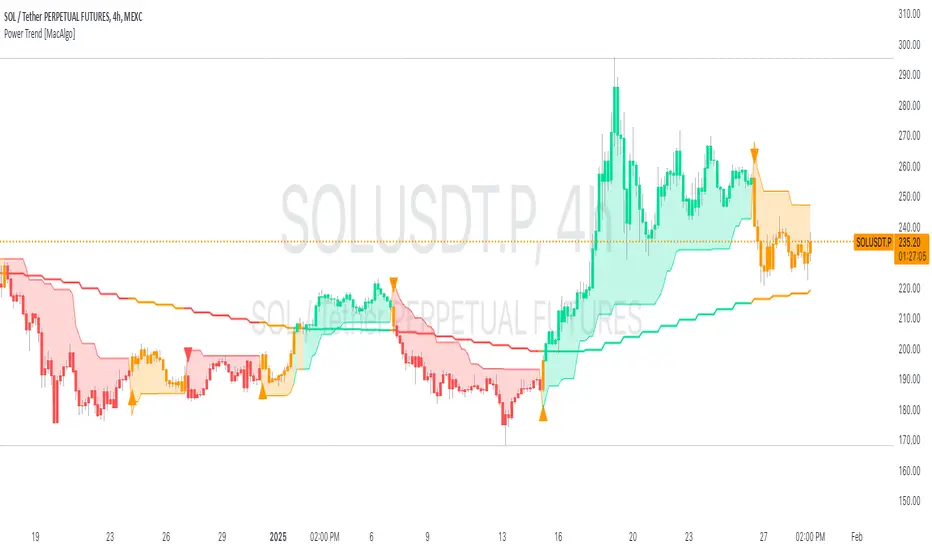

Power Trend [MacAlgo]Description:

The Power Trend Indicator is a sophisticated technical analysis tool that overlays on your trading charts to identify prevailing market trends. It utilizes a combination of ATR-based trend calculations, moving averages, volume analysis, and momentum indicators to generate reliable buy and sell signals. Additionally, it offers customizable settings to adapt to various trading styles and timeframes.

Key Features:

Adaptive ATR Calculation: Automatically adjusts the ATR (Average True Range) period and multiplier based on the selected timeframe for more accurate trend detection.

Dynamic Trend Lines: Plots continuous trend lines with color-coded bars to visually represent bullish and bearish trends.

Buy/Sell Signals: Generates standard and power buy/sell signals to help you make informed trading decisions.

Volume Analysis: Incorporates average buy and sell volumes to identify strong market movements.

Multiple Timeframe Support: Automatically adjusts the indicator's timeframe or allows for manual selection to suit your trading preferences.

Highlighting: Highlights trending bars for easy visualization of market conditions.

Alerts: Customizable alert conditions to notify you of potential trading opportunities in real-time.

How it Works:

1. ATR-Based Trend Calculation:

ATR Period & Multiplier: Calculates ATR based on user-defined periods and multipliers, dynamically adjusting according to the chart's timeframe.

Trend Determination: Identifies trends as bullish (1) or bearish (-1) based on price movements relative to ATR-based upper (up) and lower (dn) trend lines.

2. Moving Averages:

EMA & SMA: Calculates exponential and simple moving averages to smooth price data and identify underlying trends.

AlphaTrend Line: Combines a 50-period EMA and a 30-period SMA on a 4-hour timeframe to create the AlphaTrend line, providing a robust trend reference.

3. Volume Analysis:

Buy/Sell Volume: Differentiates between buy and sell volumes to gauge market strength.

Average Volume: Compares current volume against average buy/sell volumes to detect significant market movements.

4. Momentum Indicators:

RSI, MACD, OBV: Incorporates Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), and On-Balance Volume (OBV) to assess momentum and confirm trend strength.

5. Signal Generation:

Standard Signals: Basic buy and sell signals based on trend crossovers.

Power Signals: Enhanced signals requiring multiple conditions (e.g., increased volume, momentum confirmation) for higher confidence trades.

Customization Options:

Tailor the Power Trend Indicator to your specific trading needs with the following settings:

ATR Period: Set the period for ATR calculation (default: 8).

ATR Multiplier: Adjust the ATR multiplier to fine-tune trend sensitivity (default: 3.0).

Source: Choose the price source (e.g., HL2, Close) for calculations.

Change ATR Calculation Method: Toggle between different ATR calculation methods.

Show Buy/Sell Signals: Enable or disable the display of buy and sell signals on the chart.

Highlighting: Turn on or off the bar highlighting feature.

Timeframe Adjustment: Choose between automatic timeframe adjustment or manually set

the indicator's timeframe.

Manual Indicator Timeframe: If manual adjustment is selected, specify the desired timeframe (default: 60 minutes).

Visual Components:

Trend Lines: Continuous lines representing the current trend, color-coded for easy identification (green for bullish, red for bearish, orange for neutral).

Bar Coloring: Bars are colored based on the current trend and its relationship to the AlphaTrend line.

Buy/Sell Triangles: Triangular markers appear on the chart to indicate buy and sell signals.

Power Signals: Larger triangles highlight strong buy and sell opportunities based on multiple confirming factors.

Highlighting: Transparent overlays highlight trending areas to enhance visual clarity.

Alerts:

Stay informed with customizable alerts that notify you of important market movements:

SuperTrend Buy/Sell: Alerts when standard buy or sell signals are generated.

Power Buy/Sell Alerts: Notifications for strong buy or sell signals based on comprehensive conditions.

Trend Direction Change: Alerts when the trend changes from bullish to bearish or vice versa.

How to Use:

Add to Chart: Apply the Power Trend Indicator to your preferred trading chart on TradingView.

Configure Settings: Adjust the input parameters to match your trading style and the timeframe you are analyzing.

Analyze Trends: Observe the trend lines, bar colors, and AlphaTrend line to understand the current market trend.

Follow Signals: Look for buy and sell signals or power signals to identify potential entry and exit points.

Set Alerts: Enable alerts to receive real-time notifications of significant trading opportunities.

Adjust as Needed: Fine-tune the settings based on market conditions and your trading experience.

Important Notes:

Backtesting: While the Power Trend Indicator is built using robust technical analysis principles, it's essential to backtest and validate its performance within your trading strategy.

Market Conditions: The indicator performs best in trending markets. In sideways or highly volatile markets, signal reliability may vary.

Risk Management: Always employ proper risk management techniques when trading based on indicator signals to protect your capital.

Disclaimer:

This indicator is intended for educational purposes only and does not provide financial advice or guarantee future performance. Trading involves risk, and past results are not indicative of future outcomes. Always conduct your own analysis and risk management.

Cerca negli script per "backtesting"

Sunil 2 Bar Breakout StrategyDetailed Explanation of the Sunil 2 Bar Breakout Strategy

Introduction

The Sunil 2 Bar Breakout Strategy is a simple yet effective price-action-based approach designed to identify breakout opportunities in financial markets. This strategy analyzes the movement of the last three candles to detect momentum and initiates trades in the direction of the breakout. It is equipped with a built-in stop-loss mechanism to protect capital, making it suitable for traders looking for a structured and disciplined trading system.

The strategy works well across different timeframes and asset classes, including indices, stocks, forex, and cryptocurrencies. Its versatility makes it ideal for both intraday and swing trading.

Core Concept

The strategy revolves around two primary conditions: breakout identification and risk management.

Breakout Identification:

Long Trade Setup: The strategy identifies bullish breakouts when:

The current candle's closing price is higher than the previous candle's closing price.

The high of the previous candle is greater than the highs of the two candles before it.

Short Trade Setup: The strategy identifies bearish breakouts when:

The current candle's closing price is lower than the previous candle's closing price.

The low of the previous candle is lower than the lows of the two candles before it.

Risk Management:

Stop-Loss: For each trade, a stop-loss is automatically set:

For long trades, the stop-loss is set to the low of the previous candle.

For short trades, the stop-loss is set to the high of the previous candle.

This ensures that losses are minimized if the breakout fails.

Exit Logic:

The trade is closed automatically when the stop-loss is hit.

