CNTLibraryLibrary "CNTLibrary"

Custom Functions To Help Code In Pinescript V5

Coded By Christian Nataliano

First Coded In 10/06/2023

Last Edited In 22/06/2023

Huge Shout Out To © ZenAndTheArtOfTrading and his ZenLibrary V5, Some Of The Custom Functions Were Heavily Inspired By Matt's Work & His Pine Script Mastery Course

Another Shout Out To The TradingView's Team Library ta V5

//====================================================================================================================================================

// Custom Indicator Functions

//====================================================================================================================================================

GetKAMA(KAMA_lenght, Fast_KAMA, Slow_KAMA)

Calculates An Adaptive Moving Average Based On Perry J Kaufman's Calculations

Parameters:

KAMA_lenght (int) : Is The KAMA Lenght

Fast_KAMA (int) : Is The KAMA's Fastes Moving Average

Slow_KAMA (int) : Is The KAMA's Slowest Moving Average

Returns: Float Of The KAMA's Current Calculations

GetMovingAverage(Source, Lenght, Type)

Get Custom Moving Averages Values

Parameters:

Source (float) : Of The Moving Average, Defval = close

Lenght (simple int) : Of The Moving Average, Defval = 50

Type (string) : Of The Moving Average, Defval = Exponential Moving Average

Returns: The Moving Average Calculation Based On Its Given Source, Lenght & Calculation Type (Please Call Function On Global Scope)

GetDecimals()

Calculates how many decimals are on the quote price of the current market © ZenAndTheArtOfTrading

Returns: The current decimal places on the market quote price

Truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places © ZenAndTheArtOfTrading

Parameters:

number (float)

decimalPlaces (simple float)

Returns: The given number truncated to the given decimalPlaces

ToWhole(number)

Converts pips into whole numbers © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

ToPips(number)

Converts whole numbers back into pips © ZenAndTheArtOfTrading

Parameters:

number (float)

Returns: The converted number

GetPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period © ZenAndTheArtOfTrading

Parameters:

value1 (float)

value2 (float)

lookback (int)

BarsAboveMA(lookback, ma)

Counts how many candles are above the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are above the MA

BarsBelowMA(lookback, ma)

Counts how many candles are below the MA © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many recent bars are below the EMA

BarsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently © ZenAndTheArtOfTrading

Parameters:

lookback (int)

ma (float)

Returns: The bar count of how many times price recently crossed the EMA

GetPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count) © ZenAndTheArtOfTrading

Parameters:

lookback (int)

direction (int)

Returns: The bar count of how many candles have retraced over the given lookback & direction

GetSwingHigh(Lookback, SwingType)

Check If Price Has Made A Recent Swing High

Parameters:

Lookback (int) : Is For The Swing High Lookback Period, Defval = 7

SwingType (int) : Is For The Swing High Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing High

GetSwingLow(Lookback, SwingType)

Check If Price Has Made A Recent Swing Low

Parameters:

Lookback (int) : Is For The Swing Low Lookback Period, Defval = 7

SwingType (int) : Is For The Swing Low Type Of Identification, Defval = 1

Returns: A Bool - True If Price Has Made A Recent Swing Low

//====================================================================================================================================================

// Custom Risk Management Functions

//====================================================================================================================================================

CalculateStopLossLevel(OrderType, Entry, StopLoss)

Calculate StopLoss Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLoss (float) : Is The Custom StopLoss Distance, Defval = 2x ATR Below Close

Returns: Float - The StopLoss Level In Actual Price As A

CalculateStopLossDistance(OrderType, Entry, StopLoss)

Calculate StopLoss Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

StopLoss (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The StopLoss Value In Pips

CalculateTakeProfitLevel(OrderType, Entry, StopLossDistance, RiskReward)

Calculate TakeProfit Level

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, Defval = na

StopLossDistance (float)

RiskReward (float)

Returns: Float - The TakeProfit Level In Actual Price

CalculateTakeProfitDistance(OrderType, Entry, TakeProfit)

Get TakeProfit Distance In Pips

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

Entry (float) : Is The Entry Level Of The Order, NEED TO INPUT PARAM

TakeProfit (float) : Level Based On Previous Calculation, NEED TO INPUT PARAM

Returns: Float - The TakeProfit Value In Pips

CalculateConversionCurrency(AccountCurrency, SymbolCurrency, BaseCurrency)

Get The Conversion Currecny Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

AccountCurrency (simple string) : Is For The Account Currency Used

SymbolCurrency (simple string) : Is For The Current Symbol Currency (Front Symbol)

BaseCurrency (simple string) : Is For The Current Symbol Base Currency (Back Symbol)

Returns: Tuple Of A Bollean (Convert The Currency ?) And A String (Converted Currency)

CalculateConversionRate(ConvertCurrency, ConversionRate)

Get The Conversion Rate Between Current Account Currency & Current Pair's Quoted Currency (FOR FOREX ONLY)

Parameters:

ConvertCurrency (bool) : Is To Check If The Current Symbol Needs To Be Converted Or Not

ConversionRate (float) : Is The Quoted Price Of The Conversion Currency (Input The request.security Function Here)

Returns: Float Price Of Conversion Rate (If In The Same Currency Than Return Value Will Be 1.0)

LotSize(LotSizeSimple, Balance, Risk, SLDistance, ConversionRate)

Get Current Lot Size

Parameters:

LotSizeSimple (bool) : Is To Toggle Lot Sizing Calculation (Simple Is Good Enough For Stocks & Crypto, Whilst Complex Is For Forex)

Balance (float) : Is For The Current Account Balance To Calculate The Lot Sizing Based Off

Risk (float) : Is For The Current Risk Per Trade To Calculate The Lot Sizing Based Off

SLDistance (float) : Is The Current Position StopLoss Distance From Its Entry Price

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - Position Size In Units

ToLots(Units)

Converts Units To Lots

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots

ToUnits(Lots)

Converts Lots To Units

Parameters:

Lots (float) : Is For How Many Lots Need To Be Converted Into Units (Minimun 0.01 Units)

Returns: Int - Position Size In Units

ToLotsInUnits(Units)

Converts Units To Lots Than Back To Units

Parameters:

Units (float) : Is For How Many Units Need To Be Converted Into Lots (Minimun 1000 Units)

Returns: Float - Position Size In Lots That Were Rounded To Units

ATRTrail(OrderType, SourceType, ATRPeriod, ATRMultiplyer, SwingLookback)

Calculate ATR Trailing Stop

Parameters:

OrderType (int) : Is To Determine A Long / Short Position, Defval = 1

SourceType (int) : Is To Determine Where To Calculate The ATR Trailing From, Defval = close

ATRPeriod (simple int) : Is To Change Its ATR Period, Defval = 20

ATRMultiplyer (float) : Is To Change Its ATR Trailing Distance, Defval = 1

SwingLookback (int) : Is To Change Its Swing HiLo Lookback (Only From Source Type 5), Defval = 7

Returns: Float - Number Of The Current ATR Trailing

DangerZone(WinRate, AvgRRR, Filter)

Calculate Danger Zone Of A Given Strategy

Parameters:

WinRate (float) : Is The Strategy WinRate

AvgRRR (float) : Is The Strategy Avg RRR

Filter (float) : Is The Minimum Profit It Needs To Be Out Of BE Zone, Defval = 3

Returns: Int - Value, 1 If Out Of Danger Zone, 0 If BE, -1 If In Danger Zone

IsQuestionableTrades(TradeTP, TradeSL)

Checks For Questionable Trades (Which Are Trades That Its TP & SL Level Got Hit At The Same Candle)

Parameters:

TradeTP (float) : Is The Trade In Question Take Profit Level

TradeSL (float) : Is The Trade In Question Stop Loss Level

Returns: Bool - True If The Last Trade Was A "Questionable Trade"

//====================================================================================================================================================

// Custom Strategy Functions

//====================================================================================================================================================

OpenLong(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Long Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Long"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Long Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

