Turtle Trading System + ATR Trailing StopIndicator Description: Turtle ATR Trailing Stop

The **Turtle ATR Trailing Stop** is a technical indicator designed to enhance the classic Turtle Trading System by incorporating a dynamic trailing stop based on the Average True Range (ATR). This indicator is ideal for traders seeking to manage risk and lock in profits on both long and short positions in trending markets.

Key Features:

- Turtle Trading Levels: Calculates the 20-day highest high and lowest low to identify potential breakout points, a core principle of the Turtle Trading System.

- ATR-Based Trailing Stop: Utilizes a trailing stop that adjusts dynamically based on a multiple of the ATR (default multiplier: 2.0), providing a volatility-adjusted exit mechanism.

- Position Flexibility: Supports both long and short positions, with the trailing stop positioned below the highest price for long trades and above the lowest price for short trades.

- Smooth Updates: The trailing stop updates on each bar, ensuring a more responsive adjustment to price movements, rather than only on new highs or lows.

- Reset Mechanism: Automatically resets the trailing stop when the price deviates significantly (configurable threshold, default 0.1%), adapting to major trend reversals.

- Alerts: Includes customizable alerts that trigger when the price reaches the trailing stop level, notifying traders of potential exit points.

- Debugging Tools: Features an on-chart debug table displaying ATR, Close, Highest Price, Lowest Price, Potential Stop, and Trailing Stop values for real-time analysis.

How It Works:

- For **Long Positions**: The trailing stop starts below the initial close price (minus 2*ATR) and moves up as the highest price increases, locking in profits while trailing at a fixed ATR distance.

- For **Short Positions**: The trailing stop starts above the initial close price (plus 2*ATR) and moves down as the lowest price decreases, protecting against upward price movements.

- The stop resets if the price falls (for long) or rises (for short) beyond the set threshold, ensuring adaptability to new market conditions.

Customization:

- Period Settings: Adjust the length for highs/lows (default 20) and ATR period (default 14).

- ATR Multiplier: Modify the distance of the trailing stop (default 2.0).

- Reset Threshold: Fine-tune the percentage at which the stop resets (default 0.1%).

- Position Type: Switch between "Long" and "Short" modes via input settings.

Usage:

Apply this indicator to any chart in TradingView, set your preferred parameters, and monitor the trailing stop line (yellow) alongside the Turtle highs (red) and lows (blue). Use the debug table to validate calculations and set alerts to stay informed of stop triggers.

This indicator combines the trend-following strength of the Turtle System with a flexible, ATR-based stop-loss strategy, making it a powerful tool for both manual and automated trading strategies.

Cerca negli script per "atr"

NY Open Breakout [ATR-5000]# **New York Open Breakout Indicator **

## **📌 Overview**

This **Pine Script** indicator identifies high-probability breakout opportunities at the **New York market open (13:30 UTC)** based on **volatility filters** using **customizable ATR periods and thresholds**.

### **🔹 Key Features**

✅ **Fully Customizable ATR Periods** (2 to **5000** bars)

✅ **Adjustable Thresholds** (0.01% to 5.00%)

✅ **Opening Range (OR) Filter** (0.01% to 5.00%)

✅ **Clean Visuals** – Only highlights the **13:30 UTC candle** when conditions are met

✅ **Real-Time Info Panel** – Displays current ATR & threshold settings

✅ **Automatic Daily Reset** – Fresh signals every trading day

---

## **📊 How It Works**

### **1️⃣ Volatility Check (13:25 UTC)**

- Calculates **two ATR values** (user-defined periods)

- Compares them against **custom % thresholds**

- Only proceeds if **both ATRs exceed** their required volatility levels

### **2️⃣ Opening Range Confirmation (13:30 UTC)**

- Measures the **high-low range** of the 13:30 candle

- Validates if the range meets the **minimum % threshold**

- If all conditions pass → **Highlights the candle** in your chosen color

### **3️⃣ Visual Feedback**

- **🟣 Colored Candle** → Valid breakout signal

- **📊 Info Table** → Shows current ATR settings & thresholds

---

## **⚙️ Customization Options**

| **Setting** | **Default** | **Adjustable Range** |

|---------------------------|------------|----------------------|

| **First ATR Period** | 14 | **2–5000** bars |

| **Second ATR Period** | 161 | **2–5000** bars |

| **First ATR Threshold** | 0.42% | **0.01%–5.00%** |

| **Second ATR Threshold** | 0.40% | **0.01%–5.00%** |

| **OR Range Threshold** | 0.42% | **0.01%–5.00%** |

| **Candle Color** | Purple | **Any color** |

---

## **📈 Best Use Cases**

✔ **Forex (EURUSD, GBPUSD)** – Captures NY session momentum

✔ **Indices (SPX, NASDAQ)** – Works well with opening volatility

✔ **Commodities (Gold, Oil)** – Filters out low-energy days

---

## **🔧 How to Adjust Settings**

1. **Click the gear icon (⚙️)** on your TradingView chart

2. **Modify ATR periods & thresholds** as needed

3. **Change the candle color** for better visibility

---

## **🚀 Why This Indicator?**

- **No repainting** – Signals lock in after candle close

- **No clutter** – Only marks valid 13:30 candles

- **Adaptable** – Works on **any market & timeframe**

- **Fully automated** – No manual adjustments needed

---

### **📥 Apply & Start Trading!**

Simply **load the script** on TradingView and customize it to fit your strategy! 🚀

Smart Market Matrix Smart Market Matrix

This indicator is designed for intraday, scalping, providing automated detection of price pivots, liquidity traps, and breakout confirmations, along with a context dashboard featuring volatility, trend, and volume.

## Summary Description

### Menu Settings & Their Roles

- **Swing Pivot Strength**: Controls the sensitivity for detecting High/Low pivots.

- **Show Pivot Points**: Toggles the display of HH/LL markers on the chart.

- **VWMA Length for Trap Volume** & **Volume Spike Multiplier**: Identify concentrated volume spikes for liquidity traps.

- **Wick Ratio Threshold** & **Max Body Size Ratio**: Detect candles with disproportionate wicks and small bodies (doji-ish) for traps.

- **ATR Length for Trap**: Measures volatility specific to trap detection.

- **VWMA Length for Breakout Volume**, **ATR Multiplier for Breakout**, **ATR Length for Breakout**, **Min Body/Range Ratio**: Set adaptive breakout thresholds based on volatility and volume.

- **OBV Smooth Length**: Smooths OBV momentum for breakout confirmation.

- **Enable VWAP Filter for Confirmations**: Optionally validate breakouts against the VWAP.

- **Enable Higher-TF Trend Filter** & **Trend Filter Timeframe**: Align breakout signals with the 1h/4h/Daily trend.

- **ADX Length**, **EMA Fast/Slow Length for Context**: Parameters for the context dashboard (Volatility, Trend, Volume).

- **Show Intraday VWAP Line**, **VWAP Line Color/Width**: Display the intraday VWAP line with custom style.