This approach maintains discipline and prevents emotional trading.

Strategy Workflow

Entry Criteria:

Long Entry: A long trade is triggered when:

The current close is greater than the previous close.

The high of the previous candle exceeds the highs of the two candles before it.

Short Entry: A short trade is triggered when:

The current close is less than the previous close.

The low of the previous candle is below the lows of the two candles before it.

Stop-Loss Placement:

For long trades, the stop-loss is set at the low of the previous candle.

For short trades, the stop-loss is set at the high of the previous candle.

Trade Management:

Trades are exited automatically if the stop-loss level is hit.

The strategy avoids re-entering trades until new breakout conditions are met.

Default Settings

Position Sizing:

The default position size is set to 1% of the account equity. This ensures proper risk management and prevents overexposure to the market.

Stop-Loss:

Stop-loss levels are automatically calculated based on the previous candle’s high or low.

Timeframes:

The strategy is versatile and works across multiple timeframes. However, it is recommended to test it on 15-minute, 1-hour, and daily charts for optimal performance.

Key Features

Automated Trade Execution:

The strategy handles both trade entry and exit automatically based on pre-defined conditions.

Built-In Risk Management:

The automatic stop-loss placement ensures losses are minimized on failed breakouts.

Works Across Markets:

The strategy is compatible with a wide range of instruments, including indices, stocks, forex, and cryptocurrencies.

Clear Signals:

Entry and exit points are straightforward and based on objective conditions, reducing ambiguity.

Versatility:

Can be used for both day trading and swing trading, depending on the chosen timeframe.

Best Practices for Using This Strategy

Backtesting:

Test the strategy on your chosen instrument and timeframe using TradingView's Strategy Tester to evaluate its performance.

Market Conditions:

The strategy performs best in trending markets or during periods of high volatility. Avoid using it in range-bound or choppy markets.

Position Sizing:

Use the default position size (1% of equity) or adjust based on your risk tolerance and account size.

Instrument Selection:

Focus on instruments with good liquidity and volatility, such as indices (e.g., NIFTY, BANKNIFTY), forex pairs, or major cryptocurrencies (e.g., Bitcoin, Ethereum).

Potential Enhancements

To make the strategy even more robust, consider adding the following optional features:

Stop-Loss Multiplier:

Allow users to customize the stop-loss distance as a multiple of the default level (e.g., 1.5x the low or high of the previous candle).

Take-Profit Levels:

Add user-defined take-profit levels, such as a fixed risk-reward ratio (e.g., 1:2).

Time Filter:

Include an option to restrict trading to specific market hours (e.g., avoid low-liquidity times).

Conclusion

The Sunil 2 Bar Breakout Strategy is an excellent tool for traders looking to capitalize on breakout opportunities while maintaining disciplined risk management. Its simplicity, combined with its effectiveness, makes it suitable for traders of all experience levels. By adhering to the clearly defined rules, traders can achieve consistent results while avoiding emotional trading decisions.

This strategy is a reliable addition to any trader’s toolbox and is designed to work seamlessly across different market conditions and instruments.

[blackcat] L3 Bullish Grab SignalOVERVIEW

The " L3 Bullish Grab Signal" indicator is designed to identify bullish trends and potential buying opportunities in the market. It uses a combination of moving averages and custom calculations to generate signals. The indicator is set to not overlay on the price chart, meaning it will have its own panel below the main chart, and it updates based on the specified timeframe.

FEATURES

Input Parameters:

shortEmaPeriod: Default value is 13, used for the shorter-term EMA.

longEmaPeriod: Default value is 34, used for the longer-term EMA.

signalEmaPeriod: Default value is 5, used to smooth the difference between the short and long EMAs.

lookbackPeriod: Default value is 60, used to look back over a certain number of bars for specific calculations.

Variable Calculations:

priceWeightedAverage: Calculated as (close * 2 + high + low) / 4 * 10, a custom price point.

shortEma: EMA of priceWeightedAverage over the short period.

longEma: EMA of priceWeightedAverage over the long period.

signalEma: EMA of the difference between shortEma and longEma, smoothed over the signalEmaPeriod.

oscillatorValue: Calculated as 2 * (shortEma - longEma - signalEma) * 5.5, a custom oscillator.

positiveOscillatorValue: Positive part of oscillatorValue, setting negative values to zero.

bullishSignal: True when positiveOscillatorValue increases and was previously negative.

confirmedBullishSignal: True when the bullish signal is confirmed by certain conditions involving the oscillator values and price increases.

priceIncreaseThreshold: Checks if the close price increased by more than 7% from the previous bar.

strongBullishSignal: Combines the bullish signal with the confirmed signal and the price increase threshold.

confirmedStrongBullishSignal: When all conditions for a strong bullish signal are met.

weakBullishSignal: Bullish signal that doesn't meet the strong criteria but still shows some strength.

Plotting:

Oscillator Value: Plots the raw oscillator value in white.

Positive Oscillator Value: Plots only the positive part of the oscillator value in white.

Strong Bullish Signal Stick: Plots a red candlestick when a strong bullish signal is confirmed, using the highest positive oscillator value over the lookback period.

Bullish Signal Stick: Plots a white candlestick for a bullish signal that isn't necessarily strong.

Weak Bullish Signal Stick: Plots a green candlestick for a weak bullish signal.

Positive Trend: Plots yellow candlesticks when the oscillator value is positive.

Negative Trend: Plots fuchsia candlesticks when the oscillator value is negative.

Numbers on Candles: Represents the breakout strength as a percentage change in price.

HOW TO USE

Install the Script: Add the script to your TradingView chart.

Customize Inputs:

Adjust the shortEmaPeriod, longEmaPeriod, signalEmaPeriod, and lookbackPeriod as needed.

Interpret the Charts:

Red Candles: Indicate a strong bullish trend, suggesting a potential buying opportunity.

White Candles: Indicate bullish signals that are not as strong but still suggest a buying opportunity.

Green Candles: Indicate weak bullish signals, suggesting a possible buying opportunity but with less confidence.

Yellow Candles: Indicate a positive trend, suggesting the market is in an uptrend.

Fuchsia Candles: Indicate a negative trend, suggesting the market is in a downtrend.

Numbers on Candles: Show the breakout strength as a percentage change in price.

Analyze Trends and Signals:

Use red candles to identify strong bullish signals, especially if the price has increased by more than 7% from the previous bar.

Monitor white and green candles for potential entries with lower confidence.

Avoid trading during fuchsia candles, as the market is in a downtrend.

MARKET MEANING AND TRADING USAGE

Strong Bullish Signal (Red Candles): Indicates a significant price increase and momentum, suggesting a strong buying opportunity.

Bullish Signal (White Candles): Suggests a buying opportunity but with less confidence compared to strong signals.

Weak Bullish Signal (Green Candles): Indicates a possible buying opportunity with even lower confidence.

Positive Trend (Yellow Candles): Suggests the market is in an uptrend.

Negative Trend (Fuchsia Candles): Suggests the market is in a downtrend.

Trading Strategy:

Buy: When a strong bullish signal is confirmed (red candle), especially if the price has increased by more than 7% from the previous bar.

Monitor: Watch for bullish signals (white candles) and weak bullish signals (green candles) for potential entries with lower confidence.

Avoid: During negative trends (fuchsia candles), as the market is in a downtrend.

LIMITATIONS

Simplicity: The implementation is based on a combination of moving averages and custom calculations, which might not capture all aspects of market dynamics.

Close Price Dependency: Uses close prices to determine trends and signals, which might not reflect intrabar price movements and trade imbalances accurately.

Historical Data: The script is based on historical data and does not guarantee future performance.

NOTES

Educational Tool: The script is designed for educational purposes and should not be considered financial advice.

Backtesting: Users are encouraged to backtest the strategy on a demo account before applying it to live trades.

Complementary Use: Best used in conjunction with other indicators and analysis methods for more accurate trading decisions.

THANKS

Special thanks to the TradingView community for their support and feedback.

