Fisher Transform Multi-Timeframe Backtest (No Trailing)This is the Backtester without Trailing Stops

Credits to mortdiggiddy

Cerca negli script per "backtest"

All Candlestick Patterns on Backtest [By MUQWISHI]▋ INTRODUCTION :

The “All Candlestick Patterns on Backtest” indicator generates a table that offers a clear visualization of the historical return percentages for each candlestick pattern strategy over a specified time period. This table serves as an organized resource, serving as a launching point for in-depth research into candle formations. It may help to rectify any misconceptions surrounding candlestick patterns, refine trading approaches, and it could be foundation to make informed decisions in trading journey.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

Credit to public technical “*All Candlestick Patterns*” indicator.

_______________________

▋ TABLE:

_______________________

▋ CHART:

_______________________

▋ INDICATOR SETTINGS:

#Section One: Table Setting

#Section Two: Backtest Setting

(1) Backtest Starting Period.

Note: If the datetime of the first candle on the chart is after the entreated datetime, the calculation will start from the first candle on the chart.

(2) Initial Equity ($).

(3) Leverage: Current Equity x Leverage Value.

(4) Entry Mode:

- “At Close”: Execute entry order as soon as the candle confirmed.

- “Breakout High (Low for Short)”: Stop limit buy order, entry order will be executed as soon as the next candle breakout the high of last pattern’s candle (low for short)

(5) Cancel Entry Within Bars: This option is applicable with {Entry Mode = Breakout High (Low for Short)}, to cancel the Entry Order if it's not executed within certain selected number of bars.

(6) Stoploss Range: the range refers to high of pattern - low of pattern.

(7) Risk:Reward: the calculation of risk:reward range start from entry price level. For example: A pattern triggered with range 10 points, and entry price is 100.

- For 1:1~risk:reward would the stoploss at 90 and takeprofit at 110.

- For 1:3~risk:reward would the stoploss at 90 and takeprofit at 130.

#Section Three: Technical & Candle Patterns

_______________________

▋ Comments:

This table was developed for research and educational purposes.

Candlestick patterns are almost similar as seen in “*All Candlestick Patterns*” indicator.

The table results should not be taken as a major concept to build a trading decision.

Personally, I see candlestick patterns as a means to comprehend the psychology of the market, and help to follow the price action.

Please let me know if you have any questions.

Thank you.

[Autoview][BackTest] Blank R0.13BThis is a fork of JustUncleL's

Dual MA Ribbons R0.13

It is now a blank template for making new strategies / alerts for autoview

The changes are as follows:

Removed actual algo

Establish functions for long Signal, long Close Signal and short Signal, short Close Signal to minimize the places code must be edited to update / replace algos

Make allow Long and allow short and invert trade directions independent options

Added support for alternate candle types

Added autoset backtest period feature, and optional coloring

Moved strategy calls in to functions so they can all be commented out or activated / disabled in a single block at the top of the script

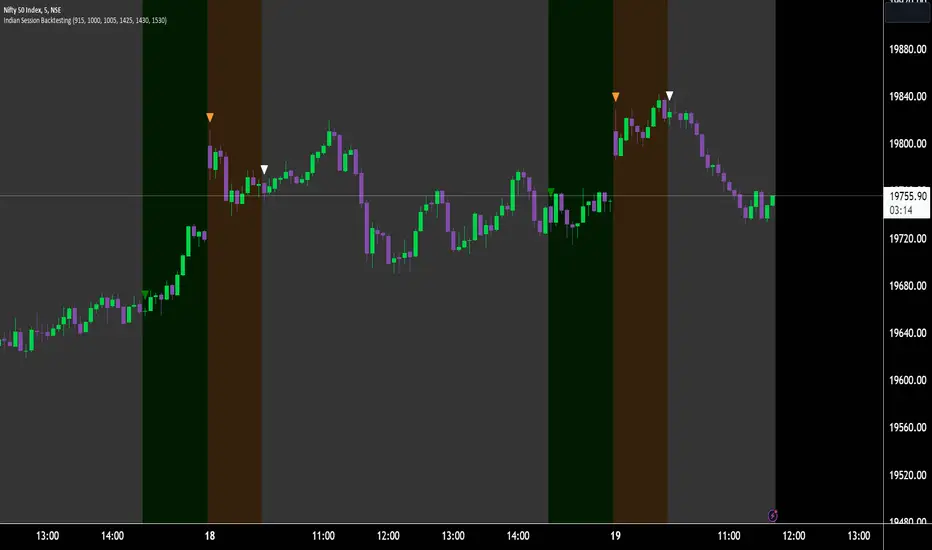

Indian Market Sessions for BacktestingThis indicator is designed to increase the quality of your backtesting in the Indian Market.