### Signal Interpretation Map

| Signal | Description | Recommended Action |

|--------------------------------|-----------------------------------------------------------|-------------------------------------------|

| 📌 **HH / LL (pivot)** | Market structure (support/resistance) | Note key levels |

| **Bull Trap(green diamond)** | Sweep down + volume spike + wick + rejection | Go long with trend filter

| **Bear Trap(red diamond)** | Sweep up + volume spike + wick + rejection | Go short with trend filter

| 🔵⬆️ **Breakout Confirmed Up** | Close > ATR‑scaled high + volume + OBV↑ | Go long with trend filter |

| 🔵⬇️ **Breakout Confirmed Down** | Close < ATR‑scaled low + volume + OBV↓ | Go short with trend filter |

| 📊 **VWAP Line** | Intraday reference to guide price | Use as dynamic support/resistance |

| ⚡ **Volatility** | ATR ratio High/Med/Low | Adjust position size |

| 📈 **Trend Context** | ADX+EMA Strong/Moderate/Weak | Confirm trend direction |

| 🔍 **Volume Context** | Breakout / Rising / Falling / Calm | Check volume momentum |

*This summary gives you a quick overview of the key settings and how to interpret signals for efficient intraday scalping.*

### Suggested Settings

- **Intraday Scalping (5m–15m)**

- `Swing Pivot Strength = 5`

- `VWMA Length for Trap Volume = 10`, `Volume Spike Multiplier = 1.6`

- `ATR Length for Trap = 7`

- `VWMA Length for Breakout Volume = 12`, `ATR Length for Breakout = 9`, `ATR Multiplier for Breakout = 0.5`

- `Min Body/Range Ratio for Breakout = 0.5`, `OBV Smooth Length = 7`

- `Enable Higher-TF Trend Filter = true` (TF = 60)

- `Show Intraday VWAP Line = true` (Color = orange, Width = 2)

- **Swing Trading (4h–Daily)**

- `Swing Pivot Strength = 10`

- `VWMA Length for Trap Volume = 20`, `Volume Spike Multiplier = 2.0`

- `ATR Length for Trap = 14`

- `VWMA Length for Breakout Volume = 30`, `ATR Length for Breakout = 14`, `ATR Multiplier for Breakout = 0.8`

- `Min Body/Range Ratio for Breakout = 0.7`, `OBV Smooth Length = 14`

- `Enable Higher-TF Trend Filter = true` (TF = D)

- `Show Intraday VWAP Line = false`

*Adjust these values based on the symbol and market volatility for optimal performance.*

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

VolatilityIndicatorsLibrary "VolatilityIndicators"

This is a library of Volatility Indicators .

It aims to facilitate the grouping of this category of indicators, and also offer the customized supply of

the parameters and sources, not being restricted to just the closing price.

@Thanks and credits:

1. Dynamic Zones: Leo Zamansky, Ph.D., and David Stendahl

2. Deviation: Karl Pearson (code by TradingView)

3. Variance: Ronald Fisher (code by TradingView)

4. Z-score: Veronique Valcu (code by HPotter)

5. Standard deviation: Ronald Fisher (code by TradingView)

6. ATR (Average True Range): J. Welles Wilder (code by TradingView)

7. ATRP (Average True Range Percent): millerrh

8. Historical Volatility: HPotter

9. Min-Max Scale Normalization: gorx1

10. Mean Normalization: gorx1

11. Standardization: gorx1

12. Scaling to unit length: gorx1

13. LS Volatility Index: Alexandre Wolwacz (Stormer), Fabrício Lorenz, Fábio Figueiredo (Vlad) (code by me)

14. Bollinger Bands: John Bollinger (code by TradingView)

15. Bollinger Bands %: John Bollinger (code by TradingView)

16. Bollinger Bands Width: John Bollinger (code by TradingView)

dev(source, length, anotherSource)

Deviation. Measure the difference between a source in relation to another source

Parameters:

source (float)

length (simple int) : (int) Sequential period to calculate the deviation

anotherSource (float) : (float) Source to compare

Returns: (float) Bollinger Bands Width

variance(src, mean, length, biased, degreesOfFreedom)

Variance. A statistical measurement of the spread between numbers in a data set. More specifically,

variance measures how far each number in the set is from the mean (average), and thus from every other number in the set.

Variance is often depicted by this symbol: σ2. It is used by both analysts and traders to determine volatility and market security.

Parameters:

src (float) : (float) Source to calculate variance

mean (float) : (float) Mean (Moving average)

length (simple int) : (int) The sequential period to calcule the variance (number of values in data set)

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length. Only applies when biased parameter is defined as true.

Returns: (float) Standard deviation

stDev(src, length, mean, biased, degreesOfFreedom)

Measure the Standard deviation from a source in relation to it's moving average.

In this implementation, you pass the average as a parameter, allowing a more personalized calculation.

Parameters:

src (float) : (float) Source to calculate standard deviation

length (simple int) : (int) The sequential period to calcule the standard deviation

mean (float) : (float) Moving average.

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Standard deviation

zscore(src, mean, length, biased, degreesOfFreedom)

Z-Score. A z-score is a statistical measurement that indicates how many standard deviations a data point is from

the mean of a data set. It is also known as a standard score. The formula for calculating a z-score is (x - μ) / σ,

where x is the individual data point, μ is the mean of the data set, and σ is the standard deviation of the data set.

Z-scores are useful in identifying outliers or extreme values in a data set. A positive z-score indicates that the

data point is above the mean, while a negative z-score indicates that the data point is below the mean. A z-score of

0 indicates that the data point is equal to the mean.

Z-scores are often used in hypothesis testing and determining confidence intervals. They can also be used to compare

data sets with different units or scales, as the z-score standardizes the data. Overall, z-scores provide a way to

measure the relative position of a data point in a data

Parameters:

src (float) : (float) Source to calculate z-score

mean (float) : (float) Moving average.

length (simple int) : (int) The sequential period to calcule the standard deviation

biased (simple bool) : (bool) Defines the type of standard deviation. If true, uses biased sample variance (n),

else uses unbiased sample variance (n-1 or another value, as long as it is in the range between 1 and n-1), where n=length.

degreesOfFreedom (simple int) : (int) Degrees of freedom. The number of values in the final calculation of a statistic that are free to vary.

Default value is n-1, where n here is length.

Returns: (float) Z-score

atr(source, length)

ATR: Average True Range. Customized version with source parameter.

Parameters:

source (float) : (float) Source

length (simple int) : (int) Length (number of bars back)

Returns: (float) ATR

atrp(length, sourceP)

ATRP (Average True Range Percent)

Parameters:

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

atrp(source, length, sourceP)

ATRP (Average True Range Percent). Customized version with source parameter.

Parameters:

source (float) : (float) Source for ATR

length (simple int) : (int) Length (number of bars back) for ATR

sourceP (float) : (float) Source for calculating percentage relativity

Returns: (float) ATRP

historicalVolatility(lengthATR, lengthHist)

Historical Volatility

Parameters:

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

historicalVolatility(source, lengthATR, lengthHist)

Historical Volatility

Parameters:

source (float) : (float) Source for ATR

lengthATR (simple int) : (int) Length (number of bars back) for ATR

lengthHist (simple int) : (int) Length (number of bars back) for Historical Volatility

Returns: (float) Historical Volatility

minMaxNormalization(src, numbars)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

minMaxNormalization(src, numbars, minimumLimit, maximumLimit)

Min-Max Scale Normalization. Maximum and minimum values are taken from the sequential range of

numbars bars back, where numbars is a number defined by the user.