Weekly Trading StrategyStrategy Overview:

This trading strategy is designed for short-term trades over weekly intervals, utilizing the combination of Simple Moving Averages (SMA) for trend identification and the Relative Strength Index (RSI) for overbought/oversold conditions. It aims to capitalize on momentum shifts while mitigating the risk of entering a market at extreme points.

Key Components:

Fast SMA (9 periods): Acts as a short-term trend indicator, providing insights into quick price changes.

Slow SMA (21 periods): Represents a longer-term trend, smoothing out price fluctuations to show a more stable trend line.

RSI (14 periods): An oscillator that measures the speed and change of price movements, helping to identify potential reversal points.

Entry Signals:

Buy Signal:

Condition 1: The fast SMA (9 periods) crosses above the slow SMA (21 periods), indicating a potential upward trend shift.

Condition 2: RSI falls below 30, suggesting the asset is potentially oversold and due for a correction upwards.

Sell Signal:

Condition 1: The fast SMA crosses below the slow SMA, signaling a possible downward trend shift.

Condition 2: RSI climbs above 70, indicating the asset might be overbought and could pull back.

Strategy Execution:

Timeframe: This strategy is optimized for a weekly chart (W), where each bar or candle represents one week of trading data.

Alert System: Alerts can be set up for buy and sell signals, allowing traders to react promptly to market conditions without constant chart monitoring.

Risk Management:

This strategy includes inherent risk management by avoiding trades when the market shows extreme conditions via RSI. However, traders should also consider:

Position sizing based on account size and risk tolerance.

Setting stop-loss orders to manage potential losses if the market moves against the position.

Considering additional market analysis or indicators for confirmation before executing trades.

Considerations:

Backtesting: Before live trading, backtest the strategy on historical data to assess performance across different market conditions.

Adaptation: Market dynamics change, so periodic review and adjustment of SMA periods and RSI thresholds might be necessary.

Complementary Analysis: Enhance this strategy with fundamental analysis or other technical indicators for a more robust trading approach.

This strategy is suited for traders looking for weekly swings in the market, balancing between following the trend and spotting potential reversals. However, like all trading strategies, it should not be used in isolation but as part of a broader trading plan.

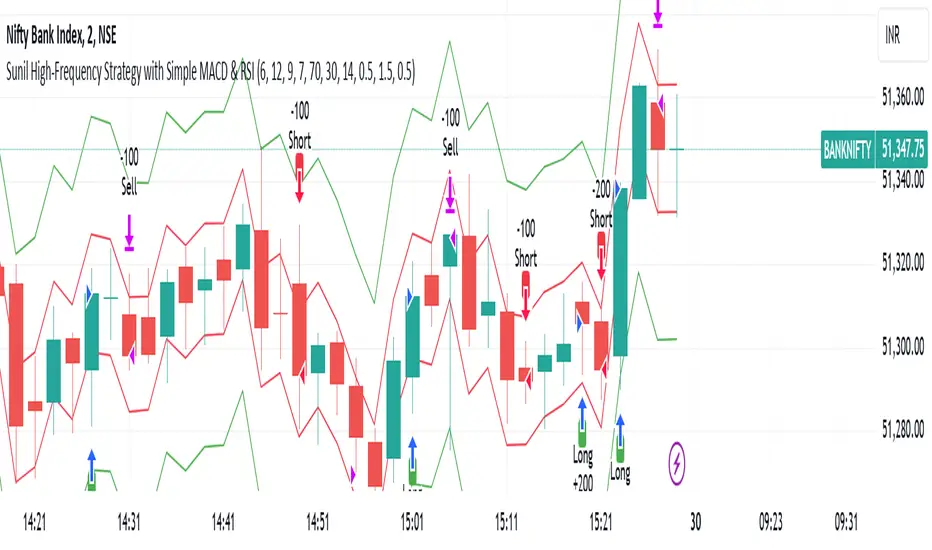

Sunil High-Frequency Strategy with Simple MACD & RSISunil High-Frequency Strategy with Simple MACD & RSI

This high-frequency trading strategy uses a combination of MACD and RSI to identify quick market opportunities. By leveraging these indicators, combined with dynamic risk management using ATR, it aims to capture small but frequent price movements while ensuring tight control over risk.

Key Features:

Indicators Used:

MACD (Moving Average Convergence Divergence): The strategy uses a shorter MACD configuration (Fast Length of 6 and Slow Length of 12) to capture quick price momentum shifts. A MACD crossover above the signal line triggers a buy signal, while a crossover below the signal line triggers a sell signal.

RSI (Relative Strength Index): A shorter RSI length of 7 is used to gauge overbought and oversold market conditions. The strategy looks for RSI confirmation, with a long trade initiated when RSI is below the overbought level (70) and a short trade initiated when RSI is above the oversold level (30).

Risk Management:

Dynamic Stop Loss and Take Profit: The strategy uses ATR (Average True Range) to calculate dynamic stop loss and take profit levels based on market volatility.

Stop Loss is set at 0.5x ATR to limit risk.

Take Profit is set at 1.5x ATR to capture reasonable price moves.

Trailing Stop: As the market moves in the strategy’s favor, the position is protected by a trailing stop set at 0.5x ATR, allowing the strategy to lock in profits as the price moves further.

Entry & Exit Signals:

Long Entry: Triggered when the MACD crosses above the signal line (bullish crossover) and RSI is below the overbought level (70).

Short Entry: Triggered when the MACD crosses below the signal line (bearish crossover) and RSI is above the oversold level (30).

Exit Conditions: The strategy exits long or short positions based on the stop loss, take profit, or trailing stop activation.

Frequent Trades:

This strategy is designed for high-frequency trading, with trade signals occurring frequently as the MACD and RSI indicators react quickly to price movements. It works best on lower timeframes such as 1-minute, 5-minute, or 15-minute charts, but can be adjusted for different timeframes based on the asset’s volatility.

Customizable Parameters:

MACD Settings: Adjust the Fast Length, Slow Length, and Signal Length to tune the MACD’s sensitivity.

RSI Settings: Customize the RSI Length, Overbought, and Oversold levels to better match your trading style.

ATR Settings: Modify the ATR Length and multipliers for Stop Loss, Take Profit, and Trailing Stop to optimize risk management according to market volatility.

Important Notes:

Market Conditions: This strategy is designed to capture smaller, quicker moves in trending markets. It may not perform well during choppy or sideways markets.

Optimizing for Asset Volatility: Adjust the ATR multipliers based on the asset’s volatility to suit the risk-reward profile that fits your trading goals.

Backtesting: It's recommended to backtest the strategy on different assets and timeframes to ensure optimal performance.

Summary:

The Sunil High-Frequency Strategy leverages a simple combination of MACD and RSI with dynamic risk management (using ATR) to trade small but frequent price movements. The strategy ensures tight stop losses and reasonable take profits, with trailing stops to lock in profits as the price moves in favor of the trade. It is ideal for scalping or intraday trading on lower timeframes, aiming for quick entries and exits with controlled risk.

Long Position with 1:3 Risk Reward and 20EMA CrossoverThe provided Pine Script code implements a strategy to identify long entry signals based on a 20-EMA crossover on a 5-minute timeframe. Once a buy signal is triggered, it calculates and plots the following:

Entry Price: The price at which the buy signal is generated.

Stop Loss: The low of the previous candle, acting as a risk management tool.

Take Profit: The price level calculated based on a 1:3 risk-reward ratio.

Key Points:

Buy Signal: A buy signal is generated when the current 5-minute candle closes above the 20-EMA.

Risk Management: The stop-loss is set below the entry candle to limit potential losses.

Profit Target: The take-profit is calculated based on a 1:3 risk-reward ratio, aiming for a potential profit three times the size of the risk.

Visualization: The script plots the entry price, stop-loss, and take-profit levels on the chart for visual clarity.

Remember:

Backtesting: It's crucial to backtest this strategy on historical data to evaluate its performance and optimize parameters.

Risk Management: Always use appropriate risk management techniques, such as stop-loss orders and position sizing, to protect your capital.

Market Conditions: Market conditions can change, and strategies that worked in the past may not perform as well in the future. Continuously monitor and adapt your strategy.

