Vertical Horizontal Filter BacktestVertical Horizontal Filter was initiated by Adam White. It was first published

in a magazine called “Issues of Futures” in August, 1991. The Vertical Horizontal

Filter (VHF) is a very common Indicator used by traders to find out the Phase of

a Price Trend. Normally, a price trend can be in a Trending Phase or a Congestion

Phase/Choppy Movement Phase. Adam White created this particular Technical Indicator

to determine whether prices are trending in a particular direction or are they going

through a transitional period. He used it to measure the range of Futures available

in the market.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Cerca negli script per "backtest"

STARC Bands Backtest A type of technical indicator that is created by plotting two bands around

a short-term simple moving average (SMA) of an underlying asset's price.

The upper band is created by adding a value of the average true range

(ATR) - a popular indicator used by technical traders - to the moving average.

The lower band is created by subtracting a value of the ATR from the SMA.

STARC is an acronym for Stoller Average Range Channels. The indicator is

named after its creator, Manning Stoller.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

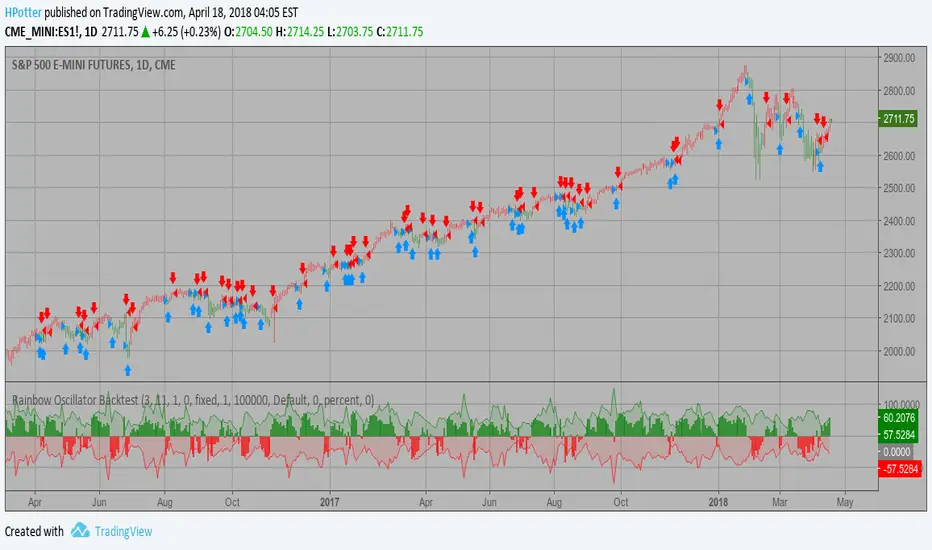

Rainbow Oscillator Backtest Ever since the people concluded that stock market price movements are not

random or chaotic, but follow specific trends that can be forecasted, they

tried to develop different tools or procedures that could help them identify

those trends. And one of those financial indicators is the Rainbow Oscillator

Indicator. The Rainbow Oscillator Indicator is relatively new, originally

introduced in 1997, and it is used to forecast the changes of trend direction.

As market prices go up and down, the oscillator appears as a direction of the

trend, but also as the safety of the market and the depth of that trend. As

the rainbow grows in width, the current trend gives signs of continuity, and

if the value of the oscillator goes beyond 80, the market becomes more and more

unstable, being prone to a sudden reversal. When prices move towards the rainbow

and the oscillator becomes more and more flat, the market tends to remain more

stable and the bandwidth decreases. Still, if the oscillator value goes below 20,

the market is again, prone to sudden reversals. The safest bandwidth value where

the market is stable is between 20 and 80, in the Rainbow Oscillator indicator value.

The depth a certain price has on a chart and into the rainbow can be used to judge

the strength of the move.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Qstick Indicator Backtest A technical indicator developed by Tushar Chande to numerically identify

trends in candlestick charting. It is calculated by taking an 'n' period

moving average of the difference between the open and closing prices. A

Qstick value greater than zero means that the majority of the last 'n' days

have been up, indicating that buying pressure has been increasing.