In this implementation, the user explicitly provides the desired minimum (min) and maximum (max) values for the scale,

rather than using the minimum and maximum values from the data.

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

minimumLimit (simple float) : (float) Minimum value to scale

maximumLimit (simple float) : (float) Maximum value to scale

Returns: (float) Normalized value

meanNormalization(src, numbars, mean)

Mean Normalization

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

mean (float) : (float) Mean of source

Returns: (float) Normalized value

standardization(src, mean, stDev)

Standardization (Z-score Normalization). How "outside the mean" values relate to the standard deviation (ratio between first and second)

Parameters:

src (float) : (float) Source to normalize

mean (float) : (float) Mean of source

stDev (float) : (float) Standard Deviation

Returns: (float) Normalized value

scalingToUnitLength(src, numbars)

Scaling to unit length

Parameters:

src (float) : (float) Source to normalize

numbars (simple int) : (int) Numbers of sequential bars back to seek for lowest and hightest values.

Returns: (float) Normalized value

lsVolatilityIndex(movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int) : (float) Length for normalization

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

lsVolatilityIndex(sourcePrice, movingAverage, sourceHvol, lengthATR, lengthHist, lenNormal, lowerLimit, upperLimit)

LS Volatility Index. Measures the volatility of price in relation to an average.

Parameters:

sourcePrice (float) : (float) Source for measure the distance

movingAverage (float) : (float) A moving average

sourceHvol (float) : (float) Source for calculating the historical volatility

lengthATR (simple int) : (float) Length for calculating the ATR (Average True Range)

lengthHist (simple int) : (float) Length for calculating the historical volatility

lenNormal (simple int)

lowerLimit (simple int)

upperLimit (simple int)

Returns: (float) LS Volatility Index

bollingerBands(src, length, mult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) A tuple of Bollinger Bands, where index 1=basis; 2=basis+dev; 3=basis-dev; and dev=multiplier*stdev

bollingerBands(src, length, aMult, basis)

Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted

two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price,

but can be adjusted to user preferences. In this version you can pass a customized basis (moving average), not only SMA.

Also, various multipliers can be passed, thus getting more bands (instead of just 2).

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) An array of multiplies used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands, where:

index 1=basis; 2=basis+dev1; 3=basis-dev1; 4=basis+dev2, 5=basis-dev2, 6=basis+dev2, 7=basis-dev2, Nup=basis+devN, Nlow=basis-devN

and dev1, dev2, devN are ```multiplier N * stdev```

bollingerBandsB(src, length, mult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation:

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands %B

bollingerBandsB(src, length, aMult, basis)

Bollinger Bands %B - or Percent Bandwidth (%B).

Quantify or display where price (or another source) is in relation to the bands.

%B can be useful in identifying trends and trading signals.

Calculation

%B = (Current Price - Lower Band) / (Upper Band - Lower Band)

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) The time period to be used in calculating the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands %B. The number of results in this array is equal the numbers of multipliers passed via parameter.

bollingerBandsW(src, length, mult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation:

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

mult (simple float) : (float) Multiplier used in standard deviation

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float) Bollinger Bands Width

bollingerBandsW(src, length, aMult, basis)

Bollinger Bands Width. Serve as a way to quantitatively measure the width between the Upper and Lower Bands

Calculation

Bollinger Bands Width = (Upper Band - Lower Band) / Middle Band

Parameters:

src (float) : (float) Source to calculate standard deviation used in Bollinger Bands

length (simple int) : (int) Sequential period to calculate the standard deviation

aMult (float ) : (float ) Array of multiplier used in standard deviation. Basically, the upper/lower bands are standard deviation multiplied by this.

This array of multipliers permit the use of various bands, not only 2.

basis (float) : (float) Basis of Bollinger Bands (a moving average)

Returns: (float ) An array of Bollinger Bands Width. The number of results in this array is equal the numbers of multipliers passed via parameter.

dinamicZone(source, sampleLength, pcntAbove, pcntBelow)

Get Dynamic Zones

Parameters:

source (float) : (float) Source

sampleLength (simple int) : (int) Sample Length

pcntAbove (simple float) : (float) Calculates the top of the dynamic zone, considering that the maximum values are above x% of the sample

pcntBelow (simple float) : (float) Calculates the bottom of the dynamic zone, considering that the minimum values are below x% of the sample

Returns: A tuple with 3 series of values: (1) Upper Line of Dynamic Zone;

(2) Lower Line of Dynamic Zone; (3) Center of Dynamic Zone (x = 50%)

Examples:

SuperTrend OptimizerHello!

This indicator attempts to optimize Supertrend parameters. To achieve this, 102 parameter combinations are tested concurrently - the top three performers are listed in descending order.

Parameters,

Factor: Changes to this parameter shifts the tested factor range. For instance, increasing the factor measure from 3.00 to 3.01 (+0.01) will remove 3.00 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower Factor threshold + 3.3 (i.e. 3.0(lower) - 6.3(upper), 4.0(lower) - 7.3(upper), 2.5(lower) - 5.8(upper))

ATR period: Changes to this parameter shifts the tested ATR period range. For instance, increasing the ATR measure from 10 to 11 (+1) will remove 10 from the tested range - this setting controls the lower threshold of the range. The upper threshold, in all instances, is the lower threshold + 2 (i.e. 10(lower) - 12(upper), 11(lower) - 13(upper), 9(lower), - 11(upper))

The Factor parameter is modifiable to any positive decimal number; the ATR parameter is modifiable to any positive integer. Changing either parameter shifts the tested parameter combination range. Both parameters can be changed in the settings, to which you control the lower threshold of the range. If, for instance, you were to change the Factor measurement from 3.0 to 4.1 (+1.1) the 4.0 Factor measurement, and all Factor measures less than 4.0, will be excluded from the performance test.

Consequently, a Supertrend test will be performed with a Factor of 4.1 and an ATR period of 10 (default). This test repeats at 0.1 Factor intervals and 1.0 ATR intervals.

Therefore, assume you modify the Factor lower threshold to 3.1 and the ATR lower threshold to 10. The indicator will test three Supertrend systems with a Factor of 3.1 and an ATR period of 10.. then 11.. 12, then three systems with a Factor of 3.2 and an ATR period of 10.. then 11.. 12... until (lower Factor threshold + 3.3) and (lower ATR threshold + 2) are tested... which in this example is... a Factor of 6.4 and an ATR period of 12.

The tested Factor range and ATR range are displayed in a bottom right table alongside the top performing parameter combinations.

Of course, you can change the the lower thresholds, which means you can test numerous Supertrend parameter combinations! However, no greater than 102 parameter combinations will be tested simultaneously; the best performing Supertrend parameters are plotted on the chart automatically.

I will be working on this indicator more tomorrow! Let me know if you have questions or anything you would like included!

(I of course added something fun in the script. Be sure to try it with bar replay!)

