

Feed signals

Buy Signal / Sell Signal inputs accept any series (price, boolean, output of request.security(), etc.).

A crossover above 0 is treated as “signal fired”.

Date filter

Start Date / End Date restricts the test window so you can exclude unwanted history.

Trade engine

Optional Long / Short enable toggles.

Choose whether opposite signals simply close the trade or reverse it (flip direction in one transaction).

Risk modules – all opt‑in via check‑boxes

Classic % block – fixed % Take‑Profit / Stop‑Loss / Break‑Even.

Fibonacci Bollinger Bands (FBB) module

Draws dynamic VWMA/HMA/SMA/EMA/DEMA/TEMA mid‑line with ATR‑scaled Fibonacci envelopes.

Every line can be used for stops, trailing, or multi‑target exits.

Separate LONG and SHORT sub‑modules

Each has its own SL plus three Take‑Profits (TP1‑TP3).

Per TP you set line, position‑percentage to close, and an optional trailing flag.

Executed TP/SLs deactivate themselves so they cannot refire.

Trailing behaviour

If Trail is checked, the selected line is re‑evaluated once per bar; the order is amended via strategy.exit().

3. Inputs Overview

Group Parameter Notes

Trade Settings Enable Long / Enable Short Master switches

Close on Opposite / Reverse Position How to react to a counter‑signal

Risk % Use TP / SL / BE + their % Traditional fixed‑distance management

Fibo Bands FIBO LEVELS ENABLE + visual style/length Turn indicator overlay on/off

FBB LONG SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a long is open

FBB SHORT SL / TP1‑TP3 Enable, Line, %, Trail Rules applied only while a short is open

Line choices: Basis, 0.236, 0.382, 0.5, 0.618, 0.764, 1.0 – long rules use lower bands, short rules use upper bands automatically.

4. Algorithm Details

Position open

On the very first bar after entry, the script checks the direction and activates the corresponding LONG or SHORT module, deactivating the other.

Order management loop (every bar)

FBB Stop‑Loss: placed/updated at chosen band; if trailing, follows the new value.

TP1‑TP3: each active target updates its limit price to the selected band (or holds static if trailing is off).

The classic % block runs in parallel; its exits have priority because they call strategy.close_all().

Exit handling

When any strategy.exit() fires, the script reads exit_id and flips the *_Active flag so that order will not be recreated.

A Stop‑Loss (SL) also disables all remaining TPs for that leg.

5. Typical Use Cases

Scenario Suggested Setup

Scalping longs into VWAP‐reversion Enable LONG TP1 @ 0.382 (30 %), TP2 @ 0.618 (40 %), SL @ 0.236 + trailing

Fade shorts during news spikes Enable SHORT SL @ 1.0 (no trail) and SHORT TP1,2,3 on consecutive lowers with small size‑outs

Classic trend‑follow Use only classic % TP/SL block and disable FBB modules

6. Hints & Tips

Signal quality matters – this script manages exits, it does not generate entries.

Keep TV time zone in mind when picking start/end dates.

For portfolio‑style testing allocate smaller default_qty_value than 100 % or use strategy.percent_of_equity sizing.

You can combine FBB exits with fixed‑% ones for layered management.

7. Limitations / Safety

No pyramiding; the script holds max one position at a time.

All calculations are bar‑close; intra‑bar touches may differ from real‑time execution.

The indicator overlay is optional, so you can run visual‑clean tests by unchecking FIBO LEVELS ENABLE.

Titan X 📈 Titan X – Optimized Trend Strategy with Gradient ZLEMA, RMI, CCI, ROC, and Volume Confirmation

Titan X is a precision-engineered trend-following strategy designed for crypto markets and high-volatility assets. It is not just a combination of indicators, but a carefully constructed, non-repainting system where each component plays a specific role in confirming high-probability trade setups. The strategy detects strong directional moves, confirms them with momentum and volume, and manages trade exits without relying on traditional stop losses.

🔍 How the Indicators Work Together

✅ 1. ZLEMA Baseline + Gradient Filter

A Zero Lag Exponential Moving Average (ZLEMA) is used to track directional trend with minimal lag.

A gradient (slope) is calculated from the ZLEMA to measure trend acceleration. This confirms whether a trend is gaining strength or losing momentum.

Entries are only taken when the ZLEMA gradient exceeds a user-defined threshold, ensuring trades are only taken in strong, developing trends.

✅ 2. RMI – Relative Momentum Index (with Memory)

RMI captures sustained momentum direction over time.

It helps validate that price isn't just spiking, but truly trending.

Titan X uses RMI as a trend memory filter, requiring consistent momentum alignment before entry.

✅ 3. Momentum Timing – ROC + CCI

The Rate of Change (ROC) determines the strength and direction of recent momentum.

The Commodity Channel Index (CCI) checks price deviation from a moving average baseline, identifying whether momentum is aligned with market structure.

This combo prevents trades in weak, flat, or conflicting conditions.

✅ 4. Volume Spike Confirmation

Titan X uses a relative volume filter, requiring the current bar’s volume to exceed a moving average threshold.

This ensures trades are only triggered when there is clear breakout interest from market participants, helping avoid fakeouts and low-volume moves.

🎯 Trade Entry & Exit Rules

✅ Entry Conditions:

All five filters must align:

Trend direction (ZLEMA slope)

Momentum (ROC & CCI)

Trend memory (RMI)

Volume (Spike filter)

Trades are entered on the next bar after all confirmations, ensuring 100% non-repainting behavior.

✅ Take Profit System (Multi-Level TP):

TP1: Closes 50% of the position at a user-defined % gain (default: 2%)

TP2: Closes the remaining 50% of the position at a higher % gain (default: 4%)

Each TP is executed via limit order to ensure realistic and backtestable fills.