OpenShort(EntryID, LotSize, LimitPrice, StopPrice, Comment, CommentValue)

Open A Short Order Based On The Given Params

Parameters:

EntryID (string) : Is The Trade Entry ID, Defval = "Short"

LotSize (float) : Is The Lot Size Of The Trade, Defval = 1

LimitPrice (float) : Is The Limit Order Price To Set The Order At, Defval = Na / Market Order Execution

StopPrice (float) : Is The Stop Order Price To Set The Order At, Defval = Na / Market Order Execution

Comment (string) : Is The Order Comment, Defval = Short Entry Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

TP_SLExit(FromID, TPLevel, SLLevel, PercentageClose, Comment, CommentValue)

Exits Based On Predetermined TP & SL Levels

Parameters:

FromID (string) : Is The Trade ID That The TP & SL Levels Be Palced

TPLevel (float) : Is The Take Profit Level

SLLevel (float) : Is The StopLoss Level

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Returns: Void

CloseLong(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Long Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Long"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

CloseShort(ExitID, PercentageClose, Comment, CommentValue, Instant)

Exits A Short Order Based On A Specified Condition

Parameters:

ExitID (string) : Is The Trade ID That Will Be Closed, Defval = "Short"

PercentageClose (float) : Is The Amount To Close The Order At (In Percentage) Defval = 100

Comment (string) : Is The Order Comment, Defval = Exit Order

CommentValue (string) : Is For Custom Values In The Order Comment, Defval = Na

Instant (bool) : Is For Exit Execution Type, Defval = false

Returns: Void

BrokerCheck(Broker)

Checks Traded Broker With Current Loaded Chart Broker

Parameters:

Broker (string) : Is The Current Broker That Is Traded

Returns: Bool - True If Current Traded Broker Is Same As Loaded Chart Broker

OpenPC(LicenseID, OrderType, UseLimit, LimitPrice, SymbolPrefix, Symbol, SymbolSuffix, Risk, SL, TP, OrderComment, Spread)

Compiles Given Parameters Into An Alert String Format To Open Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Open

UseLimit (bool) : Is If We Want To Enter The Position At Exactly The Previous Closing Price

LimitPrice (float) : Is The Limit Price Of The Trade (Only For Pending Orders)

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Risk (float) : Is The Trade Risk Per Trade / Fixed Lot Sizing

SL (float) : Is The Trade SL In Price / In Pips

TP (float) : Is The Trade TP In Price / In Pips

OrderComment (string) : Is The Executed Trade Comment

Spread (float) : is The Maximum Spread For Execution

Returns: String - Pine Connector Order Syntax Alert Message

ClosePC(LicenseID, OrderType, SymbolPrefix, Symbol, SymbolSuffix)

Compiles Given Parameters Into An Alert String Format To Close Trades Using Pine Connector

Parameters:

LicenseID (string) : Is The Users PineConnector LicenseID

OrderType (int) : Is The Desired OrderType To Close

SymbolPrefix (string) : Is The Current Symbol Prefix (If Any)

Symbol (string) : Is The Traded Symbol

SymbolSuffix (string) : Is The Current Symbol Suffix (If Any)

Returns: String - Pine Connector Order Syntax Alert Message

//====================================================================================================================================================

// Custom Backtesting Calculation Functions

//====================================================================================================================================================

CalculatePNL(EntryPrice, ExitPrice, LotSize, ConversionRate)

Calculates Trade PNL Based On Entry, Eixt & Lot Size

Parameters:

EntryPrice (float) : Is The Trade Entry

ExitPrice (float) : Is The Trade Exit

LotSize (float) : Is The Trade Sizing

ConversionRate (float) : Is The Currency Conversion Rate (Used For Complex Lot Sizing Only)

Returns: Float - The Current Trade PNL

UpdateBalance(PrevBalance, PNL)

Updates The Previous Ginve Balance To The Next PNL

Parameters:

PrevBalance (float) : Is The Previous Balance To Be Updated

PNL (float) : Is The Current Trade PNL To Be Added

Returns: Float - The Current Updated PNL

CalculateSlpComm(PNL, MaxRate)

Calculates Random Slippage & Commisions Fees Based On The Parameters

Parameters:

PNL (float) : Is The Current Trade PNL

MaxRate (float) : Is The Upper Limit (In Percentage) Of The Randomized Fee

Returns: Float - A Percentage Fee Of The Current Trade PNL

UpdateDD(MaxBalance, Balance)

Calculates & Updates The DD Based On Its Given Parameters

Parameters:

MaxBalance (float) : Is The Maximum Balance Ever Recorded

Balance (float) : Is The Current Account Balance

Returns: Float - The Current Strategy DD

CalculateWR(TotalTrades, LongID, ShortID)

Calculate The Total, Long & Short Trades Win Rate

Parameters:

TotalTrades (int) : Are The Current Total Trades That The Strategy Has Taken

LongID (string) : Is The Order ID Of The Long Trades Of The Strategy

ShortID (string) : Is The Order ID Of The Short Trades Of The Strategy

Returns: Tuple Of Long WR%, Short WR%, Total WR%, Total Winning Trades, Total Losing Trades, Total Long Trades & Total Short Trades

CalculateAvgRRR(WinTrades, LossTrades)

Calculates The Overall Strategy Avg Risk Reward Ratio

Parameters:

WinTrades (int) : Are The Strategy Winning Trades

LossTrades (int) : Are The Strategy Losing Trades

Returns: Float - The Average RRR Values

CAGR(StartTime, StartPrice, EndTime, EndPrice)

Calculates The CAGR Over The Given Time Period © TradingView

Parameters:

StartTime (int) : Is The Starting Time Of The Calculation

StartPrice (float) : Is The Starting Price Of The Calculation

EndTime (int) : Is The Ending Time Of The Calculation

EndPrice (float) : Is The Ending Price Of The Calculation

Returns: Float - The CAGR Values

//====================================================================================================================================================

// Custom Plot Functions

//====================================================================================================================================================

EditLabels(LabelID, X1, Y1, Text, Color, TextColor, EditCondition, DeleteCondition)

Edit / Delete Labels

Parameters:

LabelID (label) : Is The ID Of The Selected Label

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

Text (string) : Is The Text Than Wants To Be Written In The Label

Color (color) : Is The Color Value Change Of The Label Text

TextColor (color)

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

EditLine(LineID, X1, Y1, X2, Y2, Color, EditCondition, DeleteCondition)

Edit / Delete Lines

Parameters:

LineID (line) : Is The ID Of The Selected Line

X1 (int) : Is The X1 Coordinate IN BARINDEX Xloc

Y1 (float) : Is The Y1 Coordinate IN PRICE Yloc

X2 (int) : Is The X2 Coordinate IN BARINDEX Xloc

Y2 (float) : Is The Y2 Coordinate IN PRICE Yloc

Color (color) : Is The Color Value Change Of The Line

EditCondition (int) : Is The Edit Condition of The Line (Setting Location / Color)

DeleteCondition (bool) : Is The Delete Condition Of The Line If Ture Deletes The Prev Itteration Of The Line

Returns: Void

//====================================================================================================================================================

// Custom Display Functions (Using Tables)

//====================================================================================================================================================

FillTable(TableID, Column, Row, Title, Value, BgColor, TextColor, ToolTip)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

Column (int) : Is The Current Column Of The Table That Wants To Be Edited

Row (int) : Is The Current Row Of The Table That Wants To Be Edited

Title (string) : Is The String Title Of The Current Cell Table

Value (string) : Is The String Value Of The Current Cell Table

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

ToolTip (string) : Is The ToolTip Of The Current Cell In The Table

Returns: Void

DisplayBTResults(TableID, BgColor, TextColor, StartingBalance, Balance, DollarReturn, TotalPips, MaxDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

StartingBalance (float) : Is The Account Starting Balance

Balance (float)

