Average DownThis strategy has been published for a Pyramiding tutorial on the Backtest Rookies website.

For a full overview of the code and an introduction to Pyramiding check out our site.

Summary

The code example will create a simple script that allows us to average down whenever our portfolio is down x%. The idea will be to bring our average cost down so that we can still exit with a profit when conditions improve. With this in mind, the strategy shall also have a simple take profit exit at x% above our average price.

Inputs

Target Loss to Average Down (%) : This is the target percentage level will trigger us to average down. In other words, if we have a close below this level from our average buying price, we will average down.

Target Take Profit : A standard take profit percentage level. Use this to set how much profit you will target.

% Of Current Holdings to Buy : Is the number of shares/contracts we will aim to buy when we average down. 50 will mean we buy 50% of our current holdings. So if we have 100 shares, then we buy 50 when we average down.

SMA Period : Defines our SMA lookback period. Our strategy will enter the first/initial position when we have a close above our SMA level.

Cerca negli script per "backtest"

Dane: RSI MACD StrategyRSI / MACD Divergence Strategy . Published for customer verification and acceptance. Unfortunately, access can only be provided to the customer.

For those interested in custom development services, please visit the backtest-rookies (.com) website for more information.

Features

RSI & Price divergence detection

Open a trade window when trade conditions are met

Enter the trade on confirmation

Stop losses / take profit custom levels based of daily pivot values

Farooq: Bollinger Bands StrategyBollinger Band Strategy developed as a service and published for customer verification and acceptance.

If you are interested in development sevices, please either DM me or visit the Backtest Rookies webiste. If you are looking for free and open source scripts, there are some avaible both on the site and our Tradingview profile.

Overview

Bollinger Strategy base

Added additional, customizable 2nd and 3rd deviation levels

Added ability to switch between long only, short only or long & short strategies

Added option to select which deviation level to buy at

Added option to select which deviation level to sell at

Achmed: Heikinashi Open/CloseHeikinashi strategy that looks for large % changes between the open and close of a bar or the previous open and current close.

This strategy is published for customer verification and acceptance. As such, only the customer shall be granted access.

Features

Heikinashi based strategy that is run on a normal candle chart. This ensures accurate backtest results.

Heikinashi chart is plotted on a subplot

Inputs for defining different entry conditions

Switches to turn different entry criteria on / off

Trailing stop which trails the Heikinashi prices.

Trailing stop plotting on the subplot

Sathya: Short the highShort the High

This script has been developed as a professional service and is published only for customer verification/acceptance.

If you are interested in development services, either PM me or visit the Backtest-Rookies website (.com)

Summary

This strategy will attempt to take a short position within a time window only after X consecutive up days. Once X consecutive up days have been detected, two windows will open up. The first window tracks the high of the day. The second window will attempt to short the high of the day if price retests it.

Features

Tracking of consecutive up days using intra-day data

Opening a trade window when consecutive up days are detected

Tracking the high of a sub-session (user definable)

Shorting the high during a second sub-session (user definable)

Stop losses and take profits

End of sub-session close out option.

Buffer range from high of the day. So price does not need to retouch the high but can come with x rupees.

Background coloring of sub-sessions so it is easy to track trades

Sathya: BreakoutIntra-day Breakout Strategy: Developed as a professional service and published for customer verification/acceptance.

If you are interested in development services, please visit the backtest-rookies website.

Features

Entry on a breakout from second candle of the session

Breakout tolerance zone to prevent false breaks

Take profit

Stop loss

Timed exit (exit at a specific time of day)

nATR Reversal StrategyATR Reversal Strategy that has been extended to add an additional ATR based stoploss, trailing stop and take profit.

This script was developed as part of a professional development service. It is published for customer verification and acceptance.

For people interested in professional services, please visit the backtest-rookies (.com) website.

Features

nATR based Stop Loss added

nATR based Trailing stop added

nATR based Take profit added

Switches for each exit type to turn them on or off in the strategy

Plotting of all exit levels on the chart

Prevent reversing when using newly added exits.

Allow reversing when all exit switches are off and opposite long/short conditions are met.

CB SDB HK VOL Strategy Heikin-Ashi / Volume Filter Strategy

Custom development published for customer verification.

If you are interested in development services, please visit the backtest-rookies website to find out more.

Naresh - iJPASIMPORTANT NOTE

This strategy has been developed as a professional service. It was published only or testing and verification by the customer. As such, access cannot be granted to anyone else. Sorry about that!

Other open source scripts are available on the BacktestRookies profile.

Intra-day Japanese Candlestick Price Action Strategy

An intraday strategy which focuses on analyzing price action of the opening 3 bars to make trading decisions.

Once certain criteria are met, entry and exit targets are set and left until they are hit else we reset and start again on a new day.