Daily ATR (Shown on All Timeframes)Daily ATR (Shown on All Timeframes) displays the Daily timeframe ATR on any chart you’re viewing, so you always know the current day’s average range without switching timeframes.

True Daily ATR (not chart ATR): The script pulls ATR from the Daily chart using request.security() and shows that value on every timeframe.

On-chart table (top-right): A clean 2-row table shows:

The label: Daily ATR (Length)

The ATR value, with an optional ATR-as-% of price readout.

Custom display controls:

ATR Length input (default 14)

Toggle to show ATR % of current price

Toggle to show/hide the table

Choose table text color

Choose table text size (Tiny → Huge)

Data Window output: The Daily ATR value is also plotted invisibly so it appears in TradingView’s Data Window for quick reference.

This is useful for gauging daily volatility, setting risk/position sizing, and comparing intraday movement to the stock’s typical daily range.

Daily ATR (Shown on All Timeframes)Daily ATR (Shown on All Timeframes) displays the Daily timeframe ATR on any chart you’re viewing, so you always know the current day’s average range without switching timeframes.

True Daily ATR (not chart ATR): The script pulls ATR from the Daily chart using request.security() and shows that value on every timeframe.

On-chart table (top-right): A clean 2-row table shows:

The label: Daily ATR (Length)

The ATR value, with an optional ATR-as-% of price readout.

Custom display controls:

ATR Length input (default 14)

Toggle to show ATR % of current price

Toggle to show/hide the table

Choose table text color

Choose table text size (Tiny → Huge)

Data Window output: The Daily ATR value is also plotted invisibly so it appears in TradingView’s Data Window for quick reference.

This is useful for gauging daily volatility, setting risk/position sizing, and comparing intraday movement to the stock’s typical daily range.

Volatility State Index [Interakktive]The Volatility State Index (VSI) classifies market volatility into three behavioral states: Expansion, Decay, and Transition. It answers one question visually: Is volatility supporting price movement, withdrawing, or unstable?

Unlike traditional volatility indicators that show levels or bands, VSI diagnoses the current volatility regime so traders can adapt their approach accordingly.

█ WHAT IT DOES

• Classifies volatility into three states: Expansion (teal), Decay (grey), Transition (amber)

• Measures volatility momentum as a percentage rate-of-change

• Applies stability filtering to detect unstable/choppy conditions

• Uses persistence logic to prevent state flickering

• Exports state data for use in alerts and strategies

█ WHAT IT DOES NOT DO

• NO buy/sell signals

• NO entry/exit recommendations

• NO alerts (v1 is diagnostic only)

• NO performance claims

This is a volatility diagnostic tool, not a trading system.

█ HOW IT WORKS

The VSI processes volatility through a five-stage pipeline:

STAGE 1 — Base Volatility

Calculates ATR as the foundation for volatility measurement.

STAGE 2 — Smoothing

Applies EMA smoothing to reduce noise in the volatility series.

STAGE 3 — Volatility Momentum

Computes the percentage rate-of-change of smoothed volatility:

Volatility Momentum (%) = ((Current ATR - Previous ATR) / Previous ATR) × 100

Positive values indicate expanding volatility; negative values indicate contracting volatility.

STAGE 4 — Stability Filter

Tracks how frequently volatility momentum changes direction. Frequent sign changes indicate unstable, choppy conditions.

Stability Score = 1 - (Average Flip Rate)

Low stability forces the Transition state regardless of momentum level.

STAGE 5 — State Classification

Combines momentum thresholds and stability to determine the final state:

• Expansion: Momentum ≥ +5% (default threshold)

• Decay: Momentum ≤ -5% (default threshold)

• Transition: Between thresholds OR low stability

A persistence filter requires states to hold for multiple bars before confirming, preventing visual noise.

█ INTERPRETATION

EXPANSION (Teal)

Volatility is increasing in a sustained way. Price moves are becoming larger.

What it suggests:

• Breakouts are more likely to follow through

• Stops may need wider placement

• Trend-following approaches tend to work better

• Mean-reversion weakens

DECAY (Grey)

Volatility is decreasing. Price is compressing into tighter ranges.

What it suggests:

• Breakouts are more likely to fail

• Ranges tend to hold

• Trend-following underperforms

• Mean-reversion strengthens

TRANSITION (Amber)

Volatility behavior is unclear or unstable. This is NOT neutral — it is uncertainty.

What it suggests:

• Mixed signals — one bar huge, next bar dead

• Higher whipsaw risk

• Reduced conviction in either direction

• Consider waiting for clarity

The key insight: Amber is a warning, not a middle ground. It appears when volatility cannot decide what it wants to do.

█ VISUAL DESIGN

The indicator uses a state-first histogram design:

• Histogram height shows volatility momentum percentage

• Histogram color shows the classified state

• Zero line provides visual anchor

• Optional momentum line for confirmation

• Optional background tint (default OFF for clean charts)

The visual hierarchy prioritizes instant state recognition. A trader should understand the volatility environment in under one second without reading numbers.

█ INPUTS

Core Settings

• ATR Length: Base volatility measurement period (default: 14)

• Smoothing Length: EMA smoothing applied to ATR (default: 10)

• Momentum Length: Rate-of-change lookback (default: 10)

State Classification

• Expansion Threshold (%): Momentum above this = Expansion (default: 5.0)

• Decay Threshold (%): Momentum below this = Decay (default: -5.0)

• Persistence Bars: Bars required to confirm state change (default: 3)

• Stability Lookback: Window for stability calculation (default: 20)

• Stability Threshold: Below this = forced Transition (default: 0.5)

Visual Settings

• Show State Histogram: Toggle main display (default: ON)

• Show Momentum Line: Thin confirmation line (default: OFF)

• Show Zero Line: Baseline reference (default: ON)

• Show Background Tint: Subtle state coloring (default: OFF)

█ DATA WINDOW EXPORTS

When enabled, the following values are exported:

• ATR (Raw)

• ATR (Smoothed)

• Volatility Momentum (%)

• Stability Score (0-1)

• State (-1/0/1): Decay = -1, Transition = 0, Expansion = 1

• Is Expansion (0/1)

• Is Decay (0/1)

• Is Transition (0/1)

These exports allow VSI to be used as a filter in Pine Script strategies or alert conditions.

█ ORIGINALITY

While ATR and volatility indicators are common, VSI is original because it:

1. Classifies volatility into behavioral states rather than showing raw levels

2. Applies momentum analysis to volatility itself (rate-of-change of ATR)

3. Uses stability filtering to detect genuinely unstable conditions

4. Implements persistence logic to prevent state flickering

5. Provides a state-first visual design optimized for instant recognition

VSI is state-first: it classifies volatility regimes (Expansion/Decay/Transition) rather than plotting volatility level alone, using momentum and stability to reduce false regime reads.

This is not a modified ATR or Bollinger Band — it is a volatility regime classifier.

█ SUITABLE MARKETS

Works on: Stocks, Futures, Forex, Crypto

Timeframes: All timeframes — state classification adapts accordingly

Best on: Instruments with consistent volatility patterns

█ RELATED

• Market Efficiency Ratio — measures price path efficiency

• Effort-Result Divergence — compares volume effort to price result

█ DISCLAIMER

This indicator is for educational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own analysis before making trading decisions.

