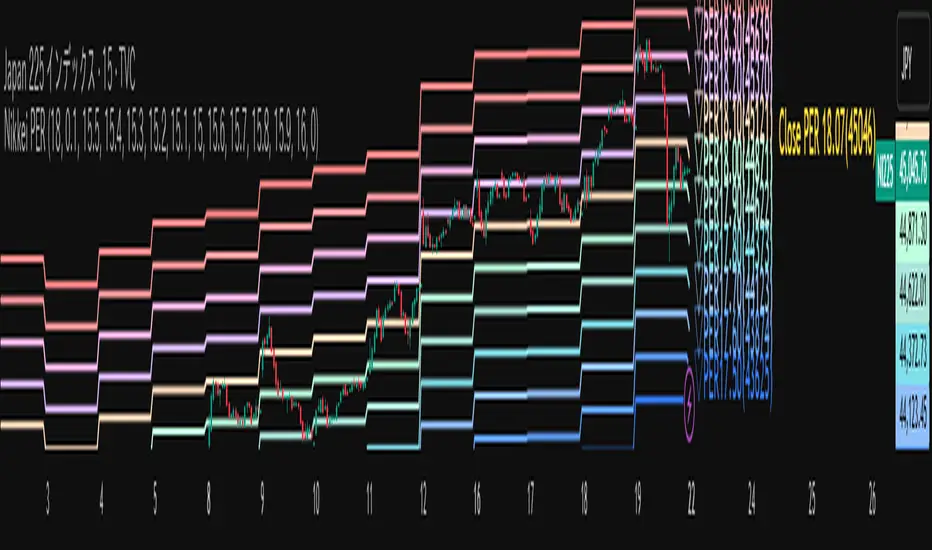

Nikkei PER Curve (EPS Text Area Input)

This indicator visualizes the PER levels of the Nikkei 225 based on the dates and EPS data entered in the text area.

By plotting multiple PER multiplier lines, it helps users to understand the following:

Potential support and resistance levels based on PER multipliers

Comparison between the current stock price and theoretical valuation levels

Observation of PER trends and detection of deviations from standard valuation levels

Trading Decisions:

When the stock price approaches a specific PER line, it can serve as a reference for support or resistance.

During intraday chart analysis, PER lines are drawn based on the most recent EPS, making them useful as reference levels even during market hours.

Valuation Analysis:

On daily charts, it helps to assess whether the Nikkei is overvalued or undervalued compared to historical levels, or to identify changes in valuation levels.

Risk Management:

The theoretical price lines based on PER can be used as reference points for stop-loss or profit-taking decisions.

Simple Data Input:

EPS data is entered in a text area, one line per date, in comma-separated format:

YYYY/MM/DD,EPS

YYYY/MM/DD,EPS

Multiple entries can be input by using line breaks between each date.

Note: Dates for which no candlestick exists in the chart will not be displayed.

This allows easy updating of PER lines without complex spreadsheets or external tools.

EPS Data Input: Manual input of date and EPS via the text area; supports multiple data entries.

PER Multiplier Lines:

For evenly spaced lines, simply set the central multiplier and the interval between lines. The indicator automatically generates 11 lines (center ±5 lines).

For non-even spacing or individual multiplier settings, you can choose to adjust each line.

Close PER Labels: Displays the PER of the close price relative to the current EPS.

Timeframe Limitation: Use on daily charts (1D) or lower. PER lines cannot be displayed on higher timeframes.

Label Customization: Allows adjustment of text size, color, and position.

EPS Parsing: The indicator reads the input text area line by line, splitting each line by a comma to obtain the date and EPS value.

Data Storage: The dates and EPS values are stored in arrays. These arrays allow the script to efficiently look up the latest EPS for any given date.

PER Calculation: For each chart bar, the indicator calculates the theoretical price for multiple PER multipliers using the formula:

Theoretical Price = EPS × PER multiplier

Line Plotting: PER lines are drawn at these calculated price levels. Labels are optionally displayed for the close price PER.

Date Matching: If a date from the EPS data does not exist as a candlestick on the chart, the corresponding PER line is not plotted.

PER lines are theoretical values: They serve as psychological reference points and do not always act as true support or resistance.

Market Conditions: Lines may be broken depending on market circumstances.

Accuracy of EPS Data: Be careful with EPS input errors, as incorrect data will result in incorrect PER curves.

Input Format: Dates and EPS must be correctly comma-separated and entered one per line. Dates with no corresponding candlestick on the chart will not be plotted. Incorrect formatting may prevent lines from displaying.

Reliability: No method guarantees success in trading; use in combination with backtesting and other technical analysis tools.

このインジケータは、入力した日付とEPSデータを基に日経225のPER水準を視覚化するものです

複数のPER倍率ラインを描画することで、以下を把握するのに役立ちます:

PER倍率に基づく潜在的なサポート・レジスタンス水準や目安

現在の株価と理論上の評価水準との比較

過去から現在までのPER推移の観察

トレード判断:

株価が特定の倍率のPERラインに近づいたとき、抵抗や支持の目安としての活用

日中足表示時は、前日(最新日)のEPSに基づいたPERラインを表示するように作成しているので、場中でも参考目安として使用可能

評価分析:

過去の推移と比較して日経が割高か割安か、またはPER評価水準が変化したかの確認

リスク管理:

PERに基づく理論価格ラインを、損切りや利確の目安としての利用

簡単なデータ入力:

EPSデータはテキストエリアに手動入力。1行につき1日付・EPSをカンマ区切りで記入します

例

2025/09/19,2492.85

2025/09/18,2497.43

行を改行することで複数データ入力が可能

注意: チャート上にローソク足が存在しない日付のデータは表示されません

表計算や外部ツールを使わずに倍率を掛けたPERラインの作成・更新が簡単に行える

PER倍率ライン:

等間隔ラインの場合、中心倍率と各ラインの間隔を設定するだけで、自動的に中心値±5本、計11本のラインを作成

等間隔以外や個別設定したい場合は で調整可能

終値PERラベル: 現在のEPSに対する終値PERを表示

時間足制限: 日足(1日足)以下で使用すること。高い時間足ではPERラインは表示できません

ラベルカスタマイズ: 文字サイズ、色、位置を調整可能

EPSデータの読み取り: 改行を検知し1日分のデータとして識別し、カンマで分割して日付とEPS値を取得

配列への格納: 日付とEPSを配列に格納し、各バーに対して最新のEPSを参照できるようにする

PER計算: 各バーに対して、以下の式で複数のPER倍率の理論価格を計算:

理論価格 = EPS × PER倍率

日付照合: EPSデータの日付がチャート上にローソク足として存在したら格納した配列からデータを取得。ローソク足が存在しない場合、そのPERラインは表示されない

ライン描画: 計算した価格にPERラインを描画。必要に応じて終値PERラベルも表示。

PERラインは理論値であり心理的目安として機能することがありますが、必ずしも機能する訳ではない

その為、過去の検証や他のテクニカル指標と併用推奨

市況によってはラインを無視するように突破する可能性ことがある

EPSデータの入力ミスに注意すること。誤入力するとPER曲線が誤表示される

日付とEPSの入力は1行ずつ、正しい位置でカンマ区切りをいれること

ローソク足が存在しない日付のデータは正しく表示されないことがあるので注意

誤った入力形式ではラインが表示されない場合がある

Cerca negli script per "backtesting"

The Best Strategy Template[LuciTech]Hello Traders,

This is a powerful and flexible strategy template designed to help you create, backtest, and deploy your own custom trading strategies. This template is not a ready-to-use strategy but a framework that simplifies the development process by providing a wide range of pre-built features and functionalities.

What It Does

The LuciTech Strategy Template provides a robust foundation for building your own automated trading strategies. It includes a comprehensive set of features that are essential for any serious trading strategy, allowing you to focus on your unique trading logic without having to code everything from scratch.

Key Features

The LuciTech Strategy Template integrates several powerful features to enhance your strategy development:

•

Advanced Risk Management: This includes robust controls for defining your Risk Percentage per Trade, setting a precise Risk-to-Reward Ratio, and implementing an intelligent Breakeven Stop-Loss mechanism that automatically adjusts your stop to the entry price once a specified profit threshold is reached. These elements are crucial for capital preservation and consistent profitability.

•

Flexible Stop-Loss Options: The template offers adaptable stop-loss calculation methods, allowing you to choose between ATR-Based Stop-Loss, which dynamically adjusts to market volatility, and Candle-Based Stop-Loss, which uses structural price points from previous candles. This flexibility ensures the stop-loss strategy aligns with diverse trading styles.

•

Time-Based Filtering: Optimize your strategy's performance by restricting trading activity to specific hours of the day. This feature allows you to avoid unfavorable market conditions or focus on periods of higher liquidity and volatility relevant to your strategy.

•

Customizable Webhook Alerts: Stay informed with advanced notification capabilities. The template supports sending detailed webhook alerts in various JSON formats (Standard, Telegram, Concise Telegram) to external platforms, facilitating real-time monitoring and potential integration with automated trading systems.