NSE & BSE run from 9:15 am IST to 3:30 pm IST.

Naturally different times have different kinds of volatility.

On your chart you will find premarked -

Saffron - 9:15 am to 10:30 am - Opening Session - High Volatility Observed Historically

White - 10:35 am to 2:25 pm - Middle Session - Lower Volatility Observed Historically

Green - 2:30 pm to 3:30 pm - Closing Session - Medium to High Volatility Observed Historically

You will also find the start of each session marked with an arrow.

Feel free to change the times from the input settings and the color and visibility from the style settings.

_______________

Usage:

When you backtest any strategies, say moving average crossovers, also mark the sessions in your sheet which will help you further increase accuracy.

Feel free to drop your doubts in the comments.

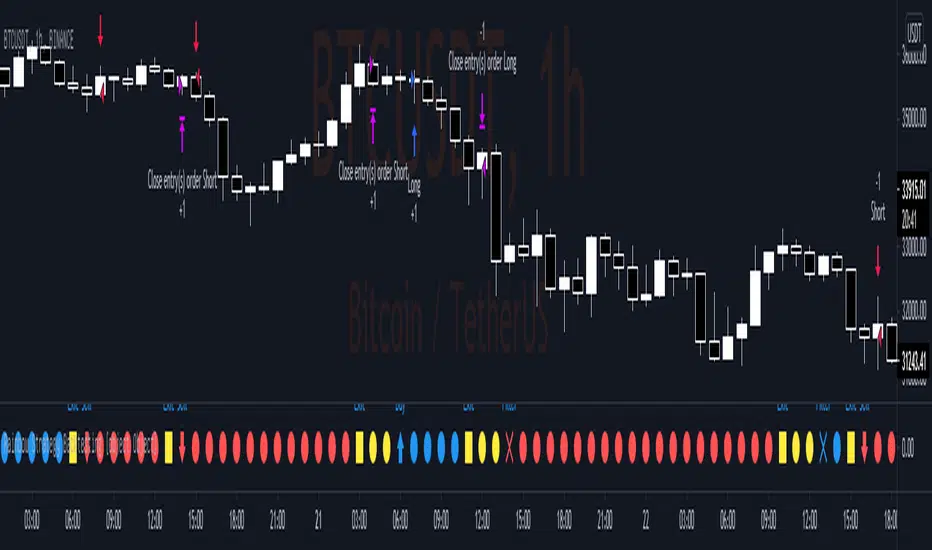

Rainbow Strategy BacktestingRainbow Strategy Backtesting base on "Rainbow Moving Average" Strategy as below:

1.Rainbow Moving Average setup

- Source: source of 1st MA

- Type: SMA/EMA

- Period: period of 1st MA

- Displacement: period of 2nd MA to 7th MA with source is previous MA

2.Trend Define

- Up Trend: Main MA moving at the top of Rainbow

- Down Trend: Main MA moving at the bottom of Rainbow

- Sideway: Main MA moving between the top and the bottom of Rainbow

3.Signal

- Buy Signal: When Rainbow change to Up Trend.

- Sell Signal: When Rainbow change to Down Trend.

- Exit: When Rainbow change to Sideway.

4.RSI Filter

- "Enable": Only signals have 1st RSI moving between Overbought and Oversold and 2nd RSI moving outside Middle Channel are accepted.

- The filter may help trader avoid bull trap, bear trap and choppy market.