Risk Recommender — (Heatmap)📊 Risk Recommender — Per-Trade & Annualized (Heatmap Columns)

Estimate the optimal risk percentage for any market regime.

This tool dynamically recommends how much of your account equity to risk — either per trade or at a portfolio (annualized) level — using volatility as the guide.

⚙️ How it works

Two distinct modes give you flexibility:

1️⃣ Per-Trade (ATR-based)

• Calculates the current Average True Range (ATR) compared to its long-term baseline.

• When volatility is high (ATR ↑), risk per trade decreases to maintain constant dollar risk.

• When volatility is low (ATR ↓), risk per trade increases within your defined floor and ceiling.

• The display is normalized by stop distance (× ATR) and smoothed to avoid noise.

2️⃣ Annualized (Volatility Targeting)

• Computes realized volatility (standard deviation of log returns) and an EWMA forecast of future volatility.

• Blends current and forecast volatilities to estimate “effective” volatility.

• Scales your base risk so that portfolio volatility converges toward your chosen annual target (e.g., 20%).

• Useful for portfolio-level or systematic strategies that maintain constant volatility exposure.

🎨 Heatmap Visualization

The vertical column graph acts like a thermometer:

• 🟥 Red → “Reduce risk” (volatility high).

• 🟩 Green → “Increase risk” (volatility low).

• Smoothed and bounded between your Floor and Ceiling risk levels.

• Optional dotted guides mark those bounds.

• Label shows the current mode, recommended risk %, and key metrics (ATR ratio or effective volatility).

🔧 Key Inputs

• Base max risk per trade (%) — your normal per-trade risk budget.

• ATR length / Baseline ATR length — control sensitivity to short- vs. long-term volatility.

• Target annualized volatility (%) — portfolio volatility target for quant mode.

• λ (lambda) — smoothing factor for the EWMA volatility forecast (0.90–0.99 typical).

• Floor & Ceiling — clamps the output to avoid extreme sizing.

• Smoothing & Hysteresis — prevent rapid changes in risk recommendations.

🧮 Interpreting the Output

• “Recommended Risk (%)” = suggested portion of equity to risk on the next trade (or current exposure).

• In Per-Trade mode: reflects current ATR ÷ baseline ATR .

• In Annualized mode: reflects target volatility ÷ effective volatility .

• Use the color and height of the column as a quick visual cue for aggressiveness.

💡 Typical Use Cases

• Position-sizing overlay for discretionary traders.

• Volatility-targeting component for algorithmic or multi-asset systems.

• Educational tool to understand how volatility governs prudent risk management.

📘 Notes

• This indicator provides risk suggestions only ; it does not place trades.

• Works on any symbol or timeframe.

• Combine with your own strategy or alerts for full automation.

• All calculations use built-in Pine functions; no proprietary logic.

Tags:

#RiskManagement #ATR #Volatility #Quant #PositionSizing #SystematicTrading #AlgorithmicTrading #Portfolio #TradingStrategy #Heatmap #EWMA #Risk

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

EMA ± ATR Channel (True Range)EMA ± ATR Channel (True Range)

Tagline: Adaptive EMA channel with ATR-based volatility bands — perfect for swing trading, intraday setups, and managing risk on high-volatility stocks.

This script plots a dynamic price channel around a configurable EMA using the Average True Range (ATR, Wilder’s True Range) as a volatility buffer.

Upper band = EMA + (ATR × multiplier)

Lower band = EMA – (ATR × multiplier)

📊 Features:

Adjustable EMA length, ATR length, and ATR multiplier

Visual channel fill between upper and lower bands

Optional on-chart help panel with practical combos

⚡ Practical Combos for Volatile Stocks:

EMA 20 + ATR 14 × 2.0 → most common swing trading setup

EMA 10 + ATR 14 × 1.5 → very responsive, good for intraday/high-beta names

EMA 20 + ATR 20 × 2.5 → smoother, wider channel, avoids whipsaws in chaotic stocks

✅ Use cases:

Identify dynamic support/resistance zones

Volatility-based stop-loss & take-profit placement

Spot overextensions from the trend midline

🔖 Tags:

ema, atr, channel, volatility, trend, support resistance, stop loss, swing trading, intraday, risk management, indicator

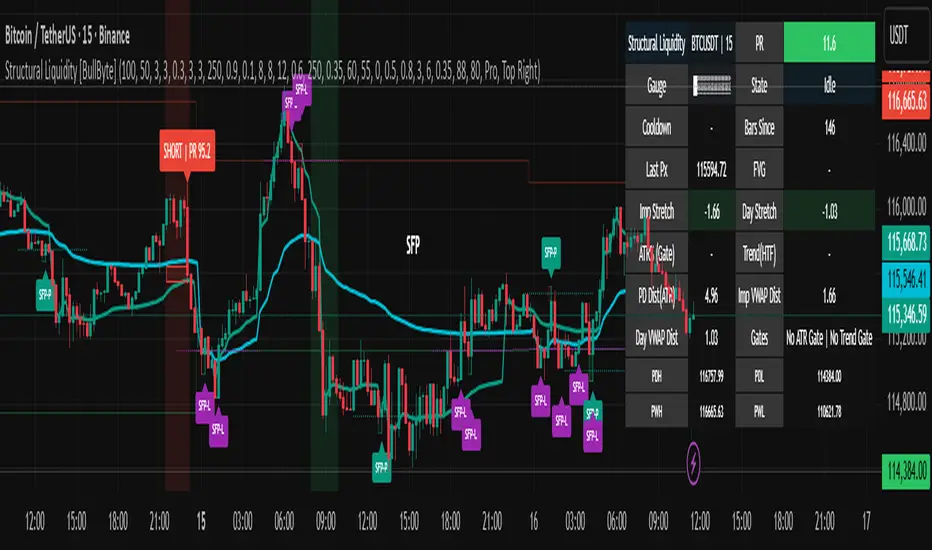

Structural Liquidity Signals [BullByte]Structural Liquidity Signals (SFP, FVG, BOS, AVWAP)

Short description

Detects liquidity sweeps (SFPs) at pivots and PD/W levels, highlights the latest FVG, tracks AVWAP stretch, arms percentile extremes, and triggers after confirmed micro BOS.

Full description

What this tool does

Structural Liquidity Signals shows where price likely tapped liquidity (stop clusters), then waits for structure to actually change before it prints a trigger. It spots:

Liquidity sweeps (SFPs) at recent pivots and at prior day/week highs/lows.

The latest Fair Value Gap (FVG) that often “pulls” price or serves as a reaction zone.

How far price is stretched from two VWAP anchors (one from the latest impulse, one from today’s session), scaled by ATR so it adapts to volatility.

A “percentile” extreme of an internal score. At extremes the script “arms” a setup; it only triggers after a small break of structure (BOS) on a closed bar.

Originality and design rationale, why it’s not “just a mashup”

This is not a mashup for its own sake. It’s a purpose-built flow that links where liquidity is likely to rest with how structure actually changes:

- Liquidity location: We focus on areas where stops commonly cluster—recent pivots and prior day/week highs/lows—then detect sweeps (SFPs) when price wicks beyond and closes back inside.