Transaction signals come from when the Qstick indicator crosses through the

zero line. Crossing above zero is used as the entry signal because it is indicating

that buying pressure is increasing, while sell signals come from the indicator

crossing down through zero. In addition, an 'n' period moving average of the Qstick

values can be drawn to act as a signal line. Transaction signals are then generated

when the Qstick value crosses through the trigger line.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Psychological line Backtest Psychological line (PSY), as an indicator, is the ratio of the number of

rising periods over the total number of periods. It reflects the buying

power in relation to the selling power.

If PSY is above 50%, it indicates that buyers are in control. Likewise,

if it is below 50%, it indicates the sellers are in control. If the PSY

moves along the 50% area, it indicates balance between the buyers and

sellers and therefore there is no direction movement for the market.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Prime Number Oscillator Backtest Determining market trends has become a science even though a high number or people

still believe it’s a gambling game. Mathematicians, technicians, brokers and investors

have worked together in developing quite several indicators to help them better understand

and forecast market movements.

Developed by Modulus Financial Engineering Inc., the prime number oscillator indicates the

nearest prime number, be it at the top or the bottom of the series, and outlines the

difference between that prime number and the respective series.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Prime Number Bands Backtest Determining market trends has become a science even though a high number

or people still believe it’s a gambling game. Mathematicians, technicians,

brokers and investors have worked together in developing quite several

indicators to help them better understand and forecast market movements.

The Prime Number Bands indicator was developed by Modulus Financial Engineering

Inc. This indicator is charted by indentifying the highest and lowest prime number

in the neighborhood and plotting the two series as a band.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Line Regression Intercept Backtest Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Center Of Gravity Backtest The indicator is based on moving averages. On the basis of these, the

"center" of the price is calculated, and price channels are also constructed,

which act as corridors for the asset quotations.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

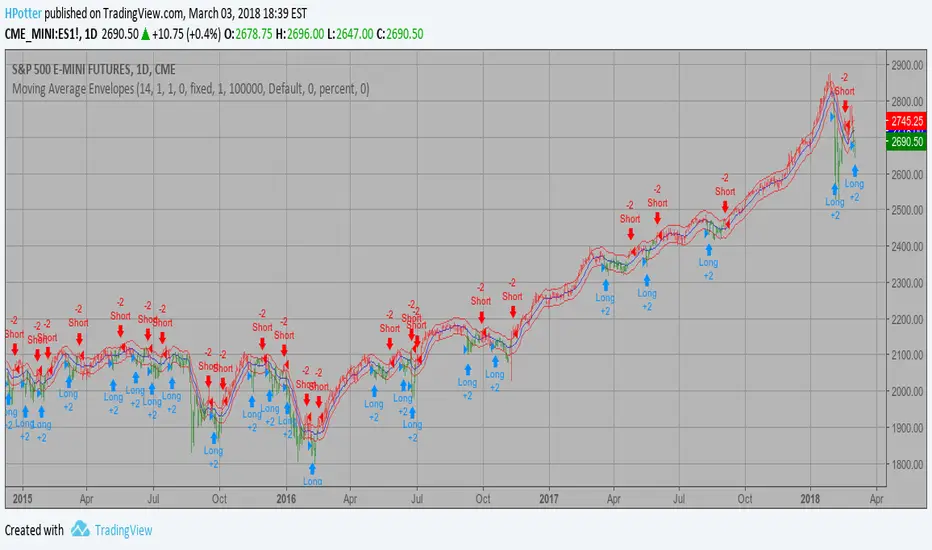

Moving Average Envelopes Backtest Moving Average Envelopes are percentage-based envelopes set above and

below a moving average. The moving average, which forms the base for

this indicator, can be a simple or exponential moving average. Each

envelope is then set the same percentage above or below the moving average.