5.Backtesting Infomation

- Ticker: BTCUSDT

- Timeframe: H1

- Rainbow parameter:

+ Source: hlc3

+ Type: SMA

+ Period: 12

+ Displacement: 3

- RSI Filter parameter:

+ Enable

+ 1st RSI filter: period 12, overbought 65, oversold 35

+ 2nd RSI filter: period 9, upper middle 56, lower middle 44

Session backtest toolWith this tool you can easily backtest your trading strategy. You can set the times of a day session and evening session separately. The days of the week were indicated at the bottom of the chart.

For me personally, this saves me a lot of time with back testing. Hopefully I can help you with this too

Bull And Bear Balance Strategy Backtest This new indicator analyzes the balance between bullish and

bearish sentiment.

One can cay that it is an improved analogue of Elder Ray indicator.

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

This modified strategy backtest from HPotter

1-2-3 Reversal Backtest StrategyThis is backtesting script.

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

MACD With Trend Filter: Visual Backtest Module TemplateSample Strategy: MACD Crossover with trend filter options

MA Filter : Price Close Above MA, Search for Buy, Price Close Below MA, Search for Sell

ADX Filter : Take trade only when ADX is above certain treshold

MACD Signal : MACD Cross above signal line while under 0 line indicate Buy Signal

MACD Cross below signal line while above 0 line indicate Sell Signal

-----------------------------

Using Alert Module:

Enable Alert --> Enable TV's alert and plot signal to chart

Alert Type --> Set to take Buy only, Sell only or Both alert

----------------------------

Using Backtest Module:

Enable Backtest --> Enable Backtest simulation

Backtest Type --> Set to take Buy only, Sell only or Both

SL Type -->

ATR : Set SL in ATR times Multiplier below/above entry price

Fixed : Set SL in fixed point below entry point (in 'Dollar'). e.g. for Stocks -> 0.5 equals to 50cent while for EURUSD currency -> 0.005 equal to 50 pips

HiLo Bar : Set SL at highest/lowest wick of previous bar plus/minus Fixed point. e.g. EURUSD HiLo=3 and Fixed Point = 0.0005, buy trade will place SL 5 Pips below lowest of previous 3 bar

SL ATR Period --> Set Lookback Period used for SL's ATR calculation

SL ATR Multi --> Set ATR Multiplier for SL

SL Fixed --> Set Fixed Level for SL (Use when SL Type is either Fixed or HiLo Bar)

SL Bar --> Set Number of previous bar to check for SL placement

TP RR Ratio --> Set TP based on RR multiplier. e.g. 2 means TP level will be twice further from entry point compared to Entry-SL distance.

Notes: The point is for preliminary testing, so it only supports 1 trade at a time and no Trailing Stop

----------------------------

Disclaimer:

This script main objective is to create my personal indicator template so that i just have to modify the indicator module for preliminary testing in future.

Testing Alert Module so i can re-use it as template in future study/indicator

Testing Visual Backtest Module so i can re-use it as template in future study/indicator

i believe using Strategy function is a better approach for this but the entry/exit level seems to be hit n miss (at least for me, still trying to figure what i did wrong)

also, i rather code the strategy in other platform where i can use the more accurate tick data if i want to validate backtest statistics.

My study scripts was built only to test/visualize an idea to see its viability and if it can be used to optimize existing strategy.

credit: ADX code are originally from "ADX and DI" by @BeikabuOyaji although i re-wrote so i can have cleaner read and use RMA instead of SMA

Back Week For BacktestIt is Backtest Calculator For Essential and Plus plan holders, the length of available intraday data is calculated as follows: from now to 6 weeks back multiplied by timeframe(in minutes), i.e. you can go 6 weeks back on the 1-minute chart, 12 weeks back on the 2-minute chart, 30 weeks back on the 5-minute chart, 90 weeks back on the 15-minute chart and so on. The higher timeframe is selected, the more intraday data is available.

This show creates a weekday label based on the data in the plans allowed by TradingView. This show creates a weekday label based on the data in the plans allowed by TradingView. How much data is available for Bar Replay? According to the article, we can replay 6 weeks backwards for a 1-minute chart. This indicator is a label that shows how far we can go back, consisting of multiplying each minute by 6 between 1 minute and 60 minutes.

1 minute => 6 week backtest

2 minutes => 12 week backtest

.....

15 minutes => 90 week backtest

...