DollarReturn (float) : Is The Account Dollar Reture

TotalPips (float) : Is The Total Pips Gained / loss

MaxDD (float) : Is The Maximum Drawdown Over The Backtesting Period

Returns: Void

DisplayBTResultsV2(TableID, BgColor, TextColor, TotalWR, QTCount, LongWR, ShortWR, InitialCapital, CumProfit, CumFee, AvgRRR, MaxDD, CAGR, MeanDD)

Filling The Selected Table With The Inputed Information

Parameters:

TableID (table) : Is The Table ID That Wants To Be Edited

BgColor (color) : Is The Selected Color For The Current Table

TextColor (color) : Is The Selected Color For The Current Table

TotalWR (float) : Is The Strategy Total WR In %

QTCount (int) : Is The Strategy Questionable Trades Count

LongWR (float) : Is The Strategy Total WR In %

ShortWR (float) : Is The Strategy Total WR In %

InitialCapital (float) : Is The Strategy Initial Starting Capital

CumProfit (float) : Is The Strategy Ending Cumulative Profit

CumFee (float) : Is The Strategy Ending Cumulative Fee (Based On Randomized Fee Assumptions)

AvgRRR (float) : Is The Strategy Average Risk Reward Ratio

MaxDD (float) : Is The Strategy Maximum DrawDown In Its Backtesting Period

CAGR (float) : Is The Strategy Compounded Average GRowth In %

MeanDD (float) : Is The Strategy Mean / Average Drawdown In The Backtesting Period

Returns: Void

//====================================================================================================================================================

// Custom Pattern Detection Functions

//====================================================================================================================================================

BullFib(priceLow, priceHigh, fibRatio)

Calculates A Bullish Fibonacci Value (From Swing Low To High) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

BearFib(priceLow, priceHigh, fibRatio)

Calculates A Bearish Fibonacci Value (From Swing High To Low) © ZenAndTheArtOfTrading

Parameters:

priceLow (float)

priceHigh (float)

fibRatio (float)

Returns: The Fibonacci Value Of The Given Ratio Between The Two Price Points

GetBodySize()

Gets The Current Candle Body Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN POINTS

GetTopWickSize()

Gets The Current Candle Top Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Top Wick Size IN POINTS

GetBottomWickSize()

Gets The Current Candle Bottom Wick Size IN POINTS © ZenAndTheArtOfTrading

Returns: The Current Candle Bottom Wick Size IN POINTS

GetBodyPercent()

Gets The Current Candle Body Size As A Percentage Of Its Entire Size Including Its Wicks © ZenAndTheArtOfTrading

Returns: The Current Candle Body Size IN PERCENTAGE

GetTopWickPercent()

Gets The Current Top Wick Size As A Percentage Of Its Entire Body Size

Returns: Float - The Current Candle Top Wick Size IN PERCENTAGE

GetBottomWickPercent()

Gets The Current Bottom Wick Size As A Percentage Of Its Entire Bodu Size

Returns: Float - The Current Candle Bottom Size IN PERCENTAGE

BullishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Engulfing Candle

BearishEC(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bearish Engulfing Candle

Parameters:

Allowance (int) : To Give Flexibility Of Engulfing Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Engulfing Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Engulfing Candle

Hammer(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Star(Fib, ColorMatch, NearSwings, SwingLookBack, ATRFilterCheck, ATRPeriod)

Checks If The Current Bar Is A Hammer Candle

Parameters:

Fib (float) : To Specify Which Fibonacci Ratio To Use When Determining The Hammer Candle, Defval = 0.382 Ratio

ColorMatch (bool) : To Filter Only Bullish Closed Hammer Candle Pattern, Defval = false

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

ATRFilterCheck (float) : To Filter Smaller Hammer Candles That Might Be Better Classified As A Doji Candle, Defval = 1

ATRPeriod (simple int) : To Change ATR Period Of The ATR Filter, Defval = 20

Returns: Bool - True If The Current Bar Matches The Requirements of a Hammer Candle

Doji(MaxWickSize, MaxBodySize, DojiType, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Doji Candle

Parameters:

MaxWickSize (float) : To Specify The Maximum Lenght Of Its Upper & Lower Wick, Defval = 2

MaxBodySize (float) : To Specify The Maximum Lenght Of Its Candle Body IN PERCENT, Defval = 0.05

DojiType (int)

NearSwings (bool) : To Specify If We Want The Doji To Be Near A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High / Low (Only In Dragonlyf / Gravestone Mode), Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Doji Candle

BullishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bullsih Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing Low, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing Low, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bullish Harami Candle

BearishIB(Allowance, RejectionWickSize, EngulfWick, NearSwings, SwingLookBack)

Checks If The Current Bar Is A Bullish Harami Candle

Parameters:

Allowance (int) : To Give Flexibility Of Harami Pattern Detection In Markets That Have Micro Gaps, Defval = 0

RejectionWickSize (float) : To Filter Out long (Upper And Lower) Wick From The Bearish Harami Pattern, Defval = na

EngulfWick (bool) : To Specify If We Want The Pattern To Also Engulf Its Upper & Lower Previous Wicks, Defval = false

NearSwings (bool) : To Specify If We Want The Pattern To Be Near A Recent Swing High, Defval = true

SwingLookBack (int) : To Specify How Many Bars Back To Detect A Recent Swing High, Defval = 10

Returns: Bool - True If The Current Bar Matches The Requirements of a Bearish Harami Candle

//====================================================================================================================================================

// Custom Time Functions

//====================================================================================================================================================

BarInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls within the given time session

BarOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session © ZenAndTheArtOfTrading

Parameters:

sess (simple string)

useFilter (bool)

Returns: A boolean - true if the current bar falls outside the given time session

DateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range © ZenAndTheArtOfTrading

Parameters:

startTime (int)

endTime (int)

Returns: A boolean - true if the current bar falls within the given dates

DayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze © ZenAndTheArtOfTrading

Parameters:

monday (bool)

tuesday (bool)

wednesday (bool)

thursday (bool)

friday (bool)

saturday (bool)

sunday (bool)

Returns: A boolean - true if the current bar's day is one of the given days

AUSSess()

Checks If The Current Australian Forex Session In Running

Returns: Bool - True If Currently The Australian Session Is Running

ASIASess()

Checks If The Current Asian Forex Session In Running

Returns: Bool - True If Currently The Asian Session Is Running

EURSess()

Checks If The Current European Forex Session In Running

Returns: Bool - True If Currently The European Session Is Running

USSess()

Checks If The Current US Forex Session In Running

Returns: Bool - True If Currently The US Session Is Running

UNIXToDate(Time, ConversionType, TimeZone)

Converts UNIX Time To Datetime

Parameters:

Time (int) : Is The UNIX Time Input

ConversionType (int) : Is The Datetime Output Format, Defval = DD-MM-YYYY

TimeZone (string) : Is To Convert The Outputed Datetime Into The Specified Time Zone, Defval = Exchange Time Zone

Returns: String - String Of Datetime

Cerca negli script per "backtesting"

Optimized Zhaocaijinbao strategyIntroduction:

The Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It generates buy and sell signals by using a combination of exponential moving averages, moving averages, volume and slope indicators. It generates buy signals when the stock is above the 35-day moving average, the trading volume is higher than the 20-day moving average, and the stock is in an upward trend on a weekly timeframe."招财进宝" is a Chinese phrase that can be translated to "Attract Wealth and Bring in Treasure" in English. It is a common expression used to wish for good luck and prosperity in various contexts, such as in business or personal finances.

Highlights:

The strategy has several special optimizations that make it unique.

Firstly, the strategy is optimized for T+1 trading in the Chinese stock market and is only suitable for long positions. The optimizations are also applicable to international stock markets.

Secondly, the trend strategy is optimized to only show indicators on the right side and oscillations. This helps to prevent false signals in choppy markets.

Thirdly, the strategy uses a risk factor for dynamic position sizing to ensure position sizes are adjusted according to the current net asset value and risk preferences. This helps to lower drawdown risks.