This creates parallel bands that follow price action. With a moving average

as the base, Moving Average Envelopes can be used as a trend following indicator.

However, this indicator is not limited to just trend following. The envelopes

can also be used to identify overbought and oversold levels when the trend is

relatively flat.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

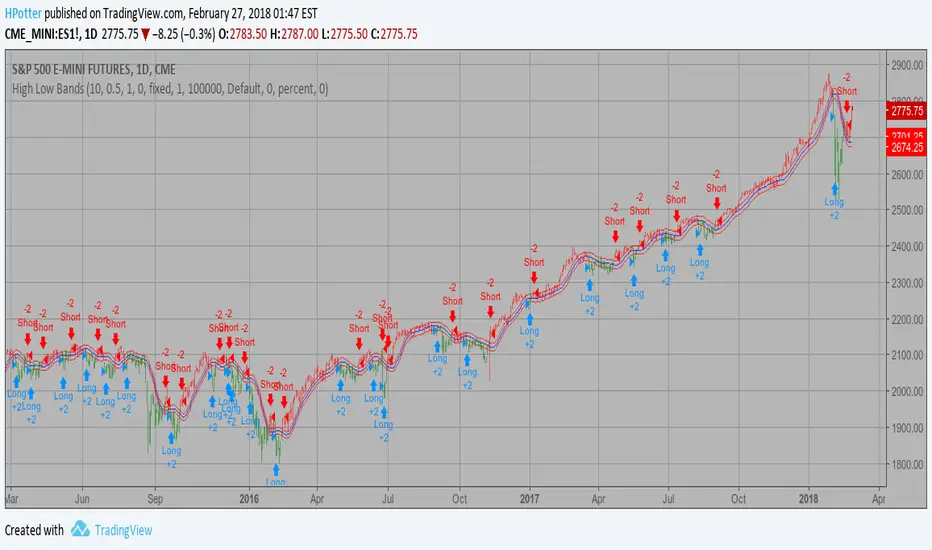

High Low Bands Backtest As the name suggests, High low bands are two bands surrounding the underlying’s

price. These bands are generated from the triangular moving averages calculated

from the underlying’s price. The triangular moving average is, in turn, shifted

up and down by a fixed percentage. The bands, thus formed, are termed as High

low bands. The main theme and concept of High low bands is based upon the triangular

moving average.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Fractal Chaos Oscillator Backtest The value of Fractal Chaos Oscillator is calculated as the difference between

the most subtle movements of the market. In general, its value moves between

-1.000 and 1.000. The higher the value of the Fractal Chaos Oscillator, the

more one can say that it follows a certain trend – an increase in prices trend,

or a decrease in prices trend.

Being an indicator expressed in a numeric value, traders say that this is an

indicator that puts a value on the trendiness of the markets. When the FCO reaches

a high value, they initiate the “buy” operation, contrarily when the FCO reaches a

low value, they signal the “sell” action. This is an excellent indicator to use in

intra-day trading.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Williams Accumulation/Distribution (Williams AD) Backtest Accumulation is a term used to describe a market controlled by buyers;

whereas distribution is defined by a market controlled by sellers.

Williams recommends trading this indicator based on divergences:

Distribution of the security is indicated when the security is making

a new high and the A/D indicator is failing to make a new high. Sell.

Accumulation of the security is indicated when the security is making

a new low and the A/D indicator is failing to make a new low. Buy.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