By understanding the core components of this script and applying sound risk management principles, you can effectively use it to identify potential long entry opportunities in the market.

[blackcat] L1 Simple Dual Channel Breakout█ OVERVIEW

The script " L1 Simple Dual Channel Breakout" is an indicator designed to plot dual channel breakout bands and their long-term EMAs on a chart. It calculates short-term and long-term moving averages and deviations to establish upper, lower, and middle bands, which traders can use to identify potential breakout opportunities.

█ LOGICAL FRAMEWORK

Structure:

The script is structured into several main sections:

• Input Parameters: The script does not explicitly define input parameters for the user to adjust, but it uses default values for short_term_length (5) and long_term_length (181).

• Calculations: The calculate_dual_channel_breakout function performs the core calculations, including the blast condition, typical price, short-term and long-term moving averages, and dynamic moving averages.

• Plotting: The script plots the short-term bands (upper, lower, and middle) and their long-term EMAs. It also plots conditional line breaks when the short-term bands cross the long-term EMAs.

Flow of Data and Logic:

1 — The script starts by defining the calculate_dual_channel_breakout function.

2 — Inside the function, it calculates various moving averages and deviations based on the input prices and lengths.

3 — The function returns the calculated bands and EMAs.

4 — The script then calls this function with predefined lengths and plots the resulting bands and EMAs on the chart.

5 — Conditional plots are added to highlight breakouts when the short-term bands cross the long-term EMAs.

█ CUSTOM FUNCTIONS

The script defines one custom function:

• calculate_dual_channel_breakout(close_price, high_price, low_price, short_term_length, long_term_length): This function calculates the short-term and long-term bands and EMAs. It takes five parameters: close_price, high_price, low_price, short_term_length, and long_term_length. It returns an array containing the upper band, lower band, middle band, long-term upper EMA, long-term lower EMA, and long-term middle EMA.

█ KEY POINTS AND TECHNIQUES

• Typical Price Calculation: The script uses a modified typical price calculation (2 * close_price + high_price + low_price) / 4 instead of the standard (high_price + low_price + close_price) / 3.

• Short-term and Long-term Bands: The script calculates short-term bands using a simple moving average (SMA) of the typical price and long-term bands using a relative moving average (RMA) of the close price.

• Conditional Plotting: The script uses conditional plotting to highlight breakouts when the short-term bands cross the long-term EMAs, enhancing visual identification of trading signals.

• EMA for Long-term Trends: The use of Exponential Moving Averages (EMAs) for long-term bands helps in smoothing out short-term fluctuations and focusing on long-term trends.

█ EXTENDED KNOWLEDGE AND APPLICATIONS

• Modifications: Users can add input parameters to allow customization of short_term_length and long_term_length, making the indicator more flexible.

• Enhancements: The script could be extended to include alerts for breakout conditions, providing traders with real-time notifications.

• Alternative Bands: Users might experiment with different types of moving averages (e.g., WMA, HMA) for the short-term and long-term bands to see if they yield better results.

• Additional Indicators: Combining this indicator with other technical indicators (e.g., RSI, MACD) could provide a more comprehensive trading strategy.

• Backtesting: Users can backtest the strategy using Pine Script's strategy functions to evaluate its performance over historical data.

Top-Down Trend and Key Levels with Swing Points//by antaryaami0

Overview

The “Top-Down Trend and Key Levels with Swing Points” indicator is a comprehensive tool designed to enhance your technical analysis by integrating multiple trading concepts into a single, easy-to-use script. It combines higher timeframe trend analysis, key price levels, swing point detection, and ranging market identification to provide a holistic view of market conditions. This indicator is particularly useful for traders who employ multi-timeframe analysis, support and resistance levels, and price action strategies.

Key Features

1. Higher Timeframe Trend Background Shading:

• Purpose: Identifies the prevailing trend on a higher timeframe to align lower timeframe trading decisions with the broader market direction.

• How it Works: The indicator compares the current higher timeframe close with the previous one to determine if the trend is up, down, or ranging.

• Customization:

• Trend Timeframe: Set your preferred higher timeframe (e.g., Daily, Weekly).

• Up Trend Color & Down Trend Color: Customize the background colors for uptrends and downtrends.

• Ranging Market Color: A separate color to indicate when the market is moving sideways.

2. Key Price Levels:

• Previous Day High (PDH) and Low (PDL):

• Purpose: Identifies key support and resistance levels from the previous trading day.

• Visualization: Plots horizontal lines at PDH and PDL with labels.

• Customization: Option to show or hide these levels and customize their colors.

• Pre-Market High (PMH) and Low (PML):

• Purpose: Highlights the price range during the pre-market session, which can indicate potential breakout levels.

• Visualization: Plots horizontal lines at PMH and PML with labels.

• Customization: Option to show or hide these levels and customize their colors.

3. First 5-Minute Marker (F5H/F5L):

• Purpose: Marks the high or low of the first 5 minutes after the market opens, which is significant for intraday momentum.

• How it Works:

• If the first 5-minute high is above the Pre-Market High (PMH), an “F5H” label is placed at the first 5-minute high.

• If the first 5-minute high is below the PMH, an “F5L” label is placed at the first 5-minute low.

• Visualization: Labels are placed at the 9:35 AM candle (closing of the first 5 minutes), colored in purple by default.

• Customization: Option to show or hide the marker and adjust the marker color.

4. Swing Points Detection:

• Purpose: Identifies significant pivot points in price action to help recognize trends and reversals.

• How it Works: Uses left and right bars to detect pivot highs and lows, then determines if they are Higher Highs (HH), Lower Highs (LH), Higher Lows (HL), or Lower Lows (LL).

• Visualization: Plots small markers (circles) with labels (HH, LH, HL, LL) at the corresponding swing points.

• Customization: Adjust the number of left and right bars for pivot detection and the size of the markers.

5. Ranging Market Detection:

• Purpose: Identifies periods when the market is consolidating (moving sideways) within a defined price range.

• How it Works: Calculates the highest high and lowest low over a specified period and determines if the price range is within a set percentage threshold.

• Visualization: Draws a gray box around the price action during the ranging period and labels the high and low prices at the end of the range.

• Customization: Adjust the range detection period and threshold, as well as the box color.

6. Trend Coloring on Chart:

• Purpose: Provides a visual cue for the short-term trend based on a moving average.

• How it Works: Colors the candles green if the price is above the moving average and red if below.

• Customization: Set the moving average length and customize the uptrend and downtrend colors.

How to Use the Indicator

1. Adding the Indicator to Your Chart:

• Copy the Pine Script code provided and paste it into the Pine Script Editor on TradingView.

• Click “Add to Chart” to apply the indicator.

2. Configuring Inputs and Settings:

• Access Inputs:

• Click on the gear icon next to the indicator’s name on your chart to open the settings.

• Customize Key Levels:

• Show Pre-Market High/Low: Toggle on/off.

• Show Previous Day High/Low: Toggle on/off.

• Show First 5-Minute Marker: Toggle on/off.

• Set Trend Parameters:

• Trend Timeframe for Background: Choose the higher timeframe for trend analysis.

• Moving Average Length for Bar Color: Set the period for the moving average used in bar coloring.

• Adjust Ranging Market Detection:

• Range Detection Period: Specify the number of bars to consider for range detection.

• Range Threshold (%): Set the maximum percentage range for the market to be considered ranging.

• Customize Visuals:

• Colors: Adjust colors for trends, levels, markers, and ranging market boxes.

• Label Font Size: Choose the size of labels displayed on the chart.

• Level Line Width: Set the thickness of the lines for key levels.

3. Interpreting the Indicator:

• Background Shading:

• Green Shade: Higher timeframe is in an uptrend.

• Red Shade: Higher timeframe is in a downtrend.

• Gray Box: Market is ranging (sideways movement).

• Key Levels and Markers:

• PDH and PDL Lines: Represent resistance and support from the previous day.

• PMH and PML Lines: Indicate potential breakout levels based on pre-market activity.