❌ No Stop Loss Used

Instead of using fixed stop losses, Titan X closes positions early when trend conditions weaken.

This dynamic exit logic is based on a reversal in ZLEMA gradient, which serves as a weak trend detection system.

⏱️ Cooldown Logic

A 1-bar cooldown is enforced between trades to avoid same-bar exit/entry violations on TradingView.

This improves execution accuracy and avoids overtrading on choppy price action.

📊 Real-Time Strategy Dashboard

Titan X includes a live dashboard that provides full transparency:

Current Position (Long / Short / Flat)

Entry Price

TP1 Hit? / TP2 Hit?

Bars Since Entry

Win Rate (%)

Profit Factor

Ideal for both manual monitoring and automated bot strategies.

🔔 Bot-Ready Multi-Exchange Alerts

Alerts can be configured for:

ENTER-LONG, ENTER-SHORT

EXIT-LONG, EXIT-SHORT

TP1 / TP2 targets

Messages are fully customizable and designed for platforms like:

WonderTrading

3Commas

TradingConnector

⚙️ Designed For:

Timeframes: 1H and 4H (optimized for crypto)

Markets: Altcoins, BTC/ETH, high-volatility pairs

Traders: Trend-followers, momentum scalpers, algo bot users

Goal: High accuracy entries, structured exits, zero repainting, and flexible trade management

⚠️ TradingView Disclosure

This strategy is provided for educational purposes only. It does not constitute investment advice, nor does it guarantee any returns. Trading carries risk; test thoroughly before using in live environments.

Dskyz (DAFE) MAtrix with ATR-Powered Precision Dskyz (DAFE) MAtrix with ATR-Powered Precision

This cutting‐edge futures trading strategy built to thrive in rapidly changing market conditions. Developed for high-frequency futures trading on instruments such as the CME Mini MNQ, this strategy leverages a matrix of sophisticated moving averages combined with ATR-based filters to pinpoint high-probability entries and exits. Its unique combination of adaptable technical indicators and multi-timeframe trend filtering sets it apart from standard strategies, providing enhanced precision and dynamic responsiveness.

imgur.com

Core Functional Components

1. Advanced Moving Averages

A distinguishing feature of the DAFE strategy is its robust, multi-choice moving averages (MAs). Clients can choose from a wide array of MAs—each with specific strengths—in order to fine-tune their trading signals. The code includes user-defined functions for the following MAs:

imgur.com

Hull Moving Average (HMA):

The hma(src, len) function calculates the HMA by using weighted moving averages (WMAs) to reduce lag considerably while smoothing price data. This function computes an intermediate WMA of half the specified length, then a full-length WMA, and finally applies a further WMA over the square root of the length. This design allows for rapid adaptation to price changes without the typical delays of traditional moving averages.

Triple Exponential Moving Average (TEMA):

Implemented via tema(src, len), TEMA uses three consecutive exponential moving averages (EMAs) to effectively cancel out lag and capture price momentum. The final formula—3 * (ema1 - ema2) + ema3—produces a highly responsive indicator that filters out short-term noise.

Double Exponential Moving Average (DEMA):

Through the dema(src, len) function, DEMA calculates an EMA and then a second EMA on top of it. Its simplified formula of 2 * ema1 - ema2 provides a smoother curve than a single EMA while maintaining enhanced responsiveness.

Volume Weighted Moving Average (VWMA):

With vwma(src, len), this MA accounts for trading volume by weighting the price, thereby offering a more contextual picture of market activity. This is crucial when volume spikes indicate significant moves.

Zero Lag EMA (ZLEMA):

The zlema(src, len) function applies a correction to reduce the inherent lag found in EMAs. By subtracting a calculated lag (based on half the moving average window), ZLEMA is exceptionally attuned to recent price movements.

Arnaud Legoux Moving Average (ALMA):

The alma(src, len, offset, sigma) function introduces ALMA—a type of moving average designed to be less affected by outliers. With parameters for offset and sigma, it allows customization of the degree to which the MA reacts to market noise.

Kaufman Adaptive Moving Average (KAMA):

The custom kama(src, len) function is noteworthy for its adaptive nature. It computes an efficiency ratio by comparing price change against volatility, then dynamically adjusts its smoothing constant. This results in an MA that quickly responds during trending periods while remaining smoothed during consolidation.

Each of these functions—integrated into the strategy—is selectable by the trader (via the fastMAType and slowMAType inputs). This flexibility permits the tailored application of the MA most suited to current market dynamics and individual risk management preferences.

2. ATR-Based Filters and Risk Controls

ATR Calculation and Volatility Filter:

The strategy computes the Average True Range (ATR) over a user-defined period (atrPeriod). ATR is then used to derive both:

Volatility Assessment: Expressed as a ratio of ATR to closing price, ensuring that trades are taken only when volatility remains within a safe, predefined threshold (volatilityThreshold).

ATR-Based Entry Filters: Implemented as atrFilterLong and atrFilterShort, these conditions ensure that for long entries the price is sufficiently above the slow MA and vice versa for shorts. This acts as an additional confirmation filter.

Dynamic Exit Management:

The exit logic employs a dual approach:

Fixed Stop and Profit Target: Stops and targets are set at multiples of ATR (fixedStopMultiplier and profitTargetATRMult), helping manage risk in volatile markets.

Trailing Stop Adjustments: A trailing stop is calculated using the ATR multiplied by a user-defined offset (trailOffset), which captures additional profits as the trade moves favorably while protecting against reversals.