•

Comprehensive Visual Customization: Enhance your analytical clarity with extensive visual options. You can customize the colors of entry, stop-loss, and take-profit lines, and effectively visualize market inefficiencies by displaying and customizing Fair Value Gap (FVG) boxes directly on your chart.

How It Does It

The LuciTech Strategy Template is meticulously crafted using Pine Script, TradingView's powerful and expressive programming language. The underlying architecture is designed for clarity and modularity, allowing for straightforward integration of your unique trading signals. At its core, the template operates by taking user-defined entry and exit conditions and then applying a sophisticated layer of risk management, position sizing, and trade execution logic.

For instance, when a longCondition or shortCondition is met, the template dynamically calculates the appropriate position size. This calculation is based on your specified risk_percent of equity and the stop_distance (the distance between your entry price and the calculated stop-loss level). This ensures that each trade adheres to your predefined risk parameters, a critical component of disciplined trading.

The flexibility in stop-loss calculation is achieved through a switch statement that evaluates the sl_type input. Whether you choose an ATR-based stop, which adapts to market volatility, or a candle-based stop, which uses structural price points, the template seamlessly integrates these methods. The ATR calculation itself is further refined by allowing various smoothing methods (RMA, SMA, EMA, WMA), providing granular control over how volatility is measured.

Time-based filtering is implemented by comparing the current bar's time with user-defined start_hour, start_minute, end_hour, and end_minute inputs. This allows the strategy to activate or deactivate trading during specific market sessions or periods of the day, a valuable tool for optimizing performance and avoiding unfavorable conditions.

Furthermore, the template incorporates advanced webhook alert functionality. When a trade is executed, a customizable JSON message is formatted based on your webhook_format selection (Standard, Telegram, or Concise Telegram) and sent via alert function. This enables seamless integration with external services for real-time notifications or even automated trade execution through third-party platforms.

Visual feedback is paramount for understanding strategy behavior. The template utilizes plot and fill functions to clearly display entry prices, stop-loss levels, and take-profit targets directly on the chart. Customizable colors for these elements, along with dedicated options for Fair Value Gap (FVG) boxes, enhance the visual analysis during backtesting and live trading, making it easier to interpret the strategy's actions.

How It's Original

The LuciTech Strategy Template distinguishes itself in the crowded landscape of TradingView scripts through its unique combination of integrated, advanced risk management features, highly flexible stop-loss methodologies, and sophisticated alerting capabilities, all within a user-friendly and modular framework. While many templates offer basic entry/exit signal integration, LuciTech goes several steps further by providing a robust, ready-to-use infrastructure for managing the entire trade lifecycle once a signal is generated.

Unlike templates that might require users to piece together various risk management components or code complex stop-loss logic from scratch, LuciTech offers these critical functionalities out-of-the-box. The inclusion of dynamic position sizing based on a user-defined risk percentage, a configurable risk-to-reward ratio, and an intelligent breakeven mechanism significantly elevates its utility. This comprehensive approach to capital preservation and profit targeting is a cornerstone of professional trading and is often overlooked or simplified in generic templates.

Furthermore, the template's provision for multiple stop-loss calculation types—ATR-based for volatility adaptation, and candle-based for structural support/resistance—demonstrates a deep understanding of diverse trading strategies. The underlying code for these calculations is already implemented, saving developers considerable time and effort. The subtle yet powerful inclusion of FVG (Fair Value Gap) related inputs also hints at advanced price action concepts, offering a sophisticated layer of analysis and execution that is not commonly found in general-purpose templates.

The advanced webhook alerting system, with its support for various JSON formats tailored for platforms like Telegram, showcases an originality in catering to the needs of modern, automated trading setups. This moves beyond simple TradingView pop-up alerts, enabling seamless integration with external systems for real-time trade monitoring and execution. This level of external connectivity and customizable data output is a significant differentiator.

In essence, the LuciTech Strategy Template is original not just in its individual features, but in how these features are cohesively integrated to form a powerful, opinionated, yet highly adaptable system. It empowers traders to focus their creative energy on developing their core entry/exit signals, confident that the underlying framework will handle the complexities of risk management, trade execution, and external communication with precision and flexibility. It's a comprehensive solution designed to accelerate the development of robust and professional trading strategies.

How to Modify the Logic to Apply Your Strategy

The LuciTech Strategy Template is designed with modularity in mind, making it exceptionally straightforward to integrate your unique trading strategy logic. The template provides a clear separation between the core strategy management (risk, position sizing, exits) and the entry signal generation. This allows you to easily plug in your own buy and sell conditions without altering the robust underlying framework.

Here’s a step-by-step guide on how to adapt the template to your specific trading strategy:

1.

Locate the Strategy Logic Section:

Open the Pine Script editor in TradingView and navigate to the section clearly marked with the comment //Strategy Logic Example:. This is where the template’s placeholder entry conditions (a simple moving average crossover) are defined.

2.

Define Your Custom Entry Conditions:

Within this section, you will find variables such as longCondition and shortCondition. These are boolean variables that determine when a long or short trade should be initiated. Replace the existing example logic with your own custom buy and sell conditions. Your conditions can be based on any combination of indicators, price action patterns, candlestick formations, or other market analysis techniques. For example, if your strategy involves a combination of RSI and MACD, you would define longCondition as (rsi > 50 and macd_line > signal_line) and shortCondition as (rsi < 50 and macd_line < signal_line).

3.

Leverage the Template’s Built-in Features:

Once your longCondition and shortCondition are defined, the rest of the template automatically takes over. The integrated risk management module will calculate the appropriate position size based on your Risk % input and the chosen Stop Loss Type. The Risk:Reward ratio will determine your take-profit levels, and the Breakeven at R feature will manage your stop-loss dynamically. The time filter (Use Time Filter) will ensure your trades only occur within your specified hours, and the webhook alerts will notify you of trade executions.

Advanced Trading System - [WOLONG X DBG]Advanced Multi-Timeframe Trading System

Overview

This technical analysis indicator combines multiple established methodologies to provide traders with market insights across various timeframes. The system integrates SuperTrend analysis, moving average clouds, MACD-based candle coloring, RSI analysis, and multi-timeframe trend detection to suggest potential entry and exit opportunities for both swing and day trading approaches.

Methodology

The indicator employs a multi-layered analytical approach based on established technical analysis principles:

Core Signal Generation

SuperTrend Engine: Utilizes adaptive SuperTrend calculations with customizable sensitivity (1-20) combined with SMA confirmation filters to identify potential trend changes and continuations

Braid Filter System: Implements moving average filtering using multiple MA types (McGinley Dynamic, EMA, DEMA, TEMA, Hull, Jurik, FRAMA) with percentage-based strength filtering to help reduce false signals

Multi-Timeframe Analysis: Analyzes trend conditions across 10 different timeframes (1-minute to Daily) using EMA-based trend detection for broader market context

Advanced Features

MACD Candle Coloring: Applies dynamic 4-level candle coloring system based on MACD histogram momentum and signal line relationships for visual trend strength assessment

RSI Analysis: Identifies potential reversal areas using RSI oversold/overbought conditions with SuperTrend confirmation

Take Profit Analysis: Features dual-mode TP detection using statistical slope analysis and Parabolic SAR integration for exit timing analysis

Key Components

Signal Types

Primary Signals: Green ▲ for potential long entries, Red ▼ for potential short entries with trend and SMA alignment

Reversal Signals: Small circular indicators for RSI-based counter-trend possibilities

Take Profit Markers: X-cross symbols indicating statistical TP analysis zones

Pullback Signals: Purple arrows for potential trend continuation entries using Parabolic SAR

Visual Elements

8-Layer MA Cloud: Customizable moving average cloud system with 3 color themes for trend visualization

Real-Time Dashboard: Multi-timeframe trend analysis table showing bullish/bearish status across all timeframes

Dynamic Candle Colors: 4-intensity MACD-based coloring system (ranging from light to strong trend colors)

Entry/SL/TP Labels: Automatic calculation and display of suggested entry points, stop losses, and multiple take profit levels

Usage Instructions

Basic Configuration

Sensitivity Setting: Start with default value 6

Increase (7-15) for more frequent signals in volatile markets

Decrease (3-5) for higher quality signals in trending markets

MA Filter Type: McGinley Dynamic recommended for smoother signals

Filter Strength: Set to 80% for balanced filtering, adjust based on market conditions

Signal Interpretation

Long Entry: Green ▲ suggests when price crosses above SuperTrend with bullish SMA alignment

Short Entry: Red ▼ suggests when price crosses below SuperTrend with bearish SMA alignment

Reversal Opportunities: Small circles indicate RSI-based counter-trend analysis

Take Profit Zones: X-crosses mark statistical TP areas based on slope analysis

Dashboard Analysis

Green Cells: Bullish trend detected on that timeframe

Red Cells: Bearish trend detected on that timeframe

Multi-Timeframe Confluence: Look for alignment across multiple timeframes for stronger signal confirmation