The strategy has good resilience even without using stop loss modules in backtesting, making it suitable for trading hourly, 2-hourly, and daily K-line charts (depending on the stock being traded). We recommend experimenting with backtesting using SSE 1-hour or 2-hour or daily Kline charts.

Backtesting outcomes:

The strategy was backtested over the period from October 13th, 2005 to April 14th, 2023, using daily candlestick charts for the commodity code SSE:600763, with a currency of CNY and tick size of 0.01. The strategy used an initial capital of 1,000,000 CNY, with order sizes set to 10% equity and a pyramid of 1 order. The strategy also had a Max Position Size of 0.01 and a Risk Factor of 2.

Here is a summary of the performance of the trading strategy:

Total net profit: 288,577.32 CNY, representing a return of 128.86%

Total number of closed trades: 61

Winning trades: 37, representing a win rate of 60.66%

Profit factor: 2.415

Largest losing trade: 222,021.46 CNY, representing a loss of 14.08%

Average trade: 21,124.22 CNY, representing a return of 3.1%

Average holding period for all trades: 12 days

Conclusion:

In conclusion, the Optimized Zhaocaijinbao strategy is a mid and long-term quantitative trading strategy that combines momentum and trend factors. It is suitable for both Chinese stocks and global stocks. While the Optimized Zhaocaijinbao strategy has performed well in backtesting, it is important to note that past performance is not a guarantee of future results. Traders should conduct their own research and analysis and exercise caution when using any trading strategy.

Heikin Ashi Candle Startegy for Long PositionThis strategy utilize Heikin-Ashi candlestick chart.

Heikin-Ashi technique is a Japanese candlestick-based technical trading tool that uses candlestick charts to represent and visualize market price data.

Heikin-Ashi candle is essentially taking an average of the movement.

There is a tendency with Heikin-Ashi for the candles to stay red during a downtrend and green during an uptrend.

This strategy only apply for long trading position.

The idea is trader will waiting 3 green candles for validation period (confirmation) before entering long position.

Different timeframe will result different result.

Number of validation period can be changed to see different result

This strategy has parameter for take profit percentage, trailing stop and stop loss.

User can set maximum active position to minimize risk and qty order.

This tool is useful for user who wants to backtest Heikin-Ashi trading strategy.

Script will emit alert when long position is opened and closed.

Warning of Backtesting

Backtesting is backward-looking. As the name implies, you are testing how something would have worked if you traded it perfectly in the past.

Past performance does not indicate future performance and you should not assume it does.

Backtesting assumes you never miss-fire, that you get in and out at the exactly perfect moment each time.

Backtesting assumes you have perfect liquidity, and your limit orders fill at a specific, pre-defined price every time (either the open, close, low, high, or some average of these).

Disclaimer

Do your own research and consider fundamental price of asset.

The indicators provided on this script is for educational purposes only.

Author does not offer advisory or brokerage services, nor does it recommend or advise users to buy or sell particular stocks or securities.

Please examined script and give feedback for further improvement.

Script are open to public, everyone see and clone source code or just apply to chart. Please make comment for improvement.

Patient Trendfollower (7)(alpha)Patient Trendfollower consists of 21 and 55 EMA, Commodity Channel Index and Supertrend indicator. It confirms a trend and gives you a signal on a pullback. Original creation worked on 1h EURUSD chart.

►Long setup:

• 21 EMA is above 55 EMA, which is above the Supertrend indicator.

• Commodity Channel Index is an oscillator, which prints into the chart if extreme levels are reached. Green is for a level above 100 or below -100, red is above 140 or below -140 and black is above 180 or below -180.

• If 21 EMA > 55EMA > Supertrend and an oversold signal appear, you can buy into the trend.

• When backtesting on 1h EURUSD, profit target 400 pips worked best with a stop-loss below Supertrend's bottom and the size of your spread.

• A picture shows two valid entries.

: This part still malfunctions and shows red dots over some green ones. It is important to disable red ones in the settings to see green ones.

Some more long signals:

Some short signals:

►Backtesting data with default settings and trading only green CCI signals with mentioned risk management strategy:

• 212 closed trades

• 58.96% profitable with average win trade 348 USD and average loss trade 263 USD when only green signals are followed.

• Profit factor 1.903, Sharpee 0.792

• 20 bars is average for all trades, short trades were 18 bars long on average.

With given data, you can see the strategy is profitable by itself. However, original risk management settings do work only on 1h charts of EURUSD and would need to be adjusted for other instruments based on average volatility.

Even though the profitability is low, you can increase your odds by a great margin, if you properly use price action (impulsive and corrective moves, patterns, bar analysis), if you trade when major exchanges are open, you may also use wave analysis such as Elliot Waves or Market Profiles to predict whether the next day might be a trending day. My backtesting program didn't consider these ideas.

Unfortunately, I won't be making backtesting strategy public with it anytime soon, because it still has some parts that do not work. I am ok with that since I understand the code and know what does malfunction and how. Then, there are parts which I am not sure how to fix yet. This is why the indicator is still considered alpha.

In the future when a strategy is published, you will also be able to set your own overbought/oversold values without entering the code itself and probably some other features. But I am not in a hurry for that. You can give me feedback on UX and try to figure out the best setups for other symbols, it might help to improve the automatic testing script when I know what I should achieve. My main point is to make this public for friends who can already be using it on EURUSD at least.

Close doesn't always have to be 400 pips, you might want to close on a logical level such as strong resistance or a trendline too.

Thanks to:

• @everget for providing Supertrend solution.

• Satik FX who hand-tested the system by hand and reported results in this article . He is my main inspiration for creating the complete indicator as one because I want to be able to show and hide it with a single click. My future scripts will also work as a whole strategy each by itself.

• The number in the script's name comes from Satik's numbering. A mentioned article was his seventh shared strategy.

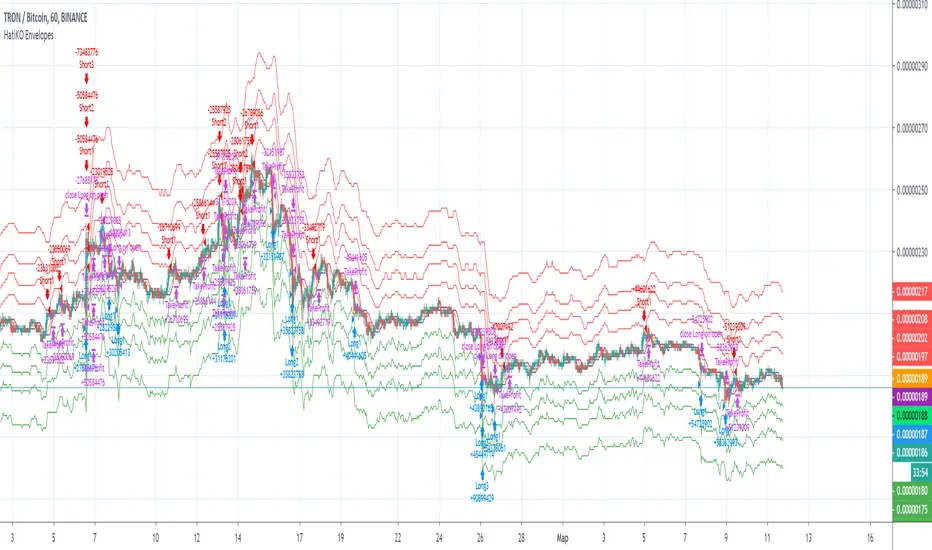

HatiKO EnvelopesPublished source code is subject to the terms of the GNU Affero General Public License v3.0

This script describes and provides backtesting functionality to internal strategy of algorithmic crypto trading software "HatiKO bot".

Suitable for backtesting any Cryptocurrency Pair on any Exchange/Platform, any Timeframe.