3. Multi-Timeframe Trend Filtering

The strategy enhances its signal reliability by leveraging a secondary, higher timeframe analysis:

15-Minute Trend Analysis:

By retrieving 15-minute moving averages (fastMA15m and slowMA15m) via request.security, the strategy determines the broader market trend. This secondary filter (enabled or disabled through useTrendFilter) ensures that entries are aligned with the prevailing market direction, thereby reducing the incidence of false signals.

4. Signal and Execution Logic

Combined MA Alignment:

The entry conditions are based primarily on the alignment of the fast and slow MAs. A long condition is triggered when the current price is above both MAs and the fast MA is above the slow MA—complemented by the ATR filter and volume conditions. The reverse applies for a short condition.

Volume and Time Window Validation:

Trades are permitted only if the current volume exceeds a minimum (minVolume) and the current hour falls within the predefined trading window (tradingStartHour to tradingEndHour). An additional volume spike check (comparing current volume to a moving average of past volumes) further filters for optimal market conditions.

Comprehensive Order Execution:

The strategy utilizes flexible order execution functions that allow pyramiding (up to 10 positions), ensuring that it can scale into positions as favorable conditions persist. The use of both market entries and automated exits (with profit targets, stop-losses, and trailing stops) ensures that risk is managed at every step.

5. Integrated Dashboard and Metrics

For transparency and real-time analysis, the strategy includes:

On-Chart Visualizations:

Both fast and slow MAs are plotted on the chart, making it easy to see the market’s technical foundation.

Dynamic Metrics Dashboard:

A built-in table displays crucial performance statistics—including current profit/loss, equity, ATR (both raw and as a percentage), and the percentage gap between the moving averages. These metrics offer immediate insight into the health and performance of the strategy.

Input Parameters: Detailed Breakdown

Every input is meticulously designed to offer granular control:

Fast & Slow Lengths:

Determine the window size for the fast and slow moving averages. Smaller values yield more sensitivity, while larger values provide a smoother, delayed response.

Fast/Slow MA Types:

Choose the type of moving average for fast and slow signals. The versatility—from basic SMA and EMA to more complex ones like HMA, TEMA, ZLEMA, ALMA, and KAMA—allows customization to fit different market scenarios.

ATR Parameters:

atrPeriod and atrMultiplier shape the volatility assessment, directly affecting entry filters and risk management through stop-loss and profit target levels.

Trend and Volume Filters:

Inputs such as useTrendFilter, minVolume, and the volume spike condition help confirm that a trade occurs in active, trending markets rather than during periods of low liquidity or market noise.

Trading Hours:

Restricting trade execution to specific hours (tradingStartHour and tradingEndHour) helps avoid illiquid or choppy markets outside of prime trading sessions.

Exit Strategies:

Parameters like trailOffset, profitTargetATRMult, and fixedStopMultiplier provide multiple layers of risk management and profit protection by tailoring how exits are generated relative to current market conditions.

Pyramiding and Fixed Trade Quantity:

The strategy supports multiple entries within a trend (up to 10 positions) and sets a predefined trade quantity (fixedQuantity) to maintain consistent exposure and risk per trade.

Dashboard Controls:

The resetDashboard input allows for on-the-fly resetting of performance metrics, keeping the strategy’s performance dashboard accurate and up-to-date.

Why This Strategy is Truly Exceptional

Multi-Faceted Adaptability:

The ability to switch seamlessly between various moving average types—each suited to particular market conditions—enables the strategy to adapt dynamically. This is a testament to the high level of coding sophistication and market insight infused within the system.

Robust Risk Management:

The integration of ATR-based stops, profit targets, and trailing stops ensures that every trade is executed with well-defined risk parameters. The system is designed to mitigate unexpected market swings while optimizing profit capture.

Comprehensive Market Filtering:

By combining moving average crossovers with volume analysis, volatility thresholds, and multi-timeframe trend filters, the strategy only enters trades under the most favorable conditions. This multi-layered filtering reduces noise and enhances signal quality.

-Final Thoughts-

The Dskyz Adaptive Futures Elite (DAFE) MAtrix with ATR-Powered Precision strategy is not just another trading algorithm—it is a multi-dimensional, fully customizable system built on advanced technical principles and sophisticated risk management techniques. Every function and input parameter has been carefully engineered to provide traders with a system that is both powerful and transparent.

For clients seeking a state-of-the-art trading solution that adapts dynamically to market conditions while maintaining strict discipline in risk management, this strategy truly stands in a class of its own.

****Please show support if you enjoyed this strategy. I'll have more coming out in the near future!!

-Dskyz

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

Gradient Sniper Elite🧠 Gradient Sniper Elite — Precision Trend Detection and Tactical Trade Execution for Crypto

Gradient Sniper Elite is a high-performance crypto trend strategy engineered for accuracy, adaptability, and smart execution on the 1-hour timeframe. This script is not just a mashup — it's a purpose-built system that combines trend, momentum, and volume filters in a structured and non-repainting framework designed for optimal entry and exit timing.

🔍 What Makes It Original?

This strategy combines several proven concepts into a unified, precision-calibrated trade engine:

✅ ZLEMA Gradient Filter: A slope-based trend filter that captures the direction and strength of momentum shifts without repainting.

✅ TEMA Confirmation: Triple EMA logic confirms trend acceleration or exhaustion by analyzing layered EMA cross-smoothing.

✅ RMI-Based Trend Direction: Replaces traditional RSI with a Relative Momentum Index (RMI), which smooths price momentum and avoids lag.

✅ ROC & Smoothed CCI: Dual momentum filters ensure that trades align with both velocity and structure of price moves.

✅ Volume Spike Filter: Filters out false breakouts and manipulation by confirming entries only during statistically significant volume surges.