59 minutes => 354 week backtest

Replica of TradingView's Backtesting Engine with ArraysHello everyone,

Here is a perfectly replicated TradingView backtesting engine condensed into a single library function calculated with arrays. It includes TradingView's calculations for Net profit, Total Trades, Percent of Trades Profitable, Profit Factor, Max Drawdown (absolute and percent), and Average Trade (absolute and percent). Here's how TradingView defines each aspect of its backtesting system:

Net Profit: The overall profit or loss achieved.

Total Trades: The total number of closed trades, winning and losing.

Percent Profitable: The percentage of winning trades, the number of winning trades divided by the total number of closed trades.

Profit Factor: The amount of money the strategy made for every unit of money it lost, gross profits divided by gross losses.

Max Drawdown: The greatest loss drawdown, i.e., the greatest possible loss the strategy had compared to its highest profits.

Average Trade: The sum of money gained or lost by the average trade, Net Profit divided by the overall number of closed trades.

Here's how each variable is defined in the library function:

_backtest(bool _enter, bool _exit, float _startQty, float _tradeQty)

bool _enter: When the strategy should enter a trade (entry condition)

bool _exit: When the strategy should exit a trade (exit condition)

float _startQty: The starting capital in the account (for BTCUSD, it is the amount of USD the account starts with)

float _tradeQty: The amount of capital traded (if set to 1000 on BTCUSD, it will trade 1000 USD on each trade)

Currently, this library only works with long strategies, and I've included a commented out section under DEMO STRATEGY where you can replicate my results with TradingView's backtesting engine. There's tons I could do with this beyond what is shown, but this was a project I worked on back in June of 2022 before getting burned out. Feel free to comment with any suggestions or bugs, and I'll try to add or fix them all soon. Here's my list of thing to add to the library currently (may not all be added):

Add commission calculations.

Add support for shorting

Add a graph that resembles TradingView's overview graph.

Clean and optimize code.

Clean up in a way that makes it easy to add other TradingView calculations (such as Sharpe and Sortino ratio).

Separate all variables, so they become accessible outside of calculations (such as gross profit, gross loss, number of winning trades, number of losing trades, etc.).

Thanks for reading,

OztheWoz

Strategy Backtesting Template [MYN]A few people have been asking me to share my backtesting template. Currently I use this as my starting point for validating existing strategies and developing new ones.

Features:

Trading Date Range

Trade Direction

4 progressive take profits with target percents and percentage of position to take profit on (Thanks adolgo)

Variable percentage Stop Loss

Automatic ProfitView Alert Syntax builder for Longs and Shorts

ADX checkbox to automatically add conditional logic to your strategy

HXRO Bot Backtest Time HighlightThis script allows you to highlight the HXROBot backtest interval with the possibility of fragmenting the view to better identify the key areas of your strategy

RePaNoCHa V4 [Backtest]This is the Backtest version of the previous one.

It's important to correctly set the "TICKS / PIPS CORRECTION" parameter in each different chart.

Enjoy!

Hull Trend with Kahlman Strategy BacktestA simple backtest version of a Hull Trend with Kahlman strategy