- Displacement context: We track the last Fair Value Gap (FVG) to account for recent inefficiency that often acts as a magnet or reaction zone.

- Stretch measurement: We anchor VWAP to the latest N-bar impulse and to the Daily session, then normalize stretch by ATR to assess dislocation consistently across assets/timeframes.

- Composite exhaustion: We combine stretch, wick skew, and volume surprise, then bend the result with a tanh transform so extremes are bounded and comparable.

- Dynamic extremes and discipline: Rather than triggering on every sweep, we “arm” at statistical extremes via percent-rank and only fire after a confirmed micro Break of Structure (BOS). This separates “interesting” from “actionable.”

Key concepts

SFP (liquidity sweep): A candle briefly trades beyond a level (where stops sit) and closes back inside. We detect these at:

Pivots (recent swing highs/lows confirmed by “left/right” bars).

Prior Day/Week High/Low (PDH/PDL/PWH/PWL).

FVG (Fair Value Gap): A small 3‑bar gap (bar2 high vs bar1 low, or vice versa). The latest gap often acts like a magnet or reaction zone. We track the most recent Up/Down gap and whether price is inside it.

AVWAP stretch: Distance from an Anchored VWAP divided by ATR (volatility). We use:

Impulse AVWAP: resets on each new N‑bar high/low.

Daily AVWAP: resets each new session.

PR (Percentile Rank): Where the current internal score sits versus its own recent history (0..100). We arm shorts at high PR, longs at low PR.

Micro BOS: A small break of the recent high (for longs) or low (for shorts). This is the “go/no‑go” confirmation.

How the parts work together

Find likely liquidity grabs (SFPs) at pivots and PD/W levels.

Add context from the latest FVG and AVWAP stretch (how far price is from “fair”).

Build a bounded score (so different markets/timeframes are comparable) and compute its percentile (PR).

Arm at extremes (high PR → short candidate; low PR → long candidate).

Only print a trigger after a micro BOS, on a closed bar, with spacing/cooldown rules.

What you see on the chart (legend)

Lines:

Teal line = Impulse AVWAP (resets on new N‑bar extreme).

Aqua line = Daily AVWAP (resets each session).

PDH/PDL/PWH/PWL = prior day/week levels (toggle on/off).

Zones:

Greenish box = latest Up FVG; Reddish box = latest Down FVG.

The shading/border changes after price trades back through it.

SFP labels:

SFP‑P = SFP at Pivot (dotted line marks that pivot’s price).

SFP‑L = SFP at Level (at PDH/PDL/PWH/PWL).

Throttle: To reduce clutter, SFPs are rate‑limited per direction.

Triggers:

Triangle up = long trigger after BOS; triangle down = short trigger after BOS.

Optional badge shows direction and PR at the moment of trigger.

Optional Trigger Zone is an ATR‑sized box around the trigger bar’s close (for visualization only).

Background:

Light green/red shading = a long/short setup is “armed” (not a trigger).

Dashboard (Mini/Pro) — what each item means

PR: Percentile of the internal score (0..100). Near 0 = bullish extreme, near 100 = bearish extreme.

Gauge: Text bar that mirrors PR.

State: Idle, Armed Long (with a countdown), or Armed Short.

Cooldown: Bars remaining before a new setup can arm after a trigger.

Bars Since / Last Px: How long since last trigger and its price.

FVG: Whether price is in the latest Up/Down FVG.

Imp/Day VWAP Dist, PD Dist(ATR): Distance from those references in ATR units.

ATR% (Gate), Trend(HTF): Status of optional regime filters (volatility/trend).

How to use it (step‑by‑step)

Keep the Safety toggles ON (default): triggers/visuals on bar‑close, optional confirmed HTF for trend slope.

Choose timeframe:

Intraday (5m–1h) or Swing (1h–4h). On very fast/thin charts, enable Performance mode and raise spacing/cooldown.

Watch the dashboard:

When PR reaches an extreme and an SFP context is present, the background shades (armed).

Wait for the trigger triangle:

It prints only after a micro BOS on a closed bar and after spacing/cooldown checks.

Use the Trigger Zone box as a visual reference only:

This script never tells you to buy/sell. Apply your own plan for entry, stop, and sizing.

Example:

Bullish: Sweep under PDL (SFP‑L) and reclaim; PR in lower tail arms long; BOS up confirms → long trigger on bar close (ATR-sized trigger zone shown).

Bearish: Sweep above PDH/pivot (SFP‑L/P) and reject; PR in upper tail arms short; BOS down confirms → short trigger on bar close (ATR-sized trigger zone shown).

Settings guide (with “when to adjust”)

Safety & Stability (defaults ON)

Confirm triggers at bar close, Draw visuals at bar close: Keep ON for clean, stable prints.

Use confirmed HTF values: Applies to HTF trend slope only; keeps it from changing until the HTF bar closes.

Performance mode: Turn ON if your chart is busy or laggy.

Core & Context

ATR Length: Bigger = smoother distances; smaller = more reactive.

Impulse AVWAP Anchor: Larger = fewer resets; smaller = resets more often.

Show Daily AVWAP: ON if you want session context.

Use last FVG in logic: ON to include FVG context in arming/score.

Show PDH/PDL/PWH/PWL: ON to see prior day/week levels that often attract sweeps.

Liquidity & Microstructure

Pivot Left/Right: Higher values = stronger/rarer pivots.

Min Wick Ratio (0..1): Higher = only more pronounced SFP wicks qualify.

BOS length: Larger = stricter BOS; smaller = quicker confirmations.

Signal persistence: Keeps SFP context alive for a few bars to avoid flicker.

Signal Gating

Percent‑Rank Lookback: Larger = more stable extremes; smaller = more reactive extremes.

Arm thresholds (qHi/qLo): Move closer to 0.5 to see more arms; move toward 0/1 to see fewer arms.

TTL, Cooldown, Min bars and Min ATR distance: Space out triggers so you’re not reacting to minor noise.

Regime Filters (optional)

ATR percentile gate: Only allow triggers when volatility is at/above a set percentile.

HTF trend gate: Only allow longs when the HTF slope is up (and shorts when it’s down), above a minimum slope.

Visuals & UX

Only show “important” SFPs: Filters pivot SFPs by Volume Z and |Impulse stretch|.

Trigger badges/history and Max badge count: Control label clutter.

Compact labels: Toggle SFP‑P/L vs full names.

Dashboard mode and position; Dark theme.

Reading PR (the built‑in “oscillator”)

PR ~ 0–10: Potential bullish extreme (long side can arm).

PR ~ 90–100: Potential bearish extreme (short side can arm).

Important: “Armed” ≠ “Enter.” A trigger still needs a micro BOS on a closed bar and spacing/cooldown to pass.

Repainting, confirmations, and HTF notes

By default, prints wait for the bar to close; this reduces repaint‑like effects.

Pivot SFPs only appear after the pivot confirms (after the chosen “right” bars).

PD/W levels come from the prior completed candles and do not change intraday.

If you enable confirmed HTF values, the HTF slope will not change until its higher‑timeframe bar completes (safer but slightly delayed).