✅ TP1/TP2 Split Take Profit Logic: 50% partial exit at TP1 and full exit at TP2. Ensures flexible profit-taking while maximizing trend continuation gains.

✅ Trend Weakness Exit: Trades are exited cleanly when the trend begins to weaken (as confirmed by RMI flip), preventing overstay and drawdown.

✅ 1-Bar Reversal Delay: The system enforces a 1-bar delay between a trade closure and any potential reversal entry, ensuring clean trend reversals and realistic live trading behavior.

✅ No Stop Loss: This strategy does not use a stop loss. Instead, it exits trades based on trend weakness or TP2 being hit. This avoids premature exits in volatile crypto environments, while maintaining controlled and dynamic trade management logic.

⚙️ How It Works

This strategy uses multi-layered confirmation:

Trend Structure

ZLEMA Gradient: Captures the slope of price action.

White Line + Fast/Slow Tether Lines: Define macro trend structure and act as dynamic S/R filters.

Momentum Alignment

Rate of Change (ROC): Measures directional velocity.

Smoothed CCI: Refines entry timing within the trend.

TEMA: Adds second-layer trend confirmation.

Volume Confirmation

Entry signals are validated by detecting relative volume spikes compared to a moving average baseline, avoiding entries on low-volume or fake breakouts.

Trade Management

Dynamic take-profits (TP1/TP2).

Immediate exit on trend weakening.

No same-bar entry/exit — reversal entries are delayed until after full exit confirmation.

No stop loss — trade management is handled via trend logic and take profit levels.

📊 Dashboard Overview

Gradient Sniper Elite includes a built-in dashboard in the top-right corner of the chart. It dynamically updates on each bar and shows:

📍 Position: Displays "Long", "Short", or "Flat" depending on the active trade

💰 Entry Price: The exact price where the trade was entered

📈 Unrealized %: Current profit/loss as a percentage

💵 Unrealized $: Estimated PnL in dollars, scaled to your backtest capital

📊 Trades / Win Rate: Live counter for total trades, win/loss count, and win rate

🎯 TP1 Hit / TP2 Hit: Shows ✅ or ❌ depending on whether each target level was reached during the current trade

This dashboard helps you monitor trade status, track live performance, and validate signal behavior in real time — all without repainting or relying on external tools.

📈 How to Use

Timeframe: Optimized for the 1-hour timeframe, but adaptable.

Asset Class: Primarily built for crypto markets, especially fast-moving alts like AVAX, LINK, QNT, etc.

Trade Mode: Supports long and short trades with clean reversal logic.

Dashboard: Live stats including position status, TP1/TP2 hit, win rate, and real-time PnL tracking.

Backtest Ready: Built with full compliance to TradingView backtest engine — results are realistic and match live-bar behavior.

⚠️ No Repainting — No Guesswork

Every element in this script is designed to work with confirmed bar data only. There is zero forward-looking logic. This makes Gradient Sniper Elite fully compatible with both backtesting and live algo execution.

🧩 Why This Isn’t Just a Mashup

Each indicator in this strategy has a specific role:

ZLEMA: Core trend slope engine.

TEMA: Trend reinforcement.

RMI: Directional decision layer.

CCI & ROC: Entry timing refinement.

Volume Filter: Risk filtering.

They’re not merged randomly, but combined in sequence to eliminate noise and optimize entries.

📌 Disclaimer

This script is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. Always do your own research and use appropriate risk management when trading. Past performance does not guarantee future results.

Buy on 5% dip strategy with time adjustment

This script is a strategy called "Buy on 5% Dip Strategy with Time Adjustment 📉💡," which detects a 5% drop in price and triggers a buy signal 🔔. It also automatically closes the position once the set profit target is reached 💰, and it has additional logic to close the position if the loss exceeds 14% after holding for 230 days ⏳.

Strategy Explanation

Buy Condition: A buy signal is triggered when the price drops 5% from the highest price reached 🔻.

Take Profit: The position is closed when the price hits a 1.22x target from the average entry price 📈.

Forced Sell Condition: If the position is held for more than 230 days and the loss exceeds 14%, the position is automatically closed 🚫.

Leverage & Capital Allocation: Leverage is adjustable ⚖️, and you can set the percentage of capital allocated to each trade 💸.

Time Limits: The strategy allows you to set a start and end time ⏰ for trading, making the strategy active only within that specific period.

Code Credits and References

Credits: This script utilizes ideas and code from @QuantNomad and jangdokang for the profit table and algorithm concepts 🔧.

Sources:

Monthly Performance Table Script by QuantNomad:

ZenAndTheArtOfTrading's Script:

Strategy Performance

This strategy provides risk management through take profit and forced sell conditions and includes a performance table 📊 to track monthly and yearly results. You can compare backtest results with real-time performance to evaluate the strategy's effectiveness.

The performance numbers shown in the backtest reflect what would have happened if you had used this strategy since the launch date of the SOXL (the Direxion Daily Semiconductor Bull 3x Shares ETF) 📅. These results are not hypothetical but based on actual performance from the day of the ETF’s launch 📈.

Caution ⚠️

No Guarantee of Future Results: The results are based on historical performance from the launch of the SOXL ETF, but past performance does not guarantee future results. It’s important to approach with caution when applying it to live trading 🔍.

Risk Management: Leverage and capital allocation settings are crucial for managing risk ⚠️. Make sure to adjust these according to your risk tolerance ⚖️.