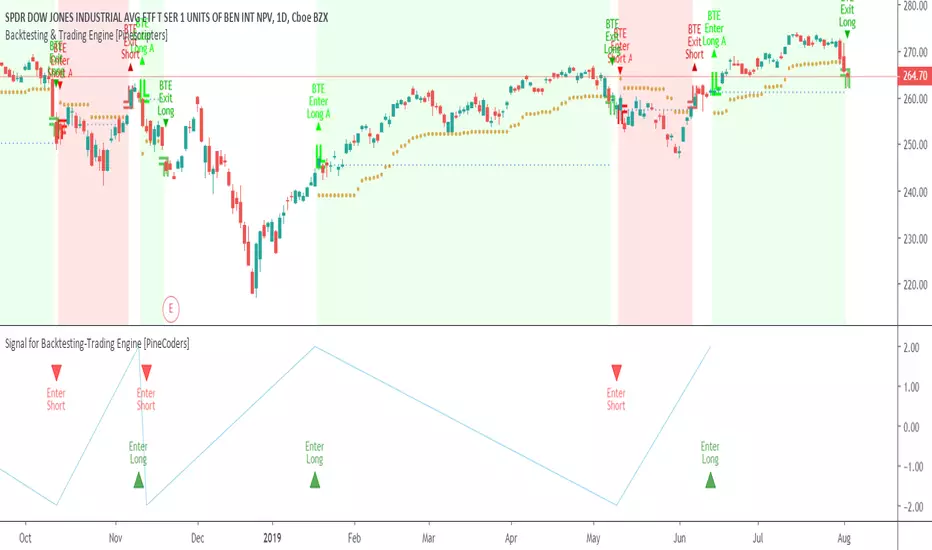

Signal for Backtesting-Trading Engine [PineCoders]This is a companion script to the PineCoders Backtesting-Trading Engine. It illustrates how to build a signal plot in another script, which can in turn be fed in the Engine to provide entry, exit, filter and stop information.

Connection to the Engine is done through its “External Indicator” input field at the very bottom of the Engine’s Settings/Inputs.

The Engine must be operating in study mode to be able to connect an external indicator to it.

The way this script builds the signal is straightforward, as you will see in the code. Two aspects are worth mentioning:

The “FudgeStop()” function used to fudge the stop value by one tick for the rare cases where it will match one of the protocol reserved values, i.e. 1, 2 or 3.

The priority and exclusivity given to the different types of signals in the signal-building “Signal = …” line. No two signals can be sent simultaneously through the signal plot, except for the entry and stop combination.

You can determine in this script’s Settings/Inputs the type of signals that will go through the signal plot.

This script respects the following protocol:

EXTERNAL SIGNAL PROTOCOL

Only one external indicator can be connected to a script; in order to leverage its use to the fullest, the engine provides options to use it as either an entry signal, an entry/exit signal or a filter. When used as an entry signal, you can also use the signal to provide the entry’s stop. Here’s how this works:

For filter state: supply +1 for bull (long entries allowed), -1 for bear (short entries allowed).

For entry signals: supply +2 for long, -2 for short.

For exit signals: supply +3 for exit from long, -3 for exit from short.

To send an entry stop level with an entry signal: Send positive stop level for long entry (e.g. 103.33 to enter a long with a stop at 103.33), negative stop level for short entry (e.g. -103.33 to enter a short with a stop at 103.33). If you use this feature, your indicator will have to check for exact stop levels of 1.0, 2.0 or 3.0 and their negative counterparts, and fudge them with a tick in order to avoid confusion with other signals in the protocol.

Remember that mere generation of the values by your indicator will have no effect until you explicitly allow their use in the appropriate sections of the Engine’s Settings/Inputs.

Look first. Then leap.

Smeared VCI BacktestThis is the strategy with backtest date range and trailing-stop / stop-loss for vitelot's Smeared VCI indicator:

Generalized SSL Backtest w/ TSSLStrategy with Backtest Date Range and Trailing-Stop / Stop-Loss for vitelot's indicator:

Linear Regression (Backtest / Trailing Stop)A Strategy with Backtest and Trailing Stop for Long/Short

Credits: Study by RafaelZioni - Thanks buddy!

Fisher Transform Multi-Timeframe (Backtest)This is the Backtest Strategy for mortdiggiddy's "Fisher Transform Multi-Timeframe"

For more details check his study:

Default Strategy Inputs (Forex / Crypto)The code in this post contains a set of default strategy inputs I use in new projects / backtests in Tradingview.

Full code commentary is available on the Backtest-Rookies website. To comply with house rules, I cannot post the direct link here.

Features

Trade Direction: So that you can limit the strategy for long only, short only or trade in both directions. It is important to note that when you select “Long Only”, you will still see Short signals on the chart. However, they are only used to close a position rather than reverse it. This is the default behaviour for strategies. The same applies to “Short Only”.

Date Ranges: So that you can isolate backtesting to specific periods of interest such as bull or bear markets.

Sessions: So you can easily get an idea of the expected results during your own session. You may also notice that performance of the strategy varies depending on which session it is deployed in.

Some example stop losses: It is not an exhaustive list but it should be enough to provide some inspiration for different types of stops that you can experiment with.

Happy Scripting. I hope the community finds it useful.