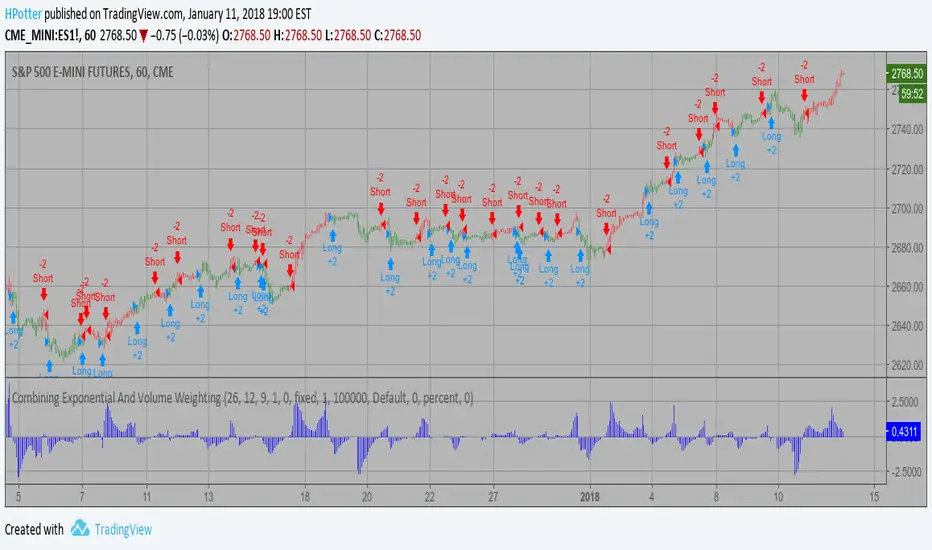

Combining Exponential And Volume Weighting Backtest The related article is copyrighted material from Stocks & Commodities 2009 Oct

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

TTM scalper indicator Backtest TTM scalper indicator of John Carter’s Scalper Buys and Sells. The methodology

is a close approximation of the one described in his book Mastering the Trade.

The book is highly recommended. Note the squares are not real-time but will

show up once the third bar has confirmed a reversal.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Trend continuation factor Backtest Trend continuation factor, by M.H. Pee

The related article is copyrighted material from Stocks & Commodities.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Trend Analysis Index Backtest In essence, it is simply the standard deviation of the last x bars of a

y-bar moving average. Thus, the TAI is a simple trend indicator when prices

trend with authority, the slope of the moving average increases, and when

prices meander in a trendless range, the slope of the moving average decreases.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

TFS: Volume Oscillator Backtest This is the second part of TFS trading strategy. The concept of this

indicator is similar to that of On-Balance Volume indicator (OBV). It

is calculated according to these rules:

If Close > Open, Volume is positive

If Close < Open, Volume is negative

If Close = Open, Volume is neutral

Then you take the 7-day MA of the results.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

TFS: Tether Line Backtest Tether line indicator is the first component of TFS trading strategy.

It was named this way because stock prices have a tendency to cluster

around it. It means that stock prices tend to move away from the midpoint

between their 50-day highs and lows, then return to that midpoint at some

time in the future. On a chart, it appears as though the stock price is

tethered to this line, and hence the name.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

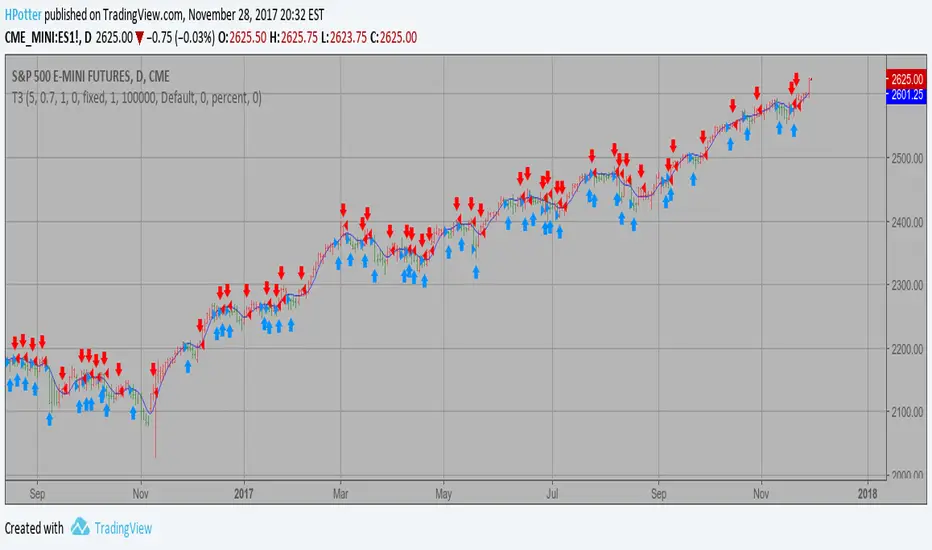

T3 Averages Backtest This indicator plots the moving average described in the January, 1998 issue