Dynamic Breakout Master by tradingbauhaus 🌟 Code Description:

This Pine Script implements a trading strategy called "Dynamic Breakout Master" 💥. The core idea of the strategy is to identify breakouts (price movements) at key support 💙 and resistance 🔴 levels, through a dynamic channel that adapts to the market’s conditions. Here's how it works:

🔧 Customizable Input Parameters:

🧭 Pivot Period: This defines the number of bars (candles) to the left and right used to detect pivots (highs and lows) that mark the support and resistance zones.

📊 Data Source: You can choose whether to use highs and lows or closes and opens of the candles to identify the pivots.

📏 Max Channel Width: Specifies the maximum width allowed for the support/resistance channel, expressed as a percentage over the last 300 bars.

💪 Minimum Pivot Strength: This defines the minimum number of pivots needed for a support or resistance level to be considered valid.

🏔 Max Support/Resistance Zones: Limits the number of key zones displayed on the chart.

📅 Lookback Period: Adjusts how many bars back the system should check to find and validate support and resistance levels.

🎨 Custom Colors: You can choose colors for the support, resistance, and in-channel zones.

📉 Moving Averages (MA): The strategy allows adding up to two moving averages (SMA or EMA) to assist in making trading decisions.

📊 Calculating Support/Resistance Levels:

The system uses an algorithm to identify pivots from prices and calculates dynamic support and resistance zones 🔒🔓.

The closer the pivots are and the stronger their influence, the more relevant the zone becomes for the strategy.

The dynamic channel is drawn on the chart, with a maximum width limit for these zones defined by the input parameter.

📈 Trading Logic:

🚀 Identifying Breakouts:

The strategy looks for when the price breaks (breakouts) a resistance or support level.

If the price breaks upward through the resistance level, a buy order 📈 is triggered.

If the price breaks downward through the support level, a sell order 📉 is triggered.

🔔 Alerts:

Resistance Break (ResBreak) and Support Break (SupBreak) alerts are configured to notify users when a significant breakout occurs.

💰 Commissions:

The strategy includes a commission (0.1%) to simulate transaction costs for each trade.

📊 Chart Visualization:

The support and resistance zones are displayed as colored rectangles:

🔴 Resistance (red) and

🔵 Support (blue).

Pivots of support and resistance can be labeled as P (for resistance) and V (for support).

Breakouts of support or resistance levels are marked with triangles that appear on the chart 🔺🔻.

📈 Trading Strategy:

If the price breaks upward through the resistance level, a long position (buy) 📈 is opened.

If the price breaks downward through the support level, a short position (sell) 📉 is opened.

🏆 Conclusion:

This script is a dynamic breakout strategy 💥 that allows traders to capture significant price movements when support or resistance channels break. The customizable parameters let users fine-tune the strategy according to their preferences, while the visual alerts on the chart make it easier to follow trading opportunities. The inclusion of moving averages and key price zones adds an extra layer of analysis to improve decision-making 💡.

Supertrend pro+ (Adaptive ATR) Supertrend Pro+ (Adaptive ATR) - Param Approach

By SKP

Overview

This advanced Supertrend Pro+ strategy improves on the classic Supertrend indicator by integrating an Adaptive ATR, ensuring dynamic volatility adjustments for more accurate trend detection. This strategy filters out false signals using ADX trend strength validation and volume confirmation, making it a powerful tool for trend-following traders.

Key Features

✔ Adaptive ATR Calculation - Dynamically adjusts to market volatility for more reliable Supertrend signals.

✔ ADX Trend Filter - Ensures trades occur only in strong trending markets, avoiding false breakouts.

✔ Volume Confirmation - Prevents trading in low-liquidity conditions by verifying volume strength.

✔ Multi-Timeframe Analysis - Displays Supertrend trends from different timeframes for enhanced trade confidence.

✔ Trailing Stop & Take Profit Options - Allows flexible risk management with stop-loss and profit-targeting mechanisms.

✔ Custom Alerts for Trade Signals - Alerts trigger on confirmed Supertrend buy/sell signals and potential trend shifts.

✔ Max Drawdown Protection - Automatically closes trades if equity drops beyond a set percentage, preventing excessive losses.

How It Works

Adaptive ATR Calculation

Instead of using a fixed ATR, this strategy calculates an adaptive ATR based on a longer-term ATR baseline.

If volatility increases, the ATR expands dynamically, ensuring stop-losses and Supertrend calculations adjust accordingly.

Supertrend Confirmation

Uses an enhanced Supertrend algorithm with adaptive ATR to determine trend direction.

If price crosses above the trendline, it signals a bullish reversal (Buy Signal).

If price crosses below the trendline, it signals a bearish reversal (Sell Signal).

ADX Trend Strength Filter

Trades are only taken when ADX is above the threshold, ensuring entry in strong trending markets.

Volume Confirmation

Uses a relative volume filter to ensure sufficient liquidity before entering trades.

Helps avoid false breakouts in low-volume conditions.

Risk Management

Trailing Stop Loss - Automatically moves the stop as price moves in favor of the trade.

Manual Stop Loss & Take Profit - Allows precise percentage-based exit points.

Max Drawdown Protection - Closes all trades if equity falls below a set threshold, reducing risk.

Multi-Timeframe Supertrend Table

Displays Supertrend signals across different timeframes (1 min, 5 min, 15 min, 1 hour, Daily)

Helps traders align their entries with higher timeframe trends for better accuracy.

Custom Alerts

Alerts notify when a new buy/sell signal appears.

Extra early warning alerts indicate potential trade setups before confirmation.

How to Use

📌 For trend-following traders:

Focus on entries in the direction of the higher timeframes.

Only enter when ADX is trending and volume confirms liquidity.

📌 For scalpers:

Use shorter timeframes (1m, 5m, 15m) for quick trades.

Adjust the ATR multiplier and Adaptive ATR sensitivity for tighter stops.