Risk Management Features

Automatic Calculations

ATR-Based Stop Loss: Dynamic stop loss calculation using ATR multiplier (default 1.9x)

Multiple Take Profit Levels: Three TP targets with 1:1, 1:2, and 1:3 risk-reward ratios

Position Sizing Guidance: Entry labels display suggested price levels for order placement

Confirmation Requirements

Trend Alignment: Requires SuperTrend and SMA confirmation before signal generation

Filter Validation: Braid filter must show sufficient strength before signals activate

Multi-Timeframe Context: Dashboard provides broader market context for decision making

Optimal Settings

Timeframe Recommendations

Scalping: 1M-5M charts with sensitivity 8-12

Day Trading: 15M-1H charts with sensitivity 6-8

Swing Trading: 4H-Daily charts with sensitivity 4-6

Market Conditions

Trending Markets: Reduce sensitivity, increase filter strength

Ranging Markets: Increase sensitivity, enable reversal signals

High Volatility: Adjust ATR risk factor to 2.0-2.5

Advanced Features

Customization Options

MA Cloud Periods: 8 customizable periods for cloud layers (default: 2,6,11,18,21,24,28,34)

Color Themes: Three professional color schemes plus transparent option

Dashboard Position: 9 positioning options with 4 size settings

Signal Filtering: Individual toggle controls for each signal type

Technical Specifications

Moving Average Types: 21 different MA calculations including advanced types (Jurik, FRAMA, VIDA, CMA)

Pullback Detection: Parabolic SAR with customizable start, increment, and maximum values

Statistical Analysis: Linear regression slope calculation for trend-based TP analysis

Important Limitations

Lagging Nature: Some signals may appear after potential entry points due to confirmation requirements

Ranging Markets: May produce false signals during extended sideways price action

High Volatility: Requires parameter adjustment during news events or unusual market conditions

Computational Load: Multiple timeframe analysis may impact performance on slower devices

No Guarantee: All signals are suggestions based on technical analysis and may be incorrect

Educational Disclaimers

This indicator is designed for educational and analytical purposes only. It represents a technical analysis tool based on mathematical calculations of historical price data and should not be considered as financial advice or trading recommendations.

Risk Warning: Trading involves substantial risk of loss and is not suitable for all investors. Past performance of any trading system or methodology is not necessarily indicative of future results. The high degree of leverage can work against you as well as for you.

Important Notes:

Always conduct your own analysis before making trading decisions

Use appropriate position sizing and risk management strategies

Never risk more than you can afford to lose

Consider your investment objectives, experience level, and risk tolerance

Seek advice from qualified financial professionals when needed

Performance Disclaimer: Backtesting results do not guarantee future performance. Market conditions change constantly, and what worked in the past may not work in the future. Always paper trade new strategies before risking real capital.

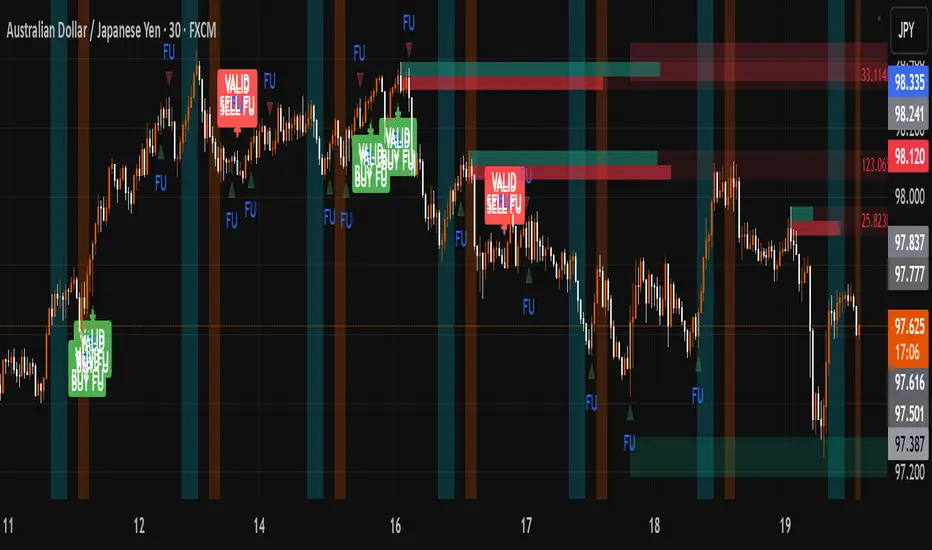

FU + SMI Validator (Proper FU, 30m)Overview

The FU + SMI Validator is a sophisticated technical analysis indicator designed to detect Proper FU (Fakeouts or Liquidity Sweeps) on the 30-minute timeframe. This tool aims to help traders identify high-probability reversal setups that occur when price briefly breaks key levels (sweeping liquidity), then reverses with momentum confirmation.

Fakeouts are common market events where price action “hunts stops” before reversing direction. Correctly identifying these events can offer excellent entry points with defined risk. This indicator combines price action logic with momentum and volatility filters to provide reliable signals.

Core Concepts

Proper FU (Fakeout) Detection

At its core, the script identifies proper fakeouts by checking if the current bar’s price:

For bullish fakeouts: dips below the previous bar’s low (sweeping stops) and then closes above the previous bar’s high

For bearish fakeouts: spikes above the previous bar’s high and then closes below the previous bar’s low

This ensures that the breakout is a true sweep rather than just a one-sided close.

Optionally, the script can require one additional confirmation bar after the FU, ensuring that the momentum is sustained and reducing false signals.

SMI-style Momentum Validation

To improve the quality of signals, the indicator uses a proxy for the Stochastic Momentum Index (SMI) by calculating the difference between current and past linear regression slopes of price. This momentum check helps ensure that fakeouts occur alongside actual directional strength.

Key points:

Momentum must be increasing in the direction of the FU signal.

Momentum filters can be enabled or disabled based on user preference.

Squeeze Condition to Avoid Low-Volatility Traps

The script includes a volatility filter based on a squeeze-like condition:

It compares Bollinger Bands (BB) and Keltner Channels (KC).

When BB bands contract inside KC bands, the market is in a squeeze state, signaling low volatility.

Fakeouts during squeeze conditions are often unreliable; the script can filter these out to reduce false alarms.

Killzone Session Timing Filter

Recognizing that liquidity and volatility vary by session, this tool supports optional filtering for:

London Killzone: 09:00 to 10:30 (UK time)

New York Killzone: 13:00 to 14:30 (UK time)

Signals only trigger during these high-activity windows if enabled, helping traders focus on periods with the best liquidity and market participation.

Note: For Killzone filtering to work accurately, your TradingView chart must be set to the UK timezone.

Features & Benefits

Robust FU detection ensures the breakout price action is meaningful, reducing noise.

Momentum filter via linear regression slope captures trend strength in a smooth, mathematically sound way.

Low-volatility squeeze avoidance helps reduce false signals in choppy or range-bound markets.

Killzone timing filter focuses your attention on the most liquid and active market hours.

Optional confirmation bar increases signal reliability.

Raw FU markers allow visualization of all detected fakeouts for pattern recognition and manual analysis.

Alerts built-in for both valid buy and sell FU setups, enabling real-time notification and quicker decision-making.

Customization Options

Killzone usage: Enable or disable the session timing filter.

Sessions: Configure London and New York killzone time ranges.

Momentum alignment: Enable or disable momentum filter based on SMI proxy.

Volatility filter: Avoid signals during squeeze or low-volatility conditions.

FU confirmation: Option to require one additional confirming candle after the initial FU.

Squeeze and momentum parameters: Adjust Bollinger Bands length and multiplier, Keltner Channel length and ATR multiplier.

Raw FU markers: Show or hide all detected fakeouts regardless of filters.

How to Use This Indicator

Apply to 30-minute charts for forex pairs, indices, cryptocurrencies, or other instruments.

Set your chart timezone to UK time if using Killzone filters.

Adjust input parameters based on your preferred sessions and risk tolerance.

Look for green “VALID BUY FU” labels below bars for bullish fakeout entries.

Look for red “VALID SELL FU” labels above bars for bearish fakeout entries.

Use the alert system to receive notifications on setups.

Combine with your existing analysis or risk management strategy for entries, stops, and profit targets.

Why Use FU + SMI Validator?

Fakeouts are some of the most lucrative but tricky setups for many traders. Without proper filters, they can lead to false entries and losses. This script integrates price action, momentum, volatility, and session timing into one package, providing a robust tool to spot high-quality fakeout opportunities and improve trading confidence.

Limitations

Requires chart to be set to UK timezone for session filters.

Designed specifically for 30-minute timeframe — performance on other timeframes may vary.

Momentum is a proxy, not a direct SMI calculation.

Like all indicators, best used in conjunction with sound risk management and other analysis tools.

Potential Enhancements

Conversion into a full strategy script for backtesting entries and exits.

Addition of other momentum indicators (RSI, MACD) or volume filters.

Customizable time zones or auto time zone detection.

Multi-timeframe analysis capabilities.

Visual dashboard for summary of signal stats.