Core Mechanics of this strategy are based on theory of price always returning to Moving Average + Envelopes indicator (Moving_average_envelope from Wiki)

Developement of this script and trading software is inspired by:

"Essential Technical Analysis: Tools and Techniques to Spot Market Trends" by Leigh Stevens (published on 12th of April 2002)

"Moving Average Envelopes" by ChartSchool, StockCharts platform (published on 13th of April 2015 or earlier)

"Коля Колеснік" from Crypto Times channel ("Метод сетка", published on 19th of August 2018)

"3 ways to use Moving Average Envelopes" by Rich Fitton, published on Trader's Nest (published on 28st of November 2018 or earlier)

noro's "Robot WhiteBox ShiftMA" strategy v1 script, published on TradingView platform (published on 29th of August 2018)

"Moving Average Envelopes: A Popular Trading Tool" Investopedia article (published 25th of June 2019)

and KROOL1980's blogpost on Argolabs ("Гридерство или Сетка как источник прибыли на форекс", published on 27th of February 2015)

Core Features:

1) Up to 4 Envelopes in each direction (Long/Short)

2) Use any of 6 different basis MAs, optionally use different MAs for Opening and Closure

3) Use different Timeframes for MA calculation, without any repainting and lookahead bias.

4) Fixed order size, not Martingale strategy

5) Close open position earlier by using Deviation parameter

6) PineScript v4 code

Options description:

Lot - % from your initial balance to use for order size calculation

Timeframe Short - Timeframe to use for Short Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Short - Type of MA to use for Short Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Short - Source of Price for Short Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short - Period used for Short Opening MA calculation, should be >=1, default is 3

MA offset Short - Offset for MA value used for Short Envelopes calculation, should be >= 0, default is 0

Timeframe Long - Timeframe to use for Long Opening MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Long - Type of MA to use for Long Opening MA calculation, can be chosen from dropdown list, default is SMA

Data Long - Source of Price for Long Opening MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long - Period used for Long Opening MA calculation, should be >=1, default is 3

MA offset Long - Offset for MA value used for Long Envelopes calculation, should be >= 0, default is 0

Mode close MA Short - Enable different MA for Short position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Short Close - Timeframe to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Short - Type of MA to use for Short Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Short Close - Source of Price for Short Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Short Close - Period used for Short Opening MA calculation, should be >=1, default is 3

Short Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Short Close - Offset for MA value used for Short Position Closure calculation, should be >= 0, default is 0

Mode close MA Long - Enable different MA for Long position Closure, default is "false". If false, Closure MA = Opening MA

Timeframe Long Close - Timeframe to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is Current Graph Timeframe

MA Type Close Long - Type of MA to use for Long Position Closure MA calculation, can be chosen from dropdown list, default is SMA

Data Long Close - Source of Price for Long Closure MA calculation, can be chosen from dropdown list, default is OHLC4

MA Length Long Close - Period used for Long Opening MA calculation, should be >=1, default is 3

Long Deviation - % to move from MA value, used to close position above or beyond MA, can be negative, default is 0

MA offset Long Close - Offset for MA value used for Long Position Closure calculation, should be >= 0, default is 0

Short Shift 1..4 - % from MA value to put Envelopes at, for Shorts numbers should be positive, the higher is number, the higher should be Shift position, example: "Shift 1 = 1, shift 2 = 2, etc."

Long Shift 1..4 - % from MA value to put Envelopes at, for Longs numbers should be negative, the lower is number, the lower should be Shift position, example: "Shift 1 = -1, shift 2 = -2, etc."

From Year 20XX - Backtesting Starting Year number, only 20xx supported as script is cryptocurrency-oriented.

To Year 20XX - Backtesting Final Year number, only 20xx supported as script is cryptocurrency-oriented.

From Month - Years starting Month, optional tweaking, changing not recommended

To Month - Years ending Month, optional tweaking, changing not recommended

From day - Months starting day, optional tweaking, changing not recommended

To day - Months ending day, optional tweaking, changing not recommended

Graph notes:

Green lines - Long Envelopes.

Red lines - Short Envelopes.

Orange line - MA for closing of Short positions.

Lime line - MA for closing of Long positions.

**************************************************************************************************************************************************************************************************************

Опубликованный исходный код регулируется Условиями Стандартной Общественной Лицензии GNU Affero v3.0

Этот скрипт описывает и предоставляет функции бектеста для внутренней стратегии алгоритмического программного обеспечения "HatiKO bot".

Подходит для тестирования любой криптовалютной пары на любой бирже/платформе, на любом таймфрейме.

Кор-механика этой стратегии основана на теории всегда возвращающейся к значению МА цены с использованием индикатора Envelopes (Moving_average_envelope from Wiki)

Разработка этого скрипта и программного обеспечения для торговли вдохновлена следующими источниками:

Книга "Essential Technical Analysis: Tools and Techniques to Spot Market Trends" Ли Стивенса (опубликовано 12 апреля 2002 года)

«Moving Average Envelopes» от ChartSchool, платформа StockCharts (опубликовано 13 апреля 2015 года или раньше)

«Коля Колеснік» с канала Crypto Times («Метод сетка», опубликовано 19 августа 2018 года)

«3 ways to use Moving Average Envelopes» Рича Фиттона, опубликованные в «Trader's Nest» (опубликовано 28 ноября 2018 года или раньше)

Скрипт стратегии noro "Robot WhiteBox ShiftMA" v1, опубликованный на платформе TradingView(опубликовано 29 августа 2018 года)

«Moving Average Envelopes: A Popular Trading Tool», статья Investopedia (опубликовано 25 июня 2019 года)

Блог KROOL1980 из Argolabs («Гридерство или Сетка как источник прибыли на форекс», опубликовано 27 февраля 2015 года)

Основные особенности:

1) До 4-х Ордеров в каждом из направлении (Лонг / Шорт)

2) Выбор из 6-ти разных базовых МА, опционально используйте разные МА для открытия и закрытия.

3) Используйте разные таймфреймы для расчета MA, без перерисовки и "эффекта стеклянного шара".

4) Фиксированный размер ордера, а не стратегия Мартингейла

5) Возможность закрытия открытой позиции заблаговременно, используя параметр Deviation

6) Код реализован на PineScript v4

Описание параметров:

Lot - % от вашего первоначального баланса, используется при расчете размера Ордера

Timeframe Short - таймфрейм, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Short - тип MA, используемый для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию SMA

Data Short - источник цены для расчета МА Открытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short - период, используемый для расчета МА Открытия Шорт позиций, должен быть >= 1, по умолчанию 3

MA Offset Short - смещение значения MA, используемого для расчета Шорт Ордеров, должно быть >= 0, по умолчанию 0

Timeframe Long - таймфрейм, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Long - тип MA, используемый для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию SMA

Data Long - источник цены для расчета МА Открытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long - период, используемый для расчета МА Открытия Лонг позиций, должен быть >= 1, по умолчанию 3

MA Offset Long - смещение значения MA, используемого для расчета Лонг Ордеров, должно быть >= 0, по умолчанию 0

Mode close MA Short - Включает отдельное MA для закрытия Шорт позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Short Close - таймфрейм, используемый для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Short - тип MA, используемый при расчете МА Закрытия Шорт позиции. Mожно выбрать из списка, по умолчанию SMA

Data Short Close - источник цены для расчета МА Закрытия Шорт позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Short Close - период, используемый для расчета МА Закрытия Шорт позиции, должен быть >= 1, по умолчанию 3

Short Deviation - % отклонения от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Short Close - смещение значения MA, используемого для расчета закрытия Шорт позиции, должно быть >= 0, по умолчанию 0

Mode close MA Long - Включает разные MA для закрытия Лонг позиции, по умолчанию «false». Если false, MA Закрытия = MA Открытия

Timeframe Long Close - таймфрейм, используемый для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию - таймфрейм текущего графика

MA Type Close Long - тип MA, используемый при расчете МА Закрытия Лонг позиции. Mожно выбрать из списка, по умолчанию SMA

Data Long Close - источник цены для расчета МА Закрытия Лонг позиций, может быть выбран из списка, по умолчанию OHLC4

MA Length Long Close - период, используемый для расчета МА Закрытия Лонг позиции, должен быть >= 1, по умолчанию 3

Long Deviation -% для перехода от значения MA, используется для закрытия позиции выше или ниже рассчитанного значения MA, может быть отрицательным, по умолчанию 0

MA Offset Long Close - смещение значения MA, используемого для расчета закрытия Лонг позиции, должно быть >= 0, по умолчанию 0

Short Shift 1..4 - % от значения MA для размещения Ордеров, для Шорт Ордеров должен быть положительным, чем выше номер, тем выше должна располагаться позиция Shift, например: «Shift 1 = 1, Shift 2 = 2 и т.д. "

Long Shift 1..4 - % от значения MA для размещения Ордеров, для Лонг Ордеров должно быть отрицательным, чем ниже число, тем ниже должна располагаться позиция Shift, например: «Shift 1 = -1, Shift 2 = -2, и т.д."