📌 For swing traders:

Use longer timeframes (1H, Daily) for more stable trends.

Enable trailing stop loss to lock in profits as the trend progresses.

Inputs & Customization

ATR Period & Adaptive ATR Sensitivity

Supertrend Multiplier

ADX Filter & Threshold

Volume Confirmation Settings

Stop Loss & Take Profit Options

Multi-Timeframe Supertrend Display

Custom Alerts

Universal Strategy | QuantEdgeBIntroducing the Universal Strategy by QuantEdgeB

The Universal Strategy | QuantEdgeB is a dynamic, multi-indicator strategy designed to operate across various asset classes with precision and adaptability. This cutting-edge system utilizes four sophisticated methodologies, each integrating advanced trend-following, volatility filtering, and normalization techniques to provide robust signals. Its modular architecture and customizable features ensure suitability for diverse market conditions, empowering traders with data-driven decision-making tools. Its adaptability to different price behaviors and volatility levels makes it a robust and versatile tool, equipping traders with data-driven confidence in their market decisions.

_______

1. Core Methodologies and Features

1️⃣ DEMA ATR

Strength : Fast responsiveness to trend shifts.

The double exponential moving average is inherently aggressive, designed to reduce lag and quickly identify early signs of trend reversals or breakout opportunities. ATR bands add a volatility-sensitive layer, dynamically adjusting the breakout thresholds to match current market conditions, ensuring it remains responsive while filtering out noise

How It Fits :

This indicator is the first responder, providing early signals of potential trend shifts. While its aggressiveness can result in quick entries, it may occasionally overreact in noisy markets. This is where the smoother indicators step in to confirm signals.

2️⃣ Gaussian - VIDYA ATR (Variable Index Dynamic Average)

Strength : Smooth, adaptive trend identification.

Unlike DEMA, VIDYA adapts to market volatility through its standard deviation-based formula, making it smoother and less reactive to short-term fluctuations. ATR filtering ensures the indicator remains effective in volatile markets by dynamically adjusting its sensitivity.

How It Fits :

The smoother complement to DEMA ATR, VIDYA ATR filters out false signals from minor price movements. It provides confirmation for the trends identified by DEMA ATR, ensuring entries are based on robust, sustained price movements.

3️⃣ VIDYA Loop Trend Scoring

Strength : Historical trend scoring for consistent momentum detection.

This module evaluates the relative strength of trends by comparing the current VIDYA value to its historical values over a defined range. The loop mechanism provides a trend confidence score, quantifying the momentum behind price movements.

How It Fits :

VIDYA For-Loop adds a quantitative measure of trend strength, ensuring that trades are backed by sustained momentum. It balances the early signals from DEMA ATR and the smoothness of VIDYA ATR by providing a statistical check on the underlying trend.

4️⃣ Median SD with Normalization

Strength : Precision in breakout detection and market normalization.

The Median price serves as a robust baseline for detecting breakouts and reversals.

SD bands expand dynamically during periods of high volatility, making the indicator particularly effective for spotting strong trends or breakout opportunities. Normalization ensures the indicator adapts seamlessly across different assets and timeframes, providing consistent performance.

How It Fits :

The Median SD module provides final confirmation by focusing on price breakouts and market normalization. While the other indicators focus on momentum and trend strength, Median SD emphasizes precision, ensuring entries align with significant price movements rather than random fluctuations.

_______

2. How The Single Components Work Together

1️⃣ Balance of Speed and Smoothness :

The strategy blends quick responsiveness (DEMA ATR) with smooth and adaptive confirmation (VIDYA ATR & For-Loop), ensuring timely reactions without overreacting to market fluctuations. Median SD with Normalization refines breakout detection and stabilizes performance across assets using statistical anchors like price median and standard deviation.

Adaptability to Market Dynamics:

2️⃣ Adaptability to Market Dynamics :

The indicators complement each other seamlessly in trending markets, with the DEMA ATR and Median SD with Normalization quickly identifying shifts and confirming sustained momentum. In volatile or choppy markets, normalization and SD bands work together to filter out noise and reduce false signals, ensuring precise entries and exits. Meanwhile, the For-Loop scoring and Gaussian-Filtered VIDYA ATR focus on providing smoother, more reliable trend detection, offering consistent performance regardless of market conditions.

_______

3. Scoring and Signal Confirmation

The Universal Strategy consolidates signals from all four methodologies, calculating a Trend Probability Index (TPI). The four core indicators operate independently but contribute to a unified TPI, enabling highly adaptive behavior across asset classes.

- Each methodology generates a trend score: 1 for bullish trends, -1 for bearish trends.

- The TPI averages the scores, creating a unified signal.

- Long Position: Triggered when the TPI exceeds the long threshold (default: 0).

- Short Position: Triggered when the TPI falls below the short threshold (default: 0).

The strategy’s customizable settings allow traders to tailor its behavior to different market conditions—whether smoother trends in low-volatility assets or quick reaction to high-volatility breakouts. The long and short thresholds can be fine-tuned to match a trader’s risk tolerance and preferences.

_______

4. Use Cases:

The Universal Strategy | QuantEdgeB is designed to excel across a wide range of trading scenarios, thanks to its modular architecture and adaptability. Whether you're navigating trending, volatile, or range-bound markets, this strategy offers robust tools to enhance your decision-making. Below are the key use cases for its application:

1️⃣ Trend Trading

The strategy’s Gaussian-Filtered DEMA ATR and VIDYA ATR modules are perfect for identifying and riding sustained trends.

Ideal For: Traders looking to capture long-term momentum or position trades.