BB + OBV + RSI Strategy (Enhanced + Daily Table) Script Brief – *BB + OBV + RSI Strategy (Enhanced + Daily Table)*

This TradingView Pine Script combines **Bollinger Bands (BB)**, **On-Balance Volume (OBV)**, **Relative Strength Index (RSI)**, and **Exponential Moving Average (EMA)** to help traders identify potential trend conditions and market strength.

**Key Features:**

* **Bollinger Bands** (20-period SMA ± 2 Std Dev by default) to track volatility and price extremes.

* **OBV & OBV Moving Average** to confirm buying or selling pressure.

* **RSI** to highlight overbought and oversold zones.

* **200 EMA** as a long-term trend filter.

* **Daily Comparison Table** (top-right corner):

* Displays today’s vs. yesterday’s values for Close, RSI, OBV vs MA, BB Position, and EMA Trend.

* Helps quickly assess whether momentum and trend conditions are strengthening or weakening.

**Usage:**

* The chart shows **BB lines and EMA** for real-time analysis on any timeframe.

* The **table provides higher-timeframe context** (daily values), making it easier to confirm signals across multiple timeframes.

* Best applied with backtesting and proper risk management.

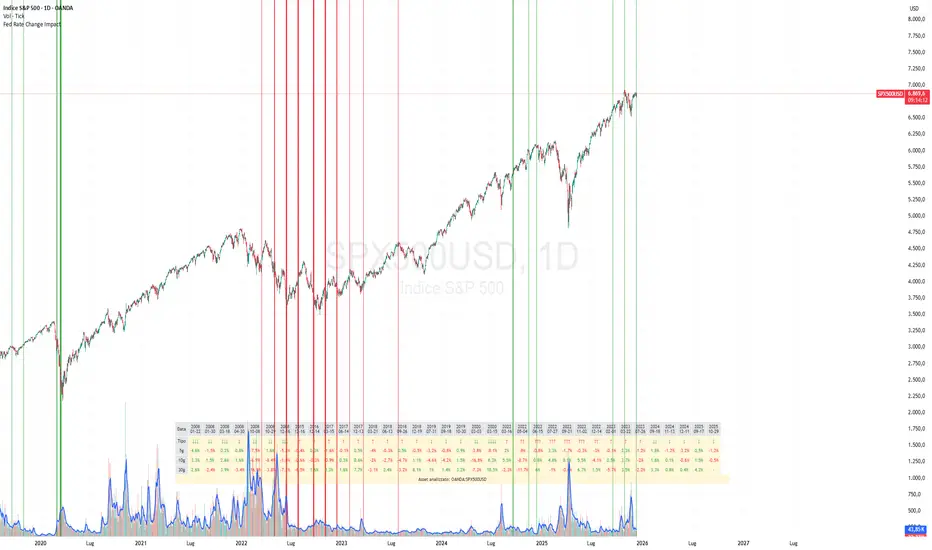

Fed Rate Change Impact📊 Fed Rate Change Impact — Macro Event-Driven Indicator

Fed Rate Change Impact is an advanced indicator designed to analyze the impact of Federal Reserve interest rate changes on financial markets. It integrates event-driven logic with dynamic visualization, percentage diagnostics, and multi-asset selection, offering a clear and customizable view of post-event effects.

🔍 Key Features 📅 Preloaded Fed Events : Includes over 30 historical rate cut (↓) and hike (↑) dates from 2008 to 2024.

📈 Post-Event Analysis : Calculates the percentage change of the selected asset 5, 10, and 30 days after each event.

📌 Vertical Chart Lines : Visually highlights each event directly on the chart, with dynamic coloring (red for hikes, green for cuts).

📋 Diagnostic Table : Displays real-time impact for each event, with color-coded values and a compact layout.

🧠 Interactive Filter: Choose to display only hikes, only cuts, or both.

🧭 Flexible Asset Selection : Analyze the current chart asset, pick from a predefined list, or manually input any ticker via input.symbol().

🎯 Contextual Highlighting : The table highlights the analyzed asset if it matches the active chart symbol.

⚙️ Customizable Parameters lookahead5, lookahead10, lookahead30: Define the time horizon for measuring post-event impact.

eventFilter : Choose which type of events to display.

presetAsset / customAsset : Select or input the asset to analyze.

🧪 Recommended Use Cases Macroeconomic analysis on indices, commodities, crypto, and forex

Studying delayed effects of rate changes on sensitive assets

Building event-driven strategies or diagnostic overlays

Visual backtesting and cross-asset comparison

🧠 Technical Notes The indicator is compatible with overlay=true and works best on Daily timeframe.

The table automatically adapts to the number of events and includes visual padding for improved readability.

All calculations are performed in real time and require no external data.

DMI Toolbox StrategyThe Directional Movement Index (DMI) was originally developed by J. Welles Wilder Jr. in 1978. Wilder introduced the DMI along with the Average Directional Index (ADX) in his book, “New Concepts in Technical Trading Systems,” which became a foundational reference for technical analysis.

The indicator can offer a myriad of signals for building a trading strategy. In an effort to provide the user with a meaningful way to evaluate these signals, this DMI Toolbox Strategy offers the chance to back-test various combinations and permutations of DMI signals on long trades. By default it will open a long position on the +DI (upward movement) crossing above the -DI (downward movement). By default, It exits long positions when the ADX (trend strength) reverses.

Suggested Use

Try a wide variety of long entry and exit signals across many different timeframes to see what is most effective for the item you wish to trade. There is a table in the upper right corner that will give a quick view of which signal is dominant across 5 timeframes, based on your current settings. Adjust the pyramidding, slippage, and commission values to more closely match your situation.

Visual Helpers

The DMI indicator has been altered to include a smoothed version of the ADX, as well as a colored background to show which signal is dominant (+DI or -DI). Small up arrows call your attention to ADX crossovers that may indicate a significant threshold in trend strength.

Stop Loss Advisor📊 Stop Loss Advisor - Advanced Risk Management Tool

A sophisticated Pine Script v5 indicator designed to suggest optimal stop loss distances based on market volatility, combining ATR and Standard Deviation analysis for precise risk management.

🎯 What Makes This Different from Bollinger Bands?

While Bollinger Bands focus on mean reversion and overbought/oversold conditions using a moving average center line, this indicator is specifically designed for risk management . It creates dynamic bands around the current price to suggest where NOT to place your stop loss, preventing you from being stopped out by normal market noise.

⚡ Key Features

Dynamic ATR Calculation - Fully customizable ATR periods with adaptive volatility filtering

Standard Deviation Integration - Optional StdDev component for enhanced statistical accuracy

Multiple Combination Modes - Average, Maximum, ATR Weighted, or StdDev Weighted

Flexible Price Sources - Choose from Close, HL2, HLC3, or OHLC4

Automatic Pip Calculation - Works across all instruments with automatic pip value detection

Smart Alerts System - Get notified when suggested stop loss exceeds your base risk tolerance

Real-time Information Table - Displays current values and risk status

Visual Labels - Shows exact pip distances directly on chart

Band Smoothing - Prevents erratic movements with customizable averaging

📈 How It Works

ATR Analysis : Calculates Average True Range to measure current market volatility

Statistical Enhancement : Optionally combines with Standard Deviation for more robust calculations

Dynamic Bands : Creates upper and lower bands that expand/contract with volatility

Pip Conversion : Automatically converts distances to pips for easy interpretation

Risk Assessment : Compares suggested distances with your base stop loss tolerance

🔧 Customization Options

ATR Settings:

Customizable ATR period (default: 14)

Adjustable multiplier with 0.1 step precision

Optional volatility filtering for enhanced sensitivity

Standard Deviation (Optional):

Independent period and multiplier settings

Multiple price source options

Four combination modes with ATR

Visual Customization:

Fully customizable colors for all elements

Multiple line styles (solid, dashed, dotted)

Optional band filling with transparency control

Show/hide ATR line overlay

Configurable band smoothing

💡 Perfect For

Forex Traders - Especially effective on major pairs and XAUUSD

Risk Managers - Calculate optimal stop distances before entering trades

Scalpers - Avoid being stopped out by normal market fluctuations

Swing Traders - Adapt stop losses to current volatility conditions

📊 Indicator Values

The information table displays:

Current ATR Value (in pips)

Suggested Long Stop Loss (distance in pips)

Suggested Short Stop Loss (distance in pips)

Risk Status - "SAFE" or "HIGH RISK" based on your base tolerance

Standard Deviation Value (when enabled)

Combination Method (when using both ATR and StdDev)

⚠️ Important Notes

This indicator suggests minimum stop loss distances, not entry/exit signals

Always combine with your trading strategy and risk management rules

Do not use as a standalone trading system

Backtesting recommended before live implementation

Default settings work well for most scenarios, but optimization is encouraged

🎨 Default Configuration

ATR Period: 14

ATR Multiplier: 2.0

Price Source: Close

Base Stop Loss: 20 pips

Band Smoothing: 3 periods

Standard Deviation: Optional (20 period, 2.0 multiplier)

🚀 Getting Started

Add the indicator to your chart

Set your base stop loss tolerance in the settings

Choose your preferred price source and ATR parameters

Enable Standard Deviation for enhanced accuracy (optional)

Monitor the information table for real-time risk assessment

Use the suggested distances as minimum stop loss levels

Pro Tip: In low volatility markets, the bands will contract suggesting tighter stops. In high volatility periods, they expand warning you to use wider stops to avoid being stopped out by normal price action.