From Year 20XX - Год начала тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

To Year 20XX - Год окончания тестирования, из-за ориентированности на криптовалюты поддерживаются только значения формата 20хх.

From Month - Начальный месяц, опционально, менять не рекомендуется

To Month - Конечный месяц, опционально, менять не рекомендуется

From day - Начальный день месяца, опционально, менять не рекомендуется

To day - Конечный день месяца, опционально, менять не рекомендуется

Пояснения к графику:

Зеленые линии - Лонг Ордера.

Красные линии - Шорт Ордера.

Оранжевая линия - MA Закрытия Шорт позиций.

Лаймовая линия - MA Закрытия Лонг позиций.

SMA Cross Entry & Exit StrategyThis is a TradingView Strategy Script meaning you can't execute real trades using your exchange API connected to your TradingView account, it is designed for backtesting only

This is a basic backtesting script for charting the bullish and bearish cross of two user defined simple moving averages, select the cog next to the name of the script ON the price chart in the left hand corner. The script will print to the screen either "Long Entry" or "Short Entry" depending on the direction of the cross. The script using TradingView strategies will subsequently close the opposite of the position that is executed when the bullish or bearish cross occurs. Simply put, if you are short and a bullish cross occurs, your short trade will close and be logged in strategies and the long will fire. You can pyramid the long and short positions to continue entering as long as the trend doesn't flip. You will find this in the script settings. Since this script is for backtesting you can manually set the "backtesting range" for TradingView Strategies and firing the "Long Entry" and "Short Entry". This as well, is in the settings.

Notice: When the SMA cross occurs, you have to wait till the next candle before TradingView Strategy will print the "Long Entry" or "Short Entry" to the screen

TradingView - How To Use Strategies: www.tradingview.com

Noro's SILA v1.6L StrategyBacktesting

Backtesting (for all the time of existence of couple) only with software configurations to default (without optimization of parameters):

US = Uptrend-Sensivity

DS = Downtrend-Sensivity

It is recommended and by default:

- the normal market requires US=DS (for example US=5, DS=5)

- very bear market requires US DS, (for example US=5, DS=0)

- very bull market requires US DS, (US=0, DS=5)

Cryptocurrencies it is very bull market (US=0, DS=5)

Backtesting BTC/FIAT

D1 timeframe

identical parameters for all pairs

BTC/USD (Bitstamp) profit of +41805%

BTC/EUR (BTC-e) profit of +1147%

BTC/RUB (BTC-e) profit of +1162%

BTC/JPY (Bitflyer) profit of +215%

BTC/CNY (BTCChina) profit of 54948%

Backtesting ALTCOIN/BTC

D1 timeframe

identical parameters for all pairs

the exchange Poloniex

top-10 of cryptocurrencies on capitalization at the time of this text

NA = TradingView can't make backtest because of too low price of this cryptocurrency, or on the website there are no quotations of this cryptocurrency

ETH/BTC (Etherium) profit of +11690%

XRP/BTC (Ripple) loss of-100%

LTC/BTC (Litecoin) NA

ETC/BTC (Etherium Classic) profit of +214%

NEM/BTC loss of-49%

DASH/BTC profit of +106%

IOTA/BTC NA

XMR/BTC (Monero) profit of +96%

STRAT/BTC (Stratis) loss of-31%

ALTCOIN/ALTCOIN - not recomended

I don't need your money, I need reputation and likes.

MA-trix Laboratory [DAFE]MA-trix Laboratory : The Ultimate Moving Average & Trend Following Engine

55+ Algorithms. Dual/Triple MA Systems. Advanced Signal Filtering. Quantum Smoothing. This is not just a moving average; it is the definitive toolkit for forging your perfect trend.

█ PHILOSOPHY: WELCOME TO THE LABORATORY

The moving average is the cornerstone of technical analysis. It is also, in its standard form, an obsolete, one-dimensional tool. A simple EMA or SMA is a blunt instrument in a market that demands surgical precision. It lags, it whipsaws, and it fails to adapt to the market's ever-changing character.

The MA-trix Laboratory was not created to be another moving average. It was engineered to be the final word on moving averages—a comprehensive, institutional-grade research and execution environment. This is not an indicator; it is a powerful, interactive sandbox where you, the trader, can move beyond the static "one-size-fits-all" approach. Here, you can experiment, test, and forge a moving average system that is perfectly synchronized with your specific market, timeframe, and analytical style.

We have deconstructed the very concept of "average" and rebuilt it from the ground up, creating a library of over 55 distinct mathematical algorithms —from timeless classics to proprietary quantum models—all housed within a single, unified, and infinitely configurable engine.

█ WHAT MAKES THIS A "LABORATORY"? THE CORE INNOVATIONS

This tool stands in a class of its own, offering a suite of features that collectively create an unparalleled analytical experience.

The 55+ Algorithm MA Core: This is the heart of the Laboratory. You are not limited to one or two MA types. You have a vast library of over 55 unique mathematical engines at your command, from classical SMAs to advanced adaptive algorithms like KAMA and FRAMA, to proprietary DAFE models like the "DAFE Flux Reactor" and "DAFE Quantum Step."

Multi-MA Architecture: Seamlessly switch between Single, Dual, and Triple MA operational modes. Build classic two-line crossover systems, three-line trend alignment confirmations, or beautiful, flowing ribbons with just a single click.

Advanced Post-Smoothing Engine: In a revolutionary step, you can apply a second layer of signal processing to your chosen MA. Select from a suite of over 20 professional-grade noise filters —including Ehlers' SuperSmoother, Kalman Filters, and the proprietary "DAFE Phase-Zero"—to surgically remove noise from your MA line after it has been calculated, achieving unprecedented smoothness without significant lag.

The Institutional Signal Filtering Suite: A signal is only as good as its filter. The Laboratory includes a powerful, multi-domain filter engine that acts as an intelligent gatekeeper for your signals. You can require signals to be confirmed by any combination of:

📦 Volume: Require a surge in volume to validate a crossover.

🌊 Volatility: Only take signals during low-volatility "squeeze" conditions or high-volatility expansions.

💪 Trend: Use the ADX to ensure you are only taking signals in the direction of a strong, established trend.

🚀 Momentum: Use RSI, MACD, or ROC to confirm that momentum is on your side.

Integrated Performance Engine: How do you know which of the 55+ algorithms is best? You test it. The built-in Performance Dashboard is a comprehensive backtesting engine that tracks every trade generated by your configuration, providing real-time data on Win Rate, Profit Factor, Net P&L, and Max Drawdown.

█ THE ARSENAL: A DEEP DIVE INTO THE ALGORITHMIC CORE

This is your library of mathematical DNA. The 55+ MA types are grouped into distinct families, each with a unique philosophy.

THE ALGORITHM FAMILIES

The Classics (SMA, EMA, WMA, etc.): The foundational building blocks. Simple, reliable, and universally understood. EMA for responsiveness, SMA for smoothness.

The Low-Lag Warriors (DEMA, TEMA, Hull MA, ZLEMA): A family of MAs engineered specifically to combat the inherent lag of classical averages. The Hull MA is a standout, offering a remarkable balance of extreme smoothness and near-zero lag.