Performance tips

If labels/zones clutter or the chart lags:

Turn ON Performance mode.

Hide FVG or the Trigger Zone.

Reduce badge history or turn badge history off.

If price scaling looks compressed:

Keep optional “score”/“PR” plots OFF (they overlay price and can affect scaling).

Alerts (neutral)

Structural Liquidity: LONG TRIGGER

Structural Liquidity: SHORT TRIGGER

These fire when a trigger condition is met on a confirmed bar (with defaults).

Limitations and risk

Not every sweep/extreme reverses; false triggers occur, especially on thin markets and low timeframes.

This indicator does not provide entries, exits, or position sizing—use your own plan and risk control.

Educational/informational only; no financial advice.

License and credits

© BullByte - MPL 2.0. Open‑source for learning and research.

Built from repeated observations of how liquidity runs, imbalance (FVG), and distance from “fair” (AVWAPs) combine, and how a small BOS often marks the moment structure actually shifts.

PumpC ATR Line LevelsPumpC ATR Line Levels

Overview

PumpC ATR Line Levels is a volatility-based indicator that projects potential expansion levels from the previous session’s close using the Average True Range (ATR). This tool builds upon the Previous OHLC framework created by Nephew_Sam_ by extending its session-handling logic and adding ATR-based levels, statistical tracking, and flexible visualization options.

How It Works

Calculates ATR from a user-selectable higher timeframe (default: Daily).

Projects levels above and below the previous session’s close (or current close when preview mode is enabled).

Supports up to 5 ATR multiples, each with independent toggles, colors, and labels.

Optionally displays only the most recent ATR session for clarity.

Includes a data table tracking how often ATR levels are reached or closed beyond.

Features

Configurable ATR timeframe and length (default: 21).

Default multiples: 0.30, 0.60, 0.90; optional: 1.236, 2.00.

Toggle for preview mode (using current close vs. locked prior session close).

Customizable line style, width, colors, and label placement.

Visibility filter to show only on chart TF ≤ 60 minutes.

Session statistics table with counts and percentages of level interactions.

Use Cases

Identify intraday expansion targets or stop placement zones based on volatility.

Evaluate historical tendencies of price respecting or breaking ATR bands.

Support volatility-adjusted trade planning with statistical validation.

Acknowledgment

This script was developed on top of the Previous OHLC indicator by Nephew_Sam_ , with major modifications to implement ATR-driven levels, extended statistics, and customizable table output.

Notes

This indicator does not generate buy/sell signals.

Best applied to intraday charts anchored to a higher-timeframe ATR.

Keep charts clean and avoid non-standard bar types when publishing.

13/48 EMA Trading Scalper (ATR TP/SL)13/48 EMA Trading Scalper (ATR TP/SL)

What it does:

This tool looks for price “touches” of the 13-EMA, only takes CALL entries when the 13 is above the 48 (uptrend) and PUT entries when the 13 is below the 48 (downtrend), and confirms with a simple candle pattern (green > red with expansion for calls, inverse for puts). Touch sensitivity is ATR-scaled, so signals adapt to volatility. Each trade gets auto-drawn entry, TP, and SL lines, colored labels with $ / % distance from entry, plus optional TP/SL hit alerts. A rotating color palette and per-bar label staggering help keep the chart readable. Old objects are auto-pruned via maxTracked.

How it works

Trend filter: 13-EMA vs 48-EMA.

Entry: ATR-scaled touch of the 13-EMA + candle confirmation.

Risk: TP/SL = ATR multiples you control.

Visuals: Entry/TP/SL lines (extend right), vertical entry marker (optional), multi-line labels.

Hygiene: maxTracked keeps only the last N trades’ objects; labels are staggered to reduce overlap.

Alerts: Buy Call, Buy Put, Take Profit Reached, Stop Loss Hit.

Key Inputs

Fast EMA (13), Trend EMA (48), ATR Length (14)

Touch Threshold (x ATR) – how close price must come to the EMA

Take Profit (x ATR), Stop Loss (x ATR)

maxTracked – number of recent trades to keep on chart

Tips

Start with Touch = 0.10–0.20 × ATR; TP=2×ATR, SL=1×ATR, then tune per symbol/timeframe.

Works on intraday and higher TFs; fewer, cleaner signals on higher TFs.

This is an indicator, not a broker—always backtest and manage risk.

Daily ATR TrackerDaily ATR Tracker

The Daily ATR Tracker is a simple yet powerful tool designed to help traders monitor the daily price movement relative to the average daily range (ATR). This indicator provides an objective view of how much price has moved compared to its recent daily volatility.

🔎 Key Features:

Customizable ATR period (default 14 days)

Live calculation of the current day's price range

ATR value displayed in pips for clear reference

Percentage of ATR covered by the current day's range

Color-coded table for quick visual interpretation:

🟢 Green: less than 60% of ATR covered

🟠 Orange: 60% to 100% of ATR covered

🔴 Red: more than 100% of ATR covered

Alert condition when daily range exceeds 100% of the ATR average

Movable table position to fit your chart layout

🎯 Why use Daily ATR Tracker?

✅ Identify exhaustion zones: When price has already covered a large portion of its typical daily range, the odds of further strong movement may diminish, helping you to manage entries, exits, and risk.

✅ Objective daily bias: Get a quantitative sense of how "stretched" the market is in real time.

✅ Works with any timeframe: While designed for daily ranges, you can monitor intraday movements with this context in mind.

⚠️ Usage Note:

This tool does not provide buy or sell signals by itself. It is designed to complement your existing strategies by offering additional context regarding daily range exhaustion.

DD ATR ReadingsThe DD ATR Readings indicator displays customizable Average True Range (ATR) multiplier values directly on your chart. Unlike standard ATR indicators that only show a line, this indicator calculates and displays the exact numeric values for three different ATR multipliers, giving you precise volatility measurements for your trading decisions.

It's specifically created for people taking the "Deep Dip Buy" stock trading course, and attempts to provide a ready-to-go solution to allow easy position size calculations as per the course, with the required ATR values visible at a glance.

The default values of 2.0, 1.5 and 0.45 are the same values used by the course instructor in his charting software, but you can change these values to any multiplier you choose.

Any input from students or the instructor is welcome to improve this indicator so it offers more value to those looking to learn how to trade.

Features

Displays three customizable ATR multiplier values (default: 2.0, 1.5, and 0.45 from the course)

Uses either SMA or EMA for ATR calculation (20-period default)

Fully customizable label appearance (position, color, size)

Real-time value updates as you move through the chart

Clean, unobtrusive display that doesn't clutter your chart with additional lines

Customization Options

ATR Length: Number of bars used in the ATR calculation (default: 20)

ATR Multipliers: Three customizable multiplier values

SMA/EMA: Choose your preferred moving average type for ATR calculation

Label Style: Multiple positioning options for the text display

Colors and Size: Fully customizable appearance

Volatility vs ATRVolatility vs ATR Indicator Description for TradingView

Volatility vs ATR is a powerful custom indicator designed to help traders analyze and compare market volatility with the Average True Range (ATR). This indicator provides valuable insights into the dynamic behavior of asset prices, enabling traders to make informed decisions about market trends, potential reversals, and risk management.