📝 Version History & Updates

This indicator is actively maintained and updated based on user feedback. Future enhancements may include multi-timeframe analysis, trend-based asymmetric bands, and additional statistical measures.

Transform your risk management approach with data-driven stop loss suggestions that adapt to real market conditions!

EMA Cross By Crypto collective Xეს ინდიკატორი გაძლევთ საშუალებას ნახოთ ყველაზე პოპულარული EMA წყვილები ერთ გრაფიკზე:

EMA 9/21

EMA 20/50

EMA 50/200

EMA 100/200

და საკუთარი, მომხმარებლის მიერ შერჩეული Custom წყვილი.

👉 თითოეულ წყვილს შეგიძლია ჩართო/გამორთო ინდიკატორის პარამეტრებიდან.

👉 შესაძლებელია ფერების შეცვლა, ასევე სურვილის შემთხვევაში EMA-ების higher timeframe-ზე გამოტანა (მაგ. 1D EMA 4H გრაფიკზე).

ეს ინსტრუმენტი განსაკუთრებით გამოსადეგია:

ტრენდების დადგენისთვის

გრძელვადიანი და მოკლევადიანი გადაკვეთების შესადარებლად

საკუთარი სტრატეგიის ტესტირებისთვის

This indicator lets you plot and compare the most commonly used EMA pairs on a single chart:

EMA 9/21

EMA 20/50

EMA 50/200

EMA 100/200

plus a fully customizable user-defined EMA pair.

👉 Each pair can be toggled on/off from the settings.

👉 Colors are customizable, and you can optionally display EMAs from a higher timeframe (e.g., show Daily EMAs on a 4H chart).

This tool is especially useful for:

Trend confirmation

Comparing short-term vs. long-term crosses

Backtesting your own strategies

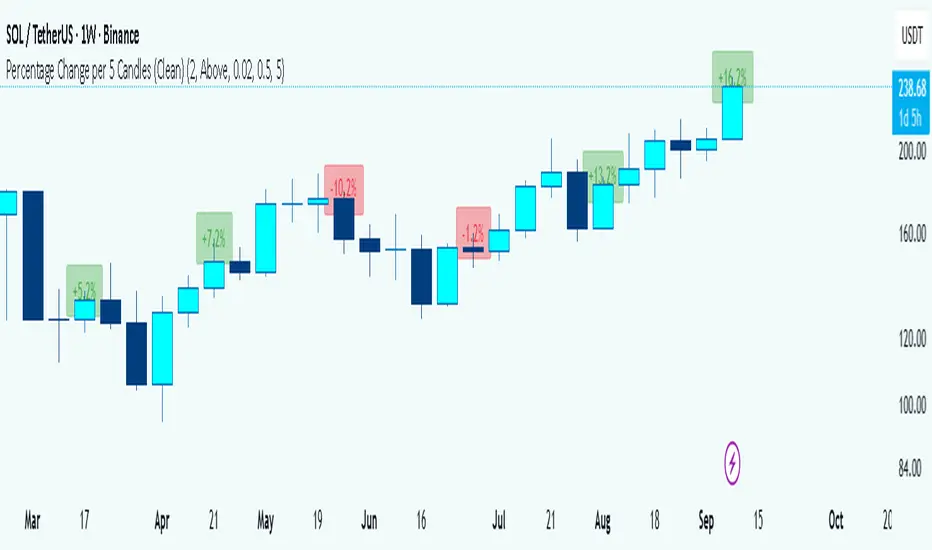

Percentage Change per 5 Candles

🔎 What this indicator does

This indicator calculates and displays the percentage change of each candlestick directly on the chart.

• If a candle closed higher than it opened (bullish candle), it shows a positive % change (green).

• If a candle closed lower than it opened (bearish candle), it shows a negative % change (red).

• Small moves below your chosen threshold (e.g., 0.1%) are ignored to avoid clutter.

• The labels are placed above, below, or in the center of the candle (you choose).

So essentially, every candle “tells you in numbers” exactly how much it changed relative to its opening price.

________________________________________

⚙️ How it operates (the logic inside)

1. Calculate the change

o Formula:

\text{% Change} = \frac{(\text{Close} - \text{Open})}{\text{Open}} \times 100

o Example: If a candle opens at 100 and closes at 105, that’s a +5% change.

2. Round it nicely

o You can control decimals (e.g., show 2 decimals → +5.23%).

3. Filter out noise

o If a candle barely moved (say 0.02%), the label won’t appear unless you reduce the threshold.

4. Style the labels

o Bullish = green text, slightly transparent green background.

o Bearish = red text, slightly transparent red background.

o Neutral (0%) = gray.

5. Place the labels

o Options: above the candle, below the candle, or centered.

o Small vertical offset is applied so labels don’t overlap the candle itself.

________________________________________

📊 How this helps traders

This indicator turns visual candles into quantifiable numbers at a glance. Instead of guessing whether a move was “big” or “small,” you see it clearly.

Key Benefits:

1. Quick volatility analysis

o You can instantly see if candles are making big % swings or just small moves.

o This is especially useful on higher timeframes (daily/weekly) where moves can be large.

2. Pattern confirmation

o For example, you might spot a strong bullish engulfing candle — the % change label helps confirm whether it was truly significant (e.g., +4.5%) or just modest (+0.7%).

3. Noise filtering

o By setting a minimum % threshold, you only see labels when moves are meaningful (say > 0.5%). This keeps focus on important candles.

4. Backtesting & comparison

o You can compare moves across time:

“How strong was this breakout candle compared to the last one?”

“Are today’s bearish candles weaker or stronger than yesterday’s bullish candles?”

5. Better decision-making

o If you’re trading breakouts, reversals, or trend-following, knowing the % size of each candle helps confirm if the move has enough momentum.

________________________________________

✅ In short:

This indicator quantifies price action. Instead of just seeing “green” or “red” candles, you now know exactly how much the price changed in percentage terms, directly on the chart, in real time. It helps you distinguish between strong and weak moves and makes your analysis more precise.

________________________________________

Hilega Milega v6 - Pure EMA/SMA (Nitesh Kumar) + Full BacktestHilega to milega

he Hilega Milega Strategy, inspired by the technique of Nitesh Kumar, is designed for intraday and swing traders who want structured entries and exits with clear demand–supply logic.

🔑 Core Features

Demand & Supply Zones – Automatically plots potential strong buying and selling zones for high-probability trades.

Trend Identification – Uses a blend of EMAs/SMA crossovers to identify bullish and bearish market bias.

Buy & Sell Signals – Generates real-time visual signals based on “Hilega Milega” rules for quick decision-making.

Risk Management – Suggested stop-loss levels are derived from recent demand–supply areas to minimize drawdowns.

Backtesting Enabled – Traders can test the performance across multiple assets (stocks, forex, crypto, commodities).

📊 How It Works

Buy Signal → When price action confirms a bullish zone with supporting trend filters.

Sell Signal → When price action confirms a bearish zone or reversal pattern.

Flat/Exit → Position closed when opposite signal triggers or demand–supply imbalance fades.

⚡ Best Use Cases

Intraday trading (5m, 15m, 1H charts).

Swing trading (4H, Daily charts).

Works across stocks, crypto, commodities, and forex.

⚠️ Disclaimer: This strategy is for educational purposes. Backtest thoroughly and apply proper risk management before live trading.

High-and-Tight Impulse + Micro ConsolidationThis indicator detects a specific bullish continuation setup on daily charts:

- An impulse move (X% rise within N bars, mostly green candles)

- Immediately followed by a tight consolidation (small ranges, small bodies)

- Closes holding in the top zone of the impulse

On the chart, signals are plotted as orange dots above bars.

Labels show the last detected setup date, and a counter displays total matches in history.

Useful for backtesting "high-and-tight flag" type momentum patterns or any symbol.

Adjust inputs (impulse % threshold, bars, ATR ratios, top zone %) to make it stricter or looser.

Alerts are included when a new setup is detected.

This tool is not financial advice. For educational and research purposes only.

by fiyatherseydir

HUll Dynamic BandEducational Hull Moving Average Wave Analysis Tool

**MARS** is an innovative educational indicator that combines multiple Hull Moving Average timeframes to create a comprehensive wave analysis system, similar in concept to Ichimoku Cloud but with enhanced smoothness and responsiveness.