2️⃣ Breakout and Volatility-Based Strategies

With its Median SD with Normalization, the strategy excels in detecting volatility breakouts and significant price movements.

Ideal For: Traders aiming to capitalize on sudden market movements, especially in assets like cryptocurrencies and commodities.

3️⃣ Momentum and Strength Assessment

By generating a trend confidence score, the VIDYA For-Loop quantifies momentum strength—helping traders distinguish temporary spikes from sustainable trends.

Ideal For: Swing traders and those focusing on momentum-driven setups.

4️⃣ Adaptability Across Multiple Assets

The strategy’s robust framework ensures it performs consistently across different assets and timeframes.

Ideal For: Traders managing diverse portfolios or shifting between asset classes.

5️⃣ Backtesting and Optimization

Built-in backtesting and equity visualization tools make this strategy ideal for testing and refining parameters in real-world conditions.

• How It Helps: The strategy equity curve and metrics table offer a clear picture of performance, helping traders identify optimal settings for their chosen market and timeframe.

• Ideal For: Traders focused on rigorous testing and long-term optimization.

_______

5. Signal Composition Table:

This table presents a real-time breakdown of each indicator’s trend score (+1 bullish, -1 bearish) alongside the final aggregated signal. By visualizing the contribution of each methodology, traders gain greater transparency, confidence, and clarity in identifying long or short opportunities.

6. Customized Settings:

1️⃣ General Inputs

• Strategy Long Threshold (Lu): 0

• Strategy Short Threshold (Su): 0

2️⃣ Gaussian Filter

• Gaussian Length (len_FG): 4

• Gaussian Source (src_FG): close

• Gaussian Sigma (sigma_FG): 2.0

3️⃣ DEMA ATR

• DEMA Length (len_D): 30

• DEMA Source (src_D): close

• ATR Length (atr_D): 14

• ATR Multiplier (mult_D): 1.0

4️⃣ VIDYA ATR

• VIDYA Length (len_V1): 9

• SD Length (len_VHist1): 30

• ATR Length (atr_V): 14

• ATR Multiplier (mult_V): 1.7

5️⃣ VIDYA For-Loop

• VIDYA Length (len_V2): 2

• SD Length (len_VHist2): 5

• VIDYA Source (src_V2): close

• Start Loop (strat_loop): 1

• End Loop (end_loop): 60

• Long Threshold (long_t): 40

• Short Threshold (short_t): 8

6️⃣ Median SD

• Median Length (len_m): 24

• Normalized Median Length (len_msd): 50

• SD Length (SD_len): 32

• Long SD Weight (w1): 0.98

• Short SD Weight (w2): 1.02

• Long Normalized Smooth (smooth_long): 1

• Short Normalized Smooth (smooth_short): 1

Conclusion

The Universal Strategy | QuantEdgeB is a meticulously crafted, multi-dimensional trading system designed to thrive across diverse market conditions and asset classes. By combining Gaussian-Filtered DEMA ATR, VIDYA ATR, VIDYA For-Loop, and Median SD with Normalization, this strategy provides a seamless balance between speed, smoothness, and adaptability. Each component complements the others, ensuring traders benefit from early responsiveness, trend confirmation, momentum scoring, and breakout precision.

Its modular structure ensures versatility across trending, volatile, and consolidating markets. Whether applied to equities, forex, commodities, or crypto, it delivers data-driven precision while minimizing reliance on randomness, reinforcing confidence in decision-making.

With built-in backtesting tools, traders can rigorously evaluate performance under real-world conditions, while customization options allow fine-tuning for specific market dynamics and individual trading styles.

Why It Stands Out

The Universal Strategy | QuantEdgeB isn’t just a trading algorithm—it’s a comprehensive framework that empowers traders to make confident, informed decisions in the face of ever-changing market conditions. Its emphasis on precision, reliability, and transparency makes it a powerful tool for both professional and retail traders seeking consistent performance and enhanced risk management.

_______

🔹 Disclaimer: Past performance is not indicative of future results. No trading strategy can guarantee success in financial markets.

🔹 Strategic Advice: Always backtest, optimize, and align parameters with your trading objectives and risk tolerance before live trading.

Autonomous 5-Minute RobotKey Components of the Strategy:

Trend Detection:

A 50-period simple moving average (SMA) is used to define the market trend. If the current close is above the SMA, the market is considered to be in an uptrend (bullish), and if it's below, it's considered a downtrend (bearish).

The strategy also looks at the trend over the last 30 minutes (6 candles in a 5-minute chart). The strategy compares the previous close with the current close to detect an uptrend or downtrend.

Volume Analysis:

The strategy calculates buyVolume and sellVolume based on price movement within each candle.

The condition for entering a long position is when the market is in an uptrend, and the buy volume is greater than the sell volume.

The condition for entering a short position is when the market is in a downtrend, and the sell volume is greater than the buy volume.

Trade Execution:

The strategy enters a long position when the trend is up and the buy volume is higher than the sell volume.

The strategy enters a short position when the trend is down and the sell volume is higher than the buy volume.

Positions are closed based on stop-loss and take-profit conditions.

Stop-loss is set at 3% below the entry price.

Take-profit is set at 29% above the entry price.

Exit Conditions:

Long trades will be closed if the price falls 3% below the entry price or rises 29% above the entry price.

Short trades will be closed if the price rises 3% above the entry price or falls 29% below the entry price.

Visuals:

The SMA (50-period) is plotted on the chart to show the trend.

Buy and sell signals are marked with labels on the chart for easy identification.

With this being said this algo is still being worked on to be autonomous

Analyze the Market Direction: Determine whether the market is in an uptrend or downtrend over the past 30 minutes (using the last 6 candles in a 5-minute chart).