of S&C, p.57, "Smoothing Techniques for More Accurate Signals", by Tim Tillson.

This indicator plots T3 moving average presented in Figure 4 in the article.

T3 indicator is a moving average which is calculated according to formula:

T3(n) = GD(GD(GD(n))),

where GD - generalized DEMA (Double EMA) and calculating according to this:

GD(n,v) = EMA(n) * (1+v)-EMA(EMA(n)) * v,

where "v" is volume factor, which determines how hot the moving average’s response

to linear trends will be. The author advises to use v=0.7.

When v = 0, GD = EMA, and when v = 1, GD = DEMA. In between, GD is a less aggressive

version of DEMA. By using a value for v less than1, trader cure the multiple DEMA

overshoot problem but at the cost of accepting some additional phase delay.

In filter theory terminology, T3 is a six-pole nonlinear Kalman filter. Kalman

filters are ones that use the error — in this case, (time series - EMA(n)) —

to correct themselves. In the realm of technical analysis, these are called adaptive

moving averages; they track the time series more aggres-sively when it is making large

moves. Tim Tillson is a software project manager at Hewlett-Packard, with degrees in

mathematics and computer science. He has privately traded options and equities for 15 years.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

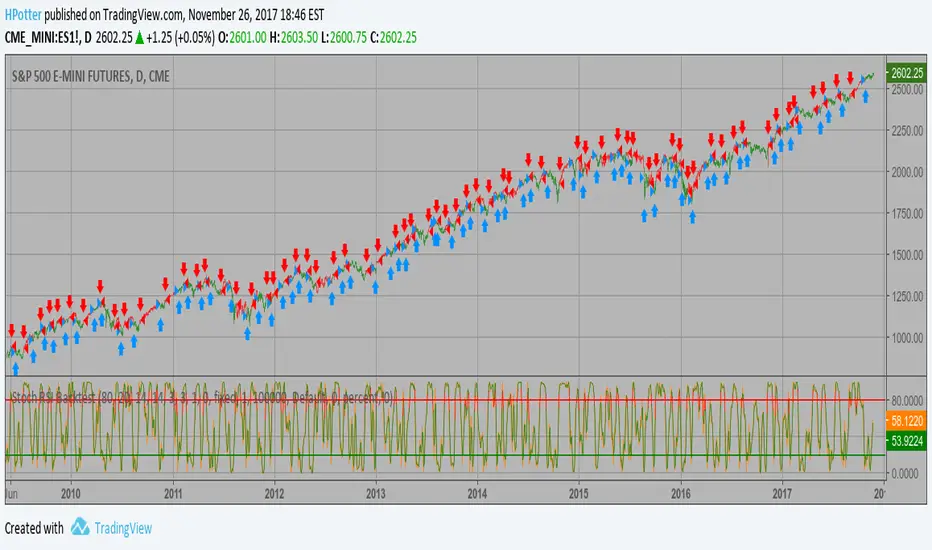

Stochastic RSI Backtest This strategy used to calculate the Stochastic RSI

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Statistical Volatility - Extreme Value Method Backtest This indicator used to calculate the statistical volatility, sometime

called historical volatility, based on the Extreme Value Method.

Please use this link to get more information about Volatility.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Smoothed RSI Backtest ver.2 This is new version of RSI oscillator indicator, developed by John Ehlers.

The main advantage of his way of enhancing the RSI indicator is smoothing

with minimum of lag penalty.

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.