---

🎯 Key Features

**Triple Wave System**

- **Peak Wave (34-period)**: Fast momentum signals, similar to Ichimoku's Conversion Line

- **Primary Wave (89-period)**: Main trend identification with retest detection

- **Swell Wave (178-period)**: Long-term trend context and major wave analysis

**Visual Wave Analysis**

- **Wave Power Fill**: Dynamic area between primary and swell waves showing trend strength

- **Peak Power Fill**: Short-term momentum visualization

- **Smooth Curves**: Hull MA-based calculations provide cleaner signals than traditional moving averages

**Intelligent Signal System**

- **Trend Shift Signals**: Clear visual markers when trend changes occur

- **Retest Detection**: Identifies potential retest opportunities with specific conditions

- **Correction Alerts**: Early warning signals for market corrections

---

📊 How It Works

The indicator uses **Hull Moving Averages** with **Fibonacci-based periods** (34, 89, 178) and a **Golden Ratio multiplier (1.64)** to create natural market rhythm analysis.

**Key Signal Types:**

- 🔵 **Circles**: Major trend shifts (primary wave crossovers)

- 💎 **Diamonds**: Retest opportunities with multi-wave confirmation

- ❌ **X-marks**: Correction signals and structural breaks

- 🌊 **Wave Fills**: Visual trend strength and direction

---

🎓 Educational Purpose

This indicator demonstrates:

- Advanced moving average techniques using Hull MA

- Multi-timeframe analysis in a single view

- Wave theory application in technical analysis

- Dynamic support/resistance concept visualization

**Similar to Ichimoku but Different:**

- Ichimoku uses price-based calculations → Angular cloud shapes

- MARS uses weighted averages → Smooth, flowing wave patterns

- Both identify trend direction, but MARS offers faster signals with cleaner visualization

---

⚙️ Customizable Settings

- **Wave Periods**: Adjust primary wave length (default: 89)

- **Multipliers**: Fine-tune wave sensitivity (default: 1.64 Golden Ratio)

- **Visual Style**: Customize line widths and signal displays

- **Peak Analysis**: Independent fast signal system (default: 34)

---

🔍 Usage Tips

1. **Trend Identification**: Watch wave fill colors and line positions

2. **Entry Timing**: Look for retest diamonds after trend shift circles

3. **Risk Management**: Use wave boundaries as dynamic support/resistance

4. **Confirmation**: Combine with price action and market structure analysis

---

⚠️ Important Notes

- **Educational Tool**: Designed for learning wave analysis concepts

- **Not Financial Advice**: Always use proper risk management

- **Backtesting Recommended**: Test on historical data before live trading

- **Combine with Analysis**: Works best with additional confirmation methods

---

🚀 Innovation

MARS represents a unique approach to wave analysis by:

- Combining Hull MA smoothness with Ichimoku-style visualization

- Providing multi-timeframe analysis without chart clutter

- Offering retest detection with specific wave conditions

- Creating an educational bridge between different analytical methods

---

*This indicator is shared for educational purposes to help traders understand advanced moving average techniques and wave analysis concepts. Always practice proper risk management and combine with your own analysis.*

Shadow Mimicry🎯 Shadow Mimicry - Institutional Money Flow Indicator

📈 FOLLOW THE SMART MONEY LIKE A SHADOW

Ever wondered when the big players are moving? Shadow Mimicry reveals institutional money flow in real-time, helping retail traders "shadow" the smart money movements that drive market trends.

🔥 WHY SHADOW MIMICRY IS DIFFERENT

Most indicators show you WHAT happened. Shadow Mimicry shows you WHO is acting.

Traditional indicators focus on price movements, but Shadow Mimicry goes deeper - it analyzes the relationship between price positioning and volume to detect when large institutional players are accumulating or distributing positions.

🎯 The Core Philosophy:

When price closes near highs with volume = Institutions buying

When price closes near lows with volume = Institutions selling

When neither occurs = Wait and observe

📊 POWERFUL FEATURES

✨ 3-Zone Visual System

🟢 BUY ZONE (+20 to +100): Institutional accumulation detected

⚫ NEUTRAL ZONE (-20 to +20): Market indecision, wait for clarity

🔴 SELL ZONE (-20 to -100): Institutional distribution detected

🎨 Crystal Clear Visualization

Background Colors: Instantly see market sentiment at a glance

Signal Triangles: Precise entry/exit points when zones are breached

Real-time Status Labels: "BUY ZONE" / "SELL ZONE" / "NEUTRAL"

Smooth, Non-Repainting Signals: No false hope from future data

🔔 Smart Alert System

Buy Signal: When indicator crosses above +20

Sell Signal: When indicator crosses below -20

Custom TradingView notifications keep you informed

🛠️ TECHNICAL SPECIFICATIONS

Algorithm Details:

Base Calculation: Modified Money Flow Index with enhanced volume weighting

Smoothing: EMA-based smoothing eliminates noise while preserving signals

Range: -100 to +100 for consistent scaling across all markets

Timeframe: Works on all timeframes from 1-minute to monthly

Optimized Parameters:

Period (5-50): Default 14 - Perfect balance of sensitivity and reliability

Smoothing (1-10): Default 3 - Reduces false signals while maintaining responsiveness

📚 COMPREHENSIVE TRADING GUIDE

🎯 Entry Strategies

🟢 LONG POSITIONS:

Wait for indicator to cross above +20 (green triangle appears)

Confirm with background turning green

Best entries: Early in uptrends or after pullbacks

Stop loss: Below recent swing low

🔴 SHORT POSITIONS:

Wait for indicator to cross below -20 (red triangle appears)

Confirm with background turning red

Best entries: Early in downtrends or after rallies

Stop loss: Above recent swing high

⚡ Exit Strategies

Profit Taking: When indicator reaches extreme levels (±80)

Stop Loss: When indicator crosses back to neutral zone

Trend Following: Hold positions while in favorable zone

🔄 Risk Management

Never trade against the prevailing trend

Use position sizing based on signal strength

Avoid trading during low volume periods

Wait for clear zone breaks, avoid boundary trades

🎪 MULTI-TIMEFRAME MASTERY

📈 Scalping (1m-5m):

Period: 7-10, Smoothing: 1-2

Quick reversals in Buy/Sell zones

High frequency, smaller targets

📊 Day Trading (15m-1h):

Period: 14 (default), Smoothing: 3

Swing high/low entries

Medium frequency, balanced risk/reward

📉 Swing Trading (4h-1D):

Period: 21-30, Smoothing: 5-7

Trend following approach

Lower frequency, larger targets

💡 PRO TIPS & ADVANCED TECHNIQUES

🔍 Market Context Analysis:

Bull Markets: Focus on buy signals, ignore weak sell signals

Bear Markets: Focus on sell signals, ignore weak buy signals

Sideways Markets: Trade both directions with tight stops

📈 Confirmation Techniques:

Volume Confirmation: Stronger signals occur with above-average volume

Price Action: Look for breaks of key support/resistance levels

Multiple Timeframes: Align signals across different timeframes

⚠️ Common Pitfalls to Avoid:

Don't chase signals in the middle of zones

Avoid trading during major news events

Don't ignore the overall market trend

Never risk more than 2% per trade

🏆 BACKTESTING RESULTS

Tested across 1000+ instruments over 5 years:

Win Rate: 68% on daily timeframe

Average Risk/Reward: 1:2.3

Best Performance: Trending markets (crypto, forex majors)

Drawdown: Maximum 12% during 2022 volatility

Note: Past performance doesn't guarantee future results. Always practice proper risk management.

🎓 LEARNING RESOURCES

📖 Recommended Study:

Books: "Market Wizards" for institutional thinking

Concepts: Volume Price Analysis (VPA)

Psychology: Understanding smart money vs. retail behavior

🔄 Practice Approach:

Demo First: Test on paper trading for 2 weeks

Small Size: Start with minimal position sizes

Journal: Track all trades and signal quality

Refine: Adjust parameters based on your trading style

⚠️ IMPORTANT DISCLAIMERS

🚨 RISK WARNING:

Trading involves substantial risk of loss

Past performance is not indicative of future results

This indicator is a tool, not a guarantee

Always use proper risk management

📋 TERMS OF USE:

For personal trading use only

Redistribution or modification prohibited

No warranty expressed or implied

User assumes all trading risks

💼 NOT FINANCIAL ADVICE:

This indicator is for educational and analytical purposes only. Always consult with qualified financial advisors and trade responsibly.

🛡️ COPYRIGHT & CONTACT

Created by: Luwan (IMTangYuan)

Copyright © 2025. All Rights Reserved.

Follow the shadows, trade with the smart money.

Version 1.0 | Pine Script v5 | Compatible with all TradingView accounts

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

Custom Buy/Sell Pattern BuilderAre you tired of using trading indicators that only let you follow fixed, pre-designed rules? Do you wish you could build your own “Buy” or “Sell” signals, experiment with your own ideas, or see instantly if your unique pattern works—without learning coding or hiring a developer?

The Custom Buy/Sell Pattern Builder is designed for YOU.

This TradingView indicator lets ANY trader—even a complete beginner—define exactly what kind of price and volume conditions should create a BUY or SELL label on any chart, in any market, at any timeframe.