• F5H/F5L Labels: Early indication of intraday momentum after market open.

• Swing Point Markers:

• HH (Higher High): Suggests bullish momentum.

• LH (Lower High): May indicate a potential bearish reversal.

• HL (Higher Low): Supports bullish continuation.

• LL (Lower Low): Indicates bearish momentum.

• Ranging Market Box:

• Gray Box Around Price Action: Highlights consolidation periods where breakouts may occur.

• Range High and Low Labels: Provide the upper and lower bounds of the consolidation zone.

4. Applying the Indicator to Your Trading Strategy:

• Trend Alignment:

• Use the higher timeframe trend shading to align your trades with the broader market direction.

• Key Levels Trading:

• Watch for price reactions at PDH, PDL, PMH, and PML for potential entry and exit points.

• Swing Points Analysis:

• Identify trend continuations or reversals by observing the sequence of HH, HL, LH, and LL.

• Ranging Market Strategies:

• During ranging periods, consider range-bound trading strategies or prepare for breakout trades when the price exits the range.

• Intraday Momentum:

• Use the F5H/F5L marker to gauge early market sentiment and potential intraday trends.

Practical Tips

• Adjust Settings to Your Trading Style:

• Tailor the indicator’s inputs to match your preferred timeframes and trading instruments.

• Combine with Other Indicators:

• Use in conjunction with volume indicators, oscillators, or other technical tools for additional confirmation.

• Backtesting:

• Apply the indicator to historical data to observe how it performs and refine your settings accordingly.

• Stay Updated on Market Conditions:

• Be aware of news events or economic releases that may impact market behavior and the effectiveness of technical levels.

Customization Options

• Time Zone Adjustment:

• The script uses “America/New_York” time zone by default. Adjust the timezone variable in the script if your chart operates in a different time zone.

var timezone = "Your/Timezone"

• Session Times:

• Modify the Regular Trading Session and Pre-Market Session times in the indicator settings to align with the trading hours of different markets or exchanges.

• Visual Preferences:

• Colors: Personalize the indicator’s colors to suit your visual preferences or to enhance visibility.

• Label Sizes: Adjust label sizes if you find them too intrusive or not prominent enough.

• Marker Sizes: Further reduce or enlarge the swing point markers by modifying the swing_marker_size variable.

Understanding the Indicator’s Logic

1. Higher Timeframe Trend Analysis:

• The indicator retrieves the closing prices of a higher timeframe using the request.security() function.

• It compares the current higher timeframe close with the previous one to determine the trend direction.

2. Key Level Calculation:

• Previous Day High/Low: Calculated by tracking the highest and lowest prices of the previous trading day.

• Pre-Market High/Low: Calculated by monitoring price action during the pre-market session.

3. First 5-Minute Marker Logic:

• At 9:35 AM (end of the first 5 minutes after market open), the indicator evaluates whether the first 5-minute high is above or below the PMH.

• It then places the appropriate label (F5H or F5L) on the chart.

4. Swing Points Detection:

• The script uses ta.pivothigh() and ta.pivotlow() functions to detect pivot points.

• It then determines the type of swing point based on comparisons with previous swings.

5. Ranging Market Detection:

• The indicator looks back over a specified number of bars to find the highest high and lowest low.

• It calculates the percentage difference between these two points.

• If the difference is below the set threshold, the market is considered to be ranging, and a box is drawn around the price action.

Limitations and Considerations

• Indicator Limitations:

• Maximum Boxes and Labels: Due to Pine Script limitations, there is a maximum number of boxes and labels that can be displayed simultaneously.

• Performance Impact: Adding multiple visual elements (boxes, labels, markers) can affect the performance of the script on lower-end devices or with large amounts of data.

• Market Conditions:

• False Signals: Like any technical tool, the indicator may produce false signals, especially during volatile or erratic market conditions.

• Not a Standalone Solution: This indicator should be used as part of a comprehensive trading strategy, including risk management and other forms of analysis.

Conclusion

The “Top-Down Trend and Key Levels with Swing Points” indicator is a versatile tool that integrates essential aspects of technical analysis into one script. By providing insights into higher timeframe trends, highlighting key price levels, detecting swing points, and identifying ranging markets, it equips traders with valuable information to make more informed trading decisions. Whether you are a day trader looking for intraday opportunities or a swing trader aiming to align with the broader trend, this indicator can enhance your chart analysis and trading strategy.

Disclaimer

Trading involves significant risk, and it’s important to understand that past performance is not indicative of future results. This indicator is a tool to assist in analysis and should not be solely relied upon for making trading decisions. Always conduct thorough research and consider seeking advice from financial professionals before engaging in trading activities.

ADM Indicator [CHE] Comprehensive Description of the Three Market Phases for TradingView

Introduction

Financial markets often exhibit patterns that reflect the collective behavior of participants. Recognizing these patterns can provide traders with valuable insights into potential future price movements. The ADM Indicator is designed to help traders identify and capitalize on these patterns by detecting three primary market phases:

1. Accumulation Phase

2. Manipulation Phase

3. Distribution Phase

This indicator places labels on the chart to signify these phases, aiding traders in making informed decisions. Below is an in-depth explanation of each phase, including how the ADM Indicator detects them.

1. Accumulation Phase

Definition

The Accumulation Phase is a period where informed investors or institutions discreetly purchase assets before a potential price increase. During this phase, the price typically moves within a confined range between established highs and lows.

Characteristics

- Price Range Bound: The asset's price stays within the previous high and low after a timeframe change.

- Low Volatility: Minimal price movement indicates a balance between buyers and sellers.

- Steady Volume: Trading volume may remain relatively constant or show slight increases.

- Market Sentiment: General market interest is low, as the accumulation is not yet apparent to the broader market.

Detection with ADM Indicator

- Criteria: An accumulation is detected when the price remains within the previous high and low after a timeframe change.

- Indicator Action: At the end of the period, if accumulation has occurred, the indicator places a label "Accumulation" on the chart.

- Visual Cues: A yellow semi-transparent background highlights the accumulation phase, enhancing visual recognition.

Implications for Traders

- Entry Opportunity: Consider preparing for potential long positions before a possible upward move.

- Risk Management: Use tight stop-loss orders below the support level due to the defined trading range.

2. Manipulation Phase

Definition

The Manipulation Phase, also known as the Shakeout Phase, occurs when dominant market players intentionally move the price to trigger stop-loss orders and create panic among less-informed traders. This action generates liquidity and better entry prices for large positions.

Characteristics

- False Breakouts: The price moves above the previous high or below the previous low but quickly reverses.

- Increased Volatility: Sharp price movements occur without fundamental reasons.

- Stop-Loss Hunting: The price targets common stop-loss areas, triggering them before reversing.

- Emotional Trading: Retail traders may react impulsively, leading to poor trading decisions.

Detection with ADM Indicator

- Manipulation Up:

- Criteria: Detected when the price rises above the previous high and then falls back below it.

- Indicator Action: Places a label "Manipulation Up" on the chart at the point of detection.

- Manipulation Down:

- Criteria: Detected when the price falls below the previous low and then rises back above it.

- Indicator Action: Places a label "Manipulation Down" on the chart at the point of detection.

- Visual Cues:

- Manipulation Up: Blue background highlights the phase.

- Manipulation Down: Orange background highlights the phase.

Implications for Traders

- Caution Advised: Be wary of false signals and avoid overreacting to sudden price changes.

- Preparation for Next Phase: Use this phase to anticipate potential distribution and adjust strategies accordingly.

3. Distribution Phase

Definition

The Distribution Phase occurs when the institutions or informed investors who accumulated positions start selling to the general market at higher prices. This phase often follows a Manipulation Phase and may signal an impending trend reversal.

Characteristics

- Price Reversal: The price moves in the opposite direction of the prior manipulation.

- High Trading Volume: Increased selling activity as large players offload positions.

- Trend Weakening: The previous trend loses momentum, indicating a potential shift.

- Market Sentiment Shift: Optimism fades, and uncertainty or pessimism may emerge.