What Does It Measure?

Volatility: Represents the degree of price variation over a given period. Calculated using standard deviation or other measures, it highlights periods of heightened or reduced market activity.

Average True Range (ATR): Measures the average range of price movement over a specific period, providing a sense of the asset's price fluctuations and market activity.

How It Works

The indicator plots both Volatility and ATR on the same chart, making it easy to visualize how these metrics interact.

Rising Volatility often signals increased market uncertainty or the beginning of strong trends.

ATR Spikes typically accompany high volatility, helping identify potential breakout or breakdown scenarios.

By tracking the interplay between these metrics, traders can anticipate shifts in momentum, recognize consolidation phases, and plan trades more effectively.

Key Features

Dual-Line Display: Clearly plots both Volatility (red) and ATR (blue) for easy comparison.

Customizable Periods: Allows you to adjust the lookback period for both metrics to match your trading style.

Versatile Application: Works across all asset classes, including stocks, forex, crypto, and commodities.

Why Use Volatility vs ATR?

Trend Analysis: Identify trending vs. ranging markets by observing the relationship between Volatility and ATR.

Breakout Confirmation: Use Volatility and ATR spikes as confirmation signals for potential breakouts.

Risk Management: Plan stop-loss levels and position sizing based on ATR values.

How to Use It

Add the indicator to your chart.

Look for periods where Volatility diverges from ATR to spot potential market shifts.

Use the indicator in conjunction with price action and other technical tools for a comprehensive analysis.

This indicator is ideal for traders looking to enhance their strategies by understanding market dynamics through the lens of volatility and average price movement.

Let me know if you’d like further refinement!

2x ATR Horizontal Rays2x ATR Horizontal Rays Indicator

This script plots horizontal rays based on the 2x ATR (Average True Range) of the previous candle. It helps traders visualize key support and resistance levels by extending lines from the last candle's price, calculated with a 2x ATR multiplier. The indicator draws two lines:

Upper ATR Line: Positioned above the previous candle’s close by 2x the ATR value.

Lower ATR Line: Positioned below the previous candle’s close by 2x the ATR value.

Key Features:

Customizable ATR Length: Allows users to input their preferred ATR period to suit different market conditions.

Dynamic Horizontal Lines: The lines update with each new candle, giving traders a clear visual of volatility levels.

Extended Right Lines: The horizontal rays extend to the right, serving as potential zones for price reversals or breakouts.

This indicator is useful for traders looking to gauge market volatility and set target levels or stops based on historical price movements.

How to Use:

Add the indicator to your chart and adjust the ATR length in the settings.

Watch how the price interacts with the upper and lower ATR lines as potential zones for support, resistance, or trend continuation.

Happy trading!

Consistent ATR Trailing Stop (ATR, 1m based) [nn1]This indicator implements a Consistent ATR (Average True Range) Trailing Stop that maintains uniform behavior across various chart timeframes. It's designed to provide traders with a reliable tool for setting dynamic stop-loss levels that adapt to market volatility while remaining consistent regardless of the chosen chart interval.

Key Features:

1. Consistent ATR Calculation: The indicator calculates the ATR based on 1-minute data, regardless of the current chart timeframe. This ensures that the ATR value remains consistent across different intervals (e.g., 10s, 15s, 30s, 60s), providing a stable base for the trailing stop.

2. Dynamic Trailing Stop: The trailing stop adjusts based on the ATR, moving up in uptrends and down in downtrends to protect profits while allowing room for price fluctuations.

3. Trend Detection: The indicator determines the trend based on the price's relationship to the trailing stop, switching between long and short modes as the trend changes.

4. Visual Cues: The trailing stop line changes color to indicate the current trend (green for uptrends, red for downtrends) and briefly turns yellow during trend changes. Small circles below or above the price action further highlight the current trend direction.

5. Information Display: A label shows the current ATR value and trend direction, providing at-a-glance information to the trader.

6. Trend Change Highlights: The background briefly changes color when a trend change occurs, drawing attention to potential trading opportunities or exit points.

Usage:

- ATR Length: Set the number of periods for the ATR calculation. This is based on 1-minute data, so a value of 14 represents 14 minutes of data.

- ATR Multiplier: Adjust how far the trailing stop is placed from the price. Higher values create a wider stop, allowing for more price movement before triggering.

This indicator is particularly useful for traders who:

- Use multiple timeframes in their analysis and want consistent signals across charts.

- Seek a dynamic stop-loss method that adapts to market volatility.

- Want clear visual cues for trend direction and changes.

By providing a consistent ATR-based trailing stop across different timeframes, this indicator helps traders maintain a unified approach to their trading strategy, regardless of the chart interval they are viewing.

Anchored Chandelier ExitThe Chandelier Exit is a popular tool among traders used to help determine appropriate stop loss levels. Originally developed by Chuck LeBeau, the Chandelier Exit takes into account market volatility and adjusts the stop loss level dynamically. This indicator builds upon the original Chandelier Exit by allowing the trader to select an anchor date or starting point for the indicator to begin calculating from.

The Original Chandelier Exit

Before we get into the details of the Anchored Chandelier Exit, let's review the original. Essentially a dynamic ATR stop loss, the Chandelier Exit provides a trailing stop that moves higher or lower based on volatility.

The Chandelier Exit is calculated based on the following criteria:

🔶ATR - The ATR is used to measure the volatility of a security over a lookback period. The ATR length determines the number of bars to consider when calculating the average true range. The shorter the length, the more responsive the level will be.

🔶ATR Multiplier - The default multiplier is set to 3. This is used to determine the sensitivity of the Chandelier Exit. The higher the ATR multiplier the wider the stop levels will be. A lower multiplier will tighten stop levels.

🔶Highest / Lowest Points - Determine the highest high (bullish trade) or lowest low (bearish trade) during the lookback period. The default length is 22 bars.

Calculating the Chandelier Exit

Bullish trades - Highest High - ATR * Multiplier

Bearish trades - Lowest Low + ATR * Multiplier

The Anchored Chandelier Exit

The Anchored Chandelier Exit is a new twist on the original, allowing traders to adapt their stop loss levels based on specific market events, levels or bars.

Similar to the original, traders can select the ATR length and multiplier, however, the high or low from which the ATR is subtracted or added is first determined at the anchor bar.

As new bars form, the indicator checks for the previous high/low to be breached. If the high or low is exceeded, the highest/lowest point is updated and the Chandelier Exit is recalculated.

When the indicator is first loaded to your chart, it will ask you to select an anchor bar and choose the bias for the trade.

A bullish (long) bias trade will plot the Chandelier Exit below price action, while a bearish (short) bias trade will plot the Chandelier Exit above price action.

Indicator Features

🔶Custom Start Date

🔶Bullish or Bearish Bias

🔶Selectable ATR Length & Multiplier

🔶Custom Colors

🔶Exit With Close or Wicks

🔶Exit Alerts

With careful parameter optimization, the Anchored Chandelier Exit can be a useful tool for helping traders manage risk based on market volatility.

[tradinghook] - Renko Trend Reversal Strategy - Renko Trend Reversal Strategy

Short Title: - Renko TRS

Description: