ATH대비 지정하락률에 도착 시 매수 - 장기홀딩 선물 전략(ATH Drawdown Re-Buy Long Only)본 스크립트는 과거 하락 데이터를 이용하여, 정해진 하락 %가 발생하는 경우 자기 자본의 정해진 %만큼을 진입하게 설계되어진 스트레티지입니다.

레버리지를 사용할 수 있으며 기본적으로 셋팅해둔 값이 내장되어있습니다.(자유롭게 바꿔서 쓰시면 됩니다.) 추가적으로 2번의 진입 외에도 다른 진입 기준, 진입 %를 설정하실 수 있으며 - ChatGPT에게 요청하면 수정해줄 것입니다.

실제 사용용도로는 KillSwitch 기능을 꺼주세요. 바 돋보기 기능을 켜주세요.

ATH Drawdown Re-Buy Long Only 전략 설명

1. 전략 개요

ATH Drawdown Re-Buy Long Only 전략은 자산의 역대 최고가(ATH, All-Time High)를 기준으로 한 하락폭(드로우다운)을 활용하여,

특정 구간마다 단계적으로 롱 포지션을 구축하는 자동 재매수(Long Only) 전략입니다.

본 전략은 다음과 같은 목적을 가지고 설계되었습니다.

급격한 조정 구간에서 체계적인 분할 매수 및 레버리지 활용

ATH를 기준으로 한 명확한 진입 규칙 제공

실시간으로

평단가

레버리지

청산가 추정

계좌 MDD

수익률

등을 시각적으로 제공하여 리스크와 포지션 상태를 직관적으로 확인할 수 있도록 지원

※ 본 전략은 교육·연구·백테스트 용도로 제공되며,

어떠한 형태의 투자 권유 또는 수익을 보장하지 않습니다.

2. 전략의 핵심 개념

2-1. ATH(역대 최고가) 기준 드로우다운

전략은 차트 상에서 항상 가장 높은 고가(High)를 ATH로 기록합니다.

새로운 고점이 형성될 때마다 ATH를 갱신하고, 해당 ATH를 기준으로 다음을 계산합니다.

현재 바의 저가(Low)가 ATH에서 몇 % 하락했는지

현재 바의 종가(Close)가 ATH에서 몇 % 하락했는지

그리고 사전에 설정한 두 개의 드로우다운 구간에서 매수를 수행합니다.

1차 진입 구간: ATH 대비 X% 하락 시

2차 진입 구간: ATH 대비 Y% 하락 시

각 구간은 ATH가 새로 갱신될 때마다 한 번씩만 작동하며,

새로운 ATH가 생성되면 다시 “1차 / 2차 진입 가능 상태”로 초기화됩니다.

2-2. 첫 포지션 100% / 300% 특수 규칙

이 전략의 중요한 특징은 **“첫 포지션 진입 시의 예외 규칙”**입니다.

전략이 현재 어떠한 포지션도 들고 있지 않은 상태에서

최초로 롱 포지션을 진입하는 시점(첫 포지션)에 대해:

기본적으로는 **자산의 100%**를 기준으로 포지션을 구축하지만,

만약 그 순간의 가격이 ATH 대비 설정값 이상(예: 약 –72.5% 이상 하락한 상황) 이라면

→ 자산의 300% 규모로 첫 포지션을 진입하도록 설계되어 있습니다.

이 규칙은 다음과 같이 동작합니다.

첫 진입이 1차 드로우다운 구간에서 발생하든,

첫 진입이 2차 드로우다운 구간에서 발생하든,

현재 하락폭이 설정된 기준 이상(예: –72.5% 이상) 이라면

→ “이 정도 하락이면 첫 진입부터 더 공격적으로 들어간다”는 의미로 300% 규모로 진입

그 이하의 하락폭이라면

→ 첫 진입은 100% 규모로 제한

즉, 전략은 다음 두 가지 모드로 동작합니다.

일반적인 상황의 첫 진입: 자산의 100%

심각한 드로우다운 구간에서의 첫 진입: 자산의 300%

이 특수 규칙은 깊은 하락에서는 공격적으로, 평소에는 상대적으로 보수적으로 진입하도록 설계된 것입니다.

3. 전략 동작 구조

3-1. 매수 조건

차트 상 High 기준으로 ATH를 추적합니다.

각 바마다 해당 ATH에서의 하락률을 계산합니다.

사용자가 설정한 두 개의 드로우다운 구간(예시):

1차 구간: 예를 들어 ATH – 50%

2차 구간: 예를 들어 ATH – 72.5%

각 구간에 대해 다음과 같은 조건을 확인합니다.

“이번 ATH 구간에서 아직 해당 구간 매수를 한 적이 없는 상태”이고,

현재 바의 저가(Low)가 해당 구간 가격 이하를 찍는 순간

→ 해당 바에서 매수 조건 충족으로 간주

실제 주문은:

해당 구간 가격에 맞춰 롱 포지션 진입(리밋/시장가 기반 시뮬레이션) 으로 처리됩니다.

3-2. ATH 갱신과 진입 기회 리셋

차트 상에서 새로운 고점(High)이 기존 ATH를 넘어서는 순간,

ATH가 갱신되고,

1차 / 2차 진입 여부를 나타내는 내부 플래그가 초기화됩니다.

이를 통해, 시장이 새로운 고점을 돌파해 나갈 때마다,

해당 구간에서 다시 한 번씩 1차·2차 드로우다운 진입 기회를 갖게 됩니다.

4. 포지션 사이징 및 레버리지

4-1. 계좌 자산(Equity) 기준 포지션 크기 결정

전략은 현재 계좌 자산을 다음과 같이 정의하여 사용합니다.

현재 자산 = 초기 자본 + 실현 손익 + 미실현 손익

각 진입 구간에서의 포지션 가치는 다음과 같이 결정됩니다.

1차 진입 구간:

“자산의 몇 %를 사용할지”를 설정값으로 입력

설정된 퍼센트를 계좌 자산에 곱한 뒤,

다시 전략 내 레버리지 배수(Leverage) 를 곱하여 실제 포지션 가치를 계산

2차 진입 구간:

동일한 방식으로, 독립된 퍼센트 설정값을 사용

즉, 포지션 가치는 다음과 같이 계산됩니다.

포지션 가치 = 현재 자산 × (해당 구간 설정 % / 100) × 레버리지 배수

그리고 이를 해당 구간의 진입 가격으로 나누어 실제 수량(토큰 단위) 를 산출합니다.

4-2. 첫 포지션의 예외 처리 (100% / 300%)

첫 포지션에 대해서는 위의 일반적인 퍼센트 설정 대신,

다음과 같은 고정 비율이 사용됩니다.

기본: 자산의 100% 규모로 첫 포지션 진입

단, 진입 시점의 ATH 대비 하락률이 설정값 이상(예: –72.5% 이상) 일 경우

→ 자산의 300% 규모로 첫 포지션 진입

이때 역시 다음 공식을 사용합니다.

포지션 가치 = 현재 자산 × (100% 또는 300%) × 레버리지

그리고 이를 가격으로 나누어 실제 진입 수량을 계산합니다.

이 규칙은:

첫 진입이 1차 구간이든 2차 구간이든 동일하게 적용되며,

“충분히 깊은 하락 구간에서는 첫 진입부터 더 크게,

평소에는 비교적 보수적으로” 라는 운용 철학을 반영합니다.

4-3. 실레버리지(Real Leverage)의 추적

전략은 각 바 단위로 다음을 추적합니다.

바가 시작할 때의 기존 포지션 크기

해당 바에서 새로 진입한 수량

이를 바탕으로, 진입이 발생한 시점에 다음을 계산합니다.

실제 레버리지 = (포지션 가치 / 현재 자산)

그리고 차트 상에 예를 들어:

Lev 2.53x 와 같은 형식의 레이블로 표시합니다.

이를 통해, 매수 시점마다 실제 계좌 레버리지가 어느 정도였는지를 직관적으로 확인할 수 있습니다.

5. 시각화 및 모니터링 요소

5-1. 차트 상 시각 요소

전략은 차트 위에 다음과 같은 정보를 직접 표시합니다.

ATH 라인

High 기준으로 계산된 역대 최고가를 주황색 선으로 표시

평단가(평균 진입가) 라인

현재 보유 포지션이 있을 때,

해당 포지션의 평균 진입가를 노란색 선으로 표시

추정 청산가(고정형 청산가) 라인

포지션 수량이 변화하는 시점을 감지하여,

당시의 평단가와 실제 레버리지를 이용해 근사적인 청산가를 계산

이를 빨간색 선으로 차트에 고정 표시

포지션이 없거나 레버리지가 1배 이하인 경우에는 청산가 라인을 제거

매수 마커 및 레이블

1차/2차 매수 조건이 충족될 때마다 해당 지점에 매수 마커를 표시

"Buy XX% @ 가격", "Lev XXx" 형태의 라벨로

진입 비율과 당시 레버리지를 함께 시각화

레이블의 위치는 설정에서 선택 가능:

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

5-2. 우측 상단 정보 테이블

차트 우측 상단에는 현재 계좌·포지션 상태를 요약한 정보 테이블이 표시됩니다.

대표적으로 다음 항목들이 포함됩니다.

Pos Qty (Token)

현재 보유 중인 포지션 수량(토큰 기준, 절대값 기준)

Pos Value (USDT)

현재 포지션의 시장 가치 (수량 × 현재 가격)

Leverage (Now)

현재 실레버리지 (포지션 가치 / 현재 자산)

DD from ATH (%)

현재 가격 기준, 최근 ATH에서의 하락률(%)

Avg Entry

현재 포지션의 평균 진입 가격

PnL (%)

현재 포지션 기준 미실현 손익률(%)

Max DD (Equity %)

전략 전체 기간 동안 기록된 계좌 기준 최대 손실(MDD, Max Drawdown)

Last Entry Price

가장 최근에 포지션을 추가로 진입한 직후의 평균 진입 가격

Last Entry Lev

위 “Last Entry Price” 시점에서의 실레버리지

Liq Price (Fixed)

위에서 설명한 고정형 추정 청산가

Return from Start (%)

전략 시작 시점(초기 자본) 대비 현재 계좌 자산의 총 수익률(%)

이 테이블을 통해 사용자는:

현재 계좌와 포지션의 상태

리스크 수준

누적 성과

를 직관적으로 파악할 수 있습니다.

6. 시간 필터 및 라벨 옵션

6-1. 전략 동작 기간 설정

전략은 옵션으로 특정 기간에만 전략을 동작시키는 시간 필터를 제공합니다.

“Use Date Range” 옵션을 활성화하면:

시작 시각과 종료 시각을 지정하여

해당 구간에 한해서만 매매가 발생하도록 제한

옵션을 비활성화하면:

전략은 전체 차트 구간에서 자유롭게 동작

6-2. 진입 라벨 위치 설정

사용자는 매수/레버리지 라벨의 위치를 선택할 수 있습니다.

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

이를 통해 개인 취향 및 차트 가독성에 맞추어

시각화 방식을 유연하게 조정할 수 있습니다.

7. 활용 대상 및 사용 예시

본 전략은 다음과 같은 목적에 적합합니다.

현물 또는 선물 롱 포지션 기준 장기·스윙 관점 추매 전략 백테스트

“고점 대비 하락률”을 기준으로 한 규칙 기반 운용 아이디어 검증

레버리지 사용 시

계좌 레버리지·청산가·MDD를 동시에 모니터링하고자 하는 경우

특정 자산에 대해

“새로운 고점이 형성될 때마다

일정한 규칙으로 깊은 조정 구간에서만 분할 진입하고자 할 때”

실거래에 그대로 적용하기보다는,

전략 아이디어 검증 및 리스크 프로파일 분석,

자신의 성향에 맞는 파라미터 탐색 용도로 사용하는 것을 권장합니다.

8. 한계 및 유의사항

백테스트 결과는 미래 성과를 보장하지 않습니다.

과거 데이터에 기반한 시뮬레이션일 뿐이며,

실제 시장에서는

유동성

슬리피지

수수료 체계

강제청산 규칙

등 다양한 변수가 존재합니다.

청산가는 단순화된 공식에 따른 추정치입니다.

거래소별 실제 청산 규칙, 유지 증거금, 수수료, 펀딩비 등은

본 전략의 계산과 다를 수 있으며,

청산가 추정 라인은 참고용 지표일 뿐입니다.

레버리지 및 진입 비율 설정에 따라 손실 폭이 매우 커질 수 있습니다.

특히 **“첫 포지션 300% 진입”**과 같이 매우 공격적인 설정은

시장 급락 시 계좌 손실과 청산 리스크를 크게 증가시킬 수 있으므로

신중한 검토가 필요합니다.

실거래 연동 시에는 별도의 리스크 관리가 필수입니다.

개별 손절 기준

포지션 상한선

전체 포트폴리오 내 비중 관리 등

본 전략 외부에서 추가적인 안전장치가 필요합니다.

9. 결론

ATH Drawdown Re-Buy Long Only 전략은 단순한 “저가 매수”를 넘어서,

ATH 기준으로 드로우다운을 구조적으로 활용하고,

첫 포지션에 대한 **특수 규칙(100% / 300%)**을 적용하며,

레버리지·청산가·MDD·수익률을 통합적으로 시각화함으로써,

하락 구간에서의 규칙 기반 롱 포지션 구축과

리스크 모니터링을 동시에 지원하는 전략입니다.

사용자는 본 전략을 통해:

자신의 시장 관점과 리스크 허용 범위에 맞는

드로우다운 구간

진입 비율

레버리지 설정

다양한 시나리오에 대한 백테스트와 분석

을 수행할 수 있습니다.

다시 한 번 강조하지만,

본 전략은 연구·학습·백테스트를 위한 도구이며,

실제 투자 판단과 책임은 전적으로 사용자 본인에게 있습니다.

/ENG Version.

This script is designed to use historical drawdown data and automatically enter positions when a predefined percentage drop from the all-time high occurs, using a predefined percentage of your account equity.

You can use leverage, and default parameter values are provided out of the box (you can freely change them to suit your style).

In addition to the two main entry levels, you can add more entry conditions and custom entry percentages – just ask ChatGPT to modify the script.

For actual/live usage, please turn OFF the KillSwitch function and turn ON the Bar Magnifier feature.

ATH Drawdown Re-Buy Long Only Strategy

1. Strategy Overview

The ATH Drawdown Re-Buy Long Only strategy is an automatic re-buy (Long Only) system that builds long positions step-by-step at specific drawdown levels, based on the asset’s all-time high (ATH) and its subsequent drawdown.

This strategy is designed with the following goals:

Systematic scaled buying and leverage usage during sharp correction periods

Clear, rule-based entry logic using drawdowns from ATH

Real-time visualization of:

Average entry price

Leverage

Estimated liquidation price

Account MDD (Max Drawdown)

Return / performance

This allows traders to intuitively monitor both risk and position status.

※ This strategy is provided for educational, research, and backtesting purposes only.

It does not constitute investment advice and does not guarantee any profits.

2. Core Concepts

2-1. Drawdown from ATH (All-Time High)

On the chart, the strategy always tracks the highest high as the ATH.

Whenever a new high is made, ATH is updated, and based on that ATH the following are calculated:

How many percent the current bar’s Low is below the ATH

How many percent the current bar’s Close is below the ATH

Using these, the strategy executes buys at two predefined drawdown zones:

1st entry zone: When price drops X% from ATH

2nd entry zone: When price drops Y% from ATH

Each zone is allowed to trigger only once per ATH cycle.

When a new ATH is created, the “1st / 2nd entry possible” flags are reset, and new opportunities open up for that ATH leg.

2-2. Special Rule for the First Position (100% / 300%)

A key feature of this strategy is the special rule for the very first position.

When the strategy currently holds no position and is about to open the first long position:

Under normal conditions, it builds the position using 100% of account equity.

However, if at that moment the price has dropped by at least a predefined threshold from ATH (e.g. around –72.5% or more),

→ the strategy will open the first position using 300% of account equity.

This rule works as follows:

Whether the first entry happens at the 1st drawdown zone or at the 2nd drawdown zone,

If the current drawdown from ATH is at or below the threshold (e.g. –72.5% or worse),

→ the strategy interprets this as “a sufficiently deep crash” and opens the initial position with 300% of equity.

If the drawdown is less severe than the threshold,

→ the first entry is capped at 100% of equity.

So the strategy has two modes for the first entry:

Normal market conditions: 100% of equity

Deep drawdown conditions: 300% of equity

This special rule is intended to be aggressive in extremely deep crashes while staying more conservative in normal corrections.

3. Strategy Logic & Execution

3-1. Entry Conditions

The strategy tracks the ATH using the High price.

For each bar, it calculates the drawdown from ATH.

The user defines two drawdown zones, for example:

1st zone: ATH – 50%

2nd zone: ATH – 72.5%

For each zone, the strategy checks:

If no buy has been executed yet for that zone in the current ATH leg, and

If the current bar’s Low touches or falls below that zone’s price level,

→ That bar is considered to have triggered a buy condition.

Order simulation:

The strategy simulates entering a long position at that zone’s price level

(using a limit/market-like approximation for backtesting).

3-2. ATH Reset & Entry Opportunity Reset

When a new High goes above the previous ATH:

The ATH is updated to this new high.

Internal flags that track whether the 1st and 2nd entries have been used are reset.

This means:

Each time the market makes a new ATH,

The strategy once again has a fresh opportunity to execute 1st and 2nd drawdown entries for that new ATH leg.

4. Position Sizing & Leverage

4-1. Position Size Based on Account Equity

The strategy defines current equity as:

Current Equity = Initial Capital + Realized PnL + Unrealized PnL

For each entry zone, the position value is calculated as follows:

The user inputs:

“What % of equity to use at this zone”

The strategy:

Multiplies current equity by that percentage

Then multiplies by the strategy’s leverage factor

Thus:

Position Value = Current Equity × (Zone % / 100) × Leverage

Finally, this position value is divided by the entry price to determine the actual position size in tokens.

4-2. Exception for the First Position (100% / 300%)

For the very first position (when there is no open position),

the strategy does not use the zone % parameters. Instead, it uses fixed ratios:

Default: Enter the first position with 100% of equity.

If the drawdown from ATH at that moment is greater than or equal to a predefined threshold (e.g. –72.5% or more)

→ Enter the first position with 300% of equity.

The position value is computed as:

Position Value = Current Equity × (100% or 300%) × Leverage

Then it is divided by the entry price to obtain the token quantity.

This rule:

Applies regardless of whether the first entry occurs at the 1st zone or 2nd zone.

Embeds the philosophy:

“In very deep crashes, go much larger on the first entry; otherwise, stay more conservative.”

4-3. Tracking Real Leverage

On each bar, the strategy tracks:

The existing position size at the start of the bar

The newly added size (if any) on that bar

When a new entry occurs, it calculates the real leverage at that moment:

Real Leverage = (Position Value / Current Equity)

This is then displayed on the chart as a label, for example:

Lev 2.53x

This makes it easy to see the actual leverage level at each entry point.

5. Visualization & Monitoring

5-1. On-Chart Visual Elements

The strategy plots the following directly on the chart:

ATH Line

The all-time high (based on High) is plotted as an orange line.

Average Entry Price Line

When a position is open, the average entry price of that position is plotted as a yellow line.

Estimated Liquidation Price (Fixed) Line

The strategy detects when the position size changes.

At each size change, it uses the current average entry price and real leverage to compute an approximate liquidation price.

This “fixed liquidation price” is then plotted as a red line on the chart.

If there is no position, or if leverage is 1x or lower, the liquidation line is removed.

Entry Markers & Labels

When 1st/2nd entry conditions are met, the strategy:

Marks the entry point on the chart.

Displays labels such as "Buy XX% @ Price" and "Lev XXx",

showing both entry percentage and real leverage at that time.

The label placement is configurable:

Below Bar

Above Bar

At Price

5-2. Information Table (Top-Right Panel)

In the top-right corner of the chart, the strategy displays a summary table of the current account and position status. It typically includes:

Pos Qty (Token)

Absolute size of the current position (in tokens)

Pos Value (USDT)

Market value of the current position (qty × current price)

Leverage (Now)

Current real leverage (position value / current equity)

DD from ATH (%)

Current drawdown (%) from the latest ATH, based on current price

Avg Entry

Average entry price of the current position

PnL (%)

Unrealized profit/loss (%) of the current position

Max DD (Equity %)

The maximum equity drawdown (MDD) recorded over the entire backtest period

Last Entry Price

Average entry price immediately after the most recent add-on entry

Last Entry Lev

Real leverage at the time of the most recent entry

Liq Price (Fixed)

The fixed estimated liquidation price described above

Return from Start (%)

Total return (%) of equity compared to the initial capital

Through this table, users can quickly grasp:

Current account and position status

Current risk level

Cumulative performance

6. Time Filters & Label Options

6-1. Strategy Date Range Filter

The strategy provides an option to restrict trading to a specific time range.

When “Use Date Range” is enabled:

You can specify start and end timestamps.

The strategy will only execute trades within that range.

When this option is disabled:

The strategy operates over the entire chart history.

6-2. Entry Label Placement

Users can customize where entry/leverage labels are drawn:

Below Bar (Below Bar)

Above Bar (Above Bar)

At the actual price level (At Price)

This allows you to adjust visualization according to personal preference and chart readability.

7. Use Cases & Applications

This strategy is suitable for the following purposes:

Long-term / swing-style re-buy strategies for spot or futures long positions

Testing rule-based strategies that rely on “drawdown from ATH” as a main signal

Monitoring account leverage, liquidation price, and MDD when using leverage

Handling situations where, for a given asset:

“Every time a new ATH is formed,

you want to wait for deep corrections and enter only at specific drawdown zones”

It is generally recommended to use this strategy not as a direct plug-and-play live system, but as a tool for:

Strategy idea validation

Risk profile analysis

Parameter exploration to match your personal risk tolerance and style

8. Limitations & Warnings

Backtest results do not guarantee future performance.

They are based on historical data only.

In live markets, additional factors exist:

Liquidity

Slippage

Fee structures

Exchange-specific liquidation rules

Funding fees, etc.

The liquidation price is only an approximate estimate, derived from a simplified formula.

Actual liquidation rules, maintenance margin requirements, fees, and other details differ by exchange.

The liquidation line should be treated as a reference indicator, not an exact guarantee.

Depending on the configured leverage and entry percentages, losses can be very large.

In particular, extremely aggressive settings such as “first position 300% of equity” can greatly increase the risk of large account drawdowns and liquidation during sharp market crashes.

Use such settings with extreme caution.

For live trading, additional risk management is essential:

Your own stop-loss rules

Maximum position size limits

Portfolio-level exposure controls

And other external safety mechanisms beyond this strategy

9. Conclusion

The ATH Drawdown Re-Buy Long Only strategy goes beyond simple “buy the dip” logic. It:

Systematically utilizes drawdowns from ATH as a structural signal

Applies a special first-position rule (100% / 300%)

Integrates visualization of leverage, liquidation price, MDD, and returns

All of this supports rule-based long position building in drawdown phases and comprehensive risk monitoring.

With this strategy, users can:

Explore different:

Drawdown zones

Entry percentages

Leverage levels

Run various backtests and scenario analyses

Better understand the risk/return profile that fits their own market view and risk tolerance

Once again, this strategy is intended for research, learning, and backtesting only.

All real trading decisions and their consequences are solely the responsibility of the user.

Cerca negli script per "backtest"

Bober XM v2.0# ₿ober XM v2.0 Trading Bot Documentation

**Developer's Note**: While our previous Bot 1.3.1 was removed due to guideline violations, this setback only fueled our determination to create something even better. Rising from this challenge, Bober XM 2.0 emerges not just as an update, but as a complete reimagining with multi-timeframe analysis, enhanced filters, and superior adaptability. This adversity pushed us to innovate further and deliver a strategy that's smarter, more agile, and more powerful than ever before. Challenges create opportunity - welcome to Cryptobeat's finest work yet.

## !!!!You need to tune it for your own pair and timeframe and retune it periodicaly!!!!!

## Overview

The ₿ober XM v2.0 is an advanced dual-channel trading bot with multi-timeframe analysis capabilities. It integrates multiple technical indicators, customizable risk management, and advanced order execution via webhook for automated trading. The bot's distinctive feature is its separate channel systems for long and short positions, allowing for asymmetric trade strategies that adapt to different market conditions across multiple timeframes.

### Key Features

- **Multi-Timeframe Analysis**: Analyze price data across multiple timeframes simultaneously

- **Dual Channel System**: Separate parameter sets for long and short positions

- **Advanced Entry Filters**: RSI, Volatility, Volume, Bollinger Bands, and KEMAD filters

- **Machine Learning Moving Average**: Adaptive prediction-based channels

- **Multiple Entry Strategies**: Breakout, Pullback, and Mean Reversion modes

- **Risk Management**: Customizable stop-loss, take-profit, and trailing stop settings

- **Webhook Integration**: Compatible with external trading bots and platforms

### Strategy Components

| Component | Description |

|---------|-------------|

| **Dual Channel Trading** | Uses either Keltner Channels or Machine Learning Moving Average (MLMA) with separate settings for long and short positions |

| **MLMA Implementation** | Machine learning algorithm that predicts future price movements and creates adaptive bands |

| **Pivot Point SuperTrend** | Trend identification and confirmation system based on pivot points |

| **Three Entry Strategies** | Choose between Breakout, Pullback, or Mean Reversion approaches |

| **Advanced Filter System** | Multiple customizable filters with multi-timeframe support to avoid false signals |

| **Custom Exit Logic** | Exits based on OBV crossover of its moving average combined with pivot trend changes |

### Note for Novice Users

This is a fully featured real trading bot and can be tweaked for any ticker — SOL is just an example. It follows this structure:

1. **Indicator** – gives the initial signal

2. **Entry strategy** – decides when to open a trade

3. **Exit strategy** – defines when to close it

4. **Trend confirmation** – ensures the trade follows the market direction

5. **Filters** – cuts out noise and avoids weak setups

6. **Risk management** – controls losses and protects your capital

To tune it for a different pair, you'll need to start from scratch:

1. Select the timeframe (candle size)

2. Turn off all filters and trend entry/exit confirmations

3. Choose a channel type, channel source and entry strategy

4. Adjust risk parameters

5. Tune long and short settings for the channel

6. Fine-tune the Pivot Point Supertrend and Main Exit condition OBV

This will generate a lot of signals and activity on the chart. Your next task is to find the right combination of filters and settings to reduce noise and tune it for profitability.

### Default Strategy values

Default values are tuned for: Symbol BITGET:SOLUSDT.P 5min candle

Filters are off by default: Try to play with it to understand how it works

## Configuration Guide

### General Settings

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Long Positions** | Enable or disable long trades | Enabled |

| **Short Positions** | Enable or disable short trades | Enabled |

| **Risk/Reward Area** | Visual display of stop-loss and take-profit zones | Enabled |

| **Long Entry Source** | Price data used for long entry signals | hl2 (High+Low/2) |

| **Short Entry Source** | Price data used for short entry signals | hl2 (High+Low/2) |

The bot allows you to trade long positions, short positions, or both simultaneously. Each direction has its own set of parameters, allowing for fine-tuned strategies that recognize the asymmetric nature of market movements.

### Multi-Timeframe Settings

1. **Enable Multi-Timeframe Analysis**: Toggle 'Enable Multi-Timeframe Analysis' in the Multi-Timeframe Settings section

2. **Configure Timeframes**: Set appropriate higher timeframes based on your trading style:

- Timeframe 1: Default is now 15 minutes (intraday confirmation)

- Timeframe 2: Default is 4 hours (trend direction)

3. **Select Sources per Indicator**: For each indicator (RSI, KEMAD, Volume, etc.), choose:

- The desired timeframe (current, mtf1, or mtf2)

- The appropriate price type (open, high, low, close, hl2, hlc3, ohlc4)

### Entry Strategies

- **Breakout**: Enter when price breaks above/below the channel

- **Pullback**: Enter when price pulls back to the channel

- **Mean Reversion**: Enter when price is extended from the channel

You can enable different strategies for long and short positions.

### Core Components

### Risk Management

- **Position Size**: Control risk with percentage-based position sizing

- **Stop Loss Options**:

- Fixed: Set a specific price or percentage from entry

- ATR-based: Dynamic stop-loss based on market volatility

- Swing: Uses recent swing high/low points

- **Take Profit**: Multiple targets with percentage allocation

- **Trailing Stop**: Dynamic stop that follows price movement

## Advanced Usage Strategies

### Moving Average Type Selection Guide

- **SMA**: More stable in choppy markets, good for higher timeframes

- **EMA/WMA**: More responsive to recent price changes, better for entry signals

- **VWMA**: Adds volume weighting for stronger trends, use with Volume filter

- **HMA**: Balance between responsiveness and noise reduction, good for volatile markets

### Multi-Timeframe Strategy Approaches

- **Trend Confirmation**: Use higher timeframe RSI (mtf2) for overall trend, current timeframe for entries

- **Entry Precision**: Use KEMAD on current timeframe with volume filter on mtf1

- **False Signal Reduction**: Apply RSI filter on mtf1 with strict KEMAD settings

### Market Condition Optimization

| Market Condition | Recommended Settings |

|------------------|----------------------|

| **Trending** | Use Breakout strategy with KEMAD filter on higher timeframe |

| **Ranging** | Use Mean Reversion with strict RSI filter (mtf1) |

| **Volatile** | Increase ATR multipliers, use HMA for moving averages |

| **Low Volatility** | Decrease noise parameters, use pullback strategy |

## Webhook Integration

The strategy features a professional webhook system that allows direct connectivity to your exchange or trading platform of choice through third-party services like 3commas, Alertatron, or Autoview.

The webhook payload includes all necessary parameters for automated execution:

- Entry price and direction

- Stop loss and take profit levels

- Position size

- Custom identifier for webhook routing

## Performance Optimization Tips

1. **Start with Defaults**: Begin with the default settings for your timeframe before customizing

2. **Adjust One Component at a Time**: Make incremental changes and test the impact

3. **Match MA Types to Market Conditions**: Use appropriate moving average types based on the Market Condition Optimization table

4. **Timeframe Synergy**: Create logical relationships between timeframes (e.g., 5min chart with 15min and 4h higher timeframes)

5. **Periodic Retuning**: Markets evolve - regularly review and adjust parameters

## Common Setups

### Crypto Trend-Following

- MLMA with EMA or HMA

- Higher RSI thresholds (75/25)

- KEMAD filter on mtf1

- Breakout entry strategy

### Stock Swing Trading

- MLMA with SMA for stability

- Volume filter with higher threshold

- KEMAD with increased filter order

- Pullback entry strategy

### Forex Scalping

- MLMA with WMA and lower noise parameter

- RSI filter on current timeframe

- Use highest timeframe for trend direction only

- Mean Reversion strategy

## Webhook Configuration

- **Benefits**:

- Automated trade execution without manual intervention

- Immediate response to market conditions

- Consistent execution of your strategy

- **Implementation Notes**:

- Requires proper webhook configuration on your exchange or platform

- Test thoroughly with small position sizes before full deployment

- Consider latency between signal generation and execution

### Backtesting Period

Define a specific historical period to evaluate the bot's performance:

| Setting | Description | Default Value |

|---------|-------------|---------------|

| **Start Date** | Beginning of backtest period | January 1, 2025 |

| **End Date** | End of backtest period | December 31, 2026 |

- **Best Practice**: Test across different market conditions (bull markets, bear markets, sideways markets)

- **Limitation**: Past performance doesn't guarantee future results

## Entry and Exit Strategies

### Dual-Channel System

A key innovation of the Bober XM is its dual-channel approach:

- **Independent Parameters**: Each trade direction has its own channel settings

- **Asymmetric Trading**: Recognizes that markets often behave differently in uptrends versus downtrends

- **Optimized Performance**: Fine-tune settings for both bullish and bearish conditions

This approach allows the bot to adapt to the natural asymmetry of markets, where uptrends often develop gradually while downtrends can be sharp and sudden.

### Channel Types

#### 1. Keltner Channels

Traditional volatility-based channels using EMA and ATR:

| Setting | Long Default | Short Default |

|---------|--------------|---------------|

| **EMA Length** | 37 | 20 |

| **ATR Length** | 13 | 17 |

| **Multiplier** | 1.4 | 1.9 |

| **Source** | low | high |

- **Strengths**:

- Reliable in trending markets

- Less prone to whipsaws than Bollinger Bands

- Clear visual representation of volatility

- **Weaknesses**:

- Can lag during rapid market changes

- Less effective in choppy, non-trending markets

#### 2. Machine Learning Moving Average (MLMA)

Advanced predictive model using kernel regression (RBF kernel):

| Setting | Description | Options |

|---------|-------------|--------|

| **Source MA** | Price data used for MA calculations | Any price source (low/high/close/etc.) |

| **Moving Average Type** | Type of MA algorithm for calculations | SMA, EMA, WMA, VWMA, RMA, HMA |

| **Trend Source** | Price data used for trend determination | Any price source (close default) |

| **Window Size** | Historical window for MLMA calculations | 5+ (default: 16) |

| **Forecast Length** | Number of bars to forecast ahead | 1+ (default: 3) |

| **Noise Parameter** | Controls smoothness of prediction | 0.01+ (default: ~0.43) |

| **Band Multiplier** | Multiplier for channel width | 0.1+ (default: 0.5-0.6) |

- **Strengths**:

- Predictive rather than reactive

- Adapts quickly to changing market conditions

- Better at identifying trend reversals early

- **Weaknesses**:

- More computationally intensive

- Requires careful parameter tuning

- Can be sensitive to input data quality

### Entry Strategies

| Strategy | Description | Ideal Market Conditions |

|----------|-------------|-------------------------|

| **Breakout** | Enters when price breaks through channel bands, indicating strong momentum | High volatility, emerging trends |

| **Pullback** | Enters when price retraces to the middle band after testing extremes | Established trends with regular pullbacks |

| **Mean Reversion** | Enters at channel extremes, betting on a return to the mean | Range-bound or oscillating markets |

#### Breakout Strategy (Default)

- **Implementation**: Enters long when price crosses above the upper band, short when price crosses below the lower band

- **Strengths**: Captures strong momentum moves, performs well in trending markets

- **Weaknesses**: Can lead to late entries, higher risk of false breakouts

- **Optimization Tips**:

- Increase channel multiplier for fewer but more reliable signals

- Combine with volume confirmation for better accuracy

#### Pullback Strategy

- **Implementation**: Enters long when price pulls back to middle band during uptrend, short during downtrend pullbacks

- **Strengths**: Better entry prices, lower risk, higher probability setups

- **Weaknesses**: Misses some strong moves, requires clear trend identification

- **Optimization Tips**:

- Use with trend filters to confirm overall direction

- Adjust middle band calculation for market volatility

#### Mean Reversion Strategy

- **Implementation**: Enters long at lower band, short at upper band, expecting price to revert to the mean

- **Strengths**: Excellent entry prices, works well in ranging markets

- **Weaknesses**: Dangerous in strong trends, can lead to fighting the trend

- **Optimization Tips**:

- Implement strong trend filters to avoid counter-trend trades

- Use smaller position sizes due to higher risk nature

### Confirmation Indicators

#### Pivot Point SuperTrend

Combines pivot points with ATR-based SuperTrend for trend confirmation:

| Setting | Default Value |

|---------|---------------|

| **Pivot Period** | 25 |

| **ATR Factor** | 2.2 |

| **ATR Period** | 41 |

- **Function**: Identifies significant market turning points and confirms trend direction

- **Implementation**: Requires price to respect the SuperTrend line for trade confirmation

#### Weighted Moving Average (WMA)

Provides additional confirmation layer for entries:

| Setting | Default Value |

|---------|---------------|

| **Period** | 15 |

| **Source** | ohlc4 (average of Open, High, Low, Close) |

- **Function**: Confirms trend direction and filters out low-quality signals

- **Implementation**: Price must be above WMA for longs, below for shorts

### Exit Strategies

#### On-Balance Volume (OBV) Based Exits

Uses volume flow to identify potential reversals:

| Setting | Default Value |

|---------|---------------|

| **Source** | ohlc4 |

| **MA Type** | HMA (Options: SMA, EMA, WMA, RMA, VWMA, HMA) |

| **Period** | 22 |

- **Function**: Identifies divergences between price and volume to exit before reversals

- **Implementation**: Exits when OBV crosses its moving average in the opposite direction

- **Customizable MA Type**: Different MA types provide varying sensitivity to OBV changes:

- **SMA**: Traditional simple average, equal weight to all periods

- **EMA**: More weight to recent data, responds faster to price changes

- **WMA**: Weighted by recency, smoother than EMA

- **RMA**: Similar to EMA but smoother, reduces noise

- **VWMA**: Factors in volume, helpful for OBV confirmation

- **HMA**: Reduces lag while maintaining smoothness (default)

#### ADX Exit Confirmation

Uses Average Directional Index to confirm trend exhaustion:

| Setting | Default Value |

|---------|---------------|

| **ADX Threshold** | 35 |

| **ADX Smoothing** | 60 |

| **DI Length** | 60 |

- **Function**: Confirms trend weakness before exiting positions

- **Implementation**: Requires ADX to drop below threshold or DI lines to cross

## Filter System

### RSI Filter

- **Function**: Controls entries based on momentum conditions

- **Parameters**:

- Period: 15 (default)

- Overbought level: 71

- Oversold level: 23

- Multi-timeframe support: Current, MTF1 (15min), or MTF2 (4h)

- Customizable price source (open, high, low, close, hl2, hlc3, ohlc4)

- **Implementation**: Blocks long entries when RSI > overbought, short entries when RSI < oversold

### Volatility Filter

- **Function**: Prevents trading during excessive market volatility

- **Parameters**:

- Measure: ATR (Average True Range)

- Period: Customizable (default varies by timeframe)

- Threshold: Adjustable multiplier

- Multi-timeframe support

- Customizable price source

- **Implementation**: Blocks trades when current volatility exceeds threshold × average volatility

### Volume Filter

- **Function**: Ensures adequate market liquidity for trades

- **Parameters**:

- Threshold: 0.4× average (default)

- Measurement period: 5 (default)

- Moving average type: Customizable (HMA default)

- Multi-timeframe support

- Customizable price source

- **Implementation**: Requires current volume to exceed threshold × average volume

### Bollinger Bands Filter

- **Function**: Controls entries based on price relative to statistical boundaries

- **Parameters**:

- Period: Customizable

- Standard deviation multiplier: Adjustable

- Moving average type: Customizable

- Multi-timeframe support

- Customizable price source

- **Implementation**: Can require price to be within bands or breaking out of bands depending on strategy

### KEMAD Filter (Kalman EMA Distance)

- **Function**: Advanced trend confirmation using Kalman filter algorithm

- **Parameters**:

- Process Noise: 0.35 (controls smoothness)

- Measurement Noise: 24 (controls reactivity)

- Filter Order: 6 (higher = more smoothing)

- ATR Length: 8 (for bandwidth calculation)

- Upper Multiplier: 2.0 (for long signals)

- Lower Multiplier: 2.7 (for short signals)

- Multi-timeframe support

- Customizable visual indicators

- **Implementation**: Generates signals based on price position relative to Kalman-filtered EMA bands

## Risk Management System

### Position Sizing

Automatically calculates position size based on account equity and risk parameters:

| Setting | Default Value |

|---------|---------------|

| **Risk % of Equity** | 50% |

- **Implementation**:

- Position size = (Account equity × Risk %) ÷ (Entry price × Stop loss distance)

- Adjusts automatically based on volatility and stop placement

- **Best Practices**:

- Start with lower risk percentages (1-2%) until strategy is proven

- Consider reducing risk during high volatility periods

### Stop-Loss Methods

Multiple stop-loss calculation methods with separate configurations for long and short positions:

| Method | Description | Configuration |

|--------|-------------|---------------|

| **ATR-Based** | Dynamic stops based on volatility | ATR Period: 14, Multiplier: 2.0 |

| **Percentage** | Fixed percentage from entry | Long: 1.5%, Short: 1.5% |

| **PIP-Based** | Fixed currency unit distance | 10.0 pips |

- **Implementation Notes**:

- ATR-based stops adapt to changing market volatility

- Percentage stops maintain consistent risk exposure

- PIP-based stops provide precise control in stable markets

### Trailing Stops

Locks in profits by adjusting stop-loss levels as price moves favorably:

| Setting | Default Value |

|---------|---------------|

| **Stop-Loss %** | 1.5% |

| **Activation Threshold** | 2.1% |

| **Trailing Distance** | 1.4% |

- **Implementation**:

- Initial stop remains fixed until profit reaches activation threshold

- Once activated, stop follows price at specified distance

- Locks in profit while allowing room for normal price fluctuations

### Risk-Reward Parameters

Defines the relationship between risk and potential reward:

| Setting | Default Value |

|---------|---------------|

| **Risk-Reward Ratio** | 1.4 |

| **Take Profit %** | 2.4% |

| **Stop-Loss %** | 1.5% |

- **Implementation**:

- Take profit distance = Stop loss distance × Risk-reward ratio

- Higher ratios require fewer winning trades for profitability

- Lower ratios increase win rate but reduce average profit

### Filter Combinations

The strategy allows for simultaneous application of multiple filters:

- **Recommended Combinations**:

- Trending markets: RSI + KEMAD filters

- Ranging markets: Bollinger Bands + Volatility filters

- All markets: Volume filter as minimum requirement

- **Performance Impact**:

- Each additional filter reduces the number of trades

- Quality of remaining trades typically improves

- Optimal combination depends on market conditions and timeframe

### Multi-Timeframe Filter Applications

| Filter Type | Current Timeframe | MTF1 (15min) | MTF2 (4h) |

|-------------|-------------------|-------------|------------|

| RSI | Quick entries/exits | Intraday trend | Overall trend |

| Volume | Immediate liquidity | Sustained support | Market participation |

| Volatility | Entry timing | Short-term risk | Regime changes |

| KEMAD | Precise signals | Trend confirmation | Major reversals |

## Visual Indicators and Chart Analysis

The bot provides comprehensive visual feedback on the chart:

- **Channel Bands**: Keltner or MLMA bands showing potential support/resistance

- **Pivot SuperTrend**: Colored line showing trend direction and potential reversal points

- **Entry/Exit Markers**: Annotations showing actual trade entries and exits

- **Risk/Reward Zones**: Visual representation of stop-loss and take-profit levels

These visual elements allow for:

- Real-time strategy assessment

- Post-trade analysis and optimization

- Educational understanding of the strategy logic

## Implementation Guide

### TradingView Setup

1. Load the script in TradingView Pine Editor

2. Apply to your preferred chart and timeframe

3. Adjust parameters based on your trading preferences

4. Enable alerts for webhook integration

### Webhook Integration

1. Configure webhook URL in TradingView alerts

2. Set up receiving endpoint on your trading platform

3. Define message format matching the bot's output

4. Test with small position sizes before full deployment

### Optimization Process

1. Backtest across different market conditions

2. Identify parameter sensitivity through multiple tests

3. Focus on risk management parameters first

4. Fine-tune entry/exit conditions based on performance metrics

5. Validate with out-of-sample testing

## Performance Considerations

### Strengths

- Adaptability to different market conditions through dual channels

- Multiple layers of confirmation reducing false signals

- Comprehensive risk management protecting capital

- Machine learning integration for predictive edge

### Limitations

- Complex parameter set requiring careful optimization

- Potential over-optimization risk with so many variables

- Computational intensity of MLMA calculations

- Dependency on proper webhook configuration for execution

### Best Practices

- Start with conservative risk settings (1-2% of equity)

- Test thoroughly in demo environment before live trading

- Monitor performance regularly and adjust parameters

- Consider market regime changes when evaluating results

## Conclusion

The ₿ober XM v2.0 represents a significant evolution in trading strategy design, combining traditional technical analysis with machine learning elements and multi-timeframe analysis. The core strength of this system lies in its adaptability and recognition of market asymmetry.

### Market Asymmetry and Adaptive Approach

The strategy acknowledges a fundamental truth about markets: bullish and bearish phases behave differently and should be treated as distinct environments. The dual-channel system with separate parameters for long and short positions directly addresses this asymmetry, allowing for optimized performance regardless of market direction.

### Targeted Backtesting Philosophy

It's counterproductive to run backtests over excessively long periods. Markets evolve continuously, and strategies that worked in previous market regimes may be ineffective in current conditions. Instead:

- Test specific market phases separately (bull markets, bear markets, range-bound periods)

- Regularly re-optimize parameters as market conditions change

- Focus on recent performance with higher weight than historical results

- Test across multiple timeframes to ensure robustness

### Multi-Timeframe Analysis as a Game-Changer

The integration of multi-timeframe analysis fundamentally transforms the strategy's effectiveness:

- **Increased Safety**: Higher timeframe confirmations reduce false signals and improve trade quality

- **Context Awareness**: Decisions made with awareness of larger trends reduce adverse entries

- **Adaptable Precision**: Apply strict filters on lower timeframes while maintaining awareness of broader conditions

- **Reduced Noise**: Higher timeframe data naturally filters market noise that can trigger poor entries

The ₿ober XM v2.0 provides traders with a framework that acknowledges market complexity while offering practical tools to navigate it. With proper setup, realistic expectations, and attention to changing market conditions, it delivers a sophisticated approach to systematic trading that can be continuously refined and optimized.

Dskyz (DAFE) Quantum Sentiment Flux - Beginners Dskyz (DAFE) Quantum Sentiment Flux - Beginners:

Welcome to the Dskyz (DAFE) Quantum Sentiment Flux - Beginners , a strategy and concept that’s your ultimate wingman for trading futures like MNQ, NQ, MES, and ES. This gem combines lightning-fast momentum signals, market sentiment smarts, and bulletproof risk management into a system so intuitive, even newbies can trade like pros. With clean DAFE visuals, preset modes for every vibe, and a revamped dashboard that’s basically a market GPS, this strategy makes futures trading feel like a high-octane sci-fi mission.

Built on the Dskyz (DAFE) legacy of Aurora Divergence, the Quantum Sentiment Flux is designed to empower beginners while giving seasoned traders a lean, sentiment-driven edge. It uses fast/slow EMA crossovers for entries, filters trades with VIX, SPX trends, and sector breadth, and keeps your account safe with adaptive stops and cooldowns. Tuned for more action with faster signals and a slick bottom-left dashboard, this updated version is ready to light up your charts and outsmart institutional traps. Let’s dive into why this strat’s a must-have and break down its brilliance.

Why Traders Need This Strategy

Futures markets are a wild ride—fast moves, volatility spikes (like the April 28, 2025 NQ 1k-point drop), and institutional games that can wreck unprepared traders. Beginners often get lost in complex systems or burned by impulsive trades. The Quantum Sentiment Flux is the antidote, offering:

Dead-Simple Setup: Preset modes (Aggressive, Balanced, Conservative) auto-tune signals, risk, and sizing, so you can trade without a quant degree.

Sentiment Superpower: VIX filter, SPX trend, and sector breadth visuals keep you aligned with market health, dodging chop and riding trends.

Ironclad Safety: Tighter ATR-based stops, 2:1 take-profits, and preset cooldowns protect your capital, even in chaotic sessions.

Next-Level Visuals: Green/red entry triangles, vibrant EMAs, a sector breadth background, and a beefed-up dashboard make signals and context pop.

DAFE Swagger: The clean aesthetics, sleek dashboard—ties it to Dskyz’s elite brand, making your charts a work of art.

Traders need this because it’s a plug-and-play system that blends beginner-friendly simplicity with pro-level market awareness. Whether you’re just starting or scalping 5min MNQ, this strat’s your key to trading with confidence and style.

Strategy Components

1. Core Signal Logic (High-Speed Momentum)

The strategy’s engine is a momentum-based system using fast and slow Exponential Moving Averages (EMAs), now tuned for faster, more frequent trades.

How It Works:

Fast/Slow EMAs: Fast EMA (Aggressive: 5, Balanced: 7, Conservative: 9 bars) and slow EMA (12/14/18 bars) track short-term vs. longer-term momentum.

Crossover Signals:

Buy: Fast EMA crosses above slow EMA, and trend_dir = 1 (fast EMA > slow EMA + ATR * strength threshold).

Sell: Fast EMA crosses below slow EMA, and trend_dir = -1 (fast EMA < slow EMA - ATR * strength threshold).

Strength Filter: ma_strength = fast EMA - slow EMA must exceed an ATR-scaled threshold (Aggressive: 0.15, Balanced: 0.18, Conservative: 0.25) for robust signals.

Trend Direction: trend_dir confirms momentum, filtering out weak crossovers in choppy markets.

Evolution:

Faster EMAs (down from 7–10/21–50) catch short-term trends, perfect for active futures markets.

Lower strength thresholds (0.15–0.25 vs. 0.3–0.5) make signals more sensitive, boosting trade frequency without sacrificing quality.

Preset tuning ensures beginners get optimized settings, while pros can tweak via mode selection.

2. Market Sentiment Filters

The strategy leans hard into market sentiment with a VIX filter, SPX trend analysis, and sector breadth visuals, keeping trades aligned with the big picture.

VIX Filter:

Logic: Blocks long entries if VIX > threshold (default: 20, can_long = vix_close < vix_limit). Shorts are always allowed (can_short = true).

Impact: Prevents longs during high-fear markets (e.g., VIX spikes in crashes), while allowing shorts to capitalize on downturns.

SPX Trend Filter:

Logic: Compares S&P 500 (SPX) close to its SMA (Aggressive: 5, Balanced: 8, Conservative: 12 bars). spx_trend = 1 (UP) if close > SMA, -1 (DOWN) if < SMA, 0 (FLAT) if neutral.

Impact: Provides dashboard context, encouraging trades that align with market direction (e.g., longs in UP trend).

Sector Breadth (Visual):

Logic: Tracks 10 sector ETFs (XLK, XLF, XLE, etc.) vs. their SMAs (same lengths as SPX). Each sector scores +1 (bullish), -1 (bearish), or 0 (neutral), summed as breadth (-10 to +10).

Display: Green background if breadth > 4, red if breadth < -4, else neutral. Dashboard shows sector trends (↑/↓/-).

Impact: Faster SMA lengths make breadth more responsive, reflecting sector rotations (e.g., tech surging, energy lagging).

Why It’s Brilliant:

- VIX filter adds pro-level volatility awareness, saving beginners from panic-driven losses.

- SPX and sector breadth give a 360° view of market health, boosting signal confidence (e.g., green BG + buy signal = high-probability trade).

- Shorter SMAs make sentiment visuals react faster, perfect for 5min charts.

3. Risk Management

The risk controls are a fortress, now tighter and more dynamic to support frequent trading while keeping accounts safe.

Preset-Based Risk:

Aggressive: Fast EMAs (5/12), tight stops (1.1x ATR), 1-bar cooldown. High trade frequency, higher risk.

Balanced: EMAs (7/14), 1.2x ATR stops, 1-bar cooldown. Versatile for most traders.

Conservative: EMAs (9/18), 1.3x ATR stops, 2-bar cooldown. Safer, fewer trades.

Impact: Auto-scales risk to match style, making it foolproof for beginners.

Adaptive Stops and Take-Profits:

Logic: Stops = entry ± ATR * atr_mult (1.1–1.3x, down from 1.2–2.0x). Take-profits = entry ± ATR * take_mult (2x stop distance, 2:1 reward/risk). Longs: stop below entry, TP above; shorts: vice versa.

Impact: Tighter stops increase trade turnover while maintaining solid risk/reward, adapting to volatility.

Trade Cooldown:

Logic: Preset-driven (Aggressive/Balanced: 1 bar, Conservative: 2 bars vs. old user-input 2). Ensures bar_index - last_trade_bar >= cooldown.

Impact: Faster cooldowns (especially Aggressive/Balanced) allow more trades, balanced by VIX and strength filters.

Contract Sizing:

Logic: User sets contracts (default: 1, max: 10), no preset cap (unlike old 7/5/3 suggestion).

Impact: Flexible but risks over-leverage; beginners should stick to low contracts.

Built To Be Reliable and Consistent:

- Tighter stops and faster cooldowns make it a high-octane system without blowing up accounts.

- Preset-driven risk removes guesswork, letting newbies trade confidently.

- 2:1 TPs ensure profitable trades outweigh losses, even in volatile sessions like April 27, 2025 ES slippage.

4. Trade Entry and Exit Logic

The entry/exit rules are simple yet razor-sharp, now with VIX filtering and faster signals:

Entry Conditions:

Long Entry: buy_signal (fast EMA crosses above slow EMA, trend_dir = 1), no position (strategy.position_size = 0), cooldown passed (can_trade), and VIX < 20 (can_long). Enters with user-defined contracts.

Short Entry: sell_signal (fast EMA crosses below slow EMA, trend_dir = -1), no position, cooldown passed, can_short (always true).

Logic: Tracks last_entry_bar for visuals, last_trade_bar for cooldowns.

Exit Conditions:

Stop-Loss/Take-Profit: ATR-based stops (1.1–1.3x) and TPs (2x stop distance). Longs exit if price hits stop (below) or TP (above); shorts vice versa.

No Other Exits: Keeps it straightforward, relying on stops/TPs.

5. DAFE Visuals

The visuals are pure DAFE magic, blending clean function with informative metrics utilized by professionals, now enhanced by faster signals and a responsive breadth background:

EMA Plots:

Display: Fast EMA (blue, 2px), slow EMA (orange, 2px), using faster lengths (5–9/12–18).

Purpose: Highlights momentum shifts, with crossovers signaling entries.

Sector Breadth Background:

Display: Green (90% transparent) if breadth > 4, red (90%) if breadth < -4, else neutral.

Purpose: Faster breadth_sma_len (5–12 vs. 10–50) reflects sector shifts in real-time, reinforcing signal strength.

- Visuals are intuitive, turning complex signals into clear buy/sell cues.

- Faster breadth background reacts to market rotations (e.g., tech vs. energy), giving a pro-level edge.

6. Sector Breadth Dashboard

The new bottom-left dashboard is a game-changer, a 3x16 table (black/gray theme) that’s your market command center:

Metrics:

VIX: Current VIX (red if > 20, gray if not).

SPX: Trend as “UP” (green), “DOWN” (red), or “FLAT” (gray).

Trade Longs: “OK” (green) if VIX < 20, “BLOCK” (red) if not.

Sector Breadth: 10 sectors (Tech, Financial, etc.) with trend arrows (↑ green, ↓ red, - gray).

Placeholder Row: Empty for future metrics (e.g., ATR, breadth score).

Purpose: Consolidates regime, volatility, market trend, and sector data, making decisions a breeze.

- VIX and SPX metrics add context, helping beginners avoid bad trades (e.g., no longs if “BLOCK”).

Sector arrows show market health at a glance, like a cheat code for sentiment.

Key Features

Beginner-Ready: Preset modes and clear visuals make futures trading a breeze.

Sentiment-Driven: VIX filter, SPX trend, and sector breadth keep you in sync with the market.

High-Frequency: Faster EMAs, tighter stops, and short cooldowns boost trade volume.

Safe and Smart: Adaptive stops/TPs and cooldowns protect capital while maximizing wins.

Visual Mastery: DAFE’s clean flair, EMAs, dashboard—makes trading fun and clear.

Backtestable: Lean code and fixed qty ensure accurate historical testing.

How to Use

Add to Chart: Load on a 5min MNQ/ES chart in TradingView.

Pick Preset: Aggressive (scalping), Balanced (versatile), or Conservative (safe). Balanced is default.

Set Contracts: Default 1, max 10. Stick low for safety.

Check Dashboard: Bottom-left shows preset, VIX, SPX, and sectors. “OK” + green breadth = strong buy.

Backtest: Run in strategy tester to compare modes.

Live Trade: Connect to Tradovate or similar. Watch for slippage (e.g., April 27, 2025 ES issues).

Replay Test: Try April 28, 2025 NQ drop to see VIX filter and stops in action.

Why It’s Brilliant

The Dskyz (DAFE) Quantum Sentiment Flux - Beginners is a masterpiece of simplicity and power. It takes pro-level tools—momentum, VIX, sector breadth—and wraps them in a system anyone can run. Faster signals and tighter stops make it a trading machine, while the VIX filter and dashboard keep you ahead of market chaos. The DAFE visuals and bottom-left command center turn your chart into a futuristic cockpit, guiding you through every trade. For beginners, it’s a safe entry to futures; for pros, it’s a scalping beast with sentiment smarts. This strat doesn’t just trade—it transforms how you see the market.

Final Notes

This is more than a strategy—it’s your launchpad to mastering futures with Dskyz (DAFE) flair. The Quantum Sentiment Flux blends accessibility, speed, and market savvy to help you outsmart the game. Load it, watch those triangles glow, and let’s make the markets your canvas!

Official Statement from Pine Script Team

(see TradingView help docs and forums):

"This warning may appear when you call functions such as ta.sma inside a request.security in a loop. There is no runtime impact. If you need to loop through a dynamic list of tickers, this cannot be avoided in the present version... Values will still be correct. Ignore this warning in such contexts."

(This publishing will most likely be taken down do to some miscellaneous rule about properly displaying charting symbols, or whatever. Once I've identified what part of the publishing they want to pick on, I'll adjust and repost.)

Use it with discipline. Use it with clarity. Trade smarter.

**I will continue to release incredible strategies and indicators until I turn this into a brand or until someone offers me a contract.

Created by Dskyz, powered by DAFE Trading Systems. Trade fast, trade bold.

SnowdexUtilsLibrary "SnowdexUtils"

the various function that often use when create a strategy trading.

f_backtesting_date(train_start_date, train_end_date, test_date, deploy_date)

Backtesting within a specific window based on deployment and testing dates.

Parameters:

train_start_date (int) : the start date for training the strategy.

train_end_date (int) : the end date for training the strategy.

test_date (bool) : if true, backtests within the period from `train_end_date` to the current time.

deploy_date (bool) : if true, the strategy backtests up to the current time.

Returns: given time falls within the specified window for backtesting.

f_init_ma(ma_type, source, length)

Initializes a moving average based on the specified type.