Emmanuel - Squeeze StrategyPlease Read

This strategy has been developed as a professional service. It was published only or testing and verification by the customer. As such, access cannot be granted to anyone else. Sorry about that!

Other open source scripts are available on the BacktestRookies profile.

Squeeze Strategy

Entry Conditions: Undisclosed

Position Sizing: % Risk of Equity when stop loss is hit

Position Management: Take off 50%

Position Management: Move to break even

Exit Conditions: Undisclosed

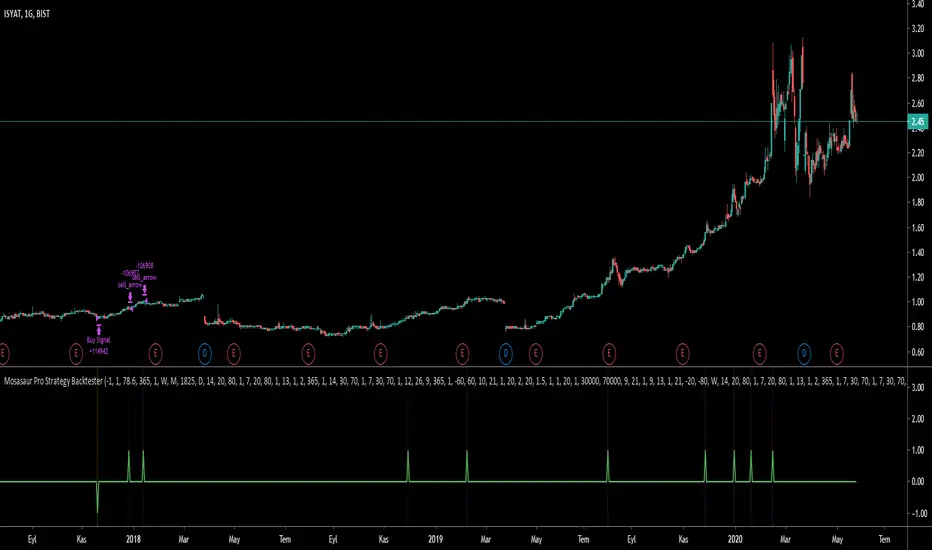

Mosasaur Pro BacktesterBacktester indicator for Mosasaur ◬ | Comprehensive & Profitable Trading Setup Builder available for free here.

Scroll all the way down in the setting menu to adjust the backtesting strategy.

Current features:

Find out the backtesting results for your customized strategy.

Set alerts for strong buy, buy, strong sell and sell signals.

Option for waiting fractal candle stick pattern before entering or exiting.

All features and setups used can be found on this tradingview page.

This backtester has settings of:

Setting 1 lets user select the source for putting a buy order.

Setting 2 lets user select the source for putting a sell order.

Setting 3 defines how much percent user wants to risk per trade to buy.

Setting 4 defines maximum possible trades for buying.

Setting 5 lets user only buy with fractal bottom after a buy signal has been found.

Setting 6 lets user only sell with fractal top after a sell signal has been found.

Setting 7 lets user only buy if the pre defined time period has elapsed on the chart.

Setting 8 lets user only sell if the pre defined time period has elapsed on the chart.

Setting 9 lets user only buy with a strong buy signal (orange color).

Setting 10 lets user only sell with a strong sell signal (purple color).

Setting 11 defines the time period to be elapsed to trigger a buy.

Setting 12 defines the time period to be elapsed to trigger a sell.

Upcoming features:

Advanced pre-defined strategies for user to select from. This will also auto adjust the setups and time frames being combined.

Stop Loss and Stop to Trailing options for the strategy.

Stop Loss and Stop to Trailing alerts.

Defining risk/reward ratio before entering the trade.

~Bo

Founder of Megalodon Indicators

Backtests Are BrokenThis script demonstrates a fatal flaw with Trading View backtests involving trailing stops. Trading View assumes the most optimistic case for trailing stops, always giving you the best case high/low of a bar instead of the worst or average case. Within a bar, the price could reverse against your position after the open and trigger your trailing stop for a loss before the price goes in your favor, but Trading View backtests do not consider this and instead always give you the best case returns. This allows a trivial strategy to appear as though it would perform miracles.

This strategy enters on a random bar and sets a trailing stop triggered one tick better than the current price with 0 trailing distance. Trading View then generously gives this strategy the difference between the open price and best possible wick as a profit. The only way this strategy can lose money in simulation is if the price goes straight down after entry and never retraces. It works on all symbols on all timeframes due to this systematic problem with the Trading View backtester.

Backtesting Period Selector | ComponentDescription

It's nice to quickly be able to set the backtesting period when writing strategies.

To make this process faster I wrote a simple 'component'.

So this is not a strategy but rather code you can plug-into your strategy and use

if you need that specific functionality.

Then it's just a matter of selecting which dates you want to backtest.