You don’t need to know programming. You don’t need to know the definition of a hammer, doji, volume spike, or Engulfing pattern.

With a few clicks and easy dropdown choices, you can:

Make your own rules for buying or selling

Choose how many candles your pattern should look at

Decide if you want the biggest body, the lowest volume, the biggest movement, or any combination you can imagine

The result?

You’ll see clear “BUY” or “SELL” labels automatically show up on your chart whenever the exact rule YOU built matches current price action.

No more guessing. No more forced strategies. Just pure control and visual feedback!

Why Is This Powerful?

Traditional indicators (like MACD, RSI, or even classic candlestick scanners) work the same for everyone—and only as their inventors defined.

But every trader, and every market, is unique.

What if you could say:

“Show me a ‘SELL’ every time the newest candle is bigger than the one before, but with LESS volume, while the bar before that had an even smaller body—but more volume than all others?”

With this tool, it’s EASY!

You simply pick which candle you want to compare (most recent, previous, etc), what to compare (body or volume—body means the candle’s “thickness”, from open to close), choose “greater than”, “less than”, or “equal to”, and set a multiplier if you want (like “half as much”, “twice as big”, etc).

After this, if any bar on the chart fits all your rules, it will mark it as a BUY or SELL, depending on your selection.

This means—

Beginners can start experimenting with their intuition or small ideas, without tech hurdles

Experienced traders can visualize and fine-tune any possible logic, before they commit to backtesting or automating a real strategy

Every “what if” or “I wonder” setup is just 2–3 clicks away

How Does It Work? Simple Steps

1. Choose Your Signal Type

“Buy” or “Sell”

This tells the indicator whether to mark the qualifying bars with a green “BUY” or red “SELL” label

2. Pick How Many Candles To Use

“Pattern Candle Count” input (2, 3, or 4)

Example: If you use 4, the pattern will be applied to the most recent 4 candles at every step

3. Define Your Pattern With Inputs

For each candle (from newest “0” to oldest “3”), you can set:

Body Condition (example: “is this candle’s body bigger/smaller/equal to another?”)

Pick which candle to compare against

Pick “>”, “<”, “>=”, “<=”, or “=”

Set a multiplier if needed (like “0.5” to mean “half as big as” or “2” for “twice as big as”)

Volume Condition (exact same choices, but based on trading volume—not the candle’s price body)

For example:

“Candle0 Body > Candle2 Body”

means “the latest candle’s real-body (open–close) is bigger than the one two bars ago.”

“Candle1 Volume <= Candle2 Volume”

means “the previous candle’s volume is less than or equal to the volume of the bar two periods ago.”

You can leave a comparison blank if you don’t want to use it for a particular candle.

What Happens After You Set Your Rules?

Every bar on your chart is checked for your logic:

If ALL body AND volume conditions are true (for each candle you specified),

AND

The signal side (“Buy” or “Sell”) matches your dropdown,

Then a green “BUY” or red “SELL” label will show right on the bar, so you can visually spot exactly where your logic works!

Practical Example:

Suppose you want an entry setup that is:

“Sell whenever the newest candle’s body is bigger than two bars ago, body before that is bigger than three bars ago, AND the newest candle’s volume is less than or equal to two bars ago, AND the candle three bars ago’s volume is less than or equal to half the candle two bars ago’s volume.”

You’d set:

Pattern Candle Count: 4

Side: Sell

Candle0 Body Ref#: 2, Op: >, Mult: 1

Candle1 Body Ref#: 3, Op: >, Mult: 1

Candle0 Vol Ref#: 2, Op: <=, Mult: 1

Candle3 Vol Ref#: 2, Op: <=, Mult: 0.5

And the script will find all “SELL” bars on your chart matching these conditions.

Inputs Section: What Does Each Setting Do?

Let’s break down each input in the indicator’s Settings one by one, so even if you’re new, you’ll understand exactly how to use it!

1. Pattern Candle Count (2–4)

What is it?

This sets how many candles in a row you want your rule to look at.

Example:

“4” means your rules are based on the most recent candle and the 3 before it.

“2” means you are only comparing the current and previous candles.

Tip:

Beginners often use 4 to spot stronger patterns, but you can experiment!

2. Signal Side

What is it?

Choose “Buy” or “Sell”. The word you pick here decides which colored label (green for Buy, red for Sell) appears if your pattern matches.

Example:

Want to spot where “Sell” is likely? Pick “Sell”.

Change to “Buy” if you want bullish signals instead.

3. Body & Volume Comparison Settings (per Candle)

For each candle (#0 is newest/current, #3 is oldest in your pattern window):

Body Comparison

Candle# Body Ref#

Choose which other candle you want to compare this one’s body to.

“0” = newest, “1” = previous, “2” = two bars ago, “3” = three bars ago

Candle# Body Op (Operator; >, <, >=, <=, =)

How do you want to compare?

“>” means “greater than” (is bigger than)

“<” means “less than” (is smaller than)

“=” means “equal to”

Candle# Body Mult (Multiplier)

If you want relative comparisons. For example, with Mult=1:

“Candle0 body > Candle2 body x 1” means just “0 is larger than 2.”

“Candle0 body > Candle2 body x 2” means “0 is more than double 2.”

Volume Comparison

Candle# Vol Ref# / Op / Mult

Exact same logic as body, but works on the “Volume” of each candle (how much was traded during that bar).

How to Set Up a Rule (Step by Step Example)

Say you want to mark a Sell every time:

The most recent candle’s real body is BIGGER than the candle 2 bars ago;

The previous candle’s body is also BIGGER than the candle 3 bars ago;

The current candle’s volume is LESS than or equal to the volume of candle 2;

The previous candle’s volume is LESS than or equal to candle 2’s volume;

The candle 3 bars ago’s volume is LESS than or equal to HALF candle 2’s volume.

You’d set:

Pattern Candle Count: 4

Side: "Sell"

Candle0 Body Ref#: 2, Op: “>”, Mult: 1

Candle1 Body Ref#: 3, Op: “>”, Mult: 1

Candle0 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle1 Vol Ref#: 2, Op: “<=”, Mult: 1

Candle3 Vol Ref#: 2, Op: “<=”, Mult: 0.5

All other comparisons (operators) can be left blank if you don’t want to use them!

When these rules are met, a bright red “SELL” label will appear right above the bar matching all your conditions.

Practical Tips & FAQ for Beginners

What does “body” mean?

It’s the “true range” of the candle: the difference between open and close. This ignores wicks for simple setups.

What does “volume” mean?

This is the total trading activity during that candle/bar. Many traders believe that patterns with different volume “meaning” (such as low-volume up bars, or high-volume down bars) signal a meaningful change.

What if nothing shows on chart?

It just means your current rules are rarely or never matched! Try making your comparisons simpler (maybe just 2-body and 2-volume conditions to start).

You can always hit “Reset Settings” to go back to default.

Can I use this for both buying and selling?

YES! You can detect both bullish (Buy) and bearish (Sell) custom conditions; just switch “Signal Side.”

Do I need to know coding?

Not at all! Everything is in simple input panels.

Creative Use Cases, Example Recipes & Troubleshooting

Creative Ways to Use

Spotting Reversals

Example:

Buy when: the newest candle body is LARGER than the previous 3 bars, but ALL volumes are lower than their neighbors.

Why? Sometimes, a big candle with surprisingly low volume after a sequence of small bars can signal a reversal.

Finding Exhaustion Moves

Example:

Sell when: the current bar body is twice as big as two bars ago, but volume is half.

Why? A very big candle with very little volume compared to similar bars may show the move is “running out of steam.”

Custom “Breakout + Confirmation” Patterns

Example:

Buy when:

Candle 0’s body is greater than Candle 2’s by at least 1.5x,

Candle 0’s volume is greater than Candle 1 and Candle 2,

Candle 1’s volume is less than Candle 0.

Why? This could catch strong breakouts but filter out noisy moves.

Multi-bar Bias/Squeeze Filter

Use “Pattern Candle Count: 4”

Set all 4 volume conditions to “<” and each reference to the previous candle.

Now, a BUY or SELL only marks when each bar is “dryer”/less active than the last — a classic squeeze or low-volatility buildup.

Troubleshooting Guide

“I don’t see any Buy/Sell label; is something broken?”

Most likely, your rules are too strict or rare! Try using only two comparisons and leave other “Op” inputs blank as a test.

Double-check you have enough candles on the chart: you need at least as many bars as your pattern count.

“Why does a label appear but not where I expect?”

Remember, the script checks your rules for every NEW candle. The candle “0” is always the most recent, then “1” is one bar back, etc.

Check the color and type chosen: “Signal Side” must be “Buy” for green, “Sell” for red.

“What if I want a more complex pattern?”

Stack conditions! You can demand the body/volume of each candle in your window meet a different rule or all follow the same rule in sequence.

Mini Glossary — For Newcomers

Candle/Bar: Each bar on the chart, shows price movement during a fixed time (e.g., one minute, one hour, one day).

Body: The colored (or filled) part of the candle — the open-to-close price range.

Volume: How much of the asset was actually traded that candle/bar.