Parameters:

ma_type (simple string) : the type of moving average (e.g., "RMA", "EMA", "SMA", "WMA").

source (float) : the input series for the moving average calculation.

length (simple int) : the length of the moving average window.

Returns: the calculated moving average value.

f_init_tp(side, entry_price, rr, sl_open_position)

Calculates the target profit based on entry price, risk-reward ratio, and stop loss. The formula is `tp = entry price + (rr * (entry price - stop loss))`.

Parameters:

side (bool) : the trading side (true for long, false for short).

entry_price (float) : the entry price of the position.

rr (float) : the risk-reward ratio.

sl_open_position (float) : the stop loss price for the open position.

Returns: the calculated target profit value.

f_round_up(number, decimals)

Rounds up a number to a specified number of decimals.

Parameters:

number (float)

decimals (int)

Returns: The rounded-up number.

f_get_pip_size()

Calculates the pip size for the current instrument.

Returns: Pip size adjusted for Forex instruments or 1 for others.

f_table_get_position(value)

Maps a string to a table position constant.

Parameters:

value (string) : String representing the desired position (e.g., "Top Right").

Returns: The corresponding position constant or `na` for invalid values.

ChartArt-Bankniftybuying5minName: ChartArt-BankNifty Buying Strategy (5-Minute)

Timeframe: 5-Minute Candles

Asset: BankNifty (Indian Stock Market Index)

Trading Hours: 9:30 AM - 2:45 PM IST (Indian Standard Time)

This strategy is designed for BankNifty intraday traders who want to capitalize on short-term price movements within a defined trading window. It combines technical indicators like Simple Moving Averages (SMA), Relative Strength Index (RSI), and candlestick patterns to identify potential buy signals during intraday downtrends. The strategy employs specific entry, stop-loss, and target conditions to manage trades effectively and minimize risk.

Technical Indicators Used

Simple Moving Averages (SMA):

EMA7: 7-period SMA on closing price.

EMA5: 5-period SMA on closing price.

Purpose: Used to identify the intraday trend by comparing short-term moving averages. The strategy focuses on situations where the market is in a minor downtrend, indicated by EMA5 being below EMA7.

Relative Strength Index (RSI):

RSI14: 14-period RSI, a momentum oscillator that measures the speed and change of price movements.

SMA14: 14-period SMA of the RSI.

Purpose: RSI is used to identify potential reversal points. The strategy looks for situations where the RSI is below its own moving average, suggesting weakening momentum in the downtrend.

Candlestick Patterns:

Relaxed Hammer or Doji (2nd Candle): A pattern where the second candle in a 3-candle sequence shows a potential reversal signal (Hammer or Doji), indicating indecision or a potential turning point.

Bearish 1st Candle: The first candle is bearish, setting up the context for a potential reversal.

Bullish 3rd Candle: The third candle must be bullish with specific characteristics (closing near the high, surpassing the previous high), confirming the reversal.

Strategy Conditions

Time Condition:

The strategy is only active during specific hours (9:30 AM to 2:45 PM IST). This ensures that trades are only taken during the most liquid hours of the trading day, avoiding potential volatility or lack of liquidity towards market close.

Intraday Downtrend Condition:

EMA5 < EMA7: Indicates that the market is in a minor downtrend. The strategy looks for reversal opportunities within this trend.

RSI Condition:

RSI14 <= SMA14: Indicates that the current RSI value is below its 14-period SMA, suggesting potential weakening momentum, which can precede a reversal.

Candlestick Patterns:

1st Candle: Must be bearish, setting up the context for a potential reversal.

2nd Candle: Must either be a Hammer or Doji, indicating a potential reversal pattern.

3rd Candle: Must be bullish, with specific characteristics (closing near the high, breaking the previous high, etc.), confirming the reversal.

RSI Crossover Condition:

A crossover of the RSI over its SMA in the last 5 periods is also checked, adding further confirmation to the reversal signal.

Entry and Exit Rules

Entry Signal:

A buy signal is generated when all the conditions (time, intraday downtrend, bearish 1st candle, hammer/doji 2nd candle, bullish 3rd candle, and RSI condition) are met. The trade is entered at the high of the bullish third candle.

Stop Loss:

The stop loss is calculated based on the difference between the entry price and the low of the second candle. If this difference is greater than 90 points, the stop loss is placed at the midpoint of the second candle's range (average of high and low). Otherwise, it is placed at the low of the second candle.

Target 1:

The first target is set at 1.8 times the difference between the entry price and the stop loss. When this target is hit, half of the position is exited to lock in partial profits.

Target 2:

The second target is set at 3 times the difference between the entry price and the stop loss. The remaining position is exited at this point, or if the price hits the stop loss.

Originality and Usefulness

This strategy is original in its combination of multiple technical indicators and candlestick patterns to identify potential reversals in a specific intraday timeframe. By focusing on minor downtrends and utilizing a 3-candle reversal pattern, the strategy seeks to capture quick price movements with a structured approach to risk management.

Key Benefits:

High Precision: The strategy’s multi-step filtering process (time condition, trend confirmation, candlestick pattern analysis, and momentum evaluation via RSI) increases the likelihood of accurate trade signals.

Risk Management: The use of a dynamic stop-loss based on candle characteristics, combined with partial profit-taking, allows traders to lock in profits while still giving the trade room to develop further.

Structured Approach: The strategy provides a clear, rule-based system for entering and exiting trades, which can help remove emotional decision-making from the trading process.

Charts and Signals

The strategy produces signals in the form of labels on the chart:

Buy Signal: A green label is plotted below the candle that meets all entry conditions, indicating a potential buy opportunity.

Stop Loss (SL): A red dashed line is drawn at the stop-loss level with a label indicating "SL".

Target 1 (1st TG): A blue dashed line is drawn at the first target level with a label indicating "1st TG".

Target 2 (2nd TG): Another blue dashed line is drawn at the second target level with a label indicating "2nd TG".

These visual aids help traders quickly identify entry points, stop loss levels, and target levels on the chart, making the strategy easy to follow and implement.

Backtesting and Optimization

Backtesting: The strategy can be backtested on TradingView using historical data to evaluate its performance. Traders should consider testing across different market conditions to ensure the strategy's robustness.

Optimization: Parameters such as the RSI period, moving averages, and target multipliers can be optimized based on backtesting results to refine the strategy further.

Conclusion

The ChartArt-BankNifty Buying Strategy offers a well-rounded approach to intraday trading, focusing on capturing reversals in minor downtrends. With a strong emphasis on technical analysis, precise entry and exit rules, and robust risk management, this strategy provides a solid framework for traders looking to engage in intraday trading on BankNifty.

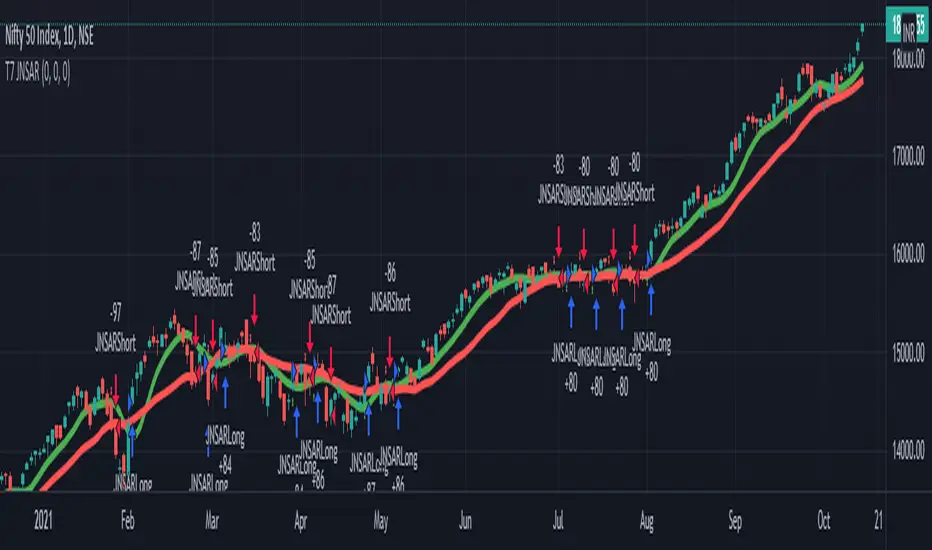

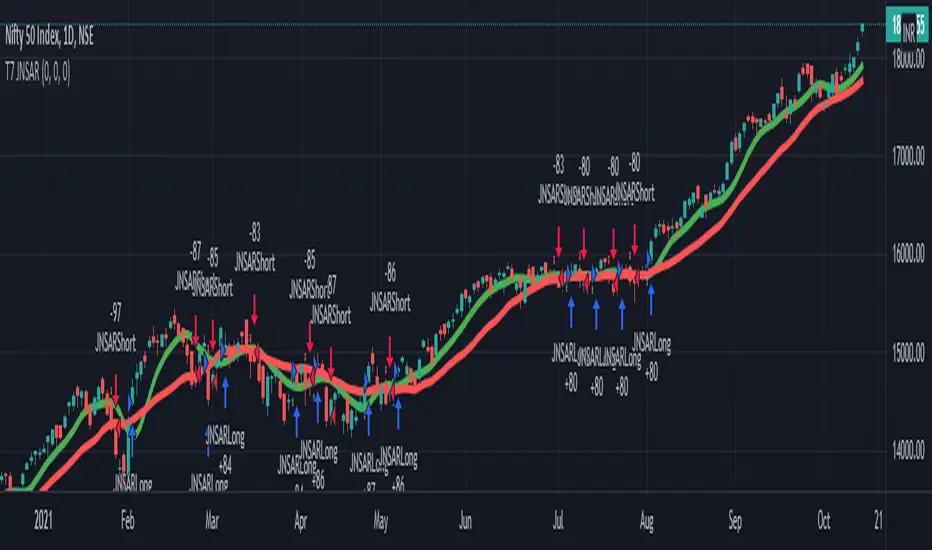

T7 JNSARUpdated code for the T7 JNSAR system earlier published here -

Following updates made to the code

1. Buy / Sell arrows now appear when the corresponding conditions are met.

2. Support for Heikin-Ashi Candles added

3. Different Backtesting Position Sizing Algorithms added for evaluation

Also am republishing the trading rules here again with some modification

1. Go Long when the daily close is above the JNSAR line. Go Short when the daily close is below the JNSAR line. JNSAR line is the varying green line overlayed over the price chart. Once a signal comes at market close enter in the direction of the signal @ market price @ next day market open.