The Adaptive Geniuses (KAMA, VIDYA, FRAMA, Volatility Adjusted MA): These are "smart" MAs. They contain internal logic that allows them to automatically change their speed based on market conditions. They will tighten up in fast-moving trends and loosen in sideways chop, intelligently filtering out noise.

The DSP & Quantitative Masters (Gaussian, Ehlers, Butterworth, Laguerre): These algorithms are born from the world of digital signal processing and advanced mathematics. They use sophisticated techniques like bell-curve weighting, non-linear feedback loops, and frequency filtering to separate the true trend "signal" from market "noise" with unparalleled precision.

The DAFE Proprietary Engines (The "Black Ops" MAs): The crown jewels of the Laboratory. These are custom-built, proprietary algorithms you will not find anywhere else:

DAFE Flux Reactor: A volatility-thermodynamic MA that adapts its alpha using a sigmoid function on Bollinger Band width, creating explosive responsiveness during volatility breakouts.

DAFE Tensor Flow: A multi-vector MA that uses a weighted average of the OHLC data (a "tensor") before applying Hull smoothing, creating an incredibly robust center of gravity.

DAFE Quantum Step: A non-linear, stepped MA that only moves if price exceeds a volatility-based quantum threshold, effectively ignoring all insignificant noise.

DAFE Gravity Well: An institutionally-focused MA that weights its calculation by both time (recency) and volume, pulling the average towards zones of heavy market participation.

THE POST-SMOOTHING FILTERS

This is a second layer of refinement. After your primary MA is calculated, you can pass it through one of over 20 advanced filters to achieve an even higher degree of clarity.

The Ehlers Filters (SuperSmoother, 2-Pole, 3-Pole): A suite of brilliant DSP filters for surgical noise removal.

The Kalman Filter: A predictive filter from robotics and aerospace engineering that provides an "optimal estimate" of the MA's true position.

DAFE Proprietary Smoothers:

DAFE Phase-Zero: Uses a de-trending feedback loop to achieve near-zero lag smoothing.

DAFE Spectral Smooth: A frequency-domain filter that removes jitter while preserving the primary trend.

█ OPERATIONAL MODES & SIGNAL GENERATION

The Laboratory is designed for ultimate flexibility.

Modes: Instantly switch between Single, Dual, and Triple MA modes. Each mode can be a standard line display or a beautiful, flowing Ribbon .

Signal Logic: You have complete control over what constitutes a "signal." Choose from nine different logic modes, including classic Price Cross , Dual MA Cross , Triple MA Alignment , or even advanced logic like Slope Change and Sequential Cross .

The Filter Gauntlet: Before a signal is plotted, it can be passed through the four-stage filtering suite. You can demand that a simple EMA crossover is also confirmed by high volume, ADX trend strength, and bullish RSI—all at the same time. This transforms a basic signal into a high-conviction, multi-factor setup.

█ THE MASTER DASHBOARD: YOUR MISSION CONTROL

The comprehensive dashboard is your unified command center for analysis and performance tracking.

Engine Status: See the currently selected Operation Mode and a detailed breakdown of the type and length of each active MA.

Market Dynamics: Get an at-a-glance view of the current Trend Status, Momentum intensity (based on MA slope), and the percentage deviation of price from your primary MA.

Filter Readout: If filters are enabled, the dashboard provides a live status for each active filter (Volume, Volatility, Trend, Momentum), showing you a "PASS" or "BLOCK" status in real-time.

Performance Readout: When enabled, this section provides a full breakdown of your backtesting results, including Trade Count, Win Rate, Profit Factor, Net P&L, and Max Drawdown.

█ DEVELOPMENT PHILOSOPHY

The MA-trix Laboratory was born from a deep respect for the moving average and a relentless desire to push its boundaries into the 21st century. We believe that in modern markets, static tools are obsolete. The future of trading lies in adaptation and customization. This indicator is for the serious trader, the tinkerer, the scientist—the individual who is not content with a black box, but who seeks to understand, test, and refine their edge with surgical precision. It is a tool for forging your own alpha, not just following someone else's.

"I don't think traders can follow rules for very long unless they reflect their own trading style. Eventually, a breaking point is reached and the trader has to quit or change, or find a new set of rules he can follow. This seems to be part of the process of evolution and growth of a trader."

█ DISCLAIMER AND BEST PRACTICES

THIS IS A TOOL, NOT A STRATEGY: This indicator provides a sophisticated trend and signal generation framework. It must be integrated into a complete trading plan that includes risk management, position sizing, and your own contextual analysis.

TEST, DON'T GUESS: The power of this tool is its adaptability. Use the Performance Dashboard to rigorously test different algorithms, settings, and filters on your chosen asset and timeframe. Find what works, and build your strategy around that data.

START SIMPLE: The possibilities can be overwhelming. Begin with a classic Dual MA mode (e.g., EMA 20/50) with no filters. Once you are comfortable, begin experimenting with more advanced MA types and layering on filters one by one.

RISK MANAGEMENT IS PARAMOUNT: All trading involves substantial risk. The backtesting results are hypothetical and do not account for slippage or psychological factors.

Never risk more capital than you are prepared to lose.

— Ed Seykota, Market Wizard

The MA-trix Laboratory is designed to be the ultimate tool for that evolution, allowing you to discover and codify the rules that truly fit you.

Taking you to school. - Dskyz, Don't be average. Trade with MA-trix. Trade with DAFE

PSAR Laboratory [DAFE]PSAR Laboratory : The Ultimate Adaptive Trailing Stop & Reversal Engine

23 Advanced Algorithms. Adaptive Acceleration. Smart Flip Logic. Parabolic SAR Reimagined.

█ PHILOSOPHY: WELCOME TO THE LABORATORY

The standard Parabolic SAR, created by the legendary J. Welles Wilder Jr., is a tool of beautiful simplicity. But in today's complex, algorithm-driven markets, its simplicity is its fatal flaw. Its fixed acceleration and rigid flip logic cause it to fail precisely when you need it most: it whipsaws in choppy conditions and gives back too much profit in strong trends.

The PSAR Laboratory was not created to be just another PSAR. It was engineered to be the definitive evolution of Wilder's original concept. This is not an indicator; it is a powerful, interactive research environment. It is a sandbox where you, the trader, can move beyond the static "one-size-fits-all" approach and forge a PSAR that is perfectly adapted to your specific market, timeframe, and trading style.

We have deconstructed the very DNA of the Parabolic SAR and rebuilt it from the ground up, infusing it with modern quantitative techniques. The result is an institutional-grade suite of 23 distinct, mathematically diverse algorithms that dynamically control every aspect of the PSAR's behavior.

█ WHAT MAKES THIS A "LABORATORY"? THE CORE INNOVATIONS

This tool stands in a class of its own. It is a collection of what could be 23 separate indicators, all seamlessly integrated into one powerful engine.

The 23 Algorithm Engine: This is the heart of the Laboratory. Instead of one rigid formula, you have a library of 23 unique mathematical engines at your command. These algorithms are not simple tweaks; they are complete re-imaginings of how the PSAR should behave, based on concepts from information theory, digital signal processing, fractal geometry, and institutional analysis.

Truly Adaptive Acceleration (AF): The standard PSAR's "gas pedal" (the AF) is dumb; it accelerates at a fixed rate. Our algorithms make it intelligent. The AF can now speed up in clean, trending environments to lock in profits, and automatically slow down in choppy, chaotic conditions to avoid whipsaws.

Advanced Flip Confirmation Logic: Say goodbye to noise-driven flips. You are no longer at the mercy of a single wick touching the SAR. The Laboratory provides multiple layers of flip confirmation, including requiring a bar close beyond the SAR, a volume spike to validate the reversal, or even a multi-bar confirmation .

Comprehensive Noise Filtering Core: In a revolutionary step, you can apply one of over 30 advanced signal processing filters directly to the SAR output itself. From ultra-low-lag filters like the Hull MA and DAFE Spectral Laguerre to adaptive filters like KAMA and FRAMA , you can surgically remove noise while preserving the responsiveness of the core signal.