Detection with ADM Indicator

- Distribution Up:

- Criteria: Detected after a verified Manipulation Up when the price subsequently falls below the previous low.

- Indicator Action: Places a label "Distribution Up" on the chart.

- Distribution Down:

- Criteria: Detected after a verified Manipulation Down when the price subsequently rises above the previous high.

- Indicator Action: Places a label "Distribution Down" on the chart.

- Visual Cues:

- Distribution Up: Purple background highlights the phase.

- Distribution Down: Maroon background highlights the phase.

Implications for Traders

- Exit Signals: Consider closing long positions if in a Distribution Up phase.

- Short Selling Opportunities: Potential to enter short positions anticipating a downtrend.

Using the ADM Indicator on TradingView

Indicator Overview

The ADM Indicator automates the detection of Accumulation, Manipulation, and Distribution phases by analyzing price movements relative to previous highs and lows on a selected timeframe. It provides visual cues and labels on the chart, helping traders quickly identify the current market phase.

Features

- Multi-Timeframe Analysis: Choose from auto, multiplier, or manual timeframe settings.

- Visual Labels: Clear labeling of market phases directly on the chart.

- Background Highlighting: Distinct background colors for each phase.

- Customizable Settings: Adjust colors, styles, and display options.

- Period Separators: Optional separators delineate different timeframes.

Interpreting the Indicator

1. Accumulation Phase

- Detection: Price stays within the previous high and low after a timeframe change.

- Label: "Accumulation" placed at the period's end if detected.

- Background: Yellow semi-transparent color.

- Action: Prepare for potential long positions.

2. Manipulation Phase

- Detection:

- Manipulation Up: Price rises above previous high and then falls back below.

- Manipulation Down: Price falls below previous low and then rises back above.

- Labels: "Manipulation Up" or "Manipulation Down" placed at detection.

- Background:

- Manipulation Up: Blue color.

- Manipulation Down: Orange color.

- Action: Exercise caution; avoid impulsive trades.

3. Distribution Phase

- Detection:

- Distribution Up: After a Manipulation Up, price falls below previous low.

- Distribution Down: After a Manipulation Down, price rises above previous high.

- Labels: "Distribution Up" or "Distribution Down" placed at detection.

- Background:

- Distribution Up: Purple color.

- Distribution Down: Maroon color.

- Action: Consider exiting positions or entering counter-trend trades.

Configuring the Indicator

- Timeframe Type: Select Auto, Multiplier, or Manual for analysis timeframe.

- Multiplier: Set a custom multiplier when using "Multiplier" type.

- Manual Resolution: Define a specific timeframe with "Manual" option.

- Separator Settings: Customize period separators for visual clarity.

- Label Display Options: Choose to display all labels or only the most recent.

- Visualization Settings: Adjust colors and styles for personal preference.

Practical Tips

- Combine with Other Analysis Tools: Use alongside volume indicators, trend lines, or other technical tools.

- Backtesting: Review historical data to understand how the indicator signals would have impacted past trades.

- Stay Informed: Keep abreast of market news that might affect price movements beyond technical analysis.

- Risk Management: Always employ stop-loss orders and position sizing strategies.

Conclusion

The ADM Indicator is a valuable tool for traders seeking to understand and leverage market phases. By detecting Accumulation, Manipulation, and Distribution phases through specific price action criteria, it provides actionable insights into market dynamics.

Understanding the precise conditions under which each phase is detected empowers traders to make more informed decisions. Whether preparing for potential breakouts during accumulation, exercising caution during manipulation, or adjusting positions during distribution, the ADM Indicator aids in navigating the complexities of the financial markets.

Disclaimer:

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

This indicator is inspired by the Super 6x Indicators: RSI, MACD, Stochastic, Loxxer, CCI, and Velocity . A special thanks to Loxx for their relentless effort, creativity, and contributions to the TradingView community, which served as a foundation for this work.

Best regards Chervolino

Overview of the Timeframe Levels in the `autotimeframe()` Function

The `autotimeframe()` function automatically adjusts the higher timeframe based on the current chart timeframe. Here are the specific timeframe levels used in the function:

- Current Timeframe ≤ 1 Minute

→ Higher Timeframe: 240 Minutes (4 Hours)

- Current Timeframe ≤ 5 Minutes

→ Higher Timeframe: 1 Day

- Current Timeframe ≤ 1 Hour

→ Higher Timeframe: 3 Days

- Current Timeframe ≤ 4 Hours

→ Higher Timeframe: 7 Days

- Current Timeframe ≤ 12 Hours

→ Higher Timeframe: 1 Month

- Current Timeframe ≤ 1 Day

→ Higher Timeframe: 3 Months

- Current Timeframe ≤ 7 Days

→ Higher Timeframe: 6 Months

- For All Higher Timeframes (over 7 Days)

→ Higher Timeframe: 12 Months

Summary:

The function assigns a corresponding higher timeframe based on the current timeframe to optimize the analysis:

- 1 Minute or Less → 4 Hours

- Up to 5 Minutes → 1 Day

- Up to 1 Hour → 3 Days

- Up to 4 Hours → 7 Days

- Up to 12 Hours → 1 Month

- Up to 1 Day → 3 Months

- Up to 7 Days → 6 Months

- Over 7 Days → 12 Months

This automated adjustment ensures that the indicator works effectively across different chart timeframes without requiring manual changes.

PTS - Bollinger Bands with Trailing StopPTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

Thought for 1m 7s

Description for the "PTS - Bollinger Bands with Trailing Stop" Strategy

PTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

How the Strategy Works

1. Initialization

Calculates Bollinger Bands and ATR based on selected parameters.

2. Entry Logic

Opens a long position when the closing price exceeds the upper Bollinger Band.

3. Exit Logic

Uses a trailing stop loss based on ATR. Exits if the closing price drops below the lower Bollinger Band.

4. Date Filtering

Executes trades only within the specified date range.

Advantages

Adaptive Risk Management: Trailing stop adjusts to market volatility. Simplicity: Clear entry and exit signals. Customizable Parameters: Tailor the strategy to different assets or conditions.

Considerations

Aggressive Position Sizing: Using 100% equity per trade is high-risk. Market Conditions: Best in trending markets; may produce false signals in sideways markets. Backtesting: Always test on historical data before live trading.

Disclaimer

This strategy is intended for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Assess your financial situation and consult a financial advisor if necessary.

Usage Instructions

1. Apply the Strategy: Add it to your TradingView chart. 2. Configure Inputs: Adjust parameters to suit your style and asset. 3. Analyze Backtest Results: Use the Strategy Tester. 4. Optimize Parameters: Experiment with input values. 5. Risk Management: Evaluate position sizing and incorporate risk controls.

Final Notes

The "PTS - Bollinger Bands with Trailing Stop" strategy provides a framework to leverage momentum breakouts while managing risk through adaptive trailing stops. Customize and test thoroughly to align with your trading objectives.

[Defaust] Fractals Fractals Indicator

Overview

The Fractals Indicator is a technical analysis tool designed to help traders identify potential reversal points in the market by detecting fractal patterns. This indicator is a fork of the original fractals indicator, with adjustments made to the plotting for enhanced visual clarity and usability.

What Are Fractals?

In trading, a fractal is a pattern consisting of five consecutive bars (candlesticks) that meet specific conditions:

Up Fractal (Potential Sell Signal): Occurs when a high point is surrounded by two lower highs on each side.

Down Fractal (Potential Buy Signal): Occurs when a low point is surrounded by two higher lows on each side.

Fractals help traders identify potential tops and bottoms in the market, signaling possible entry or exit points.

Features of the Indicator

Customizable Periods (n): Allows you to define the number of periods to consider when detecting fractals, offering flexibility to adapt to different trading strategies and timeframes.

Enhanced Plotting Adjustments: This fork introduces adjustments to the plotting of fractal signals for better visual representation on the chart.

Visual Signals: Plots up and down triangles on the chart to signify down fractals (potential bullish signals) and up fractals (potential bearish signals), respectively.

Overlay on Chart: The fractal signals are overlaid directly on the price chart for immediate visualization.