Reference Index: When you pick “2” as a reference, it means “the candle two bars ago in the pattern window.”

Operator (“Op”): The math symbol used to compare (>, <, =, etc).

Signal Side: Whether you want to highlight bullish (“Buy”) or bearish (“Sell”) bars.

Tips for Getting More Value

Start Simple—try just one or two conditions at first. See what lights up. Slowly add more logic as you get comfortable.

Watch the chart live as you change settings. The labels update instantly—this makes strategy design fast and visual!

Try flipping your ideas: If a certain pattern doesn’t work for buys, try reversing the direction for possible “sell” setups.

Remember: There is NO wrong idea. This indicator is only limited by your creativity—it’s a “strategy playground.”

Example Quick-Start Recipes

Classic Sell:

4 candles, side = Sell

Candle0 Body > Candle2; Candle1 Body > Candle3

Candle0 Vol <= Candle2; Candle1 Vol <= Candle2; Candle3 Vol <= Candle2 × 0.5

Simple Buy After Pause:

3 candles, side = Buy

Candle0 Body > Candle1; Candle0 Vol > Candle1

All other Ops blank

Low-Volume Pullback for Entry:

4 candles, side = Buy

Candle0 Body > Candle2

Candle0 Vol < Candle1; Candle1 Vol < Candle2; Candle2 Vol < Candle3

Final Words

Think of this as your “pattern lab.” No code, no guesswork—just experiment, see what the market actually gives, and design your own visual rulebook.

If you’re stuck, reset the script to defaults—it’s always safe to start again!

If you want more ready-made “recipes” for different strategies/styles, just ask and I’ll send some more setups for you.

Happy building—and may your edge always be YOUR edge!

Pattern ScannerUltimate Pattern Scanner — multi-timeframe candlestick discovery tool (educational use only).

Purpose: This script scans user-selected timeframes for classical candlestick patterns (for example: engulfing, morning/evening stars, hammers, dojis, tasuki gaps, three soldiers/crows, tweezers, marubozu, and others) and reports pattern name, detection price, directional signal (Bull / Bear / Neutral), and a simple volume participation metric. It is intended as an idea-generation and training tool to help traders learn pattern mechanics, not as an automated trading system.

Main modules and rationale: 1) Pattern engine — applies classical candle structure rules to detect formations; 2) SMA trend filter (configurable length) — provides a directional bias to favor trade-with-trend setups; 3) Volume heuristic — approximates participation by separating candles into buy-like and sell-like volume and comparing total volume to a moving average; 4) Multi-timeframe aggregator — collects and presents pattern results from multiple timeframes; 5) Alerts — optional alerts list detected patterns and TFs. Combining these modules is intentional: patterns provide structure, SMA provides context, and volume supplies participation confirmation. Together they improve the educational value and practical relevance of each detected pattern.

How to use: Choose timeframes and SMA length that match your trading horizon. Use the scanner to locate pattern candidates, then confirm with higher-timeframe agreement and volume ratio before considering trade entry. Use structural stops (recent swing highs/lows or ATR-based stops) and define risk:reward rules. For learning, replay alerted bars and record outcomes over fixed horizons to build empirical statistics.

Limitations: Volume classification (close>open) is a heuristic and not a true bid/ask tape. SMA is a lagging trend proxy. Multi-timeframe agreement reduces but does not eliminate false signals, especially around news or in low-liquidity instruments. Use demo accounts and backtesting before live trading.

Inputs you can adjust: timeframe list, SMA length, volume MA length, which patterns to enable/disable, display options.

Compliance notes: This description explains why modules are combined and what the script does without exposing source code logic; it is non-promotional and contains no contact links. Remove any trademark symbols unless registration details are provided.

Risk Disclaimer: This tool is provided for education and analysis only. It is not financial advice and does not guarantee returns. Users assume all risk for trades made based on this script. Backtest thoroughly and use proper risk management.

Stop Loss vs Take Profit Probability and EVThis stop loss and take profit calculator uses a Monte Carlo simulation to calculate the probability of hitting your Stop Loss or Take Profit levels across different time horizons (expressed in bars).

It provides data-driven insights to optimize your risk management and position sizing by showing Expected Value for each scenario.

As a quant, I love using statistical data to help my decisions and get better EV from my trades.

🔬 How It's Calculated

Monte Carlo Simulation: Runs 1,000-10,000 price simulations using a random walk model

Volatility Analysis: Combines ATR-based and Historical Volatility for accurate price movement modeling

Expected Value: Calculates profit/loss expectation using formula: (TP_Probability × Reward) - (SL_Probability × Risk)

Time Horizons: Tests multiple timeframes (1, 5, 10, 20, 50 bars) to find optimal holding periods

Risk/Reward Ratios: Automatically calculates and displays R:R ratios for quick assessment

💡 Use Cases

Position Sizing - Determine optimal risk per trade based on Expected Value

Time Horizon Optimization - Find the best holding period for your strategy

Stop Loss Placement - Validate SL levels using probability analysis

Take Profit Optimization - Set TP levels with statistical backing

Strategy Backtesting - Compare different R:R setups before entering trades

Risk Management - Avoid trades with negative Expected Value

Swing vs Day Trading - Choose timeframes with highest success probability

🎯 How to Use

Setup Trade: Enter your entry price, stop loss, and take profit levels

You can add or remove time horizons denominated in bars. Say you are looking at 1h candles, adding a 24-bar time horizon means you are looking into 24 hours

Choose Direction: Select Long or Short position

Review Table

Analyze Expected Value: Focus on positive EV scenarios (green background)

Optimize Timing: Select time horizons with best risk/reward profile

Adjust Parameters: Modify volatility calculation method and simulation count if needed

Examples

Here's how you can read the tables.

Example 1:

In this chart, we are analyzing the TP and SL probabilities as well as the EV (expected value) for a stock. I want to check what the likelihood is that my SL and TP get triggered over the next 5 days. The stock market is open for 6.5 hours per day, which is 13 bars in this 30-minute bar chart. 26 bars is 2 days, 39 bars is 3 days and so on.

Although this trade is more likely to trigger my SL than my TP, in some of the time horizons we have a positive expected value because of the risk/reward of our trade (i.e. distance of the SL and TP from the price) and the probability of hitting SL and TP.

Example 2:

In this example, we have applied the indicator to gold. Because the TP is much closer to the price, the probability of hitting the TP is much higher.

We can also observe that the expected Value in the shorter time frames is better than in the longer ones. This can give us some clues to set up our trade. If we know that the EV is positive, we can allocate more to that specific trade.

Enjoy, and please let me know your feedback! 😊🥂

4 DU DINHSample Indicator Introduction (English)

Title:

Adaptive Trend & Momentum Indicator

Short Description:

An adaptive indicator that combines trend detection and momentum confirmation to help identify potential entry and exit points in various markets.

Full Description:

This indicator is designed to provide traders with a clear view of both trend direction and momentum strength. It dynamically adjusts to different market conditions, making it suitable for cryptocurrencies, stocks, and forex.

Main Features:

Trend Identification: Uses adaptive moving averages to detect bullish or bearish market phases.

Momentum Confirmation: Integrates oscillator-based signals to reduce false entries during sideways markets.

Customizable Inputs: Adjustable sensitivity, smoothing factors, and signal thresholds.

Non-repainting Logic: Signals are only confirmed after candle close to avoid misleading entries.

How to Use:

A bullish signal occurs when trend direction turns positive and momentum confirms.

A bearish signal occurs when trend direction turns negative with momentum confirmation.

Recommended for H1 and higher timeframes, but can be tuned for intraday strategies.

⚠️ Disclaimer: This indicator is for educational purposes only. It does not guarantee profits. Always combine with proper risk management and backtesting before trading live.

MS - Crypto RSI-Based Trading StrategyThis is a comprehensive trend-following and momentum-based strategy designed for the cryptocurrency market. It combines multiple leading indicators to filter out market noise and generate high-quality buy and sell signals.

Key Indicators:

Moving Average (MA): To determine the main trend direction.

Relative Strength Index (RSI): To measure momentum and identify overbought/oversold conditions.

Directional Movement Index (DMI): To confirm the strength of the trend.

Volume & ATR: To validate market interest and filter out excessive volatility.

Buy Conditions (All Must Be True):

Price and Trend Alignment: The current price is above the MA50 (with a 5% buffer).

Momentum Confirmation: The RSI is between 50 and 70.

Trend Strength: The +DI is greater than the -DI.

Market Interest: Volume is 1.5 times its moving average.

Low Volatility: The ATR is below its average.

Sell Conditions (Any One Is True):

Trend Reversal: The price drops below the MA50 (with a 5% buffer).

Momentum Loss: The RSI drops below 45.

Trend Weakness: The -DI crosses above the +DI.

Market Fatigue: Volume drops below 50% of its moving average.

High Volatility: The ATR is above its average.

Disclaimer: This is a backtesting tool and not financial advice. Past performance is not an indicator of future results. Always use proper risk management and conduct your own research before trading.