2. Trade only Nifty Index. This system was developed and backtested only for NIFTY Index. So trade in its Futures or Options, as you may deem fit. My recommendation is to choose futures for simplicity. If you want to reduce the trading cost and go with options, trade with deep in the money options, preferably 2 strikes far from the spot price.

3. Trade all signals. Markets trend only 30-35% of the time and hence the system is only accurate to that extend. But system tends to make enough money, in this small trending window, to keep the overall profitability in good health. But one never knows when a big trend may come and when it comes its absolutely imperative that you take it. To ensure that, trade all signals and don't be choosy about what signals you are going to trade. Also I wouldn't recommend using your own analysis to trade this system. Too many drivers will crash the car.

4. Like all trend following systems, this system will have many whipsaws during flat markets along with large trade and account drawdowns. Also some months and even years may not be profitable. But to trade this system profitably, it is necessary to take these in one's stride and keep trading. As the backtester results from 1990 to 2016 proves, this system is profitable overall thus far. Take confidence from that objective fact.

5. Trade with only that amount of money you can afford to loose. Initial capital that you need to have to trade one lot of NIFTY should be atleast - (Margin Money required to take and hold 1 lot position + maximum drawdown amount per lot)*1.2. Be prepared to add more if need be, but the above formula will give a rough idea of what you need to have to start trading and be in the game always.

6. Place an After Market Order @ Market Price with your broker after market close so that you get to execute the trade next trading day @ Market open to capture near similar price as the daily open price seen on the chart. This execution mode will give you the best chance to minimise the slippage and mimic the backtester results as closely as practically possible.

7. Follow all the 6 rules above religiously, as if your life depends on it. If you cant, then don't trade this system; You will certainly loose money.

Happy Trading !!! As always am looking out for your valuable feedback.

Elliott Wave Full Fractal System v2.0Elliott Wave Full Fractal System v2.0 – Q.C. FINAL (Guaranteed R/R)

Elliott Wave Full Fractal System is a multi-timeframe wave engine that automatically labels Elliott impulses and ABC corrections, then builds a rule-based, ATR-driven risk/reward framework around the “W3–W4–W5” leg.

“Guaranteed R/R” here means every order is placed with a predefined stop-loss and take-profit that respect a minimum Reward:Risk ratio – it does not mean guaranteed profits.

Core Idea

This strategy turns a full fractal Elliott Wave labelling engine into a systematic trading model.

It scans fractal pivots on three wave degrees (Primary, Intermediate, Minor) to detect 5-wave impulses and ABC corrections.

A separate “Trading Degree” pivot stream, filtered by a 200-EMA trend filter and ATR-based dynamic pivots, is then used to find W4 pullback entries with a minimum, user-defined Reward:Risk ratio.

Default Properties & Risk Assumptions

The backtest uses realistic but conservative defaults:

// Default properties used for backtesting

strategy(

"Elliott Wave Full Fractal System - Q.C. FINAL (Guaranteed R/R)",

overlay = true,

initial_capital = 10000, // realistic account size

default_qty_type = strategy.percent_of_equity,

default_qty_value = 1, // 1% risk per trade

commission_type = strategy.commission.cash_per_contract,

commission_value = 0.005, // example stock commission

slippage = 0 // see notes below

)

Account size: 10,000 (can be changed to match your own account).

Position sizing: 1% of equity per trade to keep risk per idea sustainable and aligned with TradingView’s recommendations.

Commission: 0.005 cash per contract/share as a realistic example for stock trading.

Slippage: set to 0 in code for clarity of “pure logic” backtesting. Real-life trading will experience slippage, so users should adjust this according to their market and broker.

Always re-run the backtest after changing any of these values, and avoid using high risk fractions (5–10%+) as that is rarely sustainable.

1. Full Fractal Wave Engine

The script builds and maintains four pivot streams using ATR-adaptive fractals:

Primary Degree (Macro Trend):

Captures the large swings that define the major trend. Labels ①–⑤ and ⒶⒷⒸ using blue “Circle” labels and thicker lines.

Intermediate Degree (Trading Degree):

Captures the medium swings (swing-trading horizon). Uses teal labels ( (1)…(5), (A)(B)(C) ).

Minor Degree (Micro Structure):

Tracks short-term swings inside the larger waves. Uses red roman numerals (i…v, a b c).

ABC Corrections (Optional):

When enabled, the engine tries to detect standard A–B–C corrective structures that follow a completed 5-wave impulse and plots them with dashed lines.

Each degree uses a dynamic pivot lookback that expands when ATR is above its EMA, so the system naturally requires “stronger” pivots in volatile environments and reacts faster in quiet conditions.

2. Theory Rules & Strict Mode

Normal Mode: More permissive detection. Designed to show more wave structures for educational / exploratory use.

Strict Mode: Enforces key Elliott constraints:

Wave 3 not shorter than waves 1 and 5.

No invalid W4 overlap with W1 (for standard impulses).

ABC Logic: After a confirmed bullish impulse, the script expects a down-up-down corrective pattern (A,B,C). After a bearish impulse, it looks for up-down-up.

3. Trend Filter & Pivots

EMA Trend Filter: A configurable EMA (default 200) is used as a non-wave trend filter.

Price above EMA → Only long setups are considered.

Price below EMA → Only short setups are considered.

ATR-Adaptive Pivots: The pivot engine scales its left/right bars based on current ATR vs ATR EMA, making waves and trading pivots more robust in volatile regimes.

4. Dynamic Risk Management (Guaranteed R/R Engine)

The trading engine is designed around risk, not just pattern recognition:

ATR-Based Stop:

Stop-loss is placed at:

Entry ± ATR × Multiplier (user-configurable, default 2.0).

This anchors risk to current volatility.

Minimum Reward:Risk Ratio:

For each setup, the script:

Computes the distance from entry to stop (risk).

Projects a take-profit target at risk × min_rr_ratio away from entry.

Only accepts the setup if risk is positive and the required R:R ratio is achievable.

Result: Every order is created with both TP and SL at a predefined distance, so each trade starts with a known, minimum Reward:Risk profile by design.

“Guaranteed R/R” refers exclusively to this order placement logic (TP/SL geometry), not to win-rate or profitability.

5. Trading Logic – W3–W4–W5 Pattern

The Trading pivot stream (separate from visual wave degrees) looks for a simple but powerful pattern:

Bullish structure:

Sequence of pivots forms a higher-high / higher-low pattern.

Price is above the EMA trend filter.

A strong “W3” leg is confirmed with structure rules (optionally stricter in Strict mode).

Entry (Long – W4 Pullback):

The “height” of W3 is measured.

Entry is placed at a configurable Fibonacci pullback (default 50%) inside that leg.

ATR-based stop is placed below entry.

Take-profit is projected to satisfy min Reward:Risk.

Bearish structure:

Mirrored logic (lower highs/lows, price below EMA, W3 down, W4 retrace up, W5 continuation down).

Once a valid setup is found, the script draws a colored box around the entry zone and a label describing the type of signal (“LONG SETUP” or “SHORT SETUP”) with the suggested limit price.

6. Orders & Execution

Entry Orders: The strategy uses limit orders at the computed W4 level (“Sniper Long” or “Sniper Short”).

Exits: A single strategy.exit() is attached to each entry with:

Take-profit at the projected minimum R:R target.

Stop-loss at ATR-based level.

One Trade at a Time: New setups are only used when there is no open position (strategy.opentrades == 0) to keep the logic clear and risk contained.

7. Visual Guide on the Chart

Wave Labels:

Primary: ①,②,③,④,⑤, ⒶⒷⒸ

Intermediate: (1)…(5), (A)(B)(C)

Minor: i…v, a b c

Trend EMA: Single blue EMA showing the dominant trend.

Setup Boxes:

Green transparent box → long entry zone.

Red transparent box → short entry zone.

Labels: “LONG SETUP / SHORT SETUP” labels mark the proposed limit entry with price.

8. How to Use This Strategy

Attach the strategy to your chart

Choose your market (stocks, indices, FX, crypto, futures, etc.) and timeframe (for example 1h, 4h, or Daily). Then add the strategy to the chart from your Scripts list.

Start with the default settings

Leave all inputs on their defaults first. This lets you see the “intended” behaviour and the exact properties used for the published backtest (account size, 1% risk, commission, etc.).

Study the wave map

Zoom in and out and look at the three wave degrees:

Blue circles → Primary degree (big picture trend).

Teal (1)…(5) → Intermediate degree (swing structure).

Red i…v → Minor degree (micro waves).

Use this to understand how the engine is interpreting the Elliott structure on your symbol.

Watch for valid setups

Look for the coloured boxes and labels:

Green box + “LONG SETUP” label → potential W4 pullback long in an uptrend.

Red box + “SHORT SETUP” label → potential W4 pullback short in a downtrend.

Only trades in the direction of the EMA trend filter are allowed by the strategy.

Check the Reward:Risk of each idea

For each setup, inspect:

Limit entry price.

ATR-based stop level.

Projected take-profit level.

Make sure the minimum Reward:Risk ratio matches your own rules before you consider trading it.

Backtest and evaluate

Open the Strategy Tester:

Verify you have a decent sample size (ideally 100+ trades).

Check drawdowns, average trade, win-rate and R:R distribution.