You can also chose to color the background to visually show the testing period.

Unfortunately, the background color is fixed at 'blue' for now.

Ps. I like the idea of writing small components to be pluged into other strategies

I'll try to develop this idea a bit further and see how small pieces of code can

easily provide specific functionality to assist and make deving strategies a bit less 'Pineful'.

Usage

First copy the instructed part of the component code over to your strategy.

Next, use the testPeriod() function to limit strategies to the specified backtesting period.

Example usage:

if testPeriod()

strategy.entry("LE", strategy.long)

Todo / Improvements

There are many ways to improve this component and I'm not a very good coder so this is a very crude solutions.

Anyway, here are some things which would be nice to improve:

1. Enable color selection so that the user can choose the background color of his own liking.

2. Improve naming of variables.

3. Test for ilogical choices, such as test period start being at a later date, than test period stop.

4. Account for time zones.

As always, any feedback, corrections or thoughts are very much welcome!

/pbergden

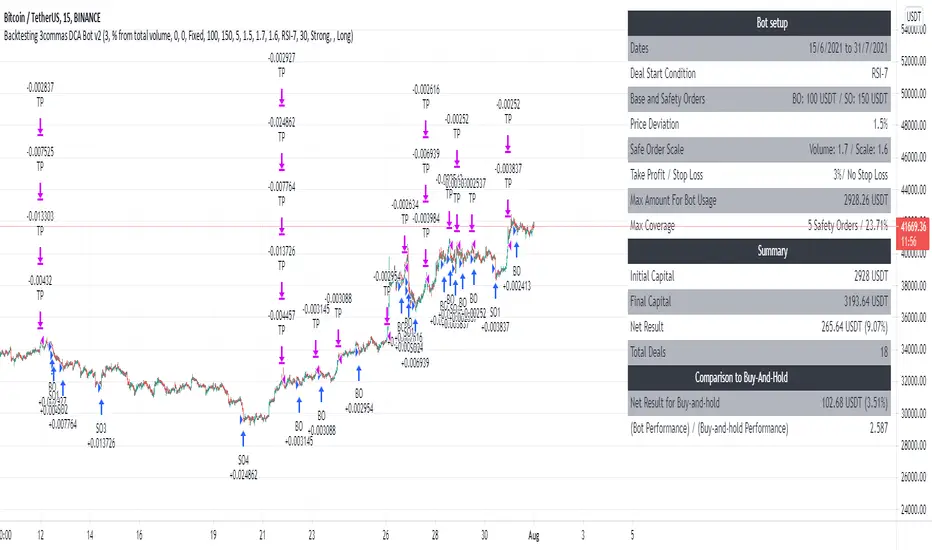

Backtesting 3commas DCA Bot v2Updating previously published simulated 3commas DCA logic with a sexier insert and more meaningful default parameters.

Backtest Signal To Noise This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

© HPotter 05/01/2021

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

Thank you for idea BlockchainYahoo

WARNING:

- For purpose educate only

- This script to change bars colors.

Strategy - Backtest Uber Baseline [UTS]Backtesting of Uber Baseline

equity 50k

2% Risk

optimized on USD pairs

start year and month input

ATR based Stop-Loss

no trade on Overshoot Up/Down

no trade against the trend

---

DM / Tip / Subscribe for access

[BACKTEST]Traders Dynamic Index Indicator Alert by JustUncleLBy request, this script is a "strategy" version of my "Traders Dynamic Index Indicator Alert" script, made available for backtesting to help find optimal trade settings for a particular asset.

RSI Alligator Strategy [forked from jedireza]Backtester for RSI alligator is Williams Alligator strategy using Relative Strength Index to predict entries

Original script can be found at

Vortex Ocillator - backtestingbacktesting strategy for the vortex oscilator indicator, slightly modified on this version so that the buy and sell signals work with the backtesting and are consistant

original idea i posted by accident

the script with alerts

not intended to be financial advice, strategy is for made for testing

Biffy

Backtest EngineThis is a simple backtest engine for your trading strategies. The idea behind this script is to make testing new strategies as easy as possible. Parameters such as take profit/stop loss and time period are built into the script and are customisable by the user via the settings interface. The only coding is to set the entry and exit conditions. Users need not touch any code beyond line 30.

For this post, I have used a 50/200 SMA crossover to demonstrate the ease of use for this script.

The features of this script include:

Backtest period start

Number of days until backtest period end

Take profit and stop loss % (via settings)

Programmable long and short entry/exit

Anti duplicate system (for entry conditions that are continuously satisfied, the engine will only make 1 trade until the is exit condition is satisfied).

DISCLAIMER: The strategy in this post is only a placeholder. The TP/SL levels are set to showcase the functionality of the engine and are in no means optimal settings.

Hope this helps! Feel free to ask any questions about the engine and happy coding!