Adjustable Precision: You can set the precision of the plotted values according to your needs.

Pine Script Code Explanation

Below is the Pine Script code for the Fractals Indicator:

//@version=5 indicator(" Fractals", shorttitle=" Fractals", format=format.price, precision=0, overlay=true)

// User input for the number of periods to consider for fractal detection n = input.int(title="Periods", defval=2, minval=2)

// Initialize flags for up fractal detection bool upflagDownFrontier = true bool upflagUpFrontier0 = true bool upflagUpFrontier1 = true bool upflagUpFrontier2 = true bool upflagUpFrontier3 = true bool upflagUpFrontier4 = true

// Loop through previous and future bars to check conditions for up fractals for i = 1 to n // Check if the highs of previous bars are less than the current bar's high upflagDownFrontier := upflagDownFrontier and (high < high ) // Check various conditions for future bars upflagUpFrontier0 := upflagUpFrontier0 and (high < high ) upflagUpFrontier1 := upflagUpFrontier1 and (high <= high and high < high ) upflagUpFrontier2 := upflagUpFrontier2 and (high <= high and high <= high and high < high ) upflagUpFrontier3 := upflagUpFrontier3 and (high <= high and high <= high and high <= high and high < high ) upflagUpFrontier4 := upflagUpFrontier4 and (high <= high and high <= high and high <= high and high <= high and high < high )

// Combine the flags to determine if an up fractal exists flagUpFrontier = upflagUpFrontier0 or upflagUpFrontier1 or upflagUpFrontier2 or upflagUpFrontier3 or upflagUpFrontier4 upFractal = (upflagDownFrontier and flagUpFrontier)

// Initialize flags for down fractal detection bool downflagDownFrontier = true bool downflagUpFrontier0 = true bool downflagUpFrontier1 = true bool downflagUpFrontier2 = true bool downflagUpFrontier3 = true bool downflagUpFrontier4 = true

// Loop through previous and future bars to check conditions for down fractals for i = 1 to n // Check if the lows of previous bars are greater than the current bar's low downflagDownFrontier := downflagDownFrontier and (low > low ) // Check various conditions for future bars downflagUpFrontier0 := downflagUpFrontier0 and (low > low ) downflagUpFrontier1 := downflagUpFrontier1 and (low >= low and low > low ) downflagUpFrontier2 := downflagUpFrontier2 and (low >= low and low >= low and low > low ) downflagUpFrontier3 := downflagUpFrontier3 and (low >= low and low >= low and low >= low and low > low ) downflagUpFrontier4 := downflagUpFrontier4 and (low >= low and low >= low and low >= low and low >= low and low > low )

// Combine the flags to determine if a down fractal exists flagDownFrontier = downflagUpFrontier0 or downflagUpFrontier1 or downflagUpFrontier2 or downflagUpFrontier3 or downflagUpFrontier4 downFractal = (downflagDownFrontier and flagDownFrontier)

// Plot the fractal symbols on the chart with adjusted plotting plotshape(downFractal, style=shape.triangleup, location=location.belowbar, offset=-n, color=color.gray, size=size.auto) plotshape(upFractal, style=shape.triangledown, location=location.abovebar, offset=-n, color=color.gray, size=size.auto)

Explanation:

Input Parameter (n): Sets the number of periods for fractal detection. The default value is 2, and it must be at least 2 to ensure valid fractal patterns.

Flag Initialization: Boolean variables are used to store intermediate conditions during fractal detection.

Loops: Iterate through the specified number of periods to evaluate the conditions for fractal formation.

Conditions:

Up Fractals: Checks if the current high is greater than previous highs and if future highs are lower or equal to the current high.

Down Fractals: Checks if the current low is lower than previous lows and if future lows are higher or equal to the current low.

Flag Combination: Logical and and or operations are used to combine the flags and determine if a fractal exists.

Adjusted Plotting:

The plotting of fractal symbols has been adjusted for better alignment and visual clarity.

The offset parameter is set to -n to align the plotted symbols with the correct bars.

The color and size have been fine-tuned for better visibility.

How to Use the Indicator

Adding the Indicator to Your Chart

Open TradingView:

Go to TradingView.

Access the Chart:

Click on "Chart" to open the main charting interface.

Add the Indicator:

Click on the "Indicators" button at the top.

Search for " Fractals".

Select the indicator from the list to add it to your chart.

Configuring the Indicator

Periods (n):

Default value is 2.

Adjust this parameter based on your preferred timeframe and sensitivity.

A higher value of n considers more bars for fractal detection, potentially reducing the number of signals but increasing their significance.

Interpreting the Signals

– Up Fractal (Downward Triangle): Indicates a potential price reversal to the downside. May be used as a signal to consider exiting long positions or tightening stop-loss orders.

– Down Fractal (Upward Triangle): Indicates a potential price reversal to the upside. May be used as a signal to consider entering long positions or setting stop-loss orders for short positions.

Trading Strategy Suggestions

Up Fractal Detection:

The high of the current bar (n) is higher than the highs of the previous two bars (n - 1, n - 2).

The highs of the next bars meet certain conditions to confirm the fractal pattern.

An up fractal symbol (downward triangle) is plotted above the bar at position n - n (due to the offset).

Down Fractal Detection:

The low of the current bar (n) is lower than the lows of the previous two bars (n - 1, n - 2).

The lows of the next bars meet certain conditions to confirm the fractal pattern.

A down fractal symbol (upward triangle) is plotted below the bar at position n - n.

Benefits of Using the Fractals Indicator

Early Signals: Helps in identifying potential reversal points in price movements.

Customizable Sensitivity: Adjusting the n parameter allows you to fine-tune the indicator based on different market conditions.

Enhanced Visuals: Adjustments to plotting improve the clarity and readability of fractal signals on the chart.

Limitations and Considerations

Lagging Indicator: Fractals require future bars to confirm the pattern, which may introduce a delay in the signals.

False Signals: In volatile or ranging markets, fractals may produce false signals. It's advisable to use them in conjunction with other analysis tools.

Not a Standalone Tool: Fractals should be part of a broader trading strategy that includes other indicators and fundamental analysis.

Best Practices for Using This Indicator

Combine with Other Indicators: Use in combination with trend indicators, oscillators, or volume analysis to confirm signals.

Backtesting: Before applying the indicator in live trading, backtest it on historical data to understand its performance.

Adjust Periods Accordingly: Experiment with different values of n to find the optimal setting for the specific asset and timeframe you are trading.

Disclaimer

The Fractals Indicator is intended for educational and informational purposes only. Trading involves significant risk, and you should be aware of the risks involved before proceeding. Past performance is not indicative of future results. Always conduct your own analysis and consult with a professional financial advisor before making any investment decisions.

Credits

This indicator is a fork of the original fractals indicator, with adjustments made to the plotting for improved visual representation. It is based on standard fractal patterns commonly used in technical analysis and has been developed to provide traders with an effective tool for detecting potential reversal points in the market.

MAC Investor V3.0 [VK]This indicator combines multiple functionalities to assist traders in making informed decisions. It primarily uses Heikin Ashi candles, Moving Averages, and a Price Action Channel (PAC) to provide signals for entering and exiting trades. Here's a detailed breakdown:

Inputs

MAC Length: Sets the length for the PAC calculation.

Use Heikin Ashi Candles: Option to use Heikin Ashi candles for calculations.

Show Coloured Bars around MAC: Option to color bars based on their relation to the PAC.

Show Long/Short Signals: Options to display long and short signals.

Show MAs? : Option to show moving averages on the chart.

Show MAs Trend at the Bottom?: Option to show trend signals at the bottom of the chart.

MA Lengths: Length settings for three different moving averages.

Change MA Color Based on Direction?: Option to change the color of moving averages based on trend direction.

MA Higher TimeFrame: Allows setting a higher timeframe for moving averages.

Show SL-TP Lines: Option to display Stop Loss and Take Profit lines.

SL/TP Percentages: Set the percentages for Stop Loss and three levels of Take Profit.

Calculations and Features

Heikin Ashi Candles: Calculations are based on Heikin Ashi candle data if selected.