Integrated Performance Engine: How do you know which of the 23 algorithms is best for your market? You test it. The built-in Performance Dashboard is a comprehensive backtesting and analytics engine that tracks every trade, providing real-time data on Win Rate, Profit Factor, Max Drawdown, and more. It allows you to scientifically validate your chosen configuration.

█ A GUIDED TOUR OF THE ALGORITHMS: 23 PATHS TO AN EDGE

b]These 23 algorithms are not simple settings; they are distinct mathematical philosophies for how a Parabolic SAR should adapt to the market. They are grouped into three primary categories: those that adapt the Acceleration Factor (AF) , those that enhance the Extreme Point (EP) detection, and those that redefine the Flip Logic .

CATEGORY A: ACCELERATION FACTOR (AF) ADAPTATION

These algorithms dynamically change the "gas pedal" of the PSAR.

1. Volatility-Scaled AF

Core Concept: Treats volatility as market friction. The PSAR should be more forgiving in high-volatility environments.

How It Works: It calculates a Volatility Ratio by comparing the short-term ATR to the long-term ATR. If current volatility is high (ratio > 1), it reduces the AF Step. If volatility is low (ratio < 1), it increases the AF Step to trail tighter.

Ideal Use Case: The best all-rounder. Excellent for any market, especially those with clear shifts between high and low volatility regimes (like indices and crypto).

2. Efficiency Ratio (ER) AF

Core Concept: The PSAR should accelerate aggressively in clean, efficient trends and slow down dramatically in choppy, inefficient markets.

How It Works: It uses Kaufman's Efficiency Ratio (ER), which measures the net directional movement versus the total price movement. A high ER (near 1.0) signifies a pure trend, triggering a high AF multiplier. A low ER (near 0.0) signifies chop, triggering a low AF multiplier.

Ideal Use Case: Markets that alternate between strong trends and sideways chop. It is exceptionally good at surviving ranging periods.

3. Shannon Entropy AF

Core Concept: Uses Information Theory to measure market disorder. The PSAR should be conservative in chaos and aggressive in order.

How It Works: It calculates the Shannon Entropy of recent price changes. High entropy means the market is unpredictable ("chaotic"), causing the AF to slow down. Low entropy means the market is organized and trending, causing the AF to speed up.

Ideal Use Case: Advanced traders looking for a mathematically pure way to distinguish between a tradable trend and random noise.

4. Fractal Dimension (FD) AF

Core Concept: Measures the "jaggedness" or complexity of the price path. A smooth path is a trend; a jagged, space-filling path is chop.

How It Works: It calculates the Fractal Dimension of the price series. An FD near 1.0 is a smooth line (high AF). An FD near 1.5 is a random walk (low AF).

Ideal Use Case: Visually identifying the moment a smooth trend begins to break down into chaotic, unpredictable movement.

5. ADX-Gated AF

Core Concept: Uses the classic ADX indicator to confirm the presence of a trend before allowing the PSAR to accelerate.

How It Works: If the ADX value is above a "Strong" threshold (e.g., 25), the AF accelerates normally. If the ADX is below a "Weak" threshold (e.g., 15), the AF is "frozen" and will not increase, preventing the SAR from tightening up in a non-trending market.

Ideal Use Case: For classic trend-following purists who trust the ADX as their primary regime filter.

6. Kalman AF Estimator

Core Concept: A sophisticated signal processing algorithm that predicts the "true" optimal AF by filtering out price "noise."

How It Works: It treats the PSAR's AF as a state to be estimated. It makes a prediction, then corrects it based on how far the actual price deviates. It's like a GPS constantly refining its position. The "Process Noise" input controls how fast it thinks the AF can change, while "Measurement Noise" controls how much it trusts the price data.

Ideal Use Case: Smooth, high-inertia markets like commodities or major forex pairs. It creates an incredibly smooth and responsive AF.

7. Volume-Momentum AF

Core Concept: A trend's acceleration is only valid if confirmed by both volume and price momentum.

How It Works: The AF will only increase if a new Extreme Point is made on above-average volume AND the Rate of Change (ROC) of the price is aligned with the trend's direction.

Ideal Use Case: Any market with reliable volume data (stocks, futures, crypto). It's excellent for filtering out low-conviction moves.

8. Garman-Klass (GK) AF

Core Concept: Uses a more advanced, statistically efficient measure of volatility (Garman-Klass, which uses OHLC data) to adapt the AF.

How It Works: It modulates the AF based on whether the current GK volatility is higher or lower than its historical average. Unlike the standard Volatility-Scaled algo, it tends to slow down more in high volatility and speed up less in low volatility, making it more conservative.

Ideal Use Case: Traders who want a volatility-adaptive model that is more focused on risk reduction during volatile periods.

9. RSI-Modulated AF

Core Concept: The RSI can identify points of potential trend exhaustion or strong momentum.

How It Works: If a trend is bullish but the RSI enters the "Overbought" zone, the AF slows down, anticipating a pullback. Conversely, if the RSI is in the strong momentum mid-range (40-60), the AF is boosted to trail more aggressively.

Ideal Use Case: Mean-reversion traders or those who want to automatically loosen their trail stop near potential exhaustion points.

10. Bollinger Squeeze AF

Core Concept: A Bollinger Band Squeeze signals a period of volatility compression, often preceding an explosive breakout.

How It Works: When the algorithm detects that the Bollinger Band Width is in a "Squeeze" (below a certain historical percentile), it boosts the AF in anticipation of a fast move, allowing the PSAR to catch the breakout quickly.

Ideal Use Case: Breakout traders. This algorithm primes the PSAR to be maximally responsive right at the moment a breakout is most likely.

11. Keltner Adaptive AF

Core Concept: Keltner Channels provide a robust measure of a trend's "normal" volatility channel.

How It Works: When price is trading strongly outside the Keltner Channel, it's considered a powerful trend, and the AF is boosted. When price falls back inside the channel, it's considered a consolidation or pullback, and the AF is slowed down.

Ideal Use Case: Trend followers who use channel breakouts as their primary confirmation.

12. Choppiness-Gated AF

Core Concept: Uses the Choppiness Index to quantify whether the market is trending or consolidating.

How It Works: If the Choppiness Index is below the "Trend" threshold (e.g., 38.2), the AF is boosted. If it's above the "Range" threshold (e.g., 61.8), the AF is significantly reduced.

Ideal Use Case: A more responsive alternative to the ADX-Gated algorithm for distinguishing between trending and ranging markets.

13. VIDYA-Style AF

Core Concept: Uses a Chande Momentum Oscillator (CMO) to create a variable-speed acceleration factor.

How It Works: The absolute value of the CMO is used to create a dynamic smoothing constant. Strong momentum (high absolute CMO) results in a faster, more responsive AF. Weak momentum results in a slower, smoother AF.

Ideal Use Case: Momentum traders who want their trailing stop's speed directly tied to the momentum of the price itself.

14. Hilbert Cycle AF

Core Concept: Uses Ehlers' Hilbert Transform to extract the dominant cycle period of the market and synchronizes the PSAR with it.

How It Works: It dynamically adjusts the AF based on the detected cycle period (shorter cycles = faster AF) and can also modulate it based on the current phase within that cycle (e.g., accelerate faster near cycle tops/bottoms).

Ideal Use Case: Markets with clear cyclical behavior, like commodities and some forex pairs.

CATEGORY B: EXTREME POINT (EP) ENHANCEMENT

These algorithms make the detection of new highs/lows more intelligent.

15. Volume-Weighted EP

Core Concept: A new high or low is more significant if it occurs on high volume.

How It Works: It can be configured to only accept a new EP if the volume on that bar is above average. It can also "weight" the EP by volume, pushing it further out on high-volume bars.

Ideal Use Case: Filtering out weak, low-conviction price probes in markets with reliable volume.