Use Trend Indicators and Volume: Implement trend-following indicators like moving averages or the SMA/EMA crossover and consider volume to decide when to enter or exit a trade.

Enter and Exit Trades: The robot will enter long positions when the trend is up and short positions when the trend is down. Additionally, it will close positions based on volume signals and price action (e.g., volume spikes, price reversals).

Adaptive Trend Flow Strategy with Filters for SPXThe Adaptive Trend Flow Strategy with Filters for SPX is a complete trading algorithm designed to identify traits and offer actionable alerts for the SPX index. This Pine Script approach leverages superior technical signs and user-described parameters to evolve to marketplace conditions and optimize performance.

Key Features and Functionality

Dynamic Trend Detection: Utilizes a dual EMA-based totally adaptive method for fashion calculation.

The script smooths volatility the usage of an EMA filter and adjusts sensitivity through the sensitivity enter. This allows for real-time adaptability to market fluctuations.

Trend Filters for Precision:

SMA Filter: A Simple Moving Average (SMA) guarantees that trades are achieved best while the rate aligns with the shifting average trend, minimizing false indicators.

MACD Filter: The Moving Average Convergence Divergence (MACD) adds some other layer of confirmation with the aid of requiring alignment among the MACD line and its sign line.

Signal Generation:

Long Signals: Triggered when the fashion transitions from bearish to bullish, with all filters confirming the pass.

Short Signals: Triggered while the trend shifts from bullish to bearish, imparting opportunities for final positions.

User Customization:

Adjustable parameters for EMAs, smoothing duration, and sensitivity make certain the strategy can adapt to numerous buying and selling patterns.

Enable or disable filters (SMA or MACD) based totally on particular market conditions or consumer possibilities.

Leverage and Position Sizing: Incorporates a leverage aspect for dynamic position sizing.

Automatically calculates the exchange length based on account fairness and the leverage element, making sure hazard control is in area.

Visual Enhancements: Plots adaptive fashion ranges (foundation, top, decrease) for actual-time insights into marketplace conditions.

Color-coded bars and heritage to visually represent bullish or bearish developments.

Custom labels indicating crossover and crossunder occasions for clean sign visualization.

Alerts and Automation: Configurable alerts for each lengthy and quick indicators, well matched with automated buying and selling structures like plugpine.Com.

JSON-based alert messages consist of account credentials, motion type, and calculated position length for seamless integration.

Backtesting and Realistic Assumptions: Includes practical slippage, commissions, and preliminary capital settings for backtesting accuracy.

Leverages excessive-frequency trade sampling to make certain strong strategy assessment.

How It Works

Trend Calculation: The method derives a principal trend basis with the aid of combining fast and gradual EMAs. It then uses marketplace volatility to calculate adaptive upper and decrease obstacles, creating a dynamic channel.

Filter Integration: SMA and MACD filters work in tandem with the fashion calculation to ensure that handiest excessive-probability signals are accomplished.

Signal Execution: Signals are generated whilst the charge breaches those dynamic tiers and aligns with the fashion and filters, ensuring sturdy change access situations.

How to Use

Setup: Apply the approach to SPX or other well suited indices.

Adjust person inputs, together with ATR length, EMA smoothing, and sensitivity, to align together with your buying and selling possibilities.

Enable or disable the SMA and MACD filters to test unique setups.

Alerts: Configure signals for computerized notifications or direct buying and selling execution through third-celebration systems.

Use the supplied JSON payload to integrate with broking APIs or automation tools.

Optimization:

Experiment with leverage, filter out settings, and sensitivity to find most effective configurations to your hazard tolerance and marketplace situations.

Considerations and Best Practices

Risk Management: Always backtest the method with realistic parameters, together with conservative leverage and commissions.

Market Suitability: While designed for SPX, this method can adapt to other gadgets by means of adjusting key parameters.

Limitations: The method is trend-following and can underperform in enormously risky or ranging markets. Regularly evaluate and modify parameters primarily based on recent market conduct.

If you have any questions please let me know - I'm here to help!

DemaRSI StrategyThis is a repost to a old script that cant be updated anymore, the request was made on Feb, 27, 2016.

Here's a engaging description for the tradingview script:

**DemaRSI Strategy: A Proven Trading System**

Join thousands of traders who have already experienced the power of this highly effective strategy. The DemaRSI system combines two powerful indicators - DEMA (Double Exponential Moving Average) and RSI (Relative Strength Index) - to generate profitable trades with minimal risk.

**Key Features:**

* **Trend-Following**: Our algorithm identifies strong trends using a combination of DEMA and RSI, allowing you to ride the waves of market momentum.

* **Risk Management**: The system includes built-in stop-loss and take-profit levels, ensuring that your gains are protected and losses are minimized.

* **Session-Based Trading**: Trade during specific sessions only (e.g., London or New York) for even more targeted results.

* **Customizable Settings**: Adjust the length of moving averages, RSI periods, and other parameters to suit your trading style.

**What You'll Get:**

* A comprehensive strategy that can be used with any broker or platform

* Easy-to-use interface with customizable settings

* Real-time performance metrics and backtesting capabilities

**Start Trading Like a Pro Today!**

This script is designed for intermediate to advanced traders who want to take their trading game to the next level. With its robust risk management features, this strategy can help you achieve consistent profits in various market conditions.

**Disclaimer:** This script is not intended as investment advice and should be used at your own discretion. Trading carries inherent risks, and losses are possible.

~Llama3

MultiLayer Awesome Oscillator Saucer Strategy [Skyrexio]Overview

MultiLayer Awesome Oscillator Saucer Strategy leverages the combination of Awesome Oscillator (AO), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Awesome Oscillator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.