Price Action Channel (PAC): Uses Exponential Moving Averages (EMA) of the high, low, and close to create a channel.

Bar Coloring: Colors the bars based on their position relative to the PAC.

Long and Short Signals: Uses crossovers of the close price and PAC upper/lower bands to generate signals.

Moving Averages (MA): Plots three moving averages and colors them based on their trend direction.

Overall Trend Indicators: Uses triangles at the bottom of the chart to show the overall trend of the MAs.

Stop Loss and Take Profit Levels: Calculates and plots these levels based on user-defined percentages from the entry price.

Alerts: Provides alerts for long and short signals.

Use Cases and How to Use

Identifying Trends: The PAC helps to identify the trend direction. If the closing price is above the PAC upper band, it suggests an uptrend; if below the lower band, it suggests a downtrend.

Entering Trades: Use the long and short signals to enter trades. A long signal is generated when the closing price crosses above the PAC upper band, and a short signal is generated when it crosses below the PAC lower band.

Exit Strategies: Utilize the Stop Loss (SL) and Take Profit (TP) levels to manage risk and lock in profits. These levels are automatically calculated based on the entry price and user-defined percentages.

Trend Confirmation with MAs: The moving averages provide additional confirmation of the trend. When all three MAs are trending in the same direction (e.g., all green for an uptrend), it adds confidence to the trade signal.

Overall Trend Indicators: The triangles at the bottom of the chart show the overall trend direction of the MAs:

Green Triangle: All three MAs are trending upwards, indicating a strong uptrend.

Red Triangle: All three MAs are trending downwards, indicating a strong downtrend.

Yellow Triangle: Mixed signals from the MAs, indicating no clear trend.

Bar Coloring for Quick Analysis: The colored bars give a quick visual cue about the market condition, aiding in faster decision-making.

Alerts: Set up alerts to get notified when a long or short signal is generated, allowing you to act promptly without constantly monitoring the chart.

Maximizing Profit

To maximize profit with this indicator:

Follow the Signals: Use the long and short signals to time your entries. Ensure you follow the trend indicated by the PAC and MAs.

Risk Management: Always set your Stop Loss and Take Profit levels to manage risk. This will help you cut losses early and secure profits.

Confirm with MAs: Look for confirmation from the moving averages. When all MAs align with the signal, it indicates a stronger trend.

Overall Trend Indicators: Pay attention to the triangles at the bottom for overall trend confirmation. Only enter trades when the overall trend is in your favor.

Heikin Ashi for Smoothing: Use Heikin Ashi candles for smoother trends and fewer false signals.

Backtesting: Test the indicator on historical data to understand its performance and adjust settings as necessary.

Adapt to Market Conditions: Adjust the lengths of PAC and MAs based on the market's volatility and timeframe you are trading on.

How to Use the Indicator

Add to Chart: Add the indicator to your TradingView chart.

Configure Settings: Customize the input settings to fit your trading strategy and timeframe.

Monitor Signals: Watch for long and short signals and observe the trend direction with the PAC and MAs.

Check Overall Trend: Look at the triangles at the bottom of the chart to see the overall trend direction of the MAs.

Set Alerts: Configure alerts to get notified of new signals.

Manage Trades: Use the SL and TP levels to manage your trades effectively.

Modern Trend IdentifierThis is an update by Lightangel112 to Trendilo (Open-Source).

Thanks @ Lightangel112

The Modern Trend Identifier (MTI) is a sophisticated technical analysis tool designed for traders and analysts seeking to accurately determine market trends. This indicator leverages the Arnaud Legoux Moving Average (ALMA) to smooth price data and calculate percentage changes, providing a clearer and more responsive trend analysis. MTI is engineered to highlight trend direction with visual cues, fill areas between the indicator and its bands, and color bars based on trend direction, making it a powerful tool for identifying market momentum and potential reversals.

Capabilities

Smoothing and Trend Calculation:

Utilizes ALMA to smooth price data, reducing noise and providing a clearer view of the trend.

Calculates percentage changes in price over a user-defined lookback period.

Dynamic Range Adjustment:

Normalizes the ALMA percentage change values to ensure they stay within a -100 to 100 range.

Uses a combination of linear and smoothstep compression to handle extreme values without losing sensitivity.

Trend Direction and Highlighting:

Determines the trend direction based on the relationship between the smoothed ALMA percentage change and dynamically adjusted RMS (Root Mean Square) bands.

Colors the trend line to visually indicate whether the market is in an uptrend, downtrend, or neutral state.

Dynamic Threshold Calculation:

Calculates dynamic thresholds using percentile ranks to adapt to changing market conditions.

Visualization Enhancements:

Fills areas between the ALMA percentage change line and its RMS bands to provide a clear visual indication of the trend strength.

Offers the option to color price bars based on the identified trend direction.

Customizable Settings:

Provides extensive customization options for lookback periods, smoothing parameters, ALMA settings, band multipliers, and more.

Allows users to enable or disable various visual enhancements and customize their appearance.

Use Cases

Trend Identification:

MTI helps traders identify the current market trend, whether it's bullish, bearish, or neutral. This can be particularly useful for trend-following strategies.

Momentum Analysis:

By highlighting areas of strong momentum, MTI enables traders to spot potential breakouts or breakdowns. This can be useful for both entry and exit decisions.

Support and Resistance Levels:

The dynamic threshold bands can act as support and resistance levels. Traders can use these levels to set stop-loss and take-profit orders.

Divergence Detection:

MTI can help in identifying divergences between price and the indicator, which can signal potential trend reversals. This is useful for traders looking to capitalize on trend changes.

Risk Management:

The fill areas and colored bars provide clear visual cues about trend strength and direction, aiding in better risk management. Traders can adjust their positions based on the strength of the trend.

Backtesting:

The extensive customization options allow traders to backtest different settings and parameters to optimize their trading strategies for various market conditions.

Multiple Timeframes:

MTI can be applied to multiple timeframes, from intraday charts to daily, weekly, or monthly charts, making it a versatile tool for traders with different trading styles.

Example Scenarios

Day Trading:

A day trader can use MTI on a 5-minute chart to identify intraday trends. By adjusting the lookback period and smoothing parameters, the trader can quickly spot potential entry and exit points based on short-term momentum changes.

Swing Trading:

A swing trader might apply MTI to a 4-hour chart to identify medium-term trends. The dynamic thresholds can help in setting appropriate stop-loss levels, while the trend direction highlighting aids in making informed decisions about holding or exiting positions.

Position Trading:

For a position trader using a daily chart, MTI can help identify the overarching trend. The trader can use the fill areas and bar coloring to assess the strength of the trend and make decisions about entering or exiting long-term positions.

Market Analysis:

An analyst could use MTI to study historical price movements and identify patterns. By examining how the indicator reacted to past market conditions, the analyst can gain insights into potential future price movements.

In summary, the Modern Trend Identifier (MTI) is a versatile and powerful tool that enhances trend analysis with advanced smoothing techniques, dynamic adjustments, and comprehensive visual cues. It is designed to meet the needs of traders and analysts across various trading styles and timeframes, providing clear and actionable insights into market trends and momentum.

Updated with the following:

Additions and Enhancements in MTI

Grouped Inputs with Descriptive Tooltips:

Inputs are organized into groups for better clarity.

Each input parameter includes a descriptive tooltip.

Dynamic Threshold Calculation:

Added dynamic threshold calculation using percentile ranks to adapt to changing market conditions.

Normalization and Compression:

Added normalization factor to ensure plots are within -100 to 100 range.

Introduced smoothstep function for smooth transition and selectively applied linear and smoothstep compression to values outside -80 to 100 range.

Enhanced Visualization:

Highlighted trend direction with RGB colors.

Enhanced fill areas between the ALMA percentage change line and its RMS bands.

Colored price bars based on the identified trend direction.

RMS Lines Adjustment:

Dynamically adjusted RMS calculation without strict capping.

Ensured RMS lines stay below fill areas to maintain clarity.

Descriptive and Organized Code:

Enhanced code clarity with detailed comments.